Embed Size (px)

Citation preview

How to grow against the odds?

Workshop with The Boston Consulting Group

10:45 – 12:00

Götz Gerecke, Nicolas Kachaner, Kermit King

medtechforum.eu

1

Corporate portfolio strategy

Identify areas to accelerate growth in the current portfolio and seek out new platforms for growth

Organizational growth enablers

Create growth mindset and remove internal barriers to growth

Business model innovation

Reinvent offering and/or operating model

M&A

Acquire or partner for access, scale, capability

Innovation

Enhance offering through successful organic innovation

Geographic expansion

Enter and grow in new markets

Go-to-market transformation

Near-term commercial initiatives

Where

to play

Maximize

the core

Expand into

adjacencies

Explore new

frontiers

Drive higher demand, penetration

or share in current fields of play

Project advantage into adjacent fields

of play (e.g. channel, category, geo)

Create or position to exploit

new emerging fields of play

| How

to win

1

2

3

4

5

6

7

Place your bets

2

Voting

Which of the following seven levers are most important to address to accelerate

profitable growth in your organization (please select up to three):

a) Corporate portfolio strategy

b) Go-to-market model transformation

c) Geographic expansion

d) Innovation

e) M&A

f) Business model innovation

g) Organizational growth enablers

LEVER 2: GO-TO-MARKET

MODEL TRANSFORMATION Near-term commercial initiatives

3

Pricing and reimbursement pressure

Stakeholders increasingly demanding value proofs

Shift in decision making to economic buyers and

market access authorities

New commercial model

for emerging markets

Innovation productivity declining

4

MedTech GTM model challenges Survey of 4'500 employees across 38 MedTech

businesses in US, EU-5, JP and BRIC countries

medtechforum.

eu

Particularly strong in Most often cited Least often cited

Key challenges reported in Commercial Benchmarking study

1

2

3

4

5

Source: BCG Commercial Excellence Benchmarking Study in Med Tech 2012 (4,500 employees surveyed)

5

MedTech today: Still high price

realization ...

COGS: Costs of Goods Sold Source: BCG Value Science Database; BCG Commercial Excellence Benchmarking in Med Tech 2012

1.6

2.4 2.2

3.6

Sales indexed to COGS (COGS = 1.0)

medtechforum.

eu

Revenue earned for each dollar of COGS

Medical Devices Medical Equipment High Tech Industrial Goods

> 1.5×

6

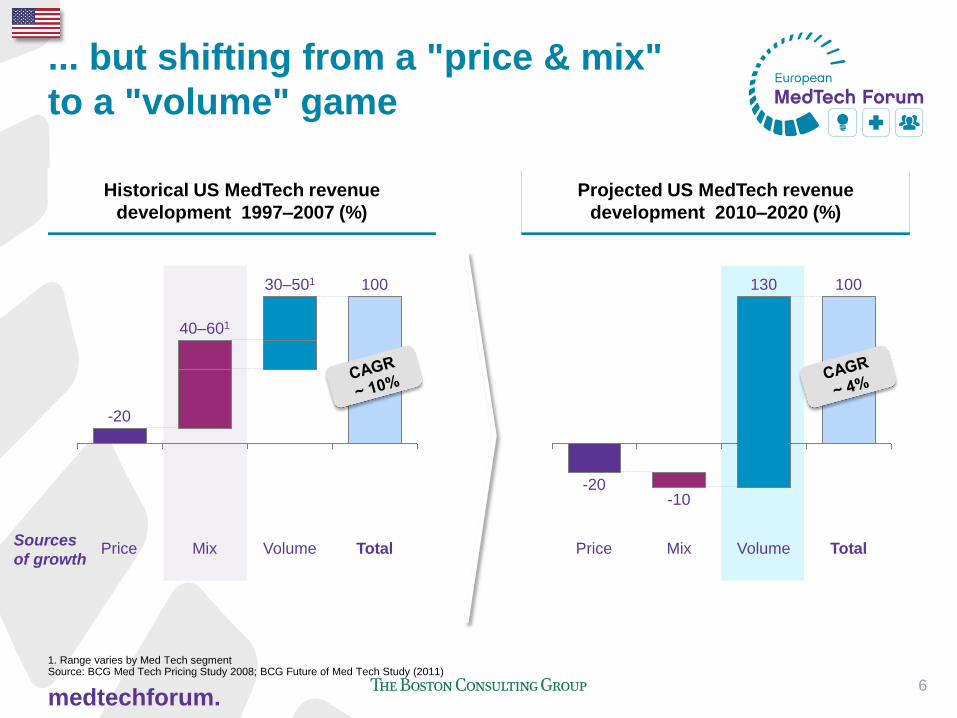

... but shifting from a "price & mix"

to a "volume" game

1. Range varies by Med Tech segment Source: BCG Med Tech Pricing Study 2008; BCG Future of Med Tech Study (2011)

medtechforum.

