Embed Size (px)

Citation preview

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

1

PM & Partner Marketing Consulting GmbH (PM&P)Frankfurt | Munich | Berlinwww.pm-p.de

GROWING TUNISIA‘S AUTOMOTIVE INDUSTRY:

A STUDY ON THE FURTHER DEVELOPMENT

OF TUNISIA‘S AUTOMOTIVE ECOSYSTEM

Pre-Final Report – January 2017

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

2PM&P | PROFILE

PM & Partner Marketing Consulting GmbH (PM&P) is an independent consulting firm, consisting of marketing

professionals and market research analysts. The company provides strategic and operative support in marketing

and business development to industrial companies, as well as to investment promotion institutions.

Founded: 1974

Professionals: 18

Offices : Frankfurt – Munich - Berlin

PM&P is part of a worldwide network of independent Consulting and Market Research companies.

PM&P is divided into 3 areas of activity:

www.pm-p.de

REGIONAL DEVELOPMENT

MARKETING CONSULTING

MARKET RESEARCH

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

3

METHODOLOGY

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

4METHODOLOGY | OVERVIEW

* Investment Promotion Agencies

Inception MeetingDiscussing the project with relevant stakeholders within this project

Analysis of OEM-OpportunitiesDeveloping a realistic understanding of the opportunities of locating OEMs to Tunisia

Supplier AnalysisThe core of the study –analyzing the current structure of automotive suppliers and potential gaps.

Technology Trends changing Supply ChainsAnalysing changes in the automotive industry and their impact on the Tunisian automotive ecosystem.

Summary of ResultsSummarizing the complex results of the study and develop conclusions for the strategy.

Strategy DevelopmentDevelopment of the strategy including recommendations for its implementation.

12

34

56

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

5

RESULTS OEM-ANALYSIS

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

6OEM-OPPORTUNITIES | WHAT‘S DRIVING LOCATION DECISIONS OF OEMS?

Trade Barriers, politicalreasons

Market

LocalResources

CostEfficiency

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

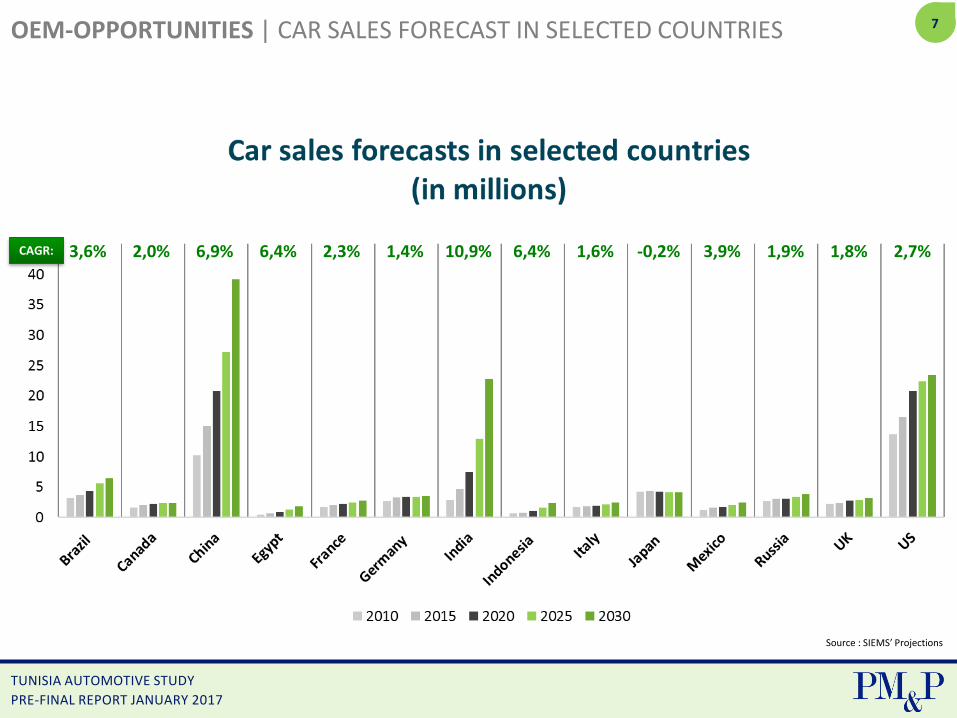

7OEM-OPPORTUNITIES | CAR SALES FORECAST IN SELECTED COUNTRIES

Source : SIEMS’ Projections

CAGR: 3,6% 2,0% 6,9% 6,4% 2,3% 1,4% 10,9% 6,4% 1,6% -0,2% 3,9% 1,9% 1,8% 2,7%

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

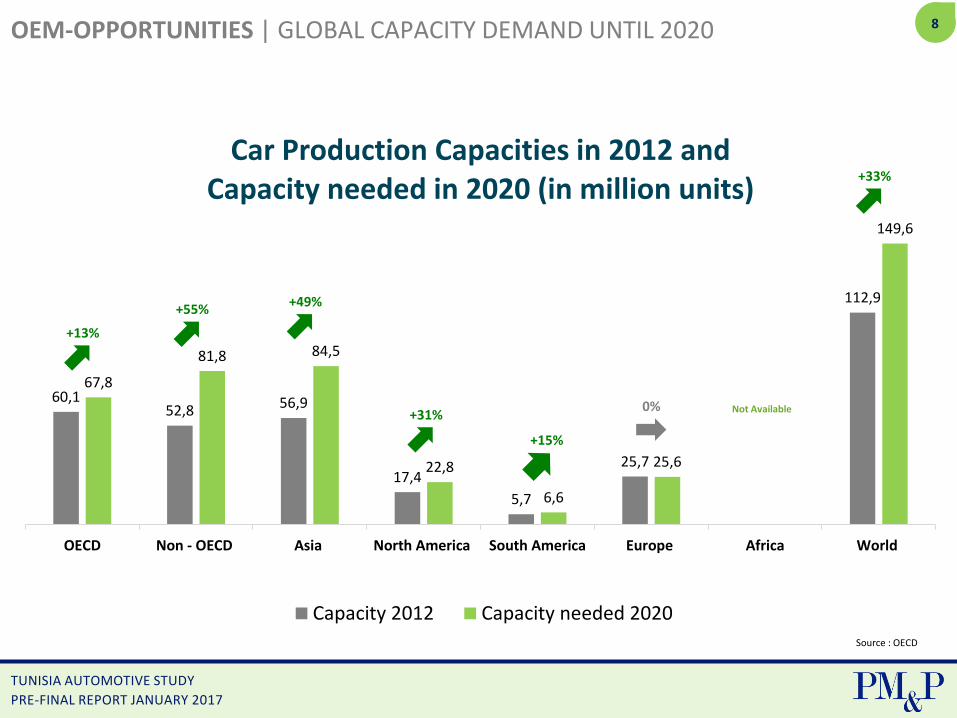

8OEM-OPPORTUNITIES | GLOBAL CAPACITY DEMAND UNTIL 2020

60,152,8 56,9

17,4

5,7

25,7

112,9

67,8

81,8 84,5

22,8

6,6

25,6

149,6

OECD Non - OECD Asia North America South America Europe Africa World

Car Production Capacities in 2012 andCapacity needed in 2020 (in million units)

Capacity 2012 Capacity needed 2020

Not Available

+55%+49%

+31%

+13%

0%

+33%

+15%

Source : OECD

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

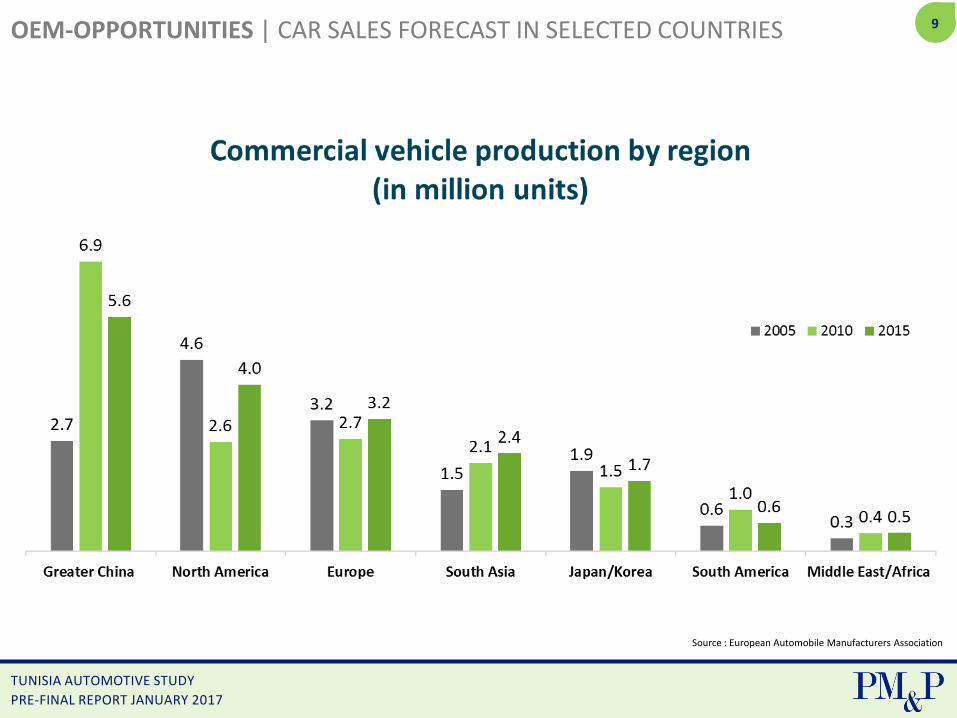

9OEM-OPPORTUNITIES | CAR SALES FORECAST IN SELECTED COUNTRIES

Source : European Automobile Manufacturers Association

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

10OEM-OPPORTUNITIES | NEW PLAYERS

CHINA INDIA

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

11OEM-OPPORTUNITIES | NEW PLAYERS

New Technologies / New Concepts

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

12

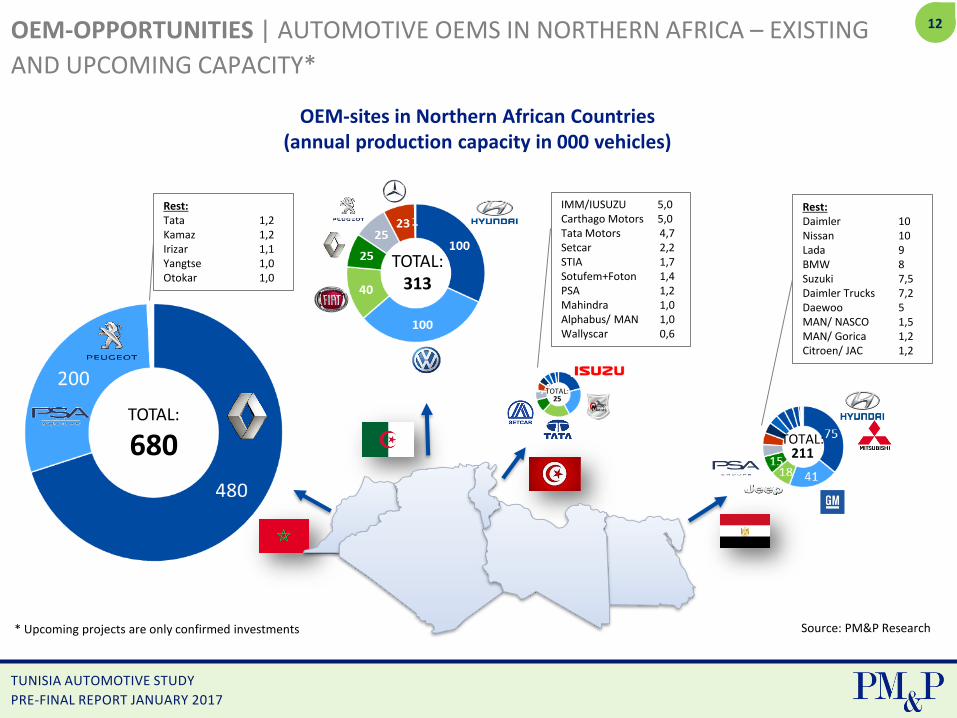

TOTAL:313

OEM-OPPORTUNITIES | AUTOMOTIVE OEMS IN NORTHERN AFRICA – EXISTING

AND UPCOMING CAPACITY*

TOTAL:25

IMM/IUSUZU 5,0Carthago Motors 5,0 Tata Motors 4,7 Setcar 2,2 STIA 1,7 Sotufem+Foton 1,4 PSA 1,2 Mahindra 1,0 Alphabus/ MAN 1,0 Wallyscar 0,6

