Embed Size (px)

Citation preview

1 © 2014 American Funds Distributors, Inc..

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. Figures are past results and

are not predictive of results

in future periods.

9638s45612 (Non CE)

RPGEPO-074-1014

Get More From the Core Investments in Your DC Plan Lineups.

What Matters Most: Participant Outcomes*

© American Funds Distributors, Inc.

* Assumes a hypothetical 40-year accumulation at 10% of pay and an 8% annual return. Source: Your Money Ratios, CBS Moneywatch contributor Charlie Farrell, 2010.

30% Contributions

70% Investment returns

2

Agenda

• Can some active managers beat the indexes

and other active managers?

• If so, how can you find and, more important,

keep successful active managers in a plan lineup?

• How can you help sponsors and participants

achieve better outcomes from plan core investments?

• What matters most?

© American Funds Distributors, Inc. 3

“The Average Active Manager Can’t Beat the Index”

This is true, but it isn’t the whole story.

Data from Morningstar. Based on calendar-year returns of actively managed funds, excluding the American Funds, whose relevant benchmark is the S&P 500 Index.

This universe excludes funds that fell in the Morningstar Moderate and World Allocation categories. Funds with incomplete data were removed from the analysis. For

more information on filtering methodology, see General Methodology at the end of this presentation.

Percentage of time led index Percentage of time lagged index

‘94 ‘95 ‘96 ‘97 ‘98 ‘99 ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13

42% of the time, U.S. equity active managers outpaced the

S&P 500 during the 20 calendar years ended 12/31/13

58% of the time, U.S. equity active managers trailed the

S&P 500 during the 20 calendar years ended 12/31/13

0

20

40

60

80

100% Percentage of funds

–20

–40

–60

–80

–100

© American Funds Distributors, Inc.

© American Funds Distributors, Inc.

How Do You Find and Keep the Right Active Managers?

5

© American Funds Distributors, Inc.

Time Frames Matter

• DiMeo Schneider methodology:

− Persistency of top quartile

mutual funds*

− 17 different categories

− 10-year period ended 12/2011

− Includes 2008–2009 bear market

“For even the best performing

investments over the long

term, underperforming during

a three- or five-year period is

an eventual near-certainty.

Falling prey to natural human

behavioral tendencies

generally leads to failure.”

© American Funds Distributors, Inc.

* Distinct portfolio share classes (only) from Morningstar mutual fund database. Not corrected for survivorship bias.

Short-term Vision Can Penalize Participants

“The Next Chapter in the Active versus Passive Debate” (2012

update)

Source: DiMeo Schneider, “The Next Chapter in

the Active versus Passive Debate,” 2012 update.

6

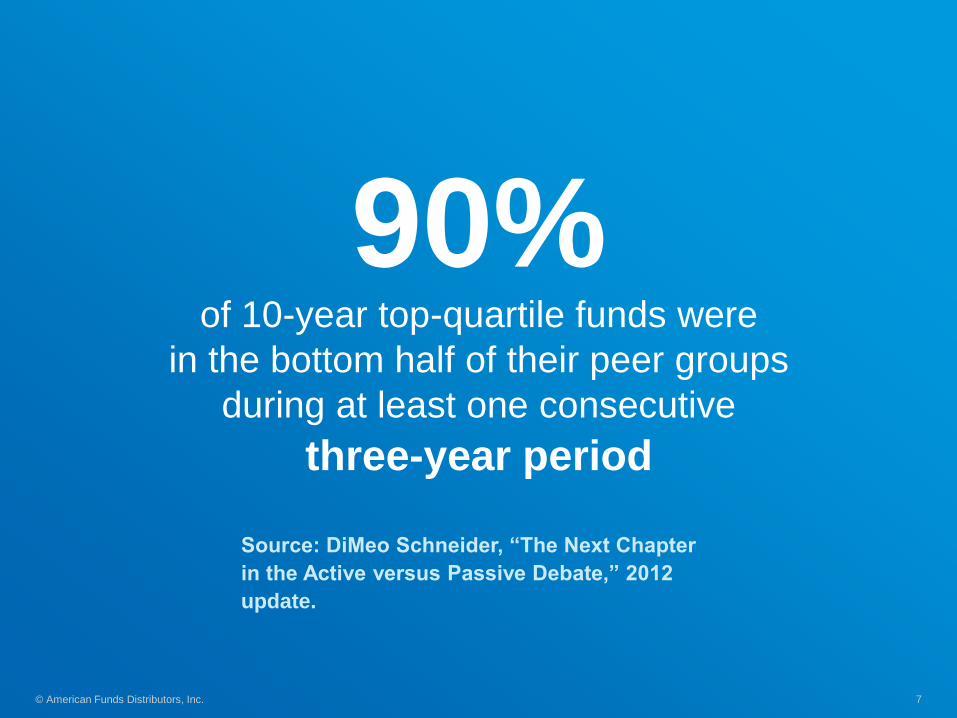

© American Funds Distributors, Inc. 7

of 10-year top-quartile funds were

in the bottom half of their peer groups

during at least one consecutive

three-year period

90%

Source: DiMeo Schneider, “The Next Chapter

in the Active versus Passive Debate,” 2012

update.

© American Funds Distributors, Inc. 8

of 10-year top-quartile funds were

in the bottom half of their peer groups for

at least one consecutive

five-year period

63%

Source: DiMeo Schneider, “The Next Chapter

in the Active versus Passive Debate,” 2012

update.

© American Funds Distributors, Inc. © American Funds Distributors, Inc.

