Embed Size (px)

Citation preview

Florida State University Libraries

Electronic Theses, Treatises and Dissertations The Graduate School

2005

An Investigation of Financial AssuranceMechanisms for Environmental LiabilitiesWendy D. Habegger

Follow this and additional works at the FSU Digital Library. For more information, please contact [email protected]

THE FLORIDA STATE UNIVERSITY

COLLEGE OF BUSINESS

AN INVESTIGATION OF FINANCIAL ASSURANCE MECHANISMS FOR ENVIRONMENTAL LIABILITIES

By

WENDY D. HABEGGER

A Dissertation submitted to the Department of Finance

in partial fulfillment of the requirements for the degree of

Doctor of Philosophy

Degree Awarded: Spring Semester, 2005

ii

The members of the Committee approve the Dissertation of Wendy D. Habegger defended on April 4, 2005.

_________________________ Pamela P. Peterson-Drake

Co-chair Directing Dissertation _________________________ Patrick F. Maroney Outside Committee Member _________________________ Gary A. Benesh Co-chair Directing Dissertation _________________________ Pamela K. Coats Committee Member

Approved: __________________________________ E. Joe Nosari, Interim Dean, College of Business The Office of Graduate Studies has verified and approved the above named committee members.

iii

I dedicate my dissertation to my savior Jesus Christ. I would not have completed the degree without His love, mercy, help, and direction. I also dedicate my dissertation to my parents, Karen and Kenneth Habegger. It is a privilege to have you as my parents and I could not have asked for better. Thank you for your unconditional love, encouragement, and financial support.

O sing unto the LORD a new song: sing unto the LORD, all the earth.

Sing unto the LORD, bless his name; shew forth his salvation from day to day. Declare his glory among the heathen, his wonders among all people.

For the LORD is great, and greatly to be praised: he is to be feared above all gods. For all the gods of the nations are idols: but the LORD made the heavens.

Honour and majesty are before him: strength and beauty are in his sanctuary. Give unto the LORD, O ye kindreds of the people, give unto the LORD glory and strength.

Give unto the LORD the glory due unto his name: bring an offering, and come into his courts. O worship the LORD in the beauty of holiness: fear before him, all the earth.

Say among the heathen that the LORD reigneth: the world also shall be established that it shall not be moved: he shall judge the people righteously.

Let the heavens rejoice, and let the earth be glad; let the sea roar, and the fullness thereof. Let the field be joyful, and all that is therein: then shall all the trees of the wood rejoice

Before the LORD: for he cometh, for he cometh to judge the earth: he shall judge the world with righteousness, and the people with his truth.

Psalm 96, KJV

iv

ACKNOWLEDGEMENTS

During the course of my studies, I had help along the way. I thank my committee members Dr. Gary Benesh, Dr. Pamela Coats, Dr. Patrick Maroney, and Dr. Pamela Peterson-Drake for their assistance and patience. I thank those Florida State University faculty members who were not on my committee but were supportive, Dr. Donald Nast and Dr. William Christiansen. I would like to thank Dr. Raid Amin from the University of West Florida, and Dr. Elton Scott, formerly from FSU for their guidance with my statistical interpretations. However, any errors of fact or interpretation are my responsibility. Finally, Dr. William Whitaker, thank you for the firm nudge to get my Ph.D. Linwood, thanks for the ear, the shoulder, the hugs, and the yeast rolls. You are next. Melita, thanks for being the best office mate. I appreciate all your prayers and support. You both are always in my heart and my prayers. To my most precious and faithful Boxer Maddie, you were there with me through it all. I would have been so lonely without your unconditional love and affection. Finally, to all the others, thank you for your prayers and continued support and interest in my life.

v

TABLE OF CONTENTS List of Tables ........................................................................................................Page vi List of Figures ........................................................................................................Page viii Abstract ..............................................................................................................Page ix 1. Introduction and Purpose ..........................................................................................Page 1 Environmental Liabilities and Financial Assurance...............................................Page 2 The Focus ........................................................................................................Page 5 The Contribution ...................................................................................................Page 6 The Findings ........................................................................................................Page 7 Outline and Summary of the Dissertation .............................................................Page 7 2. Review of the Literature .............................................................................................Page 8 What are Financial Assurance Requirements?.....................................................Page 8 What is the state of financial assurance today in the United States?...................Page 14 Reasonableness and Adequacy of Current Requirements...................................Page 23 Problems and Issues.............................................................................................Page 25 3. Analysis of Current Financial Assurance Guidelines.................................................Page 29 Review of the EPA’s Standards ............................................................................Page 29 Methods for Determining Company Health and Bankruptcy Prediction ...............Page 33 Data ........................................................................................................Page 37 Methodology ........................................................................................................Page 39 Results ........................................................................................................Page 41 Robustness Check ................................................................................................Page 49 Summary ........................................................................................................Page 51 4. Tests of financial assurance effectiveness: a sensitivity analysis .............................Page 53 Purpose for Sensitivity Analysis ............................................................................Page 53 Data ........................................................................................................Page 54 Methodology ........................................................................................................Page 54 Results ........................................................................................................Page 55 Summary ........................................................................................................Page 57 5. Conclusion ........................................................................................................Page 58 Summary of Findings ............................................................................................Page 58 Conclusions ........................................................................................................Page 60 Further Research ..................................................................................................Page 61 APPENDIX ........................................................................................................Page 105 A Major Environmental Catastrophes ................................................................Page 105 REFERENCES ........................................................................................................Page 108 BIOGRAPHICAL SKETCH ............................................................................................Page 116

