Embed Size (px)

Citation preview

Getting Control of Your Labor Burden by: Diane Gilson

Understanding and

Controlling Your

Employee Labor Burden

Costs

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 1

Contents Part I: What Do Your Employees Really Cost? ............................................................................... 5

What is Labor Burden and How Does it Impact Your Business? ................................................. 6

What is the Total Cost for Pat to Perform His/Her Job? ............................................................. 6

Part II: What Should Your Employees Contribute to the Bottom Line? ......................................... 8

Can You Project Pat’s Cost Results to Other Employees? ........................................................... 8

So What Should I Charge Per Hour? ............................................................................................ 9

And Now for the BIG Numbers… ............................................................................................... 10

Part III: To Overtime or Not to Overtime? That is the Calculation… ............................................ 11

Determine If and When Overtime Is Beneficial ........................................................................ 11

The Annual Impact .................................................................................................................... 13

People Issues… .......................................................................................................................... 14

Part IV: Using Burdened Costs & Variance Reports to Improve Operations ................................ 15

Assigning Fully Burdened Costs to Jobs in Progress.................................................................. 15

The Immediate Impact on Your Bottom Line ............................................................................ 16

Any Other Ways to Use Variance Reports? .............................................................................. 17

Part V: Assigning Direct, Indirect, Admin, and Owner’s Time to Jobs (Part 1) ............................. 18

Sorting Out Employee Roles ...................................................................................................... 18

Direct Labor Costs and Burden Assignments ............................................................................ 19

Indirect Labor Costs and Allocation Options ............................................................................. 19

Where Do Indirect Costs “Live”? ............................................................................................... 20

Part VI: Assigning Direct, Indirect, Admin, and Owner’s’ Time to Jobs – Part 2........................... 21

Sales & Owner Employment Costs ............................................................................................ 21

“Workaround” for the Owner’s Job Time & Cost ..................................................................... 22

Assigning Costs for “Mixed-Use” Employees ............................................................................ 23

Part VII: The Cost of Lost and Wasted Time – aka “Where Did Our Profits Go”? – Part 1 ........... 23

Time as “Profit” ......................................................................................................................... 23

A Story: An Unfortunate Series of Events….............................................................................. 24

What Does This Really Cost? ..................................................................................................... 24

Part VIII: The Cost of Lost and Wasted Time – aka “Where Did Our Profits Go”? – Part 2 .......... 25

How Can I Waste Thee? (Let Me Count the Ways!) ................................................................. 25

Turn Things Around!.................................................................................................................. 28

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 2

Author Diane Gilson is an Advanced Certified QuickBooks ProAdvisor and Certified QuickBooks Enterprise ProAdvisor. She is a trainer and construction accounting coach, and has been a frequent speaker at The International Builders’ Show. Her firm, Info Plus(+)Accounting Inc. offers Internet-based QuickBooks® training and accounting support services for construction companies throughout the U.S.

She developed The eCPA (employee Cost & Pricing Analyzer) Labor Burden Calculator, an Excel-based program

that automatically performs comprehensive labor burden and pricing calculations for up to 200 employees and 25 departments.

Contact Gilson by calling: 734-544-7620 (9-5 Eastern)

or visit BuildYourNumbers.com

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 3

More Essential Financial Tools & Training for QuickBooks Users and Small-to-Mid-Sized Business Owners

Two Affordable Options for Online QuickBooks Training

Is your company losing out because the advanced features you need are buried somewhere

in QuickBooks or Enterprise Solutions? Take a closer look at our accounting lessons where

you’ll learn how to structure your system, enter transactions, and create the reports that can

make a REAL difference in your financial results!

Option 1:

Subscription Program (CAMP)

When you become a member of our Construction Accounting & Manufacturing Program (CAMP) you get:

Full and immediate access to more than 60 individual workshops (listed in Option 2).

Plus: Full and immediate access to 30 subscriber-only classes.

Plus: The ability to acquire Intuit and Info Plus Accounting products at substantial discounts.

Plus: One-to-one Q&A sessions (no additional charge) with your QuickBooks coach and instructor, Diane

Gilson. More info…

Option 2:

Individual Workshops

Study specific topics in accounting, job-cost, or management reporting – day or night – from the convenience of

your home or office. More than 60 individual workshops are reasonably priced to help you jump-start, upgrade,

or master your entire job-cost accounting system. More…

Qlean$tart® Accounting Solutions from Info Plus

eCPA – employee Cost and Pricing Analyzer™

Convert Labor Burden to Profits! Calculate regular and overtime labor burden and employee

billing rates. Display actual, fully-burdened labor costs for each employee (per year, hour, or

minute). Compute exactly what to charge to achieve your desired profit on labor costs. More…

…Watch this eCPA video to see how you can determine profitable labor rates

“35-Point Checkup™” & Action Plan for your QuickBooks accounting system

Get a Clean Bill of Health… You’ll get your own individualized report after we test 35+ of your

most critical job-cost and financial elements and then outline how you can get your system back

on track. More…

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 4

Percentage of Completion Analyzer™

See True Job Profitability for Long-Term Contracts. Don’t rely on guesstimates from job-site

supervisors! Instead, use this tool to perform background calculations and see the exact $ amounts

and journal entries you need to make to accurately adjust income for long-term contracts. (Also

includes sample calculations and overview of “Percentage of Completion” concepts.) More…

Month-End Procedures

Accurate, On-Time Reports – Each and Every Month…These month-end closing, proofing, and

balancing procedures give you the tools you need to review, self-correct, and protect your monthly

records and job-cost reports. This date-driven checklist will help you meet those monthly reporting

deadlines. More…

AccountingPRO™ (QuickBooks file template for construction companies)

