Embed Size (px)

Citation preview

Habib Bank AG Zurich

Annual Report 2014

1

Habib Bank AG Zurich

Table of contents

Group key figures 2Letter from the Chairman and the President 4Habib Bank AG Zurich - the Group 5Group organisation structure 6Directors' report 8Group risk principles 12

Group Financial statements Balance sheet 16 Income statement 18 Cashflow statement 20 Statement of changes in equity 22 Summary of significant accounting principles 24 Notes to annual consolidated financial statements 28 Report of the Statutory Auditor 52

Bank Financial statements Balance sheet 54 Income statement 56 Statement of changes in equity 58 Notes to annual financial statements 59 Appropriation of profit / coverage of losses / other distributions 71 Report of the Statutory Auditor 72

Addresses 73

2

Habib Bank AG Zurich

GROUP

Group key figures*

in CHF million 31.12.10 31.12.11 31.12.12 31.12.13 31.12.14

Balance sheet

Total assets 8'032 8'354 7'850 7'772 9'804

Shareholder's equity1 827 880 877 873 987

Advances 2'892 2'645 2'351 2'871 3'408

Deposits 6'197 6'439 6'289 6'398 8'018

Income statement

Total income2 258.6 305.9 286.4 253.9 418.9

Operating expenses 141.6 151.6 159.9 175.1 178.3

Operating result 54.3 107.2 69.9 55.1 207.8

Group profit / loss 29.1 61.7 40.4 28.6 77.6

0

2000

4000

6000

8000

10000

20142013201220112010

8'032 8'3547'850 7'772

9'804

Total assets, in CHF million

0

200

400

600

800

1000

20142013201220112010

827880 877 873

987

Shareholder's equity1, in CHF million

0

500

1000

1500

2000

2500

3000

3500

20142013201220112010

2'8922'645

2'351

2'871

3'408

Advances, in CHF million

0

2000

4000

6000

8000

10000

20142013201220112010

6'197 6'439 6'289 6'398

8'018

Deposits, in CHF million

0

100

200

300

400

500

20142013201220112010

258.6305.9 286.4

253.9

418.9

Total income2, in CHF million

0

50

100

150

200

20142013201220112010

141.6151.6 159.9

175.1 178.3

Operating expenses, in CHF million

0

50

100

150

200

250

20142013201220112010

54.3

107.2

69.955.1

207.8

Operating result, in CHF million

0

10

20

30

40

50

60

70

80

20142013201220112010

29.1

61.7

40.4

28.6

77.6

Group profit / loss, in CHF million

* Effective 1 January 2013, the Group adopted the new accounting principles in accordance of FINMA Circular 2015/1 "Accounting - Banks"

1 Excl. minority interest in equity and in Group profit / loss

2 Including "Gross result from interest operations", "Result from comission business and services", "Result from trading activities and the fair value option" and "Other result from ordinary activities"

3

Habib Bank AG Zurich

GROUP

31.12.10 31.12.11 31.12.12 31.12.13 31.12.14

Key figures and ratios

Number of offices 177 197 219 253 278

Number of employees 3'289 3'308 3'823 4'140 4'456

Return on equity (ROE) (%)1 3.1% 6.4% 4.0% 2.8% 7.0%

Equity ratio (%) 11.7% 12.0% 12.7% 13.1% 12.3%

Cost / income ratio (%) 54.8% 49.6% 55.8% 69.0% 42.6%

Total capital ratio (%)2 16.1% 19.4% 21.8% 21.0% 19.5%

0

50

100

150

200

250

300

20142013201220112010

177197

219253

278

Number of offices

0

1000

2000

3000

4000

5000

20142013201220112010

3'289 3'3083'823

4'1404'456

Number of employees

0

1

2

3

4

5

6

7

8

20142013201220112010

3.1%

6.4%

4.0%

2.8%

7.0%

Return on equity (ROE) (%)1

0

3

6

9

12

15

20142013201220112010

11.7% 12.0% 12.7% 13.1%12.3%

Equity ratio (%)

0

10

20

30

40

50

60

70

80

20142013201220112010

54.8%49.6%

55.8%

69.0%

42.6%

Cost / income ratio (%)

0

5

10

15

20

25

20142013201220112010

16.1%

19.4%21.8% 21.0%

19.5%

Total capital ratio (%)2

1 Group profit / loss as percentage of equity of average at year end 2013 and 2014

2 Since 1 January 2013, capital adequacy has been determined in accordance with the standards in the "Basel III Accord"

4

Habib Bank AG Zurich

Letter from the Chairman and the President

It is our pleasure to present you with the 47th annual report of Habib Bank AG Zurich based on the new accounting principles issued by the Swiss Financial Market Supervisory Authority.

By the grace of God, Habib Bank AG Zurich delivered good results for 2014 while maintaining a strong capital base and high liquidity. Our Group maintained its conservative lending policy, with a high degree of discipline. This policy is characterised by a high percentage of fully secured and relatively short-term lending. As a result, advances to clients decreased to 43% of deposits received from clients. The remaining liquidity was placed in the interbank market or invested in investment-grade bonds.

During 2014, Ray Barnes joined our Board of Directors as a new member. Ray Barnes comes from a rich background of banking.

The Board of Directors has proposed that out of the profit for the year ended 31 December 2014 and a carry-over profit from last year adding up to a distributable amount of CHF 41'088'790.– the following appropria-tions should be made:

- Allocation to statutory retained earnings reserves CHF 2'000'000.–- Allocation to voluntary retained earnings reserves CHF 21'000'000.–- Distribution of dividend from distributable profit CHF 18'000'000.–- Profit and loss carried forward CHF 88'790.–

We would like to thank our clients for their loyalty to Habib Bank AG Zurich and for the trust they placed in us in 2014. We also wish to thank all our employees for their ongoing commitment and contribution to the success of Habib Bank AG Zurich.

Dr. Andreas Länzlinger Muhammad H. HabibChairman of the Board of Directors President

5

Habib Bank AG Zurich

Habib Bank AG Zurich - the Group

Habib Bank AG Zurich (hereinafter "the Bank") was incorporated in Switzerland in 1967 and is privately owned.

The Habib family has been actively involved in banking for over 170 years. Two family members, Mr. Muhammad H. Habib, President, and Mr. Mohamedali R. Habib, Joint President, are members of the General Management. Other members of the family are currently working their way up through the management grades.

The traditional values of the Habib family are: trust, integrity, respect, service and commitment.

The Bank has its Head Office and operation in Zurich and branches in the United Kingdom, the United Arab Emirates and Kenya. The Bank holds four wholly owned subsidiaries: Habib Canadian Bank, Canada, HBZ Bank Limited, South Africa, Habib European Bank Ltd., Isle of Man and HBZ Services FZ-LLC, United Arab Emirates. The Bank holds a 51% ownership interest in Habib Metropolitan Bank Ltd., Pakistan and HBZ Finance Ltd., Hong Kong (altogether "the Group").

The Bank and the Group are subject to the consolidated supervision of the Swiss Financial Market Supervisory Authority (FINMA). The Group has a strong capital base and liquidity ratios above industry standards and benefits from the political and economic stability of having its Head Office in Switzerland. Furthermore, the Group has close co-operation with the various regulatory bodies and central banks in the countries in which the Group operates.

The Group places a high emphasis on personal service in the countries it operates. The branches and subsidi-aries cover nine countries spread over four continents. At the end of 2014, 4'456 employees together with 278 offices are strategically well placed to provide maximum assistance to our local and international clien-tele. The Group is active in commercial banking, retail banking, trade finance business, wealth management and Islamic banking.

6

Habib Bank AG Zurich

GROUP

In 2014, the Group adapted its organisation structure to best support the achievement of the objectives set in the Group Strategic Plan 2013-2020. The new structure supports the focus on clients and the development of the client base and the business volumes. Moreover, it supports operational excellence in all countries and the centralised operations.

Board of Directors

The Board of Directors of the Bank is made up of non-executive and independent directors, all of whom have extensive experience in their respective field of competence.

Name Born Citizenship Board of Directors Audit CommitteeRisk & Control Committee

Dr. Andreas Länzlinger 1959 Swiss Chairman

Dr. Ulrich Grete 1942 Swiss Vice Chairman Member

Ray Barnes* 1945 British Member Member

Dr. Marco Duss 1943 Swiss Member Chairman

Urs Seiler 1949 Swiss Member Member Member

Ursula Suter 1954 Swiss Member Chairwoman* from 28 April 2014

General Management

General Management consists of two members of the Habib family and two non-family members. The majority of the members of General Management have residency in Switzerland.

Name Born Citizenship FunctionMuhammad H. Habib 1959 Swiss President and Head of Markets Overseas

Mohamedali R. Habib 1964 Canadian Joint President and Head of Markets Asia & Special Services

Shaun Wallis 1955 British Member of General Management and Head of Global Operations

Walter Mathis 1961 Swiss Member of General Management and Head of Shared Services

Group organisation structure

Management of the branch network

Name Born Citizenship Function CountryChristian Lerch 1959 Swiss Country Manager Switzerland

Anjum Iqbal 1952 British Country Manager United Kingdom

Arif Lakhani 1945 Pakistani Country Manager United Arab Emirates

Mohammad Ali Hussain 1954 Kenyan Country Manager Kenya

7

Habib Bank AG Zurich

GROUP

Management of the subsidiaries

Name Born Citizenship Function Country

Muslim Hassan 1955 Canadian Chief Executive Officer Canada

Zafar Khan 1952 South African Chief Executive Officer South Africa

Mohammed Jafri 1951 British Chief Executive Officer Isle of Man

Atif Mufti 1973 Pakistani Chief Executive Officer United Arab Emirates*

Sirajuddin Aziz 1956 Pakistani Chief Executive Officer Pakistan

Ikram Quraishi 1948 USA Chief Executive Officer Hong Kong

* HBZ Services FZ-LLC

Group Internal Audit

Name Born Citizenship FunctionSyed Iftikhar Ali 1948 Pakistani Head of Group Internal Audit

Group Support Functions

Name Born Citizenship FunctionDr. Pascal Mang 1964 Swiss Head of Group Legal & Compliance

Ralph Schneider 1964 Swiss Head of Group Credit

Alfred Merz 1962 Swiss Head of Group Financial Control

Felix Gasser 1959 Swiss Head of Group Risk Control

Atif Mufti 1973 Pakistani Head of Group Operations

Syam Pillai Haja Alavudeen

19621966

Indian Indian

Heads of Group Information Technology

Sibel Sanus 1954 Turkish Head of Group Financial Institutions

Dr. Sitwat Husain 1964 Pakistani Head of Group Human Resources

Adnan Fasih 1967 Pakistani Head of Group Islamic Banking

8

Habib Bank AG Zurich

GROUP

Directors' report

Economic environment

Economic uncertainty remained throughout 2014.The expectations of a robust economic rebound did not materialise and global growth picked up only modestly compared to the previous year. A number of headwinds limited activity as both developed and emerging market economies continued to grapple with the aftermath of the Global Financial Crisis. Two developments in particular characterised the global economic context in 2014: First, the rebound of the US dollar in anticipation of higher US interest rates; second, the sharp decline of the oil price from mid-year onwards as global demand trailed supplies.

