Embed Size (px)

Citation preview

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

22 March 2018Hilton Americas | Houston, TX, US

Highlights of a strong growth market –Polyester fibers & PET

Ashish PujariExecutive Director, Aromatics & FiberPolyester Fibers & PET

Polyester has today become an inseparable part of our daily lives, across all regions and social strata. China has dominated the growth in this industry in the past 20 years and alone accounts for more than 70% of the global market share. The textile industry is labor intensive and low wages and high productivity attracted invested in China. On the other have, bottle grade PET production costs are more or less same across the world, but the fast demand growth and easy availability of raw materials has helped drive most of the new investments into Asia.

Although bulk of the industry in now in Asia, its integration with other streams like olefins and refining means that any changes in polyester outlook continues to have global ramifications. The global integration is not only on the upstream side, but even in the downstream, PET recycling has now become a globally integrated industry, with China accounting processing almost 75% of global PET waste.

The industry saw sub‐par demand growth between 2012 and 2016 leading to the poor margins for a considerable period of time. However, with crude oil prices bottoming out through 2015 and continuing to move up over the last 2 years, the industry is witnessing a strong rebound in demand as well as margins. China’s new policy on imports of PET waste has put extra pressure in virgin polyester fibers, but is also expected to put pressure on global recyclers now.

Polyester industry is set for a strong 2018 – both for demand and margins, but there are developing mid term concerns which one needs to watch out!

1

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Polyester has seen anaemic growth rates in past 5 years

Questions raised as confidence shaken

• Short-term phenomenon or new trend line?

• Reasons for slowdown

• Did market overestimate polyester potential?

• Has demand moved back to cotton?0

20

40

60

80

100

12 13 14 15 16N. America S. America W. Europe C. Europe

CIS & Baltics Africa Middle East Indian Subc.

NE Asia SE Asia Capacity

Global Polyester Melt Capacity & Demand Growth

Mill

ion

Met

ric T

ons

Source: IHS Markit © 2018 IHS Markit

5% 5% 4%4% 3%

7% 2% 2%9%8%

2

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

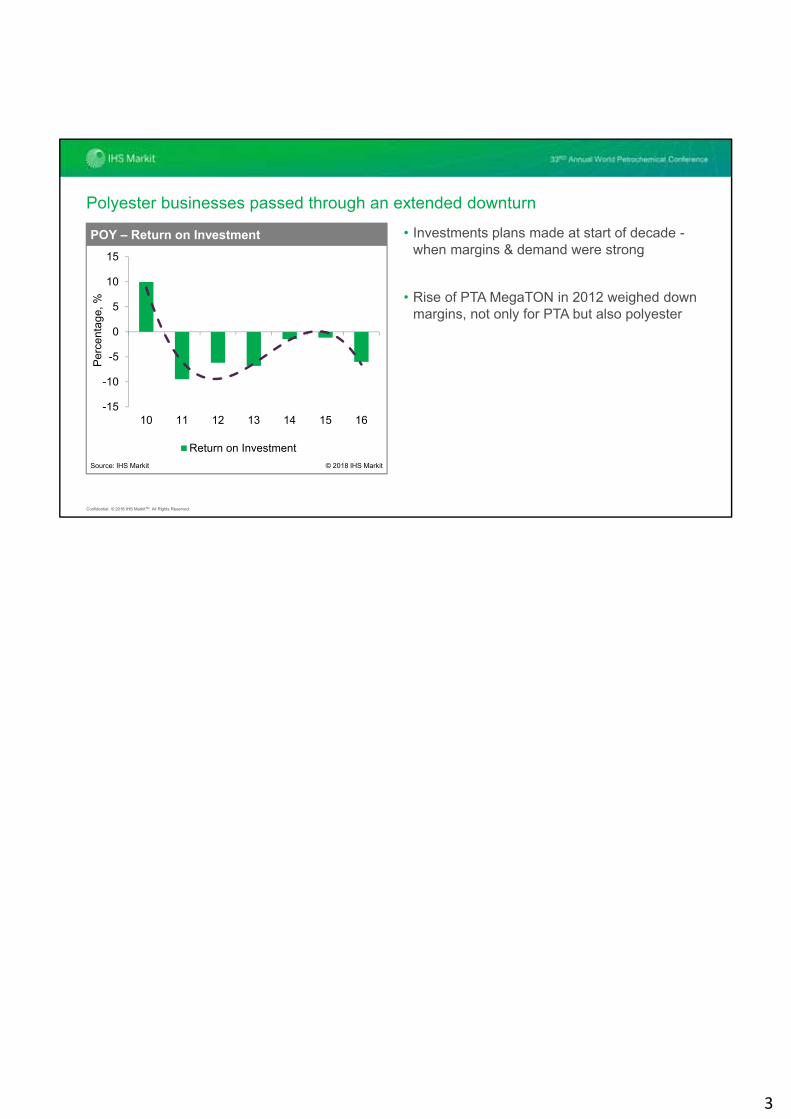

Polyester businesses passed through an extended downturn

• Investments plans made at start of decade -when margins & demand were strong

• Rise of PTA MegaTON in 2012 weighed down margins, not only for PTA but also polyester

-15

-10

-5

0

5

10

15

10 11 12 13 14 15 16

Return on Investment

Percentage,POY – Return on Investment

© 2018 IHS MarkitSource: IHS Markit

Per

cent

age,

%

3

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Signs of recovery were already evident in early 2017

4

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

What we’ll cover today

PET

Recycling

Polyester fiber

5

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

PET recyclingChinese National Sword policy has a global impact

6

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

PET growth attractive; but handling waste is growing concern

40% 46% 50%

0

10

20

30

40

50

60

0

5

10

15

20

25

30

12 17 22

Bottle Collection PET Consumption

Globally - waste collection has grown faster than virgin PET demand

Source: IHS Markit

Mill

ion

Met

ric T

ons

PE

T B

ottle

Col

lect

ion

, %

© 2018 IHS Markit

7

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

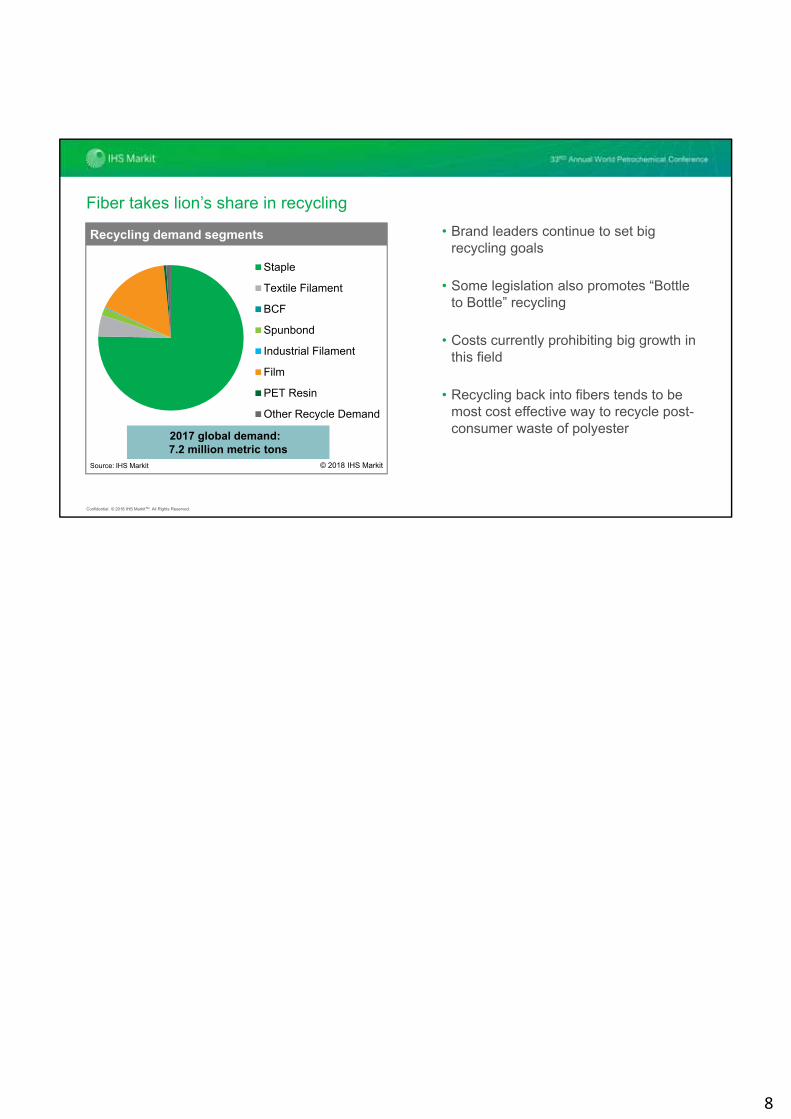

• Brand leaders continue to set big recycling goals

• Some legislation also promotes “Bottle to Bottle” recycling

• Costs currently prohibiting big growth in this field

• Recycling back into fibers tends to be most cost effective way to recycle post-consumer waste of polyester

