Embed Size (px)

Citation preview

© 2015 Kaufman, Hall & Associates, LLC. All rights reserved.

Funds Transfer PricingKen Levey, Vice-President Financial Institutions

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

As Vice President Financial Institutions, Ken focuses on shaping and executing Kaufman Hall’s

Axiom product and business development strategies for banks, credit unions and other

financial services industries. Ken brings over thirty years of experience working in the financial

services industry. Prior to joining Axiom EPM, Ken was the Senior Director for Banking

Analytics at SAP BusinessObjects. He was responsible for developing performance

management and analytic applications for the banking industry.

Ken started his career in financial services at Bear Stearns in New York and then became the

Vice President of Asset/Liability Management at Seamen’s Bank for Savings. For 17 years,

Ken held a senior position at IPS-Sendero (Fiserv) where he lead the development of their

Asset/Liability Management system and managed their ALM and Funds Transfer Pricing

implementation and consulting departments.

Ken Levey

Todays’ Speaker

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

I. The Basic Tenets of Funds

Transfer Pricing

II. Next Steps in Analysis: Roadmap to

Decision Making

Agenda

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Net Interest Margin – What is it?

A measure of the difference between the interest income generated

on assets and the amount of interest paid out for liabilities, relative

to the amount of (interest-earning) assets

FTP Basic Tenets

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Net Interest Margin – Why is it important?

Net Interest Margin (NIM) typically represents between 50-85% of

a financial institution’s net income

If you are going to measure performance, and the majority of your

performance is derived from NIM, you need to accurately and

consistently calculate your NIM

FTP Basic Tenets

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

What role does Funds Transfer Pricing play in NIM measurement?

Financial institutions can measure NIM at the institution level

However, if you want to measure NIM at a level lower than the institutional level; you need to

utilize Funds Transfer Pricing in order to do so

FTP Basic Tenets

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Funds Transfer Pricing Defined

Funds Transfer Pricing is an internal management information system designed to allocate

net interest margin (NIM) for every segment of a FI

Organizations

Products

Customers / Members

Liability Spread

Residual Spread

Asset Spread

Total

Financial

Institution

NIM

FTP Basic Tenets

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Measured on a historical basis supports profitability analysis

As it represents such a high percentage of total profitability it

really should be the first step in understanding all the

components of profitability

Which loan products are profitable?

Which branches are losing money?

Do deposits contribute to profits?

Which customers are profitable?

FTP Basic Tenets

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Measured on a forecasted basis to support strategic planning,

budgeting, forecasting and risk analysis

Enables an institution to plan and assess actual performance to the

plan based on profit, as opposed to volumes

Which products should you invest in?

Do you need to modify your pricing strategies?

Do your plans align with the strategic goals of the FI?

How did each branch perform according to plan?

Are you being appropriately compensated for credit risk?

Do you have an incentives aligned with your goals?

FTP Basic Tenets

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Goals & objectives

Accurately and rationally measure the cost or credit of funds in support of profitability,

strategic planning, and budgeting measurement & analysis

Margin management

Product pricing

Product and marketing strategies

Market strategies

Incentive compensation

Decentralized decision making

FTP Basic Tenets

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Strategic Planning Budgeting &

Forecasting

Profitability

Which products to invest in Set goals based on profit,

not volumes

Assess true sources of profits

Which products to get rid of Manage to plan based on

spread; not just yield or

cost of funds

Enable comparative analysis

Modify pricing strategies Identify opportunities to

improve based on forecast

Support profit-based incentive

compensation

Where are margin

improvements needed to

achieve strategic plan

Support in-cycle decision

making

Analyze profitability for all

segments (customers,

products, channels, branches,

officers, etc.)

