Embed Size (px)

Citation preview

March 26, 2018

Fiscal Policy Challenges in a Slow Growth Environment

Cepal

2

Summary

1. External Sector and Monetary Policy

2. Fiscal Policy: Achievements and Challenges

3. Structural Reforms

Results

1

2

3

4

3

1. External Sector

Source: IBGE, Central Bank of Brazil

1Resumption of world trade growth along with the recovery of commodity prices since 2016 created a positive background for Brazilian exports. As a result, current account is almost balanced. There is also a comfortable inflation outlook, credit to households reflecting monetary easing

4

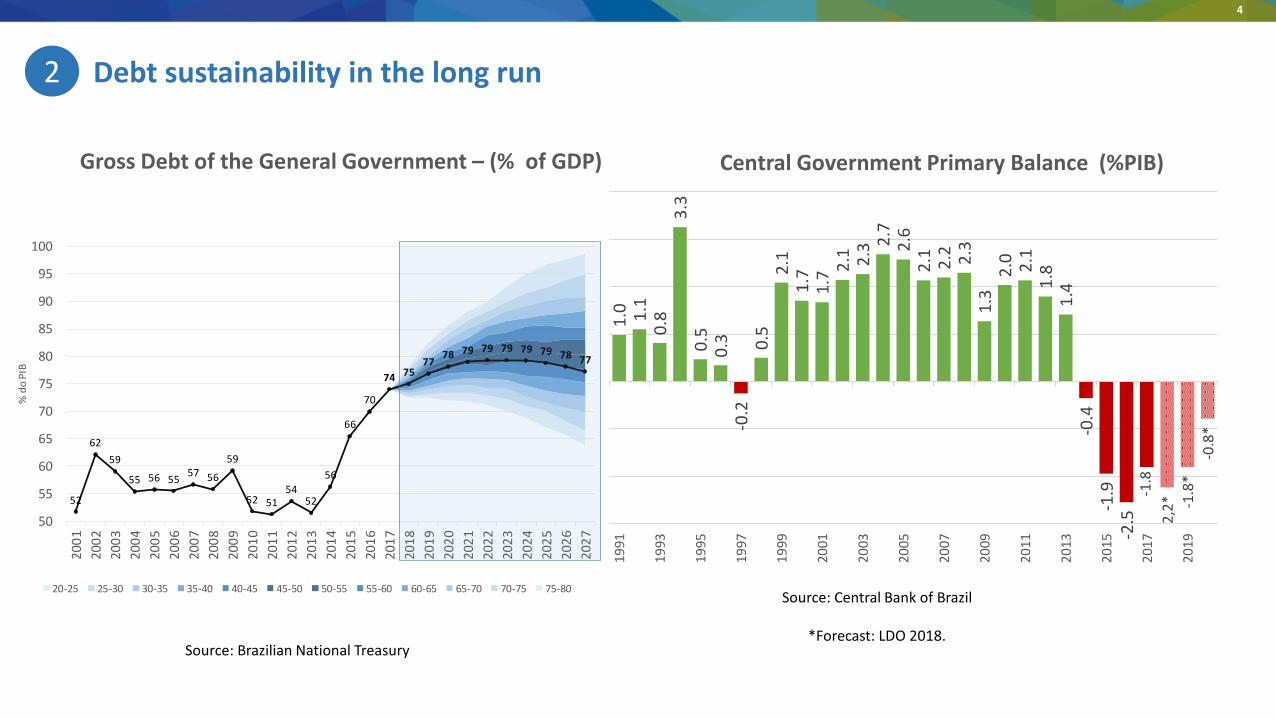

1. Debt sustainability in the long run

Source: Brazilian National Treasury

Gross Debt of the General Government – (% of GDP)

2

Source: Central Bank of Brazil

*Forecast: LDO 2018.

Central Government Primary Balance (%PIB)

