Embed Size (px)

Citation preview

Graduate Public FinanceTaxing Top Earners

Owen ZidarPrincetonFall 2017

Lecture 5

Thanks to Emmanuel Saez and David Card for sharing his slides/notes, many of whichare reproduced here. Stephanie Kestelman provided excellent assistance making theseslides.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 1 / 101

Outline

1 Motivation

2 PolicyFederal US income tax policyState and local tax deductionMortgage interest deductionPass-throughs, taxes, and inequalityRecent top income tax reforms

3 TheoryLabor supply theoryOptimal labor income tax progressivity

4 EvidenceEmpirical estimation of e and identification issuesEvidence from Zidar (2017) “Tax cuts for whom?”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 2 / 101

Outline

1 Motivation

2 PolicyFederal US income tax policyState and local tax deductionMortgage interest deductionPass-throughs, taxes, and inequalityRecent top income tax reforms

3 TheoryLabor supply theoryOptimal labor income tax progressivity

4 EvidenceEmpirical estimation of e and identification issuesEvidence from Zidar (2017) “Tax cuts for whom?”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 3 / 101

Credit to Heathcote Storesletten Violante (QJE, forthcoming) for the quote.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 4 / 101

Tax Cuts and Jobs Act

Source: Tax Policy Center.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 5 / 101

Tax Cuts and Jobs Act

Source: Tax Policy Center.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 6 / 101

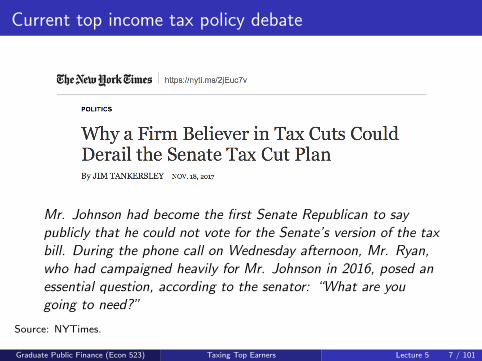

Current top income tax policy debate

Mr. Johnson had become the first Senate Republican to saypublicly that he could not vote for the Senate’s version of the taxbill. During the phone call on Wednesday afternoon, Mr. Ryan,who had campaigned heavily for Mr. Johnson in 2016, posed anessential question, according to the senator: “What are yougoing to need?”

Source: NYTimes.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 7 / 101

Current top income tax policy debate

What Mr. Johnson needs, he said in an interview from Wisconsinon Friday, is for the bill to treat more favorably small businessesand other so-called pass-through entities – businesses whoseprofits are distributed to their owners and taxed at rates forindividuals. Such entities, including Mr. Johnson’s family-runplastics manufacturing business, account for more than half ofthe nation’s business income, and the senator says the tax billwould give an unfair advantage to larger corporations.

“I just have in my heart a real affinity for these owner-operatedpass-throughs,” he said. “We need to make American businessescompetitive – they’re not right now. But in making businessescompetitive, we can’t leave behind the pass-throughs.”

Source: NYTimes.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 8 / 101

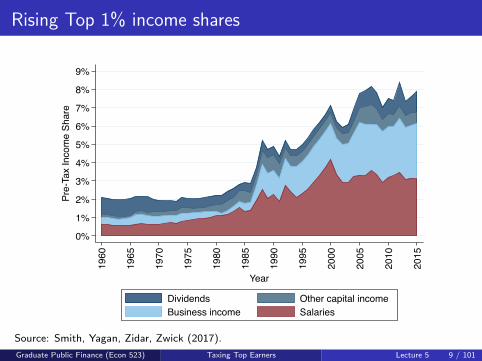

Rising Top 1% income shares

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%Pr

e-Ta

x In

com

e Sh

are

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

Year

Dividends Other capital incomeBusiness income Salaries

Source: Smith, Yagan, Zidar, Zwick (2017).

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 9 / 101

Outline

1 Motivation

2 PolicyFederal US income tax policyState and local tax deductionMortgage interest deductionPass-throughs, taxes, and inequalityRecent top income tax reforms

3 TheoryLabor supply theoryOptimal labor income tax progressivity

4 EvidenceEmpirical estimation of e and identification issuesEvidence from Zidar (2017) “Tax cuts for whom?”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 10 / 101

Federal US Income tax

US income tax assessed on annual family income (not individual)[most other OECD countries have shifted to individual assessment]

Sum all cash income sources from family members (both from laborand capital income sources) = called Adjusted Gross Income (AGI)

Main exclusions: fringe benefits (health insurance, pensioncontributions), imputed rent of homeowners, unrealized capital gains

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 11 / 101

Federal US Income tax

Taxable income = AGI - personal exemptions - deduction

personal exemptions = $4K * # family members (in 2016)

deduction is max of standard deduction or itemized deductions

Standard deduction is a fixed amount depending on family structure($12.6K for couple, $6.3K for single in 2016)

Itemized deductions: (a) state and local taxes paid, (b) mortgageinterest payments, (c) charitable giving, various small other items

About 10% of AGI lost through itemized deductions, called taxexpenditures

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 12 / 101

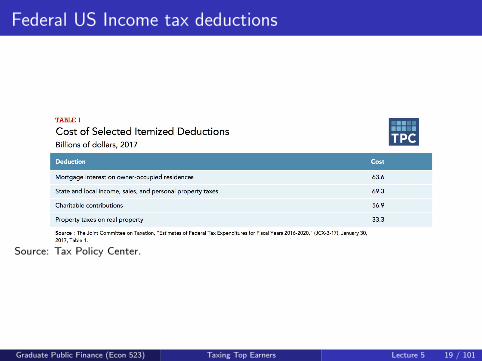

Federal US Income tax deductions

Source: Tax Policy Center.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 13 / 101

