Embed Size (px)

Citation preview

Forestry in Georgia: Industry and Resources

1

Impacts of the Growing Wood Pellet Sector on Forestry Nathan McClure Georgia Forestry Commission 1-800-GA-TREES www.gatrees.org

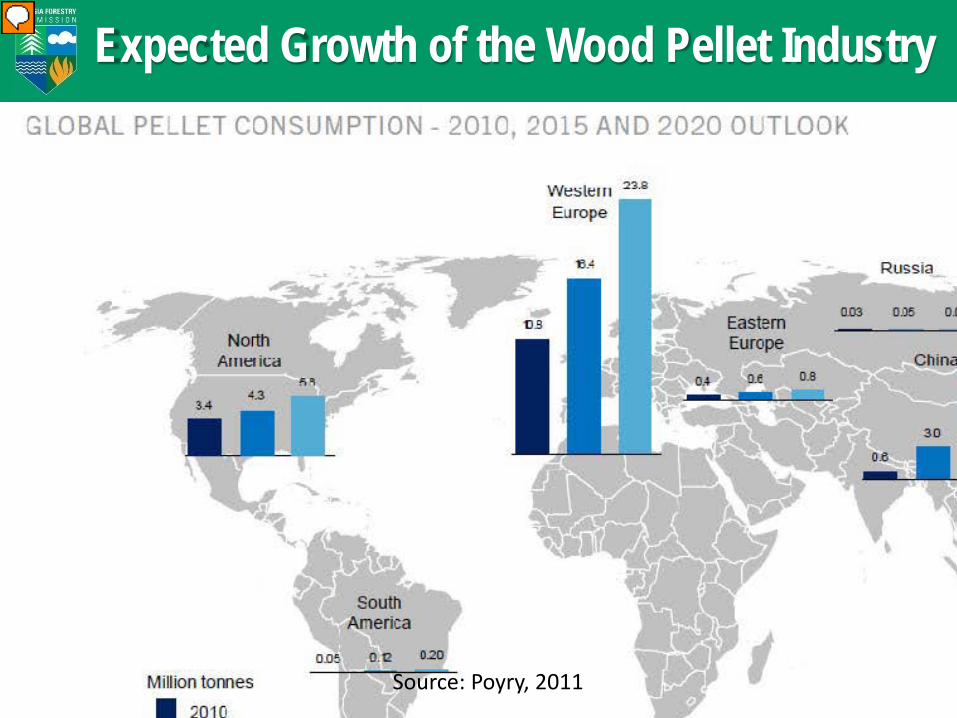

Expected Growth of the Wood Pellet Industry

Source: Poyry, 2011

0

10

20

30

40

50

60

2011 USCapacity

2011 SE USCapacity

2015 USExports to

EU -NA WoodFiber Review

2020 PoyryEU Demand

2020 IEAInternational

TradeConservative

2020 PoyryGlobal

Demand

2020 AEBIOMGlobal

Demand

2025 NewEnergyFinanceGlobal

Demand

Mill

ion

Met

ric T

onne

s Expected Growth of the Wood Pellet Industry

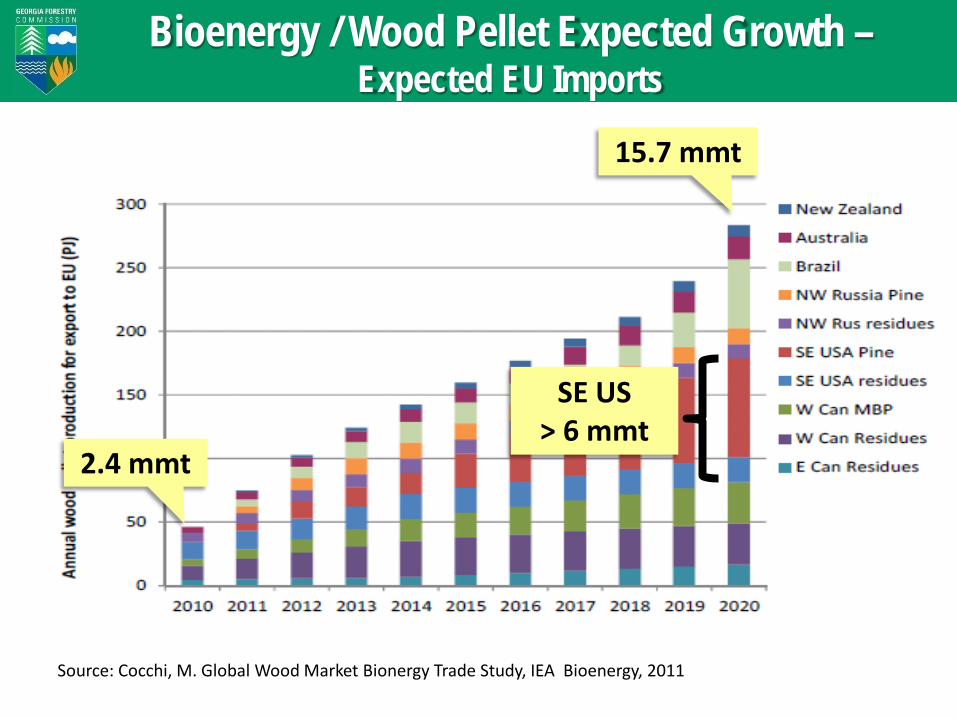

Bioenergy / Wood Pellet Expected Growth – Expected EU Imports

Source: Cocchi, M. Global Wood Market Bionergy Trade Study, IEA Bioenergy, 2011

2.4 mmt

15.7 mmt

SE US > 6 mmt

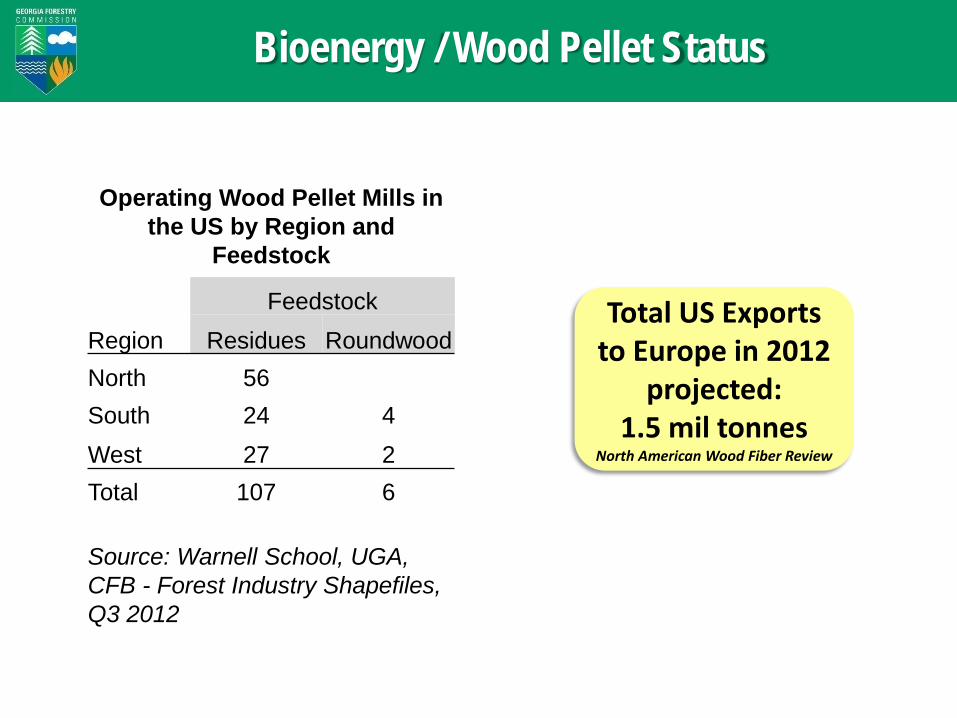

Bioenergy / Wood Pellet Status

Operating Wood Pellet Mills in the US by Region and

Feedstock

Feedstock Region Residues Roundwood North 56 South 24 4 West 27 2 Total 107 6

Source: Warnell School, UGA, CFB - Forest Industry Shapefiles, Q3 2012

Total US Exports to Europe in 2012

