Embed Size (px)

Citation preview

__________________________________________________________________ © The Garvs, LLC Phoenix Beach

Training for Business Professionals

Form 1065 Schedule K-1 Analysis – Basis Calculations & Distributions for Partnerships & LLCs – Case Suggested

Solutions

DISCLAIMER–Allproblems,exercises,activities,etc.,haveatleastonesuggestedsolution,eveniftheremaybemorethanonewaytosolvetheproblem.Therearenoofficialanswers,noristhereonlyonerightwaytosolvetheproblemortoarriveatthesolution.

Case1–PartnershipFormation&InitialBasis1. NoneofthememberswillrecognizeagainorlossonthecontributionofpropertytotheLLC.

2. Oliverwillhaveaninitialtaxbasisof$75,000(i.e.,$150,000carryoverbasis-$100,000recourse

debt+25%ofthe$100,000debtassumedbytheLLC).Suewillhaveaninitialtaxbasisof$350,000(i.e.,$300,000cashcontributed+50%ofthe$100,000debtassumedbytheLLC).Umawillhaveaninitialtaxbasisof$325,000(i.e.,$300,000carryoverbasis+25%ofthe$100,000debtassumedbytheLLC).

3. TheLLCwillnotrecognizeanygainorloss.TheLLCwilltakeacarryoverbasisintheproperty

contributed.Thus,theywillhaveaninsidetaxbasisof$150,000inthepropertyOlivercontributedand$300,000inthepropertyUmacontributed.Withthe$300,000ofcashthatSuecontributedthetotalinsidetaxbasiswouldbe$750,000.Note–the$750,000isequaltothesumofeachmember’sinitialoutsidebasis(i.e.,$75,000+$350,000+$325,000).Thetaxand§704(b)Bookbalancesheetwouldberecordedasfollows:

Tax

§704(b)Book

PropertyOlivercontributed $150,000 $250,000CashSuecontributed $300,000 $300,000PropertyUmacontributed $300,000 $150,000 $750,000 $700,000 RecourseliabilityassumedbyLLC $100,000 $100,000Oliver,capital $50,000 $150,000Sue,capital $300,000 $300,000Uma,capital $300,000 $150,000 $750,000 $700,000

PBAD Case Solutions - 1

__________________________________________________________________ © The Garvs, LLC Phoenix Beach

Training for Business Professionals

Case2-RecourseDebt–GuaranteebyLimitedPartnerInaconstructiveliquidation,the$150,000liabilitybecomesdueandpayable.Allofthepartnership'sassets,includingthedepreciableproperty,aredeemedtobeworthless.Thedepreciablepropertyisdeemedsoldforavalueofzero.Capitalaccountsareadjustedtoreflectthelossonthehypotheticaldisposition,asfollows:

Fred BarneyInitialcontribution $20,000 $80,000Lossonhypotheticalsale ($170,000) ($80,000) ($150,000) $0

Fred,asageneralpartner,wouldbeobligatedbyoperationoflawtomakeanetcontributiontothepartnershipof$150,000.BecauseFredisassumedtosatisfythatobligation,itisalsoassumedthathewouldnothavetosatisfyBarney'sguarantee.The$150,000mortgageistreatedasarecourseliabilitybecauseoneormorepartnersbeartheeconomicriskofloss.Fred'sshareoftheliabilityis$150,000,andBarney'sshareiszero.ThiswouldbesoevenifFred'snetworthatthetimeofthedeterminationislessthan$150,000,unlessthefactsandcircumstancesindicateaplantocircumventoravoidFred'sobligationtocontributetothepartnership.

Case3–PartnerInitialContribution&Non-RecourseDebtAnyincreaseinapartner'sshareofpartnershipliabilitiesistreatedasacontributionofmoneybythatpartnertothepartnership(i.e.,increaseintheiroutsidetaxbasis).Thenon-recourseliabilitiesareallocatedtothemembersontheirscheduleK-1undera3-tieredmethodasfollows:

Brutus SparkyTier1-Partners’shareif§704(b)partnershipminimumgain N/A N/ATier2–Partner’sshareof§704(c)minimumgain N/A $15,000Tier3–Profit%intheLLC $30,000 30,000TotalliabilitiesreportedtoeachmemberontheirScheduleK-1 $30,000 $45,000

Eachmember’soutsidetaxbasiswouldbecalculatedasfollows:

Brutus SparkyInitialContribution $100,000 $60,000Lessnon-recourseliabilitiescontributed N/A (75,000)DeemedcontributionforincreaseinshareofLLCliabilities 30,000 45,000Interestincome 2,000 2,000Tax-freeinterestincome 1,000 1,000 133,000 33,000Rentalrealestateloss (20,000) (20,000)Non-deductibleexpenses (3,000) (3,000) $110,000 $10,000

PBAD Case Solutions - 2

__________________________________________________________________ © The Garvs, LLC Phoenix Beach

Training for Business Professionals

Case4–AllocationPartnershipLiabilitiesPart1-Non-RecourseDebtAllocationNon-recoursedebtisallocatedbasedona3-tieredallocation.Tier1isthe§704(b)partnershipminimumgainof$10,000($30,000-$20,000)allocated50%toTom($7,500)and50%toJerry($5,000).ThereisnoTier2§704(c)pre-contributiongain.Therefore,theTier3amountof$20,000($30,000-$10,000)isallocated50%toTom($10,000)and50%toJerry($10,000).Totalnon-recoursedebtallocatedtoTomis$17,500andallocatedtoJerryis$17,500.