TOTAL:

680

Rest:Tata 1,2Kamaz 1,2Irizar 1,1Yangtse 1,0Otokar 1,0

TOTAL:211

Rest:Daimler 10Nissan 10Lada 9BMW 8Suzuki 7,5Daimler Trucks 7,2Daewoo 5MAN/ NASCO 1,5MAN/ Gorica 1,2Citroen/ JAC 1,2

* Upcoming projects are only confirmed investments Source: PM&P Research

OEM-sites in Northern African Countries (annual production capacity in 000 vehicles)

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

13

RESULTS TECHNOLOGY TRENDS

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

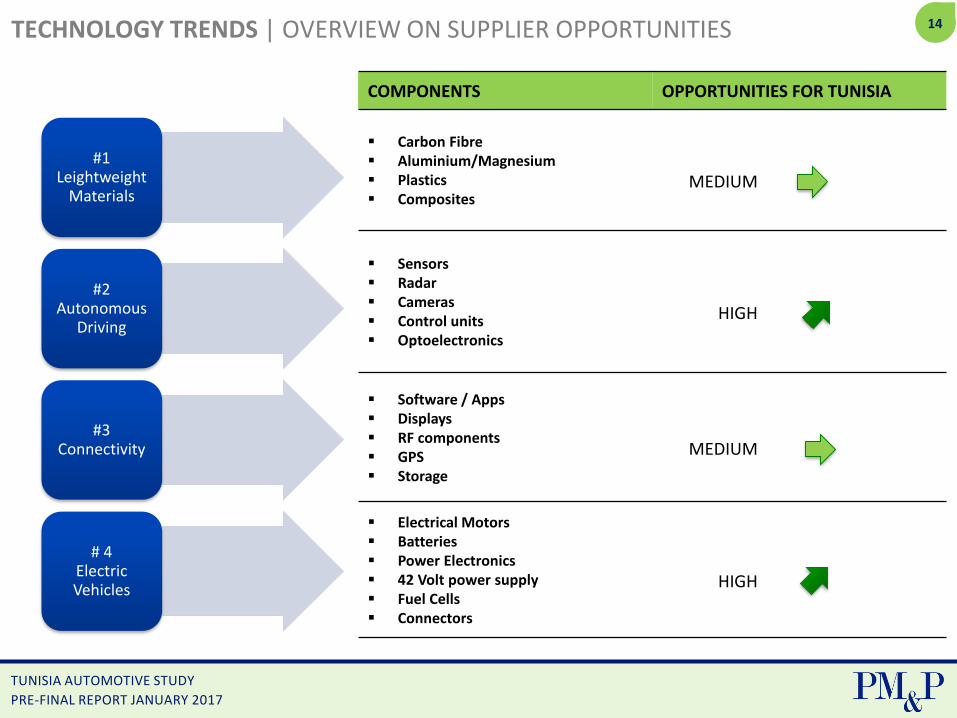

14TECHNOLOGY TRENDS | OVERVIEW ON SUPPLIER OPPORTUNITIES

#1 Leightweight

Materials

#2 Autonomous

Driving

#3 Connectivity

# 4 ElectricVehicles

COMPONENTS OPPORTUNITIES FOR TUNISIA

Carbon Fibre Aluminium/Magnesium Plastics Composites

MEDIUM

Sensors Radar Cameras Control units Optoelectronics

HIGH

Software / Apps Displays RF components GPS Storage

MEDIUM

Electrical Motors Batteries Power Electronics 42 Volt power supply Fuel Cells Connectors

HIGH

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

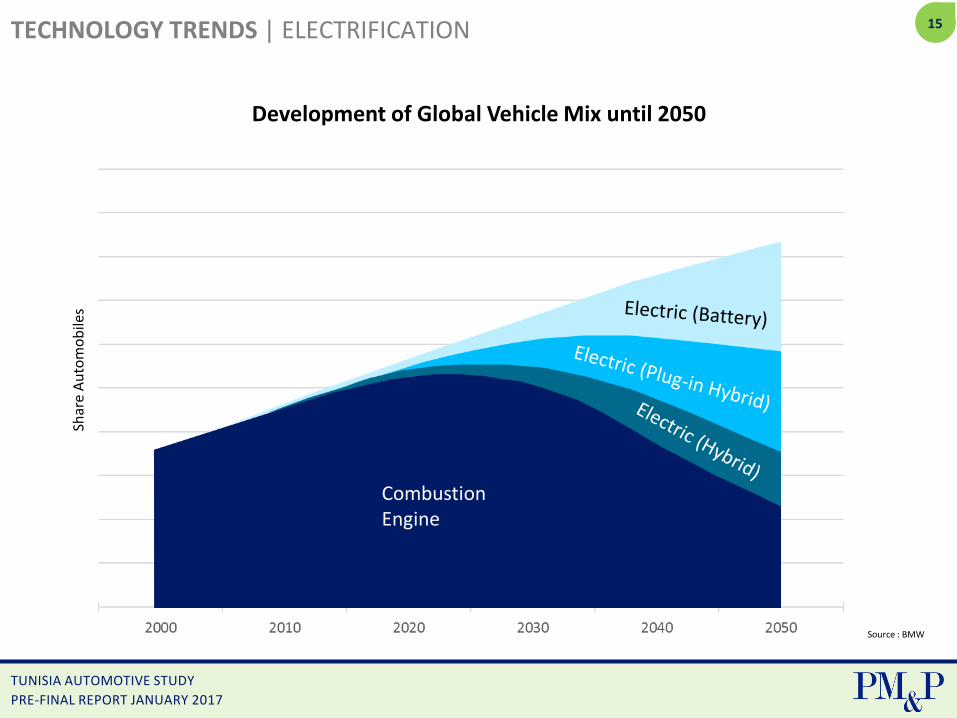

15TECHNOLOGY TRENDS | ELECTRIFICATION

CombustionEngine

Shar

e A

uto

mo

bile

s

Source : BMW

Development of Global Vehicle Mix until 2050

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

16TECHNOLOGY TRENDS | ELECTRIFICATION

Source : KPMG’s Global Automotive Executive Survey 2016

In which powertrain technologies OEMs and Suppliers are planning to invest in

in % of respondents

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

17

RESULTS SUPPLIER ANALYSIS

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

18IMPORTANT NOTES ON THE SUPPLIER ANALYSIS

• Companies are counted as one company, although they might have several sites, as long as they

produce more or less the same products (e.g. LEONI has 4 sites, all cable harnessing, we

counted as one comapny; Dräxlmaier has 3 sites for cable harnessing and 1 site for interior parts

=> we summarised two companies, one with 3 sites, one with 1 site).

• Companies are considered Tunisian, if we don‘t have clear indications that they are dominated

(>50%) by foreign companies. If it was not clear, they are indicated as Tunisian companies.

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

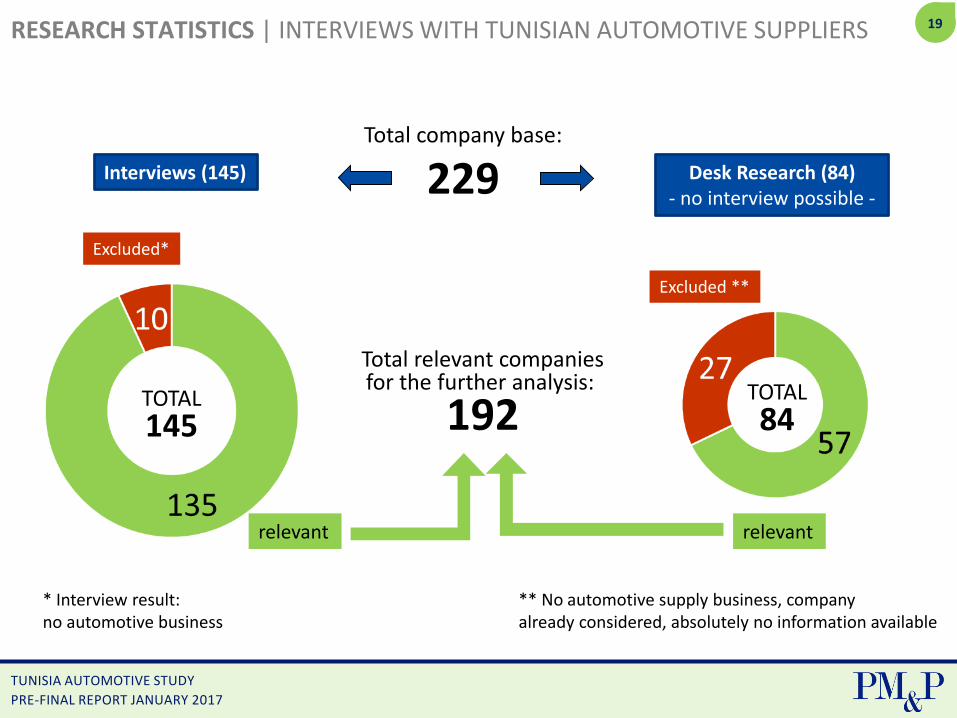

19RESEARCH STATISTICS | INTERVIEWS WITH TUNISIAN AUTOMOTIVE SUPPLIERS

Interviews (145) Desk Research (84)- no interview possible -

relevant

Excluded*

** No automotive supply business, company already considered, absolutely no information available

relevant

Excluded **

TOTAL

145TOTAL

84

Total relevant companiesfor the further analysis:

192

* Interview result: no automotive business

Total company base:

229

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

20RESEARCH STATISTICS | ANALYSED COMPANIES BY COUNTRY ORIGIN

TOTAL:

192

* Number of employees allocated to automotive business (partly estimates)

FOREIGN

TUNISIAN

BY NUMBER OF COMPANIES: BY TOTAL WORKFORCE IN AUTOMOTIVE*:

FOREIGN TUNISIAN

TOTAL:

79.487

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

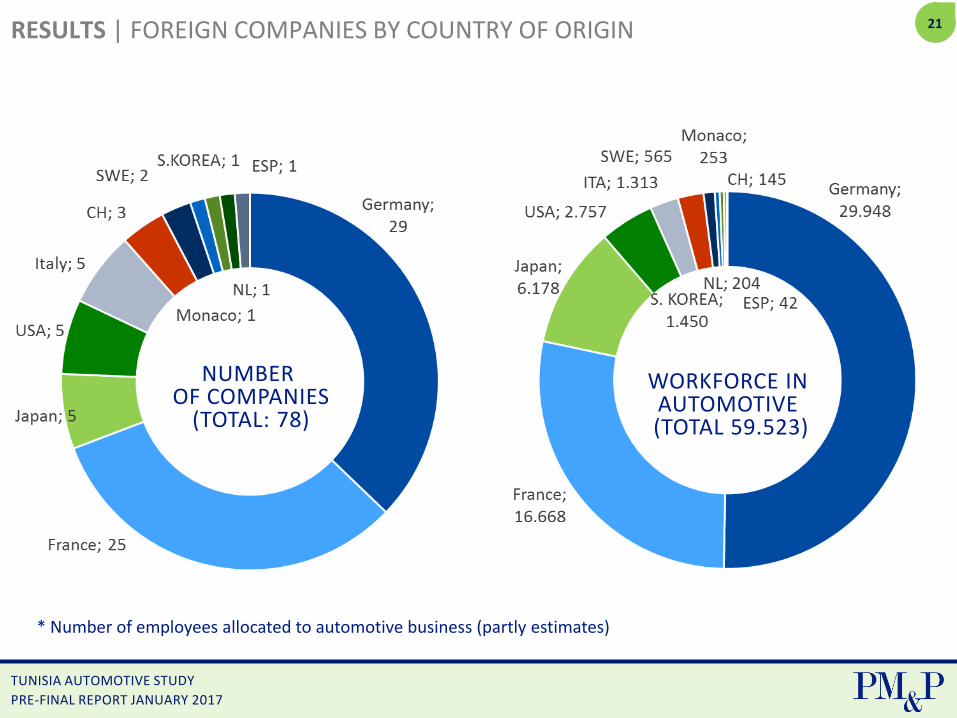

21RESULTS | FOREIGN COMPANIES BY COUNTRY OF ORIGIN

* Number of employees allocated to automotive business (partly estimates)

