Embed Size (px)

Citation preview

1©2014 MSCI Inc. All rights reserved. msci.commsci.com

Identifying Environmental & Social Risks in Supply Chains

Olga Emelianova, Senior Analyst, MSCI ESG Research

Top Commodities in Focus

Jaclyn Daitchman, Analyst, MSCI ESG Research

RIA Conference

May 27, 2014

2©2014 MSCI Inc. All rights reserved. msci.com

Agenda

About MSCI ESG Research

Identifying Environmental & Social Risks in Supply Chains

Olga Emelianova, Senior Analyst, MSCI ESG Research

Top Commodities in Focus

Jaclyn Daitchman, Analyst, MSCI ESG Research

Q&A

Please visit the MSCI ESG Research booth to find out more and pick up our reports!

3©2014 MSCI Inc. All rights reserved. msci.com

MSCI ESG Research Today

Over 70 asset owners with $2.3 trillion in assets

Over 650 clients with $15 trillion in assets globally

ESG ratings and research produced 100% in-house

Staff of 160+ in ESG, including 90+ in research

Over 40 years in ESG industry (IRRC, KLD, Innovest)

Signatory to the Principles for Responsible Investment

Global ESG Research Capabilities

Boston

New York

Toronto

San Francisco

Cape Town

Tokyo

Beijing

Sydney

MumbaiManila

London

Paris

Geneva

Monterrey

RockvilleAnn Arbor

Frankfurt

4©2014 MSCI Inc. All rights reserved. msci.com 4msci.com

Identifying Environmental & Social Risks in Supply Chains

Olga Emelianova

5©2014 MSCI Inc. All rights reserved. msci.com

Supply Chain – Impact and Risk

6©2014 MSCI Inc. All rights reserved. msci.com

Let’s take a quiz!

Labor : what industry is most likely to take the largest labor cost?

Apparel

Food Products

Electronics

Health & Safety: what country poses the highest ESG risk for Apparel industry?

Vietnam

Cambodia

Mexico

Energy: what industry would be most affected by energy price increase?

Food Products

Electronics

Apparel

7©2014 MSCI Inc. All rights reserved. msci.com

Labor Cost Health & Safety Energy Cost

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

China Vietnam Indonesia India

The wage gap between China and Vietnam has been widening since 2007

China continues to be the global manufacturing hub

The country has experienced the steepest wage increase over the last decade

Source: ILO Global Wage database, General Statistics Office of Vietnam, U.S. Bureau of Labor Statistics

8©2014 MSCI Inc. All rights reserved. msci.com

Labor Cost Health & Safety Energy Cost

Electronics are likely to be most affected

Cost of Goods Sold

Production in China 30% 50% 70% 100%

Wage Increase

10% 0.6% 1.0% 1.4% 2.0%

20% 1.2% 2.0% 2.8% 4.0%

30% 1.8% 3.0% 4.2% 6.0%

60% 3.6% 6.0% 8.4% 12.0%

Low scalability production

Dependence on local raw materials (rare earth)

Thin and shrinking profit margins

Samsung and Apple are a notable exception

Source: Thomson One Banker, company disclosure, MSCI ESG Research

Source: Thomson One Banker, company disclosure, MSCI ESG Research

9©2014 MSCI Inc. All rights reserved. msci.com 9

Labor Cost Health & Safety Energy Cost

Apparel & Textiles: Bangladesh is not the only country at risk

CountryTextile exports, USD bln

Industrial employment

Monthly wage, USD

Injury rate,per 100,000 employees

Bangladesh 16.4 15.0% 881 366

Cambodia 4.6 16.9% 80 202

El Salvador 2.2 21.5% 1862 36073

India 12.9 22.4% 1022 325

Pakistan 12.5 20.0% 92 207

Vietnam 16.0 21.3% 722 46273

Notes:1 Bangladesh monthly wage shown with a 30% increase adjustment announced in 20132 Average monthly wage for country, due to regional or sector variations.3 Injury rates include public sector and family businesses.