projected: 1.5 mil tonnes

North American Wood Fiber Review

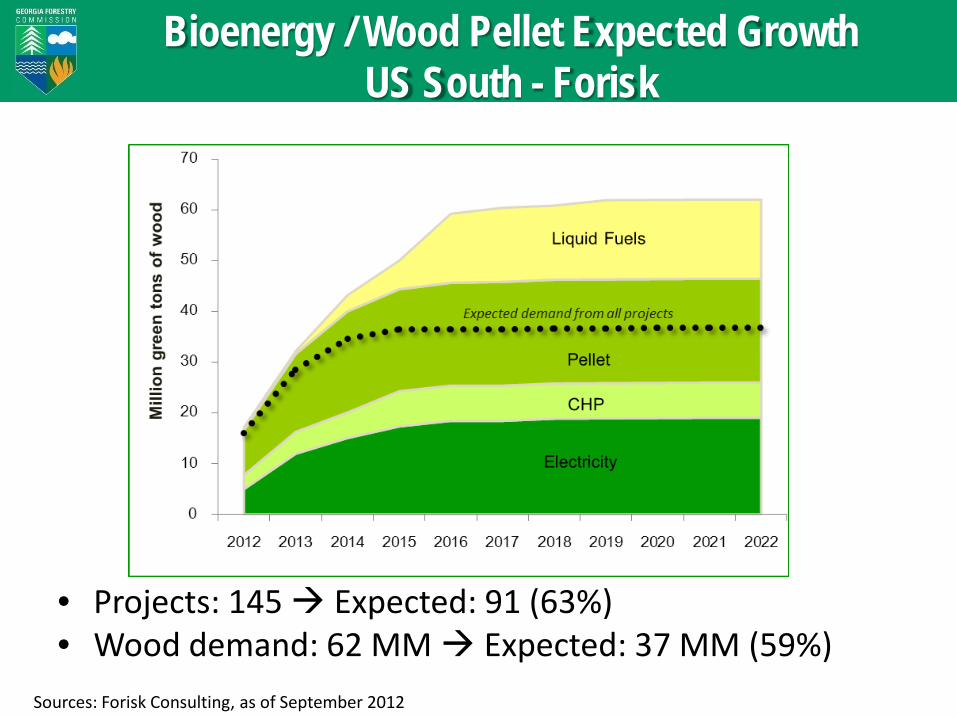

Bioenergy / Wood Pellet Expected Growth US South - Forisk

• Projects: 145 Expected: 91 (63%) • Wood demand: 62 MM Expected: 37 MM (59%)

Sources: Forisk Consulting, as of September 2012

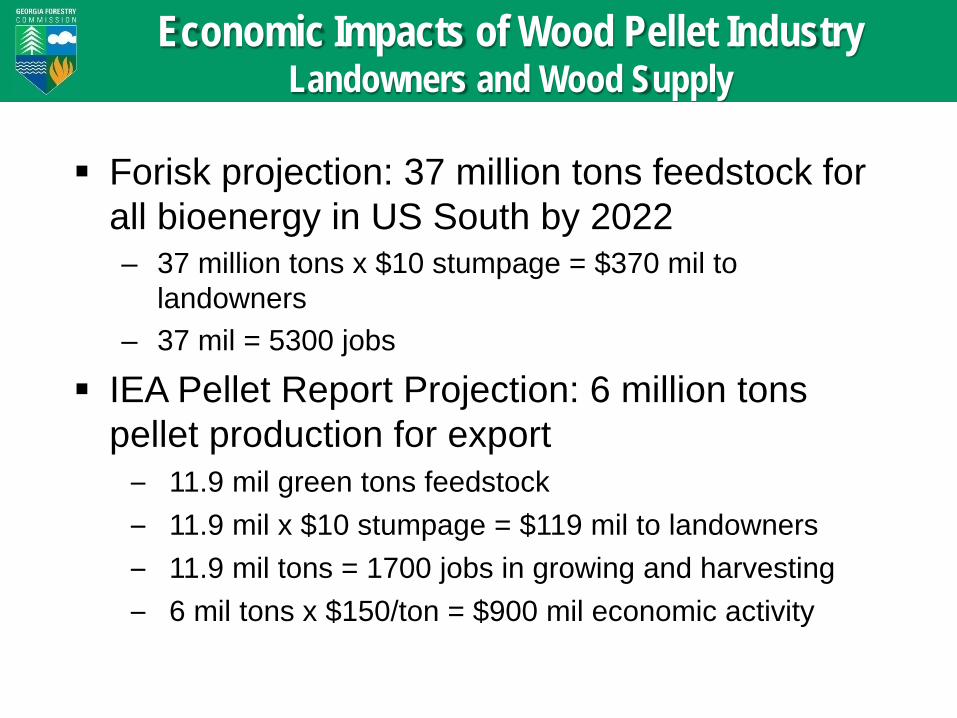

Economic Impacts of Wood Pellet Industry Landowners and Wood Supply

Forisk projection: 37 million tons feedstock for all bioenergy in US South by 2022 – 37 million tons x $10 stumpage = $370 mil to

landowners – 37 mil = 5300 jobs

IEA Pellet Report Projection: 6 million tons pellet production for export

– 11.9 mil green tons feedstock – 11.9 mil x $10 stumpage = $119 mil to landowners – 11.9 mil tons = 1700 jobs in growing and harvesting – 6 mil tons x $150/ton = $900 mil economic activity

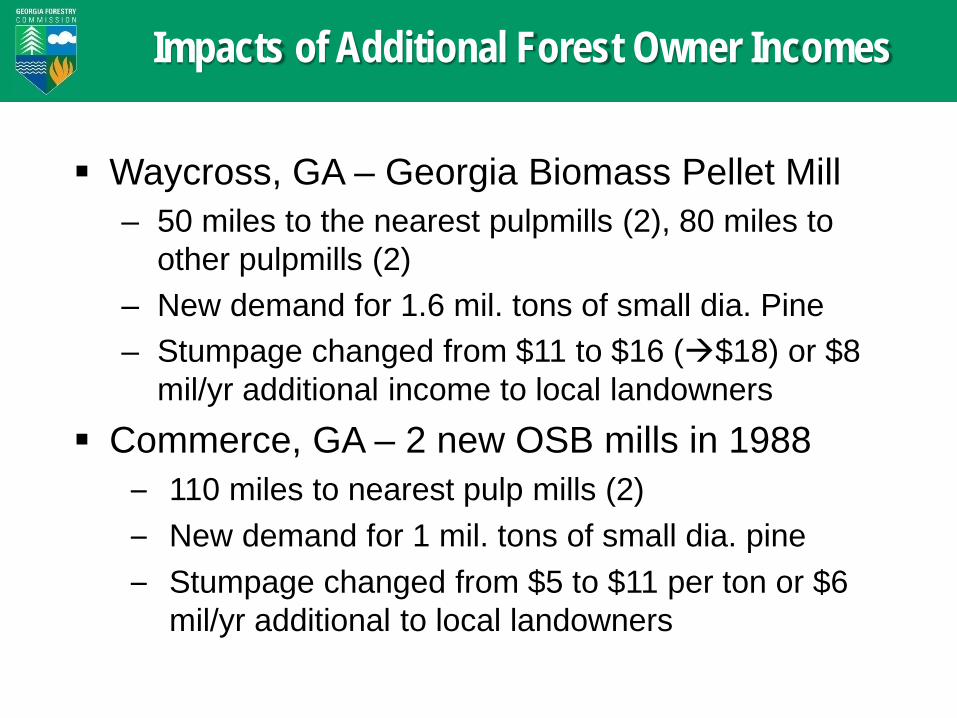

Waycross, GA – Georgia Biomass Pellet Mill – 50 miles to the nearest pulpmills (2), 80 miles to

other pulpmills (2) – New demand for 1.6 mil. tons of small dia. Pine – Stumpage changed from $11 to $16 ($18) or $8

mil/yr additional income to local landowners Commerce, GA – 2 new OSB mills in 1988

