Embed Size (px)

Citation preview

BERENBERG EQUITY RESEARCH

Global Technology

Nemesis: a source of harm or ruin?

Adnaan Ahmad

Analyst

+44 20 3207 7851

Jean Beaubois

Specialist Sales

+44 20 3207 7835

21 May 2013

Technology Hardware

Daud Khan

Analyst

+44 20 3465 2638

daud.khan @berenberg.com

Ali Khwaja

Analyst

+44 20 3207 7852

Tammy Qiu

Analyst

+44 20 3465 2673

Sebastian Grabert

Analyst

+44 20 3207 7834

For our disclosures in respect of section 34b of the German Securities Trading Act (Wertpapierhandelsgesetz – WpHG) and our disclaimer please see the end of this document. Please note that the use of this research report is subject to the conditions and restrictions set forth in the disclosures and the disclaimer at the end of this document.

3

Table of contents

Nemesis: a source of harm or ruin? 4

ARM has more legs 16

What is working 19

ARM 19

Infineon 20

Samsung Electronics 21

Apple 22

Qualcomm 23

Imagination 24

HTC 25

Foxconn International 26

Hon Hai 27

Juniper 28

Motorola Solutions 29

Foxconn Technology 30

What is not working 31

Ericsson 31

STMicro 32

BlackBerry 33

Nokia 34

Alcatel-Lucent 35

ZTE 36

TPK 37

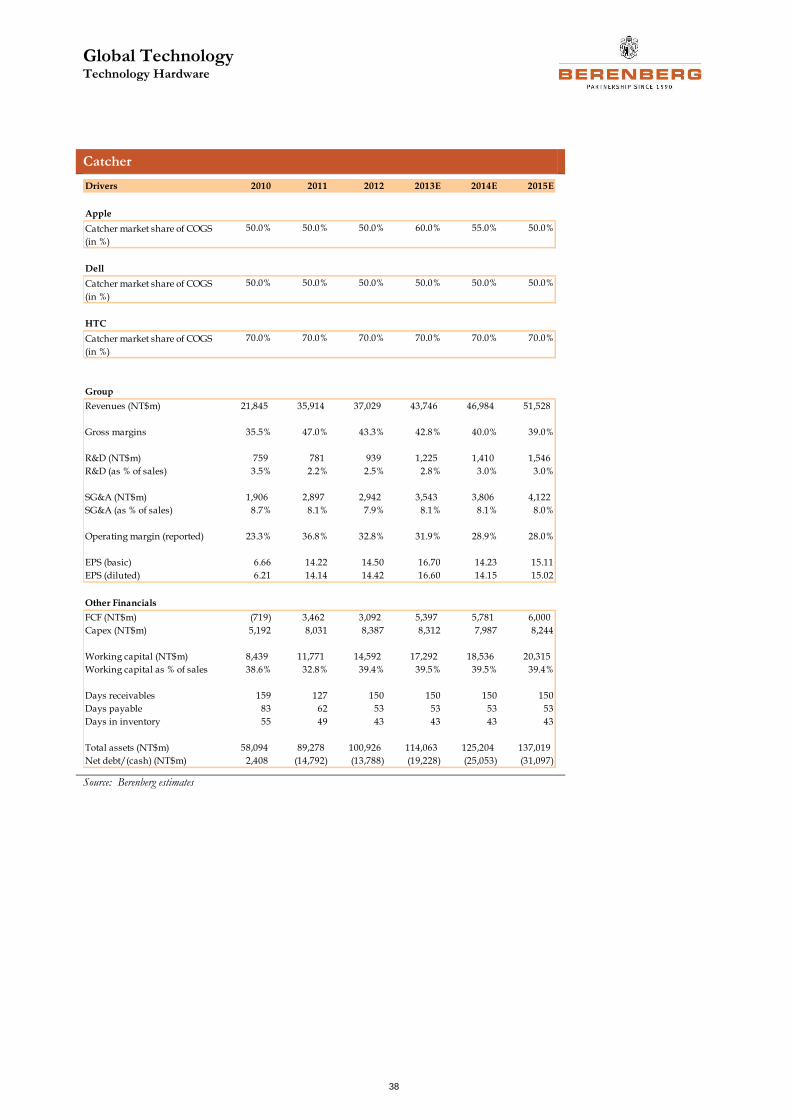

Catcher 38

MediaTek 39

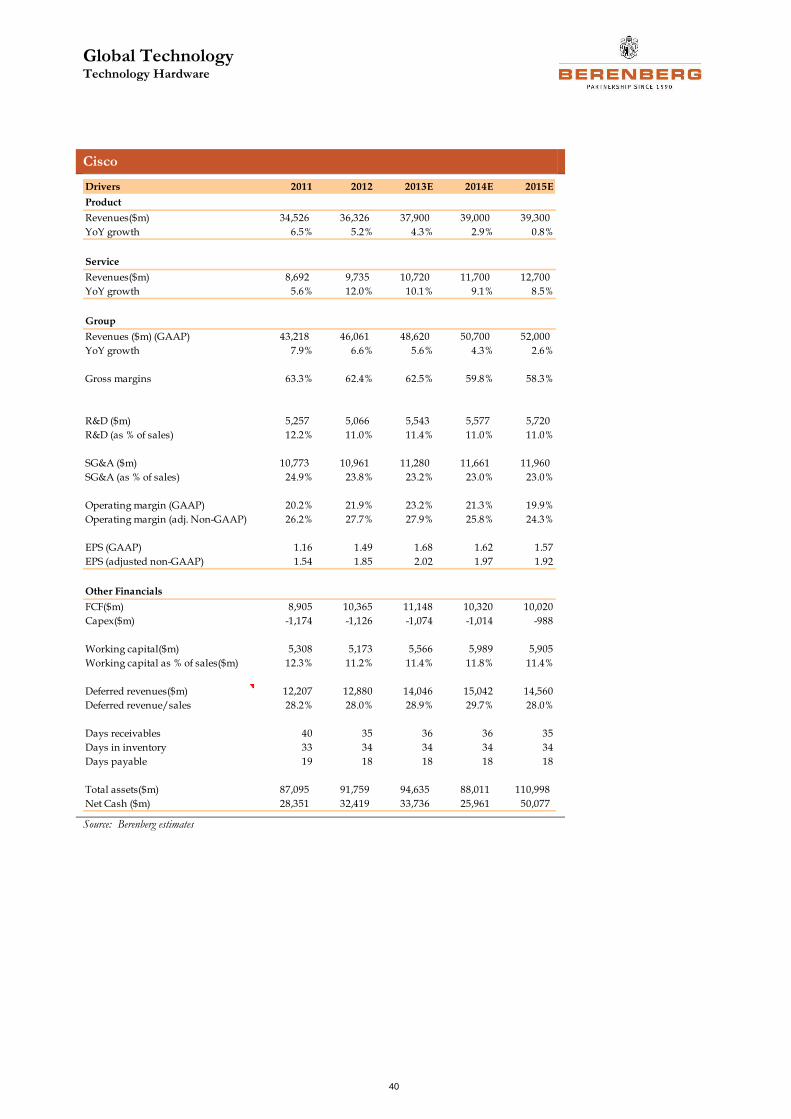

Cisco 40

Price targets and valuation 41

Disclosures in respect of section 34b of the German Securities Trading Act (Wertpapierhandelsgesetz – WpHG) 42

Contacts: Investment Banking 48

Global Technology Technology Hardware

4

Nemesis: a source of harm or ruin?

Since we initiated on the sector in January 2010, we have talked about the battle between the Apple and Google (Android) ecosystems in the post-PC era. To date, this battle has primarily been along classical tech hardware business and financial models: come out with a good device and sell it at as high an ASP as possible to try to be profitable. Amazon disturbed this business model somewhat with its Kindle Fire launch in late 2011 and Google (with its Nexus line) has used a similar strategy on occasions. However, we see the next 12 to 18 months as a potential watershed for the classical hardware profits business model as Google, Amazon and potentially Microsoft and others introduce smartphones and tablets with a “hardware at cost or a loss” strategy.

The issue here, in our view, is that if any of these “platform vendors” are successful with large consumer uptake, which admittedly has not been the case to date, then this will put a major strain on the margin dynamics of the hardware industry. We think Google’s “X” project (new smartphones and potentially tablets), coupled with the possibility of an Amazon smartphone, should be “front and centre” in investors’ minds when thinking about hardware industry margin structure in the mid-term, as these platform vendors can leverage their existing advertising, content and e-commerce financing models to offer high-end smartphone quality at up to 50% cheaper than equivalent devices from Apple, Samsung and the traditional hardware industry. Good for consumers, but also positive for telcos as they will be able to substantially lower their current subsidy levels on high-end devices.

We remain convinced that competition among traditional vendors, feature creep, the shift to lower-priced devices, slower industry growth and the potential of new platform players as described in this note will put pressure on smartphone industry margins. We keep our bearish structural views on Apple, Samsung, HTC, Nokia, BlackBerry and ZTE.

We also keep our negative stance on the infrastructure and networking segment. Yes, it has been the wrong call in the last six months; and yes, 2013 may be a positive spending cycle primarily driven by the US and Europe. But the cycle, in our opinion, will be overpowered at some point in the next 12 months by the structural headwinds that face these industries. Ericsson, ZTE, Huawei, NSN, Alcatel-Lucent, Samsung and now potentially vendors such as Cisco will hit the space from a small cell/WiFi angle. This, coupled with telecoms companies’ continued contradictory spending behaviour, should lead to further industry restructuring, exits and consolidation, in our view. Capacity needs to come out of the industry, we believe.

Rating system: Absolute

21 May 2013

Adnaan Ahmad Analyst +44 20 3207 7851 [email protected]

Jean Beaubois Specialist Sales +44 20 3207 7835 [email protected]

ARM Holdings plc BuyClosing price: GBP 10.96 PT: GBP 13.50

(Old: GBP 11.50)

20/05/2013 London

Infineon Technologies AG HoldClosing price: EUR 6.46 PT: EUR 6.00

20/05/2013 XETRA

Cisco Systems Inc SellClosing price: USD 24.24 PT: USD 16.00

(Old: USD 14.00)17/05/2013 NASDAQ

Ericsson SellClosing price: SEK 79.40 PT: SEK 60.0020/05/2013 Stockholm

TPK Holding Co Ltd SellClosing price: TWD 597.00 PT: TWD 400.0020/05/2013 Taiwan

Qualcomm Inc SellClosing price: USD 66.61 PT: USD 50.00

17/05/2013 NASDAQ

Samsung Electronics Co Ltd SellClosing price: KRW 1,497,000 PT: KRW 1,250,000

20/05/2013 Korea Stock Exchange

Apple Inc SellClosing price: USD 433.26 PT: USD 360.00

17/05/2013 NASDAQ

STMicroelectronics NV SellClosing price: EUR 7.52 PT: EUR 4.00

20/05/2013 Paris

Juniper Networks Inc SellClosing price: USD 17.61 PT: USD 14.00

17/05/2013 New York

Alcatel-Lucent SellClosing price: EUR 1.23 PT: EUR 0.70

20/05/2013 Paris

ZTE Corp SellClosing price: HKD 13.34 PT: HKD 8.50

20/05/2013 Hong Kong

MediaTek Inc SellClosing price: TWD 378.50 PT: TWD 210.00

20/05/2013 Taiwan

Imagination Technologies Group SellClosing price: GBp 337 PT: GBp 250

(Old: GBp 360)

20/05/2013 London

Catcher Technology Co Ltd SellClosing price: TWD 162.00 PT: TWD 115.00

20/05/2013 Taiwan

Foxconn Technology Co Ltd SellClosing price: TWD 80.40 PT: TWD 70.00

20/05/2013 Taiwan

Motorola Solutions Inc SellClosing price: USD 57.84 PT: USD 40.00

17/05/2013 NASDAQ

BlackBerry SellClosing price: USD 14.62 PT: USD 5.00

17/05/2013 NASDAQ

Hon Hai Precision Ind Co Ltd SellClosing price: TWD 77.10 PT: TWD 66.00

20/05/2013 Taiwan

Foxconn International Holdings SellClosing price: HKD 3.22 PT: HKD 2.50

20/05/2013 Hong Kong

Nokia Oyj SellClosing price: EUR 2.93 PT: EUR 1.50

20/05/2013 Helsinki

HTC Corporation SellClosing price: TWD 292.00 PT: TWD 150.00

20/05/2013 Taiwan

Global Technology Technology Hardware

5

ARM Holdings therefore remains our only Buy-rated stock. Royalty rate inflation and end-market diversification remain the core tenets to our thesis here, and we raise our price target to £13.50.

In this note, we discuss the potential for platform players to turn the hardware business model on its head by using “hardware at cost or a loss” strategies aggressively to gain share in smartphones and tablets. Platform players continue to face challenges – such as distribution, core expertise and product innovation cycles – but we think it is important to highlight the threat of such strategies, especially to the smartphone industry and its margin structure given the upcoming launch of Google “X” products in the next six to 12 months.

