Embed Size (px)

Citation preview

Gold Coast Tourism Industry Report

Year Ending June 2015

Dr Char-Lee McLennan

Ms Alexandra Bec

Ms Cassie Wardle

Professor Susanne Becken

Griffith Institute for Tourism Research Report No 9

November 2015

Gold Coast

Tourism Industry Report

Year Ending June 2015

Dr Char-Lee McLennan

Ms Alexandra Bec

Ms Cassie Wardle

Professor Susanne Becken

Griffith Institute for Tourism Research Report No 9

November 2015

ISSN 2203-4862 (Print)

ISSN 2203-4870 (Online)

ISBN 978-1-922216-98-4

Griffith University, Queensland, Australia

ii

Peer Reviewer

Prof Noel Scott, Griffith University

About this report:

This Gold Coast Year Ending June 2015 Tourism Industry Report provides a consistent

collation and analysis of macro and micro tourism statistics, research and trends.

The ongoing bi-annual series of Gold Coast Financial-Year and Full-Year Tourism Industry

Reports are commissioned by the Gold Coast Tourism Corporation and the City of Gold

Coast, and prepared independently by the Griffith Institute for Tourism.

These Reports are produced for, and provided to, the Gold Coast tourism industry and

general public as a reliable source of tourism intelligence.

Disclaimer:

Information is provided in good faith based on information sourced from government or

reputable companies. By using this information you acknowledge that this information is

provided by Griffith Institute for Tourism (GIFT), Gold Coast Tourism Corporation (GCT), and

the City of Gold Coast (CoGC) to you without any responsibility on behalf of GIFT, GCT,

CoGC. You agree to release and indemnify GIFT, GCT, CoGC for any loss or damage that

you may suffer as a result of your reliance on this information. GIFT, GCT, CoGC does not

represent or warrant that this information is correct, complete or suitable for the purpose for

which you wish to use it. The information is provided to you on the basis that you will use

your own skill and judgement, and make your own enquiries to independently evaluate,

assess and verify the information’s correctness, completeness and usefulness to you before

you rely on the information.

Disclaimer:

In January 2014, Tourism Research Australia (TRA) introduced mobile phone interviewing

on the National Visitor Survey to supplement existing residential fixed line interviewing in

order to provide better coverage of the Australian population. This has resulted in a break in

series because the travel patterns of people interviewed on mobile phones differ from those

of people interviewed on residential fixed lines. Consequently, readers of this report are

advised that the domestic visitor results should be interpreted with caution. For further

information please refer to: http://www.tra.gov.au/Fact-sheet-2014-Updates-to-the-IVS-

NVS.html

Note: The International and National Visitor Surveys are conducted separately with their own

methodologies; therefore care should be taken when considering their combined results.

iii

Organisations involved

Dr Char-Lee McLennan, Griffith University Ms Alexandra Bec, Griffith University Ms Cassie Wardle, Griffith University Professor Susanne Becken, Griffith University About Griffith University Griffith University is a top ranking University based in South East Queensland, Australia. Griffith University hosts the Griffith Institute for Tourism, a world-leading institute for quality research into tourism. Through its activities and an external Advisory Board, the Institute links university-based researchers with the business sector and organisations, as well as local, state and federal government bodies. For more information, visit www.griffith.edu.au/griffith-institute-tourism .

© Griffith Institute for Tourism, Griffith University 2015 This information may be copied or reproduced electronically and distributed to others without restriction, provided the Griffith Institute for Tourism (GIFT) is acknowledged as the source of information. Under no circumstances may a charge be made for this information without the express permission of GIFT, Griffith University, Queensland, Australia. GIFT Research Report Series URL: www.griffith.edu.au/business-government/griffith-institute-tourism/publications/research-report-series

4

1. Executive Summary

For the year ending June 2015:

Total Overnight and Daytrip Visitation

5%

In the year ending June 2015, total combined overnight and daytrip visitation increased 5% (up 558,000 visitors) to 11,617,000 visitors. The 5-year average growth rate for total visitors to the Gold Coast was stable.

Total Visitor Expenditure

7%

Total combined overnight and daytrip visitor expenditure to the Gold Coast decreased 7%, a result of declining spend by the domestic overnight and day trip markets.

Total Overnight Visitation

4%

Total international and domestic overnight visitation to the Gold Coast decreased by 4% (down 158,000 visitors) to 4,190,000 total overnight visitors. Of these total overnight visitors, 21% were international visitors.

Average Length of Stay

0.0 night

Average length of stay by total international and domestic overnight visitors on the Gold Coast was flat at 5.2 nights.

Domestic Overnight Visitation

6%

Domestic overnight visitors to the Gold Coast decreased by 6%, with their expenditure down 12%. Holiday visitation to the Gold Coast was the main source of the declines in visitation, down 19% (or 424,000 visitors) from the previous year. In contrast, those visiting friends and relatives increased 11% (up 106,000 visitors).

Domestic Daytrip Visitation

11%

Daytrip visitation to the Gold Coast increased 11%, with daytrip expenditure declining by 14%; a result driven by a decline in per visitor expenditure (down 22% or by $24 per visitor).

International Visitation

6%

International visitors to the Gold Coast increased 6%, with international nights up 1%. A 12% growth in expenditure per night, combined with increases in visitation drove an overall increase of 13% in international visitors’ expenditure in the region. Recent growth in the international market has been primarily from holiday visitors (up 6% or 36,000 visitors).

Tourism on the Gold Coast – Key Highlights for the year ending June 2015

International visitation to the Gold Coast increased by 6%, mainly driven by holiday visitors.

Expenditure by international visitors increased by 13%.

China has had good growth during the period, recording the largest increase in visitor

numbers (up 13% or 25,000 visitors).

Business confidence in tourism remains high.

Hotel revenue increased by 9% - double the Australian average growth rate.

5

Key Source Markets

China

New Zealand

The Gold Coast’s key international source market continues to be China, followed closely by New Zealand. China has had good growth during the period, recording the largest increase in visitor numbers (up 13% or 25,000 visitors). The New Zealand market remains strong, up 3% (or 5,000 visitors).

Gold Coast Airport Passenger Movements

2.1%

Total passenger movements at Gold Coast Airport (OOL) increased by 2.1%. Comparatively, total passenger movements at Brisbane Airport (BNE) increased by 1% for the 2015 financial year.

Total Hotel Revenue

9.1%

The total number of hotel rooms sold on the Gold Coast increased 4.5%, with the average occupancy rate improving 2.8 percentage points. Average revenue per available room also increased 8.5%, resulting in total hotel revenue growing by 9.1% to reach $761.82 million.

Theme Park Revenue

1%

The Ardent Leisure Group and Village Roadshow, the two major operators of the Gold Coast’s theme parks, recorded 0.6% and 1.4% decrease in revenue, respectively, achieved by their theme park portfolios. In contrast, Currumbin Wildlife Sanctuary, an important Gold Coast nature tourist attraction, reported a strong increase in revenue of 8.2%. Jointly, these three key attractions had a decline in revenue of 1%.

Business Confidence

High

According to Griffith University’s Business Confidence Index, business confidence in tourism on the Gold Coast remains high. City of Gold Coast also reported an increase in confidence in the Gold Coast economy amongst local businesses during the year.

