Embed Size (px)

Citation preview

Fixed Income Special

European High Yield Non-Food Retail

Author:

Jannik Prochnow

Analyst

+49 69 913090 595

19 February 2015

Overview

1. Recommendation and spreads 3

2. Company profiles 7

2.1 Hornbach Baumarkt 8

2.2 Maisons du Monde 16

2.3 BUT 23

2.4 Dufry 37

3. Appendix: Macroeconomic environment 36

4. Disclaimer 43

5. Contacts 51

19/02/2015 2

2. Recommendation and spreads

Company initiations*

Overweight on MdM and Dufry, marketweight on Hornbach

Recommendations:

(Screening Coverage)

Berenberg initiates on Dufry’s 07/22 notes with an overweight rating. This is mainly based on

Dufry’s very strong market position and large scale as well as its high profitability. More particularly,

we like Dufry’s strong free cash flow profile although we note that FCF has been constrained by its

acquisitions. On the negative side, Dufry is highly dependent on global passenger flows and its

acquisition-driven growth strategy is reflected in high leverage ratios. However, we regard the

downside risks as limited and note that Dufry’s 07/22 bonds are trading at an attractive pick-up vs.

the double-B average.

4 Source: Berenberg FI Research; *Our recommendations are based on a fundamental analysis & a relative valuation based on market spreads

We see the strong market position and brand recognition as BUT’s key strengths. We also like the

company’s multichannel distribution strategy and its ability to gain market share. However, BUT has

relatively weak operating margins which makes it more vulnerable to a setback in consumer

demand, especially given its high leverage. Moreover, credit metrics are likely to remain under

pressure due to future acquisitions, including a potential acquisition of 18 franchisee stores. As BUT

has not provided us with the latest financial information, we are not in the position to provide a

recommendation on its notes.

Maisons du Monde has exhibited very strong sales growth in recent years despite challenging

market conditions. Furthermore, we like the company’s multi-channel approach with its unique

product offering. At the same time, MdM’s high leverage and the sales shift towards less profitable

furniture products weigh on its financial profile. Nonetheless, we believe that MdM will continue its

growth story and will be able to deleverage in the near to medium term, especially given

management’s deleveraging commitment. We therefore initiate on MdM’s 08/20 notes with an

overweight rating.

Berenberg initiates with a marketweight recommendation on Hornbach’s 02/2020 bond. We like the

company’s leading market positions, its very efficient megastore network and the increasing

international presence. However, we note that Hornbach operates in a highly seasonal, cyclical and

competitive market and is strongly leveraged. We regard deleveraging potential as limited in the

near future, especially due to higher capex requirements for the expansion of the store network.

Moreover, we believe that Hornbach’s sound financial policy is already reflected in current spread

levels.

HBMGR 3 ⅞ 02/20

Senior unsecured notes

Price / Z-spread / YTW:

110.0 / 146 / 1.8 (Pricing: 19/02/2015 BGN Close)

Marketweight

MDMFP 9 08/20

Senior secured notes

Price / Z-spread / YTW:

102.5 / 797 / 8.2 (Pricing: 19/02/2015 BGN Close)

Overweight

DUFSCA 4 ½ 07/22

Senior unsecured notes

Price / Z-spread / YTW:

107.0 / 269 / 2.8 (Pricing: 19/02/2015 BGN Close)

Overweight

BUTSAS 7 ⅜ 09/19

Senior secured notes

Price / Z-spread / YTW:

95.8 / 825 / 8.5 (Pricing: 19/02/2015 BGN Close)

No recommendation

19/02/2015

AAFFP 5 ⅝ 04/19

Senior secured notes

Ratings*: B2 / B / BB-

Price / Z-spread / YTW:

94.6 / 691 / 7.1 (Pricing: 19/02/2015 BGN Close)

Marketweight (08/12/2014 – Click here)

Recommendation overview within the HY retail sector

Current valuations of retailers offer some attractive entry opportunities

5 Source: Berenberg FI Research *Moody’s / S&P / Fitch

MDMFP 9 08/20

Senior secured notes

Ratings*: B2 / B / -

Price / Z-spread / YTW:

102.5 / 797 / 8.2 (Pricing: 19/02/2015 BGN Close)

Overweight (19/02/2015)

DUFSCA 4 ½ 07/22

Senior unsecured notes

Ratings*: Ba3 / BB+ / BB

Price / Z-spread / YTW:

107.0 / 269 / 2.8 (Pricing: 19/02/2015 BGN Close)

Overweight (19/02/2015)

HBMGR 3 ⅞ 02/20

Senior unsecured notes

Ratings*: Ba2 / BB+ / -

Price / Z-spread / YTW:

110.3 / 142 / 1.7 (Pricing: 19/02/2015 BGN Close)

Marketweight (19/02/2015)

DRTYLN 5 ⅞ 03/21

Senior unsecured notes

Ratings*: - / BB- / -

Price / Z-spread / YTW:

104.2 / 450 / 4.7 (Pricing: 19/02/2015 BGN Close)

Overweight (08/12/2014 – Click here)

THOEUR 7 ⅜ 07/19

Senior secured notes

Ratings*: B2 / B / -

Price / Z-spread / YTW:

102.0 / 652 / 6.7 (Pricing: 19/02/2015 BGN Close)

Overweight (08/12/2014 – Click here)

In our screening coverage

universe of European HY

retailers, we recommend to

overweight four and to

marketweight two retailers.

Even if the macroeconomic

conditions for European

retailers remain challenging,

we believe that the above-

average spreads can offer

very attractive entry points,

particularly given the expected

recovery in most parts of

Europe.

In our view, the following key

success factors for retailers

to remain competitive are:

- online presence or

multichannel distribution

strategy

(Darty & Maisons du Monde)

- international diversification

(Dufry & Hornbach)

- Efficient supply chain and

operating flexibility

(THOM Europe)

19/02/2015

DUFSCA 07/22

AAFFP 04/19

DRTYLN 03/21

BUTSAS 09/19

HBMGR 02/20

MDMFP 08/20

SMCPFP 06/20 THOEUR 07/19

0

100

200

300

400

500

600

700

800

900

1,000

0 1 2 3 4 5 6 7 8 9 10

Z-s

pre

ad

(in

bp

s)

Time to worst

Spread landscape*

Plenty shopping opportunities for investors within retailing

Furniture and homeware retail

bonds BUTSAS 09/19 and

MDMFP 08/20 offer the most

appealing spreads within our

observed universe.

On average, single-B

consumer bonds trade

approximately 50-150bp wider

than single-B non-financials.

(B) Consumer

(B) Non-Financials

(BB) Non Financials

6 Source: Bloomberg (19/02/2015), Berenberg Fixed Income Research; *Outliers not shown and excluded from curve estimation

BBB- Non Financials

19/02/2015

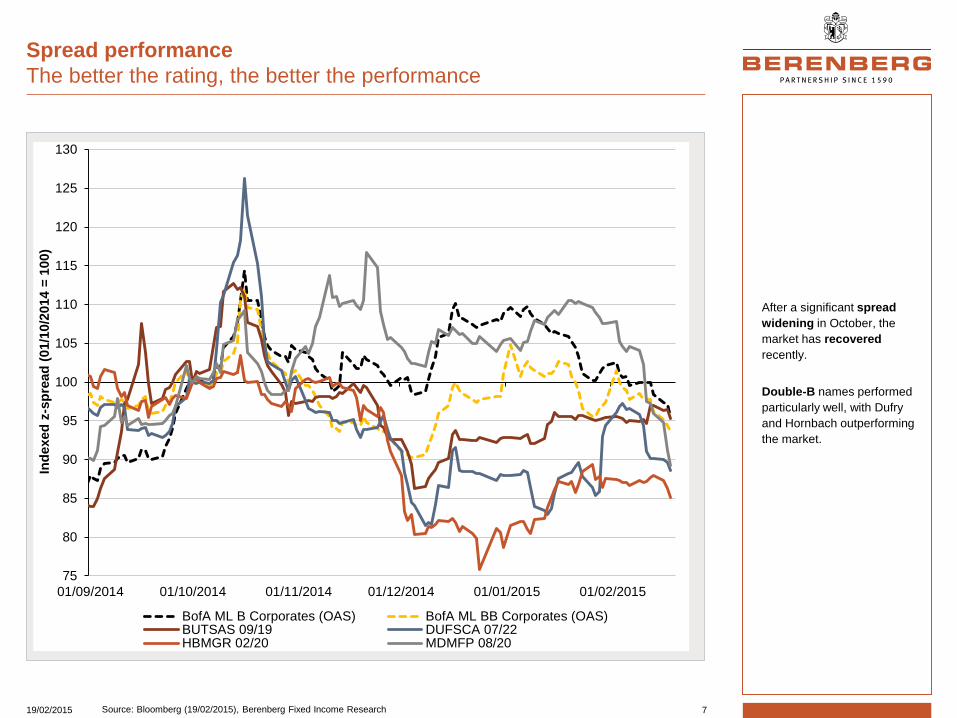

Spread performance

The better the rating, the better the performance

After a significant spread

widening in October, the

market has recovered

recently.

Double-B names performed

particularly well, with Dufry

and Hornbach outperforming

the market.

7 Source: Bloomberg (19/02/2015), Berenberg Fixed Income Research

75

80

85

90

95

100

105

110

115

120

125

130

01/09/2014 01/10/2014 01/11/2014 01/12/2014 01/01/2015 01/02/2015

Ind

exed

z-s

pre

ad

(01/1

0/2

014 =

100)

BofA ML B Corporates (OAS) BofA ML BB Corporates (OAS)BUTSAS 09/19 DUFSCA 07/22HBMGR 02/20 MDMFP 08/20

19/02/2015

2. Company profiles

2. Company profiles

2.1 Hornbach Baumarkt

Company data

Headquarter:

Bornheim (Germany)

Products:

Tools and hardware, building

materials, bathroom fittings and

tiles, paint, wall and floor

coverings, garden products

Major shareholders:

Hornbach Holding (76.4%)

Next financial release:

24/03/2015 (FY2014/15)

Trading statement

Bond data

Price / Z-spread / YTW:

110.0 / 146 / 1.8 (Pricing: 19/02/2015 BGN Close)

Callable:

No

Amount outstanding (€):

250m

Bond ratings:

Moody’s: Ba2 (positive)

S&P: BB+ (stable)

Covenants:

Covenant-lite package

Payment rank:

Senior unsecured

Hornbach Baumarkt

Investment thesis and company snapshot

Hornbach Baumarkt Recommendation:

HBMGR 3 ⅞ 02/20 (Bloomberg: HBMGR<Corp>) Marketweight

Weaknesses

• Highly seasonal and cyclical DIY market

• Challenging competitive environment, but less pressure

since bankruptcy of German competitor Praktiker

• High leverage (lease-adjusted)

Investment thesis Berenberg initiates with a marketweight recommendation on Hornbach’s 02/2020 bond. We like the company’s leading

market positions, its very efficient megastore network and the increasing international presence. However, we note that

Hornbach operates in a highly seasonal, cyclical and competitive market and is strongly leveraged. We regard deleveraging

potential as limited in the near future, especially due to higher capex requirements for the expansion of the store network.