1.0 1.1

0.8

3.3

0.5

0.3

-0.2

0.5

2.1

1.7

1.7

2.1 2.3

2.7

2.6

2.1 2.2 2.3

1.3

2.0 2.1

1.8

1.4

-0.4

-1.9

-2.5

-1.8

2,2

* -1.8

*

-0.8

*

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17

20

19

52

62

59

55 56 5557 56

59

52 5154

52

56

66

70

74 7577

78 79 79 79 79 79 78 77

50

55

60

65

70

75

80

85

90

95

100

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

202

3

202

4

202

5

202

6

202

7

% d

o P

IB

20-25 25-30 30-35 35-40 40-45 45-50 50-55 55-60 60-65 65-70 70-75 75-80

5

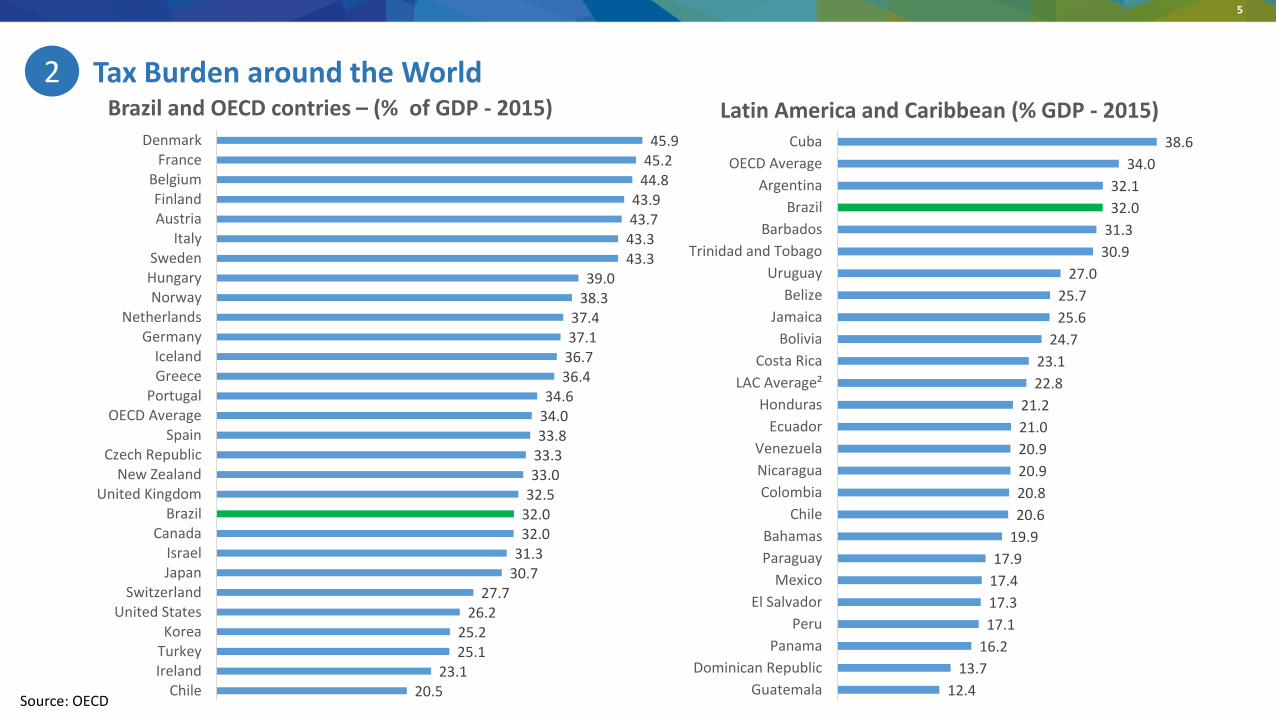

1. Tax Burden around the World

Source: OECD

Brazil and OECD contries – (% of GDP - 2015)

2Latin America and Caribbean (% GDP - 2015)

20.523.1

25.125.2

26.227.7

30.731.332.032.032.533.033.333.834.034.6

36.436.737.137.4

38.339.0

43.343.343.743.9

44.845.245.9

ChileIrelandTurkeyKorea

United StatesSwitzerland

JapanIsrael

CanadaBrazil

United KingdomNew Zealand

Czech RepublicSpain

OECD AveragePortugal

GreeceIceland

GermanyNetherlands

NorwayHungarySweden

ItalyAustriaFinland

BelgiumFrance

Denmark

12.4

13.7

16.2

17.1

17.3

17.4

17.9

19.9

20.6

20.8

20.9

20.9

21.0

21.2

22.8

23.1

24.7

25.6

25.7

27.0

30.9

31.3

32.0

32.1

34.0

38.6

Guatemala

Dominican Republic

Panama

Peru

El Salvador

Mexico

Paraguay

Bahamas

Chile

Colombia

Nicaragua

Venezuela

Ecuador

Honduras

LAC Average²

Costa Rica

Bolivia

Jamaica

Belize

Uruguay

Trinidad and Tobago

Barbados

Brazil

Argentina

OECD Average

Cuba

6

1 Cenário Macroeconômico

Fonte: STN

Forecast of Primary Spending with and without theSpending Cap Rule (% of GDP)

With the spending ceiling cap, the recover ofrevenues will be automatically channeled tostabilize public debt

Pension Outlays and BPC/LOAS (% of GDP)

Lower outlays, especially in the long run, requiresignificant structural reforms.