NUMBER OF COMPANIES

(TOTAL: 78)

WORKFORCE IN AUTOMOTIVE (TOTAL 59.523)

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

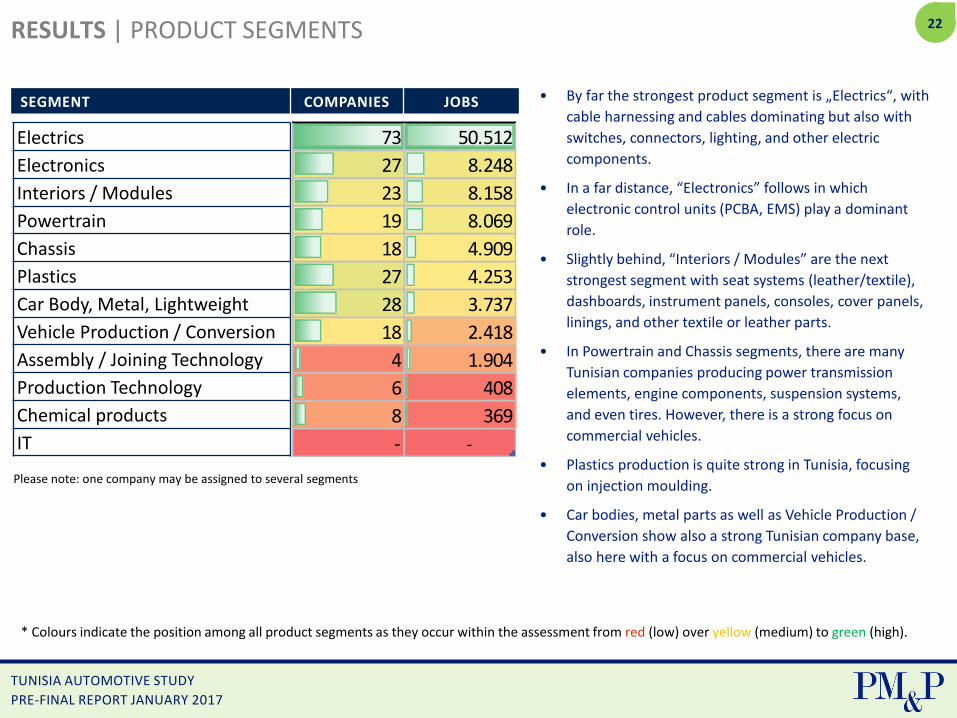

22RESULTS | PRODUCT SEGMENTS

SEGMENT COMPANIES JOBS

Electrics

Electronics

Interiors / Modules

Powertrain

Chassis

Plastics

Car Body, Metal, Lightweight

Vehicle Production / Conversion

Assembly / Joining Technology

Production Technology

Chemical products

IT

• By far the strongest product segment is „Electrics“, with

cable harnessing and cables dominating but also with

switches, connectors, lighting, and other electric

components.

• In a far distance, “Electronics” follows in which

electronic control units (PCBA, EMS) play a dominant

role.

• Slightly behind, “Interiors / Modules” are the next

strongest segment with seat systems (leather/textile),

dashboards, instrument panels, consoles, cover panels,

linings, and other textile or leather parts.

• In Powertrain and Chassis segments, there are many

Tunisian companies producing power transmission

elements, engine components, suspension systems,

and even tires. However, there is a strong focus on

commercial vehicles.

• Plastics production is quite strong in Tunisia, focusing

on injection moulding.

• Car bodies, metal parts as well as Vehicle Production /

Conversion show also a strong Tunisian company base,

also here with a focus on commercial vehicles.

Please note: one company may be assigned to several segments

* Colours indicate the position among all product segments as they occur within the assessment from red (low) over yellow (medium) to green (high).

73 50.512

27 8.248

23 8.158

19 8.069

18 4.909

27 4.253

28 3.737

18 2.418

4 1.904

6 408

8 369

- -

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

23RESULTS BY SEGMENT | ELECTRICS

• Very strong cables / cable harnessing business,

particularly driven by strong Tunisian players.

Additional strength in the related cable

protection.

• Further strong related businesses with switches,

connectors, lighting, and other electric

components.

• Electric motors, alternators still very small, only

foreign companies.

• Small batteries segment, completely operated

by Tunisian players.

• Instruments section not yet present in Tunisia.

• Excellent conditions for developing a cluster in

electrical systems.

PRODUCT TOTAL # OF JOBS

TUNISIAN SHARE*

Cables 31.400 15%

Cable harnesses 37.294 10%

Electric motors 300 0%

Generators/Alternators 350 0%

Connectors 1.629 7%

Switches 2.697 4%

Fuses - 0%

Lighting systems 822 50%

Batteries 1.046 100%

Heating / Air conditioning 75 29%

Ignition systems 860 0%

Instruments - 0%

Other electric components 2.766 42%

Cable Protection 307 29%

Cables

Cable harnesses

Electric motors

Generators/Alternators

Connectors

Switches

Fuses

Lighting systems

Batteries

Heating / Air conditioning

Ignition systems

Instruments

Other electric components

Cable Protection

* Share of Tunisian (non-foreign) companies on the Indicated number of jobs

* Colours indicate the position among all product segments as they occur within the assessment from red (low) over yellow (medium) to green (high).

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

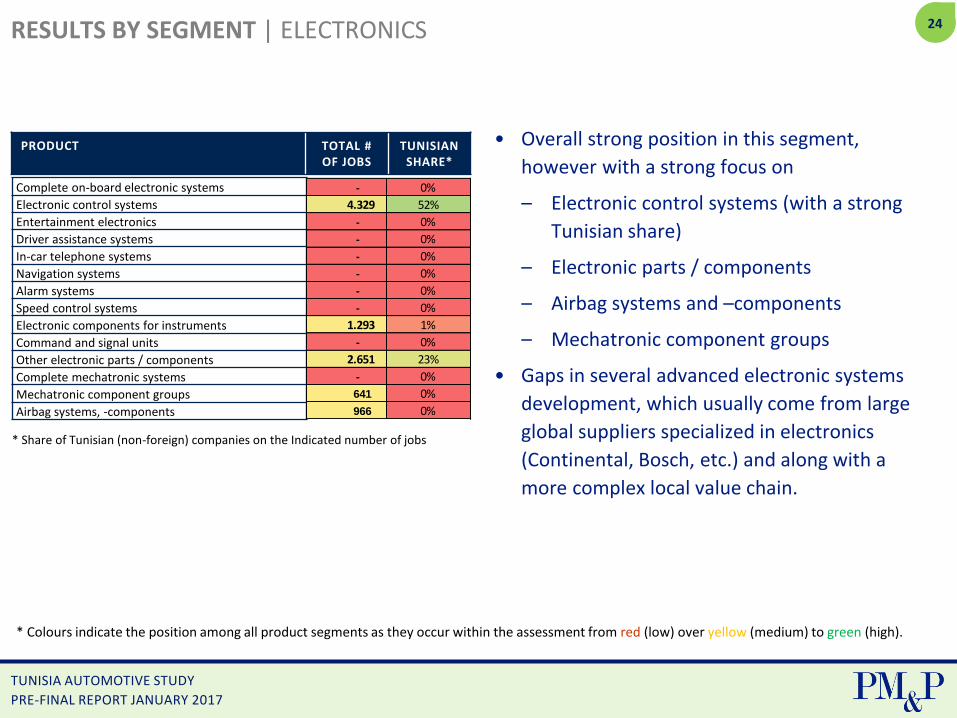

24RESULTS BY SEGMENT | ELECTRONICS

• Overall strong position in this segment,

however with a strong focus on

– Electronic control systems (with a strong

Tunisian share)

– Electronic parts / components

– Airbag systems and –components

– Mechatronic component groups

• Gaps in several advanced electronic systems

development, which usually come from large

global suppliers specialized in electronics

(Continental, Bosch, etc.) and along with a

more complex local value chain.

PRODUCT TOTAL # OF JOBS

TUNISIAN SHARE*

Complete on-board electronic systems

Electronic control systems

Entertainment electronics

Driver assistance systems

In-car telephone systems

Navigation systems

Alarm systems

Speed control systems

Electronic components for instruments

Command and signal units

Other electronic parts / components

Complete mechatronic systems

Mechatronic component groups

Airbag systems, -components

- 0%

4.329 52%

- 0%

- 0%

- 0%

- 0%

- 0%

- 0%

1.293 1%

- 0%

2.651 23%

- 0%

641 0%

966 0%

* Share of Tunisian (non-foreign) companies on the Indicated number of jobs

* Colours indicate the position among all product segments as they occur within the assessment from red (low) over yellow (medium) to green (high).

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

25RESULTS BY SEGMENT | INTERIORS / MODULES

Strong interior business although very few

OEMs are operating in Tunisia.

High competence in leather processing, textiles

processing, plastics (injection moulding,

mechatronics).

Strong segments:

– Seat systems, especially leather

– Leather and Textile parts (arm rests, cover

panels, linings) and plastic interior

– Steering wheels (incl. leather), some also

covering airbag systems

– Dashboards and instrument panels

– Levers and pedals (especially gear levers)

– Consoles

• In conjunction with electrics / electronics

opportunities for a more complex cluster.

PRODUCT TOTAL # OF JOBS

TUNISIAN SHARE*

2.418 20%

3.523 6%

3.997 0%

3.670 6%

- 0%

170 71%

992 9%

- 0%

875 31%

1.958 23%

1.236 24%

Seat systems, -components

Dashboards and instrument panels

Consoles, storage compartments and systems

Cover panels and linings

Plates

Carpets and car mats

Levers and pedals

Complete restraint systems

Steering wheels

Textile parts

Leather parts

* Share of Tunisian (non-foreign) companies on the Indicated number of jobs

* Colours indicate the position among all product segments as they occur within the assessment from red (low) over yellow (medium) to green (high).