Moreover, we believe that Hornbach’s sound financial policy is already reflected in current spread levels.

Selected Financials

Company Snapshot German Hornbach Baumarkt AG is a leading European do-it-yourself (DIY) retailer with a network of 147 stores in Europe, of

which 98 are based in Germany, representing c. 58% of sales. The company mainly focuses on operating >10,000sqm DIY

megastores combined with garden centres. In 2010, Hornbach successfully introduced an online platform in Germany,

followed by the launch of an online store in Austria 2013. The product range comprises over 50,000 products, which are

offered at permanently low prices, and primarily target DIY customers engaged in large construction or renovation projects.

Strengths

• Very efficient megastore concept, good online presence

• Leading market positions with increasing market shares

• Successful everyday low price strategy

• High customer loyalty and strong brand recognition

through original marketing campaigns

• Good and increasing international presence

€ m (FY ends 28 Feb) 2012 2013 2014 3Q2015

Net sales 3,001.0 3,020.0 3,152.0 2,669.8

Gross profit 1,122.9 1,127.7 1,178.1 1,013.0

EBITDA 184.3 155.8 161.0 182.7

Adj. net debt/EBITDAR 3.6x 4.2x 4.0x 3.6x*

EBITDA interest cover 7.3x 6.0x 9.6x 11.4x*

FCF (before dividends) -5.9 -21.6 60.7 91.0

10 Source: Company data, Bloomberg (19/02/2015), Berenberg FI Research *Based on estimated FY2015 EBITDA/R figures.

DUFSCA 07/22

BUTSAS 09/19

HBMGR 02/20

MDMFP 08/20

-200

0

200

400

600

800

1,000

0 2 4 6 8 10

Z-s

pre

ad

(in

bp

s)

Time to worst

19/02/2015

Opportunities

• Internationalisation: very

profitable European markets

(except for Germany)

• Not yet exploited potential for

online distribution

• Further market consolidation

in the mid to long term

• Cocooning as a social trend

Threats

• Continuing slow economic

recovery in Europe

• Intensifying competition in

German DIY market and other

European countries

Industry characteristics In general, a DIY retailer offers a broad range of products and solutions for the independent realization of home

improvements, in most cases targeted at private and professional consumers.

Europe is the second largest DIY market worldwide, following the US. Within Europe, Germany represents the largest DIY

market in terms of sales (c. €18.1bn in 2013). However, unlike other mature markets, the German DIY market is highly

fragmented with many regional players (comparably low market concentration in Germany with top 5 players holding roughly

70% of the market in terms of sales) and characterized by fierce price competition, causing persisting pressure on margins.

Online distribution could have important implications for the DIY market in the short to medium term. Compared to other

sectors, the DIY/home improvement industry still exhibits a relatively low level of online sales penetration and therefore

offers some potential for growth in the future.

0

10,000

20,000

30,000

-10%

0%

10%

20%

'02 '04 '06 '08 '10 '12 '14 '16

Shipping development

Demand (world container trade, Y/Y)Supply (containership fleet development, Y/Y)Aver. containership earnings* (rhs, USD/day)

Industry forces

Hornbach Baumarkt

The German DIY retail market

Preferred purchasing channel by various sectors (2012) Market share by DIY retailer in Germany (2013)

Size and sales density of European DIY markets (2012)

11 Source: Company data, Dähne, PWC, Berenberg Equity Research, Berenberg FI Research; *Only considering stores >1,000 sqm

6% 6%

7%

11%

12%

13%

15%

19%

11% Hellweg

Praktiker/Max Bahr

Globus/Hela

Hagebau/Zeus

Hornbach

Toom

Bauhaus

Obi

Other

0

1,000

2,000

3,000

4,000

0

10

20

30

40

EU

R p

er

sq

m*

EU

R b

n

Market size Sales density (rhs)

71% 67%

56% 54%

52% 50%

49% 49%

45% 39%

35% 21%

7% 17% 32%

15% 21% 30%

36% 31%

25%

56%

33% 68%

0%

20%

40%

60%

80%

100%

In-store purchases Online purchases

Pricing pressures

• Increased use of discount campaigns to compete in the market (low switching costs, undifferentiated products)

• Service will be key to differentiate

Social trends

• Cocooning/homing (consumers are staying at home more frequently)

• Increasing environmental and cost awareness (need for energy efficiency and sustainability)

State of the economy

• In crisis times, home improvements come into focus ("homing")

• A strong housing market encourages people to move which supports the DIY market

Internationalisation

• Focus on new markets considering mature and competitive German DIY market

• Increased focus on Eastern Europ. and neighbouring German markets

DIYretailing

19/02/2015

Berenberg

competitive scoring

Sensitivity to macro cycles

low / average / high

Regulatory risks

low / average / high

Scale & geographic

diversification

weak / average / strong

Competitive position

weak / average / strong

Financial policy

conservative / sound / aggressive

Distribution strategy

weak / average / strong

Brand awareness

low / average / high

Profitability

low / average / high

Revenue & cash flow volatility

low / average / high

Evolution of store network and weight. average sales / store

Hornbach Baumarkt

Strategic positioning

Strategic direction Hornbach Baumarkt is a leading German DIY retailer which offers a broad

range of high-quality building, renovation and garden products to project and

professional customers, at consistently low prices. In addition, the company

has a strong focus on offering a range of specialists advice and customer

services. According to Kundenmonitor Deutschland 2014, Hornbach ranked

top among German DIY retailers in terms of overall customer satisfaction

(ranked 1st in 6 of 9 product range disciplines).

Hornbach’s strategic concept concentrates on a large network of DIY

megastores (average store size of 11,600 sqm) located in urban catchment

areas, with the aim to permanently offer a large product selection (over

50,000 products per store on average) in close proximity to its customers.

Hornbach in particular convinces with a high efficiency (net sales/sqm) in its

domestic market , despite a challenging market environment with a rather low sales density in Germany. Moreover, Hornbach pursues an active European expansion plan with currently 49 stores in 8

non-domestic markets, which offer a higher sales density (c. 40% of sales and c. 60% of EBIT).

Since 2010, with the launch of its online shop, Hornbach also makes use of a multi-channel retailing approach, helping the

company to also attract customers outside of the catchment area of its megastores. Since 2013, an online shop is also

available for Hornbach’s second largest market, Austria.

Customer satisfaction in German DIY market

12 Source: Company data, Kundenmonitor, Dähne, Berenberg FI Research; *Bubble size = total net sales in Europe, Praktiker went bankrupt.

German industry-wide DIY efficiency (2013)*

2.51

2.49

2.45

2.39

2.36

2.29

2.23

2.22.32.42.52.6

Obi

Toom Baumarkt

Hellweg

Bauhaus

Hagebau

Globus Baumarkt

Hornbach

Industry average

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

750 1,000 1,250 1,500 1,750 2,000

Avg

sto

re s

ize

(s

qm

)

Net Sales (€/sqm)

Megastores

92 91 92 92

41 43 46 49

21.2

21.6

22

22.4

22.8

0

40

80

120

160

2011 2012 2013 2014€/s

qm

No

. o

f sto

res

Stores all over EuropeStores in GermanyWeighted Average Sales per Store (rhs)

11 10

8 1

6 5

3 5

0 10 20

Austria

Czech…

Slovakia

Sweden

19/02/2015

Senior Unsecured Notes HBMGR 3 ⅞ 02/20

Issuer:

Hornbach Baumarkt AG

Guarantor(s):

Hornbach International GmbH

Comments on Covenants

• Covenant-lite package resulting

in considerably less covenant

protection than found in most high

yield bonds (Restricted Payments,

Asset Sales, Merger, Affiliate

Transactions & Anti-Layering

provisions missing)

• No restriction on the amount of

secured bank debt (debt will be

senior to unsecured notes)

• No limit on the amount of

structurally senior subsidiary debt

which will rank ahead of notes

• Only optional redemption for tax

reasons

• Weak Change of Control clause

with double trigger (put at par; put

not effective if at end of CoC

period lower rating than BB+/Ba2

is assigned to issuer or long-term

liabilities outstanding)

• Events of Default contain both a

cross acceleration and cross

default clause (typical IG clauses;

positive for investors)

Capital structure

Corporate structure

Hornbach Baumarkt

Focus on bond structure

Maturity profile

13 Source: Company data, Berenberg FI Research; *Based on estimated FY2015 EBITDA figures

Hornbach Baustoff Union GmbH

Hornbach International GmbH

Hornbach Baumarkt AG

Hornbach Holding AG

Hornbach Immobilien AG

Senior NotesIssuer of the Notes

Guarantors of the Notes

RCF

250 250

0

100

200

300

€m

RCF 12/16 Senior Unsecured Notes 02/20

€ m 3Q2015 xEBITDA/R Maturity

Cash & cash equivalents (423.7)

Bank liabilities 101.1

Other 6.2

Senior unsecured notes 246.8 02/2020

Net cash 69.6 –

Adj. net debt (lease-adjusted) 1,313.0 3.6x*

Maximum availability under RCF 250.0 12/2016

19/02/2015

The rating agencies’ opinion*

Hornbach Baumarkt

The rating agencies’ view

Threshold for rating pressure…

Rating pressure could arise from*…

• Relatively small size compared to other retailers (M)

• Relatively high gross financial leverage (M)

• High seasonality and cyclicality of the DIY industry –

strong dependence on weather (S&P)

• Stiff competition and additional pressure from

specialized online retailers (S&P)

• High CAPEX requirement for expansion of store

network limits FCF generation (M)

• Strong position in German DIY market (M, S&P)

• Meaningful geographic diversification and further

growing international presence (M, S&P)

• Good strategy execution and customer

satisfaction (M, S&P)

• Well-positioned e-commerce platform (S&P)

• On-going negative sales trend (S&P)

• Financial leverage trends towards 5.5x (M)

• Contradiction of (S&P) adj. EBITDA margin to well

below 10% causing (S&P):

i) FFO/Debt to fall below 20%

ii) FOCF/Debt to fall below 10%

iii) EBITDA interest coverage to fall below 3.0x

• Sustainably maintain LFL revenue growth in

Germany (M)

• EBITDA margin expansion causing FFO/Debt to

sustainably increase to more than 30% (S&P)

• Adj. Debt/EBITDA trends towards 4.0x (M)

• EBITA/Interest Expense ratio remaining above 2.5x

(M)

Adjusted Debt/EBITDA (Moody’s) EBITA/Interest Expense (Moody’s)

14 Source: Company data, Moody’s, S&P, Berenberg Fixed Income Research; *M = Moody’s

Ratings

Moody’s:

Corporate Family: Ba2

Senior unsecured: Ba2

Outlook: Positive

Last update: 02/09/2014

S&P:

Corporate Family: BB+

Senior unsecured: BB+

Outlook: Stable

Last update: 31/07/2014

Fitch:

Corporate Family: NR1

Senior Secured: NR1

Outlook: n.a.

Last update: n.a.

