Embed Size (px)

Citation preview

Financial Planning & Wealth Management

By CA Rajkumar S Adukia09820061049/09323061049

Financial Planning and Wealth Management 1

Explaining the essence of Financial Planning & Wealth Management

Exploring Investment Planning/Wealth Management

Knowing about Asset Allocation Do’s and Don’ts Mantras in Financial

Planning and Wealth Management Investor Risk Awareness

Financial Planning and Wealth Management 2

Agenda

INDIAN FINANCIAL SYSTEM

Money Market Instrume

nt

Capital Market

Instrument

Forex Market

Capital Market

Money Market

Credit Market

Primary Market

Financial Instruments

FinancialMarkets

FinancialIntermediarie

s

Secondary Market

Regulators

Financial Planning and Wealth Management 3

Financial Planning and Wealth Management 4

What is Financial Planning?

Financial Planning and Wealth Management 5

Steps in Financial Planning

Salary Earners – Government/Private Self Employed/Entrepreneurs/Traders Professionals Others – Students, Housewives, Retired Individuals

They can further be categorized into Beginners Middle Level Final Level

Financial Planning and Wealth Management 6

Categorizing Individual Investors

Every month Salary is wealth accumulation Rule of Thumb : Always hold 3 months salary

in savings (job change/delay in payout) Beginners: Be more aggressive (no or less

liabilities, consistent income level) Mid career people – Be Moderate ( more

liabilities, commitments) HNIs – A balance of Moderation and

Aggressiveness ( More Money)

Financial Planning and Wealth Management 7

Salary Earners

Investment – Own Funds/Borrowed Funds Average of Income Earned every month Insurance cover for business and personal

needs Surplus funds on savings Funds for further investment in business Loan repayment

Financial Planning and Wealth Management 8

Self Employed/ Entrepreneurs/Traders

Average earnings every month Loans for setting up Professional Practice

and its repayment Monthly commitments Surplus savings Fund for further investment Investment in Real Estate Sole proprietorship/ Firm/Company

Financial Planning and Wealth Management 9

Professionals

Housewives and Retired individuals should choose investments that are safe, followed by returns and liquidity. Tax saving aspect of the investment is less important

Students should invest in very safe securities that can also yield them high returns, liquidity and tax saving aspects can be given lesser importance

Financial Planning and Wealth Management 10

Others – Students, Housewives, Retired Individuals etc

Financial Planning and Wealth Management 11

A way to plan

A Plan is a Must!

Where Am I Now? Net Worth (Assets – Liabilities) Personal Budget

Where Do I Want to Go? Goals and Objectives

Major Purchase, Children’s Education, Retirement, Marriage, Vacation

How Do I Get There? Recommendations and Implementation The Plan!

Tax Planning Insurance Planning Retirement Planning Estate Planning Investment Planning/Wealth Management

Financial Planning and Wealth Management 12

Categorizing Financial Planning

Financial Planning and Wealth Management 13

Tax Planning

Financial Planning and Wealth Management 14

Tax Saving SectionsSection Quick Description Limit

80 CCC Pension Products Maximum Rs 1 lakh deduction for 80 C, CCC and 80 CCD put together

80 CCD C. Govt Employees Pension scheme

Maximum Rs 1 lakh deduction for 80 C, CCC and 80 CCD put together

80D Premium Paid on Medical Insurance for Family and Parents

Deduction between Rs 15,000-20,000, additional deduction of 15,000 for parents and Rs, 20,000 if they senior citizens

80 DD Maintenance and medical treatment of disabled dependent

Deduction upto Rs 1 lakh

80 DDB Treatment of Certain disease or ailment

Deduction upto Rs.60,000

80U Physically Disabled Assessee Deduction upto Rs 1 lakh

Financial Planning and Wealth Management 15

Tax Saving SectionsSection Quick Description Limit

80G Donation to certain charitable fund, institutions etc

50% to 100% of donation made subject to a max of 10%of gross annual income

80 GGA Donations for scientific research or rural development

100% deduction allowed to donations made to scientific research Sec 80GGC

80 GGC Donation to Political Parties Deduction upto Rs 60,000

80 E Interest Payable on Educational loan

No limit for deduction

80 EE Interest payable on housing loan Additional deduction up to Rs 1 lakh

80 GG For paying rent in case of no HRA Deduction upto Rs,24,000

80 CCG RGESS Deduction upto Rs 25,000 (50% of amount invested)

80TTA Interested received in Saving Bank Account

Deduction upto Rs 10,000

Financial Planning and Wealth Management 16

80CCG: Investment under any Equity Saving Scheme

Eligibility: Individual Acquires listed equity shares/ units in

accordance with the central government notified Scheme i.e Rajiv Gandhi Equity Savings Scheme,

maximum deduction: 50% of amount invested or Rs 25000/- whichever is less.

