Embed Size (px)

Citation preview

Global Intelligence Letter 1

Farmland Is in Increasingly Short Supply, So We’re Adding 160,000 Acres to Our Portfolio

Dear Global Intelligence Letter subscriber,Raw soybeans taste hideous.I know this only because of a tour I took through a Uruguayan

soybean farm a few years ago. I was there with my friend, Sebastian, owner of a local farm-management company, and I wanted to know if soybeans right off the stem taste anything like the edamame I order at Japanese restaurants.

They don’t.I was on this tour as part of my effort to show American

investors the opportunities that exist in farmland. It’s a message best summed up by the bumper sticker on Sebastian’s Toyota pickup: “El Futuro Esta En La Tierra!”

The future is in the land.Perhaps a truer bumper sticker has never been printed, because

no matter where you find it—Uruguay, America, Brazil, the black soils of Eastern Europe—farmland is the future.

As the clichéd punchline about land notes: They aren’t making it anymore. In fact, when it comes to farmland, they’re taking it away.

Every year, cropland slightly larger than the size of Delaware falls victim to development in America. The 2017 USDA Census of Agriculture (the latest) reported that American farm acreage over the previous five years had vanished by the equivalent of nearly 22,400 square miles. That’s almost all of West Virginia…poof!

In a very real sense, Joni Mitchell was right: They paved paradise and put up a parking lot…and cookie-cutter tract homes and gas-station mini-marts and strip malls.

Globally, it’s just as bad, if not worse, as modernization and Westernization steam roll across developing nations, which tend to be primarily agricultural economies. Over the last four decades, the world has lost one-third of its arable land—even as the number of mouths to feed on planet Earth has increased by 78% in the same period to nearly 8 billion people.

Fewer and fewer acres of land to nourish more and more people.

In this issue

7 The Two Big Clouds Hanging Over the Global Economy

8 Malta’s Traditional Row Houses: Huge Profit Potential for Investors

11 Intel Updates

Jeff D. Opdyke is a journalist and investment analyst who spent 17 years writing about money and investing for The Wall Street Journal. Based in Prague, he has authored 10 books on topics such as investing globally and personal finance, and has visited nearly 70 countries.

Publisher Jackie FlynnEditor Jeff D. OpdykeManaging Editor Ciaran MaddenGraphic Designer Rob McGrath

globalintelligenceletter.com

© Copyright 2021 by International Living Publishing Ltd. All Rights Reserved. Reproduction, copying, or redistribution (electronic or otherwise, including online) is strictly prohibited without the express written permission of International Living, Woodlock House, Carrick Road, Portlaw, Co. Waterford, Ireland. Global Intelligence Letter is published monthly. Copies of this e-newsletter are furnished directly by subscription only. Annual subscription is $149. To place an order or make an inquiry, visit www.internationalliving.com/about-il/customer-service. Global Intelligence Letter presents information and research believed to be reliable, but its accuracy cannot be guaranteed. There may be dangers associated with international travel and investment, and readers should investigate any opportunity fully before committing to it. Nothing in this e-newsletter should be considered personalized advice, and no communication by our employees to you should be deemed as personalized financial or investment advice, or personalized advice of any kind. We expressly forbid our writers from having a financial interest in any security they personally recommend to readers. All of our employees and agents must wait 24 hours after online publication prior to following an initial recommendation. Any investments recommended in this letter should be made only after consulting with your investment adviser and only after reviewing the prospectus or financial statements of the company.

October 2021 | Issue 8

Global Intelligence Letter

October 2021 | Issue 82

That math is problematic. To be sure, technology is coming to the

rescue to various degrees. We have more efficient agricultural practices. Better use of land and machinery. Drones and other bits of whiz-bangery that can precisely gauge and meet customized fertilizer needs for individual parcels on a vast plot of land.

Still, farmland itself remains the most crucial factor in feeding us all. There are no signs that will change in our lifetime—or our kids’.

And because farmland is increasingly rare, it’s increasingly valuable. Which means that farmland deserves space inside a diversified investment portfolio.

That’s what the October issue of the Global Intelligence Letter is all about: Our path to owning farmland—nearly 160,000 acres of it, to be exact. Tracts of land stretching across 16 American states from the Pacific to the Atlantic, and growing everything from soybeans to blueberries.

Plus, a recent catalyst means that we have a rare opportunity to buy our share of this farmland, through our brokerage accounts, at a particularly good price.

Farming Has Changed in AmericaLet me start by casting your memory back to

fall 1985… Champaign, Illinois. Memorial Stadium,

where the University of Illinois plays its football games.

More than 80,000 people gathered for a weekend of performances by Alabama, Bon Jovi, Johnny Cash, and numerous other acts in what was billed as the first-ever Farm Aid.

At that point, American farmers were in dire straits amid what was then an ongoing farm crisis more severe than the Great Depression.

The Federal Reserve had jacked up interest rates to double-digit levels to tackle the inflation of the 1970s. But when inflation collapsed, so did crop prices…hitting farmers hard.

Moreover, farmers, who regularly borrow heavily for equipment, land, seeds, and supplies, were badly impacted by the higher interest rates.

Squeezed from both sides, family farms were collapsing left, right, and center.

Despite the noble efforts of Johnny Cash and Co., this sad trend has not reversed in the decades since. Corporate farms have come to dominate America’s agriculture sector, killing off the family farmer to a large extent.

Yet with this corporatization came profits. In recent times, net farm income has surged toward record levels. And it’s primed to rise even higher because of the inflationary pressures now coursing through the economy.

The U.S. Department of Agriculture’s Economic Research Service reported last month that net farm income should be in the neighborhood of $113 billion by the end of 2021. If that’s accurate, it would be well above the $94 billion average over the last two decades.

It would also mark a 20% increase from 2020’s net farm income, which was 20% higher than in 2019.

Some of that, of course, is government money that flows to farmers annually through all sorts of federal assistance programs. But a large portion of it comes from so-called “cash receipts,” the money farmers collect from selling their crops.

If the USDA is right, cash receipts will top $420 billion this year, 18% higher than last year.

That’s a function of the inflation I’ve been writing to you about all year.