18,9%

0%

5%

10%

15%

20%

25%

19

97

20

00

20

03

20

06

20

09

20

12

20

15

20

18

20

21

20

24

20

27

20

30

20

33

20

36

20

39

20

42

20

45

20

48

20

51

20

54

20

57

20

60

Cenário Atual

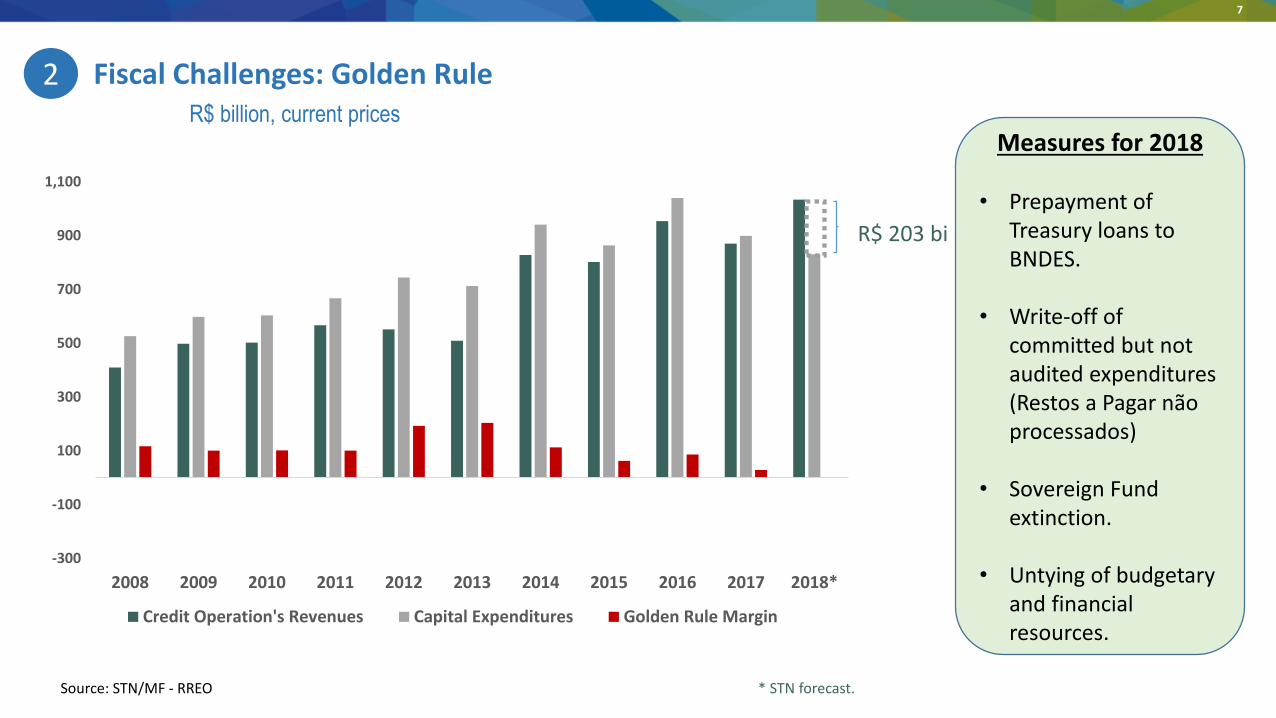

1. Fiscal Discipline in the long run: what do we need to achieve?

24,9 %

15,0 %

18,9 %

2

Current Scenario

19,4 %

7

-300

-100

100

300

500

700

900

1,100

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018*

Credit Operation's Revenues Capital Expenditures Golden Rule Margin

1. Fiscal Challenges: Golden Rule

Source: STN/MF - RREO

R$ billion, current prices

2

R$ 203 bi

* STN forecast.

Measures for 2018

• Prepayment ofTreasury loans toBNDES.

• Write-off ofcommitted but notaudited expenditures(Restos a Pagar não processados)

• Sovereign Fundextinction.

• Untying of budgetaryand financial resources.

8

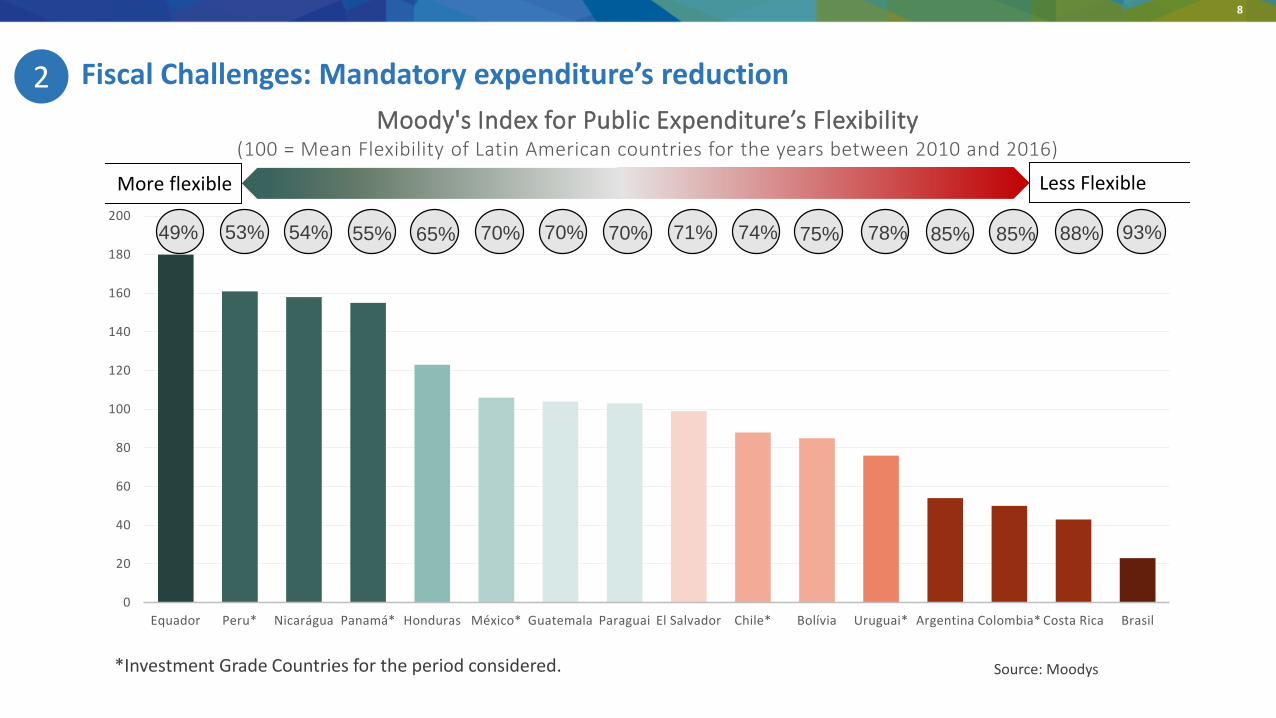

1. Fiscal Challenges: Mandatory expenditure’s reduction2

0

20

40

60

80

100

120

140

160

180

200

Equador Peru* Nicarágua Panamá* Honduras México* Guatemala Paraguai El Salvador Chile* Bolívia Uruguai* Argentina Colombia* Costa Rica Brasil

Moody's Index for Public Expenditure’s Flexibility(100 = Mean Flexibility of Latin American countries for the years between 2010 and 2016)