Staple

Textile Filament

BCF

Spunbond

Industrial Filament

Film

PET Resin

Other Recycle Demand

Recycling demand segments

Source: IHS Markit © 2018 IHS Markit

Fiber takes lion’s share in recycling

2017 global demand: 7.2 million metric tons

8

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Polyester recycling – caught between economics & regulation

Imports43%Domestic

57%

PET recylate processed in China

Source: IHS Markit © 2018 IHS Markit

2017 estimated processed volume: 5.1 million metric tons

50%

60%

70%

80%

0

2

4

6

12 13 14 15 16 17

Domestic PET Consumption Recylate Collection

China’s own recycling standards faltering!

Source: IHS Markit © 2018 IHS Markit

Mill

ion

Met

ric T

ons

Rec

ycla

te C

olle

ctio

n

9

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

0

100

200

300

400

500

0

500

1,000

1,500

2,000

2,500

2012 Q1 2013 Q3 2015 Q1 2016 Q3 2018 Q1

Crude Oil Virgin Recycle

Polyester Chip Price: Virgin vs Recycle

Source: IHS Markit

Polyester Chip Price: Virgin vs Recycle

Pric

e,D

olla

rs p

er M

etric

Ton

China - Polyester chip price: Virgin vs recycle

Diff

eren

tials

, D

olla

rsP

er M

etric

Ton

© 2018 IHS Markit

Economic incentive primary driver for consuming fibers from recycleDiscounts over virgin PSF dropped to lowest levels after China’s ban on imports of PET waste as supply has tightened

Differential

10

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

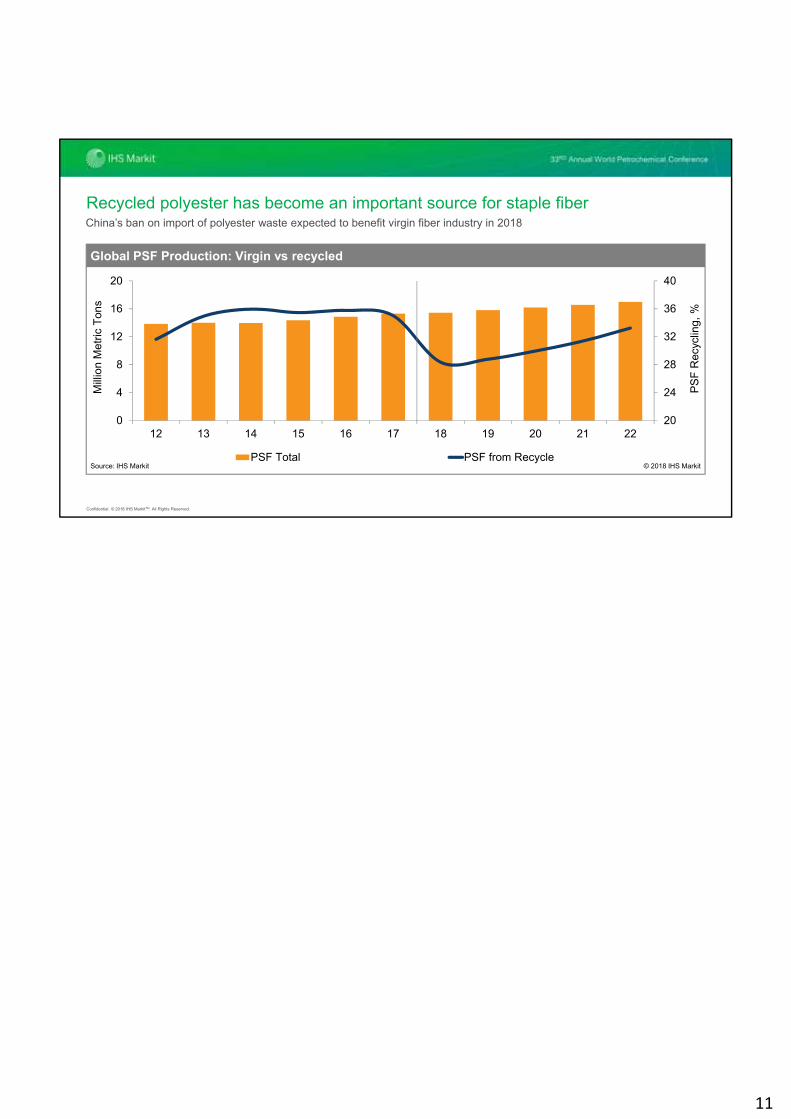

Recycled polyester has become an important source for staple fiberChina’s ban on import of polyester waste expected to benefit virgin fiber industry in 2018

20

24

28

32

36

40

0

4

8

12

16

20

12 13 14 15 16 17 18 19 20 21 22

PSF Total PSF from Recycle

Global PSF Production: Virgin vs recycled

Source: IHS Markit

Mill

ion

Met

ric T

ons

PS

F R

ecyc

ling,

%

© 2018 IHS Markit

11

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

-20%

-15%

-10%

-5%

0%

5%

10%

15%

12 14 16 18 20 22 24 26G

row

th R

ate

Virgin fibers Recycled fibers

Source: IHS Markit © 2018 IHS Markit

Global Fiber supply growth: Virgin vs. recycled

Policy measures delay growth of recycling, but economics favors more recycling

12

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

PETMost producers see better days, as few majors falter

13

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

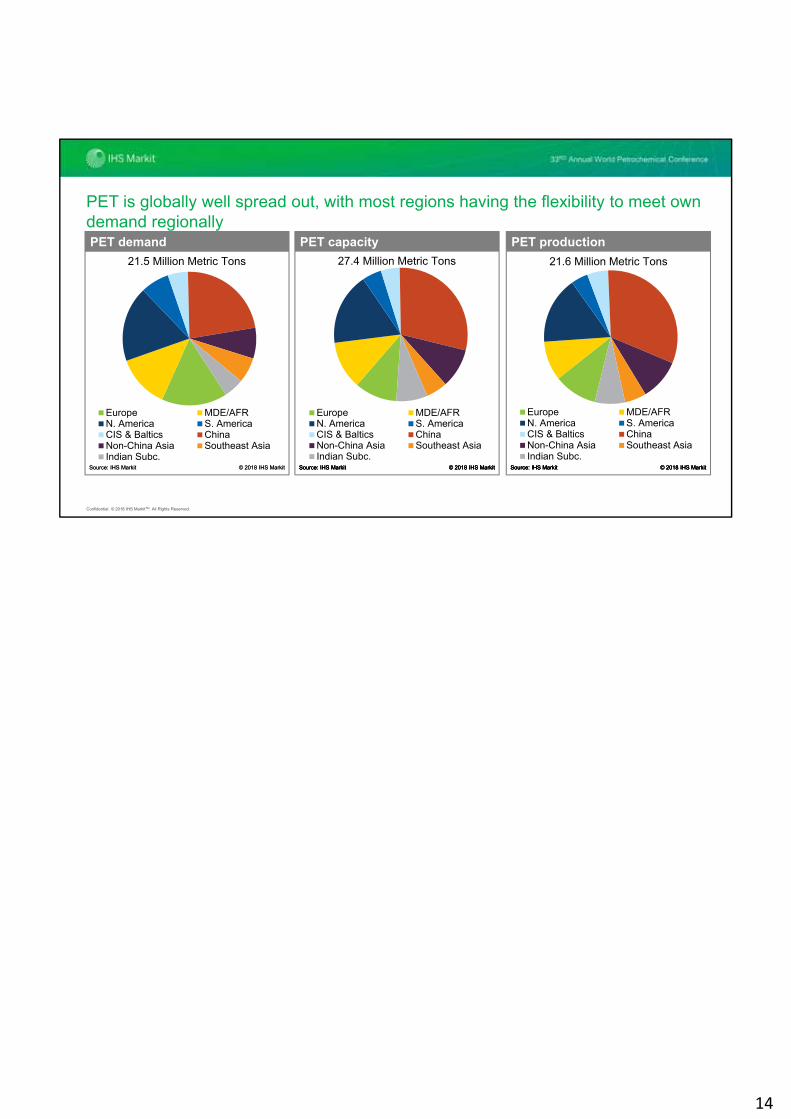

PET is globally well spread out, with most regions having the flexibility to meet own demand regionally

