Embed Size (px)

Citation preview

How to address NPLs:

The experience of the Italian

and Spanish banking sectors

Marco Lamandini, Giuseppe Lusignani, David Ramos

Lisbon, 1 June 2017

AGENDA

• The elephant in the room: a descriptive and visual approach

• Strategic decision – making matrix

• Hard choices

• Italy – The reluctant chooser

• Italy – Choosing now

• The Spanish case: multiple choosers in town

• Conclusions

The elephant: a descriptive approach

• Post-crisis deterioration of banks’ loan portfolios in advanced countries

• US bad loans/total loans ratio peaks 2009 5% then declined – in Europe it

kept rising (modest decline in June 2016 to 5.4%).

• Almost EUR 1 Trillion (gross terms), EUR 475 Billion (net terms) 5.7%

of total loans, 10% of the area’s GDP.

• Intra-EU uneven distribution of the problem: Italy/Portugal values (net

exposures) 4 x Euro average; Cyprus/Greece 10 x Euro average. > 10% EU

St. ratios > 10% (EBA).

• National differences depend also on legal/judiciary system: recovery rates

and recovery process: 10% difference in provisioning depending on duration

of court proceedings (EBA).

• Significant dispersion: for large banks the NPL ratio is below 4%

whereas for smaller banks it is approximately 25% (Andrea Enria).

The elephant at a glance (I). Uneven distribution

Source: B. Bruno, G. Lusignani, M. Onado, ‘A securitisation scheme for resolving Europe’s problem loans’,

forthcoming.

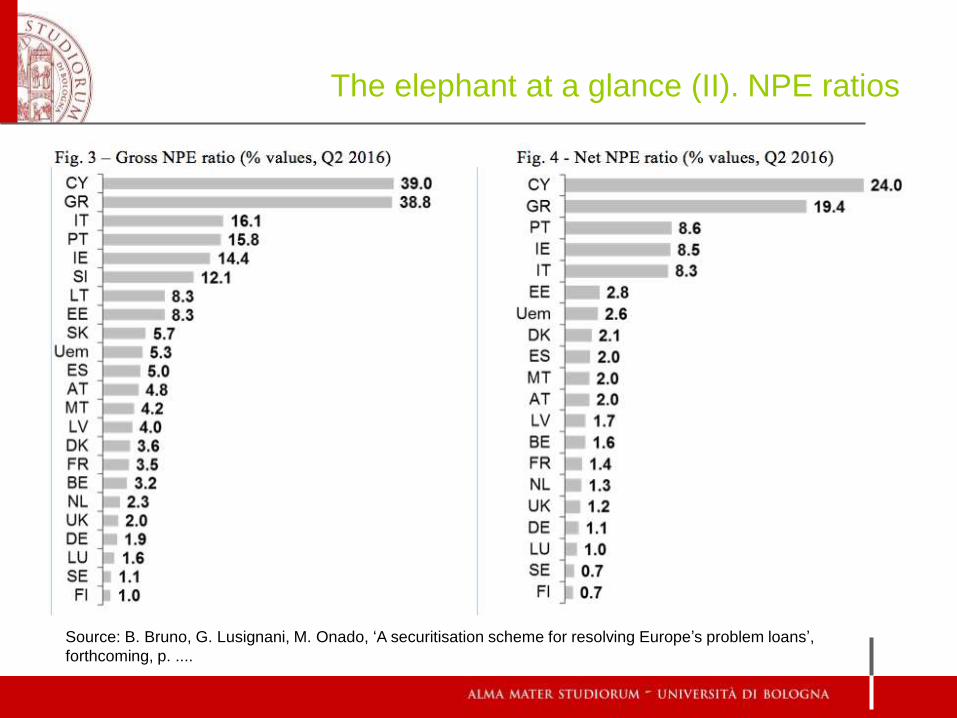

The elephant at a glance (II). NPE ratios

Source: B. Bruno, G. Lusignani, M. Onado, ‘A securitisation scheme for resolving Europe’s problem loans’,

forthcoming, p. ....

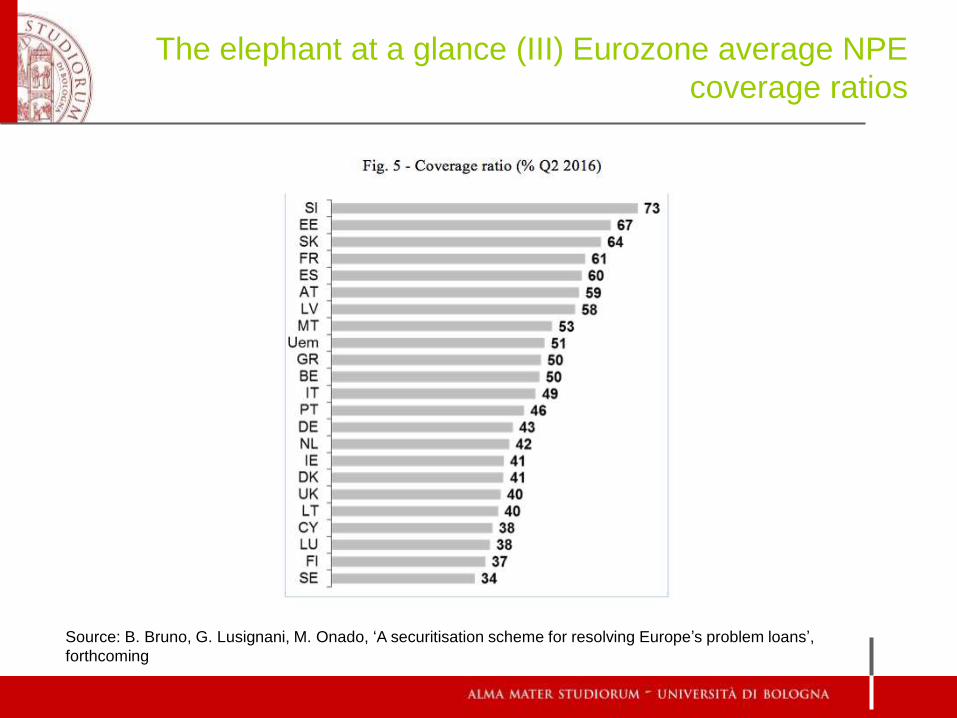

The elephant at a glance (III) Eurozone average NPE

coverage ratios

Source: B. Bruno, G. Lusignani, M. Onado, ‘A securitisation scheme for resolving Europe’s problem loans’,

forthcoming

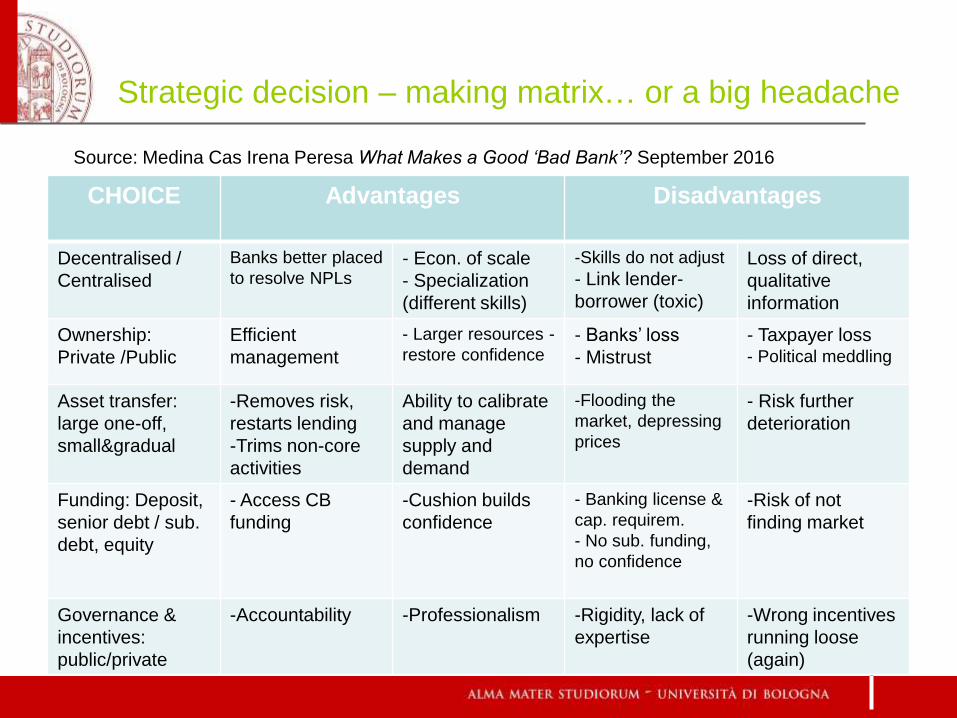

Strategic decision – making matrix… or a big headache

CHOICE Advantages Disadvantages

Decentralised /

Centralised

Banks better placed

to resolve NPLs- Econ. of scale

- Specialization

(different skills)

