Embed Size (px)

Citation preview

Globalization: An Economic

Perspective

World View

Global Education Leaders' Program

14 June 2010

Professor Peter Brews, Kenan-Flagler

Business School, the University of North

Carolina at Chapel Hill

Globalization has many facets/dimensions:

Historic...first globalization of peoples; then globalization for

resources (scramble for Africa...)

Most recently: economic globalization

Discussion today pertains to economic globalization, which relates to

the explosion of productivity experienced over the past three hundred

years or so

Economic Globalization:

Relates to understanding differences between pre-industrial,

industrial, post industrial contexts, and what drives competitiveness in

the last two

Pertains to knowing which factors/resources/competencies are

available/becoming available in other parts of the world, and then

knowing what to do/focus on to compete in this widening

productivity/resource/competence availability

Requires knowing the difference between market and supply seeking,

and to what happens to consumption/PPP as nations get in the game

Pre Industrial Industrial

Principal

factors of

production

Land

Labor

Land

Labor (physical)

Capital

Key work

units

Rural families, small

tribal societies, class

based feudal

systems

Urbanized, vertically integrated, hierarchically

controlled factories

Capability

of Capital

Minimal Dedicated, inflexible, electro-mechanical

processors, supported by dedicated humans;

hands and machines

Marketing

challenge

Meeting basic needs Meeting demands of unsophisticated consumers

with little choice

Principals

of

production

Survival,

generalization

High volume, low variety leads to high

quality/low cost; specialization, standardization,

mass production/distribution

The Pre Industrial and Industrial Worlds

Industrial Post Industrial

Principal

factors of

production

Land

Labor (physical)

Capital

Land

Labor (mental)

Capital

Key work

units

Urbanized, vertically integrated,

hierarchically controlled factories

Small/large, centralized/de-

centralized, local/global, vert. de-

integrated/IT integrated networks

Capability

of Capital

Dedicated, inflexible, electro-

mechanical processors,

supported by dedicated humans;

hands and machines

Flexible, ‘smart’ programmable

processors, operating with little

human intervention once

programmed; minds and machines

Marketing

challenge

Meeting demands of

unsophisticated consumers with

little choice

Meeting demands of informed

consumers with much choice;

services and solutions intensive

Principals

of

production

High volume, low variety leads to

high quality/low cost;

specialization, standardization,

mass production/distribution

Automation, specialization, high/low

vol., high variety, speed, flexibility,

mass customization, continuous

innovation/advantage upgrading

The Industrial and Post Industrial Worlds

In the Industrial to Post Industrial shift two categories of businesses worth

studying:

1. Classic Post Industrial firms, e.g.

Microsoft

Cisco Systems

Oracle/SAP

Amazon.com

eBay

Nike

or

2. Industrial firms moving towards Post Industrial status, e.g.

Caterpillar Siemens

Cemex GE

Medtronics GM

Industrial Post Industrial

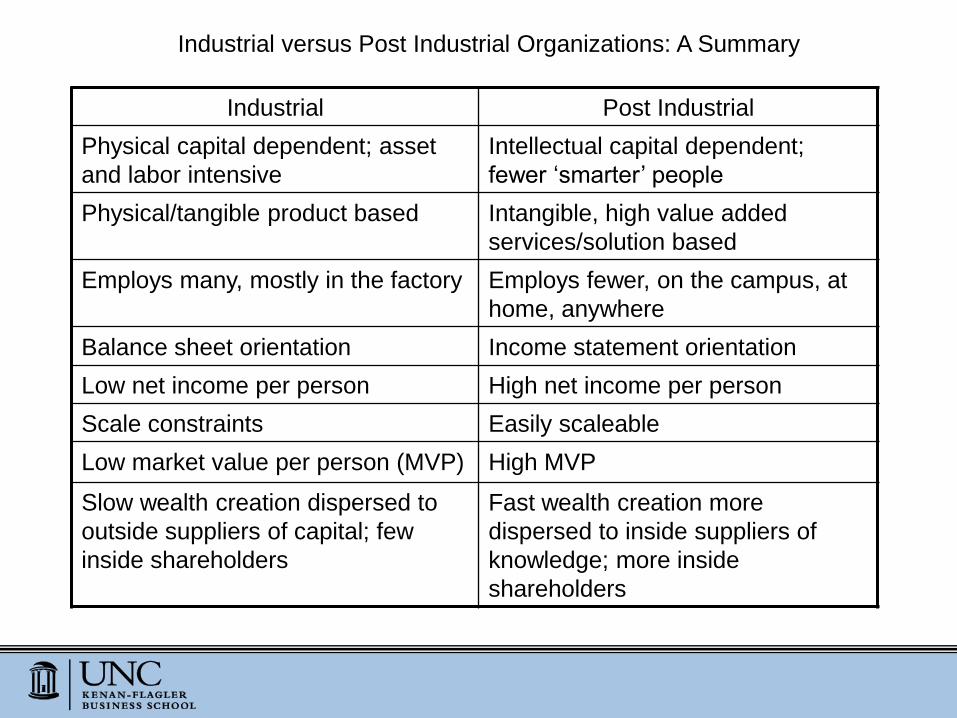

Physical capital dependent; asset

and labor intensive

Intellectual capital dependent;