Europe MDE/AFRN. America S. AmericaCIS & Baltics ChinaNon-China Asia Southeast AsiaIndian Subc.

27.4 Million Metric Tons

PET

Source: IHS Markit © 2018 IHS Markit

PET Capacity

Source: IHS Markit © 2018 IHS Markit

PET

Source: IHS Markit © 2018 IHS Markit

PET capacity

Source: IHS Markit © 2018 IHS Markit

Europe MDE/AFRN. America S. AmericaCIS & Baltics ChinaNon-China Asia Southeast AsiaIndian Subc.

21.6 Million Metric Tons

PET

Source: IHS Markit © 2018 IHS Markit

PET Capacity

Source: IHS Markit © 2018 IHS Markit

PET

Source: IHS Markit © 2018 IHS Markit

PET production

Source: IHS Markit © 2018 IHS Markit

Europe MDE/AFRN. America S. AmericaCIS & Baltics ChinaNon-China Asia Southeast AsiaIndian Subc.

21.5 Million Metric Tons

PET

Source: IHS Markit © 2018 IHS Markit

PET demand

Source: IHS Markit © 2018 IHS Markit

14

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

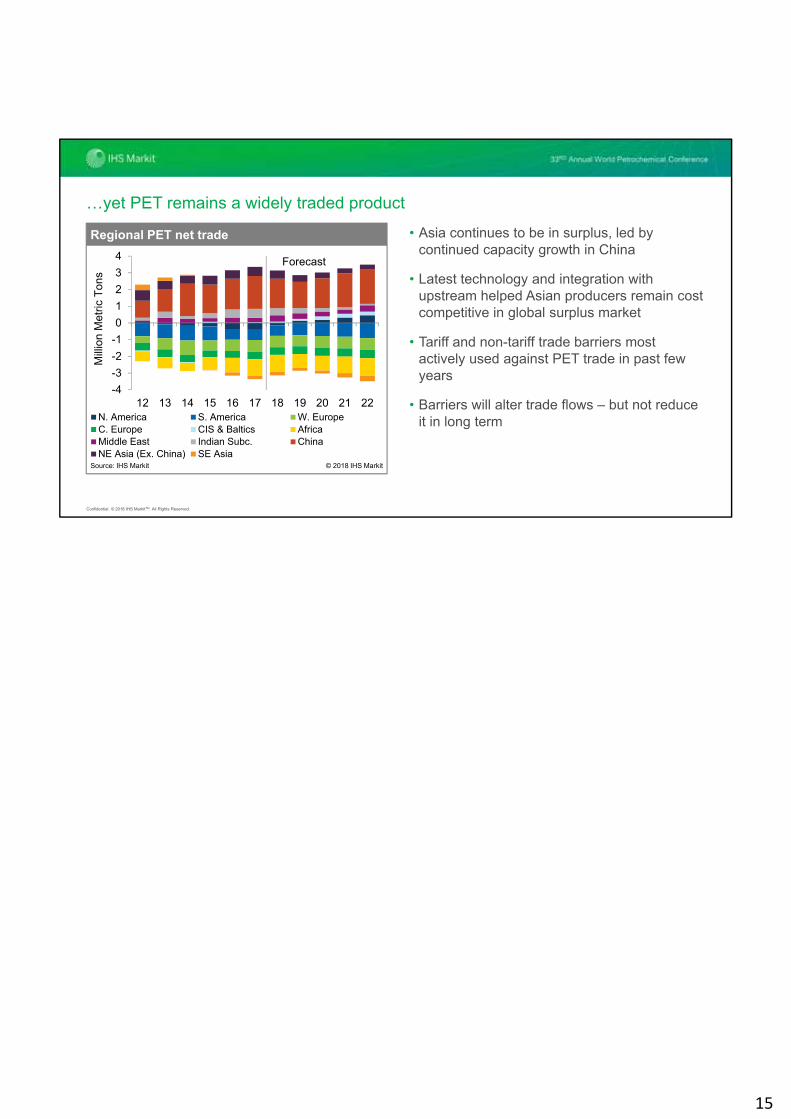

…yet PET remains a widely traded product

• Asia continues to be in surplus, led by continued capacity growth in China

• Latest technology and integration with upstream helped Asian producers remain cost competitive in global surplus market

• Tariff and non-tariff trade barriers most actively used against PET trade in past few years

• Barriers will alter trade flows – but not reduce it in long term

-4

-3

-2

-1

0

1

2

3

4

12 13 14 15 16 17 18 19 20 21 22N. America S. America W. EuropeC. Europe CIS & Baltics AfricaMiddle East Indian Subc. ChinaNE Asia (Ex. China) SE Asia

