Embed Size (px)

Citation preview

Healthcare Solutions that Work

North Bay Business Journal – Healthcare ConferenceNovember 11, 2009

Ken ShachmutSenior Vice President – Safeway Inc.

Executive Vice President – Safeway Health LLC

2

Agenda

U. S. healthcare challenge

Safeway experience

Policy implications

Safeway Health

3

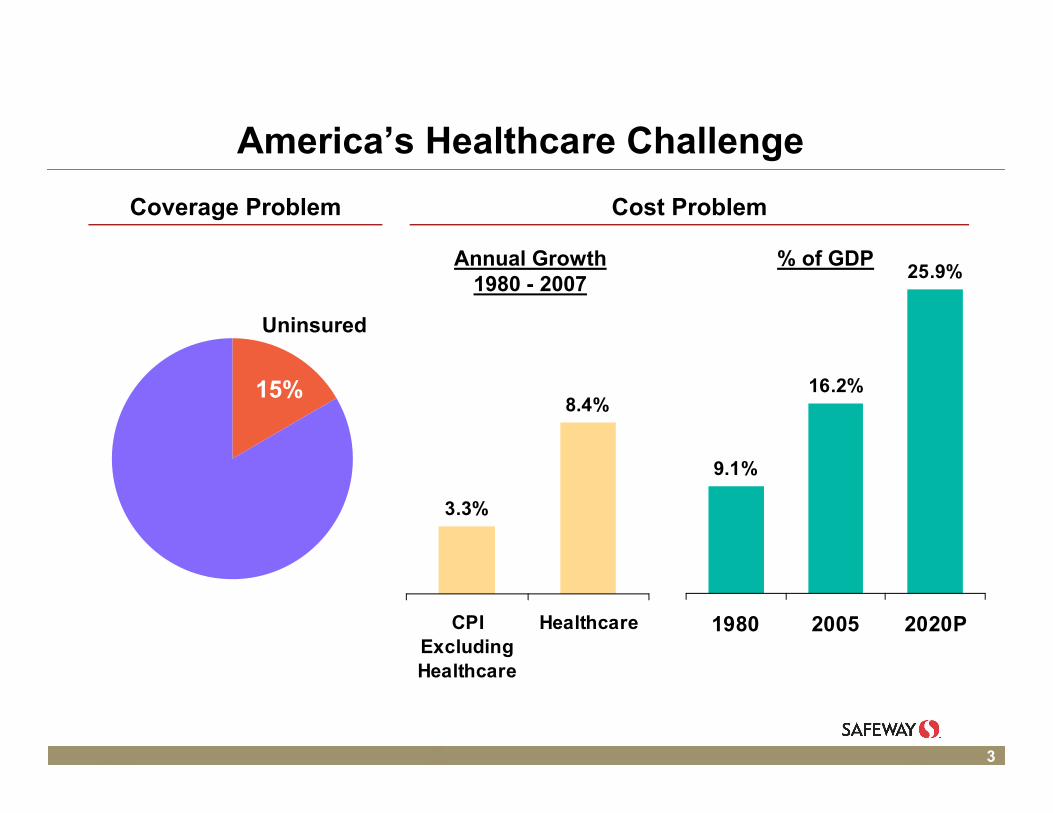

9.1%

16.2%

25.9%

1980 2005 2020P

America’s Healthcare Challenge

15%

Uninsured

3.3%

8.4%

CPIExcludingHealthcare

Healthcare

Annual Growth1980 - 2007

% of GDP

Coverage Problem Cost Problem

4

Lowering America’s Healthcare Cost Requires:

Improving the health of our population

Improving the effectiveness and efficiency of our healthcare delivery system

A market-based system in combination with universal coverage would address both of these requirements

5

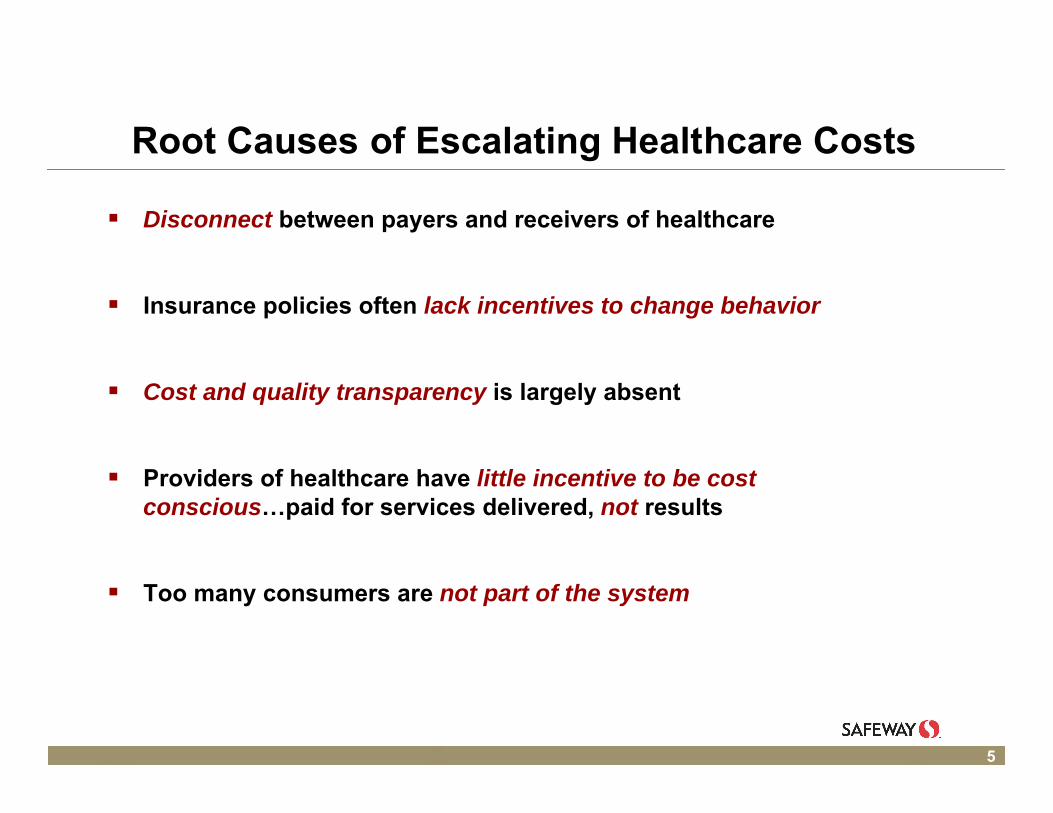

Root Causes of Escalating Healthcare Costs

Disconnect between payers and receivers of healthcare

Insurance policies often lack incentives to change behavior

Cost and quality transparency is largely absent

Providers of healthcare have little incentive to be cost conscious…paid for services delivered, not results

Too many consumers are not part of the system

6

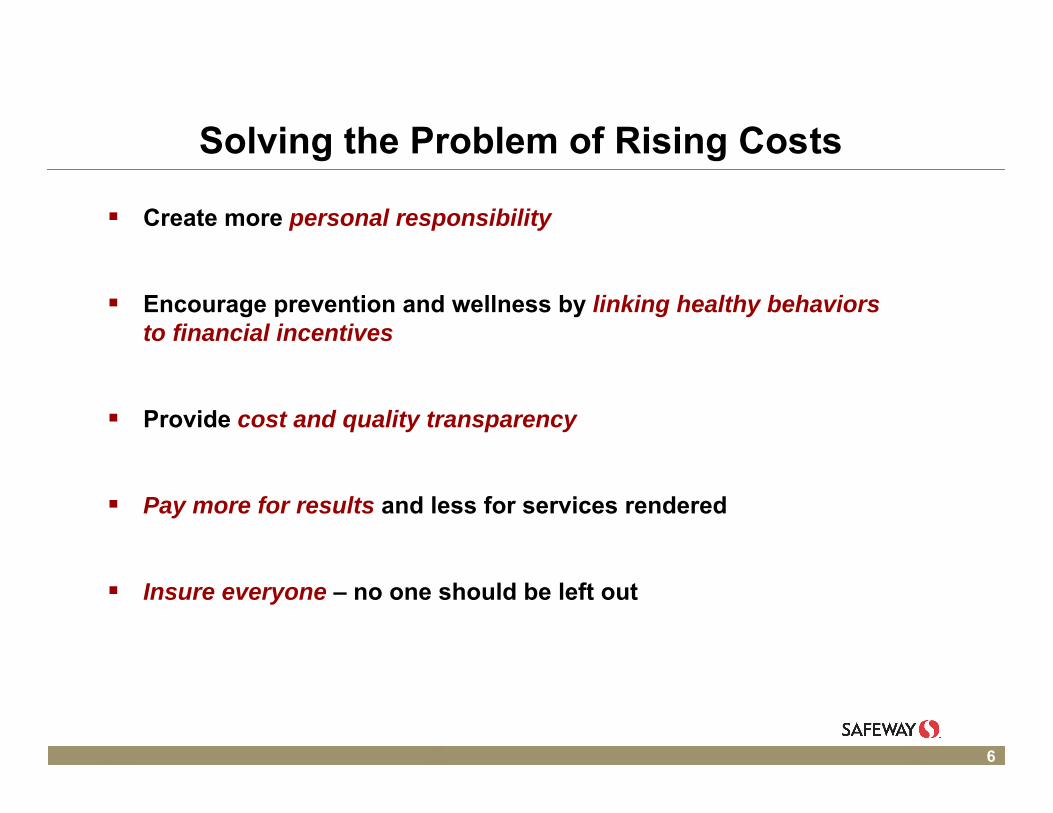

Solving the Problem of Rising Costs

Create more personal responsibility

Encourage prevention and wellness by linking healthy behaviors to financial incentives

Provide cost and quality transparency

Pay more for results and less for services rendered

Insure everyone – no one should be left out

7

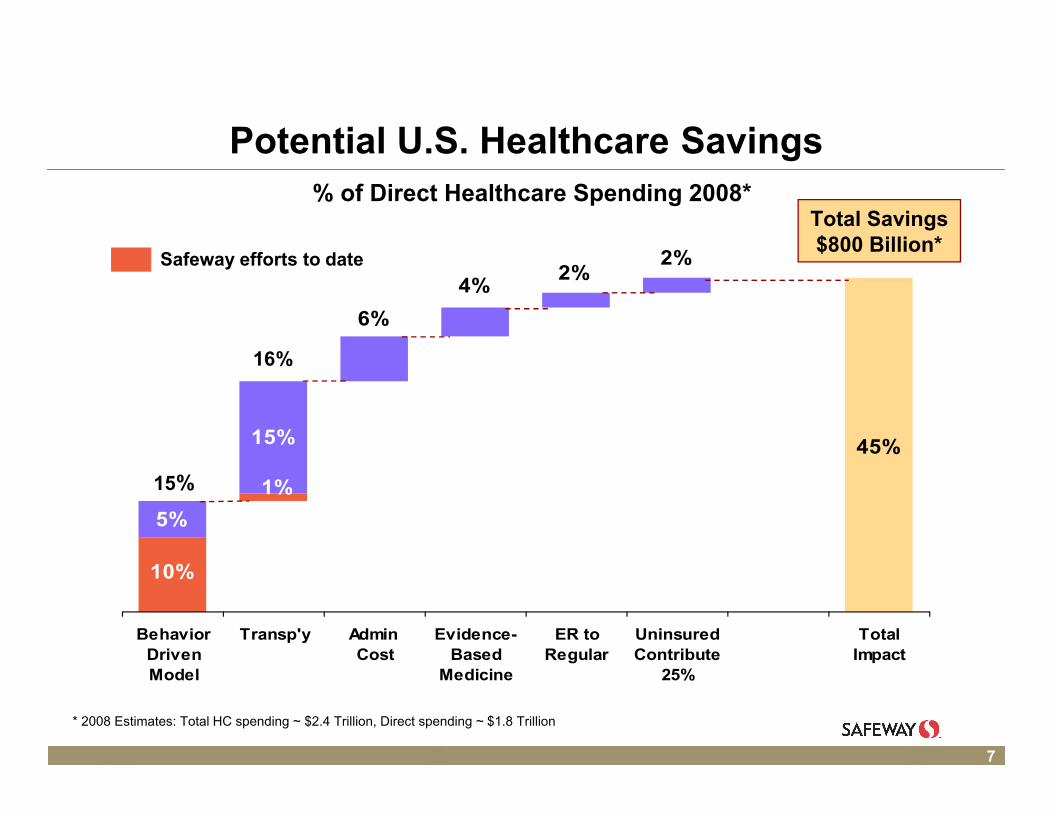

Potential U.S. Healthcare Savings

5%

10%

45%

2%2%

4%

6%

1%

15%

BehaviorDrivenModel

Transp'y Admin Cost

Evidence-Based

Medicine

ER toRegular

UninsuredContribute

25%

TotalImpact

% of Direct Healthcare Spending 2008*

* 2008 Estimates: Total HC spending ~ $2.4 Trillion, Direct spending ~ $1.8 Trillion