Set specific incentive

based goals that align with

strategy

More accurate budgeting of

compensation

Distribute consistent,

quantitative-based results to

line managers

FTP Basic Tenets - Recap Matrix

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

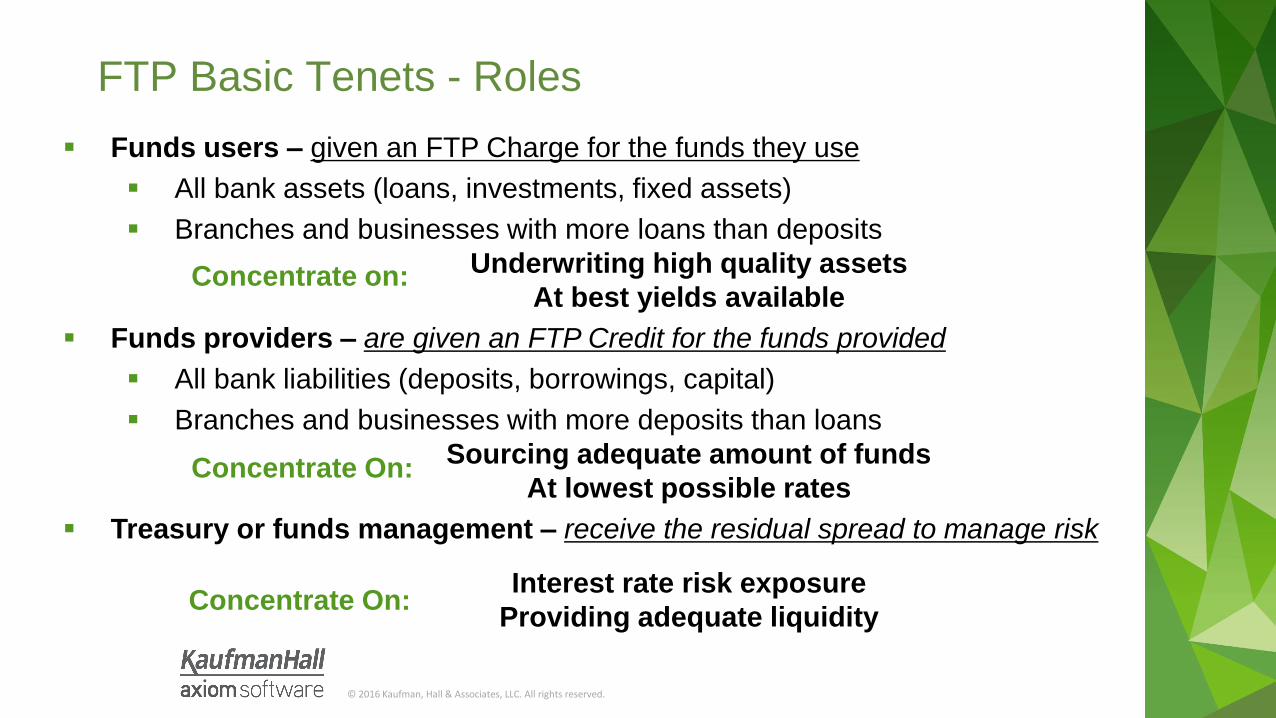

Funds users – given an FTP Charge for the funds they use

All bank assets (loans, investments, fixed assets)

Branches and businesses with more loans than deposits

Underwriting high quality assets

At best yields available

Funds providers – are given an FTP Credit for the funds provided

All bank liabilities (deposits, borrowings, capital)

Branches and businesses with more deposits than loans

Sourcing adequate amount of funds

At lowest possible rates

Treasury or funds management – receive the residual spread to manage risk

Interest rate risk exposure

Providing adequate liquidity

Concentrate on:

Concentrate On:

Concentrate On:

FTP Basic Tenets - Roles

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Role Description Concentration

Funds Users All asset generators / users• Loans, Investments, Fixed Assets

“Invest” in high quality assets

at the highest yields possible

Funds Providers All funds gatherers / sources• Savings, Checking, CDs,

Borrowings

Source necessary funds at

lowest cost possible

Treasury or

Funds Management

Money Center• Supplies funds to funds users

• Purchases funds from funds

gatherers

Manage risks• Interest rate risk

• Liquidity risk

FTP provides clarity and focus of the roles within a Financial Institution

FTP Basic Tenets - Recap

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Why Funds Transfer Pricing

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Category Product Balance Interest Rate

Assets: 3 Year Loan 100,000 4.55%

Liabilities: 6 month CD 100,000 1.15%

Margin:3.40%

Thirty years ago loan officers were thought to

bring all the “profit” to the bank – while deposit

gathers had a negative impact on bottom line

How profitable were the assets?