Financial Planning and Wealth Management 17

Invest in Equity Scheme and Save Tax

Our risks include Our Lives Medical Contingencies Assets

Insurance Planning the 1st Step Opting for adequate life insurance cover is essential Insurance requirement to be reviewed every 2 years Insurance secures our

Future Finances Loved Ones

Financial Planning and Wealth Management 18

Insurance and Health Planning

Term Insurance Whole Life Policy Endowment Policy Money Back Policies Annuities and Pension Unit Linked Insurance Plan Postal Life Insurance Riders: Comprehensive Coverage

Financial Planning and Wealth Management 19

Types of Life Insurance Policy

Covers employees of Central and State Governments, Central and State Public Sector Undertakings, Universities, Government aided Educational institutions, Nationalized Banks, Local bodies etc. Officers and staff of the Defence services and Para-Military forces

Upper limit Rs 10 lacs all schemes put together Offers Single as well as Group Insurance The policy can be assigned to Financial Institutions for taking

loan. Issue of Duplicate Policy Bond in case of the original Policy Bond

is lost Intra conversion of policies allowed

Financial Planning and Wealth Management 20

Postal Life Insurance (PLI)

PLI offers 7 (Seven) types of plans: Whole Life Assurance (SURAKSHA) Convertible Whole Life Assurance (SUVIDHA) Endowment Assurance (SANTOSH) Anticipated Endowment Assurance

(SUMANGAL) Joint Life Assurance (YUGAL SURAKSHA) Scheme for Physically handicapped persons Children Policy

Financial Planning and Wealth Management 21

Postal Life Insurance (PLI)

RPLI offers following types of plans: Whole Life Assurance ( GRAMA SURAKSHA) Convertible Whole Life Assurance (GRAMA SUVIDHA) Endowment Assurance ( GRAMA SANTOSH) Anticipated Endowment Assurance (GRAMA SUMANGAL) GRAM PRIYA Scheme for Physically handicapped persons

Min Sum Assured Rs.10,000 & Max Sum Assured Rs.3,00,000/- Max age limit of entry is 55 years in case of Whole Life and

Endowment Assurance while it is 45 years otherwise. All the schemes have compulsory medical examination. For the non-medical policies, the maximum limit of Sum

Assured is Rs.25,000/-, and maximum age is 35 years. Non-standard age proof for Rural PLI policies, the maximum

age limit is 45 years

Financial Planning and Wealth Management 22

Rural Postal Life Insurance (RPLI)

Salaried professionals in Private Sector are not eligible but they can have RPLI policies subject to fulfilling other conditions.

If one spouse is working in a Government Organization but the other is not, there is 'Yugal Suraksha' scheme under which both can jointly get a policy

If one quits the Government service, one can continue by making payment at any one of the 1, 55,000 post offices throughout the country

If the premia are not paid for 6 months in case policy is in currency for 3 years (or) 12 months in case policy is more than 3 years old, then the policy becomes void.

No Home Loan available Revival shall not be allowed on more than two occasions during the

entire term of the policy. One forgets to pay one’s premium in a month, then one can

pay the premium in the subsequent month, by paying a minimum fine of Re. 1/- per hundred of sum assured.

Surrender value depends on the surrender factor and type and term of policy

Financial Planning and Wealth Management 23

Points on PLI

Anyone

Professional opportunity for Chartered Accountants

CAs can also take up this role given their understanding of the benefits of the insurance and client base and interaction

Chartered Accountants advice is much valued upon

Financial Planning and Wealth Management 24

Who can become Insurance Brokers?

Financial Planning and Wealth Management 25

Retirement PlanningAllocation of finances for RetirementNo Government sponsored retirement planNuclear FamiliesUnforeseen Medical expensesEstate Planning The Flexibility to Deal with ChangesSystematic investment every month is a

way to a tension free healthy retirement.

Decide of age for retirement Annual income need for retirement years Current market value of all the savings and

investments Determine a realistic annualized rate of return Consider company pension plan if any Now compute the value required on retirement

Financial Planning and Wealth Management 26

Retirement Planning - Steps

Public Provident Fund (PPF) National Savings Certificate (NSC) Employees Provident Fund (EPF) Mutual Fund Products Insurance Products New Pension Schemes Reverse Mortgage

Financial Planning and Wealth Management 27

Retirement Investment Options

1.Bajaj Allianz – Suvarna Vishranti2.ING Vysya – ING New Best Years3.ICICI Pru – ICICI Pru Forever Life4.HDFC Life – Classic Pension Plan5.Metlife – Met Pension-Par6.Kotak Life – Retirement Income Plan7.SBI Life – Lifelong Pension Plus (NP)

Financial Planning and Wealth Management 28

Traditional Retirement Insurance Schemes

8. Tata AIG – Life Nirvana9. Aviva – Pension Builder10.Sahara Life – Sahara Amar Jeevan11.Bharti Axa – Wonder Years Retirement Plan12.Future Generali – Pension Plus13.Aegon Religare – Pension Plan14.IDBI Federal – Retiresurance Guaranteed

(NP)15.Birla Sunlife – Secure 58 Plan (NP)

Financial Planning and Wealth Management 29

Traditional Retirement Insurance Scheme

Accumulating and Disposing of an estate to maximize the goals of the estate owner.

Distribute wealth to a certain beneficiary or beneficiaries to whomever the owner wishes.

