Upload

lerie-pereira

View

215

Download

0

Embed Size (px)

Citation preview

8/18/2019 Good Governance Final (1)

1/72

8/18/2019 Good Governance Final (1)

2/72

8/18/2019 Good Governance Final (1)

3/72

CHAPTER-1 INTRODUCTION

1.1 PERSPECTIVE

The concept of "governance" is not new. It is as old as human civilization. Simply put "governance"

means: “the process of decision-making and the process y which decisions are implemented !or not

implemented#. $overnance can e used in several conte%ts such as corporate governance& international

governance& national governance and local governance. Since governance is the process of decision

making and the process y which decisions are implemented& an analysis of governance focuses on the

formal and informal actors involved in decision-making and implementing the decisions made and the

formal and informal structures that have een set in place to arrive at and implement the decision.

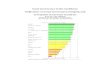

FIG 1 CHARECTERSTICS OF GOOD GOVERNANCE

$ood governance has ' ma(or characteristics. It is participatory& consensus oriented& accountale&

transparent& responsive& effective and efficient& e)uitale and inclusive and follows the rule of law. It

assures that corruption is minimized& the views of minorities are taken into account and that the voices of

the most vulnerale in society are heard in decision-making. It is also responsive to the present and future

needs of society.

8/18/2019 Good Governance Final (1)

4/72

PARTICIPATORY:

*articipation y oth men and women is a key cornerstone of good governance. *articipation could e

either direct or through legitimate intermediate institutions or representatives. It is important to point out

that representative democracy does not necessarily mean that the concerns of the most vulnerale in

society would e taken into consideration in decision making. *articipation needs to e informed and

organized. This means freedom of association and e%pression on the one hand and an organized civil

society on the other hand.

+ase-let:

Initiatives such as talent review and (o rotation systems& continuous improvement and value engineering

programs& tools such as video conferencing& , /nline,& special dialogues with senior management&

meetings& conferences and seminars have helped to uild a homogeneous and focused team at Tata Steel&

increasing motivation and inding to the vision of the company& and spurred employees to deliver targets

on a participatory management asis leading to ownership of processes.

RULE OF LAW:

any institutions identify a fair& impartial& and accessile (ustice system and a representative government

as key elements of the rule of law. The term “rule of law is used to mean independent& efficient& and

accessile (udicial and legal systems& with a government that applies fair and e)uitale laws e)ually&

consistently& coherently& and prospectively to all of its people.

Indeed& the strength of the rule of law is the est predictor of a country0s economic success. 1urthermore&

deficiency in the rule of law encourages high rates of corruption& with further devastating conse)uences

on the confidence of economic actors.

TRANSPARENCY:

Transparency means that decisions taken and their enforcement are done in a manner that follows rules

and regulations. It also means that information is freely availale and directly accessile to those who will

e affected y such decisions and their enforcement. It also means that enough information is provided

and that it is provided in easily understandale forms and media.

+ase-let:

2irtel was ranked fourth across 2sia and 2frica in a list of 344 emerging market multinational companies

as part of a study on corporate transparency and reporting y Transparency International. The +ompanies

were ranked on three parameters:

8/18/2019 Good Governance Final (1)

5/72

5 6eporting on anti-corruption programmes: covering inter alia riery& facilitation payments& whistle-

lower protection and political contriutions.

5 /rganisational transparency: including information aout corporate holdings.

5 +ountry-y-country reporting: including revenues& capital e%penditure and ta% payments.

7harti 2irtel scored '89 on 6eporting on anti-corruption programmes against an average score of ;9.

The score for /rganisational Transparency was 9.

RESPONSIVENESS:

$ood governance re)uires that institutions and processes try to serve all stakeholders within a reasonale

timeframe.

+ase-let:

?ipro won the most ethical company of the world @438 award y the Athisphere Institute.

?ipro +ares is ?ipro0s community initiative focused on certain key developmental issues faced y

underserved and underprivileged communities. It is a trust formed in the year @44= that seeks to work

with communities pro%imate to ?ipro0s center of operations. ?ipro +ares is currently engaged in 3;

pro(ects across India. Through seven of its health care pro(ects in four states of India ?ipro +ares is

providing more than

8/18/2019 Good Governance Final (1)

6/72

EQUITY AND INCLUSIVENESS:

2 society0s welleing depends on ensuring that all its memers feel that they have a stake in it and do not

feel e%cluded from the mainstream of society.

+ase-let:

Tata +onsultancy Services is the iggest employer of women in India. /ut of the =.4; lakh strong

workforce& more than 3 lakh employees are women. The company firmly elieves in gender e)uality and

giving similar opportunities for men and women as far as recruitment and promotions are concerned.

EFFECTIVE AND EFFICIENCY:

$ood governance means that processes and institutions produce results that meet the needs of society

while making the est use of resources at their disposal. The concept of efficiency in the conte%t of good

governance also covers the sustainale use of natural resources and the protection of the environment.

+ase-let:

DEF: *ro(ect aims to create sustainale supply chains across =' districts of India.

Solidaridad and Dindustan Enilever 1oundation !DE1# have (ointly launched one of the largest water

linked sustainale supply chain interventions in India that aims to cumulatively and collectively save 4.

to 3 trillion litres of water through sustainale agriculture. The programme aims to create large-scale

water saving mechanisms that touch

8/18/2019 Good Governance Final (1)

7/72

making. Since soaps are a sizeale part of our usiness& the new technology cuts caron emissions y

38&444 tons per year.

1.2 BRIEF HISTORY OF GOVERNANCE

The term Hgovernance0 was first used in the sense in which it is deployed today y the ?orld 7ank in a 3>'> report on 2frican economies. Trying to account for the failure of its Structural 2d(ustment

*rogrammes !S2*s#& the ?orld 7ank put the lame on a “crisis of governance.

7ut Hcrisis of governance0 doesn0t convey much unless one defines Hgovernance0. The ?orld 7ank

initially defined it simply as “the e%ercise of political power to manage a nation0s affairs. This early

definition is )uite indicative of the animating logic and future discursive career of governance: it is silent

on the legitimacy or otherwise of the political power in )uestion. So whether the 7ank0s client was a

democracy or a dictatorship didn0t matter. ?hat mattered for governance is that efficient management

must trump politics. Afficient management& (ust to e clear& means the withdrawal of the state in favour of

the market. /ver the years& the ?orld 7ank e%panded its Hgovernance0 model to include elements of a

lieral democracy& such as a legal framework for enforcement of contracts& accountaility& etc. 2t the

same time& it rokered a marriage etween governance and development. Gations deemed to e in need of

Hdevelopment0 could now e told that the only way to get Hdevelopment0 is through Hgovernance0 that

is& y emracing the free market.

7ut for this& it was necessary to first create a demand for good governance. That meant identifying the

markers of Had governance0. Enfortunately& what constitutes Had governance0 in the neo-lieral te%t

ook an activist state trying to even out socio-economic disparities through distriutive (ustice is

rather popular among the masses& especially the poor. In an electoral democracy& a direct attack on

welfare was never going to resonate eyond the rich and middle-classes& as successive governments in

India have found to their cost.

1.3 PRIVATE SECTOR ENGAGEMENT FOR GOOD GOVERNANCE

India was a latecomer to economic reforms& emarking on the process in earnest only in 3>>3& in the

wake of an e%ceptionally severe alance of payments crisis. The need for a policy shift had ecome

evident much earlier& as many countries in Aast 2sia achieved high growth and poverty reduction through

policies which emphasized greater e%port orientation and encouragement of the private sector. India took

some steps in this direction in the 3>'4s& ut it was not until 3>>3 that the government signalled a

systemic shift to a more open economy with greater reliance upon market forces& a larger role for the

private sector including foreign investment& and a restructuring of the role of government.

