Embed Size (px)

Citation preview

Forecasting and Analysisfor Associations

Brett McCallonDirector, FinanceMGMADenver, CO

Learning Objectives

- 2 -©2021 MGMA. All rights reserved.

Discuss financial best practices for associations

• Explain relationship between budget, forecast, and analytics• List types of reports and platforms• Review management processes and governance

Review basics of forecasting and financial analysis

• Outline goal of forecasting and various methodologies • Describe how analysis supports forecasting• Illustrate examples of analytics for associations

- -- 3 -©2021 MGMA. All rights reserved.

WHAT IS THE ROLE OF A FINANCE FUNCTION?

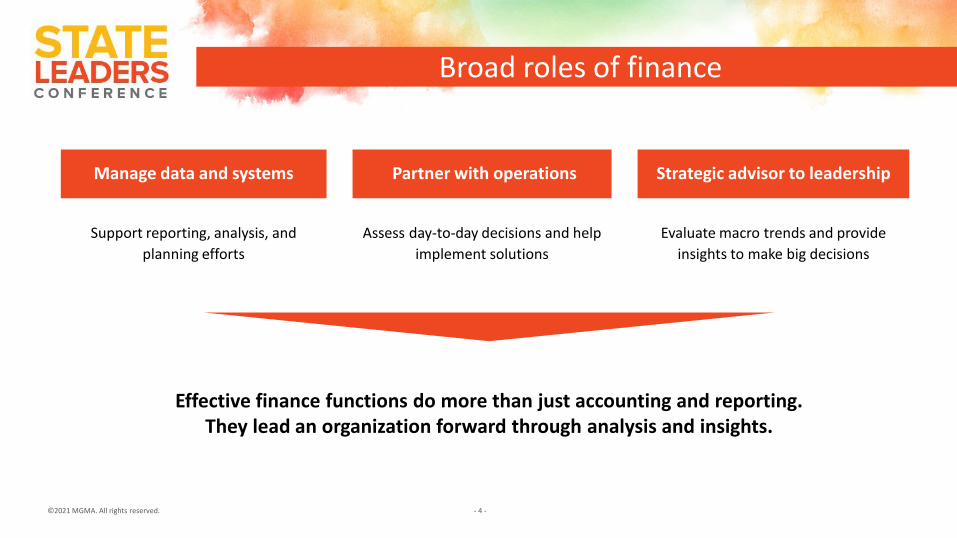

Support reporting, analysis, and

planning efforts

Assess day-to-day decisions and help

implement solutions

Evaluate macro trends and provide

insights to make big decisions

Manage data and systems Partner with operations Strategic advisor to leadership

Broad roles of finance

- 4 -©2021 MGMA. All rights reserved.

Effective finance functions do more than just accounting and reporting. They lead an organization forward through analysis and insights.

Past(Reports)

Day-to-Day(Transactions)

Future(Plans)

Accounts payable

Accounts receivable

Payroll

CRM

Month-end accounting

Reporting

KPI Monitoring

Analysis

Budget

Forecast

Strategy

Business model

Tactical roles of finance

- 5 -©2021 MGMA. All rights reserved.

today’s focus

• New forecasting and analytics function at MGMA National level

• Where are you on spectrum of financial sophistication, resource availability?

• What common elements can be applied across our associations?

• How can outsourced finance function best support you?

Level set: where are we in finance evolution?

- 6 -©2021 MGMA. All rights reserved.

- -- 7 -©2021 MGMA. All rights reserved.

FINANCIAL MANAGEMENT

BEST PRACTICES

Financial management life cycle

- 8 -©2021 MGMA. All rights reserved.

Reassess• Forecast• Trend analysis• Cash flow• Predictive analytics

Plan• Budget• Workforce• LRP / strategy• What-if, scenario analysis

Execute and Monitor• Financial / operational reporting• Variance analysis• KPIs / Dashboards• Accountability / mgmt. process

- -- 9 -©2021 MGMA. All rights reserved.

PLAN

Why do we budget?

- 10 -©2021 MGMA. All rights reserved.

• Setting goals and business priorities

• Define and measure success

• Plan for future financial needs

• Use as guidepost to change course if needed

• Serve as formal approval process

• Accountability

Types of budgets

- 11 -©2021 MGMA. All rights reserved.

