Embed Size (px)

Citation preview

1

Contents

I. Why CFMs with MPMs intent are needed

II. What are to be done in near the future

Capital Flows and Capital Flow Management Measures

Before Crisis After Crisis

2

Virtue

Sometimes Silver Bullet

to address trouble

Vice (Capital Control)

Still good, but sometimes Trouble Maker

Capital Movements

Capital Flows Management

2

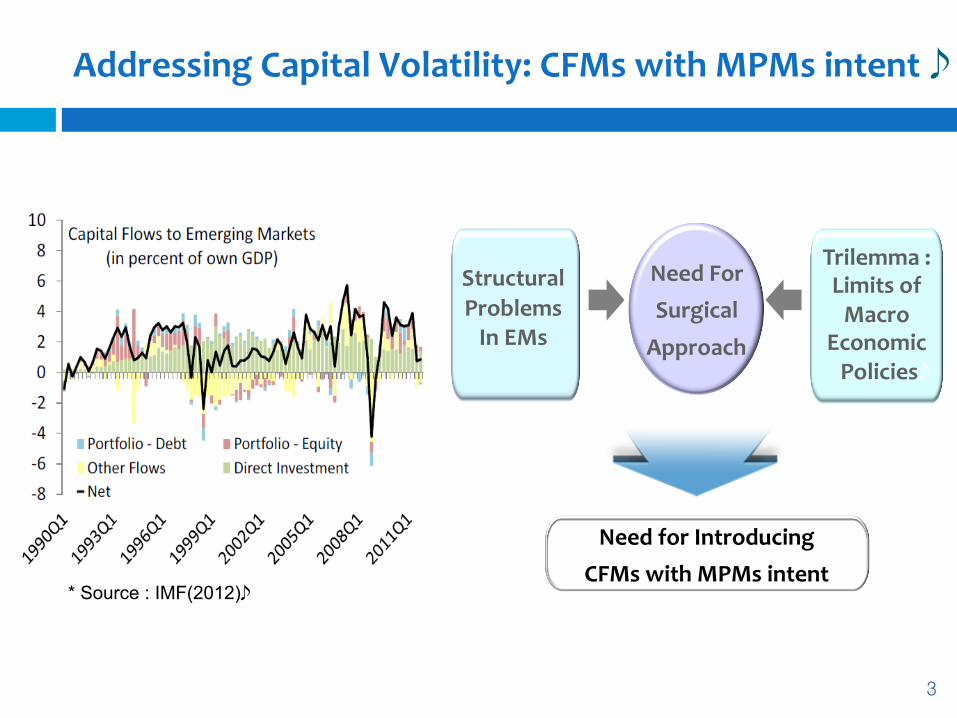

Addressing Capital Volatility: CFMs with MPMs intent

3

Structural Problems In EMs

Need For Surgical

Approach

Need for Introducing CFMs with MPMs intent

Trilemma : Limits of Macro

Economic Policies

* Source : IMF(2012)

Corporate Debts and CFMs with MPMs intent

EM Corporate Bond (bl US$ )

* Source : IMF GFSR (2015)

Domestic Banks : The Share of Corporate Loans to Total (%)

* Source : IMF GFSR (2015)