eu

Historical US MedTech revenue

development 1997–2007 (%)

Projected US MedTech revenue

development 2010–2020 (%)

-20

40–601

Price Total

100

Mix

30–501

Volume Total

100

Volume

130

Mix

-10

Price

-20

Sources

of growth

7

Even more substantial price pressure

in Europe

Source: BCG Future of MedTech Study; BCG Commercial Excellence Benchmarking Study in MedTech 2012

medtechforum.

eu

Projected US MedTech revenue

development 2010–2020 (%)

Projected European MedTech revenue

development 2010–2020 (%)

-20 -10

Price Total

US

100

Mix

130

Volume Total

Europe

100

Volume

145

Mix

-10

Price

-35

Sources

of growth

8

Unsustainably high commercial cost

structure

1. SG&A: Selling, General, and Administrative expenses (in this chart includes R&D expense) 2.COGS: Costs of Goods Sold Source: BCG Value Science Database; Company SEC reports; BCG Commercial Excellence Benchmarking in Med Tech 2012

0.3

1.6

0.5

2.4

0.9

2.2

1.7

3.6

SG&A indexed to COGS (COGS = 1.0)

Sales indexed to COGS (COGS = 1.0)

medtechforum.

eu

Revenue earned and SG&A spent for each dollar of COGS

Medical Devices Medical Equipment High Tech Industrial Goods

> 1.5×

> 3.5×

9

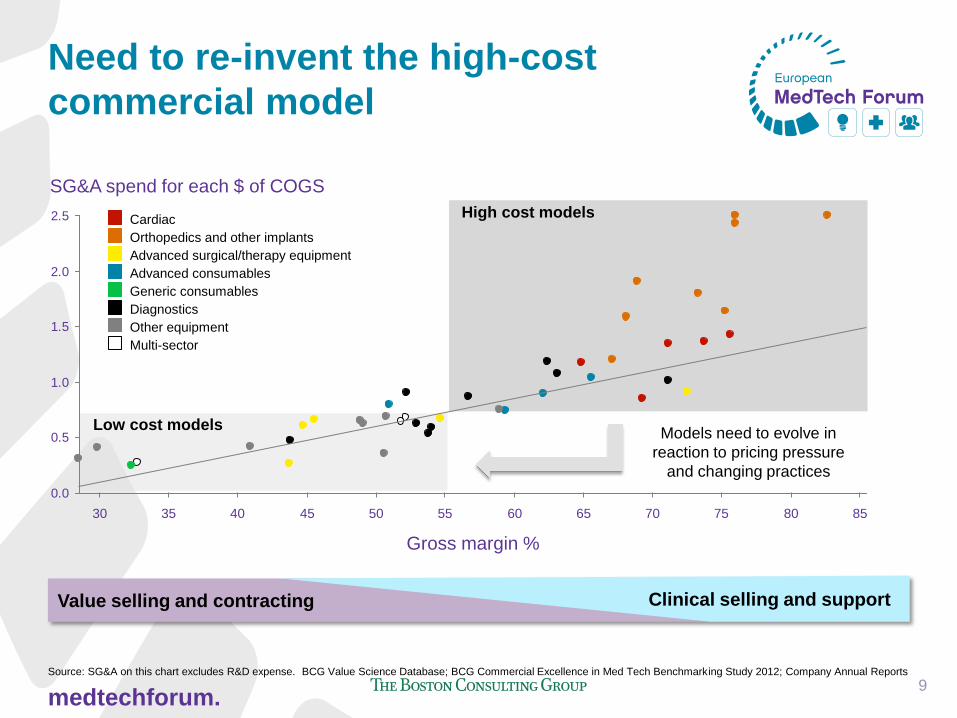

Need to re-invent the high-cost

commercial model

Source: SG&A on this chart excludes R&D expense. BCG Value Science Database; BCG Commercial Excellence in Med Tech Benchmarking Study 2012; Company Annual Reports

medtechforum.

eu

Value selling and contracting Clinical selling and support

0.0

0.5

1.0

1.5

2.0

2.5

45 40 35 30 50 85 80 75 70 65 60 55

Gross margin %

SG&A spend for each $ of COGS

Orthopedics and other implants

Advanced surgical/therapy equipment

Advanced consumables

Generic consumables

Diagnostics

Other equipment

Multi-sector

Cardiac High cost models

Low cost models Models need to evolve in

reaction to pricing pressure

and changing practices

10

Three archetype selling models in the

market today

Source: BCG's Commercial Excellence Benchmarking Study 2012

Clinical model Hybrid-model Admin model

Lower SG&A Higher SG&A

Value selling and contracting Clinical selling and support

Companies need to change the mix of these three models

medtechforum.