fewer ‘smarter’ people

Physical/tangible product based Intangible, high value added

services/solution based

Employs many, mostly in the factory Employs fewer, on the campus, at

home, anywhere

Balance sheet orientation Income statement orientation

Low net income per person High net income per person

Scale constraints Easily scaleable

Low market value per person (MVP) High MVP

Slow wealth creation dispersed to

outside suppliers of capital; few

inside shareholders

Fast wealth creation more

dispersed to inside suppliers of

knowledge; more inside

shareholders

Industrial versus Post Industrial Organizations: A Summary

Industrial versus Post Industrial Companies: Comparative Data

Microsoft Cisco Nike Wal-Mart Caterpillar Ford GM

Date established 1975 1984 1968 1962 1925 1903 1908

Number of employees 57,000 34,000 23,000 1.5 million 69,169 327,000 324,000

Market cap in US$

(at Feb. 28, 2005)

273bn 113bn 23bn 218bn 32bn 23bn 20bn

Market value per

employee ((US$)

4.8m 3.3m 1m 145,333 463,768 70,336 61,728

Net income/Sales

(%, 2004)

26.0 22.8 8.4 3.6 6.7 2.1 1.9

Net income/Employee

(US$)

175,368 158,441 47,565 6,850 29,492 11,113 11,391

Unless otherwise stated, all data based on most recent annual financial statements as at April 2005.

Net income is from continuing operations before extraordinary items for most recent 12 months ending 31

January 2005

The industrial to post industrial shift is profoundly effecting:

• Role of humans in productive work

• Structure, scope, speed, operational performance of firms

and

• Nature/complexity of goods and services (and solutions) on offer

All organizations around the world are currently adjusting to the effects

of this structural change

Why is Economic Globalization important to the state/citizens of North

Carolina?

• First, economic globalization for Americans was a supply seeking

enterprise; consumers in America greatly benefitted

• Over the 20th Century America was consumer of last resort to the global

economy

• Economic globalization will now become more a market seeking enterprise

for Americans; instead of selling only to 300 million at home the potential

market is billions of consumers elsewhere…go where the money is!

• Can producers in America offer products/services/solutions others in the

world will want?

At the leading edge innovating faster than those behind can replicate is best

route for competitive survival (remember Solow’s tfp as the major source of

national growth for the United States)

Political, community, and education leaders must ensure North Carolinians are

ready to compete in this post industrial, globalizing, fast moving world…

And that NC is an attractive location to invest in in the ongoing struggle for

productivity, as well as an attractive place to live in, holiday in, and retire in…

What must educators do?

• Prepare American human capital for knowledge intensive, creative work, so

we can innovate at a rate faster than others can replicate; high level math and

science skills are table stakes

• Discipline and deferred gratification must be instilled in students so they

make the educational investment and learn how to THINK, problem solve,

research, imagine, create, connect dots etc.

• My contract with my children…

• Schools, Universities and Community Colleges must develop curricula that

prepare workers for 21st Century, high value creative work, or for work co-

operating with smart machines delivering smart goods, services, or solutions

Digging out: America in the

Reset World

Global Education Leaders' Program

World View

Professor Peter Brews

Kenan-Flagler Business School,

University of North Carolina at Chapel Hill

14

The US is in worst shape it has been in for generations:

• 25 years living beyond means have finally caught up

• Economically, out of balance both publically and privately

• Some core industries in deep trouble (banking, automobiles, construction, retail)

while others face serious funding issues (healthcare, education, military…)

15

Not really credit crisis but over-consumption/living beyond means crisis: credit

symptom, not cause

Two propositions:

• Americans could cut consumption by 20% and probably wouldn’t notice: 20%

smaller houses, 20% smaller cars; 20% less food; 20% less clothing etc.

• In face of global imbalances and global competition/scramble for resources,

2006/7 American consumption levels unsustainable

16

US Political Economy/Public Sector Imbalances

.

US Federal Gross Debt as % of GDP: 1940-2009

Source: zFacts.com

US Gross Federal Debt is now close to 100% of US GDP

Source: http://www.usgovernmentspending.com/downchart_gs.php?year=1792_2010&view=1&expand=

Even before the Credit Crisis:

• Social Security/Medicaid surpluses being raided to balance federal budget

• Federal government borrowing to meet expenditures; foreign savers

meeting some of need…Japan, China, Saudi Arabia

Country Nov 2008 Nov 2009

China 681.9 798.9

Japan 577.1 751.5

United Kingdom 360.0 249.3

Caribbean Banking Centers 220.8 171.7

Oil Exporters 129.6 185.3

Brazil 78.1 144.9

Total 2047.5 2,301.6

MAJOR FOREIGN HOLDERS OF TREASURY

SECURITIES (in billions of dollars)

Source: Department of the Treasury/Federal Reserve Board, November 2009

21

US Private Sector Imbalances

Source: http://www.econ.yale.edu/~shiller

US Macroeconomic data: Home prices, building costs, interest rates, population

Graph constructed by Professor Christian Lundblad, Kenan-Flagler Business School, University of North Carolina at

Chapel Hill.