Regional PET net trade

Forecast

Mill

ion

Met

ric T

ons

Source: IHS Markit © 2018 IHS Markit

15

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

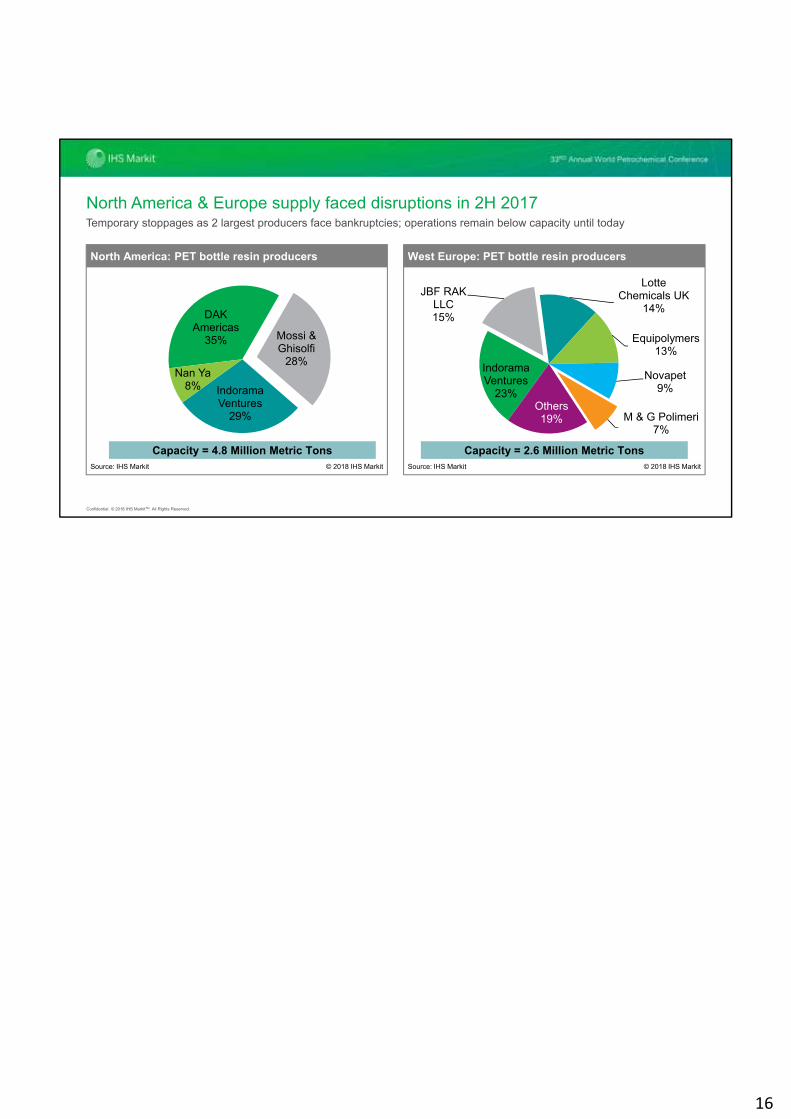

DAK Americas

35% Mossi & Ghisolfi

28%

Indorama Ventures

29%

Nan Ya8%

Capacity = 4.8 Million Metric Tons

North America: PET bottle resin producers

© 2018 IHS MarkitSource: IHS Markit

Indorama Ventures

23%

JBF RAK LLC15%

Lotte Chemicals UK

14%

Equipolymers13%

Novapet9%

M & G Polimeri7%

Others19%

Capacity = 2.6 Million Metric Tons

West Europe: PET bottle resin producers

© 2018 IHS MarkitSource: IHS Markit

Temporary stoppages as 2 largest producers face bankruptcies; operations remain below capacity until today

North America & Europe supply faced disruptions in 2H 2017

16

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

0

50

100

150

200

250

Jan-

17

Feb

-17

Mar

-17

Apr

-17

May

-17

Jun-

17

Jul-1

7

Aug

-17

Sep

-17

Oct

-17

Nov

-17

Dec

-17

Jan-

18

NAM SAM USA NEA SEA JAPISC WEP CEP AFR CIS MDE

PET: Exports from China

Tho

usan

d M

etric

Ton

s

Source: IHS Markit © 2018 IHS Markit

0

10

20

30

40

50

Jan-

17

Feb

-17

Mar

-17

Apr

-17

May

-17

Jun-

17

Jul-1

7

Aug

-17

Sep

-17

Oct

-17

Nov

-17

Dec

-17

Jan-

18

NAM SAM USA NEA SEA JAPISC WEP CEP AFR CIS MDE

PET: Exports from South Korea

Tho

usan

dM

etric

Ton

s

Source: IHS Markit © 2018 IHS Markit

Trade barriers altering trade flows, overall trade volumes still increasing

Asian exporters have benefitted from global supply disruptions

17

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

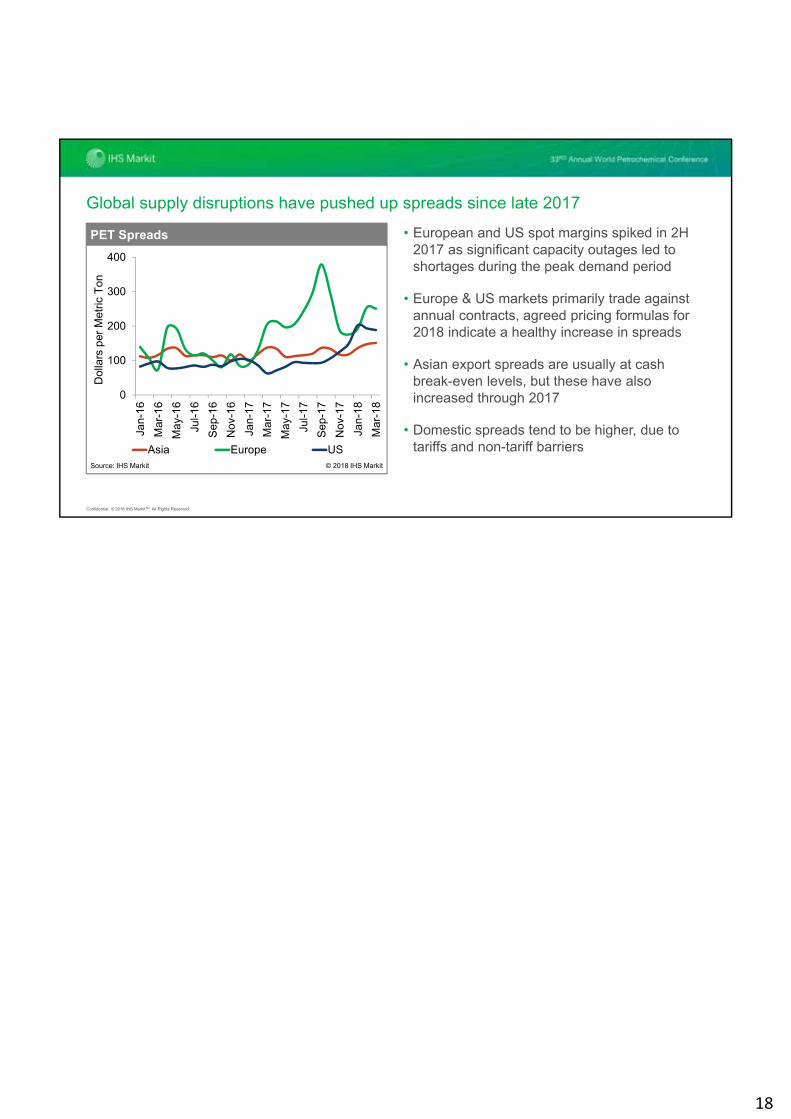

Global supply disruptions have pushed up spreads since late 2017

0

100

200

300

400

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep

-16

Nov

-16

Jan-

17

Mar

-17

May

-17

Jul-1

7

Sep

-17

Nov

-17

Jan-

18

Mar

-18

Asia Europe US

PET Spreads

Source: IHS Markit © 2018 IHS Markit

Dol

lars

per

Met

ric T

on

• European and US spot margins spiked in 2H 2017 as significant capacity outages led to shortages during the peak demand period

• Europe & US markets primarily trade against annual contracts, agreed pricing formulas for 2018 indicate a healthy increase in spreads

• Asian export spreads are usually at cash break-even levels, but these have also increased through 2017

