Embed Size (px)

Citation preview

Financial Financial StatementStatement AnalysisAnalysis

Section 6.Section 6.Section 6.Section 6.Section 6.Section 6.

Profitability and illiquidity Risk AnalysisProfitability and illiquidity Risk Analysis

Margin AnalysisMargin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Return Analysis: ROE and the Financial Profitabilit y

Section 6.Section 6.

Profitability and illiquidity Risk AnalysisProfitability and illiquidity Risk Analysis

Margin AnalysisMargin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Return Analysis: ROE and the Financial Profitabilit y

Fahmi Ben Abdelkader ©

Return Analysis: ROE and the Financial Profitabilit y Return Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and longIlliquidity risk: short and long--term ratiosterm ratiosReturn Analysis: ROE and the Financial Profitabilit y Return Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and longIlliquidity risk: short and long--term ratiosterm ratios

5/25/2017 10:44 AM 1

Students version

Learning objectives

� Understand the structure of the profitability analysis

� Prepare a common-size analysis as well as a trend analysis � Prepare a common-size analysis as well as a trend analysis

� Define, calculate and interpret key financial ratios such as profit margin, return on invested capital, and Asset turnover

� Identify the limitations in using return on invested capital

� Understand the importance of trends and levels in key financial ratios

� Recognize that benchmarking is typically based on a comparison with the

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 2

� Recognize that benchmarking is typically based on a comparison with the required rate of return or competitors

� Understand the impact of financial leverage on profitability

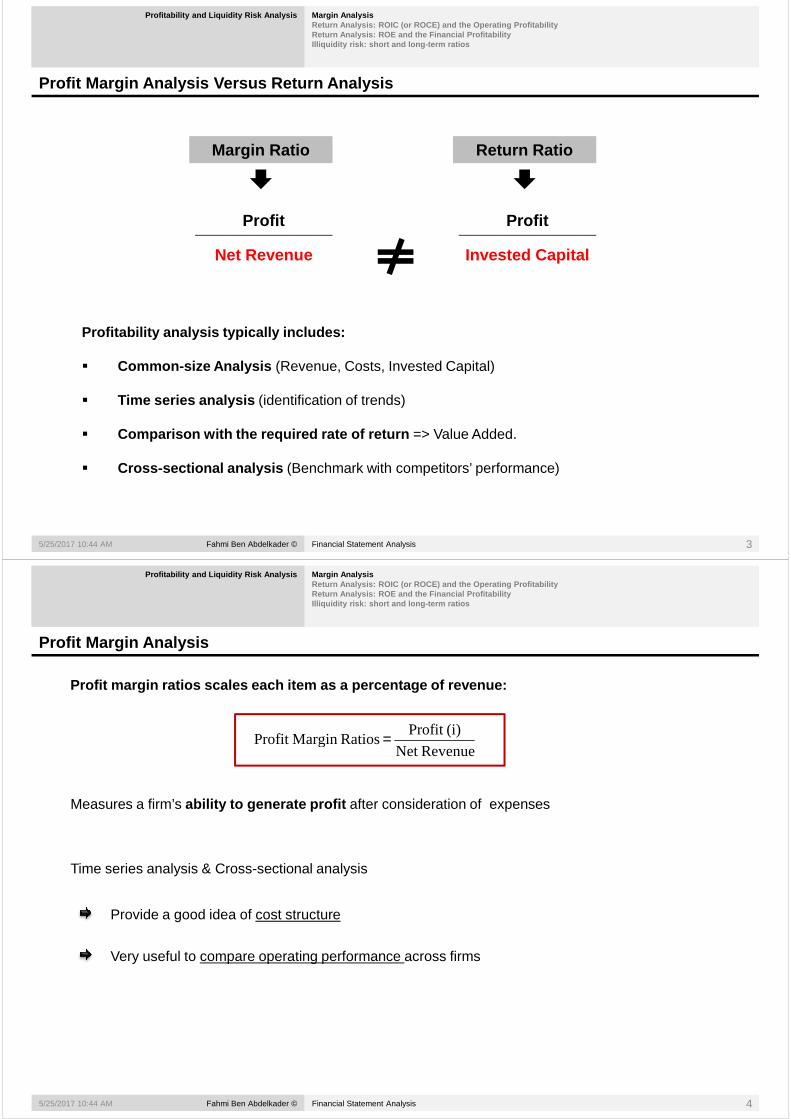

Profit Margin Analysis Versus Return Analysis

Profitability and Liquidity Risk Analysis Margin Ana lysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Margin Ratio Return Ratio

Profit

Net Revenue

Profit

Invested Capital

Profitability analysis typically includes:

� Common -size Analysis (Revenue, Costs, Invested Capital)

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 3

� Common -size Analysis (Revenue, Costs, Invested Capital)

� Time series analysis (identification of trends)

� Comparison with the required rate of return => Value Added.

� Cross-sectional analysis (Benchmark with competitors’ performance)

Profit Margin Analysis

Profitability and Liquidity Risk Analysis Margin Ana lysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Profit margin ratios scales each item as a percenta ge of revenue:

RevenueNet

(i)Profit RatiosMargin Profit =

RevenueNet RatiosMargin Profit

Measures a firm’s ability to generate profit after consideration of expenses

Provide a good idea of cost structure

Time series analysis & Cross-sectional analysis

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 4

Very useful to compare operating performance across firms

Profit Margin Analysis

Profitability and Liquidity Risk Analysis Margin Ana lysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Common-Size analysis of JIT’s revenue and operating expenses

Profit & expenses % of Net Revenue Year 2 Year 1

Net Revenue 100% 100%Net Revenue 100% 100%

Cost of sales 48,0% 46,0%

Gross Margin 52,0% 54,0%

Operating expenses 45,8% 49,2%

EBITDA Margin or Operating Margin 6,2% 4,8%

Depreciation & amortization 0,6% 0,6%

EBIT Margin 5,6% 4,2%

Net financial expenses 4,0% 2,6%

Pretax Income 1,6% 1,6%

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 5

Pretax Income 1,6% 1,6%

- Corporate income tax 0,5% 0,5%

Net Profit Margin 1,1% 1,1%

NOPAT (Net Operating Profit After Tax) 4% 3%

Profit Margin Analysis Across Competitors

Profitability and Liquidity Risk Analysis Margin Ana lysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Example: EBIT Margin for four U.S. Airlines

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 6

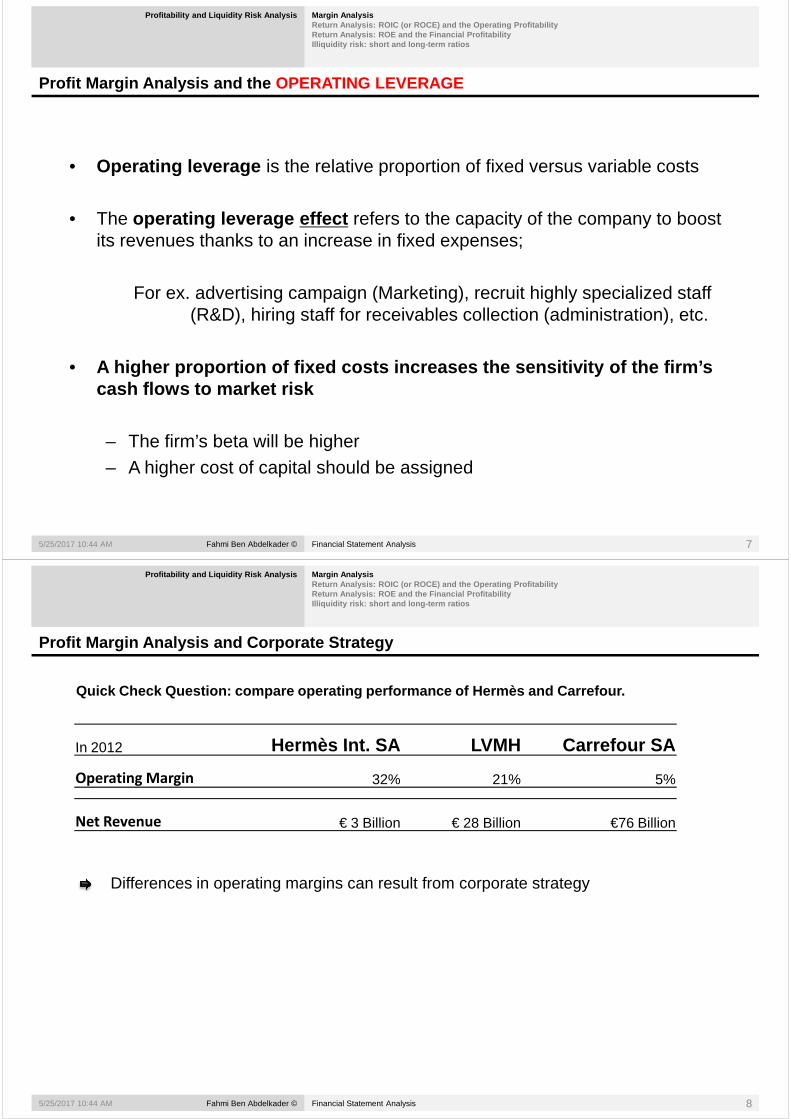

Profit Margin Analysis and the OPERATING LEVERAGE

Profitability and Liquidity Risk Analysis Margin Ana lysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

• Operating leverage is the relative proportion of fixed versus variable costs

• The operating leverage effect refers to the capacity of the company to boost its revenues thanks to an increase in fixed expenses;

For ex. advertising campaign (Marketing), recruit highly specialized staff (R&D), hiring staff for receivables collection (administration), etc.