Total Savings $800 Billion*

Safeway efforts to date

15%

16%

8

Agenda

U. S. healthcare challenge

Safeway experience

Policy implications

Safeway Health

9

Safeway’s Healthcare Expense Trend*

101102949288

150138

100

128119

110

0

20

40

60

80

100

120

140

160

2005 2006 2007 2008 2009 F 2010 E

Index 2005 = 100

Business as Usual

New Plan

* Per-capita expenses for Safeway non-union EEs moving to new plan from former PPO plan

These per-capita expenses are all-inclusive – Safeway contribution, EE premium and EE out-of-pocket expense

CAGR

8.5%

0.2%

10

Safeway Healthcare SavingsShared by Safeway and Employees

$153

$78

$47

$53

$231

$34

$19

2006 2007 2008 2009F 2005 -2009F

2010E 2005 -2010E

Savings vs. BAU in $ Millions

LivesCovered

10,100 18,000 27,900 28,000 31,000E

11

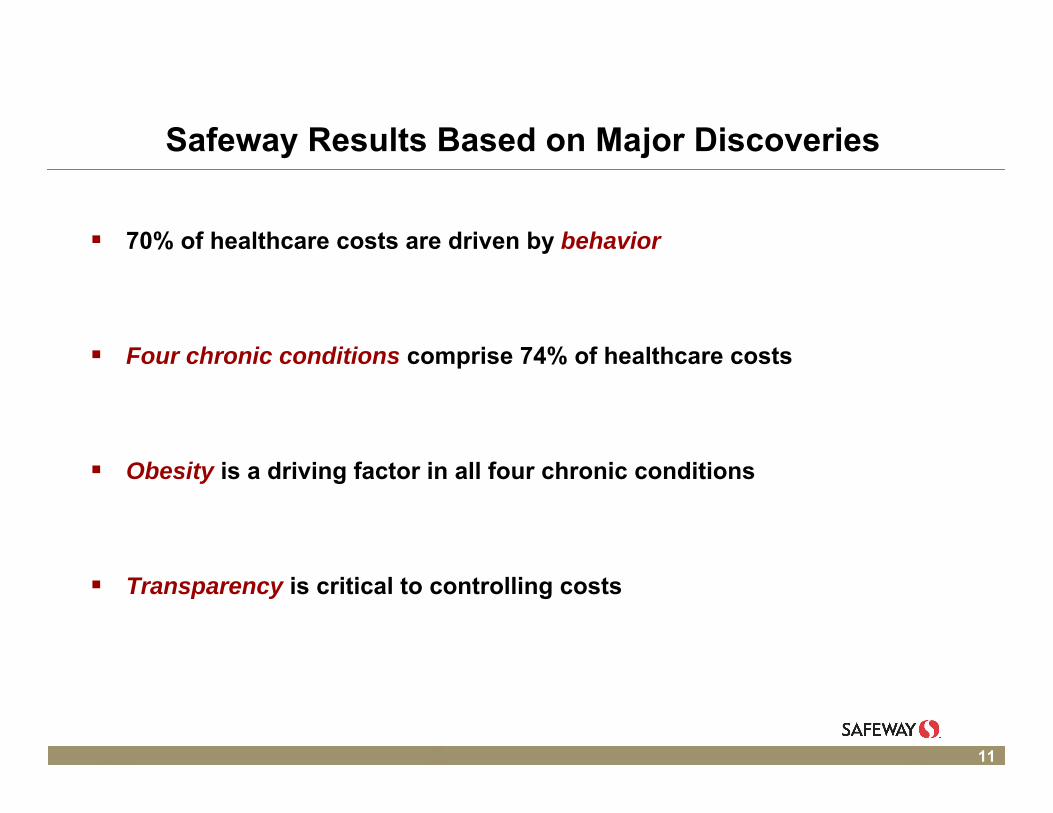

Safeway Results Based on Major Discoveries

70% of healthcare costs are driven by behavior

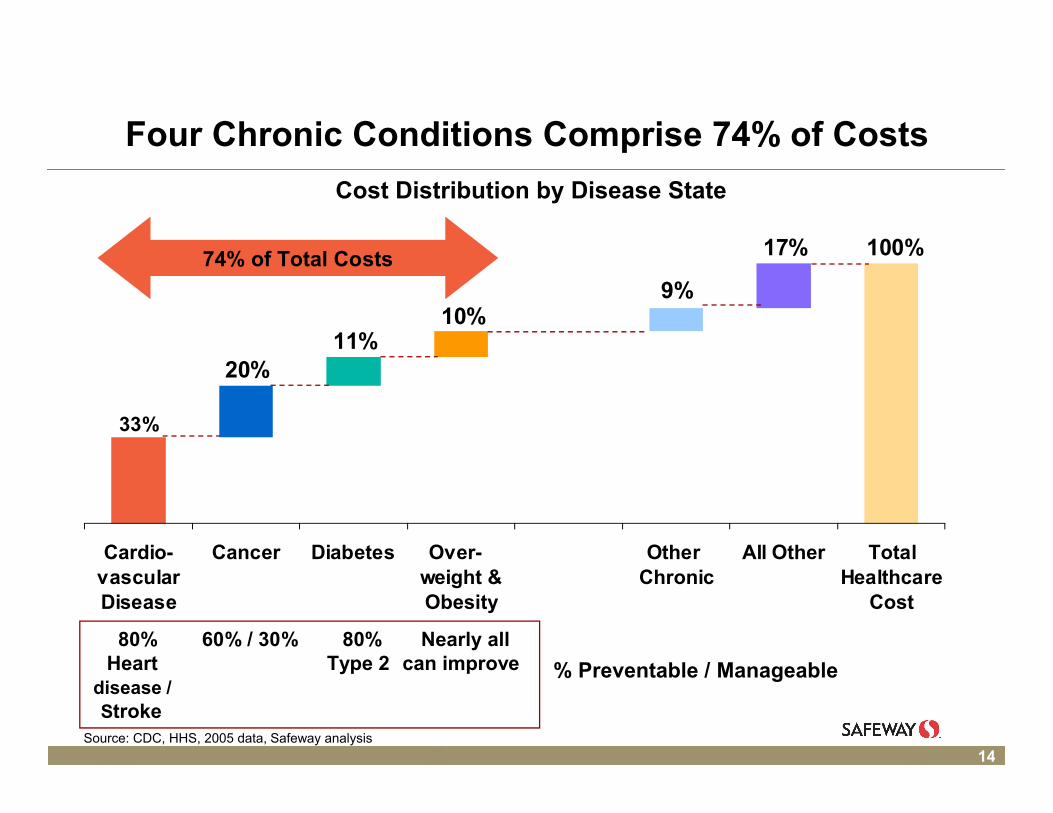

Four chronic conditions comprise 74% of healthcare costs

Obesity is a driving factor in all four chronic conditions

Transparency is critical to controlling costs

12

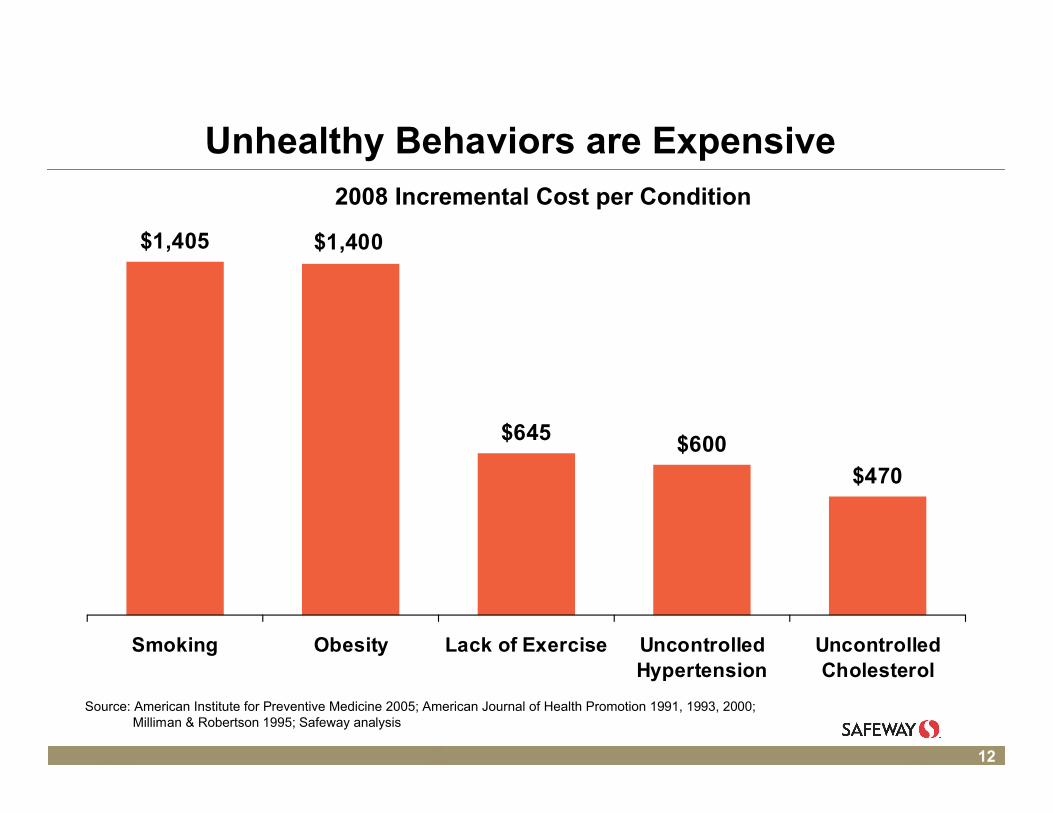

Unhealthy Behaviors are Expensive

$1,405

$645 $600

$470

$1,400

Smoking Obesity Lack of Exercise UncontrolledHypertension

UncontrolledCholesterol

2008 Incremental Cost per Condition

Source: American Institute for Preventive Medicine 2005; American Journal of Health Promotion 1991, 1993, 2000; Milliman & Robertson 1995; Safeway analysis