• Domestic spreads tend to be higher, due to tariffs and non-tariff barriers

18

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

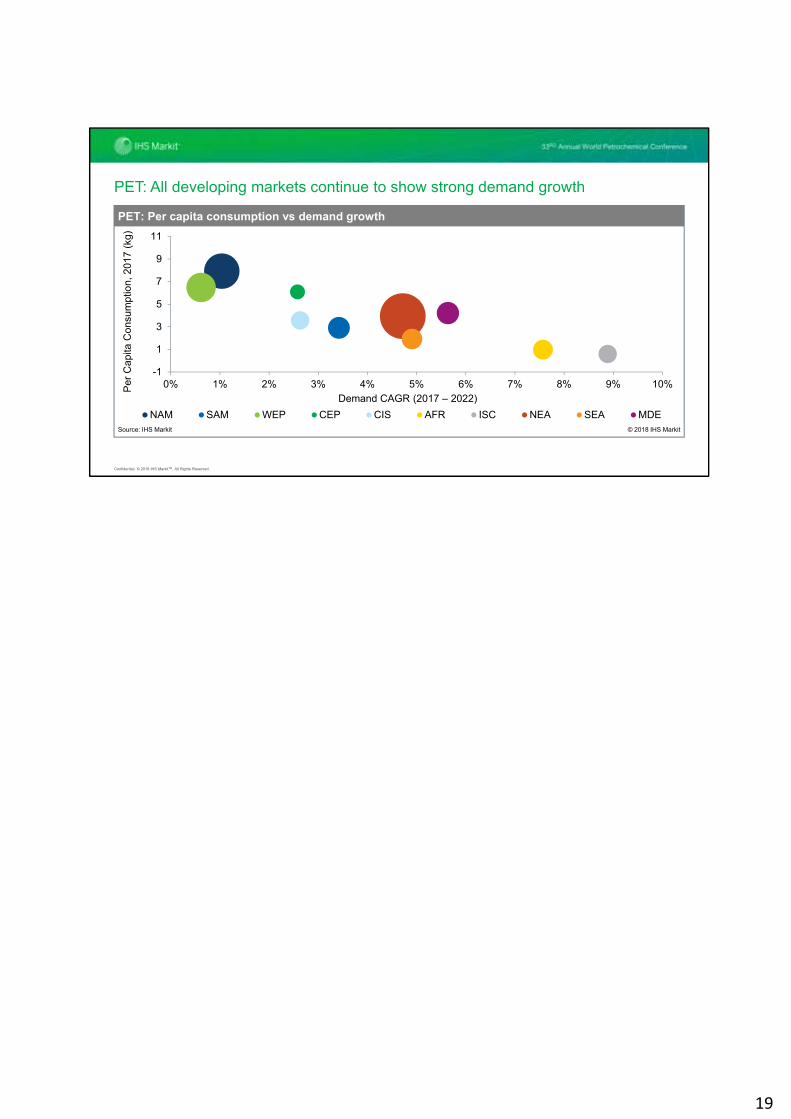

PET: All developing markets continue to show strong demand growth

-1

1

3

5

7

9

11

0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10%

NAM SAM WEP CEP CIS AFR ISC NEA SEA MDE

PET: Per capita consumption vs demand growth

Source: IHS Markit

Demand CAGR (2017 – 2022)

Per

Cap

ita C

onsu

mpt

ion,

201

7 (k

g)

© 2018 IHS Markit

19

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

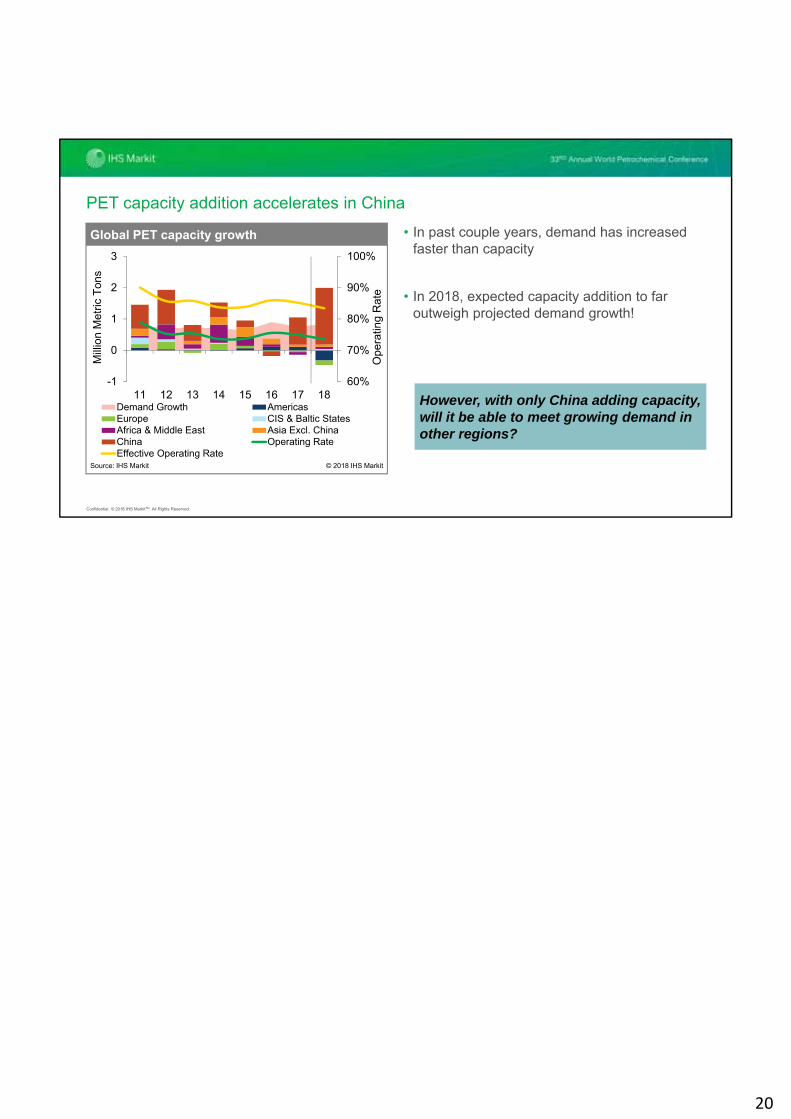

60%

70%

80%

90%

100%

-1

0

1

2

3

11 12 13 14 15 16 17 18Demand Growth AmericasEurope CIS & Baltic StatesAfrica & Middle East Asia Excl. ChinaChina Operating RateEffective Operating Rate

Global PET capacity growth

Mill

ion

Met

ric T

ons

Ope

ratin

g R

ate

Source: IHS Markit © 2018 IHS Markit

• In past couple years, demand has increased faster than capacity

• In 2018, expected capacity addition to far outweigh projected demand growth!

PET capacity addition accelerates in China

However, with only China adding capacity, will it be able to meet growing demand in other regions?

20

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

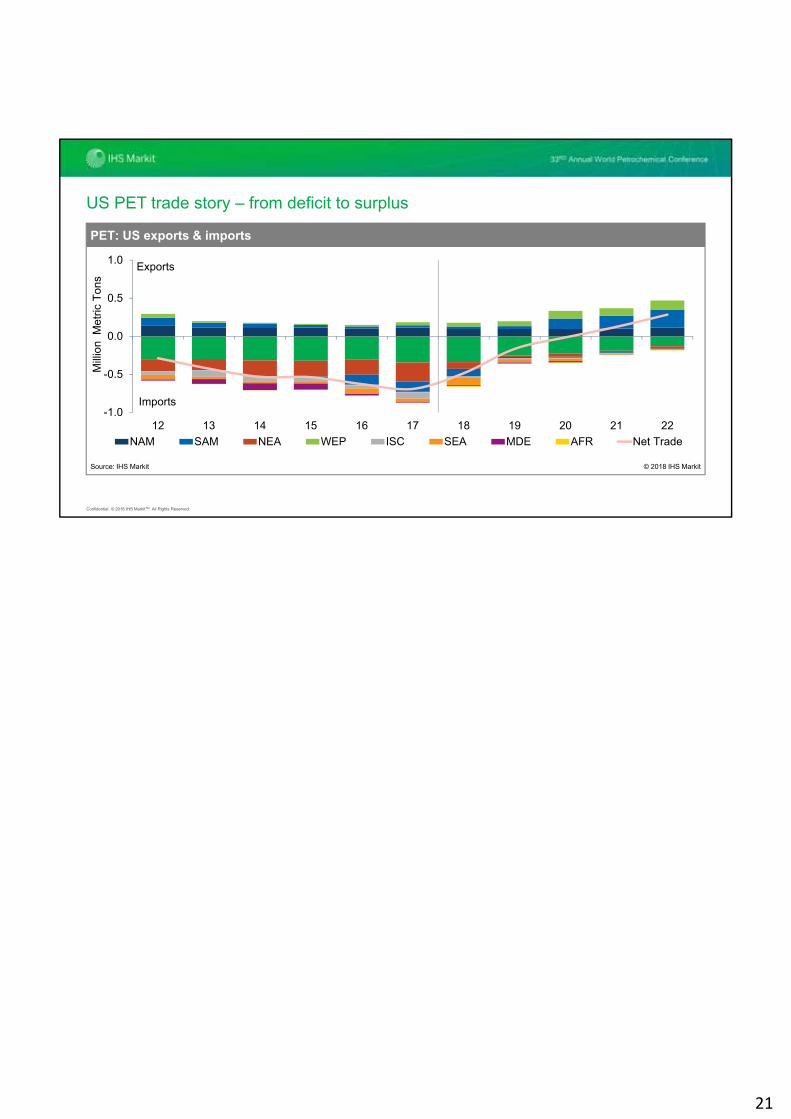

US PET trade story – from deficit to surplus

-1.0

-0.5

0.0

0.5

1.0

12 13 14 15 16 17 18 19 20 21 22

NAM SAM NEA WEP ISC SEA MDE AFR Net Trade

PET: US exports & imports

Mill

ion

Met

ric T

ons

Source: IHS Markit © 2018 IHS Markit

Imports

Exports

21

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Polyester fibersBroad-based economic growth leads to revival in fibers demand

