Embed Size (px)

Citation preview

Journal of Risk and Uncertainty, 12:271-286 (1996) © 1996 Kluwer Academic Publishers

Global Financial Markets, Derivative Securities, and Systemic Risks

MYRON S. SCHOLES* Frank E. Buck Prqlbssor of Finance, Graduate School of Business, Stanford UniversiO; and Principal, Long- Term Capital Management

Abstract

The global use of derivative instruments has grown in importance, because they are less expensive tools for hedging risks and for investing in securities. Because several entities have incurred substantial losses in deriva- tives, leading to bankruptcy in a few cases, and because the size of the derivative market appears so large, legislators and regulators around the world, who have limited information about derivatives, fear that further possible bankruptcies pose a systemic risk to the economy. This fear is unwarranted. Affected entities will continue to make infrastructure investments to support their valuable derivative business, a more beneficial alternative to political solutions.

Key words: systematic risk, derivative securities

Over the last ten to 15 years, we have witnessed an explosive growth in financial inno-

vation and new financial products, many involving derivative contracts. But derivative

contracts are not new. For example, some innovative financial entrepreneur many centuries

ago decided that it was more efficient to store gold and issue currency against the stored

gold. Derivatives are part of the tool kit used by financial intermediaries such as banks,

insurance companies, and investment banks to create myriad new financing mechanisms to facilitate the development of large-scale projects by corporations and other entities on

a global basis. The explosive growth of mutual funds in the U.S. and other investment

programs abroad have provided vehicles for individuals to save either directly on their

own account or indirectly through pension accounts. These vehicles allow individuals not

only to transfer resources through time but also to allocate resources globally. Investors

use derivatives as substitute lower cost alternatives to direct investments. New and inno- vative risk-sharing mechanisms involving derivatives have developed over the last ten

years to allow individuals and corporations to pool risks and to share them efficiently with

other parties. Organized financial markets have experienced growth on a global scale. In

*Presented at the Conference on Social Treatment of Catastrophic Risk, Donald L. Lucas Conference Center, Center for Economic Policy Research, Stanford University, October 22, 1994, and at a conference on Risks and Rewards in Derivative Markets, organized by Insititut de L'F_cole Norma[e Sup6rieure, Paris, March 24, 1995.

272 MYRON S. SCHOLES

the future, markets in developed and developing countries around the world will trade listed futures and options in conjunction with traded bonds, stocks, and commodities. Without the development of markets in standardized contracts, financial institutions could not have developed many of the over-the-counter innovations using derivative contracts. These listed markets provide liquidity to institutions and important price signals to inves- tors and corporations as to how to allocate resources among competing ends.

Derivative contracts play an important role in facilitating financial innovation. Merton (1993) and Sanford (1993), for example, emphasize that a focus on the functions of the financial system will provide a road map to future innovations in financial techniques, services, and products. Financial infrastructures will develop that provide more efficient alternatives to (1) facilitate transactions, (2) supply funding for large-scale projects, (3) transfer savings into the future and across markets, (4) provide for more efficient risk- sharing and risk-pooling mechanisms, and (5) transmit more efficient price signals to market participants. Derivatives are integral to the development of financial intrastructure in all five areas.

Market frictions increase the costs of providing financial services. In a second-best world, transaction costs enter into all financial interactions. These costs include asymmetric-information costs, the hidden-information and action-costs of dealing with other entities. For example, it is costly for an investment bank not only to design a new financial product but also to inform customers that the product provides the stated func- tions and that the price of the product is not too high. This is a hidden-information cost. Moreover, deadweight costs result when investment managers are hired as agents for investors. This is a hidden-action cost.

The successful financial innovators are those that provide financial services at lower friction costs. Although the functions of a financial system have been fairly static over many generations, the costs and faculty to provide these services are dynamic. Derivatives have reduced the coarseness of financial products, doing so at lower costs than alterna- tives.

Miller (1986), (1992) argues that all financial innovation results from a desire to miti- gate the effects of regulations, be they tax rules, accounting rules, or regulatory frictions imposed by government entities. Reducing the import of other frictions, however, plays a large role in fostering new financial innovations. Miller could be correct, however, if in a second-best world, regulations and frictions are not separable because inefficient regula- tions arise from other frictions.

Institutions change while financial functions remain stable. The development of effi- cient intrastructure necessarily follows from the functions of a financial system--a need to satisfy investor and corporate demands for products and services--not from a need to preserve particular institutions. The financial functions define institutional change. More- over, the functional approach is relatively culture free. Investors and institutions have the same demand for financial services and products around the world.

Telecommunications and computing technology have created more efficient channels through which entities can provide financial services. These new channels reduce the importance of particular financial institutions. As Sanford (1993) has argued, even without further technological advances, current computing and telecommunications technologies

GLOBAL FINANCIAL MARKETS. DERIVATIVE SECURITIES. AND SYSTEMIC RISKS 273

can completely transform the intrastructure through which financial institutions provide services in the next two decades. Further reduction of frictions and restrictions will enable investors and corporations to transact, to save, to shift and pool risks, and to reduce information asymmetries more efficiently. Although today's institutions will survive, the form in which they provide services will change dramatically.

