Embed Size (px)

Citation preview

Corporate Presentation

ASX:CMT

November 2014

www.cottoilandgas.com.au

For

per

sona

l use

onl

y

Certain statements or estimates contained in this presentation, including information as to the futurefinancial or operating performance of Cott Oil & Gas Ltd (Cott) and its projects, are forward‐lookingstatements or estimates. Such forward looking statements or estimates are necessarily based upon anumber of assumptions and estimates that, while considered reasonable by Cott, are inherently subjectto significant technical, business, economic, competitive, political and social uncertainties andcontingencies; involve known and unknown risks and uncertainties that could cause actual events orresults to differ materially from estimated or anticipated events or results reflected in such forward‐looking statements; and may include, among other things, statements regarding targets, estimates andassumptions in respect of production, prices, operating costs, results, capital expenditures, reserves,resources and anticipated flow rates, and are or may be based on assumptions and estimates related tofuture technical, economic, market, political, social and other conditions. Cott disclaims any intent orobligation to update publicly any forward‐looking statements, whether as a result of new information,future events or otherwise. All forward‐looking statements or estimates made in this presentation arequalified by the foregoing cautionary statements. Investors are cautioned that forward‐lookingstatements and estimates are not guarantees of future performance and accordingly investors arecautioned not to rely on forward‐looking statements or estimates due to the inherent uncertaintytherein.

This presentation is not an offer of securities and is not a disclosure document.

2

For

per

sona

l use

onl

y

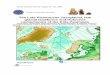

PNG focused oil & gas explorer and project developer

Flagship asset is the Pandora Gas Field (CMT:40%) an offshore gas discovery with 2C 800 bcf with exploration upside

2C Resource net to Cott of 320 bcf (50mmboe)

Previous license holders suggest Pandora could contain up to 1.3 Tcf gas in place

FLNG development concept demonstrates Pandora is technically and commercially viable

PNG is a growing LNG hub for Asia – Cott’s licenses offer excellent exposure to this market

FLN developers have expressed strong interest in a Build Own Operate (tolling) model for project

Also holds net 9,617km2 of highly prospective onshore licenses in PNG’s Western Province

3

For

per

sona

l use

onl

y

ASX Code: CMT

Issued Capital:Ordinary Shares 77.0mOptions ($0.20, Dec 2015) 22.8mOptions ($0.25, Dec 2015) 4.4mOptions ($0.30, Dec 2015) 4.4m

Market Capitalisation:($0.09/share as at 14 November 2014) $6.9m

Cash (31 October 2014): $2.7mDebt: Nil

Major Shareholders:12.9% International Exploration Services Ltd8.7% Michael O’Keeffe (ex‐Riversdale Mining Chairman/ founder)19.9% Cott Management/ Founders (escrowed until Jan 2015)

4

Directors:Mr Stephen Dennis ‐ ChairmanMr Andrew Dimsey ‐Managing DirectorMr David Bradley ‐ Non Executive Director

Company Secretary:Ms Sarah Smith

Management:Mr Marc Jamet – Technical ManagerMr Alistair Jobling – Commercial Manager

Head Office:945 Wellington StreetWest Perth WAAustralia 6005www.cottoilandgas.com.au

For

per

sona

l use

onl

y

License (Area) % Operator Target Resource Location Comment

5

Exploration Assets

PPL 435 (5,670 km2) 50% Kina Petroleum Multi Tcf/MMbbls Western Province Large acreage provides development and

commercial opportunitiesWestern ProvincePPL 436 (13,122km2) 50% Kina Petroleum Multi Tcf/MMbbls

Development Assets

PRL 38 (Pandora) 40% Talisman Energy 2C 800BCF + Offshore Gulf of Papua, PNG

Proposed FLNG or Near Shore LNG Project

EP325 11.1% Strike Energy 16 BCF Carnarvon Basin Retention License over Rivoli Discovery

For

per

sona

l use

onl

y

6

For

per

sona

l use

onl

y

World class petroleum region, proven active hydrocarbon systems, close to Asian LNG demand

Attractive fiscal regime with 2% royalty and 30% corporate tax rate

First shipment from 6.9 mtpa PNG LNG project in May 2014 with expansion up to 5 trains planned

Continued corporate activity including:

Acquisition of interests in PDL10 and PRL21 (Western Province) by Osaka Gas and Mitsubishi

Oil Search acquires 22.835% interest of PRL 15 for $900m

Total purchases 40.1% of PRL15 for fixed ($401m) and contingent payments of up to $3.5 bn

Transform Exploration acquires Eaglewood Energy

Santos farm‐in to Talisman acreage and acquisition of interests from New Guinea Energy

InterOil founder becomes strategic 20% investor in Kina Petroleum for $18m

7

For

per

sona

l use

onl

y

Joint Venture: Cott 40% Talisman 25% (Operator) Kina 25% Santos 10%

Pandora Gas Fields located in Gulf of Papua midway between Port Moresby and Daru in 120m of water at approx 1,400m TVD

Carbonate reef structure with excellent porosity and deliverability

Pandora 1X drilled in 1988 over A Structure discovering a 298m gas column which was tested at 57 mmscfpd

Pandora B1X drilled in 1992 over B Structure discovering a 110m gas column which was tested at 43 mmscfpd

Additional prospects and talus potential identified

8

For

per

sona

l use

onl

y

Discovered by IPC in 1988 with follow‐up well drilled in 1992

515 km2 of 3D seismic over permit to define a 2C Contingent Resource of 792 BCF 1

Extensive evaluation included production and pipeline studies, field development plan, acid gas management and metocean studies

Growing awareness that many gas fields will not be developed other than with FLNG is driving technological development and reducing costs making FLNG far more commercially and technically viable

Focus is on commercialising the PRL 38 interest through farmout of development program or part /full sale to advance production program.