Federal US Income tax deductions

0 10 20 30 40Share (%) of National Total

$200K+

[$100K, $200K)

[$75K, 100K)

[$50K, $75K)

[$25K, $50K)

[$0, $25K)

Returns AGIItemized Deductions

Source: Zidar’s calculations of IRS SOI 2013 data

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 14 / 101

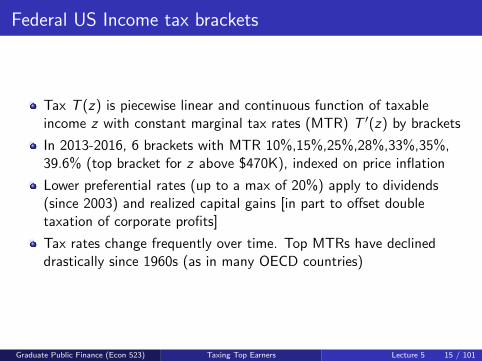

Federal US Income tax brackets

Tax T (z) is piecewise linear and continuous function of taxableincome z with constant marginal tax rates (MTR) T ′(z) by brackets

In 2013-2016, 6 brackets with MTR 10%,15%,25%,28%,33%,35%,39.6% (top bracket for z above $470K), indexed on price inflation

Lower preferential rates (up to a max of 20%) apply to dividends(since 2003) and realized capital gains [in part to offset doubletaxation of corporate profits]

Tax rates change frequently over time. Top MTRs have declineddrastically since 1960s (as in many OECD countries)

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 15 / 101

Federal US Income tax schedule

Source: Saez.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 16 / 101

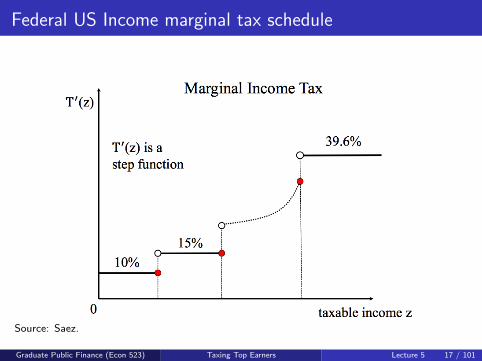

Federal US Income marginal tax schedule

Source: Saez.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 17 / 101

Federal US top income tax rate

Source: Saez.Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 18 / 101

Federal US Income tax deductions

Source: Tax Policy Center.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 19 / 101

State and Local Tax Deduction

Major tax reform proposals, such as the Tax Reform Act of 1986, the2005 President’s Advisory Panel on Federal Tax Reform, and TaxCuts and Job Acts 2017, often propose eliminating or reducing thestate and local tax deduction (SALT), which is one of the largest taxexpenditures in the U.S. tax code and was deemed by PresidentReagan “the most sacred of cows.”

SALT enables taxpayers to deduct state and local income taxes,which lowers tax liabilities by reducing the amount of taxable incomethat is subject to federal income tax.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 20 / 101

State and Local Tax Deduction2015 data from Tax Policy Center

0 50 100State and local tax deduction (billions)

WyomingSouth Dakota

AlaskaNorth Dakota

VermontWest Virginia

MontanaDelaware

New MexicoMississippi

IdahoNevada

MaineHawaii

Rhode IslandNew Hampshire

District of ColumbiaArkansasNebraskaLouisianaAlabama

TennesseeOklahoma

KansasUtahIowa

KentuckySouth Carolina

ArizonaIndiana

MissouriWashington

ColoradoOregon

WisconsinMichigan

MinnesotaNorth Carolina

GeorgiaConnecticut

OhioFloridaVirginia

MarylandMassachusetts

PennsylvaniaTexasIllinois

New JerseyNew YorkCalifornia

Source: TPC 2015 dataGraduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 21 / 101

State and Local Tax Deduction2015 data from Tax Policy Center

0 5 10 15 20Share of Total (%)

WashingtonColorado

OregonWisconsin

North CarolinaMinnesota

MichiganGeorgia

ConnecticutOhio

FloridaVirginia

MarylandMassachusetts

PennsylvaniaTexasIllinois

New JerseyNew YorkCalifornia

SALT Share Fed Income Tax Share

Source: TPC 2015 dataGraduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 22 / 101

State and Local Tax Deduction2015 data from Tax Policy Center

0 5,000 10,000 15,000 20,000Average State and local tax deduction

AlaskaTennessee

AlabamaNevada

South DakotaMississippi

WyomingLouisiana

North DakotaNew Mexico

FloridaWashington

ArizonaTexas

OklahomaUtah

IndianaSouth Carolina

IdahoColoradoArkansas

GeorgiaDelawareMontana

KansasWest Virginia

North CarolinaMichiganMissouri

HawaiiKentucky

New HampshireIowaOhio

NebraskaPennsylvania

VirginiaMaine

WisconsinVermont

Rhode IslandIllinois

OregonMaryland

MinnesotaMassachusetts

District of ColumbiaNew Jersey

CaliforniaConnecticut

New York

Source: TPC 2015 dataGraduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 23 / 101