6

TABLE OF CONTENTS

1. Executive Summary .................................................................................................... 4

2. Gold Coast Travel Trends ........................................................................................... 7 2.1. Context ..................................................................................................................... 7

2.2. Total visitation to the Gold Coast ........................................................................... 8

2.3. Domestic Visitors .................................................................................................... 9

2.4. International Visitors ............................................................................................. 10

3. Gold Coast Competitiveness Analysis .................................................................... 12

4. Gold Coast Industry Indicators ................................................................................ 14 4.1. Accommodation .................................................................................................... 14

4.2. Gold Coast Airport ................................................................................................ 15

4.3. Theme Parks .......................................................................................................... 16

4.4. Business Sentiment .............................................................................................. 17

5. Australian Travel Trends .......................................................................................... 18 5.1. Context ................................................................................................................... 18

5.2. Total Visitation in Australia .................................................................................. 19

5.3. Domestic Visitors .................................................................................................. 20

5.4. International Visitors ............................................................................................. 20

5.5. Outbound travel by Australians ........................................................................... 21

6. Global Travel Trends ................................................................................................. 22

7. Tourism Insights: New Experiences for young Chinese travellers ........................ 24

8. Data Tables ................................................................................................................ 25

9. Data Sources and Timeline of Release: ................................................................... 34

7

2. Gold Coast Travel Trends

2.1. Context

The last twelve months saw a general increase in consumer confidence globally (Nielsen,

2015), which coupled with the weakening Australian dollar generated positive impacts on

both international and domestic tourism. Whilst business confidence in Australia is

somewhat lower than the previous year (Roy Morgan, 2015)1, confidence on the Gold Coast

remains high, according to local research by both City of Gold Coast and Griffith University.

Confidence has been boosted by ongoing strength in the Chinese market, including

additional visitation during Chinese New Year due to charter flights to Gold Coast Airport

provided by China Southern and Cathay Pacific. Further growth in the Chinese market is

expected in 2016, when Hong Kong Airlines begin operations to the Gold Coast with a series

of charter flights and Jetstar begins direct flights between Wuhan and the Gold Coast.

The Gold Coast tourism industry also benefitted from major events, including the Lions

Rugby Tour, Cricket World Cup, Opera on the Beach, the Gold Coast Airport Marathon,

amongst others. The next Australian Tourism Exchange (ATE) taking place on the Gold

Coast in 2016 is expected to bring substantial economic benefits, directly and longer term

due to exposure of the Gold Coast tourism product portfolio.

Already strong investment into new infrastructure and products on the Gold Coast continues

with the recent announcement that ASF Consortium has been invited to present detailed

project plans for an integrated resort on a site between Sea World and the Gold Coast

Fishermen’s Co-operative on the Spit.

The Mayor’s International Student Ambassador Program was launched in 2014, which is a

new program designed to build relationships between the Gold Coast and international

students studying here while promoting the city as a destination to live, study and visit. The

initiative is a partnership between Study Gold Coast and the City of Gold Coast.

During the year ending June, the Gold Coast recorded above average annual rainfall,

particularly in January and February when the region received an extra 571 mms above the

long-term average of 373 mms in these two months (131 years). This was associated with

Ex-Tropical Cyclone Marcia tracking past the Gold Coast in February. Reportedly, a key

reason for the decline in domestic overnight and daytrip visitation was due to this above

average rainfall during the peak season.

1 See: http://www.roymorgan.com/morganpoll/consumer-confidence/roy-morgan-business-confidence

8

2.2. Total visitation to the Gold Coast

In the year ending June 2015, total international and

domestic overnight visitation to the Gold Coast declined 4%

to 4,190,000 visitors, of which 21% were international

visitors. The five-year average growth rate of total

international and domestic overnight visitors was flat.

During the same period, daytrip visitation to the Gold Coast

increased by 11% to 7,427,000 trips, with the 5-year average remaining steady.

Total overnight visitors’ average length of stay was steady at 5.2 nights. While total visitor

expenditure to the Gold Coast decreased 7% during the year ending June 2015, although

the 5-year average growth rate of expenditure increased slightly by 1% (refer to Table 1).

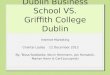

Figure 1 shows total visitor expenditure on the Gold Coast, revealing that the main source of

income from tourism is derived from the domestic overnight market and the only growth in

expenditure has been from the international market2.

Figure 1 Total visitor expenditure on the Gold Coast (Source: Tourism Research Australia).

2 Note: Tourism Research Australia (TRA) only collects expenditure data at the national level. To estimate expenditure at the

state and regional level, TRA employs the Regional Expenditure Model (REX). However, the REX model only provides limited top-line information for regional areas and is not disaggregated by purpose of visit or source market.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Jun-11 Jun-12 Jun-13 Jun-14 Jun-15

Tota

l Exp

en

dit

ure

($

mill

ion

)

Year ending

International Domestic daytrip Domestic Overnight

The number of total visitor nights

spent in Brisbane and the Gold Coast

is forecast to increase by 3.5% over

the next 10 years, above the 2.7%

average predicted for Queensland

(Tourism Research Australia, 2014).

9

2.3. Domestic Visitors

In the year ending June 2015, domestic overnight visitors3 to the

Gold Coast decreased by 6% (or 209,000 visitors) to 3,329,000

visitors4. As a result of the decline in visitation, nights spent on the

Gold Coast also fell 8% (or by 1,072,000 nights to 13,184,000

nights), with average length of stay falling by 2% to 4 nights

(although the 5-year average was steady). This weakening in

visitation, combined with reduced per visitor expenditure (down 7%

or by $61 per visitor), saw total domestic overnight expenditure on the Gold Coast decrease

by 12% (or by $393 million) (refer to Table 2). In contrast, the five year average annual

growth rate in domestic overnight expenditure showed a 1% increase for the Gold Coast

region (Figure 2).

Figure 2 Gold Coast per visitor expenditure ($) by domestic overnight and daytrip visitors (TRA – Regional Expenditure Model).

Domestic holiday visitors were the driver of the declines in overnight domestic visitation to

the Gold Coast during the period with a decline of 19% to 1,764,000 visitors (or by 424,000

visitors). Self-drive holidays accounted for much of the declines, falling by 252,000 visitors to

1,153,000 visitors (down 18%). In contrast, the Gold Coast’s visiting friends and relatives

(VFR) market increased 11% to 1,068,000 visitors (or by 106,000 visitors) suggesting some

substitution may be occurring. Indeed, domestic overnight leisure5 visitors’ use of

commercial accommodation declined 21% to 1,578,000 visitors (or by 411,000 visitors),

while use of private accommodation increased 9% to 1,277,000 visitors (or by 109,000

3 Note: The introduction of mobile phone interviewing on the National Visitor Survey in January 2014 has resulted in a break in

series (please see ‘Disclaimer’ on page ii). However, further investigation of the trends comparing the periods following the break in series (i.e. the six months ending June 2014 with the six months ending June 2015) reveal that the declining trend is also occurring during this period (with overnight trips to the Gold Coast down 6% and nights down 9%). 4 Note: The total sample size for overnight visitors to the Gold Coast is around 1,400. Once this sample is split by source

market and purpose of visit, the accuracy of the estimates is reduced. As there is considerable fluctuation in the time-series data where the sample size is small, only limited information is presented to avoid misrepresentation. 5 Those visitors travelling for the purpose of a holiday or to visit friends and relatives

792

901 847

903 841

98 106 97 107 83

0

100

200

300

400

500

600

700

800

900

1000

Jun-11 Jun-12 Jun-13 Jun-14 Jun-15

$ p

er

visi

tor

Year ending

Expenditure per overnight visitor ($) Expenditure per daytrip visitor ($)

Gold Coast ranks as

Australia’s No. 5

region in terms of

domestic overnight

visitors expenditure

10

visitors). Domestic overnight business visitation to the Gold Coast increased 27% to 408,000

visitors (or by 87,000 visitors).

The key source markets of domestic overnight visitation

to the Gold Coast for the year ending June 2015 were

Brisbane (1,140,000 visitors), Sydney (503,000 visitors),

Melbourne (288,000 visitors), North Coast New South

Wales (177,000 visitors), the Darling Downs (135,000

visitors) and the Sunshine Coast (119,000 visitors). The

Brisbane overnight market had good growth during the

year ending June 2015 (up by 6% or 61,000 visitors), as

did the Sydney market (up 9% or by 41,000 visitors).

However, the other key domestic overnight markets experienced large declines. The

Brisbane overnight market’s average length of stay on the Gold Coast was 2.3 nights (down

0.4 nights).