Finally, given our negative stance on all but one stock in our coverage universe on an absolute basis, we continue to highlight certain pair trades (see table below) and note that to date they have performed well. In this report we also assess, as always, what is working and what is not from a stock perspective. Our detailed updated models for each company are available on request.

Pair trades return between inception and 16/05/2013

Pair trades-return between inception and 16/05/2013

Long Short Return

QCOM MTK -11.1%

IFX STM -16.7%

ERIC ZTE -5.7%

Samsung HTC -8.9%

ARM IMG 45.8%

TPK FIH -2.5%

AAPL Samsung 3.5%

Nokia HTC 0.4%

CSCO ALU 6.1%

ERIC JNPR 10.2%

Source: Bloomberg data

Global Technology Technology Hardware

6

Berenberg versus consensus estimates

Source: Berenberg estimates, Bloomberg for consensus

Change in EPS estimates

Source: Berenberg estimates, Company data

Companies Berenberg Est. Consensus Delta Berenberg Est. Consensus Delta

Nokia -0.01 0.00 -348% 0.08 0.11 -20%

Ericsson 4.84 4.84 0% 5.26 5.87 -10%

Alcatel Lucent -0.26 -0.14 -86% -0.03 0.02 -227%

Apple 40.93 39.75 3% 39.79 44.03 -10%

BlackBerry* -0.35 0.37 -195% -0.61 0.02 -3884%

Infineon 0.23 0.21 8% 0.31 0.38 -19%

STMicro -0.02 0.06 -136% 0.29 0.41 -29%

ARM 0.22 0.20 12% 0.29 0.25 15%

HTC 8.86 14.61 -39% 11.79 19.67 -40%

ZTE -0.20 0.58 -134% -0.13 0.73 -117%

Motorola Solution 3.50 3.62 -3% 3.71 4.19 -11%

Cisco 2.02 2.01 0% 1.97 2.12 -7%

Juniper 1.06 1.14 -6% 1.07 1.29 -17%

Qualcomm 4.39 4.54 -3% 4.65 4.90 -5%

Mediatek 16.71 18.17 -8% 17.00 23.27 -27%

Catcher 16.70 16.11 4% 14.23 15.85 -10%

Hon Hai 7.32 8.08 -9% 6.91 9.04 -24%

TPK Holdings 52.70 52.07 1% 52.10 56.87 -8%

Foxconn Technology 6.58 7.06 -7% 6.74 7.47 -10%

Foxconn International Holding -0.01 0.00 -123% -0.01 0.02 -185%

Imagination 8.32 9.90 -16% 8.87 13.80 -36%

Samsung Electronics 234,787 212,535 10% 203,535 238,006 -14%

* for FY 2014 and 2015

2013 EPS 2014 EPS

NEW OLD NEW OLD

1 ARM Holdings (GB£) 0.22 0.22 0.29 0.27

2 Qualcomm (US$) 4.39 4.33 4.65 4.73

3 Apple (US$) 40.93 42.28 39.79 44.98

4 Alcatel Lucent (€) -0.26 -0.09 -0.03 0.03

5 ZTE (HK$) -0.20 -0.24 -0.13 -0.59

6 Ericsson (SEK) 4.84 4.65 5.26 4.98

7 Infineon (€) 0.23 0.17 0.31 0.35

8 HTC (NT$) 8.86 8.86 11.79 7.88

9 Motorola Solutions(US$) 3.50 3.62 3.71 3.98

10 Juniper (US$) 1.06 1.09 1.07 1.25

11 STMicro (€) -0.02 0.06 0.29 0.11

12 BlackBerry* (US$) -0.35 -0.66 -0.61 -0.59

13 Cisco (US$) 2.02 2.02 1.97 2.07

14 Mediatek (NT$) 16.71 11.91 17.00 11.62

15 Nokia (€) -0.01 0.01 0.08 0.05

16 Catcher (NT$) 16.70 13.17 14.23 13.31

17 Hon Hai (NT$) 7.32 8.13 6.91 6.56

18 TPK Holdings (NT$) 52.70 50.69 52.10 52.10

19 Foxconn Technology (NT$) 6.58 6.76 6.74 6.87

20 Foxconn International Holding (US$) -0.01 -0.01 -0.01 -0.01

21 Imagination (GBP) 8.32 12.47 8.87 15.03

22 Samsung (KRW) 234,787 199,442 203,535 187,517

* for FY 2014 and 2015

2013 EPS 2014 EPS

Global Technology Technology Hardware

7

Stock selection: order of preference

*All prices as of COB 16 May on the relevant home exchange Source: Berenberg estimates, Company data

1 ARM Holdings (£) Buy To 13.5 11.0 23% 55.1 Royalty rate to increase given Cortex platform mix

Smartphone/tablet volumes drive PD royalties

1.1 From 11.5 Expansion into Networking and Server markets

1.2 Intel becomes irrelevant

2 Infineon (€) Hold 6.0 6.4 -7% 30.9 Pure macro play dependent on Eurozone situation

2.1 Quality end market exposure with secular growth

2.2 Qimonda overhang persists

3 Cisco ($) Sell To 16.0 23.9 -33% 11.9 Gross margins to come under mid-term pressure given

mix and price competition

3.1 From 14.0 Huawei now has 20k Enterprise employees - focus on

emerging markets and Europe initially

3.24 Ericsson (SEK) Sell 60.0 81.4 -26% 16.8 Margin improvements baked into stock but at what

revenue growth?

4.1 LTE cycle could be cannibalised by WiFi investment

mid-term. Chinese vendors to get lion's share of China

4G deals4.25 TPK (TWD) Sell 400.0 610.0 -34% 11.7

5.1

6 Qualcomm ($) Sell 50.0 65.6 -24% 14.5 TAM for chips less than what analysts believe given

captive market (AAPL, Samsung and Huawei)

6.1 Mediatek aggressive at low-end

6.2 BRCM, NVDA, Intel et al fight-back for share

7 Samsung (KRW) Sell 1250000 1508000 -17% 7.1 Galaxy "S4" could go through iPhone 5 moment

7.1 Shift to mid- and low-end impacts margin structure

7.2 Phone business 60%+ of op profits - rest of business

cannot make up slack

8 Apple ($) Sell 360.0 434.6 -17% 10.9 iPhone at 60%+ of op profit facing growth and margin

pressure

8.1 iPad growth cannot make up for shortfall of iPhone

margin pressure

8.2 New areas: iWatch + iTV impacted by law of large

numbers

9 STMicro (€) Sell 4.0 7.2 -45% 116.5 MEMS technology could face comp pressure from

InvenSense

9.1 Spread in too many end markets with customers under

pressure (Nokia/HP) exposure

9.210 Juniper ($) Sell 14.0 17.8 -21% 15.7 Increased competition in Edge routing from mobile

## Need to invest in Enterprise impacting margin

structure

## Gross margins have downward bias on price and mix

11 Alcatel Lucent (€) Sell 0.7 1.2 -42% n/a

12 ZTE (HKD) Sell 8.5 13.6 -38% 23.6 Margin pressure in handset business from Chinese

OEMs such as Huawei## TD-LTE capex growth already in price

13 MediaTek (TWD) Sell 210.0 374.0 -44% 20.6 3G in China an opportunity but also a threat from

Qualcomm on price

## 2G competition tough: Spreadtrum, RDA both coming

out with smartphone products

##14 Imagination(£) Sell To 2.5 3.3 -24% 33.3 Move to dual and multi core GPUs positive for royalty

rate

## From 3.6 Apple position is stable for the foreseeable future

## Competition from Nvidia, QCOM, ARM, BRCM and

Vivante holds back major market share shift

15 Catcher (TWD) Sell 115.0 161.5 -29% 10.0 Potential MacBook share loss to Foxconn Tech

HTC, RIMM and Dell exposure a concern

## Not concerned in short term on light metal casing

##16 Foxconn Tech Sell 70.0 81.3 -14% 11.5 Apple casing opportunity is positive

## (TWD) But 60% of revenues from Nintendo

## Do not see games console market as structural grower

17 Motorola Solutions ($) Sell 40.0 57.5 -30% 15.9

##

##18 BBRY ($) Sell 5.0 14.7 -66% 39.6 Increase in competitive intensity in US market

## New BB10 platform not a game-changer

## Services revenues to come under attack

19 Hon Hai (NT$) Sell 66.0 78.7 -16% 9.7 45% of revenues from Apple and over 75% of Hon

Hai's growth from Apple

## Apple won't subsidise forever

## Apple concentration a double-edged sword

20 Foxconn Intl Sell 2.5 3.3 -24% n/a Headwinds for Nokia, Motorola and Sony

## (HKD) Nokia may outsource more assembly to Foxconn but

that is in price

##21 Nokia (€) Sell 1.5 2.9 -48% 970.0 NSN in harvest mode a positive

## Samsung + Android (China Inc) big threat to

## Nokia's mid-to-low-end emerging market position

22 HTC (TWD) Sell 150.0 290.0 -48% 19.8 "One" Series will only provide short-term relief

## Samsung, Apple into mid-range smartphones

HTC margins will be under pressure

## New markets at an investment cost; eg China

Buys - 16

Holds - 8

Sells - 6

Buys - 7

Holds - 3

Sells - 4

Buys - 19

Holds - 7

Sells - 21

Buys - 9

Holds - 9

Sells - 15

Buys - 8

Holds - 7

Sells - 5

Buys - 15

Holds - 9

Sells - 4

Buys - 2

Holds - 12

Sells - 8

Buys - 9

Holds - 11

Sells - 2

Government business to face challenges given catch-up

spend fall-off in next 12 months. Enterprise business

under pressure given retail capex concerns

Buys - 8

Holds - 12

Sells - 21

Buys - 8

Holds - 14

Sells - 2

Buys - 13

Holds - 21

Sells - 5

Buys - 7

Holds - 12

Sells - 10

IP business strong but competition intensifying

Cost savings will be given back in pricing

Buys - 13

Holds - 14

Sells - 7

Buys - 19

Holds - 5

Sells - 4

Buys - 51

Holds - 14

Sells - 3

P/E 2013E Consensus Investment thesis

Buys - 13

Holds - 11

Sells - 6

Buys - 18

Holds - 12

Sells - 6

Buys - 38

Holds - 9

Sells - 4

Buys - 22

Holds - 9

Sells - 5

Buys - 23

Holds - 4

Sells - 5

In-cell technology should replace glass on glass in mid-

term. Apple (55% of TPK revs) is likely to go down this

path in the next 18 months

Buys - 43

Holds - 4

Sells - 2

Buys - 49

Holds - 0

Sells - 2

% Implied

upside/

downside

Company Rating PT Price*

Global Technology Technology Hardware

8

Nemesis: a source of harm or ruin?

Nemesis: “A source of harm or ruin”; “an opponent that cannot be beaten or overcome”. The Free Dictionary.

First, since we initiated on the sector in January 2010, we have talked about the battle between the Apple and Google (Android) ecosystems in the post-PC era. To date, this battle has primarily been along classical tech hardware business and financial models: come out with a good device and sell it at as high an ASP as possible to try to be profitable. Amazon disturbed this business model somewhat with its Kindle Fire launch in late 2011 and Google (with its Nexus line) has used a similar strategy on occasions. However, we see the next 12 to 18 months as a potential watershed for the classical hardware profits (thin margins) business model as Google, Amazon and potentially Microsoft and others introduce smartphones and tablets with a “hardware at cost or a loss” strategy.

Historically, on occasions, hardware vendors have used their strong profitability with these products to “subsidise” services businesses. For example, Nokia had operating margins in the 20% range for its handset business and tried unsuccessfully to create ecosystems (Club Nokia/OVI); these proved to be loss-making. Even Apple’s Services businesses (App Store and iTunes) have only 5% margin structures. Samsung is trying to do that today by investing its “super-normal” margins in smartphones into software and services. On the other hand, Amazon initially made between a $30-50 loss on each Kindle Fire it sold (ie on the hardware) in Q4 2011, but its model was to make that money back – and then some – through subscription, services and content. Google made losses on some of its Nexus products, but that was to propel the wider Android market into an accelerated product introduction and development mode. And more recently, we think that Microsoft has been and will “subsidise” its “Surface” and “Surface Pro” efforts to push Windows 8 concepts into the mainstream. The issue here, in our view, is that if any of these “platform vendors” are successful with large consumer uptake, which admittedly has not been the case to date, then this will put a major strain on the margin dynamics of the hardware industry. We think Google’s “X” project (new smartphones and potentially tablets), coupled with the possibility of an Amazon smartphone, should be “front and centre” in investors’ minds when thinking about hardware industry margin structure.