Put a Clean Start in your Cart! AccountingPRO™ was created by Info Plus to meet the specific

needs of the construction industry. This flexible, pre-built QuickBooks data file not only saves start

up time, but is designed to help business owners (or their accountants) more easily and effectively

access QuickBooks’ powerful data collection and reporting features. More…

The Cost of Chaos™ Analyzer

“A little here, a little there… pretty soon you’re talking BIG money”

Get the sober truth by using this tool to estimate your own company’s invisible costs and the

impact of lost income. Next, you’ll see the benefits of small, but effective improvements to your

financial, operating, and accounting controls. Finally, decide for yourself: Could an investment in tighter controls and

better financial info have a substantial impact on your bottom line? More…

Cleancut Time$heets™ – English + Spanish OR Cleancut Time$heets™ – English-only

Regardless of Language, Accurate Time Reporting = Better Job-Cost Reports

Job-costing requires employees to accurately record time and activities spent on various jobs

and tasks. Originally designed as a solution for one of our construction clients with Spanish-

speaking employees, this set of Excel-based time sheet templates (construction terms included)

provides varied layouts, streamlines data entry, and is easily customized.

English + Spanish version More… English-only version More…

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 5

Part I: What Do Your Employees Really Cost?

Whether you’re a contractor, supplier, remodeler, builder, service provider, consultant, or other business professional, if you have employees, then you owe it to yourself to understand exactly what each person on your payroll really costs, and how he or she can make an appropriate contribution to your bottom line.

We all know that employees are an expensive, but necessary, component of doing business. We count on them to deliver an honest day’s work for an honest day’s pay, and if they are “direct labor” employees, we try to charge our clients appropriately so we can make a profit on the services they deliver. In the case of

staff employees, we may not be able to directly charge for their time, but we still expect excellent service and value in return for their compensation.

Employee payroll and employee-related costs comprise an extremely large portion of most business entities’ non-refundable cash outlay. And the potential for labor over-runs can be the riskiest element of any project undertaken. Yet, over our years of working with clients, we’ve found that most businesses (and business owners) have never really taken the time to compute the true, total expenses associated with each employee. As a result, those businesses have not taken advantage of the many beneficial ways they could have used that information.

This series is designed to explore the variety of ways you can:

1. Compute and understand the full, true cost of employee labor. 2. Compute what you really should be charging for direct labor employees to meet your

profit goals. 3. Creatively use employee cost (and income) information to positively impact your

bottom line. 4. Measure the cost of lost and/or wasted time. 5. Be certain you are achieving an excellent return on your investment in each employee.

6. Compare and contrast the cost of employees vs. subcontractors or outsourced services.

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 6

What is Labor Burden and How Does it Impact Your Business?

You are probably in fairly close touch with each employee’s hourly wage or salary, and may already have a good idea what payroll taxes cost. But have you taken the time to research and compute all of the additional “hidden” costs associated with each individual? Including (but not limited to):

Paid time-off

Health insurance.

Worker’s Compensation insurance

Uniforms or special work clothes

Training

Equipment and vehicle usage

Workspace (e.g., office or floor space) costs.

So how do we refer to these extra employee-related costs (including taxes)? Here are some of the terms (and calculations) frequently used by businesses who closely track employee costs:

Labor Burden: The costs – above and beyond gross compensation – that are incurred by an employee to perform the work you hired them to do.

Labor Burden Cost per Production Hour (or Fully-Burdened Cost): (Labor Burden Cost + gross payroll labor cost) ÷ the number of actual work (production) hours.

Labor Burden Rate (%) per Production Hour: The additional total labor burden cost,

expressed as a percent, above and beyond regular hourly payroll, i.e., Labor Burden Cost per hour ÷ hourly payroll cost.

After you compute an employee’s fully-burdened labor cost and then divide it by the number of hours that employee actually works on projects, businesses often find that workers typically cost the company from 50% to 150% (or more), above and beyond their gross hourly labor rate. Getting in touch with, and carefully managing, employment-related costs can be the critical difference between staying in (or needing to get out of) business. Let’s review a fairly simple example.

What is the Total Cost for Pat to Perform His/Her Job?

We’ll start with “Pat”, an employee whose hourly compensation is $17, or $35,360 gross annual payroll. As Pat’s employer, you do your research and find out that Pat has a variety of additional annualized costs “attached” to this position:

$3,005 for payroll taxes (based on 2.7% state unemployment on the first $9,000, and no

other state disability taxes).

$3,536 for Workers’ Compensation insurance (at $10 per $100).

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 7

$4,200 for health insurance ($350 per month).

$1,060 for retirement benefits (3% of compensation).

$720 for cell, telephone and/or Internet costs ($60 per

month).

$150 in uniforms (e.g., 4 company shirts at $25, 1 jacket at $50) or for office workers an equivalent amount in coffee(!).

$6,000 in company vehicle usage (depreciation, gas and oil, maintenance, license, insurance, etc.), or for office workers an equivalent amount in equipment usage, maintenance, and office space.

$300 in small tools and equipment usage (at $25 per

month) or for office workers an equivalent amount in office supplies.

$708 estimated annual bonus (2% of wages).

$100 employer-paid snacks, meals, parties, entertainment.

$250 in training fees, seminars, etc.

Total additional costs: $20,029.

How Many Hours is Pat Actually Available to Work?

Next, let’s determine how many hours Pat is potentially available for company work. Start with

52 weeks/year x 40 hours/week = 2,080 hours.

Then subtract Pat’s non-project paid time for the year:

6 holidays (changed to numerals since it’s a math calculation)

10 vacation days

6 sick or personal days

2 days of training seminars.

This equals 24 days (192 hours), leaving 1,888 available working hours.

You’ll then subtract an estimate of 2 hours from the 47 remaining work

weeks for miscellaneous administrative meetings, timekeeping, general problem-solving or prep time and so forth (breaks are assigned to jobs or projects). This reduces the available production time by another 94 hours.

Total time available for production/project work: 1,794 hours.