• A higher proportion of fixed costs increases the se nsitivity of the firm’s

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 7

• A higher proportion of fixed costs increases the se nsitivity of the firm’s cash flows to market risk

– The firm’s beta will be higher– A higher cost of capital should be assigned

Profit Margin Analysis and Corporate Strategy

Profitability and Liquidity Risk Analysis Margin Ana lysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Quick Check Question: compare operating performance of Hermès and Carrefour.

In 2012 Hermès Int. SA LVMH Carrefour SAIn 2012 Hermès Int. SA LVMH Carrefour SA

Operating Margin 32% 21% 5%

Differences in operating margins can result from corporate strategy

Net Revenue € 3 Billion € 28 Billion €76 Billion

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 8

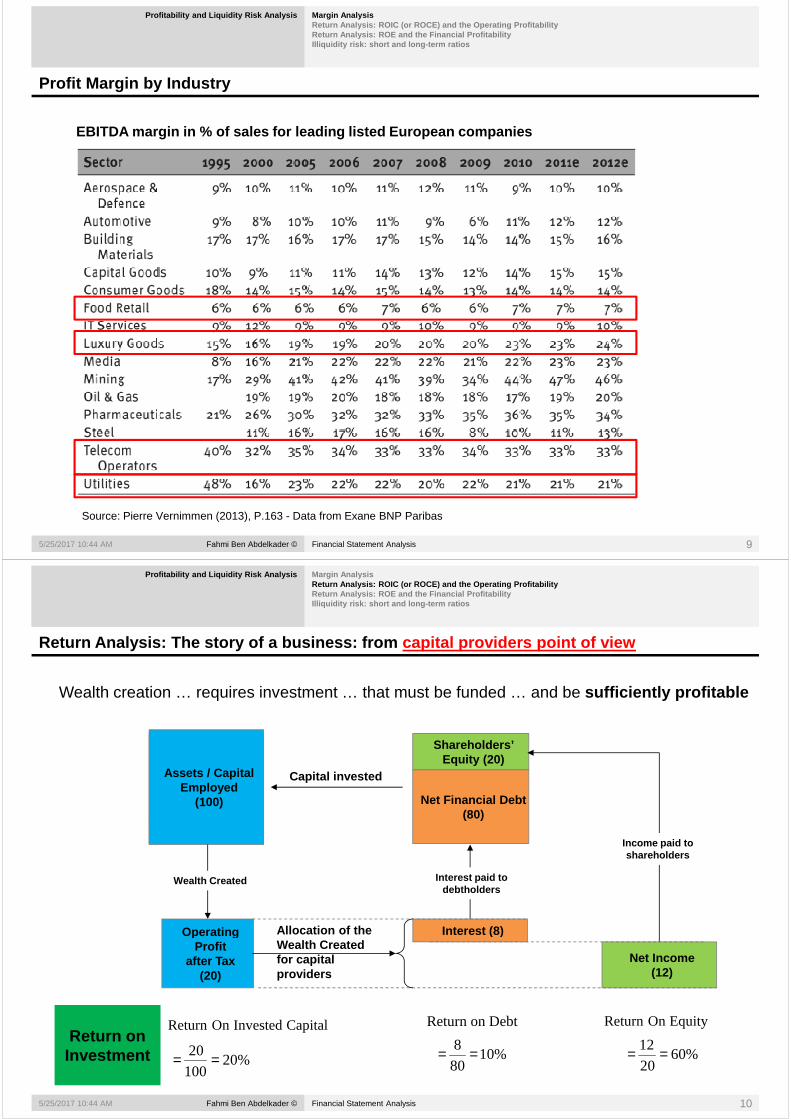

Profit Margin by Industry

Profitability and Liquidity Risk Analysis Margin Ana lysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

EBITDA margin in % of sales for leading listed Euro pean companies

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 9

Source: Pierre Vernimmen (2013), P.163 - Data from Exane BNP Paribas

Return Analysis: The story of a business: from capital providers point of view

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Wealth creation … requires investment … that must be funded … and be sufficiently profitable

Shareholders’

Fixed Assets

Shareholders’ Equity (20)

Net Financial Debt(80)

Working Capital

Capital invested Assets / Capital Employed

(100)

Interest (8) Operating

Wealth Created Interest paid to debtholders

Income paid to shareholders

Allocation of the

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 10

Interest (8)

Net Income(12)

Operating Profit

after Tax (20)

%20100

20 == %6020

12 ==%1080

8 ==

Capital InvestedOn Return Debton Return EquityOn Return

Allocation of the Wealth Created for capital providers

Return on Investment

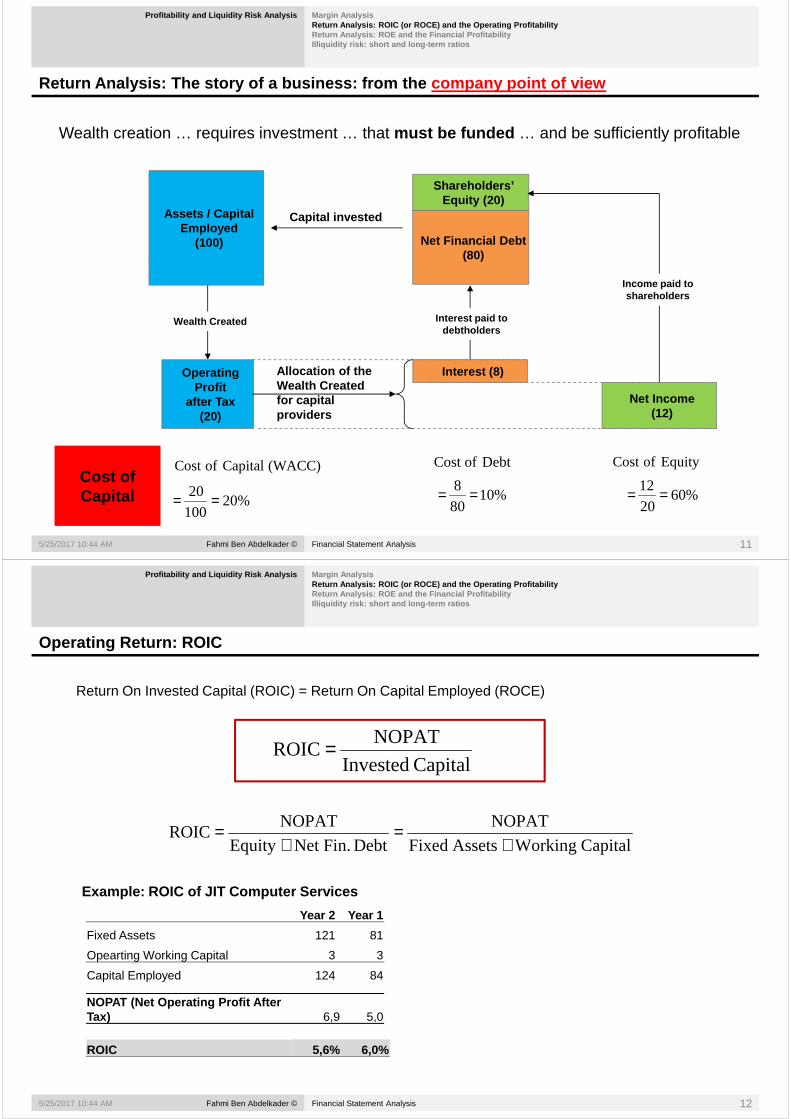

Return Analysis: The story of a business: from the company point of view

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Wealth creation … requires investment … that must be funded … and be sufficiently profitable

Shareholders’

Fixed Assets

Shareholders’ Equity (20)

Net Financial Debt(80)

Working Capital

Capital invested Assets / Capital Employed

(100)

Interest (8) Operating

Wealth Created Interest paid to debtholders

Income paid to shareholders

Allocation of the

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 11

Interest (8)

Net Income(12)

Operating Profit

after Tax (20)

Allocation of the Wealth Created for capital providers

%20100

20 == %6020

12 ==%1080

8 ==

(WACC) Capital ofCost Debt ofCost Equity ofCost Cost of Capital

Operating Return: ROIC

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Return On Invested Capital (ROIC) = Return On Capital Employed (ROCE)

