Embed Size (px)

Citation preview

Global banking and capital markets sector Key themes from 2Q14 earnings calls

August 2014

Global banking and capital markets sector 2

Content

Scope, limitations and methodology of the review 3

Top 10 key themes: 2Q14 earnings season 4

Key themes overview 6

Theme 1: Quarterly earnings performance — ROE performance remains less than “aspirational” 6

Theme 2: Expense trends — no new cost targets announced 8

Theme 3: Capital strength and plans — banks exceed known requirements for CET1 ratios 10

Theme 4: Regulation — uncertainty continues as banks await the finalization of various rules 12

Theme 5: Acquisitions and divestments — meaningful progress on reducing non-core units 13

Theme 6: Lending trends — Americas-based lenders report better growth than European peers 14

Theme 7: Cross-border — banks pursue differentiated global strategies 15

Theme 8: Credit quality — metrics point to generally positive trends in credit performance 16

Theme 9: Customer focus — innovation in products fueled by customer data 17

Theme 10: Conduct and litigation — fines related to legacy issues remain a significant headwind 18

Appendix 19

Summary of key banking sector themes 19

Select KPIs 21

Global banking and capital markets sector 3

Scope, limitations and methodology of the review The purpose of this review is to examine the key themes discussed among 32 global institutions operating within the banking and capital markets sector during the 2Q14 earnings reporting season.

This review is limited to the examination of transcripts of the earnings conference calls held from 22 May 2014 to 7 August 2014. The review does not take into consideration information from other sources.

The period covered 2Q14, which ended 30 June 2014. Exceptions include the following:

• Canadian Imperial Bank of Commerce (CIBC), Royal Bank of Canada (RBC) and Toronto-Dominion Bank, for which the 2Q14 period ended 30 April 2014

• Nomura Holdings, for which the covered period was 1Q15

Banks were selected based on their size and the availability of earnings conference call transcripts. Every effort was made to include a global sample of banks in the review. Exceptions include the following:

• Mitsubishi UFJ Group Bank, Mizuho Financial Group and Sumitomo Mitsui Financial Group were excluded from the analysis due to the lack of transcript availability.

• Bank of China and Industrial and Commercial Bank of China were excluded due to the timing of their 1Q14 results reporting.

• Macquarie Group, Australian and New Zealand Banking Corporation (ANZ) and National Australia Bank (NAB) did not hold interim earnings calls.

Net income, revenue and expense data are not provided for Standard Chartered. This bank discloses half-yearly and annual income statement figures only, which do not compare with the quarterly data reported by the other banks in this analysis.

Global banking and capital markets sector 4

Top 10 key themes: 2Q14 earnings season In 2Q14, the global banking industry continued to operate against a challenging backdrop, characterized by weak economic trends, low activity levels and elevated geopolitical, regulatory and conduct risks.

• US economic recovery continued at an uneven pace.

• In Europe, management commented on the emergence of positive — though weak — signs of economic growth.

• Following a moderate increase in 1Q14, Japan’s GDP fell in the second quarter, driven by a sales tax increase.

• Persistently low interest rates in the US and Europe are expected to remain in place for the rest of 2014, although there are mounting expectations that the US Federal Reserve and the Bank of England may begin to raise rates sometime in 2015.

• Geopolitical tensions, particularly in Central and Eastern Europe, have heightened risks for a number of European banks.

• Requirements for capital buffers and leverage ratios have not been finalized, leading to considerable uncertainty and fragmentation across the industry. In addition, banks within the Eurozone are focused on the European Central Bank’s Asset Quality Review (AQR) and stress tests. Banks in all markets are making costly investments in compliance initiatives as they seek to strengthen risk management and controls.

• Finally, despite the resolution of several high-profile legacy issues during the quarter, banks around the world remain highly vulnerable to legal and conduct-related risks.

These headwinds, which have been key challenges for the industry for a number of quarters, have made it difficult for banks to grow revenues, reduce stubbornly high expenses and generate acceptable returns. Given the expectation that many of these challenges will persist for the foreseeable future, Toronto-Dominion Bank CEO Ed Clark said, “We do not see anything in our results to date which would suggest that our fundamental operating environment has improved.” While he was not the only one to hold this view, management at a number of other global banks were not uniformly pessimistic about the outlook.

• Ruth Porat, CFO, Morgan Stanley: “While June was stronger than the first two months of the quarter, and recognizing that trading markets remain uncertain, we are of the view that it is too early to determine conditions for the rest of the year. However, we see strength and opportunities across our businesses with several encouraging trends. First, M&A volumes remain strong with a healthy backlog and growth in larger transactions, which is our sweet spot. Last quarter, we discussed three catalysts for heightened M&A activity and they remain: healthy corporate, cross-border and activist activity, suggesting M&A will remain vibrant.”

• Stuart Gulliver, Group CEO, HSBC: “We remain broadly positive about the economic outlook for the majority of our home and priority markets, and the UK in particular should maintain a firm recovery.”

• Federico Ghizzoni, CEO, UniCredit: “I don’t underestimate the challenges of the weak economy and the weak recovery in Western Europe. We know about the geopolitical tension in Central and Eastern Europe. But in spite of this, we have released also in the region very satisfying and positive results, and I am pretty confident looking forward.”

“We faced a challenging environment in the quarter as geopolitical risk increased and investors weighed the outlook for monetary policy.”

Shigesuke Kashiwagi, CFO, Nomura

Global banking and capital markets sector 5

Top 10 themes: 2Q14 earnings season

2Q14 1Q14

Rank Earnings season top 10 themes (arranged from most common to least common) — 32 banks

Rank Earnings season top 10 themes (arranged from most common to least common) — 35 banks

1 Quarterly earnings performance 1 Quarterly earnings performance

2 Expense trends and investments in the business

2

Expense trends and investments in the business

3 Capital strength and plans 3 Capital strength and plans

4 Regulation and compliance 4 Regulation and compliance

5 Acquisitions and divestments 5 Cross-border and location strategies

6 Lending trends 6 Lending trends

7 Cross-border and location strategies 7 Credit quality trends

8 Credit quality trends 8 Strategic planning

9 Customer focus 9 Acquisitions and divestments

10 Conduct and legal issues 10 Channel strategies

Note: The themes shaded in yellow are new to the list this quarter; the themes shaded in dark gray dropped out of the top 10.

Global banking and capital markets sector 6

Key themes overview

Theme 1: Quarterly earnings performance — ROE performance impacted by legacy issues

“In this environment, you’ve seen us report, give or take, 11% ROE for two-and-a-half years. But we continue to aspire to better returns.”

Harvey Schwartz, CFO, Goldman Sachs

Banks’ returns on equity (ROE) reflect ongoing drag from legacy issues. In 2Q14, only six of the banks included in this analysis generated ROEs in excess of 12%. Notably, each of these banks is headquartered in the Americas and has a strong retail banking focus. An additional seven banks reported ROEs within range of the typical 10%-12% cost of equity, but well below historical levels. Management at several banks highlighted stronger ROE performance in their strategic businesses and seemed to indicate that they believe sustainable returns will be within reach when non-core units are finally run down and resolved.

• Brady Dougan, CEO, Credit Suisse: “We made good progress on the Non-Strategic Unit (NSU). …So, having our strategic businesses make a 19% ROE in a quarter where we clearly had a lot of preoccupation with getting the cross-border settlement done and behind us is, I think, actually a good result.”