More flexible Less Flexible

49% 53% 54% 55% 65% 70% 70% 70% 71% 74% 75% 78% 85% 85% 88% 93%

*Investment Grade Countries for the period considered. Source: Moodys

9

• Annual Borrowing Plan

• Federal Government General Balance

• Fiscal Risks Annex

• National Treasury Accounting Report –An analysis of the assets and liabilitiesof the Federal Government

8

4 4

3

55

6

1

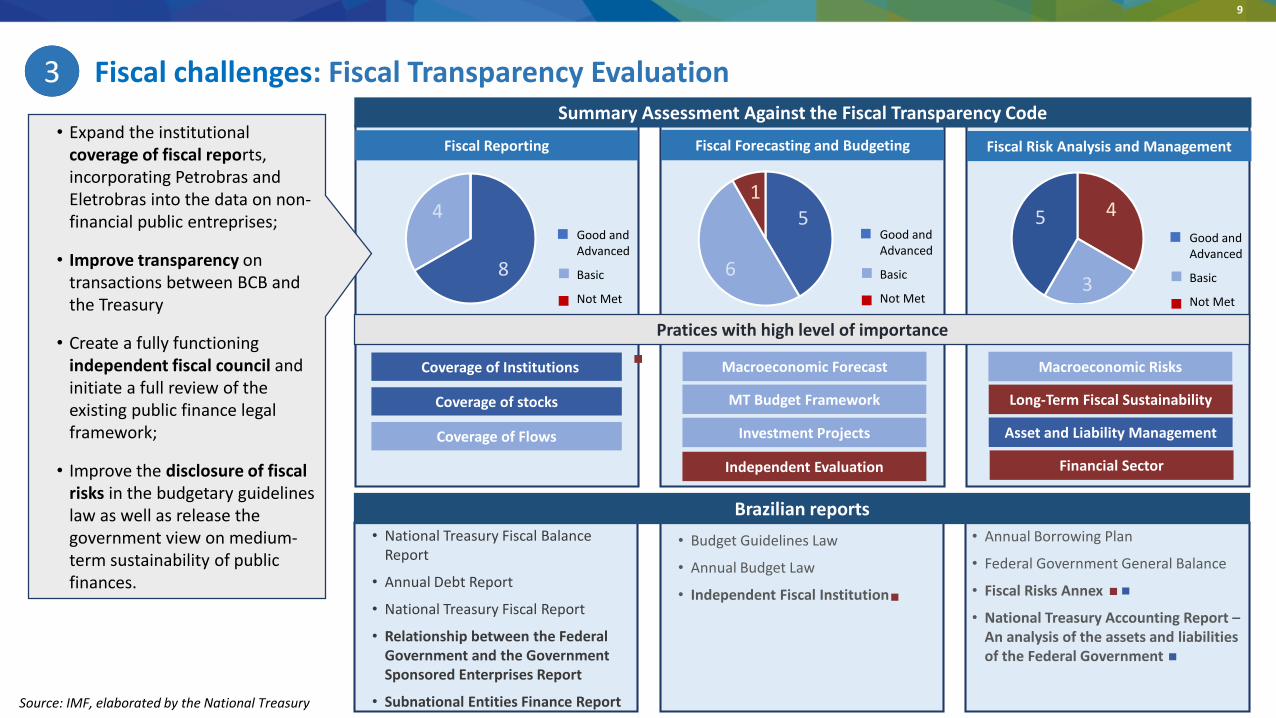

1. Fiscal challenges: Fiscal Transparency Evaluation13

Coverage of Institutions

Coverage of stocks

Coverage of Flows

Macroeconomic Forecast

MT Budget Framework

Investment Projects

Independent Evaluation

Macroeconomic Risks

Long-Term Fiscal Sustainability

Asset and Liability Management

Financial Sector

Source: IMF, elaborated by the National Treasury

Summary Assessment Against the Fiscal Transparency Code

Pratices with high level of importance

Fiscal Reporting Fiscal Forecasting and Budgeting Fiscal Risk Analysis and Management

Brazilian reports

• National Treasury Fiscal Balance Report

• Annual Debt Report

• National Treasury Fiscal Report

• Relationship between the Federal Government and the GovernmentSponsored Enterprises Report

• Subnational Entities Finance Report

• Expand the institutional coverage of fiscal reports, incorporating Petrobras and Eletrobras into the data on non-financial public entreprises;

• Improve transparency ontransactions between BCB andthe Treasury

• Create a fully functioning independent fiscal council and initiate a full review of the existing public finance legal framework;

• Improve the disclosure of fiscal risks in the budgetary guidelines law as well as release the government view on medium-term sustainability of public finances.