vi

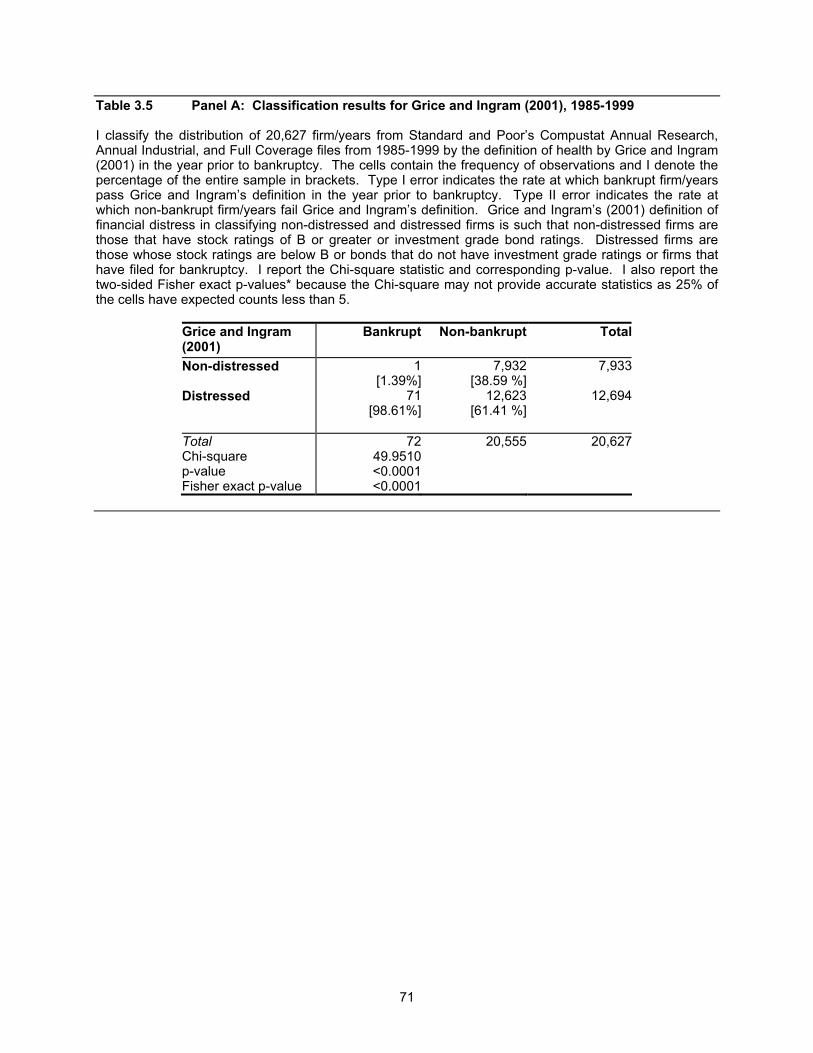

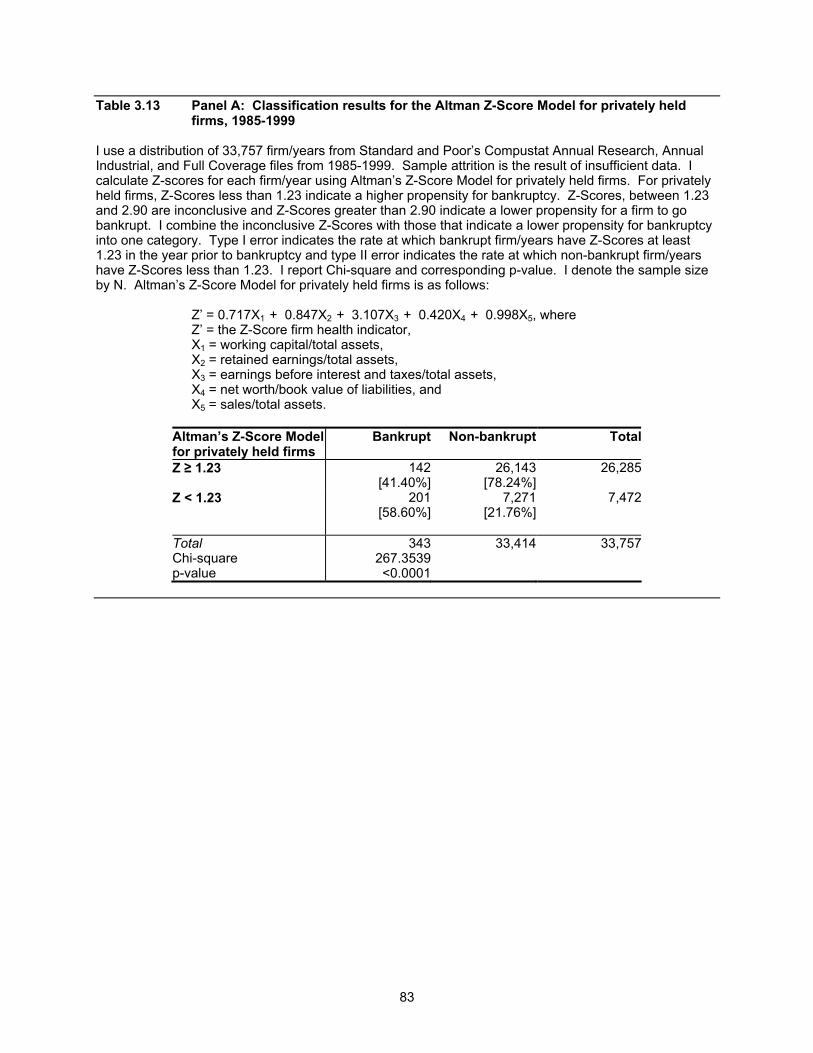

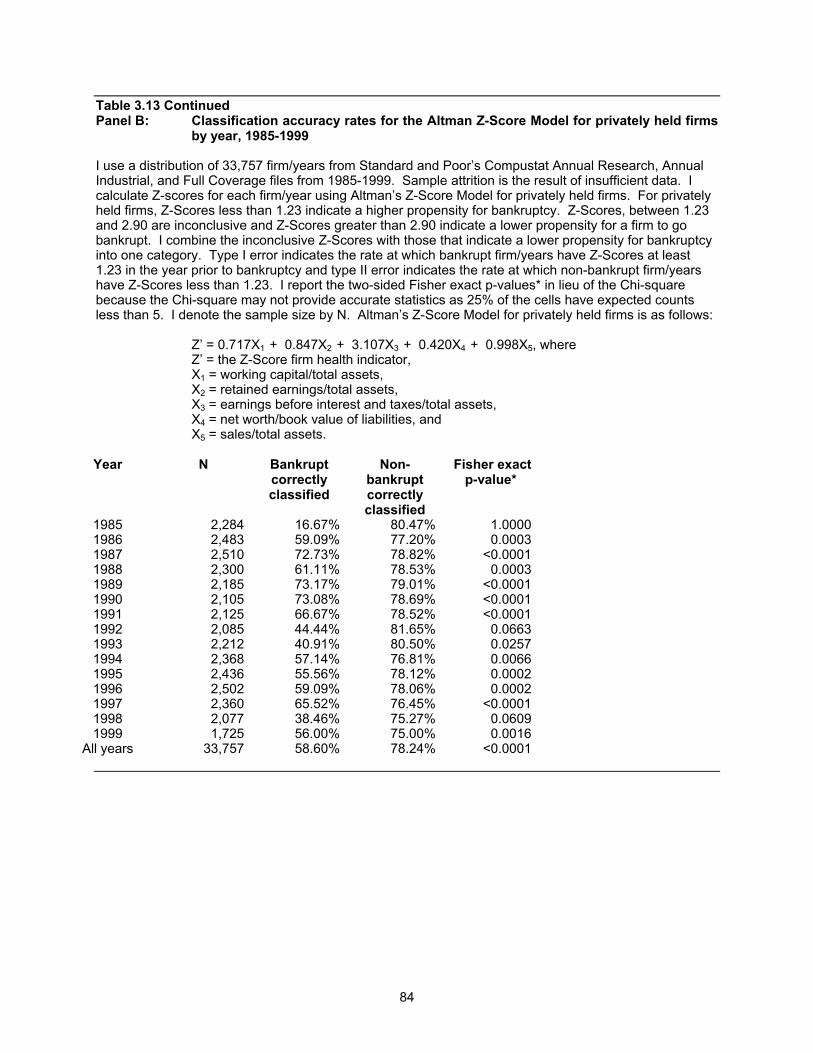

LIST OF TABLES Table 2.1: Time line of the major environmental laws ................................................... Page 62 Table 3.1: State versus federal regulations ................................................................... Page 63 Table 3.2: Comparison of methods and models ............................................................ Page 66 Table 3.3: Panel A: Classification results for the EPA’s financial tests, 1985-1999..................................................................................................... Page 67 Table 3.3: Panel B: Classification accuracy rates for the EPA’s financial tests by year, 1985-1999....................................................................................... Page 68 Table 3.4: Classification accuracy rates for the EPA’s financial tests by industry, 1985-1999..................................................................................................... Page 70 Table 3.5: Panel A: Classification results for Grice and Ingram (2001), 1985-1999 .... Page 72 Table 3.5: Panel B: Classification accuracy rates for Grice and Ingram (2001) by year, 1985-1999....................................................................................... Page 73 Table 3.6: Classification accuracy rates for Grice and Ingram (2001) by industry, 1985-1999...................................................................................................... Page 74 Table 3.7: Panel A: Classification results for bond ratings, 1985-1999........................ Page 75 Table 3.7: Panel B: Classification accuracy rates for bond ratings by year, 1985-1999 ....................................................................................................... Page 76 Table 3.8: Classification accuracy rates for bond ratings by industry, 1985-1999 ........ Page 77 Table 3.9: Panel A: Classification results auditor opinion, 1985-1999 ......................... Page 78 Table 3.9: Panel B: Classification accuracy rates for auditor opinion by year, 1985-1999....................................................................................................... Page 79 Table 3.10: Classification accuracy rates for auditor opinion by industry, 1985-1999.................................................................................................... Page 80 Table 3.11: Panel A: Classification results for the Altman Z-Score Model for publicly traded firms, 1985-1999 ................................................................ Page 81

vii

Table 3.11: Classification accuracy rates for the Altman Z-Score Model for publicly traded firms by year, 1985-1999.................................................... Page 82 Table 3.12: Classification accuracy rates for the Altman Z-Score Model for publicly traded firms by industry, 1985-1999.............................................. Page 83 Table 3.13: Panel A: Classification results for the Altman Z-Score Model for privately held firms, 1985-1999 .................................................................. Page 84 Table 3.13: Panel B: Classification accuracy rates for the Altman Z-Score Model for privately held firms by year, 1985-1999 ................................................ Page 85 Table 3.14: Classification accuracy rates for the Altman Z-Score Model for privately held firms by industry, 1985-1999........................................... Page 86 Table 3.15: Summary of classification rates for methods including logistic results, 1985-1999.................................................................................................... Page 88 Table 3.16: Summary of classification rates by method, 1985-1999............................. Page 89 Table 3.17: Summary of classification rates for each method by industry, 1985-1999..................................................................................................... Page 91 Table 3.18: Summary of overall classification rates by method, 1985-1999 ................. Page 92 Table 4.1: Distribution of error rates for the EPA’s financial tests using varying levels of PP&E for closure costs, 1985-1999................................... Page 93 Table 4.2: Distribution of classification rates for the EPA’s financial tests using varying levels of PP&E for closure costs by industry, 1985-1999 ...... Page 94 Table 4.3: Panel A Mean and median financial measures for firms subject to the EPA’s financial tests, 1985-1999............................................................ Page 101 Table 4.3: Panel B: Mean and median financial measures for firms subject to the EPA’s financial tests by industry, 1985-1999 ......................................... Page 102 Table A1: Summary of articles from trade and popular press ....................................... Page 107