• Stefan Krause, CFO, Deutsche Bank: “Our reported group post-tax ROE for the first half was 4.7%. The core bank’s adjusted post-tax return on average equity was 13.4%, which highlights the strength of our underlying franchise.”

• Antony Jenkins, Group CEO, Barclays: “Our core business has performed well, generating an ROE of 11% after costs to achieve (CTA). …We continue to work to reshape the investment bank and bring it into balance with the rest of our business. Even in this period of transition, there are signs that our strategy is working. … Excluding CTA, the investment bank is delivering an ROE of around 8%, which is where we expected it to be at this point.”

When compared to the same period last year, net earnings fell at 12 of the 31 banks* included in this analysis that disclose quarterly income statement data. The primary drivers of the declines reflect the challenges facing the overall industry.

• Settlements with US authorities drove profits down at Citigroup, Credit Suisse and BNP Paribas. Citigroup reached a US$7.0 billion mortgage settlement with the Department of Justice. Credit Suisse paid US$2.8 billion to resolve cross-border tax matters and BNP Paribas was penalized US$8.97 billion for sanctions violations.

• Bank of America added US$4.0 billion to its litigation reserves, which cut earnings by 43% on a year-over-year basis. Deutsche Bank, JPMorgan Chase and Lloyds Banking Group also increased their provisions for legal and conduct issues.

• At Nomura, earnings were impacted by reduced client activity levels. Net profit fell from the same quarter in 2013, in which record performance was driven by strong investor activity.

• The decline in net income at BBVA, CIBC and Crédit Agricole was driven by their exposure to overseas operations. CIBC and Crédit Agricole took impairment charges related to their Caribbean operations and stake in Portugal’s Banco Espirito Santo, respectively. BBVA was impacted by unfavorable currency movements in Venezuela.

• BNY Mellon reported one-time charges related to restructuring.

Reported ROE, 2Q14*

* Standard Chartered disclosed half-yearly income statement figures only. ROE was not disclosed at Crédit Agricole, Intesa Sanpaolo or Lloyds Banking Group and was not measureable at BNP Paribas due to net loss of €4.3 billion. ROE is for 1H14 for Barclays, BBVA and Standard Chartered. ROE at RBS is for core business only.

-6.7

0.2 1.6 2.2 3.2 3.7 3.8 4.2 5.8 5.9 6.1 6.4 6.9 7.0 8.8 10.4 10.7 10.9 11.0 11.5 11.7 11.9 13.4 15.1 15.9

19.1 23.3

28.8

CS C

DB

RB

S

NO

M

BA

C

CB

K

BC

S

BB

VA

UC

G

BK

UB

S

ST

D

CIB

C

SG

ST

AN

HS

BC

GS

JP

M

MS

ING

ST

T

WF

C

US

B

TD

RB

C

ITA

U

AX

P

Global banking and capital markets sector 7

Net income, percentage change from prior quarters*

*Banks not included for the following reasons: 2Q14 net loss (BNP, CS, LLD); 1Q14 net loss (BAC).

-95%

-66%

-74%

-48%

8%

-14%

-78%

-25%

13%

-35%

-3%

187%

7%

0%

71%

7%

-13%

5%

-3%

11%

12%

23%

-57%

-45%

-48%

-68%

-96%

-68%

-65%

-47%

-43%

-41%

-33%

-29%

-12%

-8%

0%

4%

4%

5%

5%

7%

9%

14%

15%

16%

19%

37%

38%

64%

87%

98%

190%

C

NOM

CIBC

CA

BAC

BBVA

BK

DB

UBS

JPM

UCG

WFC

SG

USB

GS

STT

AXP

HSBC

RBC

TD

ING

ITAU

STD

MS

INT

CBK

RBS

BCS

Change from 2Q13 Change from 1Q14

903%

Global banking and capital markets sector 8

Theme 2: Expense trends — no new cost targets announced

“We continue to see opportunities to increase efficiency through both tactical and strategic moves, investing in technology and systems that simplify our business and position us to better serve our clients.”

James Gorman, CEO, Morgan Stanley

Efficiency savings are reinvested in the business. In 2Q14, only 10 of the banks included in this analysis reported a year-over-year decline in expenses. In addition, expense growth exceeded revenue growth at 18 of the banks. While the latter was due in part to a weak revenue environment — only six banks reported revenue growth of more than 5% over the same period — management also attributed elevated expenses to legal-related provisions, regulatory compliance and restructuring costs.

Banks across regions remain focused on driving efficiencies through a combination of exercising discipline on business-as-usual costs and executing previously announced cost-reduction programs. Savings generated through these efforts are largely being reinvested in growth initiatives and compliance.

• Brian Moynihan, CEO, Bank of America: “If you go back a couple years ago when we started New BAC, we were running US$15 billion-odd of core expenses. Now we’re running US$13 billion-odd, and so we’re largely getting there. … But during the whole time period, we’ve invested literally thousands of people into the sales side to drive growth and we’ll continue to do that. The question is how you balance that investment.”

• Stephan Engels, CFO, Commerzbank: “As in previous quarters, our efficiency measures largely compensated for rising costs for regulatory requirements, investments into [the] private customer division and IT investments.”

• Iain Mackay, Group Finance Director, HSBC: “From a sustainable savings perspective, we generated over US$500 million in the first half of the year. …We saw a step-up in investment in the compliance space in the first half of the year. …It is an investment that we are making now to create a stable basis for compliance capability across financial crime and regulatory compliance in the round.”

• Jay Hooley, CEO, State Street: “On the expense front, we continue to be focused on controlling expenses across the organization. While we continue to perform as we anticipated on operating expenses, we are experiencing increased pressure from regulatory compliance costs.”

• Sergio Ermotti, CEO, UBS: “We are committed to making further investments in growth regions and businesses. Increased efficiency and effectiveness should be viewed as a complement to this investment, as the majority of our savings will be generated in our corporate center.”

Faced with lackluster revenue prospects, banks must find ways to achieve material cost reduction if they wish to generate better ROE performance. Despite this, management comments largely indicated that they are not planning to launch new expense-reduction plans.

• Goldman Sachs CFO Harvey Schwartz referred to the firm’s cost-cutting program, which was completed at the end of 2012. “Several years ago, we went through an exercise to take out roughly US$2 billion of costs out of the enterprise. At this stage, we continue to stay very focused on it.” He did not disclose new expense targets.

• Stefan Krause, CFO, Deutsche Bank: “We expect our full-year 2014 adjusted cost base to remain roughly flat versus 2013, despite regulatory headwinds, and we are confident to reach the targeted accumulated Operational Excellence savings of €2.9 billion by the end of 2014. There have been press rumors about an extension of this OpEx program, which are not accurate. According to our plan, the OpEx initiative allows us to achieve our cost/income ratio target of 65%. As part of our new culture, ongoing cost focus will remain an integral part of Deutsche Bank.”

• Ralph Hamers, CEO, ING: “In the first half, we have been able to keep expenses at around last year’s level and we’re confident that we can keep them flat overall through 2015, though quarter-on-quarter we will continue to see some volatility. So we will remain vigilant on cost, and cost growth will only [be] allowed if there is higher income growth.”

• Bernard Delpit, CFO, Crédit Agricole: “We are in line with our MUST cost-cutting program, with additional savings of €28 million in 2Q14, well on track with the €650 million [in savings] that we target for the end of 2016.”