– 110 miles to nearest pulp mills (2) – New demand for 1 mil. tons of small dia. pine – Stumpage changed from $5 to $11 per ton or $6

mil/yr additional to local landowners

Impacts of Additional Forest Owner Incomes

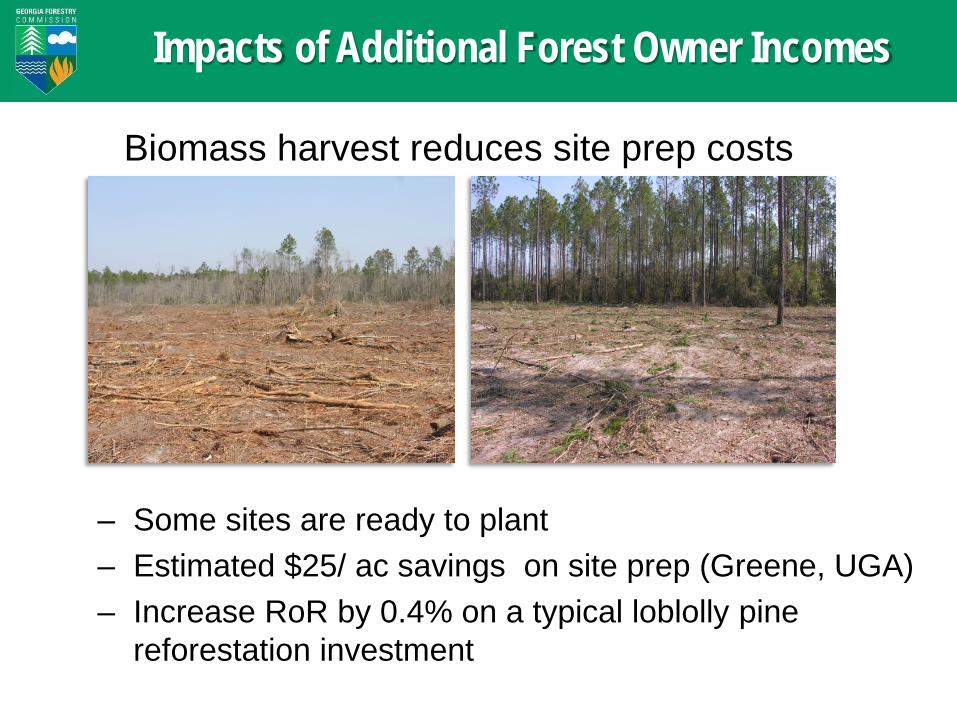

Biomass harvest reduces site prep costs

Impacts of Additional Forest Owner Incomes

– Some sites are ready to plant – Estimated $25/ ac savings on site prep (Greene, UGA) – Increase RoR by 0.4% on a typical loblolly pine

reforestation investment

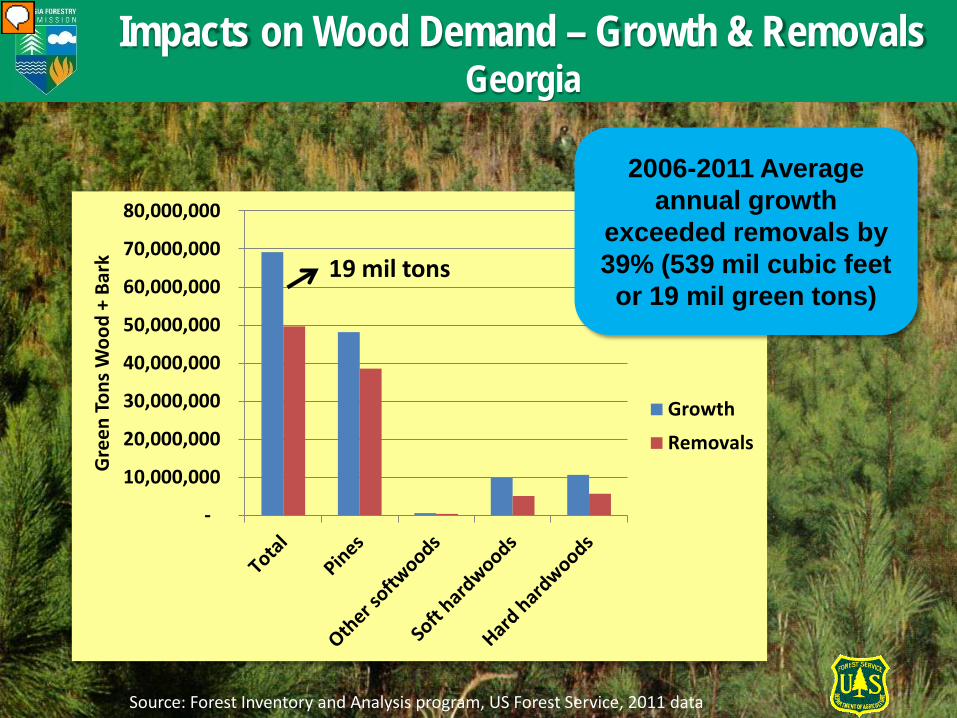

Impacts on Wood Demand – Growth & Removals Georgia

-

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

Gre

en T

ons W

ood

+ Ba

rk

Growth

Removals

2006-2011 Average annual growth

exceeded removals by 39% (539 mil cubic feet

or 19 mil green tons) 19 mil tons

Source: Forest Inventory and Analysis program, US Forest Service, 2011 data

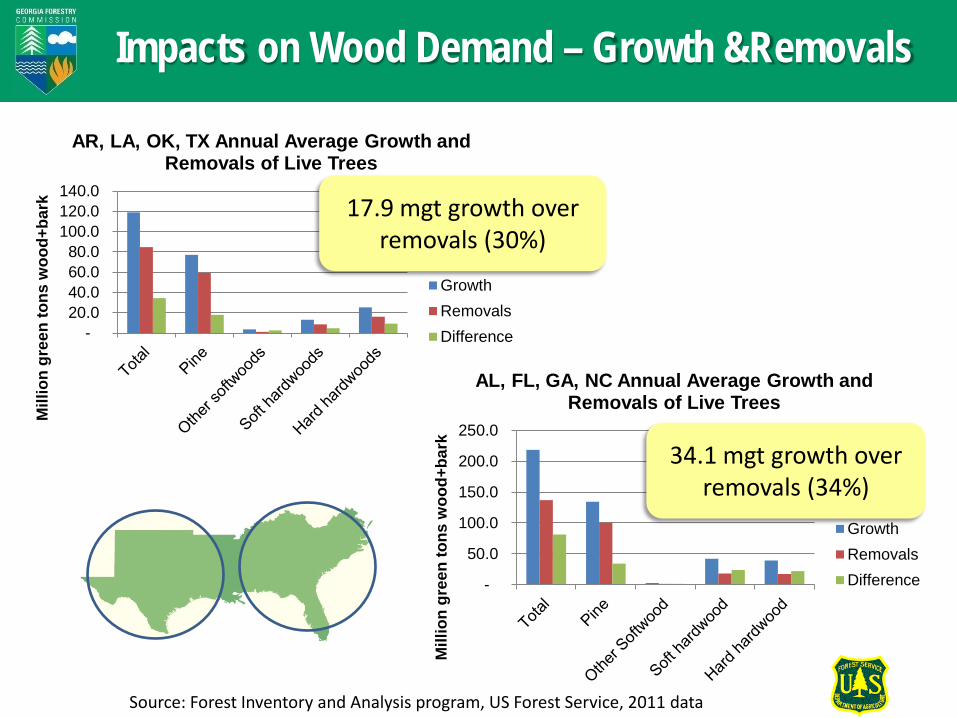

Impacts on Wood Demand – Growth &Removals

-

50.0

100.0

150.0

200.0

250.0M

illio

n gr

een

tons

woo

d+ba

rk

AL, FL, GA, NC Annual Average Growth and Removals of Live Trees

GrowthRemovalsDifference

- 20.0 40.0 60.0 80.0

100.0 120.0 140.0

Mill

ion

gree

n to

ns w

ood+

bark

AR, LA, OK, TX Annual Average Growth and Removals of Live Trees

GrowthRemovalsDifference

17.9 mgt growth over removals (30%)