State and Local Tax Deduction2015 data from Tax Policy Center

0 2 4 6 8 10SALT as % of AGI

AlaskaSouth Dakota

WyomingNorth Dakota

TennesseeNevadaFloridaTexas

LouisianaAlabama

WashingtonNew Mexico

MississippiWest Virginia

OklahomaIndianaArizona

ArkansasKansas

ColoradoMichigan

South CarolinaNew Hampshire

MissouriIdaho

DelawareUtahOhio

North CarolinaMontana

HawaiiKentucky

PennsylvaniaNebraska

IowaGeorgia

IllinoisVirginia

MaineVermont

WisconsinMinnesota

Rhode IslandMassachusetts

District of ColumbiaOregon

MarylandCalifornia

ConnecticutNew Jersey

New York

Source: TPC 2015 dataGraduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 24 / 101

State and Local Tax Deduction2015 data from Tax Policy Center

0 10 20 30 40 50Share of returns in state with deduction (%)

WyomingWest Virginia

VermontSouth DakotaNorth Dakota

MontanaDistrict of Columbia

DelawareAlaska

Rhode IslandNew Mexico

New HampshireNebraska

MaineIdaho

HawaiiNevada

MississippiKansas

ArkansasUtah

OklahomaIowa

LouisianaKentuckyAlabama

TennesseeSouth Carolina

OregonMissouriIndiana

ConnecticutArizona

WisconsinMinnesotaColorado

WashingtonNorth Carolina

MichiganMassachusetts

MarylandVirginia

OhioGeorgia

PennsylvaniaNew Jersey

IllinoisFloridaTexas

New YorkCalifornia

Source: TPC 2015 dataGraduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 25 / 101

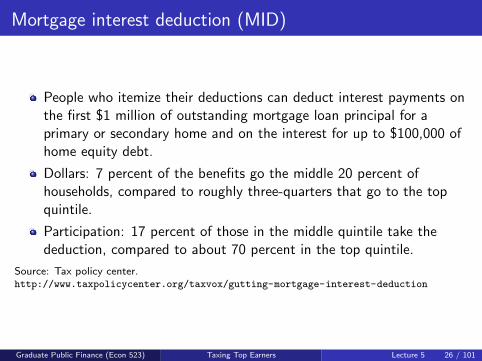

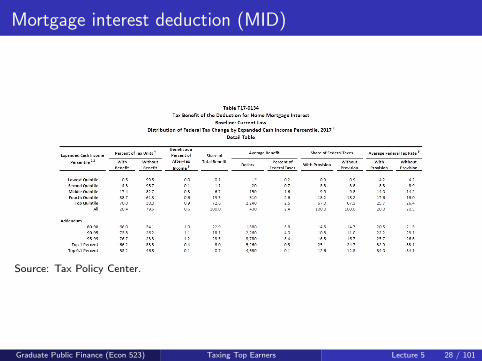

Mortgage interest deduction (MID)

People who itemize their deductions can deduct interest payments onthe first $1 million of outstanding mortgage loan principal for aprimary or secondary home and on the interest for up to $100,000 ofhome equity debt.

Dollars: 7 percent of the benefits go the middle 20 percent ofhouseholds, compared to roughly three-quarters that go to the topquintile.

Participation: 17 percent of those in the middle quintile take thededuction, compared to about 70 percent in the top quintile.

Source: Tax policy center.http://www.taxpolicycenter.org/taxvox/gutting-mortgage-interest-deduction

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 26 / 101

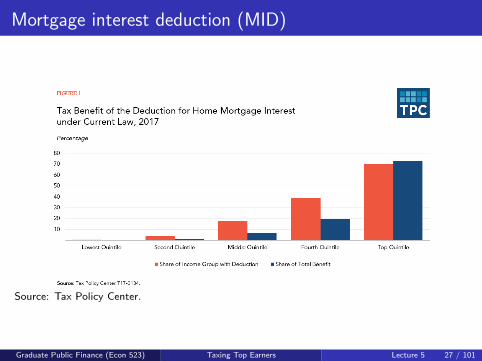

Mortgage interest deduction (MID)

Source: Tax Policy Center.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 27 / 101

Mortgage interest deduction (MID)

Source: Tax Policy Center.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 28 / 101

Recent top income tax reforms

Source: Saez (TPE, 2017).

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 29 / 101

Recent top income tax reforms

Source: Saez (TPE, 2017).

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 30 / 101

Outline

1 Motivation

2 PolicyFederal US income tax policyState and local tax deductionMortgage interest deductionPass-throughs, taxes, and inequalityRecent top income tax reforms

3 TheoryLabor supply theoryOptimal labor income tax progressivity

4 EvidenceEmpirical estimation of e and identification issuesEvidence from Zidar (2017) “Tax cuts for whom?”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 31 / 101

Progressive tax distorts consumption-leisure choices

A key question: how much do hours of work (H2 vs H1) increase when taxschedule becomes flatter?