Global banking and capital markets sector 9

Expenses and revenues, percentage change from 2Q13

Notes: Standard Chartered discloses half-yearly income statement figures only, and they are not comparable to the quarterly figures reported by other banks. The following 13 banks achieved positive operating jaws in 2Q14: AXP, BBVA, GS, ING, INT, ITAU, JPM, LLD, MS, RBS, STD, TD and UBS.

-11%

-7%

-5%

-4%

-4%

-3%

-3%

-2%

-2%

-1%

0%

0%

0%

2%

2%

2%

2%

2%

3%

4%

4%

6%

7%

8%

8%

11%

11%

16%

28%

29%

32%

-10%

-3%

-3%

-4%

-3%

-7%

-3%

-6%

1%

-9%

-1%

-14%

6%

3%

-3%

5%

-4%

9%

1%

2%

-7%

6%

1%

5%

7%

13%

15%

-4%

-6%

-7%

1%

RBS

UBS

BBVA

DB

STD

CA

JPM

UCG

MS

BCS

WFC

NOM

ING

LLD

CBK

AXP

SG

INT

STT

HSBC

BK

GS

BNP

USB

RBC

TD

ITAU

BAC

C

CS

CIBC

Revenues Expenses

Global banking and capital markets sector 10

Theme 3: Capital strength and plans — banks exceed known requirements for CET1 ratios

“Regulatory uncertainty remains. As yet, it’s not possible to determine the group’s common equity Tier 1 future requirements and the interplay of various capital buffers without clear guidance from the regulators. However, we place great importance in the group’s ability to maintain and grow distributions to our investors derived from business profit generation. To ensure that we remain able to do this on an ongoing basis, it remains our intention to maintain a management buffer above regulatory minimum requirements.”

Iain Mackay, Group Finance Director, HSBC

Banks continue to build capital levels. At the end of 2Q14, banks across all regions continued to report Common Equity Tier 1 (CET1) ratios in excess of minimum known requirements. Management at most banks intend to maintain comfortable internal cushions to absorb evolving — and increasingly complex — country-specific buffer requirements. While banks have consistently demonstrated an ability to build capital — in some cases, while also absorbing significant legal fines and provisions — they continue to face significant uncertainties surrounding leverage ratios, qualifying capital instruments and buffers for national and global systemically important banks (G-SIB).

• Marianne Lake, CFO, JPMorgan Chase: “We don’t know how things may change in the future, but between the G-SIB surcharge [and] the buffers that we and other institutions are going to [have to] run for that; with the LCR [(liquidity coverage ratio)] and NSFR [(net stable funding ratio)] and our own internal liquidity framework; [and] with capital stress testing and the CCAR [(Comprehensive Capital Review and Analysis)] under extremely severe conditions, it feels like we have a box around this. And so we are planning to run the firm based on what we know today, with an eye on listening to all of the things you hear.”

• Gerry McCaughey, CEO, CIBC: “We still believe that over the next few years the regulatory picture will become clearer. And that’s my way of saying that I think that there’s more to come. …It is my belief that when you think of targets in order to meet future regulatory requirements, you should be thinking higher, not lower.”

• Jon Peace, Chairman, Standard Chartered: “By the nature of Pillar 2A, it’s sort of a regulatory space to capture all the things they haven’t thought of and put into Pillar 1. I think that it will change from time to time. Whether it always changes upwards or just banters around, we don’t know. It’s relatively new in the way it’s being managed.”

• Stefan Krause, CFO, Deutsche Bank: “Our capital raise increased our key ratios, created capacity for further business development and gave us a buffer for a number of uncertainties, including the prudential valuation, where the precise impact and timing remain uncertain. … [Another uncertainty is the] potential incremental capital requirements from the transition to a single regulator this year. Here we have no specific known items that may impact capital but are cognizant that there could be incremental issues arising as the ECB [(European Central Bank)] takes over, possibly resulting from harmonization across Europe or from regulatory conservatism that may differ from IFRS accounting standards. [There may be] potential capital impacts from the AQR and stress test, which we will have greater certainty about in the fall. Last but not least, we expect significant increases in operational risk RWA due to the industry-wide litigation settlements.”

• Patrick Flynn, CFO, ING: “We’re getting signals that the tax deductibility issue [for additional Tier 1 instruments] will be resolved in the second half of the year. Hybrid instruments are a core feature of how [banks] look at managing their Tier 1 and leverage ratios. We haven’t issued [hybrids yet] because of this tax problem, but we will probably be looking very carefully at doing so when the tax position is clear.”

Leverage ratios,* 2Q14

*Not disclosed at American Express, CIBC, Intesa Sanpaolo, Banco Itaú, RBC, TD, U.S. Bancorp or Wells Fargo; fully loaded Basel III ratios: exceptions include US banks (US supplementary leverage ratio) and Crédit Agricole (Basel III phase-in)

3.2 3.3 3.4 3.4 3.5 3.5 3.6 3.6 3.7 4.2 4.3 4.5 4.5 4.5 4.6 4.7 4.7 4.8 4.8 5.0

5.4 5.7 5.8

6.1

CS CBK BCS DB BNP NOM RBS SG ING UBS HSBC GS LLD STD MS BK UCG CA STAN BAC JPM C BBVA STT

Global banking and capital markets sector 11

Basel III CET1 ratios,* 2Q14

13.4

9.5

12.0

10

11.6

9.8

9.9

11.7

14.3

10.0

10.4

10

10.2

10.6

12.30

9.40

11.7

10.0

9.50

11.50

9.4

9.8

10.9

11.4

11.20

11.30

10.50

12.9

13.2

10.10

9.8

11.1

11.1

13.8

13

9.7

10.1

10.2

10.9

10.5

10.7

10.92

11.3

12.8

16.0

9.2

13.5

10.37

10.83

8.9

9.6

10.1

11.3

AXP - Transitional, standardized

BAC - Standardized, fully loaded

BAC - Standardized, transitional

BBVA - Fully loaded

BBVA - Transitional

BCS - PRA CET1

BCS - Fully loaded

BK - Advanced, transitional

BK - Standardized, transitional

BK - Advanced, fully loaded

BK - Standardized, fully loaded

BNP - Fully loaded

BNP - Transitional

C - Advanced, fully loaded

CA - Fully loaded

CBK - Fully loaded

CBK - Transitional

CIBC - All-in basis

CS

DB - Fully loaded

GS - Standardized, fully loaded

GS - Advanced, fully loaded

GS - Standardized, transitional

GS - Advanced, transitional

HSBC - Transitional

HSBC - Fully loaded

ING - Fully loaded

INT - Fully loaded

INT - Transitional

ITAU - Fully loaded

JPM - Advanced, transitional

LLD - Fully loaded

LLD - Transitional

MS - Advanced, transitional

NOM

RBC - All-in basis

RBS - Transitional

SG - Fully loaded

SG - Transitional

STAN - Transitional

STAN - Fully loaded

STD - Transitional

STT - Standardized, fully loaded

STT - Advanced, fully loaded

STT - Advanced, transitional

TD - All-in basis

UBS - Fully loaded

UCG - Fully loaded

UCG - Transitional

USB - Standardized, fully loaded

USB - Standardized, transitional

WFC - Advanced, fully loaded

WFC - General approach, fully loaded

Global banking and capital markets sector 12

Theme 4: Regulation — uncertainty continues as banks await the finalization of various rules

“The regulatory environment in which banks exist has changed, I would say, forever.”