We have emphasized the physiological view of derivatives: they reduce market frictions by providing innovative products and services at lower cost. There are those, however, who only stress the pathological view of derivatives. In particular, there has been great concern in Congress about the over-the-counter derivative market frequented by large banks, investment banks, corporations, investment companies, and other large financial entities. In the over-the-counter market (OTC), private derivative contracts are written between counterparties: they are not traded on a exchange such as a futures or options exchange. In recent years, there have been many studies of the OTC market and the implications of the growth of derivative contracts, as well as the potential pathologies in using them. These include studies by the Bank for International Settlements, the Bank of England, the Group of Thirty, the Office of the U.S. Comptroller of the Currency, the Commodity Futures Trading Commission, and, most recently, the U.S. Government Accounting Office (GAO).

The GAO report concludes that there is concern that OTC derivative contracts do pose a systemic risk to financial markets.~ It raises the possibility that a default on its coun- terparty obligations by a major dealer of OTC derivatives could result in spillover effects that might "close down" OTC markets, with possible serious consequences to the financial system. In response to the report, Congressman Edward Markey (D. Mass.) proposed legislation in 1994 that would regulate OTC derivative dealers, requiring among other things additional capital requirements. In addition, Congressman Henry Gonzales (D. Texas) and Congressman Jim Leach (R. Iowa) introduced a bill in 1994, resurrected by Mr. Leach in 1995, that directs the federal banking agencies to establish capital rules, accounting, disclosure, and examination standards for financial institutions using deriva- tives. The bill also requires that U.S. bank regulatory agencies coordinate with their counterparty agencies around the world to develop comparable supervisory standards.

Although OTC derivatives have not caused any systemic risk event, such incidents as the loss of over $1 billion by Metallgesellschaft, $1.5 billion by Shell Sekiyu, $1.4 billion by Kashima Oil, $157 million by Proctor & Gamble, $113 million by Air Products and Chemicals, and $19.7 million by Gibson Greeting have fueled concerns of possible sys- temic risk problems. The collapse of Barings, with its loss of over $1 billion caused by a rogue futures trader in Singapore, and other nonderivative (but leverage-related) losses in Orange County, California have heightened concern that there is too much innovation in derivatives and other new financial structures.

The objective here is to examine the pathologies that could cause Systemic failures due to the explosive growth of the use of OTC derivatives in the last few years. Edwards (1994) argues that it is almost impossible that OTC derivatives could cause a systemic crisis. Edwards analyzes the possibility of a "financial meltdown" along the following lines: An initial shock causes a large end user to fail. This causes a large dealer to fail, spilling over and causing other dealers to have large credit problems. If some of these

274 M Y R O N S. S C H O L E S

dealers are banks, this could create a loss of confidence, causing bank runs and bank failures. As confidence deteriorates, markets become less liquid, causing price breaks and forced liquidations of securities by investors and corporations around the world. These price breaks have real effects on the economy, causing large reductions in real output.

1. Derivative contracts: many substitutes but for transaction costs

A derivative is an instrument whose payoff depends on the performance of an underlying asset, index, or security. The payoff pattern can linearly depend on the performance of the underlying asset, as in the case of a futures or a forward contract. The payoff pattern can be nonlinear, as in the case of an option contract.

1.1. Alternative ways to invest in contractuals: the building blocks

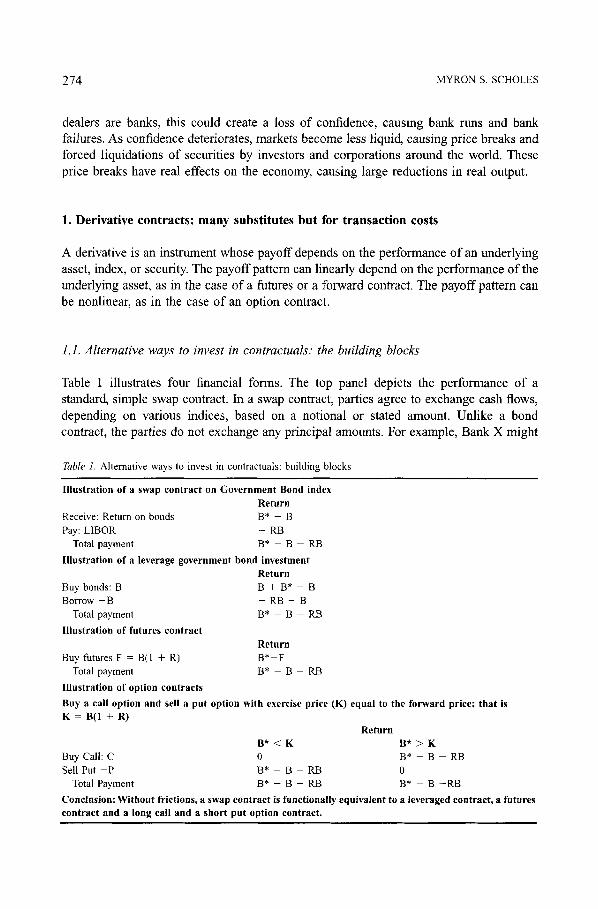

Table 1 illustrates four financial forms. The top panel depicts the performance of a standard, simple swap contract. In a swap contract, parties agree to exchange cash flows, depending on various indices, based on a notional or stated amount. Unlike a bond contract, the parties do not exchange any principal amounts. For example, Bank X might

Table 1. Alterna t ive ways to invest in contractuals : bu i ld ing blocks

Illustration of a swap contract on Government Bond index Return

Receive: Return on bonds B* - B

Pay: L1BOR - RB

Total payment B* - B - RB

I l l u s t r a t i o n o f a leverage government bond investment Return

Buy bonds: B B + B* - B

Bor row - B - RB - B

Total payment B* - B - RB

Illustration of futures contract

Buy futures F = B(1 + R)

Total payment

Illustration of option contracts

Return B * - F

B * - B - R B

Buy a call option and sell a put option with exercise price (K) equal to the forward price; that is K = B(1 + R)

Return B* < K B* > K

Buy Call : C 0 B* - B - R B

Sell Put - P B* - B - RB 0

Total Payment B* - B - RB B* - B - R B

Conclusion: Without frictions, a swap contract is functionally equivalent to a leveraged contract, a futures contract and a long call and a short put option contract.