Sources: International Labour Organization, the United Nations Statistics Division, The World Bank, Ministry of Labour and Vocational Training of Cambodia, Bangladesh Bureau of Statistics, Pakistan Bureau of Statistics, General Statistics Office ofVietnam

10©2014 MSCI Inc. All rights reserved. msci.com 10

Labor Cost Health & Safety Energy Cost• The largest portion of product carbon footprint is attributed to energy and fuel use in

raw materials production and finished goods manufacturing

Source: IERS' Comprehensive Environmental Data Archive (CEDA) data, MSCI ESG Research

Raw Materials TransportationManufacturing Trade and Administration

Cheese Pasta, cookies Footwear2528 CO2e/USD 1 mln 1058 CO2e/USD 1 mln 846 CO2e/USD 1 mln

Soap Apparel Computers

810 CO2e/USD 1 mln 566 CO2e/USD 1 mln 284 CO2e/USD 1 mln

11©2014 MSCI Inc. All rights reserved. msci.com 11

Labor Cost Health & Safety Energy CostApparel and Footwear will likely be most affected by energy price increase

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Diversified Discretionary Goods

Footwear

Apparel

Luxury

Food Products & Food Retail

Household Products

Trade and warehousing Transportation

Components and goods manufacturing Raw materials production

Cost Increase as a % of Revenue

Cost Increase as a % of Net Profit

Food Retail 0.64% 20.08%

Electronics 0.46% 14.77%

Food Products 0.59% 7.48%

Apparel 0.46% 7.06%

Footwear 0.47% 6.92%

Luxury Goods 0.35% 2.57%

Harder to push on consumers due to discretionary nature and competition based on price

Source: MSCI ESG Research, Thomson Financials, IERS' Comprehensive Environmental Data Archive (CEDA) data, company disclosure

Percent of companies monitoring energy use and emissions in supply chain:

If energy price globally goes 10% up…

Have the lowest control over the supply chain

12©2014 MSCI Inc. All rights reserved. msci.com

Let’s take a quiz!

Labor : what industry is most likely to take the largest labor cost?

Apparel

Food Products

Electronics

Health & Safety: what country poses the highest ESG risk for Apparel industry?

Vietnam

Cambodia

Mexico

Energy: what industry would be most affected by energy price increase?

