Embed Size (px)

Citation preview

If you don't save money for your retirement, you may be forced to continue working until you die, whether you want to or not. Retirement benefits from various sources can reduce the amount of work you need to do during retirement so that you can relax and enjoy your old age. In many cases, retirement benefits may be enough for you to retire fully. But, you should become familiar with the types of retirement benefits available to you.

That is Advice

by Alibaster smith

Definition of retirement

Retirement benefits are financial instruments designed to help

individuals after they stop working. Individuals typically receive

retirement benefits in the form of regular cash installments or as

protection in the form of insurance coverage

Definition benefit pension plan

Benefit pension plan is a type of pension plan in which an

employer/sponsor promises a specified monthly benefit on

retirement that is predetermined by a formula based on the

employee's earnings history, tenure of service and age, rather

than depending directly on individual investment returns.

Employer pension programs classified into two types:

1. Defined Contribution. (DC)

2. Defined Benefit. (DB)

Defined contribution. (DC)

Defined contribution (DC) plan each employee has an account into

which the employer and, if it is a contributory plan, the employee

make regular contributions. Benefit levels depend on the total

contributions and investment earnings of the accumulation in the

account.

Defined Benefit. (DB)

In a defined benefit (DB) plan the employee’s pension benefit

entitlement is determined by a formula which takes into account

years of service for the employer and, in most cases, wages or

salary. Many defined benefit formulas also take into account the

Social Security benefits to which an employee is entitled.

US Retirement History

The rise of retirement was already documented by the social reformers

of the 1920s and 1930s (e.g., U.S. Committee on Economic Security

1935) and is familiar to many researchers. These researchers generally

agree on the trend in retirement rates but disagree on explanations,

citing both factors that have enticed men out of the labor force, such

as the growth of Social Security, private pension plans, and income,

and factors that have driven them out, such as sectorial shifts in the

composition of the labor force, poor job opportunities, and ill health.