-Skills do not adjust

- Link lender-

borrower (toxic)

Loss of direct,

qualitative

information

Ownership:

Private /Public

Efficient

management

- Larger resources -

restore confidence- Banks’ loss

- Mistrust

- Taxpayer loss- Political meddling

Asset transfer:

large one-off,

small&gradual

-Removes risk,

restarts lending

-Trims non-core

activities

Ability to calibrate

and manage

supply and

demand

-Flooding the

market, depressing

prices

- Risk further

deterioration

Funding: Deposit,

senior debt / sub.

debt, equity

- Access CB

funding

-Cushion builds

confidence

- Banking license &

cap. requirem.

- No sub. funding,

no confidence

-Risk of not

finding market

Governance &

incentives:

public/private

-Accountability -Professionalism -Rigidity, lack of

expertise

-Wrong incentives

running loose

(again)

Source: Medina Cas Irena Peresa What Makes a Good ‘Bad Bank’? September 2016

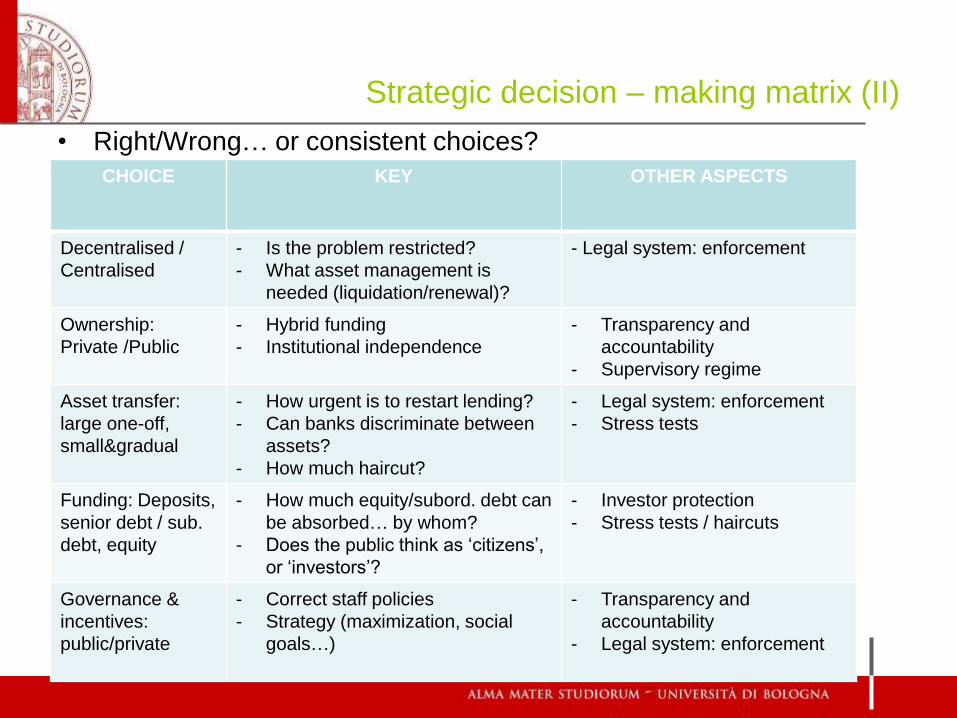

Strategic decision – making matrix (II)

• Right/Wrong… or consistent choices?

CHOICE KEY OTHER ASPECTS

Decentralised /

Centralised

- Is the problem restricted?

- What asset management is

needed (liquidation/renewal)?

- Legal system: enforcement

Ownership:

Private /Public

- Hybrid funding

- Institutional independence

- Transparency and

accountability

- Supervisory regime

Asset transfer:

large one-off,

small&gradual

- How urgent is to restart lending?

- Can banks discriminate between

assets?

- How much haircut?

- Legal system: enforcement

- Stress tests

Funding: Deposits,

senior debt / sub.

debt, equity

- How much equity/subord. debt can

be absorbed… by whom?

- Does the public think as ‘citizens’,

or ‘investors’?

- Investor protection

- Stress tests / haircuts

Governance &

incentives:

public/private

- Correct staff policies

- Strategy (maximization, social

goals…)

- Transparency and

accountability

- Legal system: enforcement

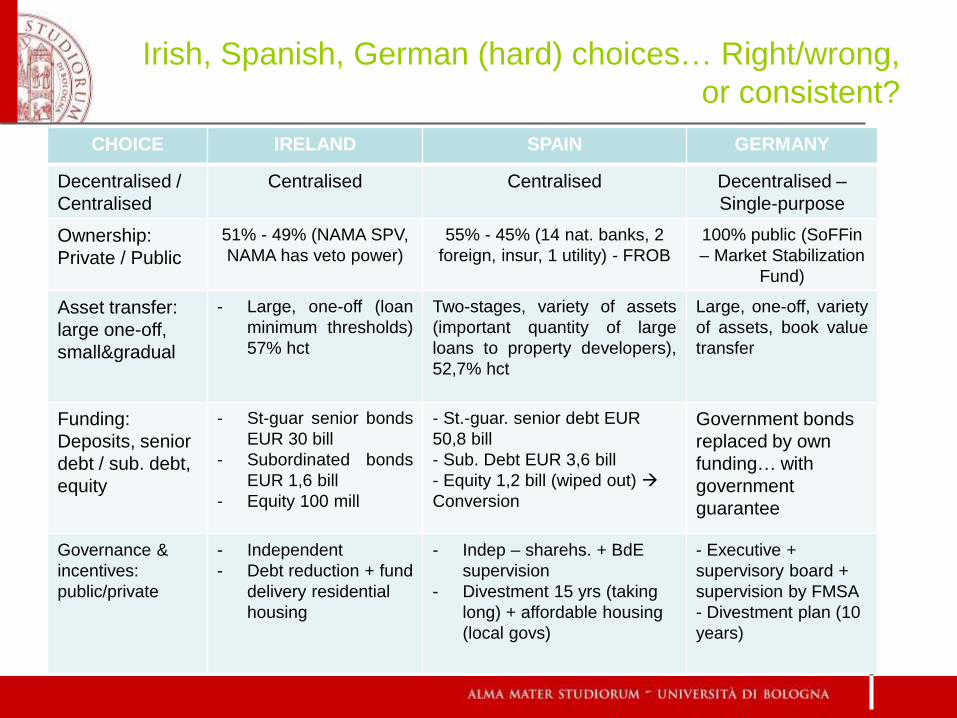

Irish, Spanish, German (hard) choices… Right/wrong,

or consistent?