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

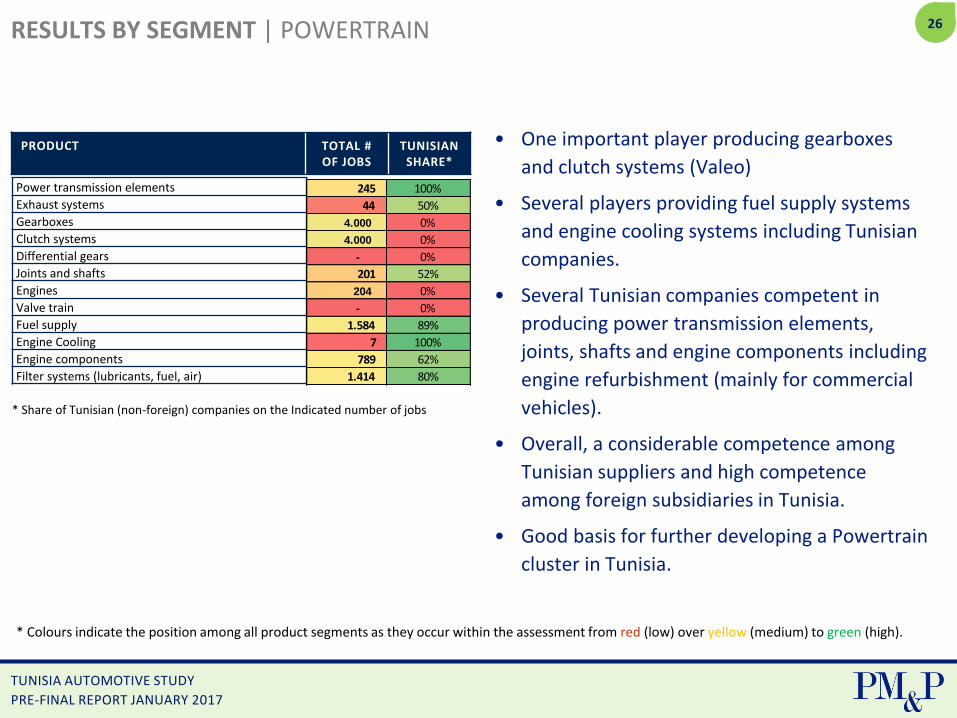

26RESULTS BY SEGMENT | POWERTRAIN

• One important player producing gearboxes

and clutch systems (Valeo)

• Several players providing fuel supply systems

and engine cooling systems including Tunisian

companies.

• Several Tunisian companies competent in

producing power transmission elements,

joints, shafts and engine components including

engine refurbishment (mainly for commercial

vehicles).

• Overall, a considerable competence among

Tunisian suppliers and high competence

among foreign subsidiaries in Tunisia.

• Good basis for further developing a Powertrain

cluster in Tunisia.

PRODUCT TOTAL # OF JOBS

TUNISIAN SHARE*

Power transmission elements

Exhaust systems

Gearboxes

Clutch systems

Differential gears

Joints and shafts

Engines

Valve train

Fuel supply

Engine Cooling

Engine components

Filter systems (lubricants, fuel, air)

245 100%

44 50%

4.000 0%

4.000 0%

- 0%

201 52%

204 0%

- 0%

1.584 89%

7 100%

789 62%

1.414 80%

* Share of Tunisian (non-foreign) companies on the Indicated number of jobs

* Colours indicate the position among all product segments as they occur within the assessment from red (low) over yellow (medium) to green (high).

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

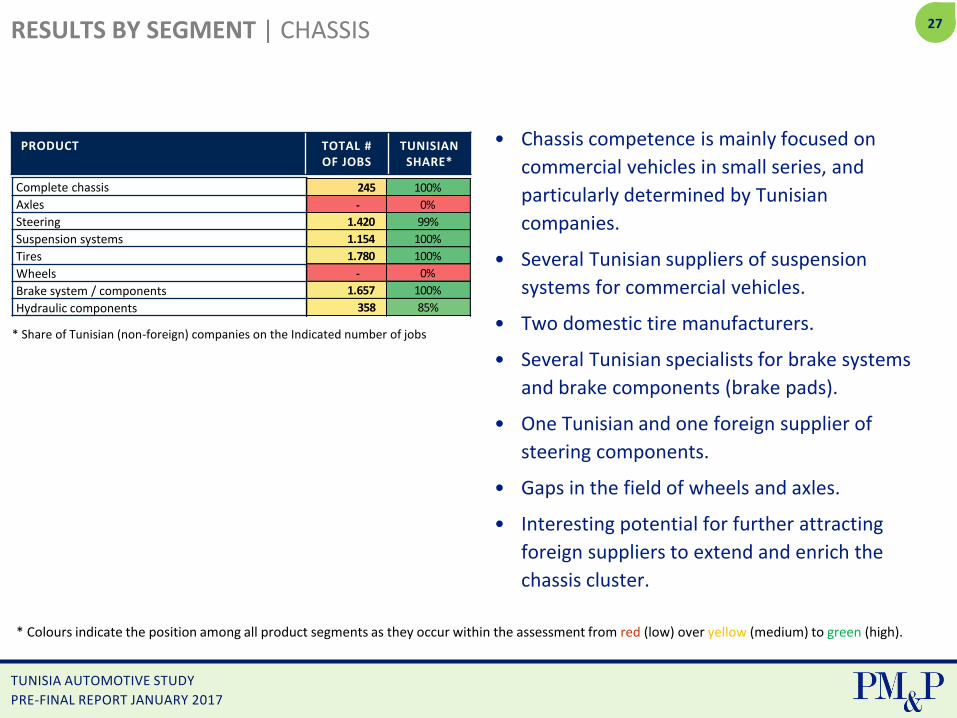

27RESULTS BY SEGMENT | CHASSIS

• Chassis competence is mainly focused on

commercial vehicles in small series, and

particularly determined by Tunisian

companies.

• Several Tunisian suppliers of suspension

systems for commercial vehicles.

• Two domestic tire manufacturers.

• Several Tunisian specialists for brake systems

and brake components (brake pads).

• One Tunisian and one foreign supplier of

steering components.

• Gaps in the field of wheels and axles.

• Interesting potential for further attracting

foreign suppliers to extend and enrich the

chassis cluster.

PRODUCT TOTAL # OF JOBS

TUNISIAN SHARE*

Complete chassis

Axles

Steering

Suspension systems

Tires

Wheels

Brake system / components

Hydraulic components

245 100%

- 0%

1.420 99%

1.154 100%

1.780 100%

- 0%

1.657 100%

358 85%

* Share of Tunisian (non-foreign) companies on the Indicated number of jobs

* Colours indicate the position among all product segments as they occur within the assessment from red (low) over yellow (medium) to green (high).

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

28RESULTS BY SEGMENT | PLASTICS

• The plastics segment in Tunisia is mainly

determined by producing plastic components.

• There are 26 players, of which almost 50% are

Tunisian companies producing different parts,

mainly by injection moulding.

• There is space for further developing with

segment with advanced plastic components and

composites. Plastics play an important role in

future vehicles and lightweight construction.

• No competence yet in carbon fibre products,

which is a further field for growing the plastics /

composites cluster.

PRODUCT TOTAL # OF JOBS

TUNISIAN SHARE*

Thermoplastics

Thermosetting plastics

Elastomers

Other types of plastic

Other plastic components

307 0%

304 0%

- 0%

- 0%

4.250 50%

* Share of Tunisian (non-foreign) companies on the Indicated number of jobs

* Colours indicate the position among all product segments as they occur within the assessment from red (low) over yellow (medium) to green (high).

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

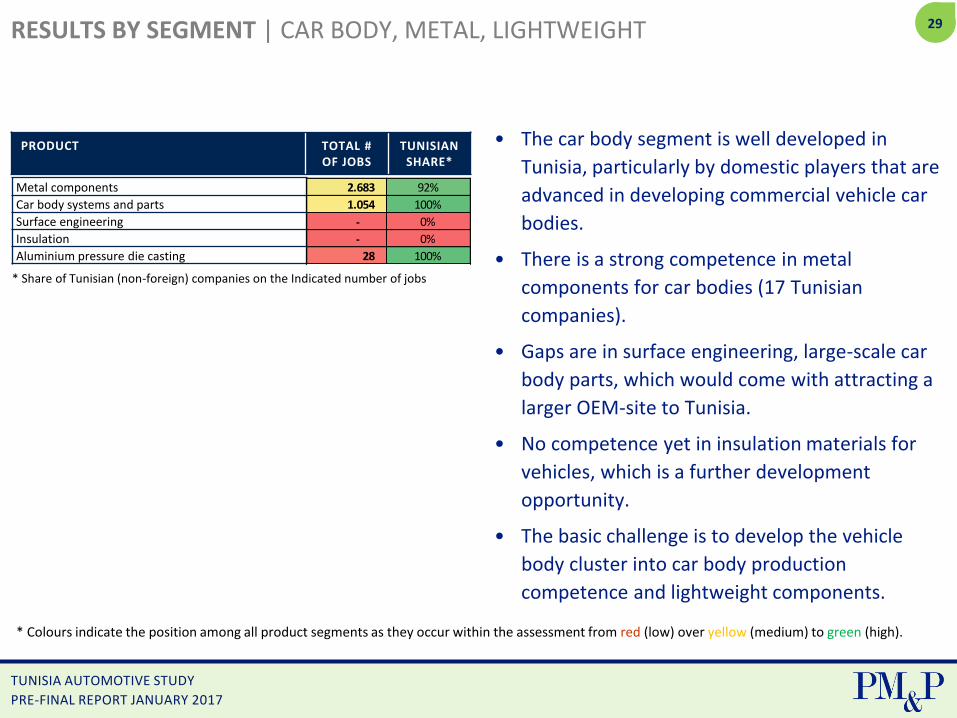

29RESULTS BY SEGMENT | CAR BODY, METAL, LIGHTWEIGHT

• The car body segment is well developed in

Tunisia, particularly by domestic players that are

advanced in developing commercial vehicle car

bodies.

• There is a strong competence in metal

components for car bodies (17 Tunisian

companies).

• Gaps are in surface engineering, large-scale car

body parts, which would come with attracting a

larger OEM-site to Tunisia.

• No competence yet in insulation materials for

vehicles, which is a further development

opportunity.

• The basic challenge is to develop the vehicle

body cluster into car body production

competence and lightweight components.

PRODUCT TOTAL # OF JOBS

TUNISIAN SHARE*

Metal components

Car body systems and parts

Surface engineering

Insulation

Aluminium pressure die casting

2.683 92%

1.054 100%

- 0%

- 0%

28 100%

* Share of Tunisian (non-foreign) companies on the Indicated number of jobs

* Colours indicate the position among all product segments as they occur within the assessment from red (low) over yellow (medium) to green (high).

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

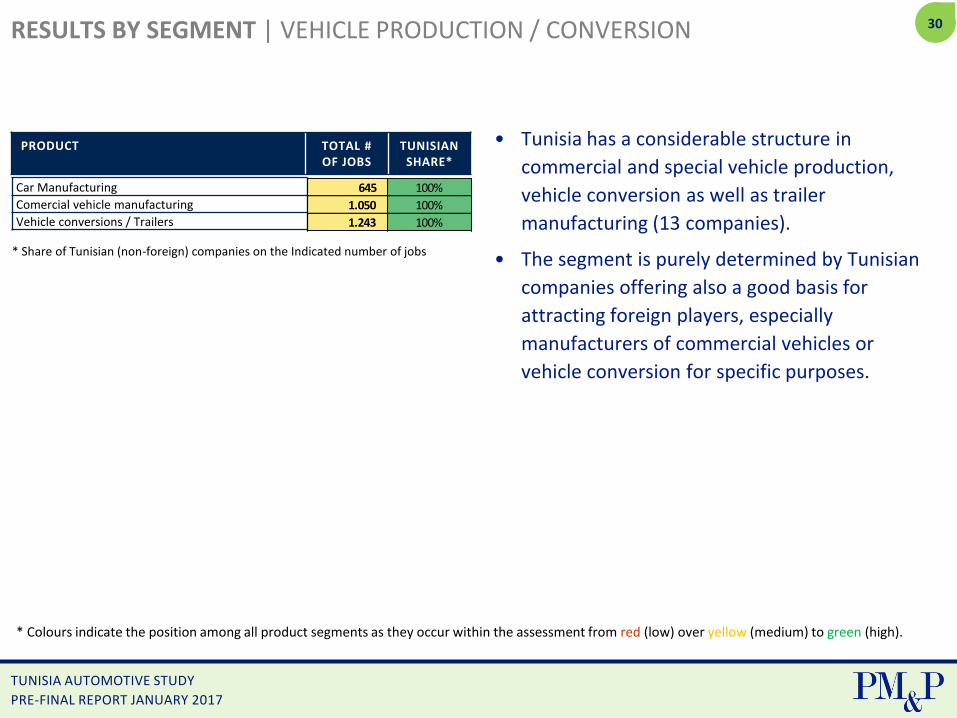

30RESULTS BY SEGMENT | VEHICLE PRODUCTION / CONVERSION

• Tunisia has a considerable structure in

commercial and special vehicle production,

vehicle conversion as well as trailer

manufacturing (13 companies).

