Embed Size (px)

Citation preview

H1 2017 RESULTS PRESENTATION

August 24th 2017

#GrupaAzoty1H17@Grupa_Azoty

PageAGENDA

3

9

11

27

34

41

46

50

Key developments

Investments

Grupa Azoty Group

Grupa Azoty PUŁAWY

Grupa Azoty POLICE

Grupa Azoty KĘDZIERZYN

Summary

Appendices

2

GRUPA AZOTY GROUP 2

KEY DEVELOPMENTS IN H1 2017

RAISING FUNDS FOR

CAPITAL PROJECTS

FEEDSTOCK SUPPLY

SECURED – GAS

CONTRACT

PDH PROJECT WITH

PREDOMINANT

POLYPROPYLENE

OPTION

LETTER OF INTENT

FOR COAL

GASIFICATION

PROJECT

UPDATE OF 2013–

2020 STRATEGY

GRUPA AZOTY IN

FTSE4GOOD

EMERGING

GRUPA AZOTY GROUP

imag

e

AWARDS: LEADER

OF POLISH EXPORT

AND TRANSPARENT

COMPANY OF THE YEAR

2016

INVESTMENTS IN

INNOVATION

R&D

3

H1 2017 PERFORMANCE DRIVERS

STRONG DEMAND FOR

PLASTICS SUPPORTS HIGH

POLYAMIDE–BENZENE DELTAS

CONTINUED STRENGTH IN

MANUFACTURING AND

CONSTRUCTION CONTRIBUTES

TO SIGNIFICANT

IMPROVEMENT IN PIGMENTS

PERFORMANCE

STRATEGY TO GROW NPK

SALES VOLUMES TO OFFSET

FALLING PRICES AND RETAIN

MARKET SHARE

RISING PROPYLENE PRICES

SQUEEZE MARGINS ON OXO

ALCOHOLS

GROWING COMPETITION IN

NITRATE FERTILIZERS

(AN/CAN) DRIVES DOWN

SALES VOLUMES

HIGHER GAS PRICES AFFECT

PERFORMANCE IN

FERTILIZERS AND CHEMICALS

4

GRUPA AZOTY GROUP

GRUPA AZOTY GROUP H1 2017 FINANCIAL HIGHLIGHTS

(PLNm)

Financial results improve year

on year

Strong GDP growth across EU

supports record earnings in

Plastics

Wide margins on pigments in

the Chemicals segment driven

by uptrends in manufacturing

and construction

EBITDA triples in Tarnów

GRUPA AZOTY GROUP

REVENUE

4,870

EBITDA

714

EBITDA MARGIN

14.7%

NET PROFIT

378

COMMENTARY

5

GROUP COMPANIES' PERFORMANCE IN H1 2017

880

1,350

1,791

856

Grupa Azoty Kędzierzyn

Grupa Azoty PoliceGroup

Grupa Azoty PuławyGroup

Grupa Azoty S.A.(stand-alone data)

101

177

282

145

(PLNm)

REVENUE EBITDA

6

CONSOLIDATED REVENUE BY SEGMENT

3,055

1,210

676

2,742

1,128

571

2,673

1,264

743

Agro Fertilizers Chemicals Plastics

(PLNm)

1H2015 1H2016 1H2017 1H2015 1H2016 1H20171H2015 1H2016 1H2017

7

DIVIDENDS PAID BY THE PARENT

GRUPA AZOTY GROUP

78.4

83.3

19.9

148.8

39.9

Dividend for 2016

Dividend for 2015

Dividend for 2013

Dividend for 2012

Dividend for 2009

Dividend amount Profit earned

(PLNm)

GRUPA AZOTY HAS PAID OVER PLN 370M TO SHAREHOLDERS SINCE IPO

8

INVESTMENTS

INVESTMENTS

10GRUPA AZOTY GROUP

Tarnów

26%Puławy

26%

Police

24%

Kędzierzyn

20%

Other

4%

BY COMPANY

Expansion

49%

Maintenance

30%

Mandatory

8%

Purchase of finished

goods

3%

Other

10%

BY TYPE

COMPLETED INVESTMENT PROJECTS: PLN 501m

2017 CAPEX – PLN 1.3bn

GRUPA AZOTY

GROUP

GRUPA AZOTY GROUP FINANCIAL HIGHLIGHTS

12GRUPA AZOTY GROUP

2,159 2,0002,323

2,687

2,183

2Q2016 3Q2016 4Q2016 1Q2017 2Q2017

REVENUE

(PLNm)

* The 2016 figures adjusted for impairment losses associated with subsidiary AIG and impairment losses on the fat processing unit; the 2017 figures

adjusted for impairment losses on the fat processing unit.

177131

180

453

261201

150 191276

8.2% 6.6% 7.7%

16.9%

12.0%

2Q 2016 3Q 2016 4Q 2016 1Q2017 2Q2017

EBITDA

EBITDA(adjusted)*

EBITDA MARGIN

47

-10

29

255

12366 5

38 135

2.2%

-0.5%

1.2%

9.5%

5.6%

2Q 2016 3Q 2016 4Q 2016 1Q2017 2Q2017

NET PROFIT

NET PROFIT(adjusted)*

NET PROFITMARGIN

4 634

4 870

1H2016 1H2017

694

714718 729

1H2016 1H2017

354

378373

390

1H2016 1H2017

GRUPA AZOTY GROUP H1 2017 EBITDA BY SEGMENT

13GRUPA AZOTY GROUP

694 714

146 16 14

17 111

positive effect on EBITDA

negative effect on EBITDA

(PLNm)

Marked improvement in Plastics performance, driven by record-high PA6/caprolactam-benzene

deltas

A deterioration in earnings reported by Fertilizers and Chemicals (technical-grade urea/melamine),

mainly as a result of higher gas prices and increased imports of nitrate fertilizers affecting prices