CHOICE IRELAND SPAIN GERMANY

Decentralised /

Centralised

Centralised Centralised Decentralised –

Single-purpose

Ownership:

Private / Public

51% - 49% (NAMA SPV,

NAMA has veto power)

55% - 45% (14 nat. banks, 2

foreign, insur, 1 utility) - FROB

100% public (SoFFin

– Market Stabilization

Fund)

Asset transfer:

large one-off,

small&gradual

- Large, one-off (loan

minimum thresholds)

57% hct

Two-stages, variety of assets

(important quantity of large

loans to property developers),

52,7% hct

Large, one-off, variety

of assets, book value

transfer

Funding:

Deposits, senior

debt / sub. debt,

equity

- St-guar senior bonds

EUR 30 bill

- Subordinated bonds

EUR 1,6 bill

- Equity 100 mill

- St.-guar. senior debt EUR

50,8 bill

- Sub. Debt EUR 3,6 bill

- Equity 1,2 bill (wiped out)

Conversion

Government bonds

replaced by own

funding… with

government

guarantee

Governance &

incentives:

public/private

- Independent

- Debt reduction + fund

delivery residential

housing

- Indep – sharehs. + BdE

supervision

- Divestment 15 yrs (taking

long) + affordable housing

(local govs)

- Executive +

supervisory board +

supervision by FMSA

- Divestment plan (10

years)

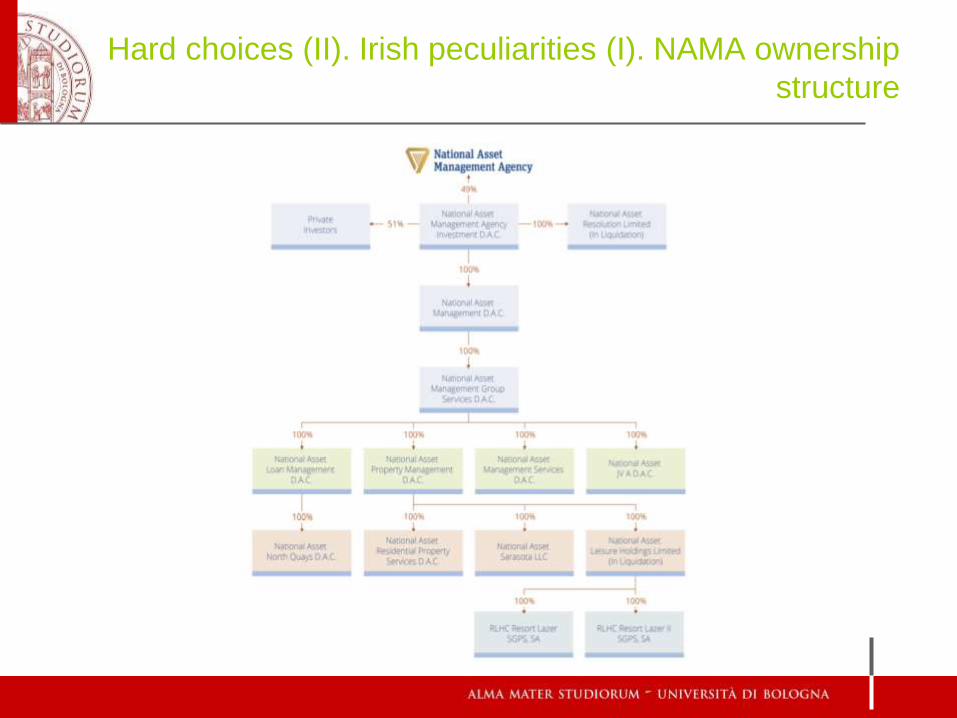

Hard choices (II). Irish peculiarities (I). NAMA ownership

structure

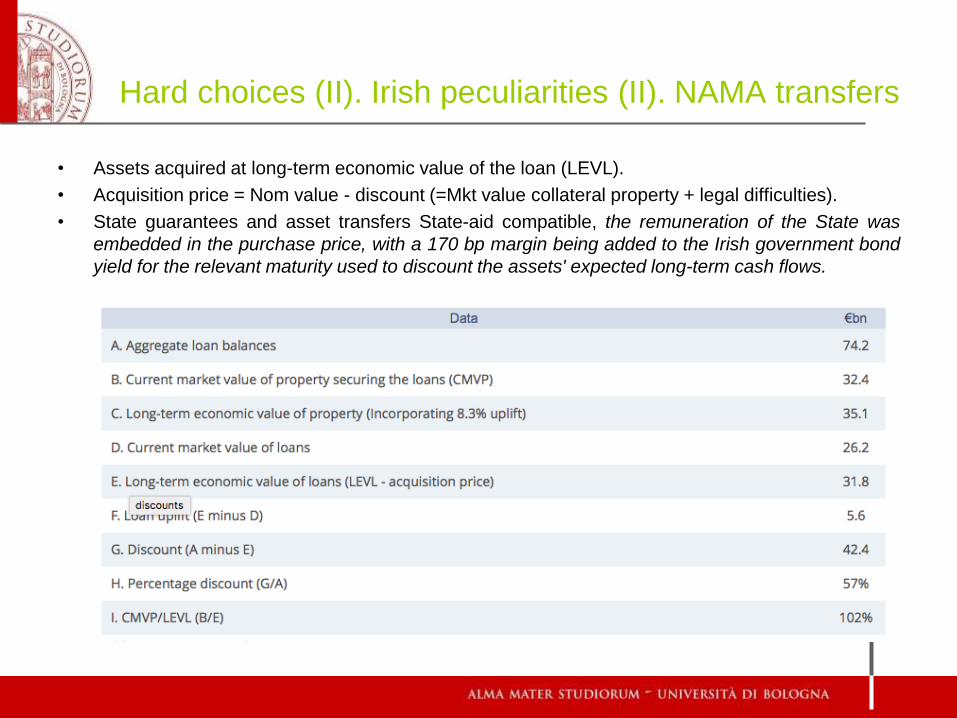

Hard choices (II). Irish peculiarities (II). NAMA transfers

• Assets acquired at long-term economic value of the loan (LEVL).

• Acquisition price = Nom value - discount (=Mkt value collateral property + legal difficulties).

• State guarantees and asset transfers State-aid compatible, the remuneration of the State was

embedded in the purchase price, with a 170 bp margin being added to the Irish government bond

yield for the relevant maturity used to discount the assets' expected long-term cash flows.

Hard choices (III). German peculiarities

• In Germany the problem was identified with the Finanzmaktstabilisierungsfondgesetz

of October 2008 and in particular with its extension of 2009. Article 8(a) granted to an

agency for financial stabilization (FMSA) and related fund (SoFFin) the possibility to

set up specialised agencies for the acquisition and management of NPEs: 1) Erste

Abwicklungsanstalt (EAA) for the WestLB non performing assets (December 2009);

2) FMS Wertmanagement called to manage NPLs of Hypo Real Estate Holding (July

2010).

• Both agencies were backed by a guarantee of SoFFin, which in turn is backed by the

guarantee of the state (regional state Hamburg for HSH Nordbank; federal state for

WestLB and HRE, but backed in turn by NordRhein Westfalen and Savings

Association respectively). NPEs were transferred via division (Betriebsabspalrtung) to

the bad banks at their book value (IFRS not applicable because bad banks are not

licensed banks!).

• The schemes were deemed compatible with State aid rules becauset (i) a clear

functional and organizational separation was traced between the beneficiary bank

and the assets, and (ii) the haircut and claw back clauses applied in setting the

transfer price actually made the banks recognize losses.

Hard choices (IV). Spanish peculiarities

• Spain established an asset management company (AMC) called SAREB to

manage NPLs (condition of the MoU signed in July 2012 with the European

Commission).

• Transfers should take place at the real (long-term) economic value (REV) of

the assets, in exchange for a “suitably small” equity participation in the

AMC.

• Bonds issued by the AMC had to be eligible for ECB refinancing and

guaranteed by the State or cash and/or high quality securities. The AMC

had to be given the “possibility to hold [problematic assets] to maturity”.

• The Commission found the asset transfer in line with State aid rules, due to

its being based on the estimated long-term real economic value of the

assets and the application of a discount (account for AMC and negative

outlook on divestment of the assets in the short-run).

Italy – The reluctant chooser: Strategies I and II

•Italy caught unaware: late slowdown (2011), and deterioration of bank assets

(2013). Result? End 2016: Italian NPEs = 349 Billion (gross terms), 173 Billion

(net terms) (9.4% of loans). Qualified NPEs: 81 Billion (4.4% total loans).