viii

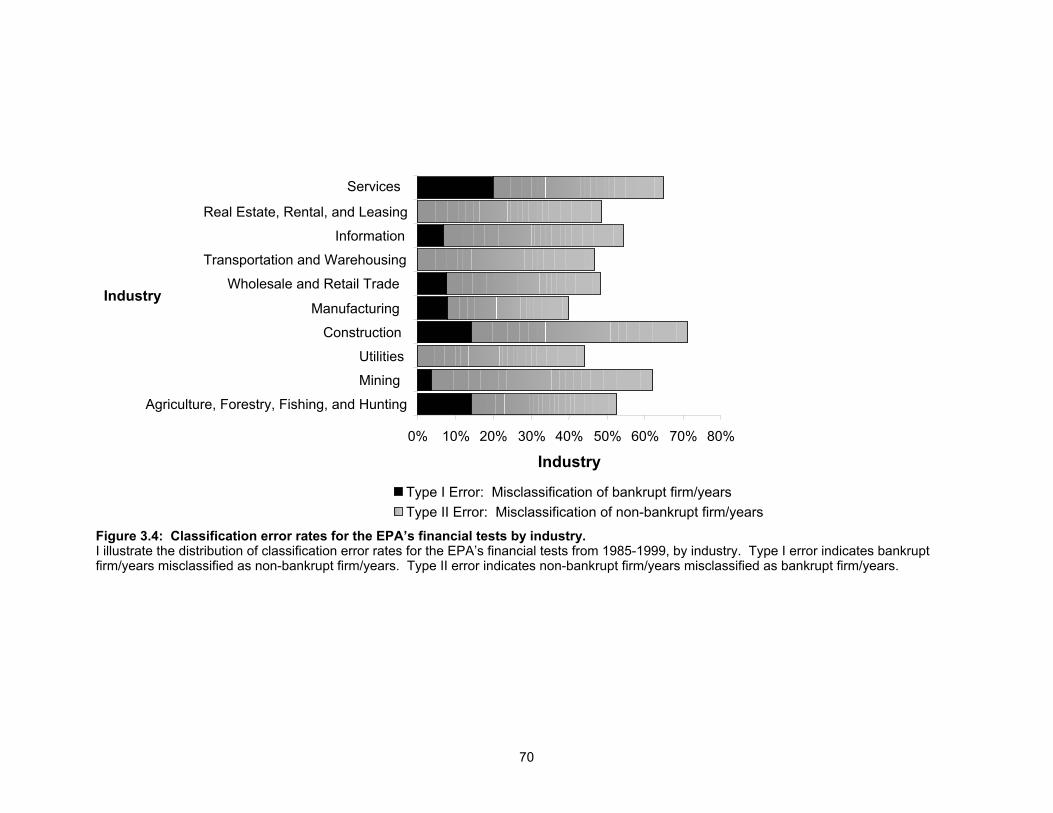

LIST OF FIGURES Figure 3.1: The proportion of bankrupt firm/years by year prior to bankruptcy for firms from 1985-1999 ............................................................................. Page 64 Figure 3.2: Proportion of bankrupt firm/years by industry for firms from 1985-1999...... Page 65 Figure 3.3: Classification error rates for the EPA's financial tests from 1985-1999 ....... Page 69 Figure 3.4: Classification error rates for the EPA's financial tests by industry ............... Page 71

ix

ABSTRACT

Firms are now required to disclose environmental activities and obligations. Prior, presumably

viable firms failed to include such obligations on financials. Firms in bankruptcy are often successful in

discharging their environmentally liabilities often at great cost to the public. The purpose of this

dissertation is to examine existing financial tests companies use to assure the Environmental Protection

Agency that they can satisfy their environmental obligations. Passing these tests allows firms to continue

engaging in potentially hazardous lines of business without actually allocating the necessary funds. I

examine the ability of the tests to detect firms that eventually go bankrupt. I compare the performance of

the tests to several methods used to predict bankruptcy such as the Altman Z-Score models, Grice and

Ingram’s definition of distress, bond ratings, and auditor opinion. I also test the sensitivity of the financial

tests to varying cost of closure.

1

CHAPTER 1 INTRODUCTION AND PURPOSE

Many firms may have undisclosed obligations for mitigation and reclamation of environmental

hazards. These mitigation and reclamation obligations may be short or long term and vary in amount.

For example, in the case of Safety-Kleen, the cost of mitigation for one landfill located in the state of

South Carolina is almost $1 billion, whereas its assets prior to the 2001 bankruptcy filing were

approximately $3 billion.1 Firms can have substantial liabilities that have the potential of becoming

catastrophic. Thus, there is incentive to manage the environmental liability to keep it from becoming an

environmental catastrophe. In Appendix A, I detail several of the major environmental catastrophes to

illustrate the importance of environmental liability mitigation and management.

Given that some of these catastrophic events are still fresh in the public’s mind, there is

increased concern about the risk the public bears for firms who fail to meet their environmental

obligations. In the popular media, such as The Wall Street Journal, The Associated Press, and state and

local newspapers, and trade publications, such as Platt’s Oilgram and Platt’s Coal Outlook, one finds

numerous articles about current environmental liability management issues and the associated costs

borne by the taxpayer [Table A1].

In light of the recent corporate scandals and bankruptcies of large firms (such as Enron,

WorldCom, Global Crossing, and Sunbeam) and coupled with the current economic downturn, the public

is increasingly concerned with firm transparency and viability. Aside from the issue of undisclosed off-

balance sheet liabilities, firms have successfully discharged environmentally related liabilities by filing for

bankruptcy protection. In this dissertation, I examine a variety of methods used to classify bankrupt firms.

Specifically, I compare the Environmental Protection Agency’s (EPA) financial tests ability to detect a

firm’s loss of viability with other methods available from the financial distress and bankruptcy prediction

literature.

Accurate assessment of firm viability is important to minimize both business and social costs.

Firms incorrectly assessed as lacking viability when in fact a firm is financially viable, these firms must

seek third party indemnification for their liabilities. Thus, the firm incurs additional business costs. Firms

lacking financial viability that are misclassified continue operations as usual and expose the public to the

potential social cost of funding the cleanup should the distressed firm default.

1 Report by Disclosure Incorporated.

2

When a firm defaults on its environmental obligation, the creditors and taxpayers ultimately bear

the burden of the cost of cleanup.2 In general, one assumes a firm will continue indefinitely and be viable

in the process by generating enough resources to maintain operations—the basic definition of “going

concern.” When an auditor issues a going concern modified opinion for a firm, this indicates that the

auditor believes the firm may struggle to remain a going concern in the next fiscal year. The definition of

“financial distress” may vary but it implies a firm continues to lack the ability to maintain going concern

status; however, the firm may still recover. Failing recovery, a firm may file for bankruptcy and reorganize

or it may liquidate.

To mitigate the costs of the environmental cleanup and hold the appropriate parties responsible,

regulators make additional requirements of firms that lose their going concern status. Regulators require

those firms to obtain an alternate form of assurance or risk losing their operating permit. However, at

times, regulators do not have much warning about a firm’s pending default.3

In this dissertation, I examine one of the existing financial mechanisms used to assure regulators

that companies will be able to satisfy their environmental obligations.4 For example, an entity that creates

and maintains a landfill must assure both state and federal regulators it has the financial means—either

through internal (that is financial wherewithal) or external (such as insurance) mechanisms—to cover the

costs of cleaning up and closing the landfill. In difficult economic environments, the need for financial

assurance is great. Yet external mechanisms are often expensive for entities to obtain. If companies

meet the criteria, they prefer to provide internal assurance.

1.1 Environmental Liabilities and Financial Assurance

1.1.1 What is financial assurance? Financial assurance is the demonstration of the ability to

fund costs associated with environmental liabilities. Such costs include closure obligations, post-closure

obligations, and corrective actions taken by an owner, operator, user, and anyone deemed a potentially

responsible party as defined and codified by The Code of Federal Regulations (CFR). Facilities are

required to prove they are financially viable to fund the following activities:

2 In reference to Safety-Kleen in South Carolina, the estimated cost is approximately $24.61 per person in

South Carolina for the Safety-Kleen issue alone. This figure is a crude estimate based on the $1 billion cost for a future repair at the landfill divided by the number of residents in the state (4,063,011) as reported by the U.S. Census Bureau at the time Safety-Kleen filed for bankruptcy protection in 2001. Although this estimate does not appear to be costly, this estimate is only for one repair at one site. It does not include estimates for other repairs, other sites, other types of hazards, or other hazards and sites owned by other companies. One can easily calculate the potential burden on the taxpayer if South Carolina has more than one site of concern. Estimating the total possible environmental liability and the potential burden for the taxpayers of each state is beyond the scope of this dissertation. 3 As reported in The Tampa Tribune on March 17, 2001, the Florida Department of Environmental

Protection took emergency control of the phosphate-mining site and phosphogypsum stacks abandoned by Mulberry Phosphates. A copy of the article is at http://www.fluoridealert.org/phosphate-industry.htm. 4 These mechanisms, directly or modified, are also used for state and local governments, as well as other

municipalities. The focus of this dissertation is on companies, though much of this research is applicable to other entities. Throughout the paper, I imply the terms “company,” “state and local governments,” and “municipalities” in the terms “entity” and “owner or operator.”