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 32 / 101

Outline

Review of basic consumer theory

Demand function

Expenditure and indirect utility

Using the expenditure function

Applications

Static labor supply

Deadweight loss of labor income taxation

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 33 / 101

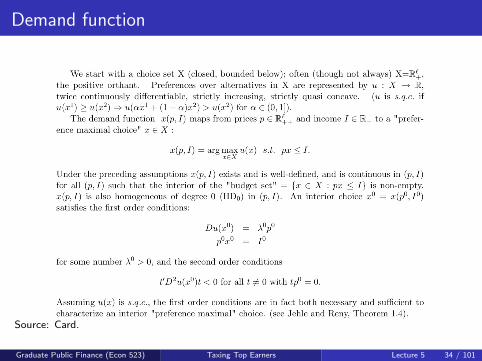

Demand function

Source: Card.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 34 / 101

Expenditure function

Source: Card.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 35 / 101

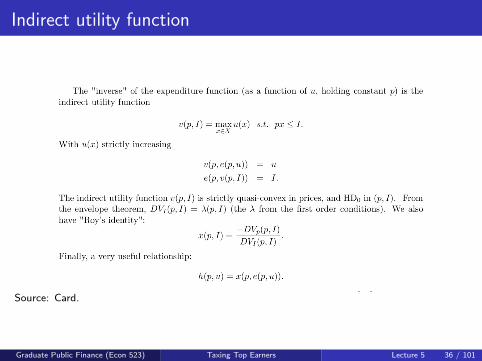

Indirect utility function

Source: Card.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 36 / 101

Slutsky decomposition

Source: Card.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 37 / 101

Using the expenditure function: setup

Source: Card.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 38 / 101

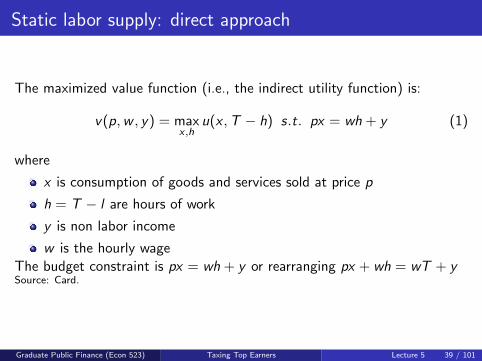

Static labor supply: direct approach

The maximized value function (i.e., the indirect utility function) is:

v(p,w , y) = maxx ,h

u(x ,T − h) s.t. px = wh + y (1)

where

x is consumption of goods and services sold at price p

h = T − l are hours of work

y is non labor income

w is the hourly wageThe budget constraint is px = wh + y or rearranging px + wh = wT + ySource: Card.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 39 / 101

Static labor supply: direct approach to solve for h(p,w , y)

Source: Card.Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 40 / 101

Static labor supply: indirect expenditure function approachto solve for hc(p,w , u)

Source: Card.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 41 / 101

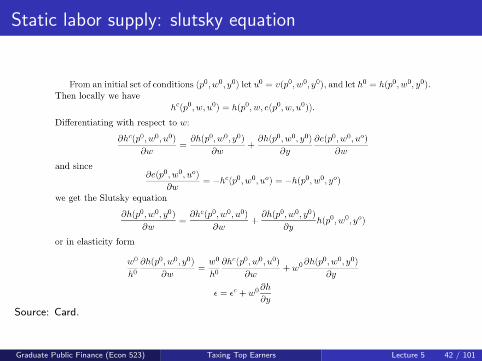

Static labor supply: slutsky equation

Source: Card.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 42 / 101

Income effect w ∂h∂y and the budget constraint

From the budget constraint

px = wh + y (2)

p∂x

∂y= w

∂h

∂y+ 1 (3)

−(1− p∂x

∂y︸︷︷︸mpe

) = w∂h

∂y(4)

where

mpe is marginal increase in total spending on goods and services ifnon-labor income goes up by 1 dollar

1−mpe is marginal increase in total spending on leisure whennon-labor income raises by 1 dollar

Leisure is a normal good so 1−mpe > 0

Source: Card.Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 43 / 101

Slutsky equation

ε = εC + w0 ∂h

∂y(5)

where the classic benchmarks for US male workers are:

ε ∈ [−.1, .2]

εc ≈ .1 to .3

1−mpe ≈ .1 to .2

Source: Card.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 44 / 101

Application of expenditure function: DWL

Source: Card.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 45 / 101

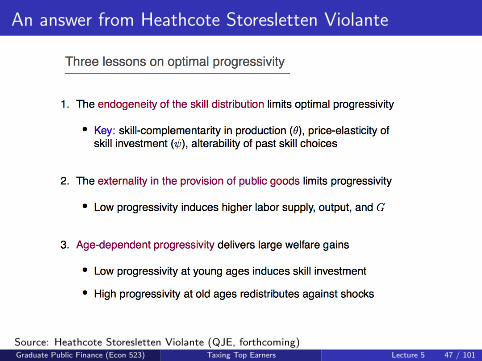

How progressive should labor income tax be?

What is the optimal degree of tax progressivity when households economicoutcomes are determined by their initial ability, partially insurable wageshocks, taste for work, and human capital investment?

Argument in favor of progressivity: missing markets

Social insurance of privately-uninsurable lifecycle shocksRedistribution with respect to unequal initial conditions

Argument against progressivity: distortions

Labor supplyHuman capital investment

Another consideration - fiscal externality

Financing of public good provision

Source: Heathcote Storesletten Violante (QJE, forthcoming)

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 46 / 101

An answer from Heathcote Storesletten Violante

Source: Heathcote Storesletten Violante (QJE, forthcoming)Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 47 / 101

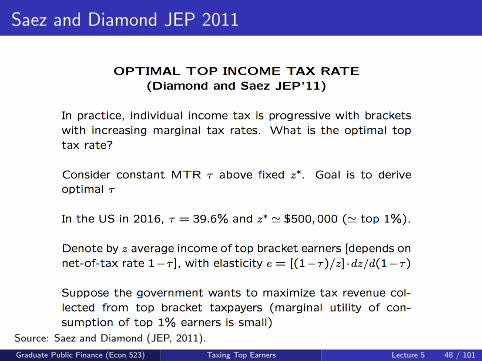

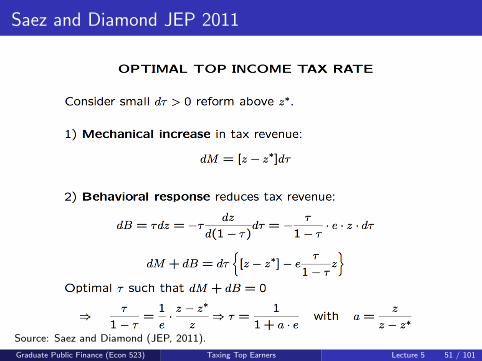

Saez and Diamond JEP 2011

Source: Saez and Diamond (JEP, 2011).