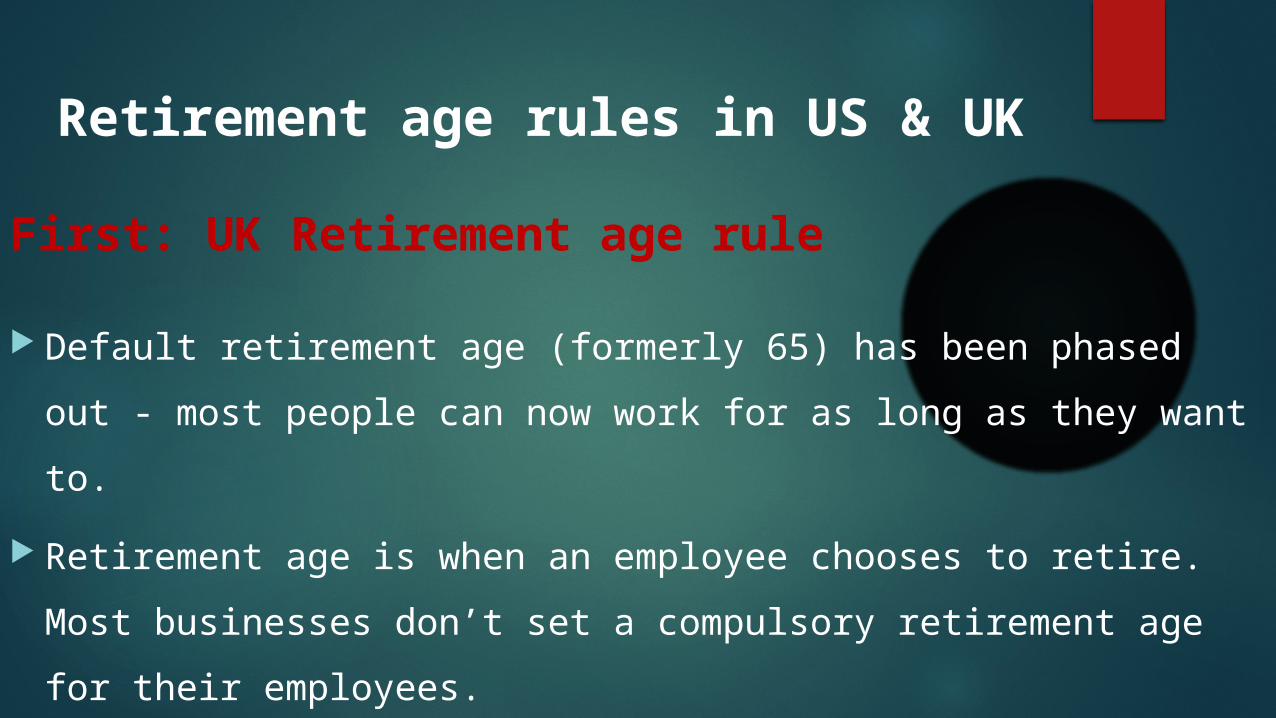

Retirement age rules in US & UK

First: UK Retirement age rule

Default retirement age (formerly 65) has been phased out - most

people can now work for as long as they want to.

Retirement age is when an employee chooses to retire. Most

businesses don’t set a compulsory retirement age for their

employees.

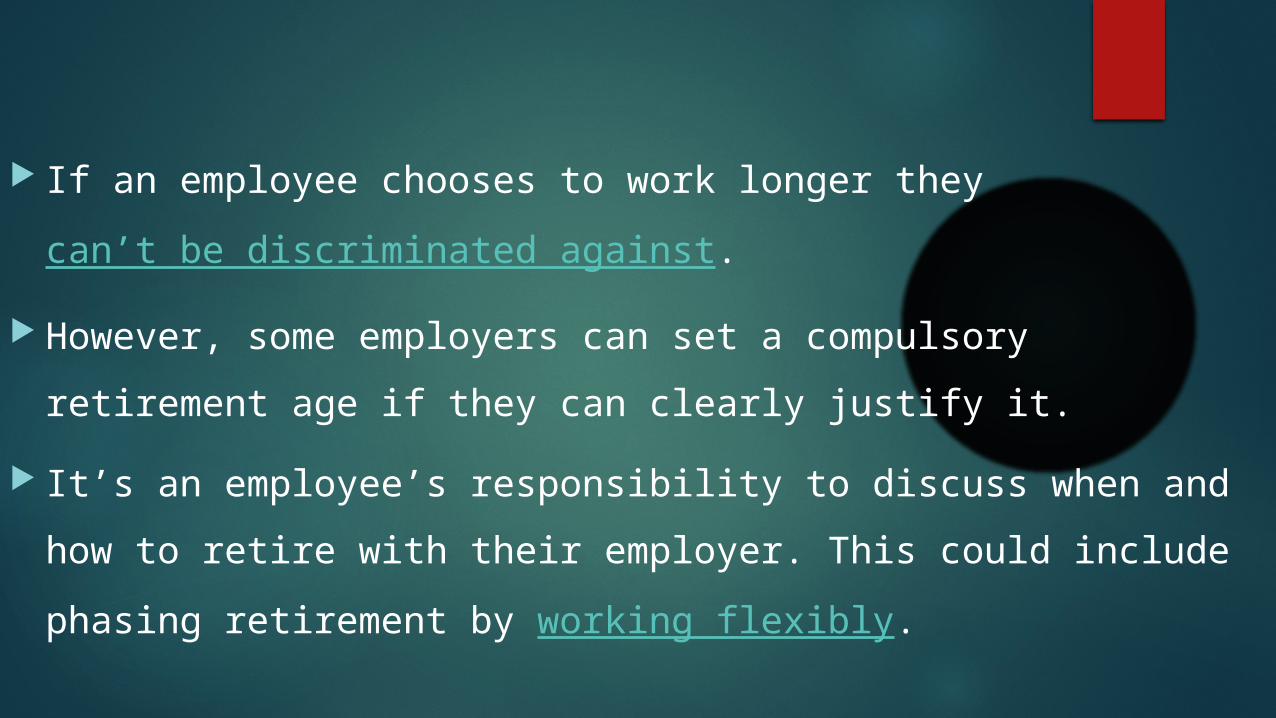

If an employee chooses to work longer they

can’t be discriminated against.

