Embed Size (px)

Citation preview

RUNNING HEAD: AFFILIATIONS, ENDORSEMENTS, AND IPO SUCCESS

GETTING OFF TO A GOOD START:

THE EFFECTS OF UPPER ECHELON AFFILIATIONS

ON INTERORGANIZATIONAL ENDORSEMENTS AND IPO SUCCESS ∗∗∗∗

MONICA C. HIGGINS Harvard Business School

Organizational Behavior Unit Soldiers Field Park Boston, MA 02163

Phone: (617) 495-6993 Fax: (617) 496-6568

e-mail: [email protected]

RANJAY GULATI Kellogg Graduate School of Management

Northwestern University Department of Organization Behavior

2001 Sheridan Road Evanston, IL 60208-2001 Phone: (847) 491-2685

Fax: (847) 491-8896 e-mail: [email protected]

∗ We thank Raphael Amit, Bharat Anand, Carliss Baldwin, Ben Esty, Morten Hansen, Michael Higgins, Linda Johanson, Rakesh Khurana, Josh Lerner, Jay Light, Jay Lorsch, Nitin Nohria, William Ocasio, Gary Pisano, Mikolaj Jan Piskorski, Woody Powell, Toby Stuart, Mike Tushman, and James Westphal for their helpful comments and discussions on the present research. We also thank Josh Lerner for the use of his equity index and Brian Bushee for the use of his institutional investor classification data. We are especially thankful to John Galvin for his research assistance and contributions to the present study, and we appreciate the research assistance of Suzanne Purdy and Paul Nguyen as well.

2

GETTING OFF TO A GOOD START:

THE EFFECTS OF UPPER ECHELON AFFILIATIONS ON

INTERORGANIZATIONAL ENDORSEMENTS AND IPO SUCCESS

ABSTRACT

This article examines the origins of interorganizational endorsements in the context of

firms undergoing an initial public offering (IPO). We propose that the affiliations associated

with the career histories of a firm’s upper echelon, including its managing officers and board

members, send important signals to external parties who are evaluating the quality of young

firms. Such signals are critical to the matching process between firms and endorsing

organizations, since young firms lack well-established networks and a favorable reputation at the

time they are being considered for endorsement. We introduce a three-way typology of upper

echelon affiliations and hypothesize that each of the three types of upper echelon affiliations with

prominent organizations enhances the perceived quality of the young firm in terms of the

personal and social resources that such ties afford. We test our assertions on a sample of public

and private biotechnology firms that were founded between 1961 and 1994 and that went public

between 1979 and 1996. Analyses of the five-year career histories of the over 3200 executives

and directors that make up the upper echelons of these firms show that the prestige of a firm’s

lead underwriter depends on the upper echelon as a whole having affiliations with prominent

downstream organizations (i.e., pharmaceutical and/or healthcare companies) and with

prominent horizontal organizations (i.e., biotechnology companies). Additionally, we find that

the success of a firm’s IPO depends on specific types and combinations of upper echelon

affiliations. Our analysis has implications for the study of organizational endorsements,

embeddedness, and entrepreneurship.

3

Research in organizational theory has long suggested that social structure affects the

outcomes of young firms (Stinchcombe 1965). Scholars have proposed an implicit hierarchy or

ranking among firms such that a firm’s socially-defined position in its marketplace (White 1981)

can affect market participants’ perceptions of the firm. In particular, a firm’s status-based

affiliations has been conceptualized as a means of enhancing a firm’s power over other

individuals (Weber 1968; Veblen 1953) or, as a signal of firm quality when other, more direct

indicators are unclear (Podolny 1993). As recent work has shown, a young firm’s ties to high-

status organizations, such as prestigious venture capital firms or investment banks, can affect the

extent to which a firm is endorsed by the investment community (Stuart, Hoang, and Hybels

1999). But while the role of interorganizational relations in facilitating the growth of firms has

received increasing attention (e.g., Zuckerman 1999; Rao 1994), scholars have paid less attention

to the origins of such ties, particularly in social networks research, since theory rests on the

notion of a pre-existing social structure of which a bounded and identified network is a necessary

precondition (Laumann, Galaskiewicz, and Marsden 1978).

In extending research on interorganizational relations to endorsements, there are some

unique elements to be considered. While all firms are subject to the demands of multiple

constituents (White 1981) and so, are subject to evaluation by groups in their environment

(Thompson 1967), receiving endorsement from an influential organization is a particular concern

for young firms, since they have not yet developed a favorable reputation (Rao 1994; Rao and

Drazin 2000). Additionally, endorsement is a particular concern for firms that face mediated

markets, such as the initial public offering (IPO), which are characterized by significant

ambiguity regarding firm valuation and depend on highly visible critics, such as investment

bankers, who wield tremendous influence over investor behavior (Zuckerman 1999). Although

4

scholars have begun to examine the consequences of organizational endorsement, the

antecedents to this important form of matching have not yet been studied.

We situate our study of interorganizational endorsement in the context of a young firm’s

IPO. In general, firms that go public do so with the endorsement of a lead investment bank that

underwrites the firm’s security offerings. In the present study, we focus our attention on the

extent to which the affiliations of a young firm’s upper echelon—that is, the firm’s top managers

and board members—serve as signals that affect a prestigious investment bank’s endorsement

decision. We propose that upper echelon affiliations that derive from members’ employment and

board memberships with prominent organizations can serve as signals of quality when other

indicators are weak, much as Spence (1974) argued that education can serve as a signal to

potential employers when the productivity of new hires is uncertain. In the IPO context, signals

associated with upper echelon members’ career backgrounds may be critical, since objective

measures of firm quality are difficult to come by. In industries such as biotechnology, the

context studied here, in which product development cycles are extremely long (seven to ten

years) and the needs for cash are in the hundreds of millions of dollars (Burrill and Lee 1993;

Dibner 1999), the upper echelon’s ability to signal the firm’s quality to the investment

community is paramount.

We examine the effects of upper echelon backgrounds on the prestige of a firm’s lead

investment bank during its IPO, and we examine the effects of upper echelon affiliations on IPO

success. Organizational scholars have shown considerable interest in the implications of

embeddedness for firm outcomes (e.g., Baum and Oliver 1992; Palmer, Zhou, Barber, and

Soysal 1995). We continue in this research tradition of examining the implications for firms of

their affiliations with other organizations. By examining both the antecedents and consequences

5

of organizational endorsements, we build on the work of Stuart, Hoang, and Hybels (1999),

which demonstrated the positive effect of ties to prominent others on firm outcomes; our

research highlights the social origins of some of those important relationships. We gauge IPO

success by the proceeds to the firm as a result of the offering and by the number and quality of

the institutional investors that choose to invest in the young firm. Looking beyond financial

indicators of IPO success to the types of investors that endorse a young firm can extend our

understanding beyond the origins of direct endorsements, such as those from prestigious

investment banks, to the origins of second-order endorsements, such as those from institutional

investors.

THEORY AND APPLICATION TO THE IPO

Recent organizational research has introduced a perspective on finance that is largely

premised on the idea that a firm’s outcomes are affected by its networks of relationships with

others (e.g., Uzzi 1999; Zuckerman 1999). Although this research has not directly refuted the

financial axiom that firms are stratified through market perceptions of a firm’s economic value, it

has suggested that social and structural relationships modify economic processes and behavior

(Granovetter 1985). As prior studies have shown, a firm’s exchange relations with high-status

others can affect a host of firm outcomes, including market share (Podolny, Stuart, and Hannan

1996), the spread between costs and price (Podolny 1993), and reactions of the financial

community (Stuart, Hoang, and Hybels 1999).