Second, given that the bill of material on high-end smartphones (such as a Samsung Galaxy S4 or an iPhone5) is in the $250-300 range, if Google, for instance, prices its “X” device at near cost, then that will be 50% cheaper than the equivalent high-end device. This is obviously good news for the consumer, but also very good news for telcos as they will be able to substantially lower their current subsidy levels on high-end devices. In this scenario, Apple and Samsung could obviously stick to their existing pricing structure and hope that their brand and/or ecosystem will deflect consumers from churning, but the likely outcome, in our view, would be to lower their respective prices and, at the same time, beef up cost (marketing to offset operator advertising of the lower-priced Google “X” as well as

Global Technology Technology Hardware

9

accelerate new product development). This is the issue that confronts hardware-centric vendors – how do you compete against companies that (given their business models) can offer hardware for free? Nokia, LG Electronics, BlackBerry, Sony Mobile, HTC, China Inc and Japan Inc are all struggling to make decent profits/returns in the smartphone business. The same is true in the PC space for Dell, HP, Acer, Asus, Toshiba and Sony. And in the tablet (hybrid/convertible) segment, both groups are also at best operating on razor-thin margins. The exceptions are obviously Apple and Samsung, which between them account for more than 100% of smartphone and tablet industry profits today. At the same time, though, given their generous margins (we estimate that Apple makes ~30-35% operating margins in its iPhone business and Samsung just posted Q1 2013 margins of ~20% for its IM division, which houses its smartphones), they both have the most to lose.

PC and handset vendor margin structures in 2012

Source: Company data, Berenberg estimates

Third, the business and financial models of hardware companies and these platform companies are very different. Google’s business model is predicated on amassing advertising revenues based around its technological advantage in search, whereas Facebook’s is centred on leveraging its social network platform. Similarly, Amazon’s model is e-commerce revenues and razor-thin margins. Microsoft’s model is licensing Office and OS purchases of Windows by hardware OEMs. The important point here is that each of these vendors can leverage their “existing” profitable platforms into the hardware space. If we look at history, Microsoft was ploughing investment into its Xbox hardware and this division was losing money hand over fist between 2005 and 2008, with -20% to -30% operating margins. But

Gross Margin Operating Margin

Nokia (Devices & Services) 21.3% -4.5%

LG Electronics (Mobile) n/a 0.2%

BlackBerry (Hardware) 1.0% -8.0%

HTC 26.0% 7.0%

ZTE (Handset Business) 16.8% 5.0%

Sony (Mobile & Products) n/a -7.9%

TCL Communications 17.4% 0.0%

Toshiba (Electronics Division) n/a 6.8%

Dell (PC ) n/a 3.2%

HP (Consumer & Products) n/a 4.7%

Acer 10.1% 0.2%

Asus 13.6% 4.9%

Global Technology Technology Hardware

10

Microsoft, with its deep pockets, persisted – which will be the case again in tablet and potentially smartphone hardware, in our view. In addition, Amazon selling a Kindle Fire at cost or at low single-digit margins is: a) around the corporate average margin structure; and b) a way to incentivise the hardware user to buy more products digitally from Amazon. In other words, these platform vendors want to drive software, services, content and subscription sales. Hardware vendors do not have that luxury. Even Apple, with ~8-10% of revenues from digital content (App Store and iTunes) will need to change tack if these platform vendors are successful with their “hardware at cost or a loss” strategies. A final interesting anecdote is that Motorola Mobility currently has negative margins; hence potentially selling new Google-inspired hardware at near-cost could actually be a positive boost to overall group margin structure!

Platform players have deep pockets to pursue “hardware at cost/a loss” strategy

Source: Company data 2012

Fourth, the platform we worry about the most is Google. According to an article in the Wall Street Journal (21 December 2012), Google’s CEO, Larry Page, has told the Motorola team to “think big” and aspire to reach the scale of Samsung’s mobile business; and promised a significant marketing budget for the unit. In the past 18 months, the Motorola products that have been launched have all been Motorola-inspired. In the next six to 12 months, we think hardware products that come out of Motorola will be Google-designed and a branded Google experience.

Commentary from Google’s earnings call in April also points to some new products. Page said: “In today’s multi-screen world, the opportunities are endless. Think about your device. Battery life is a challenge for most people. You shouldn’t need to carry around a charger with you to make it through the day. If your kids spill their drink on your tablet, the screen shouldn’t die. And when you drop your phone, it shouldn’t shatter. There is real potential to invent new and better experiences, ones that are much faster and more intuitive. So having just seen some of those upcoming products myself, I’m really excited about the potential there.” We think that these remarks

Platform Players have deep pockets to pursue "hardware at a cost/loss" strategy

Amazon Google Microsoft Facebook

($)m

Revenue 61,093 50,175 73,723 5,089

Gross Margin 25% 59% 76% 73%

EBIT 676 12,760 28,496 538

SG&A 9,723 9,988 21,426 1,788

R&D 4,564 6,793 9,811 1,399

FCF 395 13,346 29,321 377

Net Cash 7,063 44,020 51,096 7,270

Source: Company Data

Global Technology Technology Hardware

11

pertain to the much-discussed Google “X” product series, which we think could launch in H2 2013.

We also think that the origins of Google’s more aggressive hardware approach and an intention of its acquisition of Motorola Mobility could have been to replicate the “forking” strategy Amazon used with Android. In a nutshell, when Amazon launched the Kindle Fire in H2 2011, it “ostracised” Google. The problem for Google was that the Kindle Fire did not – and still does not – come installed with Google Play. It uses its own browser “Amazon Silk” and the “Amazon App Store”, through which Kindle Fire users can also access apps; ie it is Amazon that is driving the user experience. Obviously, we do not know the nature of the deal between Google and Amazon, but we note that Google monetises Android through the following methods: a) channelling mobile users to use its search engine. Google Search is the default search system on the Android OS, which leads directly to greater revenues from search-based ads; b) taking a transaction fee of up to 30% for each app sold through its Google Play; c) displaying in-app advertising through AdMob; and d) Google is also working on initiating location-based advertising in Android smartphones. It recently launched Google Wallet for mobile payments and would gain by either charging transaction fees or for ads. Obviously, with Amazon in the “hot seat”, we believe only option a) is currently certain for Google from Kindle Fire users. We note that Amazon’s business model is to get Kindle Fire users to subscribe to its “Prime” service at $79/year, which gives US, European and Japanese users the ability to tap into thousands of videos and unlimited fast shipping. In the US, “Prime” users tend to spend up to 2x more with Amazon than the average Amazon user; hence the company wants to “digitise” and grow this “Prime” user base over time. In conclusion, we think the Amazon “Android work-around” opened a “crack” in the ecosystem and Google decided to hedge its current horizontal model versus the Amazon Android model if: a) Amazon were successful; and b) others were to move to an Amazon-like model.

There are some interesting ramifications for the industry if Google launches such a product with a big distributor and telco push.

a) A top-of-the-range smartphone, Google “X”, at $300-400 versus the $600 level of the iPhone5 and Samsung Galaxy S4. Telcos, we think, will push this product given the potential for lower subsidies as Google leverages its “platform” and “hardware at cost or a loss” strategy.

b) Could this split or “fork” Android? HTC, LG Electronics, Sony Mobile and Samsung would obviously be the initial casualties if the Google “X” gains consumer momentum. LG Electronics has recently talked about a turnaround in its smartphone business; Sony expects its smartphone division to be profitable by year-end March 2014. HTC has its future riding on the “ONE” phone and Samsung has nearly 50% market share in the Android ecosystem. We think that ZTE, Huawei and China Inc will be less affected as they compete primarily in the low-priced smartphone segment and Google obviously has “brand” issues in China.

Global Technology Technology Hardware

12

c) Samsung would clearly be a major casualty given the business model difference as well as its high-end smartphone market share. Samsung is obviously in an interesting situation as it commands 50%+ share of Android smartphones and hence Google does need Samsung to continue to succeed in the short term. Interestingly, though, Samsung has upped the ante on software and services initiatives as well as publicly talking up its “hedged” OS strategy: Tizen and Microsoft. However, both of these are essentially starting from scratch, and if Samsung tries to “fork” Android like Amazon, how will it gain critical mass in content, services and subscription? Ultimately, Samsung is a very good hardware company; shifting to become a “platform” company will be extremely difficult – look what happened to Nokia with its OVI venture. Another point here is that Google is ultimately the key-holder to Android: Samsung has absolutely no control of the evolution of the platform (and hence its attractiveness to developers) and Google Play (and hence its attractiveness to end-customers).

Smartphone market share development by operating system

Source: IDC

2008 2009 2010 2011 2012

Android 0.5% 4.0% 23.3% 49.2% 68.8%

iOS 9.1% 14.5% 15.6% 18.8% 18.8%

Blackberry OS 15.6% 19.9% 16.0% 10.3% 4.5%

Symbian 48.4% 44.9% 36.4% 16.5% 3.3%

Windows Mobile 13.0% 9.3% 4.9% 1.8% 2.5%

Other 13.4% 7.4% 3.8% 3.6% 2.1%

Global Technology Technology Hardware

13

Tablet market share by operating system

Source: Gartner

Fifth is Amazon’s strategy. “We want to make money when people use our devices, not when they buy our devices,” Jeff Bezos, CEO of Amazon, said. The Kindle Fire is Amazon’s first step into the hardware world, in our view. We think that over the next 12 to 24 months, it is likely that Amazon will launch a smartphone, allowing it to leverage its platform and “hardware at cost or a loss” strategy further. As stated above, Amazon has its own “flavour” of Android and its own App store; and it is working on building an ad network through the applications it distributes. The bottom line: it is all about selling as much digital content and Amazon merchandise as possible. It has created cloud and streaming-based services for films, music and video, which it offers to customers with cloud storage and potential shopping and/or shipping discounts. We think that the key differentiator with Amazon is that it sells virtually everything, and mostly at very competitive prices. The potential for an Amazon-based smartphone has been discussed for a while but there are some pointers to suggest that it is real – smartphone screen sizes are increasing, which benefits the Amazon shopping experience. Amazon has recently hired Microsoft phone teams, the leader of which stated: “I’m building a new team going after a totally new area for Amazon. I’m hiring cloud and mobile developers and testers, program managers, and product managers.” Amazon has also acquired Liquavista (a display technology company) and a natural voice search company (think SIRI on Apple). We also know that it has been trying to gain access to wireless patents to potentially protect itself against any hostile onslaught.

Sixth, Microsoft is obviously the elephant in the room. It is very late to the game versus its platform peers, but it has shown before in the game console business that it has deep pockets and is willing to go through near-term pain for a position on the podium. Microsoft’s dabbling in hardware has been an unmitigated disaster, in our view, with the exception of the Xbox in the last few years. The “Kin”, “Slate” and “Zune” come to mind, and the “Surface” will probably go down a similar path. The more immediate issue with the “Surface” is how it “alienated” Microsoft’s historical hardware OEM partners (such as HP, Dell, Lenovo, Acer and Asus). In this instance, the “hardware at cost or a loss” strategy failed to take any volume share away

2010 2011 2012

Android 15.9% 30.7% 42.9%

iOS 83.7% 65.3% 55.8%

RIM 0.0% 0.2% 0.3%

Windows 0.0% 0.0% 0.9%

Others 0.4% 3.8% 0.0%

Global Technology Technology Hardware

14

from the traditional hardware community. The question now is does Microsoft follow a similar hardware strategy and come out with a “Surface smartphone”? We do not think that it is on the cards in the next 12 months, given: a) Microsoft needs hardware friends to garner volume and an ecosystem for Windows 8 and Windows Phone 8; b) Windows 8 is still in its infancy and there are already many user complaints on changing the OS or making it easier and less confusing; hence we think that this shift to “Windows Blue” is a priority in the near term; and c) Microsoft recently stipulated that it was not interested in building its own smartphone.

Seventh, there have been many statements about Facebook coming out with its own hardware and leveraging its social network platform and user base. We do not think that this is likely in the next 12 to 18 months given that the company needs to achieve increased usage on as wide a hardware base as possible rather than having two to three Facebook-branded smartphones. It has relationships with Apple, Microsoft, Google and BlackBerry, as well as with lower-end phones, such as Nokia’s Asha series. The mobile business is critical to Facebook’s future and its current valuation, as can be shown by the push to get “Home” on Android-based devices. Unfortunately, this initiative has not taken off and neither did Facebook’s button on HTC “Salsa” and “Cha Cha” phones in 2012.

Eighth is the position of other possible platform players. BlackBerry is obviously a niche platform currently with its own hardware, software, services and applications. As we have stated since our 2010 initiation, we just do not see how BlackBerry survives in the mid-to-long term. Similarly, Sony has hardware (smartphones, tablets, PCs, TVs), it uses Android but can “fork” it like Amazon, and it has a vast content library of music, gaming and films to leverage. The problem here is that Sony just has not been successful and is late at integrating this portfolio of assets into a powerful platform. In China, there are a few companies to be aware of that have a platform or quasi-platform approach, all based on variants of Android. Xiaomi sells high-end handsets online at ~50% discounts to its peers as it strives to make the money back with Internet/messaging services and accessory sales. It shipped over 7m handsets in 2012. Baidu, China’s Internet search giant, also uses an Android variant (Baidu Cloud) and works with TCL and Changhong to sell smartphones at RMB1,000 ($150). Sina, Alibaba and Tencent have also experimented with platform and content partnerships with hardware OEMs in the last two years but to date have not released any of their own branded devices.