“[The score] is not intended, nor should it be

used, as the sole source of information for

reaching an investment decision.” fi360

“While the RPAG Score is based on five years of

data, our process extends the review to six and

sometimes even seven years. We encourage

advisors to extend it further where applicable.

A 10-year perspective can add tremendous

value if the underlying management team was

responsible over that same time period.”

Jeff Elvander, CFA,

Chief Investment Officer

Retirement Plan Advisory Group

9

© American Funds Distributors, Inc.

Qualitative Screens Make a Difference.

10

© American Funds Distributors, Inc.

Morningstar’s “Fantastic 48”

10 American Funds are on the list

Each “fantastic” fund must have:

• Beaten the fund’s benchmark since the start

date of the longest-tenured manager

• An expense ratio in the cheapest quintile

of the category

• A manager with at least five years of experience

• A Bronze or better Morningstar Analyst Rating

• A positive Parent rating

• At least one manager with at least $500,000 or

more invested in the fund

• Overall Morningstar Risk that is not “High”

• Not been limited to institutional investors

“You want great managers,

low costs, good

stewardship,

and managers who eat their

own cooking.”

Morningstar, June 2014

11

Characteristics of Core Managers That Add Value

Two criteria have made a meaningful difference

“Firms with high levels of manager tenure, manager retention and ownership of

mutual fund shares also have delivered better outcomes for investors. The same

is true of firms that offer funds with lower expense ratios.”

2014 Morningstar U.S. Mutual Fund Industry Stewardship Survey Emphasis added.

© American Funds Distributors, Inc. 12

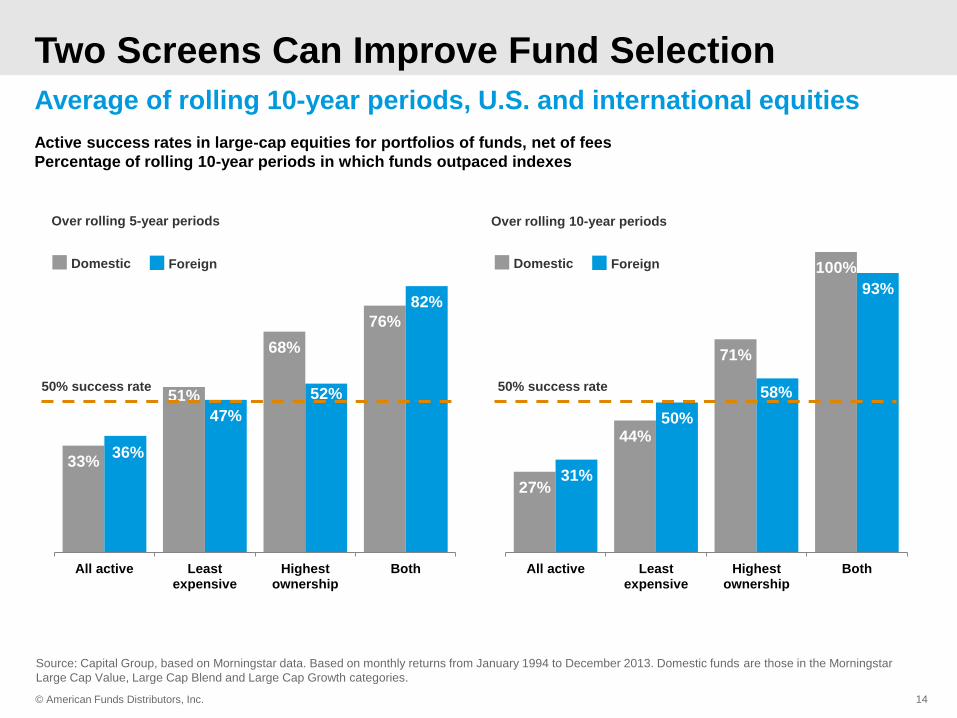

2,466 U. S. large-cap funds

Least expensive

quartile (≤89.1 bps)

Highest manager

ownership quartile

571 International large-cap funds

Funds

in both

Two Screens Can Improve Fund Selection

Rolling 1-, 3-, 5- and 10-year periods for the 20 years 1994-2013

Least expensive

quartile (≤104.0 bps)

122 funds

109 funds

Highest manager

ownership quartile

Funds

in both

20 funds

509 funds

447 funds

85 funds

Domestic Foreign

© American Funds Distributors, Inc.

Source: Capital Group based on Morningstar data. Domestic funds are those in the Morningstar Large Cap Value, Large Cap Blend and Large Cap Growth

categories. U.S. index is the S&P 500. International funds are those in the Morningstar Foreign Large Value, Foreign Large Blend and Foreign Large Growth.

International index is MSCI ACWI ex USA. Data as of May 19, 2014. The indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly

in an index.

13

33%

51%

68%

76%

36%

47%

52%

82%

All active Leastexpensive

Highestownership

Both

27%

44%

71%

100%

31%

50%

58%

93%

All active Leastexpensive

Highestownership

Both

Two Screens Can Improve Fund Selection

Average of rolling 10-year periods, U.S. and international equities

Source: Capital Group, based on Morningstar data. Based on monthly returns from January 1994 to December 2013. Domestic funds are those in the Morningstar

Large Cap Value, Large Cap Blend and Large Cap Growth categories.

© American Funds Distributors, Inc.

50% success rate

Domestic Foreign

Active success rates in large-cap equities for portfolios of funds, net of fees

Percentage of rolling 10-year periods in which funds outpaced indexes

Over rolling 5-year periods Over rolling 10-year periods

50% success rate

Domestic Foreign

14

15 © American Funds Distributors, Inc.