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 8

The Final Result of Pat’s “Numbers”

First, Pat’s additional Labor Burden Costs total just over $20,000. This brings Pat’s annual cost to $55,389.

Therefore Labor Burden Cost per Production Hour (or Fully-burdened Cost) for your company is $30.87 per production/project hour ($55,389 ÷ 1,794 hours) or $0.51 per minute.

To compute Pat’s Labor Burden Rate (%) per Production (work) hour, subtract Pat’s hourly rate from his/her fully burdened cost ($30.87 - $17.00 = $13.87) and divide the excess by the base hourly rate. We see that our additional cost to have Pat “on the job”, when computed as a percentage, adds 82% to Pat’s base hourly rate.

The bottom line: Pat is a truly costly and valuable asset whose time should be carefully assigned. And his/her related costs (and resulting contribution) should be closely measured and

monitored!

Part II: What Should Your Employees Contribute to the Bottom Line?

What do your employees really cost per production hour and how much should you charge for employee labor? Are each of your employees making a positive difference in your bottom line? Whether you have 1, 40, or 80 employees, it pays to know your labor burden numbers inside and out, so you can use that data to increase your bottom line. Here are some ideas how to use that

critical information to make a positive impact in your take-home pay!

Can You Project Pat’s Cost Results to Other Employees?

It’s tempting to think you can perform labor burden calculations for just one or two employees, or simply run totals across your company, but there are several good reasons to perform these calculations for each individual employee:

1. Paid time-off benefits can vary significantly between employees.

2. Fringe benefits can vary. 3. The cost of utilized resources can fluctuate

from employee to employee (i.e., certain

individuals may require vehicles or high-end equipment, while others don’t.)

4. Base rates of pay differ, and impact percentage calculations.

5. Knowing an individual’s results can influence goals regarding their anticipated earned income or level of contribution to company objectives.

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 9

Of course, after you’ve performed individual computations, you may want to create employee

groupings and create averages for different levels of employees (e.g., apprentice, mid-level, supervisor, admin, etc.) for estimating and/or pricing purposes. Alternatively, you may prefer to total and average results by department or (especially for manufacturers) by work process.

Get Comfortable With the Numbers!

After performing initial labor burden cost calculations, you’ll want to closely review the various elements and calculation formulas. See if it all makes sense. Spending time to get familiar with the results will help you make better business decisions. We’ll be exploring a number of ways you can use this new information to make better pricing and hiring

decisions, set employee expectations, build a stronger team, and increase profits – so you’ll want to be sure your assumptions and computations are accurate, and that you feel comfortable with what they are telling you.

So What Should I Charge Per Hour?

In this case, after performing our computations, you’ve discovered that Pat’s real cost per production hour was actually $30.87 per hour, and you’d like to know what billing rate to use for Pat. So, the next question to ask is “What is your target gross profit percentage?” Or more accurately, we should ask “What is your target gross profit percentage for employee labor?”

Why? Well, if your gross profit goal is 25% and you mark up all elements of your job equally, you would mark up all costs 33.3%. You would therefore bill Pat out at $41.15/hour to arrive at a 25% gross profit ($30.87 x 1.333).

But because your gross profit is made up of various elements (labor, subcontractors, materials, and other costs), many companies mark up individual aspects of the job differently. Therefore

look at what you want to achieve with each element to reach your “blended” total gross profit target.

For example, if your gross profit goal for a project is 25%, but your gross profit on materials is going to be 15%, and your gross profit on subcontractors is going to be 20%, you will need to reach for a much higher profit on your employees. Let’s look at the results for that type of

“mixed bag” scenario:

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 10

You can see that because your gross profit for materials and subcontractors is well below your total gross profit goal of 25%, you’ll need to make up the difference on your employee labor. So to hit your overall goal for this job you’ll need to bump your employee gross profit to 37%,

which means a markup of 58.8%. So in this case you’ll need to bill Pat at $49/hour ($30.87 x 1.588).

In this next scenario, you’ve decided you can only look for a gross profit of 10% on your job materials (we’re holding subcontractor gross profit steady for this example). This means the employee labor gross profit needs to be increased to 40%, which requires a markup of 66.7%. For Scenario 2 Pat will need to be billed at $51.50/hour ($30.87 x 1.667) to achieve your target gross profit.

So, you can see the billing rate range for these different situations is fairly broad – from $41.15 per hour to $51.50 per hour.

And Now for the BIG Numbers…

In Part 1, we determined that Pat actually has

1,794 potential production (billing) hours. Let’s look at the annual difference in potential annual income from Pat’s activities:

$41.15 x 1,794 hours = $73,823 $51.50 x 1,794 hours = $92,391 Difference = $18,568

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 11

Let’s say that you have 6 employees at Pat’s level…that means the variance between high and

low of $18,568 would be multiplied by 6 to equal a $111,408 difference in your bottom line.

I think you’ll agree that these kind of numbers make it worth your while to closely calculate what your employees’ billing rates should actually be!

Part III: To Overtime or Not to Overtime? That is the Calculation…

Is it ever a smart move to utilize overtime, and if so, when? And for which workers? Here are more creative ways to use fully burdened labor cost information to make a positive impact in your take-home pay!

Determine If and When Overtime Is Beneficial

Many company owners keep overtime to an absolute minimum or even forbid overtime work. After all, overtime costs 1.5 times regular wage rates, right?

Although that may seem logical, when you calculate burdened labor costs, overtime may actually cost less per hour because many of the fixed costs of employment (e.g., health insurance) don’t increase with overtime hours. If you compute the numbers on an employee-by-employee basis, and test various overtime scenarios, you will know the real answer. Could overtime be a good financial decision for your company? In many cases, the answer may be “yes”.