NOPATROIC =

Capital InvestedROIC =

Capital Working Assets Fixed

NOPAT

Debt Fin.Net Equity

NOPATROIC

+=

+=

Year 2 Year 1

Fixed Assets 121 81

Example: ROIC of JIT Computer Services

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 12

Fixed Assets 121 81

Opearting Working Capital 3 3

Capital Employed 124 84

NOPAT (Net Operating Profit After Tax) 6,9 5,0

ROIC 5,6% 6,0%

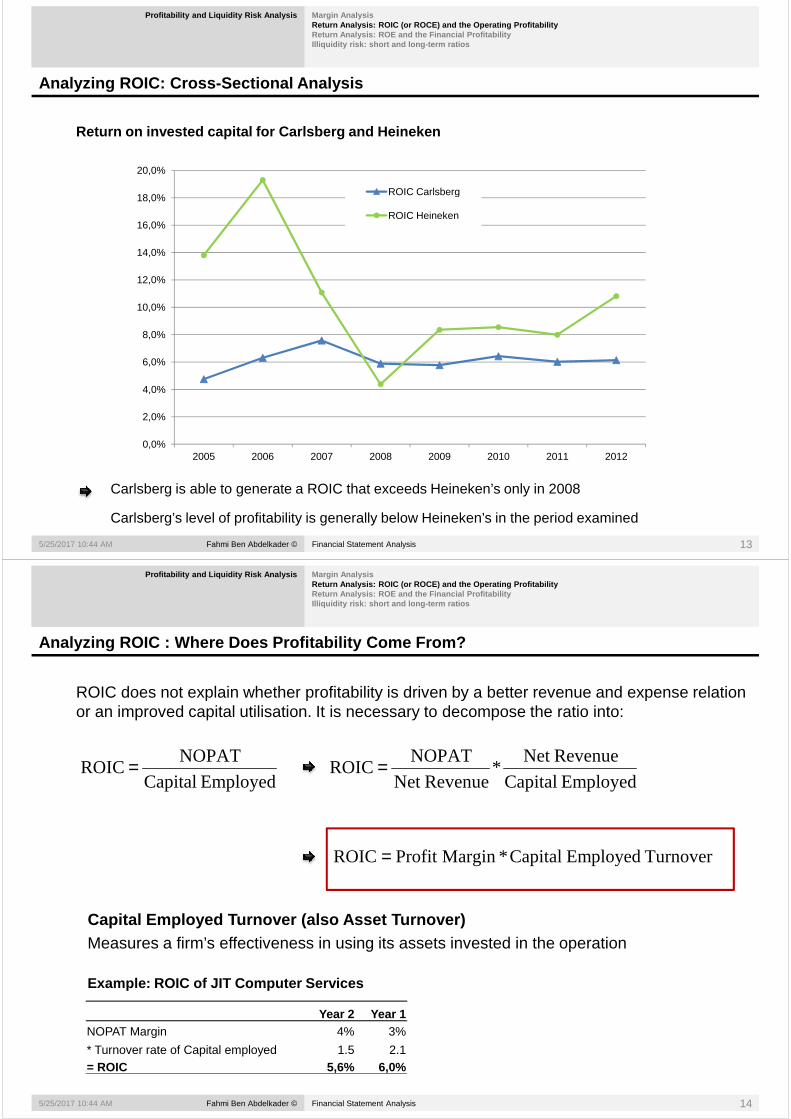

Analyzing ROIC: Cross-Sectional Analysis

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Return on invested capital for Carlsberg and Heinek en

20,0%

ROIC Carlsberg

6,0%

8,0%

10,0%

12,0%

14,0%

16,0%

18,0%ROIC Carlsberg

ROIC Heineken

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 13

Carlsberg is able to generate a ROIC that exceeds Heineken’s only in 2008

Carlsberg’s level of profitability is generally below Heineken’s in the period examined

0,0%

2,0%

4,0%

2005 2006 2007 2008 2009 2010 2011 2012

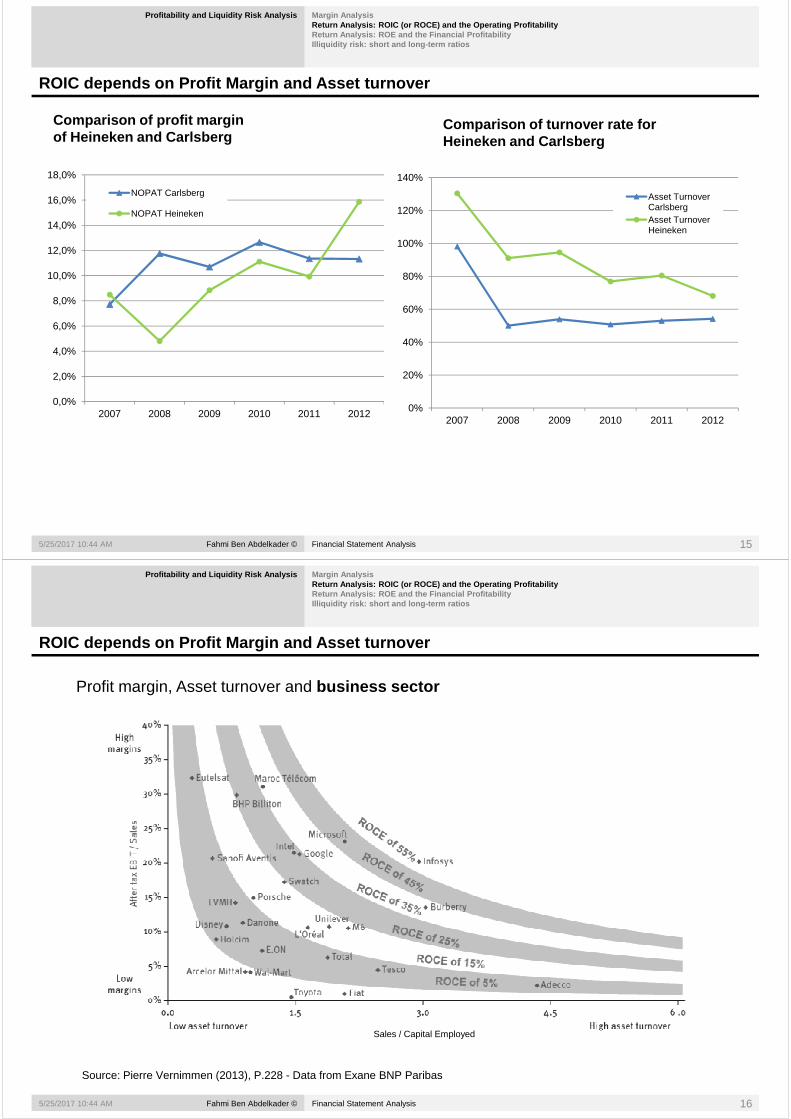

Analyzing ROIC : Where Does Profitability Come From ?

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

ROIC does not explain whether profitability is driven by a better revenue and expense relation or an improved capital utilisation. It is necessary to decompose the ratio into:

NOPAT RevenueNet NOPAT

Employed Capital

NOPATROIC =

Employed Capital

RevenueNet *

RevenueNet

NOPATROIC =

Turnover Employed Capital*MarginProfit ROIC =

Capital Employed Turnover (also Asset Turnover)

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 14

Measures a firm’s effectiveness in using its assets invested in the operation

Year 2 Year 1NOPAT Margin 4% 3%

* Turnover rate of Capital employed 1.5 2.1= ROIC 5,6% 6,0%

Example: ROIC of JIT Computer Services

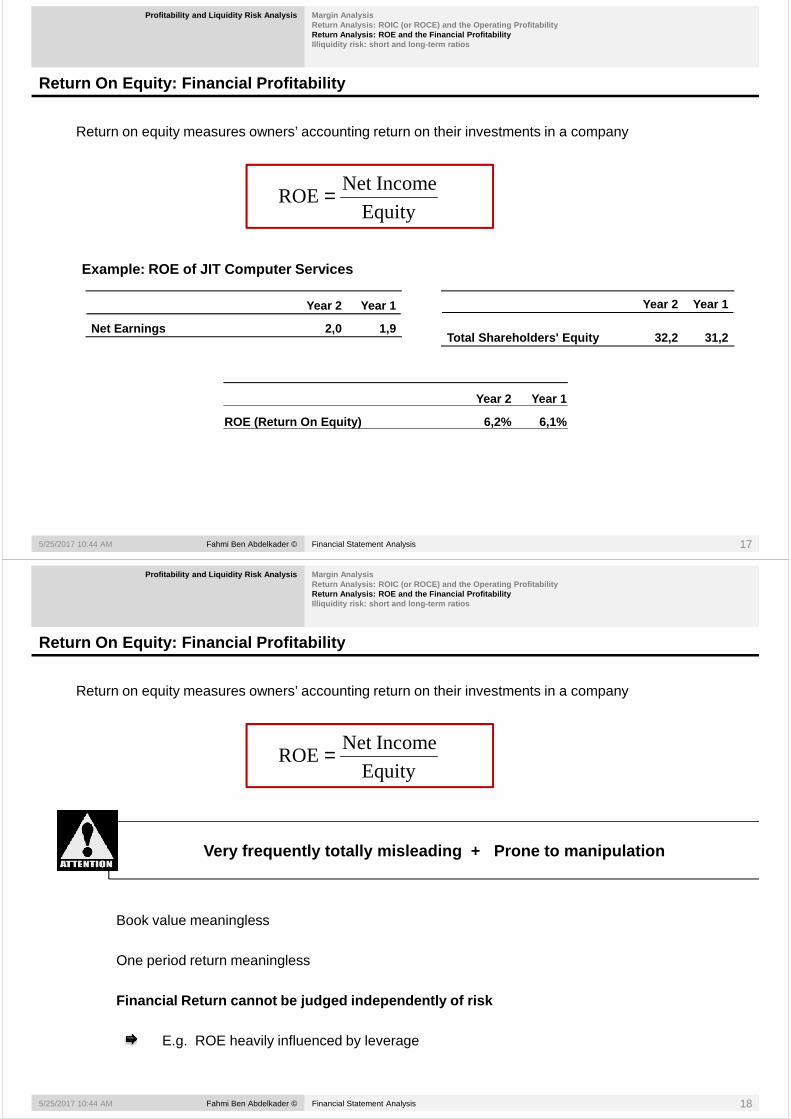

ROIC depends on Profit Margin and Asset turnover

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Comparison of profit margin of Heineken and Carlsberg