However, some employers can set a compulsory retirement age

if they can clearly justify it.

It’s an employee’s responsibility to discuss when and how to

retire with their employer. This could include phasing retirement

by working flexibly.

Second: US laws and regulations

In the US, there are many laws and regulations concerning pension plans such as:

qualified DB plans must use pay that is the smaller of actual pensionable pay

versus a dollar limit (called the 401(a)(17) limit) that changes yearly.

qualified DB plans must limit the dollar amount of the benefit paid from the plan

under certain circumstances.

Rules on distributions: lump sum must be no smaller than the lump sum

calculated using mandated mortality and interest rate

spouse consent necessary for any non joint and survivor form of benefit (joint

and survivor percent must be 50% or larger)

Rules against assignment, garnishment

Top heavy rules (IRC 416): benefits for all non highly compensated employees

must be increased if the benefits for highly compensated employees are too large

What is social security ?

Social Security is primarily the Old-Age, Survivors, and Disability

Insurance (OASDI) federal program. The original Social Security Act

(1935) and the current version of the Act, as amended, encompass

several social welfare and social insurance programs. Social Security is

funded through payroll taxes called

Federal Insurance Contributions Act tax (FICA) and/or Self Employed

Contributions Act Tax (SECA). Tax deposits are collected by the Internal

Revenue Service (IRS) and are formally entrusted to the Federal Old-

Age and Survivors Insurance Trust Fund.

Social Security and your retirement plans

Social Security is part of the retirement plan of almost every American

worker. If you are among the 96 percent of workers who are covered

under Social Security, you should know how the system works and

what you should receive from Social Security when you retire. what

you should think about in deciding when to retire and why you should

not rely only on Social Security for your retirement income.

Your retirement benefits

When you work and pay Social Security taxes, you earn “credits”

toward Social Security benefits. The number of credits you need to get

retirement benefits depends on when you were born. If you were born

in 1929 or later, you need 40 credits (10 years of work). If you stop

working before you have enough credits to qualify for benefits, the

credits will remain on your Social Security record. If you return to work

later on, you can add more credits so that you qualify. We cannot pay

any retirement benefits until you have the required number of credits.

How much will your retirement benefit be?

Your benefit payment is based on how much you earned during

your working career. Higher lifetime earnings result in higher

benefits. If there were some years when you did not work or had

low earnings, your benefit amount may be lower than if you had

worked steadily.

You can get retirement benefit estimates

You can use the online Retirement Estimator to get immediate and

personalized retirement benefit estimates to help you plan for your

retirement. The online Retirement Estimator is a convenient,

secure and quick financial planning tool, because it eliminates the

need to manually key in years of earnings information.

Full retirement age

If you were born in 1944 or earlier, you are already eligible for your

full Social Security benefit. If you were born from 1943 to 1960,

the age at which full retirement benefits are payable increases

gradually to age 67. The following chart lists the full retirement

age by year of birth.

Age to receive full Social Security benefits

Year of birth Full retirement age

1943-1954 66

1955 66 and 2 months

1956 66 and 4 months

1957 66 and 6 months

1958 66 and 8 months

1959 66 and 10 months

1960 and later 67

NOTE: People who were born on January 1 of any year should refer to the previous year.