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 48 / 101

Saez and Diamond JEP 2011

Source: Saez and Diamond (JEP, 2011).Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 49 / 101

Saez and Diamond JEP 2011

Source: Saez and Diamond (JEP, 2011).Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 50 / 101

Saez and Diamond JEP 2011

Source: Saez and Diamond (JEP, 2011).

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 51 / 101

Saez and Diamond JEP 2011

Source: Saez and Diamond (JEP, 2011).

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 52 / 101

Outline

1 Motivation

2 PolicyFederal US income tax policyState and local tax deductionMortgage interest deductionPass-throughs, taxes, and inequalityRecent top income tax reforms

3 TheoryLabor supply theoryOptimal labor income tax progressivity

4 EvidenceEmpirical estimation of e and identification issuesEvidence from Zidar (2017) “Tax cuts for whom?”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 53 / 101

Basic empirical strategy

Assume:

No income effects on reported income

Immediate and permanent response to tax rates

e constant over time and uniform across individuals at all income levels

Individuals have perfect knowledge of the tax structure and choose zitafter they know z0

it exactly

In year t, i individual reports income zit and faces τit = T ′(zit).Reported income zit = z0

it(1− τit)e , where e is ETI and z0it is income

reported when τit = 0 (i.e., potential income)

We can estimate e using

log zit = e log(1− τit) + log z0it

The last equation cannot be identified using OLS if τ is correlatedwith income z0

it , so need to instrument τit

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 54 / 101

Share AnalysisEstimating ETI using 2+ years/periods of data

Assume that no tax change for individuals outside the top groups

Estimate elasticity of reported income around a tax reform episode,where t0 and t1 are pre- and post-reform years

e =log st1 − log st0

log(1− τs,t1)− log(1− τs,t0)

st : share of income accruing to the top 1% earners in t

τs,t : income-weighted avg marginal tax rate faced by taxpayers in thisincome group in t

Identification assumption: Absent the tax change, the share wouldhave remained constant from year t0 to t1 (on average)

Using full time series: estimate a time-series regression of the form

log st = e log(1− τs,t) + εt

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 55 / 101

Saez (TPE, 2017) “Taxing the Rich More”

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 56 / 101

Use a share analysis

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 57 / 101

Relate share changes to 2013 tax rate changes

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 58 / 101

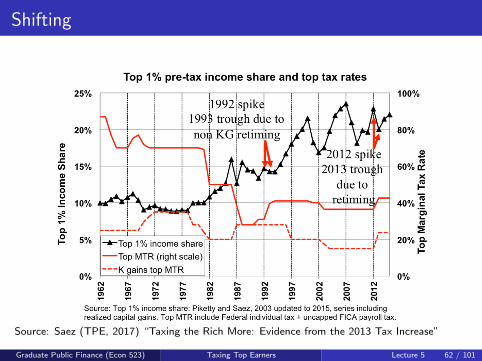

Shifting

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 59 / 101

Shifting

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 60 / 101

Shifting

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 61 / 101

Shifting

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 62 / 101

A control group?

