Embed Size (px)

Citation preview

CODA FINANCIALSUSER GUIDE

PPB Property Development Sdn Bhd

GUIDE TO GST APPLICATION AND APPROACH

CODA FINANCIALS

Yap Bee YongFebruary 2015

Coda Financials – user guide page 1

GST in CODA

This guide explains the approach adopted to GST in our specific accounting environment.

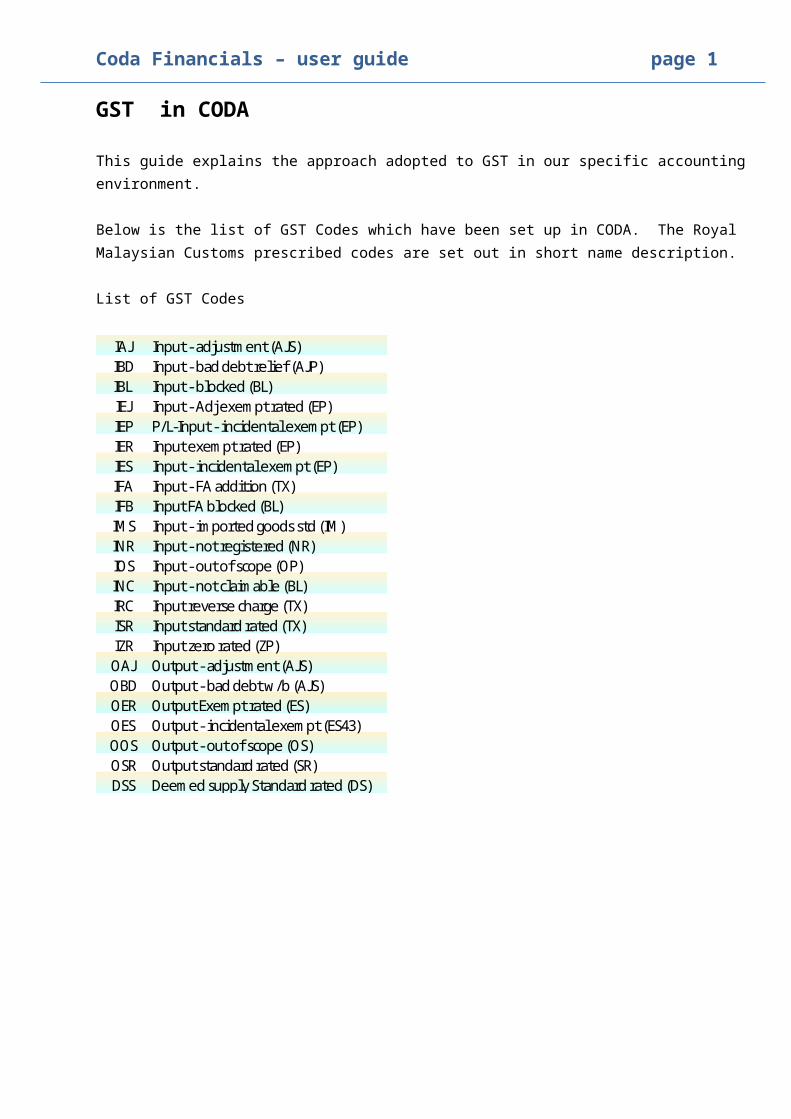

Below is the list of GST Codes which have been set up in CODA. The Royal Malaysian Customs prescribed codes are set out in short name description.

List of GST Codes

IAJ Input - adjustment (AJS)IBD Input - bad debt relief (AJP)IBL Input - blocked (BL)IEJ Input - Adj exempt rated (EP)IEP P/L-Input - incidental exempt (EP)IER Input exempt rated (EP)IES Input - incidental exempt (EP)IFA Input - FA addition (TX)IFB Input FA blocked (BL)IMS Input - imported goods std (IM)INR Input - not registered (NR)IOS Input - out of scope (OP)INC Input - not claimable (BL)IRC Input reverse charge (TX)ISR Input standard rated (TX)IZR Input zero rated (ZP)OAJ Output - adjustment (AJS)OBD Output - bad debt w/b (AJS)OER Output Exempt rated (ES)OES Output - incidental exempt (ES43)OOS Output - out of scope (OS)OSR Output standard rated (SR)DSS Deemed supply Standard rated (DS)

Coda Financials – user guide page 2

Besides this please note there are some standard terms adopted in the CODA financials environment to cater for indirect taxes.

Each posting document has 3 types of lines. These are1) Summary – this line normally carries the value of total invoiced value inclusive of GST (normally the AP

or AR line)2) Analysis – this line normally corresponds with the purchased or sold item(acquisition or supply). The

value of the acquisition or supply WITHOUT GST.3) Tax – this line would be the line that is posted to the GST accounts in the B/S or P/L and carries the

pure tax value of the acquisition or supply.There are also 3 types of values. These are

4) Document value – the amount posted in any document5) Tax turnover – the value that is reported value for GST purposes – ie it is the value of the acquisition

or supply WITHOUT GST6) Tax value – this would be the value of GST posted

There are also several accounts in the balance sheet put aside for GST. These are GST Payable SR 3600GST Payable ZR 3601GST Payable ER 3602GST Payable OOS 3603GST Receivable SR 2600GST Receivable ZR 2601GST Receivable ERGST Receivable OOS/Not reg

26022603

For the disallowed items (meaning the blocked GST, deemed supply GST and not claimable GST), the GST cost will either be re-grossed into the expenditure, or written off to the P/L

4 1,2,3 56

Coda Financials – user guide page 3

The accounts codes are hard coded to the GST codes selected. Below is the table of not recoverable GST.Code Name (36 characters) Recoverable

IBL Input - blocked (BL) Not recoverable Goods line accountIEP P/L-Input - incidental exempt (EP) Not recoverable Goods line accountIFB Input FA blocked (BL) Not recoverable Goods line accountINC Input - not claimable (BL) Not recoverable 8221.DE011DSS Deemed supply Standard rated (DS) Fully 3600 8222.DE011

Account Code

Goods line account in CODA means that the GST amount will follow the original expense code. “Fully recoverable” for deemed supply is for the Credit of 3600 account.

8221 & 8222 are for those expenditure which are not claimable for income tax purposes and therefore would be additional work for users if they were to be defined as “goods line account”.

Also, the CODA set up is such that the creation of the 3 line types is only possible if one and only one line is Dr or Cr to a AP or AR account.