What value were deposits bringing to

the organization

BUT…

FTP – Allocating the Margin

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Category Product Balance Interest Rate FTP Rate Spread

Assets: 3 Year Loan 100,000 4.55% 3.30% 1.25%

Liabilities: 6 month CD 100,000 1.15% 2.10% 0.95%

Margin:3.40% 2.20%

What happened to the

1.20% (3.40% - 2.20%)?

The bank could get

an alternative

investment

The bank could go to the capital

markets and borrow funds

The introduction of FTP enabled financial institutions to apply a

cost/credit in order to value assets and liabilities, calculating a margin

for both

FTP – Allocating the Margin

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Category Product Balance Interest Rate FTP Rate Spread

Assets: 3 Year Loan 100,000 4.55% 3.30% 1.25%

Liabilities: 6 month CD 100,000 1.15% 2.10% 0.95%

Margin:3.40% 2.20%

What happened to the 1.20%

(3.40% - 2.20%)?

EXERCISE #1

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

4.55% (Loan)

Time

Rate

Deposit Spread 0.95%

1.15% (Deposit)

3.40%2.10%

3.30%

FTP Curve

Financial risks are managed by the treasury / funding center*Residual Spread is also called the Funding Center Spread or IRR Spread.

Credit Spread 1.25%

Funds Users

Funds ProvidersTreasury/Funds

3.30-2.10

FTP Illustration

Residual Spread* 1.20%

FTP Methodologies

The Evolution of FTP

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

What methods are available to transfer price the balance sheet?

Net Funds

Pool

Record Level - Match Term

FTP Methodologies

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Net funds used/provided approach

For each profit center net all assets and liabilities and ascribe a cost/credit to

shortage/excess of funding for the branch / unit

• Branch earns $134,732 in interest;

With the funds credit on ~$450K:

• Against $58,128 in interest expense

• for a Total Margin of $76,604

Branch is self-funding and providing excess

funds of ~$456K

Branch is ‘credited’

for excess funds at

a rate of 3.00%

FTP Methodologies – Net Funding

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Some basic flaws in Transfer Pricing the net position

It assumes all assets and liabilities bring the same value to the bank

It rewards the wrong behavior

It cannot be used to support a decentralized decision making process. Other monitoring systems and directives need to be implemented.

All assets/liabilities are repriced each period, so there’s a moving target for measuring performance (risk remains in the unit)

It is arbitrary. Which transfer rate or rates to use for the net funds amount is a very subjective decision.

Cost of funds overstates the loan profits

Yield on assets overstates the deposit profits

FTP Methodologies – Net Funding

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Pricing the net funds position is the easiest approach to implement

But it really can’t be used for decision making

How do we use the same rate to transfer price fixed rate auto loans as variable

rate commercial loans?

Does an overnight deposit have the same value as a 12 month term deposit?

FTP Methodologies – Net Funding

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

• Simple to implement

• Simple to administer

• No distinction between value for

assets or liabilities

• Doesn’t support product pricing

• Risk remains with the branch /

unit

• Arbitrary in nature – no basis for

assignment of transfer rate

• Does not add value…not worth considering as a valid FTP approach

ConsPros

Recommendation

FTP Methodologies – Net Funding

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Pool based approach

Create funding pools such as short-term, medium-term and long-term

Assign each product or portfolio type to a pool

The pool rates are updated monthly

The spread earned on fixed rate assets and liabilities changes because the pool rate changes

Short Term Pool

Floating Rate Instr.