13

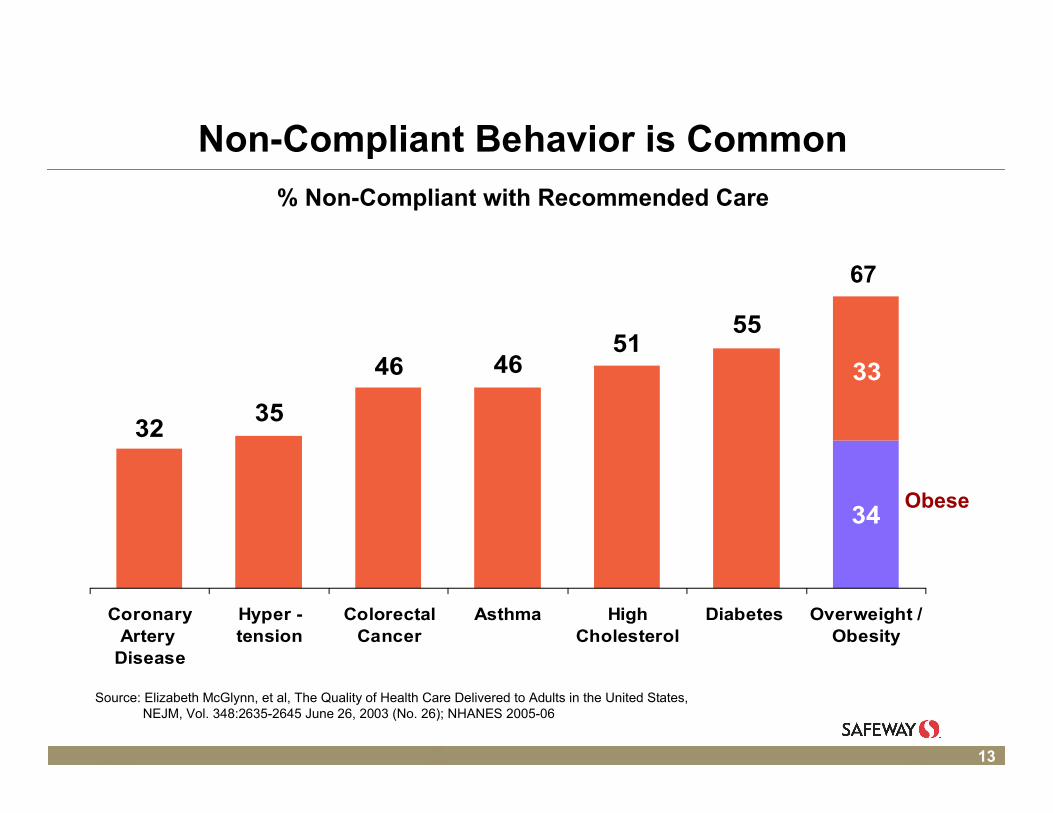

34

5551

4646

3532

33

CoronaryArtery

Disease

Hyper -tension

ColorectalCancer

Asthma HighCholesterol

Diabetes Overweight /Obesity

Non-Compliant Behavior is Common

% Non-Compliant with Recommended Care

Source: Elizabeth McGlynn, et al, The Quality of Health Care Delivered to Adults in the United States,NEJM, Vol. 348:2635-2645 June 26, 2003 (No. 26); NHANES 2005-06

Obese

67

14

% Preventable / Manageable

Four Chronic Conditions Comprise 74% of Costs

33%

20%11%

10%9%

17% 100%

Cardio-vascularDisease

Cancer Diabetes Over- weight &Obesity

Other Chronic

All Other TotalHealthcare

Cost

Cost Distribution by Disease State

74% of Total Costs

80% 60% / 30% 80% Nearly allHeart Type 2 can improve

disease /Stroke

Source: CDC, HHS, 2005 data, Safeway analysis

15

Obesity is a Major Cost Driver – Top 4

26%

19%

27%

10%

7%

1%

9%

2%

47%

CardiovascularDisease

Cancer Diabetes Overweight &Obesity

Big 4 Total

Top 4 chronic diseases - % of total healthcare spending

Obesity

All other

*2008 Estimates: Total HC spending ~ $2.4 Trillion, Direct spending ~ $1.8 Trillion

33%

20%

11%

74%

16

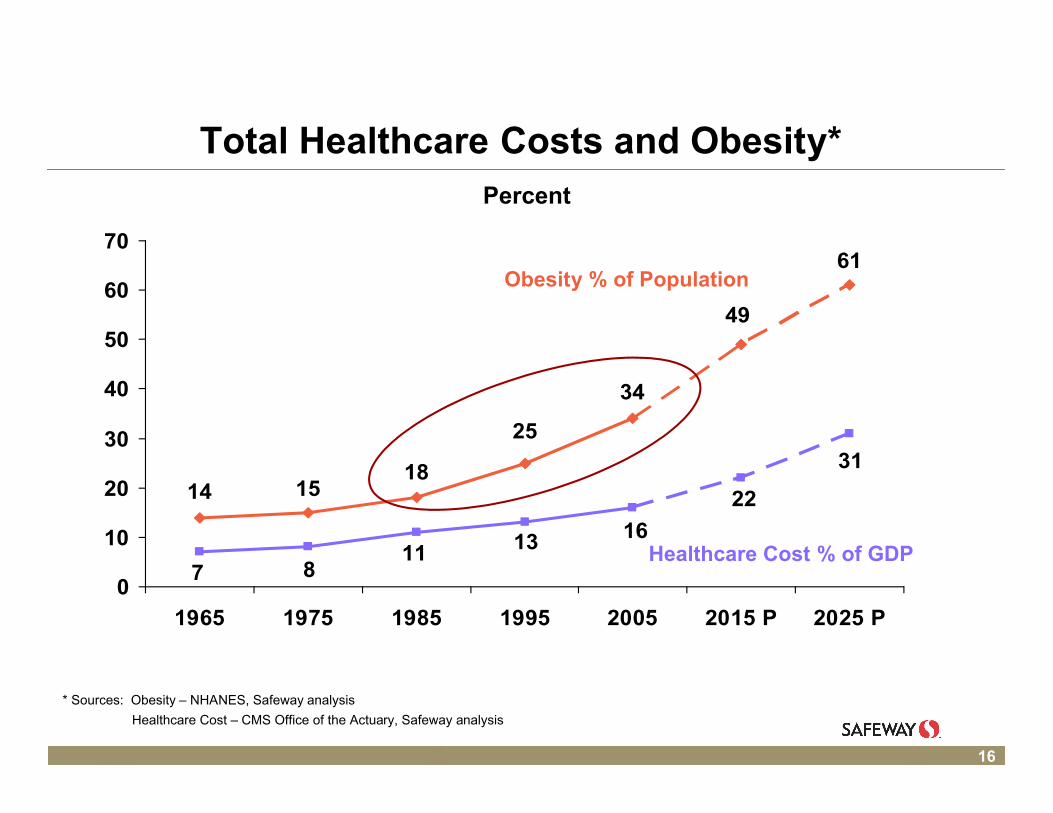

Total Healthcare Costs and Obesity*

31

22

16

7

13118

61

49

34

14

25

1815

0

10

20

30

40

50

60

70

1965 1975 1985 1995 2005 2015 P 2025 P

Percent

Obesity % of Population

Healthcare Cost % of GDP

* Sources: Obesity – NHANES, Safeway analysis

Healthcare Cost – CMS Office of the Actuary, Safeway analysis

17

Obesity Prevalence by Country

3 4

8 9 10 10 11 11 11 12 12 13 13 14 15 15 15 15 15 16 17 1719 20 20

2224

2730

34

Ja

pa

n

Ko

rea

Sw

itze

rla

nd

No

rwa

y

Ita

lyS

we

de

n

Fra

nc

eN

eth

erl

an

dD

en

ma

rk

Tu

rke

yA

us

tria

Po

lan

dB

elg

ium

Ge

rma

ny

Fin

lan

dS

pa

in

Ire

lan

dC

an

ad

aP

ort

ug

al

Gre

ec

eS

lov

ak

Cze

ch

Hu

ng

ary

Lu

xe

mb

ou

r

Ice

lan

dA

us

tra

lia UK

N Z

ea

lan

dM

ex

ico

US

A

Obesity Prevalence for Adult Population (Aged 15+) by Country1

Notes: (1) Estimates relate to the adult population (aged 15+), based on national health interview surveys for most countries. Rates are based on most recent data available, with years ranging between 2003-2007.

Source: OECD Health Data, http://www.oecd.org/document/16/0,3343,en_2649_34631_2085200_1_1_1_1,00.html

Percent of Population

18

Philosophy for Behavior Incentives

Individuals are responsible for their own behavior*

Health plans should be free to charge individuals the full cost of their behaviors

When consumers bear the true cost, they are motivated to change

The result will be improved health, higher productivity, and lower healthcare costs

*But not their genetics

19

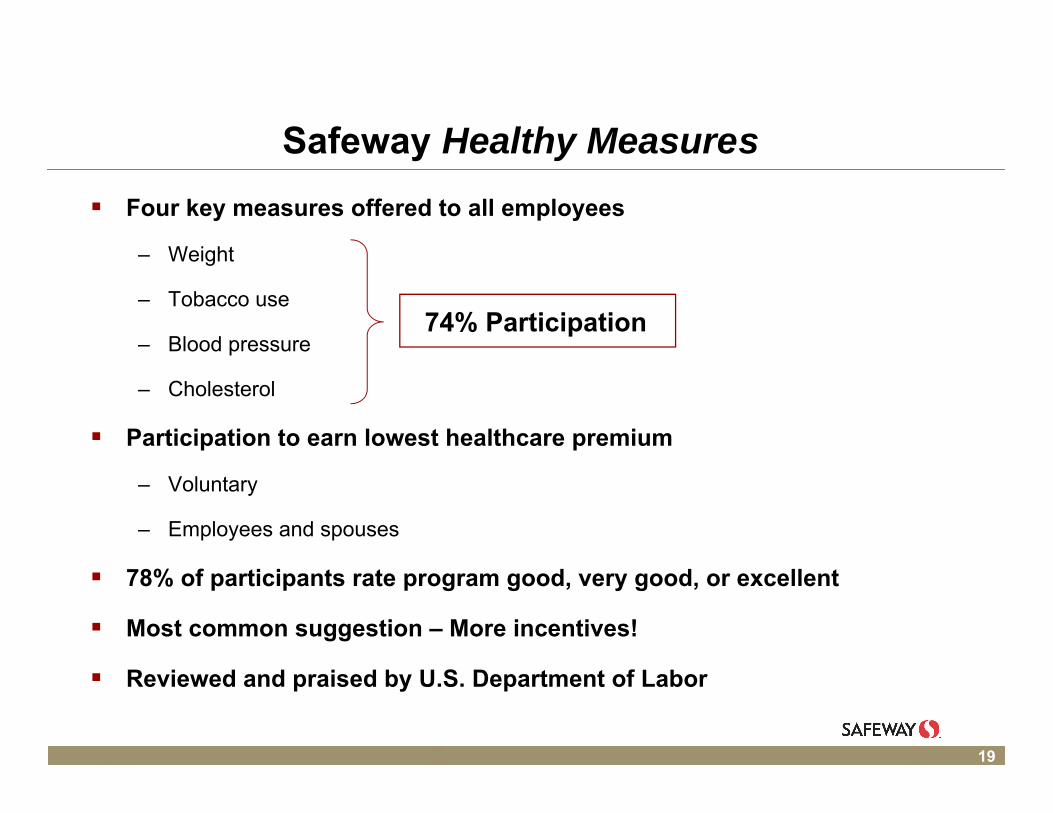

Safeway Healthy Measures

Four key measures offered to all employees

– Weight

– Tobacco use

– Blood pressure

– Cholesterol

Participation to earn lowest healthcare premium

– Voluntary

– Employees and spouses

78% of participants rate program good, very good, or excellent

Most common suggestion – More incentives!