General PrinciplesA simple double entry for purchase of standard rated item would beCr Creditor A RM106Dr Expense RM100, GST Code ISR

Note that the double entry doesn’t balance by Rm6/- which is the GST value embedded in the purchase cost of RM106/-To complete the double entry user would need to click “generate tax”(in green circle). CODA will then create the last entry which is Dr GST receivable The last line is created according to account code set up, the 6 % computed and posted to the GST account.

Coda Financials – user guide page 4

You will note that account code 2600 GST receiveable has 2 values – the actual value of RM6/- posted as well as the tax turnover value. This will enable our preparation of the GST 03 form later as we will have the value of standard rated acquisitions (tax t/o) to value of GST receivable.

The summary and analysis lines have been defaulted and hidden in the online data entry screen. However users will need select this for CODA XL journal uploads. However tax value, tax doc value & other values have been defaulted for you.

Post Actual No Account Code Description Debit Credit Line Type Tax Code Tax Line Code Inclusive/Exclusive Tax Value Tax Doc Sum Tax TurnoverPost 35 8030.DE008 Medical exp Jan15 600.00 Analysis IBL Exclusive 36.00Post 35 4000.CK001 636.00 Summary 36.00Post 36 4000.CB001 530.00 Summary 30.00Post 36 8101.DE001 500.00 Analysis IBL Exclusive 30.00

Tax generation will still need to be done in CODA and can be accessed after posting to intray.

Automated

Coda Financials – user guide page 5

In certain cases (eg Zero rated GST payable), the actual value posted against the account code (2601) will be RM0/- however the tax turnover will be accumulated against that account code 2601 to enable easy extraction & reporting later.

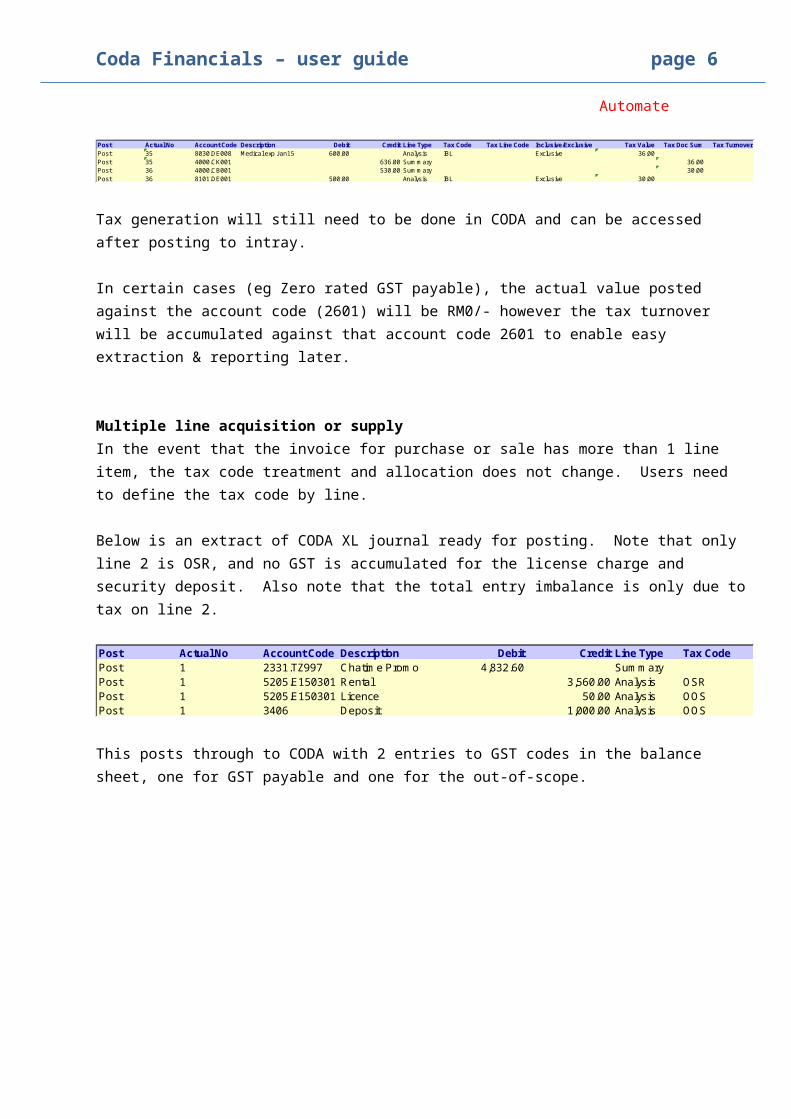

Multiple line acquisition or supplyIn the event that the invoice for purchase or sale has more than 1 line item, the tax code treatment and allocation does not change. Users need to define the tax code by line.

Below is an extract of CODA XL journal ready for posting. Note that only line 2 is OSR, and no GST is accumulated for the license charge and security deposit. Also note that the total entry imbalance is only due to tax on line 2.

Post Actual No Account Code Description Debit Credit Line Type Tax CodePost 1 2331.TZ997 Chatime Promo 4,832.60 SummaryPost 1 5205.E150301 Rental 3,560.00 Analysis OSRPost 1 5205.E150301 Licence 50.00 Analysis OOSPost 1 3406 Deposit 1,000.00 Analysis OOS

This posts through to CODA with 2 entries to GST codes in the balance sheet, one for GST payable and one for the out-of-scope.

The same would occur for other tax codes, and purchase invoice.

Coda Financials – user guide page 6

Reverse charge GSTReverse charge GST is a special scenario where we need to create the output and input tax at the same time.For our set up in CODA, this has been created as tax code IRC.

For example a purchase of service form Singapore for RM1000/- value would trigger input and output tax of Rm60/- each.

The data entry would look like this

Theoretically the document is already balanced without any GST. However we need to create the reverse charge entries and to do so, we need to define tax code as IRC.

Coda Financials – user guide page 7

Looking at the full entry both the input and output tax accounts have been debited and credited respectively and the tax turnover recognised correctly as Dr or Cr.