Important to take the help of an attorney experienced in estate law

Financial Planning and Wealth Management 30

Estate Planning

Asset transfer to beneficiaries Tax- effective transfer Planning in case of disabilities Time of distribution can be pre-decided Business succession Selection of Trustee or guardian or the

executor

Financial Planning and Wealth Management 31

Estate Planning Objectives

Steps Listing of assets and liabilities Open family discussion on selecting the guardian Update the current beneficiaries like life insurance Decide upon the distribution of the assets on death Funeral arrangements with spouse and family Assistance of an estate planning authority

Tools Life Insurance Will Trust

Financial Planning and Wealth Management 32

Steps and Tools in Estate Planning

Power of Attorney Wills Title Deed Trust Deed Partition Deed Gift Deed Insurance Papers

Financial Planning and Wealth Management 33

Documentation

Elements of Wealth Management Asset Allocation

Financial Planning and Wealth Management 34

Wealth Management

It is all about weaving an investment net with Equity Fixed Income Deposits Post Office Schemes Gold Commodities Currency

Financial Planning and Wealth Management 35

Investment and Wealth Planning

Derivatives Mutual Funds Exchange Traded Funds Real Estate Alternative Investment Investment Options for Non-Resident Indians

Financial Planning and Wealth Management 36

Investment and Wealth Planning

Financial Planning and Wealth Management 37

The Right Asset Mix

Asset mix is the balance between stocks, bonds and cash, returns and risk level monitor

Stocks - greater growth & greater volatility Gold – the bumper crop Mutual Funds – the fund equalizer EFTs – the norm Real Estate – the cash cow

Financial Planning and Wealth Management 38

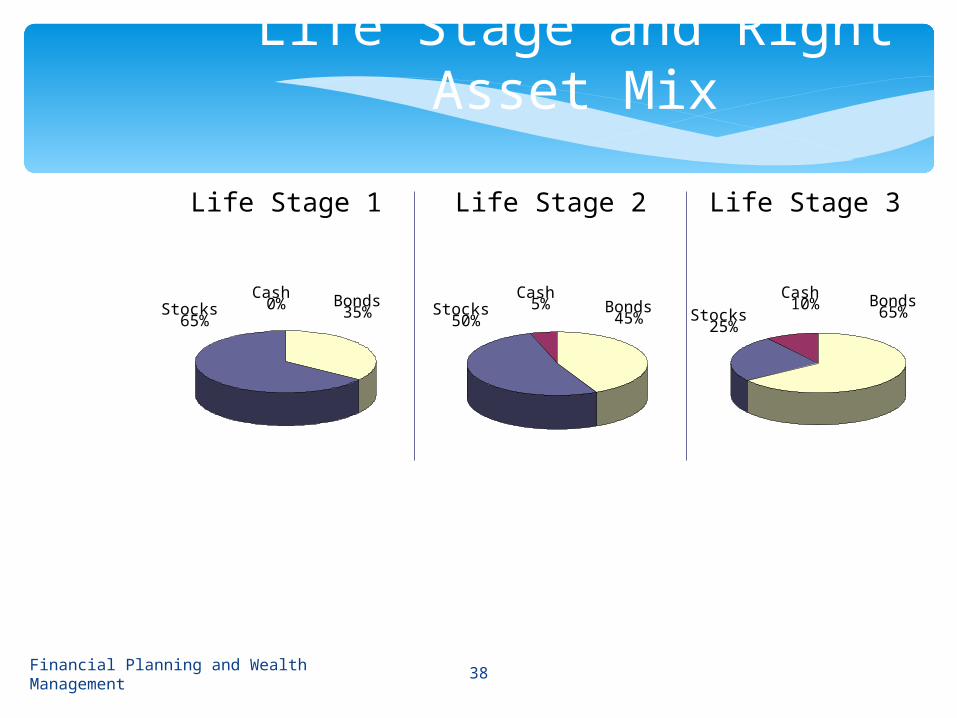

Life Stage and Right Asset Mix

Life Stage 1

Cash 0%Stocks

65%Bonds35%

Life Stage 2

Cash 5%Stocks

50%Bonds45%

Life Stage 3

Cash 10%

Stocks 25%

Bonds65%

Financial Planning and Wealth Management 39

Portfolio Management – A Balance

Containing all the asset classes in well balanced proportion.

Example of well balanced portfolio. – Equity 30% – Debt 30% – Gold 10% – Real Estate 30%

Find the best that suits you!

Comprises of – Shares & Stocks

Variety – Blue Chip, Growth Stocks, Income Stocks, Cyclical Stocks, Defensive Stocks, Speculative stocks

Advantage – Greater returns, diversification, liquidity, information, tax benefits, appreciation, dividends, pledge, voting

Regulator – BSE, NSE,

Markets – Primary & Secondary, Online Trading

Investors – Retail Institutional Investors, Non Institutional Investors, Qualified Institutional Buyers

Financial Planning and Wealth Management 40

Asset Allocation - Equity

India is the largest market for gold in the world Total consumer demand in India stood at US$ 44920

million for 12 months ended Q1 2012 International Currency Why invest in Gold??

Diversification Low Liquidity Risk Hedge against Inflation Good Returns Low Credit Risk Safe Haven Investment

Financial Planning and Wealth Management 41

Asset Allocation – Gold

Avenues of Investment1. Jewellery2. Gold Coins3. Gold Bars4. ETF5. Global Mutual Fund6. Gold Fund of Fund7. Gold Derivatives (Futures) through MCX8. E-Gold9. Gold Accumulation Schemes/Savings for Gold

Scheme10.Gold Deposit Scheme

Financial Planning and Wealth Management 42

Asset Allocation – Gold

Types – Government Securities, Public Sector Bonds, Private Sector Bonds

Varieties – Government Guaranteed Bonds, Zero Coupon Bonds, Treasury Bills, STRIPS, PSU Bonds, Commercial Paper, Debentures, Floating Rate Bonds, Inter Corporate Deposits, Certificate of Deposits

Status of Holding – Investors are Creditors to the Issuer

Market – Debt Market (WDM, RDM, G-secs) Types of Trade – Outright Sale or Purchase, Repo Trade Regulator - RBI