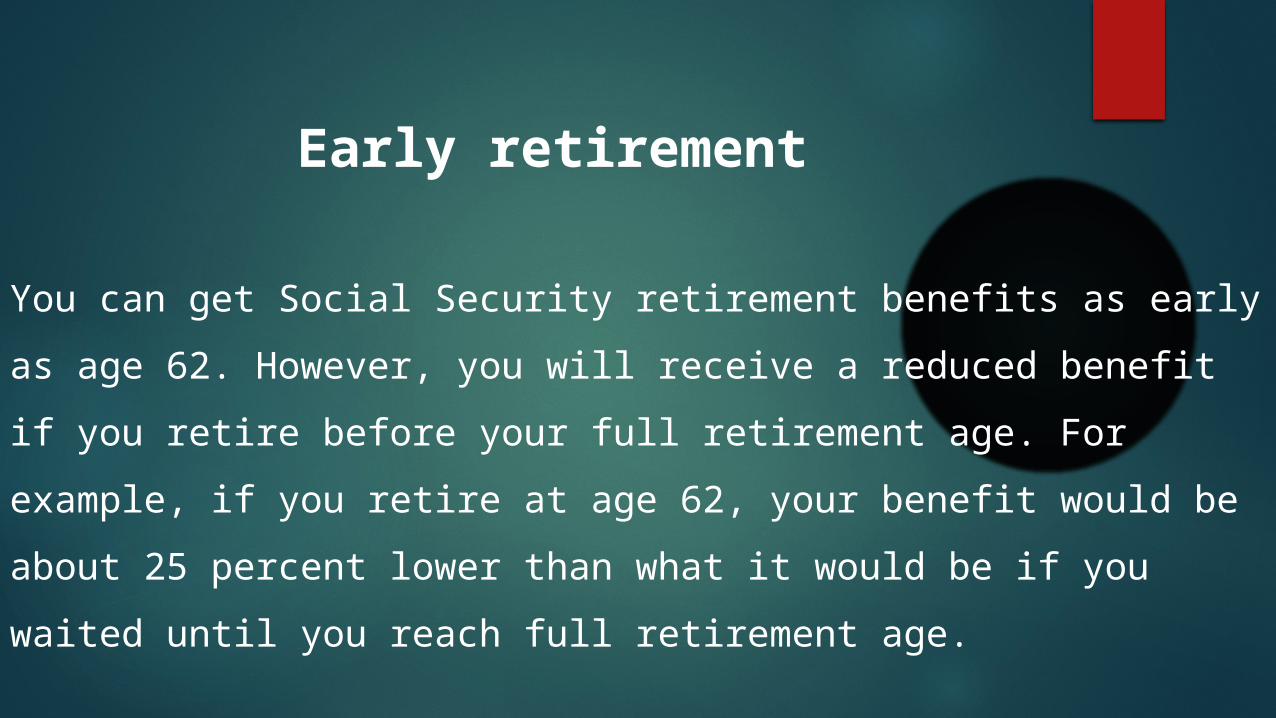

Early retirement

You can get Social Security retirement benefits as early as age 62.

However, you will receive a reduced benefit if you retire before

your full retirement age. For example, if you retire at age 62, your

benefit would be about 25 percent lower than what it would be if

you waited until you reach full retirement age.

Delayed retirement

You may choose to keep working even beyond your full retirement

age. If you do, you can increase your future Social Security

benefits in two ways. Each additional year you work adds another

year of earnings to your Social Security record. Higher lifetime

earnings may mean higher benefits when you retire.

Deciding when to retire

Choosing when to retire is an important but personal decision.

Regardless of the age you choose to retire, it is a good idea to

contact Social Security in advance to learn the available options

and make an informed decision. In some cases, your choice of a

retirement month could mean higher benefit payments for you and

your family.

If you work and get benefitsAt the same time

You can continue to work and still receive retirement benefits. Your

earnings in (or after) the month you reach your full retirement age

will not reduce your Social Security benefits. However, your

benefits will be reduced if your earnings exceed certain limits for

the months before you reach your full retirement age.