Coda Financials – user guide page 8

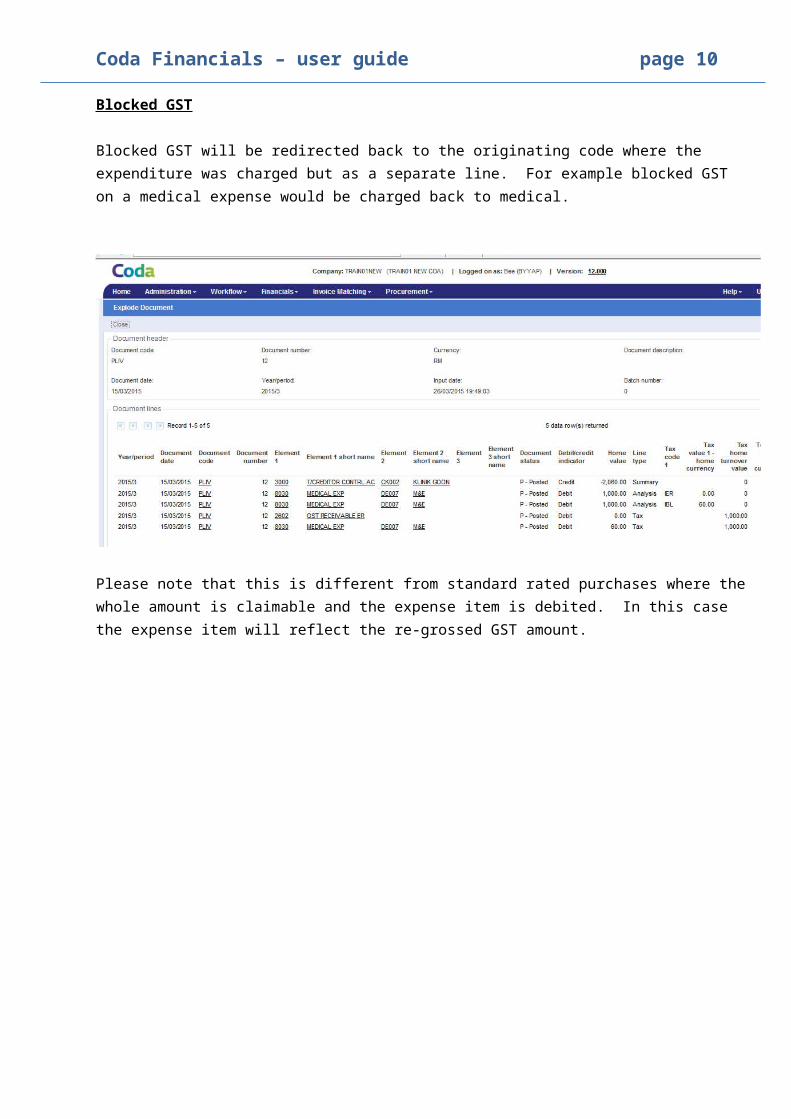

Blocked GST

Blocked GST will be redirected back to the originating code where the expenditure was charged but as a separate line. For example blocked GST on a medical expense would be charged back to medical.

Please note that this is different from standard rated purchases where the whole amount is claimable and the expense item is debited. In this case the expense item will reflect the re-grossed GST amount.

Coda Financials – user guide page 9

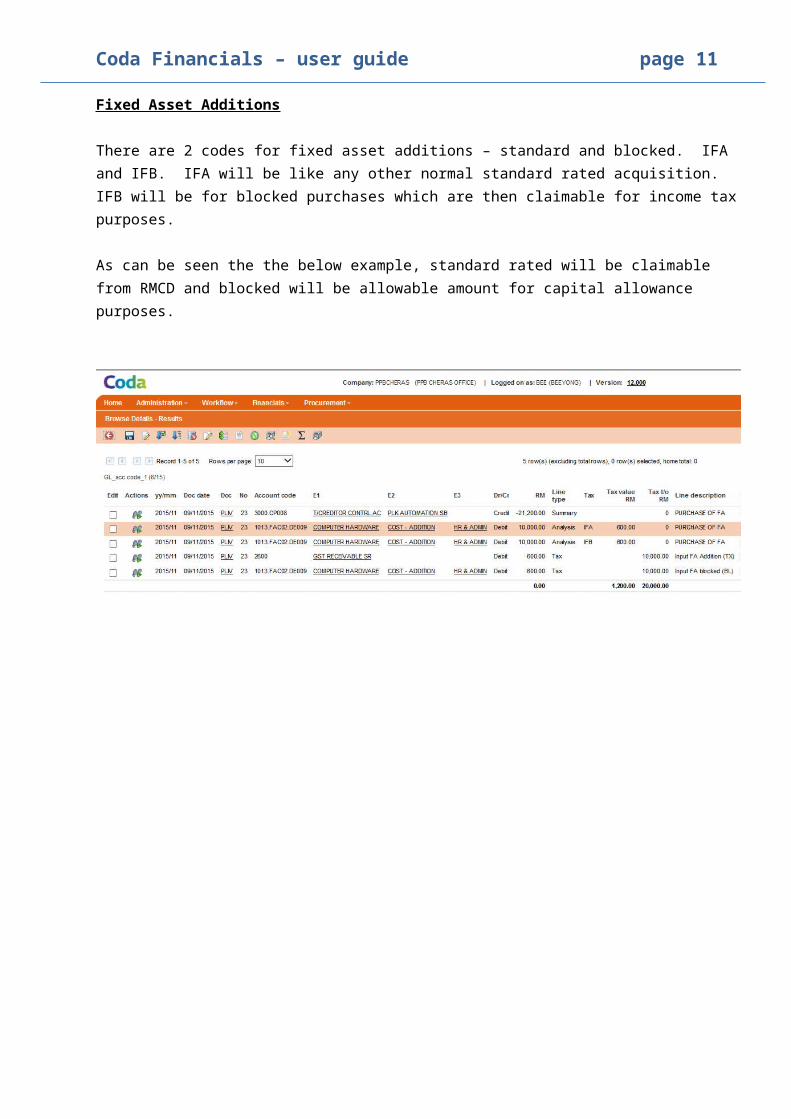

Fixed Asset Additions

There are 2 codes for fixed asset additions – standard and blocked. IFA and IFB. IFA will be like any other normal standard rated acquisition. IFB will be for blocked purchases which are then claimable for income tax purposes.

As can be seen the the below example, standard rated will be claimable from RMCD and blocked will be allowable amount for capital allowance purposes.

Coda Financials – user guide page 10

Non Recoverable GST

In general, input tax which is not claimable from RMCD should be a deductible expense under the ITA. However where we choose not to claim (for whatever reason), this is not deductible under the ITA. It is currently not clear if this includes invoices which we find are not claimable for GST purposes (eg invoices which are a bit irregular, like wrong payee name, no total amount chargeable to GST or any other missing elements). We have created a specific tax code “Input not claimable” (INC) for this. Any GST on any purchases charged to INC will be expensed to account coda “GST – not claimable”, instead of being regrossed in the specific expenditure account.

The above entry demonstrates the effect of an entry coded as INC whereby the GST is posted to a separate “GST not claimable” account instead of designated to the account where the expense was origianlly charged.