Good andAdvanced

Basic

Not Met

• Budget Guidelines Law

• Annual Budget Law

• Independent Fiscal Institution

Good andAdvanced

Basic

Not Met

Good andAdvanced

Basic

Not Met

10

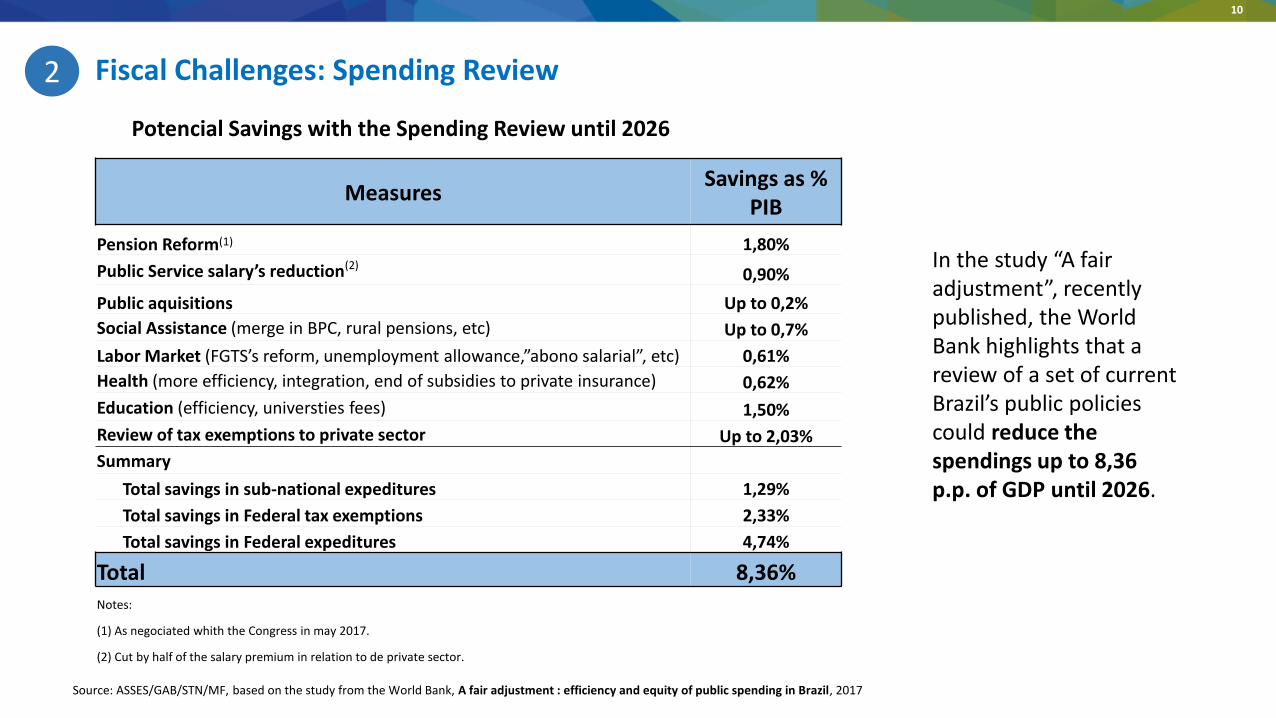

1. Fiscal Challenges: Spending Review2

Source: ASSES/GAB/STN/MF, based on the study from the World Bank, A fair adjustment : efficiency and equity of public spending in Brazil, 2017

MeasuresSavings as %

PIB

Pension Reform(1) 1,80%

Public Service salary’s reduction(2)0,90%

Public aquisitions Up to 0,2%

Social Assistance (merge in BPC, rural pensions, etc) Up to 0,7%

Labor Market (FGTS’s reform, unemployment allowance,”abono salarial”, etc) 0,61%

Health (more efficiency, integration, end of subsidies to private insurance) 0,62%

Education (efficiency, universties fees) 1,50%

Review of tax exemptions to private sector Up to 2,03%

Summary

Total savings in sub-national expeditures 1,29%

Total savings in Federal tax exemptions 2,33%

Total savings in Federal expeditures 4,74%

Total 8,36%Notes:

(1) As negociated whith the Congress in may 2017.

(2) Cut by half of the salary premium in relation to de private sector.

In the study “A fair adjustment”, recentlypublished, the World Bank highlights that a review of a set of currentBrazil’s public policies could reduce thespendings up to 8,36 p.p. of GDP until 2026.