While there was solid growth in day trip visitation to the Gold Coast (up 11%, or 717,000

visitors), the 5-year average annual growth in daytrips to the Gold Coast was flat. Eighty-six

percent of day trips occur for leisure. The Brisbane market is the key source market for day

trips to the Gold Coast accounting for 5,093,000 day trips. Total day trip expenditure

declined by 14% in the year ending June 2015, driven by a 22% decline in per visitor

expenditure. The 5-year average day trip expenditure only fell by 3% (refer to Table 3).

2.4. International Visitors

In the year ending June 2015, the Gold Coast had strong growth in international visitation,

with an increase of 6% (or 50,000 visitors) compared with the previous year. International

visitors’ average length of stay on the Gold Coast decreased 5% to 10.1 nights, compared

with the previous financial year. This has been a result of declines in more traditional longer-

stay European markets (where average length of stay fell 4.3 nights to 12.9 nights), being

offset by growth in shorter-stay Chinese market (who stay 4.8 nights on average). Despite

this, total international visitor nights in the region increased slightly by 1% (or 82,000 nights)

to 8,681,000 nights.

International visitors to the Gold Coast increased their expenditure per night by 12% (or $14

per night), which – when combined with increases in visitation – generated an overall 13%

increase in expenditure in the region. The result was an additional $131 million being spent

in the Gold Coast region in the year ending June 2015. In total, the international market

contributed $1,102 million directly to the Gold Coast economy for the year ending June 2015

(refer to Table 4).

During the reporting period, the key international source market to the Gold Coast was

China, followed closely by New Zealand. China showed solid growth with an increase of

13% (or 25,000 visitors) to a total 212,000 visitors. Despite the growth in visitor numbers,

China’s average length of stay in the region continues to remain the lowest of all

Top 5 Domestic Overnight

Source Markets (by visitors):

1. Brisbane (1.14 million)

2. Sydney (503,000)

3. Melbourne (288,000)

4. North Coast NSW (177,000)

5. Darling Downs (135,000)

11

international source markets at just 4.8 nights (refer to Table 5)6. This is primarily a result of

an underrepresentation of Chinese education visitors (less than 2% of all Chinese visitors on

the Gold Coast) when compared to 14% of Chinese visitors to Australia being education

visitors. Education visitors typically stay far longer and spend much more while in Australia

than leisure or business visitors.

New Zealand remains the key source market in terms of total visitor nights spent on the Gold

Coast, amounting to a total of 1,581,000 nights in the region for the year ending June 2015.

However, the average length of stay by New Zealand visitors declined 0.8 nights to 9.1

nights on average, which resulted in a decline of 6% in total nights spent on the Gold Coast

(or by 104,000 nights). On a positive note, the UK market has continued to rebound,

demonstrating strong growth of 10% to reach 66,700 visitors (up 6,200 visitors).

Most international visitors to the Gold Coast visited for leisure, with 679,000 coming for a

holiday and 129,000 visiting friends and relatives. The leisure market represents 95% of all

international visitors to the Gold Coast. Recent growth has been mainly from the holiday

market, which increased by 36,000 visitors (refer to Table 6). However, the education market

has also experienced significant growth of 20% (or 3,500 visitors) to reach a total of 21,000.

International visitors coming to the Gold Coast for other purposes (such as for employment,

medical, for the possibility of immigration, for a funeral or for other reasons not identified)

also increased, up 4,400 visitors to a total of 14,000 visitors in the year ending June 2015.

6 Note: Due to the volatility in the visitor night estimates for a number of key source markets over time, only average length of

stay is reported.

12

3. Gold Coast Competitiveness Analysis

The competitiveness analysis compares the Gold Coast against a key comparative set of

Brisbane, Sunshine Coast, Tropical North Queensland, Sydney, Melbourne and Perth. It is

important to understand that some of the competitor destinations (in particular Brisbane,

Sydney and Melbourne) have a broader market base, including substantial business tourism

segments.

In the year ending June 2015, the Gold Coast lost market share of the domestic overnight

visitor market, receiving 4% of all domestic overnight visitors (down 0.5% points) and 4.2%

of domestic visitor nights in Australia (down 0.6% points). Similarly, the Gold Coast lost

market share of overnight visitors total trip expenditure, receiving 5.1% in the year ending

June 2015 (down 0.9% points). This share of expenditure is less than the share received by

Brisbane (6.2%), but greater than that of the Sunshine Coast (3.2%) and Tropical North

Queensland (3.3%) (refer to Table 7).

In contrast to the Gold Coast, Melbourne improved its market share of visitor nights (up

0.3%). The other comparative regions had a slight decrease in market share of domestic

visitor nights (between 1-2%). As a result of Melbourne capturing a larger share of nights,

the region also increased its share of visitor expenditure more than any other comparative

region (up 0.4% to 12.1%). All key comparative regions experience a steady or slight

increase in market share of expenditure (<0.2% each).

Despite the declines in domestic market share, the Gold Coast maintains relatively high

average trip expenditure at $841 per visitor, particularly when compared to other key

regions. Only Tropical North Queensland and Perth have higher average trip expenditures

within the comparative set. The Gold Coast holds a mid-range position for average

expenditure per visitor per night (refer to Table 8).

The Gold Coast has a 4.4% share of the domestic daytrip market in terms of visitor numbers

and a 3.4% share in terms of trip expenditure. The Gold Coast’s average daytrip expenditure

per visitor is $83, well below the $108 average of all daytrips in Australia (refer to Table 9).

Comparatively, the Gold Coast has a strong and growing presence in the international

market, with 13.1% of international visitors stopping over in the Gold Coast. However, only

3.7% of all international visitor nights and 5.0% of all international visitors’ expenditure is

spent on the Gold Coast. This is low when compared to Capital Cities such as Sydney,

Melbourne, Perth and Brisbane, but it is above the share achieved by the Sunshine Coast

and Tropical North Queensland (refer to Table 10).

In the year ending June 2015, the Gold Coast’s market share of the international visitor

nights decreased slightly by 0.3% to 3.7%. Comparatively, other destinations which also

experienced a decline in market share included Sydney (down 0.3 percentage points to

28.6%) and the Sunshine Coast (down 0.2 percentage points to 1.1%). Tropical North

Queensland and Perth maintained their previous market shares of 2.9% and 9.8%,

respectively. Alternatively, Brisbane (up 0.5 percentage points to 9.8%) and Melbourne (up

1.3 percentage points to 20.5%) increased their respective market shares. Overall, however,

market shares are relatively stable.

13

The Gold Coast’s average international visitors’ regional expenditure is $1,280, which is the

second lowest per visitor expenditure in the comparative set, only ahead of the Sunshine

Coast. This result is primarily due to the comparatively lower average length of stay of

international visitors on the Gold Coast, particularly by the Chinese market. On a per night

basis, the Gold Coast has high average expenditure when compared to other key regions at

$127 per night, including Sydney ($102 per night) and Melbourne ($109 per night). Only

Tropical North Queensland has higher average per night expenditure within the comparative

set at $147 per night (refer to Table 11).

14

4. Gold Coast Industry Indicators

4.1. Accommodation

For the year ending June 2015, a total of 4,471,041 hotel

rooms were sold on the Gold Coast, representing an increase

of 4.5% compared with the previous year. The revenue

generated as a result was $762 million (up 9.1%). The average

revenue per available room (RevPAR) has increased by 8.5%

during the year ending June 2015, reaching $122.4 (as shown

in Figures 3).

Figure 3 Gold Coast hotel accommodation revenue per available room (RevPAR) by month and total, year ending June 2015 (Source: Smith Travel Research

7).

Comparisons between other key Australian and New Zealand destinations were available for

the six months to June 2015. During this period, average occupancy rate improved from the

same period in 2014, reaching 69.9% (up 3.9%). The month of January 2015 achieved an

occupancy rate of 81.4%, which was below the 82.1% achieved in January 2014.