GLOBAL FINANCIAL MARKETS, DERIVATIVE SECURITIES, AND SYSTEMIC RISKS 275

agree to pay Corporation Z a floating rate of interest based on LIBOR (the London Interbank Offering Rate in dollars, R) on a $100-million notional amount, while Corpo- ration Z, in turn, agrees to pay Bank X a fixed rate of interest on the same notional amount periodically for a set number of years. I f the floating rate exceeds the fixed rate, when a cash flow should be exchanged, Bank X makes a payment to Corporation Z. For example, if at the end of the year, the floating rate is 7% and the fixed rate is 6%, the bank pays the corporation $1 million or 1% of $100 million.

In the top panel of table 1, one party agrees to receive the change in value of a total-return Government Bond Index (such as a discount bond), B* - B on a notional amount B, and to pay at the LIBOR rate, R, on the same notional amount. If B* - B - RB is positive, the index has appreciated by more than RB, and the party agreeing to receive the return on bonds receives the payment. I f B* - B - RB is negative, that party must make this payment to the counterparty paying the return on bonds.

The second panel depicts a more conventional debt contract. An entity buys long-term bonds (for illustrative purposes, a zero-coupon bond) and finances its position. This is called a repurchase agreement. Although the illustration assumes that the borrower can attain financing of the entire position, in reality, financial intermediaries that finance these government bond positions require borrowers to post and maintain capital of approxi- mately 2% to guard against default. The bond buyer realizes gain or loss on the bond position and must repay the loan at the end of the period. The net payment received is B*

B - RB, exactly the same as for the swap contract. The third panel illustrates the investment returns from buying futures contacts on the

total-return Government Bond Index. To prevent arbitrage, the futures price, F, generally sells above the spot price of a commodity by an amount equal to interest on the notional amount but minus the present value of any carrying charges on the underlying instrument. Since, in this illustration, the underlying instrument has no carrying charges--the Index does not pay coupons--the futures price, F, will be equal to the current spot price of the Index B, multiplied by one plus the interest rate. 2 The return on the futures contract is equal to B* - B - RB, the same return as the swap and financed bond position.

The final panel illustrates the investment returns available from buying call options and selling put options on the total-return Government Bond Index. The exercise price, K, was selected to be the forward price of the underlying bond index to illustrate that the swap contract, financed bond position, futures contract, and options position can provide in- vestors with exactly the same total payoff pattern. I f B* - K is greater than zero, the call option will be exercised, and the put option will expire unexercised. If B* - K is less than zero, the put option will be exercised, and the call option will expire unexercised. Buying the call and selling the put is equivalent to holding a financed-bond position as in panel tWO.

Economically, these alternatives provide functionally equivalent payoffs in a world without frictions. In this world, there would be no need for swap contracts and futures contracts. Investors could participate in the returns on the bond index by either buying or selling a financed-bond position. 3 Option contracts are created to provide nonlinear payoff patterns. As Black and Scholes (1973) demonstrated, however, investors can create their own option by using financed-bond positions.

276 MYRON S. SCHOLES

Once we move to the world of frictions, each of these contracts plays an important role in financial innovation. The swap or forward market is generally an over-the-counter market frequented by large financial institutions such as banks, investment dealers, insur- ance companies, and corporations. Here dealers fashion contracts that contain combina- tions of options and forwards to suit a counterparty's particular needs. Most likely, the contractual terms are idiosyncratic. Since the contract is tailored to meet client demand, the dealer acts as a principal and acquires the other side of the contract. Dealers, however, want to mitigate general market risks. For example, they prefer to hedge the risk associ- ated with a change in the value of the underlying bond index, a risk for which they had no comparative advantage. The dealer's risk of entering into a particular contract is partially offset by the risks of other contracts in the dealer's portfolio. Most dealers, however, enter the underlying market to hedge a large part of the remaining risks. The dealer might sell or buy bonds, futures, or options to hedge the systematic risks inherent in the client's contract.

To stay competitive, the dealer is forced to select the least costly among the various alternatives to hedge the cash flows on particular contracts. With well-functioning financ- ing markets, futures markets, and options markets, dealers can provide idiosyncratic contracts to corporations and investors at lower cost than in the absence of these markets.

Dealers use the standard-form contracts in listed futures and options markets to hedge parts of the risk of these idiosyncratic contracts. It is often too costly for dealers to hedge all of the contract risks. They retain some risk, so-called "basic risk". Although corpora- tions and investors cover the dealers' costs to fashion these contracts, the dealers provide the payoff patterns at lower cost, using derivative and other instruments rather than just using older well-known financial instruments.

The put-call relationship in the last panel of table 1 brings out another important point about swap, financed bonds, and futures contracts. The buyer of a call option must rely on the seller of the call option to fulfill the obligation to pay the difference between the market price and the exercise price in the event that the buyer exercises the option. The buyer assumes the seller's credit risk. The buyer of options is exposed to the possibility of a seller's default on the contract. The seller, however, is not worried about the default risk of the buyer, since the option is the buyer's asset in the event of the buyer's bank- ruptcy.