Food Products

Electronics

Apparel

13©2014 MSCI Inc. All rights reserved. msci.com

Reputational Concerns Intensify

Workplace Safety and Raw Materials Production are high on public agenda

Number of Reported Controversies by Type

Source: MSCI Impact Monitor

14©2014 MSCI Inc. All rights reserved. msci.com 14msci.com

Top Commodities in Focus

Jaclyn Daitchman

15©2014 MSCI Inc. All rights reserved. msci.com 15msci.com

Soy

PalmOil

Cocoa

Photo source: MIXA, via WebMD

16©2014 MSCI Inc. All rights reserved. msci.com 16msci.com

Stearic Acid Sodium Lauryl Sulfate Glyceryl Stearate

Cetyl palmitate Octyl palmitate

Palmitoyl Tetrapeptide-3

17©2014 MSCI Inc. All rights reserved. msci.com 17msci.com

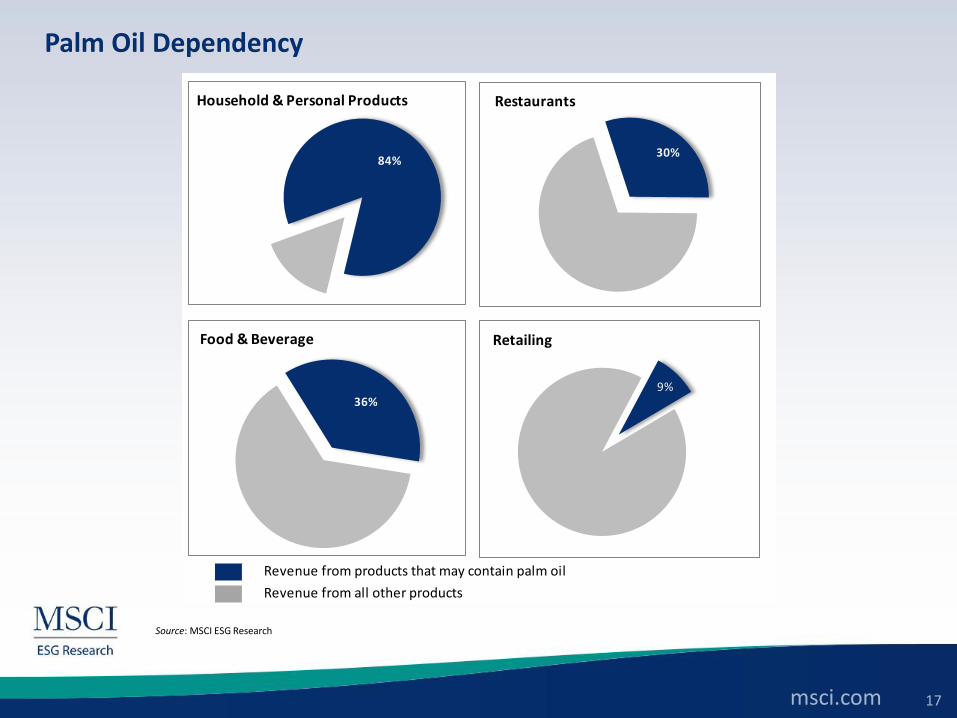

Source: MSCI ESG Research

Palm Oil Dependency

Revenue from products that may contain palm oil

Revenue from all other products

84%

Household & Personal Products

36%

Food & Beverage

30%

Restaurants

9%

Retailing

18©2014 MSCI Inc. All rights reserved. msci.com

Sources: RSPO Annual Communication on Progress 2012-2013, company disclosure

Responsible Sourcing Commitments

Company CountryVolume of palm

oil used (t) Less Stringent

(incl. GreenPalm)More Stringent

(excl. GreenPalm)

Year Year

Unilever NL 1,523,605 2012 2020

Procter & Gamble US 462,000 2015 -

PepsiCo US 457,200 2015 2020

Nestle CH 410,000 2013 -

Mondelez US 285,732 2015 -

Colgate-Palmolive US 109,259 2020 2020

Reckitt Benckiser GB 106,895 2015 2020

McDonald's US 103,336 2020 -

Kao JP 95,356 2015 2020

Johnson & Johnson US 77,800 2010 2015

Henkel DE 71,608 2015 2017

Wal-Mart US 71,463 2015 2015

L'Oreal FR 61,850 2010 2010

General Mills US 56,041 2015 2015

Kellogg US 50,000 2011 2015

Tesco GB 33,811 2012 2015

Danone FR 30,300 2011 2015

Beiersdorf Aktiengesellschaft DE 25,301 2013 2020

Associated British Foods GB 20,550 2015 -

Hershey US 20,282 2014 2014

19©2014 MSCI Inc. All rights reserved. msci.com

Responsible Sourcing Progress

Unilever NL 1,523,605

Procter & Gamble US 462,000

PepsiCo US 457,200

Nestle CH 410,000

Mondelez US 285,732

Colgate-Palmolive US 109,259

Reckitt Benckiser GB 106,895

McDonald's US 103,336

Kao JP 95,356

Johnson & Johnson US 77,800

Henkel DE 71,608

Wal-Mart US 71,463

L'Oreal FR 61,850

General Mills US 56,041

Kellogg US 50,000

Tesco GB 33,811

Danone FR 30,300

Beiersdorf Aktiengesellschaft DE 25,301

Associated British Foods GB 20,550

Hershey US 20,282

Company CountryVolume of palm oil used (t)

0 100000 200000 300000 400000 5000001,470,000

Sources: RSPO Annual Communication on Progress 2012-2013, company disclosure

No certification Mass BalanceBook & Claim (Green Palm) Segregated or Identity Preserved

20©2014 MSCI Inc. All rights reserved. msci.com

53%38%

9%

47%

27%

17%

9%

Less stringent committment: More Stringent

SELECTED COMPANY HIGHLIGHTS

No time-bound commitment Campbell, Clorox, Costco, Yum!