Yet despite this increased interest in the role of interorganizational relationships in the

financial performance of firms, there has been relatively little research on the antecedents of

powerful interorganizational relationships. Furthermore, prior research that has addressed this

question has focused on the formation of business partnerships, but not on the origins of

6

organizational endorsement. The process of endorsement has some distinct dynamics. One

distinct element is the generally limited history of interaction between a firm and its endorser.

Additionally, in mediated markets, the legitimacy of a firm largely depends on its relationship

with a powerful endorser. As recent research has found, firms that fail to gain reviews by critics

who specialize in the firm’s product can convey illegitimacy to the marketplace, affecting firm

outcomes (Zuckerman 1999). In the IPO context studied here, one important critic that can

affect the behavior of “consumers” or investors at the time of an IPO is a firm’s lead underwriter;

the more prestigious the lead underwriter, the greater the signals of quality that are conveyed,

affecting the firm’s reputation and ability to secure financial resources (Carter and Manaster

1990).

Convincing a prestigious investment bank to endorse a young firm is primarily the

responsibility of a firm’s top managers and board members, which we refer to here as the firm’s

upper echelon. Some have argued that the better the technological quality of the young firm, the

easier it is for the firm to attract the attention of a prestigious investment bank and to obtain a

sizable IPO (e.g., Deeds, DeCarolis, and Coombs 1997). But during the early stages of a young

firm’s lifetime, and particularly in industries in which the product’s underlying technology is

complex and uncertain, like the biotechnology industry studied here, providing direct evidence of

quality is problematic. Even seemingly obvious indicators, such as the number of patents held

by a firm, have received mixed reviews in recent studies of their effects on investors’ perceptions

(DeCarolis and Deeds 1999). Given such difficulties in directly evaluating the young firm’s core

technology, outsiders look for other indications that the organization and its product are viable.

One important signal of firm quality that the upper echelon can utilize in selling the

young firm is the backgrounds of the upper echelon members. Indeed, when a firm files its

7

official S-1 document with the Securities and Exchange Commission (SEC), which starts the

formal marketing process of the firm, it is required to report the five-year career histories of both

its managing officers and its board members. This company information is generally contained

in a section called “Management” and includes a listing of the firm’s directors’ and managing

officers’ prior employment and board memberships. This information, along with other portions

of the S-1 document, is reviewed carefully by potential investors who are deciding whether to

endorse a young firm (Bochner and Priest 1993). And, when the firm formally presents itself to

the investment community during the company’s “road show,” the backgrounds of the firm’s

board members and its managing officers are showcased as well. Our focus here on the

backgrounds of a firm’s entire upper echelon centers on the signaling value associated with this

information and is consistent with recent research perspectives on upper echelons (Jensen and

Zajac 2000; O’Reilly, Snyder, and Booth 1993).

Prior research has suggested that the quality of top executives’ prior jobs can indicate

high status (e.g., Davis 1991), generating advantages for the firm by creating perceptions of skill,

trustworthiness, and reputation that increase the firm’s attractiveness to potential suitors

(Eisenhardt and Schoonhoven 1996). Affiliations with specific organizations that upper echelon

members of young entrepreneurial firms worked for can be considered signals of firm-level

resources, much as other upper echelon characteristics that have been studied in the context of

well-established firms in the past (e.g., D’Aveni 1990; Hambrick and D’Aveni 1992). Such

affiliations can signal valuable information to third parties who are considering whether to

provide financial resources to a young firm. As recent research has suggested, signals regarding

the resources associated with the backgrounds of a firm’s employees can lend legitimacy to a

young firm (Rao and Drazin 2000)—legitimacy that can have an important effect on the

8

endorsement decisions of others.

We extend these ideas one step further now to consider how specific types of prominent

upper echelon affiliations can signal different aspects of firm quality in the biotechnology

industry.

A Typology of Upper Echelon Affiliations

Building upon prior research, we propose that upper echelon affiliations can be classified

into three types of firm ties—upstream, horizontal, and downstream affiliations (e.g., Baum,

Calabrese, and Silverman 2000; Cockburn and Henderson 1998) – representing different types of

relationships a firm can have with participants in its market (White 1988, 1993). Here, this

typology is used to classify the different types of organizational affiliations that derive from the

career histories of members of a firm’s upper echelon. Different types of upper echelon

affiliations can signal different aspects of firm quality. Upstream affiliations, or ties to

prominent research institutions, signal technological quality—that the firm’s product or

technology is viable or scientifically sound. Horizontal affiliations, or ties to prominent

organizations in the firm’s own industry, signal the firm’s organizational quality—its ability to

manage its own resources effectively, including its people, money, and assets. Downstream

affiliations, or ties to prominent institutions that specialize in marketing, distributing, and selling

end-stage products, signal the firm’s market-based quality—its ability to bring its products to

market, including testing, conducting trials, marketing, and selling products.

Upper echelon upstream affiliations. Upstream affiliations in the biotechnology

industry derive from upper echelon members’ employment affiliations with prominent

organizations such as research institutions, think tanks, and/or universities (e.g., to national

institutions such as the National Institutes of Health (NIH), major universities in biology and

9

chemistry, and institutions that receive substantial grants to pursue specialty areas). During the

acquaintanceship period, when a firm is seeking funding for an IPO, investment bankers are

likely to interact with several members of the firm’s upper echelon, including those who have

high-level research positions in the firm. In addition to calibrating the stage of the firm’s

products, having discussions with upper echelon members with experience from major research

institutions should bolster the analysts’ confidence in the firm’s ability to conduct high-quality

research and to manage the research process, because of the level and quality of resources

associated with such institutions. Industry contact with academia enables the diffusion of

technological knowledge that is extremely valuable to young biotechnology firms (e.g., Zucker,

Darby, and Brewer 1994); thus, a young firm’s association with elite sponsors such as

prestigious research universities should signal the potential for transfer of knowledge, affecting

future collaborations and learning (Koput, Powell, and Smith-Doerr 1997).

Moreover, upper echelon affiliations with prominent upstream institutions can signal to

others that the technological quality of the firm is sound, since one would expect top executives

with such ties to join only firms that show technological promise. To assume otherwise would

be to believe that individuals engage in relationships with firms that are other than reputation-

enhancing. An upper echelon with many ties to prominent upstream organizations, signaling

technological quality, is likely to attract a prestigious investment bank as its lead underwriter:

Hypothesis 1: The greater the number of upper echelon affiliations with prominent upstream organizations, the greater the prestige of a young company’s investment bank at the time of the IPO.

Upper echelon horizontal affiliations. An upper echelon’s horizontal affiliations in the

biotechnology industry derive from upper echelon members’ employment and board affiliations

with prominent organizations in the biotechnology industry. Through such affiliations, the firm

10

gains or has the potential to gain valuable resources in the form of information, contacts, and/or

funds that will enable it to compete effectively. Competing effectively requires industry-specific

understanding of how to secure important resources such as cash, scientists, equipment, and

laboratory space, as well as managerial knowledge of how to structure, design, and manage a

biotech organization to maximize innovation and learning (Powell, Koput, and Smith-Doerr

1996; Pisano and Mang 1993). As scholars have recently suggested, organizations can facilitate

the transfer of valuable resources such as intellectual capital and ideas by recruiting individuals

from well-established organizations in the firm’s same industry (Rao and Drazin 2000).

During the acquaintanceship period between a young firm and investment banks, it is

important for bankers to assess whether the company is worth its endorsement—by, for example,

examining the financial history provided by the company, the firm’s product development

schedule and research and development plans, and the strategic direction articulated by the firm’s

top executives. Entrepreneurs with business plans that match the expectations of the industry are

much more likely to be accepted by outsiders in the investment community (Aldrich 1999). IPO

members who have worked in the biotechnology industry are likely to have an appropriate sense

of the timing of research and financial milestones as well as human resource considerations,

including how to staff projects and structure the organization. Having upper echelon members

who worked for prominent biotechnology firms signals to outsiders that such estimates and

decisions are likely to be both appropriate and reliable, given the valuable skills and knowledge

they presumably acquired while working for such firms.