To illustrate, here are some examples showing standard and overtime costs for employees with different hourly rates in the same labor burden scenario. The first column (Standard) shows annual hourly and burdened cost results for normal work hours (in this case, 40 hours per week). The next two columns show Overtime hours and related burdened costs at the rate of 50 hours per year and 500 hours per year.

Preceding each example you will see gross base hourly pay, the additional overtime gross pay and the comparison of burdened standard vs. overtime results:

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 12

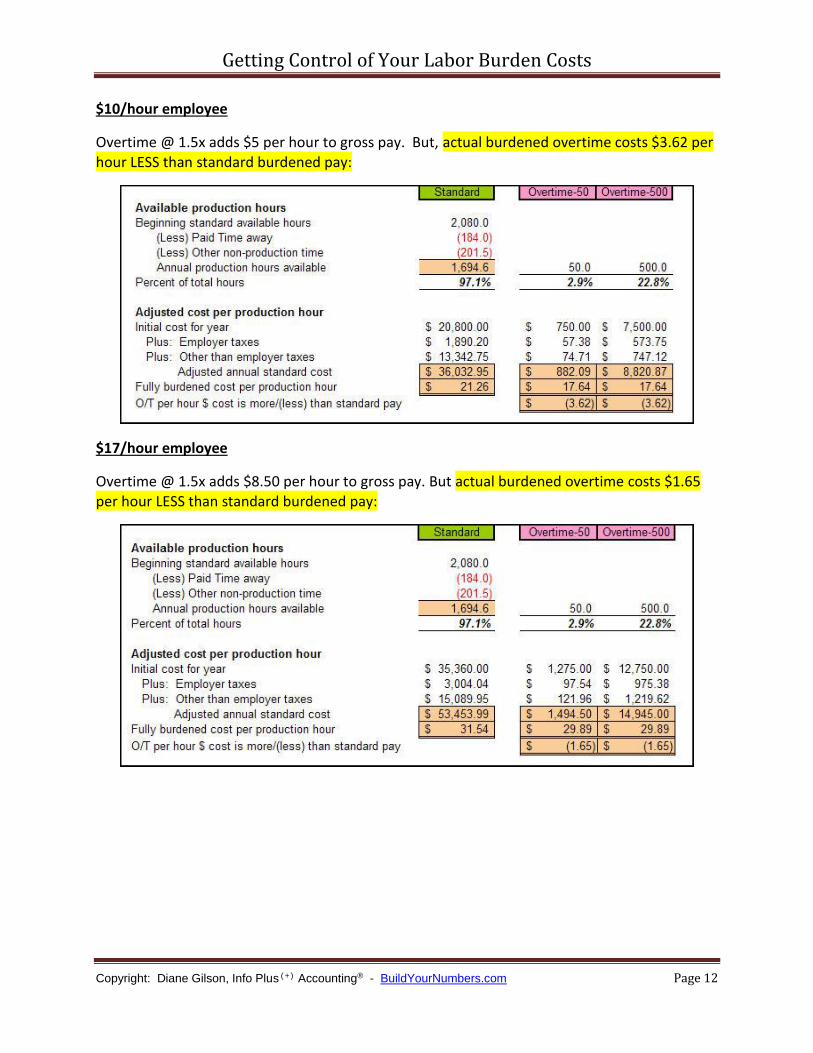

$10/hour employee

Overtime @ 1.5x adds $5 per hour to gross pay. But, actual burdened overtime costs $3.62 per hour LESS than standard burdened pay:

$17/hour employee

Overtime @ 1.5x adds $8.50 per hour to gross pay. But actual burdened overtime costs $1.65 per hour LESS than standard burdened pay:

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 13

$25/hour employee

Overtime @ 1.5x adds $12.50 per hr. to gross pay. But actual burdened overtime costs only $0.59 per hour MORE than standard pay:

As you can see from these examples (based on this set of labor burden circumstances), when you look at the burdened hourly costs, overtime does not cost 50% more than regular pay as most company owners believe. In some cases, overtime actually costs less per hour than standard hours!

The Annual Impact

As you review the preceding examples, please notice that whether the employee works 50 or 500 hours of overtime, the hourly burdened rate (and difference from standard) stays the same.

However, even though the hourly savings on burdened overtime stay consistent, the more overtime worked, the lower the “blended” annual hourly cost of the employee. For example

for our $10 per hour worker:

The standard burdened hourly rate is $21.26 per hour. If that same worker puts in 500 hours of overtime (excluding vacation that would be a

little over 10 hours per work week), at a savings of $3.62 per hour , you have paid $1,810 less for this 500 hours of work than if you were paying another similarly-

burdened worker at standard rates. Therefore the burdened “blended” annual rate for this worker lowers to $20.44 per

hour. (Total cost of [$36,032.95+$8,820.87] ÷ total hours of [1,694.6+500] = $20.44/hour.)

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 14

Unfortunately, general “rules of thumb” about burdened overtime costs (such as “overtime for

lower-paid workers pays off, but not for higher-paid workers”) aren’t accurate because every situation is the unique combination of an employee’s hours, pay rate, benefits, and other added costs. That’s why you need to compute specific numbers for individual employees to determine the best scenario for your company.

Think of the auto companies…you can bet their management accountants calculate and re-calculate labor costs and overtime scenarios on a regular basis!

People Issues…

Of course you’ll want to consider employees’ viewpoints when it comes to overtime:

Some employees find the idea of overtime a hardship and an

infringement on their personal life, and you may encounter resistance – which could ultimately negate the value of overtime work.

Others are diligent workers, could really use the money, and welcome the opportunity to contribute, and earn, a bit more. So, if you have calculated your burden numbers and reviewed the impact of overtime, you may decide that it’s actually a sound business decision to add overtime into their work mix.

In certain cases, even if you’re paying a small amount more per hour, it may still be to

your benefit to allow overtime rather than hire a new worker with the additional time, cost, and risk to your company.