34.1 mgt growth over removals (34%)

Source: Forest Inventory and Analysis program, US Forest Service, 2011 data

Source: Forest Inventory and Analysis program, US Forest Service, 2011 data

0.0

500.0

1,000.0

1,500.0

2,000.0

2,500.0

3,000.0

3,500.0

4,000.0

Mill

ion

Cub

ic F

eet

Tree Diameter (inches)

2002200320042005200620072008200920102011

Year

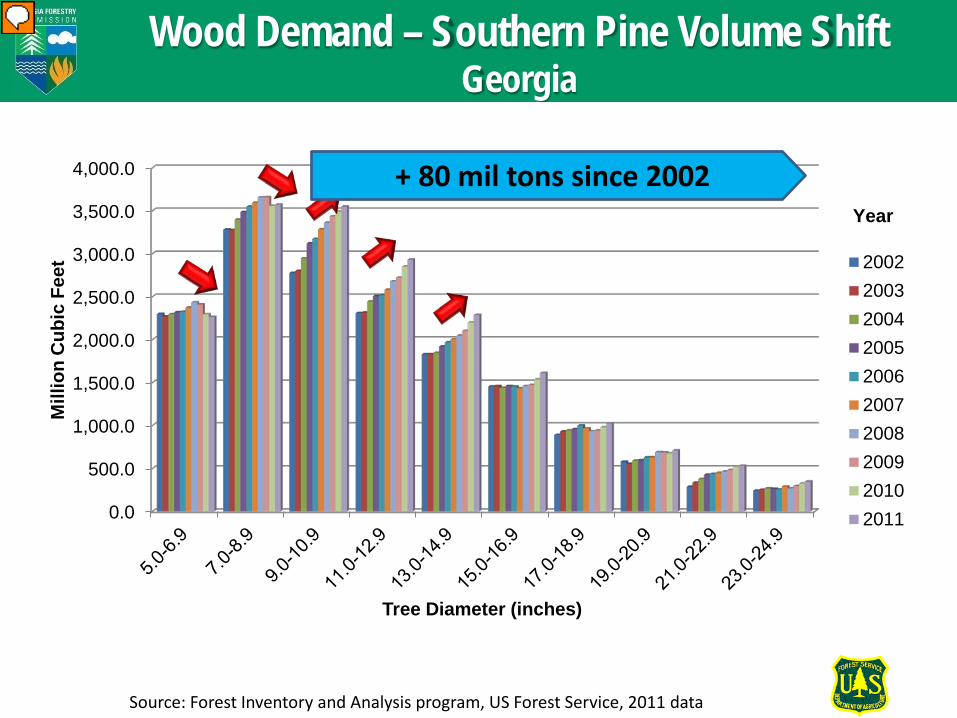

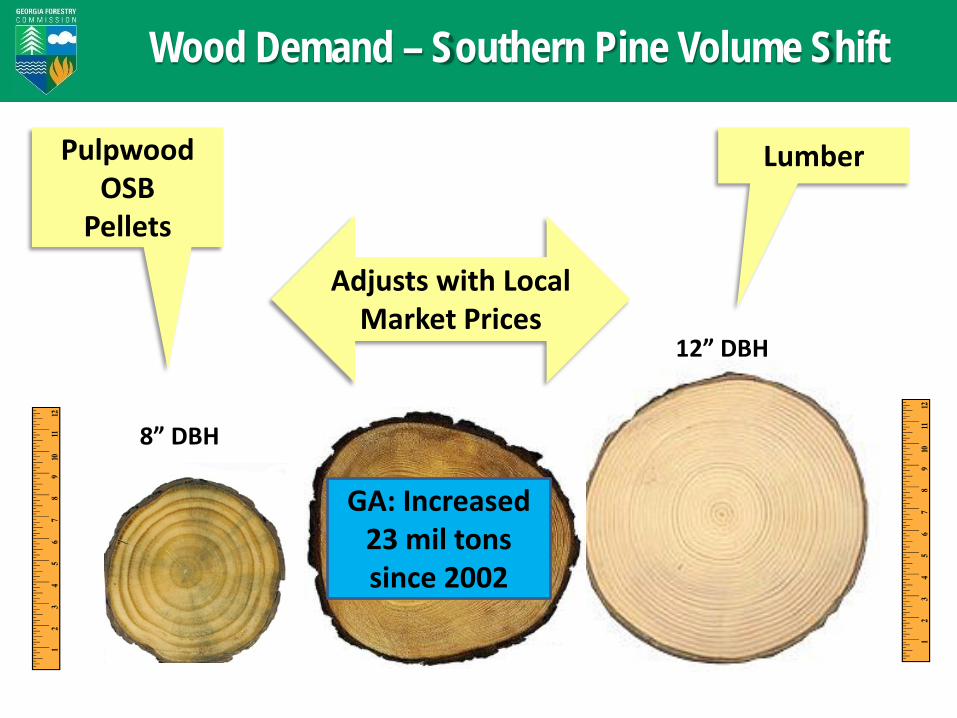

Wood Demand – Southern Pine Volume Shift Georgia

+ 80 mil tons since 2002

Source: R. Harper, Forest Inventory and Analysis program, US Forest Service, 2011 data

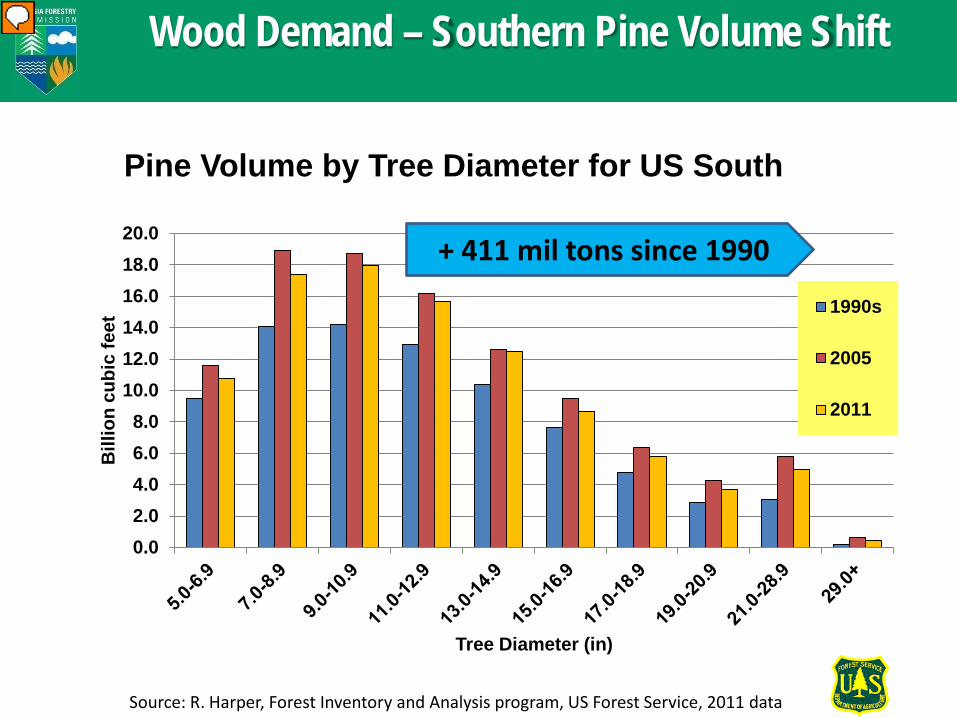

Wood Demand – Southern Pine Volume Shift

0.02.04.06.08.0

10.012.014.016.018.020.0

Bill

ion

cubi

c fe

et

Tree Diameter (in)