Occupancy levels at the Gold Coast in the six months to June 2015 were relatively low

compared with other destinations in Australia and New Zealand. The average occupancy

rates in Australia and New Zealand were 74.3% and 77.5%, respectively. Yet growth in

occupancy and RevPAR during this period was above the national average (see Table 12).

7 Note: Smith Travel Research (STR) in June 2015 collected information from 48, generally larger, hotels, motels and serviced

apartments on the Gold Coast

111.4 112.8 118.2

134.0 131.0

149.2

172.0

119.1

109.9

121.3

96.9 92.4

122.4

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

200.00

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Total

Re

ven

ue

pe

r av

aila

ble

ro

om

($

)

Revenue per available

room in hotels on the Gold

Coast has grown by 8%

since last year; more than

twice as much as the

Australian average growth.

15

4.2. Gold Coast Airport

Total passenger movements at Gold Coast Airport (OOL) amounted to 5,865,437 for the

year ended June 2015 (Figure 4). This represents an increase of 2.1% compared with the

previous financial year. Domestic tourism passenger movements grew by 2.8%, whereas

international passenger movements decreased by 1.6%. Domestic passengers at Gold

Coast airport represent 84.9% of all passenger movements.

Figure 4 Gold Coast Airport domestic and international passenger movements per month, year ending June 2015 (Source: Gold Coast Airport).

The busiest international route servicing Gold Coast Airport continues to be the Auckland-Gold Coast city pair, with 143,350 passengers in the year ended June 2015. The second busiest route is Kuala Lumpur to Gold Coast, recording a total of 92,594 passengers, despite displaying a declining trend over the year (Figure 5). In December flights to Wellington and Queenstown were added, whilst March saw the addition of flights to Nadi. These three new services equated to an additional 25,146 passengers in the year ending June 2015.

Figure 5 International Airline Activity at Gold Coast Airport: City Pairs Data, year ending June 2015 (Source: BITRE, 2015).

428,747

402,351

427,587

475,169

411,566

455,967 473,859

356,089 399,009

416,049

366,883

365,998

78,536 73,245 69,006

73,958

69,329 84,570 87,505

70,607 73,316 71,671

65,550 68,870

0

100,000

200,000

300,000

400,000

500,000

600,000

Jul

Au

g

Sep

Oct

No

v

De

c

Jan

Feb

Mar

Ap

r

May Jun

GC

Air

po

rt P

asse

nge

rs

Month

Total Domestic Passengers Total International Passengers

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15

Pas

sen

ger

nu

mb

ers

pe

r m

on

th

Month City-pair passenger arrivals at GC Airport (bitre)

Auckland

Christchurch

Kuala Lumpur

Nadi

Singapore

Tokyo

Queenstown

Wellington

16

By comparison, Brisbane Airport (BNE) recorded a growth rate of 1% in the year ending

June 2015 (Figure 6), with total passenger movements reaching 22,024,845. Growth at

Brisbane airport was mainly driven by international passenger movements (up 5.7%), while

domestic passenger movements decreased very slightly (down by 0.2%). The domestic

share of all passenger movements at Brisbane airport is 77%. Brisbane Airport is offering

new direct Qantas services from Tokyo to Brisbane and All Nippon Airlines services to

Sydney, offering the first “Star Alliance” option to Japan. Malaysian Airlines discontinued

their services into Brisbane.

Figure 6 Brisbane Airport domestic and international passenger movements year ending June

2015 (Source: Brisbane Airport).

4.3. Theme Parks

Village Roadshow, The Ardent Leisure Group and Currumbin Wildlife Sanctuary each report

on their performance for the financial year ending 2015. All three represent major tourist

attractions on the Gold Coast.

Village Roadshow operates Sea World & Sea World Resort & Water Park, Warner Bros.

Movie World and Wet ’n’ Wild on the Gold Coast. For the year ending June 2015, the three

operations of Village Roadshow recorded a 1.4% decrease in income. Income in the year

ending June 2015 reached a total of $278.5 million. Visitor numbers for the year ending June

2015 amounted to 5.2 million, representing a decline of 3.8% compared with the previous

financial year (see Table 13).

The Ardent Leisure Group Theme Parks include Dreamworld, White Water World, and the

SkyPoint Observation Deck and SkyPoint Climb. In June 2015, Dreamworld launched ABC

kids world. For the second time, in 2014 Dreamworld was awarded Queensland's Best Major

Tourist Attraction at the Queensland Tourism Awards and the third most popular tourist

attraction at the annual Australian Tourism Awards. However, due to decreased per capita

spending, overall revenue decreased slightly (by 0.6%) to $99.5 million. Visitor numbers

increased by 11.7% to 2.28 million during the 2014/2015 financial year.

1,547,258

1,456,096

1,459,502

1,572,627

1,399,985

1,469,586

1,334,089

1,200,818

1,404,321

1,403,294

1,350,493

1,348,984

446,247

437,361

426,194 433,956

400,249

469,693

470,892

373,782

405,104 413,045

380,903

407,697

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

Bri

sban

e A

irp

ort

Pas

sen

gers

Total Domestic Passengers Total International Passengers

17

Currumbin Wildlife Sanctuary, which operates as a zoo and an educational wildlife park, is

another key attraction for the Gold Coast. In the year ending June 2016, Currumbin Wildlife

Sanctuary recorded an 8.2% increase in total revenue to $17.1 million. Attendance for this

period also increased to 433,000, a growth of 6.4% (or 25,982 visitors). This was

accompanied by an overall increase of 1.8% in per guest expenditure. Growth in visitation

was mainly due to four key markets, namely China (up 26%), New Zealand (up 21%),

Sydney (up 18%) and Brisbane (up 11%).

4.4. Business Sentiment

The Griffith University’s Business Confidence Index, conducted by Spence Consulting (80-

100 respondents out of a database of 300 businesses quarterly) gathers data on Gold Coast

business sentiment on a quarterly basis. Business confidence in general has become more

positive during the 2014/2015 financial year, reflecting increased confidence in the Gold

Coast economy and property market. Confidence in the tourism market has marginally

decreased towards the end of the financial year. However, the months of September to

November 2014 displayed high confidence in the tourism market with 84% of respondents

feeling positive or highly positive (see Table 14).

A City wide business survey conducted by the City of Gold Coast Council found that

business confidence has increased over the past two years, with 40% of businesses having

confidence in the Gold Coast economy, compared with just 19% in 2013. In addition, 55% of

businesses had a positive outlook for the future, compared with just 38% in 2013. There was

a shift in focus from jobs, skills and cost of living being a key challenge for the Gold Coast in

2013, to infrastructure and public transport being the key challenge in 2015.

18

5. Australian Travel Trends

5.1. Context

According to the ANZ-Roy Morgan Australian Consumer Confidence Ratings, confidence

amongst Australian consumers fell 2.2% in the year ending June 2015. Similarly, the Roy

Morgan Business Confidence Index showed a decline of 7.6% during the same period.

The weakening Australian Dollar fuelled confidence in tourism in Australia, with expectations

that both the international and domestic markets would grow as Australia becomes relatively

cheaper to other international destinations. During the 2014/2015 financial year, the AUD fell

significantly against the USD and CNY (Figure 7). At the end of June 2015, the AUD was

worth only US$0.77. Comparatively, the AUD was relatively more stable against the Euro

and the British Pound, with the AUD increasing in strength against the NZD. Several Asian

currencies (including Korea and Indonesia) weakened, possibly resulting in weaker demand

for international outbound travel by these source markets.

Figure 7 Foreign exchange trends for the Australian dollar (Source: www.oanda.com).