Comparison of turnover rate for Heineken and Carlsberg

18,0%

NOPAT Carlsberg

140%

4,0%

6,0%

8,0%

10,0%

12,0%

14,0%

16,0%NOPAT Carlsberg

NOPAT Heineken

20%

40%

60%

80%

100%

120%Asset Turnover CarlsbergAsset Turnover Heineken

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 15

0,0%

2,0%

2007 2008 2009 2010 2011 2012 0%

20%

2007 2008 2009 2010 2011 2012

ROIC depends on Profit Margin and Asset turnover

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Profit margin, Asset turnover and business sector

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 16

Sales / Capital Employed

Source: Pierre Vernimmen (2013), P.228 - Data from Exane BNP Paribas

Return On Equity: Financial Profitability

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Return on equity measures owners’ accounting return on their investments in a company

IncomeNet ROE =

Equity

IncomeNet ROE =

Year 2 Year 1

Net Earnings 2,0 1,9

Year 2 Year 1

Total Shareholders' Equity 32,2 31,2

Example: ROE of JIT Computer Services

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 17

Year 2 Year 1

ROE (Return On Equity) 6,2% 6,1%

Return On Equity: Financial Profitability

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Return on equity measures owners’ accounting return on their investments in a company

IncomeNet ROE =

Equity

IncomeNet ROE =

Very frequently totally misleading + Prone to ma nipulation

Book value meaningless

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 18

One period return meaningless

Financial Return cannot be judged independently of risk

E.g. ROE heavily influenced by leverage

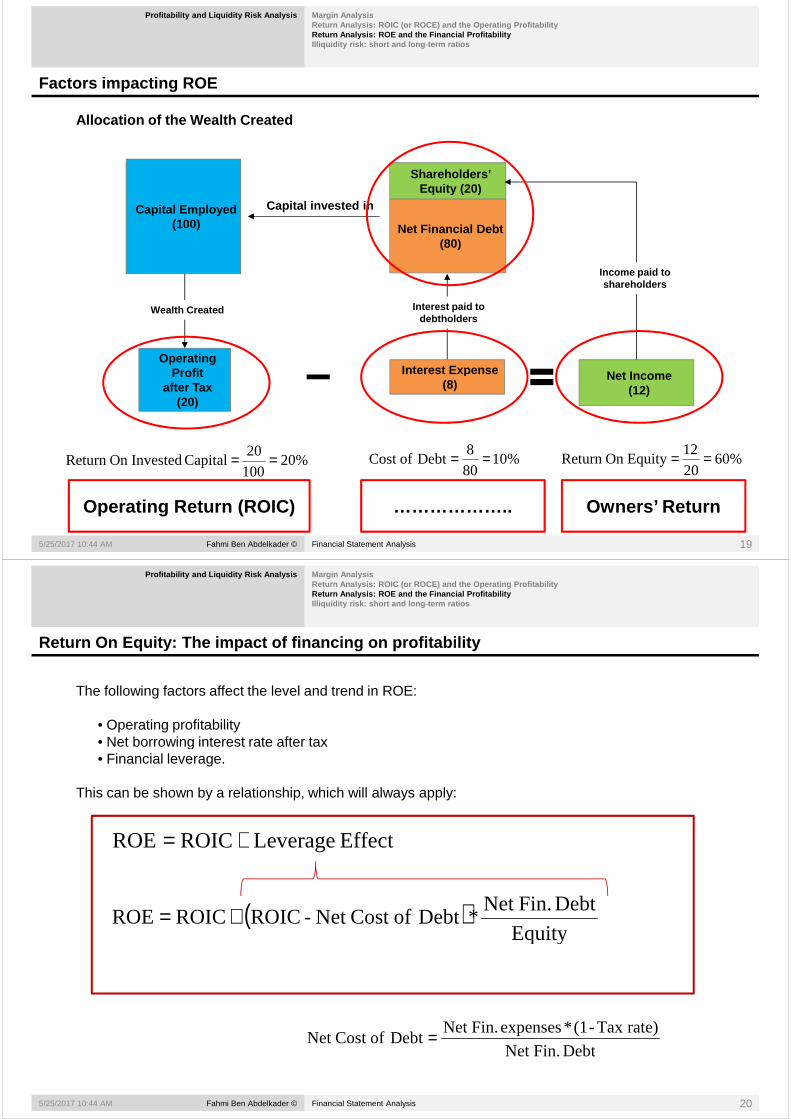

Factors impacting ROE

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Allocation of the Wealth Created

Shareholders’ Equity (20)

Fixed Assets

Equity (20)

Net Financial Debt(80)

Working Capital

Capital invested inCapital Employed(100)

Interest Expense Net IncomeOperating

Profit

Wealth Created Interest paid to debtholders

Income paid to shareholders

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 19

Interest Expense (8)

Net Income(12)

Profit after Tax

(20)

%20100

20Capital InvestedOn Return == %60

20

12EquityOn Return ==%10

80

8Debt ofCost ==

Operating Return (ROIC) Owners’ Return………………..

Return On Equity: The impact of financing on profit ability

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

The following factors affect the level and trend in ROE:

• Operating profitability • Net borrowing interest rate after tax • Net borrowing interest rate after tax • Financial leverage.

This can be shown by a relationship, which will always apply:

( )Equity

Debt Fin.Net *Debt ofCost Net - ROICROICROE +=

Effect LeverageROICROE +=

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 20

Equity

Debt Fin.Net

rate)Tax -(1*expenses Fin.Net Debt ofCost Net =

Return On Equity: The impact of financing on profit ability

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Example: 1 st case: No Tax, Cost of Debt = 5%

Cool Jazz Company

Hard Rock Company

Heavy Metal Company

Shareholders’ Equity 100 000 50 000 40 000Shareholders’ Equity 100 000 50 000 40 000

Net Financial Debt 0 50 000 60 000

Invested Capital 100 000 100 000 100 000

EBIT (or NOPAT) 10 000 10 000 10 000

Net Fin. expenses 0 2 500 3 000

Net Income

ROIC

Net Cost of Debt 0 % 5 % 5 %

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 21

ROIC – Net Cost of Debt +10% +5% +5%

* Financial Leverage 0 100% 150%

= Leverage Effect

ROE

If ROIC exceeds Net Cost of Debt, an increase in le verage is likely to improve ROE: positive leverage effect.

Return On Equity: The impact of financing on profit ability

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

If you can get cheap money, increase your leverage and boost your ROE

Cheap money (low cost of debt) is not a sufficient condition to increase

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 22

Cheap money (low cost of debt) is not a sufficient condition to increase leverage

The key question: what are you going to do with the borrowed money?

The value of a business depends primarily on the ca pacity of its assets to generate cash flows, and less on capital structu re choices

Return On Equity: The impact of financing on profit ability

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

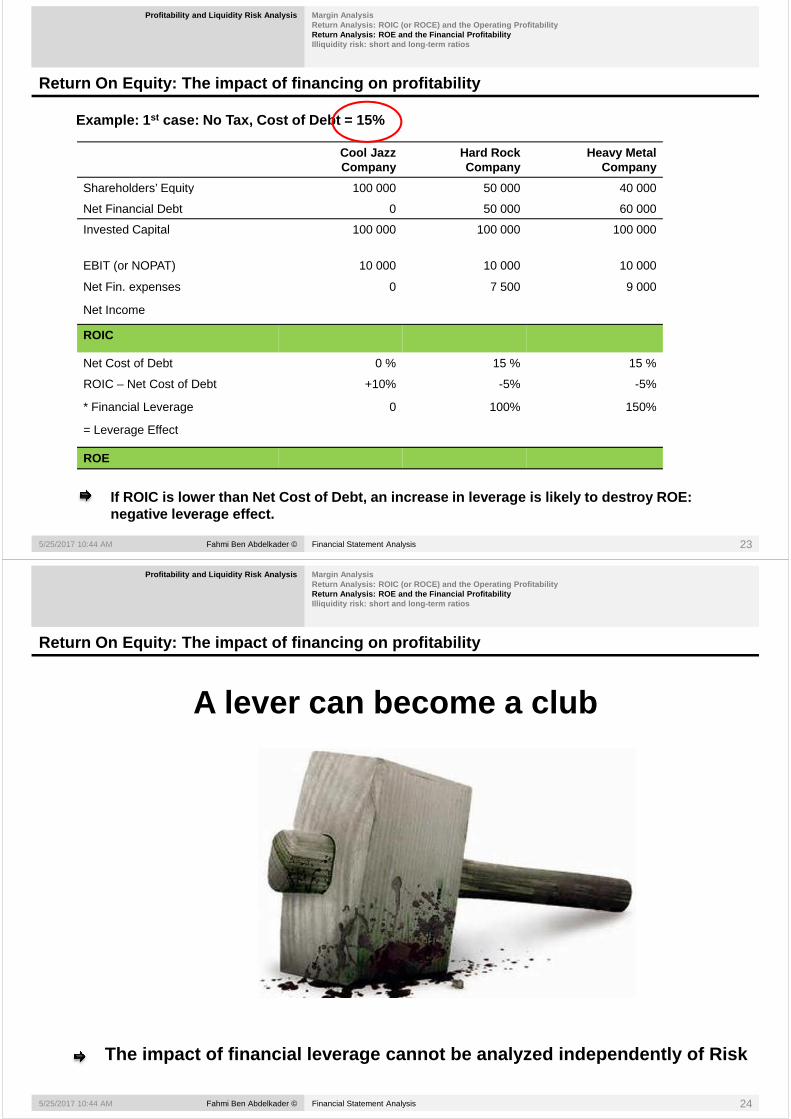

Example: 1 st case: No Tax, Cost of Debt = 15%

Cool Jazz Company

Hard Rock Company

Heavy Metal Company

Shareholders’ Equity 100 000 50 000 40 000Shareholders’ Equity 100 000 50 000 40 000

Net Financial Debt 0 50 000 60 000

Invested Capital 100 000 100 000 100 000

EBIT (or NOPAT) 10 000 10 000 10 000

Net Fin. expenses 0 7 500 9 000

Net Income

ROIC

Net Cost of Debt 0 % 15 % 15 %

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 23

ROIC – Net Cost of Debt +10% -5% -5%

* Financial Leverage 0 100% 150%

= Leverage Effect

ROE

If ROIC is lower than Net Cost of Debt, an increase in leverage is likely to destroy ROE: negative leverage effect.