Overnight Funds

Short-Term Investments

Money Market Accounts

Medium Term Pool

Autos

Certificates

ARMs

US Securities

Long Term Pool

Conv. Mortgages

DDA

MBS Securities

Cash & Due

FTP Methodologies – Pool

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Little confidence in the numbers

Results tend to be skewed

Ignores historical rates

No buy-in from line managers

The results change from period to period…cannot be managed

Risk remains in the branches / units

Ignores economic characteristics of instruments

FTP Methodologies – Pool

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

• Relatively easy to administer

• Attempts to broadly match term

• More realistic than a single rate

• Appropriate for certain product

types (non-maturity)

• Overly simplifies portfolios

• A “good” loan can become a

“bad” one

• Continuously changing results

• Too imprecise to make strategic

decisions

• Only use as an introduction to the overall concept

Only use as an introduction to the overall concept

ConsPros

Recommendation

FTP Methodologies – Pool

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Record level – matched term approach

Transfer price at the individual instrument / record level based on all individual

characteristics the instrument

Origination/Pricing date; Term; Options; etc.

Expected cash flows

Each account receives funding from a centralized “funding desk” at the point of

origination

Based on the unique attributes of that instrument

Based on alternative market investment rates / borrowing costs at that time

Which remains with it for ‘term’ of the instrument

FTP Methodologies – Matched Term

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Requires a funding desk function

An internal entity is established to receive the double-entry charges and credits

from funds providers and fund users

There will always be a balance in the funding center

The behavior of the funding center should emulate the ALM assessment of your

institution

Treasury is responsible for managing overall funding mismatch

Treasury acts as broker/dealer by “buying” all funds sourced and “selling”

all funds used at origination based on alternative market rates based on

characteristics of each deal

FTP Methodologies – Matched Term

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Borrower

%$

Bank Lending Unit Treasury Unit

$

%

Credit NIM

Deposit Gatherers

$

%

Depositor

%$

Deposit NIM

Residual Margin

Bank Net Interest Margin

FTP Methodologies – Matched Term

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Category Product Balance Interest Rate FTP Rate Spread

Assets: 3 Year Loan 100,000 4.55% 3.30% 1.25%

Liabilities: 6 month CD 100,000 1.15% 2.10% 0.95%

Margin:3.40% 2.20%

EXERCISE #2

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Borrower

%$

Bank Lending Unit Treasury Unit

$

%

Credit NIM

Deposit Gatherers

$

%

Depositor

%$

Deposit NIM

Residual Margin

Bank Net Interest Margin

EXERCISE #2

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

• Manageability – spreads are locked in

for the ‘life’ of a transaction

• Consistency - Both sides of the balance

sheet are valued against a single market

yield curve

• Risk Isolation - Line areas are insulated

from interest rate risk changes

• Margin Management - Disaggregates

margin into its proper components &

supports improved decision making

• Flexibility - Supports performance

measurement at all levels

• More time consuming to implement

• More difficult to administer (BUT NOT TO

DEFEND)

• Requires specific software to calculate

(but these solutions can bring

efficiencies to the overall process)

• The most accurate and widely used method to calculate FTP

ConsPros

Recommendation

FTP Methodologies – Matched Term

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Each transaction needs to be individually priced due to differences in

origination date, cash flow and pricing characteristics

FTP Methodologies – Matched Term

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Assigned Rate Method

Term to Maturity Method

Cash Flow Method

Repricing Term Method

FTP Methodologies – Matched Term Methods

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Primarily used for floating rate instruments or ambiguous term accounts

Uses Key Rates or Blended Rates to assign transfer rates

For example; DDA accounts may have an FTP rate derived from 20% of an overnight rate and 80% of a

2-year rate

Rates can derived through correlation or regression analysis

Apply the rolling average of the key rate or blended rate for the implied period

This reduces the volatility of the applied FTP rate and will smooth it over the pricing period (i.e., the 3-

year rolling average of the 3-year rate)

Assign short term rate based on repricing characteristics and add transfer rate

adjustment to account for liquidity

Assigned Rate Method

Funds Transfer Pricing – Matched Term Methods

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Record level – matched-term approach

Transfer price at the customer record level based on

Origination/Pricing date – Historical Yield Curves are needed!