The second type of unclaimable GST is for deemed supply which is detailed in the next page

Coda Financials – user guide page 11

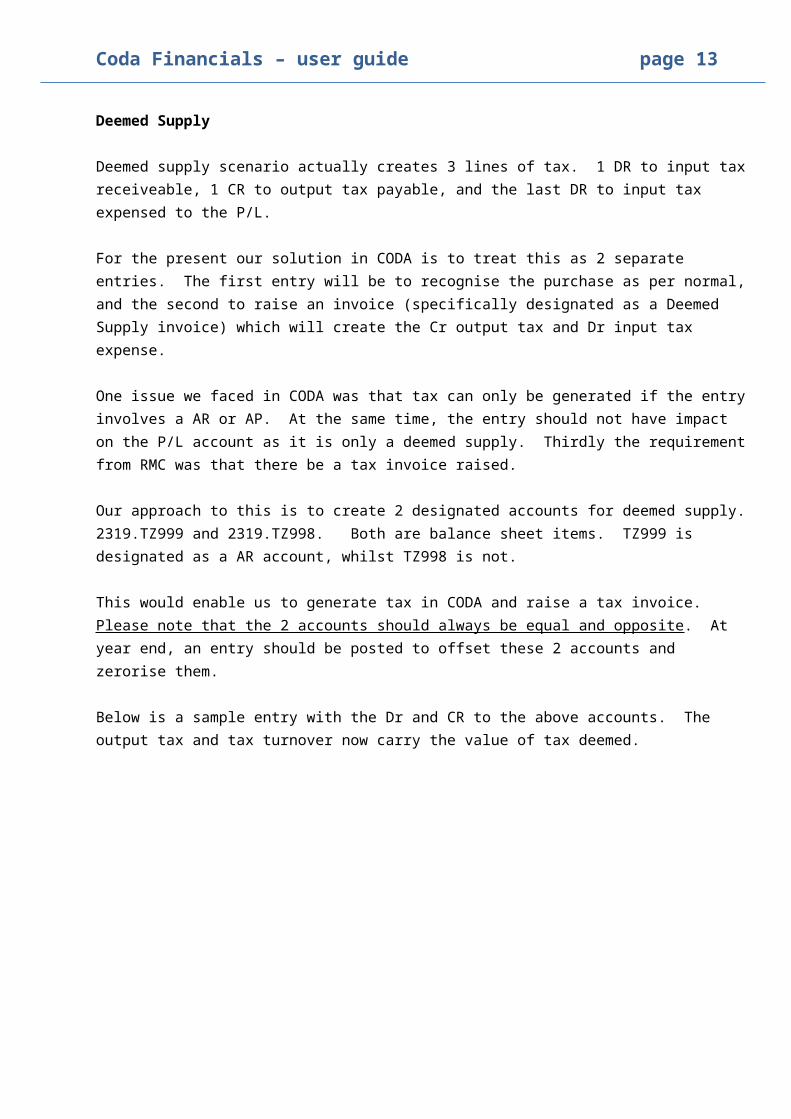

Deemed Supply

Deemed supply scenario actually creates 3 lines of tax. 1 DR to input tax receiveable, 1 CR to output tax payable, and the last DR to input tax expensed to the P/L.

For the present our solution in CODA is to treat this as 2 separate entries. The first entry will be to recognise the purchase as per normal, and the second to raise an invoice (specifically designated as a Deemed Supply invoice) which will create the Cr output tax and Dr input tax expense.

One issue we faced in CODA was that tax can only be generated if the entry involves a AR or AP. At the same time, the entry should not have impact on the P/L account as it is only a deemed supply. Thirdly the requirement from RMC was that there be a tax invoice raised.

Our approach to this is to create 2 designated accounts for deemed supply. 2319.TZ999 and 2319.TZ998. Both are balance sheet items. TZ999 is designated as a AR account, whilst TZ998 is not.

This would enable us to generate tax in CODA and raise a tax invoice. Please note that the 2 accounts should always be equal and opposite. At year end, an entry should be posted to offset these 2 accounts and zerorise them.

Below is a sample entry with the Dr and CR to the above accounts. The output tax and tax turnover now carry the value of tax deemed.

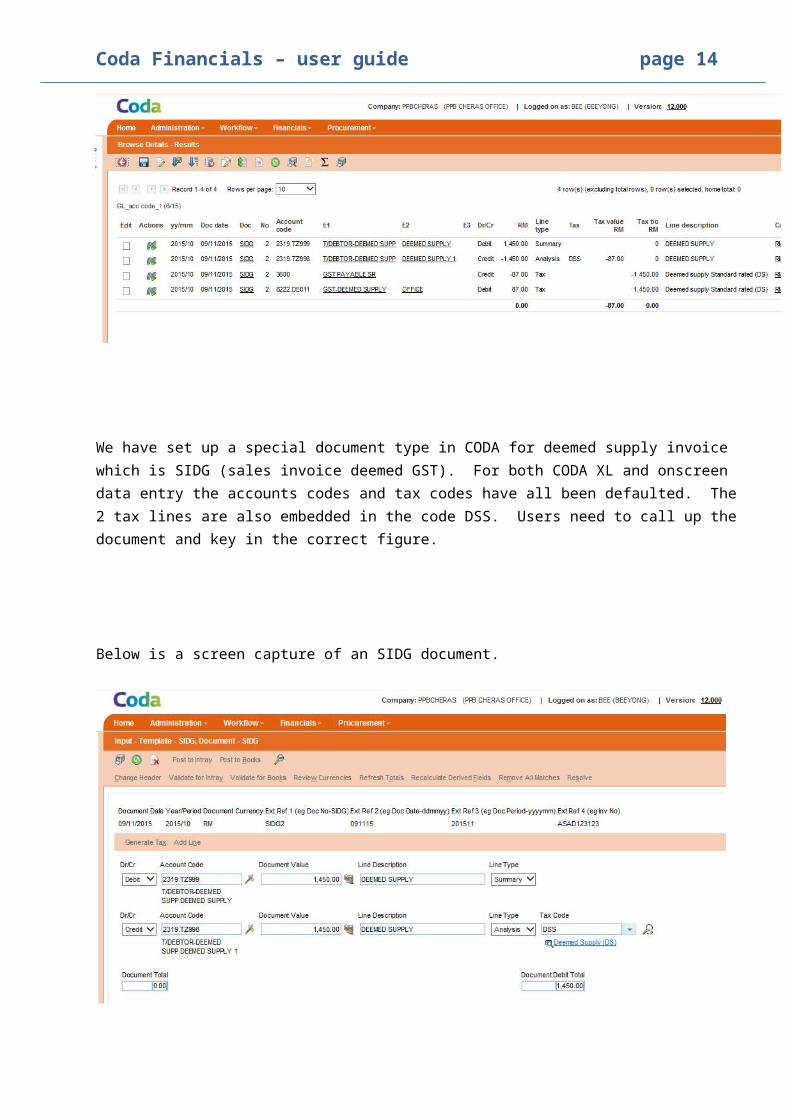

We have set up a special document type in CODA for deemed supply invoice which is SIDG (sales invoice deemed GST). For both CODA XL and onscreen data entry the accounts codes and tax codes have all been defaulted. The 2 tax lines are also embedded in the code DSS. Users need to call up the document and key in the correct figure.

