Embed Size (px)

Citation preview

FINANCIAL VIABILITY FINANCIAL VIABILITY OF LOCAL OF LOCAL

GOVERNMENTS IN GOVERNMENTS IN TURKEYTURKEY

Ayşe Güner, Marmara University, Faculty of Economic Ayşe Güner, Marmara University, Faculty of Economic and Administrative Sciences, Department of Public and Administrative Sciences, Department of Public

FinanceFinance

““Strengthening Fiscal Framework for Local Government Strengthening Fiscal Framework for Local Government Reform-Policy Design”Reform-Policy Design”

Istanbul, 8-10 September, 2003Istanbul, 8-10 September, 2003

BRIEF INFORMATION ON LOCAL BRIEF INFORMATION ON LOCAL GOVERNMENTS IN TURKEYGOVERNMENTS IN TURKEY

The Republic of Turkey is a unitary state governed by a The Republic of Turkey is a unitary state governed by a multiparty parliamentary system. Article 123 of the multiparty parliamentary system. Article 123 of the 1982 Constitution stipulates that “the administration 1982 Constitution stipulates that “the administration forms a whole with regard to its structure and functions, forms a whole with regard to its structure and functions, and shall be regulated by law”. The same article also and shall be regulated by law”. The same article also states that “the organization and functions of the states that “the organization and functions of the administration are based on the principles of administration are based on the principles of centralization and decentralization”. Thus, there is a centralization and decentralization”. Thus, there is a central government and local governments.central government and local governments.

The central administration is composed of two branches: The central administration is composed of two branches: central administrative organizations in the capital, central administrative organizations in the capital, Ankara, and provincial administrations.Ankara, and provincial administrations.

The provicial administration, comprised of provinces The provicial administration, comprised of provinces and within them districts, are established to take and and within them districts, are established to take and implement decisions on behalf of the center (working on implement decisions on behalf of the center (working on the principle of deconcentration). These units are the principle of deconcentration). These units are headed by provincial governors and district governors headed by provincial governors and district governors (sub-governors) and are appointed by the central (sub-governors) and are appointed by the central government.government.

Article 127 of the Constitution puts down the main Article 127 of the Constitution puts down the main features of local governments in Turkey.features of local governments in Turkey.

Article 127 of the Constitution Article 127 of the Constitution stipulates that:stipulates that:

Local administrative bodies are public corporate Local administrative bodies are public corporate entities established to meet the common local needs of entities established to meet the common local needs of the inhabitants of provinces, municipal districts and the inhabitants of provinces, municipal districts and villages, whose decision-making organs are elected, villages, whose decision-making organs are elected, and whose principles of structure are also determined and whose principles of structure are also determined by law.by law.

The formation, duties and powers of the local The formation, duties and powers of the local administration shall be regulated by law in accordance administration shall be regulated by law in accordance with the principle of local administration.with the principle of local administration.

The elections for local administration shall be held The elections for local administration shall be held every 5 years.every 5 years.

The procedures dealing with objections to the The procedures dealing with objections to the acquisition by elected organs of local government or acquisition by elected organs of local government or their status as an organ, and their loss of such status, their status as an organ, and their loss of such status, shall be resolved by the judiciary. However, as a shall be resolved by the judiciary. However, as a provisional measure, the Minister of Internal Affairs provisional measure, the Minister of Internal Affairs may remove from office those organs of local may remove from office those organs of local administration or their members against whom administration or their members against whom investigation or prosecution has been initiated on the investigation or prosecution has been initiated on the grounds of offences related to their duties, pending grounds of offences related to their duties, pending judgement.judgement.

Article 127 (cont.)Article 127 (cont.) Special administrative arrangements may be Special administrative arrangements may be

introduced by law for larger urban centers.introduced by law for larger urban centers. The central government has the power of The central government has the power of

administrative tutelage over the local governments administrative tutelage over the local governments in the framework of principles and procedures set in the framework of principles and procedures set forth by law with the objective of (i) ensuring the forth by law with the objective of (i) ensuring the functioning of local services in conformity with the functioning of local services in conformity with the principle of the integral unity of the administration, principle of the integral unity of the administration, (ii) securing uniform public service, (iii) (ii) securing uniform public service, (iii) safeguarding the public interest and (iv) meeting safeguarding the public interest and (iv) meeting local needs, in an appropriate manner.local needs, in an appropriate manner.

The formation of local administrative bodies into a The formation of local administrative bodies into a union with the permission of the Council of union with the permission of the Council of Ministers for the purpose of performing specific Ministers for the purpose of performing specific public services; and the functions, powers, financial public services; and the functions, powers, financial and security arrangements of these unions, and and security arrangements of these unions, and their reciprocal ties and relations with the central their reciprocal ties and relations with the central administration, shall be regulated by law.administration, shall be regulated by law.