Expected cash flows

Optionality (i.e., prepay)

* FTP Rate remains constant for ‘term’ of the instrument

Matched-Term (Term to Maturity; Cash Flow Method; Repricing Term Method)

FTP Methodologies – Matched Term Methods

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

MethodAssign

RateTerm-to-Maturity Cash flow

Repricing

Term

Rate Type Floating Fixed Fixed; Adj. Adj.

Amortization

TypeAll Bullet Amortizing Bullet; Amortizing

TermAssigned Life/

BlendedMaturity Maturity; Reprice Reprice

Pricing Date Business PeriodOrigination /

Rollover

Origination / Rollover;

Previous RepricePrevious Reprice

Standard

Accounts

Savings, Checking,

Home Equity,

Floating Notes

CDs, Bonds, etc.Auto, Mortgage and

Commercial Loans

ARMs, Adj.

Commercial Loans,

Adjustable Notes

FTP Methodologies – Methods Matrix

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Create an internal yield curve that reflects alternative market rates for

wholesale funding/investing*

Libor Swap

FHLB Advance Curve

Corporate Credit Union Curve

Additional key rates (standard indexes or blended rates to price accounts

tied to Assigned Rate Method)

Prime, Fed Funds, etc.

1 mo. FHLB; 3 mo. FHLB, etc.

Blended rates (30% Prime; 40% 3 mo. FHLB; 30% 1 yr. FHLB)

*Can be adjusted for your institution’s ability to borrow

Funds Transfer Pricing – What Rates

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

EXERCISE #3

Loan Balance: $10,000 Principal at Maturity

Interest Rate: 4.50%

Term: 12 months

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

EXERCISE #4

Loan Balance: $10,000 Amortizing

Interest Rate: 4.50%

Term: 12 months

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

What have we covered so far?

What it is:

FTP – the allocation of the institution’s Net Interest Margin to every account in the institution to help support

overall performance analysis

Why it is important:

FTP is a key component of profitability, budgeting and planning

How it is done:

Fund Users – are charged a cost for funds provided to them

Funds Providers – are given a credit for funds they provide to the institution

Funding Center – is “paid” to manage the institution’s risk (buys and sells funds from funds users and

providers)

The different methodologies to calculate FTP, all based on the underlying characteristics of each account

Assigned Rate

Term to Maturity

Cash Flow

Reprice Term

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Funds Transfer Pricing – the process of charging fund users and crediting fund providers

Service Transfer Pricing – the process of allocating centralized costs to profit centers

based on consumption or use. (Note: there are also Direct Costs/Income associated with

products, organizational units, etc.)

Capital Allocation – the process of allocating capital to allow measurement on a risk/return

basis

Multi-dimensional Reporting – the ability to flexibly slice and dice information

Components of Profitability

FTP as part of an overall Profitability Framework

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

EXERCISE #5

FTP Loans & Deposit

Service Transfers

Capital Allocation

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Recap – Implementation Objectives

Objectives for implementing a funds transfer pricing system

Provide an accurate allocation of the interest margin for profitability measurement

Provide an internal set of benchmark rates

Provide guidance when pricing new business

Evaluate investment and funding decisions

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Funds users’ focus

Underwriting high quality assets

At best yields available

Funds providers’ focus

Sourcing adequate amount of funds

At lowest possible rates

Treasury or funds management

Interest rate risk exposure

Providing adequate liquidity

Recap – Division of Responsibilities

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

An effective transfer pricing analysis enables institutions to:

Increase profitability

Make better pricing decisions

Evaluate investment and funding decisions

Identify the sources of profits

Improve the budgeting process

Evaluate the treasury group’s performance

Provide focus for the different areas of the institution

Reward desired performance & behavior

Develop teamwork & cooperation

Foster internal communication

FTP – Overall Benefits

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

EXERCISE #6 - GROUP

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

End of Section 1

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

I. The Basic Tenets of Funds Transfer

Pricing

II. Next Steps in Analysis: Roadmap

to Decision Making

Agenda

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Traditional FTP Reporting…

FTP Reporting

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.52

Funds Transfer Pricing Summary - Auto Loans - Fixed

FTP Reporting = Traditional Detail Record Report

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.53

FTP Reporting- Traditional GL Report

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

FTP Reporting

What kind of decisions can be made based on these reports?