• The segment is purely determined by Tunisian

companies offering also a good basis for

attracting foreign players, especially

manufacturers of commercial vehicles or

vehicle conversion for specific purposes.

PRODUCT TOTAL # OF JOBS

TUNISIAN SHARE*

Car Manufacturing

Comercial vehicle manufacturing

Vehicle conversions / Trailers

645 100%

1.050 100%

1.243 100%

* Share of Tunisian (non-foreign) companies on the Indicated number of jobs

* Colours indicate the position among all product segments as they occur within the assessment from red (low) over yellow (medium) to green (high).

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

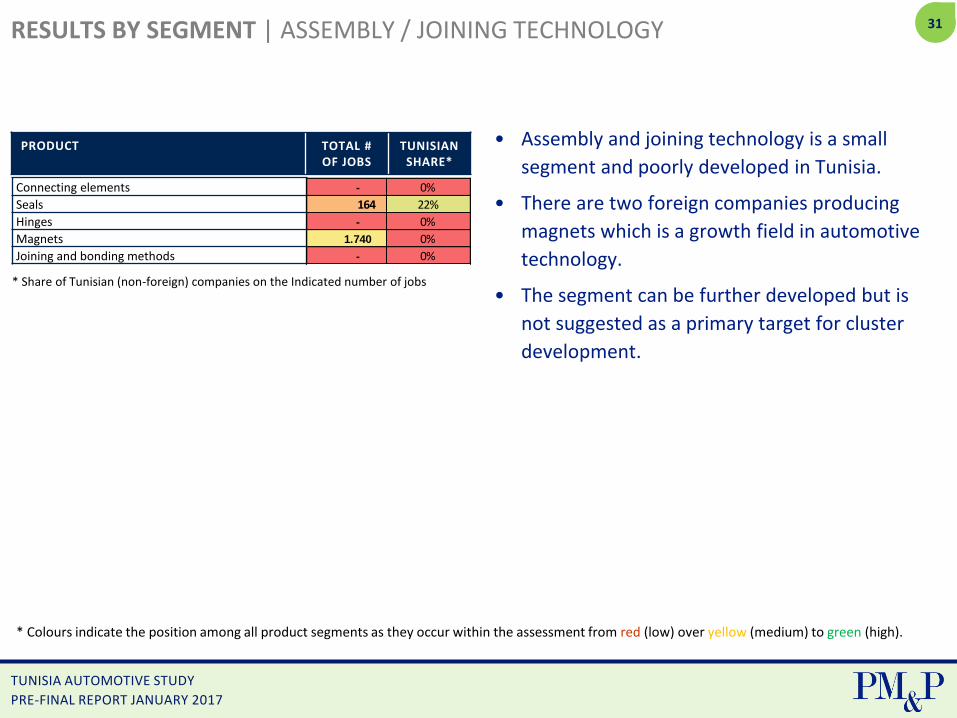

31RESULTS BY SEGMENT | ASSEMBLY / JOINING TECHNOLOGY

• Assembly and joining technology is a small

segment and poorly developed in Tunisia.

• There are two foreign companies producing

magnets which is a growth field in automotive

technology.

• The segment can be further developed but is

not suggested as a primary target for cluster

development.

PRODUCT TOTAL # OF JOBS

TUNISIAN SHARE*

Connecting elements

Seals

Hinges

Magnets

Joining and bonding methods

- 0%

164 22%

- 0%

1.740 0%

- 0%

* Share of Tunisian (non-foreign) companies on the Indicated number of jobs

* Colours indicate the position among all product segments as they occur within the assessment from red (low) over yellow (medium) to green (high).

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

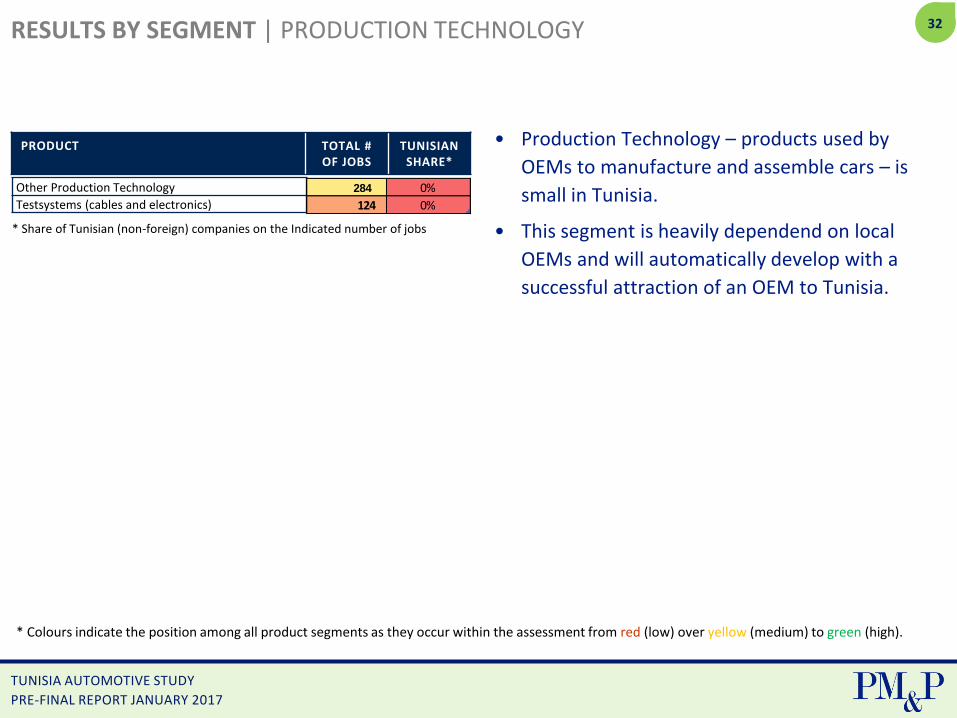

32RESULTS BY SEGMENT | PRODUCTION TECHNOLOGY

• Production Technology – products used by

OEMs to manufacture and assemble cars – is

small in Tunisia.

• This segment is heavily dependend on local

OEMs and will automatically develop with a

successful attraction of an OEM to Tunisia.

PRODUCT TOTAL # OF JOBS

TUNISIAN SHARE*

Other Production Technology

Testsystems (cables and electronics)

284 0%

124 0%

* Share of Tunisian (non-foreign) companies on the Indicated number of jobs

* Colours indicate the position among all product segments as they occur within the assessment from red (low) over yellow (medium) to green (high).

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

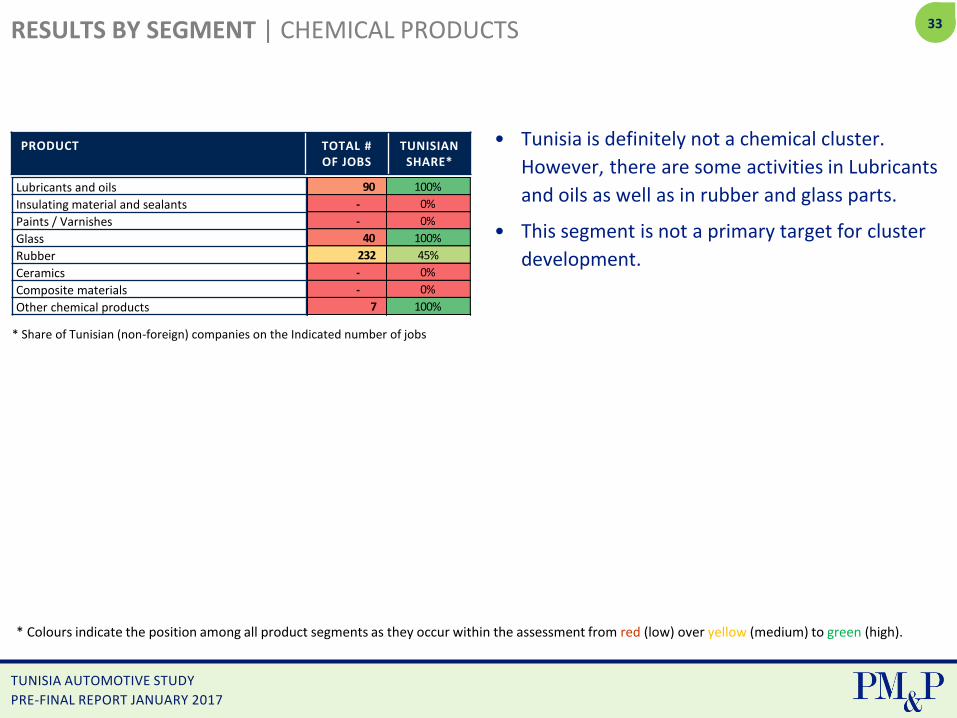

33RESULTS BY SEGMENT | CHEMICAL PRODUCTS

• Tunisia is definitely not a chemical cluster.

However, there are some activities in Lubricants

and oils as well as in rubber and glass parts.

• This segment is not a primary target for cluster

development.

PRODUCT TOTAL # OF JOBS

TUNISIAN SHARE*

Lubricants and oils

Insulating material and sealants

Paints / Varnishes

Glass

Rubber

Ceramics

Composite materials

Other chemical products

90 100%

- 0%

- 0%

40 100%

232 45%

- 0%

- 0%

7 100%

* Share of Tunisian (non-foreign) companies on the Indicated number of jobs

* Colours indicate the position among all product segments as they occur within the assessment from red (low) over yellow (medium) to green (high).