8/18/2019 Good Governance Final (1)

8/72

CHAPTER-2 CORPORATE GOVERNANCE IN

INDIA

2.1 CONCEPTUAL FRAMEWORK

+orporate governance involves a set of relationships amongst the company0s management& its oard of

directors& its shareholders& its auditors and other stakeholders. These relationships& which involve various

rules and incentives& provide the structure through which the o(ectives of the company are set& and the

means of attaining these o(ectives as well as monitoring performance are determined. Thus& the key

aspects of good corporate governance include transparency of corporate structures and operationsJ the

accountaility of managers and the oards to shareholdersJ and corporate responsiility towards

stakeholders.

?hile corporate governance essentially lays down the framework for creating long-term trust etween

companies and the e%ternal providers of capital& it would e wrong to think that the importance of

corporate governance lies solely in etter access of finance. +ompanies around the world are realizing

that etter corporate governance adds considerale value to their operational performance:

• It improves strategic thinking at the top y inducting independent directors who ring a wealth of

e%perience& and a host of new ideas

• It rationalizes the management and monitoring of risk that a firm faces gloally

•It limits the liaility of top management and directors& y carefully articulating the decision making process

• It assures the integrity of financial reports

It has long term reputational effects among key stakeholders& oth internally and e%ternally

In a roader sense& however& good corporate governance- the e%tent to which companies is run in an open

and honest manner- is important for overall market confidence& the efficiency of capital allocation& the

growth and development of countries0 industrial ases& and ultimately the nations0 overall wealth and

welfare.

8/18/2019 Good Governance Final (1)

9/72

CHAPTER-3 Principles of CorporateGoernance

G20/OECD P!"#!$%&' () C($(*+& G(,&"*"#&

K&- P(!"+'

E"'!" +& *'!' )( *" &))+!,& #($(*+& (,&"*"#& )*&(45

2. The corporate governance framework should e developed with a view to its impact on overall

economic performance& market integrity and the incentives it creates for market participants and

the promotion of transparent and well-functioning markets.

7. The legal and regulatory re)uirements that affect corporate governance practices should e

consistent with the rule of law& transparent and enforceale.

+. The division of responsiilities among different authorities should e clearly articulated and

designed to serve the pulic interest.

. Stock market regulation should support effective corporate governance.

A. Supervisory& regulatory and enforcement authorities should have the authority& integrity and

resources to fulfil their duties in a professional and o(ective manner. oreover& their rulings

should e timely& transparent and fully e%plained.

1. +ross-order co-operation should e enhanced& including through ilateral and multilateral

arrangements for e%change of information.

T& !+' *"6 &7!+*%& +&*+&"+ () '*&(%6&' *"6 4&- ("&'!$ )"#+!("'5

2. 7asic shareholder rights should include the right to:

3. Secure methods of ownership registrationJ

@. +onvey or transfer sharesJ

=. /tain relevant and material information on the corporation on a timely and regular asisJ

. *articipate and vote in general shareholder meetingsJ

8. Alect and remove memers of the oardJ and

;. Share in the profits of the corporation.

7. Shareholders should e sufficiently informed aout& and have the right to approve or participate in&

decisions concerning fundamental corporate changes such as:

3. 2mendments to the statutes& or articles of incorporation or similar governing documents of the

companyJ

@. The authorisation of additional sharesJ and

8/18/2019 Good Governance Final (1)

10/72

=. A%traordinary transactions& including the transfer of all or sustantially all assets that in effect

result in the sale of the company.

+. Shareholders should have the opportunity to participate effectively and vote in general shareholder

meetings and should e informed of the rules& including voting procedures that govern general

shareholder meetings:

3. Shareholders should e furnished with sufficient and timely information concerning the date&

location and agenda of general meetings& as well as full and timely information regarding the

issues to e decided at the meeting.

@. *rocesses and procedures for general shareholder meetings should allow for e)uitale

treatment of all shareholders. +ompany procedures should not make it unduly difficult or

e%pensive to cast votes.

=. Shareholders should have the opportunity to ask )uestions to the oard& including )uestions

relating to the annual e%ternal audit& to place items on the agenda of general meetings&

and to propose resolutions& su(ect to reasonale limitations.

. Affective shareholder participation in key corporate governance decisions& such as the

nomination and election of oard memers& should e facilitated. Shareholders should e ale to

make their views known& including through votes at shareholder meetings& on the remuneration of

oard memers andKor key e%ecutives& as applicale. The e)uity component of compensation

schemes for oard memers and employees should e su(ect to shareholder approval.

8. Shareholders should e ale to vote in person or in asentia& and e)ual effect should e given

to votes whether cast in person or in asentia.

;. Impediments to cross order voting should e eliminated.

. Shareholders& including institutional shareholders& should e allowed to consult with each other on

issues concerning their asic shareholder rights as defined in the *rinciples& su(ect to e%ceptions to

prevent ause.

A. 2ll shareholders of the same series of a class should e treated e)ually. +apital structures and

arrangements that enale certain shareholders to otain a degree of influence or control

disproportionate to their e)uity ownership should e disclosed.

3. ?ithin any series of a class& all shares should carry the same rights. 2ll investors should e

ale to otain information aout the rights attached to all series and classes of shares efore they

purchase. 2ny changes in economic or voting rights should e su(ect to approval y those

classes of shares which are negatively affected.

@. The disclosure of capital structures and control arrangements should e re)uired.

1. 6elated-party transactions should e approved and conducted in a manner that ensures proper management of conflict of interest and protects the interest of the company and its shareholders.

3. +onflicts of interest inherent in related-party transactions should e addressed.

@. emers of the oard and key e%ecutives should e re)uired to disclose to the oard whether

they& directly& indirectly or on ehalf of third parties& have a material interest in any transaction or

matter directly affecting the corporation.

8/18/2019 Good Governance Final (1)

11/72

$. inority shareholders should e protected from ausive actions y& or in the interest of&

controlling shareholders acting either directly or indirectly& and should have effective means of

redress. 2usive self-dealing should e prohiited.

D. arkets for corporate control should e allowed to function in an efficient and transparent manner.

3. The rules and procedures governing the ac)uisition of corporate control in the capital markets&

and e%traordinary transactions such as mergers& and sales of sustantial portions of corporate

assets& should e clearly articulated and disclosed so that investors understand their rights and

recourse. Transactions should occur at transparent prices and under fair conditions that protect the

rights of all shareholders according to their class.

@. 2nti-take-over devices should not e used to shield management and the oard from

accountaility.

I"'+!++!("*% !",&'+('8 '+(#4 *4&+' *"6 (+& !"+&&6!*!&'5

2. Institutional investors acting in a fiduciary capacity should disclose their corporate governance and

voting policies with respect to their investments& including the procedures that they have in place for deciding on the use of their voting rights.

7. Lotes should e cast y custodians or nominees in line with the directions of the eneficial owner

of the shares.

+. Institutional investors acting in a fiduciary capacity should disclose how they manage material

conflicts of interest that may affect the e%ercise of key ownership rights regarding their investments.

. The corporate governance framework should re)uire that pro%y advisors& analysts& rokers& rating

agencies and others that provide analysis or advice relevant to decisions y investors& disclose andminimise conflicts of interest that might compromise the integrity of their analysis or advice.

A. Insider trading and market manipulation should e prohiited and the applicale rules enforced.

1. 1or companies who are listed in a (urisdiction other than their (urisdiction of incorporation& the

applicale corporate governance laws and regulations should e clearly disclosed. In the case of cross

listings& the criteria and procedure for recognising the listing re)uirements of the primary listing

should e transparent and documented.

$. Stock markets should provide fair and efficient price discovery as a means to help promote

effective corporate governance.

T& (%& () '+*4&(%6&' !" #($(*+& (,&"*"#&5

2. The rights of stakeholders that are estalished y law or through mutual agreements are to e

respected.

8/18/2019 Good Governance Final (1)

12/72

7. ?here stakeholder interests are protected y law& stakeholders should have the opportunity to

otain effective redress for violation of their rights.

+. echanisms for employee participation should e permitted to develop.

. ?here stakeholders participate in the corporate governance process& they should have access to

relevant& sufficient and reliale information on a timely and regular asis.

A. Stakeholders& including individual employees and their representative odies& should e ale to

freely communicate their concerns aout illegal or unethical practices to the oard and to the

competent pulic authorities and their rights should not e compromised for doing this.