Tom JerryTier1-Partners’shareif§704(b)partnershipminimumgain $5,000 $5,000Tier2–Partner’sshareof§704(c)minimumgain N/A N/ATier3–Profit%intheLLC 10,000 10,000TotalliabilitiesreportedtoeachmemberontheirScheduleK-1 $15,000 $15,000

Part1-RecourseDebtAllocationTherecoursedebtisallocatedtothepartnersbasedoneconomicriskofloss.Apartnerbearstheeconomicriskoflossforapartnershipliabilitytotheextentthat,ifthepartnershipconstructivelyliquidated,thepartnerorrelatedpersonwouldbeobligatedtomakeapaymenttoanyperson(oracontributiontothepartnership)becausethatliabilitybecomesdueandpayableandthepartnerorrelatedpersonwouldnotbeentitledtoreimbursementfromanotherpartnerorpersonthatisarelatedpersontoanotherpartner.Inaconstructiveliquidation,the$50,000recourseliabilitybecomesdueandpayable.Allofthepartnership'sassets(excludingassetssecuredbythenon-recoursedebt),includingthedepreciableproperty,aredeemedtobeworthless.Thus,thecash($25,000)andAsset#2($45,000)aredeemedsoldforavalueofzero.Thisresultsinahypotheticallossof$70,000.Uponaconstructiveliquidationthecapitalaccountswouldbecalculatedasfollows: Tom(GP) Jerry(GP)Initialcontribution $5,000 $5,000Partners’shareif§704(b)partnershipminimumgain(Tier1above) $5,000 $5,000Lossonhypotheticalsale ($35,000) ($35,000)Endingcapitaluponconstructiveliquidation ($25,000) ($25,000)Asaresult,bothTomandJerrywouldbeobligatedbyoperationoflawtomakeanetcontributiontothepartnershipof$25,000.Thus,therecoursedebtwouldbeallocatedequally(i.e.,$25,000/$25,000)tobothTomandJerryontheirScheduleK-1.

Part2-Non-RecourseDebtAllocationNon-recoursedebtisallocatedbasedona3-tieredallocation.Tier1isthe§704(b)partnershipminimumgainof$10,000($30,000-$20,000)allocated90%toTom($9,000)and10%toJerry($1,000).ThereisnoTier2§704(c)pre-contributiongain.Therefore,theTier3amountof$20,000($30,000-$10,000)isallocated90%toTom($18,000)and10%toJerry($2,000).Totalnon-recoursedebtallocatedtoTomis$31,500andallocatedtoJerryis$3,500.

Tom JerryTier1-Partners’shareif§704(b)partnershipminimumgain $9,000 $1,000Tier2–Partner’sshareof§704(c)minimumgain N/A N/ATier3–Profit%intheLLC 18,000 2,000TotalliabilitiesreportedtoeachmemberontheirScheduleK-1 $27,000 $3,000