Coda Financials – user guide page 12

Below is a screen capture of an SIDG document.

Coda Financials – user guide page 13

Reimbursement versus DisbursementsThe usage here of the terms “reimbursment” & “disbursement” were as per defined by the RMCD

The following is extracted from the RMCD’s General Guide on GST dated 16th March 2015“296. Registered person may incur expenses and subsequently recover the expenses from their customers. The GST treatment for the recovery of such expenses depends on whether those expenses are acquired by such registered person as a principal or an agent. 297. Any recovery of an expense a registered person have “incurred in the course or furtherance of business” from another party is treated as a reimbursement. The recovery of the expenses from another party is a separate supply and is subject to GST. Registered person is acting as a principal in acquiring the goods and services if he himself contract with the supplier in his own capacity and since these supplies are “incurred in the course or furtherance of business”.

298. A recovery of a payment the registered person “incurred as agent” for another party is treated as a disbursement. Such recovery is incurred by a registered person in his capacity as a paying agent on behalf of another party in order to discharge its payment obligation. Such registered person does not have the legal obligation to pay for the goods or services or a party to a contract and discretion to alter the nature or value of supplies made between his customer and the third party supplier but are authorized by his customer to make payment to the supplier on his behalf. Since he is only the paying agent, no supply was made by him. Such recovery of expenses under disbursement does not constitute a supply and is not subject to GST. As such, input tax can be claimed on the subsequent reimbursement by the other party. “

A) Based on current company set up in CODA the following are the scenarios for reimbursement1) Management fees, accountancy fees2) Staff expenses & recovery of costs from project, eg travel, parking, meals, allowances3) Office expenses which are billed to the different company from which the expense originates. (eg

telephone bills in the name of PPB Hartabina but which should be for PPB PD.

B) The following are scenarios for disbursements1) Transfers of funds between 2 companies2) One company using another company’s cash to pay for its own expenses. (Eg PPB PD makes payment

for SMD expenses whereby the invoices are in SMD name)

ReimbursementsInterco Account Code

1) Management fees/Accountancy fees - for companies within CODA

Each side (billing party & receiving party) to raise separate documents to recognise income (SIWG) and expense (PLIV) with GST codes. As these are companies, not creditors/debtors, we will need to use the “deemed supply” debtor to generate the tax line in CODA.

No 2300 & 3000

- for companies where counterparty is not in CODANormal entries either SIWG alone or PLIV alone in just that one party

N/a 2300 or 3000

2) Staff expenses/recovery of costs from project- for companies within CODA- see double entry below

Yes 2501

3) Office expenses/recoveriesAs 2) above Yes 2501

2) Double entry for recoverable expenses / “reimbursements”

Coda Financials – user guide page 14

Originating company “owns” the expense as the tax invoice is in its name, or is due to its employee.Originating company will recognise the expenses/input tax receivable in its books. Originating company needs to create a tax invoice to pass the cost to the recipient company

Double entry will beSending company books

Dr Recoverable, Dr Input tax, Cr Cash or CreditorTo recognise the incoming cost (a)Dr Interco, Cr Recoverable, Cr Output tax payable To recognise the billing to the recipient (b)

Receiving companyDr Expenses, Input tax, Cr Interco To recognise the invoice from sending company on costs (c)

Auto entry using disbursements account/CODA interco functionIn Sending company booksDr Destination (IRSDxxxx) ExpenseDr Destination (IRSDxxxx) tax (d)Cr Self Cash/CreditorDr Input tax (e)Cr Output tax (f)

TO NOTE THAT WHERE POSTING INTERCOMPANY JOURNALS WITH MANUAL GST PLEASE BE MINDFUL TO FILL UP ALL THE FIELDS INCLUDING TAX TURNOVER AS THIS INFO IS REQUIRED FOR GST REPORTING