1 NR = Not rated

4.9x

4.7x5.1x 5.1x

3.0x

4.0x

5.0x

6.0x

2011 2012 2013 2014

Debt/EBITDA

threshold for upward rating pressure

threshold for downward rating pressure

2.4x2.5x

2.0x

2.3x

1.5x

2.0x

2.5x

3.0x

2011 2012 2013 2014

EBITA/Interest Expense

threshold for upward rating pressure

19/02/2015

Hornbach Baumarkt

Summary of company figures

Revenue & Profitability Adj. net debt/EBITDAR* EBITDA interest coverage

15 Source: Company data, Berenberg FI Research; *Based on estimated FY2015 EBITDA/R and FCF figures.

6.1%

5.2% 5.1%

6.8%

0%

2%

4%

6%

8%

0

1,000

2,000

3,000

4,000

2012 2013 2014 3Q2015

€ m

Revenue

EBITDA

EBITDA margin (rhs)

3.6x

4.2x 4.0x

3.6x

0.0x

1.5x

3.0x

4.5x

6.0x

0

400

800

1,200

1,600

2012 2013 2014 3Q2015

€ m

Adj. Net debtEBITDARAdj. net debt/EBITDAR (rhs)

7.3x

6.0x

9.6x

11.4x

0.0x

1.5x

3.0x

4.5x

6.0x

7.5x

9.0x

10.5x

12.0x

0

25

50

75

100

125

150

175

200

2012 2013 2014 3Q2015

€ m

EBITDACash Interest ExpenseEBITDA interest coverage

Selected profit & loss and cash flow financials (€ m)

€ m (FY ends 28 February) 2012 2013 2014 3Q2015

Customer sales 3,001.0 3,020.0 3,152.0 2,669.8

LFL growth 2.8% -1.4% 2.7% 4.9%

Gross profit 1,122.9 1,127.7 1,178.1 1,013.0

EBITDA 184.3 155.8 161.0 182.7

EBITDA Margin 6.1% 5.2% 5.1% 6.8%

Change in working capital -40.2 -13.1 19.4 34.1

Capex -95.6 -116.1 -71.9 -76.9

Cash interest -25.2 -26.1 -16.9 -12.4

Cash taxes -29.1 -22.1 -31.0 -36.5

Free Cash flow -5.9 -21.6 60.7 91.0

Selected balance sheet financials, ratios and store network evolution

€ m (FY ends 28 February) 2012 2013 2014 3Q2015

Store network (#) 134 138 141 147

Total assets 1,628.1 1,597.4 1,670.3 1,755.2

% o/w intangibles 1.0% 0.8% 0.7% 0.6%

Cash 404.3 317.2 371.1 423.7

FCF/Total debt -1.4% -5.6% 16.3% 14.1%*

Debt/EBITDA 2.3x 2.5x 2.3x 1.9x*

Net debt/EBITDA 0.2x 0.4x 0.0x Net cash*

Adj. debt/EBITDAR 4.8x 5.2x 5.2x 4.8x*

Adj. net debt/EBITDAR 3.6x 4.2x 4.0x 3.6x*

EBITDA interest coverage 7.3x 6.0x 9.6x 11.4x*

19/02/2015

2. Company profiles

2.2 Maisons du Monde

Maisons du Monde

Investment thesis and company snapshot

Maisons du Monde Recommendation:

MDMFP 9 08/20 (Bloomberg: MDMFP <Corp>) Overweight

Weaknesses

• Modest size of business operations and limited

geographical diversification (~ ⅔ of sales in France)

• High seasonality and cyclicality of the furniture and

decoration market

• High leverage

• Sales shift towards less profitable furniture products

Selected Financials

Company Snapshot Maisons du Monde (MdM) is a France-based multi-channel retailer which offers a wide range of furniture and decorative

items under its own brand label. Founded in 1996, the company currently operates a network of 241 stores across Europe,

with a primary focus on France. In addition, MdM increases its geographical reach by offering its products via its website in

countries where it has no brick-and-mortar presence. In 2013, the majority stake of MdM was acquired in an LBO by Bain

Capital. The management team around founder and CEO Xavier Marie has remained another significant shareholder.

Strengths

• Broad product range with a unique brand offering

• Multi-channel approach combining a strong French

store with an integrated European-wide online platform

• Supply-chain integrated business model

• Strong track record of achieving market share gains

and growth in earnings and profitability

€ m (FY ends 31 Dec) 2011 2012 2013 LTM

3Q2014

Customer sales 421.3 494.7 549.7 602.2*

Gross profit 257.4 305.3 366.4 424.7

EBITDA 59.6 75.0 70.9 65.6

Adj. net debt/EBITDAR 7.1x 6.5x 5.2x 6.5x

EBITDA interest coverage 3.7x 4.6x 3.2x 2.0x

Free cash flow 12.6 11.0 -5.9 -2.7

17

Company data

Headquarter:

Vertou, Nantes (France)

Products:

Furniture, large and small

decorative items

Major shareholder:

Bain Capital, management

Next financial release:

9 April 2015

FY 2014 financial statements

Bond data

Price / Z-spread / YTW:

102.5 / 797 / 8.2 (Pricing: 19/02/2015 BGN Close)

Callable (only on dates shown)

08/01/2016 @ 104.50%

08/01/2017 @ 102.25%

08/01/2018 @ 100.00%

08/01/2019 @ 100.00%

Amount outstanding (€):

325m

Bond ratings:

Moody’s: B2 (stable)

S&P: B (stable)

Covenants:

HY standard package

Payment rank:

Senior secured

Source: Company data, Bloomberg (19/02/2015), Berenberg FI Research *Reported FY 2014 sales volume according to trading statement.

Investment thesis Maisons du Monde has exhibited very strong sales growth in recent years despite challenging market conditions.

Furthermore, we like the company’s multi-channel approach with its unique product offering. At the same time, MdM’s high

leverage and the sales shift towards less profitable furniture products weigh on its financial profile. Nonetheless, we believe

that MdM will continue its growth story and will be able to deleverage in the near to medium term, especially given

management’s deleveraging commitment. We therefore initiate on MdM’s 08/20 notes with an overweight rating.

.

DUFSCA 07/22

BUTSAS 09/19

HBMGR 02/20

MDMFP 08/20

-200

0

200

400

600

800

1,000

0 2 4 6 8 10

Z-s

pre

ad

(in

bp

s)

Time to worst

19/02/2015

Opportunities

• Sophisticated multi-channel

approach: integration of web-

based and mobile platforms

• Positioning as service

specialist (home design, click-

and-collect, etc.)

• Higher growth potential for

French market due to

population trends (number of

households) and relatively low

market penetration (low

renewal rates)

Threats

• Furniture and electrical goods

generally more cyclical and

vulnerable to adverse

economic developments

• Risk of a prolonged economic

downturn in France

• Highly competitive market with

significant competition from

international online retailers

(e.g. Amazon)

Industry characteristics The homeware retail market covers products from home furniture to decorative items. This definition is extended to home

equipment when including electrical goods (white & brown goods). In general, the sub-segment for decorative items is more

resistant to economic downturns considering its less discretionary character.

Over the past years, the size of the European homeware market remained relatively stable with a CAGR of c. 0.15%. The

French market exhibited a similar development with a slightly higher CAGR of c. 0.55%. Compared to other European

homeware markets, the French market is characterized by a relatively low consumer spending per household. This is mainly

attributable to prevailing low furniture renewal rates in France, where furniture is generally replaced less often on average.

In the future, internet sales will constitute a key driver also for the French homeware industry, considering the generally high

level of web-generated sales in France compared to other European markets and further growth expectations.

0

10,000

20,000

30,000

-10%

0%

10%

20%

'02 '04 '06 '08 '10 '12 '14 '16

Shipping development

Demand (world container trade, Y/Y)Supply (containership fleet development, Y/Y)Aver. containership earnings* (rhs, USD/day)

Industry forces

Maisons du Monde

The French homeware & equipment retail market

Size of European vs French homeware market

Consumer spending on homeware across Europe Web sales evolution by European countries

18 Source: Company data, OC&C, Euromonitor, Berenberg Fixed Income Research; *No figure for other EU countries in 2012 available

16.2 16.3 15.9 15.7 16.2 16.4 16.8 17.4 17.2 16.9 16.9 17.2 16.8

143.7 147.2 149.7 147.2 149.5 152.6158.8 164.7

155.6

142.5 145.6 146.1

0

50

100

150

200

€b

n

France Other EU countries

1,142

1,020

907800

716 603500

0

200

400

600

800

1,000

1,200

€s

pe

nd

/ H

H

Home Furnishings Homewares

5.610.6 13.0

25.6

40.7

60.7

74.2

1.21.43.0

5.46.5

8.2

47.5

1.0

0

20

40

60

80

2007 2008 2009 2010 2011 2012 2013

€b

n

France Germany Italy Spain Belgium UK Austria Others

YoY Growth in %

Highly competitive market

• Increased use of discount campaigns to compete in the market (low switching costs, undifferentiated products)

• Service is key to differentiate

Homeownerhsip trend

• Rising trend in France • Demographic trends (ageing

population tend towards ownerhsip)

• Developments in housing finance

Housing market activity

• Decrease in real estate transactions negatively affects demand for furniture products

• Sales of decorative accessories less affected (less discretionary)

Consumer spending levels

• Discretionary good• Dependent on disposable income

and consumer confidence• Focus on home improvements

during crisis times ("homing")Home-ware

retailing

19/02/2015

Berenberg

competitive scoring

Sensitivity to macro cycles

low / average / high

Regulatory risks

low / average / high

Scale & geographic

diversification

weak / average / strong

Competitive position

weak / average / strong

Financial policy

conservative / sound / aggressive

Distribution strategy

weak / average / strong

Brand awareness

low / average / high

Profitability

low / average / high

Revenue & cash flow volatility

low / average / high

Maisons du Monde

Strategic positioning

Strategic direction Maisons du Monde (MdM) targets a niche segment in the homeware

market, offering a broad range of stylish and authentic products at

affordable prices. The French homeware retailer focuses on a

complementary multi-channel approach, combining a strong store

presence (241 stores as of 2014) with an increasing focus on

website and mobile application as well as catalogue offerings.

Besides the strong exposure to its core market France, MdM also

focuses on building up its presence in other European countries. As

of 2013, the company operated 45 stores outside of France and

opened a further 7 in 2014. Additionally, MdM offers a large part of

its products via its website in countries with no store presence,

including Austria and UK. In the future, Maisons du Monde aims to increase its physical presence in other promising European markets such as Germany, where Maisons du Monde opened

two stores in 2014, and Switzerland, where the company opened its first store in 2014.

With regard to its product offering, the company sets a focus on the continuous renewal and rotation of its product

collections to limit the impact of inventory and fashion risk. The focus within its product range is on small decorative items

(c.52% of sales in 2013), which have a higher net margin contribution due to the transportation costs associated with

furniture and large decorative items, which are not fully offset by delivery fees.

Competitive landscape

Sales split by product category (2013)?

