Embed Size (px)

Citation preview

MakeMyTrip Limited (NASDAQ: MMYT)Investor PresentationAugust 2017

2

Safe Harbor

Certain statements contained in this presentation are “forward-looking statements” within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. These statements reflect our current expectations or forecasts of future events and our future performance and do not relate directly to historical or current events or our historical or current performance and are subject to risks and uncertainties, some of which are outside of our control, that could cause actual outcomes and results to differ materially from historical results or current expectations. Most of these statements contain words that identify them as forward looking, such as “anticipate”, “estimate”, “expect”, “project”, “intend”, “plan”, “believe”, “seek”, “will”, “may”, “should”, “opportunity”, “target” or other words that relate to future events, as opposed to past or current events. Among the factors that could cause actual results to differ materially include, but are not limited to, the slowdown of economic growth in India and the global economic downturn, general declines or disruptions in the travel industry, the inability to successfully integrate the businesses of MMYT and ibibo Group within the anticipated timeframe or at all, the risk that the acquisition will disrupt current plans and operations, increase in operating costs and potential difficulties in customer or supplier loss and employee retention as a result of the acquisition, the inability to recognize the anticipated benefits of the combination of MMYT and ibibo Group, including the realization of revenue and cost synergy benefits within the anticipated timeframe or at all, volatility in the trading price of MMYT’s shares, MMYT’s reliance on its relationships with travel suppliers and strategic alliances, failure to further increase MMYT’s brand recognition to obtain new business partners and consumers, failure to compete against new and existing competitors, failure to successfully manage current growth and potential future growth, risks associated with any strategic investments or acquisitions, seasonality in the travel industry in India and overseas, failure to successfully develop MMYT’s corporate travel business, damage to or failure of MMYT’s infrastructure and technology, loss of services of MMYT’s key executives, and inflation in India and in other countries. In addition to the foregoing factors, a description of certain other risks and uncertainties which may cause actual results to differ materially can be found in the “Risk Factors” section of MMYT's 20-F dated July 18, 2017 and MMYT’s 6-K dated November 22, 2016, each filed with the U.S. Securities Exchange Commission (“SEC”), copies of which are available from the SEC, our website or our Investor Relations department.

We cannot assure you that the assumptions made in preparing any of the forward-looking statements will prove accurate or that any projections will be realized. We expect that there will be differences between projected and actual results. These forward-looking statements speak only as of the date of this presentation, and we do not undertake any obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise. You are cautioned not to place undue reliance on these forward-looking statements. All forward-looking statements attributable to us are expressly qualified in their entirety by the cautionary statements contained herein and in our future annual and quarterly reports as filed with the SEC.

3

Non-IFRS Metrics & Note on Unaudited Financials

The following non-IFRS metrics will be used in this presentation:

Gross Bookings represents total amount paid by our customers for travel services and products booked through us, including taxes, fees, and other charges, and are net of cancellation and refunds, but does not include other revenues that are generated from 3rd party advertisement on our website, commissions and fees earned from the sale of railway and bus operators and fees earned byfacilitating travel insurance policies to customers.

Net Revenues represents Revenues less Service Costs (costs of procuring the relevant services for sale to customers, including procurement costs paid to hotel and package suppliers for the acquisition of hotel rooms, sightseeing costs, local transport costs and on occasion the cost of air tickets when the company pre-purchases air ticket inventory in order to enjoy special negotiatedrates and revenues)

Net Revenue Margins is defined as Net Revenues as a percentage of Gross Bookings, and represents commissions, fees, incentive payments and other amounts earned in our business. We follow net revenue margin trends closely across our various lines of business to gain insight into the profitability of our various businesses.

Flight segment is defined as a flight between two cities, whether or not such flight is part of a larger or longer itinerary.

Room Nights, also referred to as a “hotel-room nights,” is the total number of hotel rooms occupied by a customer or group,multiplied by the number of nights that such customer or group occupies those rooms.

Constant Currency refers to our financial results assuming constant foreign exchange rates for the current fiscal period based on

the reporting for the historical average rate used in the prior year’s comparable fiscal period.