Financial Planning and Wealth Management 43

Asset Allocation – Fixed Income

Certificate of Deposit (CD) Commercial Paper (C.P) Inter Bank Participation Certificates (IBPC) Inter Bank term Money Treasury Bills Bill Rediscounting Call/Notice/Term Money

Financial Planning and Wealth Management 44

Money Market Instruments

Are short term borrowings by Corporates, FIs, Primary Dealers (PDs) from Money Market

CP when issued in physical form are negotiable by endorsement and delivery

Issued subject to min 5 lacs and in multiples of 5 lacs thereafter

Maturity 15 days to 1 year Unsecured and backed by the credit of the issuing

company Any private or public sector companies willing to raise

money through the CP market has to meet the following requirements

Financial Planning and Wealth Management 45

Commercial Papers

Classification of bank deposits Savings Bank Account Current Deposit Account Fixed Deposit Account Recurring Deposit Account

Fixed Deposit interest rates in India vary anywhere between 7.00 % to 9.25%

Monitoring maturity dates Policy Changes by RBI

Financial Planning and Wealth Management 46

Private Banking

Post Office Savings Account Post Office Recurring Deposit Account Post Office Monthly Income Accounts National Savings Certificate (VIII Issue) Kisan Vikas Patra Senior Citizen Saving Scheme (SCSS) Public Provident Fund Scheme Deposit Scheme for Retiring Government

Employees Deposit Scheme for Retiring Employees of Public

Sector CompaniesFinancial Planning and Wealth Management 47

Asset Allocation – Post Office Schemes

Minimum investment per financial year in PPF is Rs 500/- and w.e.f 1.12.2011 the maximum limit has been raised to Rs 1 lakh

Not more than one PPF account in one’s name PPF a/c can be extended for any number of

times after the expiry of its tenure of 15 years.

The extensions will be for the block of 5 years. Interest rate in PPF announced every year in

April. Nomination facility is available in PPF PPF has 15 years lock-in but you can get a loan

and also opt for premature withdrawal after a certain period of time.

Financial Planning and Wealth Management 48

PPF – Public Provident Fund

No HUF or association of person is allowed to open PPF a/c.

Non Resident Indian (NRI) cannot open a new Public provident fund account in India.

The PPF scheme is operated through Post Office and Nationalized banks.

Pvt Banks like ICICI bank offers this account. Deposits are exempt from wealth tax. The balance amount in PPF account is not subject

to attachment under any order or decree of court in respect of any debt or liability,

Financial Planning and Wealth Management 49

PPF – Public Provident Fund

Allow a portfolio to improve overall return at the same level of risk

Who should invest? Any investor who wants to take advantage of price movements

A kicker (side card) in the portfolio

Financial Planning and Wealth Management 50

Asset Allocation - Commodities

Commodity market in India clocks a daily average Turnover of Rs 120 – 150 billion (Rs 12,000 – 15,000 crores

Forward Markets Commission Regulates commodity trading

Demand and Supply factor and Inventory drive the commodity market

Financial Planning and Wealth Management 51

Asset Allocation - Commodities

Major Categories of Commodities Traded Industrial Metals Precious Metals: Bullion Agricultural Commodities Energy Commodities

Commodity Spot Market Offers effective method of spot price discovery Processors, end users. exporters, corporate procure

agri produce from here Helps in Futures exchange Promotes grading and standardization in agricultural

produce

Financial Planning and Wealth Management 52

Asset Allocation - Commodities

Commodities are traded in National Spot Exchange (NSEL) NCDEX Spot Exchange (NSPOT)

Commodities Derivative Market A derivative instrument whose value is derived

from the underlying commodity Example: an investor can invest directly in a

steel derivative rather than investing in the shares of Tata Steel

Financial Planning and Wealth Management 53

Asset Allocation - Commodities

Where do I need to go to trade in Commodity Futures? National Commodity and Derivative Exchange

(NCDEX) Multi Commodity Exchange of India Ltd (MCX) National Multi Commodity Exchange of India Ltd

(NMCE) ACE Derivatices and Commodity Exchange (ACE) Indian Commodity Exchange Limited (ICEX)

Financial Planning and Wealth Management 54

Asset Allocation - Commodities

Major categories of commodities one can trade Vegetable Oil Seeds, Oils and Meals Pulses Spices Metals Energy products Vegetables Fibres and Manufactures- Cotton Other – Gaurseed, Guar, Gum and Sugar

Financial Planning and Wealth Management 55

Asset Allocation - Commodities

While trade in international, currencies are national Exchange rate is affected by the suppy and demand

for the country’s currency in the international forex market

Trading in Currency Futures allowed on 3 exchanges Multi Commodity Exchange – Stock Exchange (MCX-

SX) National Stock Exchange (NSE) United Stock Exchange (USE)

Financial Planning and Wealth Management 56

Asset Allocation – Currency

Currency Options are contract that grant the buyer of the option the right and not the obligation to, to buy or sell underlying currency at a specified exchange rate during a specified period of time

USD-INR Option European Call & Put Options

Financial Planning and Wealth Management 57

Asset Allocation – Currency

Financial contracts which derive their value from a spot price called the underlying

Derivative Instruments traded are Futures and Options Derivative Exchange/Segment function as a Self