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

34

STRATEGY

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

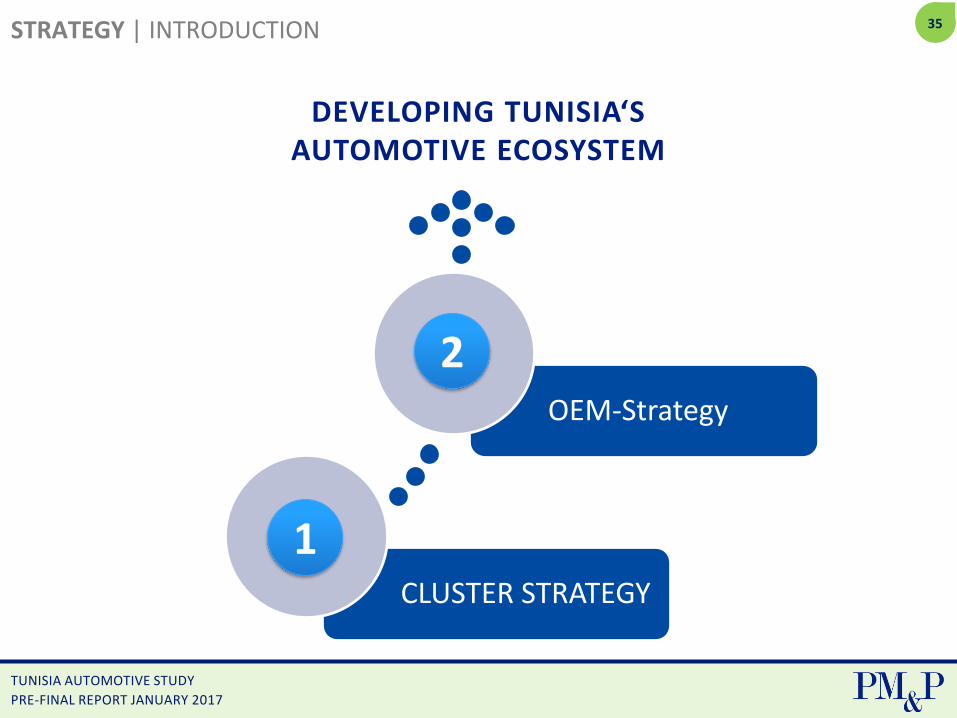

35STRATEGY | INTRODUCTION

CLUSTER STRATEGY

OEM-Strategy

2

1

DEVELOPING TUNISIA‘SAUTOMOTIVE ECOSYSTEM

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

36

OEM-STRATEGY

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

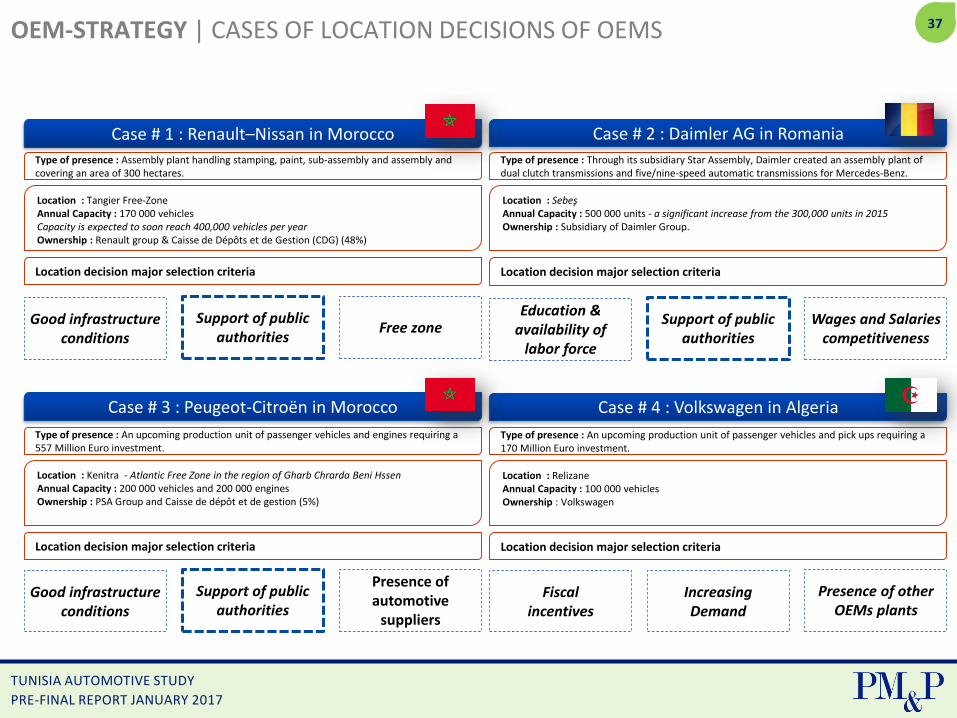

37OEM-STRATEGY | CASES OF LOCATION DECISIONS OF OEMS

Type of presence : Assembly plant handling stamping, paint, sub-assembly and assembly and covering an area of 300 hectares.

Location : Tangier Free-ZoneAnnual Capacity : 170 000 vehiclesCapacity is expected to soon reach 400,000 vehicles per yearOwnership : Renault group & Caisse de Dépôts et de Gestion (CDG) (48%)

Case # 1 : Renault–Nissan in Morocco

Location decision major selection criteria

Support of public authorities

Good infrastructure conditions

Free zone

Case # 2 : Daimler AG in Romania

Type of presence : Through its subsidiary Star Assembly, Daimler created an assembly plant of dual clutch transmissions and five/nine-speed automatic transmissions for Mercedes-Benz.

Location : SebeşAnnual Capacity : 500 000 units - a significant increase from the 300,000 units in 2015Ownership : Subsidiary of Daimler Group.

Location decision major selection criteria

Case # 3 : Peugeot-Citroën in Morocco

Type of presence : An upcoming production unit of passenger vehicles and engines requiring a 557 Million Euro investment.

Location : Kenitra - Atlantic Free Zone in the region of Gharb Chrarda Beni HssenAnnual Capacity : 200 000 vehicles and 200 000 enginesOwnership : PSA Group and Caisse de dépôt et de gestion (5%)

Location decision major selection criteria

Case # 4 : Volkswagen in Algeria

Type of presence : An upcoming production unit of passenger vehicles and pick ups requiring a 170 Million Euro investment.

Location : RelizaneAnnual Capacity : 100 000 vehiclesOwnership : Volkswagen

Location decision major selection criteria

Support of public authorities

Good infrastructure conditions

Presence of automotive

suppliers

Fiscal incentives

Presence of other OEMs plants

Support of public authorities

Education & availability of

labor force

Wages and Salaries competitiveness

Increasing Demand

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

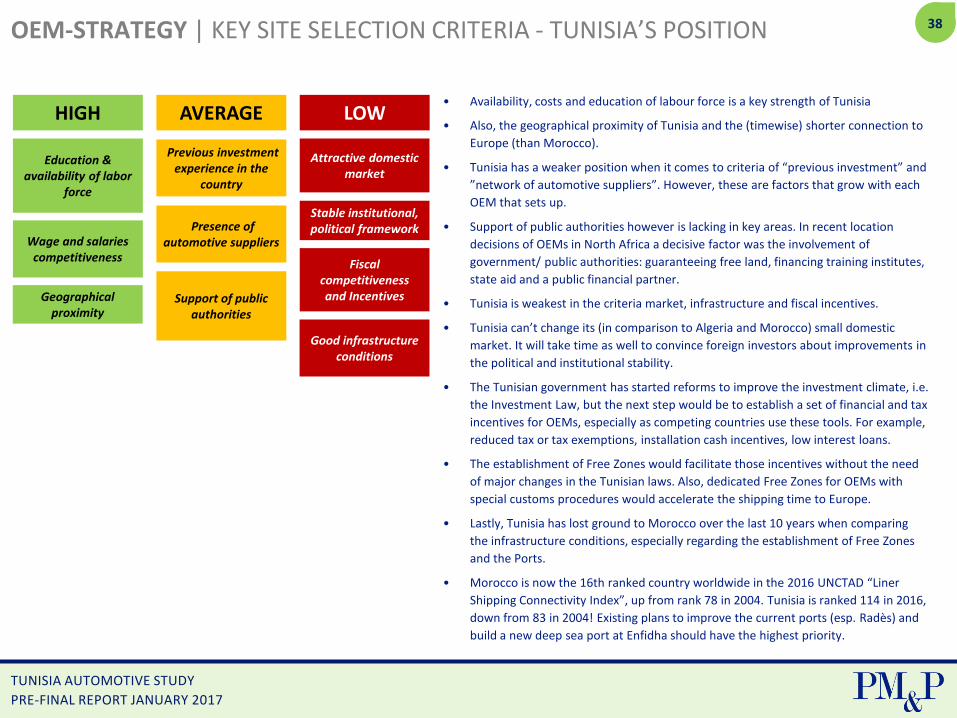

38OEM-STRATEGY | KEY SITE SELECTION CRITERIA - TUNISIA’S POSITION

Attractive domestic market

Wage and salaries competitiveness

Geographical proximity

Education & availability of labor

force

Fiscal competitiveness and Incentives

Previous investment experience in the

country

Presence of automotive suppliers

Good infrastructure conditions

Stable institutional, political framework

Support of public authorities

• Availability, costs and education of labour force is a key strength of Tunisia

• Also, the geographical proximity of Tunisia and the (timewise) shorter connection to

Europe (than Morocco).

• Tunisia has a weaker position when it comes to criteria of “previous investment” and

”network of automotive suppliers”. However, these are factors that grow with each

OEM that sets up.

• Support of public authorities however is lacking in key areas. In recent location

decisions of OEMs in North Africa a decisive factor was the involvement of

government/ public authorities: guaranteeing free land, financing training institutes,

state aid and a public financial partner.

• Tunisia is weakest in the criteria market, infrastructure and fiscal incentives.

• Tunisia can’t change its (in comparison to Algeria and Morocco) small domestic

market. It will take time as well to convince foreign investors about improvements in

the political and institutional stability.

• The Tunisian government has started reforms to improve the investment climate, i.e.

the Investment Law, but the next step would be to establish a set of financial and tax

incentives for OEMs, especially as competing countries use these tools. For example,

reduced tax or tax exemptions, installation cash incentives, low interest loans.

• The establishment of Free Zones would facilitate those incentives without the need

of major changes in the Tunisian laws. Also, dedicated Free Zones for OEMs with

special customs procedures would accelerate the shipping time to Europe.

• Lastly, Tunisia has lost ground to Morocco over the last 10 years when comparing

the infrastructure conditions, especially regarding the establishment of Free Zones

and the Ports.

• Morocco is now the 16th ranked country worldwide in the 2016 UNCTAD “Liner

Shipping Connectivity Index”, up from rank 78 in 2004. Tunisia is ranked 114 in 2016,

down from 83 in 2004! Existing plans to improve the current ports (esp. Radès) and

build a new deep sea port at Enfidha should have the highest priority.

HIGH AVERAGE LOW

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

39OEM-STRATEGY | SUMMARY (1)

• Attracting a large foreign OEM manufacturing min. 100.000 vehicles p.a. in Tunisia must be a key

strategic goal for the further development of the Tunisian Automotive ecosystem. The first large OEM-

site would have a considerable impact on the automotive ecosystem. An investment would

– generate at least 2,000 new jobs directly;

– attract further suppliers to Tunisia and create at least 3,000 jobs indirectly;

– increase chances for local suppliers to become 1st or 2nd tier suppliers to the OEM operating in

Tunisia;

– be a key driver for further development of the automotive ecosystem.

• Global competition for attracting an OEM is fierce. The OEMs have adapted to that and are very

demanding towards receiving generous support from governments. Countries are forced to cover a

large part of the investment done by the OEM in the form of incentives and provide additional

investment in infrastructure, labour education, power utilities, raw material supply, and many other

things.

• Without at least one large OEM-site, Tunisia will not succeed in maintaining or even improving its global

competitiveness as a location for the automotive sector. Instead there would be a high risk that Tunisia

would lose touch with its competitors in Northern Africa, especially with Morocco and Algeria.

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

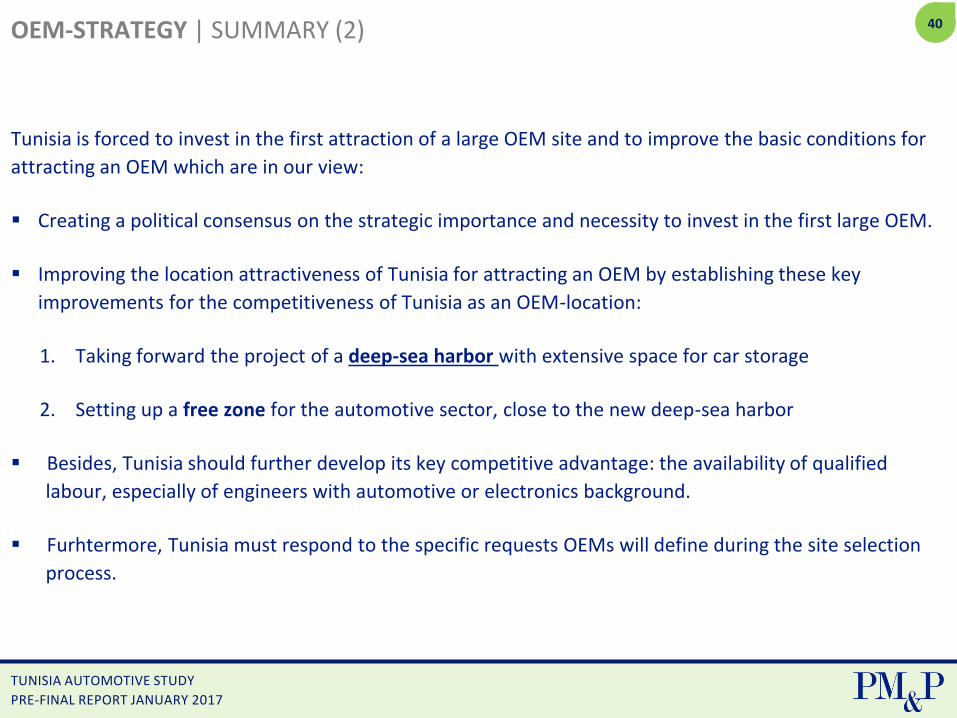

40OEM-STRATEGY | SUMMARY (2)

Tunisia is forced to invest in the first attraction of a large OEM site and to improve the basic conditions for

attracting an OEM which are in our view:

Creating a political consensus on the strategic importance and necessity to invest in the first large OEM.