Among the large developed economies, the US economy continued to be the growth leader. 2014 marked the fifth year of economic expansion for the US despite harsh weather conditions earlier in the year, which saw growth contracting in the first quar-ter. Strong final demand, a pick-up in capital spend-ing and the ongoing recovery of housing activity sustained broad-based economic and employment growth. The drag from tighter fiscal policy eased, while the US Federal Reserve kept its policy rate unchanged, close to zero. Canadian growth held up well as a result of strong consumer spending despite gathering headwinds from the lower oil price. The UK economy surprised positively. However, the much expected first rate hike by the Bank of England was postponed as inflationary pressures subsided and the outlook for the eurozone, UK's most impor-tant trading partner, remained bleak. The eurozone disappointed once again. Unsolved structural issues, such as rigid labour markets but also unsustainable high levels of public debt in many countries, all but choked off the incipient recovery. Inflation also rolled over creating the risk for the eurozone to fall back into deflation. In this context, the European Central Bank increased its monetary stimulus by cutting interest rates, introducing negative deposit rates and launching a new programme for purchas-ing assets. The European Central Bank's stress test and asset quality review showed that many eurozone banks had made significant progress in de-risking

their balance sheets and shoring-up their capital. Despite weakness among its main European trading partners, Switzerland performed well in 2014 with growth lifted by private consumption and exports to other markets.

Despite weakness in the property and external sec-tors, the Chinese economy maintained a real growth rate of some 7%. Official interventions were largely limited to smoothing out volatility in the interbank market and industry-specific weaknesses. Growth in Hong Kong slowed on weaker goods and service exports. Other emerging markets struggled even more. Brazil suffered from delayed structural reforms and a drop of business confidence and Russia came under pressure when Western governments adopted sanctions to counter the country's annexation of Crimea. The country was also hit by the steep fall in oil price, which also affected the Middle East. The United Arab Emirates, however, continued to benefit from its regional safe-haven status and its property markets sustained its remarkable recovery for another year. South African growth was ham-pered by mining strikes and numerous bottlenecks. Weak commodity prices represented another major headwind. Kenya's economy experienced decent growth as the Central Bank of Kenya held the policy rate stable. Pakistan weathered another chal-lenging year fairly successfully. Although the pro-longed political stand-off during the late summer did affect activity negatively, the economy still managed to grow at a decent pace. Inflation con-tinued to decline, which allowed the State Bank of Pakistan to cut the discount rate late in the year. The International Monetary Fund approved further disbursements under its current programme, which helped to strengthen the external funding position.

Banking sector

The business environment for the banking industry continued to be dominated by extremely low inter-est rates in the developed world. Short-term rates remained anchored by highly accommodative global

9

Habib Bank AG Zurich

GROUP

monetary policy and remained close to their histori-cal lows. Against expectations, US capital market rates tended lower despite the end of asset pur-chases by the US Federal Reserve. In the eurozone, the introduction of negative deposit rates by the European Central Bank in June depressed rates even further. To counter sustained upward pressure on the Swiss franc, the Swiss National Bank followed suit in December and announced the introduction of negative interest rates and to end the EUR/CHF floor of 1.20 in January 2015. Among emerging markets, central banks with an easing bias prevailed with the notable exception of South Africa.

The development of credit demand, on the other hand, varied greatly across economies and regions. While in the US credit growth expanded at a healthy pace, the eurozone experienced another year of credit contraction as the economy as a whole con-tinued to deleverage, albeit at a slower pace. With European banks shrinking their balance sheets further, more financing activity moved to the capi-tal markets and non-traditional lenders in Europe. Credit and loan growth in emerging markets stayed well ahead of the developed world but progressed at different rates depending on the region.

The private banking and wealth management busi-ness represented a strong franchise for many banks. With asset prices rising on average, global wealth accumulation continued unabated. The fastest growth came once again from emerging markets, in particular Asia.

The global banking sector remained the focus of official regulators. Meeting regulatory requirements, be it in terms of capital, compliance or investor pro-tection once again tied up significant financial and human resources and exerted downward pressure on operating margins. Moreover, record fines hit several global banking institutions for alleged past wrong doings in various business activities.

Operational performance and outlook

General comments

2014 was a good year for the Group. The operating result reached CHF 207.8 million, which represents an increase of CHF 152.7 million over 2013.

The after-tax return on equity was at 7.0% in 2014 compared to 2.8% in 2013.

The Group decided to apply the new regulatory requirements (FINMA Circular 2015/1 "Accounting - Banks"), coming into force beginning 2015, to the 2014 financial statements. This has required a restatement of the 2013 figures.

Income statement

The Group recorded a profit of CHF 77.6 million in 2014, which represents an increase of CHF 49 mil-lion against 2013.

"Gross result from interest operations" amounted to CHF 224.1 million, which represents an increase of CHF 39.4 million against the previous year. This development was mainly due to an increase of the balance sheet items "Amounts due in respect of cus-tomer deposits", "Amounts due from customers" and "Other financial instruments at fair value".

The "Subtotal result from commissions business and services" amounted to CHF 75.6 million, which rep-resents an increase of CHF 7.6 Million against 2013.

"Result from trading activities and the fair value option" amounted CHF 104.5 million against a nega-tive figure of CHF 2.1 million for the previous year. That difference mainly comes from two facts. First, the application of new options available within the FINMA Circular 2015/1 "Accounting - Banks", gen-erated a revaluation of the financial instruments with fair value option of CHF 54.1 million. Second, the adopted consolidation policy resulted in an income

10

Habib Bank AG Zurich

GROUP

amounting to CHF 29.4 million deriving from the translation of financial statements of branches.

"Subtotal operating expenses" increased by CHF 3.2 million to CHF 178.3 million compared to 2013.

"Personnel expenses" decreased by CHF 0.5 million compared to 2013 to CHF 121.3 million. The main rea- son for the slight decrease was the re-positioning and subsequent cost savings of the Group's UK operations.

The average number of employees during 2014 of the Group was 4'298 compared to 3'982 during 2013.

"General and administrative expenses" amounted to CHF 57.0 million, which represents an increase of CHF 3.7 million against 2013, mainly due to higher office space expenses and other operating expenses driven by the Group's branch expansion strategy.

"Changes in reserves for general banking risks" amounted to CHF 76.6 million against CHF 5.4 million for the previous year. The Group follows a prudent reserve policy in order to face uncertainty due to the strong Swiss Franc and activities in emerg-ing countries.

The increase of "Taxes", from CHF 19.1 million in 2013 up to CHF 56.2 million in 2014, was driven by the substantial improvement of the Group's profit.

Due to a strict cost control and increased income, the Group's cost / income ratio improved from 69% to 42.6%.

Balance sheet

The balance sheet reached CHF 9'803.5 million, i.e. an increase of CHF 2'031.6 million compared to 2013. This is mainly due to the increased focus on deposit mobilisation.

"Liquid assets" amounted to CHF 941.0 million against CHF 853.3 million for 2013, which repre-sents an increase of CHF 87.7 million.

"Advances" (i.e. "Amounts due from customers" and "Mortgage loans") reached CHF 3'408.2 million against CHF 2'871.3 million in 2013, i.e. an increase of CHF 536.9 million.

"Other financial instruments at fair value" and "Financial investments" amounted to CHF 3'081.8 million. The increase against 2013 is CHF 1'119.3 million. The Group invested a large part of deposited funds in local government papers. The general inter-est rate decrease provided substantial revaluation profits on these instruments.

"Amounts due in respect of customer deposits" reached CHF 8'017.8 million against CHF 6'397.6 million for the previous year. All countries contrib-uted to the increase of CHF 1'620.2 million.

Capital and liquidity

The Group has a strong capital base as well as a high liquidity ratio.

The capital adequacy ratios stand at Bank level at 24.4%, and at Group level at 19.5%, and the level of liquidity coverage ratio amounts at Bank level to 272% and at Group level to 303%.

Both significantly exceed the regulatory requirements.

Operations

In late 2013, we completed a new seven-year Group Strategic Plan 2013-2020, which was approved by the Board of Directors in early 2014. The Plan calls for three phases, the first of which covers 2014 / 2015 and involves a substantial programme of IT, operational and business projects. These projects aim at improv-ing operational efficiency, at fostering consistent systems, processes, products and services, at improv-ing regulatory compliance and at refining corporate governance and risk. All this has the intent of increa- sing consistency across the Group and providing a stable, efficient and focused platform for growth for the remainder of the Group Strategic Plan.

11

Habib Bank AG Zurich

GROUP

Significant improvements were realised concerning the Group's proprietary banking system, Master hPLUS, both from a functional and technical and organisational point of view. From a functional point of view, we worked on two plans, the first focus-ing on client service and the second concentrating on operational and regulatory issues. Concerning our clients, we have implemented a better suite of products and services (such as e-banking, SMS mobile banking, cards products and various lending products), and concerning operational and regulatory issues we have greatly improved our processes and efficiency, as well as enhancing risk controls and reporting capabilities to local regulators.

From a technical and organisational point of view, in 2014 Master hPLUS has been rolled out as a single core product in eight out of nine countries.

Finally, during 2014 we have reviewed and substan-tially improved our Group governance documents (policies, directives and guidelines), which led to a strengthening of our Group Corporate Governance and to a more focused operation.

Outlook

Thanks to our unique place in the market and inter-national presence, the previously achieved organisa-tional and technical objectives, and a sound financial basis, we are well positioned to achieve the planned increase of our business. We plan to increase our deposit base in all countries with further expansion of our branch network of our subsidiaries in Canada, South Africa and Pakistan.