3

1) maintain the site during the life of the business and comply with the EPA and related state

regulatory agency guidelines,

2) properly close the site when the business is complete,

3) restore the site to a reasonable condition as dictated by the EPA and state authorities, and

4) maintain the site after closure, and cover any costs arising from unexpected contamination,

injuries, or problems before, during, and after closure.

If a firm, new or existing, cannot provide internal financial assurance then the firm must seek

alternative external financial assurance. Inability to obtain financial assurance will leave the firm without

the necessary permits and licenses needed to operate.

1.1.2 Why is financial assurance important? The purpose of financial assurance is to

internalize all environmental liability costs to the potentially responsible party. By requiring the

responsible party to take financial responsibility for all liabilities, this mitigates the social cost borne by

taxpayers. Enforcement may be in the form of the tort laws of strict liability and joint and several liability.

When discussing the issue of liability, it is necessary to distinguish negligence from strict liability

and joint and several liability from joint liability.5 Under negligence, proof is required that the responsible

party failed to use adequate precaution and any injury sustained was the direct result of the pollution or

the unsafe work environment caused directly cause by the lack of precaution. Strict liability is

independent of negligence; therefore, the responsible party for the hazardous activity may be liable for

the potential hazard, regardless if the responsible party used adequate precaution. Negligence in

environmental cases is often difficult to prove. Therefore, in environmental cases, the state regulatory

agencies prefer the use of strict liability. It removes the burden of proving negligence, and potential

environmental hazards can be considered “unusually dangerous activities” [Cross and Miller (2001) page

277].

Joint and several liability usually applies to torts, and it means either one or all of the involved

potentially responsible parties may be responsible for the entire liability; no one is safe from the

responsibility. In a sense, it is a situation where the regulators attempt to get what they can from

whomever. If they did not get it all in the first round, then they may find other potentially responsible

parties and attempt to recover it from them as well. For joint liability, which is usually applicable in

contract situations, it may be an all or nothing situation. Thus, if it happens to one responsible party, then

it happens to all. If the state regulatory agency holds one responsible party accountable, then the agency

must hold all responsible parties accountable. Likewise, if the state regulatory agency pardons one party,

then they pardon all. Potentially responsible parties tend to use joint liability against each other for

sharing the liability and for a fairer distribution of the obligation. The state regulatory agencies tend to

5 Further discussion on types of liability can be found in Cross and Miller (2001), Chapters 12 and 25.

4

focus on the use of strict liability and joint and several liability when instigating litigation and cost recovery

from responsible parties.

To accomplish the goal of internalizing the liability, the EPA requires firms involved in potentially

hazardous lines of business to apply for permits and/or licenses. These permits give the firm permission

to perform the necessary activities related to the line of business with the potential hazard. The permits

may also predefine acceptable limits of pollution. To receive these permits, firms must meet all

guidelines required by the governing regulatory agencies. Specifically, they must show proof of financial

assurance.6 Demonstration of financial assurance contractually binds the permitee to fulfill the obligation

for which it is providing assurance.

Several financial assurance mechanisms exist. Each potential hazard can require the use of a

single mechanism or, in some cases, a combination of mechanisms. Mechanisms may include

insurance, trust funds, corporate parent guarantees, or financial tests. Many of these mechanisms

subject the responsible party of the facility to increased monitoring by state and federal regulators and,

often, an additional third-party financial provider. Misuse of assurance mechanisms can lead to the

taxpayers bearing the costs.7 In other words, a distributional concern exists as the burden shifts to the

U.S. taxpayers. The most controversial of these mechanisms, the financial test, is the focus of

investigation in this dissertation. Financial tests are the least expensive mechanism because they only

require the firm to provide financial statements attesting to the firm’s viability should it face an

environmental claim. It is a promise that binds the firm to the obligation; however, it provides no tangible

guarantee that funds will be available when needed.

Firms that are not financially viable can find third-party assurance but at a higher cost, which the

firm may not be able to afford [Boyd (2001a)]. A firm claiming it cannot afford the mechanism may be

financially beyond its means. It becomes an environmental concern. Firms may attempt to negotiate for

a temporary relaxation in the requirements. However, these relaxed requirements do not always comply

with federal law.8 In some cases, firms that negotiated a temporary reprieve filed for bankruptcy shortly

thereafter.9

6 In many cases, firms must answer to more than one regulatory agency. The many environmental acts

have established regulatory agencies relevant to the specific issue they address, while the EPA monitors all environmental hazards. For example, licensees of nuclear power reactors are also responsible to the Nuclear Regulatory Commission (NRC). The Underground Injection Control (UIC) program director for each state monitors underground injection wells for the EPA. The Office of Surface Mining Reclamation and Enforcement (OSMRE) monitors mining operations. The United States Coast Guard regulates water transportation of hazardous materials. For a review of the major regulatory acts and the statutes governing compliance and enforcement through criminal prosecution, see Lachenmayr, Lockner, Olson, and Wolpert (1998). 7 At a Florida Department of Environmental Protection (DEP) mining reclamation meeting in September

2002, the attorney for the DEP, Mr. John Alden, explained some common misuses of financial assurance mechanisms. Misuses can include approval by a representative of the company who is not an officer and, therefore, does not legally bind the company; providing fraudulent financial statements; and attempting to use one mechanism to cover sites not specified by the mechanism. 8As reported in The Greenwire on December 18, 2002, Dow Chemical Company and Michigan’s

Department of Environmental Quality came to an agreement to reduce Dow’s financial assurance costs and clean-up liability for dioxin contamination in the soil by allowing Dow to increase the amount they

5

1.2 The Focus

In this dissertation, I examine the ability of the financial tests to classify a firm according to its

financial viability. Specifically, I focus on analyzing the financial fundamentals that make up these tests.

Among the questions I address are the following:

• Are these financial tests effective in assuring that financial resources exist to fund the

cleanup of environmental accidents?10

That is, can these tests detect when a firm will go

bankrupt?

• Do the financial tests foster cost internalization, or do they hinder those responsible from

taking responsibility? That is, are these tests effective in guaranteeing the necessary

funds are available for environmental cleanups?

Whereas other studies focus on the environmental, economic, legal, and ethical effects

concerning environmental contamination, in this dissertation I investigate the financial precursor to these

issues. Specifically, I address the viability of firms to fulfill their legal financial obligation for the

maintenance, closure, and any corrective actions directly related to site operations. Other studies are

reactive studies because they are often ex-post analysis of the liability realization. They examine the

after effects on the environment and its inhabitants and the economic welfare and social costs [Riering

1992, Boyd 1993]. Other studies focus on policy-making, risk sharing, and the legal debate between

bankruptcy law and environmental law [Van ‘T Veld 1997, McGraw 1998].11

Recently, environmental law,

disclosure, and the contractual commitment of the permitee are receiving increased attention.12

This

study is a reactive study in the sense that my interest in this topic was peaked after reading about the

many firms attempting to discharge their environmental liabilities. I realized that if these firms are

successful in their bid to dismiss their obligations, then I as a taxpayer am ultimately bearing the cost. I

focus on the EPA’s financial tests applicability for social cost mitigation.

dump into the soil at no added cost to Dow. This reduction of liability means the reduction of standards. This reduction in the state standard violates the federal guidelines, so the City of Midland, Michigan, and several environmental groups have filed a lawsuit to stop the approval of the proposal. 9 Mulberry Phosphates filed for bankruptcy in 2001 and abandoned the mining site and the

phosphogypsum stacks for the State of Florida to clean up at the cost of $125 million (as of April 3, 2003). 10

Deterrence is important in some types of environmental hazards. For example, if a phosphate processing company files for bankruptcy and is unable to fund the cost of pumping the acidic water for its phosphogypsum stacks, a significant probability exists that there will be a hazardous spill into the state’s water supply. In this case, funds are necessary to deter an environmental hazard. 11

The difficulty here lays in the fact the courts must interpret congressional intent. No consensus exists among the courts. For a review of cases, see Hill (1998), Spracker and Barnette (1994), Bloom (1995), and C. Barth (1994). 12

As reported in The Ohio Law Letter in October 2002, the SEC petitioned to require full disclosure of environmental liabilities in corporate filings. This petition came in light of several major bankrupt corporations with serious environmental liabilities and on the heels of the 1998 EPA report that found 74 percent of firms fail to report environmental liability litigation in excess of $100,000. Not reporting such liabilities violates the SEC regulation S-K and can warrant criminal charges.