eu

11

Admin model with 2–3x higher rep

productivity than clinical

Source: BCG Commercial Excellence Benchmarking Study in Med Tech 2012

0

2

4

6

8

10

Revenue 2011/Sales Rep (in M$)

Clinical Hybrid Admin

Max

Min

majority

of players

5.9 2.9 1.7 Average

(in M$)

0

2

4

6

8

10

Revenue 2011/Sales Rep (in M$)

Clinical Admin Hybrid

medtechforum.

eu

3.1 2.3 1.3 Average

(in M$)

Rep productivity higher in the US than in EU5,

primarily driven by higher price levels

12

Access-buying process also evolving

by type of market

Source: BGC

Access driven market Demand driven market

Potential access guidance by region/

GPOs, price and conditions set by

hospitals, demand driven

by surgeons

Access granted/restricted by regional

authorities, payers or GPOs, with

hospitals still influencing demand

Price and conditions set by individual

hospitals, demand driven by

surgeons' choice

Clinical selling Value selling

Three archetypes of markets, requiring different models

Demand/access

driven markets

BCG's demand-access continuum

medtechforum.

eu

Reimburs. planning and execution

Information Technology

KOL and stakeholder management

13

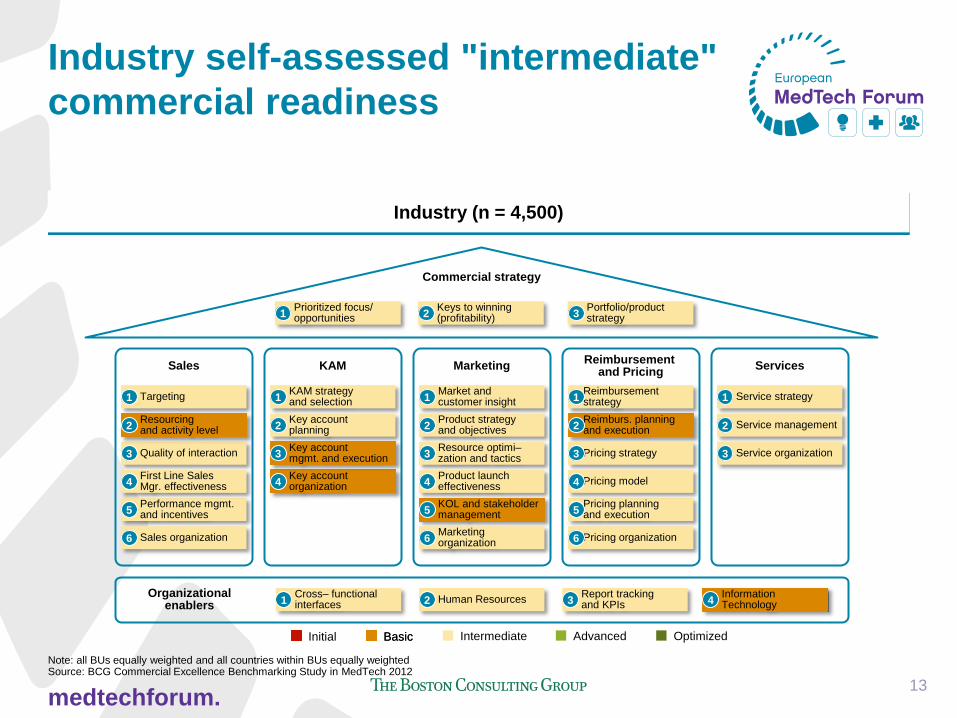

Industry self-assessed "intermediate"

commercial readiness

Note: all BUs equally weighted and all countries within BUs equally weighted Source: BCG Commercial Excellence Benchmarking Study in MedTech 2012

medtechforum.

eu

Industry (n = 4,500)

Intermediate Initial Advanced Optimized Basic

Commercial strategy

Service strategy

Service management

Service organization

Services

Performance mgmt. and incentives

Targeting

Quality of interaction

First Line Sales Mgr. effectiveness

Sales organization

Sales

KAM strategy and selection

Key account planning

KAM

Market and customer insight

Product strategy and objectives

Resource optimi– zation and tactics

Product launch effectiveness

Marketing

Organizational enablers

Cross– functional interfaces

Human Resources Report tracking and KPIs

Pricing planning and execution

Reimbursement strategy

Pricing strategy

Pricing model

Pricing organization

Reimbursement and Pricing

Marketing organization

Keys to winning (profitability)