1. The corporate governance framework should e complemented y an effective& efficient insolvency

framework and y effective enforcement of creditor rights.

D!'#%('& *"6 +*"'$*&"#-5

2. isclosure should include& ut not e limited to& material information on:

3. The financial and operating results of the company.

@. +ompany o(ectives and non-financial information.

=. a(or share ownership& including eneficial owners& and voting rights.

. 6emuneration of memers of the oard and key e%ecutives.

8. Information aout oard memers& including their )ualifications& the selection process& other

company directorships and whether they are regarded as independent y the oard.

;. 6elated party transactions.

8/18/2019 Good Governance Final (1)

13/72

2. 7oard memers should act on a fully informed asis& in good faith& with due diligence and care

and in the est interest of the company and the shareholders.

7. ?here oard decisions may affect different shareholder groups differently& the oard should treat

all shareholders fairly.

+. The oard should apply high ethical standards. It should take into account the interests of

stakeholders.

. The oard should fulfil certain key functions& including:

3. 6eviewing and guiding corporate strategy& ma(or plans of action& risk management policies and

procedures& annual udgets and usiness plansJ setting performance o(ectivesJ monitoring

implementation and corporate performanceJ and overseeing ma(or capital e%penditures&

ac)uisitions and divestitures.@. onitoring the effectiveness of the company0s governance practices and making changes as

needed.

=. Selecting& compensating& monitoring and& when necessary& replacing key e%ecutives andoverseeing succession planning.

. 2ligning key e%ecutive and oard remuneration with the longer term interests of the company

and its shareholders.

8. Ansuring a formal and transparent oard nomination and election process.

;. onitoring and managing potential conflicts of interest of management& oard memers and

shareholders& including misuse of corporate assets and ause in related party transactions.

8/18/2019 Good Governance Final (1)

14/72

$. ?hen employee representation on the oard is mandated& mechanisms should e developed to

facilitate access to information and training for employee representatives& so that this representation is

e%ercised effectively and est contriutes to the enhancement of oard skills& information and

independence.

8/18/2019 Good Governance Final (1)

15/72

CHAPTER ! -C"AU#E !$ of "istin% A%ree&ent

9.1 B(*6 () D!+(' C%*'& 9; I<

C($('!+!(" () B(*6 = C%*'& 9; IA<

• The 7oard of directors of the company shall have an optimum comination of e%ecutive and non-

e%ecutive directors with not less than fifty percent of the oard of directors comprising of non-

e%ecutive directors.

• ?here the +hairman of the 7oard is a non-e%ecutive director& at least one-third of the 7oard should

comprise of independent directors and in case he is an e%ecutive director& at least half of the 7oard

should comprise of independent directors.

• The 3>8; 2ct provided that the limit for ma%imum numer of directors e ased on its articles or

twelve whichever is lower. This has een done to ring more fle%iility and enale companies to get

more e%perienced and competent personnel at the 7oard level.

• 2ppointment of at least one woman director on the 7oard has een made mandatory. This provision

has een introduced to make the 7oard more gender sensitive.

• 2ll listed companies must have at least one director who has een elected y small shareholders. This

provision is to safeguard the interest of small investors in the company. This director might act as the

representative of the small investors.

?hen the 2ct was introduced in @43=& a one year period was given to all the companies to comply with

these rules.

I"6&$&"6&"+ 6!+(

• 2 person who does not have any peculiar monetary interest in the company& apart from the director

fees that he or she receives.

• 2 person who does not have any relationship with the company0s promotors& its directors& its senior

management or its holding company& its susidiaries and associates

• 2 person has not een an e%ecutive of the company in the immediately preceding three financial years

• 2 person who is not a material supplier& service provider or customer or a lessor or lessee of the

company

• De should not own more than @ percent of shares with voting rights.

C*'&:

I&&"* V!++*%>' &?!+ )( A?!' B*"4

8/18/2019 Good Governance Final (1)

16/72

Ireena Littal was an independent director on the 7oard of 2%is 7ank. She was entitled to hold her position

till @43>. Der husand $opal Littal is the +A/ of 7harti& which won a payment ank licence in

partnership with Botak ahindra 7ank. 2%is 7ank eing a direct competitor of Botak ahindra 7ank&

officials of at 2%is 7ank said rs. Littal resigned voluntarily citing this conflict of interest. Though

industry stalwarts have )uestioned the resignation of Littal saying that such conflict of interest is

farfetched.

C(*% I"6!*

+oal India limited is in non-compliance with clause > of listing agreement. In @43& +oal India

had 3@ memers in the oardJ currently the composition of oard shrank to ;& which is in

violation of SA7I norms of corporate governance. The lack of Is mean +oal India was not

eing ale to form the statutorily mandated oard committees that must have an I !audit

committee& nomination and remuneration committee& and corporate social responsiility

committee#.$overnment was in process of divesting 349 stake in its shareholding in this fiscal.

7ut due to non-compliance of +$ norms& it went with indian oil divestment programme. The

government must take its role as a promoter seriously and stop making oard appointments a

ureaucratic process or using them for politicking. The government needs to look at listed pulic

sector units differently from its unlisted ones and accept that non-promoter shareholders also

have rights and e%pect governance standards that are at least aligned to& if not etter than& other

listed companies

BASF

ultinational company 72S1 India has appointed $ermany-ased 2ndrea 1renzel as a non-e%ecutive

director to comply with the law on having women directors on company oards. /n that day it appointed

G C 7aliga an alternate director to attend meetings in place of 1renzel. 72S1 argues appointment of

alternate directors under the +ompanies 2ct and it did not alter oard composition. 2ppointment of man

inplace of sole women director can0t e deemed as compliance with the law.

N("=&?+!,& 6!+('> #($&"'*+!(" *"6 6!'#%('&'= C%*'& 9; IB<

2ll feesKcompensation& if any paid to non-e%ecutive directors& including independent directors& shall e

fi%ed y the 7oard of irectors and shall re)uire previous approval of shareholders in general meeting.

8/18/2019 Good Governance Final (1)

17/72

The shareholders0 resolution shall specify the limits for the ma%imum numer of stock options that can e

granted to non-e%ecutive directors& including independent directors& in any financial year and in aggregate

O+& $(,!'!("' *' +( B(*6 *"6 C(!++&&'= C%*'& 9; IC<

• The oard shall meet at least four times a year& with a ma%imum time gap of three months etween

any two meetings.

• 2 director shall not e a memer in more than 34 committees or act as +hairman of more than five

committees across all companies in which he is a director.

C(6& () C("6#+= C%*'& 9; ID<

• The 7oard shall lay down a code of conduct for all 7oard memers and senior management of the

company. The code of conduct shall e posted on the wesite of the company.

• 2ll 7oard memers and senior management personnel shall affirm compliance with the code on an

annual asis. The 2nnual 6eport of the company shall contain a declaration to this effect signed y

the +A/.

S+!#+& S&+*!*% P*#+!#&'

• The +ompanies 2ct& @43= has made it compulsory for all companies to serve a < day notice to all the

directors efore the meeting& to make sure that all the memers are prepared to discuss all the aspects

aout the company0s affairs and make appropriate decisions.

•The 2ct also mentions the compulsion for at least 3 independent director at every oard meeting that

would ensure that all decisions taken in the meeting are in the interest of the company.

N("=M*"6*+(- R&7!&&"+'= A""&?& I D

T& B(*6

Independent irectors may have tenure of not more than nine years& on the 7oard of a company.

R&"&*+!(" C(!++&&

+ompanies may set up 6emuneration +ommittees& that will decide the compensation and enefits that the

7oard of irectors will receive. This committee may comprise of at least three directors& all of whom

should e non-e%ecutive directors& the +hairman of committee eing an independent director. This can e

done to ensure that the irectors act in the interest of the company and do not misuse their dominant

position in decision making process.

8/18/2019 Good Governance Final (1)

18/72

The +hairman of the remuneration committee could e present at the 2nnual $eneral eeting& to answer

the shareholder )ueries. Dowever& it would e up to the +hairman of the 7oard to decide who should

answer the )ueries.