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 63 / 101

Standard share analysis

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 64 / 101

Elasticity estimate with shifting

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 65 / 101

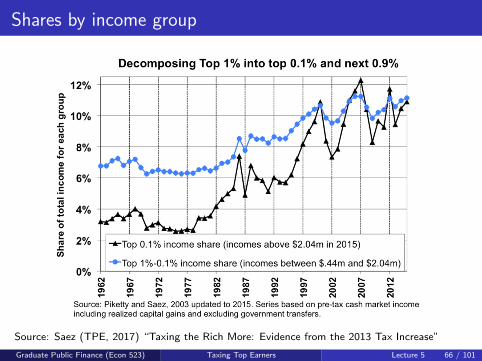

Shares by income group

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 66 / 101

Elasticity estimate with shifting for top 1% to top 0.1%

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 67 / 101

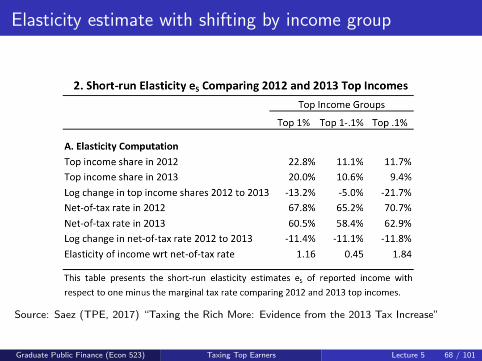

Elasticity estimate with shifting by income group

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 68 / 101

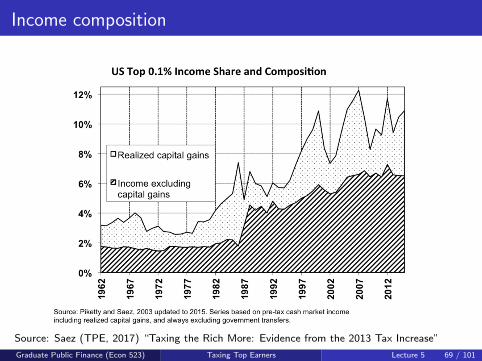

Income composition

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 69 / 101

Income composition

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 70 / 101

Income composition

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 71 / 101

Income composition

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 72 / 101

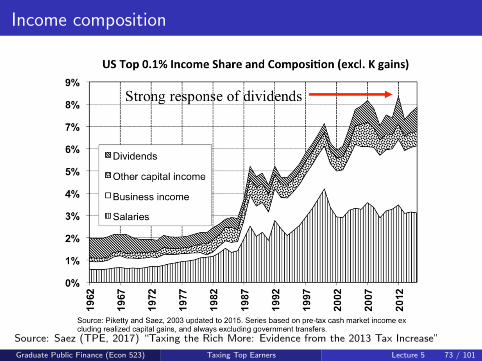

Income composition

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 73 / 101

Income composition

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 74 / 101

Income composition

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 75 / 101

Income composition

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 76 / 101

Income composition

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 77 / 101

Medium-term elasticity

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 78 / 101

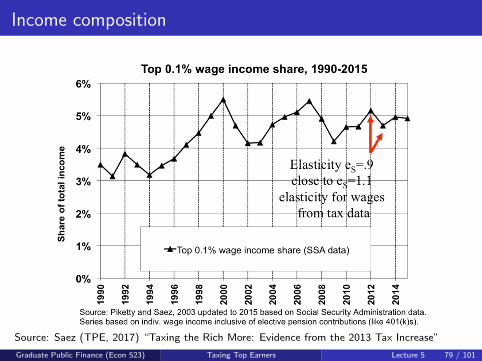

Income composition

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 79 / 101

Which trend?

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 80 / 101

Which trend?

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 81 / 101

Which trend?

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 82 / 101

Which trend?

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 83 / 101

Implied elasticity depends on trend

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 84 / 101

Implied elasticity depends on trend

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 85 / 101

Medium-term elasticity estimates

Source: Saez (TPE, 2017) “Taxing the Rich More: Evidence from the 2013 Tax Increase”

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 86 / 101

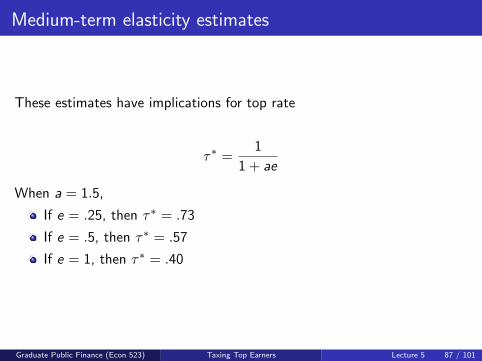

Medium-term elasticity estimates

These estimates have implications for top rate

τ∗ =1

1 + ae

When a = 1.5,

If e = .25, then τ∗ = .73

If e = .5, then τ∗ = .57

If e = 1, then τ∗ = .40

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 87 / 101

Summary of empirical evidence of ETI

e Estimation

Feldstein (1995) 1-3 Tabulated diff-in-diff, OLS. The differencein the % change in taxable income between T and C

is divided by the difference in the % change in theaverage net-of-tax-rate between T and C .

Auten and Carroll (1999) 0.55 2SLS, regress change in log AGI between 1985 and 1989against change in log net-of-tax rate. Instrument for change

in net-of-tax rate by inflating adjusted 1985 incomes by the CPI to1989 levels and then applying 1989 law to these incomes.

Moffitt and Wilhelm (2000) 0.35-0.97 Moffitt and Wilhelm calculate e using Feldstein’s (1995)approach, which yields e rom 1.76 to 1.99, and a 2SLS regressionapproach, employing alternative instruments for the change in the

net-of-tax rate. Those instruments that are successful yield e ∈ [0.35, 0.97].

Gruber and Saez (2002) 0.17 (broad income 2SLS. Instrument for the change in the net-of-tax rateof top earners) using an instrument very similar to that used by Auten and Carroll (1999).

They also construct an analogous instrument for capturing the income effect,the log change in after-tax income assuming that base year income grows at

the same rate as total income.

Kopczuk (2005) 0.12 (no deductions) and Investigates the hypothesis that the ETI is not a structural parameter.1.06 (deductible-share Includes instrumented changes in marginal tax rates and an interaction

interaction term) term between the change in tax rate and change in tax base.

Giertz (2007) 0.12-0.30, depending Methods of Gruber and Saez (2002) to larger panel data sets of tax returnson years included from 1979 to 2001. Results vary if using taxable vs. broad income.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 88 / 101

Explaining empirical findings

No reason to expect a universal parameter:

Kopczuk (2002) argues that the ETI is a function of preferences andthe breadth of the tax base and tax enforcement)

Giertz (2007): elasticity w.r.t. taxable income varies much more bydecade than the elasticity w.r.t. broad income → changing rules fordeductions affects the taxable income elasticity

Methodological issues drive the differences between decades:

Model is unable to adequately control for exogenous income trends →non-tax-related aspects of income inequality trend could bias ETIestimates upward when top tax rates fall and downward when they rise

Models fail to capture important types of income shifting, such as theshifting between the corporate and individual income tax base

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 89 / 101

A classic debate

There are two ideas of government. There are those who believethat if you just legislate to make the well-to-do prosperous, thattheir prosperity will leak through on those below. TheDemocratic idea has been that if you legislate to make themasses prosperous their prosperity will find its way up andthrough every class that rests upon it.

