Embed Size (px)

Citation preview

Financial Literacyhttp://www.youtube.com/watch?v=MQyl2ObYKaM

Savings Account• Try to save 10% every month.• Keep 6 months of expenses in savings• Look for best value

Free ATM withdrawals Low monthly rate• Carry extra money (hidden) for emergency• Recommendations:

NCSECU, Allegacy Credit Union

Checking Accounts (Debit Cards)

• Always know how much $$ you have• An overdraft (trying to pay more than what

you have <AKA bounced check>) costs 30$ to bank, 25$ to company and hurts credit score!

• You can opt out of “overdraft” on debit cards but not for “checks.”

Credit Union vs Banks

• Credit Unions are NON-PROFIT. Money earned is passed on to the members. (nicer coin machines, more tellers etc..)

• Banks are FOR PROFIT. Money earned is passed on to share holders. They can offer more services and usually better loans.

Bonds and CD’s

• Government and Banks raise money by selling bonds or CD’s at fixed rates for fixed amount of time. Ex: 5 years at 4%

• Look at Bond ratings for safe investment• Advantages: Safe, known income for a few

years later.• Disadvantages: Locked in for time

Stocks

• Long term investment• Look for low trading fees (Scottrade, Etrade etc..)• Advantages: – Average rate of increase is 7% plus dividends– Can be easily changed into money if needed

• Disadvantage: Not stable growth• Recommendation: Kiplingers Magazine• Dow Jones Index: Price of about 50 stocks• Nasdaq Index: Price of all 3000 stocks (first to use electronic sells)

Mutual Funds• Collection of stocks• Advantages: Balanced Risk• Disadvantages: Cost. Average payment is about

1.1% including some up front costs for some.

• Recommendations: Vanguard or Fidelity• https://investor.vanguard.com/what-we-offer/mutual-funds/costs

Pensions (very few around) to be paid when you retire 401K (through employer; taxes later)Deductable IRA (pay taxes later)Roth IRA (taxes now, not on earnings)

• You invest money that you get when you turn 65.• Some charge taxes now (Roth IRA) and some will

charge taxes later <also on earnings> (401 K)• There is a penalty if you take the money out early.• Advice: If a company matches your donation,

then put the maximum amount in!

Rule of 72

• Doubling $$: Divide 72 by interest rate or years to find the other number.

Ex: 4% interest rate will take 72/4 or 18 years to double. Ex: 10 years to double will take 72/10 or 7.2% interest rate

2 = 1ert

ln (2) = rt .69 = rt so rt = .69

Millionaire!!

• Millionaire: The more you invest now in a positive rate, the more you will have later!

http://www.youtube.com/watch?v=XUCYdGAWcbo

Savings Per Month at 7%

Time to be a Millionaire

$400 39 years$750 31 years$1000 27 years

Ways to save at least 10%!

• Coupons and discounts• Buy for value!• Buy for NEED not WANT• Don’t buy a new car!• Make and follow a budget!• Shop around for best value.• http://www.youtube.com/watch?v=Bf50xx-AnoY

Credit Cards

• 1-2 for now but 3-5 when you get older.• Borrow only what you can pay at the end of the month.• Pay attention to annual fees.• Look for good benefits.• Keep interest rate under 15% • Don’t withdraw money from ATM machines.• Late payment is usually $25, 10% penalty, and lower

credit rating.• Pay more than the minimum if you can’t pay in full.• http://www.youtube.com/watch?v=ebjYlbcWEv4

www.myjourneytomillions.com/articles/horror-of-just-paying-monthly-minimum-payment-credit-cards/&

Mortgages• Make down payment of at least 20% to avoid PMI

(Private Mortgage Insurance)• PMI is extra $600 a year until you have put at

least 20% into your house.• Shop for best mortgage rates. (Calculate points

carefully)• Avoid ARM (Adjustable Rate Mortgages)• Pay extra money to reduce the time on the loan.(100$ extra turns 30-yr loan to 23 years)• 28% is the maximum of your monthly income

that you should put into mortgage (or housing).