PBAD Case Solutions - 3

__________________________________________________________________ © The Garvs, LLC Phoenix Beach

Training for Business Professionals

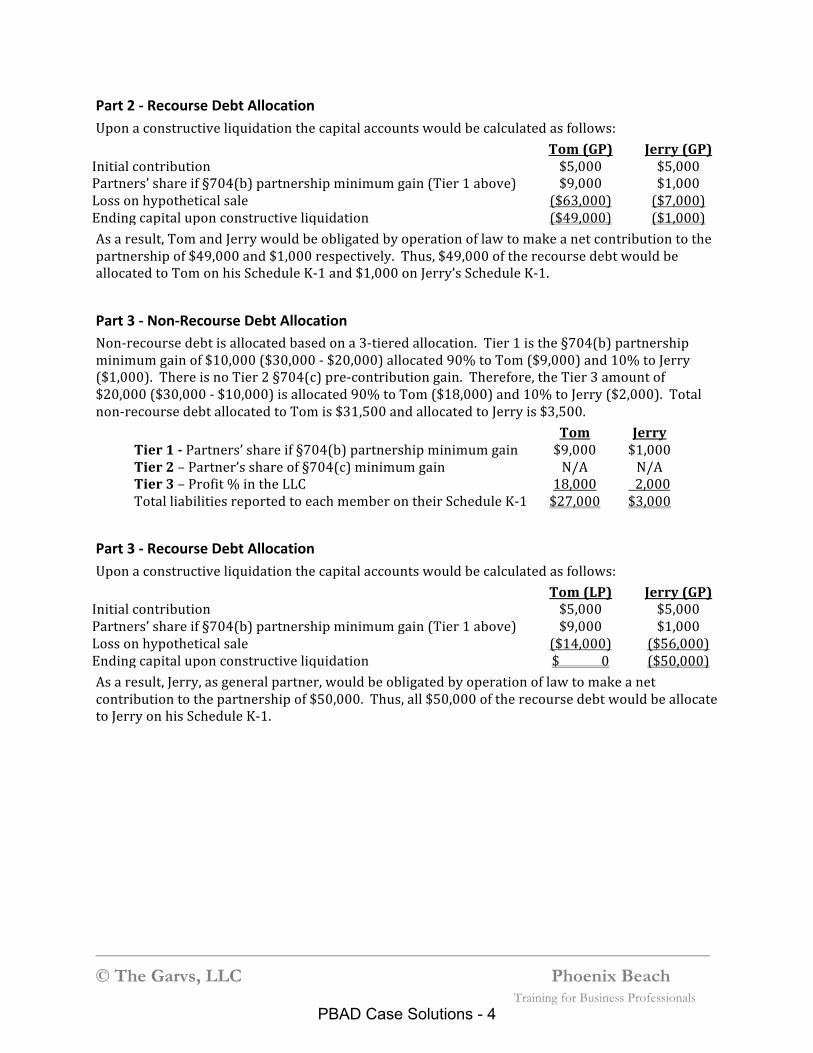

Part2-RecourseDebtAllocationUponaconstructiveliquidationthecapitalaccountswouldbecalculatedasfollows: Tom(GP) Jerry(GP)Initialcontribution $5,000 $5,000Partners’shareif§704(b)partnershipminimumgain(Tier1above) $9,000 $1,000Lossonhypotheticalsale ($63,000) ($7,000)Endingcapitaluponconstructiveliquidation ($49,000) ($1,000)Asaresult,TomandJerrywouldbeobligatedbyoperationoflawtomakeanetcontributiontothepartnershipof$49,000and$1,000respectively.Thus,$49,000oftherecoursedebtwouldbeallocatedtoTomonhisScheduleK-1and$1,000onJerry’sScheduleK-1.

Part3-Non-RecourseDebtAllocationNon-recoursedebtisallocatedbasedona3-tieredallocation.Tier1isthe§704(b)partnershipminimumgainof$10,000($30,000-$20,000)allocated90%toTom($9,000)and10%toJerry($1,000).ThereisnoTier2§704(c)pre-contributiongain.Therefore,theTier3amountof$20,000($30,000-$10,000)isallocated90%toTom($18,000)and10%toJerry($2,000).Totalnon-recoursedebtallocatedtoTomis$31,500andallocatedtoJerryis$3,500.

Tom JerryTier1-Partners’shareif§704(b)partnershipminimumgain $9,000 $1,000Tier2–Partner’sshareof§704(c)minimumgain N/A N/ATier3–Profit%intheLLC 18,000 2,000TotalliabilitiesreportedtoeachmemberontheirScheduleK-1 $27,000 $3,000

Part3-RecourseDebtAllocationUponaconstructiveliquidationthecapitalaccountswouldbecalculatedasfollows: Tom(LP) Jerry(GP)Initialcontribution $5,000 $5,000Partners’shareif§704(b)partnershipminimumgain(Tier1above) $9,000 $1,000Lossonhypotheticalsale ($14,000) ($56,000)Endingcapitaluponconstructiveliquidation $0 ($50,000)Asaresult,Jerry,asgeneralpartner,wouldbeobligatedbyoperationoflawtomakeanetcontributiontothepartnershipof$50,000.Thus,all$50,000oftherecoursedebtwouldbeallocatetoJerryonhisScheduleK-1.

PBAD Case Solutions - 4

__________________________________________________________________ © The Garvs, LLC Phoenix Beach

Training for Business Professionals

Case5–PartnerBasisCalculation1. Sheila’sendingoutsidetaxbasiswouldbe$50,000calculatedasfollows: OutsideBasis TaxFormInitialbasisDeemedcontribution(i.e.,increaseinshareofpartnershipliabilities)

$20,000

40,000

Ordinarytradeorbusinessincome 10,000 ScheduleEDividendincomeShort-termcapitalgain

3,0006,000

ScheduleBScheduleD

Tax-freeinterestincome 1,000 Form1040,line8b 80,000 Lessdistributions (0) N/ANon-deductibleRentallossEndingbasis

80,000(2,000)(28,000)$50,000

N/A

Form8582

2. Sheila’s$28,000rentallossallowableuptobasisisapassiveloss.Ingeneral,passivelossescan

onlybededucteduptopassiveincome.However,ifthetaxpayerorspouseactivelyparticipatedinapassiverentalrealestateactivity,thetaxpayercandeductupto$25,000oflossfromtherentalrealestateactivityfromtheirnon-passiveincome.Thisspecialallowanceisanexceptiontothegeneralruledisallowinglossesinexcessofincomefrompassiveactivities.Themaximumamountofthespecialallowanceisreducedifthetaxpayer’smodifiedadjustedgrossincomeismorethan$100,000($50,000ifmarriedfilingseparately).The$25,000allowablelimitonlossesisphased-outby50centsforeach$1thatmodifiedadjustedgrossincomeexceeds$100,000.SinceSheila’sMAGIis$538,000the$25,000offsetiscompletelyphased-out.Thus,noneofherrentalrealestatelossisallowableandtheentire$28,000losswouldbecarried-forwardasapassive-lossontheForm8582.