Return On Equity: The impact of financing on profit ability

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

A lever can become a club

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 24

The impact of financial leverage cannot be analyzed independently of Risk

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

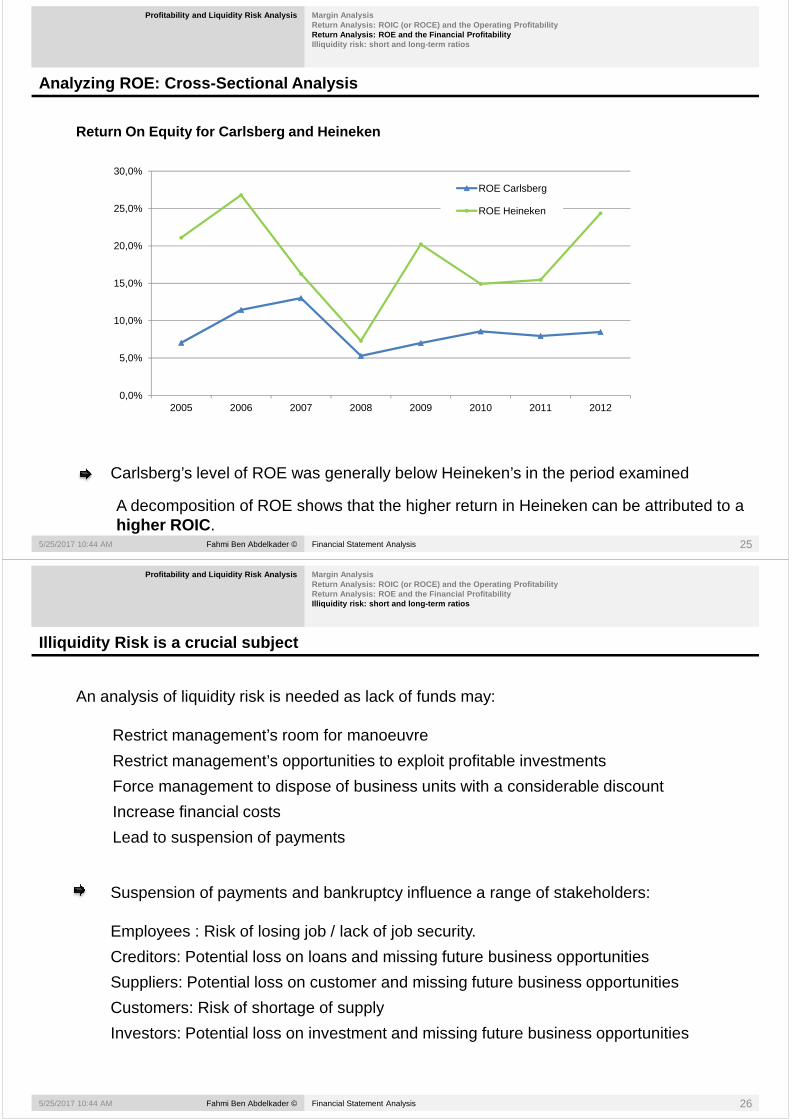

Analyzing ROE: Cross-Sectional Analysis

Return On Equity for Carlsberg and Heineken

30,0%

ROE Carlsberg

5,0%

10,0%

15,0%

20,0%

25,0%

ROE Carlsberg

ROE Heineken

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 25

Carlsberg’s level of ROE was generally below Heineken’s in the period examined

A decomposition of ROE shows that the higher return in Heineken can be attributed to a higher ROIC .

0,0%2005 2006 2007 2008 2009 2010 2011 2012

Illiquidity Risk is a crucial subject

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

An analysis of liquidity risk is needed as lack of funds may:

Restrict management’s room for manoeuvre

Restrict management’s opportunities to exploit profitable investments

Force management to dispose of business units with a considerable discount

Increase financial costs

Lead to suspension of payments

Suspension of payments and bankruptcy influence a range of stakeholders:

Employees : Risk of losing job / lack of job security.

Fahmi Ben Abdelkader © Financial Statement Analysis

Employees : Risk of losing job / lack of job security.

Creditors: Potential loss on loans and missing future business opportunities

Suppliers: Potential loss on customer and missing future business opportunities

Customers: Risk of shortage of supply

Investors: Potential loss on investment and missing future business opportunities

5/25/2017 10:44 AM 26

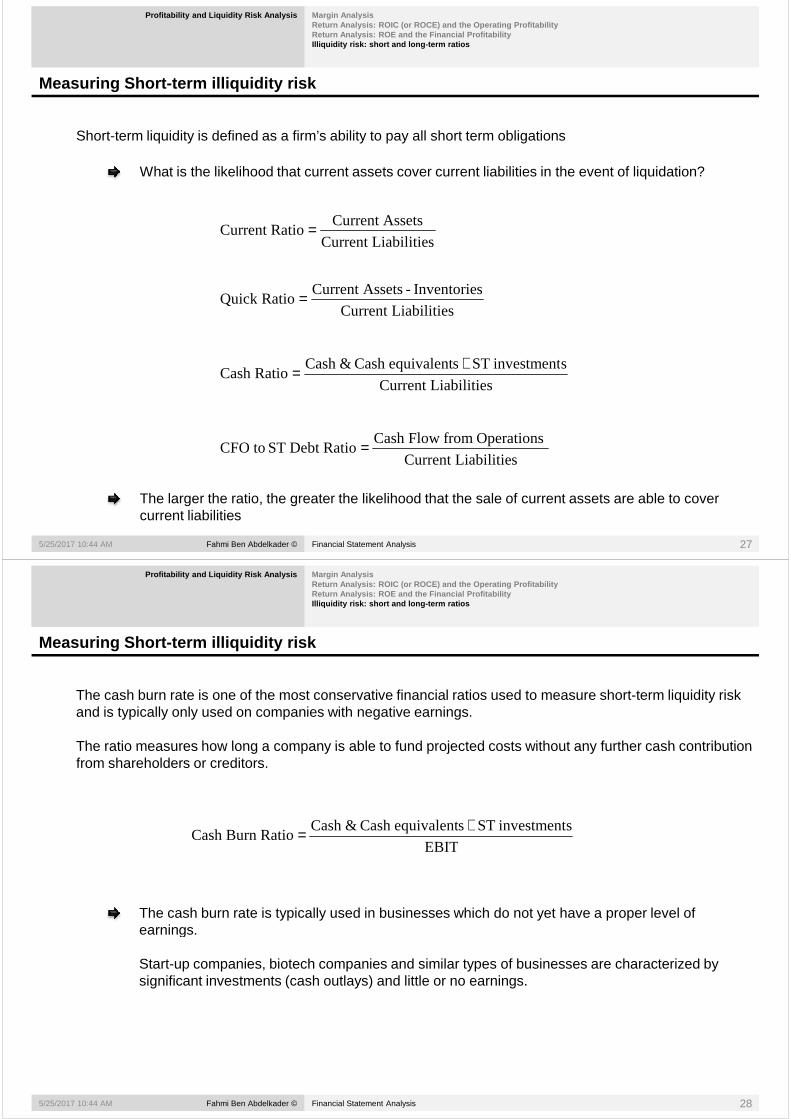

Measuring Short-term illiquidity risk

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Short-term liquidity is defined as a firm’s ability to pay all short term obligations

What is the likelihood that current assets cover current liabilities in the event of liquidation?

sLiabilitieCurrent

AssetsCurrent RatioCurrent =

sLiabilitieCurrent

sInventorie -AssetsCurrent RatioQuick =

sinvestment STsequivalentCash &Cash RatioCash

+=

Fahmi Ben Abdelkader © Financial Statement Analysis

sLiabilitieCurrent

sinvestment STsequivalentCash &Cash RatioCash

+=

sLiabilitieCurrent

Operations from FlowCash RatioDebt ST toCFO =

The larger the ratio, the greater the likelihood that the sale of current assets are able to cover current liabilities

5/25/2017 10:44 AM 27

Measuring Short-term illiquidity risk

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

The cash burn rate is one of the most conservative financial ratios used to measure short-term liquidity risk and is typically only used on companies with negative earnings.

The ratio measures how long a company is able to fund projected costs without any further cash contribution The ratio measures how long a company is able to fund projected costs without any further cash contribution from shareholders or creditors.

EBIT

sinvestment STsequivalentCash &Cash RatioBurn Cash

+=

The cash burn rate is typically used in businesses which do not yet have a proper level of earnings.