It speaks, as well, to the commodity super-cycle that’s currently underway. (See our May issue for my research on this trend.)

And it says that farmland values will very likely continue their climb higher.

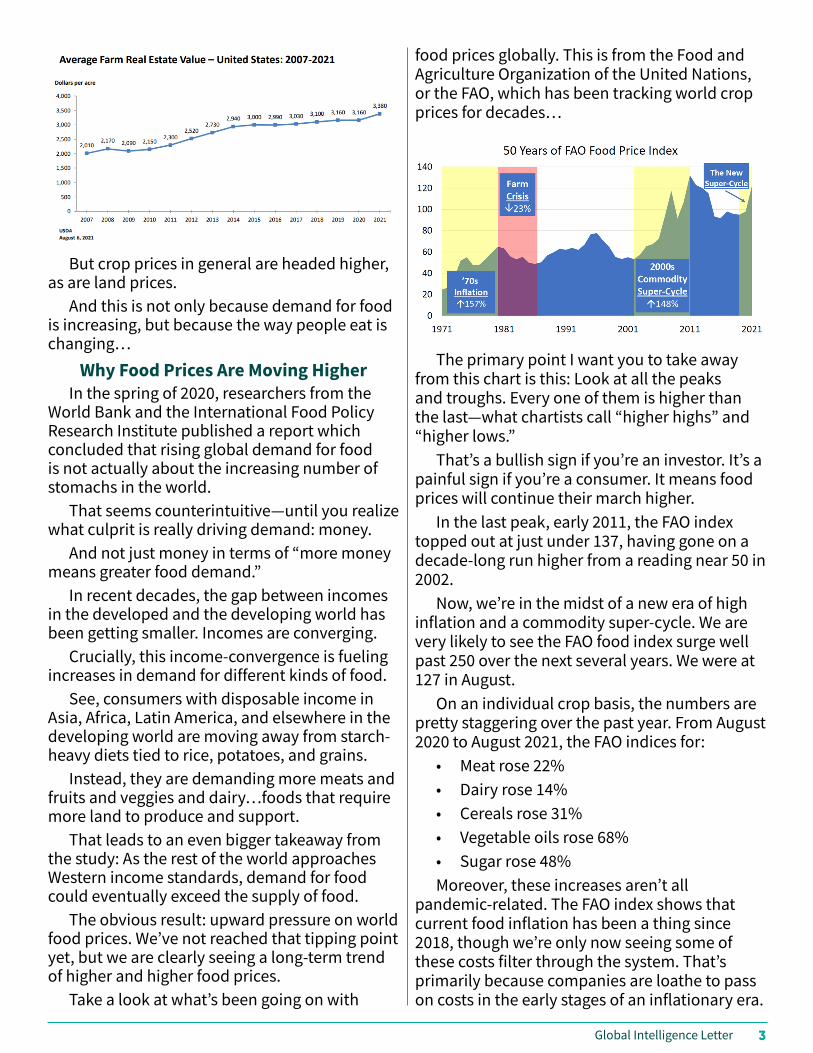

The average price for an acre of American farmland has been in an uptrend since the end of the global financial crisis in 2009. You can see that in the USDA chart on farm real estate at the top of next column. (Cropland and pasture land values have similarly trended upward.)

This is why we want to own exposure to farmland.

Farmland is going to generate increasing profits as global demand for food persistently and irreversibly climbs ever-higher from here. That’s not to say there won’t be ups and downs. Of course there will—this is a commodities market, and commodity prices fluctuate.

Global Intelligence Letter 3

But crop prices in general are headed higher, as are land prices.

And this is not only because demand for food is increasing, but because the way people eat is changing…

Why Food Prices Are Moving HigherIn the spring of 2020, researchers from the

World Bank and the International Food Policy Research Institute published a report which concluded that rising global demand for food is not actually about the increasing number of stomachs in the world.

That seems counterintuitive—until you realize what culprit is really driving demand: money.

And not just money in terms of “more money means greater food demand.”

In recent decades, the gap between incomes in the developed and the developing world has been getting smaller. Incomes are converging.

Crucially, this income-convergence is fueling increases in demand for different kinds of food.

See, consumers with disposable income in Asia, Africa, Latin America, and elsewhere in the developing world are moving away from starch-heavy diets tied to rice, potatoes, and grains.

Instead, they are demanding more meats and fruits and veggies and dairy…foods that require more land to produce and support.

That leads to an even bigger takeaway from the study: As the rest of the world approaches Western income standards, demand for food could eventually exceed the supply of food.

The obvious result: upward pressure on world food prices. We’ve not reached that tipping point yet, but we are clearly seeing a long-term trend of higher and higher food prices.

Take a look at what’s been going on with

food prices globally. This is from the Food and Agriculture Organization of the United Nations, or the FAO, which has been tracking world crop prices for decades…

The primary point I want you to take away from this chart is this: Look at all the peaks and troughs. Every one of them is higher than the last—what chartists call “higher highs” and “higher lows.”

That’s a bullish sign if you’re an investor. It’s a painful sign if you’re a consumer. It means food prices will continue their march higher.

In the last peak, early 2011, the FAO index topped out at just under 137, having gone on a decade-long run higher from a reading near 50 in 2002.

Now, we’re in the midst of a new era of high inflation and a commodity super-cycle. We are very likely to see the FAO food index surge well past 250 over the next several years. We were at 127 in August.

On an individual crop basis, the numbers are pretty staggering over the past year. From August 2020 to August 2021, the FAO indices for:

• Meat rose 22%• Dairy rose 14%• Cereals rose 31%• Vegetable oils rose 68%• Sugar rose 48%Moreover, these increases aren’t all

pandemic-related. The FAO index shows that current food inflation has been a thing since 2018, though we’re only now seeing some of these costs filter through the system. That’s primarily because companies are loathe to pass on costs in the early stages of an inflationary era.

October 2021 | Issue 84

But once the corporate pain is too great, the price hikes begin. And they’ve begun.

Food giant Conagra has been raising prices and says more hikes are coming. Domino’s pizzas cost more. PepsiCo is increasing prices. General Mills, Campbell Soup, Unilever, and J.M. Smucker have all said they’re raising prices on their supermarket products. Tyson Foods, meanwhile, told Wall Street in August to expect higher chicken prices because, in part, animal-feed costs—basically, grains—continue to rise.