3. Sheilawillhaveanendingbasisofzerowith$10,000ofrentallossessuspendedinexcessofherbasiscalculatedasfollows:

OutsideBasis TaxFormInitialbasis $50,000 Ordinarytradeorbusinessincome 2,000 ScheduleEDividendincome 1,000 ScheduleBLong-termcapitalgain 7,000 ScheduleD 60,000 Deemeddistribution-decreaseinshareofpartnershipliabilities

(20,000) N/A

40,000 Rentalloss (40,000) Form8582Endingbasis $0 $10,000

suspendedrentallossinexcessof

basis

PBAD Case Solutions - 5

__________________________________________________________________ © The Garvs, LLC Phoenix Beach

Training for Business Professionals

4. WithaMAGIof$118,000,$9,000ofthe$25,000rentalrealestateoffsetisphased-out.Thus,Sheilawillbeabletodeduct$16,000ofher$68,000rentalloss(i.e.,$28,000prioryearpassiverentallosscarry-forward+$40,000currentyearrentalloss)onscheduleE.Theremaining$52,000rentallosswillcarry-forwardasapassivelossontheForm8582.

Case6–PartnerBasisCalculationYear1

OutsideBasis

Carry-forward

Initialcontribution $1,000 Deemedcontribution–increaseinliabilities $9,000 Interestincome $1,000 Dividendincome $3,500 Tax-freeinterest $1,500 $16,000 Tradeorbusinessloss–75% ($12,000) ($6,000)Non-deductibleexpenses–25% ($4,000) ($2,000)Endingbasis–Year1 $0 ($8,000)

NOTE–Thenon-deductibleexpenses($6,000)andtradeorbusinessloss($18,000)exceedFreddie’s16,000outsidebasis.Lossesanddeductionsinexcessofbasisarereportedonthetaxreturnpro-ratauptobasis.Thusthenon-deductibleexpenseis25%(i.e.,$6,000/$24,000)andthetradeorbusinesslossis75%(i.e.,$18,000/$24,000)ofthelossesallowableuptothe$16,000outsidebasis.

Year2 Outside

BasisCarry-forward

Endingbasis–Year1 $0 Tradeorbusinessincome $27,000 $27,000 Cashdistribution ($10,000) Deemedcashdistribution–decreaseinliabilities

($7,000)

$10,000 Tradeorbusinessloss–30% ($3,000) ($3,000)Non-deductibleexpenses–10% ($1,000) ($1,000)Short-termcapitalloss–60% ($6,000) ($6,000)Endingbasis–Year2 $0 ($10,000)

NOTE–Thenon-deductibleexpensescarry-forward($2,000),tradeorbusinesslosscarry-forward($6,000)andcurrentyearshort-termcapitalloss($6,000)exceedsFreddie’s10,000outsidebasisby$10,000.Lossesanddeductionsinexcessofbasisarereportedonthetaxreturnpro-ratauptobasis.Thusthenon-deductibleexpenseis10%(i.e.,($2,000/$20,000),thetradeorbusinesslossis30%(i.e.,$6,000/$20,000)andtheshort-termcapitallossis60%(i.e.,$12,000/$20,000)ofthelossesallowableuptothe$10,000outsidebasis.The$10,000cashdistributionand$7,000deemeddistribution(i.e.,decreaseinliabilities)arenottaxablebecausetheydonotexceedFreddie’soutsidebasis.

PBAD Case Solutions - 6

__________________________________________________________________ ♥ J. Patrick Garverick, PLC Garverick CPE Training for Tax Professionals

Case7–PartnershipDistributions1. Thepartnershipwillnotrecognizeanygainorlossonthenon-liquidatingdistribution.

2. Paddywillnotrecognizeanygainorlossonthenon-liquidatingdistributionbecausethecash

doesnotexceedhisoutsidebasis.Hisoutsidebasisafterthedistributionswouldbezero.

3. Paddywilltakea$25,000basisintheinventoryand$35,000basisintheland(i.e.,$100,000outsidebasis-$40,000allocatedtocash-$25,000allocatedtoinventory).

Summaryofthebasiscalculationandbasisinpropertyreceived Outside

BasisBasisinpropertyreceived

Basispriortodistribution $100,000 1.Cash (40,000) $40,000–Cash 60,000 2.Inventory&accountsreceivable (25,000) $25,000-Inventory 35,000 3.Allocateremainingbasistootherassets (35,000) $35,000-LandEndingbasis $0

Case8–PartnershipLiquidatingDistribution1. Thepartnershipwillnotrecognizeanygainorlossontheliquidatingdistribution.