Potencial Savings with the Spending Review until 2026

11

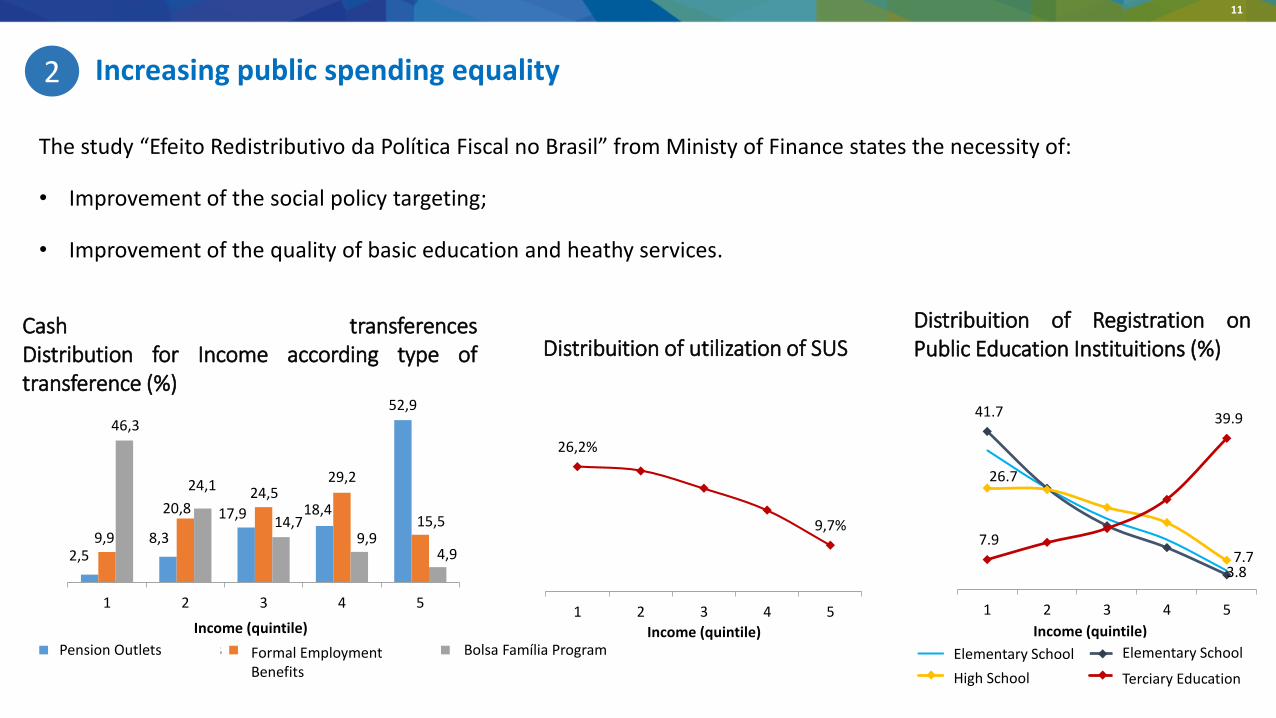

1. Increasing public spending equality2

The study “Efeito Redistributivo da Política Fiscal no Brasil” from Ministy of Finance states the necessity of:

• Improvement of the social policy targeting;

• Improvement of the quality of basic education and heathy services.

Distribuition of utilization of SUS

26,2%

9,7%

1 2 3 4 5

Income (quintile)

Cash transferencesDistribution for Income according type oftransference (%)

2,58,3

17,9 18,4

52,9

9,9

20,824,5

29,2

15,5

46,3

24,1

14,79,9

4,9

1 2 3 4 5

Income (quintile)

Aposentadorias e pensões Benefícios do trabalho formal PBF

Distribuition of Registration onPublic Education Instituitions (%)

41.7

3.8

26.7

7.7 7.9

39.9

1 2 3 4 5

Income (quintile)

Educação infantil Ensino fundamental

Ensino médio Ensino superior

Pension Outlets Formal EmploymentBenefits

Bolsa Família Program

High School

Elementary School Elementary School

Terciary Education

12

1. Improvements in Fiscal Institutions in Brazil

Economic Policy Secretariat and National Treasury´s Tutorial for calculating of the“Golden Rule” : http://www.spe.fazenda.gov.br/prisma-fiscal/arquivos/tutorial-regra-de-ouro-despesas-de-capital-e-operacoes-de-credito_final.pdfBulletin on Finances of Subnational Governments: http://www.tesouro.fazenda.gov.br/-/tesouro-nacional-lanca-boletim-de-financas-publicas-de-estados-e-municipiosResults of the National Treasury’s Report with a box explaning “Golden Rule”: http://www.tesouro.fazenda.gov.br/web/stn/-/historico-resultado-do-tesouro-nacional

12

Golden RuleSpending CapImproving Fiscal Responsibility Law

Limits the growth of public spending toinflation for, at least, the next 20 years

Creates stable and predictable rule for federal expenditure

Forces priorization of public policies

Brings importance for the Social Security reform and spending review

Incentives public policies evaluation andspending review.

Limits the federal indebtedness: CreditOperation revenues can´t exceedCapital Expediture

Intergerational alingment of theindebedtedness process

Improvement is needed to create a convergence with the Spending Caprule.

Introduction of Matrix of AccountingBalances:• Instrument for standardization of

the subnational governments’ fiscal statistics

New governance on the Federal Goverment Guarantee’s systematics

New governance for subnationalgovernment’s indebtedness

13

Microeconomic reforms are creating a business-friendly environment3

Economic Policy Strategy

EfficientAllocation

Legal security

Credit andinterest rates

Foreigntrade

• New Oil Policy (approved);• Redesim - National Network

for Simplification of Registration and Legalization of Businesses (in-progress);

• Public Accounting System(SPED) for Brazilian States (in-progress);

• Single Window for ForeignTrade (in-progress);

• Positive registration(in progress);

• Long Term Rate - TLP (approved)

• Secured Real Estate Bills – LIG (approved)

• ProductiveMicrocredit(approved)

• New Migration Law (approved)

• New Local Content Policy (approved)

• Aviation market opening (in progress)

• Acquisition of land by foreigners (in progress)

• Privatization(in progress);

• Concessions(in progress);

• Governance of state-owned enterprises (approved).

• Judicial Recovery and Bankruptcy Law (Bill ready to send to Congress);

• Changes in the regulatory framework of the electric energy sector (in progress);

• Changes in the regulatory framework of the oil sector (approved);

• electronic registration of liens and encumbrances (approved);

Outcomes: Increased productivity, fiscal adjustment, transparency and lower bureaucracy