Regulatory Organization and SEBI Acts as the oversight regulator

Futures contracts, Index Options, Stock options, Stock Futures, Mini Derivative contract on Index, Long tenure Index Option contracts, Volatility Index, Bond Index and Exchange traded Currency Derivatives are permitted by SEBI

Financial Planning and Wealth Management 58

Asset Allocation – Derivatives

Equity Linked Savings Scheme Arbitrage Funds Dynamic Funds Fixed Maturity Plans International Mutual Funds Monthly Income Plans Multi Cap Funds Quant Funds

Financial Planning and Wealth Management 59

Asset Allocation – Mutual Funds

Guidance on Purchase of Property Planning and Budgeting Research Home Loan Safety points in the Home Agreement Home Insurance

Real Estate Investment Includes Agricultural Land Farm Houses Urban Land House Property Commercial Property

Financial Planning and Wealth Management 60

Asset Allocation – Real Estate

Real Estate Investment Options in India Investment in Real Estate Stocks Investment in Property

Financial Planning and Wealth Management 61

Asset Allocation – Real Estate

Durability Heterogeneous High transaction costs Long time delays Both an investment good and consumption

good Immobility

Financial Planning and Wealth Management 62

Unique characteristics of Real Estate

Identifying Your Needs Independent House or Apartment Budget Number of rooms and bathrooms Approximate Area Proximity to work place, school etc Parking availability Water supply, power back up etc Furnished/unfurnished Connectivity Vicinity to market Special amenities such as club house, pools or spas. Available utilities such as cable or DSL, satellite. Sewer, cesspool or septic connections

Financial Planning and Wealth Management 63

Home Buying Tips from Start to Finish

Finance Own funds Loan from Banks/HFCs Funds from your employer Loan against assets Provident Fund Loan

Scouting for property Brokers Newspapers Websites Word of mouth

Financial Planning and Wealth Management 64

Home Buying Tips from Start to Finish

Cost Estimate Purchase Price Stamp duty Registration charges Khata transfer charges Utility Deposits like Water connection deposit, Electricity connection deposit,

etc. Other incidental expenses

Talk to Banks/HFCs

Loan Amount Loan Eligibility Terms and conditions of loan Interest Rate Borrowing costs like processing fee, commitment charges, prepayment

penalty, etc. Loan tenures and EMI Time taken for sanctioning the loan Time taken for disbursing the loan Freebies and corporate offers

Financial Planning and Wealth Management 65

Home Buying Tips from Start to Finish

Short listing Properties• Site or property visit• Speaking to the neighbors or occupants• Clear marketable titles• Credibility of the seller• Quality of the construction• Legal verification• Monthly payouts like maintenance charges, society charges, etc.• Municipal taxes or property taxes

Finalizing the Deal• Negotiate on price and timing of payments ( upfront / installments) Press for price negotiation if there are any modifications /repairs /painting

to be done Do not forget to collect all original property documents from the seller Before paying the seller, make sure he has fulfilled all his commitments and

promises If the transaction involves a broker, withhold some amount of money until

he delivers as promisedFinancial Planning and Wealth Management 66

Home Buying Tips from Start to Finish

Documents required when the property is purchased from a builder An allotment letter from the developer on paying the booking

amount Agreement for Sale

Documents required to be checked if you are buying a resale flat For flats being purchased in a registered co-operative society For flats being purchased in an unregistered society or flats

originally allotted by a Development Authority Check the credentials of your new property

Invitation of Claims Search at the Sub-Registrar's Office Enquiry at Municipal Corporation Enquiry with the Ward office If the owner of the property is deceased

Financial Planning and Wealth Management 67

Home Buying Tips from Start to Finish

Property Documents to be collected from the Seller

In case of a direct purchase from a builder

1. Copy of Agreement for Sale.2. Copy of Registration Receipt. 3. Copies of receipts of payment already made.4. NOC from builders.

In case of direct allotment in a Co-operative Housing Society

1. Allotment letter.2. Share certificate.3. Society registration certificate.4. Copy of sale/lease deed in favour of the society.5. NOC from society

Financial Planning and Wealth Management 68

Home Buying Tips from Start to Finish

In case of direct allotment in a Co-operative Housing Society by Public Agency

1. Allotment letter, Share certificate, Society Registration certificate.2. Lease Agreement.3. Public agency's approved list of members.4. NOC from Public Agency in favour of bank/HFC5. NOC from society.

In case of Public Agency's allotment to individuals

1. Allotment letter from Public Agency.2. Tripartite Agreement between the borrower, Bank/HFC and the

Public Agency in the prescribed format.

In case of resale

1. Copy of all previous vendors' registered documents along with copy of your purchase agreement duly stamped and registered and the registration receipt wherever applicable.