Alongside continued business growth, the prepara-tion to transform our UK operations into a sub-sidiary has been completed and we are awaiting the final regulators' approval in 2015. In March 2015, our Hong Kong deposit taking company received the regulator's authorisation to act as a Restricted License Bank, which will enable us to expand our product suite and brand image in the region and to increase our business with China. The Swiss opera-

tion will continue strengthening its offer to small and medium enterprises. The impact of negative interest rates will have a limited impact on the Group's over-all result. Finally, in 2015 we will continue to roll out the newly established "SIRAT" product suite in our Islamic branches.

12

Habib Bank AG Zurich

GROUP

Group risk principles

Risk & Control Framework

The Risk & Control Framework of the Group is the cornerstone for risk management and control. The Risk & Control Framework provides the basis to effectively identify, assess and manage risks within the Group. Furthermore, it defines which body has the overall responsibility for a particular risk class, who manages it and who performs independent risk control.

Risk organisation

At the level of the Board of Directors, the responsi-bilities are the following:• the Board of Directors is responsible for the strategic direction, supervision and control of the Group, and for defining our overall risk tolerance by means of a risk appetite statement and overall risk limits;• the Risk & Control Committee is responsible for assisting the Board of Directors in fulfilling its oversight responsibilities by providing guidance regarding risk governance and the development of the risk profile, including the regular review of major risk exposures and overall risk limits; and• the Audit Committee is responsible for assisting the Board of Directors in fulfilling its oversight responsibilities by monitoring General Manage- ment's approach with respect to financial reporting, internal controls and accounting. Additionally, the Audit Committee is responsible for monitoring the independence and the performance of the Group Internal Audit and external auditors.

At the operational level, the Group operates with a three-line of defence model whereby business functions, risk management oversight and assurance roles are performed by functions independent of one another.

Furthermore, a clear distinction is made between "risk owners", "risk managers" and "risk controllers":• Risk owners bear the overall supervision and responsibility for the management of specific risk classes or risk types;

• Risk managers focus on the monitoring and proactive management of risk. They initiate risk management measures and can change the risk profile; • Risk controllers independently monitor and assess risk as well as highlight deviations from target risk parameters and non-compliance with policies.

Risk management principles

The following general principles support the Group's effort to maintain an appropriate balance between risk and return:• We protect the financial strength of the Group by controlling our risk exposures and avoiding potential risk concentrations at individual exposure levels, at specific portfolio levels and at an aggregate Group- wide level across all risk types;• We protect our reputation through a sound risk culture characterised by a holistic and integrated view of risk, performance and reward, and through full compliance with our standards and principles;• We systematically identify, classify and measure risks applying best practice;• We ensure management accountability, whereby Business Line Management owns all risks assumed throughout the Group and is responsible for the continuous and active management of all risk expo- sures to ensure that risk and return are balanced;• We set up independent risk control functions or units, which monitor effectiveness of risk manage- ment and oversee risk-taking activities;• We disclose risks to the Board of Directors, regu- lators and other stakeholders in a comprehensive and transparent manner.

Internal controls

Internal controls are a set of instruments used to monitor and control operational and other business risks. This process involves evaluating reports from the internal and external auditors on an ongoing basis, assessing risks and adjusting business proc-esses and the internal control system. The organisa-tional units responsible for internal controls therefore work closely with other organisational units within

13

Habib Bank AG Zurich

GROUP

the Group. We see risk management as an on-going, multi-level and integral process within the Group.

Credit risk

Credit risk arises from the possibility that a counter-party, i.e. private clients, corporate clients, financial institution and issuer or sovereign does not fulfil its contractual obligations or the credit quality deterio-rates. In order to manage potential default risk and other prevailing credit risks most effectively, it is divided into the following risk types: client credit risk, credit issuer risk, credit counterparty risk, coun-try risk (including cross-border / transfer risk), settle-ment risk and credit concentration risk.

The Group manages its credit risk within a conserva-tive framework by evaluating the creditworthiness of the borrowing counterparties, setting appropriate credit limits and obtaining collateral as deemed nec-essary. For each collateral type a minimum haircut is defined in order to account for the volatility in market values according to the nature and liquidity of the collateral. Around 35% of the Group's credit exposure is secured by property and only 18% is unsecured.

The Group's credit risk appetite is defined and moni-tored through a comprehensive system of credit limits.

The Group has its own rating system for corporate clients. Each credit is assessed as to the borrower's credit worthiness, collateral coverage and collateral quality requirements, as well as the underlying trans-action rationale, business potential and any addi-tional risk mitigations. Personal credits are usually only granted on a fully collateralised basis. Collateral coverage is monitored on a regular basis and accord-ing to the prevailing market conditions.

Adequate and clear segregation of duties is established among the various organisational units involved in the acquisition of credit business, the analysis and approval of a credit request, and the subsequent administration.

Bank counterparties, issuers and sovereigns are ana-lysed according to their financial performance and their external rating. Over 75% of the credit exposure to financial institutions is of investment-grade qual-ity and the remaining 25% consists mainly of trade finance exposure in emerging markets where the Group is closely related to and monitors the portfolio with a set of country limits.

As for non-performing loans, the Group is in a com-fortable position. After taking the collateral at market value and the specific provisions into account, the net unsecured and unprovided position at the end of December 2014 was only CHF 10.5 million.

Country risks are monitored quarterly and are either guaranteed with the World Bank (MIGA) or provid-ed for in accordance with the guidelines of the Swiss Bankers Association using international ratings.

Liquidity risk

The Group applies a prudent approach to liquid-ity risk management. The Group Asset & Liability Management Committee oversees liquidity and mar-ket risks regularly.

The Group grants advances and loans to clients both on a short-term basis and with tenors generally up to five years. Funding is primarily obtained through deposits, which are mainly at sight, or short-term deposits. Wholesale funding is not significant and deposits are well diversified. No single depositor accounts for more than 5% of the Group's total deposits. Excess liquidity is held as bank placements or financial investments. The latter primarily consist of bond portfolios of sovereign issuers or other issu-ers of high quality.

The contractual maturities of the Group's financial assets exceed the contractual maturities of the finan-cial liabilities. However, when determining maturity gaps, the stickiness of deposits or economic matu-rities needs to be considered, which significantly

14

Habib Bank AG Zurich

GROUP

In addition, branches and subsidiaries have placed excess liquidity in bank placements or in financial investments with tenors usually up to three to five years. While the volume of financial investments is kept limited, the average duration of the fixed income portfolios creates interest rate risk exposure given the absence of long-term wholesale financing.

As for foreign exchange risks, the Group pursues a risk-averse approach and aims at keeping potential foreign exchange losses low. The Group neither speculates on foreign exchange movements nor pur-sues proprietary foreign exchange trading activities.

Profits earned in the Bank's branches are subject to exchange rate risk up to their remittance to Habib Bank AG Zurich, Zurich. These risks are monitored at the Head Office, and profits hedged as felt appropri-ate. Capital and reserves held in the branches are also subject to foreign exchange risk insofar as they are held in local currencies. Any foreign exchange trans- lation gains or losses on these capital and reserves are taken to the income statement in the year in which they occur.

Operational risk

Operational risk is defined as the risk of direct or indirect loss, or damaged reputation, resulting from inadequate or failed internal processes, from people or systems, or from external events.

The Group makes use of six operational risk man-agement processes, which consist of key risk indica-tors, change risk assessment, risk self-assessment, scenario analysis, risk event management and issue management and action tracking.

Furthermore, three types of risk mitigation are used and comprise control enhancement, business con-tinuity management and other mitigation measures (risk avoidance, risk reduction, risk transfer).

To proactively address risks related to potential busi-ness disruptions, business impact analyses, crisis

reduces the contractual gaps. Furthermore, individu-al clients groups in different countries will not act in the same way and at the same time.

In general, the Group is exposed to potential larger depositor outflows and sudden adverse market devel-opments. Therefore, related scenarios have been analysed as part of the three liquidity stress tests per-formed throughout the Group. The stress test results showed that the liquid assets available could absorb projected outflows in all cases.

The Group maintains a strong liquidity position, which is further supported by established repo functionalities. In addition, liquidity coverage ratio targets have been defined for all operating group companies.

The short-term liquidity disposition and liquidity situation of individual countries are monitored by the respective Country Treasury functions. In addi-tion, liquidity reserves are held both on Group and on country level and contingency funding plans are in place for the Group, all branches and subsidiaries.

Market risk

The Group is exposed to interest rate risk, foreign exchange risk and, to a very limited extent, to equi-ties and commodities risk.

The Group's market risk appetite is defined and monitored through a comprehensive system of mar-ket risk limits. Furthermore, the Group regularly performs scenarios and stress tests for interest rate and foreign exchange risks based on prevailing risk exposures.

The Group is exposed to interest rate risk due to interest periods set for advances made to clients exceeding the interest periods for client deposits taken. To limit interest rate risk, most client advances are agreed on a three or six month base rate plus a credit spread.

15

Habib Bank AG Zurich

GROUP

management teams and business continuity plans have been established for the Group as well as all branches and subsidiaries.

Legal and compliance risk

Legal risk is the risk that the Group will conduct activities or carries out transactions in which it is inadequately covered or is left exposed to potential litigation. It is the possibility that a failure to meet legal requirements may result in unenforceable con-tracts, litigation, fines, penalties or claims for dam-ages or other adverse consequences.

Compliance risk is the risk of legal or regulatory sanctions, material financial loss, or loss to the repu-tation the Group may suffer as a result of its failure to comply with laws, regulations, rules, related self-regulatory organisation standards, and codes of con-duct applicable to its banking activities.

Measures aimed at minimising legal and compli-ance risks include raising staff awareness of legal and regulatory issues through training, and internal directives and controls to ensure adherence to the legal and regulatory requirements within which the Group operates.

In line with the development of the legal and regu-latory environment of the industry, the Group has consistently invested in personnel and technical resources to ensure adequate compliance coverage. A comprehensive framework of policies and regular specialised training sessions ensure that staff receive appropriate ongoing education and training in this area.

Reputation risk

Reputation risk is the risk that illegal, unethical or inappropriate behaviour by the Group itself, employ-ees or clients or representatives of the Group may damage Habib Bank AG Zurich's reputation, leading potentially to a loss of business, fines or penalties.

The Group has established a Code of Conduct and promotes transparency and ethical behaviour.

Systemic risk

Systemic risk can be defined as a risk of disruption to financial services that is caused by an impairment of all or parts of the financial system and has the potential to have serious negative consequences for the real economy.