In addition, tourism to Australia is likely to have benefited from lower fuel costs in the fourth

quarter of 2014. The drop in fuel prices fell from US$98 per barrel of crude oil (Brent) in July

2014 to just US$59 at the end of June 2015 will have been a positive factor, especially for

0

1

2

3

4

5

6

7

0.4

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2

6/0

7/2

01

4

20

/07

/20

14

3/0

8/2

01

4

17

/08

/20

14

31

/08

/20

14

14

/09

/20

14

28

/09

/20

14

12

/10

/20

14

26

/10

/20

14

9/1

1/2

01

4

23

/11

/20

14

7/1

2/2

01

4

21

/12

/20

14

4/0

1/2

01

5

18

/01

/20

15

1/0

2/2

01

5

15

/02

/20

15

1/0

3/2

01

5

15

/03

/20

15

29

/03

/20

15

12

/04

/20

15

26

/04

/20

15

10

/05

/20

15

24

/05

/20

15

7/0

6/2

01

5

21

/06

/20

15

Exchan

ge rate

for C

NY

(Ch

ina)

Exch

ange

rat

e f

or

USD

, EU

R a

nd

NZD

Month AUD/USD AUD/EUR AUD/NZD AUD/CNY

Key facts about Australia in the global tourism context (UNWTO - Tourism Barometer):

International arrivals to Australia have increased by 7.6% in 2014.

Australia continues to rank 11th worldwide in terms of international receipts.

International receipts have increased by 9.0% in Australia in the year to August 2015, compared

with the same period in the previous year (based on preliminary data).

Australians spent US$26.3 billion overseas; they are the 9th largest spenders on tourism

globally.

19

domestic drive tourism. Only a proportion of this decrease has been reflected in the cost of

tourism transportation, with airlines being slow in adjusting their fuel surcharges.

The TTF Mastercard survey for the first quarter of 2015 shows that the tourism sector

remains concerned about the exchange rate, however this concern is lower than previous

surveys (Figure 8). Similar to the previous survey, another perceived impediment related to

taxes charged on tourists and the quality of retail offering. Compared with previous surveys,

there was also increased concern about Australia’s reputation as a desirable tourist

destination, including its reputation as a business and events destination. Labour shortages

(skilled and unskilled) are also of concern.

Figure 8 TTF Mastercard survey: perceptions of business impediments for tourism (Quarter 1 of 2015).

5.2. Total Visitation in Australia

In the year ending June 2015, total international and domestic overnight visitors aged 15

years and over in Australia increased by 5% to 89.8 million visitors, of which 6% are

international visitors. Average length of stay of total overnight visitors remained steady at 6.1

nights, maintaining the 5-year average. Daytrip visitation by domestic Australian residents

was increased slightly by 2% (or 3.9 million trips) to 169.1 million trips.

Total expenditure in Australia by international, domestic overnight and daytrip visitors

increased by 5% to $96 billion in the year ending June 2015 (refer to Table 15). During the

0

5

10

15

20

25

30

35

40

45

50

% r

esp

on

de

nts

re

po

rtin

g is

sue

am

on

gst

top

th

ree

2014 Q3 2015 Q1

20

same period the all-groups consumer price index increased by 1.5% (Reserve Bank of

Australia, 2014), indicating that real total visitor expenditure in Australia had good growth.

5.3. Domestic Visitors

In the year ending June 2015, domestic overnight visitation increased 5%. The 5-year

growth rate increased 3% per annum on average. Domestic visitors’ nights away from home

also increased 6% on the previous year, driven by the increase in number of trips. Total

domestic overnight expenditure in Australia increased 4% to $54.4 billion in the year ending

June 2015, also a result of the increase in visitation with expenditure per visitor declining

slightly (refer to Table 16). Domestic daytrip visitors in Australia increased by 2% during the

period to 169.1 million trips. However, day trip visitors’ expenditure declined 2% to $108 per

visitor (refer to Table 17).

5.4. International Visitors

In the year ending June 2015, international visitors to Australia increased by 7% (or 406,000

visitors) to 6,567,000 visitors. Visitor nights increased by 8% (up 17.9 million nights to 235.5

million nights), with the 5-year trend revealing a 4% average annual growth rate.

Total international visitor expenditure in Australia increased by 11% to $ 2,243 million in the

year ending June 2015, driven by an increase in visitation, average length of stay and per

visitor expenditure. The average length of stay increased by 2%, while expenditure on a per

visitor basis increased 4% (or by $140 per visitor) (refer to Table 18).

As for the Gold Coast, the growth in international visitation to Australia was driven by growth

in leisure visitors, which increased by 233,000 visitors to 4,728,000 visitors in the year

ending June 2015 (up 5%). This increase in visitors delivered growth in total leisure nights

(up 3%) and expenditure by leisure visitors in Australia (up 8%). However, the average

length of stay for leisure visitors decreased by 2% to 26.5 nights.

The key international market for Australia in terms of visitor numbers continues to be New

Zealand (1,154,000 visitors), followed by China (864,000 visitors), the United Kingdom

(629,000 visitors) and the United States (544,000 visitors). China leads the market in terms

of visitor nights with an average length of stay of 42.6 nights8, followed by the United

Kingdom (who stay 41.4 nights on average).

Consequently, Chinese visitors had the

highest total expenditure, spending $5.2

billion in Australia and contributing 23% to

total international expenditure (compared with

their share of arrivals of 13%).

The Chinese leisure market has been

growing strongly (up 21% or 107,300 visitors)

8 Note that the average length of stay of Chinese visitors on the Gold Coast is relatively less compared with other international

markets.

Visitors from China continue to be an

important market for Australia. The increasing

need and opportunity for differentiation this

large market is increasingly recognised by

governments and private sector trade

organisations, tourism bureaus, and those

providing market intelligence (e.g. Hurun

Reports at http://up.hurun.net).

21

and maintaining their average length of stay of 22.3 nights. The Chinese education market

also displayed strong growth, increasing by 20% (19,000 visitors) and staying 161.3 nights

on average. Education visitors represent 13% of the Chinese market in terms of visitors, but

50% of all Chinese visitor nights.

Besides China, other key growth markets in terms of visitor numbers for Australia in the year

ending June 2015 include the United States (up 43,300 visitors), New Zealand (up 38,600

visitors) and India (up 34,400 visitors).

In the year ending June 2015, Queensland received 2,229,000 visitors (an increase of 8%).

Collectively these visitors spent a total of $4.6 billion (an increase of 15%) in Queensland.

Growth rates in terms of expenditure for Queensland were lower than Tasmania (up 27%),

similar to Victoria (up 15%), New South Wales (up 10%) and Northern Territory (up 18%),

but noticeable higher than South Australia (up 5%) and Western Australia (up 1%).

5.5. Outbound travel by Australians

In the year ending March 20159, outbound travel remained attractive for Australians. The

number of all outbound trips increased 3% to 8,187,000 trips, below the five year average

annual rate of 5%. Total nights during the period were flat, well below the five year average

annual rate of 4%. This was a result of average length of stay overseas declining 0.7 nights

to 19.7 nights. Total expenditure increased 3%, driven mainly by visitor numbers, as

expenditure per visitor was flat at $5,967 per trip (refer to Table 19).

9 Note: Reporting period is year ending March as Tourism Research Australia collects information on outbound travel by

Australians, but the collection lags behind that of the overnight and daytrip results due to the duration of the domestic residents’ overseas trip.

22

6. Global Travel Trends

The year ending June 2015 saw an increase in Global consumer confidence (Nielsen, 2015).

According to the United Nations World Tourism Organisation (UNWTO), the volume of

international tourism arrivals reached 1,248 million globally in the year ending December

2014 (Figure 9). This represents an increase of 4.2% on the previous year10. The UNWTO

forecasts that international tourism will grow at a rate between 3% and 4% in 2015.

Figure 9 Global tourism expenditure (US$ billion) for the last five years (Source: United Nations World Tourism Organisation, 2015).

Europe remains the largest tourist destination in terms of international tourism receipts11,

with the region receiving 41% (US$511.6 billion) of global tourism expenditure in 2014

(Figure 10). The Asia Pacific region was the second largest receiver of tourism expenditure

(30% of global expenditure with US$377.0 billion). Tourism receipts in Asia Pacific grew by

4.6% in 2014 compared with the previous year.