These administrative bodies shall be allocated These administrative bodies shall be allocated financial resources in proportion to their functions. financial resources in proportion to their functions.

Local Governments in Turkey

Local Governments in Turkey

Special Provincial Administrations

(81)

Special Provincial Administrations

(81)

Municipalities(3215)

Municipalities(3215)

Villages(35000)Villages(35000)

SPECIAL PROVINCIAL ADMINISTRATIONS SPECIAL PROVINCIAL ADMINISTRATIONS (SPAs)(SPAs)

The reference law of SPAs dates back to a temporary law The reference law of SPAs dates back to a temporary law dated 1913 and has taken its current name (SPA Law) by dated 1913 and has taken its current name (SPA Law) by important amendments made in 1987 (Law no.3360).important amendments made in 1987 (Law no.3360).

There is no separate law covering the establisment of There is no separate law covering the establisment of SPAs. When a province, which is the field branch of the SPAs. When a province, which is the field branch of the central administration working on the principle of central administration working on the principle of deconcentration, is established, automatically SPAs are deconcentration, is established, automatically SPAs are founded. founded.

According to the law of 1913, SPAs had overtaken many According to the law of 1913, SPAs had overtaken many services ranging from social aid, health, education, services ranging from social aid, health, education, agriculture to establishing chambers and stock exchanges. agriculture to establishing chambers and stock exchanges. However, after the foundation of the Republic these duties However, after the foundation of the Republic these duties were gradually undertaken by several ministries and were gradually undertaken by several ministries and general directorates of the central government. Today, general directorates of the central government. Today, they act as an agent/intermediate to the services carried they act as an agent/intermediate to the services carried out by the central government.out by the central government.

Organs Organs - Provincial Council- Provincial Council - Provincial Executive Committee- Provincial Executive Committee - Governor- Governor

MUNICIPALITIESMUNICIPALITIES The reference law of the municipalities is the The reference law of the municipalities is the

Municipality Law of 1580 (1930).Municipality Law of 1580 (1930).

They are established in settlements that have They are established in settlements that have more than 2,000 inhabitants and in provincial more than 2,000 inhabitants and in provincial and district centers regardless of their and district centers regardless of their population.population.

The Municipality Law lists the duties of The Municipality Law lists the duties of municipalities; the services given by these local municipalities; the services given by these local governments may be termed as classic municipal governments may be termed as classic municipal services (fire, street cleaning and lightning, services (fire, street cleaning and lightning, cemetry, transportation, sewery services etc.).cemetry, transportation, sewery services etc.).

Organs:Organs: - Municipal Council- Municipal Council - Municipal Executive Committe- Municipal Executive Committe

- Mayor- Mayor

GREATER CITY MUNICIPALITIES GREATER CITY MUNICIPALITIES (METROPOLITAN MUNICIPALITIES)(METROPOLITAN MUNICIPALITIES)

In 1984 a two-tier local government system In 1984 a two-tier local government system has been introduced with Law no. 3030. has been introduced with Law no. 3030. According to this law, a greater city According to this law, a greater city municipality is a municipality which has municipality is a municipality which has more than one district or lower tier more than one district or lower tier municipality within its boundaries. municipality within its boundaries.

The duties of metropolitan municipalities is The duties of metropolitan municipalities is listed in law no. 3030. The district and lower listed in law no. 3030. The district and lower tier municipalities within the territorial tier municipalities within the territorial borders of the metropolitan municipality borders of the metropolitan municipality perform the tasks given to them by the perform the tasks given to them by the Municipality Law but which do not coincide Municipality Law but which do not coincide with those of the metropolitan municipality. with those of the metropolitan municipality.

OrgansOrgans - Metropolitan Municipal Council- Metropolitan Municipal Council - Metropolitan Executive Committe- Metropolitan Executive Committe - Metropolitan Mayor- Metropolitan Mayor

VILLAGESVILLAGES

According to the Village Law of 1924 (Law no.442), According to the Village Law of 1924 (Law no.442), villages are settlements with a population less than villages are settlements with a population less than 2,000. The law also states that “people owning 2,000. The law also states that “people owning common property such as a mosque, school, pasture, common property such as a mosque, school, pasture, grazing ground and woods and who live either in grazing ground and woods and who live either in grouped or scattered houses, together with grouped or scattered houses, together with vineyards, gardens and fields, form a village” and vineyards, gardens and fields, form a village” and that the law applies to settlements with a total that the law applies to settlements with a total population more than 150.population more than 150.