Fiscal Year End – March 31st

4

Investment Highlights

Leading OTA with Comprehensive Product Offerings via Multiple Brands

Driving Share Gains in India’s Underpenetrated Online Travel Market

Well Recognized Online Travel Brands with Superior Selection & Reach

Strong & Experienced Management Team

Strong Financial Profile with Strategic Investors Focused on High Growth6

1

2

3

4

5

Constant Product & Technology Innovations for Customers & Suppliers

5

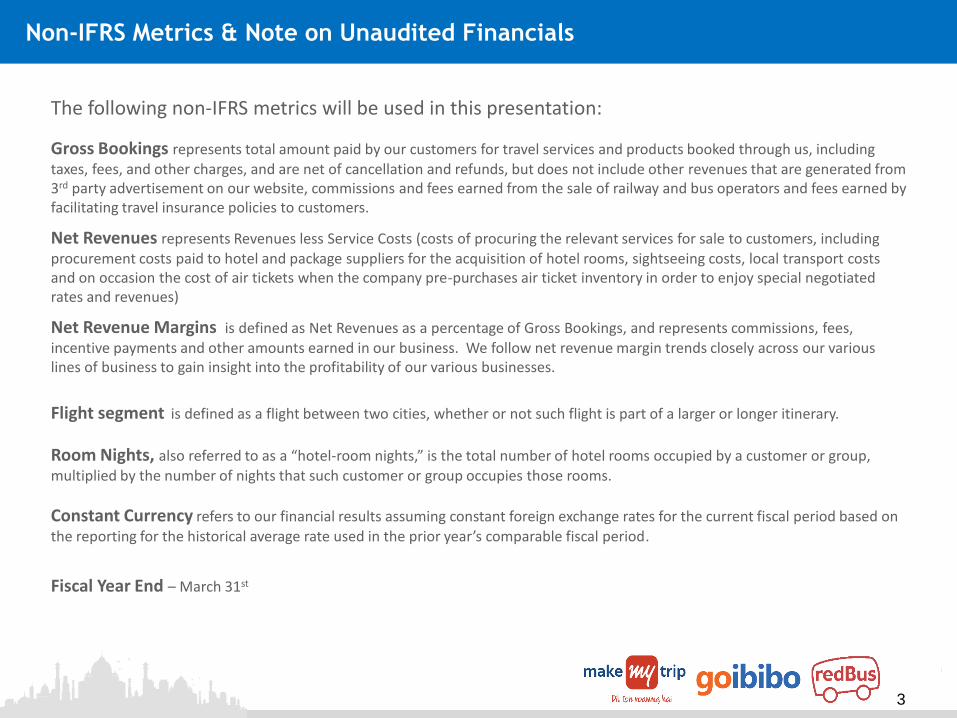

191

526

350

702

US China India India

0

5

10

15

20

25

30

35

40

2015 2017 2019 2021 2023 2025

US

4% CAGR

US$ 28 Tn

China

7% CAGR

US$ 37 Tn

India

8% CAGR

US$ 18 Tn

USUS$ 18 Tn

ChinaUS$ 19 Tn

IndiaUS$ 8 Tn

GD

P a

t P

urc

has

ing

Po

wer

Par

ity

(US$

Tn

)

Among Top 3 Global Economies with Robust Growth1

Source: 1Euromonitor; 2United Nations; *Internet Live Stats, The Future of Internet in India” NASSCOM August 2016

47%

33%

32%

48%

52%

59%

6%

15%

10%

Age 0–24 Age 25–64 Age 65+

Largest Young Population Globally (2015)2

2nd Largest Smartphone Users

287

721

462

730

US China India India

89%

52%

35%

52%

US China India India

2020E2016 2020E2016 2020E2016

Room to Grow with Low Internet Penetration

2nd Highest Internet Users

Attractive Macro Growth Drivers

6

India’s Online Travel Opportunity

Source: Morgan Stanley Research, e=Morgan Stanley Research estimates.