Coda Financials – user guide page 15

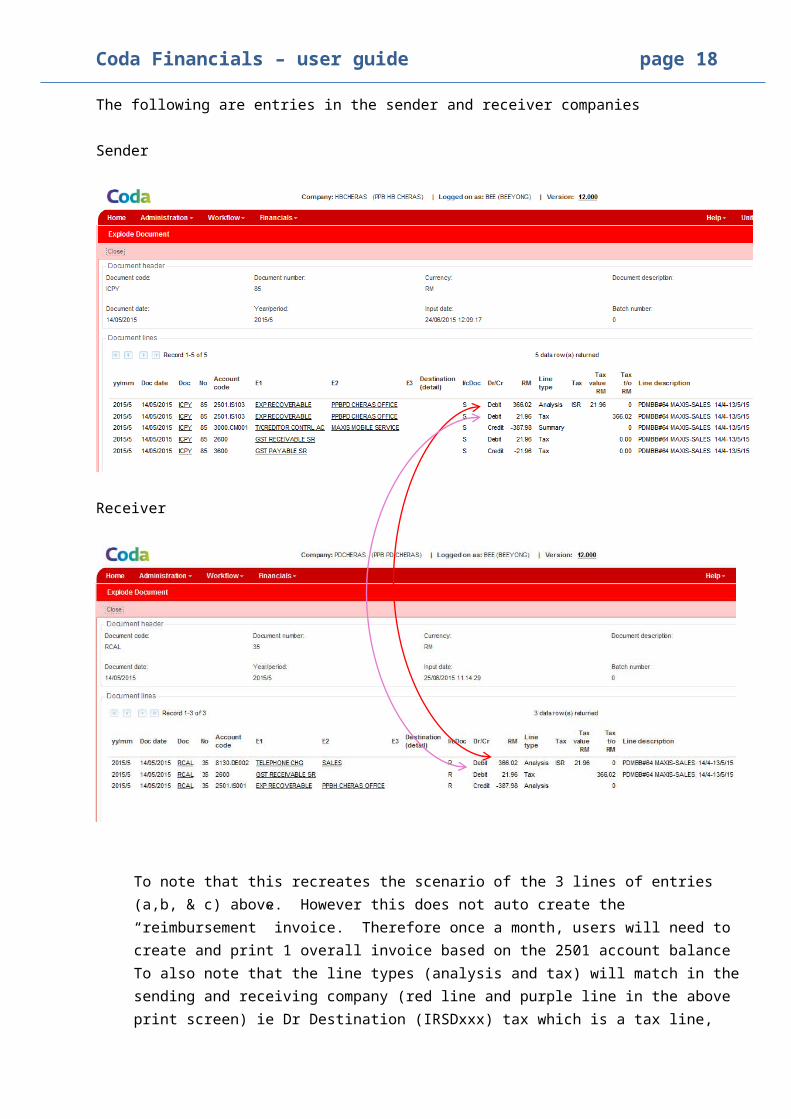

The following are entries in the sender and receiver companies

Sender

Receiver

To note that this recreates the scenario of the 3 lines of entries (a,b, & c) above. However this does not auto create the “reimbursement” invoice. Therefore once a month, users will need to create and print 1 overall invoice based on the 2501 account balanceTo also note that the line types (analysis and tax) will match in the sending and receiving company (red line and purple line in the above print screen) ie Dr Destination (IRSDxxx) tax which is a tax line, would give rise to a tax line in SENDER company books too under account code 2501. In the receiving company the 2501 account will only take up as 1 analysis line, but the expense and tax lines themselves will be split respectively.

Coda Financials – user guide page 16

B) DisbursmentsDisbursement entries will not carry GST. The most common scenario for disbursements in our current set up would be where 1 company (for example SMD) receives an invoice in its name (SMD name) and uses another company (eg PPBHartabina) to fund this purchase.

Disbursement interco will flow through as a 2903 account code & interco destination is ICXXXX

Below is an example of disbursement entry posted

Sending

Receiving

Coda Financials – user guide page 17

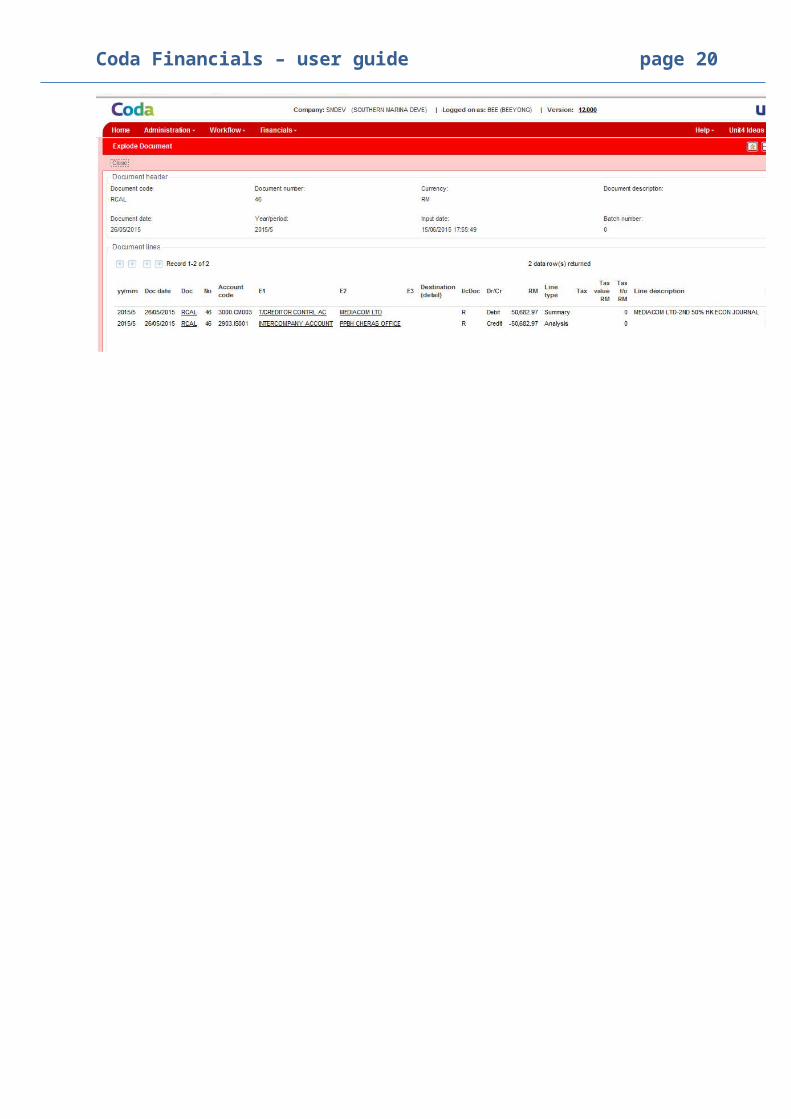

C) Interbranch

A scenario unique to our set up is that we have set up as separate companies in CODA each mall and development project. This is to ensure clear segregation of assets and liabilities as well as P/L.

The bank accounts are centralised at the 2 offices (in Cheras & Penang) and therefore would entail the use of interco function to recognise settlement entries. These entries would be posted through account code 2904 & destincation “ICXXXXX”.

The summary, analysis and tax line posting would be similar to disbursements scenario in CODA. The main difference is that the entries are technically within the same legal entity.

Sending

Receiving

Coda Financials – user guide page 18

Mixed supplier

Applicable to development projects which have commercial property as well as residential1) Input tax incurred and which is directly attributable to the development of residential properties

(exempt supplies) cannot be claimed and will be classified as exempt. 2) Input tax incurred on commercial property can be claimed as normal.3) Input tax incurred on both commercial and residential property has to be apportioned.

As a basic setting, the construction costs and other related account codes in relation to the project will be subanalysed at element 2 to the respective project components (eg Tower 1, Tower 2, retail block). There will be an element code for “shared” (non allocatable) expenses.

Another addition will be that in line with other project development expenses – which are maintained in the balance sheet & transferred to P/l as revenue is recognised, there will be an additional designated code for GST under this range which is account code 1681.

Tax codes for output tax will not change. However input tax codes will be expanded to 4 characters with the last character designating the division. So ISR for Tower 1, Tower 2, Tower 3, Shared, and Admin will be ISR1, ISR2, ISR3, ISRS, and ISRA respectively. ISR code is applicable regardless of whether the particular construction is commercial (& therefore standard rated) or exempt supply (eg residential). However please note that there is a difference in the description for each code. For example if Tower 1 is residential then ISR1 will actually be titled “Input Expt Supply (TX-N43)” and defaulted to code 1681.DV001. And if Tower 2 is commercial ISR2 will be titled “Input SR (TX)” and defaulted to code 2600 (input tax receivable). The actual allocation to the respective accounts is already hard-coded by tax code. This is to ensure consistency in coding of tax code as well as consistency in reporting.