Current period only

One dimensional, no alternative analytics capability

Gives insight into the results of what remains in the portfolio, but not the “why’s” and “how’s”

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Are we getting value from the reports we produce?

Each of the previous reporting types are important, BUT

1. What value are we getting out of the information?

2. Are we using the information to make decisions?

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

• How should information be

consumed

• What additional context is needed

• Data and report access

Considerations

57© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Best Practices Overview

DescriptiveAnalytics

DiagnosticAnalytics

PrescriptiveAnalytics

Leve

l of

Sop

his

tica

tio

n

Strategic Value

PredictiveAnalytics

What happened?

Why did it happen?

What will happen?

What is the best outcome and how can we make it happen?

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

How can we filter, segment, sort and use additional data fields to help

make FTP more analytically friendly to drive more informed decisions?

Analytical FTP

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Advance Reporting

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

FTP Margin

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

FTP Margin Report

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

FTP Decomposition Report

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

FTP Trend Report

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

The FTP Margin Composition Dashboard allocates the institution’s Net Interest Margin into its FTP

adjusted components. The margin is distributed into its three core pieces - Asset Spread, Liability

Spread and Funding Center Spread for any historical/forecasted period.

FTP Margin Decomposition Dashboard

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

FTP Margin Decomposition Dashboard

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

The Portfolio Margin Report allows the comparison of FTP Margin/Spread for any product at the

department level to that same product for the entire institution. Management can quickly understand

how historical pricing decisions effect portfolio performance.