4

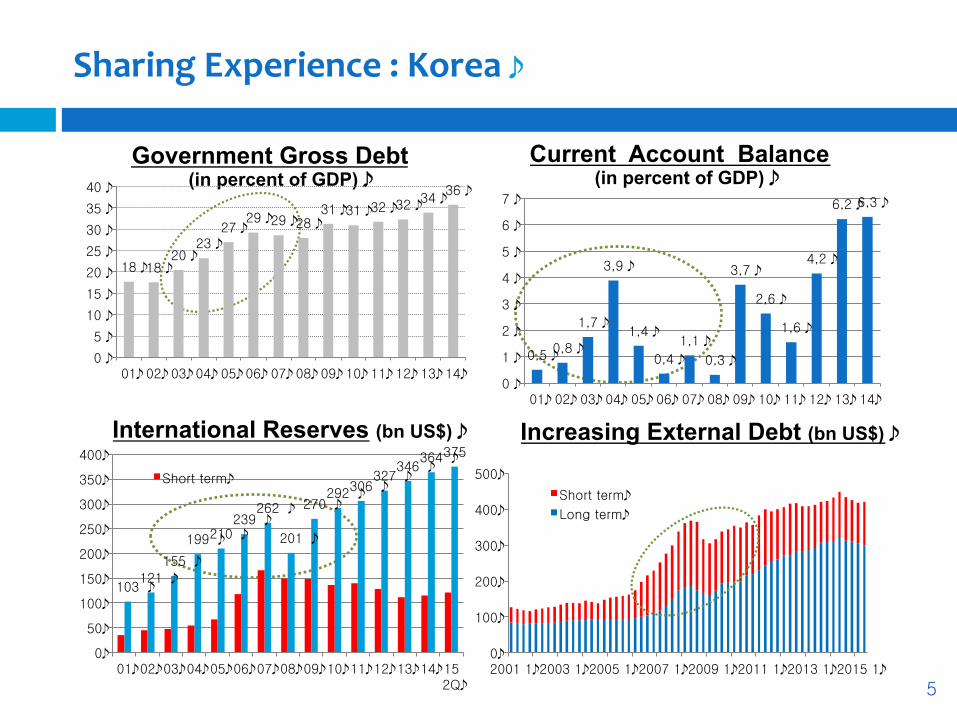

Sharing Experience : Korea

Government Gross Debt (in percent of GDP)

International Reserves (bn US$)

Current Account Balance (in percent of GDP)

Increasing External Debt (bn US$)

0

100

200

300

400

500

2001 1 2003 1 2005 1 2007 1 2009 1 2011 1 2013 1 2015 1

Short term

Long term

18 18 20

23 27

29 29 28 31 31 32 32

34 36

0

5

10

15

20

25

30

35

40

01 02 03 04 05 06 07 08 09 10 11 12 13 14

0,5 0,8

1,7

3,9

1,4

0,4

1,1

0,3

3,7

2,6

1,6

4,2

6,2 6,3

0

1

2

3

4

5

6

7

01 02 03 04 05 06 07 08 09 10 11 12 13 14

103 121

155

199 210 239

262

201

270 292

306 327

346 364 375

0

50

100

150

200

250

300

350

400

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 2Q

Short term

5

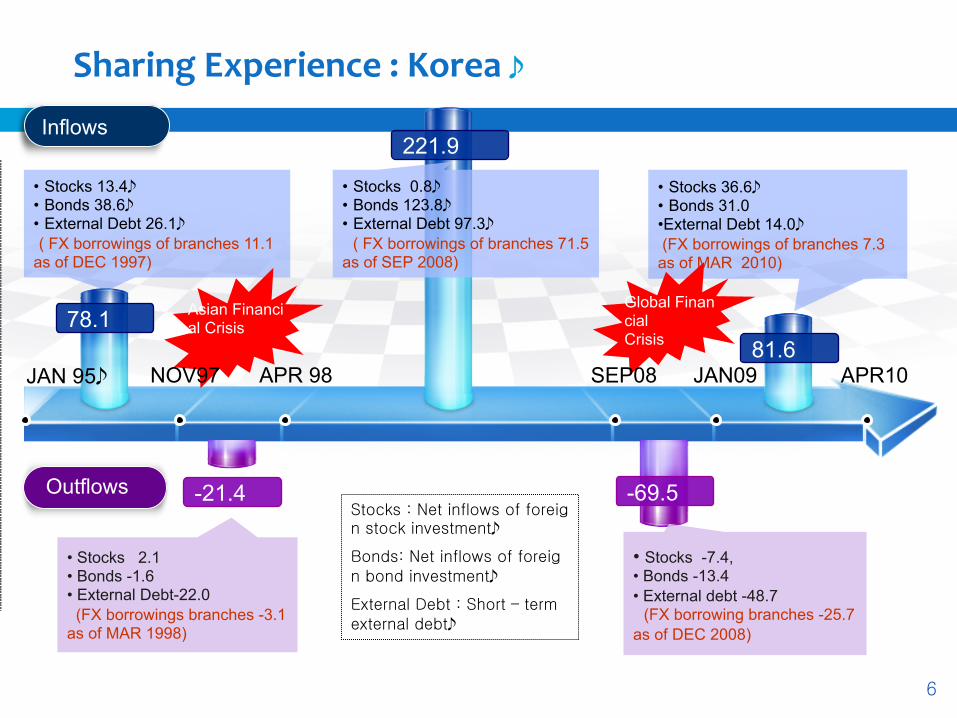

Sharing Experience : Korea

6

81.6

-21.4 -69.5

• Stocks 13.4 • Bonds 38.6 • External Debt 26.1 ( FX borrowings of branches 11.1 as of DEC 1997)