The BBC reported last month that food-price inflation in the U.K. in August saw the biggest jump since records began in 1997. In the U.S., food prices are rising at nearly 4% annually, a pace quicker than what the U.K. is experiencing.

All of this plays through the farm patch in some way or another. These rising prices are all tied to crops used to feed us, or to feed the animals that become our steaks and burgers. Which is exactly why I want to own Farmland Partners Inc.

The 8 Upsides of Our Farmland PlayFarmland Partners is a real estate investment

trust, or REIT, that owns nearly 160,000 acres of farmland across 16 ag-rich states, from California to Florida. The company doesn’t do any of the actual farming; that’s left to roughly 100 tenant farmers who rent the land and grow the crops dominant in their region.

Right now, about 70% of Farmland’s portfolio is so-called primary crops such as corn, soy, wheat, rice, and cotton—crops that have never-ending demand on a global scale because they are the basis of so many other products.

The other 30% of the company’s farmland is specialty crops, including berries, citrus, nuts, beans, and veggies.

Basically, then, the crops that grow on Farmland’s properties end up as everything from burgers to animal feed, to packaged food products and the ingredients that go into restaurant meals. We pretty much have the entirety of humanity’s food needs covered.

So, let me lay out the reasons I want Farmland’s shares in our portfolio:

1. The income streamFarmland generates the bulk of its income

from rent it charges those tenant farmers. It also shares partly in the value of the crops those farmers grow and sell. So, this is a pure play on rental income, which will increase as demand for land continues to climb, and as crop prices and crop yields rise.

Let me note that this year, rental income is slightly below 2020, even as crop prices and land prices are rising. That’s a function of the knock-on effects of the pandemic, which impacted crop-marketing cycles and such. That will straighten itself out in due course.

2. Unquenchable food demandAs I noted above, demand for food isn’t just

rising—as has been the case for millennia. We’re seeing rising demand for more crop-intensive foods (meat and dairy) as developing-nation incomes converge with the West.

The FAO expects that because of this, by 2050, the world will require 1 billion additional tons of grain each year. That’s basically double the amount of grain the U.S. produces annually. That will directly lead to higher crop prices and higher rental rates on farmland.

3. Limited land supplyLike I said, they’re simply not making

farmland anymore. There are locations in the world where new

farmland could emerge. Parts of southern Brazil, for instance, and large swaths of sub-Saharan Africa. But the complete lack of even rudimentary infrastructure relative to the land’s location, and the political climates, is not conducive to those bits of land being developed anytime soon.

4. Little need for investmentFarming is money intensive. But Farmland

isn’t farming. It rents out the land it owns.As such, there is no ongoing need every

planting season to borrow heavily to buy new equipment, seeds, and fertilizer. Farmland’s tenant farmers are responsible for all of that.

Farmland just collects rental payments and some of the fruits of the bounty. It’s earning farm income without the back-breaking labor.

5. From sea to shining seaFarmers face a lot of challenges, obviously.

Weather, pests, and global/regional crop prices

Global Intelligence Letter 5

can mean the difference between a bumper crop and a nice payday…and a bankrupt farm.

With Farmland REIT, we’re diversified across so many farms, in so many regions, growing so many different crops that we have built in diversification to buffer us from Mother Nature’s whims, and from the ebbs and flows that are natural in every commodities market.

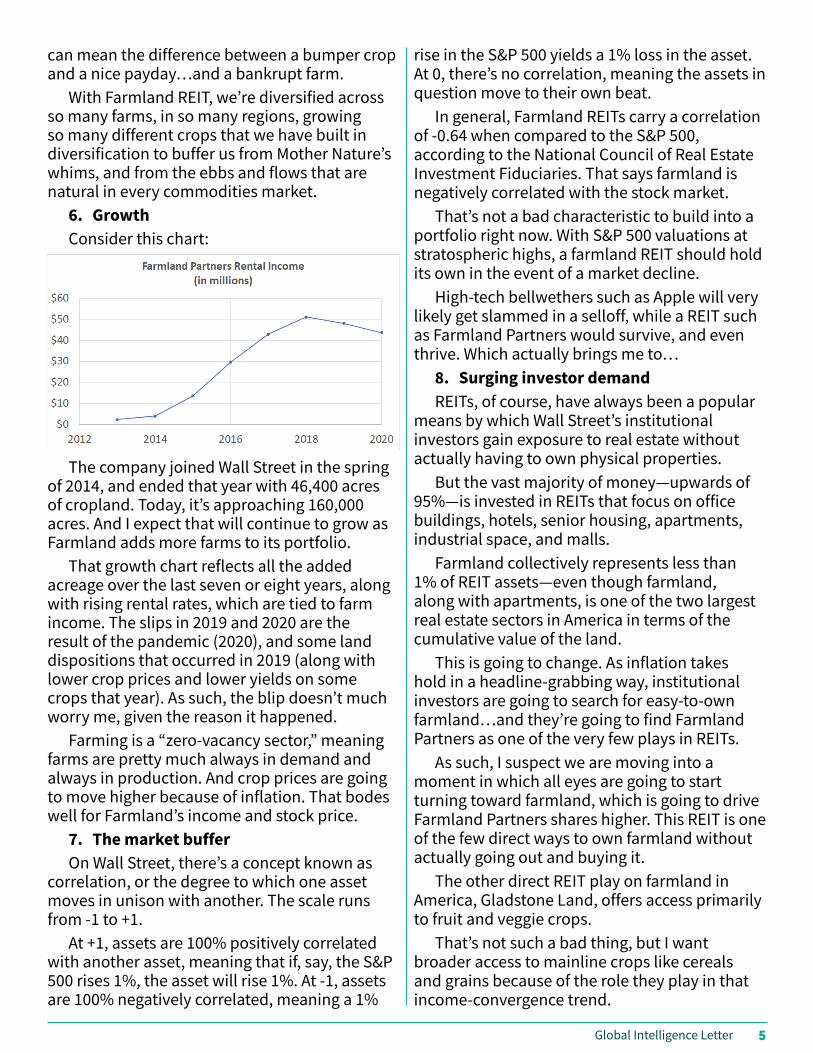

6. GrowthConsider this chart:

The company joined Wall Street in the spring of 2014, and ended that year with 46,400 acres of cropland. Today, it’s approaching 160,000 acres. And I expect that will continue to grow as Farmland adds more farms to its portfolio.