REVENUE BY SEGMENT

Agro Fertilizers

Other

Chemicals

Plastics

Energy

H/H CHANGE IN REVENUE

-3%

+12%

+30%

-1%

-3%

14GRUPA AZOTY GROUP

Agro Fertilizers

55%

Chemicals 26%

Plastics15%

Energy2%Other

2%

EU

AGRO FERTILIZERS

15

H1 2017 REVENUE

Poland

1

Agro Fertilizers

PLN 2,673mAgro

Fertilizers 55%

Chemicals26%

Plastics 15%

Energy2%Other

2%

2

MARKET POSITION

GRUPA AZOTY GROUP

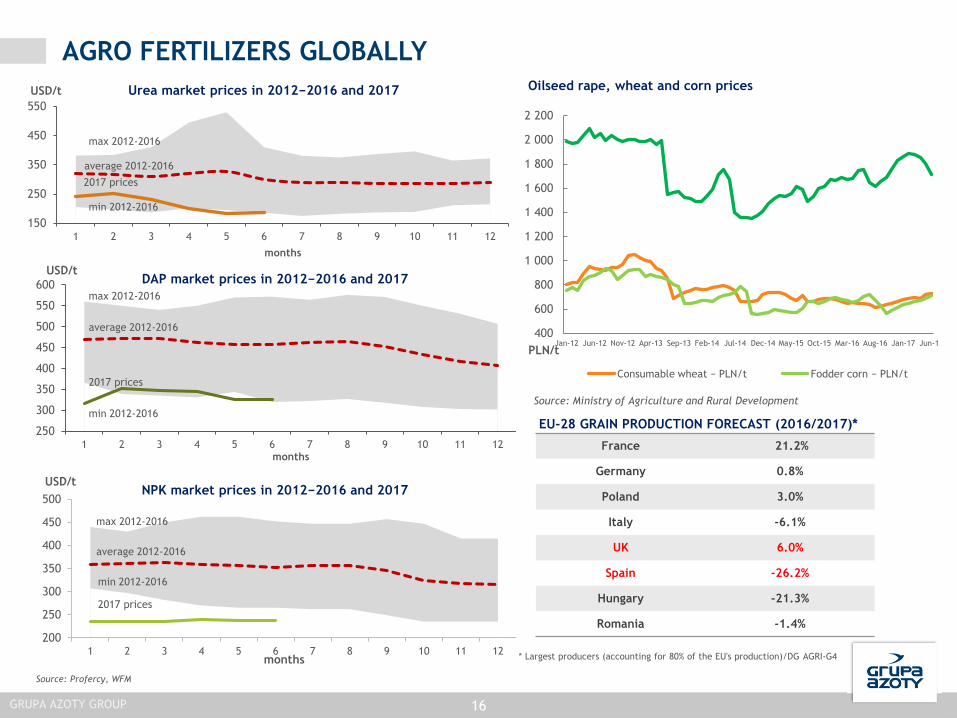

AGRO FERTILIZERS GLOBALLY

16

EU-28 GRAIN PRODUCTION FORECAST (2016/2017)*

Oilseed rape, wheat and corn prices

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

2 200

Jan-12 Jun-12 Nov-12 Apr-13 Sep-13 Feb-14 Jul-14 Dec-14 May-15 Oct-15 Mar-16 Aug-16 Jan-17 Jun-17PLN/t

Consumable wheat − PLN/t Fodder corn − PLN/t

Source: Ministry of Agriculture and Rural Development

Source: Profercy, WFM

150

250

350

450

550

1 2 3 4 5 6 7 8 9 10 11 12

USD/t

months

Urea market prices in 2012−2016 and 2017

max 2012-2016

average 2012-2016

min 2012-2016

2017 prices

250

300

350

400

450

500

550

600

1 2 3 4 5 6 7 8 9 10 11 12months

USD/tDAP market prices in 2012−2016 and 2017

average 2012-2016

min 2012-2016

2017 prices

max 2012-2016

200

250

300

350

400

450

500

1 2 3 4 5 6 7 8 9 10 11 12

USD/t

months

NPK market prices in 2012−2016 and 2017

average 2012-2016

min 2012-2016

2017 prices

max 2012-2016

* Largest producers (accounting for 80% of the EU's production)/DG AGRI-G4

France 21.2%

Germany 0.8%

Poland 3.0%

Italy -6.1%

UK 6.0%

Spain -26.2%

Hungary -21.3%

Romania -1.4%

GRUPA AZOTY GROUP

AGRO FERTILIZERS GLOBALLY

17

MARKET SPREADS PER N

PRICING TRENDS

0

100

200

300

400

500

600

Jan-1

4

Feb-1

4

Mar-

14

Apr-

14

May-1

4

Jun-1

4

Jul-

14

Aug-1

4

Sep-1

4

Oct-

14

Nov-1

4

Dec-1

4

Jan-1

5

Feb-1

5

Mar-

15

Apr-

15

May-1

5

Jun-1

5

Jul-

15

Aug-1

5

Sep-1

5

Oct-

15

Nov-1

5

Dec-1

5

Jan-1

6

Feb-1

6

Mar-

16

Apr-

16

May-1

6

Jun-1

6

Jul-

16

Aug-1

6

Sep-1

6

Oct-

16

Nov-1

6

Dec-1

6

Jan-1

7

Feb-1

7

Mar-

17

Apr-

17

May-1

7

Jun-1

7

DAP NPK 3x16 Phosphate rock

0

50

100

150

200

250

300

Jan-1

4

Feb-1

4

Mar-

14

Apr-

14

May-1

4

Jun-1

4

Jul-

14

Aug-1

4

Sep-1

4

Oct-

14

Nov-1

4

Dec-1

4

Jan-1

5

Feb-1

5

Mar-

15

Apr-

15

May-1

5

Jun-1

5

Jul-

15

Aug-1

5

Sep-1

5

Oct-

15

Nov-1

5

Dec-1

5

Jan-1

6

Feb-1

6

Mar-

16

Apr-

16

May-1

6

Jun-1

6

Jul-

16

Aug-1

6

Sep-1

6

Oct-

16

Nov-1

6

Dec-1

6

Jan-1

7

Feb-1

7

Mar-

17

Apr-

17

May-1

7

Jun-1

7

CAN (27%N) Urea (27%N) Ammonia (27%N)