Shared and admin codes - ISRS and ISRA will also be defaulted to 1681. The customs assigned code for these will be different as these will be TX-RE. Please also note that admin costs are always designated as TX-RE as admin costs cannot be directly attributable to a particular tower, as any running costs should be coded to project costs code in the balance sheet.

The coding convention will continue along this line. Reverse charge (IRC) will be expanded to IRC1,2,3, S, & A. The default account codes/customs codes will be incorporated into the individual divisions. This would ensure a consistent coding structure throughout and also not require users to be overly concerned over whether the item is incidental exempt or standard rated.

Coda Financials – user guide page 19

Below is a posting using codes ISR1, ISR2, and ISRS where Tower 2 is a commercial tower, whilst Tower 1 is residential.

Below is a posting for reverse charge with allocation to division.

Total output tax is RM480/- and is a combination of line 5 & 7. Tax turnover on output tax is RM8000/-

Coda Financials – user guide page 20

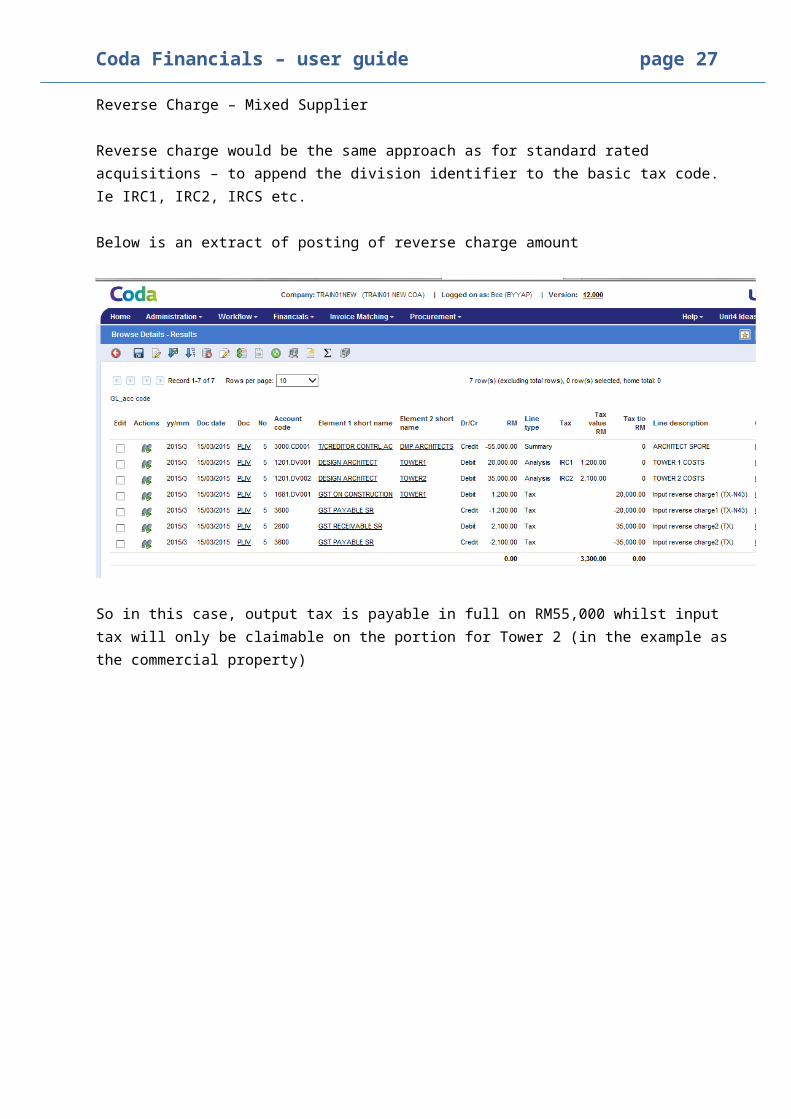

Reverse Charge – Mixed Supplier

Reverse charge would be the same approach as for standard rated acquisitions – to append the division identifier to the basic tax code. Ie IRC1, IRC2, IRCS etc.

Below is an extract of posting of reverse charge amount

So in this case, output tax is payable in full on RM55,000 whilst input tax will only be claimable on the portion for Tower 2 (in the example as the commercial property)

Coda Financials – user guide page 21

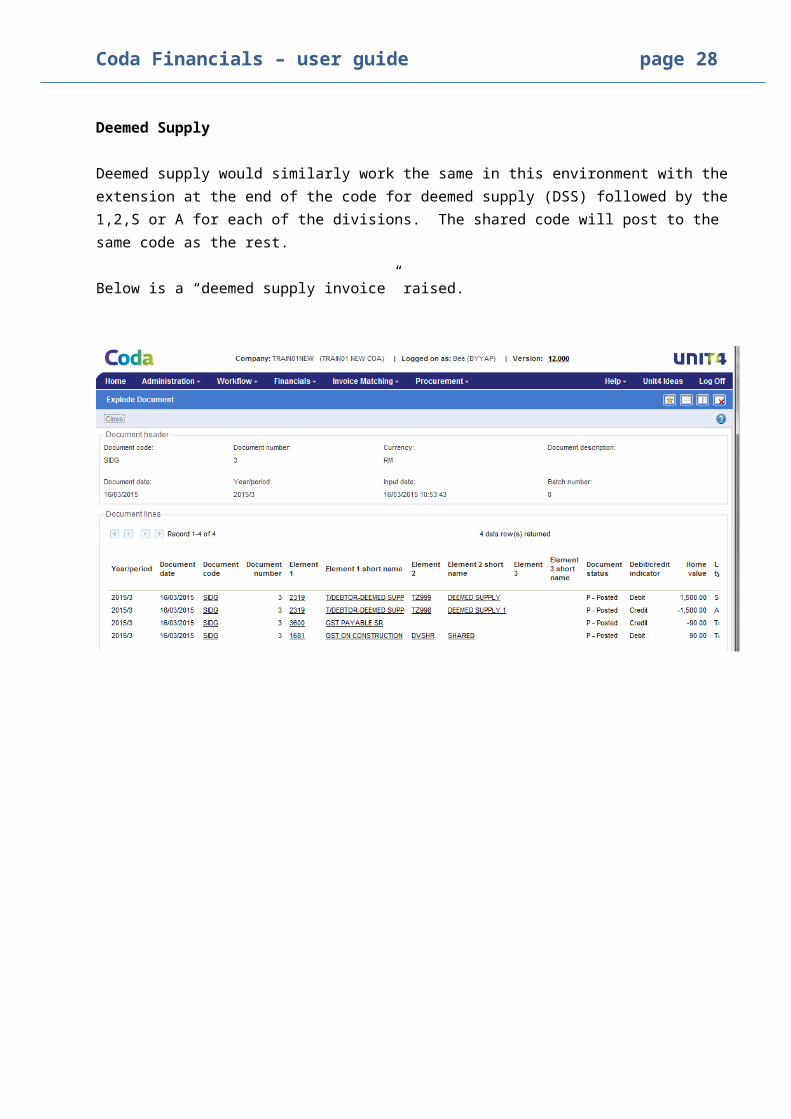

Deemed Supply

Deemed supply would similarly work the same in this environment with the extension at the end of the code for deemed supply (DSS) followed by the 1,2,S or A for each of the divisions. The shared code will post to the same code as the rest.