Ninth, if Google, for example, is successful with a smartphone product in the next 12 months, then one definite conclusion is that volumes in smartphones may be higher than investor expectations, as demand is brought forward on the back of lower price. This is obviously good for ARM and Qualcomm’s QTL licence business. The history of consumer electronics dictates that lower-priced devices do pull mid- and high-end prices down over time. In the near term, investors may be focused on the larger pie, but they should also start thinking about how this affects Apple and Samsung mid-term. A Google platform as a competitor is a very different animal to a “horizontal” Google business model, as it surely would depress industry and hence Apple and Samsung margin structures. This is

Global Technology Technology Hardware

15

already the case with the iPad in general and the iPad mini in particular, which Apple has stated has significantly lower than corporate average margins. As smartphones proliferate into the mid- and low-end in the next two to three years, there is a natural mix impact on margins, there is a feature creep impact (ie pack in more “bells and whistles” without the offsetting price uplift), and there is the competitive aspect – traditional competition from China Inc and Samsung, but also platform competition.

And finally, what are the potential pitfalls for the platform players? Well, telcos that have launched branded devices have historically failed to gain any real traction. Distribution, brand, new product innovation and scale have been challenges for the telco community. Distribution is obviously key for platform vendors. Microsoft’s “Surface” was only distributed initially via its own retail stores (a handful) and online. And distribution may only be tied to where the platform provider has sufficient content; ie Amazon does not offer “Prime” services and content in China. Securing telco and retail backing will be critical for any push in the smartphone segment. Low-priced devices could also only attract price-conscious consumers – hence the model to leverage content, services, subscription is only justified if the consumers actually go ahead and purchase these products!

ARM Holdings plc Technology Hardware

16

ARM has more legs

The key to ARM’s stock and valuation, in our view, is royalty revenue growth over the next three to five years. Obviously, this is a function of volume, chip ASP, royalty rate and market share. We have a very simple model looking at how 2012 royalty revenue was made up and where we think smartphone, tablet, networking, server etc. volumes will trend to 2016. Our conclusion is that consensus estimates of $950m in 2016 are 16-35% too low for Processor division (PD) royalty revenues; and hence even though the stock has more than doubled from its low in 2012 (£4.50), there is still further upside potential based on underlying fundamentals as well as the option value of a possible acquisition of ARM. We increase our price target to £13.50 based on our new forecasts, encapsulating 25-30% annual average PD royalty revenue growth 2013-16, with consequent operating margin leverage.

Outside of valuation and macro, we believe investors’ biggest concern with ARM is the potential threat from Intel, as Intel shrinks to 14nm node in the next two years and implements its 3D technology aggressively with a goal to markedly improve its performance per watt relative to the ARM ecosystem. This is also our biggest concern with the stock. The issue for Intel, though, is that it needs to be able to deliver a product that has: a) vastly superior technology; b) is very competitive on price; c) is able to break into the ARM ecosystem (ie smartphone and tablet industries are primarily based on ARM architecture); and last but not least d) attract the captive semi vendors to switch – Apple, Samsung and Huawei.

The problem for Intel is that: a) ARM is not standing still with its own technology innovation (for example, Big.Little processors); while b) ARM’s ecosystem partners, TSMC and Samsung, are also moving ahead with 3D/FinFet and 2x and 1x nm process technologies. In addition, if we look at the industry structure on the hardware OEM side, wireless chip vendors need to gain traction with Apple, Samsung or China Inc.

Apple is obviously using its own designers to differentiate its chip architecture and will also slowly – over a two-year process, we think – transition semiconductor foundry activities away from its arch rival, Samsung, to TSMC. We just do not see Apple then fully transitioning its process again to Intel. However, Apple could dual-source – but the problem here is that Intel’s manufacturing process and associated products (tools, masks etc.) are different to TSMC’s; hence migration of one product line to another would be costly to say the least.

The other problem facing Intel and fellow merchant wireless semi vendors is that Samsung will lose its major Foundry customer. Samsung has a few options: a) it can try to find another customer – but getting one as large as Apple is going to be very difficult, in our view; or b) Samsung can “internalise” more of its own wireless semis (ie currently Samsung’s high-end phones sport Samsung’s Exynos chip; in the future Samsung could push its own wireless semi solutions across the portfolio and even expand its portfolio to include modems and connectivity products). If this were to happen, then obviously the total addressable market for merchant wireless semi vendors would shrink further.

Buy Rating system

Current price

GBP 10.96

Absolute

Price target

GBP 13.50 20/05/2013 London Close Market cap GBP 15,125 m Reuters ARM.L Bloomberg ARM LN

Changes made in this note Rating Buy (no change) Price target GBP 13.50 (11.50) Chg 2013e 2014e 2015e

old Δ% old Δ% old Δ%

Sales 693263 2.9 818987 3.9 818987 3.9

EBIT 363614 0.5 447404 6.4 447404 6.4

EPS 22.24 0.5 27.33 6.0 34.43 4.4

Source: Berenberg estimates

Share data

Shares outstanding (m) 1,380 Enterprise value (GBP m) 14,518 Daily trading volume 4,490,310

Performance data

High 52 weeks (GBP) 11 Low 52 weeks (GBP) 5 Relative performance to SXXP SXXP 1 month 15.9 % 15.9 % 3 months 9.7 % 9.7 % 12 months 97.9 % 97.9 %

21 May 2013

Adnaan Ahmad Analyst +44 20 3207 7851 [email protected]

ARM Holdings plc Technology Hardware

17

China Inc mainly sources wireless semis from Qualcomm, MediaTek and Spreadtrum. Qualcomm’s margins have declined by 1,300bp in little over 18 months as Qualcomm tries to compete with MediaTek et al to grab China Inc (Huawei, ZTE, Lenovo and Chinese “white box” vendors) share with superior technology. The bottom line is that Intel’s product will have to have a “wow” factor for the captive vendors to want to make a switch, and even then price will still be a determining factor. In our models, we have Intel gaining 3% market share in smartphones and 10% in tablets primarily in the Windows ecosystem by 2016 and we think it will be extremely difficult for Intel to improve on this position without a major technological and price breakthrough. Our view remains that Intel should acquire Qualcomm’s QCT chip business to gain scale in this space and harvest its X86 platform. With the recent CEO change, however, we think it will be more of the same – namely tick-tock!

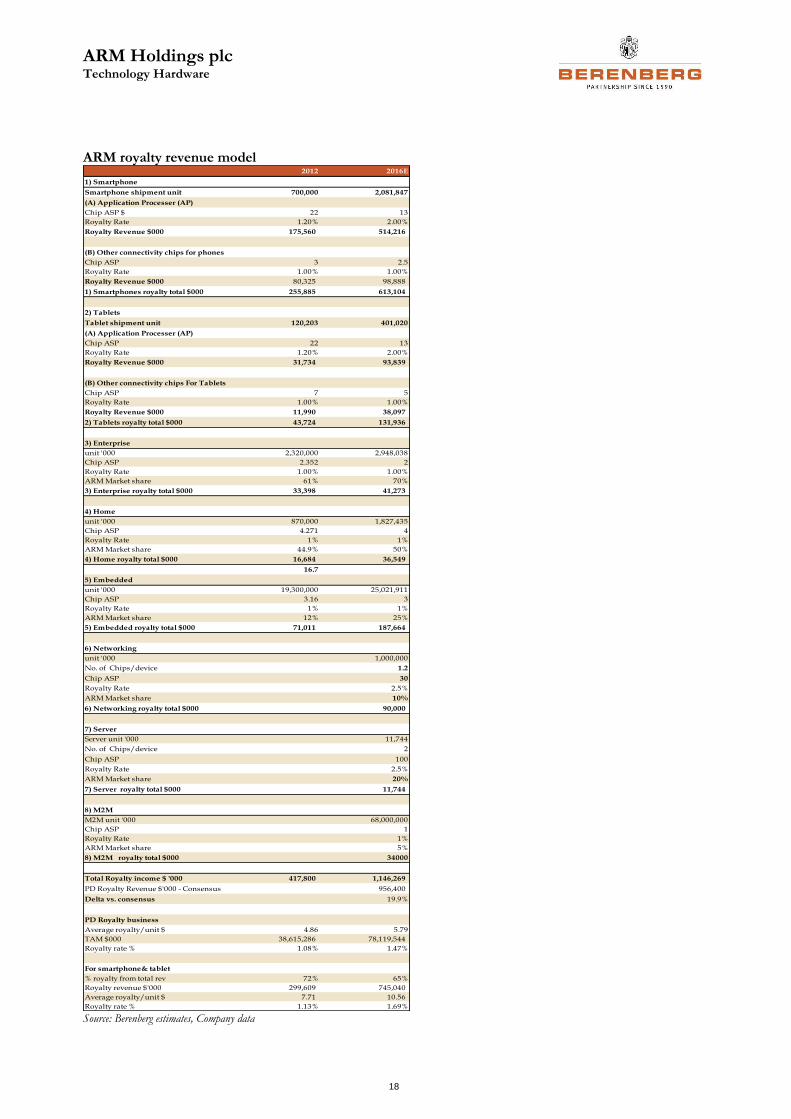

In our PD royalty model, we assume smartphone shipments increase from 700m in 2012 to nearly 2bn by 2016, with chip ASPs declining by 50% from $22 to $13. At the same time, ARM’s royalty rate should increase from 1.2% today for wireless to 2% as more Big.Little and v8 cores penetrate the base. Similarly, on tablets we assume a 120m-unit market in 2012 rising to 400m in 2016, with chip ASPs down to $13 from $22 today and royalty rates up to 2% from 1.2% today. Every 0.1% movement in ARM’s smartphone and tablet application processor royalty rate adds on $30m in PD royalties.

We also assume that ARM captures 25% of the embedded microcontroller market share by 2016 from 12% in 2012, as the market shifts to 32-bit processors away from 8-bit and 16-bit, and as proprietary solutions continue to be outsourced to ARM. For example, Renesas (leading global microcontroller vendor) has recently opened up a portion of its chip family to ARM. The volume in this market is sizable with over 20bn units shipped in 2012. The sensitivity here is that every 10% market share that ARM gains equates to $75m in PD royalties.

Similarly, we assume that ARM gains a 10% share in the networking segment by 2016 as its architecture gains sockets in data centres and infrastructure products. We think ARM can command a 2.5% royalty rate in this segment, with each chip having an ASP of around $30.

The biggest unknown in our model is the size of the machine-to-machine market. Third-party research suggests 68bn units will be shipped annually (Ericsson talked about 50bn+ in the 2015-20 timeframe). Assuming $1/chip and that ARM gets 5% market share and a 1% royalty, that is $35m in additional royalty revenue.

The bottom line is that we think ARM’s PD royalty revenue can hit between $1.1bn and $1.3bn in 2016 – 16% to 35% above the street. On the back of this, we think operating leverage is higher than the street is predicting – ARM already hit 50%+ margins in Q1 2013, and on our DCF (with an 8% WACC, 15-20% revenue growth for the next five years at the group level fading to 3% in 2022 and operating margins rising from the 50% level just posted to 65% on royalty revenue acceleration relative to licence revenues), we reach our new price target of £13.50.