Reviewed and praised by U.S. Department of Labor

74% Participation

20

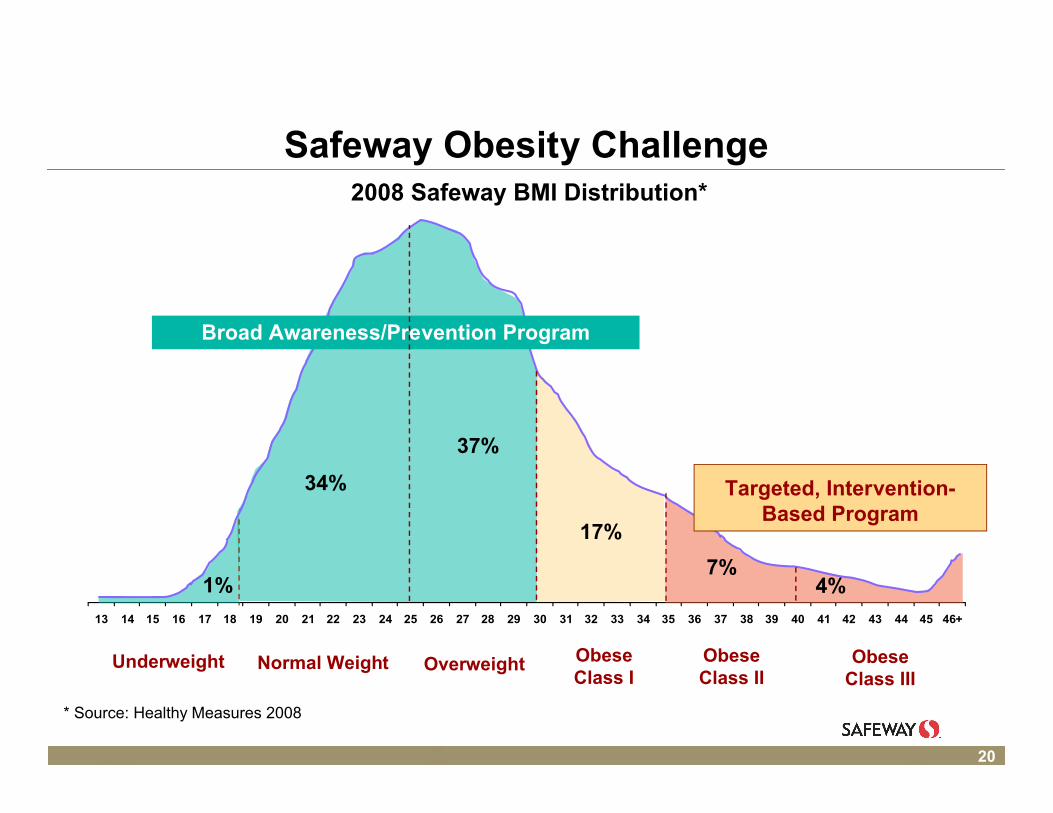

Safeway Obesity Challenge2008 Safeway BMI Distribution*

* Source: Healthy Measures 2008

13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46+

4%7%

37%

17%

34%

1%

Obese Class I

OverweightNormal WeightUnderweight Obese Class II

Obese Class III

Broad Awareness/Prevention Program

Targeted, Intervention-Based Program

21

0

50

100

150

200

250

18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46+

0

50

100

150

200

250

18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46+

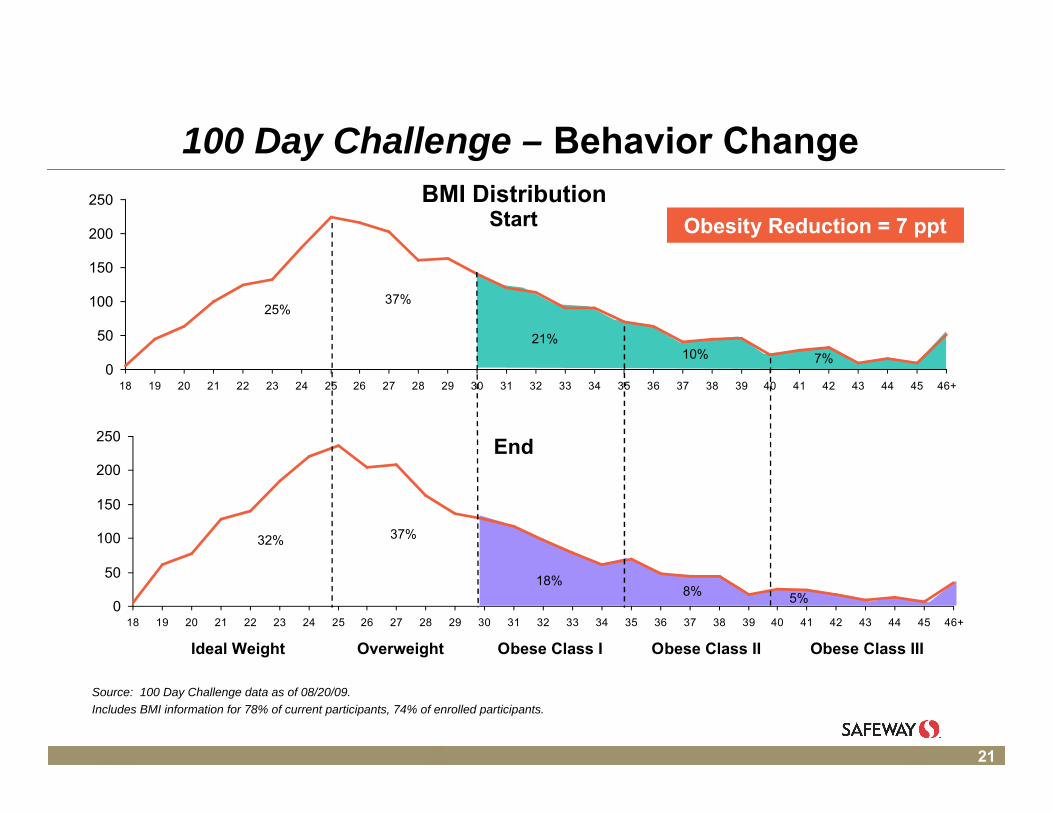

100 Day Challenge – Behavior Change

Source: 100 Day Challenge data as of 08/20/09.

Includes BMI information for 78% of current participants, 74% of enrolled participants.

Start

32% 37%

18%8% 5%

25%37%

21%10% 7%

End

Ideal Weight Overweight Obese Class I Obese Class II Obese Class III

Obesity Reduction = 7 ppt

BMI Distribution

22

Healthy Weight Commitment Foundation*Tackling Obesity Nationwide

Over 40 food manufacturers and retailers working together

Comprehensive approach to battling obesity

Focused on individual consumers, in schools, and in the workplace

Launched at National Press Club – October 5, 2009

* Food industry initiative; Safeway is Co-Founder

23

1,750 Less Calories In per WeekMany ways to achieve the goal – 250 / day

Keep the volume and taste, not the calories

Handful of raisins instead

of candy

Replace 1-traditional

dressing withvery low cal

dressing

One lesschocolate chip

cookie

Substitute 2 diet soda

for 2 reg soda

1 less Café Latte

Cutting1,750 cals/wk

24

1,750 More Calories Out per WeekMany ways to achieve the goal – 250 / day

Add activities incremental to normal movement

65 minutes shopping at

Safeway 7 days / week

45 minuteswalking at 4 mph

6 days / week

40 minutescircuit weight

training4 days / week

4.5 hoursplaying golf

walking (w/o cart)per week

1 hour of pacingwhile on the phone

6 days / week

Burning1,750 cals/wk

25

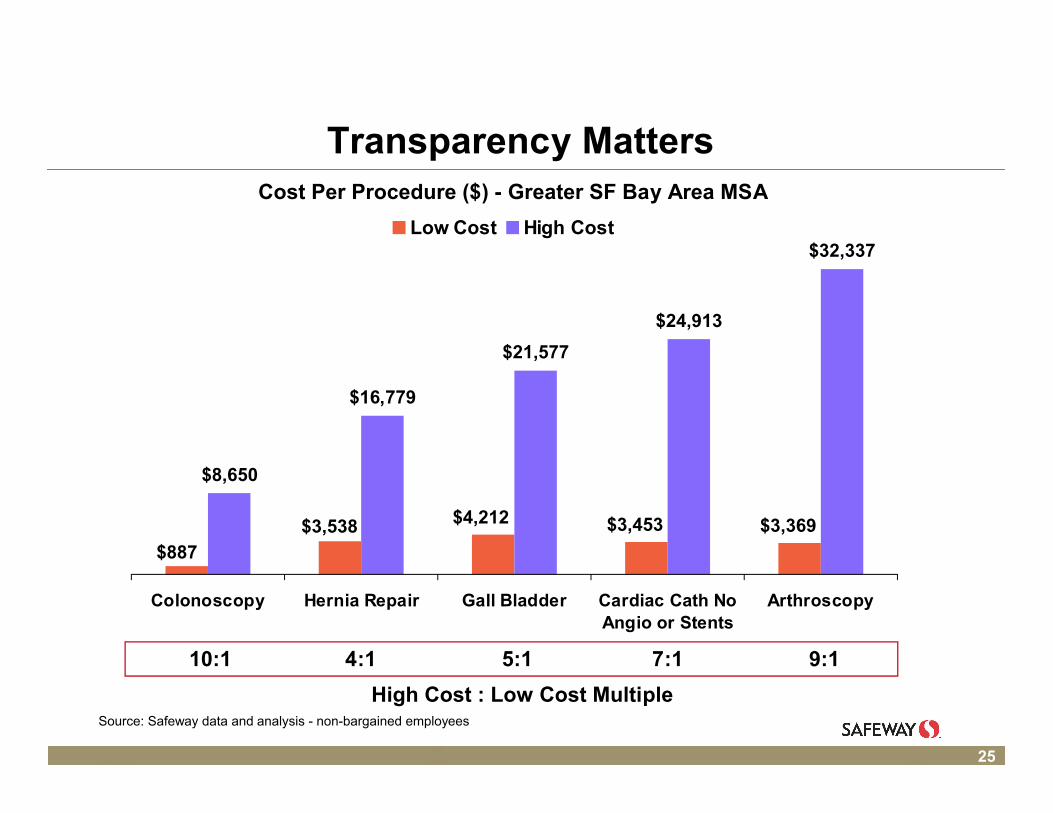

Transparency Matters

$8,650

$16,779

$21,577

$24,913

$32,337

$3,369

$887

$3,538 $4,212 $3,453

Colonoscopy Hernia Repair Gall Bladder Cardiac Cath NoAngio or Stents

Arthroscopy

Low Cost High Cost

10:1 4:1 5:1 7:1 9:1

High Cost : Low Cost MultipleSource: Safeway data and analysis - non-bargained employees