Although these contracts are zero-investment contracts at inception--no money is ex- changed-their value does change as the underlying asset value changes, because the options are only settled periodically. Since these contracts involve the sale of put options, in addition to the purchase of call options, each party is exposed to the other's credit risk. As the value of the bond index increases, the call option becomes more valuable and the put option less valuable. As a result, the receiver of the returns on the bond index has a receivable and is exposed to the credit risk of the writer of the call (the entity paying the return on bonds). As the value of the bond index falls, the put option becomes more valuable, and the call becomes less valuable; the receiver of the returns on the bond index owes money on the contract. The magnitude of the credit risk has swung in the other direction.

It has become common practice to advertise the size of the market in these derivative contracts in terms of the notional amount outstanding. Fortune (March 7, 1994) and the

GLOBAL FINANCIAL MARKETS, DERIVATIVE SECURITIES, AND SYSTEMIC RISKS 277

General Accounting Office (1994) indicate that the size of the derivative market exceeds $15 trillion of notional amount outstanding. The notional amount, however, provides a meaningless estimate of market size. Although Chemical Bank and Bankers Trust each have over $2 trillion of outstanding notional contracts, this figure gives no indication of their credit exposure. The cash-settled value of their receivables is probably less than 3% of these stated amounts. (Remember that the dealer in swap contracts does not stand to lose the value of the principal in the event of bankruptcy, as is the case with a standard- debt contract.)

2. The case for OTC derivatives and systemic risk

2.1. The tools for a meltdown: sophisticated contracts and unsophisticated counterparties

Some clues as to what might cause a market meltdown became apparent from the de- scription of derivative contracts and related securities. First, these contracts are sophisti- cated and difficult for many including government officials to understand. Second, they provide easy access to leveraged returns on underlying structures. Aggressive sales staffs might induce corporate treasurers at many different entities to enter into highly leveraged OTC-derivative contracts whose adverse performance depends on the same economic factors. These treasurers might not understand the inherent risk in these OTC contracts. Moreover, the senior managers of major financial institutions may not understand either the extent of the risk or the types of contracts that their sales force is selling to end users.

Compensation systems, based generally on year-to-year performance, encourage derivative-sales personnel to sell more complicated contracts with higher profit margins, because they are less transparent to end users. Since these contracts are not standardized, and sometimes deemed to be proprietary, end users must rely on the investment bank not only to price these contracts but also for periodic future evaluations prior to maturity. Corporate treasurers have little, if any, modeling capabilities, but generally have a view as to the future direction of systematic market factors such as interest rates or currency prices. This sets the stage for them to buy overpriced and risky derivative contracts

Although, in some cases, it may take years for actual profits to be realized on these contracts, financial institutions record the present value of their anticipated future hedged cash flows as profits in the current year. As a result, only unanticipated hedging gains or losses affect profits in any future year.

This accounting treatment is theoretically correct if valuation models provide unbiased estimates of the actual economic profit. This implies that all systematic factors are priced or that the hedging models provide unbiased hedging strategies. Systematic errors could distort current profits and current estimates of risk.

Systematic pricing errors encourage the sales force to sell more complicated contracts with apparent, but nonexistent, high profits. Some firms compete by selling similar but differentiated contracts. Other firms, however, will not sell these contracts, because their

278 MYRON S. SCHOLES

models show less or no profit at the prices quoted by competitors. When pricing errors are uncovered in the future, the initiating institutions incur losses. Previously benefiting em- ployees may no longer be employed at the firm, nor do they often return any previous compensation overpayments to their employer. The compensation system encourages em- ployees to sell contracts with the highest appearing profit margins.

In general, the more complicated and less transparent contracts are sold to a bimodal group: either to sophisticated counterparties, who view the contracts as being underpriced and profit at the expense of the financial institution, or to unsophisticated counterparties, who must rely on the institution for pricing and future valuations but who have definite views on market directions.

The short-term view of the sales force and contract designers may differ from the long-term view of more senior managers. Young traders have no market history and little long-term capital with their institution. The explosive growth of these markets over the last few years has encouraged many young and inexperienced traders to enter the business. Moreover, senior management might not be able to control the sales force in a period of explosive growth and change. They might not be able to deduce whether profits are real or long-term. This information asyrmnetry causes senior management not to reign in a sales force that is producing high reported profits.

One could claim that the short-term view, the leverage in these contracts, and the generally unsophisticated nature of buyers and issuers set the stage for a market melt- down. Many unsophisticated counterparties enter into these high-powered contracts. Many counterparties might fail as a result of a random exogenous large change in interest rates, currency prices, or equity prices around the world. This could then lead to a further meltdown and system failure in the absence of government intervention.

Although this is a possible scenario, it is highly unlikely that speculating on market directions using leveraged-derivative contracts would cause widespread failures and lead to a market meltdown. For every buyer of these contracts, there is a seller. Not all can be losers. Moreover, not every treasurer, employing derivative contracts to take a leveraged- directional speculation, has the same view of markets. Obviously, if everyone had the same view, market prices would already have changed to reflect these views. Therefore, it is likely that only a few firms would fail (while others profit) on large underlying price moves representing only a small fraction of the value of assets in the economy. Moreover, not all institutions are on the same side of the market, or offer the same contracts to investors. There is diversity in contract offerings and specifications. In addition, derivative contracts are only one of the mechanisims for corporations, investors, and institutions for taking views on market directions. Diversity might even reduce the possibility of a market meltdown. A failure of several firms might affect the underlying markets, the futures market, or the derivative market. With multiple markets there is less pressure on any one of these alternative markets. On the other hand, without these alternative channels, the pressure of several failures of corporations or financial institutions might be more intense.