2. Againwillonlyberecognizedinthisexampletotheextentcashexceedsthemember’soutside

basis.Thus,Calwillhavetorecognizea$10,000capitalgain.TimandPatwillnothavetorecognizeagain.Seesummariesbelowfortheoutsidebasisreductionandbasisinpropertyreceived.Forthecharacterandholdingperiodofthedistributedproperty,IRC§735states:

a. Gainorlossonthedispositionbyadistributeepartnerofunrealizedreceivables

distributedbyapartnership,shallbeconsideredasordinaryincomeorasordinaryloss.

b. Gainorlossonthesaleorexchangebyadistributeepartnerofinventoryitemsdistributedbyapartnershipshall,ifsoldorexchangedwithin5yearsfromthedateofthedistribution,beconsideredasordinaryincomeorasordinaryloss.

c. Apartner'sholdingperiodforpropertydistributedtohimbyapartnershipshall

includetheperiodsuchpropertywasheldbythepartnership.Ifthepropertyhasbeencontributedtothepartnershipbyapartner,thentheperiodthatthepropertywasheldbysuchpartnershallalsobeincluded.Thus,thedistributee“tacks”oraddsthepartnership’sholdingperiodontohis/herown.

PBAD Case Solutions - 7

__________________________________________________________________ © The Garvs, LLC Phoenix Beach

Training for Business Professionals

Tim’sbasiscalculationandbasisinpropertyreceived Outside

BasisBasisinpropertyreceived

Basispriortodistribution $180,000 1.Cash (40,000) $40,000–Cash 140,000 2.Accountsreceivable (0) $0–AccountsreceivableInventory (30,000) $30,000-Inventory 110,000 3.Allocateremainingbasistoland (110,000) $110,000-Land Endingbasis $0 NOTE–Ifthepartnerwhoseinterestisliquidatedreceivesanypropertyotherthanmoney,unrealizedreceivables,orinventoryitems,thennolosswillberecognized.

Pat’sbasiscalculationandbasisinpropertyreceived Outside

BasisBasisinpropertyreceived

Basispriortodistribution $120,000 1.Cash (40,000) $40,000–Cash 80,000 2.Accountsreceivable (0) $0–AccountsreceivableInventory (30,000) $30,000-Inventory 50,000 3.Allocateremainingbasistoland (50,000) $50,000-Land Endingbasis $0 NOTE–Ifthepartnerwhoseinterestisliquidatedreceivesanypropertyotherthanmoney,unrealizedreceivables,orinventoryitems,thennolosswillberecognized.

Cal’sbasiscalculationandbasisinpropertyreceived Outside

BasisBasisinpropertyreceived

Basispriortodistribution $30,000 1.Cash (30,000) $30,000–Cash* 0 2.Accountsreceivable (0) $0–AccountsreceivableInventory (0) $0–Inventory 0 3.Allocateremainingbasistoland (0) $0-Land Endingbasis $0 *NOTE–Calmustrecognizeacapitalgaintotheextentthecashdistributionexceedshisoutsidebasis(i.e.,$10,000).

PBAD Case Solutions - 8

__________________________________________________________________ © The Garvs, LLC Phoenix Beach

Training for Business Professionals

Case9-SaleofaPartnershipInterestGainonSaleofPartnershipArchiewillhavea$700,000gainonthesaleofhispartnershipinterestcalculatedasfollows: Sellingprice $750,000

Outsidebasis (50,000) Gain $700,000Archie’s$700,000gainistaxedasfollows:

Gain Rate TaxAccountsreceivable $50,000 39.6% $19,800§1245depreciationrecapture

25,000 39.6% 9,900

Collectibles 100,000 28% 28,000Unrecaptured§1250gain

20,000 25% 5,000

ResidualLTCG 505,000 20% 100,000 $700,000 $162,700

StatementRequired(§1.751-1(a)(3))Apartnersellingorexchanginganypartofaninterestinapartnershipthathasany§751propertyatthetimeofsaleorexchangemustsubmitwithitsincometaxreturnforthetaxableyearinwhichthesaleorexchangeoccursastatementsettingforthseparatelythefollowinginformation:

1. Thedateofthesaleorexchange;2. Theamountofanygainorlossattributabletothe§751property;AND3. Theamountofanygainorlossattributabletocapitalgainorlossonthesaleofthe

partnershipinterest.

NOTE–AForm8308isfiledbyapartnershiptoreportthesaleorexchangebyapartnerofallorpartofapartnershipinterestwhereanymoneyorotherpropertyreceivedinexchangefortheinterestisattributabletounrealizedreceivablesorinventoryitems(i.e.,a§751(a)exchange).