• Stocks 2.1 • Bonds -1.6 • External Debt-22.0 (FX borrowings branches -3.1 as of MAR 1998)

• Stocks 36.6 • Bonds 31.0 • External Debt 14.0 (FX borrowings of branches 7.3 as of MAR 2010)

• Stocks -7.4, • Bonds -13.4 • External debt -48.7 (FX borrowing branches -25.7 as of DEC 2008)

78.1

221.9

• Stocks 0.8 • Bonds 123.8 • External Debt 97.3 ( FX borrowings of branches 71.5 as of SEP 2008)

Asian Financial Crisis

Global Financial Crisis

SEP08 JAN09 APR10 NOV97 APR 98

Inflows

Outflows Stocks : Net inflows of foreign stock investment

Bonds: Net inflows of foreign bond investment

External Debt : Short – term external debt

JAN 95

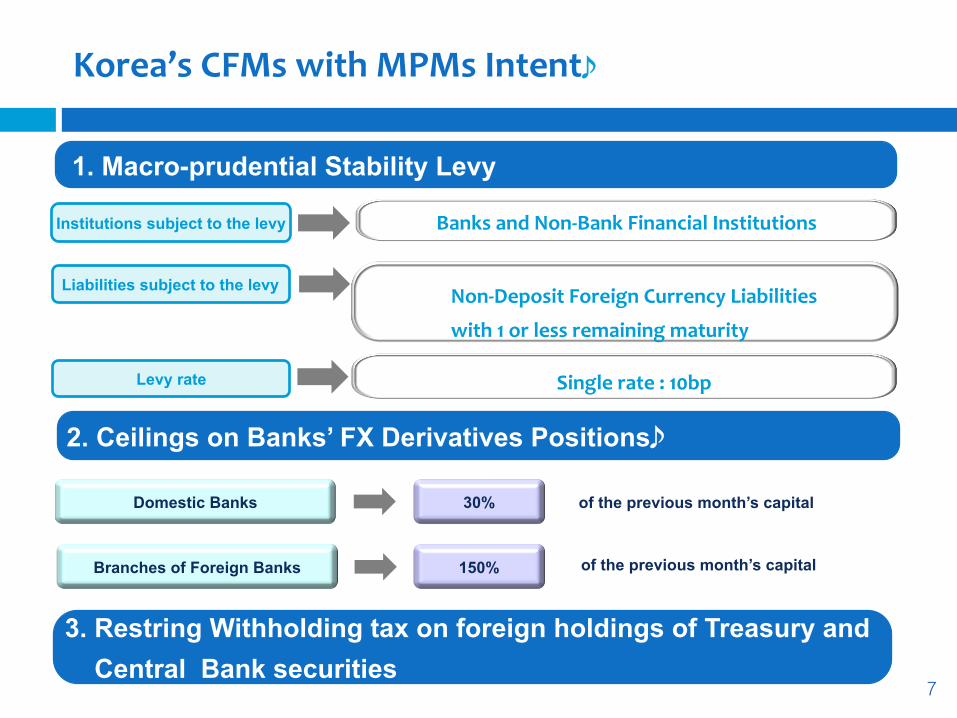

Korea’s CFMs with MPMs Intent

1. Macro-prudential Stability Levy

Institutions subject to the levy Banks and Non-‐Bank Financial Institutions

Liabilities subject to the levy

Levy rate

Non-‐Deposit Foreign Currency Liabilities

with 1 or less remaining maturity

Single rate : 10bp

2. Ceilings on Banks’ FX Derivatives Positions