That growth chart reflects all the added acreage over the last seven or eight years, along with rising rental rates, which are tied to farm income. The slips in 2019 and 2020 are the result of the pandemic (2020), and some land dispositions that occurred in 2019 (along with lower crop prices and lower yields on some crops that year). As such, the blip doesn’t much worry me, given the reason it happened.

Farming is a “zero-vacancy sector,” meaning farms are pretty much always in demand and always in production. And crop prices are going to move higher because of inflation. That bodes well for Farmland’s income and stock price.

7. The market bufferOn Wall Street, there’s a concept known as

correlation, or the degree to which one asset moves in unison with another. The scale runs from -1 to +1.

At +1, assets are 100% positively correlated with another asset, meaning that if, say, the S&P 500 rises 1%, the asset will rise 1%. At -1, assets are 100% negatively correlated, meaning a 1%

rise in the S&P 500 yields a 1% loss in the asset. At 0, there’s no correlation, meaning the assets in question move to their own beat.

In general, Farmland REITs carry a correlation of -0.64 when compared to the S&P 500, according to the National Council of Real Estate Investment Fiduciaries. That says farmland is negatively correlated with the stock market.

That’s not a bad characteristic to build into a portfolio right now. With S&P 500 valuations at stratospheric highs, a farmland REIT should hold its own in the event of a market decline.

High-tech bellwethers such as Apple will very likely get slammed in a selloff, while a REIT such as Farmland Partners would survive, and even thrive. Which actually brings me to…

8. Surging investor demandREITs, of course, have always been a popular

means by which Wall Street’s institutional investors gain exposure to real estate without actually having to own physical properties.

But the vast majority of money—upwards of 95%—is invested in REITs that focus on office buildings, hotels, senior housing, apartments, industrial space, and malls.

Farmland collectively represents less than 1% of REIT assets—even though farmland, along with apartments, is one of the two largest real estate sectors in America in terms of the cumulative value of the land.

This is going to change. As inflation takes hold in a headline-grabbing way, institutional investors are going to search for easy-to-own farmland…and they’re going to find Farmland Partners as one of the very few plays in REITs.

As such, I suspect we are moving into a moment in which all eyes are going to start turning toward farmland, which is going to drive Farmland Partners shares higher. This REIT is one of the few direct ways to own farmland without actually going out and buying it.

The other direct REIT play on farmland in America, Gladstone Land, offers access primarily to fruit and veggie crops.

That’s not such a bad thing, but I want broader access to mainline crops like cereals and grains because of the role they play in that income-convergence trend.

October 2021 | Issue 86

My Recommendation: Buy Farmland Partners (FPI) at prices up to $13.

You will find Farmland’s NYSE-listed shares available through every brokerage firm.

When you look up Farmland, you’ll notice that the company’s share price recently experienced a significant dip of about 9% to 10%. That’s because it just converted its Preferred Class B-shares into common stock.

Preferred B shares are different from common shares in that preferred shareholders don’t get a vote, but they are entitled to a dividend. This is usually a specific, set payment every quarter for as long as the preferred stocks exist.

When Farmland issued this separate class of shares some years ago, it included a clause that allowed the company to convert them into shares of common stock at a future date.

Well, in September Farmland executed this clause. And because of the conversion, the price of the common stock dropped. That’s normal. The conversion increased the total amount of common stock by more than 12 million shares, which means there are more shares over which to spread corporate earnings and, more importantly, the quarterly dividend that Farmland pays. There is, however, an upside: The company reduces its cost structure by getting rid of the mandatory dividend it had to pay on those B-shares. That, in turn, is going to sharply increase Farmland’s cash flow. And it will increase what’s known as “available funds from operations,” or AFFO.

This is a REIT-specific metric similar to “net earnings” that companies report every quarter. AFFO is also the pot of money that REITs use to determine their dividend payment.

If you recall the August issue on Slate Grocery, I noted that U.S. REITs, by law, must distribute 90% of their income as a distribution (a dividend) to shareholders. Well, with Farmland’s AFFO rising, we can expect a larger dividend payment going forward.

Right now, the annual dividend is $0.20 per share, or a yield of about 1.7%. It’s not a lot. But I expect we’re going to see that dividend rise because the B-shares are gone, meaning cash that would have gone to those preferred

shareholders will now be available to common stockholders. Some of the cash will, no doubt, also be used to expand the company’s real estate holdings.

All told, then, I think we’re getting into Farmland Partners at a particularly good moment. The shares have come down in price because of the conversion, yet the conversion strengthens the income statement and the balance sheet.

And we’re very likely to see dividend payments escalate—both as a result of the preferred-share conversion, and because of inflation manifesting as improving crop prices. Those higher crop prices, in turn, will flow through to higher rental rates and higher crop income for Farmland over the next few years.

And if we do, indeed, see institutional investors suddenly realize their exposure to farmland isn’t robust enough for the environment ahead (and I think that’s a certainty) we’ll have the best of all worlds working in our favor: a rising share price to go along with our rising dividend payments.

In time, I expect Farmland Partners to top its previous all-time market high of $14.76 per share and approach $15.25, which would mark a roughly 30% increase from current prices. And that doesn’t include whatever dividend payments we collect along the way.

With this trade, I will advise you to set a 20% stop-loss. This is just in case the world goes pear-shaped in weird ways.

The economy could retreat because of new COVID variants that might emerge, or because of White House economic and taxation policies that aren’t looking terribly friendly. So, our 20% stop-loss will give us some protection, just in case.

To set the stop-loss, subtract 20% from your purchase price, and tell your brokerage firm to set the loss there. (So, if you get in at, say, $12, you would set your stop-loss at $9.60—or $12 x 0.8). If the shares decline, your position will automatically liquidate so that you don’t have to monitor it constantly.