•Step 1. First strategy: REV Bad Bank

–Resolution scheme for 4 mid-size banks (1% deposits), Law Decree 183/2015

–NPLs EUR 8,5 Billion transferred to REV - Gestione Crediti S.p.A, (EUR 136 Mill

capital subscribed by national resolution fund): Consideration: 17,65% gross value

later adjusted to 22,3% (EUR 1,5 – 1,9 billion)

•Step 2. Second strategy: GACS

–State guarantee over senior securities issued by NPL-acquiring SPVs.

–Conditions: (i) NPL transfer price < net book value (ii) SPV issues at least two

tranches (junior, senior); (iii) only senior guarantee-eligible; (iv) servicing outsourced

–Avoiding State-aid: non-State parties’ acquisition of junior/mezzanine tranche +

market pricing of guarantee

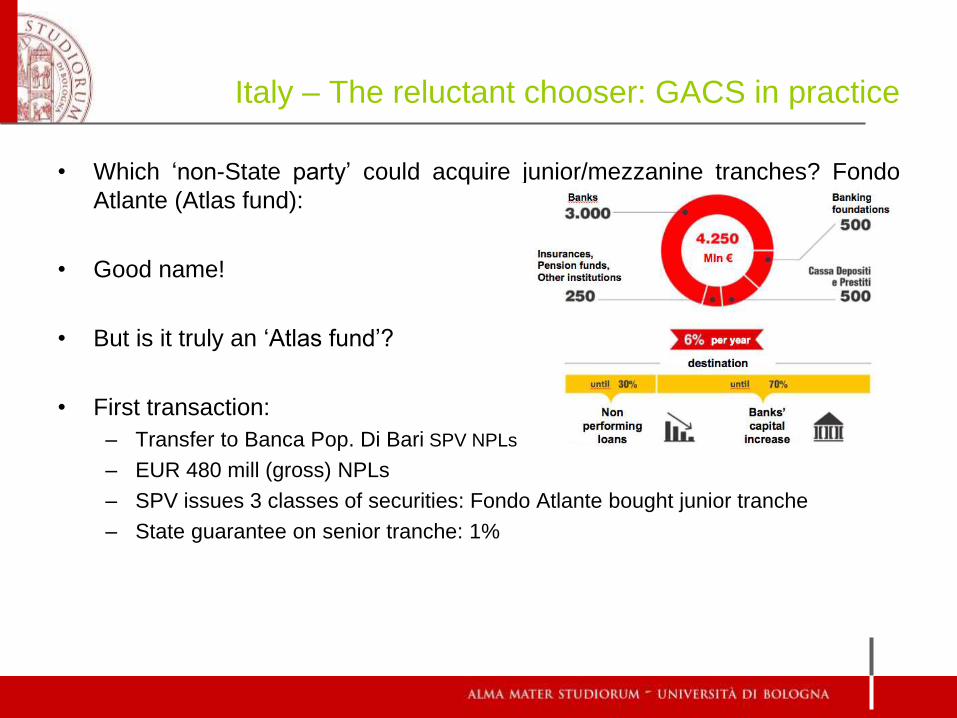

Italy – The reluctant chooser: GACS in practice

• Which ‘non-State party’ could acquire junior/mezzanine tranches? Fondo

Atlante (Atlas fund):

• Good name!

• But is it truly an ‘Atlas fund’?

• First transaction:

– Transfer to Banca Pop. Di Bari SPV NPLs

– EUR 480 mill (gross) NPLs

– SPV issues 3 classes of securities: Fondo Atlante bought junior tranche

– State guarantee on senior tranche: 1%

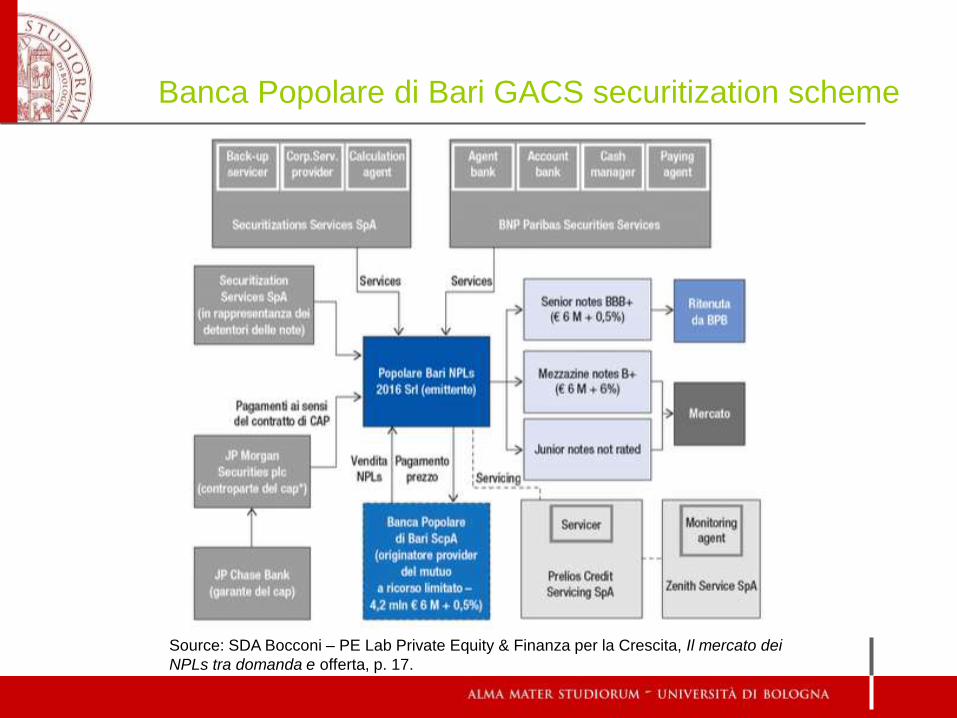

Banca Popolare di Bari GACS securitization scheme

Source: SDA Bocconi – PE Lab Private Equity & Finanza per la Crescita, Il mercato dei

NPLs tra domanda e offerta, p. 17.

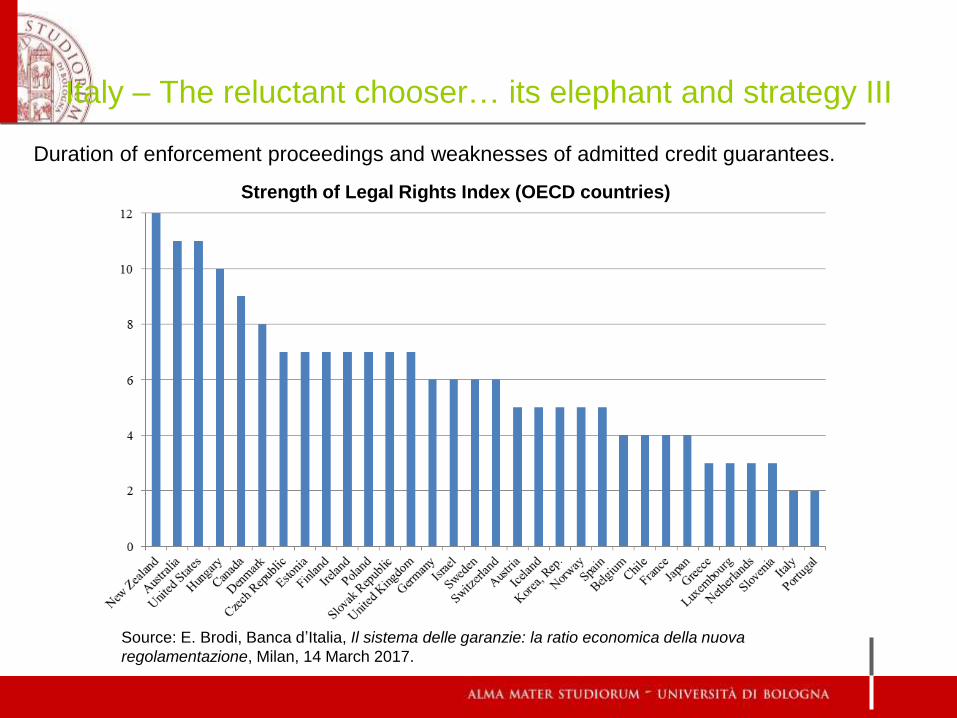

Italy – The reluctant chooser… its elephant and strategy III

Strength of Legal Rights Index (OECD countries)

Source: E. Brodi, Banca d’Italia, Il sistema delle garanzie: la ratio economica della nuova

regolamentazione, Milan, 14 March 2017.