Domestic Banks 30% of the previous month’s capital

Branches of Foreign Banks 150% of the previous month’s capital

3. Restring Withholding tax on foreign holdings of Treasury and Central Bank securities

7

8

Contents

I. Why CFMs with MPMs intent are needed

II. What are to be done in the near future

8

9

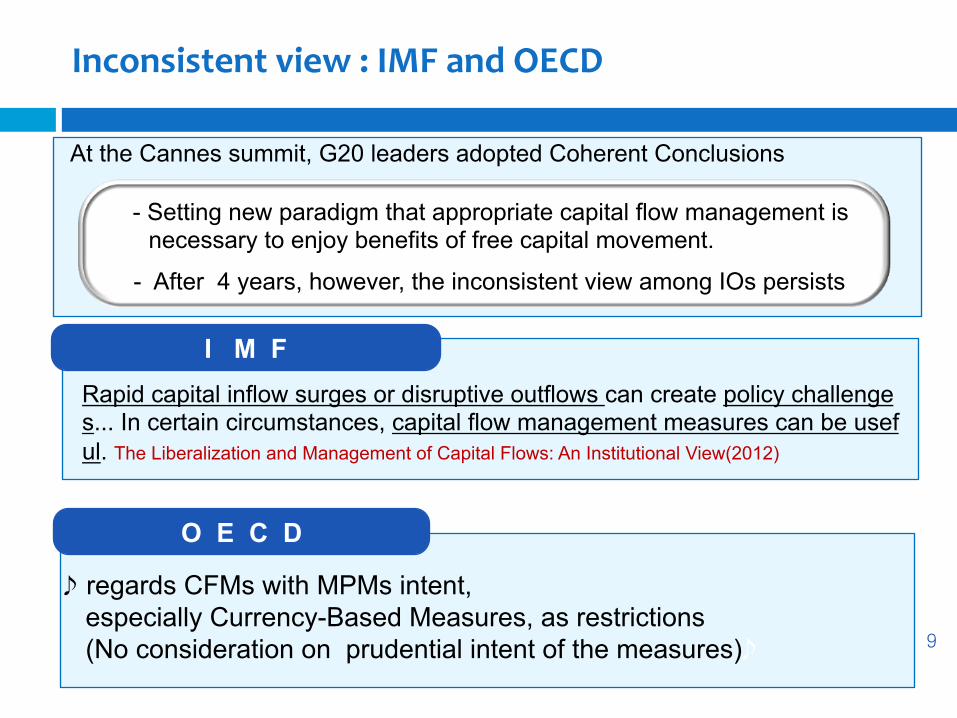

Inconsistent view : IMF and OECD

At the Cannes summit, G20 leaders adopted Coherent Conclusions

- Setting new paradigm that appropriate capital flow management is necessary to enjoy benefits of free capital movement.

I M F

O E C D

- After 4 years, however, the inconsistent view among IOs persists

Rapid capital inflow surges or disruptive outflows can create policy challenges... In certain circumstances, capital flow management measures can be useful. The Liberalization and Management of Capital Flows: An Institutional View(2012)

regards CFMs with MPMs intent, especially Currency-Based Measures, as restrictions (No consideration on prudential intent of the measures)