GLOBAL FINANCIAL MARKETS, DERIVATIVE SECURITIES, AND SYSTEMIC RISKS 279

2.2. Other potential pathologies that could lead to market failures and systemic risk

In general, financial institutions hedge the systematic risks associated with the derivative contracts that they sell to counterparties. Some would claim that, because hedging is far from an exact science, many financial institutions that improperly hedge could fail simul- taneously, leading to a market meltdown and systemic risk. Developing models to under- stand and to hedge risks is costly and, as a result, the models are inexact. Moreover, the transaction costs to hedge all of the systematic factors in many markets may be quite large. Given the economic tradeoffs, many institutions do not hedge all of the underlying systematic risks of the contracts. To hedge the risks of a sophisticated contract might require that the institution estimate variances, covariances, and the number of systematic factors on many securities around the world. If financial institutions do not have models to estimate the sensitivity of their profits to changes in market factors, or to adverse outcomes, or if the models are incomplete, multiple adverse outcomes in the bond or equity markets could cause many financial institutions to suffer large losses and fail all at the same time, leading to a market meltdown. This is particularly true for those financial institutions that do not allocate or reserve sufficient contingent capital to carry risky positions in the derivative markets. Moreover, the risk-control systems within financial institutions are rudimentary and evolutionary. Their structure and inputs do not change with changes in market conditions. A financial institution could have large but unknown and little appreciated risks that are not apparent to senior management and outside audi- tors. This sets the stage for the failure of many organizations, in particular, when the unknown risks are common across many financial institutions.

The arguments for a market meltdown apply not only to financial institutions issuing derivative contracts, but also to institutions issuing mortgages, buying less-developed country bonds, or making corporate loans or engaging in any other financial contract. With market shocks, financial firms will fail if the change in value of their liabilities is not highly correlated with the change in the value of their assets, and the level of capital is insufficient to cushion adverse market moves that dramatically reduce the value of their assets and/or increase the value of their liabilities. The question as to whether many financial institutions have similar large asset or liability concentrations on the same side of the market in derivatives, or whether asset or liability risks are not hedged, or whether risk capital is insufficient to cover derivative losses, cannot be answered without empirical evidence. But, even if the stage is set for many failures, it is not clear that this would lead to market meltdown or systemic risk. From the evidence presented in Swaps magazine, and other industry newsletters, as well as from Government studies, financial institutions around the world differ widely in their derivative exposures. Some concentrate in cross- currency forwards and options, some in common bond swaps and options, some in short- term swaps, some in equity swaps and options, depending on their expertise and the needs of their customer base. Some concentrate in matched-book, low-risk trades, while others undertake more exotic forward and options trades. The derivative books are quite hetero- geneous.

Lack of liquidity or depth in markets can lead to the failure of financial institutions. OTC-derivative contracts are illiquid. There is not a developed secondary market for these

280 MYRON S. SCHOLES

derivatives, and it is virtually impossible to remarket esoteric derivative contracts, let alone to do so over a short time period. In pricing OTC-derivative contracts, financial institutions must reserve capital or suffer large losses if forced to liquidate their positions over a short period of time. That is, if the markets are illiquid, market-price spreads are likely to increase dramatically when many dealers are trying to reduce the size of their positions and all are on the same side of the market. When losses reduce capital levels, financial institutions are forced to shrink the level of their operations. With reduced assets to support their liabilities, their capital risk would be too great: the risk level could jeopardize the survival of the financial institution.

Moreover, many of these institutions use short-term financing to acquire illiquid assets. When entity risks increase, they might not be able to maintain their level of short-term financing. It is difficult for outsiders to assess the risk of an opaque financial institution. It could become too costly to price their short-term liabilities. This will force the financial institution to not only reduce its reliance on short-term financing but also will cause it to reduce the size of its balance sheet. But, because it is very expensive to liquidate their derivative-contract positions (and other illiquid positions), many financial institutions would tend to liquidate their most liquid assets first to reduce the size of their balance sheet. Perversely, the liquid assets are also most likely to be their hedge positions. The sale of these positions exacerbates the risk of their remaining capital. Moreover, firms might be forced to liquidate their illiquid positions and suffer large losses in so doing. As a result of these large friction costs, an adverse market move could result in many failures of undercapitalized financial firms. This sets the stage for a market meltdown.

The above discussion could apply equally as well to illiquid loans to small business enterprises, illiquid mortgage contracts, less-developed country direct loans, and currency and bond trading positions. Financial institutions make money, in part, by providing liquidity. There have been many large discontinuous price moves in markets in the last ten years that have not caused massive failures. There have been large currency, stock market, real estate and interest rate moves in Japan in the last four years. There were large jumps in asset and currency prices in Mexico and South America in 1994 and 1995. Europe suffered large currency price changes in 1991, resulting in an effective collapse of cur- rency bands. There is no empirical evidence that differentiates derivative contracts from these other illiquid positions.

To the extent, however, that financial institutions and corporations use derivative con- tracts to hedge or to share the risks more broadly throughout the economy by using derivative contracts, the risk in the financial system might be less concentrated. Their risk capital is less volatile. In effect, derivatives allow for the provision of more risk capital by outsiders at less cost than does direct equity issuance. Derivative contracts that are used to hedge commitments are more targeted and less opaque than unrestricted equity issues.