Financial Planning and Wealth Management 69

Home Buying Tips from Start to Finish

Purchase of rentable properties Location Numbers High home prices Low maintenance buildings Ask to see the rental history Owner/Manager out of the country

Financial Planning and Wealth Management 70

Home Buying Tips from Start to Finish

A Buyers/Tenants Checklist Check if Use of Property would amount to Change

of Land Use Check if Non Residential Activity in Residential

Premises Is Permissible Check if the Municipal Guidelines allow Mixed Use Certain Professional Activity permissible in

Residential Areas Check if the Building adheres to the Sanctioned

Plan

Financial Planning and Wealth Management 71

Home Buying Tips from Start to Finish

1. Agreement for Sale of a House2. Agreement for Sale of Mortgaged House3. Agreement To Lease Of Land For Construction Of House4. Agreement for sale of a house when purchase money is to be

paid in installments5. Deed of Conveyance of freehold property6. Deed of Conveyance where consideration is to be paid in

installments7. Deed of Conveyance of Reversion8. Deed of Conveyance Subject to Right of Way9. Deed of Conveyance of an Interest in Property

Financial Planning and Wealth Management 72

List of DocumentsSale and Purchase of House/Building

10. Deed of Conveyance of a Part of the Building11. Sale Deed of Land with Building12. Deed in respect of Leasehold Land13. Deed of a House14. Sale deed by Liquidator in case of Voluntary winding up of a Company15. Sale by Official Liquidator of the company16. Sale of House by an Executor Appointed under Will17. Sale of Property to various Purchasers as Tenants in Commmon18. Sale of Property to various Purchasers in Different Portions19. Statement of Transfer of Immovable Property for Obtaining no-objection

certificate from Appropriate Authority, Income Tax Department Form No 37-I

20. Sale deed

Financial Planning and Wealth Management 73

List of DocumentsSale and Purchase of House/Building

21. Agreement for Sale of Apartment22. Agreement for sale of freehold property23. Agreement for sale of leasehold property24. Agreement for business centre25. Deed of Conveyance subject to mortgage26. Agreement for sale for Purchase of a Plot for

Constructing Flats

Financial Planning and Wealth Management 74

List of DocumentsSale and Purchase of Apartment

27. Development Agreements by Landlords in favour of a Builder

28. Deed of Conveyance of a property exclusive of a flat or floor in the building

29. Agreement to be entered between a Promoter and Purchaser of a Flat

30. Flat ownership Agreement31. Co-ownership Agreement32. Co Sign Agreement

Financial Planning and Wealth Management 75

List of DocumentsSale and Purchase of Apartment

33. Deed of Conveyance by Mortgage34. Deed of Conveyance in favour of Mortgage35. Mortgage deed

Financial Planning and Wealth Management 76

List of DocumentsMortgage

36. Gift Deed37. Gift Of Land Focr Building A Temple38. Gift By Father To His Son Of Land With Mortgage39. Deed Of Gift Of Immovable Property40. Gift Of A House To The Daughter41. Gift Of Property For Specified Purpose42. Gift Of Immovable Property43. Gift Of A Piece Of Land44. Gift Of Property For Hospital45. Gift Of Property To Wife

Financial Planning and Wealth Management 77

List of DocumentsGifts

46. Lease deed47. Lease Deed Of Land48. Lease Of Agricultural Land49. Lease Of A Building For Office50. Deed Of Surrender Of Lease51. Deed Of Renewal Of Lease52. Agreement For Building Lease53. Perpetual Lease Of A Land54. Lease Disguised As Licence55. Sublease Agreement

Financial Planning and Wealth Management 78

List of DocumentsLease

56. Deed of transfer in a co-operative society57. Surrender deed in a Co-operative housing

society58. Agreement for sale of apartment in Co-op.

Society

Financial Planning and Wealth Management 79

List of DocumentsCooperative Society

59. Tenancy Agreement/Rental Agreement60. Tenancy In The Form Of Letter By The

Person Proposing To Take Premises On Rent

Financial Planning and Wealth Management 80

List of DocumentsTenancy

61. Agreement for Transfer of Development Rights62. Package Deal Agreement for Sale of Flats in Bulk to a

Purchaser63. Leave and licence agreement64. Relinquishment Deed65. Family Arrangement66. Deed Of Partition Between Co-Owners67. Deed Of Partition Between Members Of A Joint Hindu

Family 68. General Power of Attorney69. Special Power of Attorney to execute Sale Deed70. Parking Agreement

Financial Planning and Wealth Management 81

List of DocumentsOther Agreements

Financial Planning and Wealth Management 82

List of Applicable Laws in Real Estate

CENTRAL LEGISLATIONS

The Indian Contract Act, 1872 The Majority Act, 1875 The Indian Evidence Act, 1872 The Transfer of Property Act, 1882 The Easement Act, 1882 The limitation Act, 1963 The Indian Stamp Act, 1899 The Registration Act, 1908 The Specific Relief Act, 1963

Financial Planning and Wealth Management 83

List of Applicable Laws in Real Estate

10. The Land Acquisition Act, 189411. The Consumer Protection Act, 1986 12. The Arbitration & Conciliation Act, 1996 13. The Income Tax Act, 196114. The Wealth Tax Act, 195715. The Co-operative Societies Act, 191216. The Multi-State Co-operative Societies Act, 191217. Finance Act in relation to Service Tax18. The Foreign Exchange Management Act, 1999/ Foreign Direct

Investment Guidelines (FDI)19. SEBI norms for Real Estate Mutual Funds20. Competition Act, 2002

Financial Planning and Wealth Management 84

List of Applicable Laws in Real Estate

21. The Land Acquisition, rehabilitation and Resettlement Bill, 2011

22. Special Economic Zone Act, 200523. The Public Premises( Eviction of Unauthorised

Occupants) Act, 197124. The Warehousing ( Development and Regulation) Act,

200725. Indian Succession Act 1925

Private Equity Venture Capital Replacement Capital Buyout Special Situation Risk of investment through PE Role of Stock Market

Financial Planning and Wealth Management 85

Investment Planning – Private Equity

Rare Coins and Paper Currency Stamp Collection Art Antiquities Wine

Financial Planning and Wealth Management 86

Investment Planning – Alternate Investment

Deposit Schemes Investments in Securities and Debt Investment in Mutual Funds Investment in Immovable Assets Investment in Tax saving options

Financial Planning and Wealth Management 87

Investment Options for NRIs

A financial market is a market in which people and entities can trade financial securities, commodities, and other fungible items of value at low transaction costs and at prices that reflect supply and demand.

