Embed Size (px)

Citation preview

Annual Report 20091

FLSmidth & Co. A/S

Annual Report 2009

Annual Report 20092

Facts about FLSmidth & Co. - a leading supplier of equipment and services to the global cement and minerals industries

A global company with a strong local presence worldwideHead office in Denmark, major engineering centres in India and USA10,664 employees worldwideStrong track record and 128 years of experience

Geographical distribution of employees

Annual Report 20093

Investing in FLSmidth & Co. A/S

2009 2008Total shareholder return : 104% (64%)Pay-out ratio: 22% (DKK 2+5 per share) 0%EPS (diluted) : DKK 31.9 28.8Number of shareholders: 44,800 42,000Market Cap: DKK 19.5bn DKK 9.6bn

Annual Report 20094

Key messages in Annual Report 2009

Historically strong performance 2009 2008– Cash flow from operations (DKK) 2,470m 2,324m– EBIT margin 9.8% 9.5%– Net profit (DKK) 1,664m 1,515m

Proposed dividend DKK 5 per share (on top of DKK 2 already paid in 2009)

Order intake in 2010 is expected to increase in both Cement and Minerals vs. 2009

Expected revenue in 2010: DKK 19-20bn

Expected EBIT margin in 2010: 8-9%

Annual Report 20095

Asset light business model is working well

Engineering house and technology provider

Flexible cost structure (payroll)

Most manufacturing is outsourced(~80-90%)

Low working capital due to prepayments from customers (typically 10-25% of total contract amount upfront)

Low maintenance CAPEX (~2% of revenue at present)

Order related engineering off-shored to India

Increased sourcing from competitive-cost-countries(~25% at present)

Annual Report 20096

Highlights 2009

DKKm 2009 2008 change

Revenue 23,134 25,285 -9%

EBITDA (before special non-recurring items) 2,725 2,911 -6%

EBIT 2,261 2,409 -6%

Profit for the year 1,664 1,515 +10%

Order intake 13,322 30,176 -56%

Order backlog 21,194 30,460 -30%

Net interest bearing receivables /(debt) 1,085 (574)

Working capital 21 207

CFFO 2,470 2,324 +6%

Free cash flow 1,965 1,453 +35%

Investments in R&D 315 268 +18%

Number of employees 10,664 11,510 -7%

Annual Report 20097

Revenue 2009

Revenue in 2009: DKK 23,134m down 9% vs. 2008

Strong order backlog at the beginning of the year provided protection against weak business climate in 2009 resulting in a soft landing

Developing countries accounted for 71% of revenue in 2009 (2008: 67%) – of which BRICs accounted for 28% (2008: 13%)

Cement is still the largest business segment accounting for 56% of revenue in 2009 (2008: 54%)

Annual Report 20098

A strong financial platform

Equity ratio 30%-target reached in 2009

No net debt (End 2009: Net interest bearing receivables DKK 1,085m)

Committed credit facilities extended to 2013Working capital close to zero (End 2009: DKK 21m)

New dividend policy: DKK 7 per share per year

574

1.583

-1000

-500

0

500

1000

1500

2000

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

(1,0)

(0,5)

-

0,5

1,0

NIBD & Gearing Equity & equity ratioEquity ratioGEARING

NIBD / EBITDANIBD (DKKm) Equity (DKKm)

Net interest bearing receivables

6.627

5.0354.214

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

0

5

10

15

20

25

30

35Equity ratio target: 30%

Net interest bearing debt

Annual Report 20099

Key strategic focus areas in coming years

Stronger focus in Minerals– Prioritize growth industries– Enhance customer intimacy– Focused technology portfolio

Stronger focus on China and India– Growing regional markets– India: internal sourcing of engineering and back-office– Group Management to be represented in India from

1 July 2009 by Bjarne Moltke Hansen– China: internal and external sourcing of manufactured

components and equipment

Increased activity in Customer Services– New and innovative service concepts– O&M contracts

One Company – One Name – ”One Source”– Subsidiaries and product companies to be named FLSmidth– Branding platform being launched