Remember that even for the enthusiastic and willing, the “law of diminishing returns” applies to overtime productivity. Most people can’t work intensive overtime, week after week, without suffering some loss of efficiency, so you’ll want to monitor results to be sure that the overtime is paying off.

Of course, these decisions ultimately lie with you. But if you have access to accurate, burdened labor cost information, you’ll be able to add additional, objective information into your decision-making resource kit.

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 15

Part IV: Using Burdened Costs & Variance Reports to Improve Operations

Using burdened cost information in tandem with internal management reports can help you bring job costs under immediate control, and provide additional ongoing insights into ways to improve your company’s overall performance and productivity!

Estimate Job Costs More Accurately

When you know how much each direct labor employee actually costs per production hour, you can use this information to estimate job costs more accurately.

If you have more than 3 or 4 employees, it’s a good idea to total, and then average, employee

production costs by job level, job stage, and/or by department. For example, you could:

Group by job level: e.g., Interns and apprentices into Category 1; “standard” laborers into Category 2; “master-level” employees Category 3; and supervisors into Category 4.

Group by job stage: If your employee costs more logically accompany work activities performed, then estimate your costs by job stage (e.g., Stage 1-design work; Stage 2-prep work; Stage 3-primary job completion; Stage 4-quality control, Stage 5-shipping, Stage 6-follow up work, etc.).

Group by department: If your company delivers services based on departments, you could group and average your employee costs by Department A, Department B, etc.

By averaging burdened employee costs in a manner that parallels your estimate of time required to complete a job, you can use those averages to achieve more accurate estimates for job costs and pricing.

Assigning Fully Burdened Costs to Jobs in Progress

The problem faced by most companies that perform job costing is that their accounting system has not been set up to automatically assign burden costs to jobs as part of the payroll process. This can be done even though the specifics of how to get your accounting system to assign these additional burden costs to your jobs is outside the scope of this article.

Q. Why is this step important?

A. If you are reviewing job cost reports, and seeing only the gross compensation and payroll tax costs assigned to that job, your job costs are seriously under-stated (i.e., you are looking at misleading information).

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 16

It’s actually possible to see a profit on each job (the appearance is good), but when you see the

total for all jobs including your burden costs, you’ll find that your profit margin has become seriously undermined (the reality is not good). A better idea is to see your true job costs, including burden, as the job progresses, so you can proactively take the steps needed to make the job (including burdened costs) truly profitable.

The Immediate Impact on Your Bottom Line

You can make an immediate impact on your bottom line by heading off labor over-runs before they get out of hand: How? It’s simple:

Regularly review and compare actual burdened job

costs to estimated burdened job costs.

Then use the information from these “variance

reports” to take immediate corrective action if needed.

Companies who keep a close watch on potential cost and labor over-runs review these reports on a weekly or bi-weekly basis. Many company owners share these numbers with job supervisors and include labor variance reviews as a part of their weekly job oversight and control meetings.

Please note that obtaining reliable “Actual vs. Estimate” (variance) reports is directly related to your ability to:

1. Create and enter accurate initial estimates for all job costs (including burdened labor) into your accounting/reporting system.

2. Track and enter estimated Change Order costs into your accounting system as they are generated.

3. Obtain reasonably accurate time-tracking information, by job stage, from employees. 4. Assign job costs (including employees’ compensation and fully burdened costs) to jobs.

Remember that actual labor costs will be accurate only through the most recent payroll posting, and most payroll lags at least a week behind actual work performed, so keep those timing differences in mind when reviewing reports. To compensate for time lag costs, some companies also monitor daily or weekly time reports (i.e., time without costs or with computed anticipated costs).

Use variance reports to continually shift your attention from the job – to the numbers – to the job – to the numbers. This “dual view” approach helps you keep job costs (including labor) on target. If you haven’t been doing this already you’ll probably see some immediate favorable bottom-line changes.

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 17

Any Other Ways to Use Variance Reports?

Yes indeed! Variance reports can be used in several ways after your job is completed. Review the entire results of the completed job. If you’ve established Estimate vs. Actual for various job stages, and segregated burdened labor costs within each major job stage, these reports can offer a wealth of information.

1) For favorable estimate vs. actual results, explore how the favorable results were achieved. You’ll want to learn how to repeat and enhance those ‘winners’.

2) For unfavorable estimate vs. actual results, take an honest look at what happened, and ask the tough questions without blame or recrimination. A clear idea of what went wrong will be the springboard for questions: a) Was the estimate wrong?

(Q. How can we provide better information for the Estimator?)

b) Did unforeseen circumstances crop up? (Q. Is there a better way to react to, or plan for, “unforeseen” circumstances?)

c) Did the workers have inaccurate information or direction? (Q.Is there a better way to provide info or direction on our next job?)

d) Were the wrong workers assigned to the task?

(Q. Which workers should have been assigned? What should happen next time?)

e) Did the customer “get in the middle” and/or were Change Orders not generated”?

(Q. Is there a way to keep clients from interacting with field staff, and/or to ensure that Change Orders are created as needed?)

f) Did the bookkeeper assign costs to the wrong job stage? (Q. How can the bookkeeper easily find out which job stages are assigned to which bills?)

As you establish systems to see fully-burdened labor costs, and take steps to control those costs, you’ll also discover ways to improve your entire operation.

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 18

Part V: Assigning Direct, Indirect, Admin, and Owner’s Time to Jobs (Part 1)

Which employees are assigned to job costs and which to company overhead? Opinions vary, but here are some guidelines and techniques to help you sort everything out and get a better handle on your financial results.

A Frequently Asked Question

“What’s the difference between ‘Direct labor’, ‘Indirect labor’, ‘Sales’, ‘Administrative labor’, and ‘Owner’s compensation’, and which costs should be assigned to jobs?”