Duration of enforcement proceedings and weaknesses of admitted credit guarantees.

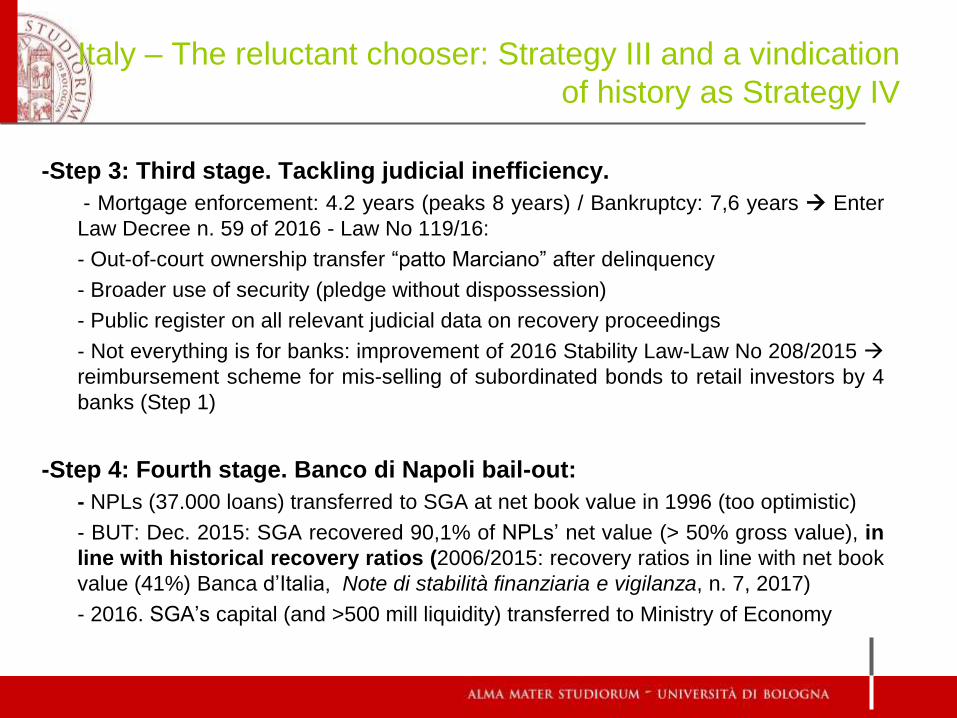

Italy – The reluctant chooser: Strategy III and a vindication

of history as Strategy IV

-Step 3: Third stage. Tackling judicial inefficiency.

- Mortgage enforcement: 4.2 years (peaks 8 years) / Bankruptcy: 7,6 years Enter

Law Decree n. 59 of 2016 - Law No 119/16:

- Out-of-court ownership transfer “patto Marciano” after delinquency

- Broader use of security (pledge without dispossession)

- Public register on all relevant judicial data on recovery proceedings

- Not everything is for banks: improvement of 2016 Stability Law-Law No 208/2015

reimbursement scheme for mis-selling of subordinated bonds to retail investors by 4

banks (Step 1)

-Step 4: Fourth stage. Banco di Napoli bail-out:

- NPLs (37.000 loans) transferred to SGA at net book value in 1996 (too optimistic)

- BUT: Dec. 2015: SGA recovered 90,1% of NPLs’ net value (> 50% gross value), in

line with historical recovery ratios (2006/2015: recovery ratios in line with net book

value (41%) Banca d’Italia, Note di stabilità finanziaria e vigilanza, n. 7, 2017)

- 2016. SGA’s capital (and >500 mill liquidity) transferred to Ministry of Economy

Italy – The reluctant chooser: Strategy V and VI

• Step 5: Fifth stage. Liquidity/solvency support L. Dec. 237/2016

– State guarantee on new and senior bonds for (still) solvent banks (to be

approved by EC);

– Conditions to inject public funds into capital of banks still solvent but with capital

shortfall in stress test Burden-sharing and conversion of subordinated debt.

– Christos Hadjiemmanuil Oxford Business Law Blog 2 May 2017.

• Step 6: MPS securitization and similar schemes

– Division of NPLs through securitization from MPs to SPV (33% gross book value)

– SPV issues 3 tranches: senior (with St-guarantee, 65%), mezzanine (subscribed

by F. Atlante 2, 18%); junior (allocated free-of-charge to MPS shareolders, 17%)

– Similar schemes for ‘shadow resolutions’ of mid-size banks by Italian DGS

(Cassa di Cesena, Cassa di Rimini, Cassa di San Miniato, pending 2017)

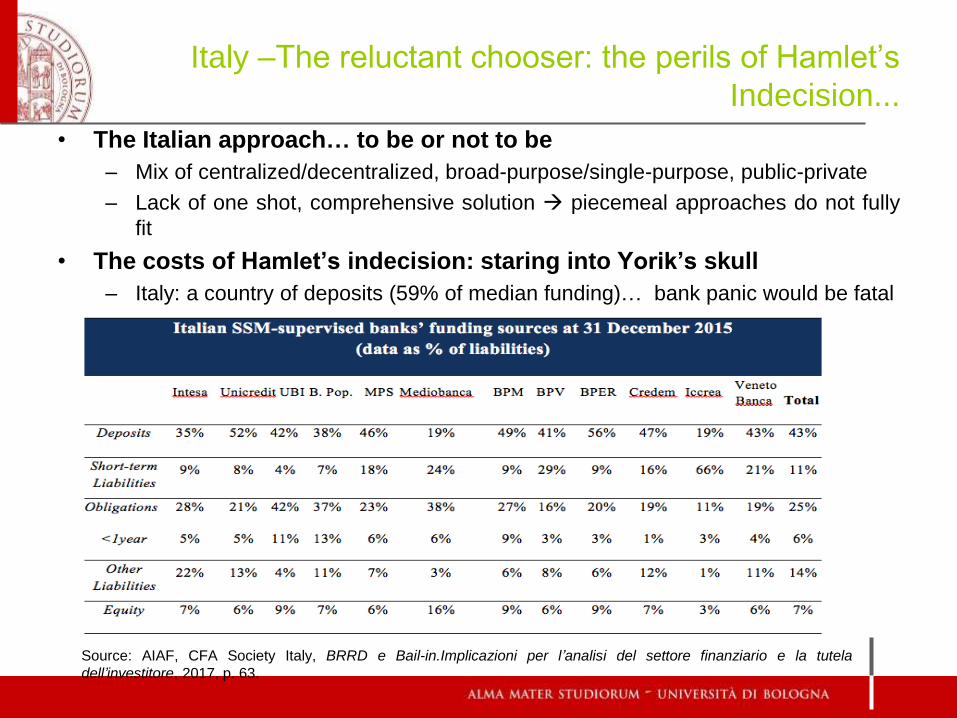

Italy –The reluctant chooser: the perils of Hamlet’s

Indecision...

• The Italian approach… to be or not to be

– Mix of centralized/decentralized, broad-purpose/single-purpose, public-private

– Lack of one shot, comprehensive solution piecemeal approaches do not fully

fit

• The costs of Hamlet’s indecision: staring into Yorik’s skull

– Italy: a country of deposits (59% of median funding)… bank panic would be fatal

Source: AIAF, CFA Society Italy, BRRD e Bail-in.Implicazioni per l’analisi del settore finanziario e la tutela

dell’investitore, 2017, p. 63.