($ in Billions)

Addressable Total Travel Market Growth Online Travel Market Growth

Segments 2015 2021e CAGR 2015 2021e CAGR

Domestic Air $5.4 $10.0 11% $2.7 $6.0 14%

International Air $3.0 $5.3 10% $1.5 $2.6 10%

Domestic Hotels $10.0 $25.2 17% $1.4 $10.1 39%

Outbound Travel $12.5 $21.9 10% $0.9 $3.3 25%

Domestic Bus $3.1 $5.0 8% $0.5 $1.5 22%

Total Booking $34.0 $67.4 12% $7.0 $23.5 23%

Large Addressable Market with +$67 billion in Travel Bookings by 2021

7

Multiple Brands & Comprehensive Offerings

• Wide Range of Travel Product Offerings• Expanded Combined Customer Reach• Cross Selling Opportunities Across all 3 Platforms

• 75+ Million Monthly Shopper Visits • 15+ Million Monthly Active Mobile Users

• 7.8 million Air Ticketing Flight Segments in 1Q FY18• 5.8 million Hotels Room Nights Stayed in 1Q FY18

Source: Company data as disclosed on Q1 FY2018 Earnings Call & SEC Form 6K Filed on August 9 2017

8

Multiple Long Term Growth Drivers

Investing in Underpenetrated Travel Segments for Long Term Growth

Domestic Hotels Alternative Accommodations International Hotels

International Outbound Flights Bus Ticketing SME Travel

9

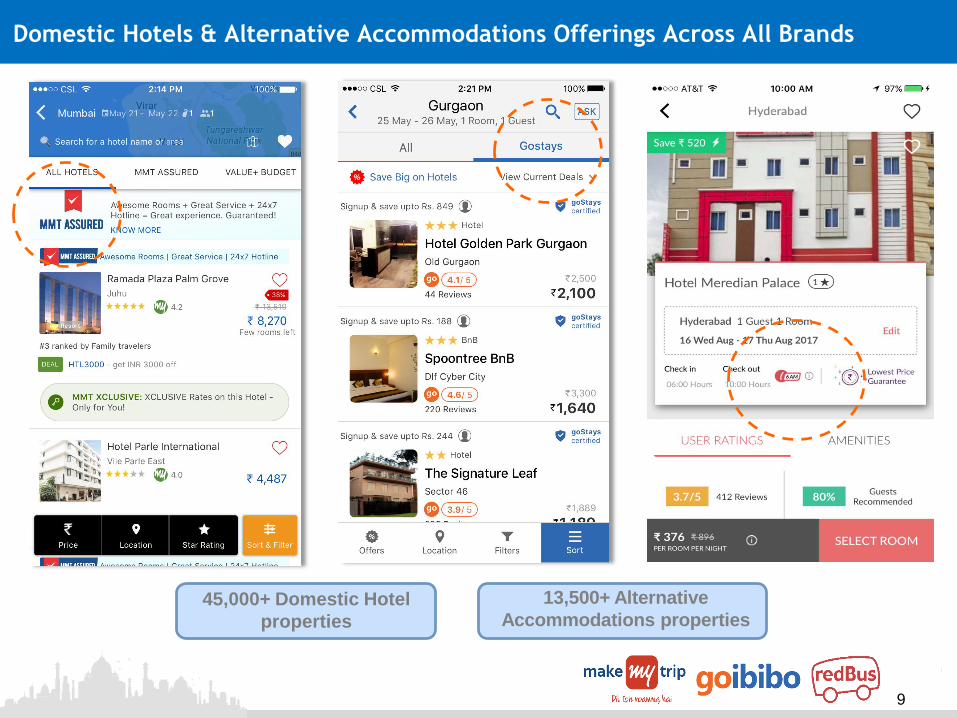

Domestic Hotels & Alternative Accommodations Offerings Across All Brands

13,500+ Alternative

Accommodations properties45,000+ Domestic Hotel

properties

10

Enhancing Customer Experience via Product & Technology Innovations

Machine Learning & Big Data to Drive

Greater Personalization

Artificial Intelligence Powered

ChatBots for Customer Support

Online Wallets &

Referrals

Unique In App Travel Reviews &

Interactions with Suppliers

Location Based Services

Live Bus Tracking Feature

11

Mobile Continues to Lead Growth & Drive Online Penetration

Mobile Air

Ticketing*:

59%

Mobile Bus

Ticketing*:

47%

Mobile Hotel

Booking*:

78%

*Q1 FY2018 mobile transactions as % of total

• Top Ranked iOS &

Google Play Apps

• Driving Tier II & III

penetration

• 1 MB Lite App

Available

• 90+ million

cumulative app

downloads to date

• 15+ million monthly

average active

mobiles users

• 78% of Monthly

Shopper Visits via

Mobile App & Web

• BHIM ready – ICICI

Bank integration

12

Highly Experienced & Integrated Management Team

Deep Kalra Co-Founder, Chairman and Group CEO- Started MakeMyTrip in 2000- Chairman of the Board of Directors- 24+ Years of Experience- Prior Experience: GE Capital India, AMF Bowing Inc.

& ABN AMRO Bank- Board member & past President of The IndUS

Entrepreneurs (TIE) New Delhi chapter- Founding member of Ashoka University & serves on

Governing Council- Bachelor’s degree in Economics - St. Stephen’s College - MBA IIM Ahmedabad, India

Rajesh MagowCo-Founder and CEO India- Senior founding team member of MakeMyTrip- Member of the Board of Directors- Previously CFO and Chief Operating Officer- 23+ Years of Experience- Prior Experience: eBookers.com, Aptech Limited &

Voltas Limited- Ex Independent FlipKart.com Board Member- Chartered Accountant from Institute of

Chartered Accountants of India, Delhi

Mohit KabraGroup Chief Financial Officer - 22+ Years of Experience- Prior Experience: Kohler India, PepsiCo,

Colgate & Seagrams- Bachelor of Commerce - St. Joseph’s Junior

College - Chartered Accountant from Institute of

Chartered Accountants of India - Cost Accountant from Institute of

Cost Accountants of India

Ashish KashyapCo-Founder & President - Founded ibibo Group in 2007- Co-founder of PayU India- Founded e-Commerce and online travel

businesses at Indiatimes.com- 20+ Years of Experience- Prior Experience: Google India- Masters of Management-IMPM - McGill University,

Desautels Faculty Of Management- Diploma: IMPM (Insead) & Economics from

Kirorimal College, Delhi University India

13

Financial Overview

Results presented include the consolidation of ibibo group from February 1, 2017 onwards,

unless otherwise noted

14

Q1 FY2018 Financial Highlights

Source: Company data, SEC 6K Filed on August 9 2017. YoY % growth on pro forma basis as disclosed

15

48 66 57 62 72 76

119 11

18 28 40

63

87

140

3

4 4

4

5

6

15

$0

$50

$100

$150

$200

$250

$300

FY11 FY12 FY13 FY14 FY15 FY16 FY17

Air Ticketing Hotels and Packages Emerging Segments

45.8 48.2 54.4INR/USD 60.4 61.1 65.4 67.1

648 839

940 944

1,175 1,276

1,545 95

154

230 318

473

566

745

$0

$500

$1,000

$1,500

$2,000

$2,500

FY11 FY12 FY13 FY14 FY15 FY16 FY17

Air Ticketing Hotels and Packages

Strong Growth Driven by Hotels and Packages

Gross Bookings

(in $ million)

45.8 48.2 54.4INR/USD 60.4 61.1 65.4

Note: 1. Net revenues represent revenues minus service costs

CCG = Constant Currency Growth

(in $ million)

Net Revenue(1)

$1,842

$1,648

$1,261$1,170

$993

$742

$169

$139

$106

$88$88

$61

$2,290

67.1

$274

16

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017

Driving Growth in Hotel & Packages

175.9 343.1 568.1

869.8 1,385.9

3,137.3

6,874.1

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017

Hotel & Packages Transactions (in 000s)

18%21%

31%

38%

45%

51% 51%

0%

10%

20%

30%

40%

50%

60%

FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017

Hotel & Packages Contribution to Net Revenue Improved to +50%

Standalone Hotels Transactions (in 000s)