OrdinaryIncome(HotAssets)Under§751,totheextentapartnerisdeemedtohavesoldhis/hershareofthepartnership’sunrealizedreceivablesorinventoryitems(i.e.,HotAssets),ordinaryincomeorlossisrecognized.Archiewillhavea$700,000gainthatmustbebrokenupintoordinaryincomeandcapitalgains.Archiewillhavetorecognize$225,000ofordinaryincometotheextentofhisshareof:

1. theaccountsreceivable-$50,000(i.e.,½x$100,000)and2. §1245depreciationontheequipment-$25,000(i.e.,½x$50,000).

NOTE–Theremaining$625,000gainisalong-termcapitalgainthemustbeallocatedtothethreecategoriesofLTCGs.

PBAD Case Solutions - 9

__________________________________________________________________ © The Garvs, LLC Phoenix Beach

Training for Business Professionals

28%LTCGRate-CollectiblesPer§1.1(h)-1:whenaninterestinapartnershipheldformorethanoneyearissoldorexchangedinatransactioninwhichallrealizedgainisrecognized,thetransferorshallrecognizeascollectiblesgaintheamountofnetgain(butnotnetloss)thatwouldbeallocatedtothatpartnerifthepartnershiptransferredallofitscollectiblesforcashequaltothefairmarketvalueoftheassetsinafullytaxabletransactionimmediatelybeforethetransferoftheinterestinthepartnership.WhenArchiesoldhis50%interestinthepartnership,theinvestmentshadaFMVof$250,000andcostbasis$50,000(i.e.unrealizedgainof$200,000).Archieisdeemedtohavesold50%oftheinvestmentstoBuckeye(i.e.adeemedgainof$100,000).

25%LTCGRate–Unrecaptured§1250GainsWhenaninterestinapartnershipheldformorethanoneyearissoldorexchangedinatransactioninwhichallrealizedgainisrecognized,thepartnershallrecognizeasunrecaptured§1250capitalgainanamountthatwouldbeallocatedtothatpartner(totheextentattributabletotheportionofthepartnershipinteresttransferredthatwasheldformorethanoneyear)ifthepartnershiptransferredallofits§1250propertyinafullytaxabletransactionforcashequaltothefairmarketvalueoftheassetsimmediatelybeforethetransferoftheinterestinthepartnership.WhenArchiesoldhis50%interestinthepartnership,thebuildinghadaFMVof$400,000andcostbasis$110,000(i.e.unrealizedgainof$290,000).Archieisdeemedtohavesold50%ofthebuildingandtotheextentofhisshareofthedepreciationnottaxedasordinaryincomeunder§1250,hemustrecognize$20,000ofunrecaptured§1250capitalgain(i.e.½x$40,000ofdepreciation).

NOTE–Anyresiduallong-termcapitalgainonthesaleofapartnershipinterestwillnotbetaxedhigherthan20%.

PBAD Case Solutions - 10

__________________________________________________________________ © The Garvs, LLC Phoenix Beach

Training for Business Professionals

Case10-SaleofPartnershipInterest&§754ElectionPart1Dougwillrecognizeatotalgainof$140,000calculatedasfollows:

SellingPrice($280,000cash+($80,000liabilityx¼)) $300,000 Less:Outsidebasis($140,000+$80,000liabilityx¼)) (160,000) Gainonsale $140,000

Dougwillhavetotreat$50,000ofthegainasordinaryincomebecauseofhotassets(i.e.,25%x$200,000oftheaccountsreceivable).Theremaining$90,000willbetreatedasacapitalgain.The$90,000capitalgainneedstobebrokendownintothedifferentlong-termcapitalgainratesasfollows:

28%–collectibles $0 25%-unrecaptured§1250gain($110,000x25%) 27,500 20%-remainingcapitalgain $62,500

Totallong-termcapitalgain $90,000

Part2The$140,000positive§743(b)adjustmentiscalculatedasfollows: Oliver’soutsidebasis: CostofLLCinterest $280,000 Oliver’sshareofliabilities($80,000x¼) 20,000 $300,000 Less:Oliver’sshareoftheinsidebasis: Cashfromhypotheticalsale (($1,200,000-$80,000liabilities)x25%) $280,000 Less:Oliver’sshareoftaxgain (($1,200,000-$640,000)x25%) (140,000) Plus:Oliver’sshareofliabilities ($80,000x¼) $20,000 $160,000 §743(b)adjustment $140,000The§743(b)adjustmentmustbeallocatedbetweenthecapitalgain/§1231assetgroupandallotherassetsasfollows: Step1:Ordinaryincomeproperty($200,000x25%) $50,000 Step2:Capitalgain/§1231assetgroup($360,000x25%) $90,000 Total§743(b)adjustment $140,000

PBAD Case Solutions - 11

__________________________________________________________________ © The Garvs, LLC Phoenix Beach

Training for Business Professionals

Nexttheadjustmentneedstobeallocatedtotheassetswithineachclassasfollows: Ordinaryincomeassets: Allallocatedtotheaccountsreceivable $50,000 Capitalgain/§1231assetgroup: Land($60,000/$360,000x$90,000) $15,000 Building($300,000/$360,000x$90,000) $75,000