Annual Report 200910

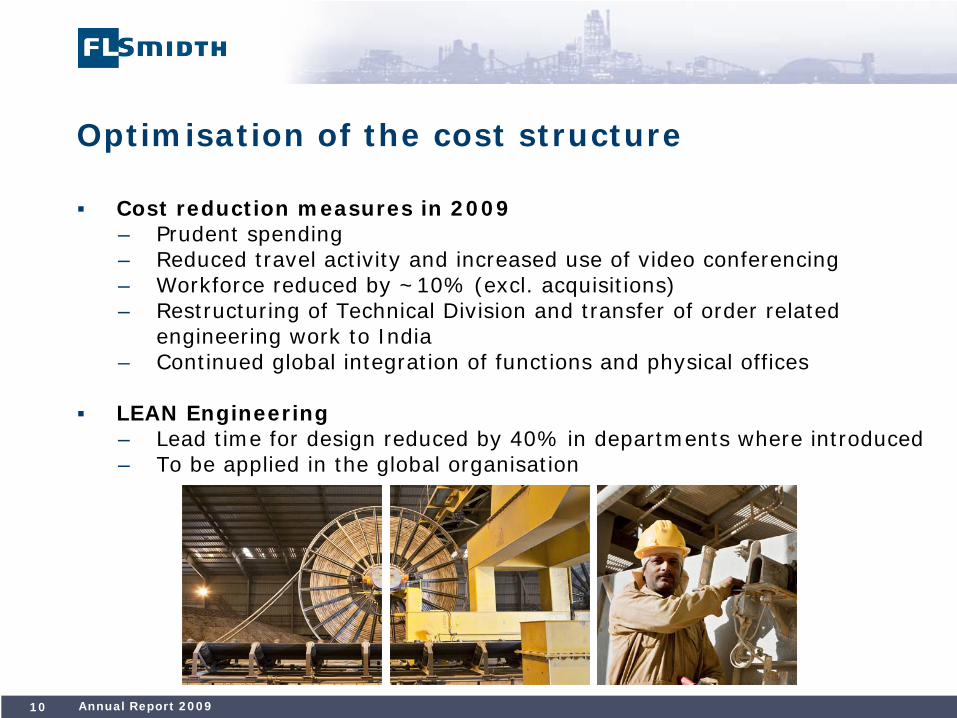

Optimisation of the cost structure

Cost reduction measures in 2009– Prudent spending– Reduced travel activity and increased use of video conferencing– Workforce reduced by ~10% (excl. acquisitions)– Restructuring of Technical Division and transfer of order related

engineering work to India– Continued global integration of functions and physical offices

LEAN Engineering– Lead time for design reduced by 40% in departments where introduced– To be applied in the global organisation

Annual Report 200911

6.535

7.574

6.479

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

Revenue (quarterly) EBIT adj.*) (quarterly)

-14% vs. Q4 2008

Satisfactory revenue and margins in 2009

Revenue down 9% yoy– Customer Services revenue up 2% yoy– Traditional seasonal quarterly pattern repeated in 2009

EBIT ratio 9.8% vs. 9.5% in 2008, exceeding own expectations– Positively impacted by improved order execution, higher than expected revenue

and finalisation of projects– Our asset light business model is working!

-10% vs. Q4 2008

*) Adjusted for effect of purchase allocation regarding GL&V Process

DKKm

788

680

873

0

200

400

600

800

1.000

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

DKKm

Annual Report 200912

Development in Cement & Minerals EBITA ratio (Group EBIT excl. Cembrit and purchase price allocations related to GL&V)

3,7%6,3%

9,9%

11,1%10,9%

0

5000

10000

15000

20000

25000

2005 2006 2007 2008 20090,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

Revenue (Cement & Minerals)

EBITA ratio (Cement & Minerals)