10

Note: Global tourism data are provided by the UNWTO’s World Tourism Barometer. 11 International tourism receipts are the receipts earned by a destination country from inbound tourism and cover all tourism

receipts resulting from expenditure made by visitors from abroad. This concept includes receipts generated by overnight as well

as by same-day trips by visitors from neighbouring countries. It excludes the receipts related to international transport

contracted by residents of other countries (e.g. ticket receipts from foreigners travelling with a national company).

966

1,082 1,117

1,198 1248

400

500

600

700

800

900

1,000

1,100

1,200

1,300

2010 2011 2012 2013 2014

Glo

bal

to

uri

sm e

xpe

nd

itu

re

(US$

Bill

ion

)

23

Figure 10 International tourism receipts in world regions (Source: United Nations World Tourism Organisation, 2015).

The Chinese continued to be the world’s largest spender on tourism activity: in 2014 they

spent US$164.9 billion on international tourism. Chinese expenditure grew by 28.2%

compared with the previous year. Travellers from the USA were the second largest spender

with US$110.8 billion in 2014 (a growth of 5.8%) (Figure 11).

Figure 11 International tourism expenditure (outbound tourism) for key source countries for Australia (Source: United Nations World Tourism Organisation, 2015).

0

200

400

600

800

1,000

1,200

1,400

World Europe Asia andthe Pacific

Americas Africa MiddleEast

Tou

rism

re

ceip

ts b

y re

gio

n

(US$

bill

ion

)

Receipts 2013 (US$ billion)

Receipts 2014 (US$ billion)

0

20

40

60

80

100

120

140

160

180

Tou

rist

exp

en

dit

ure

(U

S$ b

illio

n)

Expenditure 2013 (US$ billion)

Expenditure 2014 (US$ billion)

24

7. Tourism Insights: New Experiences for young Chinese travellers

To remain a leading Australian leisure tourism destination, the Gold Coast needs to develop

new experiential products. Here we offer new insights into young Chinese travellers from a

mixed method study that used focus groups and surveys to assist Gold Coast businesses

with improving existing and developing new tourism experiences. Eight focus groups (7 with

Chinese and 1 with mixed nationalities) were conducted with four to eight participants

studying English language and undergraduate degree programs at Griffith University and

The University of Queensland in Queensland, Australia. In addition, a survey was completed

by 366 international students living and studying in Australia, with 80% being from China.

Marketing to young Chinese travellers requires a different approach to more traditional

markets. This is a mobile-savvy market with the majority having smartphones. As a result,

they want to use Chinese mobile phone based applications, such as WeChat. They

particularly use their smartphones to take photos to show friends and family what they are

doing while in Australia and that they are safe and healthy. They also use their smartphones

to get around and find locations. Indeed, they wanted to be able to navigate around

attractions using their smartphone and desired technology-based interpretation and

translation. Importantly, they want websites to use simple English words with lots of pictures.

Young Chinese travellers are quite conservative, with only 10-20% being “adventure

seekers”. The market generally likes to stay within their comfort zone. Most students were

interested in visiting or had visited the major cities or iconic tourist attractions (such as the

Great Barrier Reef or Uluru) while in Australia. They chose these destinations because they

are familiar ‘must see’ iconic attractions. Most did not want to visit regional destinations and

the notion of getting out and dispersing in regional areas was not particularly attractive. To

attract them to visit regional areas there needs to be an iconic or one-of-a-kind attraction.

Most young Chinese travellers we talked to had visited the Gold Coast theme parks, but they

did not know about other Gold Coast tourism products (e.g. surfing, jet boating, kayaking).

They felt these products were outside their ‘comfort zone’. To feel comfortable about a new

product, this market needs to be able to relate an activity to something they were already

familiar with. For example, young Chinese travellers loved Australian koalas as they can

relate these animals to their own panda bears. By drawing links with something they are

familiar with, such as highlighting similarities between Chinese mythology and Australian

Aboriginal dreamtime stories, a new product can be introduced in a more appealing way.

Young Chinese travellers are often in Australia to study. Their leisure time is often spent

shopping or “hanging out” with friends. They enjoy looking at the beach, but do not swim.

There are significant cultural differences between young Australian and young Chinese

travellers in their attitudes to the beach and water based activities. Fear of the open surf and

avoidance of the sun are key concerns of young Chinese travellers and most cannot swim.

So, they generally prefer more passive, rather than active, activities at the beach – such as

observing the beauty and atmosphere. Regardless, the beach is very attractive to this

market and is a key motivation for visiting the Gold Coast over other destinations.

For more information, contact: Dr Sarah Gardiner ([email protected]) or Professor

Noel Scott ([email protected]), or visit the Griffith Institute for Tourism website:

https://www.griffith.edu.au/business-government/griffith-institute-tourism

25

8. Data Tables

Table 1 Total Overnight and Daytrip Visitors on the Gold Coasta, year ending June 2011

to June 2015

Expenditure

Year ending

Total Overnight

Visitors ('000)

b

Total Visitor Nights ('000)

Average Length of

Stay (nights)

Daytrip Visitors

('000)

Total Overnight

and Daytrip Visitors (‘000)

Total ($million)

c

per Visitor

($)

Jun-11 4,109 21,113 5.1 7,348 11,457 4,201 367

Jun-12 4,098 21,687 5.3 7,041 11,139 4,639 416

Jun-13 4,432 22,471 5.1 7,401 11,833 4,674 395

Jun-14 4,349 22,855 5.3 6,710 11,059 4,882 441

Jun-15 4,190 21,866 5.2 7,427 11,617 4,521 389

12-month Real

changed

-159 -990 0.0 717 558 -361 -52

12-month Percentage change (%)

-4 -4 -1 11 5 -7 -12

5-year average growth (%)

0 1 0 0 0 1 1

a. All figures relate to International Visitors and Australian residents aged 15 years and over. b. Total international and domestic overnight visitors on the Gold Coast c. Includes package expenditure. d. Some figures may not sum due to rounding. Source: Tourism Research Australia, International and National Visitor Surveys

Table 2 Domestic Overnight Visitors to the Gold Coasta, year ending June 2011 to June

2015

Expenditure

Year ending Overnight

Visitors ('000) Visitor Nights

('000)

Average length of stay

(nights)

Including airfares and

long distance transport

costs ($million)

per Visitor ($)

Jun-11 3,363 13,362 4.0 2,663 792

Jun-12 3,363 13,789 4.1 3,031 901

Jun-13 3,664 14,790 4.0 3,104 847

Jun-14 3,538 14,256 4.0 3,194 903

Jun-15 3,329 13,184 4.0 2,801 841

12-month Real change

-209 -1,072 -0.1 -393 -61

12-month Percentage change (%)

-6 -8 -2 -12 -7

5-year average growth (%)

0 0 0 1 1

a. All figures relate to Australian residents aged 15 years and over. Source: Tourism Research Australia, National Visitor Survey

26

Table 3 Domestic Daytrip Visitors on the Gold Coasta, year ending June 2011 to June

2015

Year ending Visitors ('000) Expenditure

($million) Expenditure per

visitor ($)

Jun-11 7,348 721 98

Jun-12 7,041 749 106

Jun-13 7,401 716 97

Jun-14 6,710 716 107

Jun-15 7,427 617 83

12-month Real change

717 -99 -24

12-month Percentage change (%)

11 -14 -22

5-year average growth (%)

0 -3 -3

a. All figures relate to Australian residents aged 15 years and over. Source: Tourism Research Australia, National Visitor Survey

Table 4 International Visitors on the Gold Coasta, year ending June 2011 to June 2015

Expenditure

Year ending Visitors ('000) Visitor Nights

('000)

Average length of stay

(nights)

Including package

($million) per

visitor ($)