Cost Per Procedure ($) - Greater SF Bay Area MSA

26

Colonoscopy

$887

$932

$991

$999

$1,1

57$1

,169

$1,1

78$1

,245

$1,2

49$1

,306

$1,3

58$1

,377

$1,5

30$1

,535

$1,6

32$1

,642

$1,6

43$1

,728

$1,7

60$1

,860

$1,9

36$2

,015

$2,0

78$2

,090

$2,0

99$2

,309

$2,3

16$2

,409

$2,4

43$2

,603

$2,6

86$2

,751

$2,7

71$2

,816

$2,8

45$2

,848

$2,8

69$2

,987

$3,0

00$3

,013

$3,0

47$3

,144

$3,1

88$3

,245

$3,2

71$3

,314

$3,3

18$3

,367

$3,6

55$3

,676

$3,7

69$3

,793

$3,8

30$4

,032

$4,1

72$4

,388

$4,4

73$4

,518

$4,7

23$5

,596

$5,6

82$5

,734 $7

,347 $8

,650

Gol

den

Gat

e E

ndos

copy

Ctr

The

Red

woo

d S

urg

Ctr

Eas

t B

ay E

ndos

copy

Ctr

Pre

mie

r S

urge

ry C

trS

tock

ton

End

osco

py C

trE

ndos

copy

Ctr

of

Mar

inE

ast

Bay

End

osur

gery

Inc

San

Ram

on E

ndos

copy

Ctr

Mid

Pen

insu

la E

ndos

copy

Ctr

Mer

ced

Am

b E

ndos

copy

Ctr

St

Mar

ys M

ed C

tr-S

anLa

ser

Sur

gery

Ctr

Was

hing

ton

Out

patie

nt S

urg

For

t S

utte

r S

urg

Ctr

Tur

ney

Nov

ato

End

osco

py C

trS

utte

r R

osev

ille

End

osco

pyA

spen

Sur

g C

trA

dvan

ced

End

osco

py C

trS

onom

a V

alle

y H

osp

Tow

er H

ealth

& W

elln

ess

Val

leyC

are

Med

Ctr

End

osco

py C

tr o

f S

anta

Ros

aS

an R

amon

Reg

Med

Ctr

Sam

arita

n E

ndos

copy

Ede

n M

ed C

trT

resa

nti M

edic

al C

orp

Set

on M

ed C

tr-D

aly

City

UC

Dav

is M

ed C

trS

an F

ranc

isco

End

osco

pyV

alle

ycar

e M

emor

ial H

osp

Sut

ter

Tra

cy C

omm

Hos

pS

utte

r F

airf

ield

Sur

g C

trG

reat

er B

ay A

rea

End

osco

pyT

ing

UC

SF

Med

Ctr

Met

hodi

st H

osp

ofD

amer

on H

osp

Pro

cedu

re S

uite

Fre

mon

tA

ther

ton

End

osco

py C

trA

lam

eda

Hos

pF

olso

m S

ierr

a E

ndos

copy

Ctr

Fre

mon

t A

mbu

lato

ry S

urg

Ctr

Sut

ter

Med

Ctr

Sac

ram

ento

Que

en o

f th

e V

alle

y H

osp

John

Mui

r-M

t D

iabl

o H

lth S

ysLo

di M

emor

ial H

osp

Cal

iforn

ia P

acifi

c M

ed C

trS

utte

r D

elta

Med

Ctr

Gre

ater

Bay

End

osco

py C

trS

anta

Ros

a M

emor

ial H

osp

End

osur

gery

Ctr

Doc

tors

Hos

pita

l of

Man

teca

Adv

ance

d S

urg

Ctr

Mem

oria

l Hos

ps A

ssoc

iatio

nJo

hn M

uir

Beh

av H

ealth

Tra

cy S

urg

Ctr

Pet

alum

a V

alle

y H

osp

Los

Gat

os S

urg

Ctr

Sou

th B

ay S

urg

Ctr

Bay

Are

a S

urg

Grp

Hac

iend

a S

urg

Ctr

St

Hel

ena

Hos

pP

leas

anto

n S

urg

Ctr

Room & Supplies Professional GI Services All Other

Cost Per Procedure ($) – Greater SF Bay Area MSA

Colonoscopy Providers

27

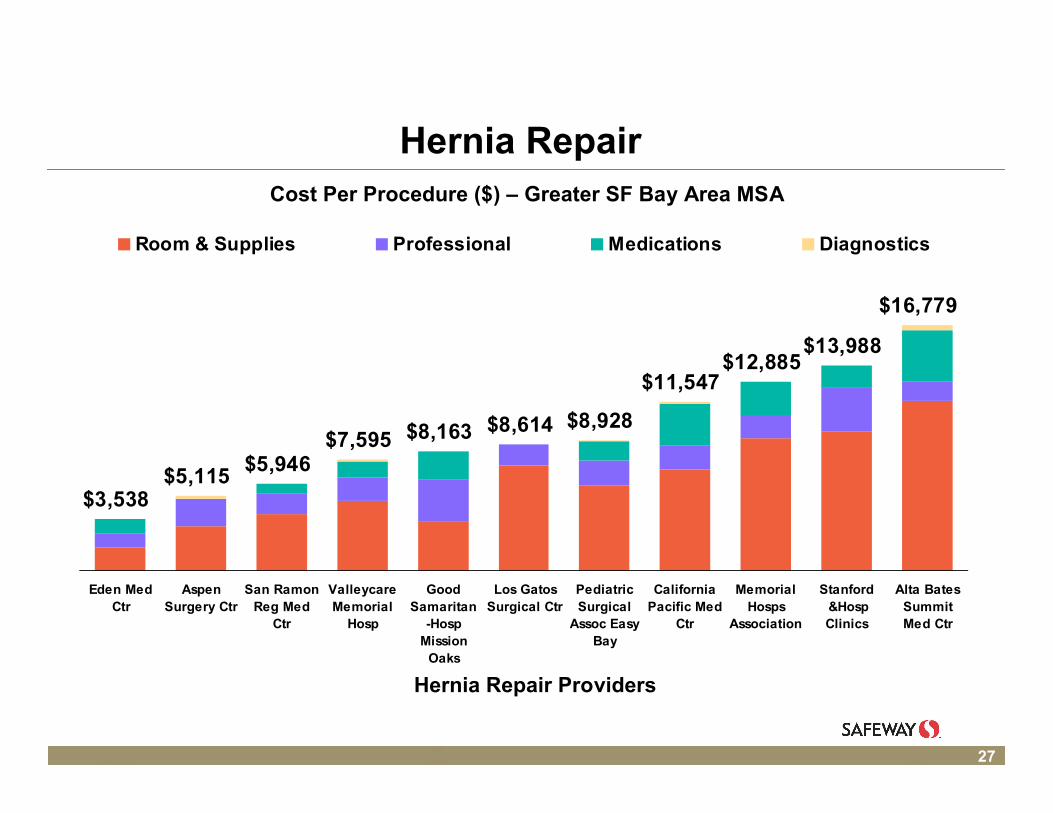

Hernia Repair

$3,538$5,115

$5,946$7,595 $8,163 $8,614 $8,928

$11,547$12,885

$13,988

$16,779

Eden MedCtr

AspenSurgery Ctr

San RamonReg Med

Ctr

ValleycareMemorial

Hosp

GoodSamaritan

-HospMission

Oaks

Los GatosSurgical Ctr

PediatricSurgical

Assoc EasyBay

CaliforniaPacific Med

Ctr

MemorialHosps

Association

Stanford &HospClinics

Alta BatesSummitMed Ctr

Room & Supplies Professional Medications Diagnostics

Cost Per Procedure ($) – Greater SF Bay Area MSA

Hernia Repair Providers

28

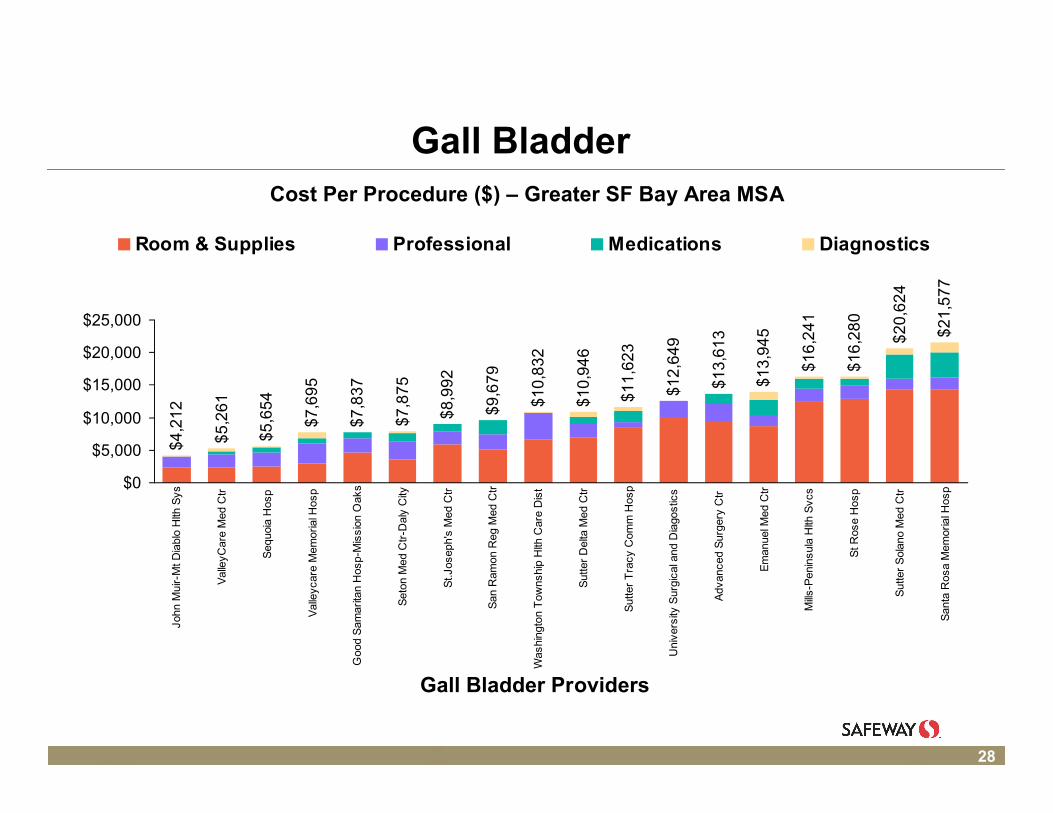

Gall Bladder$4

,21

2

$5

,26

1

$5,6

54

$7

,69

5

$7

,83

7

$7

,87

5

$8

,99

2

$9

,67

9

$1

0,8

32

$1

0,9

46

$1

1,6

23

$1

2,6

49

$1

3,6

13

$1

3,9

45

$1

6,2

41

$1

6,2

80

$2

0,6

24

$2

1,5

77

$0

$5,000

$10,000

$15,000

$20,000

$25,000

John

Mui

r-M

t Dia

blo

Hlth

Sys

Val

leyC

are

Med

Ctr