António Horta-Osório, Group CEO, Lloyds Banking Group

Finalization of post-crisis rules is ongoing. Six years after the global financial crisis sparked a wave of unprecedented regulatory reform for the global banking sector, many rules have yet to be finalized. While the broad regulatory framework that emerged from the Basel III comprehensive reform package and national and regional legislation is well known, the interpretation of many rules remains a work-in-progress. During the 2Q14 earnings season, management at banks across regions commented on the lingering uncertainties related to leverage ratios, liquidity coverage ratios, bail-in requirements and a range of other issues.

Regulatory topics addressed during 2Q14 earnings season

Single Supervisory Mechanism (Europe)

• Ralph Hamers, CEO, ING: “We are happy for European supervision to take over. I think it will force a level playing field across the whole banking system in Europe and the Eurozone. And then hopefully we will all build up quite quickly credibility across the border so that local regulators will be more open to transfer of liquidity.”

Asset Quality Review (Europe)

• Javier Marín Romano, CEO, Banco Santander: “We are precluded from giving information [on the AQR], due to the confidentiality agreement that we have signed with the European Central Bank. The only thing we can say is that we don’t expect any surprise, and we don’t any expect any kind of impact out of the AQR and from the stress test.”

Bail-in rules (US and Europe)

• John Shrewsberry, CFO, Wells Fargo: “There is no real updated intelligence [on the Orderly Liquidation Authority]. We are still hearing that the range that will probably be published at some point in the future is in the high teens to low 20%s in terms of loss absorption cushion. We see ourselves at the low end of that range and at or within striking distance of that range. So based on everything that we know today, we don’t anticipate it having a material impact.”

• Lars Machenil, CFO, BNP Paribas: “If you look at what is crystallizing in the European legislation [on the MREL (minimum requirement of own funds and eligible liabilities)], there are a whole slew of elements that are being set up. One basically says that you have to have a broad set of instruments that can be bailed in. …Given the structure of our balance sheet, the MREL should be manageable.”

Liquidity coverage ratio (US)

• John Gerspach, CFO, Citigroup: “It’s going to be interesting to see how the Fed goes about the next level of managing as far as increasing rates. Because when you look at how monetary policy is going to interact with the regulatory policy, I think we’re going to end up in a new world that none of us have lived through before, nor has the Fed.”

Leverage ratio (global and country regulators)

• Gerry McCaughey, CEO, CIBC: “Requirements over the next few years are going to increase and they could come at you from a variety of different directions. … My expectation is leverage ratio requirements are going to be higher rather than lower.”

• Shigesuke Kashiwagi, CFO, Nomura: “The Basel final rules have been announced, but the interpretation is still uncertain. Therefore, it’s not a situation where we can precisely do the calculation, but as of the end of June, we think we’re in the mid 3% range.”

• David Mathers, CFO, Credit Suisse: “We’ve certainly significantly improved our leverage ratio. It was 3.8% at the end of the second quarter, which is substantially ahead of where it was one year ago or two years ago. In terms of the Swiss discussion around that, the Brunetti Commission is looking at Swiss banking law and is due to report later this year. So we’ll see what comes out at that point in terms of what that means for the leverage ratio.”

Global banking and capital markets sector 13

Theme 5: Acquisitions and divestments — meaningful progress on reducing non-core units

“We are continuing to execute on the previously announced sales of real estate and non-core assets.”

Brady Dougan, CEO, Credit Suisse

Banks highlight sales of loan portfolios and non-core assets. During the 2Q14 earnings season, discussions about acquisition strategies were largely theoretical in nature, as only a few well-capitalized banks expressed a willingness to consider bolt-on deals that met strict internal price and return criteria.

In terms of asset sales, however, it was a different story. Management highlighted a number of deals – both completed and in progress – to dispose of non-core assets, loan portfolios and non-strategic businesses. The environment for asset sales appeared to be favorable in 2Q14, which drove higher levels of disposals for some banks.

• Bruce Thompson, CFO, Bank of America: “Our results in the quarter also benefited from the sale of US$2.1 billion in non-performing residential loans.” Later, he noted, “We continue to look at the sale of non-performing loans, but I would not expect anything near the magnitude from the sale of non-performing loans that we saw this quarter.”

• At RBS, CEO Ross McEwan commented on better-than-expected progress on selling assets from RCR (RBS Capital Resolution): “The economy is picking up; people are after these assets and that is certainly helping us. We saw that trend in the first quarter, which we called out, and we’ve revised [our guidance] upwards after our second quarter of experience.” He also cautioned, “There are only so many deals which one can do in a week. So I think the trend will continue on its current run rate. But we are getting into tougher assets. Let’s be quite honest about it, you always sell the easier ones that you can get the capital out [of] first. But I think we still have a very good market out there.”

• Stefan Krause, CFO, Deutsche Bank: “The NCOU [(Non-Core Operations Unit)] is focusing very much on the operating asset disposal. And I must say that they have been extremely successful with this. We sold BHF; we sold the casino. So I think there’s excellent progress in terms of the operating assets. We’ve had one of the best NCOU performances on the Street. They’ve been running ahead versus their original plan. …And of course now we have assets that will just take a little bit longer and our pace is expected to slow down.”

• Stephan Engels, CFO, Commerzbank: “With our capital-accretive sales of €5.1 billion in Spanish, Portuguese and Japanese assets, the high-risk cluster in commercial real estate is now almost run down in full. All in all, we have reduced our non-core assets by a further €10 billion in Q2. With the current €92 billion at the end of Q2, we have achieved our original 2016 target of €93 billion 2.5 years ahead of schedule.”

• Carlo Messina, CEO, Intesa Sanpaolo: “We have a clear strategy related to NPL [portfolio disposals]. I clearly told the market that prices are now undervaluing collateral in Italy because the real estate market is recovering. …If you need to make a disposal because you are in a difficult situation with capital and liquidity, you will accept the price in the market. But, if you are in a very good position, then you can wait [for better pricing in the market] because you are recovering much more than the amount you provisioned. That’s my strategy.”

• John Gerspach, CFO, Citigroup: “Roughly US$3.8 billion of asset sales were in process during the quarter but not yet closed as of June 30. These include US$2.7 billion of assets from the announced sale of our retail operations in Spain and Greece, as well as nearly US$1 billion of mortgage loans, each of which should close in the third quarter.”

• John Shrewsberry, CFO, Wells Fargo: “We had separated off the government-guaranteed student loan business, which is distinct from the private student loan business that we’re very committed to, into a liquidating portfolio in 2010 when we stopped originating those loans. … We see the opportunity in the market to move those loans off the books. They’re relatively low yielding. They’re not strategic. We don’t have bigger relationships with most of those customers and thus the decision. So we’ve transferred them all to held-for-sale status to signal this intent to sell, and we’re going to go about the process in the next quarter or so.”

Non-strategic business sales/exits

• Citigroup continues to look to “maximize the exit value” for OneMain Financial

• JPMorgan Chase is negotiating the sale of part of its private equity arm, One Equity Partners

• Morgan Stanley sold one of its physical oil commodities businesses, TransMontaigne

• UniCredit is evaluating offers for its debt collection unit, UCCMB

• ING listed NN Group on the Euronext stock exchange; the IPO represented ING’s “final major transaction in its restructuring and repositioning”

Global banking and capital markets sector 14

Theme 6: Lending trends — Americas-based lenders report better growth than European peers

“The low-growth environment in Europe continued to weigh on lending activity.”