Jun-11 746 7,751 10.4 818 1,097

Jun-12 735 7,898 10.7 859 1,169

Jun-13 768 7,681 10.0 854 1,112

Jun-14 811 8,599 10.6 971 1,198

Jun-15 861 8,681 10.1 1,102 1,280

12-month Real change

50 82 -0.5 131 82

12-month Percentage change (%)

6 1 -5 13 7

5-year average growth (%)

3 2 -1 6 3

a. All figures relate to International Visitors aged 15 years and over. Source: Tourism Research Australia, International Visitor Survey

27

Table 5 International Visitors on the Gold Coast by country of residencea, year ending

June 2015

Country of residence

Visitors ('000)

12-month real change

(‘000)

12-month percentage change (%)

5-year average

growth (%)

Average length of

stay (nights)

China 212 25 13% 13 4.8

New Zealand 189 5 3% 1 8.4

United Kingdom 67 6 10% 1 12.6

Japan 48 -8 -14% -10 18.8

Other Europe 46 1 2% 0 15.4

Other Countries 44 7 19% 4 18.0

Singapore 34 -8 -18% 10 6.3

United States 31 4 14% 4 11.1

Malaysia 30 -1 -3% 2 5.6

Korea 26 7 35% -5 11.8

Germany 26 8 48% 9 9.3

India 21 0 -1% 15 10.0

Other Asia 20 1 6% -1 16.4

Hong Kong 18 -1 -7% 1 14.5

Taiwan 19 3 21% 5 19.0

Canada 16 0 -3% 1 15.2

Scandinavia 13 2 15% 2 11.8

Total 861 50 6% 3 10.1 a. All figures relate to International Visitors aged 15 years and over. Source: Tourism Research Australia, International Visitor Survey

Table 6 International Visitors on the Gold Coast by purposea, year ending June 2015

Purpose of visit Visitors ('000)

12-month real change

(‘000)

12-month percentage change (%)

5-year average

growth (%)

Average length of

stay (nights)

Holiday 679 53 9% 0 6.4

Visiting friends & relatives

129 -2 -2% 0 15.3

Business 32 -8 -23% -3 6.4

Education 21 0 -1% -2 115.5

Other 14 4 45% 0 26

Total 861 42 5% 0 10.6 a. All figures relate to International Visitors aged 15 years and over main reason for stopping over in the destination. Source: Tourism Research Australia, International Visitor Survey

28

Table 7 Domestic Overnight Visitors by comparative regionsa, year ending June 2015

Comparative regions

Overnight visitors ('000)

% of Visitors

Visitor Nights ('000)

% of Visitor Nights

Trip Expenditure ($m)

% of Total Trip Expenditure

Gold Coast 3,434 4.2 13,875 4.5 3,015 5.5

Brisbane 5,166 6.3 16,983 5.5 3,166 5.8

Sunshine Coast 2,885 3.5 10,736 3.5 1,848 3.4

Tropical North Queensland

1,685 2.1 9,094 2.9 1,705 3.1

Sydney 8,527 10.5 23,417 7.6 6,063 11.1

Melbourne 7,787 9.6 22,502 7.3 6,525 12.0

Perth 3,306 4.1 11,149 3.6 2,790 5.1 a. All figures relate to Australian residents aged 15 years and over. Source: Tourism Research Australia, National Visitors Survey

Table 8 Domestic Overnight Visitor expenditure by comparative regionsa, year ending

June 2015

Comparative regions

Trip Expenditure ($m)

Average Trip Expenditure per visitor

Average expenditure per visitor per night

Average length of stay (nights)

Gold Coast 2,801 841 212 4.0

Brisbane 3,429 633 198 3.2

Sunshine Coast 1,801 627 167 3.7

Tropical North Queensland

1,836 1,021 204 5.0

Sydney 6,424 712 258 2.8

Melbourne 6,704 828 290 2.9

Perth 2,837 865 242 3.6

a. All figures relate to Australian residents aged 15 years and over. b. This is the average of only those who identified as having stayed in commercial accommodation. Source: Tourism Research Australia, National Visitors Survey

Table 9 Domestic Daytrip visitors by comparative regions, year ending June 2015a

Comparative regions Visitors ('000)

% of Visitors

Trip Expenditure ($m)

% of Trip Expenditure

Average Trip Expenditure per Visitor

Gold Coast 6,874 4.2 603 3.4 88

Brisbane 11,182 6.8 1,180 6.6 106

Sunshine Coast 5,484 3.3 546 3.0 100

Tropical North Queensland 2,173 1.3 231 1.3 106

Sydney 18,937 11.5 2,010 11.2 106

Melbourne 16,403 10.0 1,830 10.2 112

Perth 11,068 6.7 1,088 6.1 98

a. All figures relate to Australian residents aged 15 years and over. Source: Tourism Research Australia, National Visitors Survey

29

Table 10 International visitors by comparative regions, year ending June 2015a

Comparative regions Visitors ('000)

% of Visitors

Visitor Nights ('000)

% of Visitor Nights

Regional Expenditure ($m)

% of Regional Expenditure

Gold Coast 861 13.1 8,681 5.0 1,102 5.0

Brisbane 1,066 16.2 23,061 8.1 1,782 8.1

Sunshine Coast 257 3.9 2,519 0.9 194 0.9

Tropical North Queensland 759 11.6 6,801 4.5 1,000 4.5

Sydney 3,096 47.1 67,312 31.1 6,881 31.1

Melbourne 2,166 33.0 48,308 23.7 5,252 23.7

Perth 783 11.9 23,011 8.8 1,954 8.8 a. Estimates are for International Visitors aged 15 years and over Source: Tourism Research Australia, International Visitors Survey

Table 11 International Visitors expenditure and average length of stay by comparative regions

a, year ending June 2015

Comparative regions

Regional Expenditure ($m)

Average Regional Expenditure per visitor

Average Regional expenditure per visitor per night

Average length of stay (nights)

Gold Coast 1,102 1,280 127 10.1

Brisbane 1,782 2,497 77 21.6

Sunshine Coast 194 754 77 9.8

Tropical North Queensland

1,000 1,318 147 9.0

Sydney 6,881 1,671 102 21.7

Melbourne 5,252 2,425 109 22.3

Perth 1,954 2,222 85 29.4 a. Estimates are for International Visitors aged 15 years and over Source: Tourism Research Australia, International Visitors Survey

30

Table 12 Comparison of accommodation occupancy and RevPAR six months to June 2015 compared with the six months to June 2014 for key destinations in Australia and New Zealand

Occupancy (%) Revenue per available room ($)

Six months to June 2015

% Change from previous year

Six months to June 2015

% Change from previous year

Australia 74.3 1.4 134.9 3.4

Gold Coast 69.9 3.9 118.7 8.0

Adelaide 76.5 -4.2 115.5 -4.6

Brisbane 72.8 -3.3 126.4 -5.6

Cairns 73.4 8.2 89.7 10.2

Canberra 72.5 6.1 118.0 6.8

Melbourne 81.6 1.4 152.8 3.8

Perth 81.0 -1.5 161.8 -2.9

Sydney 84.6 2.3 175.3 6.9

Darwin 64.2 -10.0 106.8 -12.7

Hobart 82.3 2.8 135.6 5.2

New Zealand 77.5 4.8 119.2 14.4

Auckland 81.6 0.0 132.4 12.4

Queenstown 76.1 8.4 123.1 16.8

Wellington 77.9 6.3 124.4 15.2

Table 13 Revenue and visitation at Ardent Leisure Group and Village Roadshow theme Parks and Currumbin Wildlife Sanctuary, Gold Coast (Source: Ardent Leisure Group and Village Roadshow Annual Reports full year ended June 2015)

Revenue ($) % Change from previous year

Visitation % Change from previous year

Theme Parks (Ardent) 99,571,000 -0.6 2,281,606 11.7%

Village Roadshow 278,500,000 -1.4 5,200,000 -3.8%

Currumbin Wildlife Sanctuary

17,108,000 8.2% 433,301 6.4%

31

Table 14 Gold Coast business sentiment for three 3-month periods in the 2014/2015 financial year (Source: Spence Consulting)

What is your level of confidence over the next three months regarding the …. ?