Prioritized focus/ opportunities

Portfolio/product strategy

1

2

3

1

3

4

5

6

1

2

3

4

5

1 2 3

1

2

3

4

5

6

4

6

2 1 3

Key account organization

Key account mgmt. and execution

1

2

3

4

Resourcing and activity level 2

Basic

14

BCG recommends six transformation

moves to win in the near term

medtechforum.

eu

Partner with key

accounts

3

Invest in pricing

and reimbursement

capabilities

5

Make service a

differentiator and

a source of revenue

6

Strategy

De-average your

go-to-market

strategy and

commercial model

1

Front office

Reinvent clinical

selling

2 Build real marketing

muscle that drives

home the value proof

4

Back office

Source: BCG Commercial Excellence Benchmarking Study in MedTech 2012

LEVER 6: BUSINESS MODEL

INNOVATION Reinvent offering and/or operating model

15

medtechforum.eu

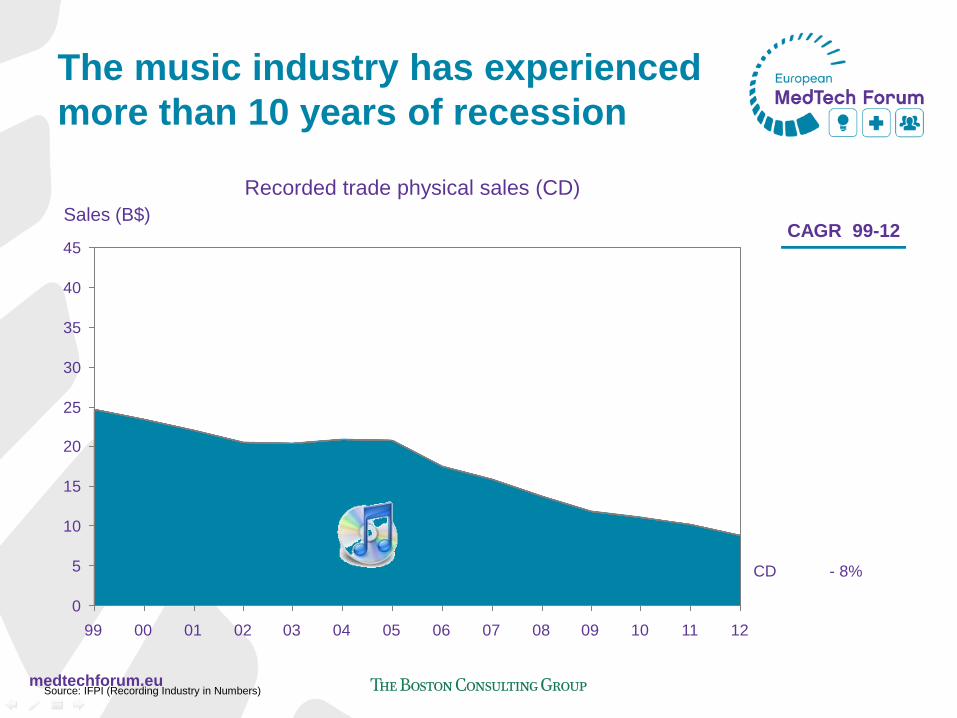

The music industry has experienced

more than 10 years of recession

Recorded trade physical sales (CD)

Source: IFPI (Recording Industry in Numbers)

45

25

40

35

30

20

15

10

5

0

CD

12 11 10 09 08 07 06 05 04 03 02 01 00 99

Sales (B$) CAGR 99-12

- 8%

medtechforum.eu

But smart incumbents have

generated new revenue streams

"The music industry is growing, the record industry is not growing"

WMG's CEO - Edgar Bronfman, June 2007

1. CAGR 06-12

Source: IFPI (Recording Industry in Numbers), BCG Study for UM

+14%

+5%

+7%

+3%

+16%1

-8%

+1%

CAGR

99-12

0

10'000

20'000

30'000

40'000

Recorded physical music

Sales (B$)

99

Recorded digital music

Publishing

Touring

Merchandising

Sponsoring

12 11 10 09 08 07 06 05 04 03 02 01 00

medtechforum.eu

Nespresso: Reinventing the mature

coffee market

• Nestlé was already #1 in coffee worldwide

• Nespresso incubated in a separate BU

medtechforum.eu

Coffee market

Nespresso

Nespresso's

share

Profit

(CHF m)

300

35%

100+

Value

(CHF bn)

8–10

5–6

> 50%

Sales

(CHF m)

2'900

20%

573

Volume

(kt)

223

3%

6.3

Growth

(p.a.)