Annual Report 200913

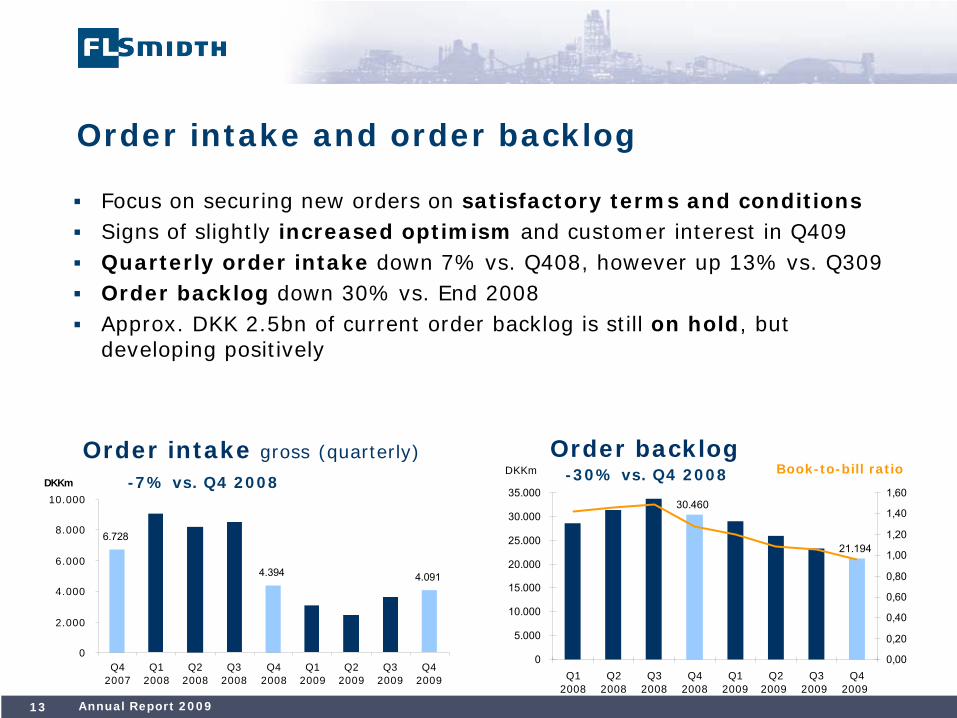

Order intake and order backlog

4.0914.394

6.728

0

2.000

4.000

6.000

8.000

10.000

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

Order intake gross (quarterly) Order backlog

Focus on securing new orders on satisfactory terms and conditionsSigns of slightly increased optimism and customer interest in Q409Quarterly order intake down 7% vs. Q408, however up 13% vs. Q309Order backlog down 30% vs. End 2008 Approx. DKK 2.5bn of current order backlog is still on hold, but developing positively

-7% vs. Q4 2008 -30% vs. Q4 2008 Book-to-bill ratioDKKm

21.194

30.460

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

0,00

0,20

0,40

0,60

0,80

1,00

1,20

1,40

1,60

Annual Report 200914

Cash management in 2009 Strong cash-flow generation and working capital under control

167

637835

451614

20721

-800

-600

-400

-200

0

200

400

600

800

1.000

Q42007

Q1 2008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

Working capital

717613

1.281

192

416

939 923

499

(400)

(200)

0

200

400

600

800

1.000

1.200

1.400

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

CFFO

1.392 1.4851.650

1.920 1.893 1.890

1.463

1.802 1.760

0

500

1.000

1.500

2.000

2.500

Q42007

Q1 2008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

Inventories-2% vs. End 2008

Dedicated effort throughout 2009 to reduce trade receivables and inventories, and to optimise trade creditors

Increasing trend in working capital reversed in Q3 and Q4

Annual Report 200915

Cash management focus areas

4.286 4.5484.908

4.333 4.2763.696

4.939 5.063

4.270

0

1.000

2.000

3.000

4.000

5.000

6.000

Q42007

Q1 2008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

3.8034.394 4.424

2.868 3.0763.538

3.0243.1933.330

0

1.000

2.000

3.000

4.000

5.000

6.000

Q42007

Q1 2008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKmPrepayments (net liability *)-5% vs. End 2008

2.132 2.2392.388 2.467

2.2762.077

2.4642.748

2.421

0

500

1.000

1.500

2.000

2.500

3.000

Q42007

Q1 2008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKmTrade receivables

-16% vs. End 2008Trade creditors-12% vs. End 2008

*) Prepayments from customers less Prepayments to sub-suppliers

337

582653

207

629

-800

-600

-400

-200

0

200

400

600

800

1.000

Q42007

Q1 2008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

Work-in-progress (net asset)