Revenue and expenses generated by day-to-day business activityOperational• Full income statement budget by month

• Primary deliverable of any budget process

• Usually consolidation of smaller department or line item budgets (see next slide)

Fixed asset investments or expendituresCapital• Estimated amounts and timing of fixed asset purchases during a given budget period

• Typically requires prioritization and approval process

• Not recognized as expenses on income statement, but rather depreciated over many years

Estimation of cash flows over budget periodCash• Measure increase or decrease in cash based on planned activities

• Calculated using assumptions from operational and capital budgets, as well as financing / investing activities

• Consider all sources of capital to fund the business

Budget life cycle

- 12 -©2021 MGMA. All rights reserved.

Best practices

• Create plan in advance

• Goal setting with leadership

• Allow time for iterations

• Generate ‘buy-in’

• Thorough review process

Life cycle dependencies

• Business needs / restrictions

• Methodology or approach

• Scale and complexity

• Operator involvement

• Approval process

Example budget cycle

- 13 -©2021 MGMA. All rights reserved.

Best practices

• Create plan in advance

• Goal setting with leadership

• Allow time for iterations

• Generate ‘buy-in’

• Thorough review process

Lifecycle dependencies

• Business needs / restrictions

• Methodology or approach

• Scale and complexity

• Operator involvement

• Approval process

Months until start of new budget year:

012345

Planning / goal setting

Budgeting

Reviews Reviews

Final Approval

Considerations for building a budget:

• Tie assumptions to operational metrics you can track

• Fixed vs flexible budgeting

• Review tools and reports

• Benchmarking (internal and external)

• Maintain clear documentation

• Operator involvement / autonomy

Budgeting mechanics

- 14 -©2021 MGMA. All rights reserved.

Budget watch-outs

- 15 -©2021 MGMA. All rights reserved.

• Padding or ‘sandbagging’

• Use it or lose it mentality

• Overly aggressive targets

- -- 16 -©2021 MGMA. All rights reserved.

REASSESS

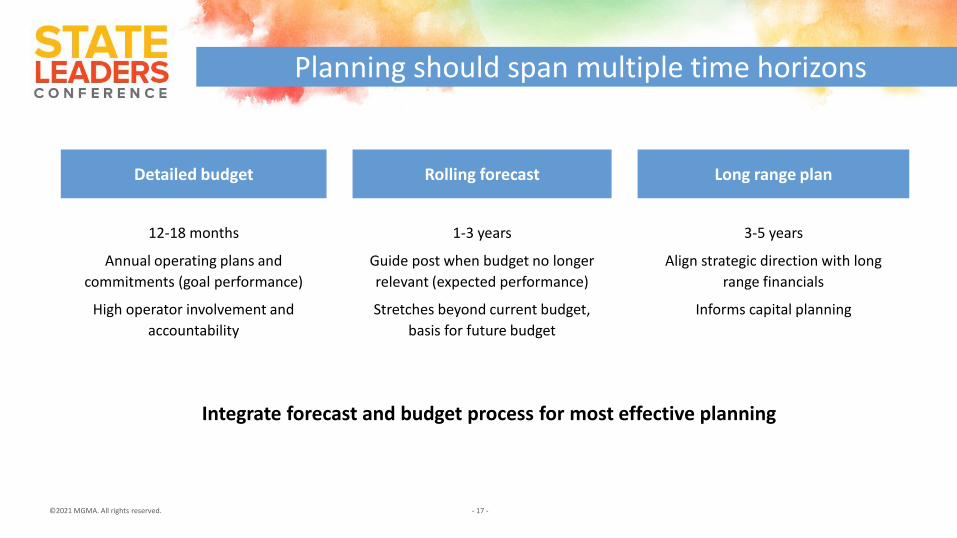

Planning should span multiple time horizons

- 17 -©2021 MGMA. All rights reserved.