The Group analyses on a regular basis factors that could have a destabilising impact on the financial system, which include amongst others fragile eco-nomic development, continued financial market uncertainty, numerous political crises, increased ex-posure to cyber attacks as well as the ever-increasing extent and complexity of regulations. Based on this analysis, the Group implements mitigating measures wherever possible.

Risk assessment

The Board of Directors conducted a risk assessment of major risk exposures of the Bank and the Group in 2014.

16

Habib Bank AG Zurich

GROUP

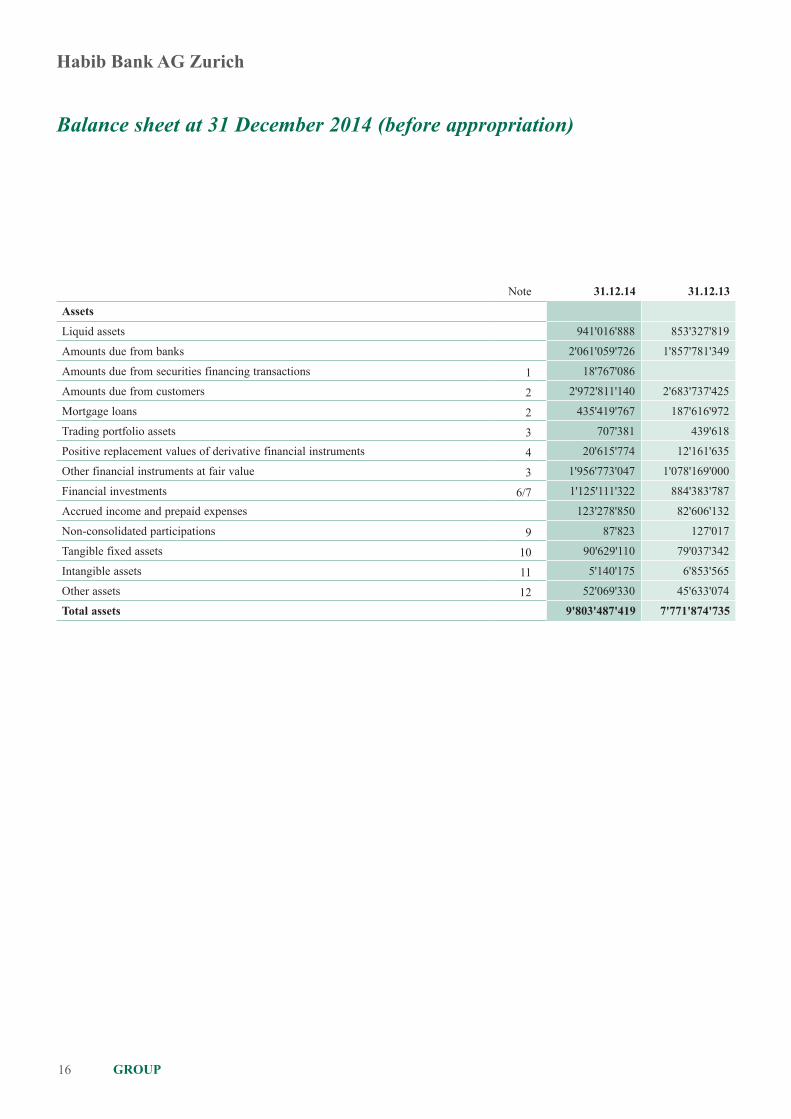

Note 31.12.14 31.12.13

Assets

Liquid assets 941'016'888 853'327'819

Amounts due from banks 2'061'059'726 1'857'781'349

Amounts due from securities financing transactions 1 18'767'086

Amounts due from customers 2 2'972'811'140 2'683'737'425

Mortgage loans 2 435'419'767 187'616'972

Trading portfolio assets 3 707'381 439'618

Positive replacement values of derivative financial instruments 4 20'615'774 12'161'635

Other financial instruments at fair value 3 1'956'773'047 1'078'169'000

Financial investments 6/7 1'125'111'322 884'383'787

Accrued income and prepaid expenses 123'278'850 82'606'132

Non-consolidated participations 9 87'823 127'017

Tangible fixed assets 10 90'629'110 79'037'342

Intangible assets 11 5'140'175 6'853'565

Other assets 12 52'069'330 45'633'074

Total assets 9'803'487'419 7'771'874'735

Balance sheet at 31 December 2014 (before appropriation)

17

Habib Bank AG Zurich

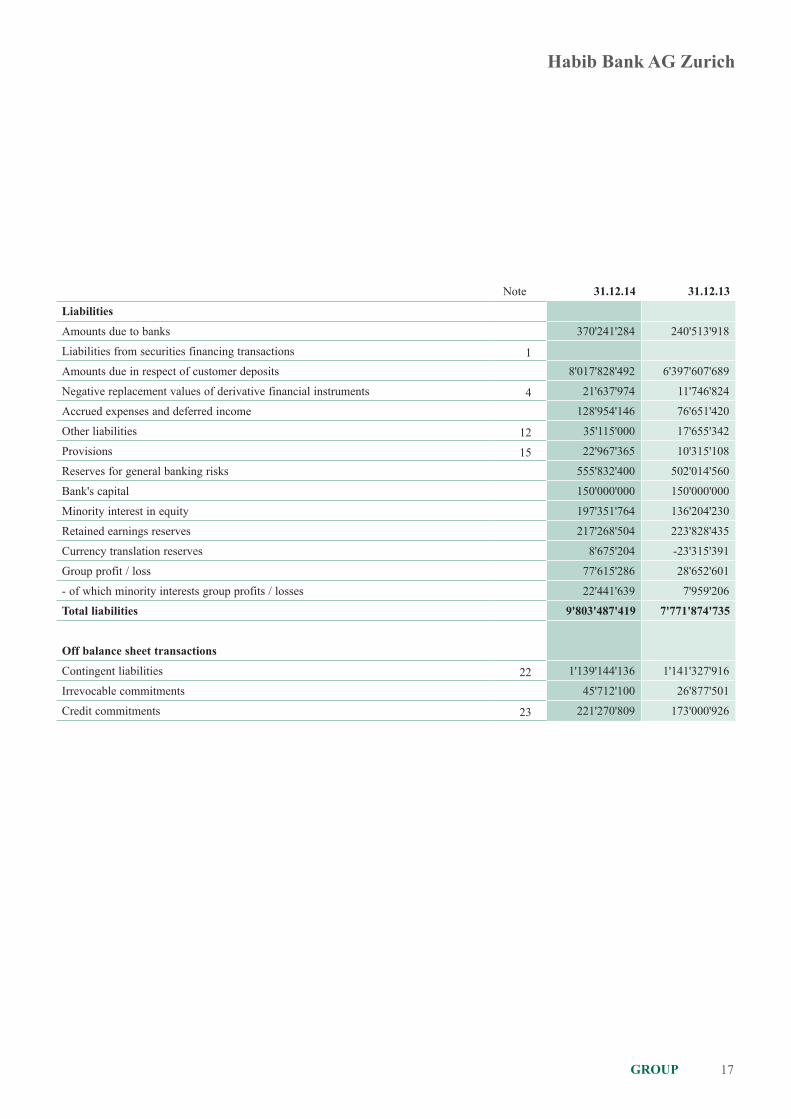

GROUP

Note 31.12.14 31.12.13

Liabilities

Amounts due to banks 370'241'284 240'513'918

Liabilities from securities financing transactions 1

Amounts due in respect of customer deposits 8'017'828'492 6'397'607'689

Negative replacement values of derivative financial instruments 4 21'637'974 11'746'824