Business Environment

14

Governance of state-owned enterprises (Law nº 13.303, June 30, 2016)3

*ExpectedSource: B3, Broadcast

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

40

2012 2013 2014 2015 2016 2017*

BR

L b

illio

n

Net Profit or Loss of State-Owned Enterprises

Financial Non-financial

0

5

10

15

20

25

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Ap

r-1

7

Jul-

17

Oct

-17

Jan

-18

BR

L

Petrobras and Eletrobras´ shares

Elet4 Petr3

15

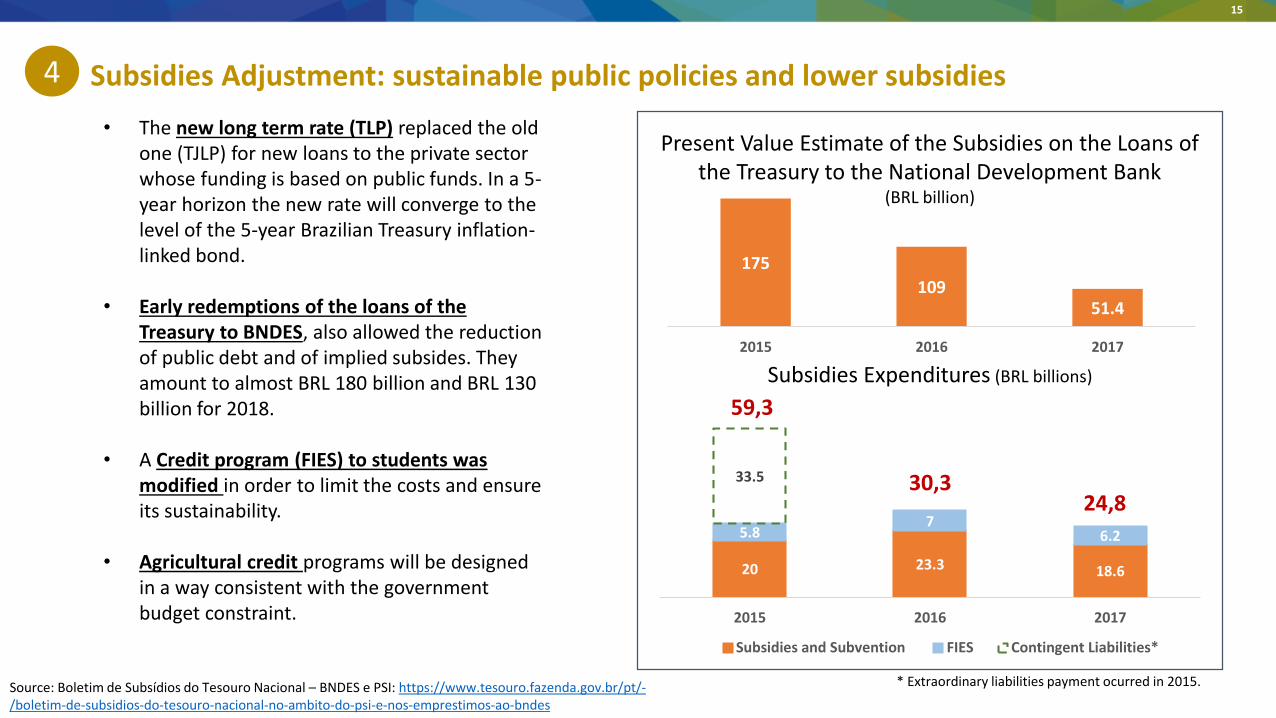

* Extraordinary liabilities payment ocurred in 2015.

20 23.3 18.6

5.87

6.2

33.5

2015 2016 2017

Subsidies and Subvention FIES Contingent Liabilities*

Source: Boletim de Subsídios do Tesouro Nacional – BNDES e PSI: https://www.tesouro.fazenda.gov.br/pt/-/boletim-de-subsidios-do-tesouro-nacional-no-ambito-do-psi-e-nos-emprestimos-ao-bndes

• The new long term rate (TLP) replaced the old one (TJLP) for new loans to the private sector whose funding is based on public funds. In a 5-year horizon the new rate will converge to the level of the 5-year Brazilian Treasury inflation-linked bond.

• Early redemptions of the loans of the Treasury to BNDES, also allowed the reduction of public debt and of implied subsides. They amount to almost BRL 180 billion and BRL 130 billion for 2018.

• A Credit program (FIES) to students was modified in order to limit the costs and ensure its sustainability.

• Agricultural credit programs will be designed in a way consistent with the government budget constraint.

1. Subsidies Adjustment: sustainable public policies and lower subsidies4

Subsidies Expenditures (BRL billions)

Present Value Estimate of the Subsidies on the Loans of the Treasury to the National Development Bank

(BRL billion)

175

10951.4

2015 2016 2017

59,3

30,324,8

16

1. Credit at market interest rates increasing again, public banks scaling back3

Source: Central Bank of Brazil

30.0%

35.0%

40.0%

45.0%

50.0%

55.0%

60.0%

65.0%

70.0%

Jan

-03

Oct

-03

Jul-

04

Ap

r-0

5

Jan

-06

Oct

-06

Jul-

07

Ap

r-0

8

Jan

-09

Oct

-09

Jul-

10

Ap

r-1

1

Jan

-12

Oct

-12

Jul-

13

Ap

r-1

4

Jan

-15

Oct

-15

Jul-

16

Ap

r-1

7

Jan

-18

Outstanding Credit by Ownership Type

Public Private

17

Brazil: aiming a greater international integration of the economy3

Internationalization of the Brazilian economy

Brazil effective member of the

Paris Club

OECD membership

(In progress)

G20/BRICS member

Trade negotiation

with EU

(in progress)