6

1.3 The Contribution

The importance of this dissertation is in its contribution to the overall well being of the

environment and society. In light of the anecdotal evidence of firms attempting to avoid their

environmental obligation and the public seeking improved disclosure requirements from the Securities

and Exchange Commission (SEC) and the Financial Accounting Standards Board (FASB), it is logical

that the next step is to look at the adequacy of the EPA’s financial tests.13

The EPA’s financial tests use

well-known financial analysis techniques and methods. When applied, the financial tests should be able

to provide regulators with guidance about a firm’s viability. Specifically, these tests should let regulators

know when a firm’s viability may be waning. Early and more accurate detection by the EPA creates

proactive enforcement of compliance, mitigates costs, and lessens the financial burden on the taxpayer.

This dissertation ties together the areas of finance, accounting, insurance, government

regulation, the environment, financial distress, and bankruptcy under the umbrella of risk management.

This topic is timely and significant, as it affects everyone. It is a serious study of the real-world

application of risk management techniques and whether these techniques accomplish their designed

purpose. Failure of risk management techniques in this arena can lead to environmental catastrophes

that no amount of money can restore. Diligent monitoring and revision are not just necessary—they are

vital to our survival.

Because these financial tests dictate whether firms may continue to engage in potentially

hazardous lines of business, there are four potential outcomes. The first two are what we hope for; non-

bankrupt firms receive permits and continue operating while firms that are quickly approaching

bankruptcy must find an alternative means of financial assurance. The other two potential outcomes may

result in additional unexpected costs. Firms quickly approaching bankruptcy that continue operations,

without providing an alternate form of assurance create potential social costs on the environment and

taxpayers if they default on their obligations. Non-bankrupt firms that must find alternate financial

assurance incur additional business costs that may be unnecessary.

These financial tests are comprised of financial ratios. We know from prior research that ratios

can be consistent indicators of distress [Beaver (1966, 1968), Altman (1968, 1977, 1993), Ohlson (1980),

Scott (1981), and Grice and Ingram (2001)]. I compare the classification accuracy of the EPA’s financial

tests and other commonly used bankruptcy prediction methods.14

My reason for doing so is to search for

alternative methods that may have better classification accuracy than the EPA’s financial tests. If such

methods exist, then perhaps the EPA might consider selecting one of these for future use. I also conduct

sensitivity analyses for differing levels of closure costs that represent the environmental liabilities. My

purpose for doing so is to determine how sensitive the tests are to varying closure costs.

13

The disclosure requirements are the Securities and Exchange Commission (SEC) Regulation S-K items 101, 103, and 303. The new accounting change is the implementation of Financial Accounting Board Standard (FASB) Statement Number 143, effective June 2002. 14

I test the null hypothesis that there is no difference in the classification of bankruptcy between bankrupt and non-bankrupt firms. Type I error indicates a bankrupt firm passes the financial tests. Type II error indicates a non-bankrupt firm fails the financial tests.

7

1.4 The Findings

I find the EPA’s financial tests are able to classify over 90 percent of the bankrupt observations

and over 60 percent of the non-bankrupt observations correctly. Annually, the results remain consistent.

The tests do classify the firms more accurately in some industries than in others. When compared to

other methods, the classification ability of the EPA’s financial tests is most comparable and consistent

with the Altman’s Z-Score methods.

I find the financial tests are somewhat sensitive to varying closure costs. As closure costs

increase, there is an insignificant decrease in type I error [the number of bankrupt observations that fail

the financial tests]. As expected, misclassification of non-bankrupt observations increases as closure

costs increase.

1.5 Outline and Summary

In Chapter 2, I describe financial assurance tests for the major environmental liabilities and

provide a review of the environmental liability literature. The major environmental liabilities are as follows:

nuclear power reactors; above and below surface mining; injection wells; municipal solid waste landfill

facilities (MSWLF) and hazardous waste treatment, storage, and disposal facilities (TSDF); underground

storage tanks (UST); and transportation of hazardous materials in water bound vessels. I explain the

types of financial assurance available to firms with environmental liabilities and discuss problems and

issues.

In Chapter 3, I provide a review of the distress and bankruptcy prediction literature and analyze

the classification accuracy of the EPA’s financial tests. I also compare the EPA’s classification rates with

various methods for detecting bankruptcy: Grice and Ingram’s (2001) definition of financial distress, bond

ratings, and auditor opinion, Altman’s Z-Scores for publicly traded and privately held firms. In Chapter 4, I

test the sensitivity of the financial tests to detecting bankruptcy with varying levels of closure costs.

Finally, in Chapter 5, I summarize my results and offer avenues for future research.

8

CHAPTER 2 REVIEW OF THE LITERATURE

2.1 What Are the Financial Assurance Requirements?

2.1.1 Development of guidelines. Financial assurance guidelines have evolved over the past

30 years from the major environmental laws and their amendments. These laws are the reaction to

negative events caused by a lack of protection for the environment and its inhabitants. I devote this

section to the introduction of some major laws and briefly explain their purpose.15

I provide a list of some

of the environmental laws over the past 65 years in Table 2.1. Many of the earlier laws listed in Table 2.1

have been amended and are subsumed in the present laws.

Congress and state legislatures establish environmental requirements by passing laws that limit

negative human impact on the environment. These statutes are included in the federal or state code of

laws respective to the legislature that passed the law. State statutes only apply to the state, whereas

federal statutes apply to all states. Regulatory entities generate rules to implement the statutes. Local

governments also pass statutes, called ordinances, rules, or orders, to govern issues not addressed by

federal or state laws. The statutes are applicable in the region governed by the local government.

The federal government relies on the state and local governments and regulatory agencies to

implement and to enforce the federal statutes within their specific states and regions. Often, the states

regulate the general law and allow more localized governmental units to interpret implementation and

execution of the law, as long as it meets the state and federal standards. For example, the federal

government regulates landfills, and the state is responsible for the management of the landfills and

compliance with using the landfills. The local government in the area in which the landfill resides may

determine the method of waste pick up and disposal.

The National Environmental Policy Act of 1969 (NEPA) established the Council on Environmental

Quality that reports annually to Congress on the state of all environmental affairs in the United States.16

15

For an extensive survey on the evolution of environmental policy from an economics perspective, please see Cropper and Oates (1992). 16

42 U.S.C. § 4321-4347, and may be found at http://ceq.eh.doe.gov/nepa/regs/nepa/nepaeqia.htm.

9

The Council investigates all aspects of quality management for the environment, both current and

forward-looking trends. In other words, the Council is the keeper of the environment, monitoring the

effects of the current and future applications of laws and compliance. It provides guidelines for the

federal government’s role and responsibility for the environment. An all encompassing law with its

amendments, the Resource Conservation and Recovery Act of 1976 (RCRA) gives the EPA complete

control over all things related to hazardous waste, barring historical and abandoned waste sites. In those

cases, Comprehensive Environmental Response, Compensation, and Liability Act of 1980 (CERCLA)

covers those sites.17

RCRA provides objectives for the rigorous treatment of hazardous waste throughout

the waste’s existence.

Congress expanded federal authority for the EPA to respond to toxic releases with the advent of

CERCLA (or Superfund) and its amendments. A key provision of CERCLA is the improvement of the

National Contingency Plan. This plan outlines the procedures for such releases. It also establishes the

National Priorities List (NPL) that contains contaminated sites that are of concern, and for which the EPA

collects taxes from the offending industries to fund the cleanup of necessary sites.18

Congress amended CERCLA with the Superfund Amendments and Reauthorization Act of 1986

(SARA), making several changes and additions to the program. In particular, SARA supports the

investigation and the implementation of new techniques for the management and maintenance of

hazardous waste and requires continuity between state and federal regulations. One of the most

important provisions is the updating of the Hazard Ranking System (HRS). The HRS is a ranking system

that provides regulators with a list of criteria used to calculate a score. This score tells the regulators the

potential threat the particular site is to the environment. SARA provides improvements to the HRS for a

more appropriate score with respect to the level of waste sites contain.19

Other laws regulate specific types of potential damage to the environment. For example,

o air emissions from all mobile sources are regulated according to the Clean Air Act of 1990

(CAA),20

o federal control of all things pesticide related is regulated by the Federal Insecticide, Fungicide

and Rodenticide Act of 1972 (FIFRA), 21

o pesticide regulation is expanded with the Food Quality Protection Act of 1996 (FQPA) and

the FIFRA and Federal Food, Drug, and Cosmetic Act (FFDCA),22

o drinking water quality is regulated by the Safe Drinking Water Act of 1974 (SDWA),23

17

42 U.S.C. § 321, and may be found at http://www.epa.gov/region5/defs/html/rcra.htm and http://www4.law.cornell.edu/uscode/42/ch82.html. 18

42 U.S.C. § 9601, and may be found at http://www.epa.gov/superfund/action/law/cercla.htm and http://www4.law.cornell.edu/uscode/42/ch103.html. 19

42 U.S.C. § 9601, and may be found at http://www.epa.gov/superfund/action/law/sara.htm and http://www4.law.cornell.edu/uscode/42/ch103.html. 20

42 U.S.C. § 7401, and may be found at http://www.epa.gov/region5/defs/html/caa.htm and http://www.epa.gov/oar/caa/contents.html. 21

7 U.S.C. § 135, and may be found at http://www.epa.gov/region5/defs/html/fifra.htm and http://www4.law.cornell.edu/uscode/7/ch6.html.