(% o

f to

tal n

et r

even

ue)

3,001

1,236

726427230

136

5,645

17

Improving Mix and Margins with Strategic Focus on Hotels and Packages

Air Ticketing Net Revenue Margin

Hotels and Packages Net Revenue Margin

• Commissions and volume incentives from airlines

• Convenience & Service fees from customers

• Fees from GDS partner

Effective Product Bundling & Scale

• Mark up on Net Rates

• Commissions & volume incentives from hoteliers

Multiple sources of Net Revenue

Combined Net Revenue Margin

*See Reconciliation of IFRS to Non-IFRS Metrics

7.9%8.5%

7.2%8.1% 8.1%

9.2%

11.3%

0%

2%

4%

6%

8%

10%

12%

FY11 FY12 FY13 FY14 FY15 FY16 FY17

7.4%7.9%

6.0%6.6%

6.1% 6.0%

7.7%

0%

2%

4%

6%

8%

10%

FY11 FY12 FY13 FY14 FY15 FY16 FY17

11.5% 11.9% 12.0% 12.6% 13.2%

15.3%

18.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

FY11 FY12 FY13 FY14 FY15 FY16 YTD FY17

18

1.9% 2.0% 2.0% 2.1% 1.9% 1.9% 2.0%

1.3% 1.3% 1.3% 1.4% 1.4% 1.4% 1.2%

2.5% 2.5% 2.7% 2.7%2.2% 2.3% 2.1%

1.7% 1.7% 1.7%2.2%

2.6%

5.9%

9.8%

0.3% 0.3% 0.3%

0.3%0.4%

0.4%

0.5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

FY11 FY12 FY13 FY14 FY15 FY16 FY17

Personnel Expenses Payment Gateway SGA Marketing Depreciation & Amortization

7.7% 7.8% 8.0%8.7% 8.5%

11.9%

15.6%

Investing to Drive Higher Hotels & Packages Net Revenue Contribution %

of

Gro

ss B

oo

kin

gs

17.9% 20.7% 31.3% 37.6% 45.1%

Hotels and Packages Net Revenue Mix

51.1% 51.3%

19

Financial Summary in Constant Currency

Source: Company data

FY2013 FY2014 FY2015 FY2016 FY17

Air Ticketing yoy yoy yoy yoy yoy

Gross bookings growth 26% 11% 26% 16% 24%

Transactions growth 2% 5% 36% 28% 35%

Net Revenue growth -3% 21% 17% 14% 59%

Net Revenue to Bookings 6% 7% 6% 6% 7.7%

Hotels & Packages

Gross bookings growth 65% 48% 50% 28% 34%

Transactions growth 66% 53% 59% 126% 119%

Net Revenue growth 66% 54% 58% 45% 66%

Net Revenue to Bookings 12% 13% 13% 15% 18.8%

Hotel and Packages as a % of total net revenue

31% 38% 45% 51% 51%

Gross Bookings and Net Revenue Growth Rates are based on constant currency rates

20

Reconciliation of IFRS to Non-IFRS Metrics

Source: Company data

Reconciliation of Adjusted Operating Profit (Loss) Year ended March 31,

in thousand USD (Unaudited) 2010 2011 2012 2013 2014 2015 2016 2017

Result from operating activities as per IFRS (6,010) 4,062 4,005 (18,062) (15,322) (14,540) (66,827) (135,387)

Add: Employee share-based compensation costs 6,771 527 6,894 11,667 11,097 12,308 13,685 26,795

Less: Income on license acquired - - - - 115 - (886)

Less: Gain on bargain purchase - - - - (1,168) -

Add: Impairment of intangible assets - - - - - 2,167 15,168

Add: Merger and acquisitions related expenses - - 241 705 439 350 178 5,972

Add: Acquisition related intangibles amortization - - 64 572 1,389 1,700 1,554 3,741

Add: Severance cost related to a prior acquisition - - - - 638 -

Adjusted Operating Profit (Loss) 762 4,589 11,205 (5,118) (3,451) 456 (50,129) (83,711)