Accrued expenses and deferred income 128'954'146 76'651'420

Other liabilities 12 35'115'000 17'655'342

Provisions 15 22'967'365 10'315'108

Reserves for general banking risks 555'832'400 502'014'560

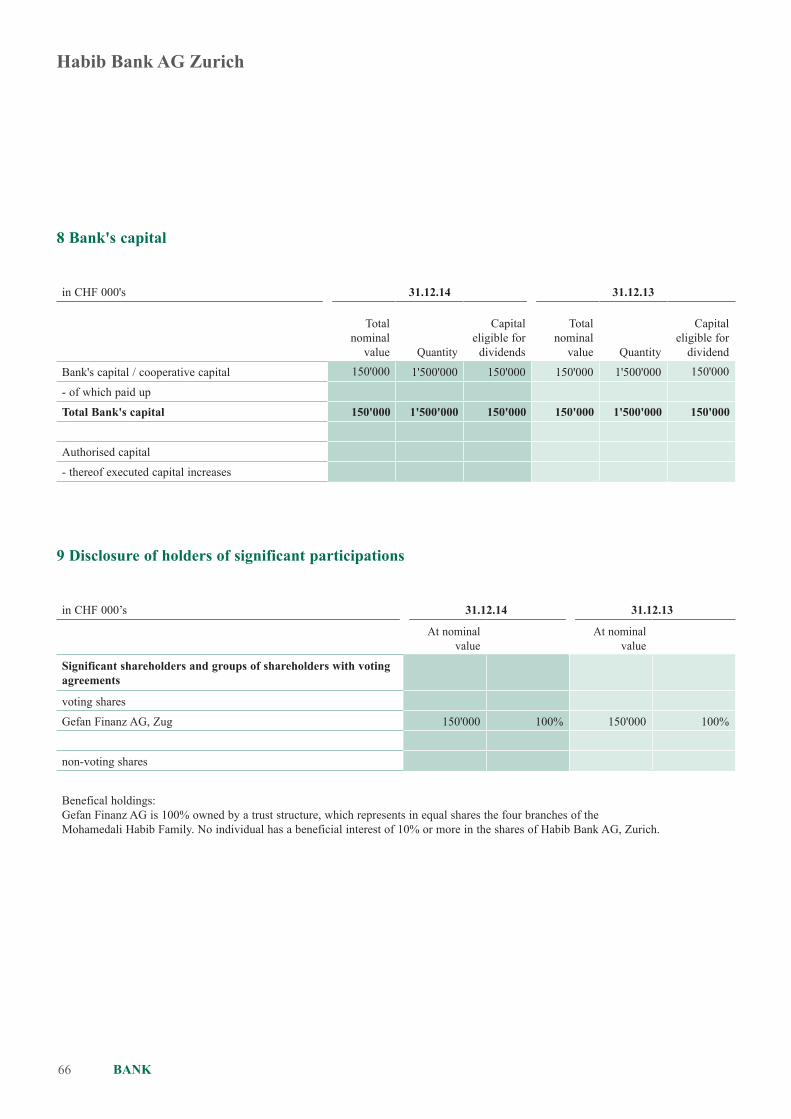

Bank's capital 150'000'000 150'000'000

Minority interest in equity 197'351'764 136'204'230

Retained earnings reserves 217'268'504 223'828'435

Currency translation reserves 8'675'204 -23'315'391

Group profit / loss 77'615'286 28'652'601

- of which minority interests group profits / losses 22'441'639 7'959'206

Total liabilities 9'803'487'419 7'771'874'735

Off balance sheet transactions

Contingent liabilities 22 1'139'144'136 1'141'327'916

Irrevocable commitments 45'712'100 26'877'501

Credit commitments 23 221'270'809 173'000'926

18

Habib Bank AG Zurich

GROUP

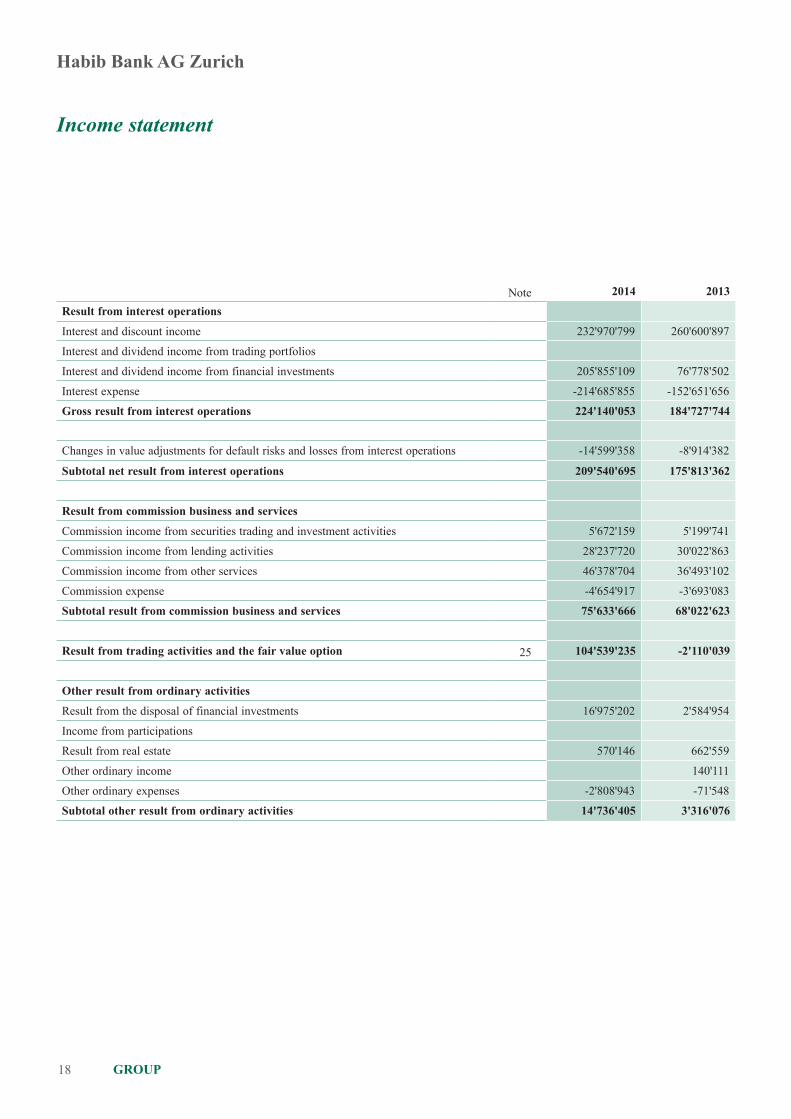

Income statement

Note 2014 2013

Result from interest operations

Interest and discount income 232'970'799 260'600'897

Interest and dividend income from trading portfolios

Interest and dividend income from financial investments 205'855'109 76'778'502

Interest expense -214'685'855 -152'651'656

Gross result from interest operations 224'140'053 184'727'744

Changes in value adjustments for default risks and losses from interest operations -14'599'358 -8'914'382

Subtotal net result from interest operations 209'540'695 175'813'362

Result from commission business and services

Commission income from securities trading and investment activities 5'672'159 5'199'741

Commission income from lending activities 28'237'720 30'022'863

Commission income from other services 46'378'704 36'493'102

Commission expense -4'654'917 -3'693'083

Subtotal result from commission business and services 75'633'666 68'022'623

Result from trading activities and the fair value option 25 104'539'235 -2'110'039

Other result from ordinary activities

Result from the disposal of financial investments 16'975'202 2'584'954

Income from participations

Result from real estate 570'146 662'559

Other ordinary income 140'111

Other ordinary expenses -2'808'943 -71'548

Subtotal other result from ordinary activities 14'736'405 3'316'076

19

Habib Bank AG Zurich

GROUP

Note 2014 2013

Operating expenses

Personnel expenses 26 -121'335'539 -121'857'921

General and administrative expenses 27 -56'991'414 -53'256'095

Subtotal operating expenses -178'326'953 -175'114'015

Value adjustments on participations, depreciation and amortisation on tangible fixed and intangible assets -11'759'200 -10'421'582

Changes to provisions and other value adjustments, and losses -6'566'683 -4'367'049

Operating result 207'797'163 55'139'374

Extraordinary income 28 2'675'030 700'398

Extraordinary expenses 28 -70'624 -2'598'445

Changes in reserves for general banking risks -76'619'639 -5'439'000

Taxes 30 -56'166'644 -19'149'726

Group profit / loss 77'615'286 28'652'601

- of which minority interests in group profit / loss 22'441'639 7'959'206

20

Habib Bank AG Zurich

GROUP

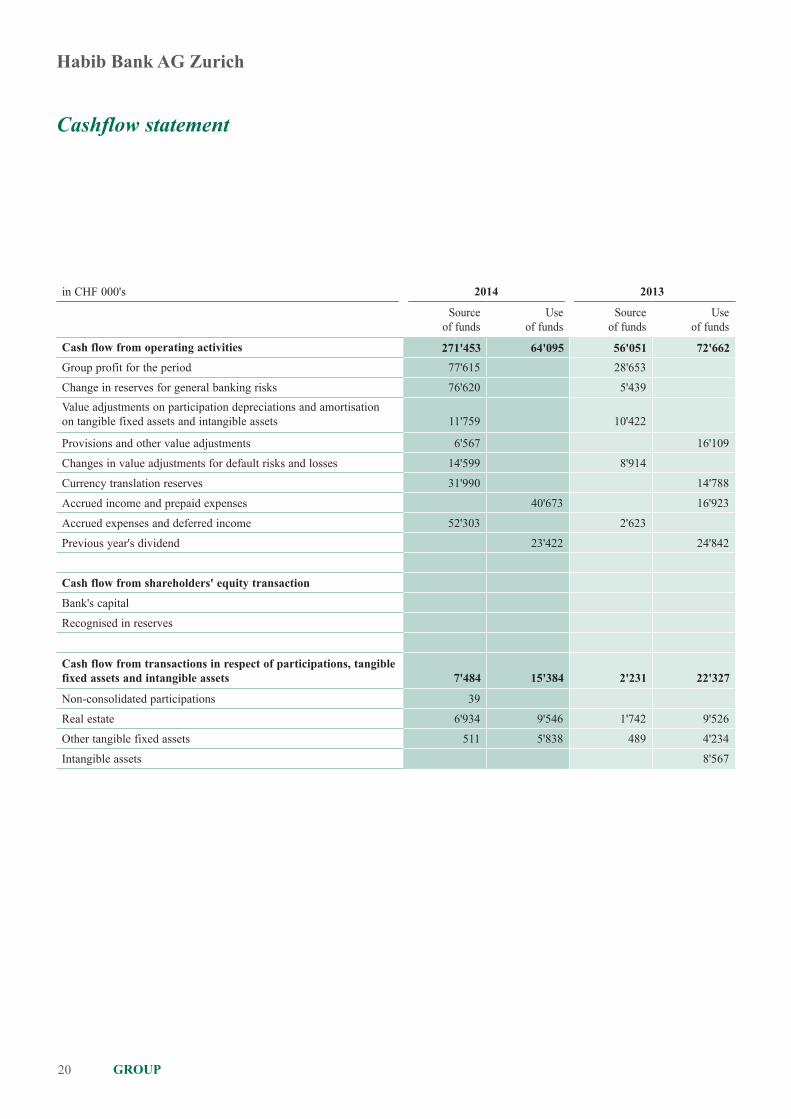

Cashflow statement

in CHF 000's 2014 2013

Source of funds

Use of funds

Source of funds

Use of funds

Cash flow from operating activities 271'453 64'095 56'051 72'662Group profit for the period 77'615 28'653

Change in reserves for general banking risks 76'620 5'439Value adjustments on participation depreciations and amortisation on tangible fixed assets and intangible assets 11'759 10'422

Provisions and other value adjustments 6'567 16'109

Changes in value adjustments for default risks and losses 14'599 8'914

Currency translation reserves 31'990 14'788

Accrued income and prepaid expenses 40'673 16'923

Accrued expenses and deferred income 52'303 2'623

Previous year's dividend 23'422 24'842

Cash flow from shareholders' equity transaction

Bank's capital

Recognised in reserves

Cash flow from transactions in respect of participations, tangible fixed assets and intangible assets 7'484 15'384 2'231 22'327

