Embed Size (px)

Citation preview

Financial crisis and quantitative methods: problems and solutions

Are European Deposit Protection Schemes

efficient enough?

Adamo UboldiJoint Research Centre

European Commission

Unit for Econometrics and Applied StatisticsFinancial Econometrics for a Single Market and Competitiveness Policies

Financial crisis and quantitative methods: problems and solutions

Plan of the talk

Deposit Protection Schemes (DPS) in the EU

Reaction to the financial crisis

Efficiency of EU DPS

Quantitative tools and risk-based contributions

Financial crisis and quantitative methods: problems and solutions

Deposit Protection in the EU

AIM: to provide a safety net for depositors so that, if a credit

institution fails, they will be able to recover their bank

deposits up to a certain limit

HOW: Directive 94/19/EC on Deposit Guarantee Schemes

(DGS) and current amendment proposal

Financial crisis and quantitative methods: problems and solutions

Protection of depositors’

wealth

through the introduction of a

minimum threshold (€20,000 till

October 08)

Directive 94/19/EC (I)

Maintenance of confidence in

the EU banking system

through protection of stability,

avoiding a run on the banks

Objectives

Financial crisis and quantitative methods: problems and solutions

Directive 94/19/EC (II)

Member States have to ensure one or more officially recognised

DGS and ALL deposit-taking credit institutions must join DGS

EU has a total of 39 DGS (some MS have more than one DGS)

Minimum coverage level set at € 20,000

MS apply different coverage levels from min. € 20,000 to max. € 103,000

Obligation for DGS to repay depositors’ claims within three

months from triggering event (possible extension up to nine

months)

90% of deposits and 70% of depositors have been repaid within 3 months

Key provisions and implementation

Financial crisis and quantitative methods: problems and solutions

Current financial crisis (I)

Quick response to crisis: DG-MARKT asked JRC to perform an

early IA on possible changes of coverage level

October 9th: delivery of a confidential Impact Assessment to

feed the amendment proposal of Directive 94/19/EC

as the situation of financial markets was requiring immediate

actions, no detailed IA was possible at that time…

Financial crisis and quantitative methods: problems and solutions

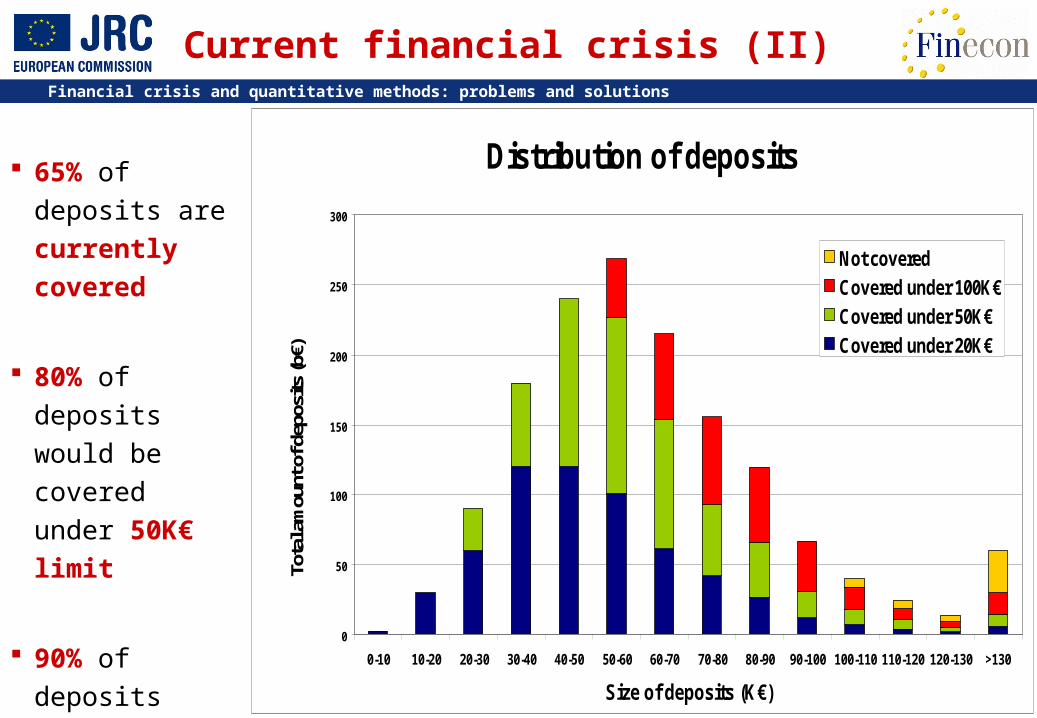

Current financial crisis (II)