Financial Planning and Wealth Management 88

FINANCIAL MARKET

Capital Market (Both Stock and Bond Markets)

Commodity Market

Derivative Market

Future Market

Forex Market

Money Market

Insurance Market

Financial Planning and Wealth Management 89

TYPES OF FINANCIAL MARKETS

Financial Planning and Wealth Management 90

Wealth Creator Speculator Hedger Arbitrageur Trader

Financial Planning and Wealth Management 91

Types of Investor

India – Most favored destination for overseas companies

$ 1 trillion economy – Taken 60 yrs Next one trillion will take only 6 years Provides tremendous prosperity amongst

Indians Urgent need for professionals to capture

this rapid growth Huge opportunity for CA’s in this scenario

Financial Planning and Wealth Management 92

India’s Growth Story

Financial Planning and Wealth Management 93

Jargon Of Equity Market

• Security

• Bond

• Stock 1) Common stocks 2) Preferred stocks

• Share

• Mutual funds.

• Par value vs. Market value

• BULLISH vs. BEARISH

Financial Planning and Wealth Management 94

Functioning of Stock MarketFunctioning of Stock Market

•Stock exchanges•Brokers•Registrars•Depositories and their participants •Securities and Exchange Board of India (SEBI) Financial RegulatorsFinancial Regulators

•SEBI•RBI•Ministry of finance

Major source of finance for trade and industry in India

Important external source for meeting funding requirements

Facilitates Transfer of Capital Provides liquidity Transaction price provides a measure of the

value of the asset

Financial Planning and Wealth Management 95

Importance of Capital Market

Financial Planning and Wealth Management 96

Role of Capital Markets

Mobilization of Savings & acceleration of Capital Formation

Promotion of Industrial Growth Raising of long term Capital Ready & Continuous Markets Proper Channelisation of Funds Provision of a variety of Services

Disseminate information efficiently Quick valuation of financial instruments Provide insurance against market risk or

price risk Enable wider participation Provide operational efficiency through - simplified transaction procedure - lowering settlement timings and - lowering transaction costs

Financial Planning and Wealth Management 97

Functions of Capital Market

Screen based Trading through NSE Capital adequacy norms stipulated Dematerialization of Shares - risks of

fraudulent paper eliminated Entry of Foreign Investors Investor awareness programs Rolling settlements Inter-action between banking and

exchangesFinancial Planning and Wealth Management 98

Capital Market – Reforms

Corporatisation of exchange memberships Banning of Badla / ALBM Introduction of Derivative products - Index

/ Stock Futures & Options Reforms/Changes in the margining system STP - electronic contracts Margin Lending Securities Lending

Financial Planning and Wealth Management 99

Reforms – Post 2000

Equity Analyst Media Tracker As an internal control specialist As an taxation expert As an international Accounting Standards

Convergence specialist As an internal auditor

Financial Planning and Wealth Management 100

Role in Capital Market

Investment advisor Profiling and Positioning of the business Formulating Financial Strategy and efficient

capital structure Due Diligence Portfolio Structuring and management Financial Services Marketing

Financial Planning and Wealth Management 101

Role in Capital Market

Market Analysis Auditor Developing capital market

communications Risk management Investment Banker Fund Manager Equity Trader Research Analyst Valuation

Financial Planning and Wealth Management 102

Role in Capital Market

Investment bankers Underwriters Stock exchanges Registrars Depositories Custodians Portfolio managers Mutual funds Primary Dealers / Satellite Dealers Self regulatory organizations

Financial Planning and Wealth Management 103

Internal Audit of Market Intermediaries

Risk Disclosure Documents Contract Notes Internal Audit Report

Financial Planning and Wealth Management 104

Documentation pertaining to Financial Markets

Arbitration - Alternative dispute resolution mechanism provided by stock exchange

Resolving disputes between trading members and their clients in respect of trades done on the exchange

Every exchange - Panel of Arbitrators Option to Choose Arbitrator –

Investors/Broker In case of disagreement - Exchange shall

decide upon the name of arbitrators.

Financial Planning and Wealth Management 105

Arbitration in Financial Markets

Invest only in Fundamentally Strong Companies Read Carefully Follow Life Cycle Investing Invest in IPO Learn to sell Deal with Registered Intermediaries Let not greed make you an easy prey Do not Over-depend on Comfort factors – IPO

Grading Avoid blind decisions based on audited accounts

Financial Planning and Wealth Management 106

Lessons on Wise Investing

Cheap shares are not necessarily worth buying Corporate Governance Awards – still have a thought Be honest Invest and do not speculate Don’t leverage on the market Beware of

Media Advertisements Fixed guaranteed return schemes Grey market premium Sectoral Frenzies Companies where promoters issues shares and warrants to

themselves

Financial Planning and Wealth Management 107

Lessons on Wise Investing

Keep surplus funds in Fixed Deposits for longer duration especially when the interest rates are likely to fall in future

FDs for smaller denominations come handy for immediate cash requirement

Auto sweeps are a great way for fund availability cum savings

Financial Planning and Wealth Management 108

Lessons on Wise Investing

Investor – One who commits money to investment products with the expectation of financial return