Non-consolidated participations 39

Real estate 6'934 9'546 1'742 9'526

Other tangible fixed assets 511 5'838 489 4'234

Intangible assets 8'567

21

Habib Bank AG Zurich

GROUP

in CHF 000's 2014 2013

Source of funds

Use of funds

Source of funds

Use of funds

Cash flow from the banking operations

Medium to long-term business (> 1 year) 717'652 600'435 405'875 265'395

Amounts due to banks 14'585 233

Amounts due in respect of customer deposits 117'165 44'458

Other liabilities 17'460 17'655

Amounts due from banks

Amounts due from customers 441'768 23'353

Mortgage loans 247'803 23'025

Other financial instruments at fair value 346'196 384'950

Financial investments 126'674 174'326

Other accounts receivable 6'436 3'270

Short-term business 1'632'432 1'861'418 410'489 403'934

Amounts due to banks 115'142 171'914

Liabilities from securities financing transactions

Amounts due in respect of customer deposits 1'503'056 122'401

Negative replacement values for derivative financial instruments 9'891 4'837

Amounts due from banks 203'279 278'063

Amounts due from securities financing transactions 18'767

Amounts due from customers 730'842 226'740

Trading portfolio assets 267 190

Positive replacement values for derivative financial instruments 8'454 5'280

Other financial instruments at fair value 532'408

Financial investments 367'401

Currency differences 4'343 4'998

Liquidity 87'689 110'328

Liquid assets 87'689 110'328

Total 2'629'021 2'629'021 874'646 874'646

22

Habib Bank AG Zurich

GROUP

Statement of changes in equity

In CHF 000's

Reserves for general

banking risk

Bank's capital

Currency translation

reserves

Minority interest

in equity

Retained earnings reserves

Groupprofit

or loss Total

Effect of the restatement 8'639 8'991 17'630

Equity at 01.01.14 502'016 150'000 -23'315 136'204 223'829 28'652 1'017'385

Transfer of profits to retained earnings 7'959 20'693 -28'652

Capital increase / decrease

Currency translation differences 31'991 26'639 58'930

Dividends and other distributions -11'422 -12'000 -23'422

Other allocations to (transfers from) the reserves for general banking risks 53'817 22'803 76'620

Other allocations to (transfers from) other reserves 14'869 -15'253 -384

Group profit / loss 77'615 77'615

Equity at 31.12.14 555'832 150'000 8'675 197'352 217'269 77'615 1'206'743

23

Habib Bank AG Zurich

GROUP

"Picture to come later"

24

Habib Bank AG Zurich

GROUP

The Habib Bank AG Zurich Group's annual financial statements have been drawn up in accordance with the accounting rules incorporated into the Swiss Banking Act and its accompanying ordinance, together with FINMA Circular 2015/1 "Accounting - Banks".

These accounts, which are based on the following consolidation and accounting policies, give a true and fair view of the Bank and the Group's assets, of its financial position and of the results of its opera-tions.

Consolidation principles

Scope of the consolidationThe Group accounts incorporate the annual financial statements of Habib Bank AG Zurich, Zurich and its subsidiaries. Refer to note 8 for a list of consolidated subsidiaries.

Method of consolidationThe Group’s capital consolidation follows the pur-chase method.

The interest in equity and profit or loss attributable to minority shareholders are disclosed separately. Intra-group assets and liabilities as well as expenses and income from intra-group transactions are eliminated.

Consolidation periodThe consolidation period for all Group companies is the calendar year. The closing date for the consoli-dated financial statements is 31 December.

Foreign currency translation

In the financial statements of individual Group compa-nies and branches, income and expenditure in foreign currencies are translated at the exchange rate ruling as at the transaction date. Amounts due from and due to third parties in foreign currencies are translated at the year-end rate. Gains and losses arising from currency translations into the local currencies are charged to the income statement as "Result from trading activities and the fair value option".

Summary of significant accounting principles

For consolidation purposes, the balance sheets of the financial statements of branches and subsidiaries based outside Switzerland are translated into Swiss francs at exchange rates prevailing at the Group reporting date. The corresponding income statements are translated at the average rates of the respective year. Foreign exchange differences arising from the translation of the financial statements of subsidiaries are recorded within the equity, whereas those from the translation of financial statements of branches are recorded in the income statement as "Result from trading activities and the fair value option".

The following exchange rates of the major currencies were used for the balance sheet: 31.12.14 31.12.131 US dollar 0.99 0.891 pound sterling 1.54 1.47100 UAE dirham 26.95 24.19100 Pakistan rupees 0.98 0.84100 South Africa rand 8.51 8.50

The following exchange rates of the major currencies were used for the income statement: 31.12.14 31.12.131 US dollar 0.92 0.921 pound sterling 1.51 1.45100 UAE dirham 24.98 25.15100 Pakistan rupees 0.91 0.92100 South Africa rand 8.48 9.60 Valuation and accounting principles

The valuation and accounting principles are consist-ent for the Bank and the Group.

The financial statements of all group companies used for consolidation comply with the below valuation and accounting principles.

25

Habib Bank AG Zurich

GROUP

Recording of transactions

Transactions are recorded at the transaction date. Prior to the value date, forward foreign exchange and precious metal transactions are carried as off balance sheet business. Receivables and payables are disclosed according to the domicile or residency of clients.

Liquid assets and amounts due to and from banks and amounts due in respect of customer deposits

These amounts, including interest due but not paid, are shown at nominal value.

Amounts due from and liabilities from securities financing transactions

The Group buys and sells securities under agree-ments to re-sell or re-purchase substantially identical securities. Such agreements do not normally con-stitute economic sales and are therefore treated as financing transactions. Securities sold subject to such agreements continue to be recognised in the balance sheet. The proceeds from the sale of these securities are treated as liabilities. Securities purchased under agreements to re-sell are recognised as loans collat-eralised by securities, or as cash deposits against which the Group's securities are pledged.

Amounts due from customers and mortgage loans

These claims are reported at nominal value. All customer loans are assessed individually for default risks and, where necessary, value adjustments made in accordance with Group policy. These value adjust-ments take into account the value of any collateral (at lending values) and the financial standing of the borrower. They are set off against the corresponding assets.

Several Islamic Banking branches in Pakistan and South Africa maintain "Assets held under Ijarah" agreements. Acquired assets under this agreement are stated at cost less accumulated depreciation and impairment, if any.

Value adjustments for default risks

Receivables where it is considered unlikely that the debtor will fulfill his obligations are considered at risk. In particular, receivables where interest and commissions are more than 90 days overdue are considered to be at risk. Interest at risk, and interest, which is impaired, are not recognised as income but are deducted, together with value adjustments against the capital amount of the respective assets. Should the collection of interest in respect of "Amounts due from customers" and "Mortgage loans" be uncertain, interest is not calculated.

For consumer loans, specific value adjustments according to time-based criteria are built where inter-est is overdue for more than 60 days.

Value adjustments for country risk are assessed in accordance with the guidelines on the management of country risk from the Swiss Bankers Association. Furthermore, country-specific general credit risk value adjustments are maintained based on the dif-ferentiated risk profiles recognised for individual sectors of the loan portfolios, or where uncertainty is reflected by additional value adjustments. Value adjustments for country risk, as well as country specific general credit risk value adjustments, are deducted from "Amounts due from customers".

Trading portfolio assets

"Trading portfolio assets" positions consist mainly of precious metals. They are valued at fair value as at the balance sheet date.

Other financial instruments at fair value

"Other financial instruments at fair value" which are traded on an active market and meet the conditions for an assessment at fair values according to FINMA Circular 2015/1 "Accounting - Banks" and which are not intended to be held until maturity are valued according to this principle.

26

Habib Bank AG Zurich

GROUP

Financial investments

"Financial investments" consist mainly of fixed inter-est securities. The majority of these are acquired with the intention of holding them until maturity and are hence carried at cost adjusted for the amortisation of premiums and discounts using the accrual method.The remaining investments in this positions are val-ued at the lower of cost or market value principle. This position also includes real estate, assumed from the lending business for resale, and a number of securities, both of which are valued at the lower of cost or market value.

Derivative financial instruments

Derivative financial instruments consist entirely of trading instruments which are reported at fair value. The realised and non-realised gains and losses from these transactions are reported under "Result from trading activities and the fair value option".

The Group had no significant open derivative trans-actions on its own account at the balance sheet date. Positive and negative replacement values of open derivative financial instruments on behalf of clients are shown in the balance sheet as a separate line item. The respective contract volumes are shown in the notes.

Non-consolidated participations

Long-term holdings in associated companies, none of which exceed 10%, are valued at cost less any economically necessary depreciation.

Tangible fixed assets

"Tangible fixed assets" used for more than one accoun- ting period and which exceed the thresholds defined by the Group are capitalised. In this case, they are depreciated on a straight-line basis over the period of their estimated useful lifetime. Estimated life times have been set as follows:

Bank buildings and residential apartments 25-50 yearsLeasehold improvements 5-10 yearsFurniture 4-7 yearsOther fixed assets 3-5 yearsSoftware (acquired) 3-5 years

No depreciation is charged on land except where value adjustments have been made to allow for a reduction in market value. The tangible fixed assets are re-assessed whenever circumstances suggest that their value may have fallen below their book value.

Intangible assets: Goodwill

Goodwill in the balance sheet results from the pre-mium paid over net asset value from an acquired company. In such cases, the recorded goodwill is reviewed for impairment every year and written off over five years on a straight line basis.

Provisions

The Group records "Provisions" to cover specific risks that are based on a past event that represent a prob-able obligation and for which the amount can be reliably estimated.

Reserves for general banking risks

These taxed reserves are held in line with the Group's prudent policies as precautionary reserves to hedge against latent risks in the Group's operating activities. They form part of the "Tier 1" capital of the Group.

Off balance sheet items

Contingent liabilities relate mainly to irrevocable commitments originating from letters of credit and guarantees. These are generally fully secured. Necessary provisions are recorded on balance sheet under "Provisions". "Contingent liabilities", together with "Irrevocable commitments", call liabilities and acceptance credits, are recorded at nominal value.

27

Habib Bank AG Zurich

GROUP

Fiduciary transactions are converted into Swiss francs at the rates prevailing at the balance sheet date and are shown at nominal value.

Taxes and deferred taxes

Income taxes are based on the tax laws of each tax authority and are expensed in the period in which the related profits are made. Deferred taxes arising from temporal differences between the stated values of assets and liabilities in the consolidated sheet and their corresponding tax values are recongnised as deferred tax assets or deferred tax liabilities. Deferred tax assets are capitalised if there is likely to be enough taxable profit to offset these differences in future.

Pension plan commitments

In Switzerland, the occupational benefit plans are covered by Allianz Suisse Insurance Company. All employees are insured in accordance with the law, the foundation document and the regulations of the benefit plan. In the other countries pension liabilities are covered by insurance companies or are posted directly to the balance sheet. The employer contribu-tion is included under "Personnel costs".

Amounts due from and due to related parties and governing bodies

Amounts due from and due to related parties include credit lines to Board Members and General Mana-gement. These transactions have been executed in accordance with the current internal regulations on staff loans, advances and deposits.

Amounts due from and due to related parties are included in table 16.

Changes from the previous year / Transition to FINMA Circular 2015/1 "Accounting - Banks".

Effective 1 January 2014, the Group adopted the FINMA Circular 2015/1 "Accounting - Banks". The aforementioned accounting policies have been

applied in the preparation of the financial statements for the year ended 31 December 2014.