Rolling forecastDetailed budget Long range plan

12-18 months

Annual operating plans and

commitments (goal performance)

High operator involvement and

accountability

1-3 years

Guide post when budget no longer

relevant (expected performance)

Stretches beyond current budget,

basis for future budget

3-5 years

Align strategic direction with long

range financials

Informs capital planning

Integrate forecast and budget process for most effective planning

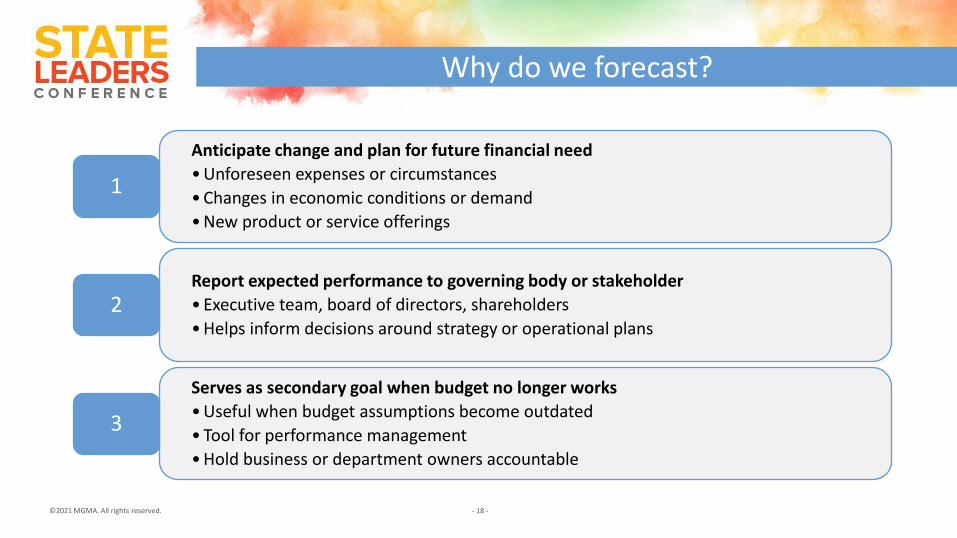

Why do we forecast?

- 18 -©2021 MGMA. All rights reserved.

Anticipate change and plan for future financial need

• Unforeseen expenses or circumstances

• Changes in economic conditions or demand

• New product or service offerings

1

Report expected performance to governing body or stakeholder

• Executive team, board of directors, shareholders

• Helps inform decisions around strategy or operational plans2

Serves as secondary goal when budget no longer works

• Useful when budget assumptions become outdated

• Tool for performance management

• Hold business or department owners accountable

3

Accurate forecasting requires context

- 19 -©2021 MGMA. All rights reserved.

Where are we going(future changes)

Where have we been(past performance)

• Budget variances

• Trends

• Events and timing

• Non-recurring items

• New initiatives / projects

• Internal and external forces

• Org strategy

• Deviation in assumptions

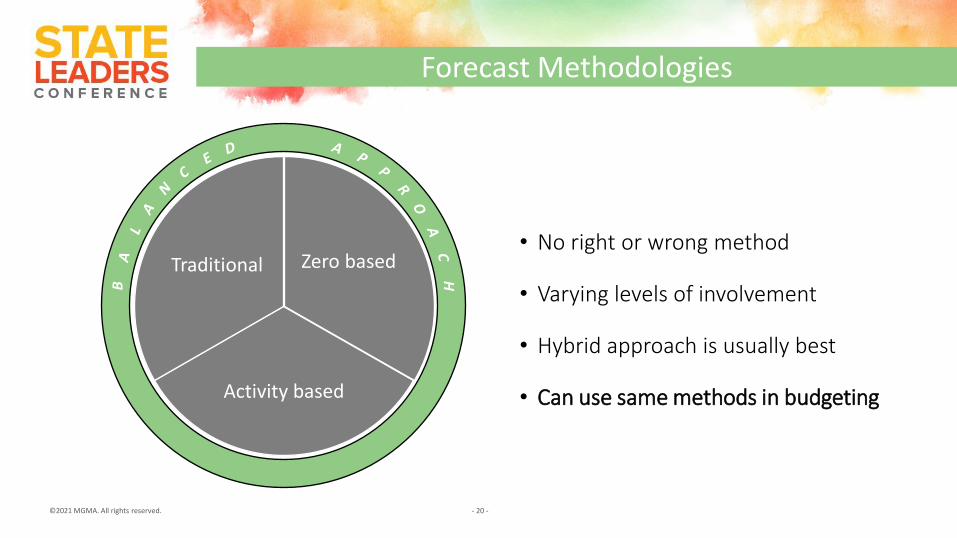

Forecast Methodologies

- 20 -©2021 MGMA. All rights reserved.