Fahmi Ben Abdelkader © Financial Statement Analysis

earnings.

Start-up companies, biotech companies and similar types of businesses are characterized by significant investments (cash outlays) and little or no earnings.

5/25/2017 10:44 AM 28

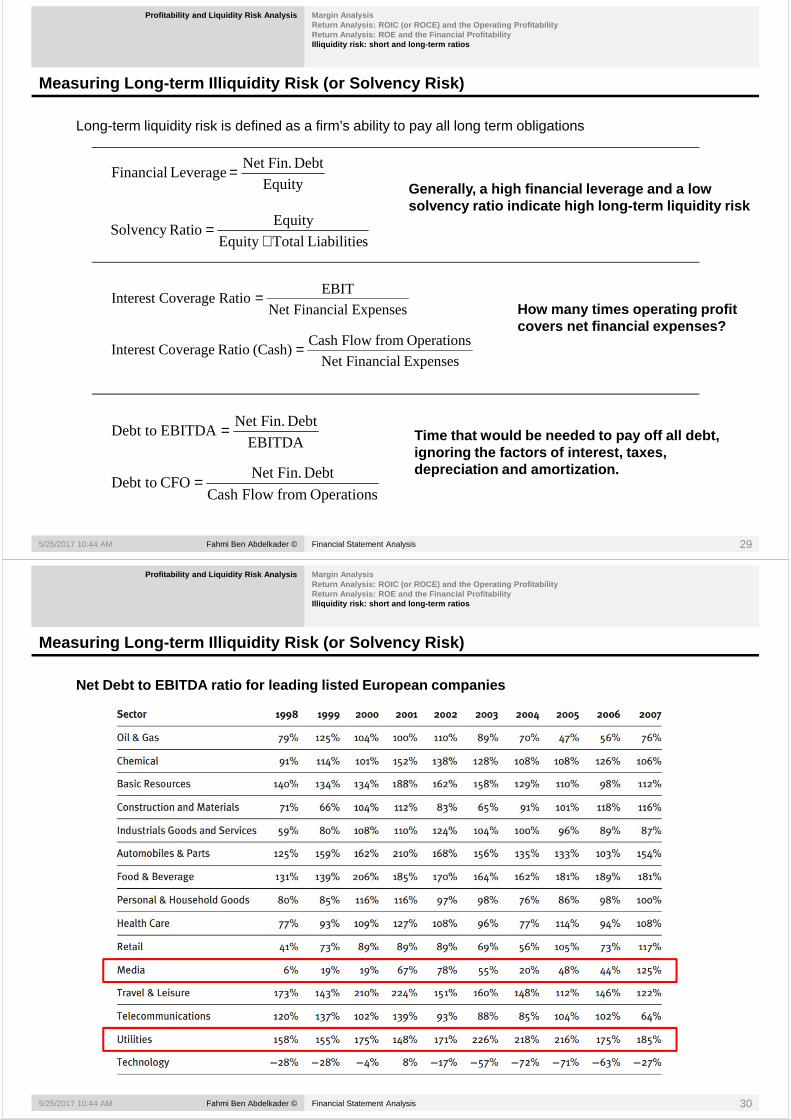

Measuring Long-term Illiquidity Risk (or Solvency R isk)

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Long-term liquidity risk is defined as a firm’s ability to pay all long term obligations

Equity

Debt Fin.Net Leverage Financial =

Generally, a high financial leverage and a low

sLiabilitie TotalEquity

EquityRatioSolvency

+=

Expenses FinancialNet

EBITRatio CoverageInterest =

Expenses FinancialNet

Operations from FlowCash (Cash) Ratio CoverageInterest =

Equity Generally, a high financial leverage and a low solvency ratio indicate high long-term liquidity ri sk

How many times operating profit covers net financial expenses?

Fahmi Ben Abdelkader © Financial Statement Analysis

EBITDA

Debt Fin.Net EBITDA Debt to =

Operations from FlowCash

Debt Fin.Net CFO Debt to =

5/25/2017 10:44 AM 29

Time that would be needed to pay off all debt, ignoring the factors of interest, taxes, depreciation and amortization.

Measuring Long-term Illiquidity Risk (or Solvency R isk)

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Net Debt to EBITDA ratio for leading listed Europea n companies

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 30

Weaknesses of financial ratios measuring liquidity risk

Knowledge of a company's liquidity is important, as lack of liquidity may lead to loss of business opportunities and, in a worst case, suspension of payments

Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Profitability and Liquidity Risk Analysis

Weaknesses of liquidity ratiosWeaknesses of liquidity ratios

Based on historical accounting information and, thus, backward-looking

Book value of assets is almost meaningless

Capital structure ratios at market value should make more sense than at book values but are very volatile

Liquidity ratios can be easily manipulated if the company knows that it is being analyzed:

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 31

E.g. Interest or other financing costs can be shifted to the future

Bad liquidity ratios can be the result of good cash management

The Income Statement The Balance Sheet : An OverviewAssetsLiabilitiesShareholders’ Equity

1. When is it useful to define ROIC before and after tax, respectively?

2. A company experiences a drop in ROIC from 12% in year 1 to 5% in year 4. Provide potential explanations for the drop in ROIC of 7 percentage points.

Concept Check and Critical Thinking

Provide potential explanations for the drop in ROIC of 7 percentage points.

3. What is the appropriate benchmark for ROIC?

4. What actions can a management take to improve the profit margin?

5. What actions can the management take to improve the turnover rate of invested capital?

6. How does financial leverage affect the return to shareholders?

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 32

7. What is the appropriate benchmark for ROE?

8. What are the potential shortcomings of financial ratios measuring liquidity risk?

9. How can these shortcomings be addressed?

The Income Statement The Balance Sheet : An OverviewAssetsLiabilitiesShareholders’ EquityAppendix