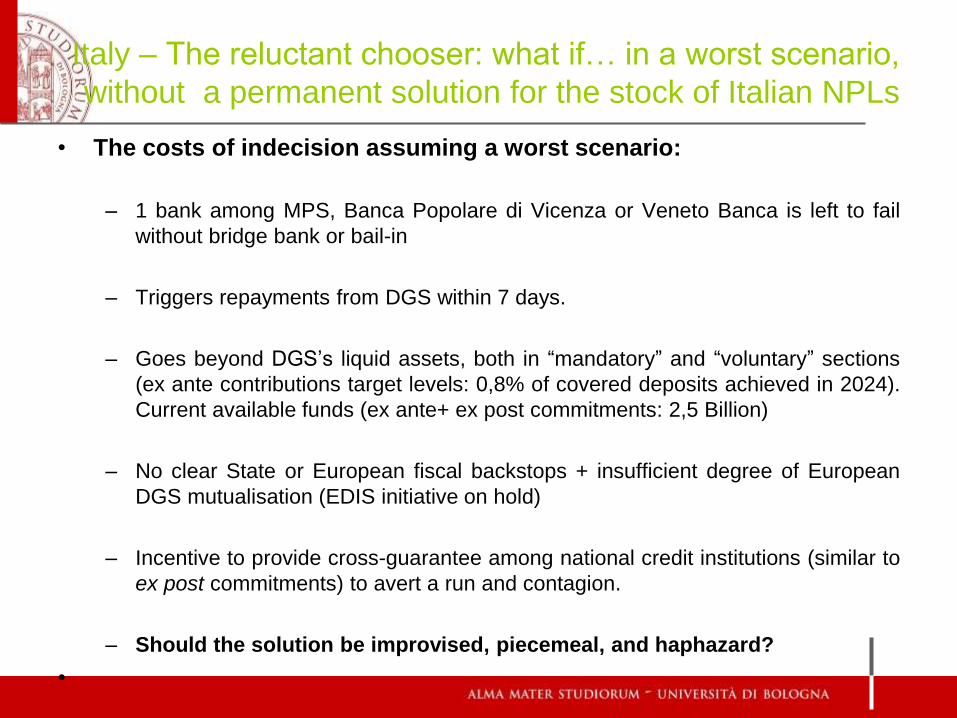

Italy – The reluctant chooser: what if… in a worst scenario,

without a permanent solution for the stock of Italian NPLs

• The costs of indecision assuming a worst scenario:

– 1 bank among MPS, Banca Popolare di Vicenza or Veneto Banca is left to fail

without bridge bank or bail-in

– Triggers repayments from DGS within 7 days.

– Goes beyond DGS’s liquid assets, both in “mandatory” and “voluntary” sections

(ex ante contributions target levels: 0,8% of covered deposits achieved in 2024).

Current available funds (ex ante+ ex post commitments: 2,5 Billion)

– No clear State or European fiscal backstops + insufficient degree of European

DGS mutualisation (EDIS initiative on hold)

– Incentive to provide cross-guarantee among national credit institutions (similar to

ex post commitments) to avert a run and contagion.

– Should the solution be improvised, piecemeal, and haphazard?

•

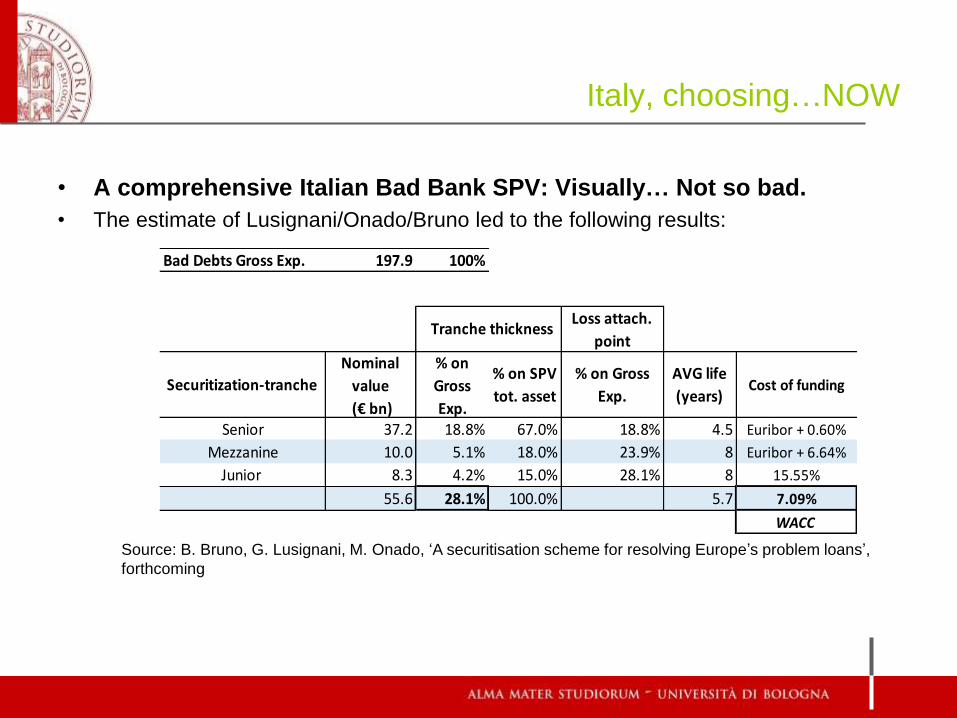

Italy, choosing…NOW

• A comprehensive Italian Bad Bank SPV: Visually… Not so bad.

• The estimate of Lusignani/Onado/Bruno led to the following results:

Bad Debts Gross Exp. 197.9 100%

Loss attach.

point

Securitization-tranche

Nominal

value

(€ bn)

% on

Gross

Exp.

% on SPV

tot. asset

% on Gross

Exp.

AVG life

(years)Cost of funding

Senior 37.2 18.8% 67.0% 18.8% 4.5 Euribor + 0.60%

Mezzanine 10.0 5.1% 18.0% 23.9% 8 Euribor + 6.64%

Junior 8.3 4.2% 15.0% 28.1% 8 15.55%

55.6 28.1% 100.0% 5.7 7.09%

WACC

Tranche thickness

Source: B. Bruno, G. Lusignani, M. Onado, ‘A securitisation scheme for resolving Europe’s problem loans’,

forthcoming

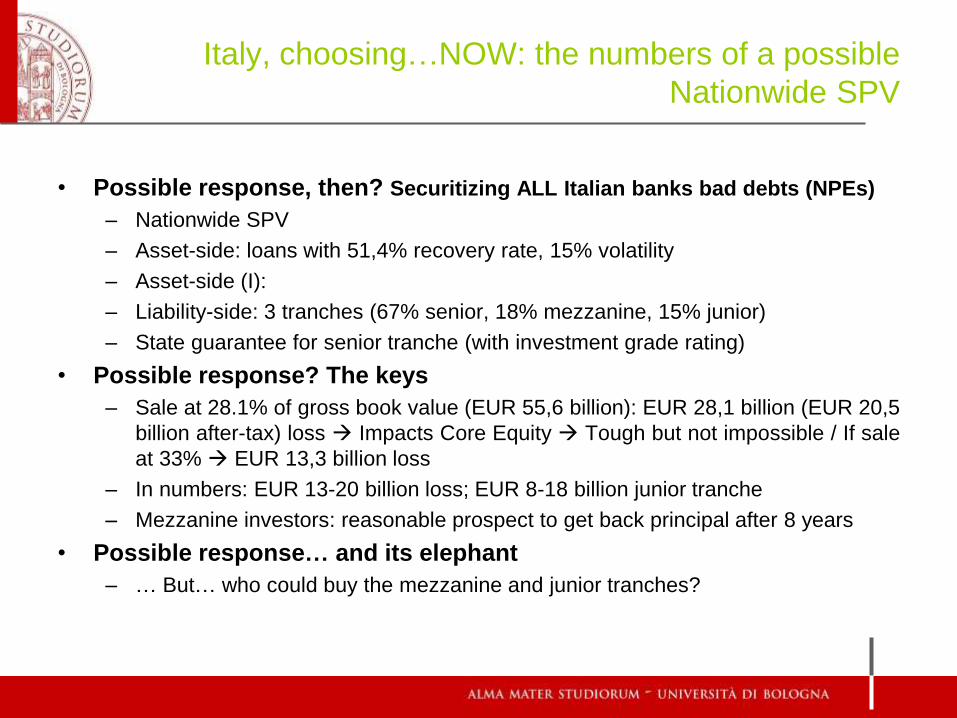

Italy, choosing…NOW: the numbers of a possible

Nationwide SPV

• Possible response, then? Securitizing ALL Italian banks bad debts (NPEs)