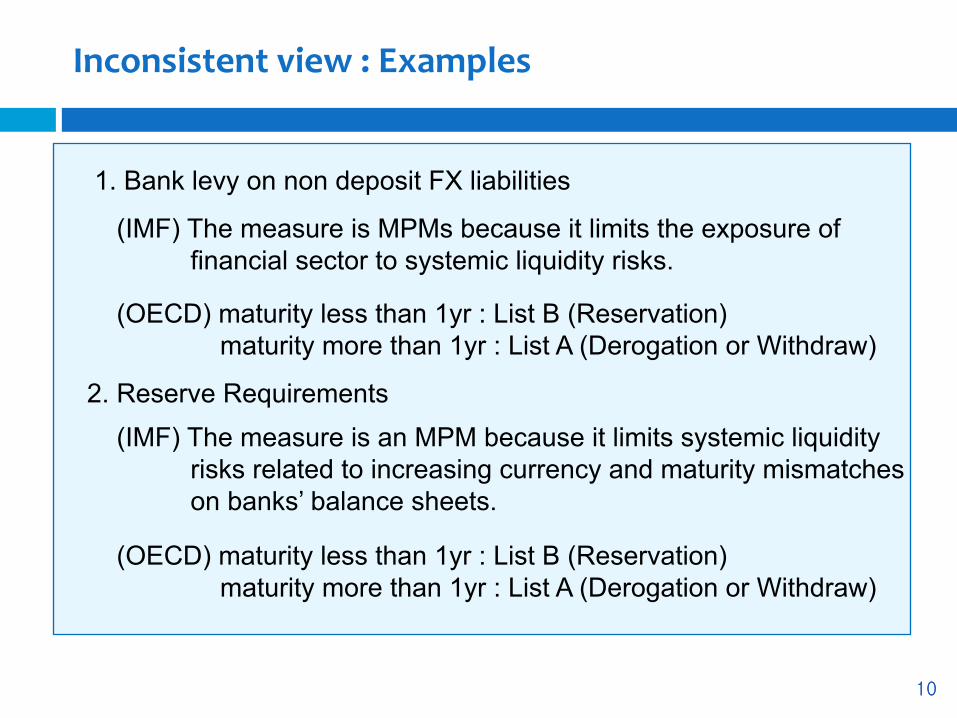

Inconsistent view : Examples

10

1. Bank levy on non deposit FX liabilities

(IMF) The measure is MPMs because it limits the exposure of financial sector to systemic liquidity risks. (OECD) maturity less than 1yr : List B (Reservation) maturity more than 1yr : List A (Derogation or Withdraw)

2. Reserve Requirements

(IMF) The measure is an MPM because it limits systemic liquidity risks related to increasing currency and maturity mismatches on banks’ balance sheets. (OECD) maturity less than 1yr : List B (Reservation) maturity more than 1yr : List A (Derogation or Withdraw)

10

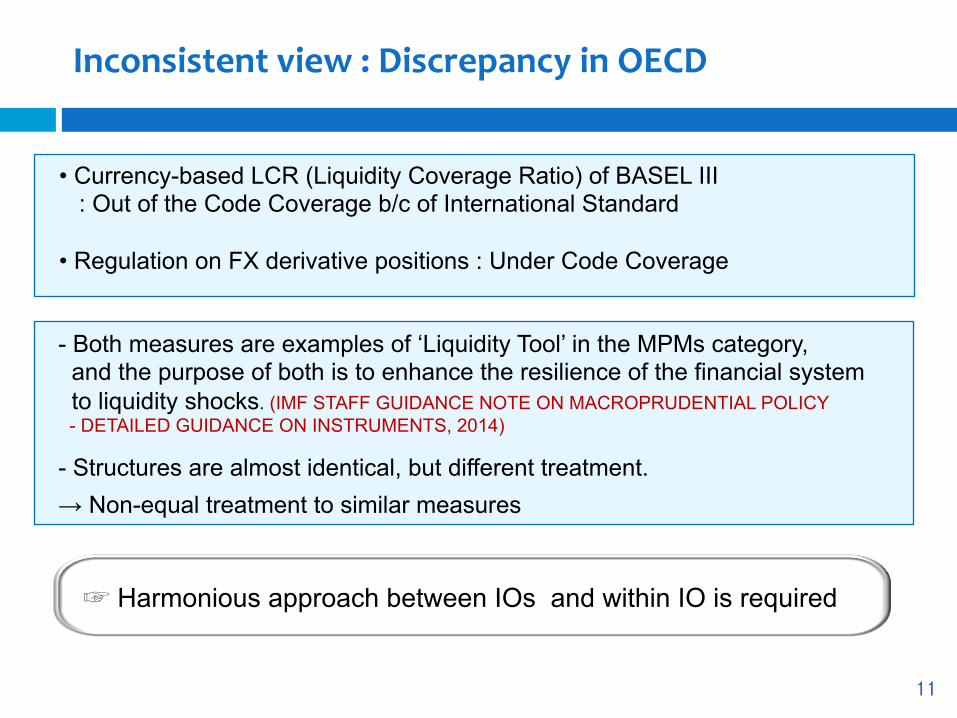

Inconsistent view : Discrepancy in OECD

11

• Currency-based LCR (Liquidity Coverage Ratio) of BASEL III : Out of the Code Coverage b/c of International Standard • Regulation on FX derivative positions : Under Code Coverage

☞ Harmonious approach between IOs and within IO is required

- Both measures are examples of ‘Liquidity Tool’ in the MPMs category, and the purpose of both is to enhance the resilience of the financial system to liquidity shocks. (IMF STAFF GUIDANCE NOTE ON MACROPRUDENTIAL POLICY - DETAILED GUIDANCE ON INSTRUMENTS, 2014)

- Structures are almost identical, but different treatment.