Obviously, I am not expecting a 20% selloff. I’m setting the stop-loss out of an abundance of caution. I see a bright future for crop prices, for farmland, and for Farmland Partners.

Global Intelligence Letter 7

We have to start our portfolio assessment with the two big elephants stomping around global stock markets at the moment: the congressional fight over the debt ceiling, and the global worries about a Chinese real estate firm called Evergrande.

For weeks, the GOP threatened to thwart Democrats’ efforts to raise the debt ceiling, an absolute necessity for Uncle Sam. Alas, the GOP has softened—a bit—in recent days. But that just means the debt-ceiling pugilistics have moved to another day later this year.

Either way, the Street is displeased because if Uncle Sam defaults on his debt payments, that would forever destroy that credo about “full faith and credit of the United States government.”

Evergrande, meanwhile, could default on its own debts, which are estimated at a massive $300 billion. This would rip through the Chinese economy, which would flow through the global economy.

Those events are playing through the Global Intelligence portfolio at the moment. One day we’re up, the next we’re backsliding on fear, confusion, and “what if.”

I counsel patience. America had a debt-ceiling moment in 2011. Life was no fun for a couple months on Wall Street, and then stocks started climbing ever-higher once again. And China has experienced real estate issues before. They come…they go. And all returns to normal.

So, I am simply not worried about the long-term effects of these two situations. We just have to tolerate them for the moment. In the meantime, we’re collecting dividends.

Yara International, our Norwegian fertilizer company, put another $1.16 per share into our account in September. With that, we’ve collected $2.3675 in two dividend payments since May—nearly 10% of our original purchase price. That has offset the price weakness we’ve seen in Yara. That weakness is largely tied to dollar strength in the last few months.

In Oslo, Yara’s home market, the shares are down about 4%. In the U.S., our ADRs are down

a bit more than 6%, all because of currency adjustments. Our dividend income has stepped in and covered our paper losses.

As we move past this particular moment in the world (a moment of fear tied to the events I mentioned above and the ongoing pandemic worries), Yara’s share price should turn favorable for us—and our 10% dividends at that point will be a jump start into the green.

We’ve also picked up our first couple of dividends from Slate Grocery, the Canadian firm that generates income from shopping centers across the eastern half of America.

Slate dropped $0.072 per share into our accounts in mid-August and mid-September, for a total of $0.144 thus far. And we’ll continue to receive these payments in our accounts around the 15th or 16th of every month.

There’s also the real prospect that these dividends will rise in the near term. As I mentioned during my Slate analysis in the August issue, the company had reached a deal to acquire a swath of new properties. Well, that $390 million deal closed in September, meaning 25 new properties are now officially part of Slate’s portfolio. And since Slate is legally required to pay to shareholders 90% of its net cash flows, we should start receiving a meatier dividend sometime in the new year.

Finally, I want to quickly address an email I received from a reader who was charged $100 to buy Slate shares because, she was told, it’s a foreign investment. I don’t know what brokerage firm or the process she used (buying online directly, or with the help of a broker), but no one should ever pay $100 these days to trade a stock.

Slate trades on Fidelity for $0 commission. On E-Trade, it’s $6.95. My point here is this: If you’re given a trading fee that exceeds a few dollars, don’t make the trade. Ask your brokerage firm how you can trade the stock more cost effectively. If you’re not given that option, then switch to a low-cost, online brokerage firm (I recommend Fidelity). Seriously: $100 trades went out decades ago. No reason anyone should be paying that today.

Portfolio ReviewThe Two Big Clouds Hanging Over the Global Economy

October 2021 | Issue 88

I’d stopped to take a picture of a row of colorfully painted balconies—these beautifully ornate, 17th-century wood-and-glass protrusions on just about every old property you come across on the Mediterranean island of Malta.

As soon as I snapped the picture, a door opened right behind me. A worker was emerging from an old row house under repair.

I peeked in through the open door to catch a glimpse of ancient glory: an old, shotgun-style townhouse with 12- to 15-foot ceilings, intricately designed plaster columns, gorgeous hand-painted floor tiles from eons ago, and what looked like a quaint, stone courtyard out back.

But the place was a disaster. I mean an unholy mess. As though all 300 years of this townhouse’s heritage had degraded into a pile of debris, crumbling plaster, and desiccated wood.

Yet there was the hint of what it might become…

It seemed like a dream for just about every fixer-upper homeowner/real estate investor on the planet. Which means Malta might just be one of the most unique real estate opportunities I’ve stumbled upon in my global travels over the past 20 years.

Here in this sun-soaked island nation just south of Sicily, there’s an opportunity to create something truly special: a family, real estate heirloom. A piece of history in an old, stone home that has survived for generations, and which will certainly last generations more.

When all is said and done, you’ll have a masterpiece—the kind of architecturally pleasing abode that pops up in magazines for its unique style, and which you will want to pass down to your heirs.

But here at the outset, let me provide fair warning: Malta can be a challenging place when it comes to real estate…and particularly when it comes to this opportunity.

The upside is that once you’ve navigated the process and successfully completed your project, you’ll own a very valuable piece of property in a European location where demand is persistent.

You’ll be able to sell your property for nice gains (doubling or tripling your total investment); live in it for a high-quality, Mediterranean lifestyle; or generate annual returns in the 5% to 8% range as a rental property in a market to which the rest of Europe flocks for a sunny, beachside, island holiday.

The homes I’m talking about are traditional, Maltese row houses.

Some date back centuries; some are much younger. Either way, these are solidly constructed stone houses in town centers on the main island of Malta, and on its sister island to the north, Gozo.

The preponderance of Maltese row homes exists in the main, metro area of Valletta (the capital city), Sliema, and St. Julian’s, where much of the nation’s 500,000 residents live. You’ll also find them in Mdina, a hillside city in

Malta’s Traditional Row Houses: Huge Profit Potential for Investors

Global Intelligence Letter 9

the center of the main island that once served as the country’s medieval capital.

On Gozo, the quaint town of Victoria is littered with traditional Maltese row homes.

That this opportunity exists is due to a mix of history, family dynamics, and the fact that Malta imposes no property taxes.