CAN equivalent

NPK equivalent

EUR/t

USD/t

OUTLOOK

Weather conditions in the spring

with a minor impact on grain

yields in Poland

Global oversupply of grains

Low oil prices likely to drive

oilseed prices

Economic upturn and growth in

demand for food products

expected in Poland

Direct subsidies support demand

for fertilizers

Low ammonia prices;

potassium chloride prices

expected to remain strong

Oversupply of DAP fertilizers

and urea − production cuts likely

to help stabilize prices

GRUPA AZOTY GROUP

NITROGEN FERTILIZER IMPORTS 2016–2017

18

COMPARISON OF AMMONIUM NITRATE IMPORT VOLUMES

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Source: Analytical Centre, the Tax Administration Chamber in Warsaw

MONTHLY

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 2017CUMULATIVELY

131%

COMPARISON OF UREA IMPORT VOLUMES

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 2017MONTHLY CUMULATIVELY

-21%

GRUPA AZOTY GROUP

GRUPA AZOTY GROUP: AGRO FERTILIZERS

VOLUMES

19

'000 tonnes

(PLNm) 1H2016 1H20172Q

2016

2Q

2017

Change

Q/Q

Segment revenue

including:2,742 2,673 1,166 1,150 -1%

Nitrogen fertilizers,

and ammonia1,645 1,614 653 684 5%

Compound fertilizers 877 836 410 404 -1%

EBITDA 496 385 117 124 6%

EBITDA margin 18% 14% 10% 11% +1pp

0

300

600

900

1H2016 1H2017

0

100

200

300

400

2Q2016 2Q2017

GRUPA AZOTY GROUP

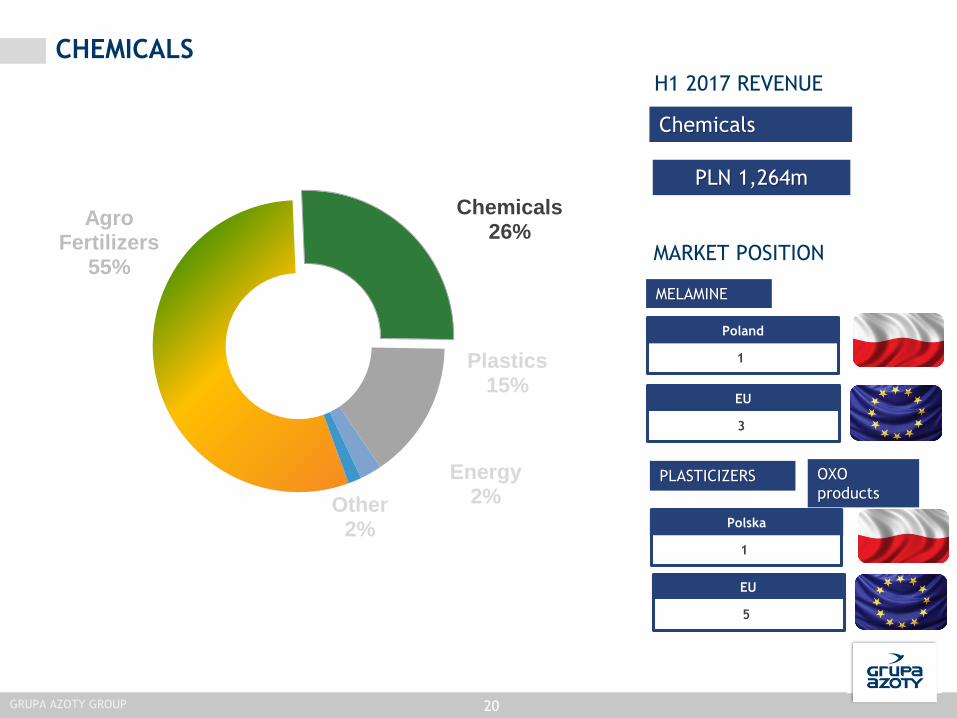

CHEMICALS

Other

Plastics

Chemicals

Energy

+XX%

+XX%

+XX%

+XX%

MARKET POSITION

EU

5

Polska

1

Chemicals

PLN 1,264m

PLASTICIZERS

MELAMINE

EU

3

Poland

1

OXO

products

H1 2017 REVENUE

20GRUPA AZOTY GROUP

Agro Fertilizers

55%

Chemicals26%

Plastics15%

Energy2%Other

2%

CHEMICALS GLOBALLY

MARKET SPREADS

PRICING TRENDS

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

DEHT (DOTP) 2-EH Propylene

EUR/t

OUTLOOK

Expected double-digit rise in

melamine prices

Projected rise in titanium white

prices

Increase in titanium white

feedstock prices

Movements in feedstock prices,

chiefly propylene, likely to trigger

strong reactions

Growing demand and higher prices

expected in the plasticizers market

during maintenance shutdowns

21GRUPA AZOTY GROUP

GRUPA AZOTY GROUP: CHEMICALS

VOLUMES

22

(PLNm) 1H2016 1H20172Q

2016

2Q

2017

Change

Q/Q

Segment revenue

including:1 128 1 264 593 617 4%

OXO alcohols 209 251 113 115 2%

Plasticizers 96 115 49 54 10%

Urea (technical grade) 208 248 98 122 24%

Melamine 216 227 116 108 -7%

Titanium white 150 178 82 93 13%

EBITDA 165 151 78 52 -33%

EBITDA margin 15% 12% 13% 8% -5pp

'000 tonnes

0

100

200

300

OXO alcohols Plasticizers Urea (technicalgrade)

Melamine Titanium white

1H2016 1H2017

0

50

100

150

OXO alcohols Plasticizers Urea (technicalgrade)