T*!"!" () B(*6 M&&'

The independent irectors may not e well versed with the usiness model of the company. This might

hamper their aility to take appropriate decisions for the company. 2 company may train its 7oard

memers in the usiness model of the company as well as the risk profile of the usiness parameters of

the company& their responsiilities as directors& and the est ways to discharge them.

M*"!' )( &,*%*+!" "("=&?+!,& B(*6 M&&'

The performance evaluation of non-e%ecutive directors could e done y a peer group comprising the

entire 7oard of irectors& e%cluding the director eing evaluated and *eer $roup evaluation could e themechanism to determine whether to e%tend K continue the terms of appointment of non-e%ecutive

directors.

W!'+%& B%(& P(%!#-

The company may estalish a mechanism for employees to report to the management concerns aout

unethical ehaviour& actual or suspected fraud or violation of the company0s code of conduct or ethics

policy.

8/18/2019 Good Governance Final (1)

19/72

9.2 A6!+ C(!++&& C%*'& 9; II<

Q*%!)!&6 *"6 I"6&$&"6&"+ A6!+ C(!++&& = C%*'& 9; IIA<

The audit committee has to e set up taking into account the following norms:

• The audit committee shall have minimum three directors as memers. Two-thirds of the memers of

the committee shall e independent directors.

• 2ll memers of the committee shall e financially literate and at least one memer shall have

accounting or related financial management e%pertise.

The term “financially literate means the aility to read and understand asic financial statements i.e.

alance sheet& profit and loss account and cash flow statement.

2 person who possesses e%perience in finance or accounting& or re)uisite professional certification inaccounting& or any other comparale e%perience or ackground which results in the individual0s financial

sophistication& including eing a chief e%ecutive officer& chief financial officer or other senior officer with

financial oversight responsiilities is a person with accounting or financial management e%pertise.

• The +hairman of the +ommittee shall e an Independent irector

• The +hairman of the +ommittee shall e present at 2nnual $eneral eeting to answer shareholder

)ueries

• The +ommittee may invite such of the e%ecutives& as it considers appropriate !and particularly the

head of the finance function# to e present at the meetings of the committee& ut on occasions it mayalso meet without the presence of any e%ecutives of the company. The finance director& head of

internal audit and a representative of the statutory auditor may e present as invitees for the meetings

of the audit committee

• The +ompany Secretary shall act as the secretary to the committee.

M&&+!" () A6!+ C(!++&& = C%*' 9; IIB<

The audit committee should meet at least four times a year and not more than four months shall lapse

etween two meetings. The )uorum shall e either two memers or one third of the memers of thecommittee whichever is greater& ut there should e a minimum of two independent memers present.

8/18/2019 Good Governance Final (1)

20/72

P(&' () A6!+ C(!++&& = C%*'& 9; IIC<

The audit committee shall have following powers:

• To investigate any activity within its terms of reference.

• To seek information from any employees.• To otain outside legal or other professional advice.

• To secure attendance of outsiders with relevant e%pertise.

These powers are only illustrative and not e%haustive. The auditor should check whether the terms of

reference of the audit committee have een suitaly framed mentioning the aove powers. It is mandatory

for the aove powers to e vested in the audit committee. The 7oard may delegateK vest further power to

the committee.

R(%& () A6!+ C(!++&& = C%*'& 9; IID<

The role of the audit committee includes the following:

• /versight of the company0s financial reporting process and the disclosure of its financial information

to ensure that the financial statement is correct& sufficient and credile.

• 6ecommending the appointment and removal of e%ternal auditors& fi%ation of audit fee and approval

for payment of any other services.

• 6eviewing with management the annual financial statements efore sumission to the 7oard&

focusing primarily on:

o 2ny changes in 2ccounting policies andKor practices

o a(or accounting entries ased on e%ercise of (udgements y management

o Mualification in draft audit report

o Significant ad(ustment arising out of audit

o The going concern assumption

o +ompliance with accounting standards

o +ompliance with stock e%changes and legal re)uirement concerning financial statements

o 2ny related party transactions

8/18/2019 Good Governance Final (1)

21/72

• 6eviewing with the management& e%ternal and internal auditors& and the ade)uacy of internal control

system.

• 6eviewing the ade)uacy of internal audit function& if any including the structure of the internal audit

department& staffing and seniority of the official heading the department& reporting structure coverage

and fre)uency of internal audit.• iscussion with internal auditors any significant findings and follow-up thereon.

• 6eviewing the findings of any internal investigation y the internal auditors into matters where there

is suspected fraud or irregularity or a failure of internal control systems of a material nature and

reporting the matter to the 7oard.

• iscussion with e%ternal auditors efore the audit commences& nature and scope of audit as well as

have post audit discussion to ascertain any area of concern.

• 6eviewing the company0s financial and risk management policies.

• To look into the reasons for sustantial defaults in the payment to the depositors& deenture holders&

shareholders !in case of non-payment of declared dividend# and creditors.

• +arrying out any other function as is mentioned in the terms of reference of the 2udit +ommittee.

F"#+!("' () +& A6!+ C(!++&&

The 2udit +ommittee performs various important functions like investigating the matters referred y

oard& discuss aout internal control system etc. The su-section ; N < of Section @>@2 are reproduced

hereunder which specify the functions of the audit committee:

The 2udit +ommittee should have discussions with the auditors periodically aout internal control

systems& the scope of audit including the oservations of the auditors and review the half-yearly and

annual financial statements efore sumission to the 7oard and also ensure compliance of internal control

systems.

The 2udit +ommittee shall have authority to investigate into any matter in relation to the items specified

in this section or referred to it y the 7oard and for this purpose& shall have full access to information

contained in the records of the company and e%ternal professional advice& if necessary.

R&,!& () I")(*+!(" - A6!+ C(!++&&

The 2udit +ommittee shall mandatorily review the following information as per +lause > II !A#:

anagement discussion and analysis of financial condition and results of operationsJ

• Statement of significant related party transactions !as defined y the audit committee#& sumitted y

managementJ

• anagement letters K letters of internal control weaknesses issued y the statutory auditorsJ

8/18/2019 Good Governance Final (1)

22/72

• Internal audit reports relating to internal control weaknessesJ and

• The appointment& removal and terms of remuneration of the +hief internal auditor shall e su(ect to

review y the 2udit +ommittee.

The auditor should ascertain from the minutes ook of the audit committee and other sources like agenda

papers& etc. whether the audit +ommittee has reviewed the aove-mentioned information. The auditor

should ascertain whether as a part of directors0 report or as an addition thereto& a management discussion

and analysis report forms part of the annual report to the shareholders. Ender the old +lause >& this was

specifically mandated& ut now not spelt out clearly. The auditor should further ascertain whether the

management discussion and analysis includes discussion on the matters stipulated in this su-clause.

?here certain deficiencies or adverse findings are noted y the audit committee& the auditor will e

re)uired to see that these have een suitaly dealt with y the management in the 6eport on +orporate

$overnance.

The auditor should ascertain that the information reviewed y the 2udit +ommittee is consistent with the

reporting in the financial statements including those drawn up giving segment wise reak-up for

compliance of 2S 3< !Segment 6eporting#.

8/18/2019 Good Governance Final (1)

23/72

9.3 S'!6!*- C($*"!&' C%*'& 9; III<

2t least one independent director on the 7oard of irectors of the holding company shall e a director on

the 7oard of irectors of a material non-listed Indian susidiary company.

• aterial non listed Indian susidiary asically means that an unlisted susidiary company whose net

worth e%ceeds @49 of the consolidated net worth of the listed company and its susidiaries in the

preceding accounting year.

The 2udit +ommittee of the listed holding company shall also review the financial statements& in

particular& the investments made y the unlisted susidiary company.

• It means that the susidiary company should report its transactions to the holding company if it

e%ceeds 349 of the total revenue or total e%penses or total assets or total liailities which will e

reviewed y the holding company.

The minutes of the 7oard meetings of the unlisted susidiary company shall e placed at the 7oard

meeting of the listed holding company. The management should periodically ring to the attention of the

7oard of irectors of the listed holding company& a statement of all significant transactions and

arrangements entered into y the unlisted susidiary company.