19 Source: Company data, OC&C, Berenberg Fixed Income Research

Decorative objects

Household textile

Kitchenware

Lighting

Mirrors & frames

Tableware

Small decorative itemsArmchairs &

couches

Beds & bedsides

Bookshelves & shelves

Coffee& side tables

Cupboard & wardrobes

Dressers & welsh dressers

Junior

Outdoor furniture

Tables & chairs

Others

Large decorative items

12%

3%

4%

9%

9%

9%

3%

10%

2%

1%

4%

7%

6%

3%

2%

8% 6%

Web Stores

69%

18%

6%4%2%

1%

14%

86%

France Italy Belgium Spain Germany Others

€ 550m

Sales distribution by country and channel

Click & MortarStore-based retailers

Internet-only retailers

Mail order & Internet

Department stores

Home equipment

Furniture & furnishing stores

Sp

ec

iali

sts

No

n-

sp

ec

iali

sts

High share of decoration

High share of furniture

19/02/2015

Senior Secured Notes

MDMFP 9 08/20

Issuer:

Magnolia (BC) S.A.

Guarantor(s):

Magnolia (BC) Midco S.A.R.L.,

Magnolia (BC) S.A.S.,

Maisons du Monde S.A.S. &

Maisons du Monde Italie S.R.L.

Comments on Covenants

• Holdco issuance level - Issuer

without revenue-generating

operations, depending on cash

from subsidiaries to service notes

• RCF ranks pari passu to notes, but

poss. super priority status of RCF

and certain hedging debt up to

AMT of €80m during enforcement

• Certain post-completion mergers

should be completed latest by

31/12/2014 (cf. corpor. structure).

Following completion i.a. IPO Debt

Pushdown could take place (under

certain conditions), which would

trigger certain changes to the

Indenture, i.a. the removal of

certain covenants, the substitution

of BidCo for the issuer and the

release of certain security interests

over the collateral.

• Weak LMT on Liens covenant

allows substantial additional debt

(contribution debt, purchase

money debt, credit facility basket,

general debt basket, uncapped

hedging debt) to be secured on

the collateral. Moreover, ratio debt

(including additional notes) may

also be secured on collateral

without a monetary cap only

subject to a CSSLR ≤3.5x

Capital structure

Corporate structure

Maisons du Monde

Focus on bond structure

Maturity profile

20 Source: Company data, Berenberg FI Research *Based on LTM figures

60

325

0

100

200

300

400

€m

RCF 08/19 Senior Secured Notes 08/20

€ m 3Q2014 xEBITDA/R Maturity

Cash & cash equivalents (14.2)

Senior secured RCF (€60m) 20.0 08/2019

Senior secured notes 325.0 08/2020

Net senior secured debt 330.8 5.0x*

Net senior secured debt (lease-adj.) 689.4 6.5x*

Bain Capital

Senior SecuredNotes

RCF€ 60m€ 325m

(Restricted Group)

Magnolia (BC) S.A.

Magnolia (BC) Holdco S.a.r.l.

("LuxCo 1")

Magnolia (BC) Midco S.a.r.l.

("LuxCo 3")

Magnolia (BC) Luxco S.C.A.

("LuxCo 2")

Maisons du Monde Italie S.R.L.

Non-Guarantor Subsidiaries

Issuer of the Notes

Guarantors of the Notes

€ 269.7m notes proceeds loan

Cadr' Academy 1 S.A.S.

Cadr' Academy 2 S.A.

Ginkgo B. S.A.S.("Target")

(Post-closing merger 1)

Magnolia (BC) S.A.S.("BidCo")

Maisons du Monde S.A.S.

Abaco S.A.S.

19/02/2015

Ratings

Moody’s:

Corporate Family: B2

Senior Secured: B2

Outlook: Stable

Last update: 05/11/2014

S&P:

Corporate Family: B

Senior Secured: B

Outlook: Stable

Last update: 27/03/2014

Fitch:

Corporate Family: NR1

Senior Secured: NR1

Outlook: n.a.

Last update: n.a.

1 NR = Not rated

Rating pressure could arise from…

The rating agencies’ opinion

Maisons du Monde

The rating agencies’ view

Thresholds for rating pressure…

• Large exposure to the fragmented, low-growth

French furniture market (M/S&P)

• High cyclicality and seasonality of the business

(M/S&P)

• Fashion and inventory risk with regard to the

business model (S&P)

• Highly leveraged (S&P)

• Good track record of achieving revenue growth

(M)

• Diversity of the product range – often renewed

(M)

• Above average operating efficiency (S&P)

• Complementary distribution channels with a

successful e-commerce platform (M/S&P)

• Significantly positive LfL growth rates (S&P)

• Successful execution of store repositioning (M)

• Continued positive FCF generation and above

industry-average profitability (M)

• Adj. (Gross) Debt/EBITDA sustainably below 5.0x

and EBITA/interest expense above 2.0x (M)

• EBITDA/cash interest falling below 2.0x (S&P)

• EBITDA deterioration due to increased competition

or failure to manage fashion and inventory risks

(S&P)

• Adj. (Gross) Debt/EBITDA remaining above 6.0x

(M)

• Deterioration of the liquidity profile (S&P)

21 Source: Company data, Moody’s, S&P, Berenberg Fixed Income Research *M = Moody’s

Moody‘s 12-18m forward view

(as of 15/10/2014)

Adj. (Gross) Debt/EBITDA 5.8x-6.2x

Threshold for upward rating pressure 5.0x

Threshold for downward rating pressure 6.0x

EBITA/Interest Expenses 1.3x-1.5x

Threshold for upward rating pressure 2.0x

S&P 12m forward view

(as of 27/03/2014)

EBITDA/cash interest >2.5x

Threshold for upward rating pressure 3.0x

Threshold for downward rating pressure 2.0x

19/02/2015

Revenue & profitability

Maisons du Monde

Summary of company figures

Adj. net debt/EBITDAR EBITDA interest coverage

22 Source: Company data, Berenberg FI Research; *FY 2014 figures according to trading statement

Selected profit & loss and cash flow financials

€ m (FY ends 31 December) 2011 2012 2013 LTM 3Q14

Customer sales 421.3 494.7 549.7 602.2*

LFL growth 13.4% 5.9% -0.1% 1.2%*

Gross profit 305.3 366.4 404.7 424.7

EBITDA 59.6 75.0 70.9 65.6

EBITDA Margin 14.1% 15.2% 12.9% 10.7%

Change in working capital -9.2 -4.6 -11.9 -1.4

Capex -20.2 -39.3 -42.1 -32.4

Cash interest -16.0 -16.3 -22.2 -32.9

Cash taxes -1.6 -3.9 -0.6 -1.7

Free Cash flow 12.6 10.9 -5.9 -2.8

7.1x

6.5x 5.2x

6.5x

0.0x

1.5x

3.0x

4.5x

6.0x

7.5x

9.0x

0

150

300

450

600

750

900

2011 2012 2013 LTM3Q2014

€ m

Adj. net debtEBITDARAdj. net debt/EBITDAR

14.1%

15.2%

12.9%

10.7%

0%

4%

8%

12%

16%

0

200

400

600

800

2011 2012 2013 LTM3Q2014

€ m

Customer salesEBITDAEBITDA margin (rhs)

3.7x

4.6x

3.2x

2.0x

0.0x

1.5x

3.0x

4.5x

6.0x

0

20

40

60

80

2011 2012 2013 LTM3Q2014

€ m

EBITDACash interest expensesEBITDA interest cover (rhs)

Selected balance sheet financials, ratios and store network evolution*

€ m (FY ends 31 December) 2011 2012 2013 LTM 3Q14

Store network (#) 215 224 236 241*

Total assets 509.1 549.9 827.6 808.9

% o/w intangibles 54.5% 47.9% 59.1% 58.5%

Cash 62.2 70.0 62.8 14.2

FCF/Total debt 2.5% 2.0% -1.8% -0.8%

Debt/EBITDA 8.5x 7.4x 4.7x 5.3x

Net debt/EBITDA 7.5x 6.5x 3.8x 5.0x

Adj. debt/EBITDAR 7.7x 7.1x 5.7x 6.6x

Adj. net debt/EBITDAR 7.1x 6.5x 5.2x 6.5x

EBITDA interest coverage 3.7x 4.6x 3.2x 2.0x

19/02/2015

2. Company profiles

2.3 BUT

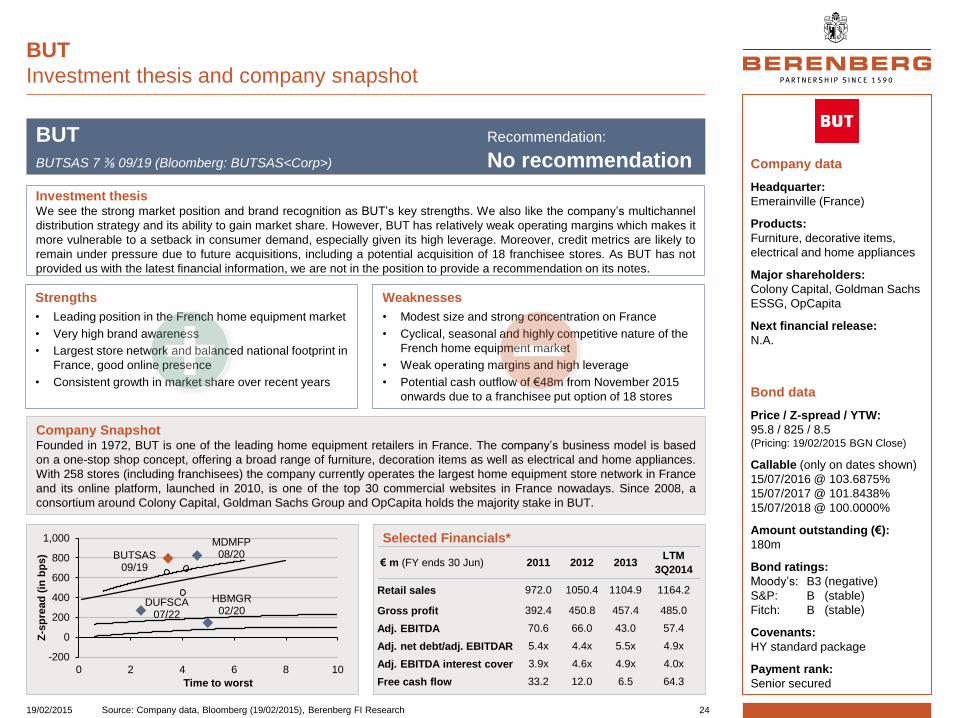

BUT

Investment thesis and company snapshot

BUT Recommendation:

BUTSAS 7 ⅜ 09/19 (Bloomberg: BUTSAS<Corp>) No recommendation

Weaknesses

• Modest size and strong concentration on France

• Cyclical, seasonal and highly competitive nature of the

French home equipment market

• Weak operating margins and high leverage

• Potential cash outflow of €48m from November 2015

onwards due to a franchisee put option of 18 stores

Selected Financials*

Company Snapshot Founded in 1972, BUT is one of the leading home equipment retailers in France. The company’s business model is based

on a one-stop shop concept, offering a broad range of furniture, decoration items as well as electrical and home appliances.

With 258 stores (including franchisees) the company currently operates the largest home equipment store network in France

and its online platform, launched in 2010, is one of the top 30 commercial websites in France nowadays. Since 2008, a

consortium around Colony Capital, Goldman Sachs Group and OpCapita holds the majority stake in BUT.