Credit: Shutterstock

22

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

40

70

100

130

46,000 51,000 56,000 61,000 66,000 71,000 76,000 81,000 86,000 91,000 96,000

20112013

2017

2015

Total Natural and Man-Made Fibers

Source: IHS Markit © 2018 IHS MarkitGDP (Billion 2010 $)

Fib

ers,

Mill

ion

Met

ric T

ons 2019

2000

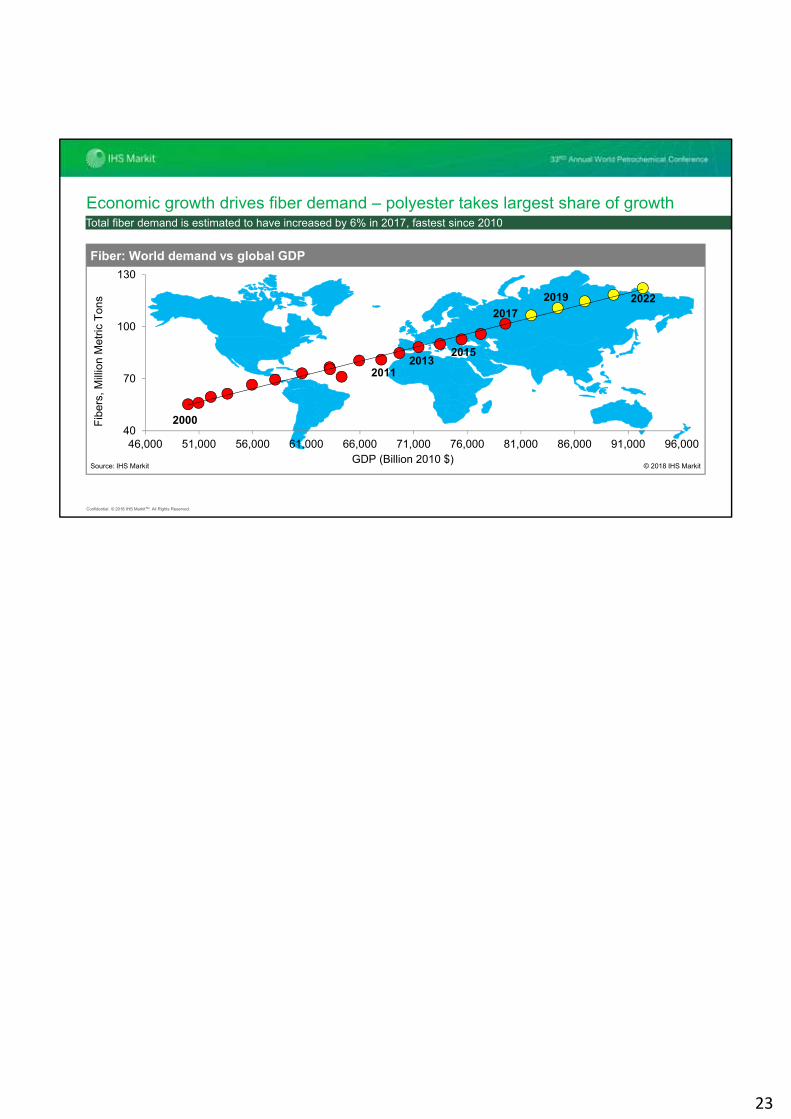

Fiber: World demand vs global GDP

2022

Economic growth drives fiber demand – polyester takes largest share of growthTotal fiber demand is estimated to have increased by 6% in 2017, fastest since 2010

23

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Global Fibers mix – dominated by polyester & cotton

Polyester49%

Cotton26%

Olefin10%

Cellulosic6%

Nylon4%

Acrylic2%

Other Synthetic Fibers1%

Wool, Silk & Linen2%

Polyester

Cotton

Olefin

Cellulosic

Nylon

Acrylic

Other Synthetic Fibers

Wool, Silk & Linen

World fiber demand in 2017

Source: IHS Markit © 2018 IHS Markit

2017 total fiber demand: 101.7 Million Metric Tons

24

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

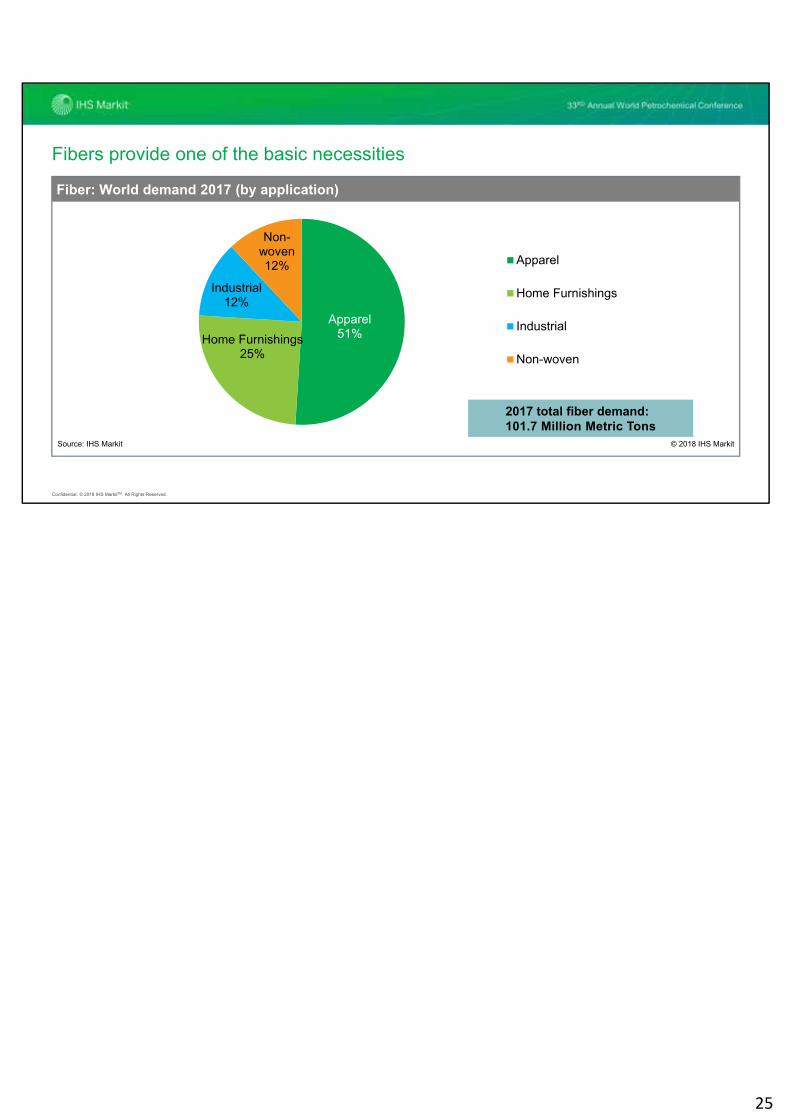

Fibers provide one of the basic necessities

2017 total fiber demand: 101.7 Million Metric Tons

Apparel51%Home Furnishings

25%

Industrial12%

Non-woven12% Apparel

Home Furnishings

Industrial

Non-woven

Fiber: World demand 2017 (by application)

Source: IHS Markit © 2018 IHS Markit

25

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Europe MDE/AFRN. America S. AmericaCIS & Baltics ChinaNon-China Asia Southeast Asia

World: Total Polyester Fiber Demand (2017)

Source: IHS Markit © 2018 IHS Markit

Polyester fibers demand…heavily skewed towards China

• In 2017, China alone accounts for

• 66% of global demand

• 71% of global production

• up from a 25% share in the year 2000

• In total, Asia accounts for 86% of global demand.

• Lower labor costs initially attracted investments in the textile sector in Asia.

• Fast developing economies, rapid urbanization and strong growth in disposable income is now sustaining the growth in regional textile industry.