—William Jennings Bryan (July, 1896)

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 90 / 101

Two views

Consequences of changing tax policy for different groups are fiercelydebated

1 Tax changes for high income earners “trickle down” and are the mosteffective way to affect prosperity

Higher marginal tax rates for top-income taxpayers lead to largedistortions in labor supply, investment, and hiring, so tax cuts fortop-income taxpayers most effectively increase aggregate economicactivity.

2 Others contend the opposite

Lower-income groups have higher marginal propensities to consumeand disincentives to work from means-tested benefits, so tax cuts forlower-income groups generate sizable consumption and labor supplyresponses, and thereby, more overall activity

Source: Zidar (2017)

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 91 / 101

Research Question

Question:

Do tax changes for high-income earners “trickle down?”

Would these effects be larger if the tax changes were less targeted atthe top?

Variation in income tax policy in the U.S. can help us answer thesequestions and inform this debate

Source: Zidar (2017)

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 92 / 101

Tax changes for each income percentile

Source: Zidar (2017)

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 93 / 101

Zidar (2017)

Quantifies the importance of the distribution of tax changes for theiroverall impact on economic activity

New data using tax returns from NBER TAXSIM

New variation from federal tax shocks × variation in incomedistribution across states

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 94 / 101

Federal tax changes by income group

Source: Zidar (2017)

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 95 / 101

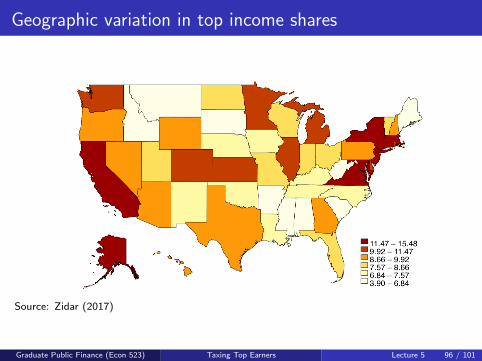

Geographic variation in top income shares

Source: Zidar (2017)

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 96 / 101

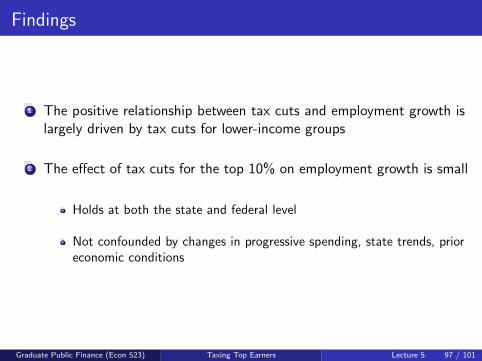

Findings

1 The positive relationship between tax cuts and employment growth islargely driven by tax cuts for lower-income groups

2 The effect of tax cuts for the top 10% on employment growth is small

Holds at both the state and federal level

Not confounded by changes in progressive spending, state trends, prioreconomic conditions

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 97 / 101

State: employment to populaiton

Source: Zidar (2017)Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 98 / 101

State: employment

Source: Zidar (2017)Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 99 / 101

State: real wage increase ⇒ LS response

Source: Zidar (2017)

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 100 / 101

State: consumption effects ⇒ demand response

Source: Zidar (2017)

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 101 / 101

Appendix

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 102 / 101

Basic model of top income taxation

Top-income individual solves

maxc,l

u(c , l) s.t. c = wl(1− τ) + E

c : disposable incomel : labor supply measured in hours of workw : the exogenous wage rateτ is the top marginal tax rateE is non-taxable endowment/virtual income

Issue: w might depend on individual effort, tax rates andopportunities for evasion ⇒ reported taxable income might differfrom wl

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 103 / 101

Feldstein (1999): Using reported income

Feldstein (1999): Individual problem is

maxc,z(l)

u(c , z(l)) s.t. c = z(l)(1− τ) + E

z : reported taxable income s.t. ∂u/∂z < 0τ : top marginal tax rate for earners with income above z̄

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 104 / 101

Elasticity of taxable income (ETI) in basic framework

Individual ETI e is

ei =1− τzi

∂zi∂(1− τ)

Aggregate ETI is the weighted average of individual ETI

e =1− τzm

∂zm

∂(1− τ)

zm: average reported taxable income across N individuals in the topbrackete captures not only the hours of work response, but also all otherbehavioral responses to marginal tax rates

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 105 / 101

Effects of tax change in basic framework

Suppose gov increases top rate τ

Assume no income effects, revenue changes through two channels:

1 Mechanical effect M: “mechanical” increase in tax revenue due highertax rate, absent behavioral response

dM ≡ N(zm − z̄)dτ > 0

2 Behavioral response B: changes in reported income due to greaterincentive to evade and lower incentive to generate income

dB ≡ −Nezm τ

1− τdτ < 0

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 106 / 101

Impact of tax change on total revenue in basic framework

Total change in revenue R is the sum of the mechanical andbehavioral effects:

dR = dM + dB

= N(zm − z̄)

[1− e

zm

zm − z̄

τ

1− τ

]dτ

Define a = zm

zm−z̄ to measure the “thinness” of the top tail of theincome distribution. Rewrite the above equation as

dR = dM

[1− τ

1− τea

]⇒ The fraction of tax revenue lost through behavioral responses is afunction increasing in τ , e and a