Active Core Funds Have Outpaced Indexes

Data from published sources were calculated internally. Hypothetical results are based on average monthly returns for rolling five-year periods of monthly returns

from January 1994 to December 2013. Past results are not predictive of results in future periods. Porfolios were rebalanced annually. Please note: These sample

portfolios exclude fixed-income allocations typical of core portfolio holdings. The components of each allocation can be found at the end of this presentation.

The potential for excess return and low cost in the core Figures shown are past results for American Funds Class A shares and are not predictive of results in future

periods. Current and future results may be lower or higher than those shown here. Returns shown at net asset value

(NAV) have all distributions reinvested. If a sales charge had been deducted, the results would have been lower.

Share prices and returns will vary, so investors may lose money. Investing for short periods makes losses more

likely. For current information and month-end results, visit americanfunds.com.

American Funds Core Alpha =

2.21% over rolling 5-year periods

© American Funds Distributors, Inc. 16

The American Funds Core Screening Results

© American Funds Distributors, Inc. 17

Low expense ratios and high firm manager ownership

American Funds Core

Pensions & Investments’

“most used equity funds

in DC plans”

Domestic equities

• The Growth Fund of America® #2

• Fundamental Investors® #9

• Washington Mutual Investors FundSM #10

• The Investment Company of America® #23

• AMCAP Fund® #29

• American Mutual Fund® #35

• The New Economy Fund® –

International/Global equities

• EuroPacific Growth Fund® #1

• International Growth and Income FundSM #4

© American Funds Distributors, Inc.

What Matters Most? Participant Outcomes.

18

19 © American Funds Distributors, Inc.

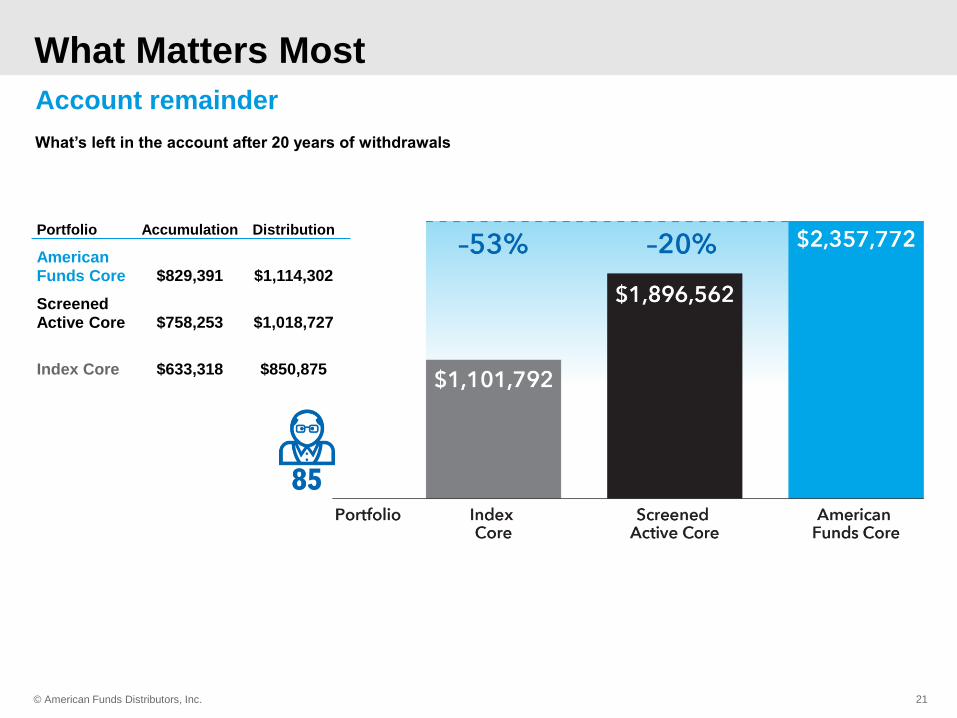

What Matters Most

Participant case study: accumulation phase

Past results are not predictive of results in future periods. Portfolio details can be found in the Methodology section at the end of this presentation.

* Represents the account value from a prior employer’s plan, based on average account balance from the ages of 40 to 50, according to EBRI 2012

Hypothetical 45-year-old employee rolls over $85,000,*

then invests $500 each month for next 20 years (through 12/31/13).

Figures shown on this and the following

slides are past results for the American

Funds Class A shares and are not predictive

of results in future periods. Current and

future results may be lower or higher than

those shown. Returns shown at net asset

value (NAV) have all distributions

reinvested. If a sales charge had been

deducted, the results would have been

lower. Share prices and returns will vary, so

investors may lose money. Investing for

short periods makes losses more likely. For

current information and month-end results,

visit americanfunds.com/retirement.

20 © American Funds Distributors, Inc.

Participant case study: distribution phase

What Matters Most

Hypothetical 65-year-old employee withdraws 5% in 1994 and increases that dollar amount

by 3% each year (cost of living) in each of the subsequent 19 years (through 12/31/13).

What Matters Most

Account remainder

© American Funds Distributors, Inc.

What’s left in the account after 20 years of withdrawals

21

Portfolio Accumulation Distribution

American Funds Core $829,391 $1,114,302

Screened Active Core $758,253 $1,018,727

Index Core $633,318 $850,875

Not All Managers Are Average

© American Funds Distributors, Inc.

“[American Funds] very visibly accomplishes

what index-fund proponents claim cannot be

done: outperform year after year, decade

after decade.”