– Nationwide SPV

– Asset-side: loans with 51,4% recovery rate, 15% volatility

– Asset-side (I):

– Liability-side: 3 tranches (67% senior, 18% mezzanine, 15% junior)

– State guarantee for senior tranche (with investment grade rating)

• Possible response? The keys

– Sale at 28.1% of gross book value (EUR 55,6 billion): EUR 28,1 billion (EUR 20,5

billion after-tax) loss Impacts Core Equity Tough but not impossible / If sale

at 33% EUR 13,3 billion loss

– In numbers: EUR 13-20 billion loss; EUR 8-18 billion junior tranche

– Mezzanine investors: reasonable prospect to get back principal after 8 years

• Possible response… and its elephant

– … But… who could buy the mezzanine and junior tranches?

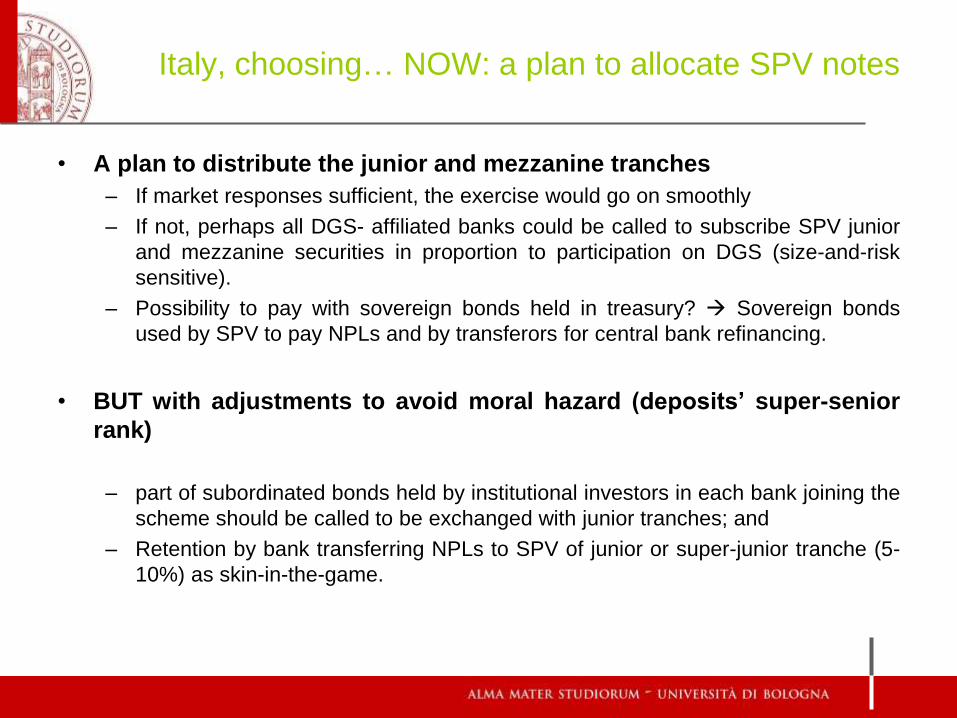

Italy, choosing… NOW: a plan to allocate SPV notes

• A plan to distribute the junior and mezzanine tranches

– If market responses sufficient, the exercise would go on smoothly

– If not, perhaps all DGS- affiliated banks could be called to subscribe SPV junior

and mezzanine securities in proportion to participation on DGS (size-and-risk

sensitive).

– Possibility to pay with sovereign bonds held in treasury? Sovereign bonds

used by SPV to pay NPLs and by transferors for central bank refinancing.

• BUT with adjustments to avoid moral hazard (deposits’ super-senior

rank)

– part of subordinated bonds held by institutional investors in each bank joining the

scheme should be called to be exchanged with junior tranches; and

– Retention by bank transferring NPLs to SPV of junior or super-junior tranche (5-

10%) as skin-in-the-game.

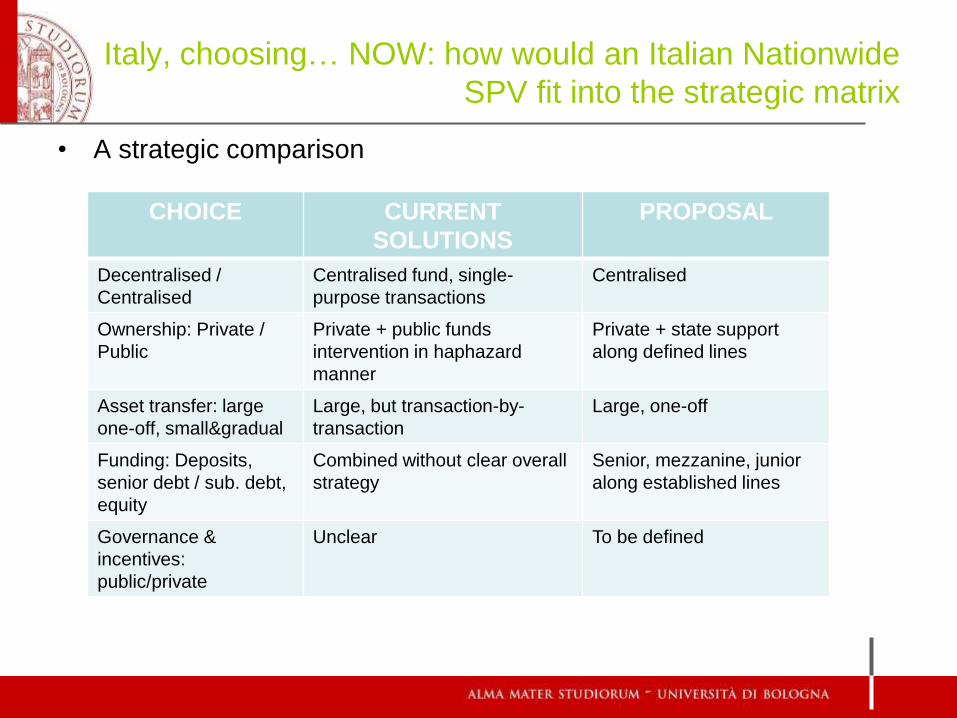

Italy, choosing… NOW: how would an Italian Nationwide

SPV fit into the strategic matrix

• A strategic comparison

CHOICE CURRENT

SOLUTIONS

PROPOSAL

Decentralised /

Centralised

Centralised fund, single-

purpose transactions

Centralised

Ownership: Private /

Public

Private + public funds

intervention in haphazard

manner

Private + state support

along defined lines

Asset transfer: large

one-off, small&gradual

Large, but transaction-by-

transaction

Large, one-off

Funding: Deposits,

senior debt / sub. debt,

equity

Combined without clear overall

strategy

Senior, mezzanine, junior

along established lines

Governance &

incentives:

public/private

Unclear To be defined

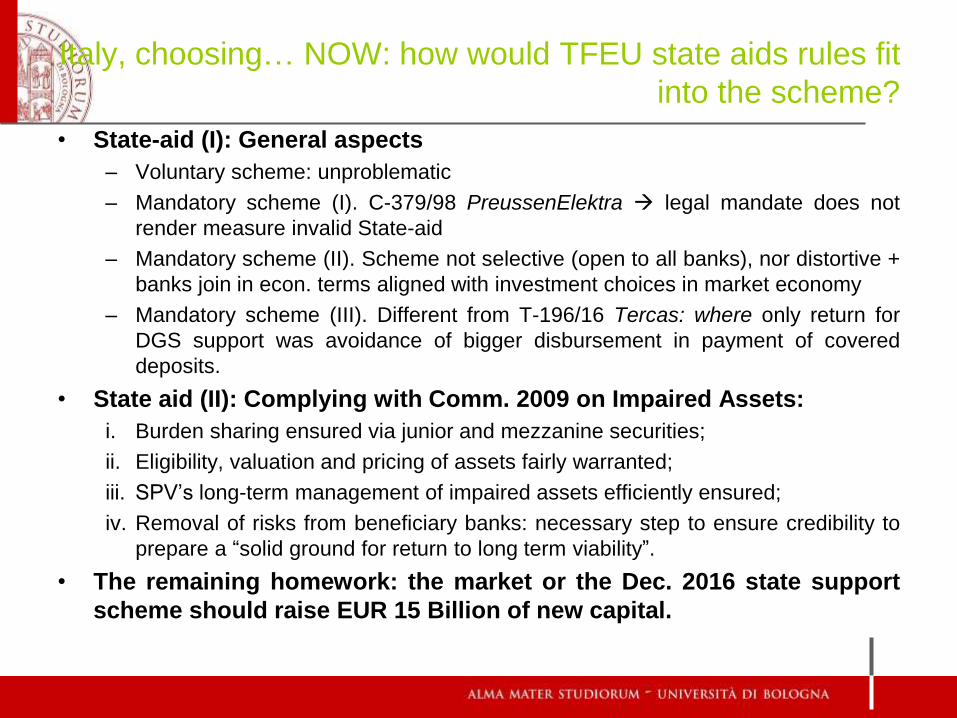

Italy, choosing… NOW: how would TFEU state aids rules fit

into the scheme?

• State-aid (I): General aspects

– Voluntary scheme: unproblematic

– Mandatory scheme (I). C-379/98 PreussenElektra legal mandate does not

render measure invalid State-aid

– Mandatory scheme (II). Scheme not selective (open to all banks), nor distortive +

banks join in econ. terms aligned with investment choices in market economy

– Mandatory scheme (III). Different from T-196/16 Tercas: where only return for

DGS support was avoidance of bigger disbursement in payment of covered

deposits.

• State aid (II): Complying with Comm. 2009 on Impaired Assets:

i. Burden sharing ensured via junior and mezzanine securities;

ii. Eligibility, valuation and pricing of assets fairly warranted;

iii. SPV’s long-term management of impaired assets efficiently ensured;

iv. Removal of risks from beneficiary banks: necessary step to ensure credibility to

prepare a “solid ground for return to long term viability”.

• The remaining homework: the market or the Dec. 2016 state support

scheme should raise EUR 15 Billion of new capital.

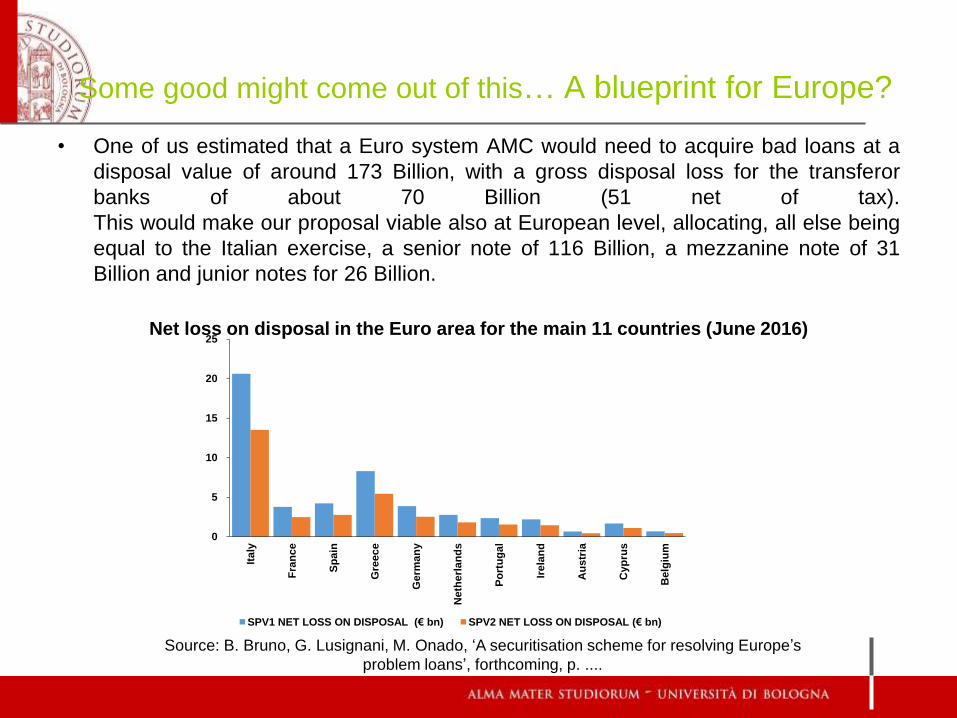

Some good might come out of this… A blueprint for Europe?

• One of us estimated that a Euro system AMC would need to acquire bad loans at a

disposal value of around 173 Billion, with a gross disposal loss for the transferor

banks of about 70 Billion (51 net of tax).

This would make our proposal viable also at European level, allocating, all else being

equal to the Italian exercise, a senior note of 116 Billion, a mezzanine note of 31

Billion and junior notes for 26 Billion.

Net loss on disposal in the Euro area for the main 11 countries (June 2016)

0

5

10

15

20

25

Ita

ly

Fra

nce

Sp

ain

Gre

ec

e

Germ

an

y

Neth

erl

an

ds

Po

rtu

gal

Irela

nd

Au

str

ia

Cyp

rus

Belg

ium

SPV1 NET LOSS ON DISPOSAL (€ bn) SPV2 NET LOSS ON DISPOSAL (€ bn)

Source: B. Bruno, G. Lusignani, M. Onado, ‘A securitisation scheme for resolving Europe’s

problem loans’, forthcoming, p. ....

The Spanish case: multiple choosers in town

(and a warning on microeconomic choices clashing with

macroeconomic ones)

• Spain made some mistakes (optimistic valuations) but overall sound and

consistent ‘macro’ choices… which have been harmed by ‘micro’ issues: a

‘non-performing loans’ problem followed by a ‘performing loans’ one.

• Spanish legal system: efficient creditor-protection tool… and debtors’

bogeyman

• Step 1: Court of Justice’s decisions on unfair contract terms set in

motion a soul-searching process: how creditor-friendly do we want to be?

• Step 2: Misselling of financial instruments (preferred shares)

reconsideration of MiFID effects over validity…

• Step 3: The pendulum swings… hard court decisions on ‘floor clauses’ +

enhanced cons. protection upon enforcement + wave of annulment cases

The Spanish case: multiple choosers in town

• Step 4: government provides ‘macro’ solution to misselling: partly botched

attempt cases continue

• Step 5: Court of Justice annuls Spanish Supreme Court limitation of effects

on annulment

• Result 1: Banks squeezed on the asset side

– performing loans: no floor clauses

– non-performing loans: consumer protection and longer recovery periods)

• Result 2: Banks squeezed on the liability side (mis-selling cases)

• Result 3: Greater legal uncertainty

Concluding remarks

• US-EU comparisons… or economics v. politics

• Choices can differ… but need to be consistent, and based on clear

answers to clear questions

• Italy? if you do not like the fancy answer…try a different question…

until questions are exhausted

• Italy (II)? there is still hope… and maybe even a blueprint for Europe

• Spain: Do not dismiss ‘micro’ issues… (nor blindly rely only on

European rules sometimes at war with themselves)