Seq

uoia

Hos

p

Val

leyc

are

Mem

oria

l Hos

p

Goo

d S

amar

itan

Hos

p-M

issi

on O

aks

Set

on M

ed C

tr-D

aly

City

St.J

osep

h's

Med

Ctr

San

Ram

on R

eg M

ed C

tr

Was

hing

ton

Tow

nshi

p H

lth C

are

Dis

t

Sut

ter

Del

ta M

ed C

tr

Sut

ter

Tra

cy C

omm

Hos

p

Uni

vers

ity S

urgi

cal a

nd D

iago

stic

s

Adv

ance

d S

urge

ry C

tr

Em

anue

l Med

Ctr

Mills

-Pen

insu

la H

lth S

vcs

St R

ose

Hos

p

Sut

ter

Sol

ano

Med

Ctr

San

ta R

osa

Mem

oria

l Hos

p

Room & Supplies Professional Medications Diagnostics

Cost Per Procedure ($) – Greater SF Bay Area MSA

Gall Bladder Providers

29

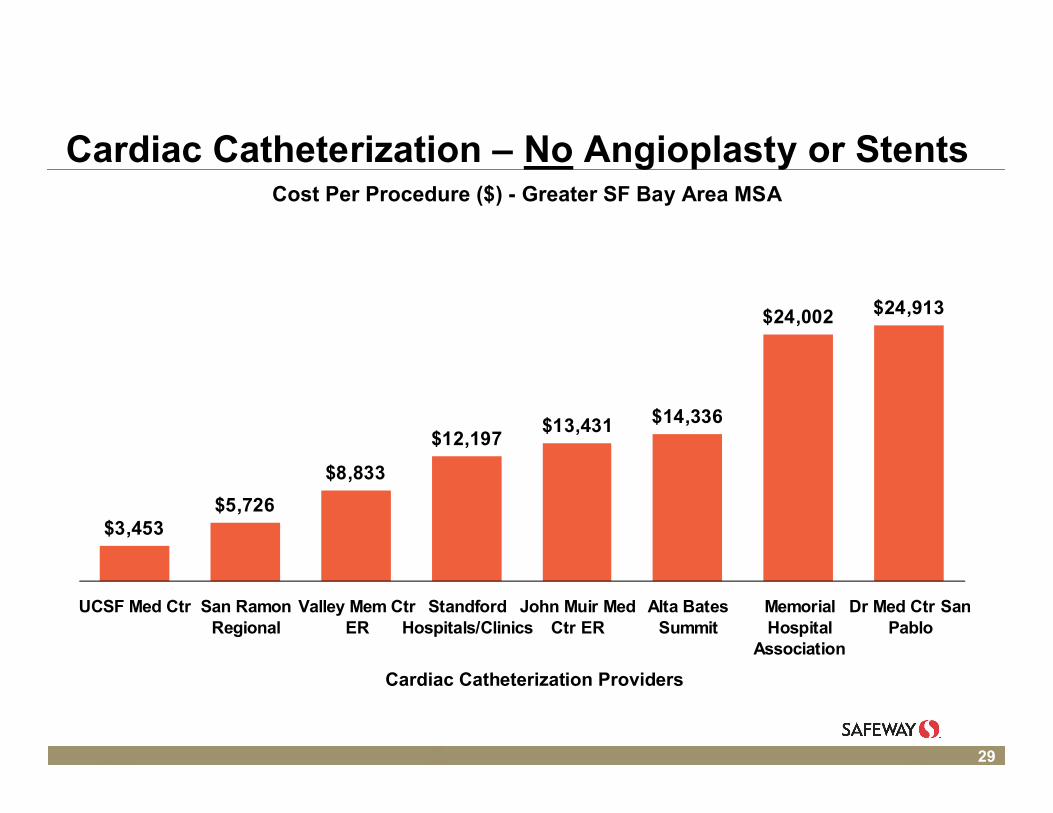

Cardiac Catheterization – No Angioplasty or Stents

$3,453$5,726

$8,833

$12,197$13,431 $14,336

$24,002 $24,913

UCSF Med Ctr San RamonRegional

Valley Mem CtrER

StandfordHospitals/Clinics

John Muir MedCtr ER

Alta BatesSummit

MemorialHospital

Association

Dr Med Ctr SanPablo

Cost Per Procedure ($) - Greater SF Bay Area MSA

Cardiac Catheterization Providers

30

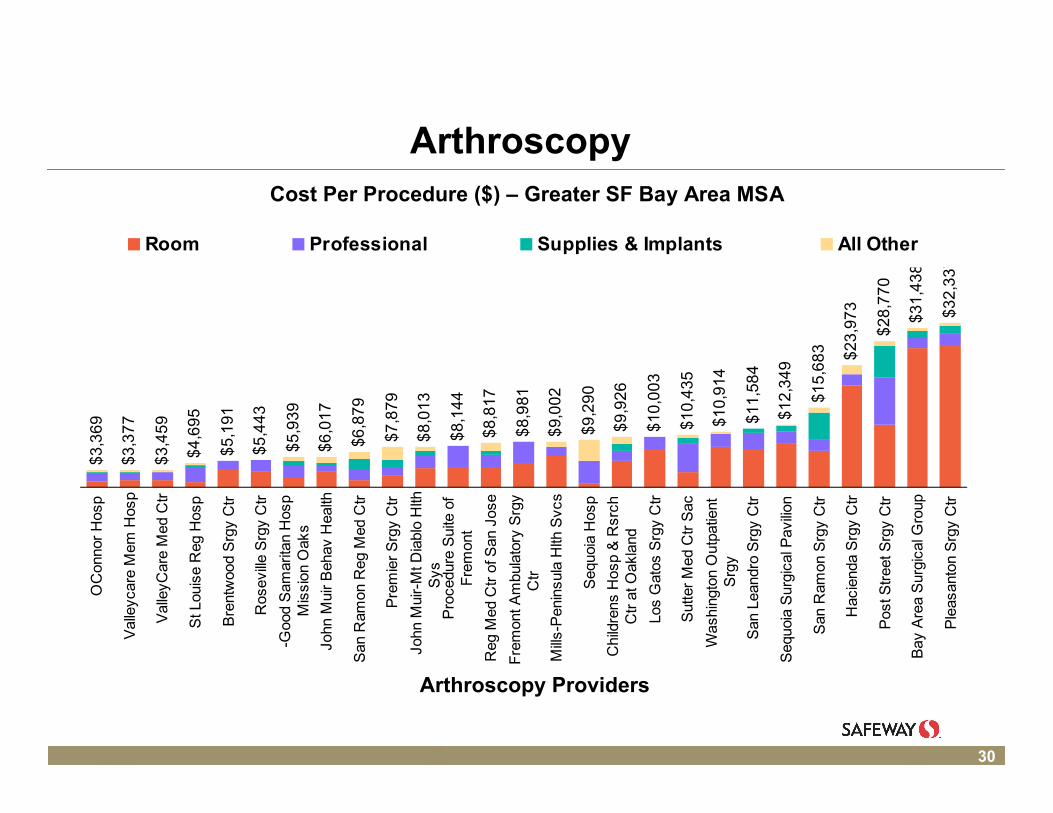

Arthroscopy

$3

,36

9

$3

,37

7

$3

,45

9

$4

,69

5

$5,

191

$5

,44

3

$5

,93

9

$6

,01

7

$6,8

79

$7

,87

9

$8

,01

3

$8

,14

4

$8

,81

7

$8,

981

$9,

002

$9

,29

0

$9

,92

6

$1

0,0

03

$1

0,4

35

$1

0,9

14

$1

1,58

4

$1

2,3

49

$1

5,6

83 $23

,97

3

$2

8,7

70

$3

1,4

38

$3

2,3

37

OC

onno

r H

osp

Val

leyc

are

Mem

Hos

p

Val

leyC

are

Med

Ctr

St L

ouis

e R

eg H

osp

Bre

ntw

ood

Srg

y C

tr

Ros

evill

e S

rgy

Ctr

-Goo

d S

amar

itan

Hos

pM

issi

on O

aks

John

Mui

r B

ehav

Hea

lth

San

Ram

on R

eg M

ed C

tr

Pre

mie

r S

rgy

Ctr

John

Mui

r-M

t Dia

blo

Hlth

Sys

Pro

cedu

re S

uite

of

Fre

mon

t

Reg

Med

Ctr

of S

an J

ose

Fre

mon

t Am

bula

tory

Srg

yC

tr

Mill

s-P

enin

sula

Hlth

Svc

s

Seq

uoia

Hos

p

Chi

ldre

ns H

osp

& R

srch

Ctr

at O

akla

nd

Los

Gat

os S

rgy

Ctr

Sut

ter

Med

Ctr

Sac

Was

hing

ton

Out

patie

ntS

rgy

San

Lea

ndro

Srg

y C

tr

Seq

uoia

Sur

gica

l Pav

ilion

San

Ram

on S

rgy

Ctr

Hac

iend

a S

rgy

Ctr

Pos

t Str

eet S

rgy

Ctr

Bay

Are

a S

urgi

cal G

roup

Ple

asan

ton

Srg

y C

tr

Room Professional Supplies & Implants All Other

Cost Per Procedure ($) – Greater SF Bay Area MSA

Arthroscopy Providers

31

Holistic Approach – Genuine Focus on Employee Health & Wellness

Free fitness center and gym membership discounts

Care management, wellness, 24-hour nurse line

Healthy foods discount in cafeteria

CareConnect program for breast and prostate cancer

Cancer fundraising since 2002 – more than $100 million to date

Engagement in policy discussion

Slide showing major elements of the Safeway health plan is omitted

32

Core Principles for Healthcare Reform

Market-based healthcare system

Universal coverage with individual responsibility

Financial assistance for low income

Healthier behavior and incentives

Equal tax treatment

33

CAHR Membership Playtex

Price Chopper

Procter & Gamble

Publix

Raley’s

RenderX

Rockwell Automation

Rockwell Collins

Roll International

Safeway

Schnuck’s

Smucker

SuperValu

Unified Western

United Healthcare

United Supermarkets

USAA

Wakefern

Wegmans

Winco Foods

Wrigley

Hershey

Humana

Illinois Tool Works

InnerLink

Jax Markets

KKR

Kaiser Permanente

Kimberly Clark

Kohl’s

Kraft Foods

Kroger

Land ‘O Lakes

Lund Food Holdings

Merck

McKesson

Medtronic

Morgan Stanley

Norfolk Southern

PG&E

PepsiCo

Pfizer

Aetna

Alex Lee Inc.