~ 0%

> 20%

> 100%

Value created is very significant

Example: Switzerland and France

medtechforum.eu

Mercedes: From selling trucks to

selling kilometers

Source: BCG Automotive Practice

Customer as system integrator Supplier as system integrator

Customer

Manufacturer Mercedes Charterway Dealer

Distribution

Admin.

Development

Manufacturing

Purchasing

Financing

Spare parts

Service

Margin

Financing

Overhead and selling commission

Depreciation

Running cost (registration, repairs, etc.)

Truck

mounting

Service

Inspection

Spare

parts

Financing

Contract

•

•

•

•

•

DM

From product to service, leveraging existing

structures, borrowing from other industries

medtechforum.eu

What is a business model ?

Value proposition

Operating model

Business model

Target

segment

Product/ service

offering

Revenue

model

Value chain Cost

Model Organization

medtechforum.eu

Understanding the spectrum of

choices is useful to guide a

Business Model diagnostic

• Existing

• Underserved

• Non users

• Adjacencies

• New markets

• Product

• Product

bundle

• Service

• Service

bundle

• Experience /

relationship

• Outcome /

facilitation

• Per unit sold

• "Razor

model"

• Subscription /

license

• Dynamic

pricing

• Per unit used

• Results

based / risk-

sharing

• Single step

focus

• Horizontal

integration

• Vertical

integration

• Orchestration

• Low cost

• Premium

• Fixed vs

Variable

• Asset Light

• By product

• By geography

• By customer

group

• By business

model

Target

segment Offering

Revenue

model Value Chain Cost model Organization

Value proposition Operating model

medtechforum.eu

7 major business model innovation

patterns

1) Trading up / trading down (low cost)

2) From product to service - Variabilization

3) Asset light (orchestrators) vs. integrators

4) Direct distribution

5) Free and 'razor & blade'

6) Open – ecosystems

7) Digital

Nike

medtechforum.eu

Organizing for BMI: value of a separate

incubation

Separate low cost fleet

Separately run

Separate labor contracts

Low cost

Mid-level prices

Clearly different brand

Differentiated offering between parent airline and

lowest cost airlines

Accessing new customers

Same mgmt team

Walled-off portion of parent fleet

No real labor cost advantage

Lower unit cost via

larger airplane

Low pricing for many seats, but

“managed up”

Differentiation limited to on-board

experience

Cannibalizing offering (better

value than Delta)

Customer confusion

Results:

Profitable,

growing

Results:

Reabsorbed

into parent

medtechforum.eu

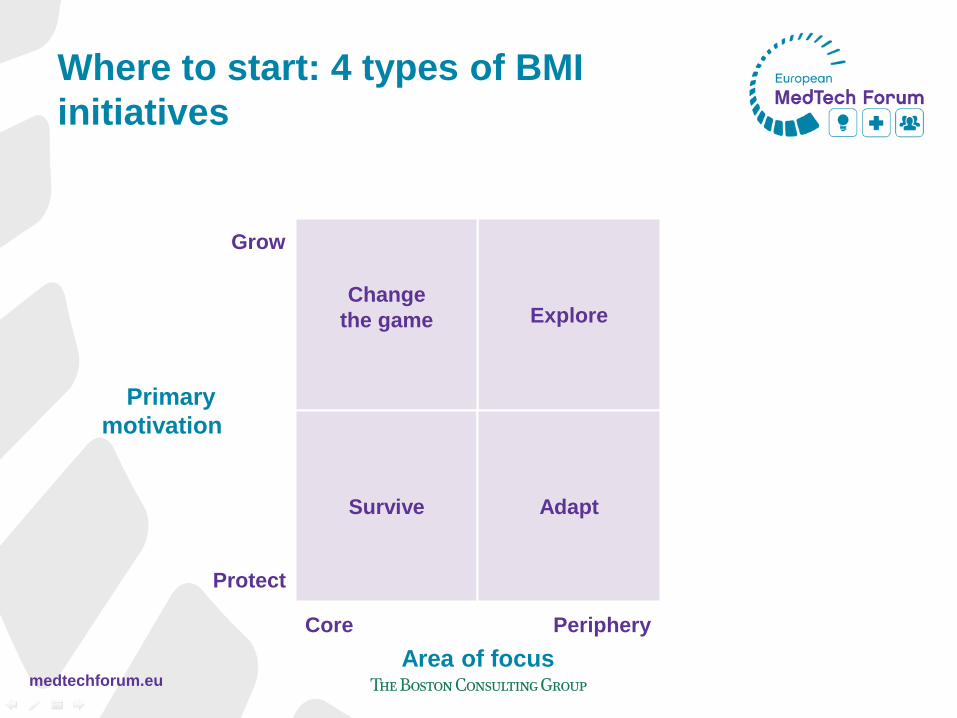

Where to start: 4 types of BMI

initiatives

Explore Change

the game

Survive Adapt

Core Periphery

Area of focus

Protect

Grow

Primary

motivation

medtechforum.eu

Core Periphery

Area of focus

Protect

Grow

Primary

motivation

Example: GE Health Care filling the

matrix

Partner

3rd party Consulting

Asset

Management

Teleradiology

Home

Health

Pay per use

Miniaturir-

-zation

medtechforum.eu

Some lessons

• Business model innovation (BMI) can create massive value

– Even in mature or declining markets (music, coffee, trucks,…)

– As an incumbent or as an attacker

• BMI should be managed like any R&D activity

– Dedicated resources, systematic approach

– Project portfolio, trial and error (pilots)

– Open research: learn from outside

• New models often benefit from separate incubation

– Dual branding often adviseable

• Successful BMI does not require breakthrough innovation

– Following is usually OK

– Execution quality more decisive than novelty

medtechforum.eu

SIX ESSENTIALS

28

medtechforum.eu 29

Voting

Which of the following six success factors represents the greatest barrier to

profitable growth in your organization (please select up to three):

a) Set your aspiration

b) Know your advantage

c) Stretch the thinking

d) Force tough choices

e) Fund the journey

f) Build aligned capability

30

1. Set your aspiration

Six essentials

31

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Net sales

(M$)

Historical growth

Current trajectory

Aspirational growth

+3.9%

+10% Growth gap

+2.3%

% CAGR 1998–2003 % CAGR 2003–2008

Source: BCG case experience

Defining the gap

32

0

20

40

60

80

100

-20 0 20 40 60

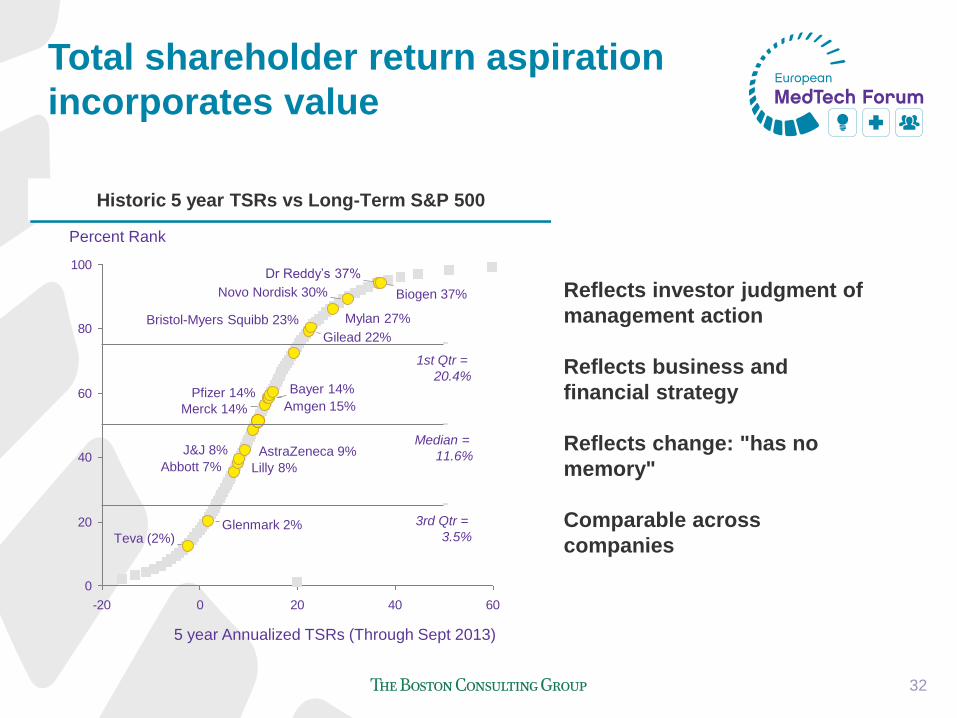

Percent Rank

5 year Annualized TSRs (Through Sept 2013)

Dr Reddy’s 37%

Biogen 37% Novo Nordisk 30%

Mylan 27% Bristol-Myers Squibb 23%

Gilead 22%

Amgen 15%

Bayer 14% Pfizer 14%

Merck 14%

AstraZeneca 9% J&J 8%

Lilly 8% Abbott 7%

Glenmark 2% Teva (2%)