The duties of the village administration are listed in The duties of the village administration are listed in the Village Law (compulsory and optional duties). the Village Law (compulsory and optional duties). The services to be performed by the village are too The services to be performed by the village are too numerous, vast and varied to be realized under the numerous, vast and varied to be realized under the current situation. That is why most services (such as current situation. That is why most services (such as construction of roads and building of water construction of roads and building of water installations) are being performed by central installations) are being performed by central government agencies.government agencies.

OrgansOrgans - Village Council- Village Council - Council of Elderly- Council of Elderly - Headman- Headman

GENERAL REMARKSGENERAL REMARKS

The laws of local governments are outdated and The laws of local governments are outdated and are unable to respond to changing conditions and are unable to respond to changing conditions and needs.needs.

SPAs and villages are not known and considered SPAs and villages are not known and considered as local governments in the society. as local governments in the society.

There is strict administrative tutelage on local There is strict administrative tutelage on local governments. This supervision of local governments. This supervision of local governments by the central administration are governments by the central administration are both administrative and financial in context. The both administrative and financial in context. The reserves Turkey has placed on the European reserves Turkey has placed on the European Charter of Local Self-Government is a good Charter of Local Self-Government is a good indicator of central government control over indicator of central government control over local governments. local governments.

LOCAL GOVERNMENT REVENUESLOCAL GOVERNMENT REVENUES (% of GNP)(% of GNP)

With new laws enacted in 1981, the share of local With new laws enacted in 1981, the share of local revenues in GNP has increased significantly. Although revenues in GNP has increased significantly. Although SPA revenues have grown considerably, they still form a SPA revenues have grown considerably, they still form a small share in the total. The biggest increase has occured small share in the total. The biggest increase has occured in municipalities, from 1.63 percent to 4.41 percent of in municipalities, from 1.63 percent to 4.41 percent of GNP in 20 years. The share of village administrations GNP in 20 years. The share of village administrations have remained constant, indicating that they are being have remained constant, indicating that they are being funded by central government agencies and SPAs.funded by central government agencies and SPAs.

YearYear MunicipaliMunicipalitiesties

SPAsSPAs VillagesVillages TotalTotal

19801980 1.511.51 0.060.06 0.060.06 1.631.63

19901990 2.302.30 0.120.12 0.060.06 2.482.48

20002000 4.414.41 0.290.29 0.060.06 4.764.76

REVENUES OF VILLAGE ADMINISTRATIONSREVENUES OF VILLAGE ADMINISTRATIONS

SalmaSalma : a household tax levied by the council of elderly : a household tax levied by the council of elderly (maximum 20 TL!).(maximum 20 TL!).

ImeceImece: the physical working of the villagers for the common : the physical working of the villagers for the common needs of the village; decision taken by the council of elderly.needs of the village; decision taken by the council of elderly.

Village MoneyVillage Money: income generated from operations and : income generated from operations and rental of properties of the village, fines and donations, fees rental of properties of the village, fines and donations, fees and charges on issuance of official documents, etc.and charges on issuance of official documents, etc.

GrantsGrants: Central government ministries, general directorates, : Central government ministries, general directorates, the Province Bank, SPAs provide aid to villages to the Province Bank, SPAs provide aid to villages to compensate the inefficiency of revenues.compensate the inefficiency of revenues.Today salma, imece and village money, which may be named Today salma, imece and village money, which may be named as the genuine revenues of the village, are far from being as the genuine revenues of the village, are far from being able to meet the expenditures of the villages. The main able to meet the expenditures of the villages. The main source of revenue is grants which are distributed on an source of revenue is grants which are distributed on an ad ad hochoc basis. These grants may be in cash, but also (and basis. These grants may be in cash, but also (and mainly) in-kind.mainly) in-kind.

REVENUES OF SPAsREVENUES OF SPAs

Share From General Budget Tax RevenuesShare From General Budget Tax RevenuesWith law no. 2380 (1981), a certain percentage of With law no. 2380 (1981), a certain percentage of general budget collected tax revenues are distributed general budget collected tax revenues are distributed to SPAs, based on the criteria of population (according to SPAs, based on the criteria of population (according to the latest census). Currently, this share is 1,12 to the latest census). Currently, this share is 1,12 percent.percent.

Own RevenuesOwn RevenuesRevenues generated from taxes, duties, fees which are Revenues generated from taxes, duties, fees which are authorized by special laws; income from the yields from authorized by special laws; income from the yields from investments and activities; revenues from the renting investments and activities; revenues from the renting and selling of immovable property etc. In addition, 15 and selling of immovable property etc. In addition, 15 percent of the property tax collected by the percent of the property tax collected by the municipalities is transferred to SPAs.municipalities is transferred to SPAs.