Furthermore, upper echelon members’ affiliations with prominent horizontal institutions

can positively influence outsiders’ expectations of the firm’s future organizational quality (cf.

Benjamin and Podolny 1999). Even if upper echelon members do not tap into their prior

11

employment-based ties during the IPO process, horizontal affiliations signal to outsiders that the

firm has the potential to access high-quality information that can assist the firm in managing its

resources effectively in the future. Thus,

Hypothesis 2: The greater the number of upper echelon affiliations with prominent horizontal organizations, the greater the prestige of a young company’s investment bank at the time of the IPO.

Upper echelon downstream affiliations. In biotechnology, an upper echelon’s

downstream affiliations derive from team members’ affiliations with prominent pharmaceutical

and/or healthcare companies – companies that have resources such as information, contacts, and

funds that can help the young firm bring its core technology, product, and/or service to market.

The wealth, status, and power associated with prominent pharmaceutical firms are likely to have

provided the upper echelon member with valuable knowledge when he or she worked for the

firm, including knowledge of product testing (e.g., clinical trials), of the Food and Drug

Administration (FDA) approval process, of product marketing, and of how to sell a product or

technology. Pharmaceutical companies, unlike small biotechnology firms, are well equipped and

have unique information in each of these areas (Powell, Koput, and Smith-Doerr 1996). Further,

since this information was derived from upper echelon members’ employment at prominent

pharmaceutical firms, the capabilities and connections afforded the young biotechnology firm are

likely to be substantial, attracting the attention of the investment community.

During the acquaintanceship period, analysts typically meet with the firm’s top

executives. Knowing that an individual whom they met had been employed by a major

pharmaceutical company is likely to increase their perception of firm quality, since such

affiliations suggest that the person leading the firm has gilt-edged qualifications and powerful

friends (Finkelstein 1992). Knowing that several key members of the young firm are affiliated

12

with major pharmaceutical companies should provide additional confidence in the firm’s

leadership and, in particular, the firm’s ability to bring its product to market. Such affiliations

are important resources for the firm since they indicate that valuable information, access, and

influence has been and/or can be, in the future, made available to the firm.

In addition, the upper echelon’s affiliations with prominent downstream organizations are

likely to be a healthy signal to outsiders of structural advantages for the firm in the future (cf.

Lin, Ensel, and Vaughn 1981). There is a risk associated with individuals who already have

prominent affiliations deciding to work for and/or sit on the board of a young firm, a decision

that is based on their own judgment of the firm’s potential. Hence, the upper echelon’s

affiliations with prominent downstream firms can positively influence outsiders’ expectations

about the firm’s ability to navigate through the many stages it takes to bring a product to market

in the future. In biotechnology, this positive regard is especially salient, since, at the time of

IPO, the firm has yet to engage in such downstream activities; thus, directly observing the firm’s

capability in this domain is impossible. Thus,

Hypothesis 3: The greater the number of upper echelon affiliations with prominent downstream organizations, the greater the prestige of a young company’s investment bank at the time of the IPO.

Although we have argued thus far that more of each of three types of upper echelon

affiliations are better, a young firm must convince outsiders that it has, concurrently,

technological, organization-based, and market-based quality when courting an investment bank.

Having prominent upper echelon affiliations across all three categories signals the potential for a

firm’s access to capabilities and connections with respect to all of the aforementioned aspects of

firm quality. Signals of such skills and connections complement one another; they are not

perfect substitutes since they tap into different dimensions of firm quality that are relevant to

13

external evaluations of the firm’s potential. Thus, a firm with an upper echelon with coverage

across all three types should have an advantage in securing interorganizational endorsements

over a firm with an upper echelon that does not have such range.

From a potential underwriter’s perspective, as an evaluator and decision-maker in the

highly uncertain context that characterizes IPOs in this industry, it is reasonable to expect that

simplified models of reality will be adopted (Simon 1955; March and Simon 1958). As Cyert

and March (1963) described, decision-makers who face uncertain environments are apt to

economize on their evaluation processes by looking for external referents that can allay specific

concerns governing their decision-making. Different types of upper echelon affiliations can

serve as such referents for endorsing organizations—collectively, presenting a simplified story or

social construction of the endorsement situation (Berger and Luckman 1966) that allays multiple

concerns regarding the endorsement decision. The greater the range of ties represented by a

firm’s upper echelon, the greater the confidence an endorsing organization should have in the

firm’s overall ability to attend to multiple aspects of quality, indicating its potential to succeed in

the marketplace. Such a diverse set of affiliations should signal to outsiders both the breadth and

depth of the upper echelon’s capabilities and connections—signaling that the firm both has and

could in the future obtain a variety of valuable resources from prominent firms. Therefore,

Hypothesis 4: The greater the range of prominent upstream, horizontal, and downstream affiliations of a young company’s upper echelon, the greater the prestige of the firm’s investment bank at the time of the IPO. Upper Echelon Affiliations and IPO Success

There is a growing body of organizational research on the factors affecting IPO success

(e.g., Welbourne and Andrews 1996; Mavrinac 1999; Stuart, Hoang, and Hybels 1999;

Welbourne and Cyr 1999). In biotechnology, recent estimates suggest that bringing a product to

14

the market can cost as much as $250 million (Dibner 1999). Moreover, at seven to ten years, the

time to market is very long in this industry (Hamilton 1994). Therefore, it is extremely difficult

for young biotechnology firms to generate internally the resources they need to survive (Aldrich

and Pfeffer 1976). The IPO therefore plays a crucial role in a biotechnology firm’s ability to

maintain itself.

Prior research on IPOs in the biotechnology industry has demonstrated that

interorganizational affiliations can affect IPO success. For instance, research on biotechnology

firms has shown that IPO success is influenced by the number of directors from top venture

capital firms (Finkle 1998), by the number of alliances and geographical position of the firm

(DeCarolis and Deeds 1999), and by the prominence of the firm’s equity investors, alliance

partners, and lead investment bank (Stuart, Hoang, and Hybels 1999). An underlying claim of

these studies is that prominent affiliations benefit firms because of a transfer of status through

which prominent associations provide endorsements of the young firm’s quality; thus, the

reputation of firm-level affiliations can have implications for a firm’s identity (Benjamin and

Podolny 1999). An upper echelon’s affiliations may therefore be significant not only for

investment bank choice but also for IPO success. Upper echelon affiliations should affect IPO

success not only through their effect on the firm’s ability to partner with a prestigious investment

bank but through their effect on perceptions of firm quality in the eyes of potential investors.

Throughout the IPO process, the primary role of the investment bankers, particularly the

lead bank in the syndicate of managing underwriters, is to broker the IPO deal. Firms do not sell

shares to the public directly; rather, firms sell stock to the banks at a negotiated discount, and the

banks, in turn, sell stock to dealers and to their institutional and retail investors. Thus, the capital

raised at the time of the IPO is a direct result of the investors’ interactions principally with the

15

managing underwriter. Furthermore, given the relative inexperience of investors compared to an

investment bank’s research analysts in evaluating young firms undertaking an IPO, investors are

apt to rely on the endorsement of the managing underwriter when deciding whether to buy stock

in the young firm (see Bochner and Priest 1993). The more prestigious the lead investment bank,

the more valuable the bank’s role as mediator, since prestigious banks are regarded as especially

adept at evaluating the quality of young firms (Carter and Manaster 1990).