Loans

• College loans (Federal Government)• Family member/friend loans (not the best idea)• Don’t borrow too much $$$$ (only what you can

afford to pay back!)• Home Equity Loans (up to 80% of what you have put

into the house)

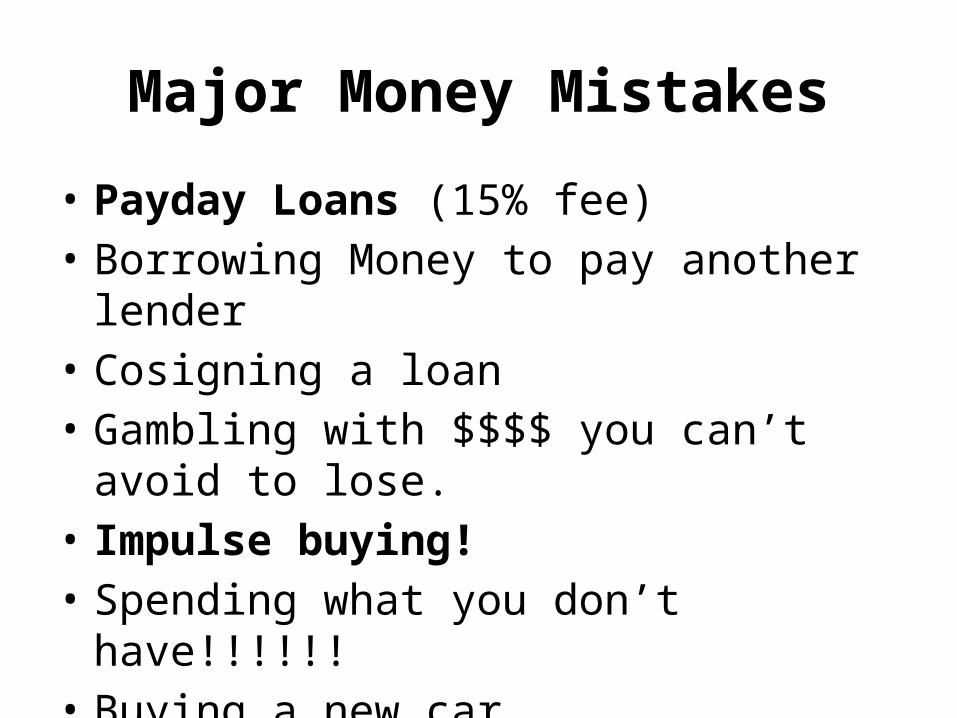

Major Money Mistakes

• Payday Loans (15% fee)• Borrowing Money to pay another lender• Cosigning a loan• Gambling with $$$$ you can’t avoid to lose.• Impulse buying!• Spending what you don’t have!!!!!!• Buying a new car.

Job Searching and Keeping

• It’s not what you know but who you know.• Maintain safe Social Media Sites.• Use correct English when communicating with

prospective employers.• Write a thank-you letter shortly after the

interview.• Stay away from illegal drugs!

Identity Fraud

• Use different passwords.• Pay attention to your bank/credit card

statements.• Never give out your password or Social

Security Number. (Phishing!!!)• Use https and not httphttp://www.youtube.com/watch?v=DuhjKasJA04• Keep copy of passport/license/insurance at home

and one with you when travelling!

Credit/Debit/Gift Card

• Contact institutions if traveling• Keep a copy at home• Keep track of automatic drafts especially if

your card gets cancelled or lost.• Treat Gift cards like $$$ and try to use them

quickly before they get lost or money is debited from non-use.

Credit Score

• Three agencies give credit score based on your history of paying off loans. (200-820)

• Higher Credit Score means more likely that you will get a loan at a lower rate

• Having few credit cards, Paying off credit cards, paying rent, paying car loans etc… ON TIME increases your credit score!