• No right or wrong method

• Varying levels of involvement

• Hybrid approach is usually best

• Can use same methods in budgeting

Zero based

Activity based

Traditional

B

H

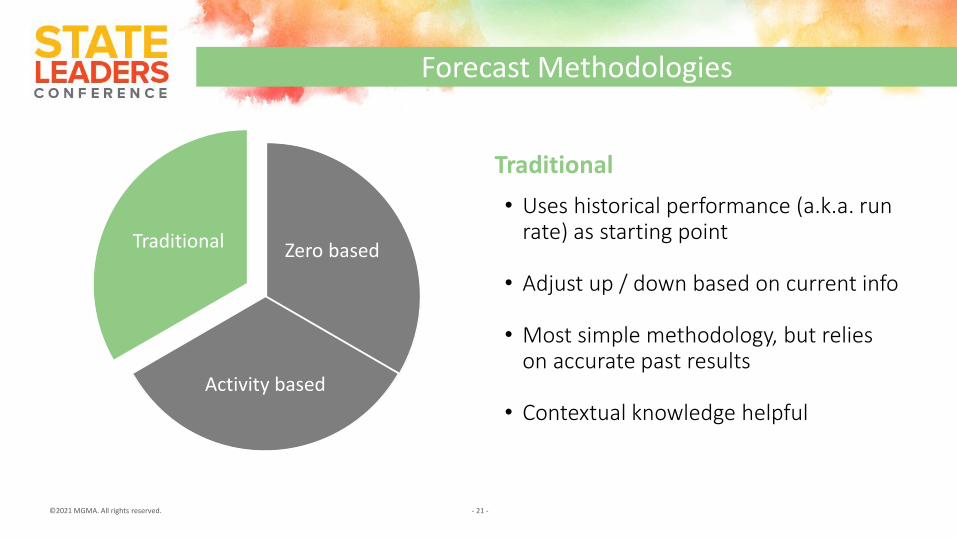

Forecast Methodologies

- 21 -©2021 MGMA. All rights reserved.

• Uses historical performance (a.k.a. run rate) as starting point

• Adjust up / down based on current info

• Most simple methodology, but relies on accurate past results

• Contextual knowledge helpful

Traditional

Zero based

Activity based

Traditional

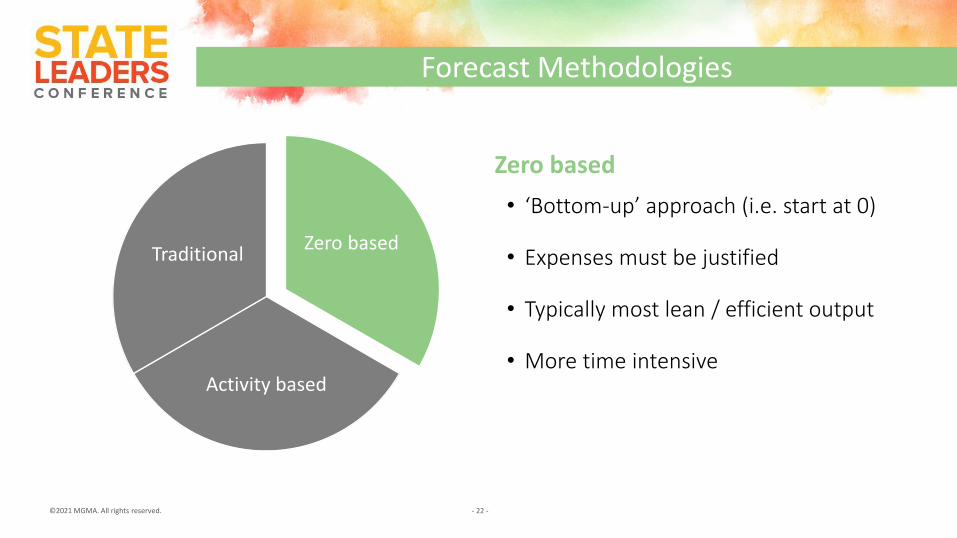

Forecast Methodologies

- 22 -©2021 MGMA. All rights reserved.