3rd Qtr =

3.5%

Median =

11.6%

1st Qtr =

20.4%

Historic 5 year TSRs vs Long-Term S&P 500

Reflects investor judgment of

management action

Reflects business and

financial strategy

Reflects change: "has no

memory"

Comparable across

companies

Total shareholder return aspiration

incorporates value

33

"I will build a motor car for the great

multitude. It will be so low in price that

any man making a good salary will be

able to own one—and enjoy God’s

great open spaces"

Henry Ford

34

1. Set your aspiration

2. Know your advantage

Six essentials

35

36

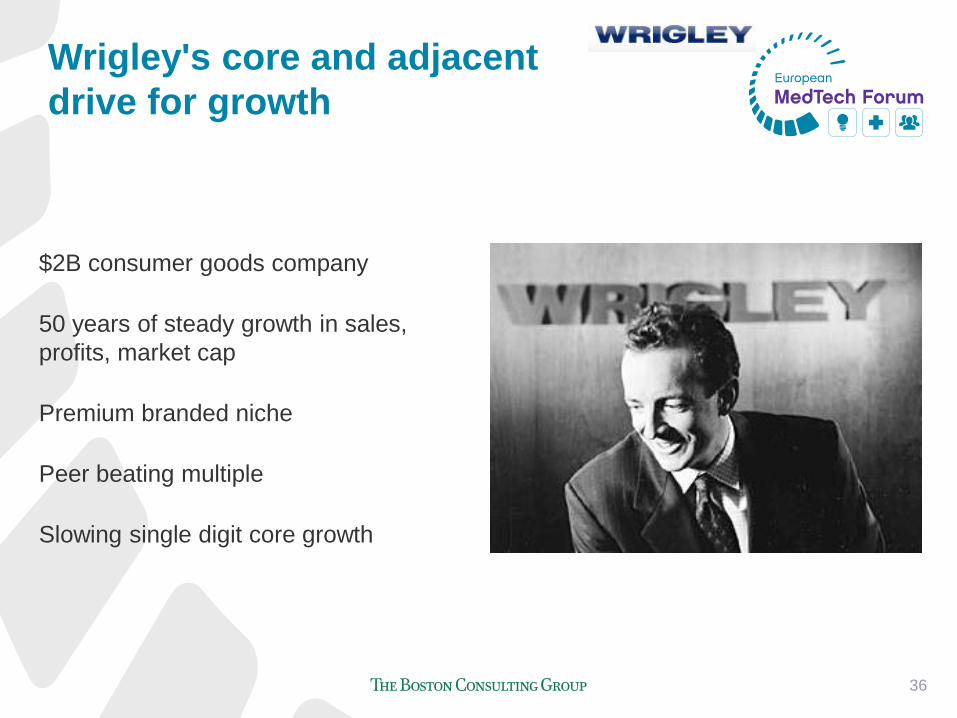

$2B consumer goods company

50 years of steady growth in sales,

profits, market cap

Premium branded niche

Peer beating multiple

Slowing single digit core growth

Wrigley's core and adjacent

drive for growth

Brand management

Branded share (%)

Importance of flavor

Value density ($/M )

Shelf life (months)

% Sold in impulse locations

Purchase frequency

(x/year)

HH Penetration (%)

Ad spend as % of sales

Gross margin

Relative market share Industry

structure

Innovation Selling and

merchandising

~15%

~60%

~2

~95%

5

~9K

~12

~90%

~14x

~70%

Sales

OP

RTSR

'98 - 05

2.1x

2.0x

1.5x

37

Wrigley's core and adjacent

drive for growth

Importance

today

Importance

in 2014

Degree of

advantage

• Local market knowledge (customers, consumers)

• Advantaged cost position

• Ability to pilot initiatives in low-risk ways

• Ability to efficiently scale (latent advantage)

38

1 2 3 4 5

Not important Very important

Not advantaged Highly advantaged

Response scale

• XXX national brand

• Strong, local geographic brands

• Credibility

4

4 4 3

4

4

4

5 5

5

5

5

5

5

5

5

5 5 5

5

4

5

3 4

5

5

5

5

5

5

4

5 2 3

5

3

4

3 5

4

1

5

5

3

4

• National online verticals

• Online marketing advertising services

– Local (latent advantage)

– National

• Culture: Productive, resilient, loyal employees (Great executors)

• Strong editorial staff across platforms/media

• Strong balance sheet (generate cash flow, pay down debt, invest)

• Access to major customers

• Largest local sales and news-curation staffs (newspaper markets)

• Large audience reach (aggregated audience is increasing)

Positions, capabilities or assets which

potentially confer Client advantage

The "advantage audit"