Still, it is also the case that during the “road show,” when the firm is pitched to potential

investors, the backgrounds of the managing officers and directors are presented; thus, the quality

of the affiliations of a firm’s upper echelon may also have direct effects on investors’ decisions

to provide financial resources. Therefore, while we expect to find that the prestige of the

investment bank mediates the relationships between upper echelon affiliations and IPO success

due to the broker role that the lead underwriter plays in the IPO process, we do not expect this to

be a strong form of mediation. We expect that upper echelon affiliations will have a direct effect

on IPO success before considering the prestige of the lead underwriter and that, after considering

investment bank prestige, these effects should weaken, yielding the following predictions:

Hypothesis 5a: The greater the number of upper echelon affiliations with prominent downstream, horizontal, and upstream organizations, the more successful the firm’s IPO. Hypothesis 5b: The prestige of the firm’s investment bank will partially mediate the relationship between the number of upper echelon affiliations with prominent organizations and indicators of IPO success.

METHOD

Sample and Data Collection

Our sample frame includes U.S. biotechnology firms that were founded between 1961

and 1994. Of these 838 firms, 296 went public between 1979 and 1996. Approximately 86% of

the public firms specialized in the development of therapeutics and/or human diagnostics; the

16

majority of the remaining firms specialized in agriculture and/or other biological products,

generally with the explicit intention of engaging in therapeutic applications in the future. The

average time to IPO in our dataset was 4.87 years.

We compiled our data from both published and unpublished sources, striving to be as

thorough as possible, yet focused on true, dedicated biotechnology firms. Our primary list of

public biotechnology firms was obtained from the BioWorld Stock Report for Public

Biotechnology Companies in 1996 (n = 281). Unlike other sources (e.g., BioScan), this listing

does not include large corporations (e.g., General Electric) that participate tangentially in the

biotechnology industry; hence, ours is a narrower definition of biotechnology than that employed

by other researchers (e.g., Barley, Freeman, and Hybels 1992) and is in line with more recent

research on the industry (e.g., Powell, Koput, and Smith-Doerr 1996; Stuart, Hoang, and Hybels

1999). Further, to guard against sample selection bias associated with this listing, we collected

information on firms that went public in the same time frame as our sample but that did not

survive in their original form by 1996. To do this, we obtained information from organizations

that specialize in conducting research on the biotechnology industry, including BIO, the North

Carolina Center for Biotechnology Information, Recombinant Capital (ReCap), and the Institute

for Biotechnology Information. We also compared three editions of Biotechnology Guide USA

(Dibner 1988, 1991, 1995). From these sources, we identified an additional 15 dedicated U.S.

biotechnology firms that went public but were not in existence in their original form in 1996.

Such firms had experienced name changes, merged, or had been acquired. These firms were

founded in the same time period and all had gone public by the end of 1996.

We also collected information on biotechnology firms that were founded in the same time

period as our sample but that did not go public by 1996 (n = 542) from the 1998 edition of the

17

Institute for Biotechnology Information (IBI) database. We added to this list private

biotechnology companies that were listed as “dead,” merged, or acquired in the first three

editions of the Biotechnology Guide USA (Dibner 1988, 1991, 1995) and that had a founding

date in the same time period as our core sample. Combining these private firms with our sample

of firms that did go public yielded a final combined sample size of 838 firms.

Our main variables of interest were drawn from the career histories of the over 3200

managing officers and directors that comprise the upper echelons of the 296 firms in our core

sample. Information on these individuals and their firms was manually obtained from the firms’

final prospectuses. The upper echelon was defined as the directors and managing officers listed

in the final prospectus. In filing with the SEC, firms are required to list the last five years of

experience of the firm’s managing officers and board members; additional information (e.g.,

educational background) may be listed but is not required by the SEC. We consulted additional

sources such as Dun and Bradstreet for cross-verification.

Finally, we conducted field and ethnographic analysis at 14 biotechnology firms in the

U.S., two investment banks, one venture capital firm, and one of the Big 6 audit firms. The

individuals to whom we spoke at the service organizations were all intimately involved in

various IPO deals in the biotechnology industry during the period of our study and provided

extremely helpful information to us about the complexities involved in taking a firm public.

Among the biotechnology firms, we completed 12 formal interviews, ranging in length from 1.5

to 4.5 hours each. Five of those interviewed were in business-related positions (chief executive

officer, chief financial officer or chair of the board), while the other seven were in senior

research positions. We gathered career history information through semi-structured interviews

for all of the individuals in the biotechnology firms, as well as information on their roles in their

18

firms and in the IPO process. In addition, we solicited ongoing input from one expert informant

who has worked at two different biotechnology firms, one large and one small, and who was

centrally involved in two IPO deals.

Dependent Measures

Prestige of investment bank. Investment bank prestige was measured using an index

developed by Carter and Manaster (1990) and then updated by Carter, Dark, and Singh (1998).

The measures are based on analyses of investment banks’ positions in the tombstone

announcements for IPOs and have been cited widely in both finance and organizational research

(e.g., Bae, Klein, and Bowyer 1999; Podolny 1994; Rau 2000; Stuart, Hoang, and Hybels 1999);

this information was available for all but 25 of the underwriters in our dataset (accounting for 55

of our firms). Scores may assume a value ranging from 0, indicating lowest prestige, to 9,

indicating highest prestige. In our data set, the mean score was 7.63. Carter and Dark’s (1992)

analyses suggest that these measures provide a finer-grained evaluation than a simpler market

share alternative (e.g., Megginson and Weiss 1991). We obtained the name of the lead

investment bank from the front page of the final prospectuses.

IPO success measures. We used three indicators of IPO success, both financial and

nonfinancial indicators, to provide a comprehensive test of IPO success. The indicators we used

reflect the immediate or short-run success of the IPO; we did not consider longer-run measures.

(a) Net proceeds that a firm obtains as a result of the offering is one important indicator

of IPO success. This is the amount of cash the firm receives as a result of the offering, less costs

incurred during the IPO process. This information was on the first page of the prospectuses.

(b) Number of institutional investors captures the quantity and type of investors that the

firm attracts during the IPO process. Upper echelons with prominent organizational affiliations

19

should be more likely to obtain endorsements from key members of the investment community,

including not only prestigious investment banks but also quality investors. For firms,

institutional investors are preferable to retail investors, since, unlike high net-worth individuals,

they tend not to churn the stock of a young firm. Their goals also tend to be more aligned with

those of young firms, and thus are better positioned to help firms build long-term earning power

(Porter 1992). Therefore, the extent to which a firm is endorsed by institutional investors may

also be an indicator of IPO success.

We obtained information on the institutional investors who endorsed our firms from

CDA/Spectrum Institutional Ownership Database from Thomson Financial Publishing. The SEC

requires institutions to reveal all of their stock holdings by filing 13-F forms. The Spectrum

database “reverse”-compiles these on a quarterly basis, so that information may be obtained for

companies invested in, rather than the company doing the investing. For our study, we looked at

listings for our biotech companies for the first report after the IPO date. From Spectrum, we

were able to determine every institutional investor at that time and the percentage of available

shares that each of those investors held. Using these data, we first determined the number of

institutional investors that invested in the firm.

(c) Number of “dedicated” institutional investors was a third way we calibrated IPO

success. Research by Bushee and Noe (2000) has shown that institutional investors may be

classified into three different categories based on the rate at which they turn over their portfolios

and the extent to which the blocks of shares they purchase are diversified. The most savvy or

relationship-oriented investors, what Bushee (1998) termed “dedicated” investors, tend to have

low portfolio turnover and low diversification strategies. Compared with other more “transient”

institutional investors, dedicated institutional investors are most likely to be focused and

20

interested in the company’s longer-term growth prospects and so, most likely to have the young

firm’s interests at heart (cf. Porter 1992). We used Bushee’s coding scheme, which classified

institutional investors by year to categorize our institutional investors. We then calculated the

number of dedicated institutional investors that invested in each of our firms.