The opening balances of the consolidated financial statement as at 1 January 2013, as well as the con-solidated income statement for 2013 have undergone a restatement.

The following paragraphs explain the principal adjustments made by the Group in restating its con-solidated financial statements as per 1 January 2013.

Financial investments at fair valueFinancial investments held by Habib Metropolitan Bank Ltd., which fulfill the criteria for the applica-tion of the fair value option, were revalued from amortised costs to fair value as of 1 January 2013 and reclassified to the balance sheet position "Other financial instruments at fair value". The net impact of the revaluation amounted to CHF 17.6 million (CHF 27.1 million less deferred tax liabilities of CHF 9.5 million) was recognised in equity with no effect on the consolidated income statement 2013. The result-ing effects on the Group's equity are disclosed in the statement of changes in equity.

Due to decreasing market values, the Group expe-rienced a net loss of CHF 7.5 million in 2013 on its "Other financial instruments at fair value".

Foreign exchange impactUnder the previous accounting principles year-end rates were used for the translation of income statements from foreign branches and subsidiaries. Following the new accounting standard and hence applying average rates for the translation of these income statements, the consolidated income state-ment 2013 increased by CHF 2.0 million.

Events after the balance sheet date

No events that would adversely affect the financial statements included in this report occurred after the balance sheet date.

28

Habib Bank AG Zurich

GROUP

1 Structure of securities financing transactions (assets and liabilities)

Notes to annual consolidated financial statements

in CHF 000's 31.12.14 31.12.13

Book value of receivables from cash collateral related to securities borrowing and reverse-repurchase transactions* 18'767

Book value of payables from cash collateral posted for securities lending and repurchase transactions*

Book value of securities lent in connection with securities lending or delivered as collateral in connection with securities borrowing as well as securities in own portfolio transferred in connection with repurchase transactions 18'767

- of which those with an unrestricted right to resell or pledge

Fair value of securities serving as collateral posted for securities lending or securities borrowed or securities received in connection with reverse-repurchase transactions with an unrestricted right to resell or repledge them

- of which repledged securities

- of which resold securities

* Before taking into consideration any netting agreements

29

Habib Bank AG Zurich

GROUP

2 Collateral for loans and off-balance sheet transactions, as well as impaired loans / receivables

Type of collateral

in CHF 000'sMortgage coverage

Secured by other

collateral Unsecured Total

Loans (before offsetting any value adjustments)

Due from customers 941'930 1'620'927 639'268 3'202'124

Mortgage loans 435'420 435'420

- Residential and commercial property 402'780 402'780

- Commercial premises 32'640 32'640

Total loans (before netting any value adjustments) 31.12.14 1'377'350 1'620'927 639'268 3'637'544

31.12.13 1'108'156 1'544'138 406'725 3'059'019

Total loans (after netting any value adjustments) 31.12.14 1'201'558 1'583'367 623'304 3'408'229

31.12.13 1'021'585 1'469'959 379'810 2'871'354

Off balance sheet

Contingent liabilities 15'874 451'050 672'220 1'139'144

Irrevocable commitments 45'712 45'712

Credit commitments 3'241 150'961 67'069 221'271

Total off balance sheet 31.12.14 19'115 602'011 785'001 1'406'127

31.12.13 28'222 1'194'732 118'252 1'341'206

in CHF 000's Gross debt

amount

Est. liqui-dation value of the

collateral Net debt

amount

Individual value

adjustments

Impaired loans / receivables

31.12.14 368'461 117'555 250'906 226'708

31.12.13 308'902 71'268 237'634 185'938

30

Habib Bank AG Zurich

GROUP

3 Breakdown of trading portfolios and other financial instruments at fair value

in CHF 000's 31.12.14 31.12.13Assets

Trading portfolios 707 440Debt instruments, money-market instruments, money-market transactions

- of which listed

Equity interests

Precious metals and commodities 707 440Other trading assets

Other financial instruments at fair value 1'956'773 1'078'169Debt instruments 1'839'980 974'070Structure products

Others 116'793 104'099

Total assets 1'957'480 1'078'609 - of which determined by valuation model 17'223 4'806 - of which securities allowed for repo transactions in accordance with liquidity requirements 1'298 1'334

31

Habib Bank AG Zurich

GROUP

32

Habib Bank AG Zurich

GROUP

4 Presentation of derivative financial instruments

Trading instruments

in CHF 000's

Positivereplacement

values

Negativereplacement

valuesContractvolume

Interest rate instruments

Forward contracts, including FRAs

Swaps

Futures

Options (OTC)

Options (exchange-traded)

Foreign exchange / precious metals

Forward contracts 18'949 13'335 3'035'469 Combined interest rates / currency swaps

Futures

Options (OTC)

Options (exchange-traded)

Equity interests / indices

Forward contracts

Swaps

Futures

Options (OTC)

Options (exchange-traded) 5'416

Credit derivatives

Credit default swaps

Total return swaps

First-to-default swaps

Other credit derivatives

Other

Forward contracts 1'668 8'303 1'138'035 Swaps

Futures

Options (OTC)

Options (exchange-traded)

Total before taking into consideration netting agreements

Total at 31.12.14 20'616 21'638 4'178'919 - of which determined by using a valuation model

33

Habib Bank AG Zurich

GROUP

in CHF 000's

Positive replacement

value(accumulated)

Negative replacement

value(accumulated)

Total after taking into consideration netting agreements

Total at 31.12.14 20'616 21'638

at 31.12.13 12'162 11'747

5 Breakdown by counterparties of derivative financial instruments

in CHF 000's

Central clearing

parties

Banks and securities

dealers Other clientsPositive replacement values (after taking into consideration netting contracts) 291 18'634 1'691

The Group has no hedging instruments.

Trading instruments

in CHF 000's

Positivereplacement

values

Negativereplacement

valuesContractvolume

Total at 31.12.13 12'162 11'747 2'350'164 - of which determined by using a valuation model

34

Habib Bank AG Zurich

GROUP

6 Breakdown of financial investments

Book value Fair value

in CHF 000's 31.12.14 31.12.13 31.12.14 31.12.13

Debt instruments 1'115'015 874'397 1'116'937 879'570

- of which held until maturity 1'115'015 874'397 1'116'937 879'570

- of which not held until maturity

Equity interests 1'120 647 1'044 647

Real estate 8'976 9'340 13'833 10'039

Total 1'125'111 884'384 1'131'813 890'256

- of which securities allowed for repo transactions in accordance with liquidity requirements 177'029 225'642

in CHF 000's AAA AA A BBB BB to B Unrated

Book values 230'189 106'707 194'841 250'108 330'171 13'095

Rating category is based on the sovereign foreign currency long-term rating system from S&P.

7 Breakdown of the counterparty according to rating

35

Habib Bank AG Zurich

GROUP

8 List of consolidated companies in which the Bank permanently holds direct or indirect participation of significance

Business activities

Share capital (in 1'000)

Capital share

Proporti-on of vo-

ting rights Direct

ownership

Indirect

ownership

Company name and registered office

Habib Canadian Bank Limited, Toronto, Canada Bank CAD 30'000 100% 100% 100% 0%

HBZ Bank Limited, Durban, South Africa Bank ZAR 50'000 100% 100% 100% 0%

Habib European Bank Limited, Douglas, Isle of Man Bank GBP 5'000 100% 100% 100% 0%

HBZ Services FZ-LLC, Dubai, UAE Service centre AED 300 100% 100% 100% 0%

Habib Metropolitan Bank Ltd., Karachi, Pakistan Bank PKR 10'478'315 51% 51% 51% 0%HBZ Finance Ltd., Hong Kong Deposit-taking

company HKD 300'000 51% 51%

51%

0%

36

Habib Bank AG Zurich

GROUP

Reporting year

In CHF 000's Acquisition cost

Accumulated amortisations or

value adjustments (equity valuation)

Book value at 31.12.13 Reclassifications Investments Divestments Amortisations

Value adjustments of participations

interestBook value at

31.12.14 Market valueOther participation with no market value

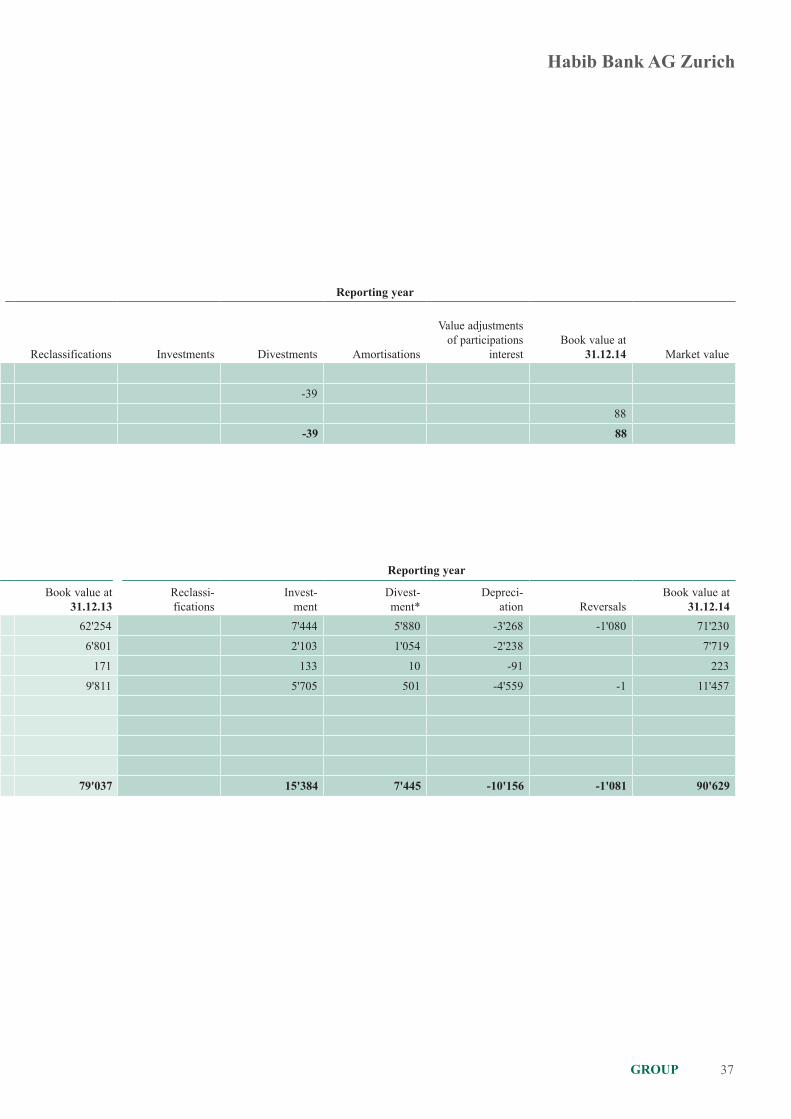

- HBZ Int. Exchange Co (Singapore) Pte Ltd., Singapore 39 39 -39- S.W.I.F.T. SCRL, Belgium 88 88 88Total 127 127 -39 88