Annual Report 200916

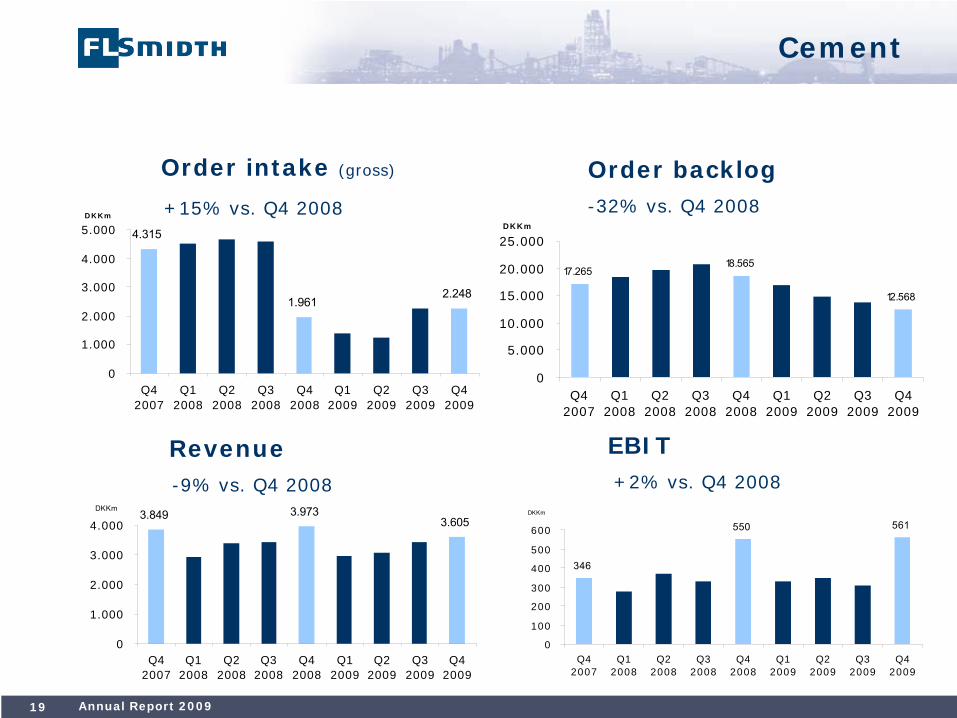

Cement

Highlights 2009

Revenue down by 5%, whileEBIT was up by 2%, and as such, record high - due to higher than expected revenue, improved order execution and finalisation of projects

Acquisition of EEL Limited India

The largest cement plant in the world, Holcim’s Ste. Genevieve, USA, was successfully commissioned in 2009

200913,059

1,54811.9%

200813,7081,521

11.1%

DKKm YTDRevenueEBITEBIT ratio

Current business environment

Market outlook remains somewhat weak, resulting in intensified price competition

Local business opportunities prevail,particularly in:

- North Africa - India - Indonesia - Latin/South America

Annual Report 200917

Holcim, Ste. Genevieve, Missouri, USA The world’s largest cement production line with a capacity of 12,000 tonnes clinker per day

Designed and delivered by FLSmidth

Facts about Ste. Genevieve

Commissioned in 2009

State-of-the art technology

Largest capacity in the world

Lowest OPEX per tonne ordinary portland cement produced

Complies with most stringent environmental regulations

Annual Report 200918

Large cement orders received in 2009

21 July 2009 Uruguay DKK 225m 30 July 2009 Indonesia DKK 420m31 July 2009 Indonesia DKK 420m22 Sep. 2009 Libya (O&M) DKK 330m

14 Oct. 2009 Libya DKK 970m

Annual Report 200919

Order intake (gross)

+15% vs. Q4 2008

Order backlog-32% vs. Q4 2008

Revenue-9% vs. Q4 2008

EBIT+2% vs. Q4 2008

Cement

D KKm

2.2481.961

4.315

0

1.000

2.000

3.000

4.000

5.000

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

12.568

18.56517.265

0

5.000

10.000

15.000

20.000

25.000

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

3.6053.9733.849

0

1.000

2.000

3.000

4.000

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

561550

346

0

100

200

300

400

500

600

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

Annual Report 200920

Expected future average:

~ 60-75 mty

New global contracted cement kiln capacity (excl. of China)

Cement

0

20

40

60

80

100

120

140

160

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

E

mty

2009: 45 mty

2010E: ~50 mty

Expected future average of 60-75 mty is based on an assumption of 3-4% global GDP (excl. China) and a conservative replacement need of 10 mty per annum

Annual Report 200921

Geographical distribution of new global contracted cement kiln capacity

(excl. China)