Strengths

• Leading position in the French home equipment market

• Very high brand awareness

• Largest store network and balanced national footprint in

France, good online presence

• Consistent growth in market share over recent years

€ m (FY ends 30 Jun) 2011 2012 2013 LTM

3Q2014

Retail sales 972.0 1050.4 1104.9 1164.2

Gross profit 392.4 450.8 457.4 485.0

Adj. EBITDA 70.6 66.0 43.0 57.4

Adj. net debt/adj. EBITDAR 5.4x 4.4x 5.5x 4.9x

Adj. EBITDA interest cover 3.9x 4.6x 4.9x 4.0x

Free cash flow 33.2 12.0 6.5 64.3

24

Company data

Headquarter:

Emerainville (France)

Products:

Furniture, decorative items,

electrical and home appliances

Major shareholders:

Colony Capital, Goldman Sachs

ESSG, OpCapita

Next financial release:

N.A.

Bond data

Price / Z-spread / YTW:

95.8 / 825 / 8.5 (Pricing: 19/02/2015 BGN Close)

Callable (only on dates shown)

15/07/2016 @ 103.6875%

15/07/2017 @ 101.8438%

15/07/2018 @ 100.0000%

Amount outstanding (€):

180m

Bond ratings:

Moody’s: B3 (negative)

S&P: B (stable)

Fitch: B (stable)

Covenants:

HY standard package

Payment rank:

Senior secured

Source: Company data, Bloomberg (19/02/2015), Berenberg FI Research

Investment thesis We see the strong market position and brand recognition as BUT’s key strengths. We also like the company’s multichannel

distribution strategy and its ability to gain market share. However, BUT has relatively weak operating margins which makes it

more vulnerable to a setback in consumer demand, especially given its high leverage. Moreover, credit metrics are likely to

remain under pressure due to future acquisitions, including a potential acquisition of 18 franchisee stores. As BUT has not

provided us with the latest financial information, we are not in the position to provide a recommendation on its notes.

DUFSCA 07/22

BUTSAS 09/19

HBMGR 02/20

MDMFP 08/20

-200

0

200

400

600

800

1,000

0 2 4 6 8 10

Z-s

pre

ad

(in

bp

s)

Time to worst

19/02/2015

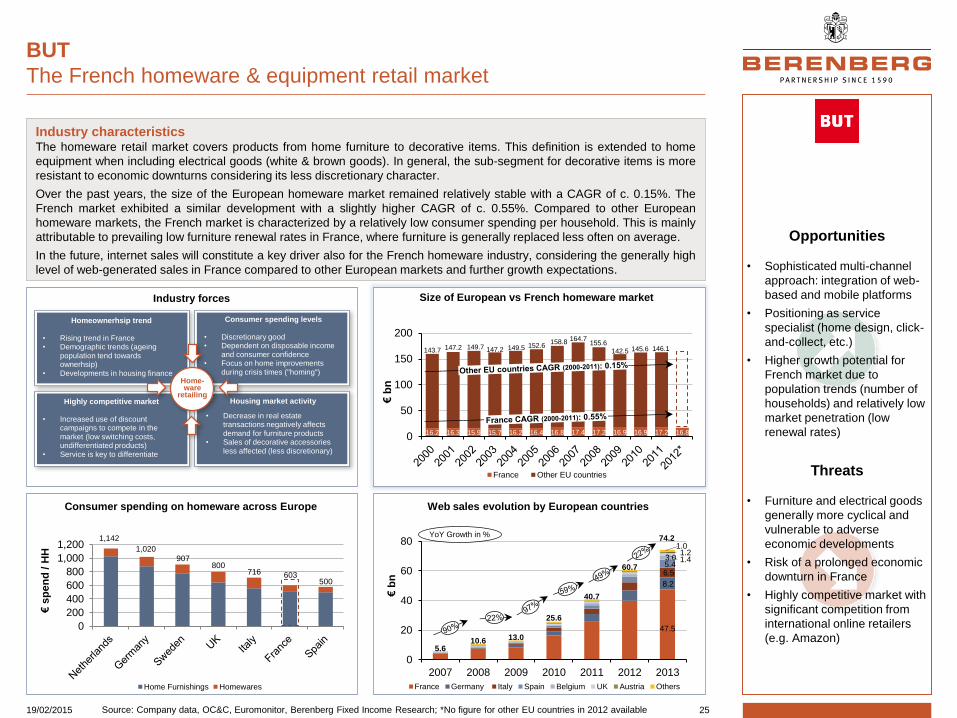

Opportunities

• Sophisticated multi-channel

approach: integration of web-

based and mobile platforms

• Positioning as service

specialist (home design, click-

and-collect, etc.)

• Higher growth potential for

French market due to

population trends (number of

households) and relatively low

market penetration (low

renewal rates)

Threats

• Furniture and electrical goods

generally more cyclical and

vulnerable to adverse

economic developments

• Risk of a prolonged economic

downturn in France

• Highly competitive market with

significant competition from

international online retailers

(e.g. Amazon)

Industry characteristics The homeware retail market covers products from home furniture to decorative items. This definition is extended to home

equipment when including electrical goods (white & brown goods). In general, the sub-segment for decorative items is more

resistant to economic downturns considering its less discretionary character.

Over the past years, the size of the European homeware market remained relatively stable with a CAGR of c. 0.15%. The

French market exhibited a similar development with a slightly higher CAGR of c. 0.55%. Compared to other European

homeware markets, the French market is characterized by a relatively low consumer spending per household. This is mainly

attributable to prevailing low furniture renewal rates in France, where furniture is generally replaced less often on average.

In the future, internet sales will constitute a key driver also for the French homeware industry, considering the generally high

level of web-generated sales in France compared to other European markets and further growth expectations.

0

10,000

20,000

30,000

-10%

0%

10%

20%

'02 '04 '06 '08 '10 '12 '14 '16

Shipping development

Demand (world container trade, Y/Y)Supply (containership fleet development, Y/Y)Aver. containership earnings* (rhs, USD/day)

Industry forces

BUT

The French homeware & equipment retail market

Size of European vs French homeware market

Consumer spending on homeware across Europe Web sales evolution by European countries

25 Source: Company data, OC&C, Euromonitor, Berenberg Fixed Income Research; *No figure for other EU countries in 2012 available

16.2 16.3 15.9 15.7 16.2 16.4 16.8 17.4 17.2 16.9 16.9 17.2 16.8

143.7 147.2 149.7 147.2 149.5 152.6158.8 164.7

155.6

142.5 145.6 146.1

0

50

100

150

200

€b

n

France Other EU countries

1,142

1,020

907800

716 603500

0

200

400

600

800

1,000

1,200

€s

pe

nd

/ H

H

Home Furnishings Homewares

5.610.6 13.0

25.6

40.7

60.7

74.2

1.21.43.0

5.46.5

8.2

47.5

1.0

0

20

40

60

80

2007 2008 2009 2010 2011 2012 2013

€b

n

France Germany Italy Spain Belgium UK Austria Others

YoY Growth in %

Highly competitive market

• Increased use of discount campaigns to compete in the market (low switching costs, undifferentiated products)

• Service is key to differentiate

Homeownerhsip trend

• Rising trend in France • Demographic trends (ageing

population tend towards ownerhsip)

• Developments in housing finance

Housing market activity

• Decrease in real estate transactions negatively affects demand for furniture products

• Sales of decorative accessories less affected (less discretionary)

Consumer spending levels

• Discretionary good• Dependent on disposable income

and consumer confidence• Focus on home improvements

during crisis times ("homing")Home-ware

retailing

19/02/2015

Berenberg

competitive scoring

Sensitivity to macro cycles

low / average / high

Regulatory risks

low / average / high

Scale & geographic

diversification

weak / average / strong

Competitive position

weak / average / strong

Financial policy

conservative / sound / aggressive

Distribution strategy

weak / average / strong

Brand awareness

low / average / high

Profitability

low / average / high

Revenue & cash flow volatility

low / average / high

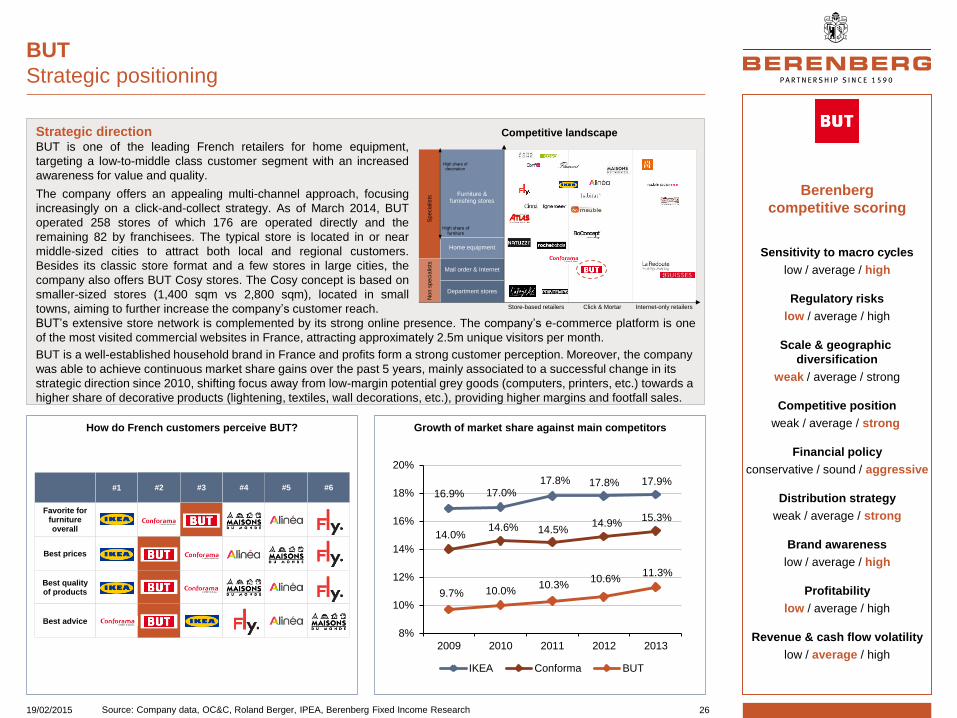

How do French customers perceive BUT?

BUT

Strategic positioning

Strategic direction BUT is one of the leading French retailers for home equipment,

targeting a low-to-middle class customer segment with an increased

awareness for value and quality.

The company offers an appealing multi-channel approach, focusing

increasingly on a click-and-collect strategy. As of March 2014, BUT

operated 258 stores of which 176 are operated directly and the

remaining 82 by franchisees. The typical store is located in or near

middle-sized cities to attract both local and regional customers.

Besides its classic store format and a few stores in large cities, the

company also offers BUT Cosy stores. The Cosy concept is based on

smaller-sized stores (1,400 sqm vs 2,800 sqm), located in small

towns, aiming to further increase the company’s customer reach.

BUT’s extensive store network is complemented by its strong online presence. The company’s e-commerce platform is one

of the most visited commercial websites in France, attracting approximately 2.5m unique visitors per month.

BUT is a well-established household brand in France and profits form a strong customer perception. Moreover, the company

was able to achieve continuous market share gains over the past 5 years, mainly associated to a successful change in its

strategic direction since 2010, shifting focus away from low-margin potential grey goods (computers, printers, etc.) towards a

higher share of decorative products (lightening, textiles, wall decorations, etc.), providing higher margins and footfall sales.