Grants Grants Central government agencies provide aid to SPAs in Central government agencies provide aid to SPAs in order that they be able to accomplish certain services order that they be able to accomplish certain services within the boundaries of the province. These grants are within the boundaries of the province. These grants are conditional, that is, to be used for the performing of conditional, that is, to be used for the performing of specified servicesspecified services

REVENUES OF SPAs (cont.)REVENUES OF SPAs (cont.)

BorrowingBorrowingSPAs have important limitations concerning borrowing. SPAs have important limitations concerning borrowing. Firstly, they are only permitted to borrow for education, Firstly, they are only permitted to borrow for education, health and construction services. Secondly, there is a health and construction services. Secondly, there is a limit on the amount of borrowing: (i) the provincial limit on the amount of borrowing: (i) the provincial council may take the decision to borrow if the amount council may take the decision to borrow if the amount does not exceed one third of its budget revenues, (ii) does not exceed one third of its budget revenues, (ii) when this amount is exceeded, the decision of the when this amount is exceeded, the decision of the Council of Ministers and the approval of the President Council of Ministers and the approval of the President is necessary, (iii) if the amount to be borrowed is over is necessary, (iii) if the amount to be borrowed is over its budget revenues, then a special law is to be issued. its budget revenues, then a special law is to be issued.

Unfortunately own revenues is the least important item Unfortunately own revenues is the least important item in the total revenues of SPAs. It is possible to in the total revenues of SPAs. It is possible to generalize that the most important type of revenue is, generalize that the most important type of revenue is, first of all, grants from the central government, and first of all, grants from the central government, and secondly, the share distributed from general budget tax secondly, the share distributed from general budget tax revenues. These two items add up to 85 percent of total revenues. These two items add up to 85 percent of total revenues on averagerevenues on average

REVENUES OF MUNICIPALITIESREVENUES OF MUNICIPALITIES

Share From General Budget Tax RevenuesShare From General Budget Tax RevenuesA certain percentage of the collected general A certain percentage of the collected general budget tax revenues is distributed to budget tax revenues is distributed to municipalities on the basis of population. Recently municipalities on the basis of population. Recently this share has been reduced from 6 to 5 percent. this share has been reduced from 6 to 5 percent.

Own RevenuesOwn RevenuesThe own revenues of municipalities (except for the The own revenues of municipalities (except for the Property Tax which has its own law) are covered in Property Tax which has its own law) are covered in the Municipality Revenue Law No. 2464 (1981). the Municipality Revenue Law No. 2464 (1981). This law may be divided to 3 parts: (i) municipal This law may be divided to 3 parts: (i) municipal taxes, (ii) municipal fees and (iii) contributions to taxes, (ii) municipal fees and (iii) contributions to municipal expenditures.municipal expenditures.This law also states that municipalities, with the This law also states that municipalities, with the decision of the municipal council, may set tariffs decision of the municipal council, may set tariffs for municipal services that have not been subject for municipal services that have not been subject to the above revenue types.to the above revenue types.

REVENUES OF MUNICIPALITIES REVENUES OF MUNICIPALITIES (CONT.)(CONT.)

Municipal TaxesMunicipal Taxes Property Tax (specific and ad valorem)Property Tax (specific and ad valorem) Fire Insurance Tax (ad valorem)Fire Insurance Tax (ad valorem) Entertainment Tax (fixed value and ad Entertainment Tax (fixed value and ad

valorem)valorem) Electricity and Gas Tax (ad valorem)Electricity and Gas Tax (ad valorem) Communication Tax (ad valorem)Communication Tax (ad valorem) Announcement and Advertisement Tax Announcement and Advertisement Tax

(specific)(specific) Environmental Cleanliness Tax (specific Environmental Cleanliness Tax (specific

and ad valorem)and ad valorem)

REVENUES OF MUNICIPALTIES (CONT.)REVENUES OF MUNICIPALTIES (CONT.)Municipal FeesMunicipal Fees

Occupation FeeOccupation Fee Weekend Business FeeWeekend Business Fee Natural Water FeeNatural Water Fee Broker’s FeeBroker’s Fee Slaughter FeeSlaughter Fee Construction FeeConstruction Fee Business Opening FeeBusiness Opening Fee Regisratation FeeRegisratation Fee Health Certificate FeeHealth Certificate Fee Property Development FeesProperty Development Fees Fee for Inspection of Measurement and Weighing Fee for Inspection of Measurement and Weighing

InstrumentsInstruments Fee for Inspection of LicenseFee for Inspection of License

All these fees, except for the broker’s fee, have a fixed All these fees, except for the broker’s fee, have a fixed tariff which has last been updated in 1992. Keeping in mind tariff which has last been updated in 1992. Keeping in mind the high rate of inflation from since then, today, the the high rate of inflation from since then, today, the collection costs of these fees have become higher than the collection costs of these fees have become higher than the revenues received.revenues received.