Morningstar,

January 2014

22

Strong funds that have consistently outpaced their peer indexes

American Funds Target Date Series

© American Funds Distributors, Inc.

* Based on Class R-6 share results for rolling periods through December 31, 2013. Periods covered are the shorter of the fund’s lifetime or since the comparable

Lipper inception date.

23

93% did

outpace

peers

7% did not

outpace

peers

95%

“Few other target-date series

have as many highly

regarded

underlying holdings.”

— Morningstar Target-Date Fund

Series Report, December 31, 2013.

The underlying funds have outpaced their respective Lipper peer indexes in 93% of rolling 10-year periods*

AMCAP Fund® RAFGX

Committed to established growth companies

© American Funds Distributors, Inc.

Active success rate is the percentage of time a fund (or a group of funds) has outpaced its relevant index (or peer group) over rolling periods. The active success rate and average

relative returns are based on Class R-6 shares over rolling monthly 10-year periods from the first month-end following the fund’s inception on May 1, 1967, through December 31, 2013.

Class R-6 shares were first offered on May 1, 2009. Class R-6 share results prior to the date of first sale are hypothetical based on Class A share results without a sales charge,

adjusted for typical estimated expenses. Please see americanfunds.com for more information on specific expense adjustments and the actual dates of first sale. For the fund’s

comparable index (or index blend), see slides at end of presentation. Market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

There have been periods when the fund has lagged the index. The fund’s expense ratio is based on Class R-6 shares as of its prospectus available at the time of publication, as of

December 31, 2013. The source for the industry average expense ratio is Morningstar, excluding funds of funds, is as of December 31, 2013. The expense ratios do not reflect sales

charges or fees charged by financial intermediaries. The relevant category used for the expense ratio comparison for AMCAP Fund is Morningstar’s Large Cap Retirement, Large. Past

results are not predictive of results in future periods.

24

0.67%

0.37%

Percentage of time fund

led/lagged index

Average relative return when fund

led/lagged index (average of when

fund’s returns in excess of the index

were positive/negative)

Active success rate

Fund led index Fund lagged index

Expense ratio

Fund Industry average

71%

3.74%

-1.33%

Class R-6 shares vs. Morningstar Large

Cap Retirement, Large category

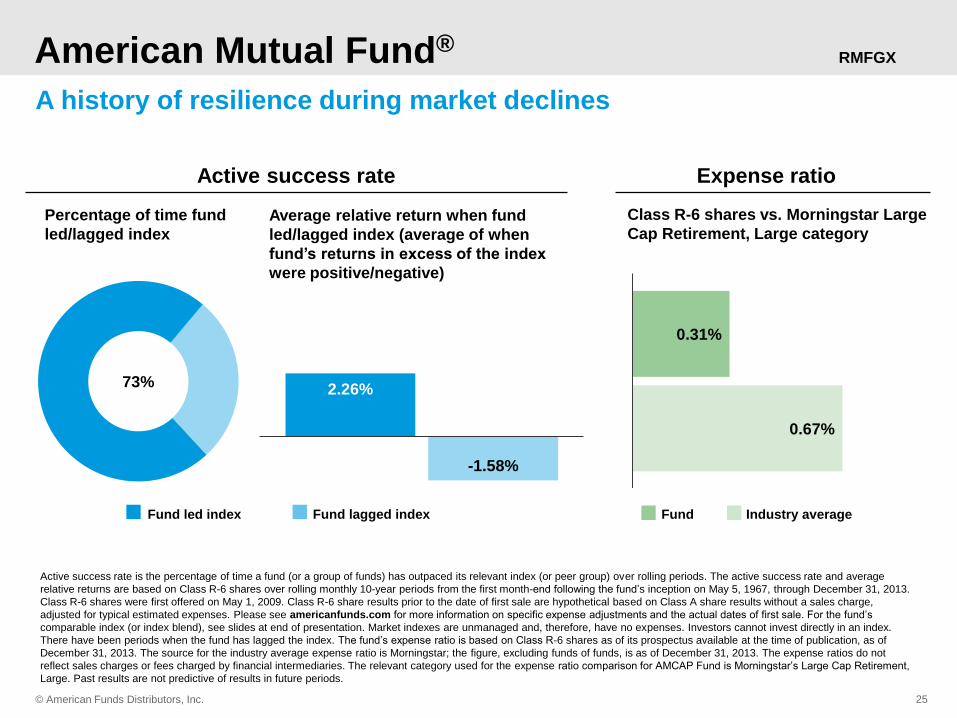

American Mutual Fund® RMFGX

A history of resilience during market declines

© American Funds Distributors, Inc.

Active success rate is the percentage of time a fund (or a group of funds) has outpaced its relevant index (or peer group) over rolling periods. The active success rate and average

relative returns are based on Class R-6 shares over rolling monthly 10-year periods from the first month-end following the fund’s inception on May 5, 1967, through December 31, 2013.

Class R-6 shares were first offered on May 1, 2009. Class R-6 share results prior to the date of first sale are hypothetical based on Class A share results without a sales charge,

adjusted for typical estimated expenses. Please see americanfunds.com for more information on specific expense adjustments and the actual dates of first sale. For the fund’s

comparable index (or index blend), see slides at end of presentation. Market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

There have been periods when the fund has lagged the index. The fund’s expense ratio is based on Class R-6 shares as of its prospectus available at the time of publication, as of

December 31, 2013. The source for the industry average expense ratio is Morningstar; the figure, excluding funds of funds, is as of December 31, 2013. The expense ratios do not

reflect sales charges or fees charged by financial intermediaries. The relevant category used for the expense ratio comparison for AMCAP Fund is Morningstar’s Large Cap Retirement,

Large. Past results are not predictive of results in future periods.