39

1. Set your aspiration

2. Know your advantage

3. Stretch the thinking

Six essentials

40

Where to play

Maximize

the core

Expand into

adjacencies

Explore new

frontiers

Faint signals

Favoritism

Trade up/down

Extend advantage

Periphery

Repeatability

Look out, look in

Partnerships

BMI archetypes

Wider field of vision

41

1. Set your aspiration

2. Know your advantage

3. Stretch the thinking

4. Force tough choices

Six essentials

42

43

1

2

3

SIZE OF PRIZE

RIGHT TO WIN

PATH TO ACHIEVE

Attractiveness

Advantage

Rigorous qualification of ideas

44

Option

lens

Reinforcement

lens

Cluster

lens

Collective

lens

+

+

+

Ideas must be evaluated in context

45

1. Set your aspiration

2. Know your advantage

3. Stretch the thinking

4. Force tough choices

5. Fund the journey

Six essentials

46

0

20

40

60

80

0 3

23

75

% performers

Neither Margin Only Growth Only Both growth and margin

0

20

40

60

80

% performers

2 6

23

69

0

20

40

60

80

% performers

2 9

45 44

0

20

40

60

80

13 6

56

25

% performers

Top Quartile TSR 2nd Qtr TSR 3rd Qtr TSR Bottom Qtr TSR

Based on S&P Global 1200, 2003-2012 Source: Capital IQ; BCG analysis

Top value creators simultaneously

grow revenue and improve margins

47

Initiative Description Addressable cost base Owner

COGS improvement

and promo optimization

• Negotiate vendor contracts to improve margin

• Standardization of methodologies & process

XX XX

Indirect Sourcing and

Procurement

• Reduce indirect sourcing costs through standardization of

processes and centralization of systems

XX XX

Business Process

Outsourcing

• Increase portion of labor pool outsourced/offshored XX XX

Sales Force • Headcount reduction, increase use of inside sales force,

productivity improvements

XX XX

Bank Charges • Incentivize customers to use different payment options XX XX

Logistics/Supply Chain

• Network

• Inventory

• Consolidate, optimize, and align delivery network

• Optimize inventory stocking decisions fo sales and margin

XX XX

Division A:

• Store labor

• Inventory

• IT

• Operational improvement

• Network optimization

• Payroll optimization

• Inventory reduction

• Transition to VOIP

• POS improvements

• Close closure/downsizing

XX XX

Division B:

• Customer service

• Reduce call center contacts through self-service options

XX XX

Division C:

• Store closure and

downsizing

• Store labor

• Property sale &

leaseback

• Close underperforming stores

• Downsizing of stores

• Rationalize store management structure

• Adjust or redeploy level of hourly staff labor

• Sell store and home office properties and leaseback

XX XX

Example: funding the reinvention

48

1. Set your aspiration

2. Know your advantage

3. Stretch the thinking

4. Force tough choices

5. Fund the journey

6. Build aligned capability

Six essentials

49

• Effective, strategic HQ selling

• Best-in-class category management and distribution

• Strategic customer/channel segmentation/targeting

• Effective trade spend and merchandising

• Cutting edge data and analytics

• Flawless retail execution

• Synced sales/marketing

• End-to-end supply chain built for lowest cost

• Net revenue management/pricing and margin optimization

• Unparalleled safety

• Organizational efficiency

• Aligned culture and dedication to success

• Agility/flexibility to support growth and innovation

• Differential, effective concept to market processes and metrics

• Sustained post-launch support

• Culture of innovation and learning

• Holistic organization alignment

• Clear, expansive definition of innovation

• Clear innovation strategy linked to division/function strategies

• Comprehensive market, trend, and consumer knowledge

• Optimal media mix

• Product quality linked to brand strategies

• Effective consumer targeting/messaging

• Clear portfolio strategy and aligned resources

• Deep consumer/shopper empathy

• Effective insights to action

• Brand positioning, extendibility

• Agency management

• Price architecture

Leading customer

growth

Operational

excellence

Breakthrough

innovation

Brand

building

Current gap

Client strength

Mixed strength/gap

Capabilities evaluation

50

Gannett's transformation

51

Gannett's transformation

medtechforum.eu 52

Final voting

If your organization made a special effort to accelerate profitable growth, by

how much do you think you can flex your momentum trajectory:

a) +1% p.a.

b) +2%

c) +3%

d) +4%

e) +5% and more

53

Thank you!

Götz Gerecke Partner, BCG Zurich Mail to : [email protected] Phone : +41 79 373 8631

Nicolas Kachaner Senior Partner, BCG Paris Mail to : [email protected] Phone : +33 6 17 81 36 36

Kermit King Senior Partner, BCG Chicago Mail to : [email protected] Phone : +1 312 498 45671