2017 demand: 49.8 Million Metric Tons

26

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

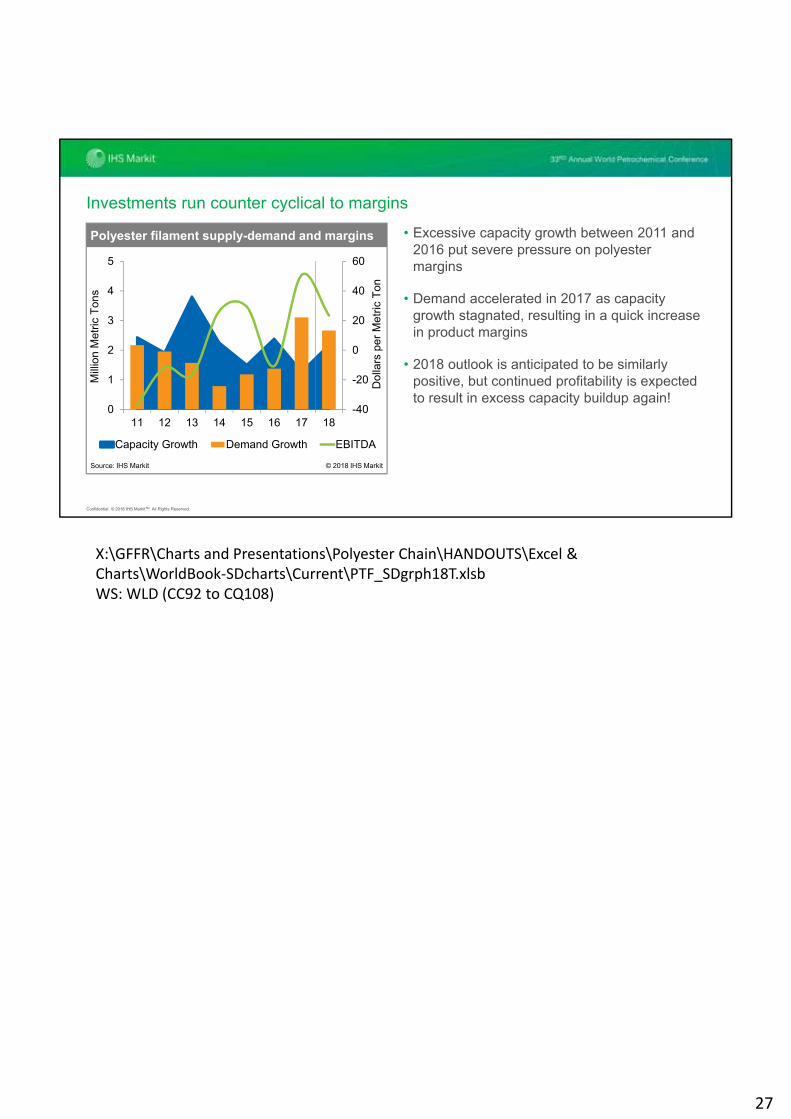

Investments run counter cyclical to margins

• Excessive capacity growth between 2011 and 2016 put severe pressure on polyester margins

• Demand accelerated in 2017 as capacity growth stagnated, resulting in a quick increase in product margins

• 2018 outlook is anticipated to be similarly positive, but continued profitability is expected to result in excess capacity buildup again!

-40

-20

0

20

40

60

0

1

2

3

4

5

11 12 13 14 15 16 17 18

Capacity Growth Demand Growth EBITDA

Mill

ion

Met

ric T

ons

Polyester filament supply-demand and margins

Source: IHS Markit © 2018 IHS Markit

Dol

lars

per

Met

ric T

on

X:\GFFR\Charts and Presentations\Polyester Chain\HANDOUTS\Excel & Charts\WorldBook‐SDcharts\Current\PTF_SDgrph18T.xlsbWS: WLD (CC92 to CQ108)

27

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

0

20

40

60

80

12 13 14 15 16 17 18 19 20 21 22N. America S. America W. Europe C. Europe CIS & BalticsAfrica Middle East Indian Subc. NE Asia SE Asia

Mill

ion

Met

ric T

ons

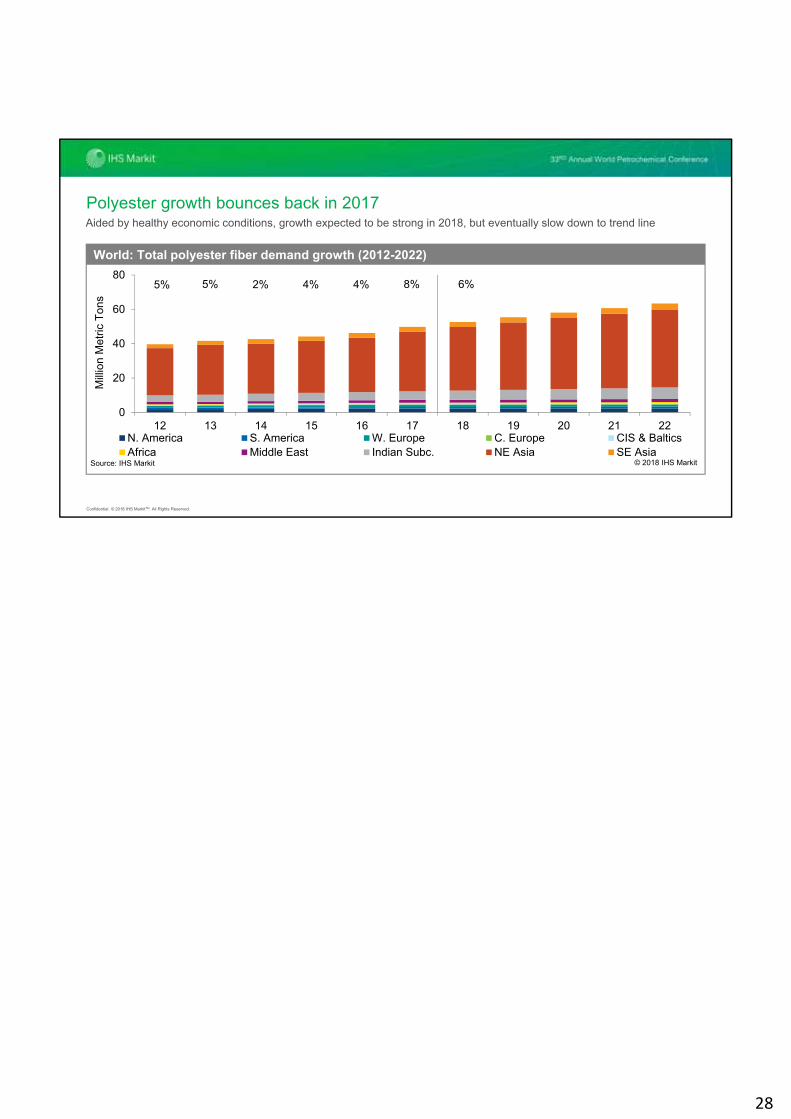

World: Total polyester fiber demand growth (2012-2022)

Source: IHS Markit © 2018 IHS Markit

5% 4% 4% 8% 6%5% 2%

Polyester growth bounces back in 2017Aided by healthy economic conditions, growth expected to be strong in 2018, but eventually slow down to trend line