65% of deposits are currently covered

80% of deposits would be covered under 50K€ limit

90% of deposits would be covered under 100K€ limit

Distribution of deposits

0

50

100

150

200

250

300

0-10 10-20 20-30 30-40 40-50 50-60 60-70 70-80 80-90 90-100 100-110 110-120 120-130 >130

Size of deposits (K€)

Tota

l am

ount

of d

epos

its (b

€)

Not covered

Covered under 100K€

Covered under 50K€

Covered under 20K€

Financial crisis and quantitative methods: problems and solutions

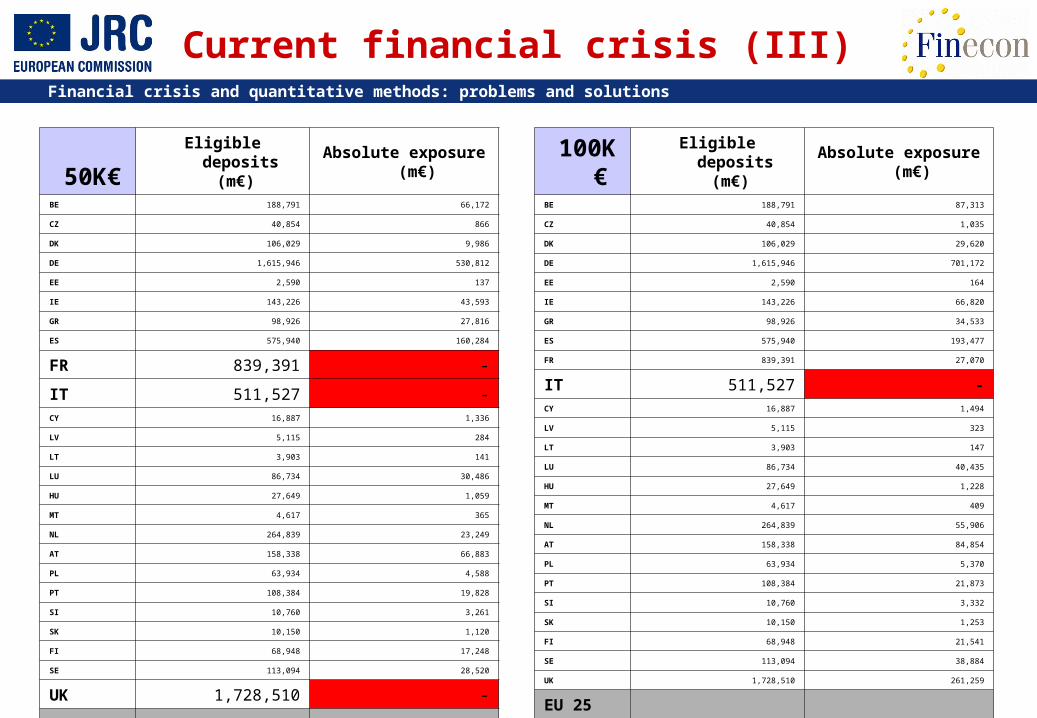

50K€ Eligible deposits (m€) Absolute exposure (m€)

BE 188,791 66,172

CZ 40,854 866

DK 106,029 9,986

DE 1,615,946 530,812

EE 2,590 137

IE 143,226 43,593

GR 98,926 27,816

ES 575,940 160,284

FR 839,391 -

IT 511,527 -CY 16,887 1,336

LV 5,115 284

LT 3,903 141

LU 86,734 30,486

HU 27,649 1,059

MT 4,617 365

NL 264,839 23,249

AT 158,338 66,883

PL 63,934 4,588

PT 108,384 19,828

SI 10,760 3,261

SK 10,150 1,120

FI 68,948 17,248

SE 113,094 28,520

UK 1,728,510 -

EU 25 total 6,795,082 1,038,035

Current financial crisis (III)

100K€ Eligible deposits (m€) Absolute exposure (m€)