Melamine Titanium white

2Q2016 2Q2017

GRUPA AZOTY GROUP

PLASTICS

Other

Plastics

Chemicals

Energy

+XX%

+XX%

+XX%

+XX%

MARKET POSITION – PA6

EU *

5

Poland

1

Plastics

PLN 743m

* Integrated basis

H1 2017 REVENUE

23GRUPA AZOTY GROUP

PA6

Agro Fertilizers

55%

Chemicals26%

Plastics15%

Energy2%Other

2%

GLOBAL PLASTICS MARKET

24

WIDER MARKET SPREADS

PRICING TRENDS

0

500

1 000

1 500

2 000

2 500

Jan-1

4

Feb-1

4

Mar-

14

Apr-

14

May-1

4

Jun-1

4

Jul-

14

Aug-1

4

Sep-1

4

Oct-

14

Nov-1

4

Dec-1

4

Jan-1

5

Feb-1

5

Mar-

15

Apr-

15

May-1

5

Jun-1

5

Jul-

15

Aug-1

5

Sep-1

5

Oct-

15

Nov-1

5

Dec-1

5

Jan-1

6

Feb-1

6

Mar-

16

Apr-

16

May-1

6

Jun-1

6

Jul-

16

Aug-1

6

Sep-1

6

Oct-

16

Nov-1

6

Dec-1

6

Jan-1

7

Feb-1

7

Mar-

17

Apr-

17

May-1

7

Jun-1

7

EUR/t

Polyamide 6 Benzene

OUTLOOK

Strong impact of supply-demand

dynamics and oil prices

PA6 prices trending upwards in H1

2017

CPL and PA6 shortages due to

unscheduled plant shutdowns and

market conditions in Asia

Reduced PA6 oversupply; upswing

in the automotive and textile sectors

Year-on-year improvement in PA6

and CPL price spread

Changes expected in PA6 demand

structure, with the engineering

plastics, film and flexible packaging

sector gaining prominence

GRUPA AZOTY GROUP

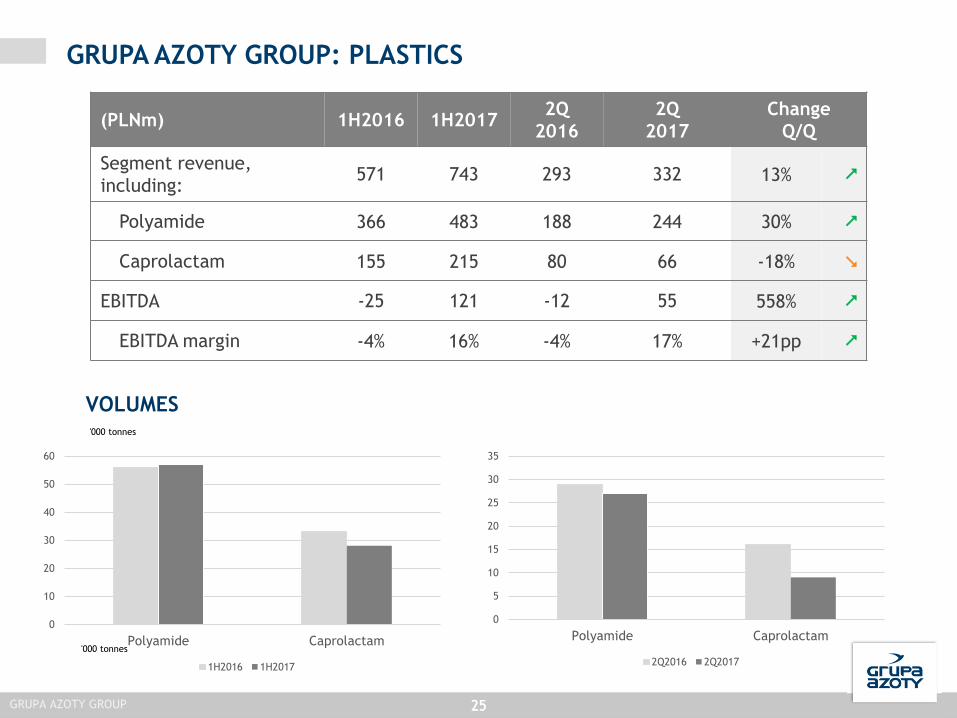

GRUPA AZOTY GROUP: PLASTICS

VOLUMES

25

(PLNm) 1H2016 1H20172Q

2016

2Q

2017

Change

Q/Q

Segment revenue,

including:571 743 293 332 13%

Polyamide 366 483 188 244 30%

Caprolactam 155 215 80 66 -18%

EBITDA -25 121 -12 55 558%

EBITDA margin -4% 16% -4% 17% +21pp

'000 tonnes

25

'000 tonnes

0

10

20

30

40

50

60

Polyamide Caprolactam

1H2016 1H2017

0

5

10

15

20

25

30

35

Polyamide Caprolactam

2Q2016 2Q2017

GRUPA AZOTY GROUP

GRUPA AZOTY GROUP FINANCING SOURCES AT JUNE 30TH 2017

26GRUPA AZOTY GROUP

RATIOS 1H2016 1H2017

Net debt (PLNm) 134 631

12-month net debt/EBITDA (ratio) 0.11 0.62

81%

10%

9%

FINANCING STRUCTURE

923

489 3

AVAILABLE FUNDS

Corporate credit facilities

Overdraft and multi-purposefacilities

(PLNm)

GRUPA AZOTY PUŁAWY GROUP

GRUPA AZOTY PUŁAWY GROUP FINANCIAL HIGHLIGHTS

28GRUPA AZOTY PUŁAWY

808 710 875 1,003788

2Q2016 3Q2016 4Q2016 1Q2017 2Q2017

REVENUE*

(PLNm)

11765 81

204

78119

65 93

212

93

14.4%

9.2% 9.2%

20.3%

9.9%

2Q 2016 3Q 2016 4Q 2016 1Q2017 2Q2017

EBITDA*

EBITDA(adjusted)**

EBITDA MARGIN

66 1627

138

2669 16

39

146

41

8.2%

2.2%3.1%

13.8%

3.3%

2Q 2016 3Q 2016 4Q 2016 1Q2017 2Q2017

NET PROFIT

NET PROFIT(adjusted)**

NET PROFITMARGIN

1 759

1 791

1H2016 1H2017

343282

346305

1H2016 1H2017

227

164

230187

1H2016 1H2017

* Restated initially to ensure data comparability following changes to the accounting policy as of January 1st 2017

** Adjusted for impairment losses on assets, including mainly the fat processing unit at ZA Chorzów and Elektrownia Puławy's assets