10

o all manner of chemicals are regulated under the Toxic Substances Control Act of 1976

(TSCA),24

and

o the Clean Water Act of 1977 regulates pollutants discharged into the United States waters

(CWA), which amends the Federal Water Pollution Control Act Amendments of 1972.25

These laws provide guidance to the EPA and state regulatory agencies on business compliance

and regulation. Any business activity that may produce an environmental hazard requires some form of

financial assurance. The hazards include the licensing and decommissioning of nuclear power plants;

surface and underground mining and reclamation; plugging and abandoning injection wells; waste

management landfill facilities; hazardous waste treatment, storage, and disposal facilities; and

underground storage tanks for hazardous materials.26

I discuss these types of hazards in the next

sections. For the analyses in this dissertation, I examine the hazards as a whole, meaning I do not treat

hazards uniquely.

2.1.2 Federal and state guidelines. Before discussing the guidelines for the hazards, I

address preemption. The states have the main responsibility to monitor and to enforce compliance,

provided they have the capability to do so. In cases where the state lacks the necessary laws, personnel,

equipment, or overall ability to implement the federal laws—for example, if the state does not have an

EPA office or Regional Administrator or a state regulatory agency—then federal law is the precedent. If

the state has the state-level framework and the federal and state laws are concurrent, then federal law

preempts state law [Cross and Miller (2000), Copeland (1997)].

Although states have some leeway from the federal government, the federal government may

intervene in the activities within a state at any time it sees fit if a federal law exists. However, if a federal

law does not exist but a state law does, then state law may preempt federal law. The degree of federal

government intervention depends upon the varying level of preemption [Meltz (1999)]. Preemption may

be general, in which the federal government may intervene at will, or it may be highly specific in that the

state may or may not be given certain variances or waivers for certain types of environmental activities.

The ability to receive the waiver depends upon a multitude of factors, such as the type of hazard, the

accessibility to treatment facilities, and the financial viability of the firm responsible for the hazard.

RCRA Section 3009 ensures states that have implemented federal programs may impose stricter

regulations than the federal programs require. If the federal program tightens the regulations, the states

must likewise tighten their regulations. In other words, the state may be more rigorous than federal

requirements, but it cannot be more lenient. Thus, the states may require additional or more stringent

financial assurance requirements. In states that do not have approved programs implemented, the EPA

22

Public Law 104-170, August 3, 1996, and may be found at http://www.epa.gov/opppsps1/fqpa/ and http://www4.law.cornell.edu/uscode/21/ch9.html. 23

42 U.S.C. § 300f, and may be found at http://www.epa.gov/region5/defs/html/sdwa.htm and http://www4.law.cornell.edu/uscode/42/300f.html. 24

15 U.S.C. § 2601, and may be found at http://www.epa.gov/region5/defs/html/tsca.htm and http://www4.law.cornell.edu/uscode/15/ch53.html. 25

33 U.S.C. § 1251, and may be found at http://www.epa.gov/region5/water/cwa.htm and http://www4.law.cornell.edu/uscode/33/ch26.html.

11

Regional Director evaluates the equivalency of the state-required mechanism to the federal-required

mechanism. The next section describes the guidelines for firms that may engage in the following types of

business activities that pose potential environmental hazards:

(a) nuclear power reactors,

(b) above and below surface mining,

(c) municipal solid waste landfill facilities (MSWLF) and hazardous waste treatment, storage,

and disposal facilities (TSDF),

(d) underground storage tanks (UST), and

(e) the transportation of hazardous waste across bodies of water.

2.1.2.1 Nuclear power reactors. The regulatory agency for the licensing and decommissioning

of nuclear power reactors is the Nuclear Regulatory Commission (NRC).27

The NRC defines two types of

nuclear reactors: power and non-power. Power nuclear reactors are commercial reactors used to

generate electricity. Non-power reactors are those used in research, testing, and training by non-profit

organizations. These types of entities are beyond the scope of this dissertation, as I focus on those firms

that are for-profit institutions. The NRC evaluates the financial qualifications of an applicant for a nuclear

power reactor license at various stages of business and for several reasons. Evaluations of applicants’

financials occur for the following:

• initial licensing,

• prior to being sold, acquired, or restructured because the license to operate transfers to

the buyer,

• license renewal for nuclear power reactors that are not electric utilities, and

• if the NRC suspects the firm is no longer a going concern.

Financial qualifications refer to an applicant’s ability to meet the necessary requirements as

dictated by the NRC and the EPA to acquire the operating license and comply with environmental

regulations while in operation. Financial assurance is different from financial qualification in that financial

assurance refers to the applicant’s ability to cover costs associated with hazard-related incidents and

accidents during operation and costs related to the decommissioning of the plant. Both are related; if an

applicant shows proof of financial assurance, then the financial qualifications follow. However, satisfying

the financial qualifications does not imply financial assurance is satisfied, as financial assurance is

accident related and financial qualifications relate to the day-to-day operations.

Nuclear power reactors that are electric utilities are not required to resubmit financial information

upon license renewal. The NRC argues that because electric utilities are highly regulated, they must

already be financially viable to operate the plant safely. Therefore, electric power reactors are not

required to submit proof of financial qualifications upon renewing the operating license. Nuclear power

reactors that are non-electric utilities and non-power reactors must always submit financial information.

Owners and operators of non-power reactors are typically private, state, federally operated nonprofit

26

I use the terms owners, operators, applicants, and licensees interchangeably. 27

10 CFR Parts 30 and 50.

12

educational institutions, or research institutions. The financial information for these types of institutions is

harder to obtain. Therefore, increased and regular scrutiny of their financials is necessary.

The NRC likewise monitors current license holders through the trade press and popular media. If

negative information exists about a license holder, the NRC reserves the right to investigate the firm’s

financials.28

The NRC provides flexible, case-by-case analysis of the financial assurance requirements

for each applicant and may provide some variances or waivers to these requirements. The mechanisms

available are specific to the type of nuclear entity: qualified nuclear entities, unqualified nuclear entities,

and all others. Qualified and unqualified nuclear entities may use any of the mechanisms discussed in

this dissertation. Those in the “others” category are limited, as they may not be as financially viable or

transparent.

2.1.2.2 Above and below surface mining. The Office of Surface Mining Reclamation and

Enforcement (OSMRE) is the regulating authority for surface and underground mining operations and

reclamation.29

To receive a permit to mine, companies must conduct mining operations according to the

permit and provide the required financial assurance for any incidents that occur during operation, closure,

and reclamation. A dilemma with financial assurance mechanisms is the lack of a long-term mechanism.

Often, events occur that are not included and accounted for at the beginning or during the course of

operations. When reclamation begins, unexpected environmental needs may arise for which the firm

lacks the financial assurance, and the firm may not have deep pockets to cover the costs from another

funding source.

As mentioned in the anecdotal evidence in Table A.1., Appendix A, one such unforeseen

environmental need with mining is the need for continual treatment of acid or toxic mine drainage (AMD).

AMD is a toxic byproduct of the mining activity. Currently, mining companies have been using

performance bonds (surety bonds, self-bonds, cash bonds, negotiable federal or state bonds, and

negotiable certificates of deposit) to cover the funds needed to complete the reclamation plan, without

considering the need for AMD treatment. When re-estimating financial assurance, often the affected

firms forfeit the bonds in lieu of reestablishing new bonds for higher amounts that the firm cannot afford.

Forfeiting bonds increases regulator scrutiny as the next step after bond forfeiture is often filing for

bankruptcy protection against all creditors—and especially the environmental liability.

2.1.2.3 Injection wells. The Director or Regional Administrator for the EPA office within the

specified state or region is responsible for regulating injection wells. The EPA classifies injection wells

based on the type of material injected into the ground and the depth of the injection. The office regulates

the investigation of actual and potential aquifers, injection procedures, and monitoring of the injected

waste.

Owners and operators of injection wells are limited to using only procedures specified by the EPA

for the injection process and must frequently monitor the wells for contamination. Prior to beginning the

process, they must demonstrate financial assurance for any possible contamination that may result

28

Federal Register, Volume 67, Number 107, June 4, 2002, p. 38427-38431.

13

during operations and for the eventual plugging and abandonment of the well. In cases where the

Underground Injection Control (UIC) program is state administered, the state may have more regulations

and mechanisms than the EPA requires. These state regulations may be more stringent as long as they

satisfy the EPA guidelines.