ARM Holdings plc Technology Hardware

18

ARM royalty revenue model

Source: Berenberg estimates, Company data

2012 2016E

1) Smartphone

Smartphone shipment unit 700,000 2,081,847

(A) Application Processer (AP)

Chip ASP $ 22 13

Royalty Rate 1.20% 2.00%

Royalty Revenue $000 175,560 514,216

(B) Other connectivity chips for phones

Chip ASP 3 2.5

Royalty Rate 1.00% 1.00%

Royalty Revenue $000 80,325 98,888

1) Smartphones royalty total $000 255,885 613,104

2) Tablets

Tablet shipment unit 120,203 401,020

(A) Application Processer (AP)

Chip ASP 22 13

Royalty Rate 1.20% 2.00%

Royalty Revenue $000 31,734 93,839

(B) Other connectivity chips For Tablets

Chip ASP 7 5

Royalty Rate 1.00% 1.00%

Royalty Revenue $000 11,990 38,097

2) Tablets royalty total $000 43,724 131,936

3) Enterprise

unit '000 2,320,000 2,948,038

Chip ASP 2.352 2

Royalty Rate 1.00% 1.00%

ARM Market share 61% 70%

3) Enterprise royalty total $000 33,398 41,273

4) Home

unit '000 870,000 1,827,435

Chip ASP 4.271 4

Royalty Rate 1% 1%

ARM Market share 44.9% 50%

4) Home royalty total $000 16,684 36,549

16.7

5) Embedded

unit '000 19,300,000 25,021,911

Chip ASP 3.16 3

Royalty Rate 1% 1%

ARM Market share 12% 25%

5) Embedded royalty total $000 71,011 187,664

6) Networking

unit '000 1,000,000

No. of Chips/device 1.2

Chip ASP 30

Royalty Rate 2.5%

ARM Market share 10%

6) Networking royalty total $000 90,000

7) Server

Server unit '000 11,744

No. of Chips/device 2

Chip ASP 100

Royalty Rate 2.5%

ARM Market share 20%

7) Server royalty total $000 11,744

8) M2M

M2M unit '000 68,000,000

Chip ASP 1

Royalty Rate 1%

ARM Market share 5%

8) M2M royalty total $000 34000

Total Royalty income $ '000 417,800 1,146,269

PD Royalty Revenue $'000 - Consensus 956,400

Delta vs. consensus 19.9%

PD Royalty business

Average royalty/unit $ 4.86 5.79

TAM $000 38,615,286 78,119,544

Royalty rate % 1.08% 1.47%

For smartphone& tablet

% royalty from total rev 72% 65%

Royalty revenue $'000 299,609 745,040

Average royalty/unit $ 7.71 10.56

Royalty rate % 1.13% 1.69%

Source: Berenberg estimates,Company data

Global Technology Technology Hardware

19

What is working

ARM

Source: Berenberg estimates

Drivers 2010 2011 2012 2013E 2014E 2015E

PD (£ '000)

Licence revenues 107,613 149,300 181,100 216,129 241,935 266,129

Royalty revenues 188,065 222,200 264,300 360,229 466,452 592,465

PIPD (£ '000)

Licence revenues 26,645 31,200 33,000 34,839 36,774 37,419

Royalty revenues 28,323 30,200 35,400 40,000 43,226 45,806

Group

Revenues (£ '000) 407,290 491,826 576,800 713,132 850,968 1,006,335

Gross margins (IFRS) 94.0% 95.1% 94.8% 94.8% 95.5% 96.0%

Gross margins (ex. special items) 94.0% 95.1% 94.8% 94.8% 95.5% 96.0%

Gross margin (ex. special items ex. SBC) 93.5% 94.4% 94.5% 94.6% 95.3% 95.8%

R&D (ex. special items) 132,765 153,663 159,800 178,283 191,468 211,330

R&D (as % of sales) 32.6% 31.2% 27.7% 25.0% 22.5% 21.0%

SG&A (ex. special items) 125,330 146,481 167,700 178,283 191,468 211,330

SG&A (as % of sales) 30.8% 29.8% 29.1% 25.0% 22.5% 21.0%

Operating margin (IFRS) 26.3% 30.3% 36.1% 44.0% 49.8% 53.4%

Operating margin (ex. special items ex. SBC) 40.3% 45.1% 45.6% 51.3% 55.9% 58.6%

Operating margin (ex. special items) 26.3% 30.3% 36.1% 44.0% 49.8% 53.4%

EPS (IFRS) (pence) 6.39 8.66 11.53 18.66 25.28 32.27

EPS (ex. special items ex SBC) (pence) 9.45 12.45 14.72 22.35 28.98 35.96

EPS (ex. special items) (pence) 7.17 9.49 12.02 19.12 25.74 32.72

Other Financials

FCF (£ '000) 170,896 181,696 136,700 227,094 298,752 399,985

Capex (£ '000) 6,036 12,112 20,200 19,968 19,572 19,020

Working capital (£ '000) 31,098 11,235 (5,500) 7,260 9,387 11,715

Working capital as % of sales 7.6% 2.3% -1.0% 1.0% 1.1% 1.2%

DSO 94.7 88.8 78.8 79.0 79.0 79.0

DSI 25.0 32.5 26.4 26.0 26.0 26.0

DPO 60.3 114.2 67.7 68.0 68.0 68.0

Total assets (£ '000) 1,084,662 1,299,790 1,466,800 1,711,275 1,973,781 2,339,465

Net debt (£ '000) -275,101 -345,891 -386,300 -607,095 -836,747 -1,167,632

Source: Berenberg Bank estimates

Global Technology Technology Hardware

20

Infineon

Source: Berenberg estimates

Drivers 2010 2011 2012 2013E 2014E 2015E

Automotive

Revenues (€ m) 1,268 1,552 1,660 1,677 1,760 1,848

Operating margin (reported) 15.6% 18.0% 13.1% 9.0% 10.0% 13.0%

Industrial Power Control (IPC)

Revenues (€ m) - - 728 626 689 723

Operating margin (reported) 0.0% 0.0% 16.2% 1.5% 12.0% 14.0%

Power management & Multimarker (PMM)

Revenues (€ m) - - 929 957 1,033 1,085

Operating margin (reported) 0.0% 0.0% 15.3% 13.0% 15.0% 15.0%

Chip card and Security

Revenues (€ m) 407 428 457 443 465 489

Operating margin (reported) 5.4% 12.6% 12.3% 9.0% 10.0% 10.0%

Group

Revenues (€ m) 3,295 3,997 3,904 3,724 3,962 4,159

Gross margins (reported) 37.5% 41.4% 36.6% 33.0% 35.5% 36.0%

R&D (€ m) 399 399 455 484 515 541

R&D (as % of sales) 12.1% 10.0% 11.7% 13.0% 13.0% 13.0%

SG&A (€ m) 386 386 475 428 436 458

SG&A (as % of sales) 11.7% 9.7% 12.2% 11.5% 11.0% 11.0%

Operating margin (reported) 10.6% 18.4% 11.7% 7.4% 10.5% 11.0%

EPS (reported) (from continuing ops) 0.27 0.60 0.38 0.23 0.31 0.34

Other Financials

FCF (€ m) 650 407 (189) 122 479 490

Capex (€ m) 322 845 832 420 410 396

Working capital (€ m) 536 365 484 466 462 494

Working capital as % of sales 16.3% 9.1% 12.4% 12.5% 11.7% 11.9%

Days receivables 76 54 50 50 50 50

Days in inventory 91 79 84 84 84 84

Days payable 118 115 92 91 91 91

Total assets (€ m) 4,993 5,873 5,898 5,933 6,346 6,792

Net debt/(cash) (inc. pension liab) (€ m) (1,331) (2,387) (1,940) (2,026) (2,461) (2,907)

Source: Berenberg Bank estimates

Global Technology Technology Hardware

21

Samsung Electronics

Source: Berenberg estimates

Drivers 2010 2011 2012 2013E 2014E 2015E

Revenue(won bn)

Semiconductor 37,640 36,993 34,910 37,008 41,514 45,032

DP 29,912 29,232 33,245 33,851 34,123 36,057

IM 40,830 55,545 106,979 134,854 154,101 157,237

Digital media 57,613 59,004 48,727 46,800 49,563 52,299

Smartphones

Units in million 24 98 218 323 420 483

ASP($) 343 304 313 257 231 204

Operating Margin in %

Semiconductor 26.8% 17.0% 12.7% 18.0% 14.0% 13.0%

DP 6.7% -2.6% 9.7% 12.0% 10.0% 10.0%

IM 10.6% 14.9% 18.3% 20.0% 15.0% 12.5%

Digital media 0.8% 2.4% 5.0% 5.0% 4.0% 4.0%

Group

Group Revenues(won bn) 154,630 165,002 201,848 245,448 259,300 270,625

Gross margins 33.6% 32.0% 37.3% 39.2% 36.0% 34.0%

R&D (won bn) 9,099 9,980 11,539 14,236 14,780 14,884

R&D (as % of sales) 5.9% 6.0% 5.7% 5.8% 5.7% 5.5%

SG&A (won bn) 26,243 27,422 34,063 37,051 44,081 46,006

SG&A (as % of sales) 17.0% 16.6% 16.9% 16.7% 17.0% 17.0%

Operating margin 11.2% 9.8% 14.7% 16.3% 13.3% 11.5%

EPS 106,577 96,386 170,448 234,787 203,535 184,100

EPS - diluted 105,755 95,645 169,147 234,787 203,535 184,100

Other Financials

FCF(won bn) 2,206 150 14,994 27,358 22,008 20,864

Capex(won bn) -21,621 -21,963 -22,972 -21,400 -21,003 -20,568

Working capital (won bn) 23,369 9,989 15,491 25,747 27,975 29,137

Working capital as % of sales(won bn) 15.1% 6.1% 7.7% 10.5% 10.8% 10.8%

Days receivables 45 48 43 42 41 40

Days in inventory 48 51 51 51 51 51

Days payable 33 32 27 28 27 27

Total assets(won bn) 134,289 155,631 181,071 230,451 253,035 273,506

Net Cash (won bn) 9,643 9,037 17,914 42,871 62,112 80,472

Source: Berenberg Bank estimates

Global Technology Technology Hardware

22

Apple

Source: Company data, Berenberg estimates

Drivers 2010 2011 2012 2013E 2014E 2015E

Mac

Units ('000)

Desktops 4,627 4,669 4,656 2,891 4,200 4,250

Portables 9,035 12,066 13,502 9,613 11,762 11,234

ASP ($)