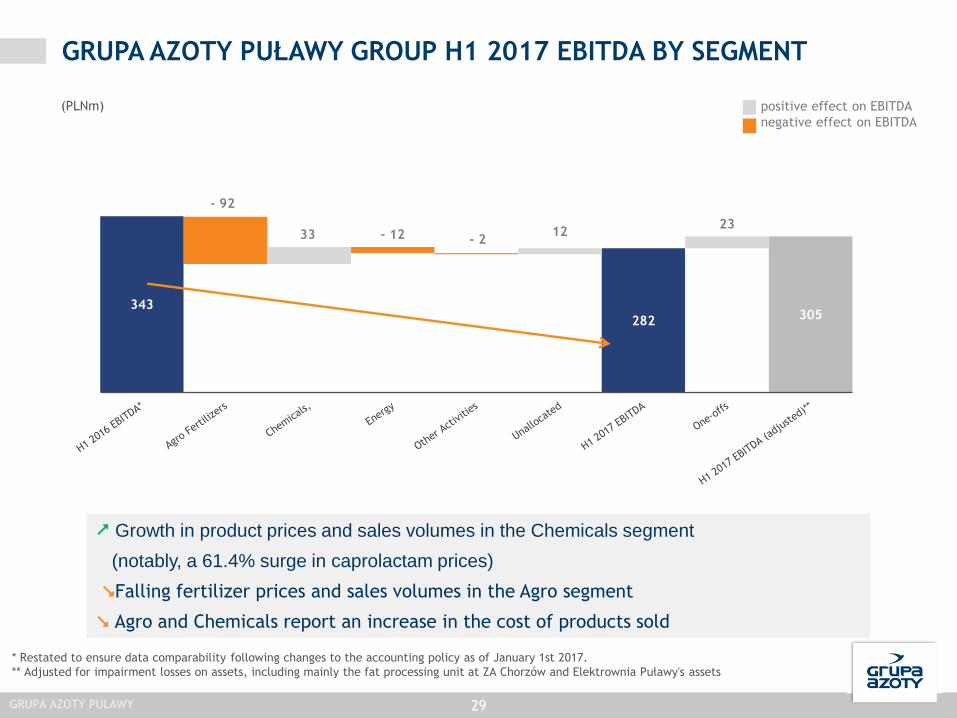

GRUPA AZOTY PUŁAWY GROUP H1 2017 EBITDA BY SEGMENT

29

343

282 305

- 92

33 - 12 - 212

23

positive effect on EBITDA

negative effect on EBITDA

(PLNm)

GRUPA AZOTY PUŁAWY

Growth in product prices and sales volumes in the Chemicals segment

(notably, a 61.4% surge in caprolactam prices)

Falling fertilizer prices and sales volumes in the Agro segment

Agro and Chemicals report an increase in the cost of products sold

* Restated to ensure data comparability following changes to the accounting policy as of January 1st 2017.

** Adjusted for impairment losses on assets, including mainly the fat processing unit at ZA Chorzów and Elektrownia Puławy's assets

GRUPA AZOTY PUŁAWY GROUP BY SEGMENT

Fertilizers

Other

Chemicals

Energy

H/H CHANGE IN REVENUE

-7%

+22%

- 11%

-9%

GRUPA AZOTY PUŁAWY 30

Fertilizers59%

Chemicals 37%

Energy2%

Other2%

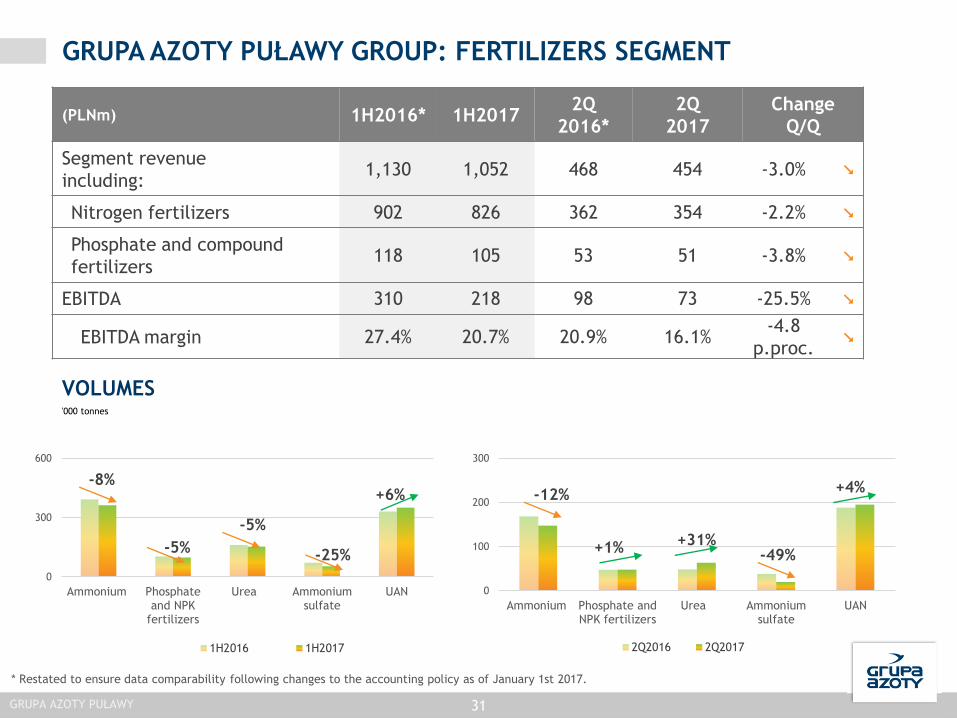

GRUPA AZOTY PUŁAWY GROUP: FERTILIZERS SEGMENT

VOLUMES

31

(PLNm) 1H2016* 1H20172Q

2016*

2Q

2017

Change

Q/Q

Segment revenue

including:1,130 1,052 468 454 -3.0%

Nitrogen fertilizers 902 826 362 354 -2.2%

Phosphate and compound

fertilizers118 105 53 51 -3.8%

EBITDA 310 218 98 73 -25.5%

EBITDA margin 27.4% 20.7% 20.9% 16.1%-4.8

p.proc.

'000 tonnes

GRUPA AZOTY PUŁAWY

0

300

600

Ammonium Phosphateand NPK

fertilizers

Urea Ammoniumsulfate

UAN

1H2016 1H2017

0

100

200

300

Ammonium Phosphate andNPK fertilizers

Urea Ammoniumsulfate

UAN

2Q2016 2Q2017

+6%-8%

-5%

-5%

-25%

+4%

-49%

-12%

+1%+31%

* Restated to ensure data comparability following changes to the accounting policy as of January 1st 2017.