2.1.2.4 Municipal solid waste landfill facilities (MSWLF), hazardous waste treatment,

storage, and disposal facilities (TSDF). A state’s division of solid and hazardous waste management,

under RCRA, regulates waste disposal landfills and facilities. The term “landfill” applies to all facilities

that participate in land disposal activities. Subtitle C classification is for those that generate hazardous

waste in large quantities, such as corporations, schools, and hospitals. Subtitle D classification is for

those that generate a small quantity of hazardous waste, such as households and small businesses.30

Facilities may acquire multiple types of permits to operate. These permits, classified as standard

or special, depend upon the purpose of the facility and the degree of permission needed to perform an

activity.31

For example, facilities that store the hazardous waste may only receive a standard permit,

whereas a facility that burns waste would receive a special permit because the facility must maintain the

proper equipment to conduct such activities. The facility must provide for safety precautions related to

the changing chemical composition of the waste during burning and provide for proper disposal after the

activity is complete.

2.1.2.5 Underground storage tanks. The EPA Office of Underground Storage Tanks (OUST)

is responsible for regulating all manner of underground storage tanks, petroleum-based products, and

any hazardous material such as polychlorinated biphenyls (PCBs).32

The term “underground storage

tank” means either a lone tank or a system of tanks and associated components that are underground.

Some types of tanks are exempt from federal regulations, although some state and local

governments may include these tanks in their regulations, as the states may have more stringent

regulations than federally required. Currently, 29 states and the District of Columbia and Puerto Rico are

implementing the approved UST programs. Some tanks may only be required to meet federal regulations

in the event they become involved in a hazardous cleanup process. The UST programs provide clear

guidelines for owners as to the proper construction of the tank, the appropriate application of the tank,

maintenance, and disposal upon completion of use of the tank. The basis for financial assurance

standards for underground storage tanks is the number of tanks in the various stages of the life of the

tank.

29

30 C.F.R. Parts 700 – 800 and Federal Register, Volume 67, Number 96, May 17, 2002, p. 35070-35073. 30

ICF Consulting Group’s report entitled Analysis of Subtitle C and D Financial Tests with subsections disseminated from July 14, 1995, to December 9, 1997. 31

U.S. Department of Energy, Office of Environmental Policy and Assistance, RCRA Information Brief, DOE/EH-413/9715, September 1997, p. 1-4. 32

40 CFR 280, and may be found at http://www.access.gpo.gov/nara/cfr/cfrhtml_00/Title_40/40cfr280_00.html.

14

2.1.2.6 Transportation of hazardous materials in water bound vessels. The EPA regulates

domestic marine facilities, whereas the U.S. Coast Guard regulates domestic water bound vessels.33

The

International Convention for the Prevention of Pollution from Ships (MARPOL) Convention and

international treaties regulate foreign water bound vessels.34

According to regulations, the water

transportation industry must exercise extreme caution with the maintenance of all vessels, the fueling of

vessels, and the types of leaks or discharges from the vessels. Operators and owners of water-related

facilities and water bound vessels must apply for general permits as to the nature of their existence and

other permits pertaining to the cargo, purpose, and destination.

2.2 What is the state of financial assurance today in the United States?

2.2.1 Measuring environment liability. Environmental liabilities encompass a variety of

levels and types of liabilities. In this dissertation, I do not categorize liabilities. That is, I focus on total

liabilities as opposed to it’s the individual parts.35

When I refer to “liabilities,” I intend it to mean any

environmentally related obligation.

The difficulty in measuring environmental liabilities is undisputed in the literature. The difficulty

lies in quantifying the total cost. Because the total cost encompasses those known and unknown costs,

the estimates are, from the onset, inexact. Even the known costs—those related to site closure,

remediation, reclamation, and post-closure treatment—are inexact, as they are historical costs. However,

they are less inaccurate than the unknown costs. This inaccuracy is not due to lack of rigorous study.

The costs relate more to property damage and health-related claims. The extent of the damage is

unknown. For example, as mentioned in Appendix A, Table A.1, the mining operations in Pennsylvania

were unaware when they began mining decades earlier that a byproduct of the operation is the

production of acid mine drainage (AMD). AMD is extremely toxic and severely contaminates the land,

water, and, in turn, the people inhabiting the nearby land and using the nearby sources of water. The

total cost for this environmental liability is unknown. The only costs the state of Pennsylvania can

estimate are the costs for closure, cleanup, and maintenance of the AMD.

Often, both certain and uncertain costs must be estimated on a case-by-case basis if no set

standard or precedence is followed within an industry. These case-by-case estimations may include

scientifically based decision techniques, contingent scenario evaluation, and a variety of economic

valuation techniques.36

Hence, the literature provides a variety of estimation methods for these illusive

33

33 CFR 138, 151-158 and 40 CFR 263-265 and 279, and may be found at http://www.access.gpo.gov/nara/cfr/cfrhtml_00/Title_33/33cfr138_00.html, http://www.access.gpo.gov/nara/cfr/cfrhtml_00/Title_33/33cfr153_00.html, http://www.access.gpo.gov/nara/cfr/cfrhtml_00/Title_40/40cfr263_00.html, and http://www.access.gpo.gov/nara/cfr/cfrhtml_00/Title_40/40cfr279_00.html. 34

http://www.imo.org/Conventions/contents.asp?doc_id=678&topic_id=258. 35

For an explanation of the variety of categories, please see Valuing Potential Environmental Liabilities for Managerial Decision-Making: A Review of Available Techniques (1996), p 17. 36

For an introduction to and application of valuation techniques, please see Valuing Potential Environmental Liabilities for Managerial Decision-Making: A Review of Available Techniques (1996), p 22.

15

unknown costs; however, the techniques provide no guarantees of accuracy or consensus in the

estimates. Likewise, for the techniques themselves, there is no consensus on accuracy or acceptance by

those using them.

Academicians use market valuation models to evaluate a firm’s value. In these models, we input

proxies for the characteristics. These characteristics include whether or not a firm has an environmental

liability and accurately discloses this information [Landsman (1986); Beaver, Eger, Ryan, Wolfson (1989);

Harris and Ohlson (1987, 1990); Barth, Beaver, Stinson (1991); Barth (1991, 1994); Barth and McNichols

(1994); Nelson (1996); Barth, Beaver, and Landsman (1996); Campbell, Sefcik, and Soderstrom (2001)].

A byproduct of these characteristics is whether the information is believable by market participants [Barth

and McNichols (1994), Harris and Ohlson (1987, 1990), Campbell, Sefcik, and Soderstrom (2001)]. If a

liability is significantly greater than what the market perceived, the market will devalue the firm

accordingly. The above researchers show that honest disclosure ultimately is good for the firm.

Other methods used for measuring environmental damages are the hedonic pricing method, the

travel cost method, and the contingent valuation method. These methods attempt to estimate the use

and non-use values of the environment. The hedonic pricing method is often used to estimate the

change in value due to the presence or lack of an environmental characteristic [Hite, Chern, Hitzhusen,

and Randall (2000); Buschena, Anderson, and Leonard (2001); Ready, Berger, and Blomquist (1997);

Thayer, Murdoch, and Beron (1999)]. For example, a house’s price depends upon its location to a

landfill. Typically, regression analysis generates such prices or values.

Although the hedonic pricing method applies an existing pricing scheme within the market for

valuation purposes, the travel cost method does not. Instead, it estimates the value of items for which a

pricing scheme does not exist [Smith (1997), Fix and Loomis (1998)]. In other words, it attempts to value

the enjoyment of scenic natural areas, such as lakes, parks, beaches, and forests. Those who enjoy

these areas pay real costs for their enjoyment in the form of time, money, and opportunity cost. The

method of valuation is in the form of cost-benefit and impact analyses.

The contingent valuation method is used to estimate the value of environmental services and the

surrounding environment [Coller and Harrison (1995); Cummings, Harrison, and Rutstrom (1995);

Cummings and Harrison (1994); and Harrison and Lesley (1994)]. Of the three, this method is the most

controversial, as it does not depend on a pricing system. Instead, it depends on a measure of social

benefit or social opportunity cost that researchers extract from opinion surveys.

Selecting the most appropriate model or method is difficult, as they may be more appropriate for

some environmental hazards and not others. Likewise, the use of more than one model or method may

be appropriate for robustness sake; however, if the model or method is incomplete or computationally

expensive, then the purpose of the model or method is defeated. Although no consensus exists on which

valuation model or method is the best, these are concentrated efforts to estimate the liabilities for

accurate reporting.

2.2.2 Methods companies use to provide financial assurance for environment liabilities

16

2.2.2.1 Internal assurance versus external assurance. The financial assurance mechanisms

available are common for most potential environmental hazards. Although the potential environmental

hazards are different in nature, the outcome is the same. Regardless of the material, contamination is

contamination. The EPA requires mechanisms but allows for some deviation by allowing state and local

governments to apply rules that are more stringent and increase regulation requirements.

