Embed Size (px)

Citation preview

INTRODUCTION TO MICROECONOMICSECO 110Msection 2345

Dr. Hamilton Lankford

Business Administration 111A [email protected] Office hours: Tuesday 10:30-11:30

Thursday 2:30- 3:30

and by appointment

Textbook:Principles of Economics, 3rd edition, by Gregory

Mankiw

Study Guide for Principles of Economics by David R. Hakes

Barnes & Nobles Mary Jane Books

Campus Center 215 Western Ave.

price: $107 price: $88

Course Websites

My website:

www.albany.edu/faculty/hamp/aeco110m/

Textbook websites:

http://mankiwxtra.swlearning.com

www.harcourtcollege.com/econ/mankiw/

Read a good news source to keep up with current economic issues.

New York Times

www.nytimes.com

Wall Street Journal

www.wsj.com

Economist Magazinewww.economist.com

GRADING

quiz Tuesday, Sept. 23 5% first exam Thursday, Oct. 9 20% quiz Thursday, Oct. 30 5% second exam Tuesday, Nov. 18 20% exercises and quizzes 15% cumulative final examination 35%

Monday, Dec. 15

This course is a social sciences general education course intended to help students better understand:

that human behavior is subject to scientific inquiry

the difference between rigorous and systematic thinking and uncritical thinking about social phenomena

the kinds of questions social scientists ask and the ways they go about answering these questions

the major concepts, models and issues of at least one discipline in the social sciences

the methods social scientists use to explore social phenomena.

Economics

Economics is the study of how individuals and society choose to

employ scarce resources to produce and distribute goods and services.

Scarcity . . .

. . . means that society has limited resources and therefore cannot produce all the goods and services people wish to have.

Economists study. . .

How individuals and organizations make decisions.

How individuals and organizations interact with each other.

The forces and trends that affect the economy as a whole.

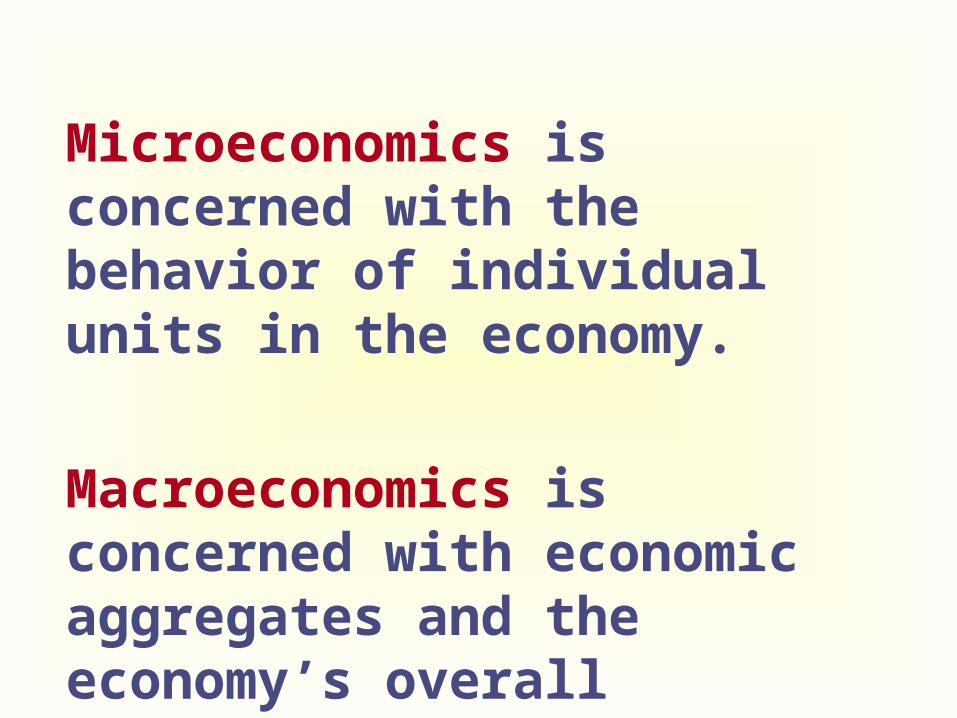

Microeconomics is concerned with the behavior of individual units in the economy.

Macroeconomics is concerned with economic aggregates and the economy’s overall performance.

The goal of this course is to help students understand, and think critically about, basic economic problems and current economic issues.

Understand the major economic problems of modern society.

Grasp basic economic principles and concepts.

Be able to use analytical tools to think about economic problems and issues.

The “economic way of thinking” ...

… is an approach emphasizing the process of applying economic concepts and principles in the analysis of economic issues and problems.

The study of economics is unified by several central ideas.

These ideas are reflected in the following ten principles:

1. People face tradeoffs.

To get one thing, we usually have to give up another thing. Guns v. butter Food v. clothing Leisure time v. work Efficiency v. equity

Making decisions requires trading off one goal against another.

2. The cost of something is what you give up to get it.

Decisions require comparing costs and benefits of alternatives.

Whether to go to college or to work? Whether to study or go out on a date? Whether to go to class or sleep in?

3. Rational people think at the margin.

Marginal changes are small, incremental adjustments to an existing plan of action.

People make decisions by comparing costs and benefits at the margin.