REVENUES OF MUNICIPALITIES REVENUES OF MUNICIPALITIES (CONT.)(CONT.)

Contributions to Municipal ExpendituresContributions to Municipal Expenditures Contributions may only be collected in three cases: Contributions may only be collected in three cases:

sewage, water and road construction or improvement sewage, water and road construction or improvement services. The municipality sets the amount to be services. The municipality sets the amount to be contributed from the property owners who benefit from contributed from the property owners who benefit from the service. But there is a ceiling, such that the amount the service. But there is a ceiling, such that the amount cannot exceed 2 percent of property tax values. cannot exceed 2 percent of property tax values.

BorrowingBorrowingAccording to the Municipality Law there are no According to the Municipality Law there are no restrictions on borrowing. But due to their poor credit restrictions on borrowing. But due to their poor credit history, the Provice Bank was almost the only source of history, the Provice Bank was almost the only source of borrowing for municipalities until mid-1980s. Since then borrowing for municipalities until mid-1980s. Since then external debt has become an important source of external debt has become an important source of revenue, especially for metropolitan municipalities. The revenue, especially for metropolitan municipalities. The Law on Regulating Public Finance and Debt Law on Regulating Public Finance and Debt Management that passed on March 2002, aiming to Management that passed on March 2002, aiming to control public borrowing in line with overall control public borrowing in line with overall macroeconomic policies, has restricted the foreign macroeconomic policies, has restricted the foreign borrowing of local governments, such that they have to borrowing of local governments, such that they have to receive the opinion of the State Planning Organization receive the opinion of the State Planning Organization with the approval of the Treasury.with the approval of the Treasury.

MUNICIPALITY REVENUES (%)MUNICIPALITY REVENUES (%)19911991 19921992 19931993 19941994 19951995 19961996 19971997 19981998