Pine Volume by Tree Diameter for US South

1990s

2005

2011

+ 411 mil tons since 1990

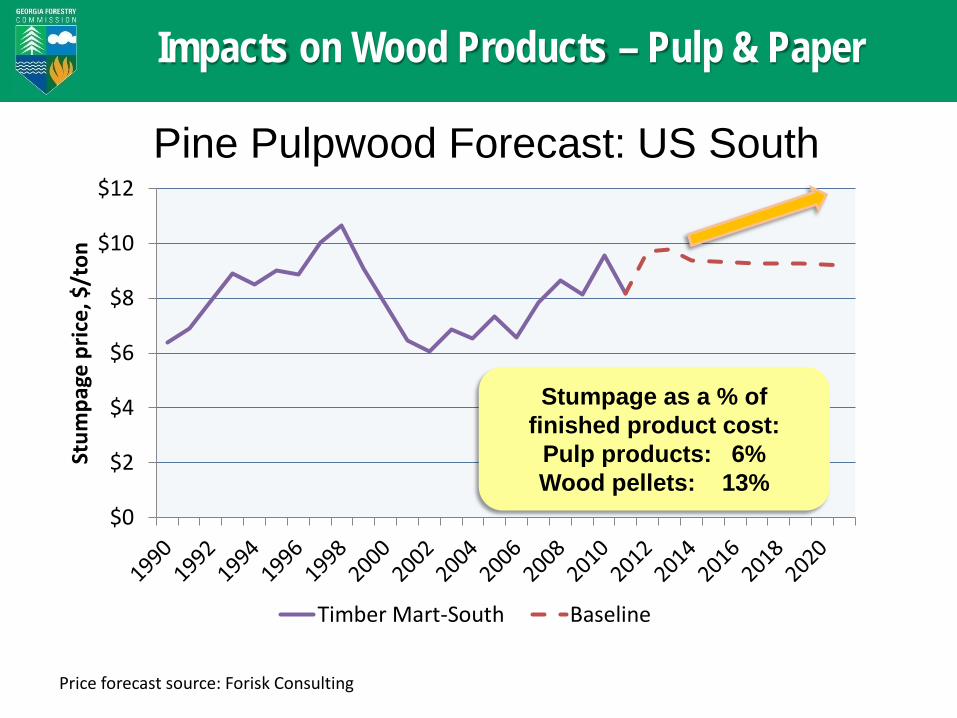

Impacts on Wood Products – Pulp & Paper

Source: TPO reports, Southern Research Station, US Forest Service, 2009 and Forisk

Impacts on Wood Products – Pulp & Paper

$0

$2

$4

$6

$8

$10

$12

Stum

page

pric

e, $

/ton

Timber Mart-South Baseline

Price forecast source: Forisk Consulting

Pine Pulpwood Forecast: US South

Stumpage as a % of finished product cost:

Pulp products: 6% Wood pellets: 13%

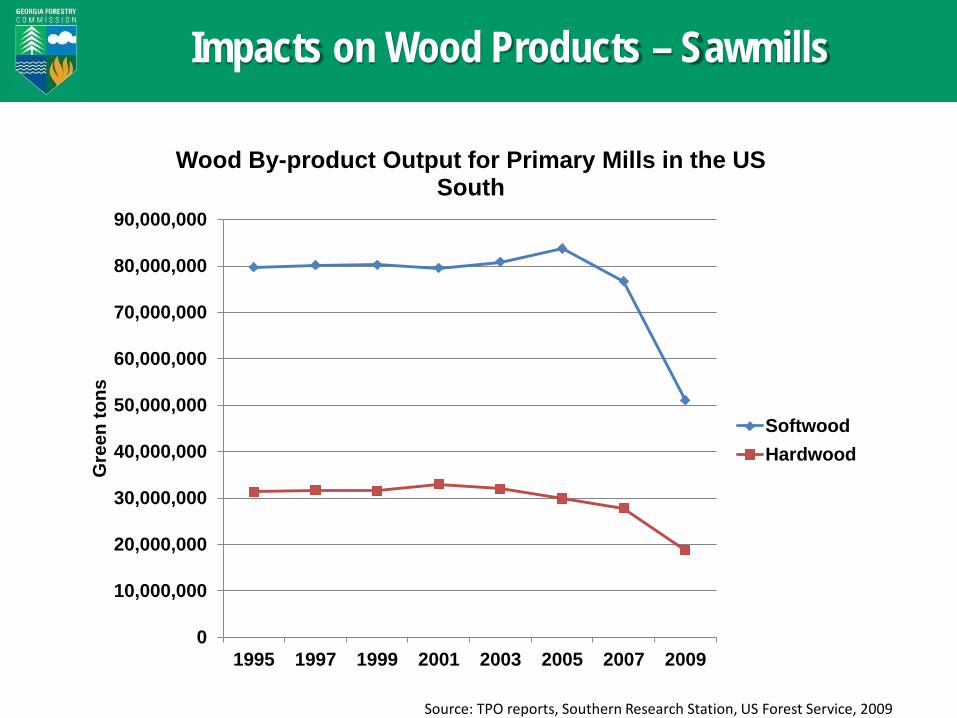

Impacts on Wood Products – Sawmills

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

90,000,000

1995 1997 1999 2001 2003 2005 2007 2009

Gre

en to

ns

Wood By-product Output for Primary Mills in the US South

SoftwoodHardwood

Source: TPO reports, Southern Research Station, US Forest Service, 2009

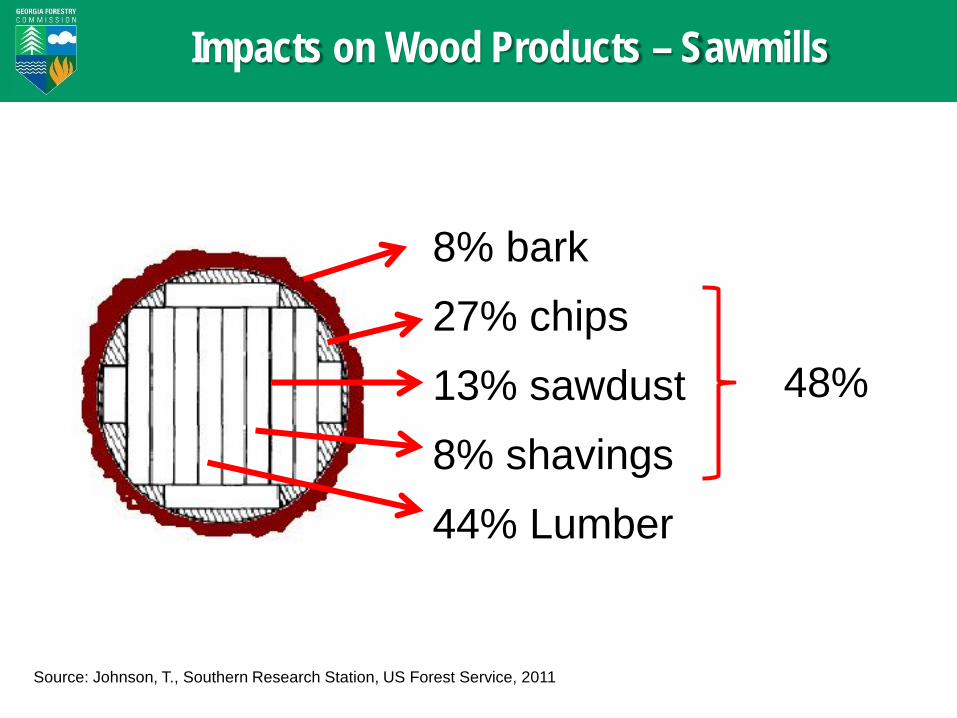

Impacts on Wood Products – Sawmills

8% bark 27% chips 13% sawdust 8% shavings 44% Lumber

48%

Source: Johnson, T., Southern Research Station, US Forest Service, 2011

Wood Demand – Southern Pine Volume Shift

Pulpwood OSB

Pellets

Lumber

Adjusts with Local Market Prices

8” DBH

12” DBH

GA: Increased 23 mil tons since 2002

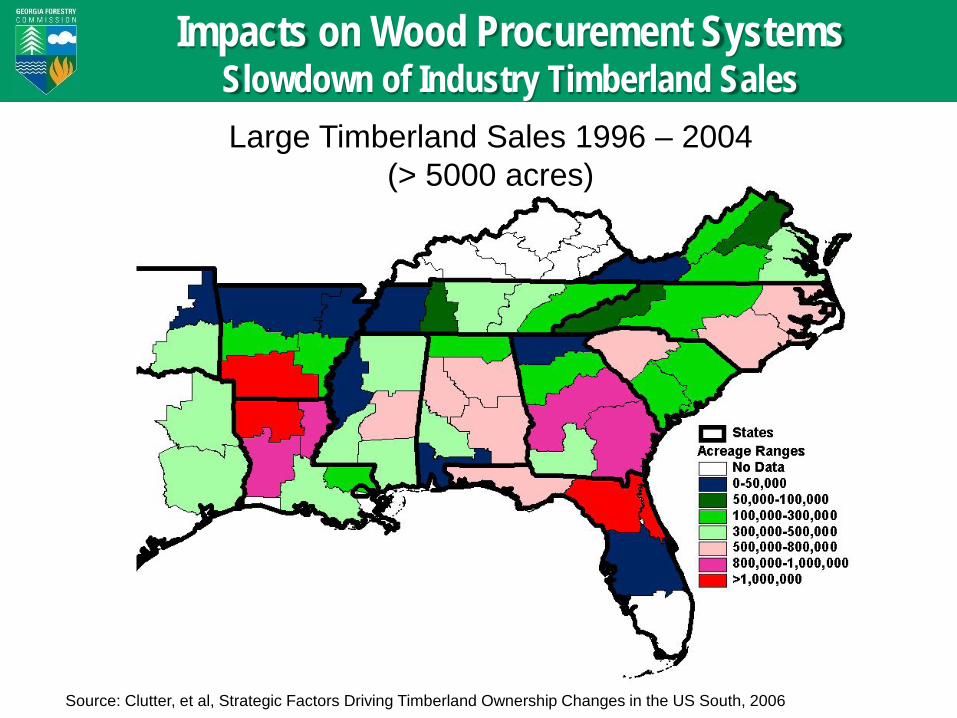

Impacts on Wood Procurement Systems Slowdown of Industry Timberland Sales Large Timberland Sales 1996 – 2004

(> 5000 acres)

Source: Clutter, et al, Strategic Factors Driving Timberland Ownership Changes in the US South, 2006

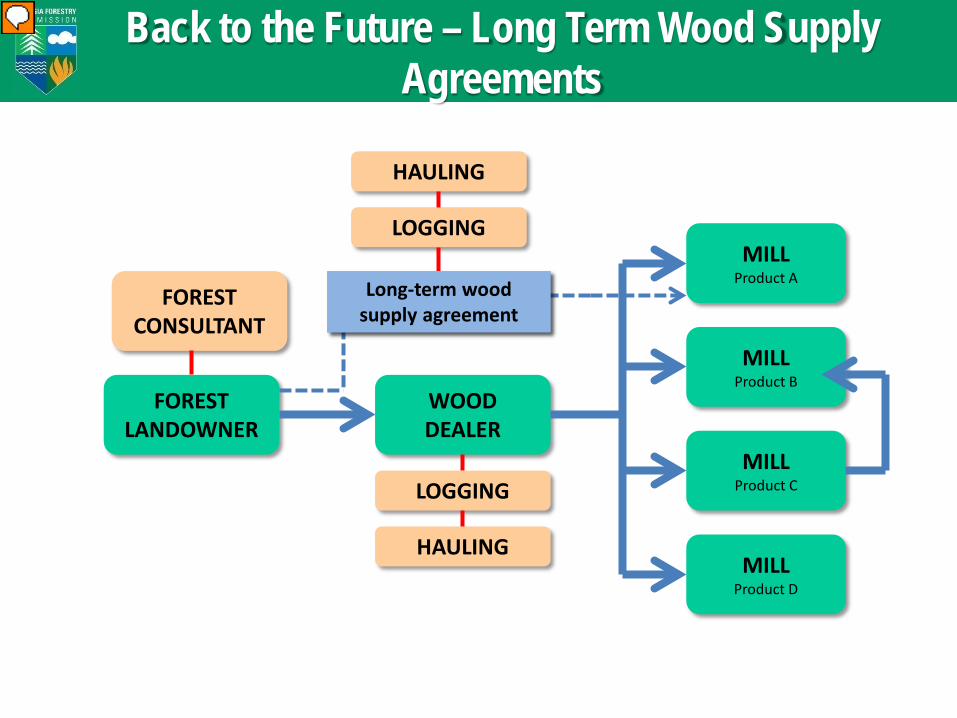

Back to the Future – Long Term Wood Supply Agreements

MILL Product A

MILL Product B

MILL Product C

MILL Product D

FOREST LANDOWNER

FOREST CONSULTANT

WOOD DEALER

LOGGING

HAULING

LOGGING

HAULING

Long-term wood supply agreement Long-term wood

supply agreement

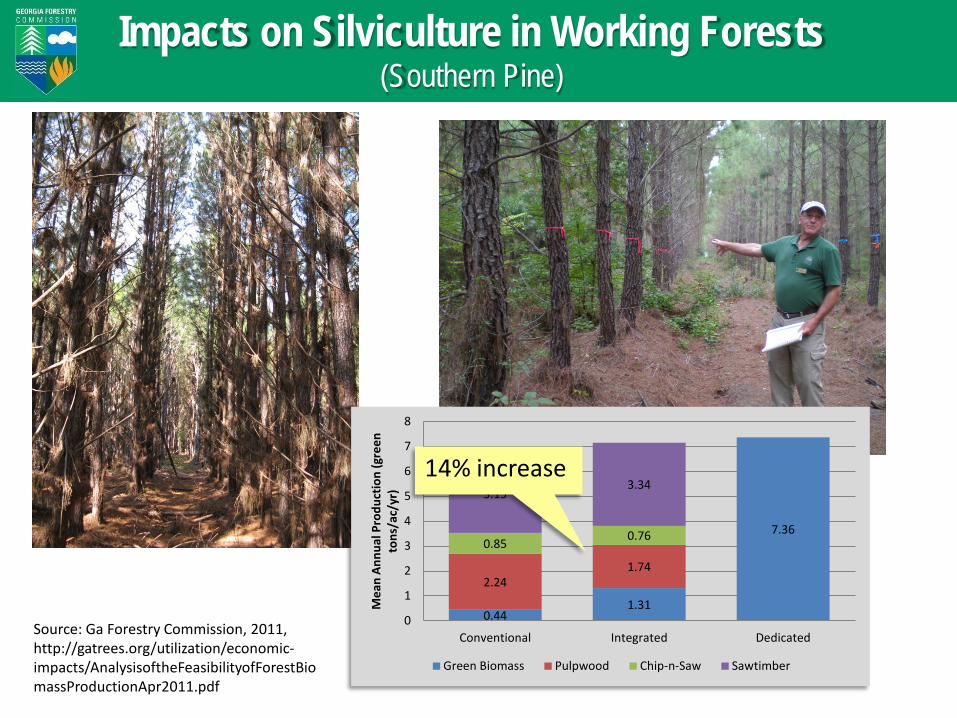

Impacts on Silviculture in Working Forests (Southern Pine)

0.44 1.31

7.36

2.24 1.74

0.85 0.76

3.15 3.34

0

1

2

3

4

5

6

7

8

Conventional Integrated Dedicated

Mea

n An

nual

Pro

duct

ion

(gre

en

tons

/ac/

yr)

Green Biomass Pulpwood Chip-n-Saw Sawtimber

14% increase

Source: Ga Forestry Commission, 2011, http://gatrees.org/utilization/economic-impacts/AnalysisoftheFeasibilityofForestBiomassProductionApr2011.pdf