Some have argued that the credit risk of derivatives could lead to defaults, which would cause failures and market meltdown. Counterparties can default on OTC-derivative con- tracts. Many corporate counterparties lack the facility to post the collateral or mark their derivative contracts to market. In fact, one reason for the explosive growth in OTC- derivative contracts has been that corporations do not have the facility to post the intra-day margin on futures or options contracts as required by the futures and options exchanges.

GLOBAL FINANCIAL MARKETS, DERIVATIVE SECURITIES, AND SYSTEMIC RISKS 281

These entities undertake a similar OTC contract with a financial institution, which hedges its commitment to the corporation by offsetting its liability in the futures or options market. In effect, for a fee, the financial institution posts collateral for the corporation.

This creates two potential problems for a financial institution. First, it may be required to post margin against its futures or options contracts when it does not have offsetting cash flow from the futures contract. It will need to rely on financial market issues to provide the capital. This mismatch, presumably, was part of the cause of the downfall of Metallge- sellschaft: it had to post large sums to carry its exchange-traded contracts. Second, at the same time, the financial institution will be exposed to the credit risk of its counterparty (as discussed in the options example in table 1). If hedged, the financial institution will have an offsetting OTC contract that has substantial unrealized value except for credit risk. The opposite would be true if the financial entity generated cash flow. Its counterparty would be exposed to its credit risk. Although entities are not exposed to default risk on the notional amount of the derivative contract, as they would be on the principal on a parallel loan (the leveraged-financing example in table 1), the credit exposures could become very large. With large credit exposures, failure of several large corporations could cause fi- nancial institutions to fail; or a failure of several financial entities could cause corpora- tions to fail; or a combination of both could cause massive other failures. Once again, default risk is not unique to derivative contracts. The default risk in a derivative contract, however, is far less than that for an outright loan, since the derivative contract does not have the risk of less than full repayment of principal on default.

Another pathology that sets the stage for systemic failures is that of operational risks and controls. If OTC-derivative dealers have not build the correct operational controls into their respective organizations, adverse market price movements could expose previously unknown problems, possibly across many firms, which could lead to large losses and cause failures of many organizations. Internal controls and an adequate accounting system are necessary to operate and to pass the correct information on to external accountants. Pathologies do occur (for example, the Kidder Peabody fictitious income generated by it head bond trader, Joseph Jett).

3. Causes of systemic risk

The first cause of systemic risk is behavioral. Essentially this is the bank-run phenom- enon. A scare causes a panic that spreads widely among many entities. For example, the losses incurred by a bank-derivative dealer make the market believe that the bank wilt fail. This causes runs on this and other banks that have large OTC-derivative positions, leading to widespread collapse of the system. As discussed, this is unlikely to apply to the derivatives market.

The second cause of systemic risk is a structural failure. In some unknown way, the financial infrastructure is flawed. A breakdown in the system causes widespread failure. For example, a large derivatives dealer's record keeping is flawed, causing it and others to default. The concentration of a large amount of the OTC derivatives in a few large banks, as reported by the GAO, could make the problem even worse. Yet the concentration is

282 MYRON S. SCHOLES

based on notional amounts, not on the liquidation value of the contracts. In addition, OTC-derivative dealers are in far different derivative businesses; they are not homoge- neous. But, as discussed, this is an unlikely cause of systemic risk in the derivatives market.

Another risk that could lead to a systemic problem is innovation risk. Innovations could be so numerous and so large that the volume of transactions could be too large for the financial infrastructure to handle. Since there are huge costs to build financial infrastruc- ture, the system could be quite weak in a fast-growth, diverse-product environment. In a dynamic environment, change leads to system weaknesses. These are natural forces. Industry participants and external monitors, however, act to protect their business fran- chises.

In general, innovators are faster than infrastructure builders in the financial markets. Innovation in OTC-derivative contracts has been extensive, and the market has exploded in size. Economics suggests that innovators use existing infrastructures to build prototype products. It is most likely that only after innovators anticipate that new products will be successful is infrastructure built to support the business. With explosive growth, it is in this initial phase that the system is the weakest.

It is for this reason that we might have seen the breakdowns in the last several years. But, even with the reported losses, there have been relatively few failures. With the explosive growth in the market, we might have anticipated even more failures and losses.

To preserve their business, entities are building the infrastructure to control and under- stand the risks in the OTC-derivative business. This has lead their normal support groups such as accountants, lawyers, software providers, consultants, and regulators to become deeply involved in the process. Without these controls, internal management and external regulators will curtail the growth of the market. Whole teams at accounting firms are devoting resources to building controls and educating management and regulators about OTC derivatives. Legal forms and institutions are adapting to the new environment. There is more understanding of OTC-derivative contracts by senior managers at financial insti- tutions and at corporations, including members of the boards of directors; there are more risk controls and systems being put into place; more resources are being used to effect operational controls; there have been clear responses to credit risk; and standards are being set for dealing with unsophisticated counterparties.

Another cause of systemic risk is unanticipated changes in regulatory, legislative, legal, and other rules, which cause dislocations in the very markets that the rules are deemed to benefit. Many OTC derivatives are long-dated contracts. Regulatory rules might change (see proposed bills in Congress), causing markets to collapse. Specific derivative contracts could become illegal to issue. Prior contractual arrangements could be deemed invalid. The nature of prior contracts could be changed by the courts and legislators. For example, with losses, many entities (in particular, state entities) claim that they did not understand the nature of the risk in a contract and ask that their initial investment be deemed invalid. Various states in the U.S. have bills pending that would make it inappropriate for state entities to use derivative contracts in their investment activities.