25

0.67%

0.31%

Active success rate

Fund led index Fund lagged index

Expense ratio

Fund Industry average

73% 2.26%

-1.58%

Percentage of time fund

led/lagged index

Average relative return when fund

led/lagged index (average of when

fund’s returns in excess of the index

were positive/negative)

Class R-6 shares vs. Morningstar Large

Cap Retirement, Large category

Fundamental Investors® RFNGX

Our most flexible growth-and-income fund

© American Funds Distributors, Inc.

Active success rate is the percentage of time a fund (or a group of funds) has outpaced its relevant index (or peer group) over rolling periods. The active success rate and average

relative returns are based on Class R-6 shares over rolling monthly 10-year periods from the first month-end following the fund’s inception on May 5, 1967, through December 31, 2013.

Class R-6 shares were first offered on May 1, 2009. Class R-6 share results prior to the date of first sale are hypothetical based on Class A share results without a sales charge,

adjusted for typical estimated expenses. Please see americanfunds.com for more information on specific expense adjustments and the actual dates of first sale. For the fund’s

comparable index (or index blend), see slides at end of presentation. Market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

There have been periods when the fund has lagged the index. The fund’s expense ratio is based on Class R-6 shares as of its prospectus available at the time of publication, as of

December 31, 2013. The source for the industry average expense ratio is Morningstar; the figure, excluding funds of funds, is as of December 31, 2013. The expense ratios do not

reflect sales charges or fees charged by financial intermediaries. The relevant category used for the expense ratio comparison for AMCAP Fund is Morningstar’s Large Cap Retirement,

Large. Past results are not predictive of results in future periods.

26

0.67%

0.31%

Active success rate

Fund led index Fund lagged index

Expense ratio

Fund Industry average

86% 1.97%

-0.72%

Percentage of time fund

led/lagged index

Average relative return when fund

led/lagged index (average of when

fund’s returns in excess of the index

were positive/negative)

Class R-6 shares vs. Morningstar Large

Cap Retirement, Large category

The Growth Fund of America® RGAGX

Paints with a broad brush

© American Funds Distributors, Inc.

Active success rate is the percentage of time a fund (or a group of funds) has outpaced its relevant index (or peer group) over rolling periods. The active success rate and average

relative returns are based on Class R-6 shares over rolling monthly 10-year periods from the first month-end following the fund’s inception on May 5, 1967, through December 31, 2013.

Class R-6 shares were first offered on May 1, 2009. Class R-6 share results prior to the date of first sale are hypothetical based on Class A share results without a sales charge,

adjusted for typical estimated expenses. Please see americanfunds.com for more information on specific expense adjustments and the actual dates of first sale. For the fund’s

comparable index (or index blend), see slides at end of presentation. Market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

There have been periods when the fund has lagged the index. The fund’s expense ratio is based on Class R-6 shares as of its prospectus available at the time of publication, as of

December 31, 2013. The source for the industry average expense ratio is Morningstar; the figure, excluding funds of funds, is as of December 31, 2013. The expense ratios do not

reflect sales charges or fees charged by financial intermediaries. The relevant category used for the expense ratio comparison for AMCAP Fund is Morningstar’s Large Cap Retirement,

Large. Past results are not predictive of results in future periods.

27

0.67%

0.34%

Active success rate

Fund led index Fund lagged index

Expense ratio

Fund Industry average

79%

3.61%

-0.74%

Percentage of time fund

led/lagged index

Average relative return when fund

led/lagged index (average of when

fund’s returns in excess of the index

were positive/negative)

Class R-6 shares vs. Morningstar Large

Cap Retirement, Large category

The Investment Company of America® RICGX

Seven decades of consistency

© American Funds Distributors, Inc.

Active success rate is the percentage of time a fund (or a group of funds) has outpaced its relevant index (or peer group) over rolling periods. The active success rate and average

relative returns are based on Class R-6 shares over rolling monthly 10-year periods from the first month-end following the fund’s inception on May 5, 1967, through December 31, 2013.

Class R-6 shares were first offered on May 1, 2009. Class R-6 share results prior to the date of first sale are hypothetical based on Class A share results without a sales charge,

adjusted for typical estimated expenses. Please see americanfunds.com for more information on specific expense adjustments and the actual dates of first sale. For the fund’s

comparable index (or index blend), see slides at end of presentation. Market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

There have been periods when the fund has lagged the index. The fund’s expense ratio is based on Class R-6 shares as of its prospectus available at the time of publication, as of

December 31, 2013. The source for the industry average expense ratio is Morningstar; the figure, excluding funds of funds, is as of December 31, 2013. The expense ratios do not

reflect sales charges or fees charged by financial intermediaries. The relevant category used for the expense ratio comparison for AMCAP Fund is Morningstar’s Large Cap Retirement,

Large. Past results are not predictive of results in future periods.

28

0.67%

0.30%

Active success rate

Fund led index Fund lagged index

Expense ratio

Fund Industry average

76% 2.13%

-1.73%

Percentage of time fund

led/lagged index

Average relative return when fund

led/lagged index (average of when

fund’s returns in excess of the index

were positive/negative)

Class R-6 shares vs. Morningstar Large

Cap Retirement, Large category

The New Economy Fund® RNGGX

Growth and innovation

© American Funds Distributors, Inc.