This is a common question when company owners begin to compute the true hourly (fully-

burdened) cost for individual employees. Because of the impact each of these expense categories can have on how individual employees’ costs are assigned to specific jobs, each company needs to decide what makes sense for their management and tax reporting needs.

Sorting Out Employee Roles

Although some companies combine employment-related costs into a few accounts (e.g., Salaries, Wages, Payroll Taxes, and other employee burden and benefit accounts), you should organize your Chart of Accounts to display compensation, payroll taxes, and the burden for various employee roles in clearly identifiable groupings. Note: Generally speaking, differentiating between “Salaries” and “Wages”

doesn’t provide any truly useful information for either owners or tax purposes, whereas grouping by direct labor vs. sales, admin, and owner categories is much more useful.

For instance, accounts for Direct Labor gross compensation, payroll taxes, and various burden cost accounts should all be grouped together and sub-totaled. Indirect labor employees, Administrative employees, Sales employees, and Owner’s compensation and benefits should likewise have their own similarly titled account groupings. This separation allows you to:

1) See the cost of each employee category, 2) View your gross profit results clearly, and 3) More easily make any Work in Process and/or Percentage of Completion adjustment entries

that may be required.

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 19

Direct Labor Costs and Burden Assignments

Let’s start out with the easiest employee grouping: Direct labor employees. These individuals are also commonly referred to as “field employees”, “front-line workers”, or “hands-on” employees. They are assigned by company management to work on specific jobs and perform specific activities. It should be fairly easy to assign their time to individual jobs and/or job phases, so this is a clear-cut case where computed fully-burdened employee costs should be assigned to jobs.

For paid time not spent directly on production jobs – such as holiday, vacation, training, etc. – costs should be assigned to a special category called “NJS (Non-Job Specific)”. I usually view all

costs associated with direct labor employees to be part of Cost of Goods Sold (COGS) or production costs, but some accountants assign paid time-off costs to company overhead. Since these costs should be allocated back to jobs as labor burden, it seems more efficient to leave them in the COGS section of the Chart of Accounts under the NJS job – where labor burden costs can be ‘pooled’ until they are allocated back to jobs.

Indirect Labor Costs and Allocation Options

Indirect labor can be more complex since it covers a wide variety of employee titles. Job functions that fall into the “indirect” category include: “Order Taker”, “Designer”, “Scheduler”, “Production Manager”, “Job Supervisor”, “Foreman”, “Lead

Carpenter”, “Production Support”, “Purchasing Agent”, “Estimator”, “Shipping”, “Warehouse”, etc. In short, we’re looking at jobs related to getting production underway or completed, but are a step or two away from “being on the job”. So how should we handle those costs?

The answer varies by company, and type of employee cost, but if you want to see what each job truly costs, here are some general guidelines:

First choice: Assign indirect labor employees directly to production jobs and allocate fully burdened costs accordingly.

Second choice: If production supervision or support cannot be accurately assigned,

then ask for reasonable estimates or percentages of time spent on jobs in progress and assign fully burdened costs accordingly.

Third choice: If the first two options are impractical, then assign the fully burdened cost of supervision or support to the direct labor employees who require or utilize their service.

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 20

For example: Your production supervisor is in charge of 6 direct labor employees and

has a fully burdened cost of $72,000/year. You also have a person who runs errands, delivers materials, and handles various cleanup tasks for the same 6 employees at a fully burdened cost of $30,000 per year. You could add the two costs, and divide by 6 to arrive at the additional $17,000 required to “support” each direct employee. Then add that $17,000 to each direct employee’s burden costs.

This will increase the burdened costs of direct labor employees, and accomplishes the task of pushing (allocating) the indirect employees’ costs out to jobs.

Remaining costs: For employees not providing direct supervision or support to other employees (e.g., “Estimating”, “Purchasing”, “Shop”, etc.), you could create special jobs for each major type of indirect cost

and assign time and fully burdened costs to those jobs (Estimating, Purchasing, or Shop “jobs”). This will allow you to identify all the costs not assigned to production jobs.

Where Do Indirect Costs “Live”?

Some accountants believe that all indirect costs should be part of company overhead as they are somewhat “fixed” in nature, but others (myself included) argue for a more “production-cost placement” approach. I like to see as many of those costs allocated out to jobs as possible, and where allocation is not feasible, assign those costs to special, clearly identified “jobs” as described above.

Why?

1) If all indirect production costs are assigned into COGS accounts, it offers (in my opinion) a more realistic view of production costs.

2) Keeping production costs in one section of the Profit & Loss report allows everyone to see,

at the end of the year, whether burden allocations were accurate.

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 21

Part VI: Assigning Direct, Indirect, Admin, and Owner’s’ Time to Jobs – Part 2

Assigning Sales time and costs, Owner’s time spent on job production activities, and employees’ time on direct, indirect, or admin activities (depending upon need), present special job-costing and measurement challenges. Here are some ideas and insights to help you logically assign unique “time” circumstances to job costs – so your job cost reports truly reflect time spent on jobs!

Sales & Owner Employment Costs

General sales compensation and burden costs are typically considered to be company overhead costs so, in addition to establishing the expense accounts for Sales employees as described in the previous sections, I normally recommend establishing a special “Sales” job for payroll (so that related payroll taxes can be clearly identified and ultimately moved into the correct account grouping). Exception: Most of my clients like to assign sales commissions for specific jobs to the related job. This seems reasonable as it’s a cost clearly linked to the job.

Like sales compensation, Owner’s compensation and burden costs are usually classified as company overhead. But several job-costing issues often arise when I work with owners:

1) Owners who put in production time on specific jobs should be able to see the value of their time assigned to those jobs. But, if their payroll and payroll taxes are assigned to expense accounts as company overhead, then the value of their time doesn’t show up on job cost reports, right?