Competitive landscape

Growth of market share against main competitors

26 Source: Company data, OC&C, Roland Berger, IPEA, Berenberg Fixed Income Research

Click & MortarStore-based retailers Internet-only retailers

Mail order & Internet

Department stores

Home equipment

Furniture & furnishing stores

Sp

ecia

lists

No

n s

pe

cia

lists

High share of decoration

High share of furniture

16.9% 17.0%17.8% 17.8% 17.9%

14.0%14.6% 14.5%

14.9%15.3%

9.7% 10.0%10.3%

10.6%11.3%

8%

10%

12%

14%

16%

18%

20%

2009 2010 2011 2012 2013

IKEA Conforma BUT

Favorite for furniture overall

#5 #6#1 #2 #3 #4

Best prices

Best quality of products

Best advice

19/02/2015

Senior Secured Notes

BUTSAS 7⅜ 09/19

Issuer:

BUT S.A.S.

Guarantor(s):

Décomeubles Partners S.A.S,

BUT International,

Cogesem S.A.S.

Comments on Covenants

• Subsidiary guarantees from BUT

International and Cogesem

essentially useless unless/until

issue proceeds downstreamed

(French corporate law)

• Weak Change of Control clause

due to leverage-based portability

feature (immediate portability)

• LMT on Indebtedness provision

with aggressive features leaving

some immediate headroom i.a. for

ratio debt (higher-than-standard

FCCR at 2.25x BUT opening level

at 4.0x) and Credit Facilities

(c.€10m immediate headroom).

Moreover, material Permitted Debt

baskets (~€125m over all baskets)

in context of notes’ issue size

• Alarming LMT on Liens provision

with scope of Permitted Collateral

Liens allowing to secure additional

notes under any permitted debt

basket on collateral pari with initial

notes without CSSLR test (dilution

of initial noteholders)

• Risk of uncapped cash leakage

due to Restricted Payments

provision allowing unlimited

dividends if NLR ≤2.25x (just

below 2.5x opening level)

Capital structure*

Corporate structure

BUT

Focus on bond structure

Maturity profile

27 Source: Company data, Berenberg FI Research; *Based on pro forma figures **Based on LTM adj. EBITDA/R

Private Equity Consortium

Senior SecuredNotes

RCF

100%

Issuer of the Notes

Guarantors of the Notes

Fair Partners Sàrl-SCA(Luxembourg)

Décomeubles Partners SAS

(France)

Fair Finance Sàrl-SCA(Luxembourg)

Non-GuarantorSubsidiaries

BUT International(France)

Immobut SCI (France)

BUT SAS(France)

€ 180m

€ 30m

100%

100%

100%

99.9%Fair Finance Sàrl-SCA

(Luxembourg)

100%

0.1%

Cogesem SAS(France)

Non-GuarantorSubsidiaries

30

180

0

50

100

150

200

250

300

2014 2015 2016 2017 2018 2019

€m

RCF 11/18 Senior Secured Notes 09/19

€ m 3Q2014 xEBITDA/R Maturity

Cash & cash equivalents (54.0)*

Super senior secured RCF (€30m) - 11/2018

Senior Secured Notes 180.0 09/2019

Other debt 18.3

Net debt 144.3 2.5x**

Net debt (lease-adjusted) 657.1 5.4x**

19/02/2015

Ratings

Moody’s:

Corporate Family: B2

Senior Secured: B3

Outlook: Negative

Last update: 18/06/2014

S&P:

Corporate Family: B

Senior Secured: B

Outlook: Stable

Last update: 11/09/2014

Fitch:

Corporate Family: NR1

Senior Secured: NR1

Outlook: n.a.

Last update: n.a.

1 NR = Not rated

Rating pressure could arise from…

The rating agencies’ opinion*

BUT

The rating agencies’ view

Thresholds for rating pressure…

• Strong exposure to fragmented, competitive

French home equipment market (M/S&P)

• Exposure to discretionary spending with regard to

the furniture retail business (M/S&P)

• Weak current profitability levels (M/S&P)

• Highly leveraged (M/S&P)

• Inadequate liquidity for further acquisitions (M)

• Good position and growing market share in the

French home equipment market (M/S&P)

• Good brand recognition (M)

• Turnaround initiated in 2013 and expectation of

continuing improvements (S&P)

• Management initiatives (flexible pricing policy,

cost control, etc.) created positive operating

momentum (S&P)

• Financial policy remains commensurate (S&P)

• Sustainable FCF generation combined with a on-going

improvement of its market position (M/S&P)

• Unadj. FFO/Cash Interest in the high end of the 2.5x-

3.0x range (M)

• Adj. (Gross) Debt/EBITDA sustainably below 5.5x (M)

• Unable to restore sustainable levels of FOCF (S&P)

• More aggressive financial policy (S&P)

• Adj. leverage exceeding 5.0x or unadj. FFO/Cash

Interest below 2.0x on a long-term basis (S&P)

• Adj. (Gross) Debt/EBITDA remaining above 6.5x for

a prolonged period of time (M)

• Any weakening of the liquidity profile (M)

28 Source: Company data, Moody’s, S&P, Berenberg Fixed Income Research *M = Moody’s

S&P ‘15 forward view

(as of 27/03/2014)

Adj. Debt/EBITDA 3.7x

Threshold for downward rating pressure >5.0x

FFO/Cash Interest >2.0x

Threshold for upward rating pressure 2.5x-3.0x

Threshold for downward rating pressure <2.0x

Adjusted (Gross) Debt/EBITDA (Moody’s)

8.7x8.4x

6.4x

7.6x

4.0x

5.0x

6.0x

7.0x

8.0x

9.0x

2010 2011 2012 2013

Adj. (Gross) Debt/EBITDA

threshold for upward rating pressure

threshold for downward rating pressure

19/02/2015

Revenue & profitability

BUT

Summary of company figures

Adj. net debt/EBITDAR Adj. ÉBITDA interest cover

29 Source: Company data, Berenberg FI Research

7.3%

6.3%

3.9% 4.9%

0%

3%

6%

9%

0

400

800

1,200

2011 2012 2013 LTM3Q2014

€ m

Retail salesAdj. EBITDAAdj. EBITDA margin (rhs)

5.4x

4.4x

5.5x 5.4x

0.0x

1.5x

3.0x

4.5x

6.0x

7.5x

0

150

300

450

600

750

2011 2012 2013 LTM3Q2014

€ m

Adj. net debtAdj. EBITDARAdj. net debt/adj. EBITDAR (rhs)

3.9x

4.6x 4.9x

4.0x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

0

15

30

45

60

75

2011 2012 2013 LTM3Q2014

€ m

Adj. EBITDACash interest expensesAdj. EBITDA interest cover (rhs)

Selected profit & loss and cash flow financials (€ m)

€ m (FY ends 30 June) 2011 2012 2013 LTM 3Q14

Retail sales 972.0 1050.4 1104.9 1164.2

LFL growth -2.4% 3.5% -3.0% 0.1%

Gross profit 392.4 450.8 457.4 485.0

EBITDA 70.6 66.0 43.0 57.4

EBITDA Margin 7.3% 6.3% 3.9% 4.9%

Change in working capital 9.3 4.9 11.9 47.7

Capex -28.6 -33.9 -31.3 -24.8

Cash interest -17.9 -14.3 -8.8 -14.3

Cash taxes -0.2 -10.7 -8.3 -1.7

Free cash flow 33.2 12.0 6.5 64.3

Selected balance sheet financials, ratios and store network evolution

€ m (FY ends 30 June) 2011 2012 2013 LTM 3Q14

Store network (#) 213 217 228 258

Total assets 880.1 774.7 732.2 723.7

% o/w intangibles 17.2% 22.3% 25.0% 26.1%

Cash 38.5 58.9 77.9 54.0

FCF/Total debt 9.9% 7.0% 4.1% 32.4%

Debt/adj. EBITDA 4.8x 2.6x 3.7x 3.5x

Net debt/adj. EBITDA 4.2x 1.7x 1.9x 2.5x

Adj. debt/adj. EBITDAR 5.7x 4.9x 6.2x 5.9x

Adj. net Debt/adj. EBITDAR 5.4x 4.4x 5.5x 5.4x

Adj. EBITDA interest cover 3.9x 4.6x 4.9x 4.0x

19/02/2015

2. Company profiles

2.4 Dufry

Company data

Headquarter:

Basel (Switzerland)

Products:

Beauty products, alcohol,

confectionary & food, fashion &

jewellery, electronics, etc.

Major shareholders:

Family Dynasty Trust (22.2%)

Franklin Resources (5.1%)

Next financial release:

12/03/2015 (FY2014)

Bond data

Price / Z-spread / YTW:

107.3 / 258 / 2.7 (Pricing: 19/02/2015 BGN Close)

Callable (on and anytime after:)

15/07/2017 @ 103.375%

15/07/2018 @ 102.250%

15/07/2019 @ 101.125%

15/07/2020 @ 100.000%

Amount outstanding (€):

500m

Bond ratings:

Moody’s: Ba3 (stable)

S&P: BB+ (stable)

Fitch: BB (negative)

Covenants:

Covenant-lite package

Payment rank:

Senior unsecured

Dufry

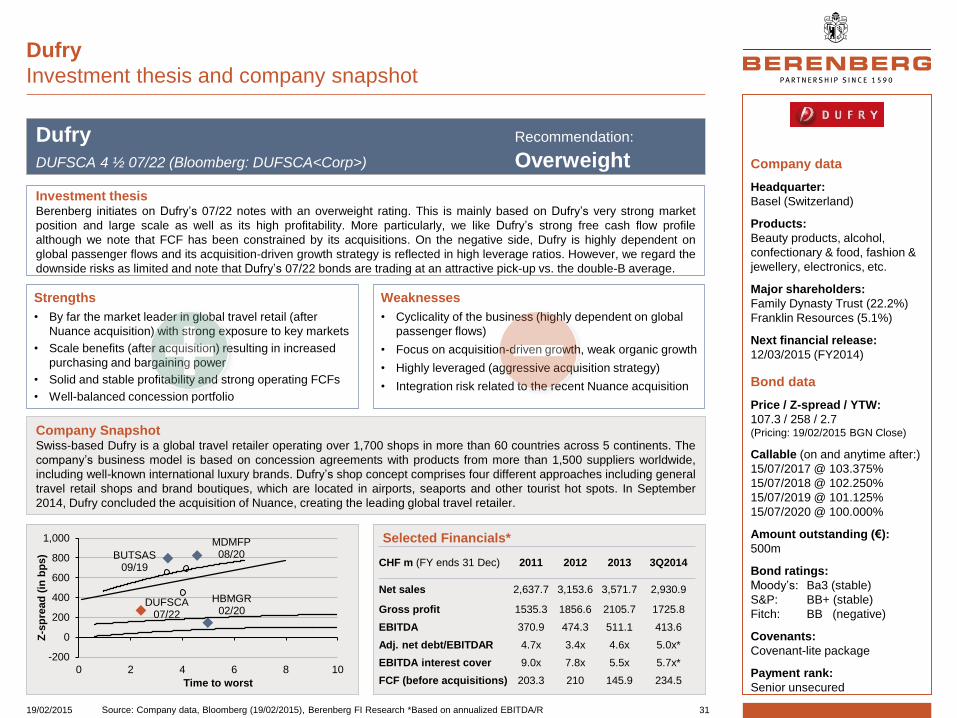

Investment thesis and company snapshot

Dufry Recommendation:

DUFSCA 4 ½ 07/22 (Bloomberg: DUFSCA<Corp>) Overweight

Weaknesses

• Cyclicality of the business (highly dependent on global

passenger flows)

• Focus on acquisition-driven growth, weak organic growth

• Highly leveraged (aggressive acquisition strategy)

• Integration risk related to the recent Nuance acquisition

Selected Financials*

Company Snapshot Swiss-based Dufry is a global travel retailer operating over 1,700 shops in more than 60 countries across 5 continents. The

company’s business model is based on concession agreements with products from more than 1,500 suppliers worldwide,

including well-known international luxury brands. Dufry’s shop concept comprises four different approaches including general

travel retail shops and brand boutiques, which are located in airports, seaports and other tourist hot spots. In September

2014, Dufry concluded the acquisition of Nuance, creating the leading global travel retailer.