→ Non-equal treatment to similar measures

11

12

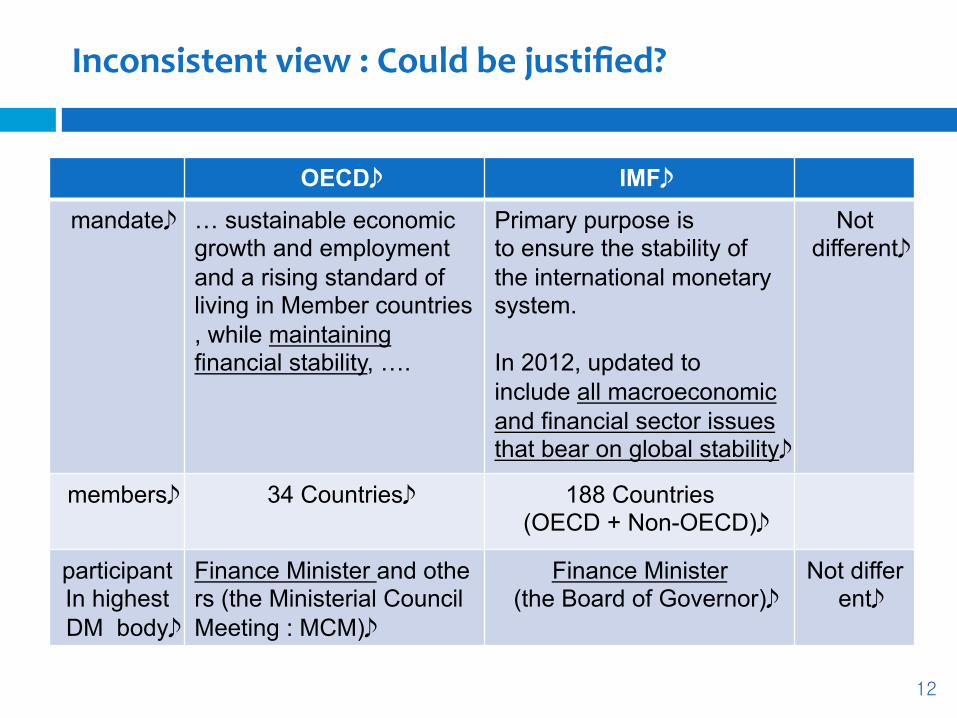

Inconsistent view : Could be justified?

OECD IMF

mandate … sustainable economic growth and employment and a rising standard of living in Member countries, while maintaining financial stability, ….

Primary purpose is to ensure the stability of the international monetary system. In 2012, updated to include all macroeconomic and financial sector issues that bear on global stability

Not different

members 34 Countries 188 Countries (OECD + Non-OECD)

participant In highest DM body

Finance Minister and others (the Ministerial Council Meeting : MCM)

Finance Minister (the Board of Governor)

Not different

13

Inconsistent view : Other Institutions

IMF (GFSR Oct 2015 ) FSB Brookings Institution

The corporate debt of nonfinancial firms across major emerging market economies quadrupled between 2004 and 2014. Although greater leverage can be used for investment, thereby boosting growth, the upward trend in recent years naturally raises concerns because many financial crises in emerging markets have been preceded by rapid leverage growth. Third, macro- and microprudential policies could help limit a further buildup of foreign exchange balance sheet exposures and contain excessive increases in corporate leverage.

The credit risk associated with firms with large foreign currency debts is significantly higher… In addition, banks that lend in foreign currency can also be exposed to roll-over risks. To alleviate these risks, targeted macroprudential policy measures such as higher risk-weights, and outright limits on banks’ lending in foreign currency can help. Tightly calibrated macroprudential tools … include limits on net open position in foreign exchange; differentiated reserve requirements across currencies; or liquidity requirements differentiated by currency. Corporate Funding Structures and Incentives ( Aug 2015)

It is also possible to identify new sources of risk to financial stability, especially in situations in which corporates acting as financial speculators and/or domestic banks fail to fully understand the underlying domestic and international exposures of the corporate sector. Accordingly, it is timely for governments and financial regulators to review risk surveillance and macroprudential policies … in order to ensure that these risks are suitably contained. Corporate Debt in Emerging Economies: A Threat to Financial Stability? (Sep 2015)

14

Inconsistent view : G20 FM and CBG meetings

G20 Finance Minister & Central Bank Governor meeting in Feb 2015 We ask the IMF and the OECD, with input from the BIS and FSB, to assess whether further work is needed on their respective approaches to measures which are both macro-prudential and capital flow measures, taking into account their individual mandates, by our meeting in April.