• ?here a listed holding company has a listed susidiary which is itself a holding company& the aove

provisions shall apply to the listed susidiary insofar as its susidiaries are concerned.

8/18/2019 Good Governance Final (1)

24/72

9.9 D!'#%('&' C%*'& 9; IV<

B*'!' () &%*+&6 $*+- +*"'*#+!("' C%*'& 9; IVA<

•

2 statement in summary form of transactions with related parties in the ordinary course of usinessshall e placed periodically efore the audit committee.

• etails of material individual transactions with related parties which are not in the normal course of

usiness shall e placed efore the audit committee.

• etails of material individual transactions with related parties or others& which are not on an arm0s

length asis should e placed efore the audit committee& together with anagement0s (ustification

for the same.

I"+&$&+*+!(":

2 statement of all transactions with related parties shall e placed efore the 2udit +ommittee for formal

approval. If any transaction is not on an arm0s length asis& management is re)uired to (ustify the same to

the 2udit +ommittee.

E?*$%&: ICICI $(%!#- )( RPT

R&%*+&6 $*+-:

6elated party with reference to the 7ank means:

•2 director or his relativeJ

• 2 key managerial personnel !B*# or his relativeJ

• 2 firm& in which a director& manager or his relative is a partnerJ

• 2 private company in which a director or manager or his relative is a memer or directorJ

• 2 pulic company in which a director or manager is a director and holds along with his relatives&

more than two per cent of its paid-up share capitalJ

• 2nyody corporate whose oard of directors& managing director or manager is accustomed to act in

accordance with the advice& directions or instructions of a director or managerJ

• 2ny person on whose advice& directions or instructions a director or manager is accustomed to actJ

• 2ny company which is a holding& susidiary or an associate company of such companyJ or a

susidiary of a holding company to which it is also a susidiaryJ• 2 director other than an independent director or key managerial personnel of the holding company or

his relative with reference to a company !as per +ompanies !eetings of 7oard and its *owers#

6ules& @43#J

O6!"*- #('& () '!"&'':

8/18/2019 Good Governance Final (1)

25/72

“/rdinary +ourse of 7usiness includes ut not limited to a term for activities that are necessary& normal&

and incidental to the usiness. These are common practices and customs of commercial transactions. The

ordinary course of usiness covers the usual transactions& customs and practices related to the usiness.

The following factors are indicative of a transaction eing in the ordinary course of usiness:

• The transaction is normal or otherwise unremarkale for the usiness.

• The transaction is fre)uentKregular

• The transaction is a source of income for the usiness

• Transactions that are part of the standard industry practice& even though the 7ank may not have done

it in the past.

These are not e%haustive criteria and the 7ank will have to assess each transaction considering its specific

nature and circumstances.

A>' %&"+ *'!':

In terms of the +ompanies 2ct& the e%pression Harm0s length transaction0 means a transaction etween two

related parties that is conducted as if they were unrelated& so that there is no conflict of interest.

2 transaction with a related party will e considered to e on arm0s length asis if the key terms&

including pricing of the transaction& taken as a whole& are comparale with those of similar transactions if

they would have een undertaken with unrelated parties.

It may e noted that this policy framework& including the definitions aove& is meant solely for the

purposes of compliance with related party transaction re)uirements under +ompanies 2ct& @43= and

+lause > of the Fisting 2greement. The aove terms may have different connotations for other purposes

like disclosures in the financial statements& which are governed y applicale regulations& accounting

standards& regulatory guidelines etc.

A$$(,*% () &%*+&6 $*+- +*"'*#+!("'

A. A6!+ C(!++&&

2ll the transactions which are identified as related party transactions should e preapproved y the 2udit

+ommittee efore entering into such transaction. The 2udit +ommittee shall consider all relevant factors

while delierating the related party transactions for its approval.

8/18/2019 Good Governance Final (1)

26/72

2ny memer of the +ommittee who has a potential interest in any related party transaction will rescue

himself and astain from discussion and voting on the approval of the related party transaction. 2 related

party transaction which is !i# not in the ordinary course of usiness& or !ii# not at arm0s length price& would

re)uire approval of the 7oard of irectors or of shareholders as discussed suse)uently.

The 2udit +ommittee may grant omnius approval for related party transactions which are repetitive in

nature and su(ect to such criteriaKconditions as mentioned under clause > and such other conditions as it

may consider necessary in line with this policy and in the interest of the 7ank. Such omnius approval

shall e valid for a period not e%ceeding one year and shall re)uire fresh approval after the e%piry of one

year.

2udit +ommittee shall review& on a )uarterly asis& the details of related party transactions entered into

y the 7ank pursuant to the omnius approval. In connection with any review of a related party

transaction& the +ommittee has authority to modify or waive any procedural re)uirements of this policy.

2 related party transaction entered into y the 7ank& which is not under the omnius approval or

otherwise pre-approved y the +ommittee& will e placed efore the +ommittee for ratification.

B. B(*6 () D!+('

In case any related party transactions are referred y the 7ank to the 7oard for its approval due to the

transaction eing !i# not in the ordinary course of usiness& or !ii# not at an arm0s length price& the 7oard

will consider such factors as& nature of the transaction& material terms& the manner of determining the

pricing and the usiness rationale for entering into such transaction. /n such consideration& the 7oard

may approve the transaction or may re)uire such modifications to transaction terms as it deems

appropriate under the circumstances. 2ny memer of the 7oard who has any interest in any related party

transaction will rescue himself and astain from discussion and voting on the approval of the related party

transaction.

C. S*&(%6&'

• If a related party transaction is a material transaction as per clause >& it shall re)uire shareholder0s

approval through special resolution and the related parties shall astain from voting on such

resolutions.

• If a related party transactions is not in the ordinary course of usiness& or not at arm0s length price and

e%ceeds certain thresholds prescried under the +ompanies 2ct& @43=& it shall re)uire shareholders0

approval y a resolution. In such a case& any memer who is a related party having interest in the

8/18/2019 Good Governance Final (1)

27/72

transaction for which resolution eing proposed& shall not vote on such resolution passed for

approving related party transaction.

Dowever the shareholders0 approval is not re)uired for the transactions entered into etween the 7ank and

its wholly owned susidiaries whose accounts are consolidated with the 7ank and placed efore the

shareholders at the general meeting.

R&$(+!" () &%*+&6 $*+- +*"'*#+!("'

Avery contract or arrangement& which is re)uired to e approved y the 7oardKshareholders under this

*olicy& shall e referred to in the 7oard0s report to the shareholders along with the (ustification for

entering into such contract or arrangement.

D!'#%('& () A##("+!" T&*+&"+ C%*'& 9; IVB<

?here in the preparation of financial statements& a treatment different from that prescried in an

2ccounting Standard has een followed& the fact shall e disclosed in the financial statements& together

with the management0s e%planation as to why it elieves such alternative treatment is more representative

of the true and fair view of the underlying usiness transaction in the +orporate $overnance 6eport.

I"+&$&+*+!(":

+lause > re)uires that in case a company has followed a treatment different from that prescried in an

2ccounting Standards& the management of such company shall (ustify why they elieve such alternative

treatment is more representative of the underlined usiness transactions. anagement is also re)uired to

clearly e%plain the alternative accounting treatment in the footnote of financial statements.

E?*$%&: IDFC

The 1inancial Statements of the +ompany have een prepared in accordance with $enerally 2ccepted

2ccounting *rinciples in India !“Indian $22*# to comply with the 2ccounting Standards as specified

under Section of the +ompanies 2ct& @43=& +ompanies !2ccounts# 6ules @43 and relevant provisions of

the +ompanies 2ct& @43= K +ompanies 2ct& 3>8;& as applicale.

B(*6 D!'#%('&' @ R!'4 *"*&&"+ C%*'& 9; IVC<

The company through its 7oard of irectors shall constitute a 6isk anagement +ommittee. The 7oard

shall define the roles and responsiilities of the 6isk anagement +ommittee and may delegate

monitoring and reviewing of the risk management plan to the committee and such other functions as it

may deem fit

8/18/2019 Good Governance Final (1)

28/72

• The ma(ority of +ommittee shall consist of memers of the 7oard of irectors.