Independent Measures

Upper echelon affiliations. The affiliations of the upper echelon were assessed by

identifying and manually coding the last five years of their employment and board memberships,

as listed in the firms’ final prospectuses. We assessed the number of ties each individual had to

prominent upstream, horizontal, and downstream organizations. We created indices of

organizational prominence for each of our three categories, only looking at ties linking

individuals with prominent organizations. Since the number of ties covaries with the size of the

upper echelon, we divided upstream, horizontal, and downstream tie measures by upper echelon

size, consistent with recent research (Geletkanycz and Hambrick 1997).1

To gauge whether particular downstream and horizontal affiliations were with prominent

institutions or not, we used the amount of domain-specific firm revenues as a proxy for

prominence. To gauge whether upstream affiliations were with prominent organizations, we

employed external evaluations of the research institutions.2

For upper echelon upstream affiliations, we assessed the number of prominent research-

based affiliations of members of a firm’s upper echelon through board seats or employment (e.g.,

professorship). Seven editions of the Gourman Report (Gourman 1980, 1983, 1985, 1987, 1989,

1993, 1996) were used to compile the list of prominent research institutions. We coded any

academic institution that appeared on the top 10 in any of the following disciplines as prominent:

microbiology/bacteriology, biochemistry, biomedical engineering/bioengineering, molecular

21

biology, cellular biology, chemistry, and medicine. A total of 21 academic institutions were thus

coded as prominent. National government institutions such as the NIH were added to

this list, as were non-university research institutions that received a high ratio of grant money per

employee (e.g., the Salk Institute) (n = 9). The upper echelons in our sample generally had two

people with at least one tie to a prominent research institution. Amount of upper echelon

upstream affiliations was measured as the total number of upper echelon affiliations with

prominent research organizations, as defined above.

For upper echelon horizontal affiliations, we assessed the number of affiliations that

members of a firm’s upper echelon had to prominent biotechnology firms through employment

and/or board memberships. We generated the list of prominent biotechnology companies by

taking the list of worldwide revenues for the top 30 biotechnology companies in each of the

years 1990-1996, from POV Inc., “Biotechnology’s Top 50 in Pharmaceuticals and Diagnostics:

A Competitive Analysis” (1997). We coded a biotechnology company as prominent if it

appeared anywhere on this top-30 listing at any time from 1990 through 1996.3 A total of 38

companies were coded as prominent biotechnology firms; therefore, this was a relatively stable

list. The firms in our sample generally had one or two people with an affiliation to a prominent

biotechnology company. The amount of horizontal affiliations was measured as the total number

of upper echelon affiliations with prominent biotechnology organizations, as defined above.

For upper echelon downstream affiliations, we assessed the number of affiliations that

upper echelon members had to prominent pharmaceutical and/or healthcare institutions through

prior employment and/or board memberships. To determine which institutions were prominent,

we generated a list of the top pharmaceutical and healthcare organizations by sales since 1979,

using COMPUSTAT. International companies are only ranked by COMPUSTAT from 1988 on,

22

so our rankings are based on the top 30 U.S. organizations from 1979 to 1987 and from the top

30 U.S. and international organizations from 1988 to 1996. We coded any organization that

appeared on these lists at least once during the 1979-1996 period as prominent. We

supplemented our list with major pharmaceutical and healthcare companies that were private or

based in Europe or Japan that were not listed in COMPUSTAT but were listed in

PharmaBusiness and had comparable sales, since many young biotechnology firms rely on

international resources for support and talent. A total of 56 pharmaceutical/healthcare

companies were thus coded as prominent. The firms in our sample had between two and three

team members with at least one tie to a prominent pharmaceutical or healthcare institution. The

amount of upper echelon downstream affiliations was measured as the total number of

affiliations with prominent pharmaceutical and/or healthcare organizations, as defined above.

We measured range of upper echelon affiliations two ways. First, we used a variation of

the Herfindahl-Hirschman index,

3 H = 1 - ∑ pi

2 (1) i=1

in which H is the measure of heterogeneity or range and p is the percentage of individuals who

have ties to prominent institutions in each of our three categories. This variable was set to equal

zero when the upper echelon had no relevant affiliations. This measure is equivalent to Blau’s

(1977) index of heterogeneity. Second, we measured range as the count, 0 to 3, of the number of

affiliation categories covered. For example, a firm with an upper echelon with 10 members, two

of whom had ties to prominent pharmaceutical organizations, would receive a score of 1, while a

firm with the same-sized upper echelon that included one member who sat on the board of a

prominent biotechnology company’s board and another member who worked for a prominent

pharmaceutical company would receive a score of 2.

23

Control variables. We included several control variables in our analyses to ensure the

robustness of our claims. First, we controlled for uncertainty associated with the stock market

for biotechnology companies at the time our firms went public. We employed a financial index

developed by Lerner (1994) and cited extensively in research in the industry (e.g., Baum,

Calabrese, and Silverman 2000; Stuart, Hoang, and Hybels 1999; Zucker, Darby, and Brewer

1994), that gauges the receptivity of the equity markets to biotechnology offerings. Lerner’s

(1994) index was constructed based on an equal amount of dollar shares of 13 publicly traded,

dedicated biotechnology firms. The findings of Lerner’s study suggest that an industry-specific

index is the preferred method of capturing the favorability of the equity markets, as times of high

valuations vary across industries and not always in complete conjunction the general market.

We used the value of Lerner’s equity index at the end of the month prior to the IPO date for each

of our firms as our indicator of industry uncertainty at the time of the IPO.

In addition, we controlled for technological uncertainty associated with the product stage

of the firm’s lead product at the time of the IPO. We reviewed the company sections of the

prospectuses to determine how advanced the firm’s technology was (Pisano 1991; Pisano and

Mang 1993). We coded the product that was at the latest stage into one of the following nine

categories: discovery stage, research and development, pre-clinical indication, phases I through

III clinical trials, new drug approval (NDA) filing/FDA approval pending, final market approval,

and revenue-generating, relatively speaking. We also examined the use-of-proceeds section of

the prospectus to confirm that the lead product, as defined above, was also that which was

designated to receive the most significant funding. We then used this coding to create a nine-

point categorical variable for product stage, such that those with lower numbers (i.e., earlier

stages of development) were accorded higher uncertainty, while those that had higher numbers

24

(i.e., later stages of development) were accorded lower uncertainty.

We also included controls for firm size and firm age, consistent with prior research on

entrepreneurial firms and studies of IPOs. And, while not a direct indication of the size of the

firm, the amount of private financing the firm received prior to the IPO does provide a reliable

measure of the success the firm has had in the past in securing financial capital and so, is an

indicator of the firm’s potential for growth as well. Our measure of private financing was

calculated by adding up the rounds of financing listed in the final prospectuses. This measure

was adjusted to constant 1996 dollars and logged in our analyses.

We also coded our firms for their geographical location. Young firms located in areas

that are rich with industry-related activity will likely have greater access to resources, including

qualified personnel, suitable lab space, and technology, that can give them an advantage

(Saxenian 1994). Given the research and technology centers of the United States, locational

advantage is likely to accrue to firms that choose to operate in central areas like San Francisco

where the concentration of biotechnology firms is high (Deeds, DeCarolis, and Coombs 1997).

A dummy variable for location took a value of 1 if the main offices of a young biotechnology

company were located in one of the following areas that were consistently rated among the top

four biotechnology locations for the period of our study (Burrill and Lee 1990, 1993; Lee and

Burrill 1995): San Francisco, Boston, or San Diego. Location took a value of 0 otherwise.