More restrictive regulatory rules in the derivative markets might destroy well- functioning markets. This would destroy market liquidity. Derivative dealers could incur

GLOBAL FINANCIAL MARKETS, DERIVATIVE SECURITIES, AND SYSTEMIC RISKS 283

large losses in the event that these markets were made less liquid through regulations. Reduced liquidity limits the use of hedging. This increases dealers' exposure to market risk, which in turn, could lead to unanticipated losses, and potential dealer failures. Moreover, the business would become less attractive and financial institutions would fail to attract and keep the most talented personnel. Managing an existing book of business might become more difficult.

Regulatory rigidities also create the potential for pathological outcomes. For example, the first pass at global capital requirements for financial institutions--the Bank for Inter- national Settlement bank-capital-adequacy requirements--is based on rigid and somewhat arbitrary standards, which induce banks to enter into swap and other OTC-derivative contracts, instead of acquiring the underlying assets.

3. Regulation and financial infrastructure

Technological improvements have reduced the costs to control risks. More tools to un- derstand derivatives and to price risk have become available to investors, corporate man- agers, investment intermediaries, accountants, lawyers, rating agencies, and other. Finan- cial institutions have developed sophisticated risk-management reports and controls to manage risk. Accountants have become more familiar with control problems associated with derivatives. The rating agencies have increased their understanding of derivative instruments through their rating of structured bonds, collateralized mortgage obligations, contingent corporate debt, and myriad other contracts. Tax and corporate lawyers have become involved in the structuring of derivative contracts. In general, users of derivatives have become better educated.

As the market broadens, costs of using these instruments fall. More investors under- stand how to value and use them in their global activities. Investment intermediaries convert contracts from one form into another to satisfy demands. For them, the costs to produce these contracts fall as futures and options markets develop worldwide.

The press, the public, and regulators fear derivatives, because they are new and com- plex. Although pervasive and growing, derivatives are still mysterious to the general public. Because of the uncertainties associated with new infrastructure, there are regula- tory uncertainties. Regulators worry whether investors, corporations, banks, and other entities know now to price and hedge risks. They worry about their own political expo- sures to failures and to market disruptions.

Unfortunately, regulators and legislators around the world are prone to concentrate almost exclusively on systemic risk. Their focus should be on building the proper infra- structure to support the evolving nature of derivatives and other financial contracts. With this focus, regulators could encourage and help to coordinate the development. The in- frastructure is being built. If governments concentrate only on systemic risk issues and write new rules to address this question, they might create disruptive effects. There may be severe limits to the role of governments in the evolving global financial arena.

We have illustrated the substitutability of many contracts. But, for market frictions, there are many alternatives that provide the same functionality to investors (for example,

284 MYRON S. SCHOLES

those described in table 1). Measuring systemic risk induced by particular financial in- novations is only appropriate relative to the next best alternative. With many substitutes, the risk is greatly reduced that any one vehicle, for example, OTC derivatives, can cause widespread market failures.

There is an important concern associated with the changing financial infrastructure. The speed of institutional change has increased in recent years. As new financial innovations have succeeded, regulatory conventions have become obsolete, or lagged behind the new innovations. New finance does not easily fit into the old regulatory boxes. Tax laws have been strained. The definitions of securities and contracts have been tangled. The role of the various regulatory bodies has been changing.

Because of the dynamics of innovation, it has become very difficult for Congress to draft specific rules to regulate institutions. The half-life of the regulations is very short. As a result, regulators must rely more on the industry that is motivated by their own self- interest to provide the appropriate economic level of risk controls and management.

A whole new system of risk accounting must be developed. Current accounting systems concentrate on static valuations. Swaps, foreign exchange contracts, and other OTC de- rivatives have no initial value. As a result, they are "off balance sheet." There is no place for them in the current accounting world. The economic balance sheets of financial firms and corporations are dynamic. Financial instruments alter the risk characteristics of eco- nomic balance sheets and do have value. Regulators can encourage the accounting pro- fession to develop a dynamic accounting system with a focus on risk exposures--on how the balance sheet changes in response to various risk exposures such as interest rate movements, currency price movements, and commodity price movements. If the regula- tory response to systemic risk, however, is to require more reporting, the outcome might be bad. More information is not necessarily good. It might divert attention from the long-term need to develop a more dynamic accounting system.

Systemic risk is not well understood. What is the cost to taxpayers? Who should stand by to reduce systemic risk if not government agencies? If there is a chain reaction of some sort that leads to potential defaults, the government should provide liquidity to the system. What is the externality? The externality is that market chaos causes many bankruptcies and destroys valuable infrastructure that is costly to rebuild. The argument goes as fol- lows: I f market participants had had more time to sort out and incorporate information into new valuations, prices would rebound, and society could have prevented these bank- ruptcies, avoiding their consequential deadweight costs. On the other hand, even after the time needed to assess information has passed, if market prices do not rebound, entities will fail at no further deadweight cost to society.

The regulatory agencies can supply liquidity on a secured basis to financial entities for the short period needed to assess market conditions. By providing only short-term secured financing, governments do not create incentives for institutions to undertake activities that are essentially subsidized by taxpayers; for example, certain banks are deemed to be "too big to fail." With secured financing, the loss, if any, resides with the stockholders of the financial entity. Although the government might suffer some loss if the value of its collateral falls or if it was overvalued in the first place, there may not be less expensive

GLOBAL FINANCIAL MARKETS, DERIVATIVE SECURITIES, AND SYSTEMIC RISKS 285

alternatives unless the government can enter into risk-sharing arrangements with financial entities.