38% 3%

21% 2% 15%

0% 0% 21%

Annual Report 200922

Market share 2009 Contracted new kiln capacity globally excl. China

Relationship between cement consumption and GDP per capita

Angola Brazil

China

Denmark

Egypt

Germany

Iran

Italy

Libya

Malaysia

MexicoRussia

Saudi Arabia

Spain

ThailandVietnam USA

France

IndiaIndonesia

Japan

Nigeria

Tyrkey

0

200

400

600

800

1000

1200

1400

- 5.000 10.000 15.000 20.000 25.000 30.000 35.000 40.000 45.000 50.000

Cement consumption per capita (kg per year)

GDP per capita (USD per year)

Emerging markets Steep increase in cement consumption per capita as urbanisation and industrialisation increase

Developed countries Declining cement consumption per capita as the economy matures

Cement

Annual Report 200924

Minerals

20099,037

798895

8.8%9.9%

200810,470

9601,2389.2%

11.8%

DKKm YTDRevenueEBITEBIT adj.EBIT ratioEBIT ratio adj.

Highlights 2009

Order intake considerably lower, although improvement seen in Q409

Revenue down by 14% andEBIT by 17% in 2009

Management focus in 2009:1.Stabilise the business2.Prepare for the future3.Redefine our strategic roadmap

Current business environment

Supported by improved market conditions, the mining industry is taking a more optimistic view on 2010 activities, although still cautious

Announced 2010 Capex budgets are supporting increased business activity

Large inquiry list and improved customer interaction, particularly in coal, iron ore, gold, phosphate and copper

Annual Report 200925

1) Stabilise the business

Order intake and backlog developmentMining companies focused on balance sheet optimisation and cash preservationOnly few large projects became contractsIntensified price competition as a result

Minerals

Order intake (gross)

-25% vs. Q4 2008

Order backlog-31% vs. Q4 2008

DKKm

190725442464

0

1000

2000

3000

4000

5000

Q4 2007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

8.777

12.606

8.712

0

5000

10000

15000

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

+39%

Annual Report 200926

Order intake in 2009

Activity has primarily been within coal and alumina

Demand has primarily been for material handling and separation equipment

India has been the most active market

Major contracts in Q409– India, coal DKK 262m– Vietnam, coal DKK 201m

MineralsBreakdown of large order intake in 2009 (orders>DKK 50m)

1) Stabilise the business

Annual Report 200927

1) Stabilise the business

Backlog execution in 2009Some contracts and shipments were postponed or put on hold, resulting in delayed income recognitionSome normalisation in Q4, resulting in the highest levels of revenue and EBIT compared to previous quarters 2009Several contracts on hold are in process of being revitalized

Minerals

Revenue-22% vs. Q4 2008

EBIT adj. -37% vs. Q4 2008

DKKm

2.332

3.414

2.658

0

1000

2000

3000

4000

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

275

441

277

0

100

200

300

400

500

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

*) Adjusted for effect of purchase price allocations related to GL&V Process; DKK -24m in Q4 2008 and DKK -24m in Q4 2009

Annual Report 200928

2) Prepare for the future

Actions to reduce costs in 2009 and protect margins going forwardReduction in forceReduced working weekMonitor operational costsImproved utilisation of resources in IndiaImproved sourcing in cost competitive countriesContinued integration with Cement

Acquisitions in 2009Enhanced flowsheet coverage through acquisition of:

Conveyor Engineering, USA(supplier of major bulk material handling systems)

Summit Valley Equipment & Engineering, USA(modular gold and silver extraction plants and equipment)

Minerals

Annual Report 200929

3) Redefine our strategic roadmap

Strategic review with aligned focus and management attention towardsImproved customer intimacySelected growth industriesKey technologiesGrow Customer Services segmentR&D activities directed towards growth industries and key technologies Acquisitions directed towards growth industries Further develop supply chain management Improved internal coordination and communication through delayeringand simplified management structure in place February 2010

Minerals

Mining equipment suppliers

Exploration Development Extraction Material Handling

Crushing, Grinding & Sizing

Separation Refining

Exploration for mineral resources

•Remote sensing

•Geophysical / geochemical tests

•Samples

Feasibility studies

Drilling and modeling of the ore body

Selection of appropriate mining technique

Capital investment in mine infrastructure

Mining of the ore body

Rock breaking

Surface mining

Underground mining

Mined minerals transported to processing site

Use of loaders, trucks, trains, at the face mining systems and conveyors

Materials are crushed and ground to achieve finer particles

Particles sized for optimum recovery of minerals specie

Flotation, leaching, sedimentation and filtration are used to increase the mineral content to an economic level

Refining to increase concentration of minerals further

Key techniques:

•Pyro-metallurgy

•Electro-winning

Source: Morgan Stanley, FLSmidth

FLSmidth MineralsMetso Minerals

Outotec

SandvikAtlas Copco

Boart Longyear

TerexAstec

Komatsu

Joy GlobalCAT

Chinese (var.)

