Embed Size (px)

Citation preview

Financing geothermal projects in challenging timesIslandsbanki Geothermal Research April 2009

Introduction

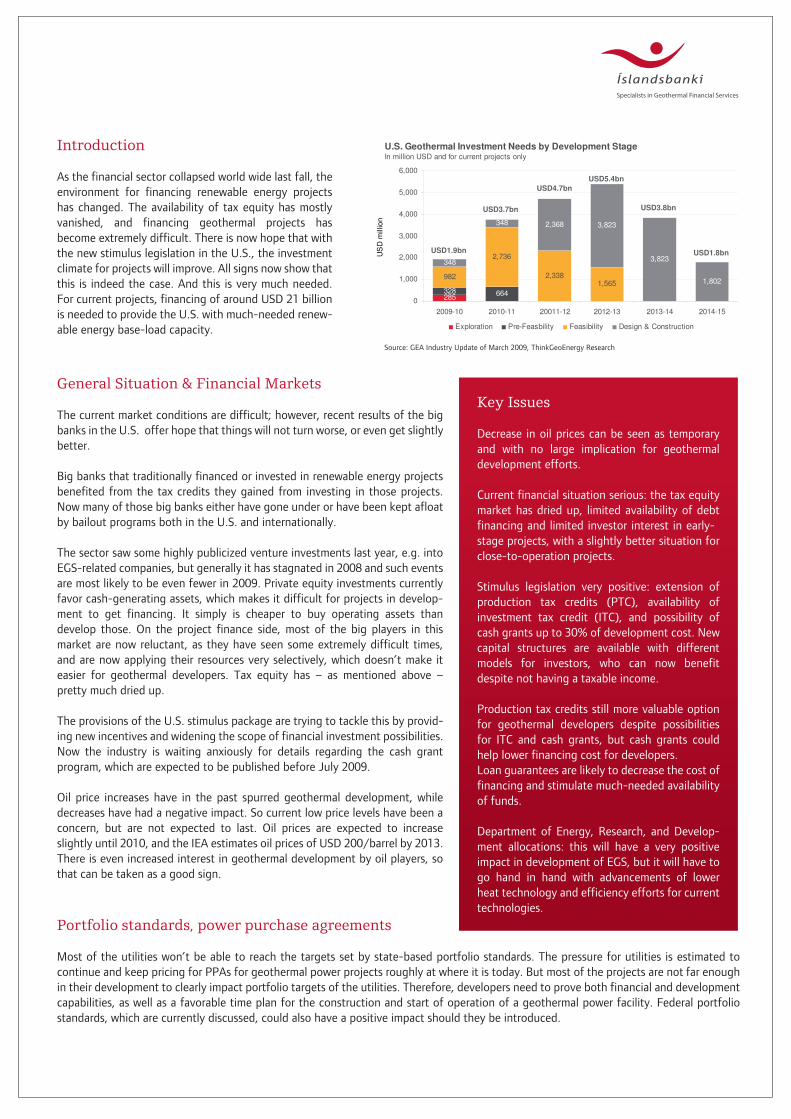

As the financial sector collapsed world wide last fall, the environment for financing renewable energy projects has changed. The availability of tax equity has mostly vanished, and financing geothermal projects has become extremely difficult. There is now hope that with the new stimulus legislation in the U.S., the investment climate for projects will improve. All signs now show that this is indeed the case. And this is very much needed. For current projects, financing of around USD 21 billion is needed to provide the U.S. with much-needed renew-able energy base-load capacity.

General Situation & Financial Markets

The current market conditions are difficult; however, recent results of the big banks in the U.S. offer hope that things will not turn worse, or even get slightly better.

Big banks that traditionally financed or invested in renewable energy projects benefited from the tax credits they gained from investing in those projects. Now many of those big banks either have gone under or have been kept afloat by bailout programs both in the U.S. and internationally. The sector saw some highly publicized venture investments last year, e.g. into EGS-related companies, but generally it has stagnated in 2008 and such events are most likely to be even fewer in 2009. Private equity investments currently favor cash-generating assets, which makes it difficult for projects in develop-ment to get financing. It simply is cheaper to buy operating assets than develop those. On the project finance side, most of the big players in this market are now reluctant, as they have seen some extremely difficult times, and are now applying their resources very selectively, which doesn’t make it easier for geothermal developers. Tax equity has – as mentioned above – pretty much dried up.