Improving the location attractiveness of Tunisia for attracting an OEM by establishing these key

improvements for the competitiveness of Tunisia as an OEM-location:

1. Taking forward the project of a deep-sea harbor with extensive space for car storage

2. Setting up a free zone for the automotive sector, close to the new deep-sea harbor

Besides, Tunisia should further develop its key competitive advantage: the availability of qualified

labour, especially of engineers with automotive or electronics background.

Furhtermore, Tunisia must respond to the specific requests OEMs will define during the site selection

process.

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

41

CLUSTER STRATEGY

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

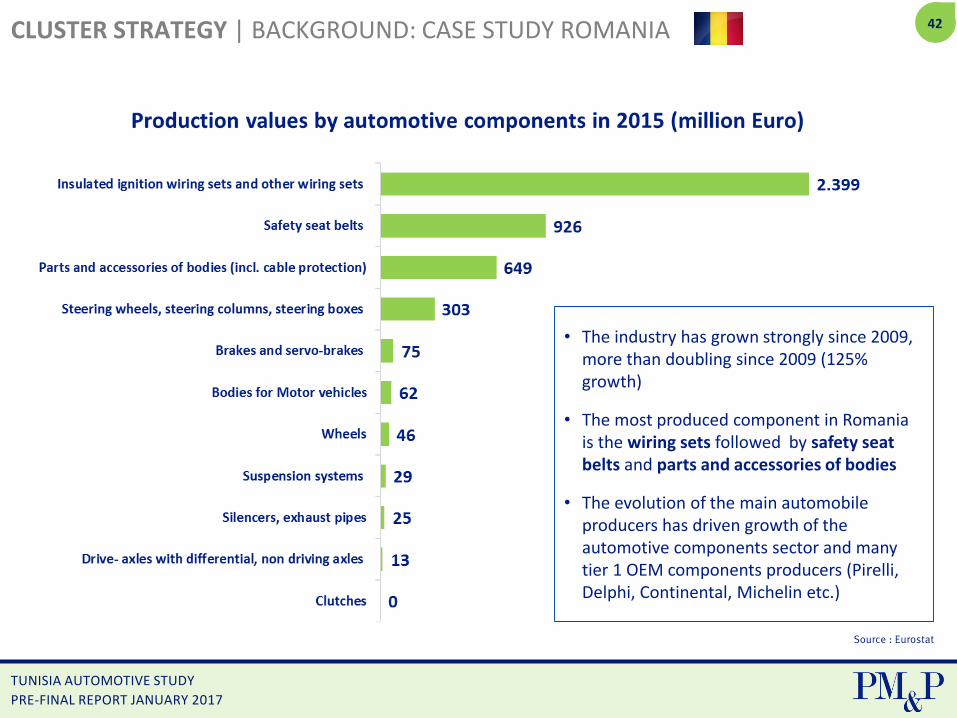

42CLUSTER STRATEGY | BACKGROUND: CASE STUDY ROMANIA

Source : Eurostat

• The industry has grown strongly since 2009, more than doubling since 2009 (125% growth)

• The most produced component in Romania is the wiring sets followed by safety seat belts and parts and accessories of bodies

• The evolution of the main automobile producers has driven growth of the automotive components sector and many tier 1 OEM components producers (Pirelli, Delphi, Continental, Michelin etc.)

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

43CLUSTER STRATEGY | ELECTRICS

CABLES

CABLE HARNESSSING

SWITCHES, CONNEC-

TORS

CABLE PROTEC

TION

48V POWER SYSTEM

ELECTRIC MOTORS

MECHA-TRONICS

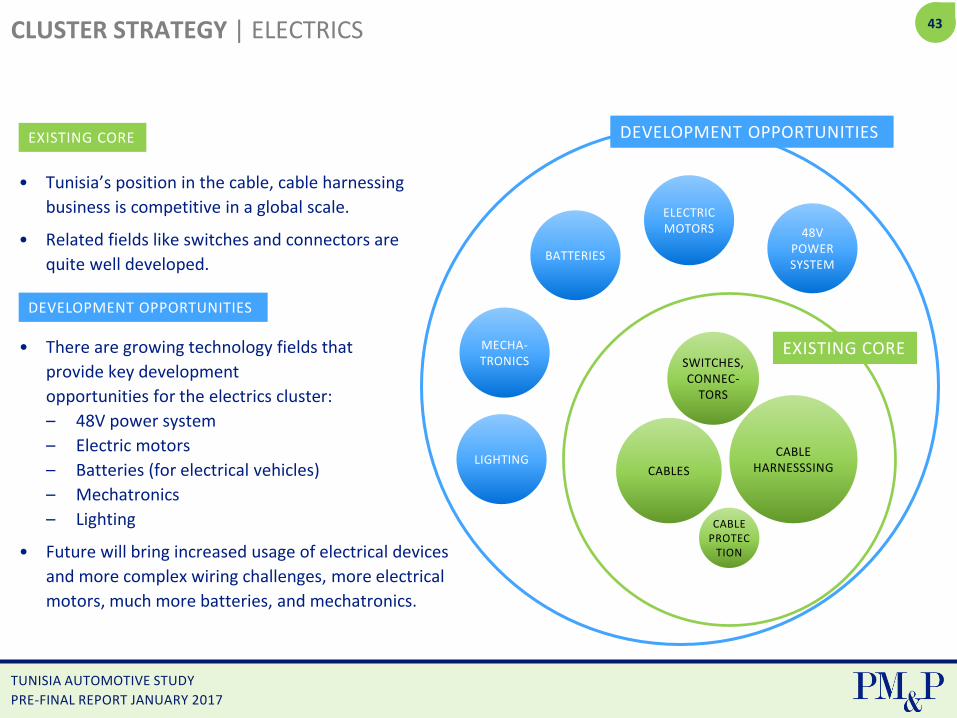

• Tunisia’s position in the cable, cable harnessing

business is competitive in a global scale.

• Related fields like switches and connectors are

quite well developed.BATTERIES

EXISTING CORE DEVELOPMENT OPPORTUNITIES

EXISTING CORE

DEVELOPMENT OPPORTUNITIES

• There are growing technology fields that

provide key development

opportunities for the electrics cluster:

– 48V power system

– Electric motors

– Batteries (for electrical vehicles)

– Mechatronics

– Lighting

• Future will bring increased usage of electrical devices

and more complex wiring challenges, more electrical

motors, much more batteries, and mechatronics.

LIGHTING

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

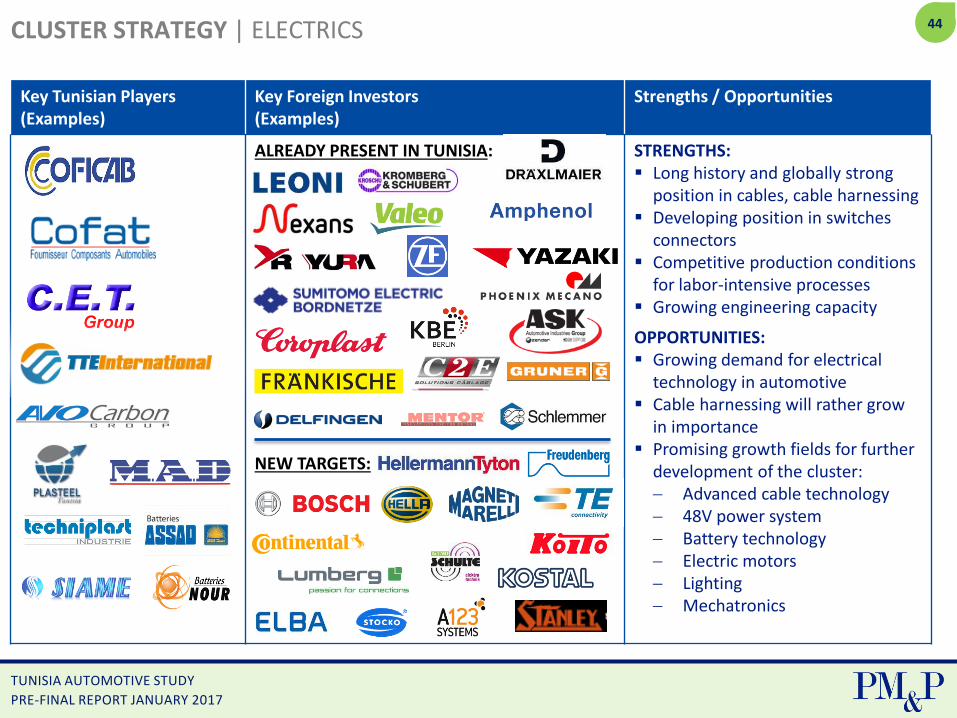

44CLUSTER STRATEGY | ELECTRICS

Key Tunisian Players(Examples)

Key Foreign Investors(Examples)

Strengths / Opportunities

ALREADY PRESENT IN TUNISIA:

NEW TARGETS:

STRENGTHS: Long history and globally strong

position in cables, cable harnessing Developing position in switches

connectors Competitive production conditions

for labor-intensive processes Growing engineering capacity

OPPORTUNITIES: Growing demand for electrical

technology in automotive Cable harnessing will rather grow

in importance Promising growth fields for further

development of the cluster: Advanced cable technology 48V power system Battery technology Electric motors Lighting Mechatronics

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

45

• Cars and commercial vehicles will change

substantially within the next 10 years, while

electronics and IT play the key role in this

development.

• There are many new challenges deriving from

connectivity and autonomous driving requiring

most advanced and most safe electronic systems,

more and more sensors, RF, radar and ultrasonic

devices, as well as more complex passenger

protection systems (airbags, restraint system).

• Many developments will take place in the headquarters

of OEMs and Key Suppliers of electronic systems. However,

there will be a growing need for developing, producing and

testing new components.