G20 Finance Minister & Central Bank Governor meeting in Apr 2015 When dealing with macroeconomic and financial stability risks arising from large and volatile capital flows, the necessary macroeconomic adjustment could be supported by macro-prudential measures and, as appropriate, capital flow management measures. In this regard, we welcome the continued cooperation between the relevant IOs on their respective approaches to measures that are both macro-prudential and capital flow management measures.

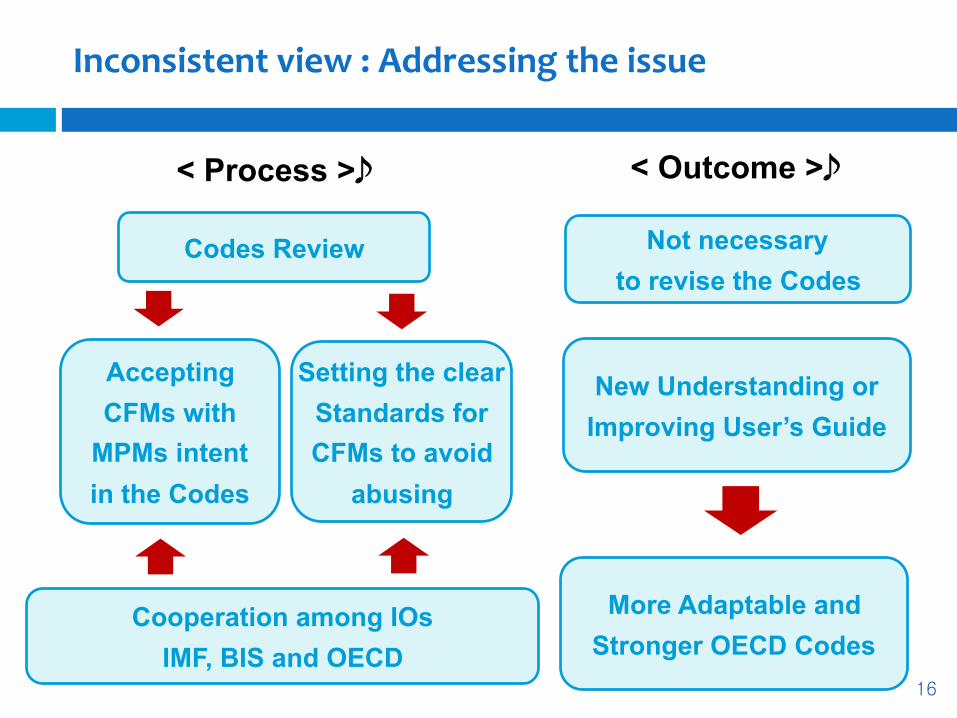

Inconsistent view : The OECD Codes

15

1. No Review on the Codes since 1992 → less adaptability of the Codes to the changing financial markets (No rules relating to CFMs with MPMs intent)

2. The OECD Codes : only legally binding multilateral convention on Capital Movements. → impossible to introduce CFMs with MPMs intent when the Codes are interpreted rigidly

3. Flexibility of the OECD Codes ? : No For flexibility : Reservation and Derogation (OECD argument) → Reservation : Signaling to markets measures will be abolished and undermining the legitimacy of measures → Derogation : very limited situations and not in a preemptive way

Codes Review

Accepting CFMs with

MPMs intent in the Codes

Cooperation among IOs IMF, BIS and OECD

Setting the clear Standards for CFMs to avoid

abusing

Not necessary to revise the Codes

New Understanding or Improving User’s Guide

More Adaptable and Stronger OECD Codes

< Process > < Outcome >

Inconsistent view : Addressing the issue

16

Thank����������� ������������������ You����������� ������������������ Thank You !!����������� ������������������

17