Brands

McDonald's, Mondelez,

Nestle, Procter & Gamble

Unlikely to achieve certifcation

by target year

On track to achieve certification

by target year

Colgate-Palmolive, McDonald's,

PepsiCo, Procter & Gamble, Wal-

Mart

Johnson & Johnson,

PepsiCo, Unilever

Heinz, Kellogg, Metro,

Sainsbury

-

Heinz, Nestle, Metro, Sainsbury

Have already achieved

certification

Johnson & Johnson, Kellogg, L'Oreal,

Marks & Spencer, Tesco, Unilever

Less Stringent Commitment (incl. GreenPalm) by 2015

More Stringent Commitment (excl. GreenPalm) by 2020

Source: RSPO Annual Communication on Progress 2012-2013, WWF “Palm Oil Buyers Scorecard” (2013), company disclosure , MSCI ESG Research

Responsible Sourcing Progress

21©2014 MSCI Inc. All rights reserved. msci.com

Perceived constraints to meeting commitments

Many companies claim that their limited use of certified product is triggered by the lack of availability of certified sustainably produced palm oil and high premiums charged for certified palm oil.

83%

8%

3%

2%

4%

non-certified

certified, but not purchased

purchased by Unilever

purchased by the next 9 top buyers

purchased by rest of the world

Cost, USD % of

Revenue Cost, USD

% of

Revenue

Unilever (NL) 9,141,630 0.014% 309,291,815 0.457%

Procter & Gamble (US) 2,772,000 0.003% 93,786,000 0.118%

PepsiCo (US) 2,743,200 0.004% 92,811,600 0.140%

Nestle (CH) 2,460,000 0.003% 83,230,000 0.086%

Mondelez (US) 1,714,392 0.005% 58,003,596 0.161%

Colgate-Palmolive (US) 655,554 0.004% 22,179,577 0.135%

Reckitt Benckiser (GB) 641,370 0.004% 21,699,685 0.150%

McDonald's (US) 620,016 0.002% 20,977,208 0.076%

Kao (JP) 572,136 0.004% 19,357,268 0.139%

Johnson & Johnson (US) 466,800 0.001% 15,793,400 0.023%

Scenario 1

Less Stringent

(GreenPalm)

Scenario 2

More Stringent

(Segregated)

Supply exceeds demand Compliance cost is low

Source: RSPO Annual Communication on Progress 2012-2013, company disclosure , MSCI ESG Research

22©2014 MSCI Inc. All rights reserved. msci.com

0.00%

0.08%

0.16%

0.24%

0.32%

0.40%

0.48%

-

25,000

50,000

75,000

100,000

125,000

150,000

Un

ileve

r (N

L)

Mo

nd

ele

z (U

S)

Re

chit

t B

en

ckis

er (

GB

)

Pe

psi

Co

(U

S)

Kao

(JP

)

Co

lgat

e-P

alm

oliv

e (

US)

Pro

cte

r &

Gam

ble

(U

S)

Ge

ne

ral M

ills

(US)

Ne

stle

(C

H)

Co

nA

gra

* (U

S)

McD

on

ald

's (

US)

Yu

m!

Bra

nd

s (U

S)

He

nke

l (D

E)

Ke

llogg

(U

S)

Gru

po

Bim

bo

(M

X)

Be

iers

do

rf (

DE)

Ori

flam

e (

BE)

He

rsh

ey

(US)

L'O

real

(FR

)

Ork

la**

(N

O)

Tin

gyi (

CN

)

Avo

n (

US)

Dan

on

e (

FR)

AB

F (G

B)

Joh

nso

n &

Jo

hn

son

(U

S)

Shis

eid

o (

JP)

Ke

rry

(IE)

Este

e L

aud

er

(US)

Lin

dt

& S

pru

en

gli (

CH

)

Cam

pb

el (

US)

He

inz

(US)

Dar

de

n (

US)

L B

ran

ds

(US)

Sain

sbu

ry (

GB

)

Tesc

o (

GB

)

Du

nki

n B

ran

ds

(US)

Nis

sin

Fo

od

s (J

P)

WM

Mo

rris

on

(G

B)

MEI

JI (

JP)

Ah

old

(N

L)

Aji

no

mo

to (

JP)

Mar

ks &

Sp

ence

r (G

B)

Wh

itb

read

(G

B)

Wal

-Mar

t (U

S)

Ae

on

(JP

)

Sod

exo

(FR

)

Seve

n &

i (J

P)

Wo

olw

ort

hs

(AU

)

We

sfar

me

rs (

AU

)

Nat

ura

Co

sme

tico

s (B

R)

Co

mp

ass

(GB

)

Mas

smar

t (Z

A)

BR

F (B

R)

He

rbal

ife

(KY

)

Wh

ole

Wo

od

s (U

S)