Here’s how all of that plays out:• History: As noted, many of these row

homes are quite old, and they have passed down through families over decades, often a century or more. Nowadays, numerous family members across multiple generations and branches of a family tree own these houses.

• Family dynamics: Some family members want to sell. Some don’t. Those who do can’t agree on price. So, the easiest option is to bag the argument and come back to it some other time in the future.

• Property taxes: No property tax means no carrying costs. So, arguing family members have no pressing need to sell what costs them nothing to hold.

The upshot of all of this: familial inertia. Far easier to keep the family peace by simply

sitting on an empty property for decades than fight about how to sell it.

“It’s a sad situation, really,” Patrick Xuereb told me. He’s a regional manager with local Frank Salt Real Estate. He and I spent a day touring Malta and its real estate options. “These properties, they’re beautiful. They retain all their former glory. They just need someone who wants to come in” and deal with the process of turning trash into treasure.

Instead, Malta is all but blanketed by construction cranes building anew seemingly everywhere you look.

Since it’s so hard to separate these row houses from generations of owners, builders meet increasing demand for residential property by throwing up new, modern apartment towers.

Nevertheless, you will come across old townhouses and row houses for sale. Some in better shape than others. Some in terrible shape. And it’s readily apparent that there’s a push now to address these abandoned properties.

I spent days walking around Sliema and Valletta and saw an abundance of remodeling underway. I saw far fewer “For Sale” signs, but they certainly exist.

Here’s what you need to know, if this kind of foreign real estate investment appeals to you:The Pros and Cons of Maltese Row Houses

The costs: For the most part, you’re going to spend €250,000 to about €300,000 ($290,000 to $350,000) on a property you wouldn’t let a dog live in. Many really are that dilapidated.

But you’re paying for location and the current owner’s/owners’ recognition of what the property will become. Realize, as well, that the property-tax issue is a huge incentive for sellers to demand what they want or walk away. They’ve got nothing at stake.

You can negotiate on price, but don’t expect a lot of give. Maybe 5%.

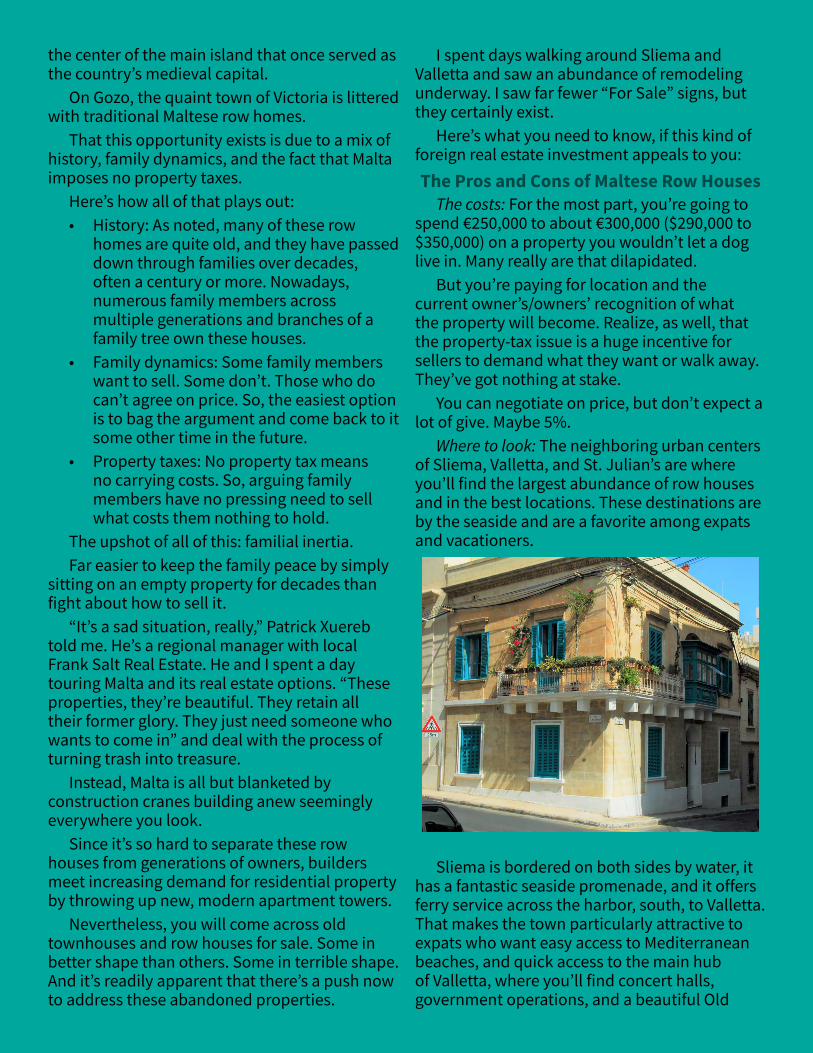

Where to look: The neighboring urban centers of Sliema, Valletta, and St. Julian’s are where you’ll find the largest abundance of row houses and in the best locations. These destinations are by the seaside and are a favorite among expats and vacationers.

A traditional row house in Sliema.

Sliema is bordered on both sides by water, it has a fantastic seaside promenade, and it offers ferry service across the harbor, south, to Valletta. That makes the town particularly attractive to expats who want easy access to Mediterranean beaches, and quick access to the main hub of Valletta, where you’ll find concert halls, government operations, and a beautiful Old

October 2021 | Issue 810

Town packed with shopping, entertainment, and top-notch eateries.

Valletta is less expensive than Sliema—though only slightly.

And just across a second harbor from Valletta are the “Three Fingers” of Senglea, Birgu, and Kalkara. They’re cheaper still, and are much more local and industrial in flavor. But I don’t say “industrial” in a negative way.

These are very appealing areas, and quite pretty in their own right. It’s just that this is where you’ll find working dockyards and such that give the area its industrial ambiance.

As for St. Julian’s, it’s a larger enclave north of Sliema. And while you’ll certainly find row houses there, they seem to be fewer in number because this area is less densely populated.

Still, prices are similar to Sliema because the district is highly walkable, popular with tourists and expats, and offers easy access to beaches and yacht harbors, and an abundance of ethnic restaurants ranging from sushi to Greek to Cuban to an authentic Irish pub.