Specific financial contracts do not necessarily increase systemic risk to the system. As we have seen, new innovations reduce the costs of providing financial services. As insti- tutions develop many more ways to provide financial services to different entities more efficiently, no one mechanism has as large an impact on the global market in financial services. As a result, we reduce systemic risk by reducing the import of any one mecha- nism in the provision of financial services. The regulatory agenda should not concentrate on OTC derivatives. The policy should be comprehensive and include both derivatives and other alternatives.

4. Conclusions

There is no empirical evidence that supports the conjectures that derivative contracts can lead to massive failures and create systemic risk. Although we can list the possibilities, we must also estimate the probabilities of a derivative-contract-based financial meltdown.

The future agenda is rich for financial institutions who must continue to understand how to provide products and services at lower friction costs. On a micro level, they must build more efficient pricing mechanisms and risk control systems. They must model and price credit risk.

Regulatory effort must be aimed at fostering the functions of the financial system and not at preserving its institutions. With global competition in the provision of goods and services, including financial services, it is not profitable for agencies to concentrate on narrow institutional definitions. The entity that provides services at lower cost, and po- tentially in far different ways than anticipated, will succeed despite the regulatory protec- tion of other entities.

Acknowledgements

I would like to thank Robert C. Merton, Kenneth Scott, and the participants of these conferences for their discussions of the issues.

Notes

United States General Accounting Office, "'Financial Derivatives: Actions Needed to Protect the Financial System," Report to Congressional Requesters, GAO GAD-94-133, May. 1994. As shown in the third panel of the illustration, ifF > B(I + R) by an amount X, market participants would sell the future and hedge their position by buying government bonds (financed as in panel two). Market participants would receive B* - B - RB on their bonds and pay B* B RB - X on the future, realizing a sure profit of X. If futures were selling for a price of X below this amount, market participants would follow the opposite strategy and make a sure profit of X.

286 MYRON S. SCHOLES

It is not necessary to finance any of these positions at the 100% level. Any other fixed level of capital illustrates the same functional equivalence. A sale of bonds with a promise to repurchase them is a financing trade called a repurchase agreement. The seller receives the bond rate on the proceeds of the sale. A direct financing trade on a long position is sometimes called a reverse repuchase agreement.

References

Benson, G. J., and C. Smith. (1976). "A Transaction Cost Approach to the Theory of Financial Intermediation," Journal of Finance 31 (May), 215-231.

Black, E, and M.S. Scholes. (1974). "From Theory to a New Financial Product," Journal of Finance 29 (May), 399-4 12.

Edwards, F. (1994). "Systemic Risk in OTC Derivatives Markets: Much Ado About Not Too Much." Working paper, Graduate School of Business, Columbia University, New York.

Fama, E. (1980). "Agency Problems and the Theory of the Firm," Journal of Political Economy 88 (April), 288-307

Finnerty, J. D. (1992). "'An Overview of Corporate Securities Innovation." Journal of Applied Corporate Finance 4, (Winter), 23-39

Freeman, A. (1993). "A Survey of International Banking: New Tricks to Learn," The Economist, April 10, 1-37. General Accounting Office. (1994). "Financial Derivatives, Actions Needed to Protect the Financial System."

GAO/GGD-94-133, Washington, D.C. Grossman, S. J., and O. D. Hart. (1982). "Corporate Financial Structure and Managerial Incentives." in J.J.

McCall (ed.), The Economics oflnJbrmation and Uncertainty, Chicago: University of Chicago Press. Jensen, M.C., and W. Meckling. (1976). "Theory of the Firm: Managerial Behavior, Agency Costs and Own-

ership Structure," Journal of Financial Economics 3 (October), 305-360. Jensen, M. C., and W. Meckling. (1989). "'Eclipse of the Public Corporation," Harvard Business Review, 67

(September/October), 61-74. Litzenberger, R.H. (1992). "Swaps: Plain and Fanciful," Journal of Finance 47 (July), 831-850. Loomis, C.J. (1992). "A Whole New Way to Run a Bank," Fortune, September 7, 1992:76 Loomis, C.J. (1994). "The Risk That Won't Go Away," Fortune, March 7, 78. Merton, R.C. (1992). "Financial Innovation and Economic Performance," Journal of Applied Corporate Finance

4 (Winter), 12 22. Merton, R.C. (1993). "Operation and Regulation in Financial lntermediation: A Functional Perspective." Work-

ing Paper 93-020, Harvard Business School Miller, M. H. (1986). "Financial Innovation: The Last Twenty Years and the Next," Journal of Financial and

Quantitative Analysis 2l (December), 459-471 Miller, M. H. (1992). "Financial Innovation: Achievements and Prospect," Journal of Applied Corporate Finance

4 (Winter), 4-11 National Research Council. (1994). "Investing for Productivity and Prosperity." Board on Science, Technology,

and Economic Policy, National Economic Press, Washington, D.C. Ross, S.A. (1973). "The Economic Theory of Agency: The Principal's Problem," American Economic Review 63

(May), 134-139. Ross, S. A. (1989). "Institutional Markets, Financial Marketing, and Financial Innovation," Journal of Finance

44 (July), 541-556. Sanford Jr, C. (1993). "Financial Markets in 2020." Economic Symposium, Federal Reserve Bank of Kansas

City, 1-12. Scholes, M.S., and M.A. Wolfson. (1992). Taxes and Business Strategy: A PlanningApproach. Englewood Cliffs,

NJ: Prentice-Hall.