BE 188,791 87,313

CZ 40,854 1,035

DK 106,029 29,620

DE 1,615,946 701,172

EE 2,590 164

IE 143,226 66,820

GR 98,926 34,533

ES 575,940 193,477

FR 839,391 27,070

IT 511,527 -CY 16,887 1,494

LV 5,115 323

LT 3,903 147

LU 86,734 40,435

HU 27,649 1,228

MT 4,617 409

NL 264,839 55,906

AT 158,338 84,854

PL 63,934 5,370

PT 108,384 21,873

SI 10,760 3,332

SK 10,150 1,253

FI 68,948 21,541

SE 113,094 38,884

UK 1,728,510 261,259

EU 25 total 6,795,082 1,679,510

Financial crisis and quantitative methods: problems and solutions

Data Problems

Deposits/Fund/Premiums

Past DGS actions

Payout delays

Cross-border exposure

Qu

an

t.Q

ualit

. Triggering event

Intervention procedure

Authorities involved

Dataset incomplete

Confidentiality

Definitions

Late answers (DE missing)

Aggregation of data

Missing information

Heterogeneity of data

Overlapping with bankruptcy law

Investigating DGS Efficiency

Financial crisis and quantitative methods: problems and solutions

DGS Actions

Types

Payout (16 DGS out of 37)

Preventive (21 DGS out of 37)

Since 1994 only 22/37 DGS

have intervened

67 payouts (37 EU-15, 22

UK)

27 preventive (26 EU-15)