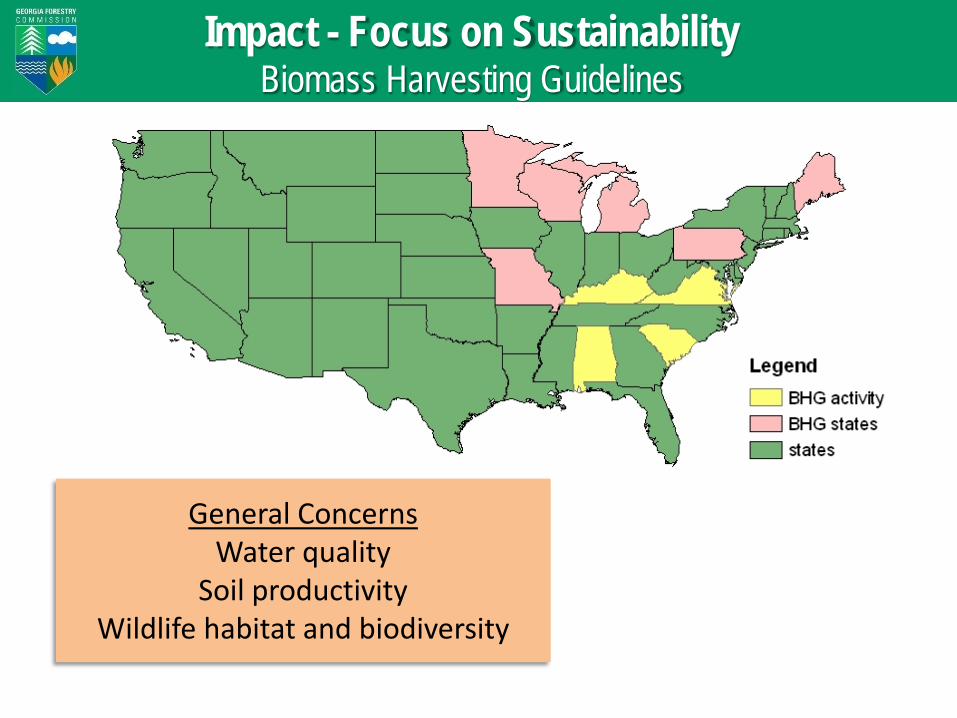

General Concerns Water quality

Soil productivity Wildlife habitat and biodiversity

Impact - Focus on Sustainability Biomass Harvesting Guidelines

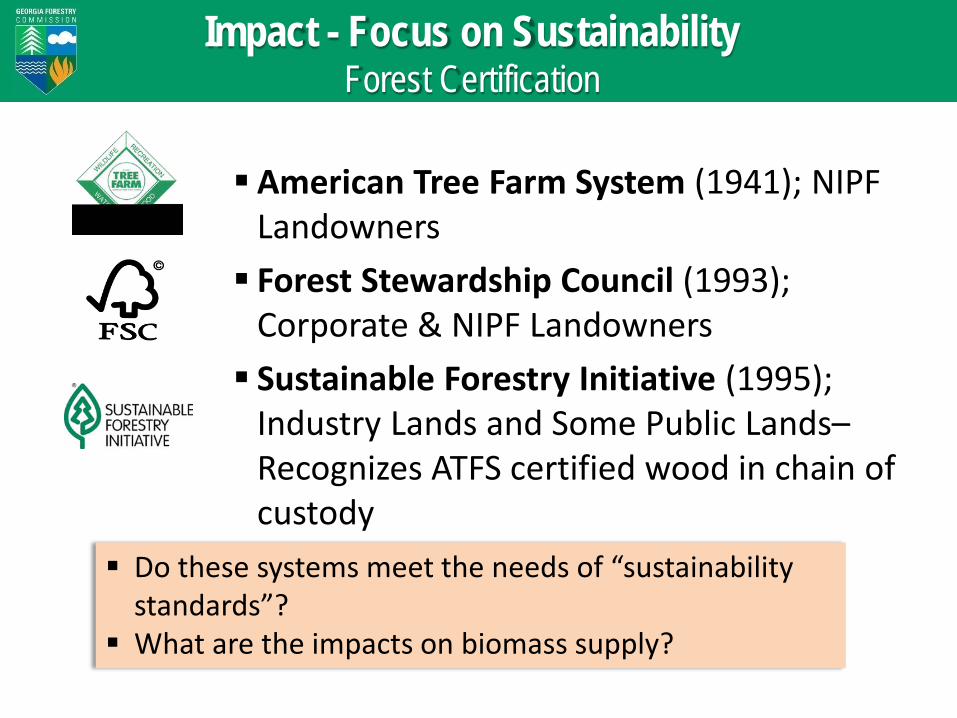

American Tree Farm System (1941); NIPF Landowners Forest Stewardship Council (1993);

Corporate & NIPF Landowners Sustainable Forestry Initiative (1995);

Industry Lands and Some Public Lands– Recognizes ATFS certified wood in chain of custody

Do these systems meet the needs of “sustainability standards”?

What are the impacts on biomass supply?

Impact - Focus on Sustainability Forest Certification

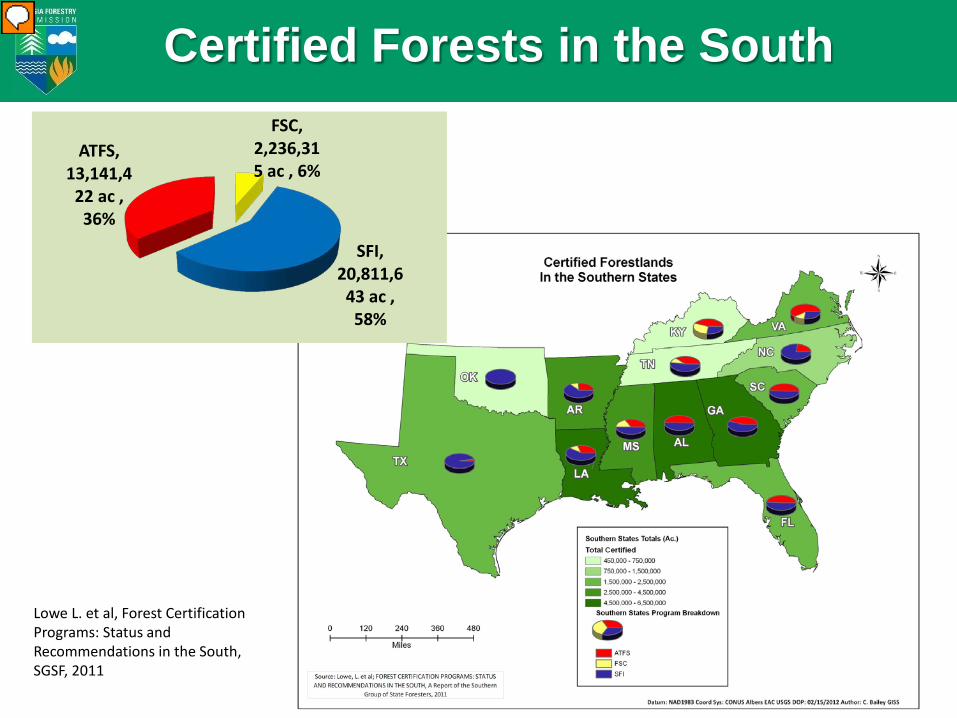

Certified Forests in the South

Lowe L. et al, Forest Certification Programs: Status and Recommendations in the South, SGSF, 2011