Below is a “deemed supply invoice” raised.

Coda Financials – user guide page 22

Adjustment for allocation of GST on common costs to exempt and non exempt accounts

This is a manual adjustment in CODA. Over the course of the month each of the individual “divisions” being the respective development phase and block, will start accumulating GST. One division will be the common costs division – where costs are not directly attributable and therefore the GST on it.

At month end closing, one of the month end processes for a mixed supplier would be the computation of GST expense between the individual divisions in CODA. (For Southern Marina the basis – pending approval - will be Gross Floor Area)

Tax codes for adjustments are ASR1, ASRA2, ASRA3, ASRAS and ASRAA (customs code TX-RE).

In order to create a “tax” line type we need to create an entry with a supplier code. We adopted the same approach as for “deemed supplier” of having 2 equal and opposite accounts but only 1 designated as AR.

Assuming Tower 1 is residential & therefore the GST not claimable, and Tower 2 is commercial & therefore GST claimable. Assuming the computed split of common construction costs between Tower 1 & Tower 2 is Rm700, and Rm800 respectively. We would Cr out the total common costs of RM1,500 from 2302.DVSHR, and debit RM700 to Tower 1 and to Tower 2 RM800 with codes ASRA1, & ASRA2..

The end result is that the Shared division is zerorised. Also RM48/- is added to GST receivable with tax turnover of RM800/-.

Knock off each other. Raised to trigger tax lines only

Coda Financials – user guide page 23

Admin expenses

The initial entries for admin expenses are similar to that for construction cost shared account except that the GST tax code is ISRA. This is to enable easy reversal and clearance of account later.

For admin expenses in a developer company, the GST apportionment is more complex in terms of management. This is because the admin expenses are already by department. We also cannot afford to do a line by line reversal of all GST costs.

We have created a general reversal account under the admin exps series “8999”, and two element 2 “DE999 for reversal shared, DE998 for allocation.

The total of 8999 will always be zero.

Below is a screenshot of the initial entry and month end entry.

Coda Financials – user guide page 24

The end result is that GST SR will accumulate the RM12, with RM200 as Tax Turnover, and GST expensed to P/l via construction cost = RM48.

The argument as to why the GST is expensed via construction is that if it was not for the construction project of residential property in the first place, this GST expense would have been 100% claimable. This disallowed cost is therefore related to the construction process.

Coda Financials – user guide page 25

Reporting

We have not created a “GST03” form format in CODA. However, each field in the GST03 form can be extracted by a combination of account code, tax type and even document type.

Below is an extract of “tax” lines per posting, but GST account. This is specifically for account codes GST payable Standard rated (3600). Total RM value charges to GST Payable account = RM4,2630.60 and total value of standard rated supplies = RM70,510.00. The GST payable amount is 6% of the standard rated supply. The list of documents raised is also traceable and identifiable by document type.

Coda Financials – user guide page 26

The extract below shows totals for Standard Rated Acquisitions (RM2,256/- tax versus RM37,600 total value of SR acquisitions), and for Exempt Rated Acquisitions of RM1,900/- with RM0/- tax.

Coda Financials – user guide page 27

GST REPORTING / GST 03 FORM

We have set up a worksheet format to extract the information for GST reporting in CODA XL. There are 2 forms – The main form to pick up most of the entries (via tax line) and one for fixed asset purchases only (capital acquisitions).

Due to our splitting of the various companies in CODA by mall/projection/line of business, we would need to pull together a few CODA companies to create 1 legal entity. This is done by creating “Group” of companies representing the legal entity. We have 4 reporting legal entities in CODA - ie PPB Group, PPB Hartabina, PPB PD, and SMD .Within these are clustered the various operating entities.

The following is a screen shot of our GST extraction which extracts the tax line only.

Coda Financials – user guide page 28

This is accompanied by the recon page below which extracts the total from the previous sheet (using dynamic range functionRecon For the year 2015 1.5.2015

For the month 05Element total RM Total tax t/o

3600 GST Payable SR (184,801.03) (3,083,901.04) 6%3601 GST Payable ZR 0.00 0.00 0%3602 GST Payable ER 0.00 (64,438.71) 0%3603 GST Payable OOS 0.00 (241,659.61) 0%2600 GST Receiveable SR 36,412.79 606,879.56 6%2601 GST Receiveable ZR 0.00 0.00 0%2602 GST Receiveable ER 0.00 1,830.24 0%2603 GST Receiveable OOS 0.00 124,866.71 0%1681 GST on Cost of Construction 0.00 0.00 0%8000 8999 Expensed 0.00 0.00 0%2903 2904 Disbursements 75.73 12,325.98 1% Low % due to recovery of expenses before 1 Apr 20152501 Reimbursements 0.00 0.00 0%

Total by tax code (148,312.51) (2,644,096.87)

Total per worksheet (148,312.51) (2,644,096.87)

There is another sheet to extract Fixed asset addition (based on E2 code for additions). This is not tax line purchaes.

Group of Companies

Company code

Year/period fm

Year/period to

Element 1 fm

Element 1 to

Doc code

PPB 2015/05 2015/05 1001 1019

Company code Year/period Doc date Doc code No Element 1 Element 1 Details Description Tax code RM Tax T/O (RM) Ext Ref 1 Ext Ref 2 Ext Ref 3 Ext Ref 4 User

PPBTWA 2015/5 11.05.2015 RCAL 41 1016 PLANT & MACHINERY ROSTAN-KDK CEILING FAN INV#POS/01178ISR 165.00 0.00 ICPC2 110515 201505 P164/05 YTLEE

Books

The final GST -03 form extraction is from a combination of both sheets.