No cross-border cases

Financial crisis and quantitative methods: problems and solutions

Triggering Event of Payouts

Following the Directive the

event triggering the payout in all

EU MS is the unavailability of

deposits

The DGS intervenes only after

the declaration by the competent

authority

No common rules

Financial crisis and quantitative methods: problems and solutions

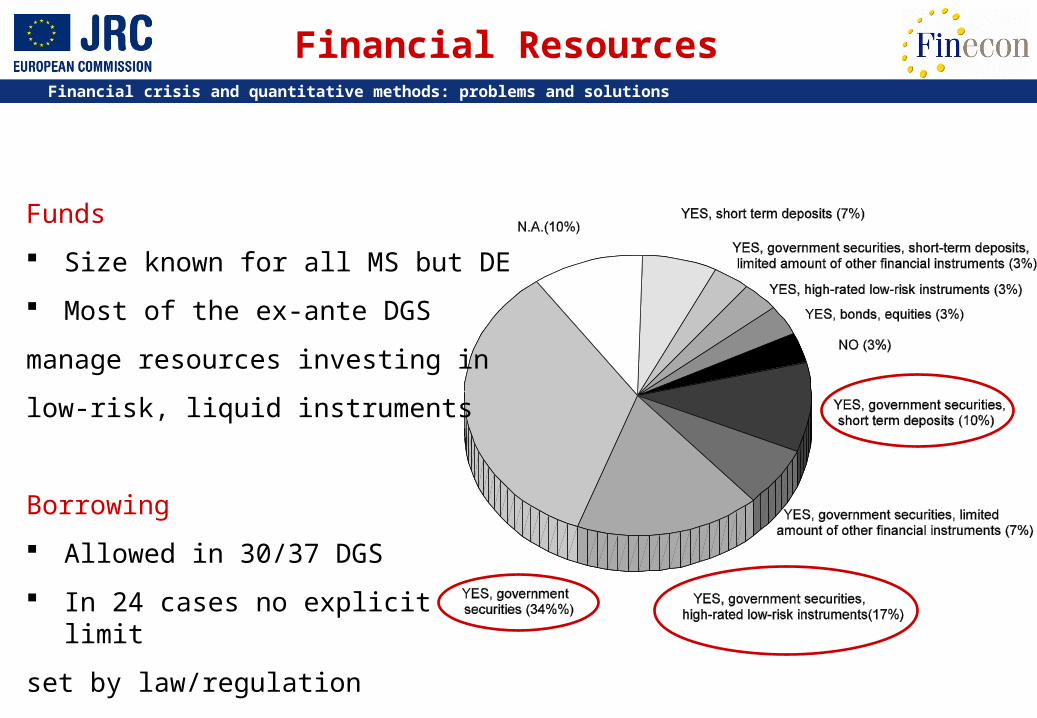

Financial Resources

Funds

Size known for all MS but DE

Most of the ex-ante DGS

manage resources investing in

low-risk, liquid instruments

Borrowing

Allowed in 30/37 DGS

In 24 cases no explicit limit

set by law/regulation

Financial crisis and quantitative methods: problems and solutions

Payout Delays

AmountNumber

Financial crisis and quantitative methods: problems and solutions

Scenarios Definition

Scenario 1: High

Scenario 2: Medium

Scenario 3: Small

Scenario 4: Medium

Scenario 5: Very High

Payout

Preventive

Cross-border

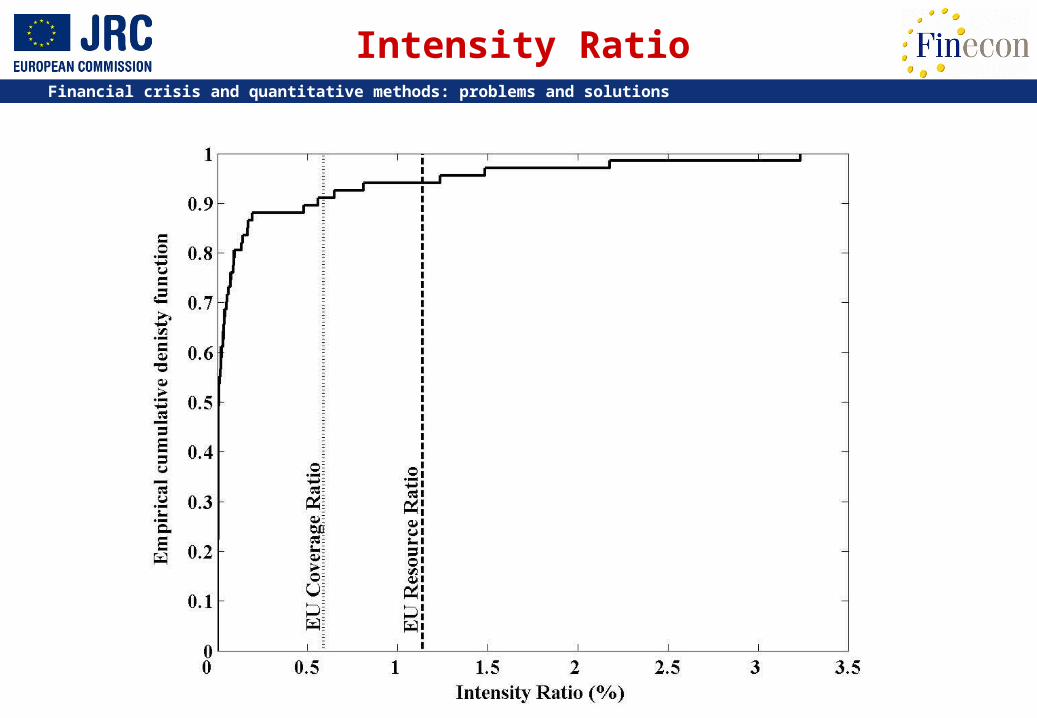

IR = 3.24, highest in EU-12

IR = 0.81, 2003 failure in EU-12

IR = 0.035, highest in EU-15

IR = 0.16, 2003 failure EU-15

Fictitious, due to lack of data

Deposits Eligible of Amount TotalonInterventi ofCost Total Intensity Ratio =

Financial crisis and quantitative methods: problems and solutions

Scenarios Results EU-15

BB

Financial crisis and quantitative methods: problems and solutions

BBB B BB

B B

Scenarios Results EU-12

Financial crisis and quantitative methods: problems and solutions

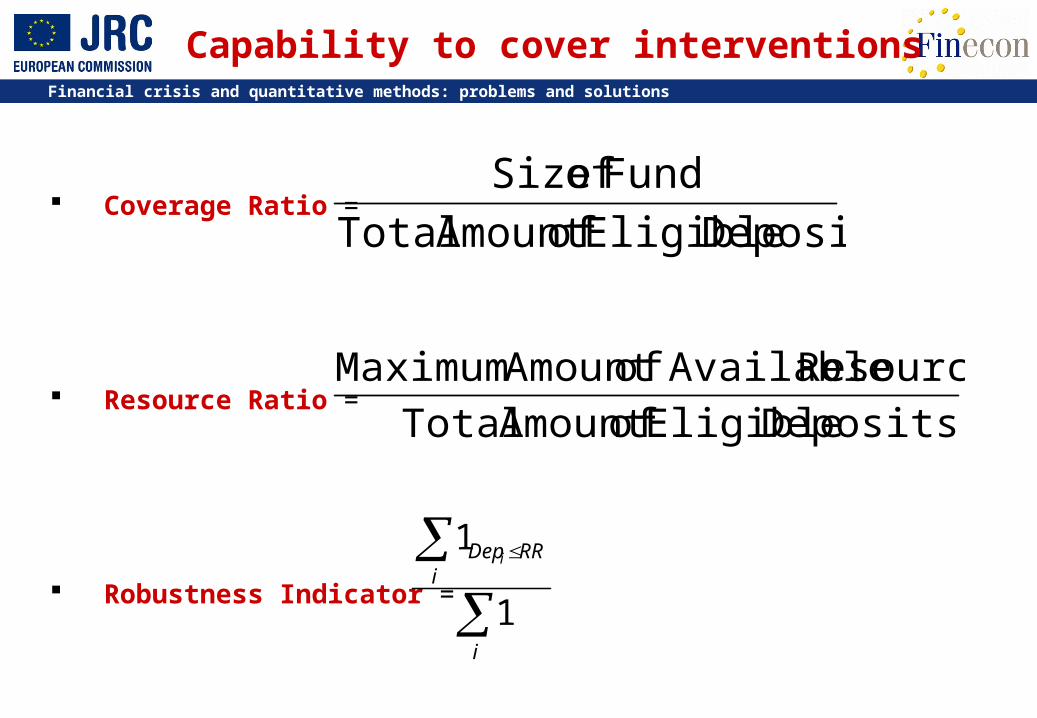

Coverage Ratio =

Resource Ratio =

Robustness Indicator =