• ‘Bottom-up’ approach (i.e. start at 0)

• Expenses must be justified

• Typically most lean / efficient output

• More time intensive

Zero based

Zero based

Activity based

Traditional

Forecast Methodologies

- 23 -©2021 MGMA. All rights reserved.

• ‘Top-down’ approach

• Targets set first

• Must ‘back into’ inputs and assumptions that achieve targets

• Expenses based on output needed

Activity based

Zero based

Activity based

Traditional

Initiatives based forecasting

- 24 -©2021 MGMA. All rights reserved.

• Use prior methods• “Steady state” assumptions

Base Case

New Initiatives

Final Output

• Cost reduction• Member acquisition• Long-term investments

• Financial statements• Operational metrics

- -- 25 -©2021 MGMA. All rights reserved.

BUT… HOW DO WE KNOW WHAT ASSUMPTIONS TO USE IN

FORECASTING?

- -- 26 -©2021 MGMA. All rights reserved.

EXECUTE / MONITOR

Reporting to support financial management process

- 27 -©2021 MGMA. All rights reserved.

DASHBOARDS

Overall health

Quantitative or qualitative

Most important metrics only

Aligned with strategy and goals

FINANCIAL STATEMENTS

Income statement

Balance sheet

Cash flow

General ledger

WHAT

VARIANCE ANALYSIS

Budget

Prior periods

Forecast

Trend

Benchmarks

Goals / targets

WHERE

ANALYTICS / KPIs

Rate + volume

Customer mix

Labor

Fixed + variable costs

Marketing effectiveness

Sales conversion

WHY

Increasing level of detail

• Standard reports to track key operational metrics

• Ad hoc analysis to evaluate outliers

• Normalize for unusual items

• Peel back layers of metrics to find insights or trends

• Compare to internal trends or external benchmarks / ratios

The role of analytics

- 28 -©2021 MGMA. All rights reserved.

Analytics go deeper than surface-level variance reporting.

They address the underlying drivers of top-level financials.

• New member acquisition

• Member or customer retention

• Customer demographics

• Seasonality

• Customer engagement

• Marketing effectiveness (and return)

• Staffing and productivity

Examples of association analytics

- 29 -©2021 MGMA. All rights reserved.

Most importantly, effective reporting is actionable

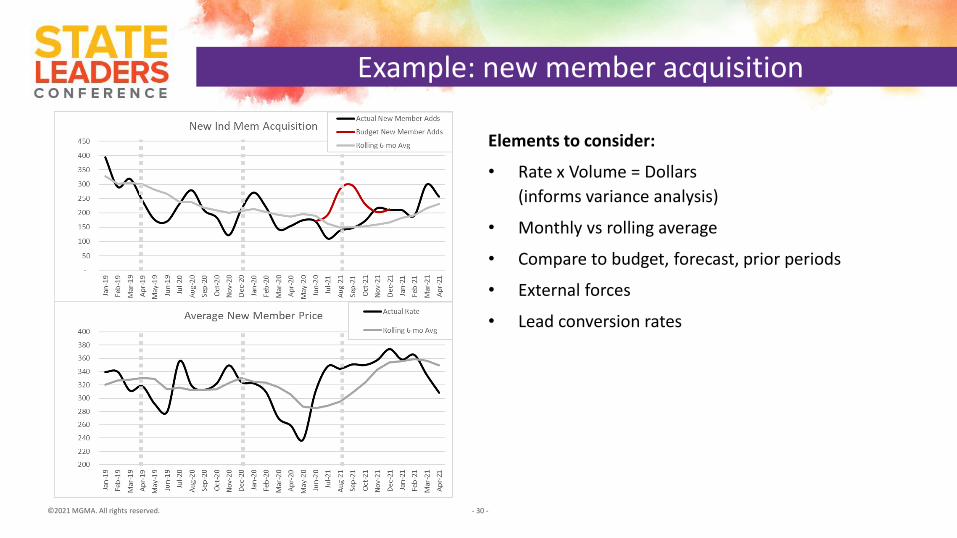

Example: new member acquisition

- 30 -©2021 MGMA. All rights reserved.

Elements to consider:

• Rate x Volume = Dollars

(informs variance analysis)

• Monthly vs rolling average

• Compare to budget, forecast, prior periods

• External forces

• Lead conversion rates

Example: new member acquisition (cont’d)

- 31 -©2021 MGMA. All rights reserved.

