Embed Size (px)

Citation preview

Hon. Irene Ovonji-Odida, Member AU/ UNECA High Level Panel on IFFs from Africa, Outgoing Chair ActionAid Int.,

CEO FIDA-Uganda.

Background & Concept HLP on IFFs from Africa set up Feb. 2012

by AU/ECA Ministers of Finance, Planning & Economic Development.

ToR: to establish IFF nature, patterns, scale & effects on development, sensitize stakeholders including governments, & make proposals to reverse it.

Chair H.E. Thabo Mbeki & 9 members.

Method: ECA study on trade mispricing, 2 visits, sub-regional & global consultations, IEC/ advocacy, 6 country studies. Algeria, DRC, Kenya, Liberia, Mozambique, Nigeria.

GFI definition: ‘money illegally earned, transferred or used’ ie illicit in origin, movement or use.

Means: commercial, criminal & corruption by govt officials

Commercial mainly by MNEs eg aggressive tax avoidance schemes, concessionary agreements, cash smuggling, capital transfers through services or intangibles like IPRs, trade mispricing, tax evasion, money laundering is 60% of IFF.

Criminal- trafficking, counterfeiting, contraband, terrorist financing is 35%.

Government corruption-bribery, abuse of office constitutes 5%. However government corruption enables other practices contributing to IFFs.

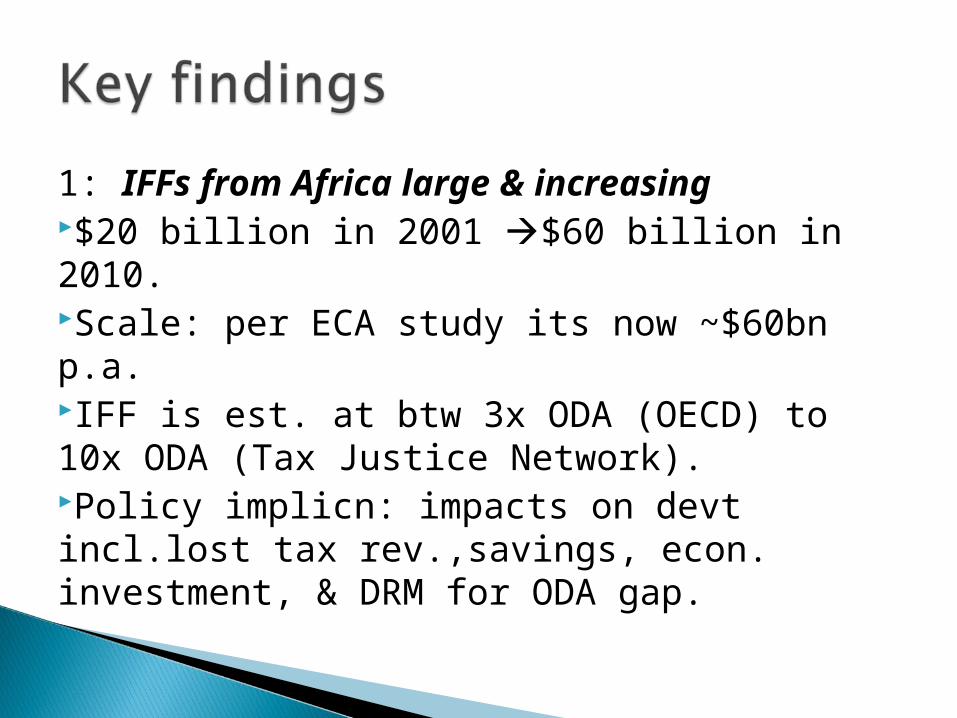

1: IFFs from Africa large & increasing $20 billion in 2001 $60 billion in 2010.Scale: per ECA study its now ~$60bn p.a. IFF is est. at btw 3x ODA (OECD) to 10x ODA (Tax Justice Network).Policy implicn: impacts on devt incl.lost tax rev.,savings, econ. investment, & DRM for ODA gap.

The pol. econ of IFFs core to ending it – v. powerful actors/interests & harmful gov. effects. Polit.commitment key to action.

3: Transparency key to all aspects of IFF Eg decl. of profits in financ. Secrecy jurisd/

use of low tax jurisd; opaque MNC in-hse trading of inputs, IP, outputs, services;

Commerc mispricing in trade imports & exports thru transp. in fin. reporting incl. country-by-country account of sales, profits & taxes paid by MNEs.

Tax avoid/ evasn declaration of benef. ownership in comm. entities, incl. banking & securities accts & cross-border exch of tax info.