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 107 / 101

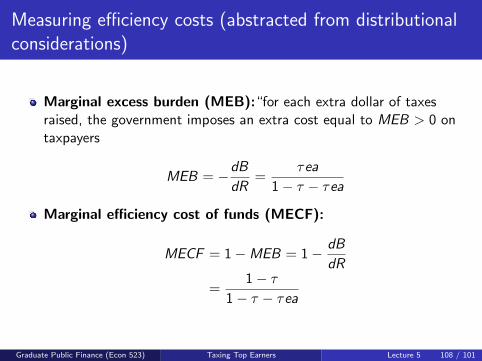

Measuring efficiency costs (abstracted from distributionalconsiderations)

Marginal excess burden (MEB):“for each extra dollar of taxesraised, the government imposes an extra cost equal to MEB > 0 ontaxpayers

MEB = −dB

dR=

τea

1− τ − τea

Marginal efficiency cost of funds (MECF):

MECF = 1−MEB = 1− dB

dR

=1− τ

1− τ − τea

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 108 / 101

Revenue maximizing τ in basic framework

Revenue maximizing τ∗ is the rate when dR = dM + dB = 0:

τ∗ =1

1 + ae

Using e = 0.25 and a = 1.5, τ∗ = 72.7% >> 42.5% when combiningall taxes

In the basic model e is a sufficient statistic to estimate the efficiencycosts of taxation

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 109 / 101

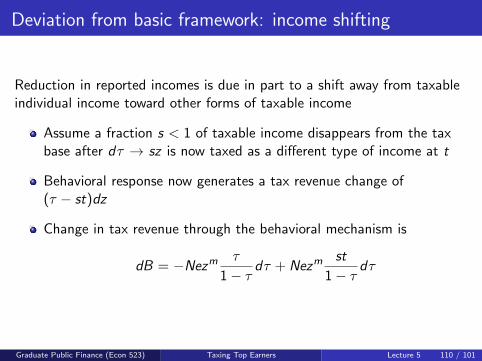

Deviation from basic framework: income shifting

Reduction in reported incomes is due in part to a shift away from taxableindividual income toward other forms of taxable income

Assume a fraction s < 1 of taxable income disappears from the taxbase after dτ → sz is now taxed as a different type of income at t

Behavioral response now generates a tax revenue change of(τ − st)dz

Change in tax revenue through the behavioral mechanism is

dB = −Nezm τ

1− τdτ + Nezm

st

1− τdτ

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 110 / 101

Deviation from basic framework: income shifting

Total revenue change dR is

dR = dM

[1− τ − st

1− τea

]MEB is

MEBs =(τ − st)ea

1− τ − (τ − st)ea

Revenue maximizing tax rate τ∗ is

τ∗s =1 + stae

1 + ae> τ∗

Using e = 0.25, a = 1.5, τ = 42.5%, s = .5 and t = 30% ,τ∗s = 76.8%

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 111 / 101

Deviation from basic framework: income shifting

Implications of income shifting:

s and t must be included in the calculations about DWL of taxation

Individual vs Corporate taxation Responsiveness of incomeclassification to tax rates on different bases

Timing responses: if individuals and firms expect tax changes, theyhave incentives to accelerate or slow taxable income realizationsbefore the tax change takes place. Similarly, if current vs. futureincome taxes change, individuals have an incentive to change theirbehavior

Short vs long run responses may differ due to adjustment costs. LRresponses are particularly important for understanding savings andcapital accumulation

Tax evasion: elasticity of reported vs. actual income may differ

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 112 / 101

Deviation from basic framework: classic externalities

Suppose a fraction s of taxable income response to a tax rate increasedτ is due to higher expenditures on activities that create anexternality

Externality has social marginal value of exactly t dollars per dollar ofadditional expenditure

Behavioral effect is the same as when income shifts

dB = −Nezm τ

1− τdτ + Nezm

st

1− τdτ

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 113 / 101

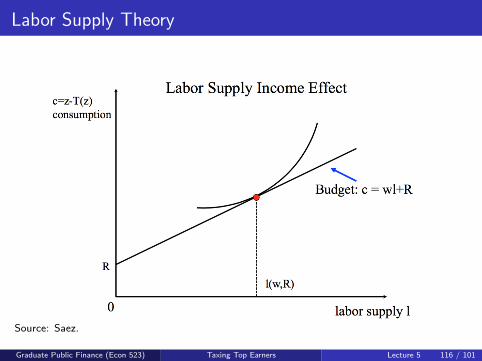

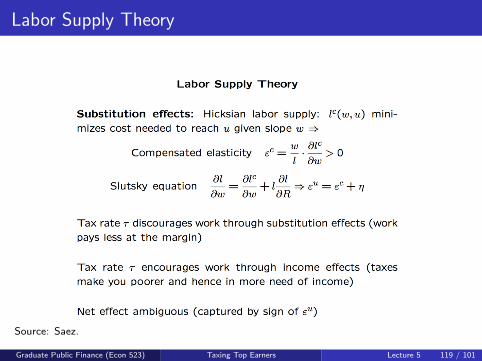

Labor Supply Theory

Source: Saez.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 114 / 101

Labor Supply Theory

Source: Saez.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 115 / 101

Labor Supply Theory

Source: Saez.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 116 / 101

Labor Supply Theory

Source: Saez.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 117 / 101

Labor Supply Theory

Source: Saez.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 118 / 101

Labor Supply Theory

Source: Saez.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 119 / 101

Labor Supply Theory

Source: Saez.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 120 / 101

Labor Supply Theory

Source: Saez.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 121 / 101

Labor Supply Theory

Source: Saez.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 122 / 101

Labor Supply Theory

Source: Saez.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 123 / 101

Labor Supply Theory

Source: Saez.

Graduate Public Finance (Econ 523) Taxing Top Earners Lecture 5 124 / 101