In addition, we controlled for the total number of alliances a firm has with business

and/or research organizations at the time of the IPO, since prior research has demonstrated that

strategic alliances have important implications for organizational outcomes. And, given prior

research on the important role of venture capitalists during initial public offerings (e.g., Gompers

et al. 1998), we included a control for the prominence of venture capital firms at the time of the

25

IPO. Firms were coded as 1 if any of the biotechnology firm’s venture capital firms (with a

minimum of a 5% stake) were listed as among the top 20 venture capital firms in the period of

our study and 0 otherwise. Our list of prominent venture capital firms was based on information

compiled by Venture Economics, a company that has tracked the venture capital industry since

the 1960s; rankings are based on total dollars raised each year for the venture funds.

We also included four variables that account for characteristics assessed in upper

echelons research. First, we included a variable for the average prior position level that reflects

the caliber of the prior jobs the executives held. We created a 0 to 5 ranking, ranging from low

to high, beginning with nonmanagement positions and ending with CEO/president, similar to that

employed by Eisenhardt and Schoonhoven (1996) and then calculated the mean level of prior

position for each upper echelon in our dataset. Second, we controlled for the average age of the

executives and directors, which may be considered indicators of the amount and breadth of

experience of the upper echelon. Additionally, we assessed the amount of dispersion of upper

echelon members’ characteristics. We included a variable for the diversity of the tenure with the

firm among upper echelon members. Consistent with prior research, we used the coefficient of

variation for the demographic variable of tenure in the group (Bantel and Jackson 1989; Allison

1978). And, we included a variable for the functional heterogeneity of the upper echelon

members. We coded the previous functional positions of all of the top managers and directors in

our dataset, based on an extension of the coding scheme used by Hambrick, Cho, and Chen

(1996) that also included categories associated with younger research-based firms: chief

scientific officer, founder, researcher, lab manager, and professor. Consistent with prior

research, we used a variation of the Herfindal-Hirschman index,

22 H = 1 - ∑ pi

2 (2) i=1

26

in which H is the measure of heterogeneity or range and p is the percentage of individuals who

have held positions in each of 22 functional categories.

Finally, we included a variable that accounts for the type of business the biotechnology

company was in. Biotechnology is a fairly segmented industry. The applications of its products

range from tissue repair in humans to agricultural products. From the main company description

in the prospectuses, firms were coded as being in therapeutics, diagnostics, both diagnostics or

therapeutics, agriculture, chemical, or other. To verify the firm’s business, we referred to the IBI

database and BioScan. For the private companies, we had information on up to 30 such

categories. For this business type variable, we coded whether the company was in a core

biotechnology field, i.e., therapeutics or therapeutics and diagnostics, or not.

Analysis

There are four dependent variables for this study—prestige of investment bank and three

measures of IPO success. For each set of analyses, we used Heckman selection models to guard

against the possibility of sample selection bias (Heckman 1979). In general, sample selection

can arise when the criteria for selecting observations are not independent of the outcome

variables. As an example, studies of earnings and status achievement of women can run the risk

of sample selection bias if they do not account for factors that affect women’s participation in the

workforce. To correct for potential bias in such studies, sample selection models can be run that

account for women’s entry into the labor market and for the market rewards that they receive (for

a review, see Winship and Mare 1992). Here, since we are studying factors that influence the

prestige of the investment banks that underwrite the firms’ security offerings and IPO success,

both of which only occur when a firm goes public, we want to guard against the possibility that

there is some other factor, in addition to those we study, that accounts for the likelihood of firms

27

being able to go public in the first instance.

Heckman’s procedure generates consistent, asymptotically efficient estimates that can

enable us to generalize to the larger population of biotechnology firms (cf. Heckman 1979). In

essence, the Heckman model is a two-stage procedure that uses the larger risk set of public and

private firms, including firms that ceased to exist as of 1996 in both categories (n = 838). Probit

regression was used to estimate the likelihood of completing an IPO during the first stage, and

estimates of parameters from that model were then incorporated into a second-stage regression

model to predict prestige of investment bank and, in subsequent analyses, IPO success (Van de

Ven and van Praag 1981). For the first stage models, we used the information we had available

for our public and private firms—geographical location, year of founding, and type of

business—to predict likelihood of going public. In the second stage, though the sample includes

all 838 firms, the standard errors reported reflect the smaller sample of firms (n = 296).

To account for the fact that we had net proceeds information that spanned two decades,

we transformed our net proceeds estimates into constant 1996 dollars and logged the estimates

for our firms. And, in order to account for the time-varying market conditions firms faced when

trying to go public, we included the equity index variable described earlier in all of our analyses.

The numbers we used were calibrated not just by the year but also by the month preceding the

offering, which produces fairly fine-grained estimates.

Table 1 summarizes the main variables we test in our analyses and their predicted effects.

**** Insert Table 1 about here ****

RESULTS

Correlations between our main variables of interest are provided in Table 2. This table

shows that the relationships between our key variables of interest are in the directions predicted.

28

The tables that follow, Tables 3 and 4a-4c present our findings for the effects of upper echelon

affiliations with prominent upstream, horizontal, and downstream organizations on the prestige

of the firm’s lead investment bank (Table 3) and for IPO success (Tables 4a-4c). In each table,

the results are presented in a similar fashion: we begin with Heckman selection models that

include the firm and industry-level control variables, traditional upper echelon variables, and

then we include our core measures of upper echelon affiliations. In analyses predicting IPO

success, we test as well for the mediating effects of investment bank prestige (Baron and Kenny

1986). We begin with our analyses predicting investment bank prestige, as shown in Table 3.

**** Insert Tables 2 and 3 about here **** Model 1 in Table 3 includes the control variables associated with the firm and the

industry. As expected, the prominence of the firm’s venture capital firms and the amount of

private financing raised were positively and significantly related to the prestige of the young

company’s lead investment bank at the time of the IPO. Both of these factors remained

significant across all of the models predicting investment bank prestige. Model 2 includes upper

echelon variables that have been investigated in prior research. Here we find that the average

prior position level of the upper echelon members and firm size are positively related to

investment bank prestige.

Hypothesis 1 predicted that upper echelon affiliations with prominent upstream

organizations would be positively related to the prestige of the firm’s lead investment bank. As

shown in model 3, we did not find support for hypothesis 1. However, hypothesis 2, that upper

echelon affiliations with prominent horizontal organizations would be positively related to

investment bank prestige, was supported, as shown in models 4 and 5. Moreover, we found

support for hypothesis 3 with respect to downstream affiliations, as shown in model 5: the

29

greater the upper echelon members’ ties to prominent pharmaceutical and/or healthcare

organizations, the greater the prestige of the firm’s lead investment bank. We also found

substantial support for hypothesis 4, as shown in model 6 of Table 3: the range of upper echelon

affiliations had a significant and positive effect on investment bank prestige. Since range was

constructed from the three forms of upper echelon affiliations, it is informative to present the

results for range apart from the proportion of variance explained by our three types of upper

echelon affiliations. Our heterogeneity measure of range was correlated > .90 with our count

measure of range; the latter, count measure is reported in our tables. The final model does

include all upper echelon affiliation variables and shows a significant effect for both downstream

affiliations and range of affiliations on investment bank prestige. We expect that the loss of the

effect for horizontal affiliations in this final model is due to the significant correlation between

range and the other affiliation variables from which range was constructed.