28

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

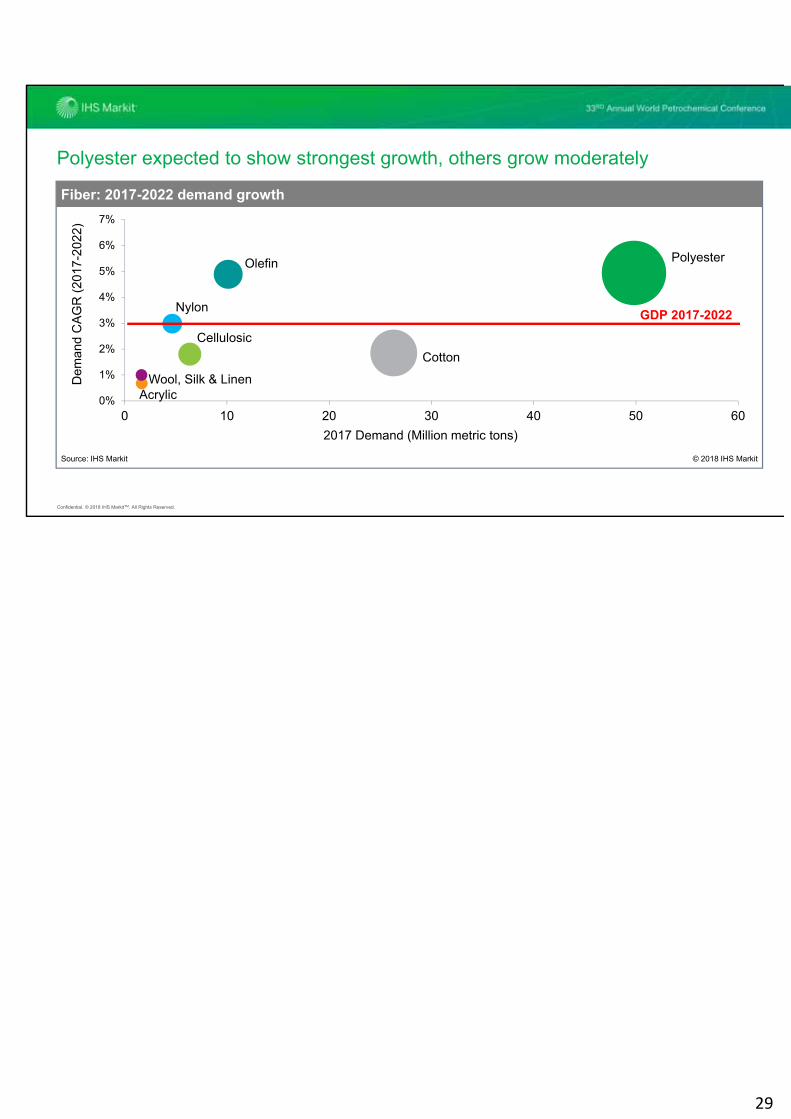

Polyester expected to show strongest growth, others grow moderately

Cotton

Polyester

Nylon

Olefin

Cellulosic

AcrylicWool, Silk & Linen

0%

1%

2%

3%

4%

5%

6%

7%

0 10 20 30 40 50 60

Fiber: 2017-2022 demand growth

Source: IHS Markit

2017 Demand (Million metric tons)

Dem

and

CA

GR

(20

17-2

022)

© 2018 IHS Markit

GDP 2017-2022

29

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

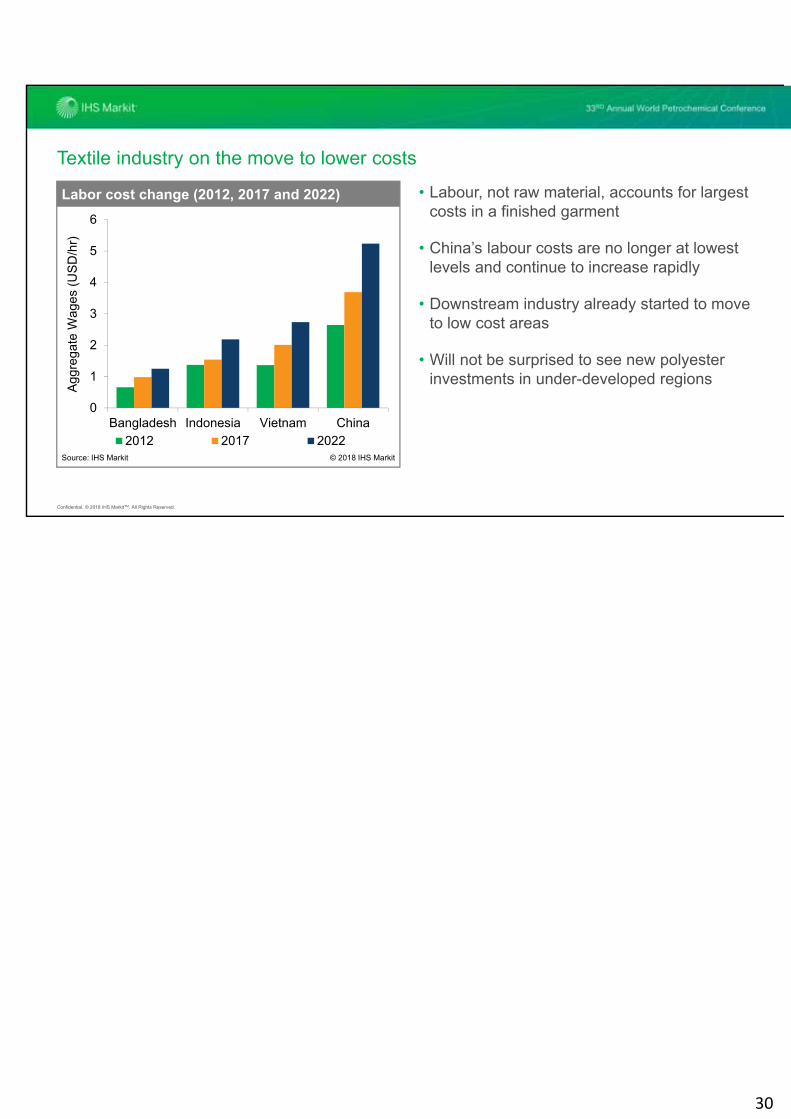

Textile industry on the move to lower costs

• Labour, not raw material, accounts for largest costs in a finished garment

• China’s labour costs are no longer at lowest levels and continue to increase rapidly

• Downstream industry already started to move to low cost areas

• Will not be surprised to see new polyester investments in under-developed regions

0

1

2

3

4

5

6

Bangladesh Indonesia Vietnam China

2012 2017 2022

Labor cost change (2012, 2017 and 2022)

Source: IHS Markit © 2018 IHS Markit

Agg

rega

teW

ages

(US

D/h

r)

30

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Key takeaways

Demand growth expected to be strong in 2018

Fastest growing fiber for many years to come

Polyester fibersMarkets expected

to remain tight through 2018

Increasing brand owner focus on

recycling

PET

Sudden policy changes affect

short-term growth

Newer recycling avenues expected

in longer term

Recycling

31

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Contact details

Ashish PujariExecutive Director \ Aromatics & Fibers

+65 6439 [email protected]

33

IHS Markit Customer [email protected]

Americas: +1 800 IHS CARE (+1 800 447 2273)

Europe, Middle East, and Africa: +44 (0) 1344 328 300

Asia and the Pacific Rim: +604 291 3600

DisclaimerThe information contained in this presentation is confidential. Any unauthorized use, disclosure, reproduction, or dissemination, in full or in part, in any media or by any means, without the prior written permission of IHS Markit Ltd. or any of its affiliates ("IHS Markit") is strictly prohibited. IHS Markit owns all IHS Markit logos and trade names contained in this presentation that are subject to license. Opinions, statements, estimates, and projections in this presentation (including other media) are solely those of the individual author(s) at the time of writing and do not necessarily reflect the opinions of IHS Markit. Neither IHS Markit nor the author(s) has any obligation to update this presentation in the event that any content, opinion, statement, estimate, or projection (collectively, "information") changes or subsequently becomes inaccurate. IHS Markit makes no warranty, expressed or implied, as to the accuracy, completeness, or timeliness of any information in this presentation, and shall not in any way be liable to any recipient for any inaccuracies or omissions. Without limiting the foregoing, IHS Markit shall have no liability whatsoever to any recipient, whether in contract, in tort (including negligence), under warranty, under statute or otherwise, in respect of any loss or damage suffered by any recipient as a result of or in connection with any information provided, or any course of action determined, by it or any third party, whether or not based on any information provided. The inclusion of a link to an external website by IHS Markit should not be understood to be an endorsement of that website or the site's owners (or their products/services). IHS Markit is not responsible for either the content or output of external websites. Copyright © 2017, IHS MarkitTM. All rights reserved and all intellectual property rights are retained by IHS Markit.

29