9

For

per

sona

l use

onl

y

FLNG vessel with 170,000m3

storage 2 x 0.5 mtpa water‐cooled

liquefaction trains (Black & Veatch PRICO™)

External turret mooring Side‐by‐side or tandem

offloading to be determined (subject to review of metocean conditions)

Onboard gas treatment , incl amine tower and molecular sieve, to enable reinjection of acid gas stream into reservoir

10

For

per

sona

l use

onl

y

Cott undertook Concept Study for Pandora Gas Field

1 mtpa vessel with 170,000m3 storage

Onboard gas treatment to enable re‐injection of sour gas

Estimated Capex US$900m – US$1,100m (US$900 – US$1,100/ tpa)

Operating Expenses

Vessel operational expense (includes manning, maintenance, reagents) of US$1.50 –US$2.00/mmBtu

‘Cost of ownership’ approximately US$2.50 – US$3.20/mmBtu 1

Combined operating cost of US$4 – US$5.20/mmBtu should enable owner/operator to provide toll service at less than US$6/mmBtu

With field development costs and transport costs both at less than $1.00/mmBtu, the Joint Venture should be able to deliver LNG to North Asia for approximately US$8/mmBtu1 Based on complete amortisation over 10 years at 8% cost of capital

11

For

per

sona

l use

onl

y

12

Project Vessel Owner

Capacitymtpa

Water depth (m)

Status First Gas

Caribbean FLNG Exmar 0.5 Near Shore Practical completion Yard commissioning 2H 2015

PFLNG1 (Kanowit) Petronas 1.2 80 Topside Lifting underway 2016

PFLNG2 (Rotan) Petronas 1.5 1,128 EPCIC awarded 2018

Golar Hilli ‐ Conversion Golar LNG 2.3‐2.8 TBC* Keppel commencing conversion 2015 2017*

Equatorial Guinea FLNG ExcelerateEnergy

2.5 1,800 Midstream Partner appointed 2019

Peru FLNG Exmar 0.5 Near Shore Cooperation Agreement with PRE TBC

* Vessel yet to be committed to a project. Second conversion contract expected Caribbean FLNG Vessel at Wison Nantong Yard

PFLNG 1 at DSME’s Okpo Yard (April 2014)

For

per

sona

l use

onl

y

Several parties with expertise in shipping, including Excelerate Energy, Exmar Marine, Golar LNG and Hoegh LNG, plan to provide toll liquefaction and storage to gas owners

Build Own Operate Terminate (BOOT) contract underpinned by resource

Vessel would be funded by equity and debt and therefore requires proponents with strong technical and financial credentials as well as appropriate insurance cover

Liquefaction tariff to be determined to achieve vessel owner’s required return on investment but likely to be around US$4‐6/mmBtu depending on scale

Commercially acceptable liquefaction tariff to be determined through open‐book analysis of construction, operation and finance costs

Debt funding may be available from Export Credit Agencies, such as World Bank, China EXIM Bank and Australian Export Finance Insurance Corp (EFIC)

13

For

per

sona

l use

onl

y

Pandora FLNG has potential to be a high margin LNG project: Acquired as an existing discovery therefore

minimal sunk costs to recover Field development requires max 4 shallow

wells with dry completions Acid gas can be removed on vessel or

floating platform and re‐injected Toll treatment of pipeline quality gas can be

delivered for less than US$6/mmBtu LNG can be transported to key Asian

markets for US$1/mmBtu

14

For

per

sona

l use

onl

y

15

Cott has identified the optimum pathway for development of the Pandora Gas Field and, potentially, other gas discoveries. It now looks to develop a working group that includes potential owner‐operators, contractors and adjoining licensees

For

per

sona

l use

onl

y

16

5,346 km2 licence approximately 50 Km southwest of PRL 21

2 large leads with basal Cretaceous sand potential adjacent to Lake Murray‐1 gas flow

Shallow (<1,500m) drilling targets with potential for gas and oil

Good potential port infrastructure at Aiambak enabling access for barge‐mounted rig

Aerogravity and aeromagnetic survey complete

For

per

sona

l use

onl

y

13,122 km2 permit with good liquids potential

Excellent river access for barge‐mounted rig

Proximity to proposed gas export infrastructure at Daru

Good seismic correlation with existing aerogravity

No wells drilled on Oriomo High Fairway structure

17

For

per

sona

l use

onl

y

18

The following chart shows the value of recent pre‐development transactions for PNG gas discoveries compared to the current value of Cott

Upside

Base

For

per

sona

l use

onl

y

Stephen Dennis (Non‐Executive Chairman)25 years active involvement in the resources industry. He spent 14 years in senior management roles at MIMHoldings Limited, was Group General Manager and Chief Financial Officer of Minara Resources Limited until late2005. Mr Dennis is currently the CEO and Managing Director of CBH Resources Limited.

Andrew Dimsey (Managing Director)Co‐founder of Cott. 30 years of commercial experience as a senior executive of Beach Petroleum, Alliance Oil,Claremont Petroleum, Elders Resources, Arc Energy, Origin Energy. Focus on all commercial aspects of O&Gindustry ‐‐mergers and acquisition, corporate restructuring, JV arrangements, operations and production.

David Bradley (Non‐Executive Director)Energy industry commercial specialist with 30 years of business development experience including seniormanagement roles with El Paso Corporation, Epic Energy, and consulting roles with Wood McKenzie as well asprivately advising a broad range of upstream, midstream and downstream energy players in developing andexecuting commercialization strategies and business development initiatives. Experience includes significant M&Acoordination roles realising over $2 billion in closed transactions.

Board with considerable senior experience withASX‐listed resources companies.

19

For

per

sona

l use

onl

y