Total Total RevenuesRevenues

100100 100100 100100 100100 100100 100100 100100 100100

Tax Tax RevenuesRevenues

6565 60.760.7 5353 61.261.2 61.661.6 60.860.8 56.956.9 61.961.9

General General BudgetBudget

53.753.7 50.750.7 44.944.9 44.544.5 47.447.4 50.150.1 48.148.1 48.848.8

MunicipaliMunicipality Taxesty Taxes

8.78.7 6.66.6 4,84,8 13,913,9 10,810,8 7,97,9 6,36,3 10,910,9

Property Property TaxTax

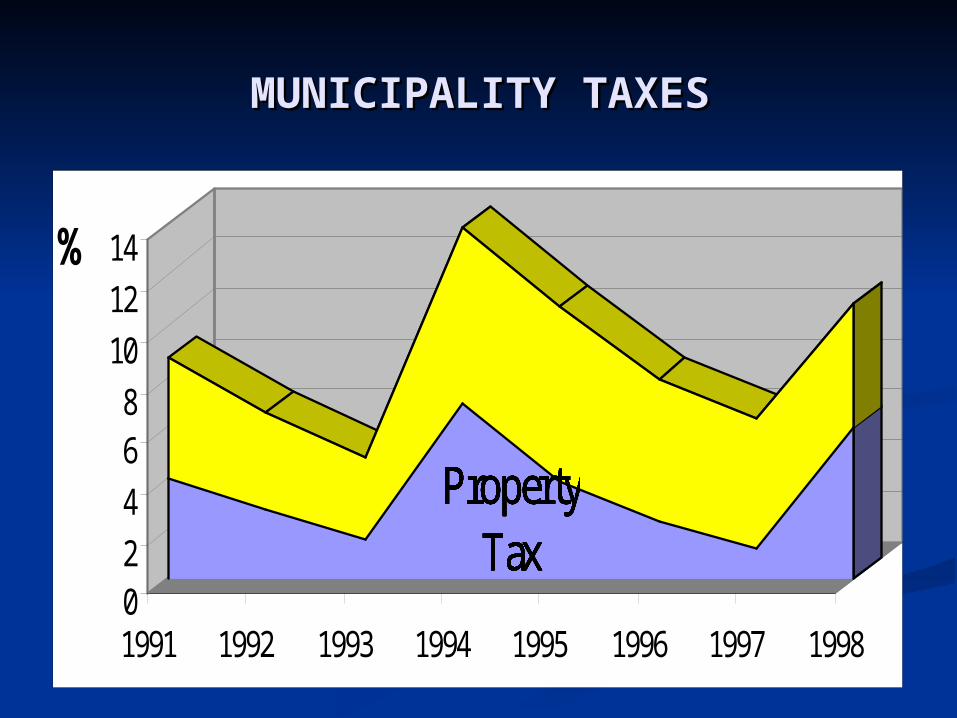

44 2,82,8 1,61,6 6,96,9 3,83,8 2,32,3 1212 66

MunicipaliMunicipality Feesty Fees

3.53.5 3,43,4 3,43,4 2,82,8 3,43,4 2,82,8 2,52,5 2,22,2

ContributiContributionon

1,61,6 1,41,4 2,12,1 1,11,1 1,41,4 1,41,4 11 1,11,1

Internal Internal BorrowingBorrowing

1,91,9 1,71,7 3,13,1

External External BorrowingBorrowing

6,76,7 7,27,2 5,75,7

MUNICIPALITY REVENUESMUNICIPALITY REVENUES

MUNICIPALITY REVENUES (%)MUNICIPALITY REVENUES (%)

0

10

20

30

40

50

60

1991 1992 1993 1994 1995 1996 1997 1998

%

General Budget Municipality TaxesMunicipality Fees Contributions

MUNICIPALITY TAXESMUNICIPALITY TAXES

Property Tax

Property Tax

Property Tax

Property Tax

Property Tax

Property Tax

Property Tax

Property Tax

Property Tax

02468

101214%

1991 1992 1993 1994 1995 1996 1997 1998

REVENUES OF GREATER CITY REVENUES OF GREATER CITY MUNICIPALITIESMUNICIPALITIES

A certain percentage of the general budget taxes A certain percentage of the general budget taxes collected within the boundaries of their provinces collected within the boundaries of their provinces (derivation principle). The Council of Ministers has (derivation principle). The Council of Ministers has the authority to determine this share between 3-6 the authority to determine this share between 3-6 percent. 60 percent of this amount is placed in a pool, percent. 60 percent of this amount is placed in a pool, from there it is again disrtibuted to the Greater City from there it is again disrtibuted to the Greater City Municipalities but on a population basis. Municipalities but on a population basis.

35 percent of each municipality (within the 35 percent of each municipality (within the metropolitan municipality) share of general budget metropolitan municipality) share of general budget tax revenues.tax revenues.

50 percent of the Electricity and Gas Tax.50 percent of the Electricity and Gas Tax. Contribution to expenditures.Contribution to expenditures. 20 percent of the Property Tax collected by the 20 percent of the Property Tax collected by the

municipalities within their boundaries. Recently the municipalities within their boundaries. Recently the Property Tax has been increased by 100 percent in Property Tax has been increased by 100 percent in municipalities within the boundaries of the Greater municipalities within the boundaries of the Greater City Municipalities, this share also being transferred City Municipalities, this share also being transferred to the metropolitan municipalities. to the metropolitan municipalities.

Grants from other public administrations, external Grants from other public administrations, external and internal borrowing, bond issuing, revenues from and internal borrowing, bond issuing, revenues from the selling and renting of immovables, use charges, the selling and renting of immovables, use charges, etc.etc.