Product Margin Dashboard

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Product Margin Dashboard

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.68

Funds Transfer Pricing Summary - Consumer Loan - Fixed

FTP Report – Traditional Detail Record Report

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

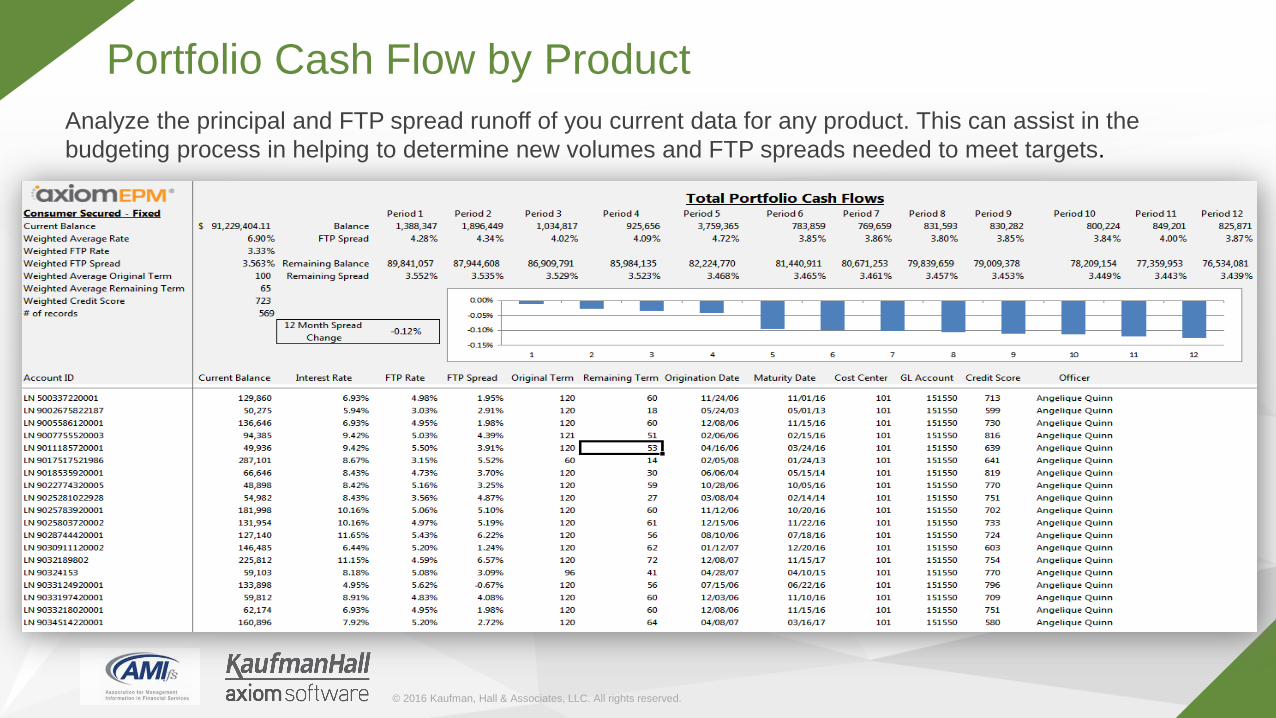

Analyze the principal and FTP spread runoff of you current data for any product. This can assist in the

budgeting process in helping to determine new volumes and FTP spreads needed to meet targets.

Portfolio Cash Flow by Product

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

FTP Spread Simulation by Product

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Analyze the principal and FTP spread runoff of you current data for any department. This can assist in the

budgeting process in helping to determine new volumes and FTP spreads needed to meet targets.

Portfolio Cash Flow by Department

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

The Portfolio Spread Credit Analysis report will analyze the risk-return profile (FTP Spread v Credit

Score) of any product in the institution. By reviewing the results in the graph, management can quickly

understand if risk based pricing is being deployed, within reason, in their pricing framework.