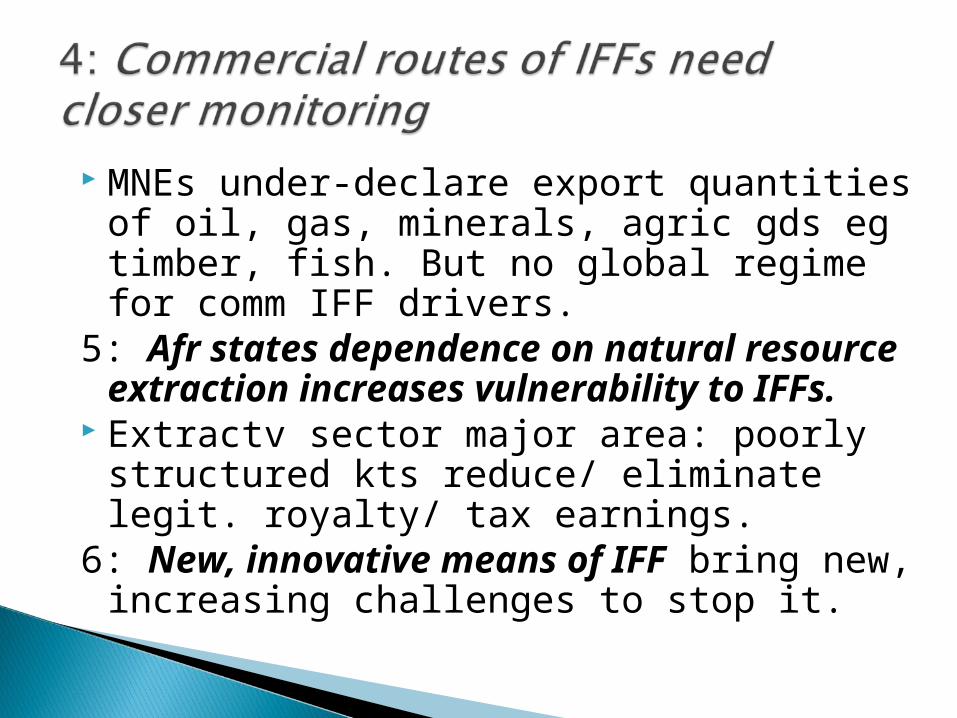

MNEs under-declare export quantities of oil, gas, minerals, agric gds eg timber, fish. But no global regime for comm IFF drivers.

5: Afr states dependence on natural resource extraction increases vulnerability to IFFs.

Extractv sector major area: poorly structured kts reduce/ eliminate legit. royalty/ tax earnings.

6: New, innovative means of IFF bring new, increasing challenges to stop it.

Corruptn key driver of tax incentvs like tax holidays-no relatn btw FDI/ tax incentives – FDI idue to pol. stability, cost of biznss.

Higher tax burden on SMEs due to MNE tax abuse; yet small domestic firms boost employ’t more than MNCs.

8: Corruption, abuse of pwr a cont. concern

IFFs kill state institutions, rule of law, state capacities, undo public confid. & divert public money to private uses -> skew income distribution, linked to inequality.

IFF primarily go to ext destinations – tradit. & new incl. tax havens (old & emerging).

Tunisia post-MENA uprising shows role of banks, acctg firms, lawyers to enable MNE practices & outdo govt cap

OECD BEPS process ->asset recov. for OECD states! 10: Money laundering continues to require

attention Harmonized crim. laws reqd. MNEs misprice imports/

exports to avoid duties or transfer monies esp. foreign exch abroad ~ Liberia challenge worse w USD as legal tender.

De-regulatn, liberalizn ->hard to stem laundering

Af. Govts lack funds for public services ~ health, educ, infrast.-direct cost esp. on poor citizens.

IFF weaken fin. sector, tax collecn, mkt reguln, integty of public fin. systems, stability & security. Liberalized & de-regulated econ enable IFFs cut regulatory cap.eg customs to stop trade mis-pricing; ensure negot of gd kts in extractives & monitor resource exploitation.

Strong neg cap. req to shape global architecture

ATAF initiatives relevant for cap. bldg

Uneven/ missing inst. global architecture - UNCAC ~ corruption, crime but not MNEs.

13: Financial secrecy jurisd req closer scrutiny

Transpcy, uncovering secrecy & information, collaboration, cooperation key challenges.

Tax havens & fin. secrecy jurisds ease regn & enable corporate SPVs & nominal owners (fronts) to mask beneficial owners.

Global initiatives but many not univ. applic & don’t cover Africa eg OECD BEPs.

Coop of OECD, G8, G20 reqd~richest states & IFF destination to close global gov gaps on means of IFFs.

15: IFFs esp comm. MNC transactns shd be incl. in UN f/works eg SDGs, FFDs.

Conclusion: IFFs linked to DRM & FfD: Req. polit. will & technic cap re. powerful

interests & complexity.

![UNECA Macro Training 4[1]](https://img.dokumen.tips/doc/110x75/5571feda49795991699c2e32/uneca-macro-training-41.jpg)