The mechanisms described below guarantee funds for closure, post-closure, and corrective

action costs. This means funds must be available for the closing, maintaining and monitoring after the

closing, and any potential accident that may occur during operation and after closure, including bodily

injury, property damage, or any other liability. Because many potential accidents can occur, it can be

difficult to quantify the funds necessary for assuring against all the possibilities. Likewise, it would be

difficult to afford the amount of assurance necessary for every conceivable accident. The purpose is to

guarantee the EPA will have access to the funds when necessary and that the appropriate PRP will pay.

If an owner or operator has deep pockets, it often provides internal assurance with self-

assurance mechanisms, such as self-assurance/self-insurance, trust funds, or internal bonds. Those that

do not have deep pockets or prefer third-party mechanisms select external assurance mechanisms.

Owners or operators who may have enough capital to provide self-assurance may prefer third-party

mechanisms to signal to the public their stability or to be more transparent. Usually, third-party

mechanisms require due diligence for qualification. Environmental due diligence means an applicant

must pass a regulator’s and/or creditor’s risk screening. The risk screening is a costly procedure. The

property under question is examined, and the potential and highly probable risks associated with the

property and its use, are assessed. Likewise, the applicant for the mechanism must pass an inspection

of its financials.

Most mechanisms have similarities, such as:

• cost estimates must be updated annually,

• mechanisms must be reevaluated with respect to these new cost estimates for their

appropriateness,

• adjustment of the necessary funds to reflect the new estimates must be made available,

• regulators must be informed of a change in funding and/or mechanism, and

• new mechanisms or additional funds must be in place within four months of the end of

the fiscal year.

2.2.2.2 External assurance

2.2.2.2.1 Trust funds. Two trust fund methods are available: a prepayment fund or an

external sinking fund. The prepayment method requires complete advanced funding in a trust fund,

escrow account, government fund, certificate of deposit, or government securities. Well-known organized

trust funds include the Superfund, Abandoned Mine Reclamation Fund, Leaking Underground Storage

Fund, Environmental Response Fund, and Oil Spill Liability Trust Fund. Unlike the trust funds initiated by

individual firms, federal and state industry-specific taxes fund the organized trust funds.

17

With an external sinking fund, annual payments are made until it is completely funded which must

be prior to the expiration of the permit or upon closure, whichever occurs first. Similar to the prepayment

fund, the external sinking fund may take on any of the forms listed above. According to the regulations,

the payment depends upon the current closure cost estimate minus the current value of the trust fund

divided by the number of years remaining in the pay-in period.

2.2.2.2.2 Surety methods: bonds, letter of credit, or line of credit. A surety

mechanism is one that provides a performance guarantee, meaning a firm that holds this type of

mechanism promises to close, clean up, and/or maintain the expressly named site. To satisfy regulators,

surety mechanisms:

• do not expire, unless otherwise noted in advance by the issuer of the mechanism,

• certify the surety will pay the full face value to the designated recipient upon the holder’s

default,

• remain in effect until regulators revoke the permit, and

• issued by surety companies approved under the U.S. Department of the Treasury

Circular 570 and the EPA.

Surety bonds, also called payment bonds, performance bonds, or financial guarantee bonds,

certify the surety company will provide the available funds when the owner or operator defaults on their

responsibilities. Similarly, parent corporations or other third parties may issue letters or lines of credit.

The assurance providers perform the same function as the surety company, meaning they guarantee the

availability of funds upon the mechanism holder’s default.

2.2.2.2.3 Insurance. Insurance policies are available for a variety of environmental

liabilities. The insurance policy contains provisions that guarantee funds will be available in the event a

claim arises. Like the surety mechanism, insurance policies remain in affect unless the policyholder

defaults on the premium payment or regulators verify closure of the site according to the indicated

guidelines. External and internal insurance are popular mechanisms for insuring closure costs and

insuring against liability claims. Internal insurance, or self-insurance, I discuss below.

2.2.2.3 Internal assurance

2.2.2.3.1 Statement or letter of intent. Typically, those who provide self-, parent, or

corporate guarantees, and those who are federal, state, or local government licensees use this

mechanism. The statement or letter of intent includes the guaranteeing entity’s obligation to provide the

funds when needed. It also denotes the estimated cost of closure and indicates the source of guaranteed

funds to cover the closure costs in the event the company or subsidiary defaults. This mechanism is

especially tenuous when a company is providing a self-guarantee. If the company fails, then the funds

are not available to meet the guarantee. Similarly, parent firms have been known to divest a failing

subsidiary, leaving regulators without recourse for reimbursement [Ringleb and Wiggins (1990) and

MacMinn and Brockett (1995)].

18

2.2.2.3.2 Self-, parent, or corporate guarantee. Passing one of two possible financial

test options is required for self-, parent, grandparent, sibling, or any other corporate guarantee.37

Companies that use the financial tests to provide self-guarantees (e.g., self-bonding or self-insuring)

must:

• provide a letter from a company manager, typically the chief financial officer, attesting to

the company’s compliance with environmental rules,

• provide the firm’s independently audited financial statements for the current fiscal year,

and

• verify the current fiscal financial statements pass the financial test.

The financial tests vary slightly according to the type of hazard. Below is a list of requirements for

passing the financial tests by each type of hazard:

2.2.2.3.2.1 Nuclear power reactor licenses. To provide self-guarantees for nuclear power reactor

licenses, companies must satisfy all the following requirements: Tangible net worth of at least $10 million

or at least 10 times the total current closure cost estimate for all facilities. They must also have at least

90 percent of total assets located in the United States or at least 10 times the current closure cost

estimate for all facilities. For those companies without bond ratings, the company must have a ratio of

cash flow divided by total liabilities greater than 0.15 and a ratio of total liabilities divided by net worth less

than 1.5. For those companies with bond ratings, the most current bond issue rated at A or higher by

Standard and Poor’s or Moody’s. Finally, the company must have at least one class of equity securities.

For those providing parent or other corporate guarantees, all the following must be satisfied. Two

of the following three ratios: a ratio of total liabilities to net worth less than 2.0; a ratio of the sum of net

income plus depreciation, depletion, and amortization to total liabilities greater than 0.1; and a ratio of

current assets to current liabilities greater than 1.5. The company must have net working capital at least

six times the sum of the current closure cost estimate for all facilities. Likewise, tangible net worth must

be at least $10 million and at least six times the sum of the current closure cost estimate for all facilities.

At least 90 percent of total assets located in the United States or at least six times the current closure

cost estimate for all facilities.

Otherwise, the parent or other company must satisfy the following requirements. The most

current bond issue rated at A or higher by Standard and Poor’s or Moody’s. The company must have net

working capital at least six times the sum of the current closure cost estimate for all facilities. Tangible

net worth must be at least $10 million and at least six times the sum of the current closure cost estimate

for all facilities. At least 90 percent of total assets must be located in the United States or at least six

times the current closure cost estimate for all facilities.

2.2.2.3.2.2 Nuclear non-power reactor licenses. Although examination of owners and

operators of non-power reactors is beyond the scope of this study, those entities may obtain parent or

37

A corporate parent must own at least 50 percent of the voting stock of the firm or subsidiary for which it is providing the guarantee. A corporate grandparent owns over 50 percent of a firm through a subsidiary, and a corporate sibling is a firm that shares the same corporate parent.

19

corporate guarantees that may not be from non-profit organizations. To provide parent and other

corporate guarantees for nuclear non-power reactor licenses, companies must satisfy the following

financial test:38

Two of the following three ratios: a ratio of total liabilities to net worth less than 2.0; a ratio of the

sum of net income plus depreciation, depletion, and amortization to total liabilities greater than 0.1; and a

ratio of current assets to current liabilities greater than 1.5. Net working capital must be at least six times

the sum of the current closure cost estimate for all facilities. Tangible net worth must be at least $10

million and at least six times the sum of the current closure cost estimate for all facilities. At least 90

percent of total assets located in the United States or at least six times the current closure cost estimate

for all facilities.

Otherwise, the parent or other company must satisfy the following requirements. For those

companies with bond ratings, the most current bond issue rated at BBB by Standard and Poor’s or Baa

by Moody’s. Net working capital must be at least six times the sum of the current closure cost estimate

for all facilities. Tangible net worth must be at least $10 million and at least six times the sum of the

current closure cost estimate for all facilities. At least 90 percent of total assets located in the United

States or at least six times the current closure cost estimate for all facilities.

According to the regulations, each nuclear power license applicant presents proof of financial

assurance and a decommissioning funding plan. Liability coverage estimates and cost estimates are

available in the decommissioning funding plan. These estimates depend on the type of power used; the

type of waste produced; all costs related to the servicing of the site, equipment, and waste; the number of

reactors at a site; and the number of incidents occurring at the site.39

These cost estimates determine the

amount and the type of financial protection and financial assurance required. “Financial protection” is the

terminology used by the NRC when discussing liability coverage. Financial protection is an additional

requirement beyond the financial assurance amounts and applies to liability claims and legal costs.40