Desktops 1,340 1,379 1,297 1,206 1,146 1,089

Portables 1,248 1,272 1,272 1,226 1,202 1,189

Revenue ($m) 17,479 21,783 23,221 22,370 20,619 19,000

iPOD

Units 50,342 42,620 35,165 27,100 20,000 17,500

ASP ($) 164 175 160 166 158 142

Revenue ($m) 8,274 7,453 5,615 4,538 3,162 2,490

iPhone

Global Smartphone shipments (units m) 281 461 603 911 1200 1400

iPhone shipments (units m) 40 72 125 139 180 220

Apple's market share 14% 16% 21% 15% 15% 16%

ASP ($) 630 651 644 606 461 384

Revenue ($m) 25,179 45,998 78,692 85,154 83,232 84,527

iPhone gross margins 52.6% 52.8% 56.1% 45.0% 41.0% 36.0%

iPAD

Units 7,458 32,394 58,310 74,500 85,000 95,000

ASP ($) 665 628 556 454 432 410

Revenue ($m) 4,958 20,358 32,424 30,232 36,689 38,955

Group

Revenues ($bn) 65.2 108.2 156.5 168.1 166.7 169.7

Gross margins 39.4% 40.5% 43.9% 37.5% 35.0% 32.5%

R&D ($bn) 1.8 2.4 3.4 4.4 3.8 3.9

R&D (as % of sales) 2.7% 2.2% 2.2% 2.6% 2.3% 2.3%

SG&A ($bn) 5.5 7.6 10.0 11.1 10.8 11.0

SG&A (as % of sales) 8.5% 7.0% 6.4% 6.6% 6.5% 6.5%

Operating margin 28.2% 31.2% 35.3% 28.3% 26.2% 23.7%

EPS (non-GAAP) 16.41 29.79 47.86 40.93 39.79 38.82

Other financials

FCF ($m) 16,590 33,269 42,561 46,839 33,521 31,292

Capex ($m) 2,005 4,260 8,295 7,649 7,502 7,468

Working capital ($m) -5,454 -8,487 -9,454 -12,146 -12,765 -13,334

Working capital as % of sales -8.4% -7.8% -6.0% -7.2% -7.7% -7.9%

Days receivable 31 18 25 26 26 26

Days in inventory 10 4 3 3 3 3

Days payable 111 83 88 86 86 84

Total assets ($m) 75,183 116,371 176,064 232,268 234,860 237,323

Net debt ($m) -51,011 -81,570 -121,251 -156,824 -157,711 -158,368

Source:Company data, Berenberg Bank

Global Technology Technology Hardware

23

Qualcomm

Source: Company data, Berenberg estimates

Drivers 2010 2011 2012 2013E 2014E 2015E

Integrated Circuits

Unit shipped(m) 399 483 590 700 880 1,050

ASP($) 17 18 21 23 21 17

Revenue($m) 6,701 8,840 12,160 15,960 18,040 18,270

Technology Licensing

Handset Sales(m) 569 726 853 992 1,150 1,300

Handset ASP($) 186 207 220 220 202 190

Market size($m) 105,976 149,919 187,276 218,240 232,300 247,000

Blended royalty rate 3.5% 3.5% 3.5% 3.3% 3.2% 3.2%

Revenue($m) 3,709 5,247 6,555 7,202 7,434 7,781

Group

Revenues ($m) (GAAP) 10,981 14,958 19,121 23,782 26,124 26,701

Gross margins (GAAP) 71.0% 68.0% 64.5% 62.5% 61.0% 60.0%

R&D ($m) 2,143 2,585 3,363 4,043 4,493 4,619

R&D (as % of sales) 19.5% 17.3% 17.6% 17.0% 17.2% 17.3%

SG&A ($m) 1,262 1,511 1,860 2,117 2,351 2,403

SG&A (as % of sales) 11.5% 10.1% 9.7% 8.9% 9.0% 9.0%

Operating margin (GAAP) 29.9% 33.0% 29.7% 30.6% 29.4% 28.4%

Operating margin (adj. Non-GAAP) 40.0% 40.6% 37.1% 36.6% 34.8% 33.7%

EPS (GAAP) 1.96 2.56 3.20 3.80 4.05 4.05

EPS (adjusted non-GAAP) 2.49 3.20 3.80 4.39 4.65 4.64

Other Financials

FCF($m) 3,689 4,308 4,714 6,230 6,547 6,757

Capex($m) 426 594 1,284 1,105 1,071 1,015

Working capital($m) -2,492 -1,113 455 563 652 673

Working capital as % of sales($m) -22.7% -7.4% 2.4% 2.4% 2.5% 2.5%

Days receivables 24 16 28 28 28 28

Days in inventory 60 44 55 55 55 55

Days payable 87 40 70 70 70 70

Total assets($m) 30,572 36,422 43,012 49,696 52,228 54,490

Net Cash ($m) 16,231 19,919 26,837 32,458 34,586 36,707

Source: Berenberg Bank estimates

Global Technology Technology Hardware

24

Imagination

Source: Berenberg estimates

Drivers FY2010 FY2011 FY2012 FY2013E FY2014E FY2015E

Royalty revenues

Revenues (£m) 24 41 64 85 101 115

Licensing revenues

Revenues (£m) 23 28 34 27 30 33

Total units & ASPs

Total units 126 245 325 501 653 766

ASPs 0.19 0.17 0.20 0.17 0.16 0.15

Group

Revenues (£m) 81 98 127 140 161 179

Gross margins 69.1% 78.8% 83.5% 84.4% 84.0% 84.0%

R&D (£m) 35 45 60 75 85 95

R&D (as % of sales) 43.7% 45.6% 46.8% 53.2% 53.0% 53.0%

SG&A (£m) 10 16 18 29 34 38

SG&A (as % of sales) 12.9% 16.6% 14.5% 21.0% 21.0% 21.0%

Operating margin (reported) 12.5% 16.6% 22.2% 10.2% 10.0% 10.0%

EPS (reported) 5.99 7.47 7.93 4.44 5.00 5.56

EPS (adjusted) 7.44 10.44 11.93 8.32 8.87 9.44

Other Financials

FCF (£m) 8 (22) 17 22 23 29

Capex (£m) 1 12 12 12 12 12

Working capital (£m) 14 16 20 21 24 27

Working capital as % of sales 16.9% 16.5% 15.8% 15.3% 14.9% 14.9%

Days receivables 93 103 118 110 110 110

Days payable 174 309 458 440 440 440

Days in inventory 73 109 94 92 92 92

Total assets (£m) 81 175 213 234 262 290

Net debt/(cash) (£m) (28.9) (43.8) (60.7) (80.0) (100.2) (125.3)

Source: Berenberg Bank Estimates

Global Technology Technology Hardware

25

HTC

Source: Berenberg estimates

Drivers 2010 2011 2012 2013E 2014E 2015E

Global smartphone market (m units) 281 461 603 911 1,200 1,400

HTC market share 8.8% 9.9% 5.5% 3.5% 2.8% 2.5%

Handsets

Units shipped (m) 24.6 45.5 33.0 32.0 33.6 35.3

ASP (NT$) 11,003 10,000 8,485 7,976 7,737 7,350

Revenues (NT$ m) 270,680 455,000 280,020 255,322 260,046 259,396

Group

Revenues (NT$ m) 278,761 465,795 289,020 261,322 266,046 265,396

Gross margins 30.1% 28.3% 25.2% 22.0% 21.0% 21.0%

R&D (NT$ m) 12,940 15,961 15,490 15,679 13,302 12,474

R&D (as % of sales) 4.6% 3.4% 5.4% 6.0% 5.0% 4.7%

SG&A (NT$ m) 26,796 47,049 38,615 33,972 31,925 31,847

SG&A (as % of sales) 9.6% 10.1% 13.4% 13.0% 12.0% 12.0%

Operating margin 15.8% 14.8% 6.5% 3.0% 4.0% 4.3%

EPS 47.89 73.76 20.24 8.86 11.79 12.60

Other financials

FCF (NT$ m) 41,057 80,096 16,525 7,781 9,440 11,232

Capex (NT$ m) 4,991 8,411 6,772 6,165 5,587 5,308

Working capital (NT$ m) 24,895 15,127 (1,955) (3,918) (4,598) (4,587)

Working capital as % of sales 8.9% 3.2% -0.7% -1.5% -1.7% -1.7%

Days receivables 82 50 60 60 60 60

Days in inventory 49 31 40 40 40 40

Days payable 120 84 124 124 124 124

Total assets (NT$ m) 190,382 254,592 206,603 201,277 207,766 214,302

Net cash/(debt) (NT$ m) 75,355 90,656 55,400 58,907 61,484 65,853

Global Technology Technology Hardware

26

Foxconn International

Source: Berenberg estimates

Market share (of COGS in %) 2010 2011 2012 2013E 2014E 2015E

Nokia

FIH market share of COGS (in %) 15.6% 14.0% 12.0% 12.0% 12.0% 12.0%

Motorola

FIH market share of COGS (in %) 30.0% 27.0% 25.0% 25.0% 25.0% 25.0%

Sony Ericsson

FIH market share of COGS (in %) 20.2% 16.0% 16.0% 16.0% 16.0% 16.0%

Group

Revenues (USDm) 6,626 6,354 5,240 5,135 5,032 4,932

Gross margins 4.3% 5.3% 0.0% 4.5% 4.3% 4.0%

R&D (USDm) 220 194 173 149 146 143

R&D (as % of sales) 3.3% 3.1% 3.3% 2.9% 2.9% 2.9%

SG&A (USDm) 279 275 236 211 206 202

SG&A (as % of sales) 4.2% 4.3% 4.5% 4.1% 4.1% 4.1%

Operating margin (reported) -3.3% -2.1% -7.8% -2.5% -2.7% -3.0%

Operating margin (adj.)

EPS (basic) -0.03 -0.01 -0.04 -0.01 -0.01 -0.02

EPS (diluted) -0.03 -0.01 -0.04 -0.01 -0.01 -0.02

Other Financials

FCF (USDm) (360) 310 560 232 233 199

Capex (USDm) 254 178 42 42 41 39

Working capital (USDm) 995 805 277 309 301 293

Working capital as % of sales 15.0% 12.7% 5.3% 6.0% 6.0% 5.9%

Days receivables 91 81 79 79 79 79

Days payable 81 74 84 84 84 84

Days in inventory 43 37 24 24 24 24

Total assets (USDm) 6,017 5,612 5,088 4,758 4,919 5,073

Net debt (USDm) (762.1) (1,439.0) (2,142.2) (2,030.5) (2,360.5) (2,655.5)

Source: Berenberg Bank estimates

Global Technology Technology Hardware

27

Hon Hai

Source: Berenberg estimates

Market share (of COGS in %) 2010 2011 2012 2013E 2014E 2015E

Apple

53.1% 56.0% 60.0% 58.0% 57.0% 57.0%

HP

15.1% 15.5% 15.5% 15.5% 15.5% 15.5%

Sony

77.7% 78.0% 78.0% 78.0% 78.0% 78.0%

Group

Revenues (NT$m) 2,997,205 3,452,681 3,905,395 3,932,654 3,847,106 3,883,611

Gross margins 8.1% 7.7% 8.4% 8.2% 8.1% 8.0%

R&D (NT$m) 38,791 40,847 45,627 47,192 46,165 46,603

R&D (as % of sales) 1.3% 1.2% 1.2% 1.2% 1.2% 1.2%

SG&A (NT$m) 119,265 142,691 175,552 165,171 161,578 163,112

SG&A (as % of sales) 4.0% 4.1% 4.5% 4.2% 4.2% 4.2%

Operating margin (reported) 2.9% 2.4% 2.8% 2.8% 2.7% 2.6%

EPS (basic) 8.01 7.72 8.03 7.32 6.91 6.72

EPS (diluted) 7.75 7.44 7.79 7.10 6.70 6.52

Other Financials

FCF (NT$m) (10,260) 14,036 109,661 95,165 89,570 84,760

Capex (NT$m) 72,716 87,170 70,144 66,855 63,477 62,138

Working capital (NT$m) 234,889 308,077 344,560 347,808 339,934 340,949

Working capital as % of sales 7.8% 8.9% 8.8% 8.8% 8.8% 8.8%

Days receivables 49 50 59 59 59 59

Days payable 57 63 65 65 65 65

Days in inventory 34 44 36 36 36 36

Total assets (NT$m) 1,380,532 1,730,311 2,044,404 2,124,651 2,182,254 2,257,591

Net debt /(cash) (NT$m) (12,064) (15,671) (115,736) (200,281) (279,233) (353,376)

Source: Berenberg Bank estimates

Hon Hai market share of COGS

(in %)

Hon Hai market share of COGS

(in %)

Hon Hai market share of COGS

(in %)

Global Technology Technology Hardware

28

Juniper

Source: Berenberg estimates

Drivers 2010 2011 2012 2013E 2014E 2015E

Product

Revenues ($'000) 3,258,700 3,478,300 3,262,100 3,353,317 3,400,903 3,395,143

Gross Margin 69.6% 67.6% 65.5% 65.0% 62.0% 59.0%

Service

Revenues ($000) 834,600 902,100 1,038,200 1,117,772 1,133,634 1,192,888

Gross Margin 59.7% 54.8% 58.0% 62.0% 61.0% 61.0%

Group

Revenues ($'000) 4,093,300 4,380,400 4,300,300 4,471,089 4,534,537 4,588,031

Gross margins 68% 65% 64% 64% 62% 60%

R&D ($'000) 837,188 925,711 992,021 983,640 952,253 917,606

R&D (as % of sales) 20.5% 21.1% 23.1% 22.0% 21.0% 20.0%

SG&A ($'000) 945,970 1,071,465 1,132,267 1,108,830 1,065,616 1,055,247

SG&A (as % of sales) 23.1% 24.5% 26.3% 24.8% 23.5% 23.0%

Operating margin (GAAP) 21.1% 15.2% 7.2% 12.1% 12.0% 11.3%

Operating margin (adjusted) 24.0% 19.4% 14.3% 17.5% 17.3% 16.5%

EPS (GAAP) 1.15 0.66 0.25 0.74 0.74 0.71

EPS (adjusted) 1.32 1.07 0.79 1.06 1.07 1.04

Other Financials

FCF($'000) 492,717 918,275 293,700 467,524 502,439 564,115

Capex($'000) 185,291 266,314 348,700 344,451 340,090 339,514

Working capital($'000) 705,542 733,095 843,200 789,234 775,510 803,831

Working capital as % of sales($'000) 17.2% 16.7% 19.6% 17.7% 17.1% 17.5%

Days receivables 53 48 37 37 37 37

Days payable 79 75 46 46 46 46

Total assets($'000) 8,467,851 9,983,820 9,832,100 10,862,863 11,422,403 12,084,351