As I noted above, on Gozo you’re going to largely focus on Victoria, the economic, social, and physical center of the island. But this is only if you want small-town living.

While several hundred thousand people populate the metro area on Malta, Victoria is home to only about 7,000 people.

Still, demand for properties is high because the Maltese love to own property, and many who live on the main island, buy property in Gozo as their weekend/summer getaway—or to rent to tourists.

As such, prices in Gozo, while definitely cheaper, are not cheap. Expect to pay about €200,000 ($232,000) for a fixer-upper row house.

Note that in all of these locations, you are right on the street. And these streets can be infuriatingly narrow and impossible to find parking. That’s an important fact if owning a car is paramount to your lifestyle. (Malta is well served by Uber-like ride-share apps, and the country is so small that you can get around easily and quickly with these.)

Money and mortgages: Malta is a member of the European Union and uses the euro, so it has

a highly stable currency and economy. And, yes, mortgages are available to foreigners through traditional Maltese banks and specialty lenders, though some banks can be reluctant to lend to non-residents. Mortgage rates are in the 3% to 4.5% range at the moment.

You will have to open a local bank account, gain permission from the Central Bank of Malta to buy local property, and you’ll need a life insurance policy.

Some expats tell me that opening a Maltese bank account can be a hassle. Others tell me that if you have an account at a major, global bank in the U.S. such as HSBC, Citi, or Chase, then the hassles are minimal.

If you’re buying a primary residence, you can borrow up to 90% of the value of the property for up to 40 years. If it’s a secondary residence, you can borrow up to 75% of the value for up to 25 years. But be aware that Maltese mortgages often impose a penalty for early repayment.

Remodeling: Unless you are good with your hands and accustomed to working with old, stone properties that are not up to local codes, you will want to hire a contractor.

This might well be the biggest challenge. There’s so much demand for contractors with all the building going on in the country that finding one can take a while. And once you do find one, don’t expect quick results. The remodel will take longer than you expect.

Regardless of where you buy, you can expect to put between $175,000 and $230,000 into the remodel, depending on your tastes, style, and build-out preferences.

All in, you’re going to have between $350,000 and $580,000 in this fixer-upper. But it’s going to be worth €850,000 ($985,000) to well over €1 million ($1.15 million) on the resale market.

Or, you can list it on the rental market and expect to collect between $2,000 and $4,500 per month, depending on location, quality, amenities, size, and all the other rental factors.

Certainly, this isn’t a play for everybody. But for a fan of fixer-uppers who wants to own a foreign property, taking on a Maltese row house can be a profitable opportunity.

Global Intelligence Letter 11

Intel UpdatesChina’s war against crypto reaches its inevitable conclusion. In late September, China’s central bank declared all cryptocurrency-related transactions illegal…marking the country’s biggest move yet in its ongoing crypto crackdown.The reason for this crackdown is the digital yuan. China is rapidly pushing ahead with the development of a central bank digital currency—a digital version of the yuan based on the same blockchain technology as bitcoin and all other cryptos. And the Chinese government doesn’t want any crypto competitors to its new digital sovereign currency.This latest move against crypto caused a significant drop in crypto prices. On Sept. 24, the day China announced the policy, bitcoin fell about 9% from around $45,000 per coin to around $41,000. Ethereum, meanwhile, dropped about 11% from $3,100 to about $2,750.First, let me say, “Yawn…”China has banned crypto in one way or another 20 times in 12 years. How do you say, “Boy who cried wolf” in Mandarin? Bitcoin and crypto have recovered and marched higher every time.Second, I see this latest move as a positive development. Here’s why.This time, the drop in crypto prices was relatively tame, especially when you consider the inherent volatility of the crypto markets. By Sept. 27, prices had largely recovered from this price dip, with bitcoin and Ethereum trading at around $44,000 and $3,100, respectively. (And since then prices have surged higher.) It seems like the market as a whole looked at this latest move by China, and reacted with the same shrug of the shoulders as I did.Plus, now that it’s taken this inevitable step and banned all crypto-related transactions, China has few, if any, cards left to play. For much of this past year, China has been dropping periodic bombs on the crypto market. Now crypto may be able to move beyond this phase of China-inspired turmoil.Crypto prices won’t be stable anytime soon; this asset class is still too new. But China’s

diminishing influence on crypto prices should lead to more long-term stability. And it radically minimizes China’s role in crypto, while opening the world and the technology to other players (i.e., America, if D.C. bureaucrats don’t shoot themselves in the foot first).To be clear, crypto does not need China. Internet giants like Google, Amazon, Facebook, et al. have prospered just fine without access to the Chinese market. And so will crypto.Twitter is rolling out a bitcoin tip jar…but I’d advise against using it.On Sept. 23, Twitter announced a new feature called Tips that will allow users to give and receive one-time payments in bitcoin or money. Tips is designed to give Twitter users a quick and easy way to offer creators a little cash or crypto for their efforts. Initially, the feature is being offered to a select group of influencers, experts, journalists, and nonprofits. The company plans to make it more widely available later. To receive bitcoin through the new feature, Twitter users will be able to add their bitcoin wallet address or a bitcoin Lightning wallet to their account. Cash transfers will be facilitated by third-party apps like Venmo or PayPal.At present, Tips is only available on iOS. Twitter says Android and web versions will follow.While I have no particular objection to this new Tips option, I certainly won’t be using the bitcoin payment option. Bitcoin is an appreciating asset. Since just the start of this year, the crypto is up roughly 80%. The dollar, on the other hand, is losing value amid high inflation and Uncle Sam’s profligate spending.I believe bitcoin will reach six and then seven figures at some point this decade, so frankly, tipping someone in bitcoin is overly generous. If you want to show someone your gratitude on Twitter, I’d stick to the cash option. What this development does show, however, is just how ingrained bitcoin and crypto are becoming in the wider economy.You can still support small businesses when shopping on Amazon. Here’s how.The decline of local mom-and-pop stores over my lifetime has been truly sad to see. That said,