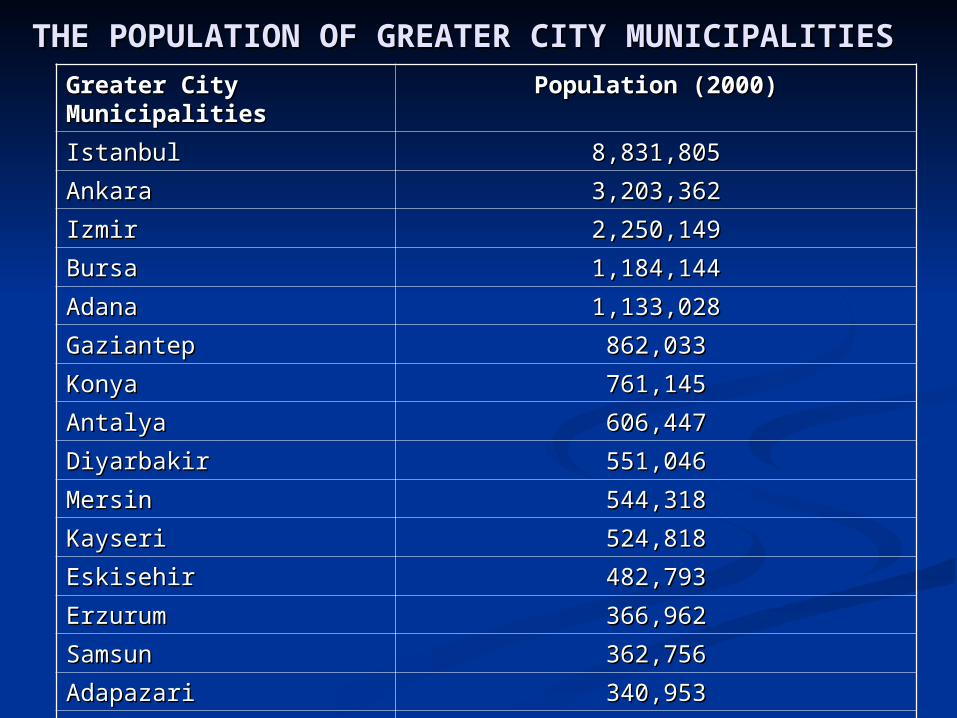

THE POPULATION OF GREATER CITY THE POPULATION OF GREATER CITY

MUNICIPALITIESMUNICIPALITIES Greater City Greater City MunicipalitiesMunicipalities

Population (2000)Population (2000)

IstanbulIstanbul 8,831,8058,831,805

AnkaraAnkara 3,203,3623,203,362

IzmirIzmir 2,250,1492,250,149

BursaBursa 1,184,1441,184,144

AdanaAdana 1,133,0281,133,028

GaziantepGaziantep 862,033862,033

KonyaKonya 761,145761,145

AntalyaAntalya 606,447606,447

DiyarbakirDiyarbakir 551,046551,046

MersinMersin 544,318544,318

KayseriKayseri 524,818524,818

EskisehirEskisehir 482,793482,793

ErzurumErzurum 366,962366,962

SamsunSamsun 362,756362,756

AdapazariAdapazari 340,953340,953

IzmitIzmit 195,193195,193

YearsYears Metropolitan Metropolitan Municipality Municipality

Revenues/MunicipRevenues/Municipality Revenues (%)ality Revenues (%)

19911991 37,837,8

19921992 37,537,5

19931993 37,937,9

19941994 43,443,4

19951995 40,740,7

19961996 40,640,6

19971997 42,242,2

19981998 38,838,8

AverageAverage 39,839,8

The share of metropolitan The share of metropolitan municipality revenues in municipality revenues in total revenues of total revenues of municipalities is around 40 municipalities is around 40 percent on average.percent on average.

GENERAL BUDGET TAX REVENUES/TOTAL GENERAL BUDGET TAX REVENUES/TOTAL REVENUES (%)REVENUES (%)

YeaYearsrs

AdaAdanana

AnkarAnkaraa

AntalAntalyaya

BursBursaa

DiyarbaDiyarbakirkir

ErzuruErzurumm

EskiseEskisehirhir

G.anteG.antepp

IstanbIstanbulul

IzmiIzmirr

IzmiIzmitt

KayseKayseriri

KonyKonyaa

MersiMersinn

SamsSamsunun

19919944

74,74,66

35,235,2 53,253,2 7777 63,763,7 50,550,5 58,658,6 32,832,8 67,767,7 29,29,66

25,25,88

49,149,1 57,657,6 51,551,5 --

19919955

80,80,22

4848 15,615,6 62,62,11

59,259,2 49,149,1 55,155,1 4040 75,475,4 54,54,33

29,29,44

37,337,3 59,659,6 61,661,6 64,364,3

19919966

77,77,33

64,864,8 40,640,6 68,68,99

6363 50,650,6 66,166,1 40,140,1 7979 42,42,55

15,15,22

40,840,8 47,647,6 77,777,7 66,866,8

19919977

3131 62,562,5 33,833,8 6969 55,255,2 62,462,4 68,468,4 57,657,6 67,267,2 30,30,99

25,25,77

47,747,7 38,438,4 71,971,9 57,357,3

19919988

55,55,44

78,878,8 44,344,3 44,44,44

43,543,5 65,765,7 60,260,2 48,648,6 73,273,2 33,33,55

25,25,77

42,942,9 42,942,9 80,180,1 49,149,1

19919999

28,28,99

80,180,1 3939 5353 52,152,1 52,152,1 59,659,6 53,853,8 68,968,9 39,39,77

48,48,55

43,643,6 38,338,3 7474 58,258,2

20020000

16,16,22

84,984,9 53,553,5 31,31,99

61,661,6 47,547,5 60,560,5 58,158,1 75,575,5 67,67,77

64,64,99

4848 32,532,5 75,175,1 51,951,9

BORROWING/TOTAL REVENUESBORROWING/TOTAL REVENUES(%)(%)