Net Cash ($'000) 2,123,491 2,378,648 1,668,600 2,540,544 3,042,980 3,607,095

Source: Berenberg Bank estimates

Global Technology Technology Hardware

29

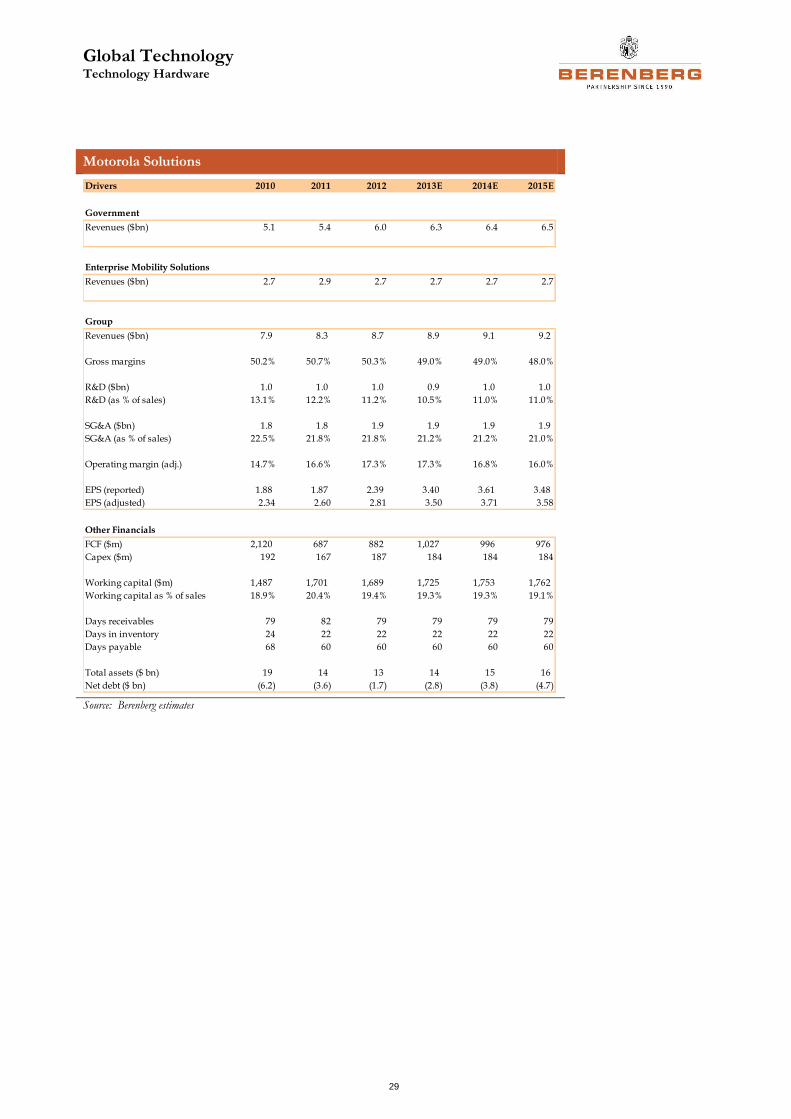

Motorola Solutions

Source: Berenberg estimates

Drivers 2010 2011 2012 2013E 2014E 2015E

Government

Revenues ($bn) 5.1 5.4 6.0 6.3 6.4 6.5

Enterprise Mobility Solutions

Revenues ($bn) 2.7 2.9 2.7 2.7 2.7 2.7

Group

Revenues ($bn) 7.9 8.3 8.7 8.9 9.1 9.2

Gross margins 50.2% 50.7% 50.3% 49.0% 49.0% 48.0%

R&D ($bn) 1.0 1.0 1.0 0.9 1.0 1.0

R&D (as % of sales) 13.1% 12.2% 11.2% 10.5% 11.0% 11.0%

SG&A ($bn) 1.8 1.8 1.9 1.9 1.9 1.9

SG&A (as % of sales) 22.5% 21.8% 21.8% 21.2% 21.2% 21.0%

Operating margin (adj.) 14.7% 16.6% 17.3% 17.3% 16.8% 16.0%

EPS (reported) 1.88 1.87 2.39 3.40 3.61 3.48

EPS (adjusted) 2.34 2.60 2.81 3.50 3.71 3.58

Other Financials

FCF ($m) 2,120 687 882 1,027 996 976

Capex ($m) 192 167 187 184 184 184

Working capital ($m) 1,487 1,701 1,689 1,725 1,753 1,762

Working capital as % of sales 18.9% 20.4% 19.4% 19.3% 19.3% 19.1%

Days receivables 79 82 79 79 79 79

Days in inventory 24 22 22 22 22 22

Days payable 68 60 60 60 60 60

Total assets ($ bn) 19 14 13 14 15 16

Net debt ($ bn) (6.2) (3.6) (1.7) (2.8) (3.8) (4.7)

Source: Berenberg Bank estimates

Global Technology Technology Hardware

30

Foxconn Technology

Source: Berenberg estimates

Drivers 2010 2011 2012 2013E 2014E 2015E

Apple

Apple revenues 22,234 30,161 34,971 34,664 37,272 40,120

% of total revenues 16.3% 22.9% 26.2% 25.7% 26.2% 26.9%

Nintendo

Nintendo revenues 90,330 76,186 59,400 60,200 57,190 51,170

% of total revenues 66.1% 57.9% 44.5% 44.6% 40.1% 34.4%

Group

Revenues (NT$m) 136,724 131,498 133,617 134,895 142,499 148,935

Gross margins 10.8% 9.0% 10.5% 10.4% 10.0% 10.0%

R&D (NT$m) 1,290 1,132 1,121 1,079 1,140 1,191

R&D (as % of sales) 0.9% 0.9% 0.8% 0.8% 0.8% 0.8%

SG&A (NT$m) 4,070 3,612 3,758 3,777 3,705 3,872

SG&A (as % of sales) 3.0% 2.7% 2.8% 2.8% 2.6% 2.6%

Operating margin (reported) 6.9% 5.4% 6.8% 6.8% 6.6% 6.6%

EPS (basic) 6.85 6.84 6.78 6.58 6.74 7.03

EPS (diluted) 6.81 6.80 6.78 6.58 6.74 7.03

Other Financials

FCF (NT$m) 8,037 3,675 12,116 8,970 6,011 6,230

Capex (NT$m) 3,662 3,851 2,016 2,037 2,066 1,936

Working capital (NT$m) 14,872 17,932 17,176 17,352 18,231 19,054

Working capital as % of sales 10.9% 13.6% 12.9% 12.9% 12.8% 12.8%

Days receivables 74 95 104 104 104 104

Days payable 55 64 81 81 81 81

Days in inventory 16 14 17 17 17 17

Total assets (NT$m) 92,552 97,723 107,031 114,268 123,063 131,866

Net debt/(cash) (NT$m) (15,032) (23,472) (27,380) (34,989) (39,641) (44,511)

Source: Berenberg Bank estimates

Global Technology Technology Hardware

31

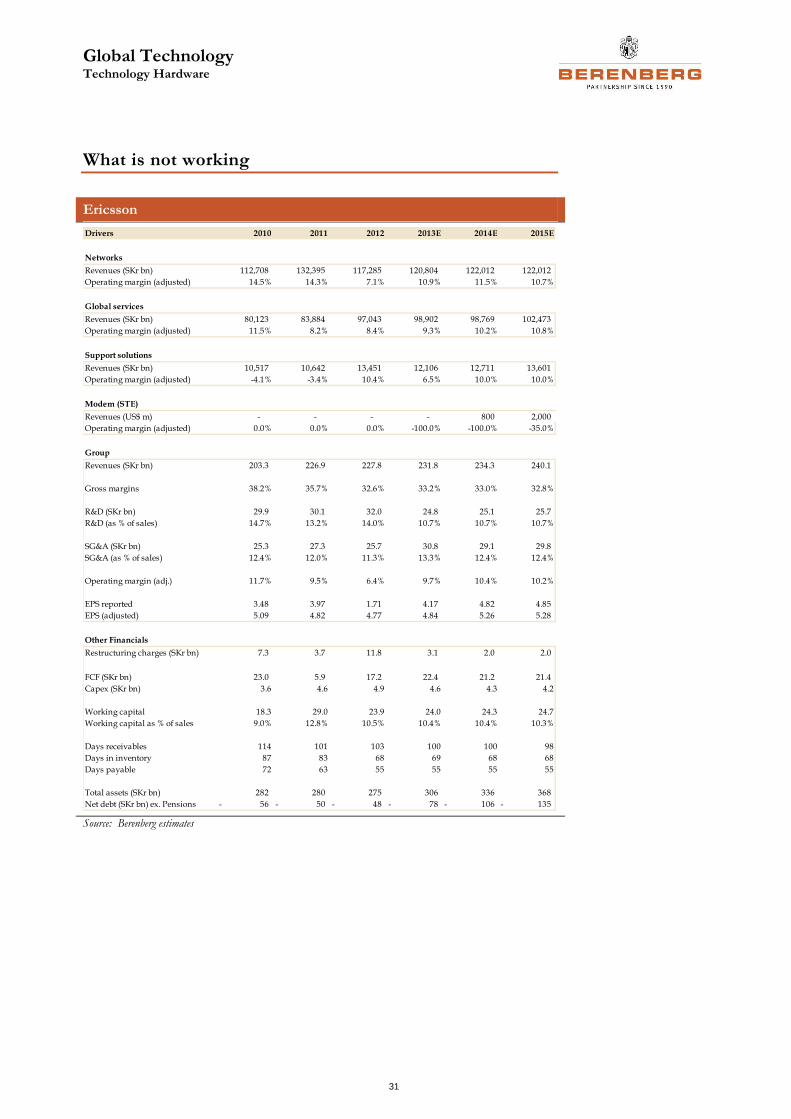

What is not working

Ericsson

Source: Berenberg estimates

Drivers 2010 2011 2012 2013E 2014E 2015E

Networks

Revenues (SKr bn) 112,708 132,395 117,285 120,804 122,012 122,012

Operating margin (adjusted) 14.5% 14.3% 7.1% 10.9% 11.5% 10.7%

Global services

Revenues (SKr bn) 80,123 83,884 97,043 98,902 98,769 102,473

Operating margin (adjusted) 11.5% 8.2% 8.4% 9.3% 10.2% 10.8%

Support solutions

Revenues (SKr bn) 10,517 10,642 13,451 12,106 12,711 13,601

Operating margin (adjusted) -4.1% -3.4% 10.4% 6.5% 10.0% 10.0%

Modem (STE)