Ch

urc

h &

Dw

igh

t (U

S)

Sho

pri

te (

ZA)

Car

refo

ur

(FR

)

Ke

sko

(FI

)

Clo

rox

(US)

Cas

ino

(FR

)

Cen

cosu

d (

CL)

Met

ro (

DE)

Lob

law

(C

A)

Ge

org

e W

est

on

(C

A)

Safe

way

(U

S)

Kro

ger

(US)

Sup

erv

alu

(U

S)

Co

stco

(U

S)

Targ

et

(US)

Companies that purchase certified palm oil

Cost to revenue (most stringent certification)

422,600

Companies that do not purchase certified palm oil

Cost to revenue, %

Source: RSPO Annual Communication on Progress, company disclosure, media reports, MSCI ESG Research

Brand Visibility vs. Compliance Costs

23©2014 MSCI Inc. All rights reserved. msci.com

1 21

1013

18

14

5

55

0

10

20

30

40

50

60

2005 2006 2007 2008 2009 2010 2011 2012 2013

Total Controversies and Proxies Filed on Palm Oil Issues: 2005-2013

Trends

Source: CERES

24©2014 MSCI Inc. All rights reserved. msci.com

Regulatory costs

-2%

0%

2%

4%

6%

8%

10%

12%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Ind

on

esia

Mal

aysi

a

Thai

lan

d

Co

lom

bia

Nig

eria

Pap

ua

New

Gu

inea

Ecu

ado

r

Ho

nd

ura

s

Ivo

ry C

oas

t

Bra

zil

Co

sta

Ric

a

Cam

ero

on

Gu

atem

ala

DR

C

Gh

ana

Ph

ilip

pin

es

Mex

ico

An

gola

Do

min

ican

Rep

ub

lic

Gu

inea

Ind

ia

Ben

in

Ven

ezu

ela

Per

u

Lib

eria

Res

t o

f th

e w

orl

dA

nn

ual

Pro

du

ctio

n G

row

th (

%)

Pro

du

ctio

n (

'00

0 M

T)

Source: United States Department of Agriculture (2013 preliminary estimate)

Trends

Production in Latin America and Africa

25©2014 MSCI Inc. All rights reserved. msci.com 25msci.com

Thank you

26©2014 MSCI Inc. All rights reserved. msci.com 26msci.com

MSCI ESG Global Client Service

Americas + 1.212.804.5299

Asia Pacific + 612.9033.9339

Europe, Middle East and Africa + 44.207.618.2510

www.msci.com/esg

27©2014 MSCI Inc. All rights reserved. msci.com 27msci.com

Notice and Disclaimer This document and all of the information contained in it, including without limitation all text, data, graphs, charts (collectively, the “Information”) is the property of MSCI Inc. or its subsidiaries (collectively, “MSCI”), or MSCI’s

licensors, direct or indirect suppliers or any third party involved in making or compiling any Information (collectively, with MSCI, the “Information Providers”) and is provided for informational purposes only. The Information may not be modified, reverse-engineered, reproduced or redisseminated in whole or in part without prior written permission from MSCI.

The Information may not be used to create derivative works or to verify or correct other data or information. For example (but without limitation), the Information may not be used to create indexes, databases, risk models, analytics, software, or in connection with the issuing, offering, sponsoring, managing or marketing of any securities, portfolios, financial products or other investment vehicles utilizing or based on, linked to, tracking or otherwise derived from the Information or any other MSCI data, information, products or services.

The user of the Information assumes the entire risk of any use it may make or permit to be made of the Information. NONE OF THE INFORMATION PROVIDERS MAKES ANY EXPRESS OR IMPLIED WARRANTIES OR REPRESENTATIONS WITH RESPECT TO THE INFORMATION (OR THE RESULTS TO BE OBTAINED BY THE USE THEREOF), AND TO THE MAXIMUM EXTENT PERMITTED BY APPLICABLE LAW, EACH INFORMATION PROVIDER EXPRESSLY DISCLAIMS ALL IMPLIED WARRANTIES (INCLUDING, WITHOUT LIMITATION, ANY IMPLIED WARRANTIES OF ORIGINALITY, ACCURACY, TIMELINESS, NON-INFRINGEMENT, COMPLETENESS, MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE) WITH RESPECT TO ANY OF THE INFORMATION.