9 Presentation of participations

10 Tangible fixed assets

Reporting year

in CHF 000'sAcquisi- tion cost

Accumulated depreciation

Book value at 31.12.13

Reclassi-fications

Invest- ment

Divest- ment*

Depreci- ation Reversals

Book value at 31.12.14

Bank buildings 91'436 -29'181 62'254 7'444 5'880 -3'268 -1'080 71'230

Other real estate 15'037 -8'236 6'801 2'103 1'054 -2'238 7'719

Proprietary or separately acquired software 2'980 -2'809 171 133 10 -91 223

Other tangible fixed assets 39'825 -30'013 9'811 5'705 501 -4'559 -1 11'457

Tangible assets acquired under financial leases:

- of which bank buildings

- of which other real estate

- of which other tangible fixed assets

Total 149'277 -70'240 79'037 15'384 7'445 -10'156 -1'081 90'629

* including net of foreign currency adjustments

37

Habib Bank AG Zurich

GROUP

Reporting year

In CHF 000's Acquisition cost

Accumulated amortisations or

value adjustments (equity valuation)

Book value at 31.12.13 Reclassifications Investments Divestments Amortisations

Value adjustments of participations

interestBook value at

31.12.14 Market valueOther participation with no market value

- HBZ Int. Exchange Co (Singapore) Pte Ltd., Singapore 39 39 -39- S.W.I.F.T. SCRL, Belgium 88 88 88Total 127 127 -39 88

Reporting year

in CHF 000'sAcquisi- tion cost

Accumulated depreciation

Book value at 31.12.13

Reclassi-fications

Invest- ment

Divest- ment*

Depreci- ation Reversals

Book value at 31.12.14

Bank buildings 91'436 -29'181 62'254 7'444 5'880 -3'268 -1'080 71'230

Other real estate 15'037 -8'236 6'801 2'103 1'054 -2'238 7'719

Proprietary or separately acquired software 2'980 -2'809 171 133 10 -91 223

Other tangible fixed assets 39'825 -30'013 9'811 5'705 501 -4'559 -1 11'457

Tangible assets acquired under financial leases:

- of which bank buildings

- of which other real estate

- of which other tangible fixed assets

Total 149'277 -70'240 79'037 15'384 7'445 -10'156 -1'081 90'629

* including net of foreign currency adjustments

38

Habib Bank AG Zurich

GROUP

12 Breakdown of other assets and other liabilities

Other assets Other liabilities

in CHF 000's 31.12.14 31.12.13 31.12.14 31.12.13

Compensation account 4'245 11'338 4'513

Deferred income tax recognised as assets 29'341 37'602

Others 18'483 8'031 23'777 13'142

Total 52'069 45'633 35'115 17'655

11 Intangible assets

Reporting year

in CHF 000's

Acqui- sition

cost

Accumu- lated

amorti-sations

Book value at31.12.13

Invest- ment

Divest- ment

Amorti- sations

Book value at31.12.14

Goodwill 8'567 -1'713 6'854 -1'714 5'140

Patents

Licenses

Other intangible assets

Total 8'567 -1'713 6'854 -1'714 5'140

39

Habib Bank AG Zurich

GROUP

13 Disclosure of assets pledged or assigned to secure own commitments and of assets under reservation at ownership*

in CHF 000's Book valueEffective

commitments

Assets pledged

Amounts due from banks 391 Financial investments 11'298 Assets put under ownership reservation

Total 11'689

* Excluding securities financing transactions

14 Payable to own employee benefit plans

31.12.14 31.12.13

Payables to employee benefit plans 141 123

Commitments to own pension and welfare plans

The Group does not maintain its own pension plans. The occupational benefit plans in the countries are covered by insurance companies. All employees are insured in accordance with the law, the foundation document and the regulations of the benefit plan.

In accordance with the contractual and legal conditions of the benefit plan in the countries, there can be neither economic liabilities that exceed the contributions set by the regulations of the benefit plan, nor economic benefits for the Group. In addition, during both the reporting year and during the previous year, there were no non-committed plans, nor was there an employer-paid contribution reserve, such that the expenses shown in the income statement equal the actual expenses for pension and welfare plans for the reporting period.

40

Habib Bank AG Zurich

GROUP

In CHF 000's Balance at 31.12.13

Use in conformity with designated

purpose ReclassificationsCurrency

differencesPast due interest,

recoveriesNew creations

charged to income Releases to income Balance at 31.12.14Provisions for deferred taxes 1'947 555 1'344 -221 3'624 Provisions for pension fund obligations

Provisions for default risks 3'909 512 4'421 Provisions for other business risks 8'368 -1'356 682 7'047 14'741 Provisions for restructuring

Other provisions 181 181 Total provisions 10'315 -1'356 3'909 1'237 9'084 -221 22'967

Reserves for general banking risks 502'015 53'818 555'832

Value adjustments for default risks and country risks 187'665 -6'903 -3'909 27'027 8'116 44'367 -27'056 229'308 - of which value adjustments for default risks in respect of impaired loans 185'938 -6'903 -3'909 27'027 8'116 43'494 -27'056 226'708 - of which value adjustments for latent risks 1'727 873 2'600

15 Value adjustments and provisions and reserves for general banking risks

41

Habib Bank AG Zurich

GROUP

In CHF 000's Balance at 31.12.13

Use in conformity with designated

purpose ReclassificationsCurrency

differencesPast due interest,

recoveriesNew creations

charged to income Releases to income Balance at 31.12.14Provisions for deferred taxes 1'947 555 1'344 -221 3'624 Provisions for pension fund obligations

Provisions for default risks 3'909 512 4'421 Provisions for other business risks 8'368 -1'356 682 7'047 14'741 Provisions for restructuring

Other provisions 181 181 Total provisions 10'315 -1'356 3'909 1'237 9'084 -221 22'967

Reserves for general banking risks 502'015 53'818 555'832

Value adjustments for default risks and country risks 187'665 -6'903 -3'909 27'027 8'116 44'367 -27'056 229'308 - of which value adjustments for default risks in respect of impaired loans 185'938 -6'903 -3'909 27'027 8'116 43'494 -27'056 226'708 - of which value adjustments for latent risks 1'727 873 2'600

42

Habib Bank AG Zurich

GROUP

16 Disclosure amounts due from / to related parties

in CHF 000's Amounts due from Amounts due to

31.12.14 31.12.13 31.12.14 31.12.13

Qualified holdings 44'473 32'195

Associates 20

Transactions with members of governing bodies 1'224 750 10'349 12'153

Other related parties

43

Habib Bank AG Zurich

GROUP

17 Maturity structure of financial instruments

Due

in CHF 000'sOn

demand CallableWithin

3 months

Between 3 and 12

months

Between 12 months

and 5 yearsAfter

5 yearsNo

maturity Total

Asset / financial instruments

Liquid assets 587'358 293'886 59'773 941'017

Amounts due from banks 132'303 23'810 1'746'595 158'352 2'061'060

Amounts due from securities financing transactions

18'767

18'767

Amounts due from customers 489'410 1'414'922 710'899 315'551 42'029 2'972'812

Mortgage loans 27'751 13'978 341'050 52'640 435'420

Trading portfolio assets 707 707

Positive replacement values of derivative financial instruments

657

19'958 20'616

Other financial instruments at fair value 11'671 941'223 586'550 300'536 116'793 1'956'773

Financial investments 677'067 13'010 54'055 212'980 158'387 9'612 1'125'111

Total 31.12.14 1'887'504 23'810 3'546'561 1'938'280 1'456'132 553'592 126'404 9'532'283

31.12.13 997'446 638'201 2'892'322 996'593 1'555'867 467'849 9'340 7'557'618

Liabilities / financial instruments

Amounts due to banks 156'415 119'935 79'306 9'494 5'092 370'242

Liabilities from securities financing transactions

Amounts due in respect of customer deposits

4'570'261

362'335

1'924'402

949'625

186'005 25'200 8'017'828

Negative replacement values of derivative financial instruments 589 21'049

21'638

Total 31.12.14 4'727'266 362'335 2'065'386 1'028'931 195'499 30'292 8'409'708

31.12.13 3'559'800 11'746 2'185'564 783'577 97'021 12'160 6'649'868

44

Habib Bank AG Zurich

GROUP

18 Assets and liabilities broken down by domestic and foreign origin in accordance with domicile principle

in CHF 000's 31.12.14 31.12.13

Domestic Foreign Domestic ForeignAssets

Liquid assets 124'037 816'980 103'019 750'309

Amounts due from banks 295'693 1'765'367 267'519 1'590'262

Amounts due from securities financing transactions 18'767

Amounts due from customers 95'126 2'877'685 23'619 2'660'118

Mortgage loans 435'420 187'617

Trading portfolio assets 476 231 440

Positive replacement values of derivative financial instruments 24 20'592 91 12'071

Other financial instruments at fair value 1'956'773 1'078'169

Financial investments 120'985 1'004'127 54'059 830'325

Accrued income and prepaid expenses 14'225 109'054 6'693 75'913

Non-consolidated participations 88 127

Tangible fixed assets 10'909 79'721 11'540 67'497

Intangible assets 5'140 6'854

Other assets 4'939 47'130 449 45'184

Total 671'552 9'131'934 467'429 7'304'446

Liabilities

Amounts due to banks 1'083 369'159 240'514 Liabilities from securities financing transactions

Amounts due in respect of customer deposits 122'289 7'895'538 114'408 6'283'200

Negative replacement values of derivative financial instruments 9 21'629 140 11'607

Accrued expenses and deferred income 5'933 123'021 1'598 75'053

Other liabilities 9'380 25'736 17'655

Provisions 10'636 12'331 10'315

Reserves for general banking risks 229'382 326'450 202'690 299'325

Bank's capital 150'000 150'000