Revenues (US$ m) - - - - 800 2,000

Operating margin (adjusted) 0.0% 0.0% 0.0% -100.0% -100.0% -35.0%

Group

Revenues (SKr bn) 203.3 226.9 227.8 231.8 234.3 240.1

Gross margins 38.2% 35.7% 32.6% 33.2% 33.0% 32.8%

R&D (SKr bn) 29.9 30.1 32.0 24.8 25.1 25.7

R&D (as % of sales) 14.7% 13.2% 14.0% 10.7% 10.7% 10.7%

SG&A (SKr bn) 25.3 27.3 25.7 30.8 29.1 29.8

SG&A (as % of sales) 12.4% 12.0% 11.3% 13.3% 12.4% 12.4%

Operating margin (adj.) 11.7% 9.5% 6.4% 9.7% 10.4% 10.2%

EPS reported 3.48 3.97 1.71 4.17 4.82 4.85

EPS (adjusted) 5.09 4.82 4.77 4.84 5.26 5.28

Other Financials

Restructuring charges (SKr bn) 7.3 3.7 11.8 3.1 2.0 2.0

FCF (SKr bn) 23.0 5.9 17.2 22.4 21.2 21.4

Capex (SKr bn) 3.6 4.6 4.9 4.6 4.3 4.2

Working capital 18.3 29.0 23.9 24.0 24.3 24.7

Working capital as % of sales 9.0% 12.8% 10.5% 10.4% 10.4% 10.3%

Days receivables 114 101 103 100 100 98

Days in inventory 87 83 68 69 68 68

Days payable 72 63 55 55 55 55

Total assets (SKr bn) 282 280 275 306 336 368

Net debt (SKr bn) ex. Pensions 56- 50- 48- 78- 106- 135-

Source: Berenberg Bank estimates

Global Technology Technology Hardware

32

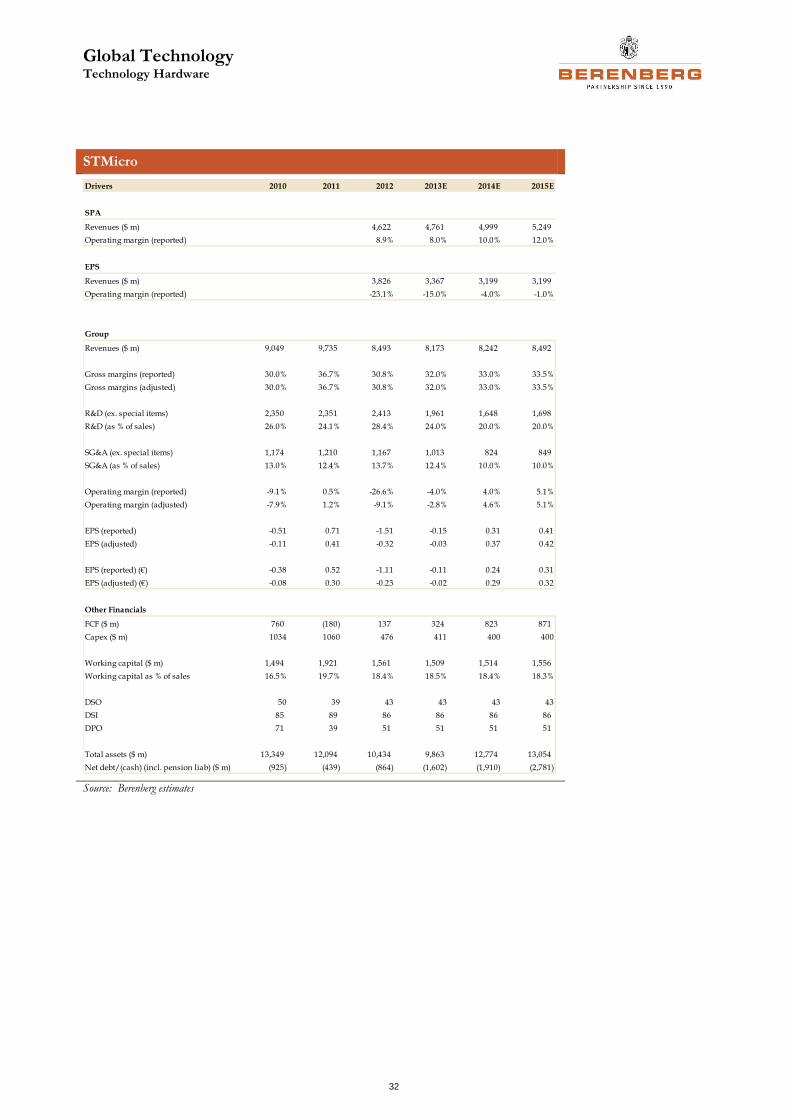

STMicro

Source: Berenberg estimates

Drivers 2010 2011 2012 2013E 2014E 2015E

SPA

Revenues ($ m) 4,622 4,761 4,999 5,249

Operating margin (reported) 8.9% 8.0% 10.0% 12.0%

EPS

Revenues ($ m) 3,826 3,367 3,199 3,199

Operating margin (reported) -23.1% -15.0% -4.0% -1.0%

Group

Revenues ($ m) 9,049 9,735 8,493 8,173 8,242 8,492

Gross margins (reported) 30.0% 36.7% 30.8% 32.0% 33.0% 33.5%

Gross margins (adjusted) 30.0% 36.7% 30.8% 32.0% 33.0% 33.5%

R&D (ex. special items) 2,350 2,351 2,413 1,961 1,648 1,698

R&D (as % of sales) 26.0% 24.1% 28.4% 24.0% 20.0% 20.0%

SG&A (ex. special items) 1,174 1,210 1,167 1,013 824 849

SG&A (as % of sales) 13.0% 12.4% 13.7% 12.4% 10.0% 10.0%

Operating margin (reported) -9.1% 0.5% -26.6% -4.0% 4.0% 5.1%

Operating margin (adjusted) -7.9% 1.2% -9.1% -2.8% 4.6% 5.1%

EPS (reported) -0.51 0.71 -1.51 -0.15 0.31 0.41

EPS (adjusted) -0.11 0.41 -0.32 -0.03 0.37 0.42

EPS (reported) (€) -0.38 0.52 -1.11 -0.11 0.24 0.31

EPS (adjusted) (€) -0.08 0.30 -0.23 -0.02 0.29 0.32

Other Financials

FCF ($ m) 760 (180) 137 324 823 871

Capex ($ m) 1034 1060 476 411 400 400

Working capital ($ m) 1,494 1,921 1,561 1,509 1,514 1,556

Working capital as % of sales 16.5% 19.7% 18.4% 18.5% 18.4% 18.3%

DSO 50 39 43 43 43 43

DSI 85 89 86 86 86 86

DPO 71 39 51 51 51 51

Total assets ($ m) 13,349 12,094 10,434 9,863 12,774 13,054

Net debt/(cash) (incl. pension liab) ($ m) (925) (439) (864) (1,602) (1,910) (2,781)

Source: Berenberg Bank estimates

Global Technology Technology Hardware

33

BlackBerry

Source: Berenberg estimates

Drivers 2011 2012 2013 2014E 2015E

CY 2010 2011 2012 2013E 2014E

Global smartphone market 281 461 603 911 1,200

(m units)

market share 18.6% 10.6% 4.7% 3.3% 2.3%

Hardware

Units shipped (m) 52.3 49.0 28.1 30.3 27.9

ASP ($) 305 282 237 268 255

Revenues ($m) 15,956 13,794 6,663 8,131 7,107

Services

Subscriber base 60,900 77,850 76,000 69,000 64,000

Net additions 19,600 16,950 -1,850 -7,000 -5,000

ARPU ($) 5.0 4.7 4.4 3.8 3.3

Revenues ($m) 3,197 4,086 4,086 3,340 2,633

Group

Revenues ($m) 19,907 18,421 11,072 12,287 10,579

Gross margins 44.3% 35.6% 31.0% 36.0% 27.0%

R&D ($m) 1,351 1,559 1,509 1,474 1,164

R&D (as % of sales) 6.8% 8.5% 13.6% 12.0% 11.0%

SG&A ($m) 2,400 2,604 2,111 2,457 1,587

SG&A (as % of sales) 12.1% 14.1% 19.1% 20.0% 15.0%

Operating margin 23.3% 8.0% -11.2% -2.0% -4.0%

EPS (reported) 6.36 2.22 -1.23 -0.35 -0.61

EPS (adjusted) 6.36 1.54 -1.87 -0.35 -0.61

Other financials

FCF ($m) 2,970 2,010 1,890 949 483

Capex ($m) 1,039 902 413 405 391

Working capital ($m) 3,741 3,345 1,892 2,174 1,807

Working capital as % of sales 18.8% 18.2% 17.1% 17.7% 17.1%

Days receivables 60 70 78 78 78

Days in inventory 20 32 29 29 28

Days payable 27 23 51 50 50

Total assets ($m) 12,875 13,731 13,165 12,936 12,367

Net cash ($m) 2,121 1,774 2,654 3,603 4,086

Global Technology Technology Hardware

34

Nokia

Source: Berenberg estimates

Drivers 2011 2012 2013E 2014E 2015E

Global handset market size 1,511 1,800 1,900 2,200 2,400

(m units)

Global smartphone market (m units) 461 603 911 1,200 1,400

Nokia Device and Services

Nokia's market share 27.6% 18.5% 14.4% 11.2% 9.4%

Units shipped (m) 417 333 273 245 226

ASP (€) 56.9 47.2 49.0 49.0 46.6

Revenues (€m) 23,943 15,686 13,374 12,036 10,520

Operating margin (adjusted) 6.6% -4.5% 0.5% 1.0% 1.0%

NSN

Revenues (€m) 14,041 13,779 13,300 13,300 13,300

Operating margin (adjusted) 1.6% 5.6% 6.0% 6.0% 3.0%

Location & Commerce

Revenues (€m) 1,050 1,104 850 900 950

Operating margin (adjusted) 19.4% 13.9% -1.0% 2.0% 10.0%

Group

Revenues (€ bn) 38.7 30.2 27.5 26.2 24.8

Gross margins (adjusted) 29.4% 28.0% 29.0% 27.0% 25.0%

R&D (adjusted) (€bn) 5.2 4.4 4.0 3.1 2.7

R&D (as % of sales) 13.4% 14.6% 14.5% 12.0% 11.0%

SG&A (adjusted) (€ bn) 4.4 3.9 3.3 2.9 2.7

SG&A (as % of sales) 11.5% 12.8% 12.0% 11.0% 11.0%

Operating margin (IFRS) -2.7% -7.6% 0.3% 1.7% 0.6%

Operating margin (adjusted) 4.7% 0.4% 2.5% 4.0% 3.0%

EPS (IFRS) 0.15- 1.14- 0.07- 0.00- 0.05-

EPS (adjusted) 0.29 0.17- 0.01- 0.08 0.05

Other Financials

FCF (€bn) 0.54 (0.82) (0.75) 0.51 0.27

Capex (€m) 597 461 330 315 297

Working capital (€bn) 4.0 2.7 2.8 2.7 2.5

Working capital as % of sales 10.3% 8.9% 10.4% 10.2% 9.9%

Days receivable 67 66 66 66 66

Days in inventory 31 26 31 31 31

Days payable 73 73 72 72 72

Total assets (€bn) 36.2 29.9 29.4 28.1 27.4

Net debt (€bn) (5.8) (3.8) (3.7) (3.6) (3.5)

Source: Berenberg Bank estimates

Global Technology Technology Hardware

35

Alcatel-Lucent

Source: Berenberg estimates

Drivers 2010 2011 2012 2013E 2014E 2015E

Network and platforms

Revenues (€mn) 11,924 11,315 10,933 10,667

Operating margin (ex. restructuring) -0.7% -1.1% -0.4% 0.4%

Focused business

Revenues (€mn) 1,236 1,298 1,363 1,431

Managed services

Revenues (€mn) 1,000 1,050 1,103 1,158

Group

Revenues (€bn) 16.00 15.33 14.45 13.66 13.40 13.26

Gross Margins (pro-forma) 34.8% 36.3% 30.1% 29.3% 28.2% 27.8%

R&D (pro-forma) (€bn) 2.5 2.4 2.3 2.3 2.0 1.9

R&D (as % of sales) 15.6% 15.4% 16.1% 16.5% 15.0% 14.0%

SG&A (pro-forma) (€bn) 2.8 2.7 2.3 2.0 1.8 1.7

SG&A (as % of sales) 17.4% 17.4% 15.7% 14.5% 13.5% 13.0%

Operating margin (pro-forma ex. restructuring) 1.8% 3.4% -1.8% -1.7% -0.3% 0.8%

EPS (pro-forma) excl restruct. pension & discont. ops. -0.07 0.49 -0.48 -0.26 -0.03 0.03

Other Financials

Free cash flow (€m) 818- 477- 679- 797- 633- 833-

Capex (€m) 692 570 582 492 472 456

Working capital (€m) 1,634 1,490 1,072 991 961 942

as % of sales 10.2% 9.7% 7.4% 7.2% 7.2% 7.1%

Days receivable 84 81 72 72 72 72

Days in inventory 80 74 70 68 70 70

Days payable 151 145 135 133 134 134

Total assets (€m) 24,876 24,203 21,354 22,477 21,803 20,916

Net debt -311 146 -118 865 1,497 2,330

Source: Berenberg Bank estimates

Global Technology Technology Hardware

36

ZTE

Source: Berenberg estimates

Drivers 2010 2011 2012 2013E 2014E 2015E

Networks

Revenues (CNY '000) 41,990 46,522 41,603 45,763 48,966 52,394

YoY growth 5.0% 10.8% -10.6% 10.0% 7.0% 7.0%

Handsets

Revenues (CNY '000) 17,927 26,934 25,839 32,299 40,373 47,640

YoY growth 37.1% 50.2% -4.1% 25.0% 25.0% 18.0%

Others

Revenues (CNY '000) 10,346 12,799 16,778 18,120 19,026 19,977

YoY growth 24.5% 23.7% 31.1% 8.0% 5.0% 5.0%

Group

Revenues (CNY '000) 70,263 86,254 84,219 96,182 108,366 120,012

Gross margins 30.8% 30.3% 22.2% 24.0% 23.0% 23.0%

R&D 7,092 8,493 8,829 9,522 10,511 11,641

R&D (as % of sales) 10.1% 9.8% 10.5% 9.9% 9.7% 9.7%

SG&A 11,414 13,385 13,790 13,465 14,088 14,401

SG&A (as % of sales) 16.2% 15.5% 16.4% 14.0% 13.0% 12.0%

Operating margin (reported) 7.2% 5.7% -0.2% 0.6% 0.7% 1.7%

Operating margin (adjusted) 3.4% 3.3% -5.5% 0.1% 0.3% 1.3%

EPS (reported) CNY 1.17 0.61 -0.84 -0.16 -0.10 0.21

EPS (adjusted) CNY 1.25 0.66 -0.77 -0.16 -0.10 0.21

EPS (reported) (HK$) 1.35 0.70 -0.96 -0.20 -0.13 0.26

EPS (adjusted) (HK$) 1.44 0.76 -0.88 -0.20 -0.13 0.26

Other Financials

FCF (CNY '000) (2,125) (5,877) (828) (139) 181 285

Capex (CNY '000) 3,067 4,065 2,378 2,308 2,276 2,220

Working capital (CNY '000) 19,668 15,135 8,082 9,813 10,756 11,912

Working capital as % of sales 28.0% 17.5% 9.6% 10.2% 9.9% 9.9%

Days receivables 172 139 114 114 114 114

Days in inventory 91 91 64 64 64 64

Days payable 192 198 165 165 165 165

Total assets (CNY '000) 85,509 105,368 107,446 110,355 114,684 119,441

Net debt (CNY '000) (1,530) 1,039 (1,194) (1,055) (1,236) (1,521)

Source: Berenberg Bank estimates

Global Technology Technology Hardware

37

TPK

Source: Berenberg estimates

Drivers 2010 2011 2012 2013E 2014E 2015E

SFF touch module

Revenue from SFF touch module 14,771 17,464 12,096 13,439 13,200 12,456

LFF touch module

Revenue from LFF touch module 19,305 57,314 77,625 78,408 91,351 95,386

Touch display

Revenue from touch display 25,623 68,595 83,938 115,425 127,680 134,064

Apple market share 60.0% 55.0% 45.0% 45.0% 40.0% 40.0%

Group

Revenues (NT$m) 59,699 143,372 173,659 207,272 232,231 241,906

Gross margins 16.8% 16.9% 17.1% 16.5% 15.0% 14.7%

R&D (NT$m) 1,574 3,491 4,644 5,804 6,735 7,015

R&D (as % of sales) 2.6% 2.4% 2.7% 2.8% 2.9% 2.9%

SG&A (NT$m) 2,210 4,751 4,764 6,218 6,502 6,773

SG&A (as % of sales) 3.7% 3.3% 2.7% 3.0% 2.8% 2.8%

Operating margin (reported) 10.5% 11.4% 11.6% 10.7% 9.3% 9.0%

EPS (basic) 22.69 35.81 42.42 52.70 52.10 52.52

EPS (diluted) 21.93 35.81 42.42 52.70 52.10 52.52

Other Financials

FCF (NT$m) (4,770) (5,482) 970 3,031 4,873 6,088