Strengths

• By far the market leader in global travel retail (after

Nuance acquisition) with strong exposure to key markets

• Scale benefits (after acquisition) resulting in increased

purchasing and bargaining power

• Solid and stable profitability and strong operating FCFs

• Well-balanced concession portfolio

CHF m (FY ends 31 Dec) 2011 2012 2013 3Q2014

Net sales 2,637.7 3,153.6 3,571.7 2,930.9

Gross profit 1535.3 1856.6 2105.7 1725.8

EBITDA 370.9 474.3 511.1 413.6

Adj. net debt/EBITDAR 4.7x 3.4x 4.6x 5.0x*

EBITDA interest cover 9.0x 7.8x 5.5x 5.7x*

FCF (before acquisitions) 203.3 210 145.9 234.5

31 Source: Company data, Bloomberg (19/02/2015), Berenberg FI Research *Based on annualized EBITDA/R

Investment thesis Berenberg initiates on Dufry’s 07/22 notes with an overweight rating. This is mainly based on Dufry’s very strong market

position and large scale as well as its high profitability. More particularly, we like Dufry’s strong free cash flow profile

although we note that FCF has been constrained by its acquisitions. On the negative side, Dufry is highly dependent on

global passenger flows and its acquisition-driven growth strategy is reflected in high leverage ratios. However, we regard the

downside risks as limited and note that Dufry’s 07/22 bonds are trading at an attractive pick-up vs. the double-B average.

DUFSCA 07/22

BUTSAS 09/19

HBMGR 02/20

MDMFP 08/20

-200

0

200

400

600

800

1,000

0 2 4 6 8 10

Z-s

pre

ad

(in

bp

s)

Time to worst

19/02/2015

Opportunities

• Growth in global passenger

numbers

• Increasing international

tourism travel

• Increasing passenger traffic

from EM (particularly from

China, the world’s leading

market for luxury goods)

• Further market consolidation

in the medium to long term

Threats

• Increasing security and

product regulations (varying

by region)

• Growing political tensions and

terroristic acts negatively

impact passenger numbers

• Highly competitive,

fragmented market

(competition for concession

rights)

Industry characteristics According to Generation Research, the global retail travel market had an approximate size of $60bn in 2013. In general,

travel retailing primarily takes place at airports, seaports, and at international borders, whereby airport retailing constitutes

the largest sector in terms of sales. Within the industry it can be distinguished between duty-free shops, targeted towards

international travellers, and duty-paid shops, focused on domestic costumers, both offering primarily brand products.

The global travel retail market is highly fragmented with the top 10 players holding roughly 55% of the market in 2013, which

indicates further potential for market consolidation, particularly after Dufry’s recent acquisition of Nuance.

In terms of growth drivers, the industry is profiting from steadily increasing passenger numbers, predicted to grow at a CAGR

of c. 4.1% until 2031. In this context, Europe currently represents the major market, followed by North America and the

Asia/Pacific region. However, the Asia/Pacific and ME/Africa regions offer the greatest growth potential in the medium term.

0

10,000

20,000

30,000

-10%

0%

10%

20%

'02 '04 '06 '08 '10 '12 '14 '16

Shipping development

Demand (world container trade, Y/Y)Supply (containership fleet development, Y/Y)Aver. containership earnings* (rhs, USD/day)

Industry forces

Dufry

The global travel retail industry

Regional distribution of global passenger travel (2013) Long term global passenger forecast (2012)

Market share by sales of key airport retailers (2013)

32 Source: Company data, Generation Research, ACI-DKMA, Verdict Research, Berenberg Fixed Income Research

~15%

8.0%6.2% 5.7% 5.4% 5.3% 4.8% 4.5% 3.8%

2.6% 1.9%

9.5%

0%

5%

10%

15%

20%

0

2

4

6

8

10

12

14

bn

pa

ss

en

ge

rs

Force majeure

• Regional travel impacted by certain events (e.g. political turmoil, epidemics, forces of nature etc.)

Increasing global passenger travel

• Increasing world population and tourism trends

• Growth opps in emerging markets• Improvements in air transport

(greater accessibility, affordability)

Regulatory environment

• Increasing security procedures at airports

• Regulations on transportation of liquids and hand baggage

Need to adapt product offering

• Low-cost carriers gaining ground• Increasing number of "budget"

passengers• Need to adapt offering for cheaper

products

Travelretailing

30%

8%

7% 27%

28%

Europe

Latin America

Middle East/Africa

Asia/Pacific

North America

19/02/2015

Berenberg

competitive scoring

Sensitivity to macro cycles

low / average / high

Regulatory risks

low / average / high

Scale & geographic

diversification

weak / average / strong

Competitive position

weak / average / strong

Financial policy

conservative / sound / aggressive

Distribution strategy

weak / average / strong

Brand awareness

low / average / high

Profitability

low / average / high

Revenue & cash flow volatility

low / average / high

Sales by remaining term of concession portfolio (2013)

Dufry

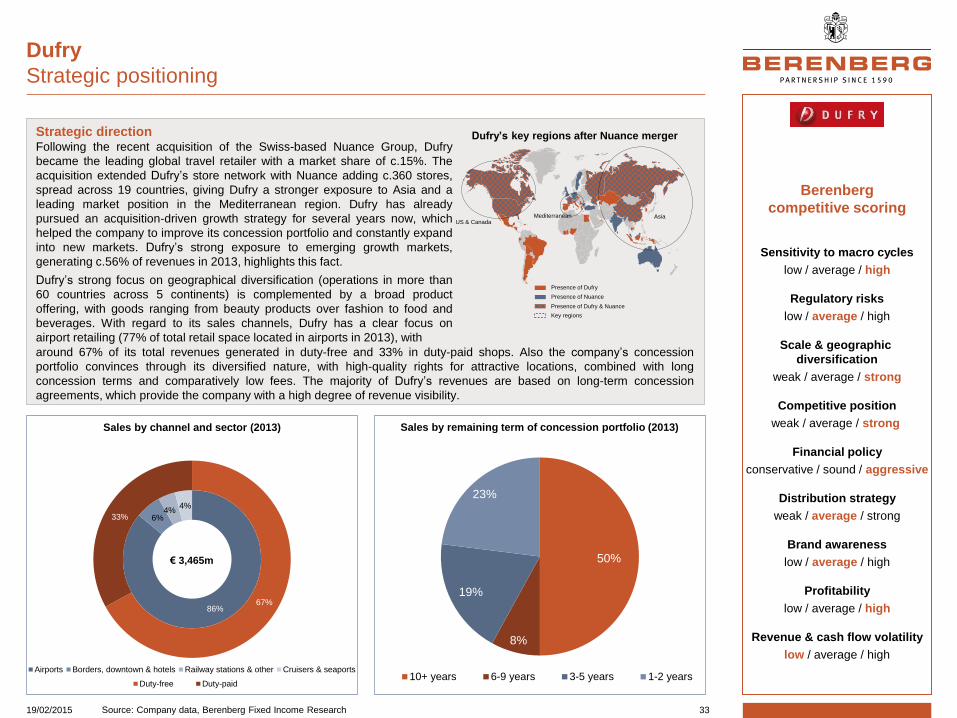

Strategic positioning

Strategic direction Following the recent acquisition of the Swiss-based Nuance Group, Dufry

became the leading global travel retailer with a market share of c.15%. The

acquisition extended Dufry’s store network with Nuance adding c.360 stores,

spread across 19 countries, giving Dufry a stronger exposure to Asia and a

leading market position in the Mediterranean region. Dufry has already

pursued an acquisition-driven growth strategy for several years now, which

helped the company to improve its concession portfolio and constantly expand

into new markets. Dufry’s strong exposure to emerging growth markets,

generating c.56% of revenues in 2013, highlights this fact.

Dufry’s strong focus on geographical diversification (operations in more than

60 countries across 5 continents) is complemented by a broad product

offering, with goods ranging from beauty products over fashion to food and

beverages. With regard to its sales channels, Dufry has a clear focus on

airport retailing (77% of total retail space located in airports in 2013), with

around 67% of its total revenues generated in duty-free and 33% in duty-paid shops. Also the company’s concession

portfolio convinces through its diversified nature, with high-quality rights for attractive locations, combined with long

concession terms and comparatively low fees. The majority of Dufry’s revenues are based on long-term concession

agreements, which provide the company with a high degree of revenue visibility.

Dufry’s key regions after Nuance merger

33 Source: Company data, Berenberg Fixed Income Research

Duty-free Duty-paid

86%

6%4%

4%

67%

33%

Airports Borders, downtown & hotels Railway stations & other Cruisers & seaports

€ 3,465m

Sales by channel and sector (2013)

50%

8%

19%

23%

10+ years 6-9 years 3-5 years 1-2 years

Presence of Dufry

Presence of Nuance

Presence of Dufry & Nuance

US & CanadaAsiaMediterranean

Key regions

19/02/2015

Senior Unsecured Notes DUFSCA 4½ 07/22

Issuer:

Dufry Finance SCA

Guarantor(s):

Dufry AG &

Dufry International AG &

Dufry Holdings/Investments AG &

Hudson Group Inc. &

Dufry Financial Services B.V.

Comments on Covenants

• Covenant-lite package (Asset

Sales, Affiliate Transactions &

Anti-Layering provisions missing)

• Subsidiary guarantees may cease

to apply before final redemption

(upon guarantee of new CF and

notes maturing 2019 and 2020)

• Fall-Away provision does not

require reinstallation of covenants

after IG is subsequently lost again

• Weak LMT on Indebtedness

provisions (i.a. credit facility

≤CHF900m+ $1,010m +€500m;

debt basket ≤ $125m/11% NTA)

• Weak LMT on Liens allowing to

secure substantial amounts of

additional debt without notes

having to be equally secured over

such assets

• Weak Restricted Payments

provision allows very generous

Permitted Investments and has

various generous carve-outs (i.a.

general RP basket >$200m & 22%

of con. NTA; basket for unlimit.

payments (divid., subord. oblig.) if

con. Total Leverage ratio ≤3.25x)

• No requirement for Nuance to

guarantee notes after acquisition

Capital structure

Corporate structure

Dufry

Focus on bond structure

Maturity profile

34 Source: Company data, Berenberg FI Research;

Senior UnsecuredNotes (due 2020)

RCF

Issuer of the Notes

Guarantors of the Notes

Dufry AG

Dufry Holdings & Investments AG

Dufry Finance SCAHudson Group (HG)

Inc.Dufry Financial Services B.V.