Part3ThejournalentrytorecordOliverasamemberis: Debit(Credit)

Accountsreceivable-Oliver’s§743(b)adjustment $50,000Land-Oliver’s§743(b)adjustment 15,000Building-Oliver’s§743(b)adjustment 75,000Capitalaccount-Oliver (140,000)

Part4TheendingtaxbalanceforThwirs,LLCafterOliverbecomesamemberis: Cash $320,000 Accountsreceivable($0+$50,000) 50,000 Land($40,000+$15,000) 55,000 Building($280,000+$75,000) 355,000 $780,000 Liabilities $80,000 Al,capital $140,000 Bill,capital $140,000 Charlie,capital $140,000 Oliver,capital $280,000 $780,000

Part5Oliverwillgetallocateddepreciationonhis§743(b)adjustmenttothebuilding.The$75,000willbetreatedasifitwasnewlyacquiredproperty.Therefore,Oliverwilldepreciatethe$75,000over39years.

PBAD Case Solutions - 12

__________________________________________________________________ © The Garvs, LLC Phoenix Beach

Training for Business Professionals

Case11–RedemptionofPartner’sInterestPart1SinceGinadoesnotreceiveherproportionateshareof"hotassets"fromthedistribution,§751(b)istriggered.§751(b)treatsthedisproportionatedistributionasasaleorexchangebetweentheFROGpartnershipandGina.Thus,partorallofthetransactionmaybetaxable.ThecalculationofthegaintaxabletoGinaiscalculatedasfollows:1. Ginaisdeemedtohavereceivedacurrentdistributionofhershareoftheaccountsreceivable

(i.e.FMV=$45,000andadjustedbasis=$0).Gina'soutsidebasisafterthecurrentdistributionis$75,000(i.e.$75,000-$0deemedreceivables).

2. Ginaisdeemedtosellthereceivablebacktothepartnership.Asaresultshewillrecognizeanordinarygainof$45,000(i.e.$45,000-$0).TheFROGpartnershipwilltakea$45,000basisinthosereceivablesitwasdeemedtohavepurchasedfromGina.

3. Ginaisdeemedtoreceivetheremaining$105,000cashinaliquidatingdistribution.Asaresult,

Ginamustrecognizeanadditionalcapitalgainof$30,000calculatedasfollows:

CashproceedstoGina $150,000Less:deemedcashfromsaleofreceivables (45,000)Remainingliquidatingcashdistribution 105,000Less:Gina'sbasis (75,000)Capitalgain $30,000

NOTE–thetotalgainrecognizedbyGinaof$75,000(i.e.$45,000ordinarygainand$30,000capitalgain)accountsforthedifferencebetweenGina'sbasis($75,000)andFMV($150,000)ofassetsinthepartnership.Also,thepartnershipdoesnotrecognizeanygainorlossfromthistransaction.

Thetaxand§704(b)balancesheetafterthedistributionwouldberecordedasfollows:

Tax

§704(b)Book

Cash $30,000 $30,000Accountsreceivable $45,000 $180,000Land $150,000 $240,000 $225,000 $450,000 Frank,capital $75,000 $150,000Ross,capital $75,000 $150,000Oliver,capital $75,000 $150,000 $225,000 $450,000

PBAD Case Solutions - 13

__________________________________________________________________ © The Garvs, LLC Phoenix Beach

Training for Business Professionals

Part2SinceGinareceivesmorethanherproportionateshare(i.e.$45,000)of"hotassets"§751(b)istriggered.Thetaxableamountofthetransactioniscalculatedasfollows:1. Ginaisdeemedtohavereceivedher25%proportionateshareofpartnershipassetsinacurrent

distribution.Therefore,Ginaisdeemedtohavereceived: Carryover

Basis

FMVCash $45,000 $45,000Accountsreceivable $0 $45,000Land $30,000 $60,000 $75,000 $150,000

2. SinceGinaisalreadydeemedtohavereceived$45,000worthofreceivables,theremaining

$105,000ofreceivablesaredeemedtohavebeenpurchasedbyGinasellinghershareofcashandlandbacktothepartnership.Thus,Ginawillhaveacapitalgainof$30,000calculatedasfollows:

FMVofaccountsreceivablereceived $105,000Less:adjustedbasisofassetssold: Cash (45,000)Land (30,000)Capitalgainondeemedsale $30,000

NOTE–Ginawillnowhaveacostbasisinthereceivablesof$105,000andaFMVof$150,000.Thus,$45,000ofordinarygaintoGinawillbedeferreduntilshereceivespaymentforthereceivables.