October 2021 | Issue 812

when it comes time to buy something, I still generally opt for the convenience of shopping at Amazon or another big online retailer.However, there are ways you can support small businesses, even when shopping on Amazon. The company operates a Support Small page that features a huge number of products from small and medium-sized businesses. This service is not restricted to U.S. businesses. So, if you want to support local businesses, click on the Shop Local button at the top of the Support Small page and click on your area. Unfortunately, it only allows you to pick a region, say Southeast or Midwest, but it’s a start. If you want to refine your selection to a specific type of owner, you can visit the Meet the Business Owners page. This allows you to sort by a variety of different categories, say “military-family owned” or “women-owned.”Of course, if you shop through this service, you’re still giving Jeff Bezos a cut of whatever you spend. But at least it’s a viable way to support small businesses while retaining the convenience of shopping on Amazon.Sick of getting tons of junk mail through the door? These services want to help.Catalog Choice is a registered nonprofit organization that aims to stop junk mail for good. Simply register for free with the organization. Then you can apply through its website to unsubscribe from specific catalogs, and Catalog Choice will handle the opt-out process on your behalf. It’s also a good idea to sign up with DMA choice. This service, a nonprofit organization from the Data and Marketing Association, charges a nominal fee of $2 for a 10-year registration, but allows you to remove your name from the prospecting lists that direct marketing companies share amongst themselves.Note, however, that using these services will not prevent you from receiving catalogs from businesses that you’ve previously purchased from. If you’re a former customer of a business, you generally have to unsubscribe through that company’s website.To unsubscribe from preapproved credit and insurance offers, try OptOutPrescreen. This service is offered by major credit bureaus

and recommended by the Federal Trade Commission. You can opt out for five years through the website, or mail in a form to opt out permanently.Don’t believe the marketing hype. 5G is not worth the price of admission…yet.For years, the media has been heralding the potential of 5G…the ultra-fast wireless network that’s going to transform how we use the internet. And for years, nothing much has happened. Sure, smartphone companies have been selling us 5G-enabled phones. And wireless networks have been promoting their 5G services. But real-world testing has found these 5G offerings are often little better (and in some cases, actually a little slower) than 4G LTE networks.This is not to say that 5G doesn’t have potential. 5G services and speeds are improving incrementally. And if 5G ultimately delivers on its promise to be 10 times faster than 4G, it will revolutionize all kinds of industries. For instance, it will be crucial for self-driving vehicles.However, for the moment, 5G is more hype than substance.The problem is companies have co-opted 5G as a branding tool, consistently over-promising and underdelivering. Take the example of AT&T, which was displaying a “5Ge” logo on some of its non-5G phones. This “5Ge” label was just marketing nonsense, a cynical way of repackaging 4G LTE.More 5G services are coming on stream, and the marketing hype around 5G is only building, but the reality is that it’s likely to be well into 2022 or beyond before this technology becomes desirable or necessary for ordinary customers. My advice: Don’t feel any pressure to upgrade your current phone or data plan for a 5G alternative. This revolution is still in its infancy.This free app will help you pick the perfect wine.I am a huge fan of wine. I ghostwrote a book on wine as an investment class. I tour vineyards when I can on my trips. And at one point, I had a 600-bottle cellar of high-end French Bordeaux and California cult-cabernets, which I sold at auction after my divorce for somewhere near $80,000.

Global Intelligence Letter 13

That said, the world is filled with a vast array of grape varietals I’ve never heard of and which leave me unsure at restaurants and wine shops. So I venture outside the box, only to be disappointed. That’s the way it goes with wine…unless you start using Vivino.With this free app, available for both Android and iOS, you can scan the label for most wines and get lots of information about them. This includes an average rating and price, which is great for finding out if you’re being overcharged or have found a good deal. Vivino also gives you access to reviews, pairing suggestions, and vintage comparisons. And you can add any wines you like to a My Wines list. For more serious wine drinkers or even wine investors, WineRatings+ is worth a look. Developed by Wine Spectator, the bible of wine rating, the app offers free wine vintage charts. For $2.99 a month, you can also get access to Wine Spectator’s ratings and reviews, including recommendations on whether you should hold on to a particular wine or go ahead and serve it with dinner. Never rent a modem and router from your internet service provider.For the internet to work in your home, you need two pieces of equipment: a modem and a router. The modem is the box that connects the internet to your home network. The router allows all your devices, both wired and wireless, to connect to the internet at once.Internet service providers will generally give you one box that does both jobs. The problem is that some providers rent these boxes to their customers, and the fees can be outrageous, often $10 to $25 per month. You can purchase a combined router and modem for as little as $50. A good option, such as the Motorola MG7700 or the Netgear Nighthawk C7000, will cost in the $150 to $170 range. And setting up these devices is not as difficult as it seems. So, if your internet provider is charging you rent for your router/modem, my advice is to go out and buy your own. You could be in profit after just a few months.

It’s generally accepted wisdom that your metabolism slows as you age…except that now appears to be false.Your metabolism refers to the rate at which your body burns calories. It’s been widely accepted for some time that this rate slows as you age. Now, a new study says this belief is false.The paper, published in Science, looked at data from nearly 6,500 people of all ages and found that resting metabolism holds steady between the ages of 20 and 60. And after age 60, it declines at a rate of less than 1% per year. What this means is that the slowing down we experience as we age is, in fact, related to lifestyle factors. As we get older, we tend to sleep less and be less active. This has the effect of reducing our metabolic rate. However, if we have the ability to slow our rate through inactivity, that means we also have the ability to reverse the decline by living a more active lifestyle.Steps you can take to boost your metabolism, regardless of age, include getting more sleep, eating foods high in protein, remaining active throughout the day, and doing more strength training. Sleep is important for rest and recovery. Eating increases metabolism for a few hours, especially if you eat foods high in protein, since your body uses caloric energy to process nutrients. Strength training such as weight lifting, meanwhile, has been shown as among the most effective exercises when it comes to boosting metabolism. However, it’s less effective if you remain sedentary for long periods, so it’s equally important to get up and do short bouts of high-intensity exercise, like a quick jog or a brisk walk, during the day. Thanks for reading, and here’s to living richer.

Jeff D. OpdykeEditor, Global Intelligence Letter