Bucyrus

Furukawa

Typical mining site plant

Annual Report 200931

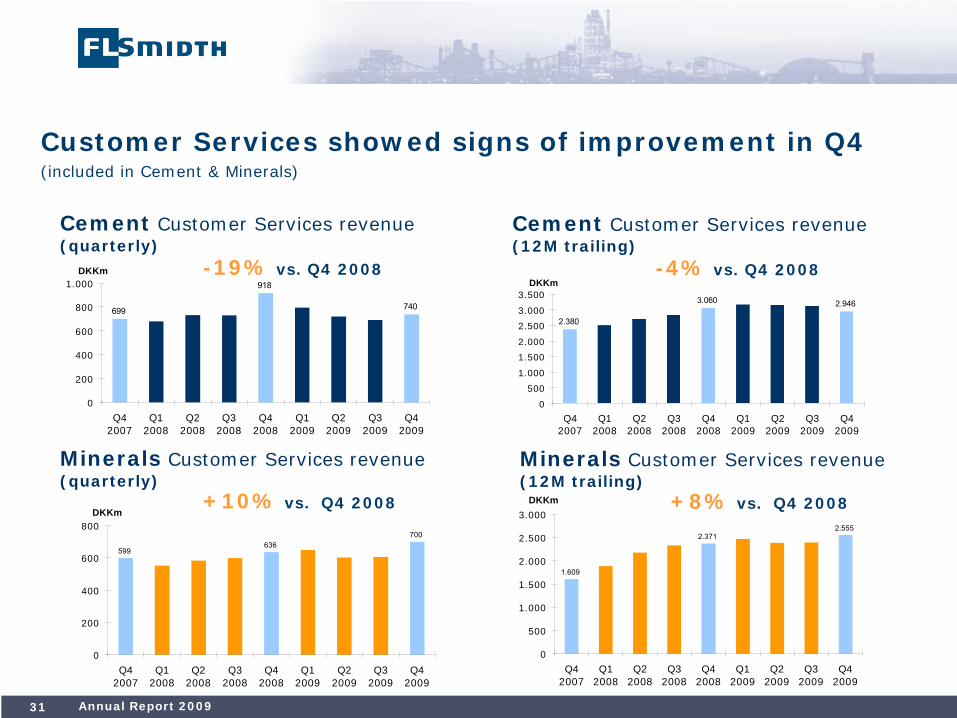

Customer Services showed signs of improvement in Q4(included in Cement & Minerals)

Cement Customer Services revenue (12M trailing)

-4% vs. Q4 2008

2.380

3.060 2.946

0

500

1.000

1.500

2.000

2.500

3.000

3.500

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

1.609

2.3712.555

0

500

1.000

1.500

2.000

2.500

3.000

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

Minerals Customer Services revenue (12M trailing)

+8% vs. Q4 2008

Cement Customer Services revenue (quarterly)

-19% vs. Q4 2008

699

918

740

0

200

400

600

800

1.000

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

599636

700

0

200

400

600

800

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

Minerals Customer Services revenue (quarterly)

+10% vs. Q4 2008

Operation & Maintenance contracts (O&M)

Dedicated work over the past 3 years to establish operation & maintenance of cement and minerals processing plants as a new business area

First Cement O&M contract in Egypt has been in operation for 1 year with very satisfying results

First Minerals Maintenance contract at Los Pelambres in Chile has just celebrated 10 year-anniversary

Negotiations ongoing with several other interested customers

Current contracts

Cement (O&M)

• Egypt (contracted in 2007)

• Libya (contracted in 2009)

Minerals (M)

• Los Pelambres, Chile (prolonged in 2008)

• Collahuasi, Chile (prolonged in 2008)

• Peñasquito, Mexico (contracted in 2008)