2) If we assign their time & related costs out to jobs as direct production cost, this could potentially solve the problem, but owners often don’t pay themselves “standard” paychecks (many take draws, distributions, or dividends which reduce equity rather than increase cost), and if they do take compensation, it is often not

scheduled or predictable.

This means we need to get a bit more creative if we want to see owner’s time assigned to jobs and still follow the standardized ways of recording their payroll, payroll taxes, and/or draws or distributions.

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 22

“Workaround” for the Owner’s Job Time & Cost

Here’s an approach that avoids owners’ varying payment-method issues (or erratic owner payroll payments), and yet assigns reasonable owner costs out to job-cost reports:

Determine a “reasonable” fully-burdened cost for the owner’s time IF the owner was charged out to jobs at the going market-rate. I.e., given the owner’s experience and expertise, compute the fully-burdened rate that a comparable employee would cost. For example, let’s say that comes to $110/hour.

Track the time the owner spends on individual jobs.

If the owner receives regular, recurring payroll checks, then:

Post the owner’s payroll and payroll taxes through the standard company overhead accounts.

Establish a new account within the owner’s compensation grouping called “(Less) $ Assigned to Job Costs”. This will be a cost-offset account.

Create an entry that charges (debits) the owner’s hourly costs out to individual jobs.

Post the credit side of the entry into the “(Less) $ Assigned to Job Costs” account. This leaves the actual owner’s payroll and payroll taxes paid out clearly visible in their own accounts, and also shows how much of the owner’s cost has been assigned to jobs.

You will be able to see more accurate (and comparable) job-cost reports, even though

the impact to the bottom line before work-in-process adjustments = $0.

If the owner doesn’t receive regular, recurring payroll (e.g., receives distributions or

dividends vs. payroll), then: Create an entry that charges (debits) the owner’s hourly costs out to individual jobs.

Post the credit side of the entry into the same account as the job costs for individual

jobs, but assign the credit side of the entry to the “Owner” job.

Obtain more accurate job-cost reports, even though the impact to the bottom line = $0.

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 23

Assigning Costs for “Mixed-Use” Employees

Q. I have a production manager (or estimator) who also does field work…how do I assign their costs?

OR

Q. I have office staff members that end up getting pulled out into the field making deliveries or working directly with clients…how do I assign their costs?

Well, with QuickBooks, we’re able to establish Payroll Items that link into the correct account,

so when you enter employee time you can choose Payroll Items that reflect the “mix” that should be assigned when converted into a paycheck. The Payroll Item you choose for the work performed dictates how their time and costs are ultimately assigned into accounts and job costs.

The result? Part of their time and payroll cost is assigned to direct job costs (and regular jobs), while the rest of their time and payroll cost is assigned to “Admin” or “Indirect” compensation or job assignment (this way payroll taxes can be moved into the correct expense accounts).

Part VII: The Cost of Lost and Wasted Time – aka “Where Did Our Profits Go”? – Part 1

Did someone forget to bring the right tool to the job site? Were the wrong parts ordered, or not ordered at all? Did the work crew return 15 minutes late from lunch? Is Pat making or taking frequent personal calls? If these scenarios sound familiar, you may want to share the following information with your employees.

Time as “Profit”

Time is money. We’ve heard that over and over.

That’s definitely the case for your employees because they’re trading their time for your money. Consequently

you should safeguard that time as carefully as you would a new vehicle, state-of-the-art computer, or the money in your wallet.

When you realize waste of time is really theft, then it’s time to present your revised view to your employees.

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 24

To help with that mental transition, let’s look at the following examples in terms of cold, hard

cash coming out of your pocket.

A Story: An Unfortunate Series of Events…

Several years ago I hired a start-up landscaper to help landscape my new home. He was starting his business as an adjunct to another company he owned and wanted to see if the landscaping business would work out for him.

My new home had large windows with a view of the backyard. I worked from home on several occasions when the work was taking place. Because my car was in the garage, the crew didn’t realize I was watching – and what I saw from my windows was not pretty.

The owner arrived with four workers, showed them the site and gave them instructions. He then left to get additional equipment needed for the job, and to supervise another job.

About 15 minutes later, I saw that the work had slowed noticeably. Within another 10 minutes or so, two of the four workers had stopped working completely and were engaged in an earnest conversation while leaning on their shovels and rakes.

Shortly after that, worker #3 decided to join in while worker #4 continued to work diligently in the hot sun. Eventually worker #4 seemed to catch on. He too, stopped working and joined the group.

I continued to periodically check on their progress, and saw

the most productive activity involved worker #2 tossing a rock from one hand to the other. I also noticed “group meditation” – when all four workers stared intently for prolonged periods at one of the holes dug in the ground.

When I shared this with the owner of the fledgling landscaping business, he wasn’t totally surprised — after all, work had been progressing quite slowly.

My landscaping was eventually finished, but unfortunately, so was his start-up business.

What Does This Really Cost?

Most of my seminar attendees, when polled, believe they, and their employees, lose at least 45

minutes per day with unproductive activities. Here’s an example that may help to illustrate the financial impact of lost and wasted time.

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 25

When you multiply these time/money losses by the number of employees on your payroll, you’ll see that time loss can have an enormous impact on your bottom line. Run some time and money loss calculations of your own the next time you encounter one of these situations. Be sure to include the cost of all parties involved. Compute

the daily, weekly, monthly and annual projections.

You may want to share the results of your calculations with your employees. They’ll probably be quite surprised when you show them what they’re costing you in wasted time and squandered assets. They’ll probably realize how aware you are of their time, and that you’ll be

watching how they handle the “time funds” you’ve entrusted to them.

Part VIII: The Cost of Lost and Wasted Time – aka “Where Did Our Profits Go”? – Part 2

Did one of your workers make the wrong assumption about the next task to be completed? Did you have to perform frequent warranty work, or redo’s? Do your employees spend too much time complaining? If you’re frustrated by the loss of employee time, consider how much that time costs. Sharing your viewpoint about lost and wasted time with employees could be the beginning of a more profitable future.