Aug-14 Nov-14 May-15 Aug-15

Gold Coast economy generally

Highly positive 6% 13% 3% 9%

Positive 54% 56% 47% 63%

Neutral 31% 24% 36% 21%

Negative 9% 6% 9% 4%

Highly negative 0% 1% 5% 3%

Gold Coast property market

Highly positive 6% 10% 63% 7%

Positive 62% 54% 25% 59%

Neutral 23% 35% 7% 28%

Negative 8% 1% 0% 6%

Highly negative 0% 0% 4% 0%

Gold Coast tourism market

Highly positive 14% 27% 57% 12%

Positive 57% 57% 30% 57%

Neutral 29% 15% 9% 27%

Negative 0% 1% 0% 4%

Highly negative 0% 0% 0% 0%

Gold Coast retail market

Highly positive 0% 7% 34% 3%

Positive 40% 53% 50% 43%

Neutral 37% 39% 13% 47%

Negative 23% 1% 3% 7%

Highly negative 0% 0% 3% 0%

Table 15 Total Overnight and Daytrip Visitors in Australiaa, year ending June 2011 to

June 2015

Year ending

Total Overnight Visitors ('000)

b

Total Visitor nights ('000)

Average length of stay

Daytrip visitors ('000)

Total expenditure in Australia ($000)

c

Expenditure per visitor ($)

c

Jun-11 76,347 456,438 6.0 156,287 79,407 341

Jun-12 78,807 477,004 6.1 168,847 85,547 345

Jun-13 80,982 500,765 6.2 167,857 88,758 357

Jun-14 85,257 512,613 6.0 165,237 91,589 366

Jun-15 89,796 548,932 6.1 169,108 96,011 371

12-month Real

change 4,539 36,319 0 3,871 4,423 5

12-month Percentage change (%)

5 7 2 2 5 1

5-year average

growth (%) 3 4 0 2 4 2

a. All figures relate to International Visitors and Australian residents aged 15 years and over. b. Total international and domestic overnight visitors in Australia. c. Includes international and domestic overnight visitor expenditure, as well as daytrip expenditure.

Source: Tourism Research Australia, International and National Visitor Surveys

32

Table 16 Domestic Overnight Visitors in Australiaa, year ending June 2011 to June 2015

Year ending Overnight trips (‘000) Nights (‘000)

Average length of stay

Total Expenditure in Australia ($000)

Expenditure per visitor ($)

Jun-11 70,977 266,235 3.8 46,588,920 656

Jun-12 73,369 278,348 3.8 49,826,532 679

Jun-13 75,268 286,056 3.8 51,442,035 683

Jun-14 79,096 294,980 3.7 53,297,712 674

Jun-15 83,229 313,383 3.8 55,425,704 666

12-month Real change

4,133 18,403 0.0 2,127,992 -8

12-month Percentage change (%)

5 6 1 4 -1

5-year average growth (%)

3 3 0 4 0

a. All figures relate to Australian residents aged 15 years and over. Source: Tourism Research Australia, National Visitor Survey

Table 17 Domestic Daytrip Visitors in Australiaa, year ending June 2011 to June 2015

Year ending Daytrips (‘000) Expenditure ($000)

Expenditure per visitor ($)

Jun-11 156,287 15,157,562 97

Jun-12 168,847 17,544,380 104

Jun-13 167,857 18,065,154 108

Jun-14 165,237 18,230,931 110

Jun-15 169,108 18,282,986 108

12-month Real change

3,871 52,055 -2

12-month Percentage change (%)

2 0 -2

5 year annual average (%)

2 4 2

a. All figures relate to Australian residents aged 15 years and over. Source: Tourism Research Australia, National Visitor Survey

33

Table 18 International Visitors to Australiaa, year ending June 2011 to June 2015

Year ending Visitors ('000) Visitor nights ('000)

Average length of stay

Total expenditure in Australia ($000)

Expenditure per visitor ($)

Jun-11 5,370 190,203 35.4 17,660 3,289

Jun-12 5,438 198,656 36.5 18,176 3,342

Jun-13 5,714 214,709 37.6 19,251 3,369

Jun-14 6,161 217,633 35.3 20,060 3,256

Jun-15 6,567 235,549 35.9 22,303 3,396

12-month Real change

406 17,916 1 2,243 140

12-month Percentage change (%)

7 8 2 11 4

5-year average

growth (%) 4 4 0 5 1

a. All figures relate to International Visitors aged 15 years and over. Source: Tourism Research Australia, International Visitor Survey

Table 19 Outbound trips by Australian residentsa, nights and expenditure, year ending

March 2015

Year ending Outbound Trips ('000)

Nights on trip ('000)

Average length of stay

Expenditure ($000)

Expenditure per visitor ($)

Mar-11 6,467 131,321 20.3 38,135,546 5,897

Mar-12 7,032 143,377 20.4 42,595,844 6,057

Mar-13 7,341 147,761 20.1 44,619,757 6,078

Mar-14 7,925 161,466 20.4 47,322,171 5,971

Mar-15 8,187 161,115 19.7 48,851,396 5,967

12-month Real change

262 -351 -0.7 1,529,225 -4

12-month Percentage change (%)

3 0 -3 3 0

5-year average

growth (%) 5 4 -1 5 0

a. All figures relate to Australian residents aged 15 years and over. Source: Tourism Research Australia, National Visitor Survey

34

9. Data Sources and Timeline of Release:

Source Data/Publication Release Frequency

BITRE Transport Statistics

International Airline Activity - Time Series - City Pairs Data http://www.bitre.gov.au/publications/ongoing/international_airline_activity-time_series.aspx

Monthly

Brisbane Airport

Passenger Statistics http://www.bne.com.au/corporate/media-centre/passenger-statistics

Monthly

Bureau of Meteorology

Rainfall Data (Southport Station)

http://www.bom.gov.au/climate/data/ Monthly

Deloitte Access Economics

Tourism and Hotel Market Outlook http://www2.deloitte.com/au/en/pages/consumer-business/articles/tourism-hotel-outlook.html

Biannual

Gold Coast Airport

Gold Coast Airport Passengers

http://goldcoastairport.com.au/corporate/statistics/ Monthly

City of Gold Coast

2015 Citywide Business Survey Annual

Nielsen

Consumer Confidence Q1/2015

http://www.nielsen.com/content/dam/nielsenglobal/apac/docs/reports/2015/nielsen-global-consumer-confidence-report-q1-2015.pdf

Quarterly

Smith Travel Research

Hotel Survey, Gold Coast (Gold Coast Tourism) Quarterly

Spence Consulting

Griffith University’s Business Confidence Index Quarterly

Tourism Australia

Tourism Australia Aviation Quarterly Market Updates

http://www.tourism.australia.com/statistics/8696.aspx Quarterly

Tourism Research Australia

Regional Forecasts

http://www.tra.gov.au/publications-list-State-tourism-forecasts-2014-2014.html Annual

Tourism Research Australia

Tourism Forecasts

http://www.tra.gov.au/research/State-tourism-forecasts-2014-2014.html Biannual

Tourism Research Australia

Australian Residents’ outbound trips – NVS release

http://www.tra.gov.au/statistics/Australians-travelling-overseas.html Quarterly

TRA/GCCC

Domestic Overnight Tourism – NVS release

Overnight trips in Australia by residents

http://www.tra.gov.au/research/domestic-travel-by-australians.html

Quarterly

TRA/GCCC Daytrip Tourism – NVS release Quarterly

TRA/GCCC International Tourism – IVS release Quarterly

Tourism and Transport Forum

Mastercard Sentiment Survey

http://www.ttf.org.au/Content/sentimentsurvey.aspx Quarterly

UNWTO World Tourism Barometer & Statistical Annex Quarterly