Active success rate is the percentage of time a fund (or a group of funds) has outpaced its relevant index (or peer group) over rolling periods. The active success rate and average

relative returns are based on Class R-6 shares over rolling monthly 10-year periods from the first month-end following the fund’s inception on May 5, 1967, through December 31, 2013.

Class R-6 shares were first offered on May 1, 2009. Class R-6 share results prior to the date of first sale are hypothetical based on Class A share results without a sales charge,

adjusted for typical estimated expenses. Please see americanfunds.com for more information on specific expense adjustments and the actual dates of first sale. For the fund’s

comparable index (or index blend), see slides at end of presentation. Market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

There have been periods when the fund has lagged the index. The fund’s expense ratio is based on Class R-6 shares as of its prospectus available at the time of publication, as of

December 31, 2013. The source for the industry average expense ratio is Morningstar; the figure, excluding funds of funds, is as of December 31, 2013. The expense ratios do not

reflect sales charges or fees charged by financial intermediaries. The relevant category used for the expense ratio comparison for AMCAP Fund is Morningstar’s Large Cap Retirement,

Large. Past results are not predictive of results in future periods.

29

0.67%

0.48%

Active success rate

Fund led index Fund lagged index

Expense ratio

Fund Industry average

59% 1.63%

-1.05%

Percentage of time fund

led/lagged index

Average relative return when fund

led/lagged index (average of when

fund’s returns in excess of the index

were positive/negative)

Class R-6 shares vs. Morningstar Large

Cap Retirement, Large category

Washington Mutual Investors FundSM RWMGX

The bluest of the blue chips

© American Funds Distributors, Inc.

Active success rate is the percentage of time a fund (or a group of funds) has outpaced its relevant index (or peer group) over rolling periods. The active success rate and average

relative returns are based on Class R-6 shares over rolling monthly 10-year periods from the first month-end following the fund’s inception on May 5, 1967, through December 31, 2013.

Class R-6 shares were first offered on May 1, 2009. Class R-6 share results prior to the date of first sale are hypothetical based on Class A share results without a sales charge,

adjusted for typical estimated expenses. Please see americanfunds.com for more information on specific expense adjustments and the actual dates of first sale. For the fund’s

comparable index (or index blend), see slides at end of presentation. Market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

There have been periods when the fund has lagged the index. The fund’s expense ratio is based on Class R-6 shares as of its prospectus available at the time of publication, as of

December 31, 2013. The source for the industry average expense ratio is Morningstar; the figure, excluding funds of funds, is as of December 31, 2013. The expense ratios do not

reflect sales charges or fees charged by financial intermediaries. The relevant category used for the expense ratio comparison for AMCAP Fund is Morningstar’s Large Cap Retirement,

Large. Past results are not predictive of results in future periods.

30

0.67%

0.30%

Active success rate

Fund led index Fund lagged index

Expense ratio

Fund Industry average

87% 2.12%

-0.86%

Percentage of time fund

led/lagged index

Average relative return when fund

led/lagged index (average of when

fund’s returns in excess of the index

were positive/negative)

Class R-6 shares vs. Morningstar Large

Cap Retirement, Large category

EuroPacific Growth Fund® RERGX

Purely international

© American Funds Distributors, Inc.

Active success rate is the percentage of time a fund (or a group of funds) has outpaced its relevant index (or peer group) over rolling periods. The active success rate and average

relative returns are based on Class R-6 shares over rolling monthly 10-year periods from the first month-end following the fund’s inception on May 5, 1967, through December 31, 2013.

Class R-6 shares were first offered on May 1, 2009. Class R-6 share results prior to the date of first sale are hypothetical based on Class A share results without a sales charge,

adjusted for typical estimated expenses. Please see americanfunds.com for more information on specific expense adjustments and the actual dates of first sale. For the fund’s

comparable index (or index blend), see slides at end of presentation. Market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

There have been periods when the fund has lagged the index. The fund’s expense ratio is based on Class R-6 shares as of its prospectus available at the time of publication, as of

December 31, 2013. The source for the industry average expense ratio is Morningstar; the figure, excluding funds of funds, is as of December 31, 2013. The expense ratios do not

reflect sales charges or fees charged by financial intermediaries. The relevant category used for the expense ratio comparison for AMCAP Fund is Morningstar’s Large Cap Retirement,

Large. Past results are not predictive of results in future periods.

31

0.88%

0.49%

Active success rate

Fund led index Fund lagged index

Expense ratio

Fund Industry average

96% 3.95%

-0.59%

Percentage of time fund

led/lagged index

Average relative return when fund

led/lagged index (average of when

fund’s returns in excess of the index

were positive/negative)

Class R-6 shares vs. Morningstar Large

Cap Retirement, Large category

International Growth and Income FundSM RIGGX

International growth with a dividend focus

© American Funds Distributors, Inc.

Active success rate is the percentage of time a fund (or a group of funds) has outpaced its relevant index (or peer group) over rolling periods. The active success rate and average

relative returns are based on Class R-6 shares over rolling monthly 10-year periods from the first month-end following the fund’s inception on May 5, 1967, through December 31, 2013.