Elements to consider:

• Member type “drill-throughs”

(e.g. how product mix impacts rate)

• Impact of marketing campaigns or initiatives

• Discounting

Avg New Member Price Total 2019 2020 L3M L6M L12M

[Member type 1] 297 299 294 300 300 300

[Member type 2] 156 153 155 179 170 163

[Member type 3] 380 379 389 376 378 384

[Member type 4] 691 686 693 685 684 687

[Member type 5] 348 - 349 344 347 348

[Member type 6] 287 285 285 299 294 291

[Member type 7] 349 - - 349 349 349

[Member type 8] 290 - - - - -

[Member type 9] 34 33 35 35 35 35

[Member type 10] 35 35 35 35 35 35

Total 321 317 308 336 350 337

Example: member renewal

- 32 -©2021 MGMA. All rights reserved.

Elements to consider:

• Monthly vs rolling average

• Member vs revenue renewal rate

• Movement across member types

• Eligibility timing and process

• Member count trends (new + renew)

• Payment and renewal timing

Product Movement

From: REG_N < select

To: REG_R < select

Example: member renewal (cont’d)

- 33 -©2021 MGMA. All rights reserved.

Count of Paid Invoices by Days to Renew

(days between current invoice paid date and prior invoice cycle end date)

Renewal Report Status: Renew New Total

Product Code Type: Renew New Total Renew New Total

- (365) 1 - 1 - - - 1

(365) (270) - - - - - - -

(270) (180) - - - - - - -

(180) (90) 2 - 2 - - - 2

(90) (60) 8 - 8 - - - 8

(60) (30) 31 - 31 - - - 31

(30) - 257 1 258 - - - 258 paid early

- 30 118 1 119 - - - 119

30 60 18 - 18 - - - 18 grace period

60 90 3 - 3 - - - 3

90 180 - - - 6 10 16 16 lapsed

180 270 - - - 2 7 9 9

270 365 - - - 3 5 8 8

365 + - - - 3 24 27 27

438 2 440 14 46 60 500

Example: seasonality

- 34 -©2021 MGMA. All rights reserved.

Elements to consider:

• Intra-year seasonality

• Changes year-over-year

• Internal business process

• External forces

• Changes in customer behavior

Example: customer demographics

- 35 -©2021 MGMA. All rights reserved.

Elements to consider:

• Geographical distribution (and white space)

• Size and type (e.g. specialty)

• Member title / position within organization

• Customer purchasing tendencies, by type

• Top customers

Analytics watch outs

- 36 -©2021 MGMA. All rights reserved.

• Oversimplification

• Outliers

• Dirty data

• Overcomplication

Consider most appropriate reporting medium

- 37 -©2021 MGMA. All rights reserved.

Format / platform

• PDF, memo

• Excel

• Interactive dashboard

Delivery method

• Push v pull

• Written v verbal presentation

• On-demand

Frequency

• Ad hoc v recurring

• Level of detail

• Management process dependence

Establishing a management process

- 38 -©2021 MGMA. All rights reserved.

Content

• Prior period variances, trends, forecast

• Operational metrics and initiatives

• Feedback, input, approval

Frequency

• Business need

• Huddles vs formal monthly / quarterly

• Beware of meeting overload

Audience

• Align with frequency and content

• Decision-makers, operators

• Stakeholders (direct, indirect)

Why is this important?

• Proactively manage the business, adapt quickly

• Accountability to budgets, goals, long-term plans

• Cross-functional information flow and awareness

Effective boards have deep understanding of their organization, enabled by effective reporting and analytics

• Financial statement review

• Internal controls and compliance

• Review and approve budget

• Assess current and future risks

• Understand financial implications of vision, strategy, and goals

Board role in financial management

- 39 -©2021 MGMA. All rights reserved.

References

- 42 -©2021 MGMA. All rights reserved.

• CLA• https://www.claconnect.com/resources/articles/2019/whole-organization-finance-mapping-nonprofit-financial-leadership

• MGMA and Kaufman Hall• https://www.mgma.com/event-registration/mgma18-the-operations-conference/session-handouts/con501_no-surprises-

better-budgeting-and-forecasti

• Strategic Finance• https://sfmagazine.com/post-entry/november-2017-12-principles-of-best-practice-fpa/