Portfolio Spread – Credit Analysis

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

FTP SPREAD CREDIT ANALYSIS

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.74

Product Analysis

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

FTP Spread Credit Analysis

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

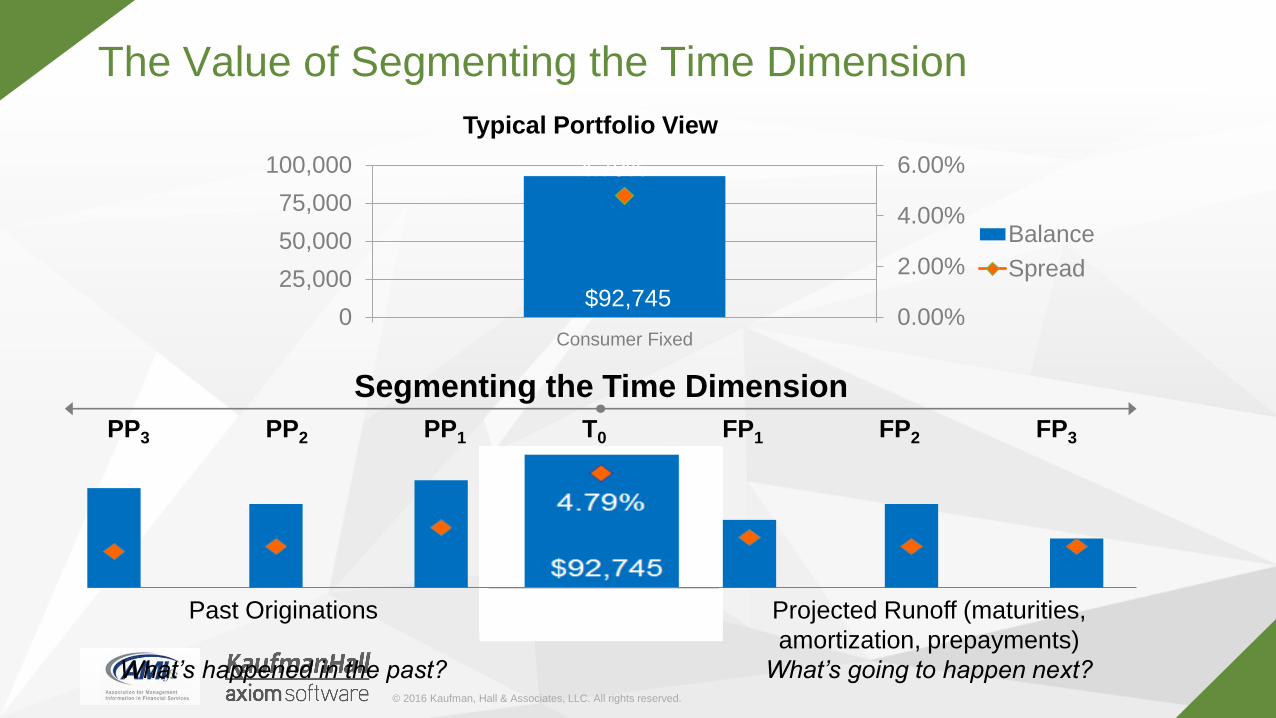

$92,745

4.79%

0.00%

2.00%

4.00%

6.00%

0

25,000

50,000

75,000

100,000

Consumer Fixed

Balance

Spread

Typical Portfolio View

Segmenting the Time Dimension

PP3 PP2 PP1 T0 FP1 FP2 FP3

Projected Runoff (maturities,

amortization, prepayments)

Past Originations

What’s going to happen next?What’s happened in the past?

The Value of Segmenting the Time Dimension

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Analyze the principal and FTP spread runoff of you current data for any officer. This can assist in the

budgeting process in helping to determine new volumes and FTP spreads needed to meet targets.

Portfolio Cash Flow by Officer

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

The New Origination Spread by Officer allows a manger to quickly rank which loan officers have

originated the most volumes in the defined time period. It will also rank the average FTP Spread that

has been booked for those volumes, so management can gain insight to the pricing decisions those

officers have made. This can be processed for any product type.

New Origination Spread by Officer

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Used in conjunction with the previous report (New Origination Spread by Officer), the Spread Trend

Report allows management to analyze an officer’s historical pricing trends by product for any

designated year.

Product Spread Trend by Officer

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Analyze the principal and FTP spread runoff of you current data for any officer This can assist in

the budgeting process in helping to determine new volumes and FTP spreads needed to meet

targets.

Portfolio Officer Analysis

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Segmenting the Time Dimension

PP 3 PP2 PP1 T0 FP1 FP2 FP2

Projected Runoff (maturities,

amortization, prepayments)

Past Originations

The Value of Segmenting the Time Dimension

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

1. Underlying Data Structure – most FTP systems are

transaction/calculation oriented – not analytics oriented

2. System Integration – FTP information could enrich other

systems & processes but integration often proves

challenging (i.e. Budgeting, Incentive Compensation, Loan

Pricing)

3. Data integration – FTP systems often don’t include

important data elements that would improve analytics –

e.g. officer code or credit score

4. Reporting – reporting capabilities are often limited to

transaction or G/L focused reports not analytically focused

reports

What are the challenges to deriving more value

from FTP:

What’s Stopping Us?

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

− Decomposing the margin

− Inclusion of additional fields allows for better visibility into the contributors of margin

− Standard FTP reports typically do not explain the “why” and cannot give insights into the “what will

be”

Advanced Analytics Recap

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Append additional fields to the transfer record

Credit Score, Risk Ratings

Officer

Zip Code

Sort and Filter – Don’t think of these as fields just to report on

Organizational Dimension (Market, Region, Line of Business, Branch)

Product Dimension (Category, Product, Sub-Product)

Officer Dimension (SVP, VP, Loan Officer)

Time Dimension: Reporting Period, QTD, YTD

Perform Segmentation Analysis on the Time Dimension

Historical – focusing on historical originations

Current – focusing on most recent period’s originations

Prospective – projecting changes looking forward at maturities

Risk Return Analysis

Insure a more risk based pricing mindset is being adopted by your institution

Incorporate FTP in other Systems or Processes

Forward Rate FTP in the budgeting process

FTP Spreads as part of the Incentive Compensation Management Process

On Demand Loan Pricing

Examples for Deriving More Value from FTP

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

Focus should be on analyzing and using information, not just scrubbing and compiling data

Add data fields that enhance analysis

Look at projected maturities and historical trends to help focus on possible future trends

Analyze data by various dimensions (officer, product, organization)

Consider including FTP in other process (Budgeting, ICM)

Think outside system constraints…..

Recap

© 2016 Kaufman, Hall & Associates, LLC. All rights reserved.

End of Section 2