The provisions of the U.S. stimulus package are trying to tackle this by provid-ing new incentives and widening the scope of financial investment possibilities. Now the industry is waiting anxiously for details regarding the cash grant program, which are expected to be published before July 2009.

Oil price increases have in the past spurred geothermal development, while decreases have had a negative impact. So current low price levels have been a concern, but are not expected to last. Oil prices are expected to increase slightly until 2010, and the IEA estimates oil prices of USD 200/barrel by 2013. There is even increased interest in geothermal development by oil players, so that can be taken as a good sign.

Portfolio standards, power purchase agreements

Most of the utilities won’t be able to reach the targets set by state-based portfolio standards. The pressure for utilities is estimated to continue and keep pricing for PPAs for geothermal power projects roughly at where it is today. But most of the projects are not far enough in their development to clearly impact portfolio targets of the utilities. Therefore, developers need to prove both financial and development capabilities, as well as a favorable time plan for the construction and start of operation of a geothermal power facility. Federal portfolio standards, which are currently discussed, could also have a positive impact should they be introduced.

Key Issues

Decrease in oil prices can be seen as temporary and with no large implication for geothermal development efforts.

Current financial situation serious: the tax equity market has dried up, limited availability of debt financing and limited investor interest in early-stage projects, with a slightly better situation for close-to-operation projects.

Stimulus legislation very positive: extension of production tax credits (PTC), availability of investment tax credit (ITC), and possibility of cash grants up to 30% of development cost. New capital structures are available with different models for investors, who can now benefit despite not having a taxable income.

Production tax credits still more valuable option for geothermal developers despite possibilities for ITC and cash grants, but cash grants could help lower financing cost for developers.Loan guarantees are likely to decrease the cost of financing and stimulate much-needed availability of funds.

Department of Energy, Research, and Develop-ment allocations: this will have a very positive impact in development of EGS, but it will have to go hand in hand with advancements of lower heat technology and efficiency efforts for current technologies.

U.S. Geothermal Investment Needs by Development StageIn million USD and for current projects only

285328 664

982

2,736

2,3381,565

348

348 2,368 3,823

3,823

1,802

0

1,000

2,000

3,000

4,000

5,000

6,000

2009-10 2010-11 20011-12 2012-13 2013-14 2014-15

US

D m

illio

n

Exploration Pre-Feasbility Feasibility Design & Construction

USD1.9bn

USD3.7bn

USD4.7bnUSD5.4bn

USD3.8bn

USD1.8bn

Source: GEA Industry Update of March 2009, ThinkGeoEnergy Research

Structure Of Geothermal Financing

Financing for geothermal project development has always depended strongly on equity investments, mostly because of the risk structure and time frame of geothermal project development.

The resource element and the “drilling risk” also demands investors that understand the challenges in the development process. Traditionally, debt financing was only available when the developer was able to prove the resource through successful drilling results. Mezzanine/bridge financing structures then had been made available through Glitnir, which had built its business strongly on a specialization in geothermal energy, industry experience, and knowledge. This kind of financing will most likely not be available

for some time, so drilling will most likely have to be covered by equity provided by the developer, a private equity player, or through public markets. In other countries, governmental drilling risk insurance models have had a large impact on getting investors to provide financing at that stage. Construction/project financing is then the earliest stage for debt financing and the entry of tax equity player.

In the last few years, the largest part of project finance for geother-mal projects has been provided by “tax equity investors,” which were typically large investment banks and insurance companies. In those very specialized financing structures, federal support for renewable power technologies was capitalized. As a result of the financial crisis, the number of active tax equity investors has declined dramatically.

As a result, the U.S. stimulus legislation was designed to make federal incentives for renewable power technologies more useful. The provisions in the act include an extension of the production tax credits (PTC), with the possibility to elect an investment tax credit (ITC) instead. ITC-eligible projects can also receive a cash grant of equivalent value.