GRUPA AZOTY PUŁAWY GROUP: CHEMICALS

VOLUMES

32

(PLNm) 1H2016* 1H20172Q

2016*

2Q

2017

Change

Q/Q

Segment revenue

including:543 661 291 296 1.7%

Melamine 216 227 116 108 -6.9%

Caprolactam 162 228 92 87 -5.4%

Urea 102 136 52 67 28.8%

EBITDA 98 131 56 40 -28.6%

EBITDA margin 18.0% 19.8% 19.2% 13.5%-5.7

p.proc.

'000 tonnes

GRUPA AZOTY PUŁAWY

-50

50

150

250

Melamine Caprolactam Urea

1H2016 1H2017

0

20

40

60

80

Melamine Caprolactam Urea

2Q2016 2Q2017

+30%

-35%

+28%

-13%-10%+2%

* Restated to ensure data comparability following changes to the accounting policy as of January 1st 2017.

GRUPA AZOTY PUŁAWY FINANCING SOURCES AT JUNE 30TH 2017

33

RATIOS 1H2016 1H2017

Net debt (PLNm) -682.9 -514.8

6-month net debt/EBITDA (ratio) -2.0 -1.8

500

97

AVAILABLE FUNDS

Corporate credit facilities

Overdraft and multi-purposefacilities

GRUPA AZOTY PUŁAWY

(PLNm)

GRUPA AZOTY POLICE GROUP

GRUPA AZOTY POLICE GROUP FINANCIAL HIGHLIGHTS

35

1,4541,249 1,440 1,292 1,350

1H 2013 1H 2014 1H 2015 1H 2016 1H 2017

REVENUE

(PLNm)

114 105

178136

177170

7.8%

8.4%

12.4%10.5%

13.1%

1H 2013 1H 2014 1H 2015 1H 2016 1H 2017

EBITDA

EBITDA (adjusted)*

EBITDA MARGIN

56 48107

77 100102

3.9%3.8%

7.4% 6.0% 7.4%

1H 2013 1H 2014 1H 2015 1H 2016 1H 2017

NET PROFIT

NET PROFIT (adjusted)*

NET PROFIT MARGIN

GRUPA AZOTY POLICE GROUP

* Net of one-off items relating to AFRIG

The H1 2013, H1 2014 and H1 2015 results are reported data; they do not include impairments recognised through profit or loss brought forward.

136

177

34 17

34 10

170

EBITDA net of

one-off items

GRUPA AZOTY POLICE GROUP H1 2017 EBITDA BY SEGMENT

36

(PLNm)

GRUPA AZOTY POLICE GROUP

positive effect on EBITDA

negative effect on EBITDAone-off items concerning

AFRIG

- effect on EBITDA

GRUPA AZOTY POLICE GROUP BY SEGMENT

Fertilizers

Other

Pigments

H/H CHANGE IN REVENUE

+3%

+19%

-3%

GRUPA AZOTY POLICE GROUP 37

Fertilizers84%

Pigments14%

Other2%

GRUPA AZOTY POLICE GROUP: FERTILIZERS

VOLUMES

38GRUPA AZOTY POLICE GROUP

+14%

+4%

0

300

600

900

1H2016 1H2017 1H2016 1H2017 1H2016 1H2017

Poland Exports

Urea Ammonia

+40%

+53%

+1%

+14%

Compound

fertilizers,

0

300

600

2Q2016 2Q2017 2Q2016 2Q2017 2Q2016 2Q2017

Poland Exports

Urea AmmoniaCompound

fertilizers

'000 tonnes

(PLNm) 1H2016 1H20172Q

2016

2Q

2017Change

Q/Q

Segment revenue, including: 1,112 1,141 507 543 7%

Compound fertilizers, 792 745 366 351 -4%

Urea 173 192 72 85 18%

Ammonia 106 158 47 82 74%

EBITDA 122 139 20 75 275%

EBITDA margin 11% 12% 4% 14% +10pp.

GRUPA AZOTY POLICE GROUP: PIGMENTS

VOLUMES

39

(PLNm) 1H2016 1H20172Q

2016

2Q

2017Q/Q change

Segment revenue, including: 157 186 85 97 14%

Titanium white 150 178 82 93 13%

Other 7 8 3 4 33%

EBITDA 10 44 8 24 200%

EBITDA margin 6% 24% 9% 25% +16pp.

+2%

'000 tonnes

GRUPA AZOTY POLICE GROUP

15

20

25

1H2013 1H2014 1H2015 1H2016 1H2017

Titanium white

GRUPA AZOTY POLICE GROUP FINANCING SOURCES AT JUNE 30TH 2017

40

RATIOS 1H2016 1H2017

Net debt (PLNm) 275 319

6-month net debt/EBITDA (ratio) 2.03 1.80

14%

52%

34%

FINANCING STRUCTURE

438

209

AVAILABLE FUNDS

Corporate creditfacilities

Overdraft and multi-purpose facilities

(PLNm)

GRUPA AZOTY POLICE GROUP

GRUPA AZOTY ZAKŁADY AZOTOWE KĘDZIERZYN S.A.

GRUPA AZOTY KĘDZIERZYN: FINANCIAL HIGHLIGHTS

42

411 379 465 485 395

2Q2016 3Q2016 4Q2016 1Q2017 2Q2017

REVENUE

(PLNm)