Class R-6 shares were first offered on May 1, 2009. Class R-6 share results prior to the date of first sale are hypothetical based on Class A share results without a sales charge,

adjusted for typical estimated expenses. Please see americanfunds.com for more information on specific expense adjustments and the actual dates of first sale. For the fund’s

comparable index (or index blend), see slides at end of presentation. Market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

There have been periods when the fund has lagged the index. The fund’s expense ratio is based on Class R-6 shares as of its prospectus available at the time of publication, as of

December 31, 2013. The source for the industry average expense ratio is Morningstar; the figure, excluding funds of funds, is as of December 31, 2013. The expense ratios do not

reflect sales charges or fees charged by financial intermediaries. The relevant category used for the expense ratio comparison for AMCAP Fund is Morningstar’s Large Cap Retirement,

Large. Past results are not predictive of results in future periods.

32

0.88%

0.51%

Active success rate

Fund led index Fund lagged index

Expense ratio

Fund Industry average

100%

1.41%

N/A

Percentage of time fund

led/lagged index

Average relative return when fund

led/lagged index (average of when

fund’s returns in excess of the index

were positive/negative)

Class R-6 shares vs. Morningstar Large

Cap Retirement, Large category

The American Funds Advantage

Aligned with

investor success

The Capital

SystemSM

Superior long-term

track record

© American Funds Distributors, Inc.

• Since 1931, American Funds, part of Capital Group, has helped investors pursue long-term investment success.

• Our consistent approach — in combination with The Capital SystemSM — has resulted in a superior long-term track record.

33

• A compelling body of evidence

• Use non-results-oriented (qualitative) screens

• Consider implementing these concepts in your plan

© American Funds Distributors, Inc.

Summary

34

© American Funds Distributors, Inc.

Robert Shiller,

Nobel Prize-winning economist

“People make better decisions

with financial advisors.”

35

© American Funds Distributors, Inc. 36

Investors should carefully consider investment objectives, risks, charges and

expenses. This and other important information is contained in the fund prospectuses

and summary prospectuses, which can be obtained from a financial professional and

should be read carefully before investing.

37

Methodology

Compiling the fund universe

The database built to represent the universe of both large-cap domestic and large-cap foreign funds drew from

Morningstar’s U.S. Open-End Large Value, Large Blend and Large Growth U.S. and Foreign categories, with live and dead

funds combined to eliminate survivorship bias. For live funds, only the oldest share class was used. For dead funds with

multiple share classes, the median monthly returns were used. For fee-related illustrations that include dead funds with

multiple share classes, the median expense ratios were used. This screening resulted in seven qualifying domestic

American Funds (AMCAP Fund, The Growth Fund of America, The New Economy Fund, American Mutual Fund,

Fundamental Investors, The Investment Company of America and Washington Mutual Investors Fund) and two qualifying

foreign American Funds (EuroPacific Growth Fund and International Growth and Income Fund). Funds are identified as

domestic or foreign based on Morningstar categories. A number of the U.S.-focused American Funds can invest some

assets in non-U.S. securities; likewise, the two foreign-focused American Funds can invest some assets in U.S.-issued

securities.

Tracking the least expensive quartile and the highest manager ownership quartile

In conducting our research, we searched Morningstar’s database for large-cap actively managed funds that were in both

the lowest quartile ranked by expense ratio and the highest quartile ranked by manager ownership at the firm level. For

this analysis we relied on Morningstar Direct data analysis software. Least expensive quartile was calculated using annual

report Net Expense Ratio (NER) for all observed Morningstar categories for the 20-year period indicated. For funds with

missing expense ratios, gaps between two available data points were filled in using linear interpolation. Highest manager

ownership quartile was calculated using weighted averages of Morningstar screens of manager holdings at the firm level.

Each fund was assigned the weighted average of its firm manager holding. Funds without values were excluded from the

quartile rankings. The combination of least expensive NER and highest manager ownership quartiles (the screened active

core) was the result of a cross-section of the two screens. Only those funds with both the lowest expense ratios and the

highest manager ownership were included. Investors who wish to identify funds that ranked in the least expensive quartile

by NER can rely on the following rule of thumb: The least expensive quartile of funds ranked by net expense ratio for

Class A shares roughly corresponded with those reporting expenses below 0.99% for large-cap domestic funds and below

1.10% for large-cap foreign funds. Expense ratios for institutional and advisory share classes would be approximately 25

basis points lower, or below 0.74% for large-cap domestic funds and below 0.85% for large-cap foreign funds.

© American Funds Distributors, Inc.

38

Methodology (cont.)

Investors who wish to identify funds that ranked in the top quartile by manager ownership can rely on the following rule of

thumb:

• The least expensive quartile of funds ranked by net expense ratio roughly corresponded with those reporting expenses

below 0.99% for large-cap domestic funds and below 1.10% for large-cap foreign funds. Expense ratios for institutional

and advisory share classes would be approximately 25 basis points lower, or below 0.74% for large-cap domestic funds

and below 0.85% for large-cap foreign funds.

Investors who wish to identify funds that ranked in the top quartile by manager ownership can rely on the following rule of

thumb:

• The top quartile of funds ranked by manager ownership roughly corresponded with firms that had 55% or more assets in

the fund family complex in which at least one fund manager had invested a minimum of $1 million.

The Securities and Exchange Commission requires that mutual funds disclose all fees and expenses in a standardized table

published in the front portion of the fund prospectus. The SEC also requires that a fund disclose in its statements of

additional information (SAI) certain information about its portfolio managers, including ownership of securities in the fund.

Ownership disclosure is made using the following seven ranges: none; $1 to $10,000; $10,001 to $50,000; $50,001 to

$100,000; $100,001 to $500,000; $500,001 to $1,000,000; and over $1,000,000.