Capability to cover interventions

Deposits Eligible of Amount TotalResources Availableof Amount Maximum

Deposits Eligible of Amount TotalFund of Size

i

iRRDepi

1

1

Financial crisis and quantitative methods: problems and solutions

Coverage and Resource Ratio

Financial crisis and quantitative methods: problems and solutions

Intensity Ratio

Financial crisis and quantitative methods: problems and solutions

Cross-border exposures: branches

Financial crisis and quantitative methods: problems and solutions

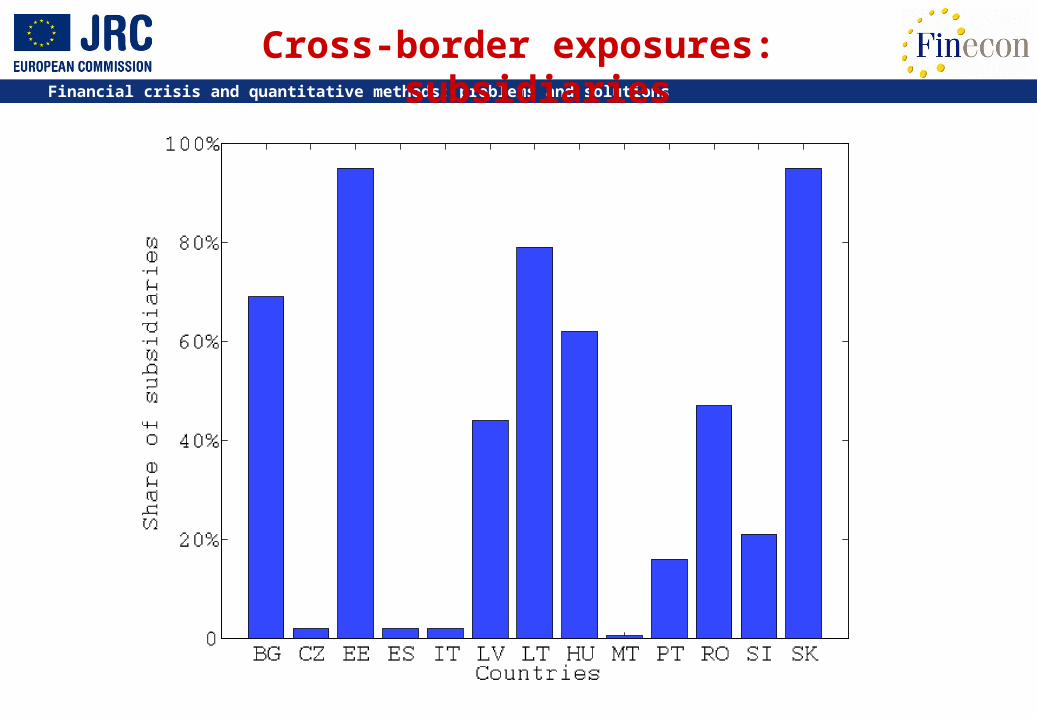

Cross-border exposures: subsidiaries

Financial crisis and quantitative methods: problems and solutions

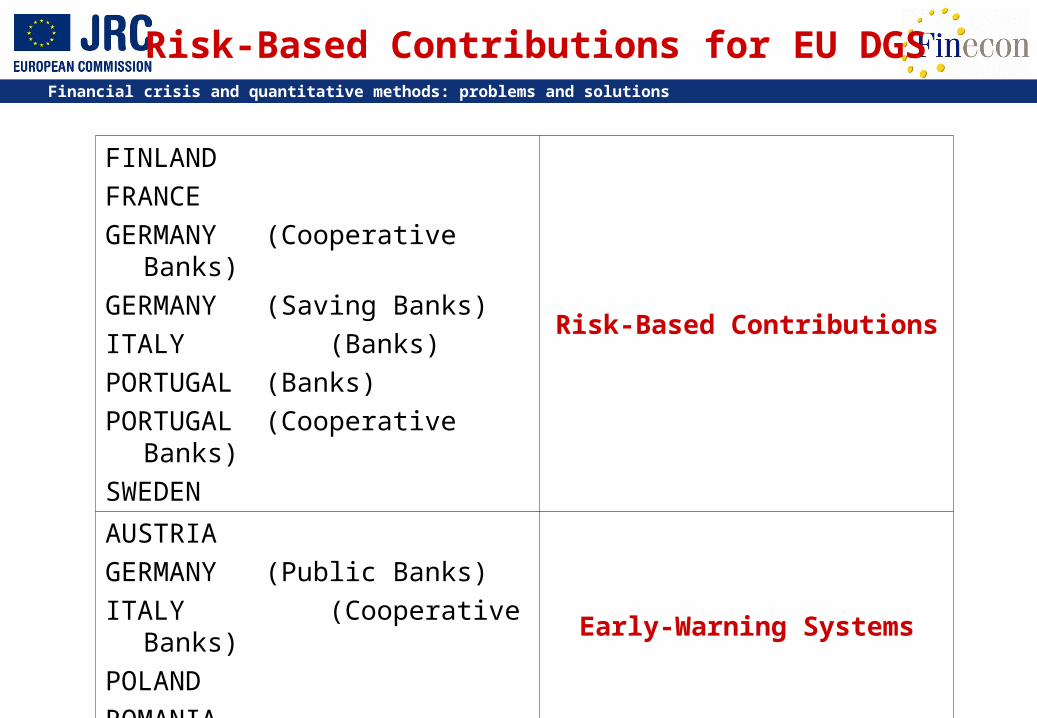

Risk-Based Contributions for EU DGS

FINLANDFRANCEGERMANY (Cooperative

Banks)GERMANY (Saving Banks)ITALY (Banks)PORTUGAL (Banks)PORTUGAL (Cooperative

Banks)SWEDEN

Risk-Based Contributions

AUSTRIAGERMANY (Public Banks)ITALY (Cooperative Banks)POLANDROMANIA

Early-Warning Systems

Financial crisis and quantitative methods: problems and solutions

Indicators

Capital Structure / Solvency Profile

Riskiness / Exposure

Profitability / Income

Maturity transformation / Duration

Classes ofIndicators

• The risk is assessed using indicators

• The indicators are built using financial ratios based on balance-sheet data, financial statement data or other types of accounting data

• Current ratios are quite heterogeneous

Financial crisis and quantitative methods: problems and solutions

Towards a common Risk-Based System

iii xc

Homogenous Framework: identification of a generalized formula for risk-based contributions ci of the i-th member