The extension of the PTCs, particularly for geothermal, is positive, and the possibility of utilizing investment tax credits and even a cash grant are destined to help the industry. The rules for invest-ment tax credits (ITC) are very stringent and the basis for any utilization of the cash grant program to be put in place. The rules for the cash grant are currently being worked on by the U.S. Treasury. The new system makes financing structures more complicated, and while it will reduce the need for tax investors, who are currently rather scarce anyway, it will not eliminate them.

Grants will be available for property placed in service in 2009 or 2010, and for geothermal if construction begins in 2009 or 2010, the grant can be claimed for property placed in service before 2014 and in some instances until 2017. Companies that are eligible for the ITC are eligible for the Cash Grant program by the U.S. Treasury. Guidance and application material will be available in July 2009.

Generally, the possibility of getting a cash grant, which is non-taxable, permits investors to monetize credits, even though those investors do not have sufficient taxable income. This should widen the scope for possible investors. Furthermore, it allows for different financing structures for the project than found in the limited traditional PTC focused set-up, where it was necessary for

the tax investor to have sufficient tax appetite.The new rules in effect allow for structures that reduce the developer’s financing costs since 30% of the purchase price would be captured in the form of the cash grant, in a structure where the developer sells the project to a tax equity investor and leases it back.

The above diagram shows the structure which allows for two scenarios, either the traditional sale-leaseback, or the possibility for the developer retaining the cash grant and the depreciation in the special purpose vehicle.

Investors can therefore benefit from the new rules, even though they might not have a taxable income. The depreciation can be separated from the credit, allocating the depreciation to a party with a tax appetite and the credit part of the financing to a party with no tax appetite. This widens the scope of financial structuring with the possibility to choose a lease structure, something that wasn’t possible before in a PTC scenario. It allows parties to pass the cash grant to the lessee, so the geothermal project could be sold to a party having the ability to utilize depreciation, either for current income or the ability to use carry backs. The cash grant could then be retained as benefit by the investor, or be passed to the developer, now lessee. Projects may still have to monetize their depreciation benefits, but a 30% cash grant instead of having to monetize investment tax or production tax credits provides developers with substantial certainty about their capital structure.

Overall, it seems like that the PTC/ITC structure favors lower capacity projects, such as wind and solar, but the decrease in financing cost for the developer as such, given the lack of tax equity appetite, is still very positive for geothermal development.

Tax considerations (ptc, itc, and the new cash grants)

Start-up Exploration/ Pre-

Feasibility

Feasibility Detailed Design &

Construction

Start of Operation

Venture Capital

Development Equity

DrillingEquity

ProjectEquity

TaxEquity

Mezz./ Bridge Debt, Const.

Financing

ProjectFinancing

Special Purpose Vehicle

Developer

Project Sale

LeasebackPower Sale

Power Purchaser

Tax Investor

Loan guarantees

What cash grants should do for the disruption in the tax equity markets, the new loan guaranty program should do for the debt markets. The legislation provides for a new Department of Energy loan guarantee program available to renewable energy and transmission projects, supporting loans up to 80 percent of project costs. To be eligible, projects must commence construction by Sept. 30, 2011. The expansion of the existing loan guarantee program to cover commercial (rather than just “innovative non-commercial”) projects incentivizes debt financing of projects. The program appropriates USD 6 billion to reduce or eliminate the cost of providing the guarantee; this amount could support USD 60–100 billion in new loans, depending on the risk profiles of the underlying projects. The program also is expected to lower interest rates on loans supported by these guarantees.

DOE research & development

The USD 400 million put aside for geothermal research and devel-opment to be administered by the U.S. Department of Energy (DOE) will have a very positive impact, if put into the right efforts. While it will be important to support research and development for enhanced geothermal systems (EGS), it will be essential that efforts are put towards R&D that has the possibility to impact today’s projects. Drilling and other related risks are always mentioned and so is the need for better mapping of geothermal resources in the U.S. So if parts of the support provided can help decrease the risk and costs of current projects, then this could have a tremendous impact. Another element that should be considered is the fact that more educational efforts are needed to attract and educate the new generations of geothermal specialists that are in such high demand in the industry.