Bashas

Blue Shield of CA

Brookshire

Bumblebee Seafoods

C&S Wholesale

CIGNA

Clorox

Coca Cola

CVS / Caremark

Del Monte Foods

Edison International

Eli Lilly

GAP Stores

General Mills

Giant Eagle

GlaxoSmithKline

HCA

Health Net

Heinz

34

Agenda

U. S. healthcare challenge

Safeway experience

Policy implications

Safeway Health

35

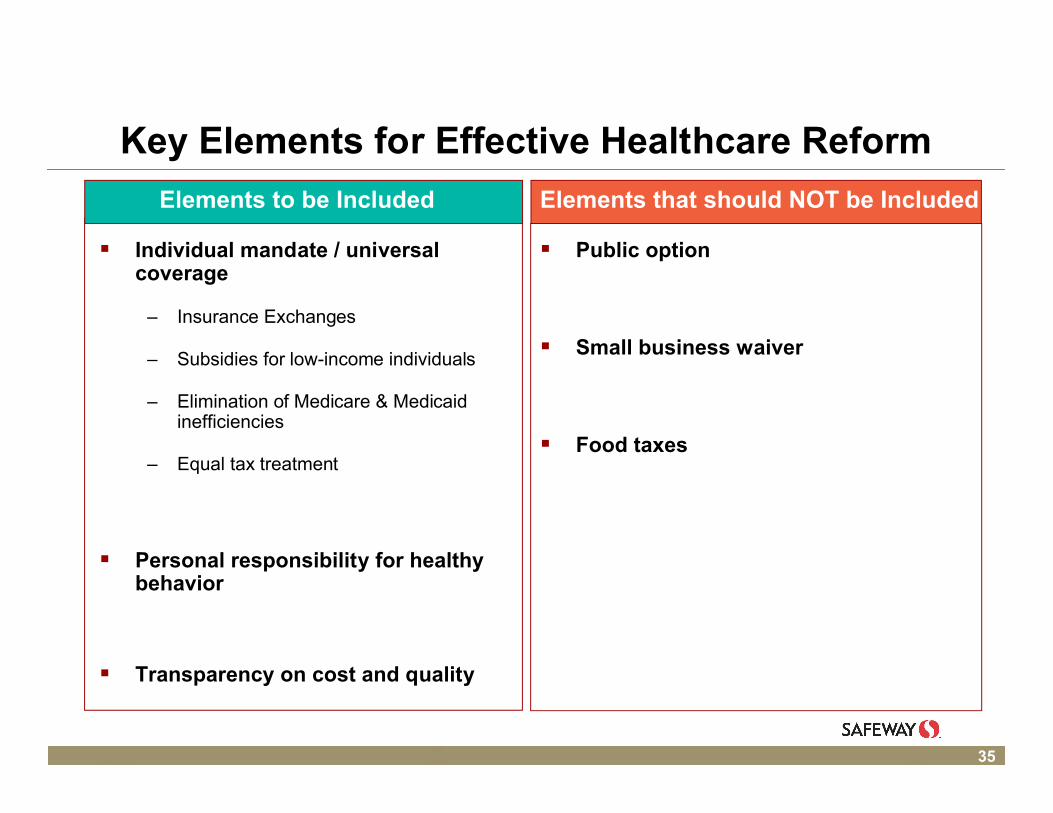

Key Elements for Effective Healthcare Reform

Elements to be Included

Individual mandate / universal coverage

– Insurance Exchanges

– Subsidies for low-income individuals

– Elimination of Medicare & Medicaid inefficiencies

– Equal tax treatment

Personal responsibility for healthy behavior

Transparency on cost and quality

Elements that should NOT be Included

Public option

Small business waiver

Food taxes

36

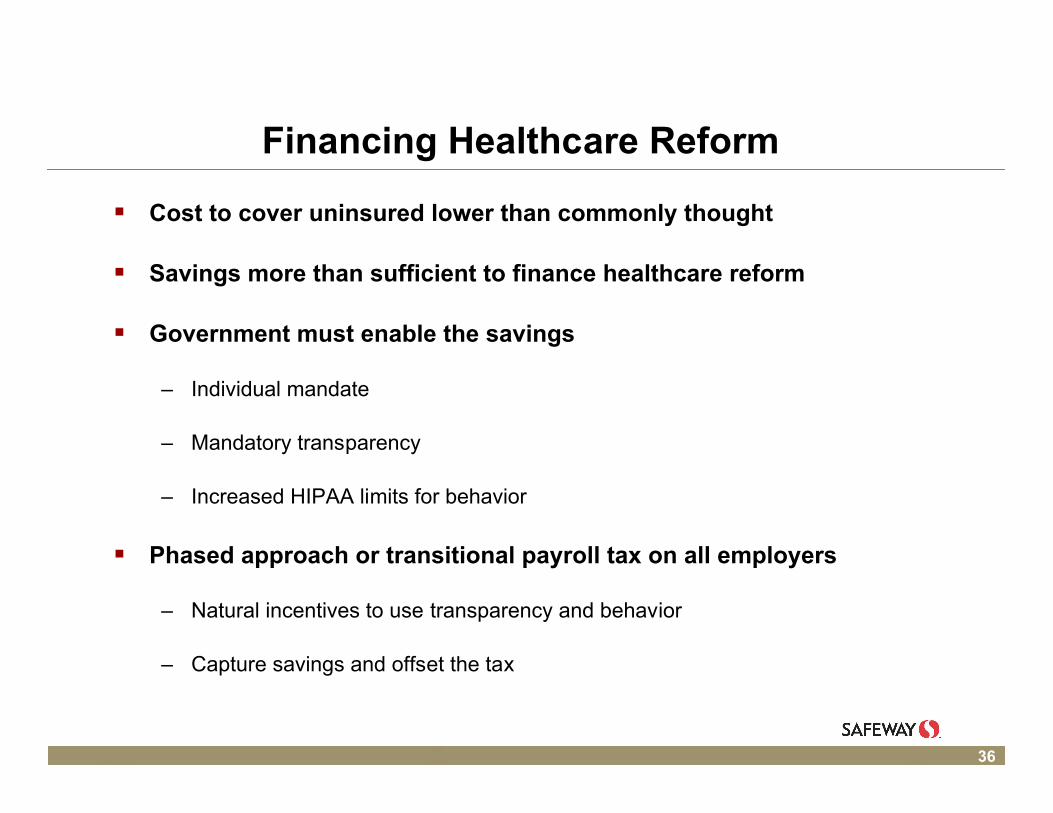

Financing Healthcare Reform

Cost to cover uninsured lower than commonly thought

Savings more than sufficient to finance healthcare reform

Government must enable the savings

– Individual mandate

– Mandatory transparency

– Increased HIPAA limits for behavior

Phased approach or transitional payroll tax on all employers

– Natural incentives to use transparency and behavior

– Capture savings and offset the tax

37

Individual mandate; no subsidy

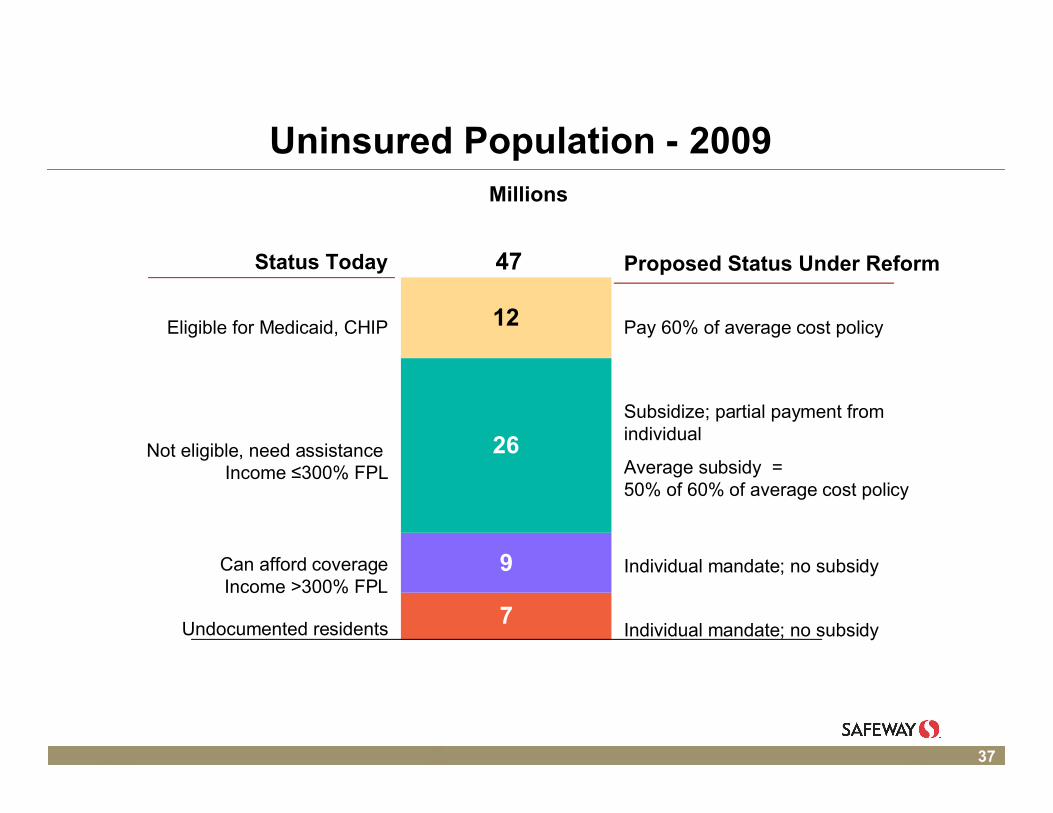

Uninsured Population - 2009

7

9

26

12

Millions

47Status Today

Eligible for Medicaid, CHIP

Not eligible, need assistance Income ≤300% FPL

Can afford coverageIncome >300% FPL

Undocumented residents

Proposed Status Under Reform

Pay 60% of average cost policy

Subsidize; partial payment fromindividual

Average subsidy = 50% of 60% of average cost policy

Individual mandate; no subsidy

38

Cost to Cover Uninsured

$3,694

$4,194

$2,077

$46.5

$41.6

Current Cost ofUninsuredEligible forMedicaid

60% of Avg Plan Not EligibleToday; 300%FPL; Subsidize

@ 50%

≤

$88.1

Total Cost to Cover ($ Billion)Per Person Cost

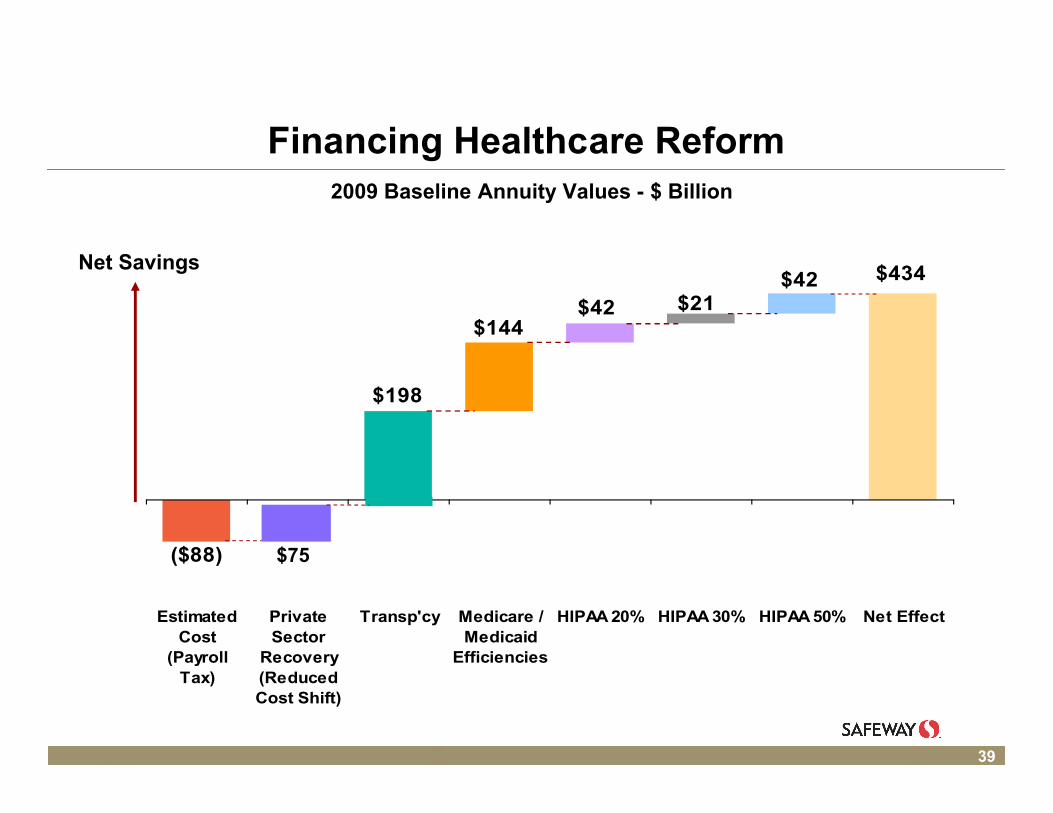

39

Financing Healthcare Reform2009 Baseline Annuity Values - $ Billion

$198

$144$42 $21

$42 $434

($88)