Consumption and GDP data from the Bureau of Economic Analysis (BEA). Mortgage equity withdrawals are measured as

the year-over-year change in mortgage debt (from the Federal Reserve Flow of Funds) minus 70 percent of residential

investment spending (from the BEA). (Source: L. Josh Bivens, Economic Policy Institute)

US Macroeconomic data: Consumption and Mortgage Equity Withdrawals

Private sector imbalances:

• Private consumption expenditure sustained by freely available low cost

capital, tax cuts, real estate asset bubble/boom, credit card debt

• World’s largest ponzi scheme ever operating between US consumers and

PRC

• US private savings rate also very low/even negative over past decade

Immediate credit crisis result of many factors accumulating over last decade

or so:

• Securitization of financial instruments/misalignment of incentives

• Poor financial market oversight/regulation

• Political desire to increase home ownership through Freddie Mae/Mac

• Expansionary US fiscal and monetary policy

• Real estate asset bubble that developed over 00s

All led to Borrow and Spend

Structural Effects of Crisis: Globally

Geo Politically

• Age of American driven global economy ending; 300 million cannot drive 6.8 billion:

new global consumer(s) of last resort needed, but consumption patterns will differ

(emerging consumers ≠ rich uncle)

• America moves from last super power left standing to first among equals, emerging

countries (BRICs) power > as economies strengthen

Macro-economically

• Re-regulation of financial markets likely

• Consumer growth mostly in emerging economies

US adjustments needed:

• < 5 - 10 % in US Consumption as % of GDP

• > in US Savings to 5 - 10% of GDP

• > in US taxes 3 - 5 of GDP %

• < 20% in average US body weight

i.e. we all must save more, consume less, adjust consumption expectations,

de-lever

Note: 2009 QIII Personal Consumption Expenditure was estimated to be just

over 71% of GDP; GDP in 2009 < by more than 3 percent

Year Growth Rate

2009 -3.2

2008 0.43

2007 2.13

2006 2.65

2005 3.08

2004 3.58

2003 1.83

U.S. Bureau of Economic Analysis

2009 estimate until Sept.

Average Real GDP Growth

Year

US$ billions

(2005 base year)

2009 1,453.0

2008 1,989.4

2007 2,146.2

2006 2,230.4

2005 2,172.2

2004 2,058.2

2003 1,871.6

U.S. Bureau of Economic Analysis

2009 2nd Quarter estimate

Gross Private Domestic Fixed Investment

Future US Scenarios:

Party On, Dude

To

Tighten Belts

Party On, Dude

• Bailouts continue/budget deficits grow, pandering rather than pain: no pay as

you go imposed

• Government borrowing increases, private investment/GDFI crowded out,

welfare grows - corporate and consumer

• Protectionist impulses lead to closing of American economy to buffer against

foreign competition/protect US jobs

• World eventually becomes nervous of US$/Economy, dumps US$, status of

world reserve currency lost to Euro or Rmb

• US descends into second class status, paying off today’s debt through

inflation, debasing currency into Mickey Mouse money

• This is worst case scenario, unlikely but possible

• If we don’t discipline ourselves the market will eventually discipline us…the

US could be Greece in five year’s time

Tighten Belts: Take the Pain, Adjust, Emerge..

• After stabilization, tightening occurs: interest rates rise to encourage

savings/counter inflation, budget deficit stabilizes, federal govt. > discipline

• Short to near term economic growth declines/moderates, jobs lost, Americans

reduce consumption, increase savings to de-lever balance sheets, increase

savings/cushions

• Adjustments will probably be required at the Federal, State, and Local levels

• After initial adjustment US economy resumes growth based on ongoing

productivity gains, clean tech/high tech/innovation, local and export led growth

• China, Brazil, India, others become locomotives of global growth, lasting well

into the 21st Century, consumption model evolves

• US evolves from last Superpower to First Among Equals

Likely macro trends over the next two generations:

• Curbing Climate Change/Global Warming > energy, transport costs; boom in

clean energy, production techniques, products and sevices

• Consumption models change in face of > commodity prices, > energy costs, >

transport costs, need for cleaner, more re-cyclable products

• US consumption levels < relatively as emerging markets >; US becomes global

market seeker, not supply seeker

• Global inequality diminishes, but does not disappear; but in 2050 US PPP per

capita still exceeds those of most residents in emerging world, and remember, not

a zero sum game!!!

For the sake of children/grand children US must deal with its current

economic imbalances (short term), as well as with Global

Warming/Climate Change (long term)

Country is currently mortgaging descendants futures, economically

and environmentally…

BIG TIME

But don‘t go from irrational exuberance to irrational depression

It is a question of balance...

Whether US declines or revitalizes depends upon political

choices/leadership, and willingness of all to confront reality and adjust

accordingly

And remember end of world not nigh, it could be far worse…

You could be an Icelander, or in Ireland, Mexico, or Zimbabwe

US economy still envy of the world, flexible, innovative, open for

business, productive

While recovering from party/hangover, all in US must work to keep it that

way!!!!