A special monthly rule

A special rule applies to your earnings for one year, usually your

first year of retirement. Under this rule, you can receive a full

Social Security check for any month you earn under a certain

limit, regardless of your yearly earnings.

Leaving the United States

If you are a U.S. citizen, you can travel to or live in most foreign

countries without affecting your Social Security benefits. There are,

however, a few countries where we cannot send Social Security

payments. These countries are Azerbaijan, Belarus, Cuba, Georgia,

Kazakhstan, Kyrgyzstan, Moldova, North Korea, Tajikistan. If you work

outside the United States, different rules apply in determining you

can get benefits.

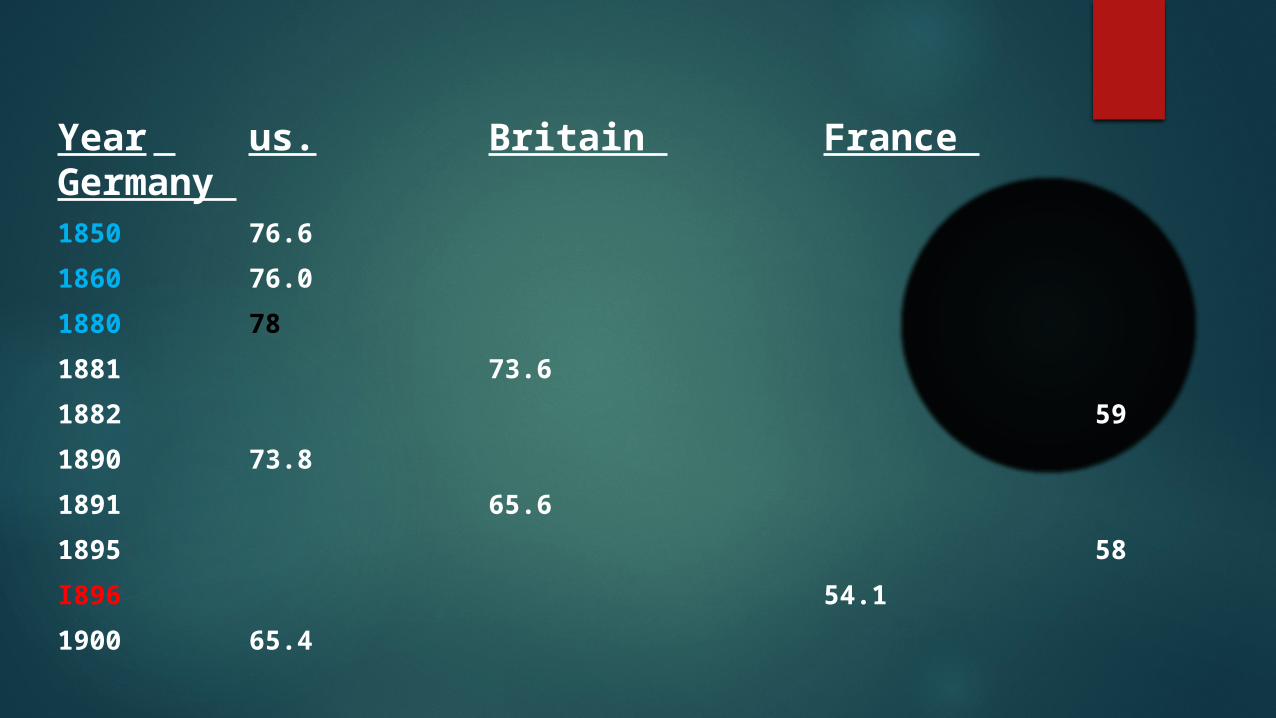

pension extended backward to1850 and forward to 1990

Labor Force Participation Rates of Men Aged 65 and over,

1850-1990 in :

United States

Britain

France

Germany

Notice: this participation rates for men aged 60-69 and 70 or older.

First country to start pension .

Last country to start retirement.

Minimum record retirement.

Maximum record retirement.