EstimatedCost

(PayrollTax)

PrivateSector

Recovery(ReducedCost Shift)

Transp'cy Medicare /Medicaid

Efficiencies

HIPAA 20% HIPAA 30% HIPAA 50% Net Effect

Net Savings

$75

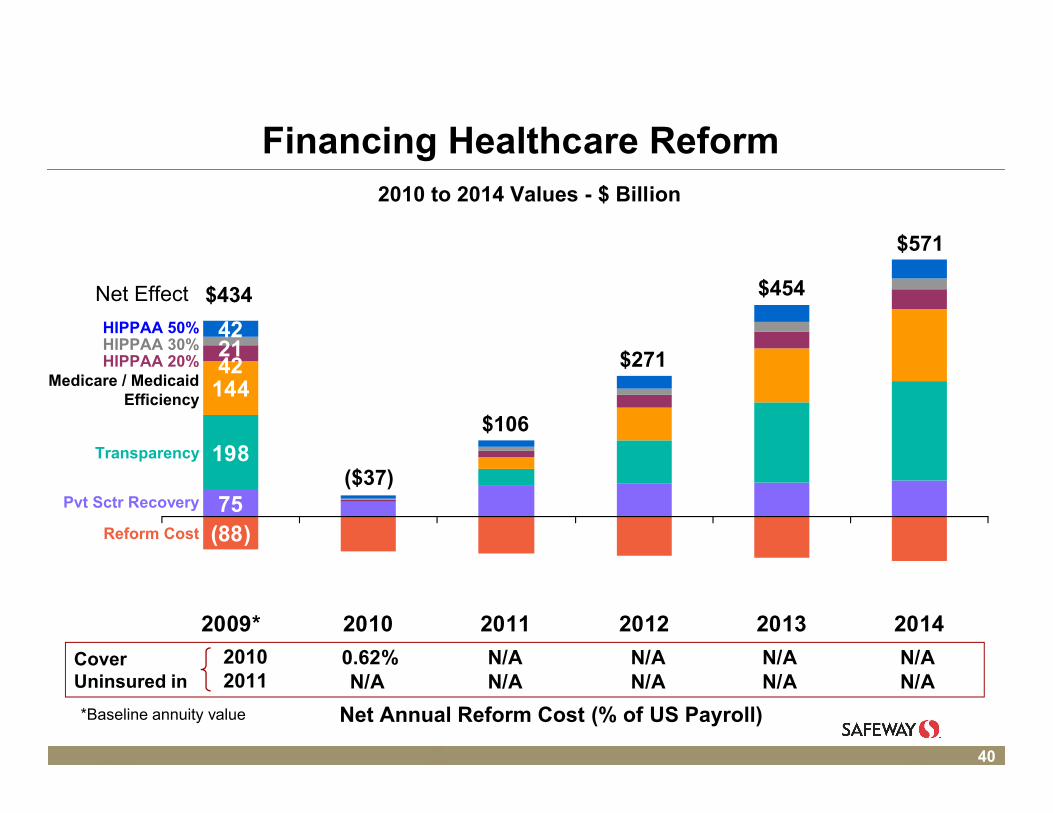

40

Financing Healthcare Reform

(88)75

198

144422142

2009* 2010 2011 2012 2013 2014

Reform Cost

Pvt Sctr Recovery

Transparency

Medicare / MedicaidEfficiency

HIPPAA 20%HIPPAA 30%HIPPAA 50%

2010 to 2014 Values - $ Billion

Net Annual Reform Cost (% of US Payroll)

$434

($37)

$106

$271

$454

$571

Net Effect

*Baseline annuity value

0.62% N/A N/A N/A N/AN/A N/A N/A N/A N/A

20102011

Cover Uninsured in

41

Why This Approach is Good Policy

Establishes an appropriate benefit for today’s uninsured, and achieves universal coverage

Finances reform completely and generates a surplus

Provides powerful financial incentives to the private sector to implement key reform elements in their own organizations . . .

– Behavior incentives

– Transparency

– Evidence-based medicine

. . . and more than offset the effect of a payroll tax quickly

Normalizes Medicare service levels and adjudication nation-wide

42

Agenda

U. S. healthcare challenge

Safeway experience

Policy implications

Safeway Health

43

Safeway Health Concept

Partner with client organizations

Replicate the Safeway experience

Strengthen the client’s healthcare paradigm

Reduce healthcare costs

– Plan design medical

– Plan design Rx – proprietary tools

– Transparency

Share savings achieved

44

Re-Designed Healthcare What’s it Worth For Individual Companies?

Lower, sustained per capita healthcare costs

Healthier employees

Improved productivity

Safeway Health a vehicle for achieving results

45

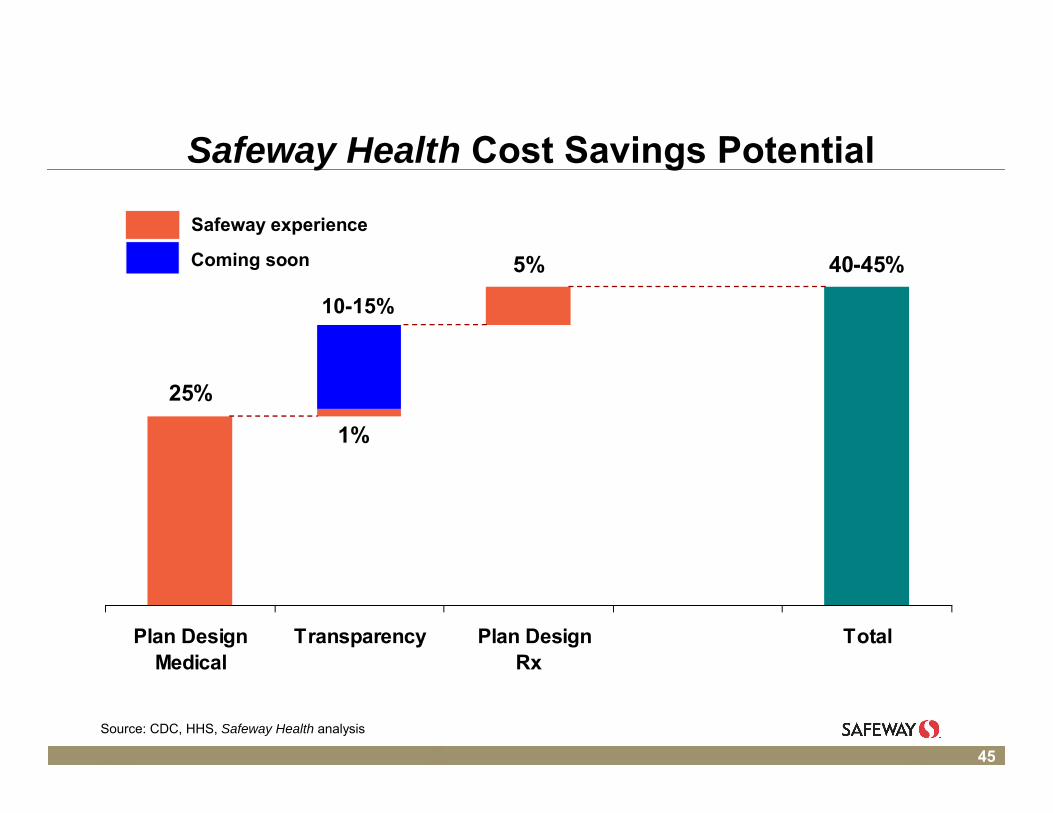

Safeway Health Cost Savings Potential

25%

1%

5% 40-45%

Plan DesignMedical

Transparency Plan Design Rx

Total

Source: CDC, HHS, Safeway Health analysis

Safeway experience

Coming soon

10-15%

46

Re-Designed Healthcare What’s it Worth For the Nation ?

Savings more than sufficient to fund today’s uninsured

Healthier citizens

Market forces in healthcare; lower costs and trends

Improved U.S. competitiveness in global markets

47

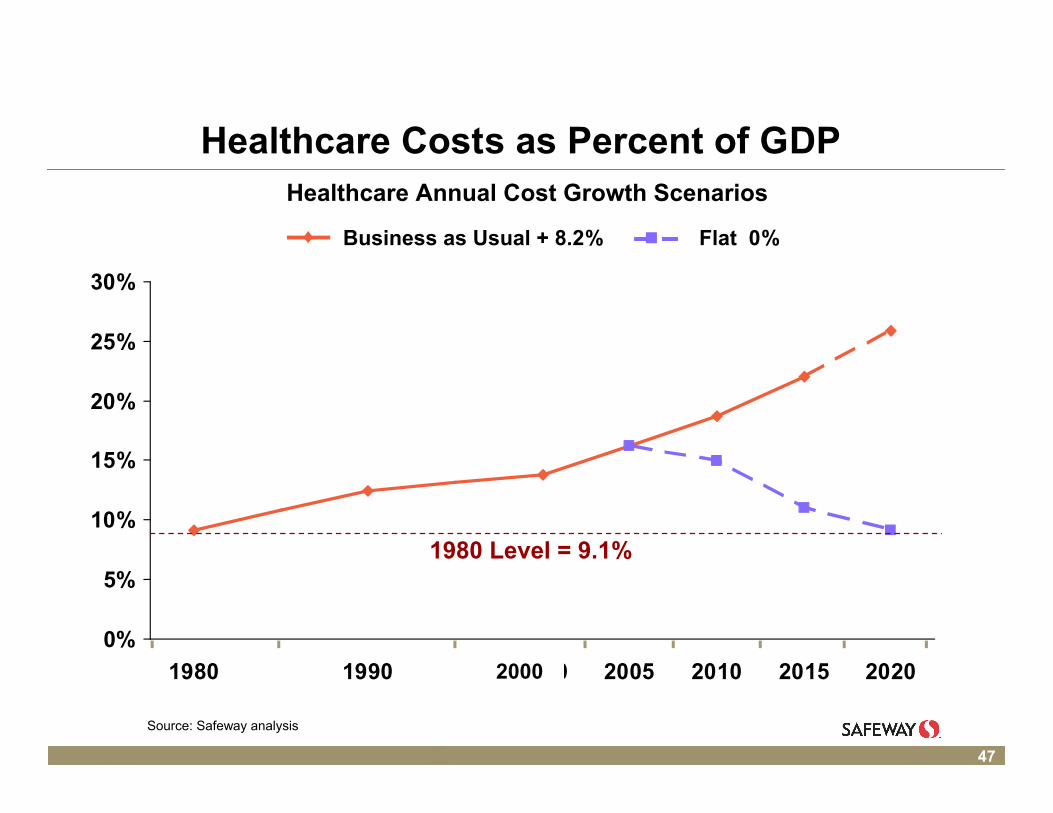

Healthcare Costs as Percent of GDP

0%

5%

10%

15%

20%

25%

30%

1980 1990 2000 2005 2010 2015 2020

Source: Safeway analysis

1980 Level = 9.1%

Business as Usual + 8.2% Flat 0%

Healthcare Annual Cost Growth Scenarios

2000

48

Safeway Health Contact Information

Ken Shachmut – Executive Vice President

Office (925) 467-3426

Brad Wolfsen – Vice President

Office (925)-467-2164

Dave Vielehr – Business Development Manager

Office (925) 778-1211

Safeway Health LLC

5918 Stoneridge Mall Road

Pleasanton, CA 94588-3229

Fax (925) 467-3632