50

1830

81

20

12.2%

4.8%6.6%

16.6%

5.1%

2Q2016 3Q2016 4Q2016 1Q2017 2Q2017

EBITDA

EBITDA MARGIN

28-3

8

48

-3

6.8%

-0.7%

1.6%

9.8%

-0.8%

-3,0%

-1,0%

1,0%

3,0%

5,0%

7,0%

9,0%

11,0%

2Q2016 3Q2016 4Q2016 1Q2017 2Q2017

NET PROFIT

NET PROFITMARGIN

852880

1H2016 1H2017

154

101

1H2016 1H2017

94

44

1H2016 1H2017

GRUPA AZOTY KĘDZIERZYN

GRUPA AZOTY KĘDZIERZYN BY SEGMENT

Fertilizers

Other

OXO alcohols

Fertilizers48%

OXO alcohols

46%

Other6%

H/H CHANGE IN REVENUE

-8.8%

+18.9%

+9.1%

43GRUPA AZOTY KĘDZIERZYN

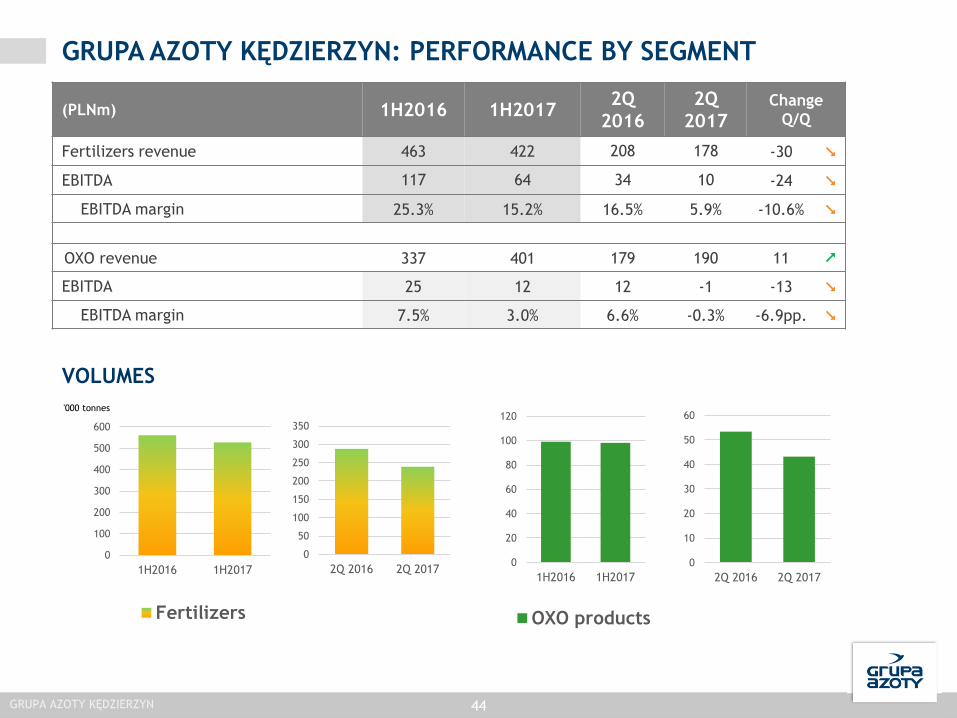

GRUPA AZOTY KĘDZIERZYN: PERFORMANCE BY SEGMENT

0

20

40

60

80

100

120

1H2016 1H2017

OXO products

0

10

20

30

40

50

60

2Q 2016 2Q 2017

44

(PLNm) 1H2016 1H20172Q

2016

2Q

2017Change

Q/Q

Fertilizers revenue 463 422 208 178 -30

EBITDA 117 64 34 10 -24

EBITDA margin 25.3% 15.2% 16.5% 5.9% -10.6%

OXO revenue 337 401 179 190 11

EBITDA 25 12 12 -1 -13

EBITDA margin 7.5% 3.0% 6.6% -0.3% -6.9pp.

'000 tonnes

GRUPA AZOTY KĘDZIERZYN

0

100

200

300

400

500

600

1H2016 1H2017

Fertilizers

VOLUMES

0

50

100

150

200

250

300

350

2Q 2016 2Q 2017

GRUPA AZOTY KĘDZIERZYN FINANCING SOURCES AT JUNE 30TH 2017

45

RATIOS 1H2016 1H2017

Net debt (PLNm) 140 219

12-month net debt/EBITDA (ratio) 0.57 1.60

90%

9% 1%

FINANCING STRUCTURE

210 62

AVAILABLE FUNDS

Corporate creditfacilities

Overdraft and multi-purpose facilities

* footnotes

(PLNm)

GRUPA AZOTY KĘDZIERZYN

SUMMARY

GRUPA AZOTY'S PRIORITIES

GRUPA AZOTY'S PRIORITIES

NEAR TERM

OPERATIONAL

PHASE

INNOVATION

Successful completion of the

Polyamides project

Securing funding for the project

Grupa Azoty Research and Development

Centre

Biotechnology

Innovations − services for precision

agriculture, plasticizers, catalysts, plastics.

SUMMARY

Corporate decisions:

- on the PDH project including PP production

plant

- on the coal gasification project once the

PREFEED stage is completed. Working with

Tauron on the project implementation

47

DISCLAIMER

48

The information presented below has been prepared by the Grupa Azoty Group (the “Group”) solely for the purpose of presentation to investors and market analysts on

August 24th 2017 (the “Presentation”). By participating in the meeting at which the Presentation is presented or by referring to this Presentation, you agree to the following

specific restrictions and disclaimers.

This Presentation does not constitute or form any part of, and should not be considered as, an offer to sell or as an invitation to subscribe for, or as a guarantee to purchase

or acquire in other way, any securities of any company of the Group. Neither this Presentation nor any part hereof may form the basis of, or be relied upon in connection

with, any subscription for any securities of the Group, or their acquisition. Neither this Presentation nor any part hereof may form the basis of, or be relied upon in

connection with, any investment agreement, commitment or decision relating to securities of the Group companies. This Presentation does not constitute a recommendation

regarding any securities of the Group companies.

No statement or assurance, expressed or implied, has been made by or on behalf of the Group or any of its shareholders, members of its bodies, officers, employees, agents

or advisers or any other person, as to the accuracy, completeness or reliability of information or opinions contained in this Presentation.

This Presentation may contain forward-looking statements. Forward-looking statements are different from statements of historical facts. Statements containing such words as

"expects", "intends", "plans", "believes", "anticipates", "will", "aims", "can", "would", "could", "continues" or similar words are examples of such forward-looking statements.

Forward-looking statements include statements about the financial performance, business strategy, plans and objectives of the Group (including development plans relating

to the Group). All forward-looking statements contained in this Presentation relate to matters involving known and unknown risks, issues that are impossible to predict, and

other factors. Actual results and achievements of the Group may be materially different from those described in statements concerning the past, and from the results and

achievements of the Group in the past.

Forward-looking statements are made based on various assumptions of future events, including numerous assumptions regarding present and future business strategies of the

Group and its future business environment. Although the Group believes that its estimates and assumptions are reasonable, they may prove to be incorrect. The information,

opinions and forward-looking statements contained herein are valid only on the date of this Presentation and are subject to change without notice. The Group and its

advisers are not obliged to publish any updates or modify any information, data or statements contained in this Presentation in the event of a change of strategy or the

intentions of the Group, or of facts or circumstances that will have an impact on the strategy or intentions of the Group, unless such an obligation arises under law. Please

note that the only reliable source of data on the Group's financial results, forecasts, events and indicators of the Group are the current and periodic reports released by the

Group as part of its disclosure obligations under Polish law.