Morningstar tracks manager ownership as a percentage of assets at the firm level. This information can be found using

Morningstar Direct software, which can be downloaded by visiting global.morningstar.com/direct and clicking on

“Download Morningstar Direct.” Advisors seeking to incorporate manager ownership as part of their fund screening

criteria can take the following steps using Morningstar Direct. Start by creating a new open-end fund advanced search and

defining a universe. For example, for the broad large-cap domestic fund universe, select U.S., then Large Value, Large

Blend and Large Growth; to avoid duplication, screen for the oldest share class available. With the universe selected, the

snapshot page will show a set of default screens, including “Annual Report Net Expense Ratio.” It is necessary to manually

add a field for manager ownership. Under Available Data Points, select “Firm % Assets Manager Investment Over $1

million.” This selection will allow you to sort the chosen fund universe by both the expense ratio and manager ownership

fields. Due to the dynamic nature of the Morningstar database, results for the Morningstar Large U.S. and Foreign universes

may change.

© American Funds Distributors, Inc.

39

Methodology (cont.)

Working with indexes

Market indexes referenced in this brochure are defined as follows:

• MSCI All Country World ex USA Index is a free float-adjusted market capitalization-weighted index that

is designed to measure results of more than 40 developed and emerging equity markets, excluding the

United States. Results reflect dividends gross of withholding taxes through December 31, 2000, and

dividends net of withholding taxes thereafter.

• Standard & Poor’s 500 Composite Index is a market capitalization-weighted index based on the average

weighted results of 500 widely held common stocks.

The market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in

an index. There have been periods when the funds have lagged the index. Past results are not predictive

of results in future periods.

Investment disclosure

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and

price volatility, as more fully described in the prospectus. These risks may be heightened in connection

with investments in developing countries. The return of principal for bond funds and for funds with

significant underlying bond holdings is not guaranteed. Fund shares are subject to the same interest rate,

inflation and credit risks associated with the underlying bond holdings. Investments in mortgage-related

securities involve additional risks, such as prepayment risk, as more fully described in the prospectus.

Higher yielding, higher risk bonds can fluctuate in price more than investment-grade bonds, so investors

should maintain a long-term perspective.

© American Funds Distributors, Inc.

American Funds Investment Results Results as of September 30, 2014

Figures shown are past results for Class A shares and are not predictive of results in future periods. Current and

future results may be lower or higher than those shown. Results shown below reflect deduction of the maximum

sales charge of 5.75%. Share prices and returns will vary, so investors may lose money. Investing for short periods

makes losses more likely. For current information and month-end results, visit americanfunds.com.

AMCAP Fund® 5/1/67 12.17% 14.50% 8.07% 11.51% 0.70%

EuroPacific Growth Fund® 4/16/84 0.49 5.51 7.63 11.13 0.84

The Growth Fund of America® 12/1/73 9.71 12.82 8.11 13.58 0.70

The New Economy Fund® 12/1/83 7.88 13.73 9.58 11.18 0.83

Growth-and-income funds

American Mutual Fund® 2/21/50 9.12 12.73 7.21 11.64 0.61

Fundamental Investors® 8/1/78 9.67 12.77 8.66 12.43 0.63

International Growth and Income FundSM 10/1/08 0.49 6.73 — 8.85 0.91

The Investment Company of America® 1/1/34 13.72 12.85 7.25 12.17 0.61

Washington Mutual Investors FundSM 7/31/52 11.30 14.43 6.98 11.87 0.60

Average annual total returns (%)

Growth funds Inception date 1 year 5 years 10 years Lifetime Expense ratio

40

© American Funds Distributors, Inc. 41

This material must be preceded or accompanied by a summary prospectus or prospectus for AMCAP

Fund, American Mutual Fund, EuroPacific Growth Fund, Fundamental Investors, The Growth Fund of

America, International Growth and Income Fund, The Investment Company of America, The New Economy

Fund and Washington Mutual Investors Fund.

Investment results assume all distributions are reinvested and reflect applicable fees and expenses.

Expense ratios are as of each fund's prospectus available at the time of publication. When applicable,

investment results reflect fee waivers and/or expense reimbursements, without which the results would

have been lower. Please see americanfunds.com for more information.

If used after December 31, 2014, this presentation must be accompanied by a current American Funds

quarterly statistical update.

Glossary

• Active success rate is the percentage of time a fund (or a group of funds) has outpaced its

relevant index (or peer group) over rolling periods.

• Alpha is a measure of the difference between a portfolio’s actual returns and its expected results,

given its level of risk as measured by beta. A positive alpha figure indicates the portfolio has performed

better than its beta would predict. In contrast, a negative alpha indicates the portfolio has

underperformed, given the expectations established by beta.

• Capture ratio reflects the annualized product of fund versus index returns for all months in

which the index had a positive return (upside capture) or negative return (downside capture).

• Standard deviation (annualized, based on monthly returns) is a common measure of absolute

volatility that tells how returns over time have varied from the mean. A lower number signifies

lower volatility.

42 © 2014 American Funds Distributors, Inc..

9638s45612 (Non CE version)

RPGEPO-074-1014

Get More From the Core Investments in Your DC Plan Lineups.

![MADE IN JAPAN DC Micro Motors - toamec.co.jp製品一覧 List of products Lineups ラ g y ¾] º µ»Ú w v a ¼ a Òå³èµÞ Ó» ¯ èµÞ Ó» . Þ Ó» «½ ÿ¤ Ó» 種 類](https://img.dokumen.tips/doc/110x75/60c83ed771c82a77527a5ba7/made-in-japan-dc-micro-motors-ee-list-of-products-lineups-f-g-y-.jpg)