3. Thepartnershipwillrecognizea$105,000ordinarygainfromthedeemedsaleofaccounts

receivableasfollows:Cashreceived $45,000FMVlandreceived 60,000Totalproceedsreceived 105,000Less:adjustedbasisinaccountsreceivable (0)Ordinarygaintopartnership $105,000

Thetaxand§704(b)balancesheetafterthedistributionwouldberecordedasfollows:

Tax§704(b)Book

Cash $180,000 $180,000Accountsreceivable $0 $30,000Land $150,000 $240,000 $330,000 $450,000 Frank,capital $110,000 $150,000Ross,capital $110,000 $150,000Oliver,capital $110,000 $150,000 $330,000 $450,000

PBAD Case Solutions - 14

__________________________________________________________________ © The Garvs, LLC Phoenix Beach

Training for Business Professionals

Case12–Partner&LLCMemberBasis&AtRiskLimitationsRequired#1AssumingGradyEnterpriseswasageneralpartnership,Kathleen’sbasiswouldbecalculatedasfollows: Capitalcontributed $1,000 50%ofloantopartnership 4,000 50%ofpersonalguarantee 10,000 Outsidebasisbeforereductionstobasis 15,000 Tradeorbusinessloss(80%x$15,000) (12,000) Non-deductibleexpenses(20%x$15,000) (3,000) Endingoutsidebasis $0

NOTE1–Eachgeneralpartnerisjointlyandseverallyliableforthepartnershipdebt.Thus,eachgeneralpartnerwouldbeallocated50%oftheliabilities.NOTE2–Thenon-deductibleexpenses($4,000)andtradeorbusinessloss($16,000)exceedKathleen’s15,000outsidebasisby$5,000.Lossesanddeductionsinexcessofbasisarereportedonthetaxreturnpro-ratauptobasis.Thus,thenon-deductibleexpenseis20%(i.e.,$4,000/$20,000)andthetradeorbusinesslossis80%(i.e.,$16,000/$20,000)ofthelossesallowableuptothe$15,000outsidebasis.Kathleenwouldhavea$4,000tradeorbusinesslossand$1,000non-deductibleexpensecarriedforwardinexcessofherbasis.

Required#2

ProposedRegulationsProp.Reg.§1.465-6(d)states:Ifataxpayerguaranteesrepaymentofanamountborrowedbyanotherperson(primaryobligor)foruseinanactivity,theguaranteeshallnotincreasethetaxpayer'samountatrisk.Ifthetaxpayerrepaystothecreditortheamountborrowedbytheprimaryobligor,thetaxpayer'samountatriskshallbeincreasedatsuchtimeasthetaxpayerhasnoremaininglegalrightsagainsttheprimaryobligor.Thus,ingeneralalimitedliabilitycompanymemberwouldnotbeat-riskforpersonalguarantees.

NOTE–Thisregulationwasissuedin1979beforethedevelopmentofLLCsundervariousstatelaws,andatatimewhenentitiestreatedaspartnershipsforfederaltaxpurposeswereusuallystatelawgeneralpartnershipsandlimitedpartnerships.

CCA201308028&TAM2014-003ItappearstheIRSisnowinterpreting§1.465.6(d)differentlyforLLCmembers:CCA201308028states:“Accordingly,weconcludethatanLLCmemberisatriskwithrespecttoLLCdebtguaranteedbythemember(wheretheLLCistreatedaseitherapartnershiporadisregardedentityforfederaltaxpurposes),butonlytotheextentthatthememberhasnorightofcontributionorreimbursementfromotherguarantorsandisnototherwiseprotectedagainstlosswithinthemeaningof§465(b)(4)withrespecttotheguaranteedamounts.Therefore,weconcludethatProp.§1.465-6(d)isgenerallynotapplicabletosituationsinvolvingbonafideguaranteesofLLCdebtbyoneormoremembersoftheLLCthatisenforceablebycreditorsoftheLLCunderlocallaw,wheretheLLCistreatedaseitherapartnershiporadisregardedentityforfederaltaxpurposes.”

PBAD Case Solutions - 15

__________________________________________________________________ © The Garvs, LLC Phoenix Beach

Training for Business Professionals

TAM2014-003states:“WhenamemberofanLLCclassifiedasapartnershipordisregardedentityforfederaltaxpurposesguaranteestheLLC’sdebt,thememberisatriskwithrespecttotheamountoftheguaranteeddebt,withoutregardtowhethersuchmemberwaivesanyrighttosubrogation,reimbursement,orindemnificationfromtheLLC,butonlytotheextentthat:1. thememberhasnorightofcontributionorreimbursementfrompersonsotherthantheLLC,2. thememberisnototherwiseprotectedagainstlosswithinthemeaningof§465(b)(4),and3. theguaranteeisbonafideandenforceablebycreditorsoftheLLCunderlocallaw.”Thus,assumingGradyEnterpriseswasaLLCandthethreerequirementsunderTAM2014-003aremet,itappearsKathleen’sbasiswouldbecalculatedasfollows: Capitalcontributed $1,000 100%ofloantopartnership 8,000 100%ofpersonalguarantee 20,000 Outsidebasisbeforereductionstobasis 29,000 Tradeorbusinessloss (16,000) Non-deductibleexpenses (4,000) Endingoutsidebasis $9,000

PBAD Case Solutions - 16