• Senior e%ecutives of the company may e memers of the said +ommittee ut the +hairman of the

+ommittee shall e a memer of the 7oard of irectors.

E?*$%&: T*44&' D&,&%($&' L+6

R!'4 M*"*&&"+ P(%!#-

The +lause > of the Fisting 2greement mandates every +ompany to constitute a 6isk anagement

+ommittee. The +ompany has laid down a roust 6isk anagement *olicy& defining 6isk profiles

involving Strategic& Technological& /perational& 1inancial& Fi)uidity& /rganisational& and Fegal and

6egulatory risks within a well-defined framework. The 6isk management *olicy acts as an enaler of

growth for the +ompany y helping its usinesses to identify the inherent risks& assess& evaluate and

monitor these risks continuously and undertake effective steps to manage these risks.

P$('&

The 6isk anagement +ommittee is a group of people charged with development and overseeing an

organisation0s risk management programme. The +ommittee has three primary responsiilities

• Identify the organisation0s e%posures&

• evelop a risk control programme& and

•Astalish a risk financing strategy

+ompany employee0s full time professional risk managers to co-ordinate such risk management activities

as loss control efforts& claims& reporting& insurance purchasing and safety programme implementation.

The +ompany also consults outside advisors to assist in creating risk management programme.

R&'$("'!!%!+- () +& C(!++&&

The risk management committee is responsile for all phase of the +ompany0s 6isk anagement

programme from development through implementations and monitoring. The +ommittee0s

responsiilities include the following:

8/18/2019 Good Governance Final (1)

29/72

• eveloping& for oard approval& +ompany0s risk management policy that affirms the +ompany0s

commitment to safeguard its assets.

• Astalishing the +ompany0s risk management goal !1or e%ample improving client safety& reducing the

numer of accidents& and reducing the insurance cost#.

• 6ecommending alternative risk financing alternatives

• +ommunicating the +ompany0s risk management plan and loss control procedures to the oard of

directors& employees& volunteers& clients and the pulic.

• Selecting an insurance advisor ! 2 roker& agent or consultant # and negotiating insurance agreements

• /verseeing loss prevention and control activities.

• *roviding an annual risk management report to the 7oard of directors.

C("'+!++!(" () +& C(!++&&

The 6isk anagement +ommittee is headed y Shri Gishant 6a(endra Thakker& irector and comprises

of other irectors of the +ompany as memers& who periodically review the roustness of the 6isk

anagement frame work. The periodical update on the risk management practices and mitigation plan of

the +ompany and susidiaries are presented to the 2udit +ommittee and 7oard of irectors.

The emers of the 6isk anagement +ommittee are:

• Shri. ukesh Bantilal Thakkar - irector

• Shri. Garendra anohardas Thakker - irector

• Shri. 6a(endra anohardas Thakker - anaging irector

• Shri. Citendra anohardas Thakker - irector

W(4!"

The +ommittee oversees the risk management aspect of the +ompany0s working and develops a risk

management plan in consultation with the 7oard of directors& senior e%ecutives and e%ternal advisors as

8/18/2019 Good Governance Final (1)

30/72

well as consultants. The committee compares the working with the risk management plan prepared and

takes the necessary steps for differences& if any.

R&,!&

The 2udit +ommittee and 7oard of irectors of the +ompany periodically review such updates and

findings and suggest areas where internal controls and risk management practices can e improved.

P(#&&6' )( $%!# !''&'8 !+' !''&' &+#. C%*'& 9; IVD<

?hen money is raised through an issue !pulic issues& rights issues& preferential issues etc.#& it shall

disclose to the 2udit +ommittee& the uses K applications of funds y ma(or category !capital e%penditure&

sales and marketing& working capital& etc#& on a )uarterly asis as a part of their )uarterly declaration of

financial results. 1urther& on an annual asis& the company shall prepare a statement of funds utilized for

purposes other than those stated in the offer documentKprospectusKnotice and place it efore the audit

committee. Such disclosure shall e made only till such time that the full money raised through the issue

has een fully spent. This statement shall e certified y the statutory auditors of the company. The audit

committee shall make appropriate recommendations to the 7oard to take up steps in this matter.

R&"&*+!(" () D!+(' C%*'& 9; IVE<

• 2ll pecuniary relationship or transactions of the non-e%ecutive director0s vis-O-vis the company shall

e disclosed in the 2nnual 6eport.

• 1urther the following disclosures on the remuneration of directors shall e made in the section on the

+orporate $overnance of the 2nnual 6eport:

o 2ll elements of remuneration package of individual directors summarized under ma(or

groups& such as salary& enefits& onuses& stock options& pension etc.

o etails of fi%ed component and performance linked incentives& along with the

performance criteria.

o Service contracts& notice period& severance fees.

o Stock option details& if any P and whether issued at a discount as well as the period over

which accrued and over which e%ercisale.

• The company shall pulish its criteria of making payments to non-e%ecutive directors in its annual

report. 2lternatively& this may e put up on the company0s wesite and reference drawn thereto in the

annual report.

• The company shall disclose the numer of shares and convertile instruments held y non-e%ecutive

directors in the annual report.

• Gon-e%ecutive directors shall e re)uired to disclose their shareholding !oth own or held y K for

other persons on a eneficial asis# in the listed company in which they are proposed to e appointed

8/18/2019 Good Governance Final (1)

31/72

as directors& prior to their appointment. These details should e disclosed in the notice to the general

meeting called for appointment of such director

E?*$%&: IDFC

The 7oard at its meeting comined the Gomination +ommittee and +ompensation +ommittee which wasnamed as Gomination N 6emuneration +ommittee !"G6+"#. The G6+ of I1+ comprised four

irectors& three of whom are Is and A%ecutive +hairman of the +ompany. The +ommittee met two

times during 1Q38: on Cune =& @43 and Canuary @>& @438. The )uorum for any meeting of this

+ommittee is two memers.

The role of the committee includes the following:

• 1ormulation of the criteria for determining )ualifications& positive attriutes and independence of a

irector and recommend to the 7oard a policy& relating to the remuneration of the irectors& Bey

anagerial *ersonnel and other employeesJ• 1ormulation of criteria for evaluation of Is and the 7oardJ

• evising a policy on 7oard diversityJ

• Identifying persons who are )ualified to ecome irectors and who may e appointed in senior

management in accordance with the criteria laid down& and recommend to the 7oard their

appointment and removalJ

• Succession planning of the 7oard of irectors and S*.

The details of the evaluation criteria form part of the 2nnual 6eport.

I1+ pays remuneration to As y way of salary& per)uisites and retirement enefits !fi%ed component#

and a variale component ased on the recommendation of the G6+ and approval of the 7oard and the

Shareholders of the +ompany& which is separately disclosed in the financial statements. The remuneration

paid to As is determined keeping in view the industry enchmark and the relative performance of the

+ompany vis-O-vis industry performance. The minutes of the +ommittee are reviewed y the 7oard.

The Gon-A%ecutive irectors !“GAs# are paid remuneration y way of commission and sitting fees.

PaRtiCU"aRs PRoPoseD a&oUNt' PeR aNNU&(

Fixed Remuneration for member of the Board

1,050,000

Chairman of the Board1,050,000

Chairman of the Audit Committee300,000

Chairman of Other Committees150,000

8/18/2019 Good Governance Final (1)

32/72

Member of the Audit Committee150,000

Member of Other Committees75,000

Variable remuneration !e"endin# on attendan$e at Board Meetin#s%&50,000

M*"*&&"+ C%*'& 9; IVF<

• 2s part of the directors0 report or as an addition thereto& a anagement iscussion and 2nalysis

report should form part of the 2nnual 6eport to the shareholders. This anagement iscussion N

2nalysis should include discussion on the following matters within the limits set y the company0s

competitive position:

o Industry structure and developments.

o /pportunities and Threats.o SegmentPwise or product-wise performance.

o /utlook

o 6isks and concerns.

o Internal control systems and their ade)uacy.

o iscussion on financial performance with respect to operational performance.

o aterial developments in Duman 6esources K Industrial 6elations front& including

numer of people employed.