**** Insert Tables 4a through 4c about here ****

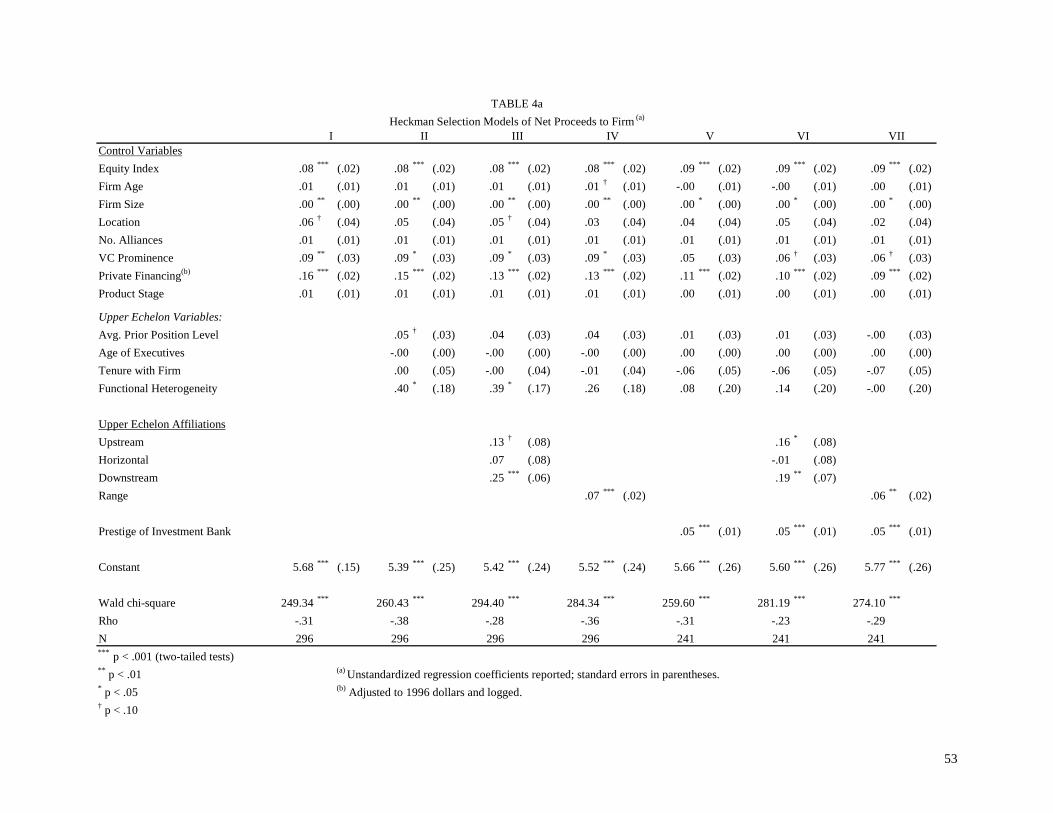

Table 4a shows the effects of upper echelon affiliations and investment bank prestige on

the first of the three measures of IPO success, net proceeds to the firm. As expected, the

affiliations of the upper echelon were significantly related to the firm’s proceeds from the

offering. Models 3 and 4 of Table 4a support hypothesis 5a by demonstrating direct effects for

the upper echelon’s downstream affiliations and for the range of the upper echelon’s affiliations

on the firm’s net proceeds. These effects for upper echelon downstream affiliations and range of

affiliations remained significant even after we accounted for the prestige of the investment bank,

as shown in models 6 and 7. In addition, we note that upper echelon upstream affiliations was

significant in model 6. These results provide support for hypothesis 5a.

To test for partial mediation, we followed procedures outlined in Baron and Kenny

30

(1986) and Sobel (1982). The results, as presented in Table 4a, suggest evidence of mediation

since (a) downstream and range of upper echelon affiliations were positively associated with

investment bank prestige and with net proceeds, (b) investment bank prestige was positively

associated with net proceeds, and (c) when the investment bank prestige variable was entered

into the analyses along with downstream or range of affiliations, these effects on net proceeds

decreased both in magnitude and in significance level. Further, we tested the significance of the

indirect effects of the independent variables on the dependent variable via the mediator, as

outlined in Baron and Kenny (1986). Specifically, for each upper echelon affiliation variable,

we calculated the regression coefficient corresponding to the mediated path, which is the product

of the coefficient from the first stage regression (predicting investment bank prestige) and the

coefficient from the full second stage regression (predicting net proceeds, with all the other

variables in the model). The standard error for this combined coefficient is calculated using

Sobel’s (1982) formula. Both with respect to upper echelon downstream affiliations and range

of affiliations, we did find corresponding p-values < .05, (for range, p = .01; for downstream

affiliations, p < .01), suggesting that investment bank prestige did partially mediate the

relationships between upper echelon affiliations and IPO success, as hypothesis 5b predicted.

Table 4b shows the results for the effects of upper echelon affiliations on a nonfinancial

indicator of IPO success—the number of institutional investors that endorsed the young firm.

These results also support hypothesis 5a: upper echelon downstream affiliations had a

significant and positive effect on IPO success. We also found that the effect for downstream

affiliations weakened once we included the prestige of the firm’s lead investment bank,

suggesting that investment bank prestige may partially mediate the effects observed. To confirm

the finding of partial mediation, we used the same procedure as before; here, we tested the

31

significance of the indirect effect of IPO downstream affiliations on the dependent variable,

number of institutional investors, via investment bank prestige, the proposed mediator. Again,

we found evidence of partial mediation (p < .05), lending support to hypothesis 5b.

Table 4c presents our results with respect to the effects of upper echelon affiliations on

IPO success, gauged by investment in the firm by dedicated institutional investors. Once again,

we found that the greater the number of downstream (i.e., pharmaceutical/healthcare affiliations)

the upper echelon had, the greater the success of the IPO as indexed by the number of dedicated

institutional investors who invested in the firm. These results also support hypothesis 5a. We

found additional support for the effect of upper echelon range on the extent of endorsement by

dedicated institutional investors, but, as was the case in the prior series of analyses, we found no

effects for upstream and horizontal affiliations on IPO success. When we added investment bank

prestige to our models (models 6 and 7), the effect for downstream upper echelon affiliations on

the number of dedicated institutional investors disappeared but the significance level of the effect

for the range of upper echelon affiliations remained the same. Further analyses, using Sobel’s

(1982) formula to test for partial mediation, suggested that while the effect of upper echelon

downstream ties disappeared in model 6 of Table 4c, the drop in magnitude of the coefficient

was not sufficient enough to suggest full mediation. Rather, we found additional support for

hypothesis 5b – here, that investment bank prestige partially mediates the relationship between

upper echelon downstream affiliations and the number of dedicated institutional investors that

invested in the firm at the time IPO (p < .05).

Looking across Tables 4a through 4c, there are some interesting patterns with respect to

our control variables as well. First, in all of the analyses, the prominence of the firm’s venture

capital firms had a significant and positive impact on IPO success. Second, in all but three

32

models across all of our sets of analyses, the amount of private financing the firm received prior

to the offering had a significant and positive impact on IPO success. And in most instances, our

results suggest that larger firms tend to have more successful IPOs. We also found evidence to

suggest that older firms in this industry have more successful initial public offerings than

younger firms, consistent with prior research, although the prestige of the investment bank seems

to account for most of this variance.

Additional Analyses

We conducted two sets of additional analyses. First, since our claims centered on the

signaling value of upper echelon affiliations, we tested whether our effects were especially

strong during times of high uncertainty. In particular, we tested whether having ties to

prominent organizations was especially valuable to a firm when its lead product was in early

stages of development. Results revealed significant and negative interaction effects between

product stage and upper echelon horizontal and downstream affiliations suggesting that upper

echelon horizontal affiliations are particularly helpful to young firms in securing the backing of a

prestigious investment bank when the firm’s lead product is in early stages of development.

Further, upper echelon downstream affiliations have a particularly beneficial effect on IPO

success when the firm’s lead product is in early stages. The latter results held for two of our

three measures of IPO success (number of institutional investors and number of dedicated

institutional investors) and remained significant and in the direction expected, even after we

accounted for the prestige of the firm’s lead investment bank.