Annual Report 200933

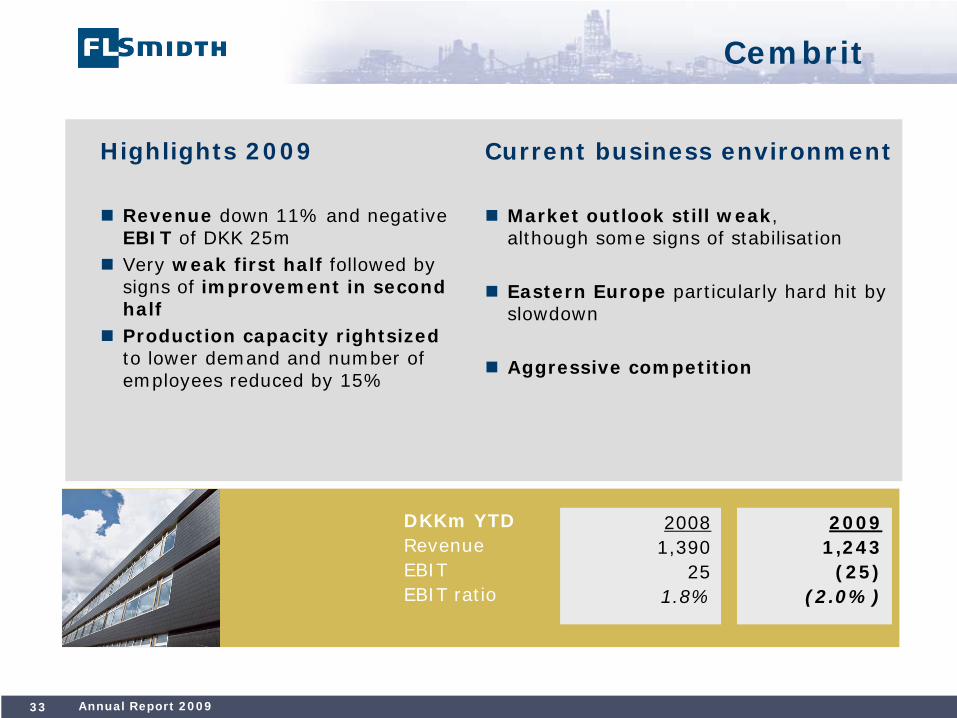

Highlights 2009

Revenue down 11% and negative EBIT of DKK 25mVery weak first half followed by signs of improvement in second halfProduction capacity rightsizedto lower demand and number of employees reduced by 15%

20091,243

(25)(2.0%)

20081,390

251.8%

DKKm YTDRevenueEBITEBIT ratio

Cembrit

Current business environment

Market outlook still weak, although some signs of stabilisation

Eastern Europe particularly hard hit by slowdown

Aggressive competition

Annual Report 200934

Turnover (DKKm) EBIT (DKKm)

Quarterly developments

DKKm

348297

329

0

100

200

300

400

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

DKKm

29

(20)

(30)(30)

(20)

(10)

0

10

20

30

40

50

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

Signs of improvement in second half of 2009Revenue up 11% in Q4 vs. last yearQ1 and Q4 are typically low season

Annual Report 200935

2010 2009■

New cement kiln capacity 50mty 45mty■

Revenue DKK 19-20bn DKK 23,134m■

EBIT-ratio 8-9% 9.8%■

Tax rate 30% 19%■

CFFI (excl. acquisitions) DKK -400m DKK -244m

■

Order intake in both Cement and Minerals is expected to increase in 2010 vs. 2009

Guidance 2010

Revenue EBIT■

Cement DKK 9-10bn ~9%■

Minerals DKK 8-9bn ~9%■

Cembrit DKK ~1.2bn ~2%

Segments

Group

Annual Report 200936

Unchanged long term growth and earnings prospects

Urbanisation and industrialisation in developing countries are expected to continue to generate increasing demand for cement and minerals in future.

In periods of high activity: Expected EBIT ratio: 10-12%

In periods of low activity: Expected EBIT ratio: 8-9%

Annual Report 200937

Concluding remarks

71% of revenue generated in emerging markets

Record high CFFO, EBIT ratio and profits in 2009

Asset light business model is working well

Increased optimism among customers

Strong financial position allows dividend paymentto be increased in 2010

New dividend policy: DKK 7 per share per year

A number of strategic initiatives are ongoing to further enhance the competitive and financial position of FLSmidth

Annual Report 200938

Questions