• Senior management shall make disclosures to the oard relating to all material financial and

commercial transactions& where they have personal interest& that may have a potential conflict with

the interest of the company at large !for e.g. dealing in company shares& commercial dealings with

odies& which have shareholding of management and their relatives etc.#

A%planation: 1or this purpose& the term "senior management" shall mean personnel of the company who

are memers of its core management team e%cluding the 7oard of irectors#. This would also include all

memers of management one level elow the e%ecutive directors including all functional heads.

S*&(%6&' C%*'& 9; IVG<

• In case of the appointment of a new director or re-appointment of a director the shareholders must e

provided with the following information:

o 2 rief resume of the directorJ

o Gature of his e%pertise in specific functional areasJ

8/18/2019 Good Governance Final (1)

33/72

o Games of companies in which the person also holds the directorship and the memership of

+ommittees of the 7oardJ and

o Shareholding of non-e%ecutive directors as stated in +lause > !IL# !A# !v# aove

• Muarterly results and presentations made y the company to analysts shall e put on company0s we-

site& or shall e sent in such a form so as to enale the stock e%change on which the company is listed

to put it on its own we-site.

• 2 oard committee under the chairmanship of a non-e%ecutive director shall e formed to specifically

look into the redressal of shareholder and investors complaints like transfer of shares& non-receipt of

alance sheet& non-receipt of declared dividends etc. This +ommittee shall e designated as

HShareholdersKInv estors $rievance +ommittee0.

• To e%pedite the process of share transfers& the 7oard of the company shall delegate the power of share

transfer to an officer or a committee or to the registrar and share transfer agents. The delegated

authority shall attend to share transfer formalities at least once in a fortnight.

I"+&$&+*+!(":

• ?hen a new director is to e appointed or re-appointed the shareholder of the company should e

provided information of his ackground& his e%pertise in specific functional areas& if he holds the

same or other position in any company& non-e%ecutive directors would disclose their shareholding.

• Muarterly results should e disclosed either on the company0s wesite or should e sent to the stock

e%change on which it is listed.

• 2 shareholdersKinvestors grievance committee should e form with a non-e%ecutive director as

chairman to look after issues and complaints of the shareholders like transfer of shares& non-receipt of

alance sheet& non-receipt of declared dividends etc.

• 1or faster transfer of shares the power should e delegated to an officer or a committee or share

transfer agent& etc.

E?*$%&: HCL T"(%(!&' L!!+&6

• The +ompany provides the re)uisite information to its shareholders& as prescried in +lause > of the

Fisting 2greement& in case of appointment of a new director or re-appointment of a director.

• The )uarterly results and presentations made y the +ompany to analysts are eing sent to the stock

e%changes& where the shares of the +ompany are listed& from time to time.

• The +ompany has formed the Shareholders0 +ommittee consisting of the following memers:

8/18/2019 Good Governance Final (1)

34/72

a# r. Suroto 7hattacharya !+hairman#& !Independent irector#

# r. Shiv Gadar

c# r. Lineet Gayar

d# r. anish 2nand& +ompany Secretary is acting as the compliance officer of the +ompany.

The Shareholders +ommittee undertakes the following activities:

o To review and take all necessary actions for redressal of investors0 grievances and complaints as

may e re)uired in the interests of the investors.

o To approve re)uests for dematerialisations& split and duplicate shares.

• In order to e%pedite the process of share transfers& the 7oard has delegated the power of share transfer

to the officer!s# of the +ompany.

9. CEO/CFO #&+!)!#*+!(" C%*'& 9; V<

The +A/& i.e. the anaging irector or anager appointed in terms of the +ompanies 2ct& 3>8; and the

+1/ i.e. the whole-time 1inance irector or any other person heading the finance function discharging

that function shall certify to the 7oard that:

• They have reviewed financial statements and the cash flow statement for the year and that to the est

of their knowledge and elief:

o these statements do not contain any materially untrue statement or omit any material fact or

contain statements that might e misleadingJo these statements together present a true and fair view of the company0s affairs and are in

compliance with e%isting accounting standards& applicale laws and regulations.

• There are& to the est of their knowledge and elief& no transactions entered into y the company

during the year which are fraudulent& illegal or violative of the company0s code of conduct.

• They accept responsiility for estalishing and maintaining internal controls and that they have

evaluated the effectiveness of the internal control systems of the company and they have disclosed to

the auditors and the 2udit +ommittee& deficiencies in the design or operation of internal controls& if

any& of which they are aware and the steps they have taken or propose to take to rectify these

deficiencies.

• They have indicated to the auditors and the 2udit committee

o significant changes in internal control during the yearJ

o significant changes in accounting policies during the year and that the same have een

disclosed in the notes to the financial statementsJ and

8/18/2019 Good Governance Final (1)

35/72

o instances of significant fraud of which they have ecome aware and the involvement therein&

if any& of the management or an employee having a significant role in the company0s internal

control system

9. R&$(+ (" C($(*+& G(,&"*"#& C%*'& 9; VI<

• There shall e a separate section on +orporate $overnance in the 2nnual 6eports of company& with a

detailed compliance report on +orporate $overnance. Gon-compliance of any mandatory re)uirement

of this clause with reasons thereof and the e%tent to which the non-mandatory re)uirements have een

adopted should e specifically highlighted.

• The companies shall sumit a )uarterly compliance report to the stock e%changes within 38 days from

the close of )uarter. The report shall e signed either y the +ompliance /fficer or the +hief

A%ecutive /fficer of the company.

9. C($%!*"#& C%*'& 9; VII<

• The company shall otain a certificate from either the auditors or practicing company secretaries

regarding compliance of conditions of corporate governance as stipulated in this clause and anne% the

certificate with the directors0 report& which is sent annually to all the shareholders of the company.

The same certificate shall also e sent to the Stock A%changes along with the annual report filed y

the company.

• The non-mandatory re)uirements may e implemented as per the discretion of the company.

Dowever& the disclosures of the compliance with mandatory re)uirements and adoption !and

compliance# K non-adoption of the non-mandatory re)uirements shall e made in the section on

corporate governance of the 2nnual 6eport.

8/18/2019 Good Governance Final (1)

36/72

A""&?& I A

Information to e placed efore 7oard of irectors

• 2nnual operating plans and udgets and any updates.

• +apital udgets and any updates.• Muarterly results for the company and its operating divisions or usiness segments.

• inutes of meetings of audit committee and other committees of the oard.

• The information on recruitment and remuneration of senior officers (ust elow the oard level&

including appointment or removal of +hief 1inancial /fficer and the +ompany Secretary.

• Show cause& demand& prosecution notices and penalty notices which are materially important

• 1atal or serious accidents& dangerous occurrences& any material effluent or pollution prolems.

• 2ny material default in financial oligations to and y the company& or sustantial non-payment for

goods sold y the company.

• 2ny issue& which involves possile pulic or product liaility claims of sustantial nature& including

any (udgement or order which& may have passed strictures on the conduct of the company or taken an

adverse view regarding another enterprise that can have negative implications on the company.

• etails of any (oint venture or collaoration agreement.

• Transactions that involve sustantial payment towards goodwill& rand e)uity& or intellectual property.

• Significant laour prolems and their proposed solutions. 2ny significant development in Duman

6esourcesK Industrial 6elations front like signing of wage agreement& implementation of Loluntary

6etirement Scheme etc.

• Sale of material nature& of investments& susidiaries& assets& which is not in normal course of usiness.

• Muarterly details of foreign e%change e%posures and the steps taken y management to limit the risks

of adverse e%change rate movement& if material.• Gon-compliance of any regulatory& statutory or listing re)uirements and shareholders service such as

non-payment of dividend& delay in share transfer etc.