Conclusion

The overall outlook for the geothermal sector is good, while it will remain challenging. The industry will see a new set of players coming from new and old angles, e.g. from the oil and mining sectors, but also more remotely related industries. The new “stimu-lus” legislation in the U.S. will have a positive impact and is seen by many as “a lifeline to better days” setting off some of the impact the global recession has on the industry. The legislation’s key elements are the much needed certainty on production tax credits. But the most important elements are the ITC and cash grant elements, which make the application of new structures for financing of geothermal projects possible. The cash grants effectively decrease the financing cost for the developer, and investors benefit from the new rules as well even though they might not have a taxable income. The loan guarantees will provide a stimulus to much-needed debt financing for construction and project financing and likely decrease financing cost as well. The allocation of USD 400 million for research and development in geothermal energy is also a very positive step towards helping the industry, but the money will have to be allocated wisely towards efforts to decrease development costs today, the advancement and development of new technologies, as well as helping educa-tional efforts.

Islandsbanki

Islandsbanki builds its value proposition of the success of the Glitnir Global Geothermal Energy Team. The nature of geothermal projects demands a strong understanding of the underlying techni-cal issues and risks. Islandsbanki has formed a team of experienced bankers who focus on the geothermal energy industry.

Unique basis for sustainable energy services• Home market Iceland with more than 99% of electricity production from renewables (~8% in the United States).• Iceland, one of the leaders of geothermal energy utilization for electricity production & direct use. • Currently installed capacity (geothermal) in Iceland is 570 MWe.• Strategic partners with leading positions in the sector.

Islandsbanki business origination• Extensive geographical and industry research.• Industry player mapping & networks.• Advisory in the geothermal sector, across the whole value chain.• Islandsbanki Geothermal Team members are located in Reykjavík, Iceland.

Geothermal Energy Team

Islandsbanki, Kirkjusandi, IS-155 Reykjavik, IcelandTel: +354-440-4500

For more information:[email protected]/energy

Islandsbanki cooperates with:

ThinkGeoEnergy is a news and service website focused on the geothermal power sector globally and is the key resource for indus-try news, deals, and development globally.

This document was written on behalf of Islandsbanki by:Alexander Richter, [email protected] H I N K

G EO EN E R G Y

· ··

· ··

· ··

Glitnir’s selected customers & deals

Disclaimer

This introduction is made by Íslandsbanki hf.

The information in this report is based on publicly available data and information from various sources deemed reliable. The information has not been independently verified by Íslandsbanki hf. which therefore does not guarantee that the information is comprehensive and accurate. All views expressed herein are those of the author(s) at the time of writing and may change without notice. Íslandsbanki hf. holds no obligation to update, modify or amend this publication or to otherwise notify a reader or recipient of this publication in the event that any matter contained herein changes or subsequently becomes inaccurate.

This report is informative in nature, and should not be interpreted as a recommendation to take, or not to take, any particular investment action. This report does not represent an offer or an invitation to buy, sell or subscribe to any particular financial instruments.

Íslandsbanki hf. accepts no liability for any possible losses or other consequences arising from decisions based on information in this report. Any loss arising from the use of the information in this report shall be the sole and exclusive responsibility of the investor. Before making an investment decision, it is important to seek expert advice and familiarise oneself with the investment market and different investment alternatives.

Various financial risks are always related to investment activities, such as the risk of no yield or the risk of losing the capital invested. It should further be noted that international investing includes risks related to political and economic uncertainties as well as currency risk. Each investorʼs investment objectives and financial situation is different. Past performance does not indicate nor guarantee future performance of an investment.

Reports and other information received from Íslandsbanki hf. are meant for private use only. The materials may not be copied, quoted or distributed, in part or in whole, without a written permission from Íslandbanki hf.

This report is a brief summary and does not purport to contain all available information on the subjects covered.

Regulator: The Financial Supervisory Authority of Iceland (www.fme.is)

UNITED STATES

This report or copies of it must not be distributed in the United States or to recipients who are citizens of the United States against restrictions stated in the United States legislation. Distributing the report in the United States might be seen as a breach of these laws.

CANADA

The information provided in this publication is not intended to be distributed or circulated in any manner in Canada and therefore should not be construed as any kind of financial recommendation or advice provided within the meaning of Canadian securities laws.

OTHER COUNTRIES

Laws and regulations of other countries may also restrict the distribution of this report.

For further information relating to this introduction see: https://www.islandsbanki.is.

This document does not constitute any solicitation of services by Íslandsbanki in the United States or Canada.