FSC, 2,236,315 ac , 6%

SFI, 20,811,6

43 ac , 58%

ATFS, 13,141,4

22 ac , 36%

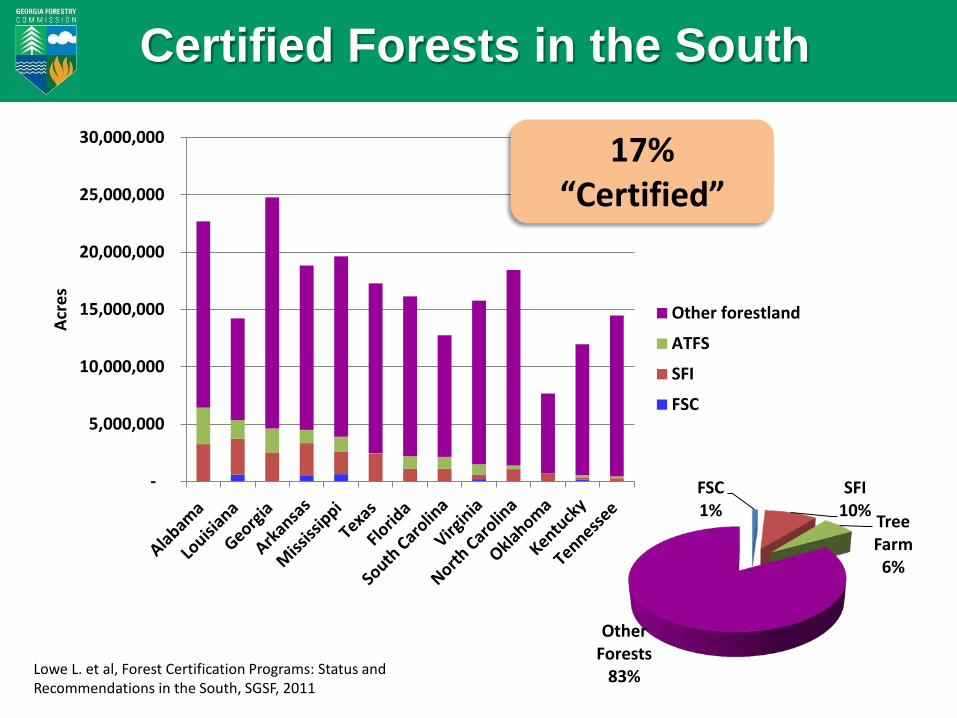

Certified Forests in the South

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

Acre

s

Other forestland

ATFS

SFI

FSC

17% “Certified”

FSC 1%

SFI 10% Tree

Farm 6%

Other Forests

83% Lowe L. et al, Forest Certification Programs: Status and Recommendations in the South, SGSF, 2011

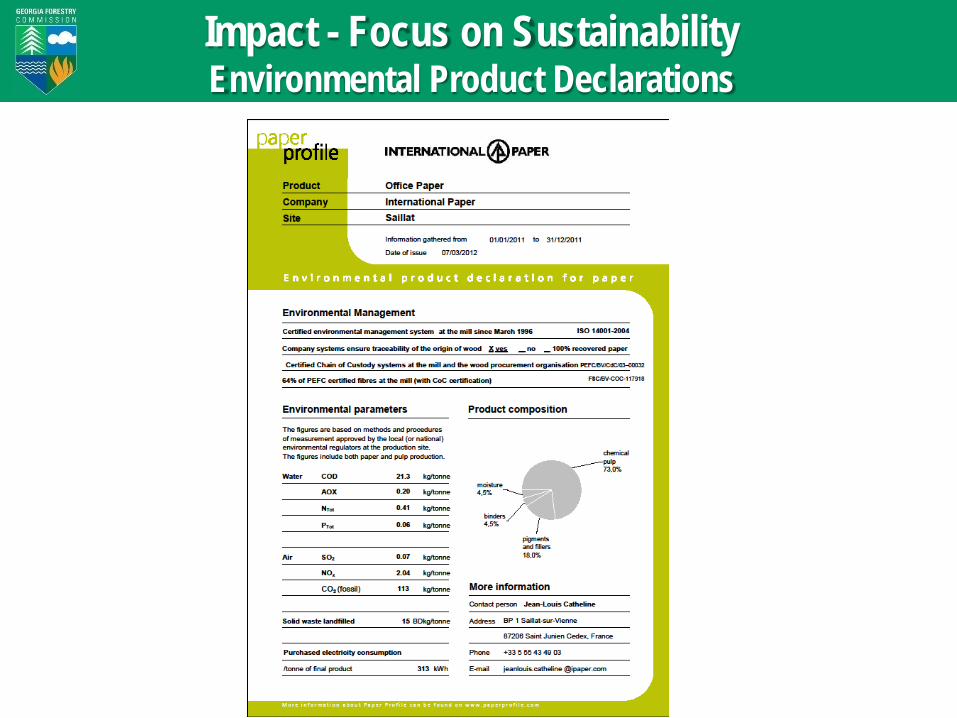

Impact - Focus on Sustainability Environmental Product Declarations

Land Prep- Rake & Pile 0.71 gl Diesel

Land Prep- Bedding 0.86 gl Diesel

Land Prep- Herbicide .149 gl Diesel

Harvest - Final 0.4- 0.6 gl Diesel

Harvest - Thinning 0.6-0.9 gl Diesel

Hand Planting 0 gl Diesel

Chipping 0.4 – 0.6 gl Diesel

Mechanical Tree Planting 0.46 gl Diesel

Transport to Mill – 50 mi. 0.73 gl Diesel

Drying – fossil supplement 319,000 btu

Drying – bark fuel 1,032,000 btu

Mill Processing 242,000 btu

Land Prep- Rake & Pile Mech. Tree Planting, Firebreaks

1.2 gl Diesel (156,600 btu)

Harvest, Chipping & Transport 1.9 gl Diesel (247,950 btu)

Drying & Mill Processing (1,593,000 btu)

1 green ton of small diameter wood

(8,600,000 btu)

0.49 ton wood pellets (6,602,450 btu)

1

4

3

3

3

Pre-suppression Firebreaks 0.01 gl Diesel

2

Energy Balance of Wood Pellets from Small Pine

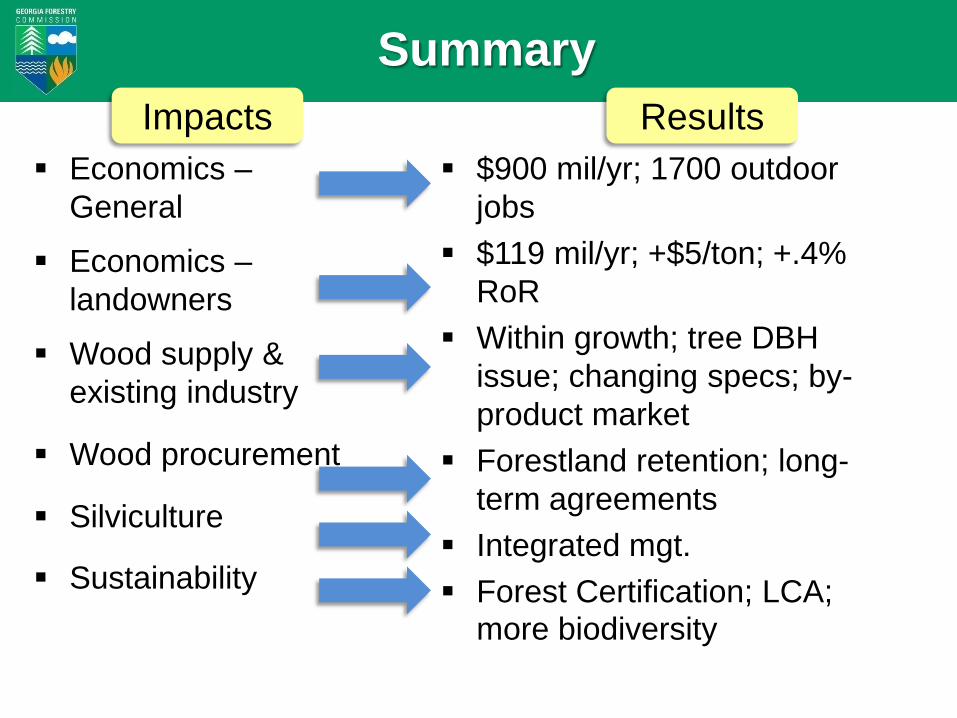

Summary

Economics – General

Economics – landowners

Wood supply & existing industry

Wood procurement

Silviculture

Sustainability

$900 mil/yr; 1700 outdoor jobs

$119 mil/yr; +$5/ton; +.4% RoR

Within growth; tree DBH issue; changing specs; by-product market

Forestland retention; long-term agreements

Integrated mgt. Forest Certification; LCA;

more biodiversity

Impacts Results