Without limiting any of the foregoing and to the maximum extent permitted by applicable law, in no event shall any Information Provider have any liability regarding any of the Information for any direct, indirect, special, punitive, consequential (including lost profits) or any other damages even if notified of the possibility of such damages. The foregoing shall not exclude or limit any liability that may not by applicable law be excluded or limited, including without limitation (as applicable), any liability for death or personal injury to the extent that such injury results from the negligence or willful default of itself, its servants, agents or sub-contractors.

Information containing any historical information, data or analysis should not be taken as an indication or guarantee of any future performance, analysis, forecast or prediction. Past performance does not guarantee future results.

The Information should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. All Information is impersonal and not tailored to the needs of any person, entity or group of persons.

None of the Information constitutes an offer to sell (or a solicitation of an offer to buy), any security, financial product or other investment vehicle or any trading strategy.

It is not possible to invest directly in an index. Exposure to an asset class or trading strategy or other category represented by an index is only available through third party investable instruments (if any) based on that index. MSCI does not issue, sponsor, endorse, market, offer, review or otherwise express any opinion regarding any fund, ETF, derivative or other security, investment, financial product or trading strategy that is based on, linked to or seeks to provide an investment return related to the performance of any MSCI index (collectively, “Index Linked Investments”). MSCI makes no assurance that any Index Linked Investments will accurately track index performance or provide positive investment returns. MSCI Inc. is not an investment adviser or fiduciary and MSCI makes no representation regarding the advisability of investing in any Index Linked Investments.

Index returns do not represent the results of actual trading of investible assets/securities. MSCI maintains and calculates indices, but does not manage actual assets. Index returns do not reflect payment of any sales charges or fees an investor may pay to purchase the securities underlying the index or Index Linked Investments. The imposition of these fees and charges would cause the performance of an Index Linked Investment to be different than the MSCI index performance.

The Information may contain back tested data. Back-tested performance is not actual performance, but is hypothetical. There are frequently material differences between back tested performance results and actual results subsequently achieved by any investment strategy.

Constituents of MSCI equity indexes are listed companies, which are included in or excluded from the indexes according to the application of the relevant index methodologies. Accordingly, constituents in MSCI equity indexes may include MSCI Inc., clients of MSCI or suppliers to MSCI. Inclusion of a security within an MSCI index is not a recommendation by MSCI to buy, sell, or hold such security, nor is it considered to be investment advice.

Data and information produced by various affiliates of MSCI Inc., including MSCI ESG Research Inc. and Barra LLC, may be used in calculating certain MSCI equity indexes. More information can be found in the relevant standard equity index methodologies on www.msci.com.

MSCI receives compensation in connection with licensing its indices to third parties. MSCI Inc.’s revenue includes fees based on assets in investment products linked to MSCI equity indexes. Information can be found in MSCI’s company filings on the Investor Relations section of www.msci.com.

MSCI ESG Research Inc. is a Registered Investment Adviser under the Investment Advisers Act of 1940 and a subsidiary of MSCI Inc. Except with respect to any applicable products or services from MSCI ESG Research, neither MSCI nor any of its products or services recommends, endorses, approves or otherwise expresses any opinion regarding any issuer, securities, financial products or instruments or trading strategies and neither MSCI nor any of its products or services is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Issuers mentioned or included in any MSCI ESG Research materials may include MSCI Inc., clients of MSCI or suppliers to MSCI, and may also purchase research or other products or services from MSCI ESG Research. MSCI ESG Research materials, including materials utilized in any MSCI ESG Indexes or other products, have not been submitted to, nor received approval from, the United States Securities and Exchange Commission or any other regulatory body.

Any use of or access to products, services or information of MSCI requires a license from MSCI. MSCI, Barra, RiskMetrics, IPD, FEA, InvestorForce, and other MSCI brands and product names are the trademarks, service marks, or registered trademarks of MSCI or its subsidiaries in the United States and other jurisdictions. The Global Industry Classification Standard (GICS) was developed by and is the exclusive property of MSCI and Standard & Poor’s. “Global Industry Classification Standard (GICS)” is a service mark of MSCI and Standard & Poor’s.

© 2014 MSCI Inc. All rights reserved. May 2014