Lars Machenil, CFO, BNP Paribas

Lending trends and outlook are more positive in the Americas than in Europe. In general, Americas-based banks reported stronger loan growth than their European peers did. Furthermore, they presented a more optimistic outlook for growth trends for the remainder of the year. While many economies in Europe have stabilized, GDP growth during the quarter was not yet strong enough to spur loan demand. As observed by Société Générale CEO Frédéric Oudéa, “Our economic forecast for France has been for many months at 0.7%, 0.8% [GDP growth]. We see a slight increase of investment by corporates, but limited. …It’s pretty normal to see loan demand in line with such a scenario.”

Separately, management at several banks that do not typically highlight lending trends commented on their strategies and target customer segments.

• David Mathers, CFO, Credit Suisse: “We provide an update of our strategy of expanding the lending business in the ultra-high net worth client segment. In the first quarter, we talked about the strength of this initiative when we increased lending by CHF2.2 billion compared to 1Q13. We’ve continued to make progress on this in the second quarter, albeit at a slower pace in the emerging markets of Europe. In the first half of the year we’ve increased our lending to the segment by CHF2.8 billion, almost double the level achieved in the first half of 2013. Loan growth has been particularly pronounced in Asia-Pacific.”

• Tom Naratil, CFO, UBS: “Growing lending balances is a critical component of our strategy [in Wealth Management Americas]. It’s attractive not only for clients and financial advisors for providing more holistic products and services, but it also supports high-quality growth in recurring net interest income and in pretax margin. This initiative has been very successful as we’ve grown lending balances steadily since the end of 2011, adding US$12 billion in five quarters, which equates to a 40% growth rate.”

• James Gorman, CEO, Morgan Stanley: “In the last several months, we drove new production records in both mortgages and securities-based lending despite sluggish demand for mortgages across the industry. Our success has been driven by the relatively low penetration of our product within wealth management versus peer firms. … Lending growth will enhance the stability of revenue and earnings for the firm as a whole and make our client relationships deeper and stickier.”

• Harvey Schwartz, CFO, Goldman Sachs: “Lending for us has always been an important component of how we provide strategic capital to our clients. Obviously, our corporate clients are an important component of our private wealth business. We don’t target loan growth. Again, these activities, while well collateralized, particularly, for example, in private wealth … this is risk-based capital. And so the way we manage it is through a limit process and through an individual approval process.”

End of period net loans,* group level, percentage change from 2Q13

* Comparable loan data from 2Q13 not available for BK, GS and STT.

-8% -7% -7% -7% -6% -4% -3% -3%

-1% -1% 0%

0% 1% 3% 3% 3% 3% 4% 4% 4% 5% 5%

6% 7% 7%

11% 12%

23%

26%

RB

S

INT

CB

K

UC

G

BC

S

LL

D

BB

VA

CA

ING

ST

D

BA

C

DB

SG

CIB

C

BN

P

UB

S

CS

JP

M

WF

C C

ST

AN

AX

P

TD

RB

C

US

B

ITA

U

HS

BC

NO

M

MS

Targeted long-term refinancing operation (TLTRO)

• In an effort to spur lending to small businesses and households in Europe, the European Central Bank is planning to conduct TLTROs in September and December 2014.

• During the 2Q14 earnings calls, management at European banks stated that they would consider participating in the program.

Global banking and capital markets sector 15

Theme 7: Cross-border — banks pursue differentiated global strategies

“The Russian business is a very important business for us, but I wouldn’t describe this business as critical in terms of affecting our target and our long-term prospects for growth. We are watching the situation very carefully. But I really don’t believe that this is going to be of long-term significance in our capabilities to grow in emerging markets in general.”

Sergio Ermotti, CEO, UBS

Heightened global risks underscore the need for differentiated location strategies. While a broad global footprint can provide banks with certain competitive advantages, it also heightens their exposure to country-specific risks, such as regulatory reform in Korea, prolonged economic challenges in the Caribbean and the impact of sanctions on Russia. Successfully managing such risks requires a willingness to adjust strategies in certain markets and take a differentiated approach based on geography and growth expectations.

Global strategies discussed in 2Q14 earnings season

Exit • Barclays: Spain

• Citigroup: Greece and Spain consumer banking

• Crédit Agricole: Bulgaria and Morocco

• RBC: Jamaica

• RBS: United States

• Standard Chartered: Hong Kong and Korea consumer banking

Mike Corbat, CEO, Citigroup: “We need to have a line of sight to those businesses or geographies making sense over the intermediate or longer time frame. And so, if we discover or believe there are businesses that can’t get there, they’ll absolutely come under strategic review.”

Restructure • CIBC: Caribbean

• Citigroup and Standard Chartered: Korea (non-consumer businesses)

• Crédit Agricole: Portugal

Peter Sands, Group CEO, Standard Chartered: “There is no silver bullet in Korea. Turning this business around will take time and a lot of work on multiple fronts, not least because the industry as a whole faces huge challenges. We are making progress.”

Monitor • BNP Paribas, Intesa Sanpaolo, Société Générale, UBS and UniCredit: Russia and the Ukraine

Federico Ghizzoni, CEO, UniCredit: “Ukraine clearly is a very, very key situation that we monitor almost on a daily basis.”

Maintain commitment

• BNP Paribas: United States

• Commerzbank and UniCredit: Central and Eastern Europe

• Goldman Sachs and Morgan Stanley: Europe

• HSBC: Global network

• Nomura: Europe/Americas

• Société Générale: Africa

Stuart Gulliver, Group CEO, HSBC: “Developed over nearly 150 years, [our unique international network] is highly distinctive and difficult to replicate. It sits absolutely at the heart of our strategy, which capitalizes on the growth of global trade and capital flows and economic development in developing markets.”

Invest • Bank of New York Mellon, State Street, Credit Suisse, UBS, BNP Paribas: Asia-Pacific

• Barclays: Africa

• RBC and TD: United States

David McKay, President, RBC: “We still see very good opportunities to deploy capital for organic growth in the US through our Capital Markets business. When you think about our broker-dealer franchise and our high net worth and affluent customer base there, there certainly are organic opportunities to provide credit- and deposit-related services that we don’t do today through our bank or online bank capability.”

Global banking and capital markets sector 16

Theme 8: Credit quality — metrics point to generally positive trends in credit performance

“This is proving to be a good year in terms of the evolution of credit quality.”

Javier Marín Romano, CEO, Banco Santander

Positive credit quality trends are evident across all regions. During the 2Q14 earnings season, many banks reported lower levels of impaired or non-performing loans (NPL). While NPL reduction was not uniformly evident across the industry, virtually every bank included in this analysis highlighted improvements in one or more other credit metrics, ranging from declining levels of credit costs to reduced NPL inflows or increased coverage of NPLs. Improvements have been driven by stabilizing economic trends in a number of countries, as well as stricter underwriting standards and disposals of non-performing loan portfolios.

• John Shrewsberry, CFO, Wells Fargo: “Non-performing assets have declined for seven consecutive quarters and were down US$686 million from first quarter, although the pace of improvement has slowed.”

• Stefan Krause, CFO, Deutsche Bank: “In our core bank, we continued to record very low levels of provisions for credit losses. These reflect the current benign economic environment and demonstrate the consistently strong credit quality of our book.”