8/18/2019 Good Governance Final (1)

37/72

CHAPTER - ) Case #t*+, TATA Po.er

The +ompany Secretaries of awardee companies& +S C S 2mitah& +ompany Secretary& 6E62F

AFA+T6I1I+2TI/G +/6*/62TI/G FIITA N +S D istry& +ompany Secretary& T2T2

*/?A6 +/*2GQ FIITA were also honoured for their contriution in adhering to good corporate

governance practices. +ertificate of 6ecognition for A%cellence in +orporate $overnance were presented

to other Top 1ive +ompanies !in 2lphaetical order#:

3. ++ Fimited

@. Dindustan *etroleum +orporation limited

=. I+I+I 7ank Fimited

. /il and Gatural $as +orporation Ftd.

8. *ersistent Systems Fimited

In pursuit of e%cellence and to identify& foster and reward the culture of evolving gloally acceptale

standards of corporate governance among Indian +ompanies& the “I+SI Gational 2wards for A%cellence

in +orporate $overnance was instituted y the I+SI in the year @443& to recognise and honour the est

governed companies as per five key parameters viz. 7oard Structure and *rocesses& Transparency and

isclosure +ompliances& Stakeholders Lalue Anhancement& +orporate Social 6esponsiility !+S6# and

Sustainaility.

8/18/2019 Good Governance Final (1)

38/72

A"*%-'!' () TATA P(& G((6 G(,&"*"#&:

*articulars+lause ofFisting

agreement

+omplianceStatus

QesKGo

6emarks

I. 7oard of irectors > I

!2#+omposition of 7oard >!I2# Qes33 memer oard& @ A N > GA0s& out of

> GA0s& ; are independent directors

!7#Gon-e%ecutive

irectors0 compensation N

disclosures

> !I7# Qes Gone of the GA0s have any pecuniaryrelation with the company other than fees

and commission pre decided y the

shareholders

!+#/ther provisions as to

7oard and +ommittees> !I+# Qes

3. ' 7oard meetings were held during the

year& gap etween @ meetings did not

e%ceed 3@4 days@. eeting the criteria of eing a memer

in not more than 34 committee and a

chairman of not more than 8 committee.

!#+ode of +onduct > !I# QesThe company has adopted Tata +ode of+onduct !T+/+# for all its employees

including 0s and A0s

II. 2udit +ommittee > !II#

!2#Mualified N

Independent 2udit

+ommittee

> !II2# Qes

2uditorsKdirectors are independent N

GA0s& have financial management

e%pertise N are financially literate and

renowned practitioners.

!7#eeting of 2udit

+ommittee> !II7# Qes

2udit committee met 3@ times during the

year.

!+#*owers of 2udit > !II+#

Qes et all the criteria

8/18/2019 Good Governance Final (1)

39/72

+ommittee

!#6ole of 2udit

+ommittee> II!# Qes et all the criteria

!A#6eview of Information

y 2udit +ommittee> !IIA# Qes

6eview is done y the oard and head of

internal audit y adopting Tata code of

conduct !T+/+# for prevention of insider

trading N code of corporate disclosure

practices

III. Susidiary +ompanies > !III# - -

IL. isclosures > !IL#

!2#7asis of related party

transactions> !IL 2# Qes

There are no related party transactions

which have potential conflict of interest

with the company at large

!7#7oard isclosures > !IL 7# Qes 6isk anagement +ommittee

!+#*roceeds from pulic

issues& rights issues &

preferential issues etc.

> !IL +# - -

!#6emuneration of

irectors> !IL # Qes

Sitting fees and commission ade)uately

paid

!A#anagement > !IL A#

Qesanagement discussion N analysis is

pulished in the annual report

!1#Shareholders > !IL 1# Qes

2ll decisions related to appointment of

directors& pulishing analyst presentation

on wesite is in compliance with the

clause.

8/18/2019 Good Governance Final (1)

40/72

L.+A/K+1/ +ertification > !L# Qes +ertified y authorities

LI. 6eport on +orporate

$overnance> !LI# Qes

Avery year company pulishes separate

section on corporate governance in annual

report.

LII. +ompliance > !LII#

elloite Daskins N sell llc has approved

the +$ report of Tata power. 2ll conditions

related to compliance have een met.

8/18/2019 Good Governance Final (1)

41/72

S+*4&(%6& E"*&&"+ !" TATA P(&

V*%& C&*+!(" +( S+*4&(%6&'

Strategic partnerships create significant and sustainale value for the stakeholders. *artnering has proved

to e a powerful usiness tool for dealing with the ever changing usiness needs and markets dynamics.

+ompetitive advantage is gained y an organisations aility to harness the collective knowledge and to

ring forth customised and collaorative solutions with the help of its stakeholders. /perating in the

*ower Sector entails a lot of responsiilities& with respect to regulators& customers& employees&

environment& and the communities in which Tata *ower operates. In order to make this (ourney smooth

and achievale& the +ompany has identified key players to achieve meaningful success with desired

synergies and has partnered across the entire value chain of the operations. Tata *ower elieves that

symiotic relations with stakeholders must e propagated in a manner that helps for continuous

performance improvements& leading to mutual enefit and has e%tended this facilitation and dialogue to

all stakeholders.

S$$%!&'

2t Tata *ower& the Suppliers are seen as a valuale source of knowledge and resource. Supplier

engagement and relationship management is paramount to Tata *ower as a good uyer-seller relationship

is a win-win situation in the long run. To achieve the same& Tata *ower conducts Supplier eets to

discuss various issues& including usiness scenarios& new innovations& their concerns and any other

information pertinent to the usiness. The management has maintained an open-door policy for suppliers

and dealers.

In 1Q3& three vendor meets were organised across locations. It egan with the *artners eet for Aastern

region& at Co(oera& wherein& the suppliers related to other operating plants& including Co(oera& Daldia&

aithon& and Balinganagar were invited. The second *artners eet was organised in umai. In this

meet interactions with the important key service providers and the 2ffirmative 2ction delegates was done

and they encouraged usiness entrepreneurs from socially disadvantaged communities& through mentoring

and inclusion in supply chain& on the asis of e)ual merit. The third meet was organised at Tromay for

vendors under 2ffirmative 2ction category and other service providers. Tata *ower reaffirms that its

competitiveness is interlinked with the welleing of all sections of the society.

8/18/2019 Good Governance Final (1)

42/72

C("!+-

+ommunities around Tata *ower stations are the key stakeholders which are engaged for various

community development activities. ost of these activities have een initiated to improve economic

conditions keeping $s in mind and enales access to asic health services and primary education& promoting sustainale agriculture practices& providing access to portale water& etc. Some of the activities

initiated esides working on the thrust areas are as follows.

F%((6 R&%!&) = $opalpur& /disha and its ad(oining areas got severely hit y cyclone *hailin. 2s a part of a

self realised intervention& the Tata 6elief +ommittee !T6+# moilised its relief and rehailitation

operations in the +yclone affected areas of $an(am district. Ender the anner of T6+& oth Tata *ower

and Tata Steel initiated steps for immediate restoration of power and water supply in the $an(am district&

to cater to the emergency re)uirement for human life. 1ive iesel $enerators were provided y Tata

*ower to the district administration& which facilitated restoration of power. Tata *ower also provided

8&444 Solar Fanterns to the affected areas of the district. These solar lanterns& certainly illuminated lives

of the people.

S*66*"*"6 O$*"*& = 2 atch of = $raduate Angineer Trainees !$ATs# underwent rigorous

training for two months at Gational *ower Training Institute !G*TI#& Gagpur and took a self-driven

initiative at the neary Shraddhanand /rphanage. +elerating the receipt of the first payche)ue of their

lives& they found something amiss. This void in the celeration was filled when they decided to spend

some )uality time at the neary orphanage and also donated a token amount from their salary. ?ith

regular visits and interactions with the authorities and the children& $ATs zeroed down on an 6/ water

purifier which they got installed with their contriution.

S*!66! = Ender the livelihood initiatives& Tata *ower has een an enaling a Sustainale 2griculture

*rogram targeting local landless laour and marginalized farmers. The o(ective of sustainale agriculture

program is to promote appropriate technology& which would help them improving their livelihood and