18

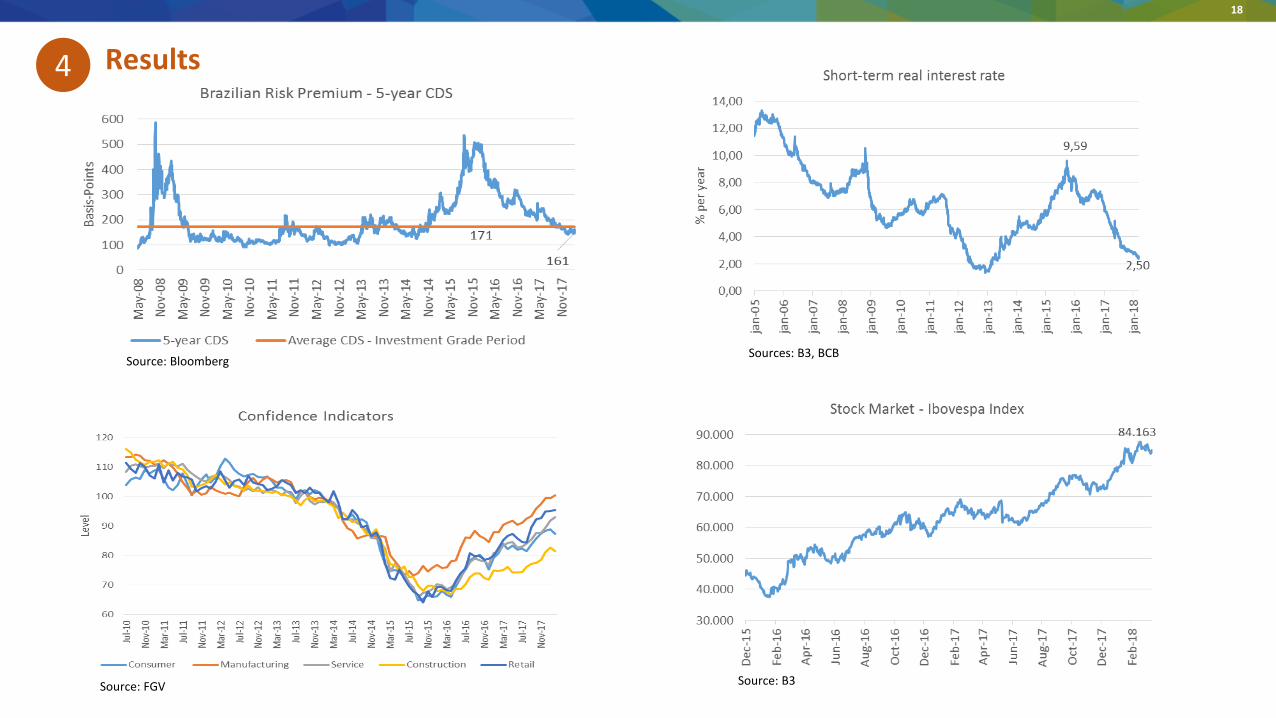

2. Results

Sources: B3, BCB

4

Source: Bloomberg

Source: FGV Source: B3

19

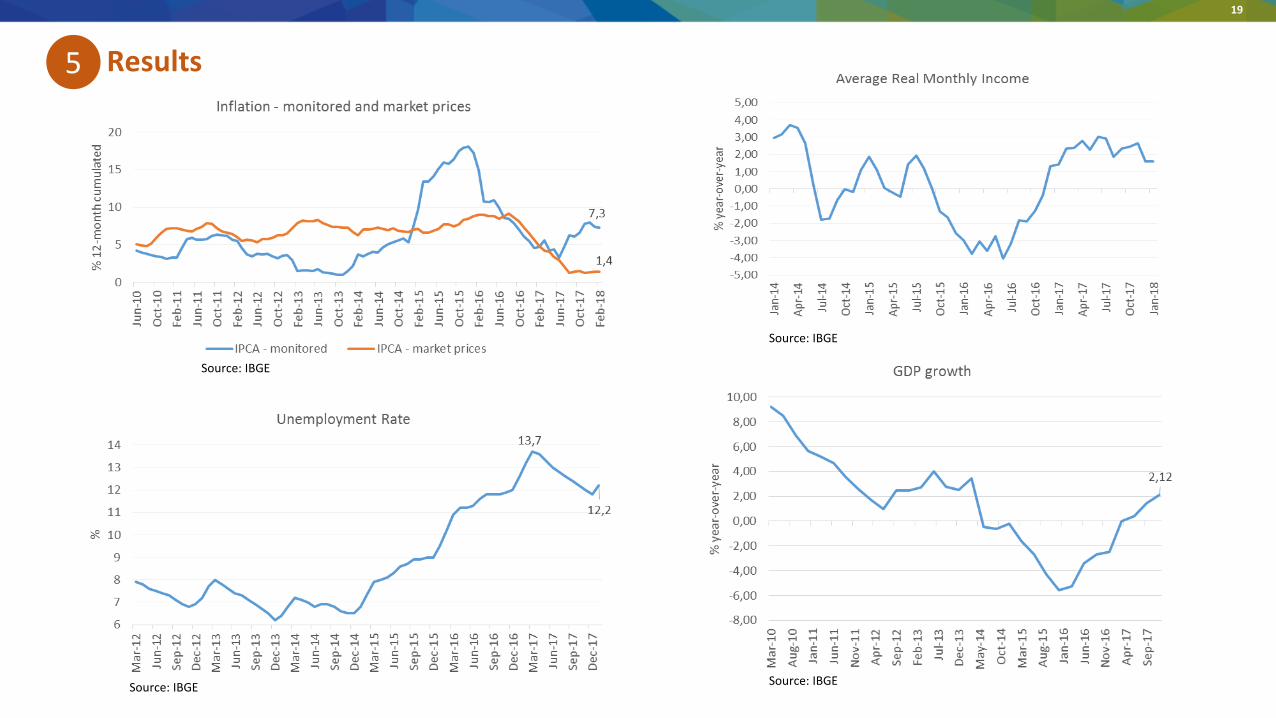

1. Results5

Source: IBGE

Source: IBGE

Source: IBGESource: IBGE