• George Culmer, CFO, Lloyds: “Impairments reduced in every division and continue to benefit from better credit quality, improving economic conditions, provision releases and the reductions in the run-off portfolio. …We are revising our full-year guidance and we now expect the asset quality ratio for full-year 2014 to be around 35 basis points, a further improvement to the revised guidance of around 45 basis points that we gave at Q1.”

• Carlo Messina, CEO, Intesa Sanpaolo: “After years of operating in a very difficult macro environment, we are starting to see improvement in net NPL inflow, which is down 9% on a yearly basis but down 22% excluding two large positions. Consistent with the improvement in NPL inflows, we reduced provisions by 11%, but we further increased the NPL cash coverage ratio to 46.6%, 2.5 percentage points higher than one year ago.”

• Ralph Hamers, CEO, ING: “Risk costs are continuing their downward trend. Risk costs decreased from both the second quarter last year as well as from the first quarter this year and came out at €405 million. And that is basically driven by lower risk costs across the different countries and segments.”

Impaired loans, percentage change from 2Q13 NPLs, percentage change from 2Q13

* Impaired loans and NPLs presented for banks that report this metric.

A few banks reported deterioration in certain credit indicators in specific regions. Management provided specific reasons for the declines, but also expressed confidence that they were not indicative of elevated risk patterns.

• John Gerspach, CFO, Citigroup: “In Latin America, we saw a modest uptick in both net credit losses and delinquency rates. These trends were driven primarily by Mexico cards, as that portfolio continued to season, and consumers continued to adjust to fiscal reforms, as well as the impact of slower economic growth.”

• Peter Sands, Group CEO, Standard Chartered: “The increase in NPLs was actually driven by a relatively small number of loans with no particular pattern or concentration. …We don’t see a particular pattern or concern in the shape of the book and the credit quality.”

• Jaime Sáenz de Tejada, CFO, BBVA: “It is true that cost of risk in 2Q14 has increased in Mexico from 3.5% to 3.7%; the reason being the slower start of the year has increased the cost of risk on the credit card portfolio. …Going forward, our guidance remains intact and we will converge to the 3.5% cost of risk that we mentioned in 1Q14.”

8%

8%

0%

-10%

-10%

-12%

-13%

-19%

-37%

TD

DB

UCG

RBC

CIBC

BCS

HSBC

RBS

LLD

12%

6%

4%

4%

-12%

-13%

-14%

-19%

-28%

BBVA

INT

STD

USB

C

ITAU

WFC

JPM

BAC

Global banking and capital markets sector 17

Theme 9: Customer focus — innovation in products fueled by customer data

“Our client segment strategies are the primary drivers of our overall strategy. We’re focused on who our clients are, what they need and how we can be distinctive in meeting those needs.”

Peter Sands, Group CEO, Standard Chartered

Innovation in banking extends beyond channel strategy. During the 2Q14 earnings season, as in previous quarters, management discussed innovative channel strategies in the form of reformatted branches and digital banking adoption.

• Barclays and Wells Fargo highlighted new supermarket and neighborhood branch formats, respectively.

• At Bank of America, CIBC, JPMorgan Chase and Société Générale, management commented on awards for and/or growing adoption of mobile and digital banking applications.

At a number of banks, discussions around innovation went a step further, as management revealed innovative approaches to managing product portfolios and developing new offerings. Notably, many strategies surrounding product offerings appear to be driven by information and data that banks have gathered on their core customer segments.

• Bruce Thompson, CFO, Bank of America: “We’re simplifying the product set as we reduce the number of offerings and focus the smaller product set on customer feedback and offer greater rewards to customers who bring us more of their relationships.”

• David Williamson, Group Head of Retail and Business Banking, CIBC: “We’ve been investing in [the multi-product sales origination platform] for some time now. …The way that system is set up is that based on client data it puts forward what’s the most likely array of products that client with that profile would want. And whether it’s savings deposits, overdrafts, credit card, which credit card, insurance protection, the upshot is that in using that software, we’re seeing a substantive lift in depth [of customer relationships]. …We’re not driving a product. … What we’re really trying to do is broaden the relationship with clients depending on their needs and we’re using our data warehouse to better surface ‘what are the needs of those clients based on their profile?’”

• Carlo Messina, CEO, Intesa Sanpaolo: “We launched the big financial data program to create integrated management of customer and financial data and we created the innovation center with the objectives of developing new product processes, the ideal branch training center and incubator for start-ups of our customers.”

• John Stumpf, CEO, Wells Fargo: “We can sell a card to a customer at a fraction of the cost of someone else from the outside. We know these people better and we can give them better products.”

• Richard Davis, CEO, U.S. Bancorp: “One of the things that we haven’t talked much about is the research and development that we’ve been doing on mobile payments, not banking so much as payments, which is a space we should be leading in. There are so many derivatives of what could possibly happen next as people want to pay for things and track things and move things. And we’re in just about every single prototype we can think of, testing all kinds of different programs.”

• Antony Jenkins, CEO, Barclays: “Barclaycard continues to lead innovation in payments. We have just launched the bPay wristband, allowing users to make contactless payments of up to £20 at over 300,000 locations in the UK. The bPay band is free, there are no usage charges for customers, and it can be linked to any UK debit or credit card account, truly opening up innovation to everyone.”

• Jeffrey Campbell, CFO, American Express: “We have many different products in all of the countries around the globe in which we do business because they all serve different target segments. And we think there is tremendous value in having the right card for the right customer. …It seems very natural to put the consumer in the driver’s seat so that they can make a choice.”

Global banking and capital markets sector 18

Theme 10: Conduct and litigation — fines related to legacy issues remain a significant headwind

“We are monitoring our legal cases very closely and ensure that all matters are at all times appropriately reflected. It is in our interests to resolve these matters as swiftly as possible. However, there is significant uncertainty as to the timing and size of potential litigation.”

Stefan Krause, CFO, Deutsche Bank

Legacy conduct issues remain an ongoing and significant source of concern. In 2Q14, Citigroup, Credit Suisse and BNP Paribas disclosed major settlements with US authorities over various legacy conduct issues. These announcements follow deals struck by other banks, including JPMorgan Chase, in previous quarters. Progress on high-profile issues prompted management at only a very few banks to suggest that the worst might be behind them in terms of litigation risk.

• Marianne Lake, CFO, JPMorgan Chase: “We’re going to have some elevated and lumpy litigation costs as we work through the issues that you are aware of. And then, with respect to mortgage, we have settled a large proportion of our mortgage-backed securities risks with the governmental counterparties, but we do still have some other civil claims. But we would characterize it as more behind us than in front of us, and we’re working through it.”

• Brady Dougan, CEO, Credit Suisse: “We did resolve the Federal Housing Finance Agency matter earlier this year, and we’ve continued to address and resolve [smaller] mortgage matters on an ongoing basis. But there are still a number of matters out there. …Our possible losses above [the] reserves number has come down from CHF2.4 billion to CHF1 billion this quarter. …We hope we do have most of the major issues behind us.”

More commonly, however, management remained cautious about the status of legal and conduct-related issues. Many highlighted additions to litigation reserves and their commitment to elevating conduct standards to avoid future problems. Uncertainties related to the size and timing of fines are significant, and as regulators continue to launch new investigations into issues such as currency manipulation and high-frequency trading, it is difficult for most banks to foresee the end of legal headwinds.

• Antony Jenkins, CEO, Barclays: “Our sector faces unprecedented scrutiny for reasons I understand and accept. This reinforces the critical importance of the ongoing cultural change we are undertaking. Our approach is very clear: where there is a case to answer, we will take responsibility, accept the sanction, learn the lessons, and move on. Let me be very clear, I will not tolerate behavior that is inconsistent with our purpose and values.”