Some stories on margin trends

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 33

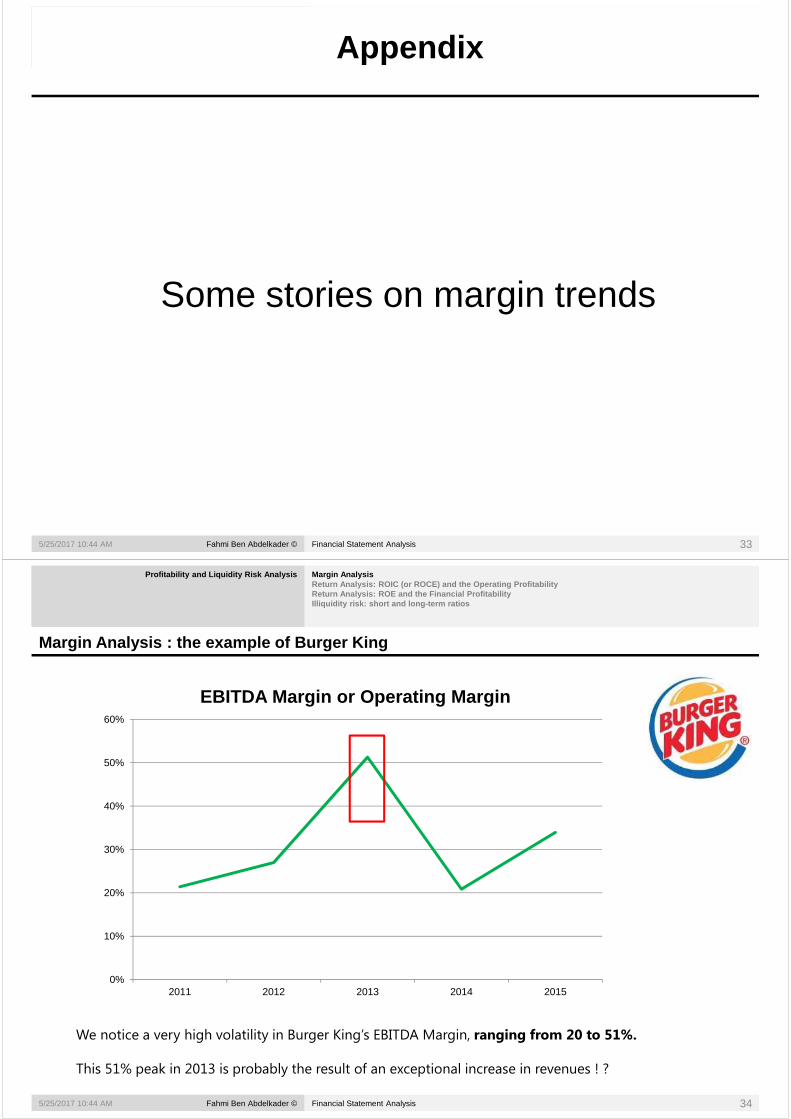

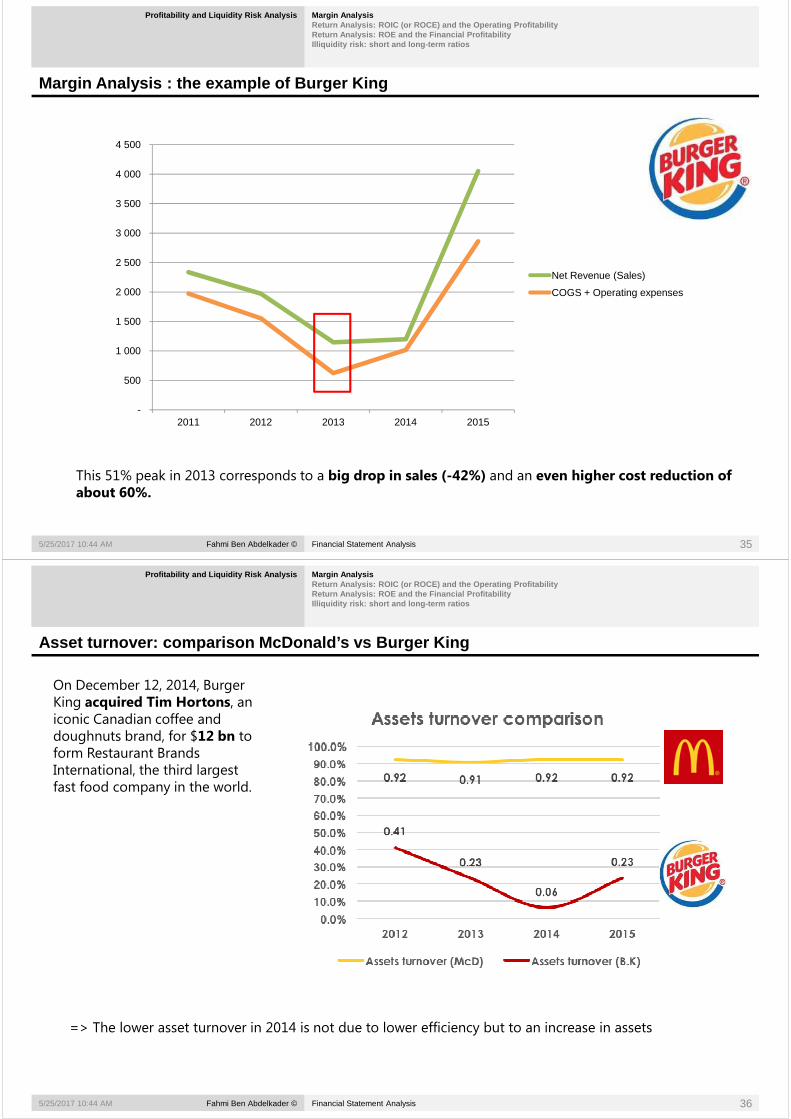

Margin Analysis : the example of Burger King

Profitability and Liquidity Risk Analysis Margin Ana lysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

60%

EBITDA Margin or Operating Margin

20%

30%

40%

50%

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 34

0%

10%

2011 2012 2013 2014 2015

We notice a very high volatility in Burger King’s EBITDA Margin, ranging from 20 to 51%.

This 51% peak in 2013 is probably the result of an exceptional increase in revenues ! ?

Margin Analysis : the example of Burger King

Profitability and Liquidity Risk Analysis Margin Ana lysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

4 000

4 500

1 000

1 500

2 000

2 500

3 000

3 500

Net Revenue (Sales)

COGS + Operating expenses

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 35

-

500

2011 2012 2013 2014 2015

This 51% peak in 2013 corresponds to a big drop in sales (-42%) and an even higher cost reduction of about 60%.

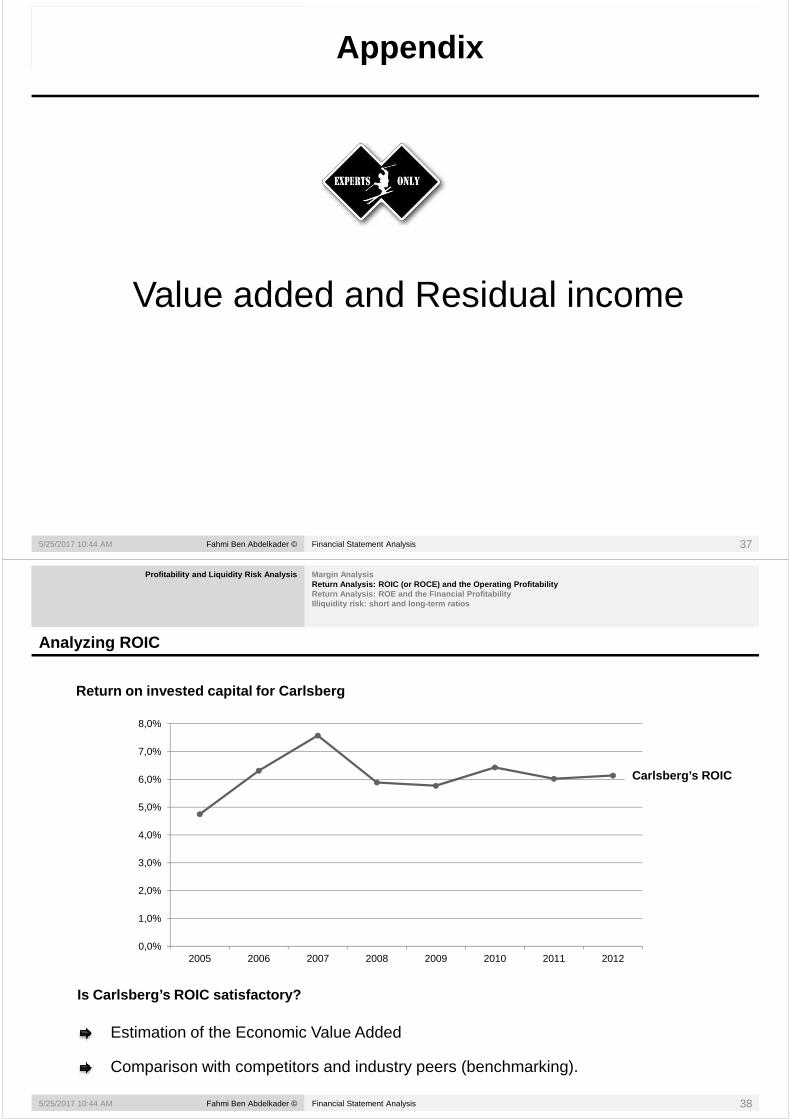

Asset turnover: comparison McDonald’s vs Burger Kin g

Profitability and Liquidity Risk Analysis Margin Ana lysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

On December 12, 2014, Burger King acquired Tim Hortons, an iconic Canadian coffee and doughnuts brand, for $12 bn to form Restaurant Brands form Restaurant Brands International, the third largest fast food company in the world.

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 36

=> The lower asset turnover in 2014 is not due to lower efficiency but to an increase in assets

The Income Statement The Balance Sheet : An OverviewAssetsLiabilitiesShareholders’ EquityAppendix

Value added and Residual income

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 37

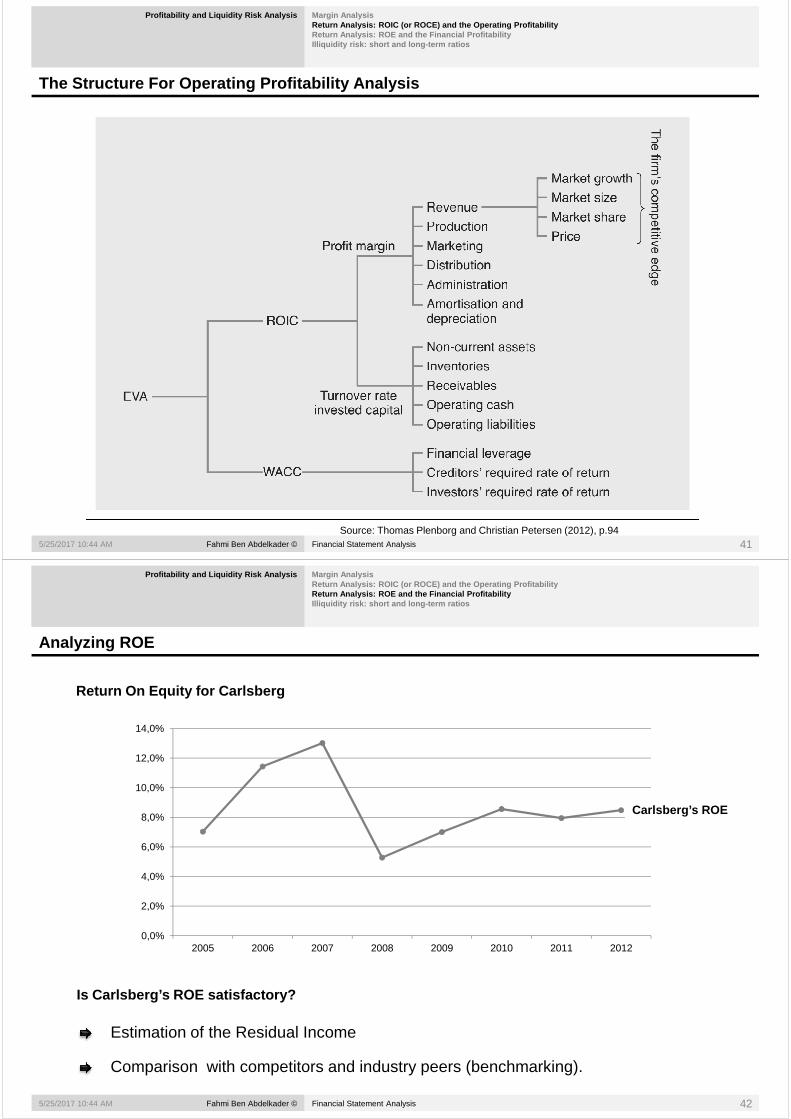

Analyzing ROIC

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Return on invested capital for Carlsberg

7,0%

8,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

Carlsberg’s ROIC

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 38

Is Carlsberg’s ROIC satisfactory?