Second, we investigated the effects of the sum of downstream, horizontal, and upstream

affiliations for the entire upper echelon versus for just the core members of the upper echelon

who tend to be most engaged in the IPO process (the chief executive officer (CEO), head of

33

finance (e.g., chief financial officer), and the head of research (e.g., chief scientific officer or

equivalent)). We found that the sum of our three types of prominent affiliations across the entire

upper echelon was significantly and positively associated with the prestige of the firm’s lead

investment bank and with all of our measures of IPO success. With respect to the core team,

however, we found different results. Including a variable for the sum of core upper echelon

affiliations across our three categories did not have a significant effect on IPO success. Thus, we

found evidence to suggest that it is the affiliations of the entire team, rather than that of a few key

members of the upper echelon, that account for the effects of upper echelon affiliations on firm-

level outcomes.

DISCUSSION AND CONCLUSIONS

The present study shows that the proclivity of firms to enter partnerships with prestigious

intermediaries and to garner the support of investors is influenced by the amount and kind of

career-based affiliations associated with the firm’s upper echelon at the time of its IPO. An

upper echelon’s affiliations with prominent organizations differentially affect a young

company’s ability to secure the endorsement of prestigious others. In particular, the greater the

number of the upper echelon’s horizontal affiliations with prominent biotechnology

organizations and the greater the number of the upper echelon’s downstream affiliations with

prominent pharmaceutical and/or healthcare organizations, the greater the prestige of the firm’s

lead investment bank. In addition, the greater the range of upper echelon affiliations across these

three categories, the greater the prestige of the firm’s investment bank. These results suggest

that important intermediaries such as investment banks look beyond objective measures such as

firm size, age, or product stage, to the career histories of those leading the firm, for indicators of

firm quality when deciding whether to endorse them.

34

In most cases, we did not find evidence to suggest that upper echelon upstream

affiliations affect interorganizational endorsement or IPO success. One possible explanation is

that investment bankers look at alternative information to assess whether a firm’s science is

sound. Alternatively, a firm’s scientific-based affiliations may be underrepresented in the firm’s

final prospectus, limiting the extent to which we were able to capture signals of technological

quality associated with a firm’s affiliations with upstream organizations in the present study.

Our analyses predicting IPO success suggest that investors attend to multiple types of

affiliations—to upper echelon affiliations with prominent institutions and to the prestige of the

lead investment bank with which the firm is tied. As a contribution to the growing body of

organizational research on IPOs, we tested our hypotheses with a comprehensive set of indicators

of IPO success. We found significant and positive effects for downstream affiliations for all of

our measures and, in subsequent analyses, for the sum of downstream, horizontal, and upstream

affiliations of the upper echelon as well. Further, our additional analyses on the contingent value

of upper echelon affiliations demonstrates that under conditions of uncertainty, when the firm’s

lead product is in early stages of development, upper echelon affiliations are especially valuable

to a young firm’s ability to secure organizational endorsements and to have a successful IPO.

These analyses lend support to the signaling claims set forth in the present study.

When the prestige of the firm’s lead investment bank was accounted for in our main

analyses predicting IPO success, some interesting results emerged. We expected to find that

investment bank prestige partially mediates the relationships between upper echelon affiliations

and IPO success—for example, that the positive effects for upper echelon downstream

affiliations with prominent pharmaceutical and/or healthcare companies on IPO success would

weaken after we included investment bank prestige in our analyses. We found consistent

35

evidence that investment bank prestige does partially mediate the relationships between upper

echelon downstream affiliations and IPO success. Interestingly, however, this was not always

the case for the other types of upper echelon affiliations. We found that the range of upper

echelon affiliations remained significant throughout our analyses predicting number of dedicated

institutional investors, suggesting that the ultimate investors in a young firm attend directly to

signals of firm quality, particularly when such investors are focused and “dedicated” in their

decision-making. In such instances, the range of affiliations of a firm’s upper echelon may

project a simple story that signals the young firm’s potential, affecting valuable second-order

endorsements of a start-up firm.

The results for the other independent variables included in our analyses yielded additional

insights. Looking across the OLS regression and sample selection model results for prestige of

investment bank, we found consistent evidence that the prominence of venture capital

organizations was associated with the prestige of the firm’s investment bank and some

suggestive evidence for the number of strategic alliances a firm had as well. These results are

consistent with the view that external parties look to the involvement of other firms when

gauging whether to join up with a young firm. The present research supports the idea that the

firm’s affiliations with prior organizations affects subsequent alliance formation (Kogut, Shan,

and Walker 1992; Gulati and Gargiulo 1999; Powell, Koput, and Smith-Doerr 1996) and extends

prior research by considering the affiliations made available to firms through the preexisting ties

of its upper echelon members.

The present study contributes to research on interorganizational relationships in several

respects. First, it highlights the important role that intermediaries play in the life of a young

firm. In general, the role of third parties in helping a firm obtain much-needed resources from its

36

environment has been underexamined (for a recent exception, see Zuckerman 1999). More

specifically, the origins of organizational endorsements have been overlooked. Our results

suggest that the backgrounds of those who lead and manage a young firm send powerful signals

to external parties that affects the endorsement process. In mediated markets such as the IPO,

organizations have limited prior interaction patterns with one another. In such contexts, a wide

variety of indicators of firm quality—including those that derive from a firm’s connections

through its upper echelon members—can provide important cues that may facilitate

organizational endorsement.

Future research could examine more fully the array of factors that motivate an

intermediary’s decision to endorse a young firm. Comparative research may support our

contention that intermediaries have different motivations and interests than do those in other

types of arrangements such as strategic alliances. The joining up process with a prestigious

investment bank generally reflects a process of endorsement rather than a process of selection on

the part of the focal firm. Moreover, the investment bank assumes relatively little long-term

financial risk compared with, for example, an alliance partner in a joint venture. Finally,

intermediaries serve as brokers between investors and the firms they endorse; they are boundary

spanners that enable a firm to obtain resources. The triadic nature of the process by which firms

and their top executives secure resources in their environments is worthy of future research.

Second, our research adds to the significant stream of research on prominence (e.g.,

Benjamin and Podolny 1999; Podolny 1993; Stuart, Hoang, and Hybels 1999). Such research

builds directly from the principal of the Matthew effect, which refers to the tendency for credit or

benefits to accrue to those have already obtained success: as Merton (1973) argued in his study

of elite scientists, prestige tends to beget prestige. The typology we employ in the present study

37

introduces sharp distinctions between organizational affiliations, enabling a richer understanding

of the conditions under which transfers of status—here, from prominent upper echelon

affiliations to prestigious investment bank affiliations—are likely to occur. And by focusing on

one particular industry and on one critical resource allocation event in the life of a young firm,

the IPO, we are able to take an in-depth look at the specific aspects of firm quality that are likely

signaled by an upper echelon’s affiliations with prominent firms.

Additionally, the present study is distinctive in that the interfirm relationships we focused

on were assessed at the individual (career history) level, at the upper echelon level, and at the

firm level with regard to the firm’s affiliation with its investment bank and institutional

investors. Seldom has empirical research addressed either how individual-level affiliations can

affect the formation of firm-level affiliations or how group-level ties embedded in members’

employment and board memberships affect the formation of interorganizational ties. Our

findings have implications for research that links micro-level ties to more macro-level

interorganizational ties (Coleman 1990) and to the growth of young firms (Burton, Sørensen, and

Beckman 1998). Our additional analyses investigating the effects of the ties of those with

specific roles on the upper echelon enabled us to specify further the level of analyses that

accounted for the effects observed.

More broadly, the present research extends the embeddedness perspective proposed by

organizational scholars studying the consequences of interorganizational relationships (e.g., Uzzi