YeaYearsrs

AdaAdanana

AnkarAnkaraa

AntalAntalyaya

BursBursaa

DiyarbaDiyarbakirkir

ErzuruErzurumm

EskiseEskisehirhir

G.anteG.antepp

IstanbIstanbulul

IzmiIzmirr

IzmiIzmitt

KayseKayseriri

KonyKonyaa

MersiMersinn

SamSamsunsun

19919944

00 55,855,8 00 00 1,61,6 14,514,5 00 12,112,1 15,515,5 60,60,44

71,71,77

00 00 2222 --

19919955

00 40,540,5 63,363,3 6,56,5 18,418,4 18,518,5 00 0,40,4 1,11,1 28,28,22

63,63,44

00 00 00 00

19919966

00 25,825,8 26,726,7 3,73,7 00 0,70,7 00 00 00 36,36,88

81,81,77

00 00 0,60,6 00

19919977

60,60,22

11,311,3 2727 1,81,8 00 00 00 00 4,64,6 53,53,55

40,40,55

00 00 00 00

19919988

28,28,99

5,55,5 0,80,8 37,37,77

00 00 00 00 1,91,9 52,52,99

49,49,77

00 00 00 6,36,3

19919999

59,59,66

0,50,5 11,611,6 19,19,88

4,14,1 00 00 1,71,7 7,27,2 17,17,11

1616 00 00 00 8,78,7

20020000

74,74,22

00 5,85,8 44,44,55

00 00 00 00 7,27,2 7,27,2 2,22,2 00 00 00 77

CONCLUDING REMARKSCONCLUDING REMARKS Central control of local governments is causing Central control of local governments is causing

inefficiencies, delaying the decisions and acts of these inefficiencies, delaying the decisions and acts of these administrations, thus leading to cost increases. Local administrations, thus leading to cost increases. Local governments should have more administrative and fiscal governments should have more administrative and fiscal autonomy. autonomy.

New accounting systems and budget classifications are New accounting systems and budget classifications are necessary in order to be able to view the real revenue and necessary in order to be able to view the real revenue and expenditure structure of local governments.expenditure structure of local governments.

The transfer system, based on population criteria, is simple The transfer system, based on population criteria, is simple and objective, providing stability and predictability in local and objective, providing stability and predictability in local government revenues. But the population criteria alone is government revenues. But the population criteria alone is not efficient; other criteria such as lenght of roads within not efficient; other criteria such as lenght of roads within local governments, ratio of day/night population, average of local governments, ratio of day/night population, average of summer and winter population etc. should be considered. In summer and winter population etc. should be considered. In order to accomplish this distribution a detailed data bank is order to accomplish this distribution a detailed data bank is necessary.necessary.

Article 73 of the Constitution stipulates that “taxes, duties, Article 73 of the Constitution stipulates that “taxes, duties, and other such financial impositions shall be imposed, and other such financial impositions shall be imposed, amended, or revolved by law” which means that only the amended, or revolved by law” which means that only the Turkish Grand National Assembly has this power. As a result Turkish Grand National Assembly has this power. As a result local governments are not empowered to set and adjust local local governments are not empowered to set and adjust local tax bases and rates. This article has to be changed in order tax bases and rates. This article has to be changed in order to enable them to set and/or adjust their own rates and thus to enable them to set and/or adjust their own rates and thus obtain a buoyant revenue structure meeting their service obtain a buoyant revenue structure meeting their service needs.needs.

Local government reforms aim to meet the revenue Local government reforms aim to meet the revenue demands of local governments through increased demands of local governments through increased allocations from the central government budget. But, allocations from the central government budget. But, for the moment, this does not seem possible because for the moment, this does not seem possible because of macroeconomic fiscal pressures. Besides, this of macroeconomic fiscal pressures. Besides, this structure does not stimulate local govenments efforts structure does not stimulate local govenments efforts to raise their own revenues. Central funding should to raise their own revenues. Central funding should be replaced by locally controlled taxes, fees and user be replaced by locally controlled taxes, fees and user charges. This will strenghten the link between charges. This will strenghten the link between taxation and spending, leading to accountability and taxation and spending, leading to accountability and more participation by local residents.more participation by local residents.

There are a wide variety of local taxes an fees. Some There are a wide variety of local taxes an fees. Some of these are costly to administer and generate small of these are costly to administer and generate small amounts of revenue. These types of revenues should amounts of revenue. These types of revenues should be eliminated. On the other hand, new mass be eliminated. On the other hand, new mass productive taxes that strengthen the revenue productive taxes that strengthen the revenue structure of local governments should be introduced structure of local governments should be introduced (e.g. a tourist tax, a share of the motor vehicle tax). In (e.g. a tourist tax, a share of the motor vehicle tax). In addition, the fixed amounts of taxes and fees should addition, the fixed amounts of taxes and fees should be updated, and a rate of revaluation should be be updated, and a rate of revaluation should be applied annually on these amounts. applied annually on these amounts.

Paralel to these reforms, the financial management Paralel to these reforms, the financial management system of local governments should be strengthened.system of local governments should be strengthened.