Estimation of the Economic Value Added

Comparison with competitors and industry peers (benchmarking).

0,0%2005 2006 2007 2008 2009 2010 2011 2012

Analyzing ROIC: Economic Value Added

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Comparing ROIC and WACC provides an idea on EVA: va lue creation for capital providers

Employed Capital*WACC)-(ROICEVA =

)1(**%*% TrDebtrEquityWACC DE −+=

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 39

Fig. 13.3 (B&DM – FCF – p.392)

Analyzing ROIC: Economic Value Added

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Return on invested capital for Carlsberg Versus WAC C

8,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0% WACC=7%

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 40

Carlsberg is only creating value for its shareholders in 2007

0,0%

1,0%

2005 2006 2007 2008 2009 2010 2011 2012

The Structure For Operating Profitability Analysis

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Market growth

Market size

Market shareRevenue

Market share

Price

Administration

Amortisation and

depreciation

Non-current assets

Inventories

ReceivablesTurnover rate

Profit Margin

ROIC

Production

Marketing

Distribution

Revenue

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 41

Operating cash

Operating liabilities

Turnover rateInvested capital

EVA

WACC

Financial leverage

Creditors’ required rate of return

Investors’ required rate of return

Source: Thomas Plenborg and Christian Petersen (2012), p.94

Analyzing ROE

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Return On Equity for Carlsberg

14,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

Carlsberg’s ROE

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 42

Is Carlsberg’s ROE satisfactory?

Estimation of the Residual Income

Comparison with competitors and industry peers (benchmarking).

0,0%2005 2006 2007 2008 2009 2010 2011 2012

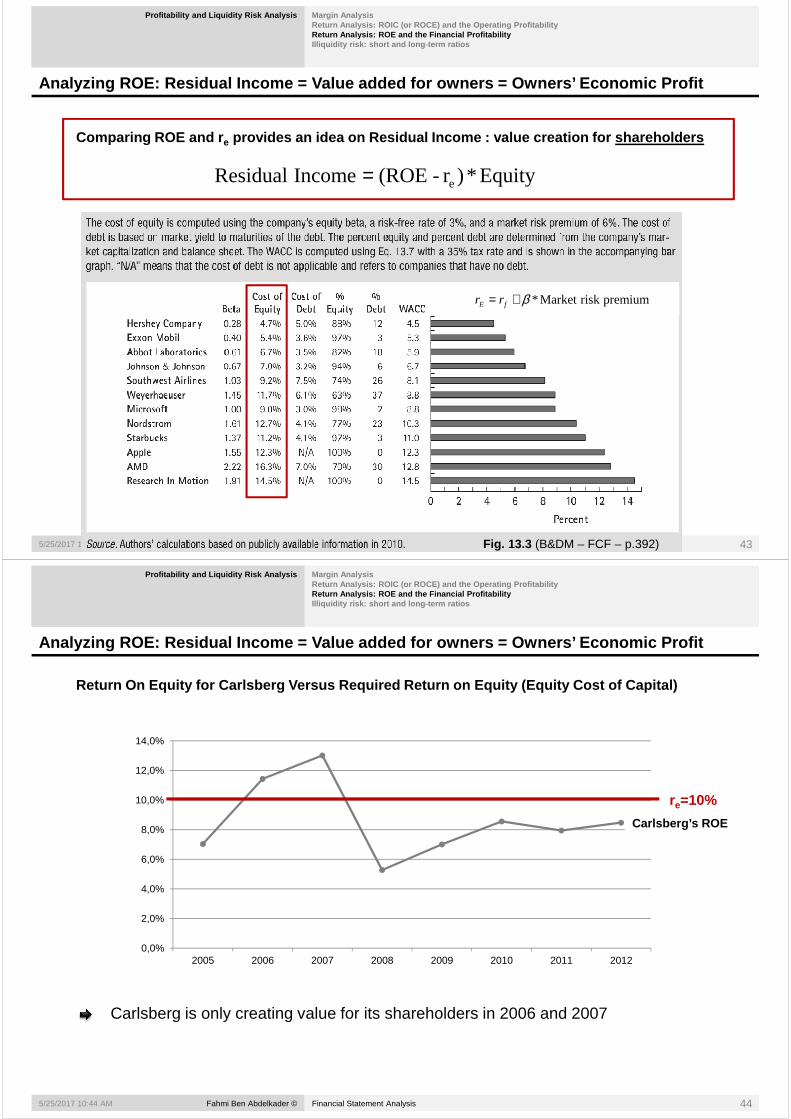

Analyzing ROE: Residual Income = Value added for ow ners = Owners’ Economic Profit

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Comparing ROE and re provides an idea on Residual Income : value creatio n for shareholders

Equity*)r-(ROEIncome Residual e= e

premiumrisk Market *β+= fE rr

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 43Fig. 13.3 (B&DM – FCF – p.392)

Analyzing ROE: Residual Income = Value added for ow ners = Owners’ Economic Profit

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Return On Equity for Carlsberg Versus Required Retu rn on Equity (Equity Cost of Capital)

14,0%

re=10%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

Carlsberg’s ROE

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 44

Carlsberg is only creating value for its shareholders in 2006 and 2007

0,0%2005 2006 2007 2008 2009 2010 2011 2012

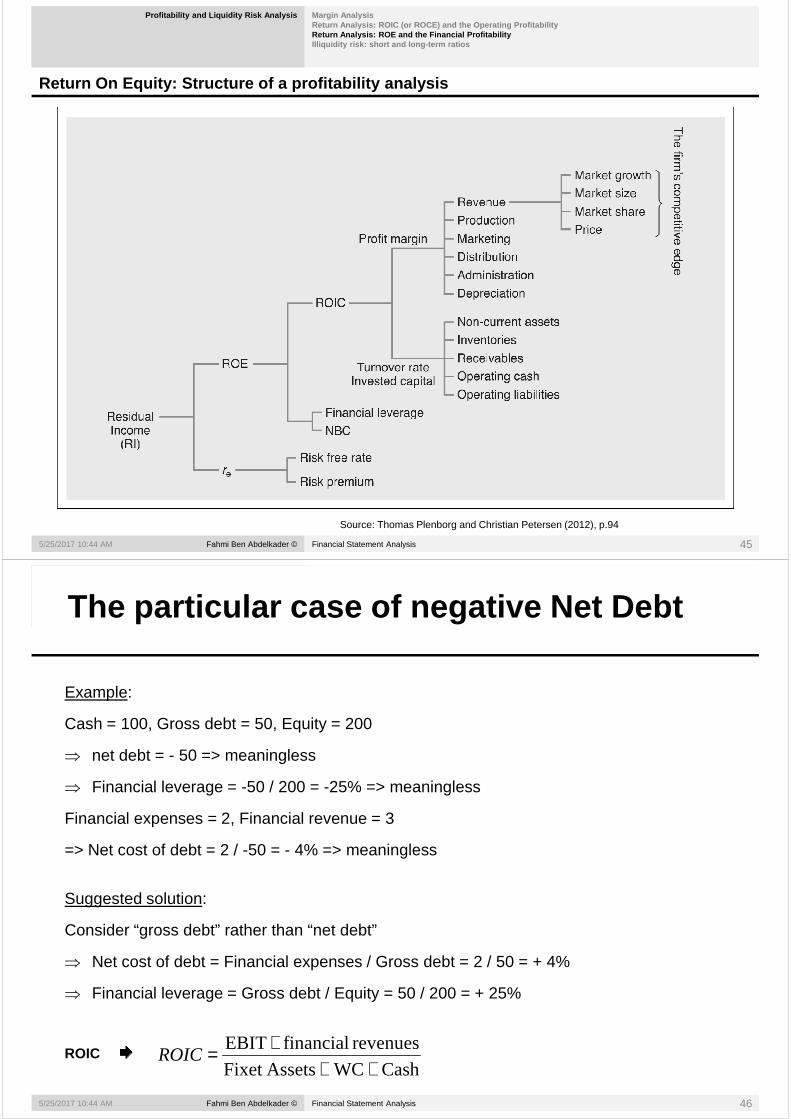

Return On Equity: Structure of a profitability anal ysis

Profitability and Liquidity Risk Analysis Margin AnalysisReturn Analysis: ROIC (or ROCE) and the Operating P rofitabilityReturn Analysis: ROE and the Financial Profitabilit y Illiquidity risk: short and long-term ratios

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 45

Source: Thomas Plenborg and Christian Petersen (2012), p.94

The Income Statement The Balance Sheet : An OverviewAssetsLiabilitiesShareholders’ Equity

Example:

Cash = 100, Gross debt = 50, Equity = 200

⇒ net debt = - 50 => meaningless

The particular case of negative Net Debt

⇒ net debt = - 50 => meaningless

⇒ Financial leverage = -50 / 200 = -25% => meaningless

Financial expenses = 2, Financial revenue = 3

=> Net cost of debt = 2 / -50 = - 4% => meaningless

Suggested solution:

Consider “gross debt” rather than “net debt”

Fahmi Ben Abdelkader © Financial Statement Analysis5/25/2017 10:44 AM 46

Consider “gross debt” rather than “net debt”

⇒ Net cost of debt = Financial expenses / Gross debt = 2 / 50 = + 4%

⇒ Financial leverage = Gross debt / Equity = 50 / 200 = + 25%

ROICCash WC AssetsFixet

revenues financialEBIT

+++=ROIC