Dufry International AG

The Nuance Group AG

Non-guarantorsubsidiaries

Senior UnsecuredNotes (due 2022)

CHF m 3Q2014 xEBITDA/R Maturity

Cash & cash equivalents (798)

USD term loan ($1,010m) 896

EUR term loan (€500m) 607.5

EUR syndicated CF (€250m) 301.7 2019

RCF (CHF900m) and other 124.4 2019

Senior unsecured notes ($500m) 442.1 10/2020

Senior unsecured notes (€500m) 607.5 07/2022

Net debt 2,181.2 n.m.

Net debt (lease-adj.) 3,399.9 n.m.

900.0

1503.5

301.7

442.1 607.5

0

500

1,000

1,500

2,000

2,500

3,000

CH

F m

RCF 2019 Term Loan 2019 (EUR+USD)

Syndicated facility 2019 Senior Notes 10/20 (USD)

Senior Notes 07/22 (EUR)

19/02/2015

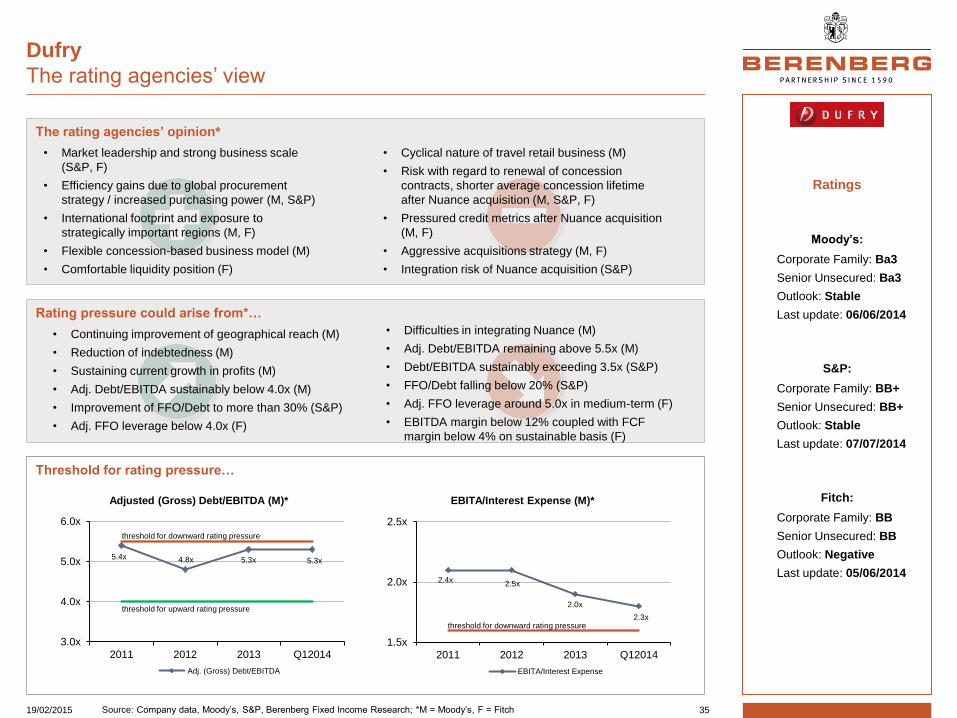

Ratings

Moody’s:

Corporate Family: Ba3

Senior Unsecured: Ba3

Outlook: Stable

Last update: 06/06/2014

S&P:

Corporate Family: BB+

Senior Unsecured: BB+

Outlook: Stable

Last update: 07/07/2014

Fitch:

Corporate Family: BB

Senior Unsecured: BB

Outlook: Negative

Last update: 05/06/2014

The rating agencies’ opinion*

Dufry

The rating agencies’ view

Threshold for rating pressure…

Rating pressure could arise from*…

• Cyclical nature of travel retail business (M)

• Risk with regard to renewal of concession

contracts, shorter average concession lifetime

after Nuance acquisition (M, S&P, F)

• Pressured credit metrics after Nuance acquisition

(M, F)

• Aggressive acquisitions strategy (M, F)

• Integration risk of Nuance acquisition (S&P)

• Market leadership and strong business scale

(S&P, F)

• Efficiency gains due to global procurement

strategy / increased purchasing power (M, S&P)

• International footprint and exposure to

strategically important regions (M, F)

• Flexible concession-based business model (M)

• Comfortable liquidity position (F)

• Difficulties in integrating Nuance (M)

• Adj. Debt/EBITDA remaining above 5.5x (M)

• Debt/EBITDA sustainably exceeding 3.5x (S&P)

• FFO/Debt falling below 20% (S&P)

• Adj. FFO leverage around 5.0x in medium-term (F)

• EBITDA margin below 12% coupled with FCF

margin below 4% on sustainable basis (F)

• Continuing improvement of geographical reach (M)

• Reduction of indebtedness (M)

• Sustaining current growth in profits (M)

• Adj. Debt/EBITDA sustainably below 4.0x (M)

• Improvement of FFO/Debt to more than 30% (S&P)

• Adj. FFO leverage below 4.0x (F)

Adjusted (Gross) Debt/EBITDA (M)* EBITA/Interest Expense (M)*

35 Source: Company data, Moody’s, S&P, Berenberg Fixed Income Research; *M = Moody’s, F = Fitch

5.4x 4.8x 5.3x 5.3x

3.0x

4.0x

5.0x

6.0x

2011 2012 2013 Q12014

Adj. (Gross) Debt/EBITDA

threshold for upward rating pressure

threshold for downward rating pressure

2.4x2.5x

2.0x

2.3x

1.5x

2.0x

2.5x

2011 2012 2013 Q12014

EBITA/Interest Expense

threshold for downward rating pressure

19/02/2015

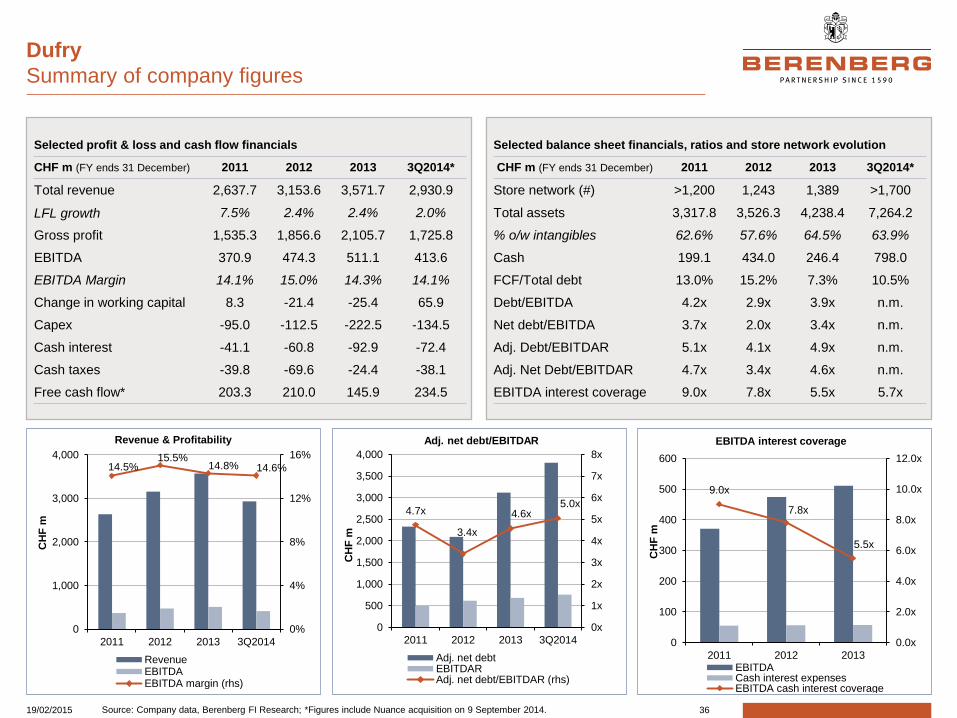

Dufry

Summary of company figures

Revenue & Profitability Adj. net debt/EBITDAR EBITDA interest coverage

36 Source: Company data, Berenberg FI Research; *Figures include Nuance acquisition on 9 September 2014.

14.5% 15.5%

14.8% 14.6%

0%

4%

8%

12%

16%

0

1,000

2,000

3,000

4,000

2011 2012 2013 3Q2014

CH

F m

RevenueEBITDAEBITDA margin (rhs)

4.7x

3.4x

4.6x 5.0x

0x

1x

2x

3x

4x

5x

6x

7x

8x

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2011 2012 2013 3Q2014

CH

F m

Adj. net debtEBITDARAdj. net debt/EBITDAR (rhs)

Selected profit & loss and cash flow financials

CHF m (FY ends 31 December) 2011 2012 2013 3Q2014*

Total revenue 2,637.7 3,153.6 3,571.7 2,930.9

LFL growth 7.5% 2.4% 2.4% 2.0%

Gross profit 1,535.3 1,856.6 2,105.7 1,725.8

EBITDA 370.9 474.3 511.1 413.6

EBITDA Margin 14.1% 15.0% 14.3% 14.1%

Change in working capital 8.3 -21.4 -25.4 65.9

Capex -95.0 -112.5 -222.5 -134.5

Cash interest -41.1 -60.8 -92.9 -72.4

Cash taxes -39.8 -69.6 -24.4 -38.1

Free cash flow* 203.3 210.0 145.9 234.5

Selected balance sheet financials, ratios and store network evolution

CHF m (FY ends 31 December) 2011 2012 2013 3Q2014*

Store network (#) >1,200 1,243 1,389 >1,700

Total assets 3,317.8 3,526.3 4,238.4 7,264.2

% o/w intangibles 62.6% 57.6% 64.5% 63.9%

Cash 199.1 434.0 246.4 798.0

FCF/Total debt 13.0% 15.2% 7.3% 10.5%

Debt/EBITDA 4.2x 2.9x 3.9x n.m.

Net debt/EBITDA 3.7x 2.0x 3.4x n.m.

Adj. Debt/EBITDAR 5.1x 4.1x 4.9x n.m.

Adj. Net Debt/EBITDAR 4.7x 3.4x 4.6x n.m.

EBITDA interest coverage 9.0x 7.8x 5.5x 5.7x

9.0x

7.8x

5.5x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

0

100

200

300

400

500

600

2011 2012 2013C

HF

m

EBITDACash interest expensesEBITDA cash interest coverage

19/02/2015

3. Appendix: Macroeconomic environment

Macro driver #1: Economic growth (I)

Close link between development of retail sales and GDP

Retail sales growth is

strongly correlated with

overall economic growth.

Eurozone retail sales have

showed stronger growth

than GDP since end of

October 2013, particularly