xi = i-th member’s contribution base (e.g. eligible or covered deposits…)

i = i-th member’s risk-based adjustment

= fixed percentage determining the aggregated contribution (i.e. NOT influenced by single members’ risk, common value for ALL members)Indicators Scores Rating

Classi

Financial crisis and quantitative methods: problems and solutions

Contribution

OAC ∙ NSR

Overall Amount

of Contribution

(OAC)

Net Risk Amount

(xi + i) ∙i

Correction i

Contribution base (xi + i)

Indicators

Scores i

Net Share of

Risk (NSR)

France

Financial crisis and quantitative methods: problems and solutions

Contribution Quotas

Risk

Correction (i)

Indicators (WAAI)

ContributionRegressive Quotas

Dimension Correction (i)

Proportional Quotas

Covered Deposits

Italy – Commercial banks

Financial crisis and quantitative methods: problems and solutions

Elasticity analysis

Financial crisis and quantitative methods: problems and solutions

Reliability and time evolution

Financial crisis and quantitative methods: problems and solutions

Real mathematical modelling...

Merton framework: it assesses the credit risk of a bank by characterizing the bank's equity as a call option on its assets.

The bank has a certain amount of zero-coupon debt that will become due at a future time T.

The bank defaults if the value of its assets is less than the promised debt repayment at time T.

The equity of the bank is a European call option on the assets of the bank with maturity T and a strike price equal to the face value of the debt. The model can be used to estimate the risk-neutral probability of the bank.