How Can I Waste Thee? (Let Me Count the Ways!)

Examples of wasted time surround us constantly. Employees who would never dream of stealing tools or taking a $20 bill out of the cash drawer, often think nothing of “carrying off” multiples of those amounts in the routine way they

mismanage their time.

Let’s use our employee Pat, from Part 1 of this series, as an example. If you recall, Pat’s fullyburdened cost per production hour was $30.87, or $0.51 per minute. What’s the impact when we quantify time loss on an employer’s bank balance?

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 26

Breaks and lunches. A friend of mine used to say, “Well, I came in late today, so I’d better

leave early.” He was just being humorous, but less diligent workers often take advantage of breaks and lunches by taking extra time for coffee, cigarettes, the restroom, personal errands, etc.

It’s amazingly easy to slip in an extra five or 10 minutes of non-productive time here and there. Let's say Pat takes an extra five minutes at lunch, and four 10-minute coffee, restroom or smoke breaks during the day, and then leaves 10 minutes early to run a personal errand. That’s 55 minutes of time lost in bits and pieces throughout the day. At $30.87 per (burdened) production hour, Pat’s time is worth 51 cents a minute so he has just stolen $28.05 worth of your money.

If Pat does this every working day for a year, you’re looking at nearly $6,600 out of your

pocket? It’s sad, but true.

Taking this much extra time for breaks and lunches may seem a little extreme, but for some employees, extra breaks or lunch time may be just the tip of the iceberg. Think of the following scenarios that also divert their time and your money.

Personal phone calls and e-mail. With cell phones, office phones and computers continually at hand, the temptation is always present to fritter away time on personal matters.

Personal conversations with co-workers. Depending upon the number of participants, this

can be a double, triple or even quadruple dip into your pocketbook!

Playing games, daydreaming, gazing into holes, etc. I call this “doing nothing when you could be doing something”. These are acceptable activities for folks who are off work, retired, or on vacation, but you shouldn’t finance these pastimes while your employees are supposed to be working.

Being unprepared. Companies can lose a truly staggering amount of time and money when

employees forget or lose tools, arrive at the job site in improper clothing, mix-up driving directions, and forget or don’t bring enough job materials. Inefficiency, extra trips and repeat work abound when workers are not thinking “ahead of the game.”

Lack of direction, or “wrong” direction. When employees lack initiative or receive unclear

instructions, they wander about trying to figure out what to do first, second, or third. It’s just as harmful when employees work very quickly at the wrong thing, then have to undo the mistakes created in the process.

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 27

Carelessness and mistakes. When employees don’t pay

attention to the job at hand, mistakes are made and materials wasted. Consequently, the client may lodge a complaint, the owner may need to spend time re-establishing the relationship, supervisors may need to re-order materials, and the work must be re-done.

And remember, the owner or supervisor will also need to inspect the results. (Because who wants a second complaint on the same issue?)

Unreliability and disruption. How much stress and chaos can you stand? An unreliable

worker will eat up not only his time but your time and your team’s time. Can you afford it?

Personal crises (kids, spouse, parents, pets, car-trouble, sickness, etc.). Even the most

dependable employees have an emergency now and then, or get ill, but some workers seem to live in a continual cloud of crisis situations. Don’t try to fix their drama. Simply find someone who’s in a better position to safeguard your “worker funds.”

Passive-aggressive behavior. A passive-aggressive person is often very nice and agrees

wholeheartedly with you — until you walk away. Then the employee turns around and does what he or she pleases. If you’ve got one of these folks on your staff, you’ll lose production time and then more time wondering if something is wrong with your communication skills. Remember, this pattern typically repeats itself, so don’t continue the investment.

Grudges, grousing, carping, and complaining. Experience has shown that employees can find lots to grumble about in the workplace, and employee feuds fuel the loss of tremendous amounts of time and energy. Who pays the employees while they vent and enlist others to their cause? Unfortunately, we all know the answer…

Note: I recently read an article about a movement that challenges people to stop complaining for 21 days (the number of days to supposedly create a new habit). If you’re interested in learning more about this unique challenge, visit http://www.msnbc.msn.com/id/17362505/.

Alcohol, marijuana, or other impairments. You’ll definitely lose assets and resources if your employees

abuse substances. You’ll lose their time and skills when they don’t show up, or under-perform due to the previous night’s (or weekend’s) activities. Other employees’ productivity and morale may suffer too. Employees are downright dangerous to themselves and others if they use alcohol or drugs on the job. They often struggle with money issues and may ask you for loans in-between paychecks.

Getting Control of Your Labor Burden Costs

Copyright: Diane Gilson, Info Plus ( + ) Accounting® - BuildYourNumbers.com Page 28

You can also face liability issues as a result of employing someone impaired by alcohol or

drugs. And be very careful about safeguarding your assets if you’re dealing with a substance abuser!

Outright time theft (fraudulent clock-ins, reporting work time when not working). You should make it clear via policies and conversations with employees that such activities are grounds for immediate dismissal. No “ifs, ands or buts” about it — you will not tolerate theft.

At the end of the day, it’s a wonder that anything at all gets done, right?

Turn Things Around!

If your employees engage in any of the above time and money drains, you are not receiving an honest day’s work in return for your valuable time, trust, and hard-earned money. And you can imagine how lost and wasted time costs a company even more by raising owners’ stress levels, reducing employee morale, and degrading client satisfaction.

Make a decision to not let these time-wasters bring your company to its knees. Hold company meetings and discuss how time loss negatively impacts your company, clients, and co-workers. Let employees know that these kinds of activities and offenses can bring dismissal, and then back-up your words with action. If you pay your employees a competitive wage on a timely basis, you deserve their commitment to provide an honest delivery of time and talent in exchange.