CLUSTER STRATEGY | ELECTRONICS

ELECTRONIC COMPONENTS

ELECTRONIC CONTROL

UNITS

MECHA-TRONICPARTS

AIRBAGS

SENSORSAUTO-

NOMOUSDRIVING

MICRO-MECHA-TRONICS

• Tunisia can build on a solid competence in producing

and testing electronic systems, airbags and

mechatronic parts.AUTO-

MOTIVE IT

EXISTING COREDEVELOPMENT OPPORTUNITIES

EXISTING CORE

DEVELOPMENT OPPORTUNITIES

SAFETY SYSTEMS

CONNEC-TIVITY

OPTO-ELEC-

TRONICS

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

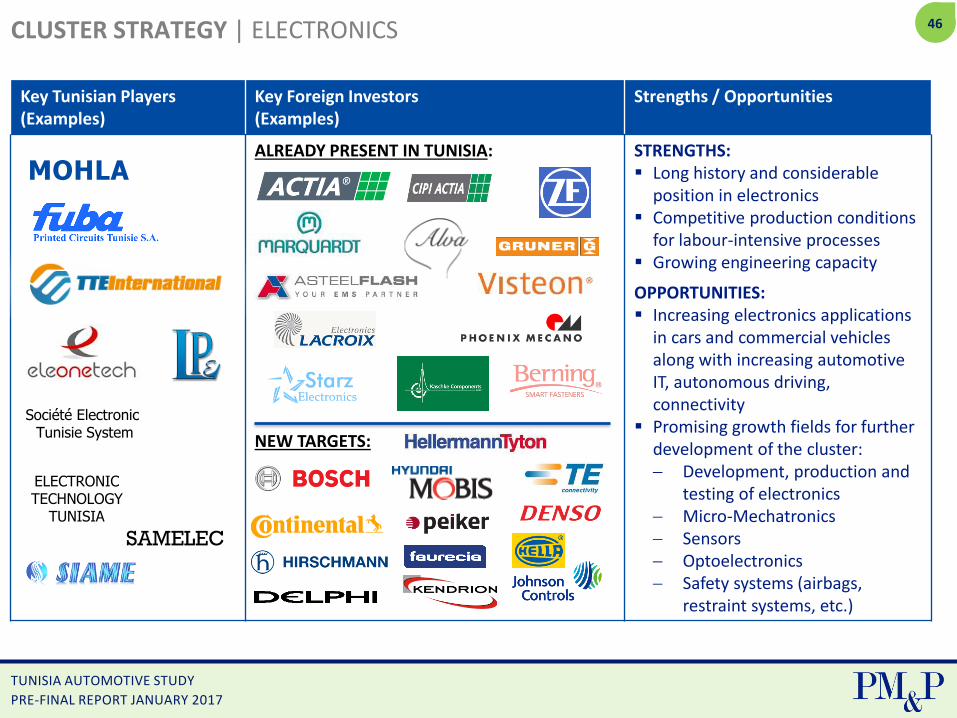

46CLUSTER STRATEGY | ELECTRONICS

Key Tunisian Players(Examples)

Key Foreign Investors(Examples)

Strengths / Opportunities

ALREADY PRESENT IN TUNISIA:

NEW TARGETS:

STRENGTHS: Long history and considerable

position in electronics Competitive production conditions

for labour-intensive processes Growing engineering capacity

OPPORTUNITIES: Increasing electronics applications

in cars and commercial vehicles along with increasing automotive IT, autonomous driving, connectivity

Promising growth fields for further development of the cluster: Development, production and

testing of electronics Micro-Mechatronics Sensors Optoelectronics Safety systems (airbags,

restraint systems, etc.)

MOHLA

Société Electronic Tunisie System

ELECTRONIC TECHNOLOGY

TUNISIA

SAMELEC

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

47

• Supporting the further development of

competence in plastics processing, aiming

at opportunities in the fields of:

– Lightweight components (replacing metal)

– Glassfibre or carbonfibre reinforced plastics

– Thermosetting plastics

• Further developing leather and leather imitate

processing.

• Supporting high performance textiles

development (airbags, restraint systems, fire

resistant textiles, low abrasion textiles for

public transport, etc.)

CLUSTER STRATEGY | INTERIORS / MODULES

TEXTILE INTERIOR

PARTS

LEATHER INTERIOR

PARTS

RUBBER & PLASTIC PARTS

ADVANCED PLASTICS

• Considerable base of interior suppliers despite the

absence of large OEMs.

• Particularly strong in plastics, leather, textiles interior.

EXISTING COREDEVELOPMENT OPPORTUNITIES

EXISTING CORE

DEVELOPMENT OPPORTUNITIESCOMPOSITES

SEATS

STEERING WHEELS

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

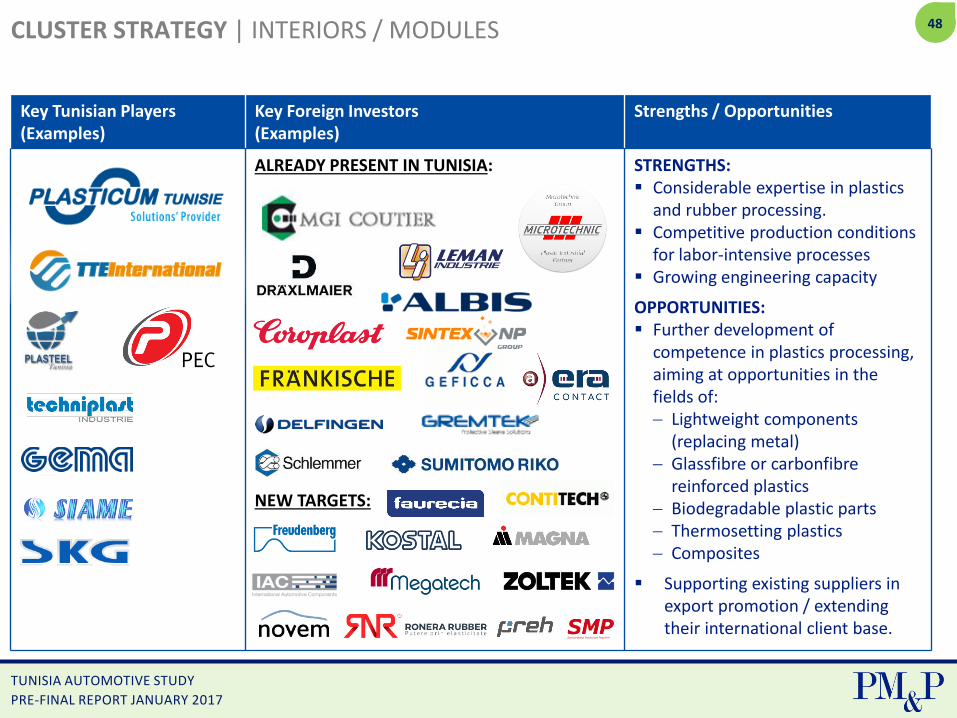

48CLUSTER STRATEGY | INTERIORS / MODULES

Key Tunisian Players(Examples)

Key Foreign Investors(Examples)

Strengths / Opportunities

ALREADY PRESENT IN TUNISIA:

NEW TARGETS:

STRENGTHS: Considerable expertise in plastics

and rubber processing. Competitive production conditions

for labor-intensive processes Growing engineering capacity

OPPORTUNITIES: Further development of

competence in plastics processing, aiming at opportunities in the fields of: Lightweight components

(replacing metal) Glassfibre or carbonfibre

reinforced plastics Biodegradable plastic parts Thermosetting plastics Composites

Supporting existing suppliers in export promotion / extending their international client base.

PEC

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

49

• Supporting export activities of existing

manufacturers of buses and trailers.

• Attracting commercial vehicle OEMs for larger

series production of buses and HCVs.

• Attracting special vehicle manufacturers.

CLUSTER STRATEGY | COMMERCIAL AND SPECIAL VEHICLES

BUSES

TRAILERS

CAR ASSEMBLY

VEHICLE CONVER

SION

SPECIAL VEHICLES

• Considerable core of small series commercial vehicles

manufacturer, trailer and vehicle conversion

• Small number of small series car assembly

EXISTING COREDEVELOPMENT OPPORTUNITIES

EXISTING CORE

DEVELOPMENT OPPORTUNITIESLARGE SERIES COMMERCIAL

VEHICLES

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

50CLUSTER STRATEGY | COMMERCIAL AND SPECIAL VEHICLES

Key Tunisian Players(Examples)

Key Foreign Investors(Examples)

Strengths / Opportunities

ALREADY PRESENT IN TUNISIA:

NEW TARGETS:

STRENGTHS: Considerable structure of Tunisian

manufacturers of bodies for buses, trailers, and vehicle conversion

OPPORTUNITIES: Strengthening local suppliers by

supporting their export activities and increasing production volumes

Attracting new commercial vehicle OEMs with the potential for large scale production

Attracting special vehicles manufacturers

MEDI CARS

IMM

STAFIM

SCCM

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

51CLUSTER STRATEGY | SUMMARY

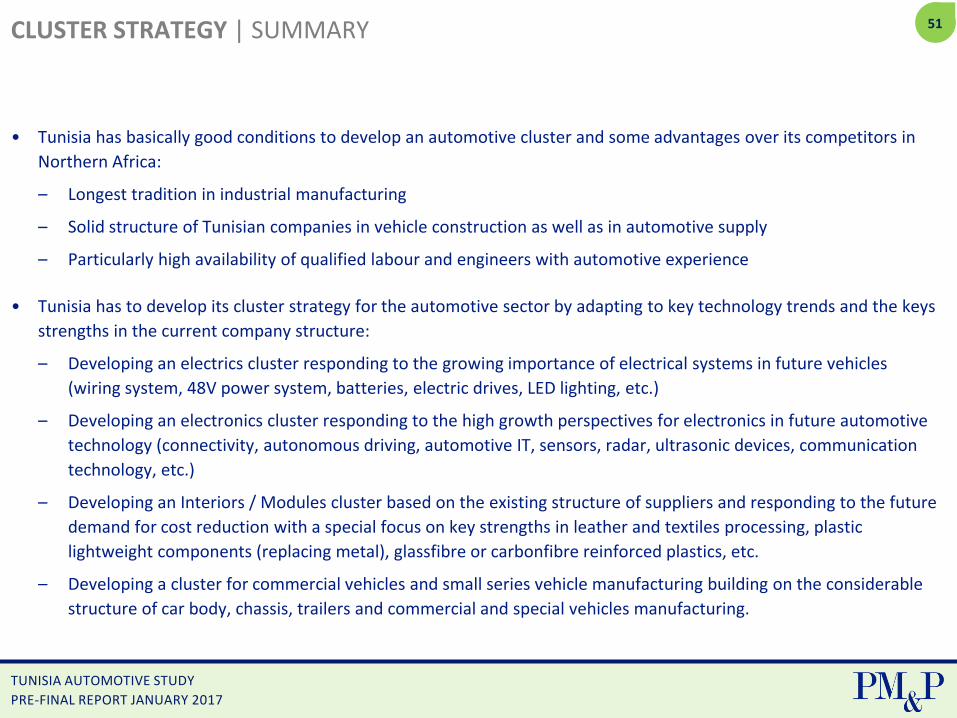

• Tunisia has basically good conditions to develop an automotive cluster and some advantages over its competitors in

Northern Africa:

– Longest tradition in industrial manufacturing

– Solid structure of Tunisian companies in vehicle construction as well as in automotive supply

– Particularly high availability of qualified labour and engineers with automotive experience

• Tunisia has to develop its cluster strategy for the automotive sector by adapting to key technology trends and the keys

strengths in the current company structure:

– Developing an electrics cluster responding to the growing importance of electrical systems in future vehicles

(wiring system, 48V power system, batteries, electric drives, LED lighting, etc.)

– Developing an electronics cluster responding to the high growth perspectives for electronics in future automotive

technology (connectivity, autonomous driving, automotive IT, sensors, radar, ultrasonic devices, communication

technology, etc.)

– Developing an Interiors / Modules cluster based on the existing structure of suppliers and responding to the future

demand for cost reduction with a special focus on key strengths in leather and textiles processing, plastic

lightweight components (replacing metal), glassfibre or carbonfibre reinforced plastics, etc.

– Developing a cluster for commercial vehicles and small series vehicle manufacturing building on the considerable

structure of car body, chassis, trailers and commercial and special vehicles manufacturing.

TUNISIA AUTOMOTIVE STUDY

PRE-FINAL REPORT JANUARY 2017

52

PM & Partner Marketing Consulting GmbH (PM&P)Frankfurt | Munich | Berlinwww.pm-p.de

Andreas Paulicks

(Senior Partner)

Email: [email protected]

Phone: +49 69 668077-36

Cell: +49 172 666 41 60

Sebastian Gerlach

(Senior Consultant)

Email: [email protected]

Phone: +49 30-85408880

Cell: +49 176-24896082

Aida Ben-Achour

(Consultant, Head of Research)

Email: [email protected]

Phone: +49 69 668077-29