Wealth Creator Speculator Hedger Arbitrageur Trader

Financial Planning and Wealth Management 109

Investor Awareness - Investor

Purpose of investment Investment options Investment objectives Care before making investment Market watch after investing Exit at right time

Financial Planning and Wealth Management 110

Basic Awareness

To Raise Capital To Increase Market Exposure To Increase Valuation To Increase Opportunity for Financing To Increase Opportunity for Strategic

Acquisitions Share Liquidity

Financial Planning and Wealth Management 111

Need for Awareness

Market Risk Industry Risk Regulatory Risk Business Risk

Financial Planning and Wealth Management 112

Types of Risks

Portfolio Managers/Wealth Managers / Investment

Advisors (IA) Regulation

Financial Planning and Wealth Management 113

Chartered Accountants Certified Financial Planners Chartered Financial Analyst Management Graduates with specialization in

FinanceProfessional Opportunity for Chartered Accountants Chartered accountants are best suited for this

role given their financial acumen and knowledge in tax and laws

Financial Planning and Wealth Management 114

Who can become Portfolio Managers?

On January 21, 2013 SEBI issued The (Investment Advisors) Regulation 2013

These regulations shall come into force on the 90th day from the date of notification i.e April 20, 2013.

Regulating the activity of Investment Advice Investment Advice – Advice on Investment Products

and Financial Planning Regulation exempts number of intermediaries and

intermediation activities from Registration Consultation on hedging and cash management

services likely to be covered

Financial Planning and Wealth Management 115

Investment Advisors Regulation in India

Registration with SEBI as Investment Advisor (IA)

Subject to fulfillment of certain basic Criteria Minimum educational qualification Affiliation with National Institute of Securities

Market

Financial Planning and Wealth Management 116

Investment Advisors (IA) Registration

Regulation imposes responsibility on IAs Fiduciary responsibility towards client Record keeping Suitability Appropriateness Code of Conduct Disclosures of conflict of interests Segregation of Activities other than investment advisory Payment of Commission

Stock Brokers and Merchant bankers (exempted from IA registration) Are required to comply with provisions relating to

Manner in which clients are to be boarded Investment advice is to be rendered

Financial Planning and Wealth Management 117

Regulation of Investment Advisors

Any member of ICAI, ICSI, ICWAI, Actuarial Society of India or any other professional body as may be specified by the

Board, who provides investment advice to their clients, incidental to his professional service.

Any stock broker or sub-broker registered under SEBI (Stock Broker and Sub-Broker) Regulations, 1992,

Portfolio manager registered under SEBI (Portfolio Managers) Regulations, 1993 or

Merchant banker registered under SEBI (Merchant Bankers) Regulations, 1992, who provides any investment advice to its clients incidental to their primary activity.

Financial Planning and Wealth Management 118

Exemptions

Any fund manager, by whatever name called of a mutual fund, alternative investment fund or any other intermediary or entity registered with the Board;

Any person who provides investment advice exclusively to clients based out of India. Any representative and partner of an investment adviser which is registered under these regulations

Any other person as may be specified by the Board.

Financial Planning and Wealth Management 119

Exemptions

Every applicant shall pay non-refundable application fees of five thousand rupees (Rs. 5,000) along with the application for grant or renewal of certificate of registration.

Applicants which are individuals and firms shall pay a sum of ten thousand rupees (Rs. 10,000) as registration/ renewal fee at the time of grant or renewal of certificate by the Board.

A body corporate shall pay a sum of one lakh rupees (Rs. 1,00,000) as registration/ renewal fee

at the time of grant or renewal of certificate by the Board.

The above fees shall be paid by the applicant within fifteen days (15 days) from the date of receipt of intimation from the Board by a demand draft (DD) in favor of 'Securities and Exchange Board of India' payable at Mumbai or at respective regional or local office.

Financial Planning and Wealth Management 120

Registration Fees

The Applicant for grant of registration as an Investment Adviser under SEBI (Investment Advisers) Regulations, 2013 should make an application to SEBI in Form A

the applicant will receive a reply from SEBI within one month.

Financial Planning and Wealth Management 121

Registration Procedure

In Case of Body Corporates: Net worth of not less than twenty five lakh rupees (Rs. 25, 00,000) “Net Worth" means the aggregate value of paid

up share capital plus free reserves (excluding reserves created out of revaluation) reduced by the aggregate value of accumulated losses, deferred expenditure not written off, including miscellaneous expenses not written off, and capital adequacy requirement for other services offered by the advisers in accordance with the applicable rules and regulations.

In Case of Individuals / Partnership firms: Net tangible assets of value not less than one lakh rupees (Rs. 1, 00,000)

Financial Planning and Wealth Management 122

Capital requirement

Existing investment advisers shall comply with the capital adequacy requirement within one year from the date of commencement of these regulations.

Financial Planning and Wealth Management 123

What about existing investment advisers?

Period of Validity of the Certificate is five years (5 years) from the date of issue.

Renewal of Certificate: Three months before the expiry of the period of validity of the certificate, the Investment adviser may, if he so desires, make an application in FORM-A for grant of renewal of certificate of registration. The renewal application also dealt in the same manner as if investment advisor is applying for the first time.

Financial Planning and Wealth Management 124

Period of Validity

Questions???

Financial Planning and Wealth Management 125

Thank You!!!

Financial Planning and Wealth Management 126