• Frédéric Oudéa, CEO, Société Générale: “We are at preliminary stages [in various litigations]. Sometimes enquiries are just starting and sometimes there will be potentially no risk. Prudently, we think it makes sense to add to the provisions.”

• Bernard Delpit, CFO, Crédit Agricole: “On litigation, again, I would like to reiterate what I already said – we have carried out an in-depth review, [which] we will shortly be handing over to the relevant US investigators. We don’t have a timeline and, no, we do not have any estimate in terms of figures or in terms of schedule. That’s all I can say.”

• Ross McEwan, Group CEO, Royal Bank of Scotland: “We are actively managing down a slate of significant legacy issues. This includes significant conduct and litigation issues that will hit our profits in the months and years to come. I’m pleased we’ve had two good quarters, but no one should get ahead of themselves here; there are bumps in the road ahead of us.”

Settlements discussed during the 2Q14 earnings season*

C US$7 billion settlement with the Department of Justice to resolve substantially all legacy claims over residential mortgage-backed securities (RMBS) and collateralized debt obligations (CDO)

CS US$2.6 billion settlement with the Department of Justice to resolve cross-border tax evasion matter

BCS US$280 million settlement with the US Federal Housing Finance Agency to resolve private-label mortgage-backed securities claims from Fannie Mae and Freddie Mac

£26 million fine to the Financial Conduct Authority related to gold price manipulation claims

BNP €5.95 billion comprehensive settlement with US authorities over sanctions violations

BAC US$650 million settlement with AIG to resolve all outstanding RMBS litigation between BAC and AIG

USB US$200 million settlement with the Department of Justice to resolve an investigation into the endorsement of mortgage loans under the Federal Housing Administration’s insurance program

* Additional significant settlements have been announced since the close of the 2Q14 earnings season.

Global banking and capital markets sector 19

Appendix

Summary of key banking sector themes 2Q14 earnings season

Top initiatives and issues (arranged from most common to least common)

Top themes # of banks

AXP ITU STD BAC BK BCS BNP CIBC C CBK CA CS DB GS BBVA HSBC ING

Quarterly earnings performance

32 √ √ √ √ √ √ √ √ √ √ √ √ √ √ √ √ √

Expense trends

32 √ √ √ √ √ √ √ √ √ √ √ √ √ √ √ √ √

Capital strength and plans

32 √ √ √ √ √ √ √ √ √ √ √ √ √ √ √ √ √

Regulation and compliance

30

√ √ √ √ √ √ √ √ √ √ √ √ √ √ √ √

Acquisitions and divestments

30 √ √ √ √ √ √ √ √ √ √ √ √ √ √ √ √ √

Lending trends

30 √ √ √ √ √ √ √ √ √ √ √ √ √ √ √ √ √

Cross-border and location strategies

28 √

√

√ √ √ √ √ √ √ √ √ √ √ √ √

Credit quality trends

27 √ √ √ √ √ √ √ √ √ √ √

√

√ √ √

Customer focus

24 √

√ √ √ √ √ √ √ √

√ √

√

Conduct and legal issues

23 √ √ √

√ √

√ √ √ √ √ √

√

Legend

AXP — American Express ITAU — Banco Itaú STD — Banco Santander BAC — Bank of America

BK — BNY Mellon BCS — Barclays BNP — BNP Paribas CIBC — Canadian Imperial Bank of Commerce

C — Citigroup CBK — Commerzbank CA — Crédit Agricole CS — Credit Suisse

DB — Deutsche Bank GS — Goldman Sachs BBVA — Grupo BBVA HSBC — HSBC Holdings

ING — ING Groep

Global banking and capital markets sector 20

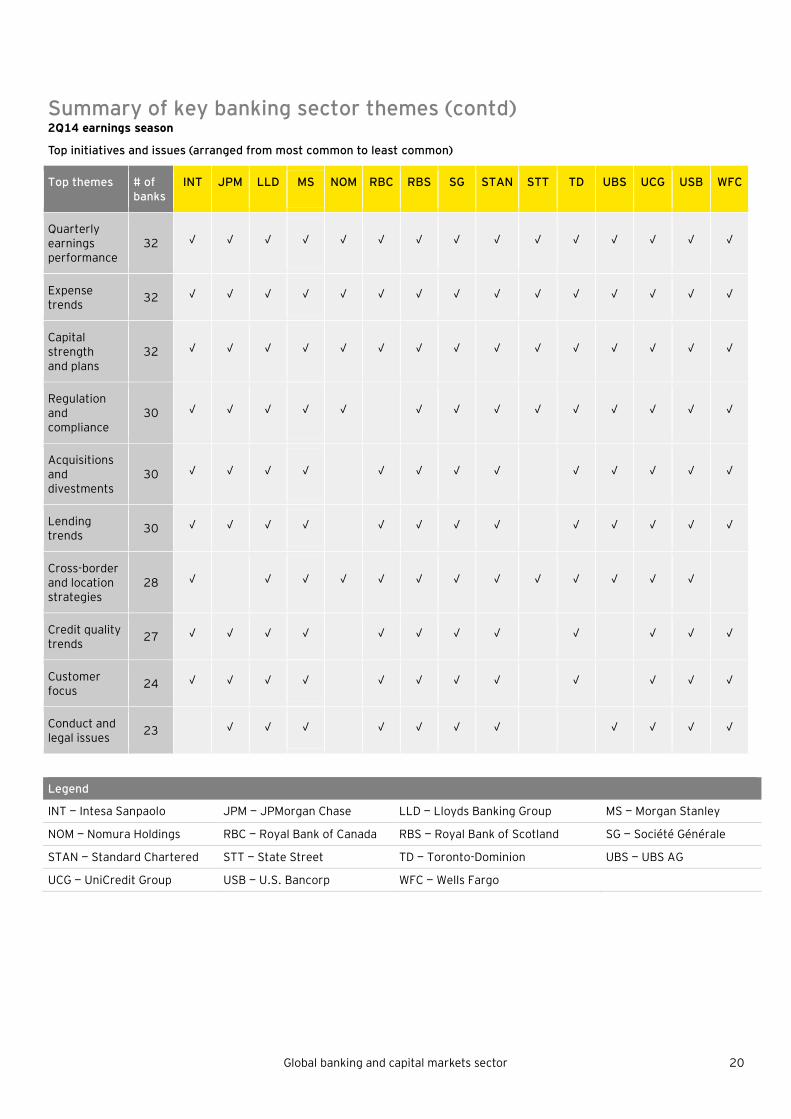

Summary of key banking sector themes (contd) 2Q14 earnings season

Top initiatives and issues (arranged from most common to least common)

Top themes # of banks

INT JPM LLD MS NOM RBC RBS SG STAN STT TD UBS UCG USB WFC

Quarterly earnings performance

32 √ √ √ √ √ √ √ √ √ √ √ √ √ √ √

Expense trends

32 √ √ √ √ √ √ √ √ √ √ √ √ √ √ √

Capital strength and plans

32 √ √ √ √ √ √ √ √ √ √ √ √ √ √ √

Regulation and compliance

30 √ √ √ √ √

√ √ √ √ √ √ √ √ √

Acquisitions and divestments

30 √ √ √ √

√ √ √ √

√ √ √ √ √

Lending trends

30 √ √ √ √ √ √ √ √

√ √ √ √ √

Cross-border and location strategies

28 √

√ √ √ √ √ √ √ √ √ √ √ √

Credit quality trends

27 √ √ √ √

√ √ √ √

√

√ √ √

Customer focus

24 √ √ √ √ √ √ √ √ √

√ √ √

Conduct and legal issues

23 √ √ √

√ √ √ √

√ √ √ √

Legend

INT — Intesa Sanpaolo JPM — JPMorgan Chase LLD — Lloyds Banking Group MS — Morgan Stanley