• http://www.youtube.com/watch?v=_9fVnE63bz0

Lower Taxes

• Charity donations (keep receipts)• Deduct “$$ interest” from loans• Put $$ in 401K or IRA’s • Combine winnings and losses in same year (stocks, gambling etc…)

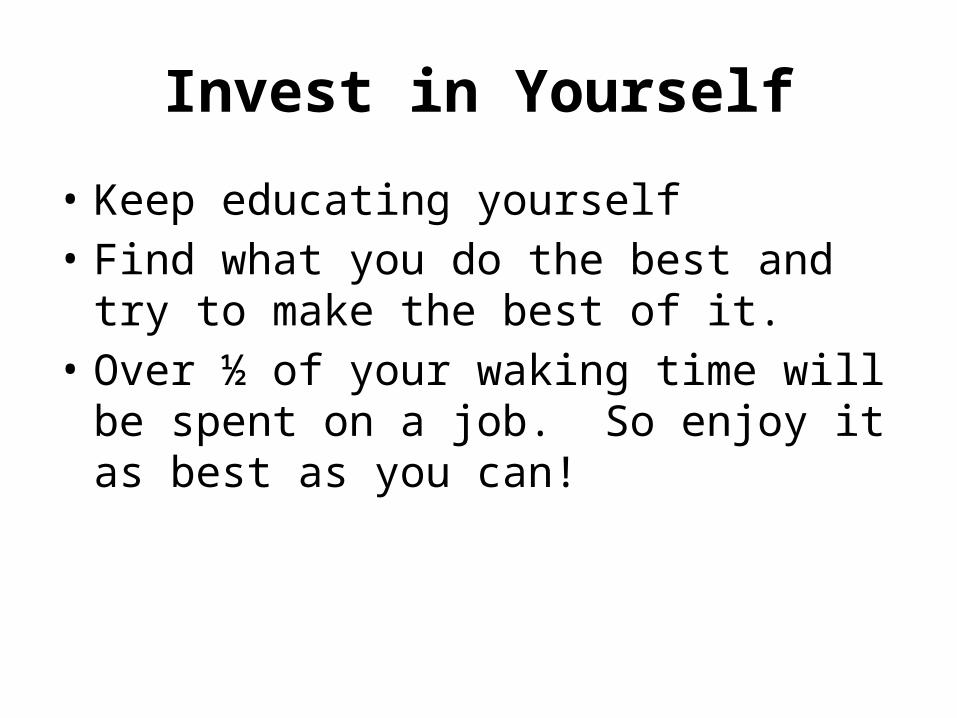

Invest in Yourself

• Keep educating yourself• Find what you do the best and try to make the

best of it.• Over ½ of your waking time will be spent on a

job. So enjoy it as best as you can!

•Tip #1: Make Financial Goals •Tip #2: Follow a Budget •Tip #3: Respect and Build Credit•Tip #4: Education and Learning Matter •Tip #5: Save Money - Use Coupons Responsibly•Tip #6: Protect Yourself - Get Insurance •Tip #7: Plan for the Future - Save & Invest •Tip #8: Own Your Home

Ways to be better with $$$$$

WAYS TO WASTE MONEY!!!1. Buying a new car.2. Borrowing to buy things that lose value.3. Earning squat while paying plenty.4. Ignoring your credit score. AnnualCreditReport.com. If you don’t like what you see take steps to improve it.5. Wasting a windfall.6. Overpaying your taxes.7. Buying name brands.8. Getting scammed.9. Missing new technologies.10. Settling for more.

Other Videos to show

http://www.youtube.com/watch?v=n1XNK7fXlIchttp://www.youtube.com/watch?v=UK8Fw8pPT7ohttp://www.youtube.com/watch?v=J0mOcLil0Mghttp://www.youtube.com/watch?v=n1XNK7fXlIc

Look at North Carolina CPA course on Financial Literacy for better information