Year us. Britain France Germany 1850 76.6

1860 76.0

1880 78

1881 73.6

1882 59

1890 73.8

1891 65.6

1895 58

I896 54.1

1900 65.4

Year us. Britain France Germany1901 61.4

1907 52

1910 58.1

1911 56.9 51.1

1920 60.1

1921 58.9 53.5

I925 47.4

1930 58.0

1931 47.9 48.1

1933 29.2

1936 42.7

Year us. Britain France Germany

I939 29.5

1940 43.5

1950 47.0 26.8

195 1 31.1

1954 36.2

1960 40.8

1961 24.4 22.9

1962 27.8

1970 35.2 17.2

1973 18.6

1975 10.6

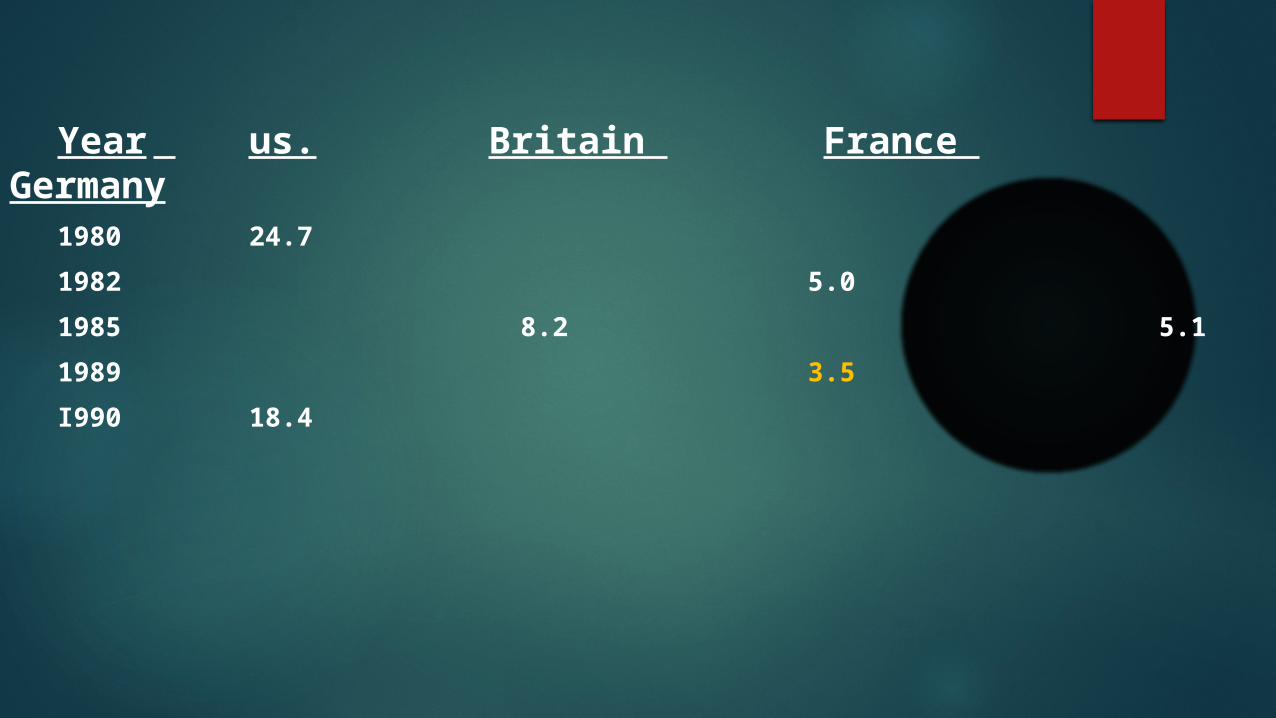

Year us. Britain France Germany

1980 24.7

1982 5.0

1985 8.2 5.1

1989 3.5

I990 18.4

ENJOY YOUR OLD AGEWITH PENSION