Neither the Group nor any of its shareholders, members of its bodies, officers, employees, agents or advisers nor any other person shall be liable for any loss arising from the

use of this Presentation or its contents or otherwise arising in connection with this Presentation.

Neither the Group nor any of its shareholders, members of its bodies, officers, employees, agents or advisers nor any other person shall be required to provide the recipients

of this Presentation with any additional information or to update this Presentation.

This Presentation contains information on the chemical industry in Poland and globally, including information on market shares of the Company and some of its competitors.

The source of this information is always provided in this Presentation and the Group or any other entity acting on behalf of the Group has independently verified the

information referred to above.

This Presentation is not intended for distribution to or use by any person or any entity in any jurisdiction where such distribution or use would be contrary to local law or

oblige the Group or any of its affiliates to obtain an authorization or licence, or to comply with the registration requirements under applicable laws. Neither this Presentation

nor any part hereof may be copied or transmitted into the United States of America, and cannot be disseminated, directly or indirectly, in the United States of America.

Failure to comply with this restriction may constitute a violation of U.S. securities laws. Persons who come into possession of this Presentation are required to inform

themselves of, and to observe all of the above restrictions. None of the securities referred to herein

have been or will be registered under the U.S. Securities Act of 1933. Any such securities

may not be offered or sold in the United States of America, except pursuant to an exemption

or in a transaction not required to be registered under the Act.

Thank you for your attention.For more information, visit www.grupaazoty.com

APPENDIX 1 THE PARENT

GRUPA AZOTY S.A.: FINANCIAL HIGHLIGHTS

51

436 357 366 393 479377

1Q 2016 2Q2016 3Q2016 4Q2016 1Q2017 2Q2017

REVENUE

56

-7

5 11

8659

12.8%

-2.0% 1.4%

2.8%

18.0%15.6%

1Q 2016 2Q 2016 3Q 2016 4Q 2016 1Q2017 2Q2017

EBITDA

EBITDA(adjusted)*

EBITDAMARGIN

(PLNm)

22

236

-17 -16

45

283

-37

-19 51

5.0%

66.1%

-4.6%-4.1%

9.4%

75.1%

-50

50

150

250

1Q 2016 2Q 2016 3Q 2016 4Q 2016 1Q2017 2Q2017

NET PROFIT

NET PROFIT(adjusted)*

NET PROFITMARGIN

* NET PROFIT was adjusted for dividends received (in all periods).

** Restated following application of uniform accounting policies across the Grupa Azoty Group

GRUPA AZOTY S.A.

793

856

1H2016 1H2017

49

145

1H2016 1H2017

258328

-15

96

1H2016 1H2017

0

100

200

300

400

Nitrogen fertilizers

1H2016 1H2017

GRUPA AZOTY S.A.: FERTILIZERS

VOLUMES

GRUPA AZOTY S.A. 52

(PLNm) 1H2016 1H20172Q

2016

2Q

2017

Change

Q/Q

Segment revenue

including344 333 126 121 -4%

Nitrogen fertilizers, 310 296 110 102 -7%

EBITDA 40 43 -9 1 111%

EBITDA margin 12% 13% -7% 1% +8pp

0

50

100

150

Nitrogen fertilizers

2Q2016 2Q2017

'000 tonnes

0

5

10

15

20

25

30

Polyamide Caprolactam

2Q2016 2Q2017

0

10

20

30

40

50

60

Polyamide Caprolactam

1H2016 1H2017

GRUPA AZOTY S.A.: PLASTICS

VOLUMES

GRUPA AZOTY S.A. 53

(PLNm) 1H2016 1H20172Q

2016

2Q

2017

Change

Q/Q

Segment revenue

including423 488 217 233 7%

Polyamide 306 236 156 110 -29%

Caprolactam 22 151 12 73 508%

EBITDA -2 87 -3 50 1 767%

EBITDA margin -0.5% 18% -1% 21% +22pp.

'000 tonnes

Increase since June 30th 2008: 328%

High (Dec 8 2015) PLN 113.00

Low (Feb 3 2009) PLN 6.00

SHARE PERFORMANCE

GRUPA AZOTY S.A.

60

62

64

66

68

70

72

74

76

78

80

0

50

100

150

200

250

300

350

400

450

Jan-17 Jul-17Volume Price

54

APPENDIX 2

MARKET PRICES

PRICES OF AMMONIA, AMMONIUM SULFATE AND CALCIUM AMMONIUM NITRATE

100

150

200

250

300

50

150

250

350

450

550

Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017EUR/tUSD/t

Ammonia USD/t Ammonium sulfate AS USD/t Calcium ammonium nitrate CAN EUR/t

56

NATURAL GAS PRICES

10

15

20

25

30

Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017

EUR/MWh

PGNiG tariff TTF DA net of transmission costs EEX GPL DA net of transmission costs

57

PRICES OF BENZENE, PHENOL, CPL, PA6

250

750

1 250

1 750

2 250

Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017

EUR/t

Benzene Liquid caprolactam PA6 Phenol

58

150

200

250

300

100

200

300

400

Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017USD/t

EUR/t

Ammonium nitrate EUR/t UAN EUR/t Urea USD/t

PRICES OF AN, UAN AND UREA

59

MELAMINE AND CAPROLACTAM PRICES

1000

1400

1800

2200

1300

1400

1500

Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017USD/tEUR/t

Melamine EUR/t Crystalline caprolactam USD/t

60

PRICES OF NPK, DAP, PHOSPHATE ROCK, POTASSIUM CHLORIDE

50

150

250

350

450

550

Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017

USD/t

NPK DAP Phosphate rock Potassium chloride

61

PRICES OF TITANIUM WHITE, ILMENITE AND TITANIUM SLAG

0

100

200

300

400

500

600

700

800

1900

2000

2100

2200

2300

2400

Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017

USD/tEUR/t

Titanium white EUR/t Ilmenite USD/t Titanium slag USD/t

62