NOM — Nomura Holdings RBC — Royal Bank of Canada RBS — Royal Bank of Scotland SG — Société Générale

STAN — Standard Chartered STT — State Street TD — Toronto-Dominion UBS — UBS AG

UCG — UniCredit Group USB — U.S. Bancorp WFC — Wells Fargo

Global banking and capital markets sector 21

Select KPIs

Operational metrics (% Y-o-Y growth)

KPIs Share price

Text legend: Better than average Worse than average

Ass

et

Co

mp

co

st

No

n-c

om

p c

ost

Re

ve

nu

es/

em

plo

ye

e

(US

$0

00

)

Co

st/e

mp

loy

ee

(U

S$

00

0)

Co

st-i

nco

me

ra

tio

Op

era

tin

g m

arg

in

Ne

t in

tere

st m

arg

in

Co

st o

f e

qu

ity

Re

turn

on

av

era

ge

e

qu

ity

Th

ree

- m

on

th c

ha

ng

e

On

e-y

ear

cha

ng

e

Best performer 24.2% -6.6% -44.4% 281.6 30.4 45.9% 54.1% 3.3% 5.5% 30.4% 10.4% 81.9%

Worst performer -16.9% 27.4% 83.7% 46.9 194.6 107.0% -7.0% 1.0% 25.5% -18.6% -18.5% -19.0%

Average -0.2% 2.5% 3.9% 95.3 69.5 70.1% 29.9% 2.2% 10.6% 6.9% -3.3% 23.8%

AXP 0.3% 7.5% 12.9% 128.7 111.2 86.4% 13.6% NA 8.7% 30.4% 4.1% 25.4%

BBVA -0.2% -6.5% 7.4% 64.9 36.1 55.7% 44.3% 2.4% 10.7% 7.0% 4.5% 46.3%

STD -5.7% -5.8% -3.6% 70.6 35.0 49.6% 50.4% NA 10.5% 7.7% 10.4% 65.1%

BAC 2.2% -2.6% 36.9% 91.7 79.5 86.7% 13.3% 2.2% 9.4% 3.9% -11.4% 18.9%

BK 11.1% -4.6% 5.3% 73.3 55.2 75.4% 24.6% 1.0% 14.5% 6.1% 5.8% 31.6%

BARC -14.2% 27.4% -44.4% 79.8 61.7 77.3% 22.7% 1.7% 8.4% 2.4% -10.4% -19.0%

BNP 2.4% NA NA NA NA 68.1% 31.9% NA 11.6% -18.6% -13.8% 16.8%

CIBC 0.0% 7.3% 11.7% 66.5 41.5 62.5% 37.5% 2.1% 5.5% 6.6% 1.8% 30.1%

C 1.4% -0.8% -6.3% 80.3 49.9 62.1% 37.9% 2.9% 10.0% 0.4% -1.5% -2.4%

CBK -8.5% -2.0% 21.7% 60.5 47.1 77.9% 22.1% NA 9.0% 1.8% -17.0% 77.9%

CA -14.9% NA NA NA NA 70.5% 29.5% NA 10.6% 0.9% -13.6% 54.3%

CS -3.1% 1.6% 83.7% 148.6 156.7 105.4% -5.4% NA 10.6% -6.1% -12.5% -2.2%

DB -12.8% -6.6% 0.1% 107.5 90.6 84.3% 15.7% NA 9.6% 1.5% -18.5% -16.8%

GS -8.4% 6.0% 5.1% 281.6 194.6 69.1% 30.9% NA 9.1% 10.3% 0.9% 10.3%

HSBC 4.1% NA NA 62.8 36.8 58.6% 41.4% NA 9.4% 9.8% -3.3% -14.7%

ING -1.3% 0.3% 11.8% 97.9 55.5 56.7% 43.3% 1.5% NA 10.5% NA NA

INT -2.7% 10.8% -9.1% 66.3 30.4 45.9% 54.1% NA 10.4% 2.1% -10.9% 81.9%

ITAU 7.3% 11.5% 8.9% NA NA 51.7% 48.3% NA 25.5% 22.2% 3.1% 28.2%

JPM 3.3% -5.1% -0.7% 99.7 63.0 63.1% 36.9% 2.2% 12.9% 10.7% -5.0% 9.8%

LLD -3.7% NA NA 46.9 50.2 107.0% -7.0% 2.5% 7.6% -4.3% -1.9% 16.0%

MS 3.0% 3.1% -8.8% 153.3 118.0 76.9% 23.1% NA 8.5% 11.1% 3.6% 31.5%

NOM 4.7% 3.4% -2.9% 125.3 107.8 86.1% 13.9% NA 17.2% 3.4% 8.6% -4.4%

RBC 3.4% 5.9% 4.3% 111.7 69.6 62.3% 37.7% 2.3% 5.8% 17.1% 4.2% 24.5%

RBS -16.9% 0.3% -19.9% 53.7 43.5 81.1% 18.9% 2.2% 10.3% 4.4% 3.6% 16.5%

SG 5.5% NA NA 53.2 35.2 66.1% 33.9% NA 11.0% 8.1% -18.0% 43.2%

STT 24.2% 6.7% -2.8% 88.3 62.2 70.5% 29.5% 1.2% 11.2% 11.6% -3.3% 2.3%

TD 8.5% 9.3% 12.1% 92.5 57.9 62.6% 37.4% 2.3% 6.0% 14.8% 6.4% 30.1%

USB 10.1% 0.5% -0.9% NA NA 51.9% 48.1% 3.3% 13.0% 14.0% 0.8% 19.3%

UBS -13.0% -0.3% -17.2% 129.2 107.3 83.0% 17.0% NA 10.5% 7.1% -12.6% -0.6%

UCG -3.6% -0.9% -3.5% 58.7 35.0 59.6% 40.4% NA 9.5% 3.8% -9.1% 68.1%

WFC 11.2% -1.4% 0.9% 79.9 46.3 57.9% 42.1% 3.2% 11.2% 12.9% 5.6% 27.1%

Source: SNL Financial and company reports.

Notes: 2Q14 numbers for Canadian banks are from January 2014–April 2014; operating margin= (net revenue-operating expenses)/net revenue; all numbers are non-annualized (except RoAE and NIM).

EY | Assurance | Tax | Transactions | Advisory

About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com. About EY’s Global Banking & Capital Markets Center In today’s globally competitive and highly regulated environment, managing risk effectively while satisfying an array of divergent stakeholders is a key goal of banks and securities firms. EY’s Global Banking & Capital Markets Center brings together a worldwide team of professionals to help you succeed — a team with deep technical experience in providing assurance, tax, transaction and advisory services. The Center works to anticipate market trends, identify the implications and develop points of view on relevant sector issues. Ultimately it enables us to help you meet your goals and compete more effectively.

© 2014 EYGM Limited. All Rights Reserved.

EYG no. EK0305 CSG/GSC2014/1445557 ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com