Consider the decision regarding studying or going out on a date.

4. People respond to incentives.

Marginal changes in costs or benefits motivate people to respond.

The decision to choose one alternative over another occurs when that alternative’s marginal benefits exceed its marginal costs!

5. Trade can make everyone better off.

People gain from their ability to trade with one another.

Competition results in gains from trading.

Trade allows people to specialize in what they do best.

6. Markets are usually a good way to organize economic

activity.

In a market economy, households decide what to buy and

who to work for, and firms decide who to hire and what to

produce.

7. Governments can sometimes improve market

outcomes.

When the market fails (breaks down) government often can intervene to

promote efficiency and equity.

8. The standard of living depends on a country’s

production.

Productivity is the amount of goods and services produced from each

hour of a worker’s time.

Higher productivity Higher standard of living

A Game of Jeopardy

Answer: compound interest

Question: What was Einstein’s answer to the question, ‘what is the human race’s greatest

invention?’‘what is the most powerful force in the

universe?’‘what is the greatest law of the universe?’

annual rate of increase in productivity1.60% 2.50%

years index of total outputpassed 100.0 100.0

1 101.6 102.52 103.2 105.13 104.9 107.74 106.6 110.45 108.3 113.16 110.0 116.07 111.8 118.98 113.5 121.89 115.4 124.9

10 117.2 128.0

15 126.9 144.8

20 137.4 163.9

30 161.0 209.8

40 188.7 268.5

50 221.1 343.7

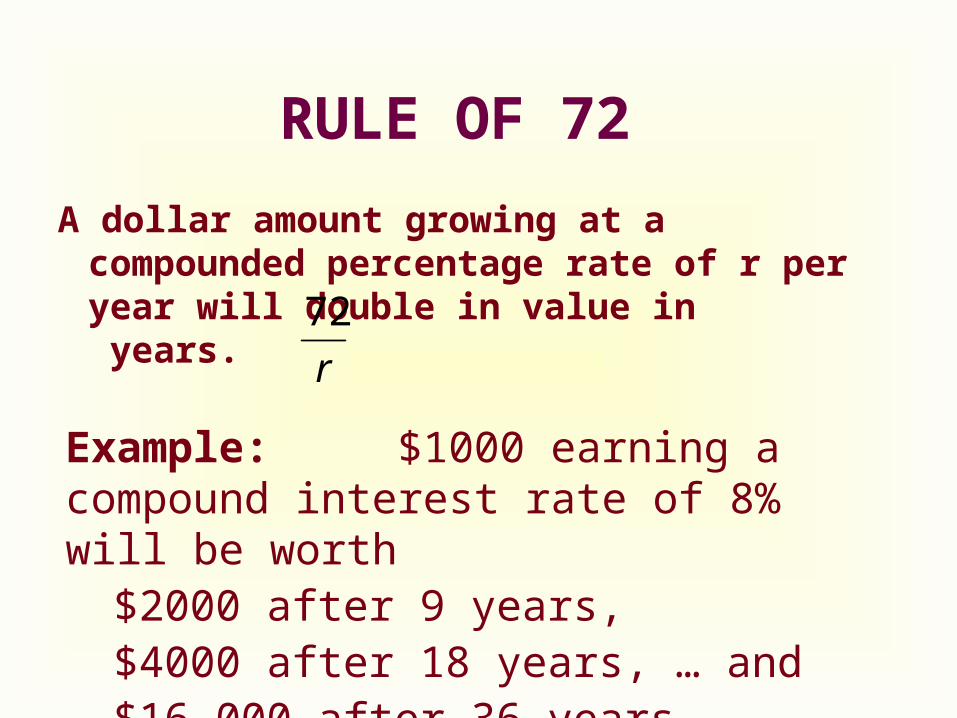

RULE OF 72

A dollar amount growing at a compounded percentage rate of r per year will double in value in years.

r

72

Example: $1000 earning a compound interest rate of 8% will be worth

$2000 after 9 years, $4000 after 18 years, … and $16,000 after 36 years.

9. Prices rise when the government prints too much

money.

Inflation is an increase in the overall level of prices in the economy.

One cause of inflation is the growth in the quantity of money.

When the government creates large quantities of money, the value of the money falls.

10. Society faces a short-run tradeoff between inflation and

unemployment.

Inflation Unemployment

This is a short-run tradeoff!

Summary

When individuals make decisions, they face tradeoffs.

Rational people make decisions by comparing marginal costs and marginal benefits.

Summary

People can benefit by trading with each other.

Markets are usually a good way of coordinating trades.

Government can potentially improve market outcomes.

The “economic way of thinking” is an approach emphasizing the process of applying economic concepts and principles in the analysis of economic issues problems.

Why many students find economics difficult?

Economics has its own language, employing precise meanings of words.

Economics is at times abstract and employs models as tools of analysis.

The emphasis on understanding and analysis has implications regarding

the way you study.

Be open to the study tips in the syllabus!

Auction - Case 1

oral sequential bids ($1.00 increments)

highest bidder gets $20.00. highest bidder pays last bid. no collusion.

Illustration of the effects of incentives on behavior

Auction - Case 2

oral sequential bids ($1.00 increments)

highest bidder gets $20.00. Second highest bidder pays last bid. no collusion.