Embed Size (px)

DESCRIPTION

Financial magazine of the Luxembourg financial industry. This edition includes a finance

Citation preview

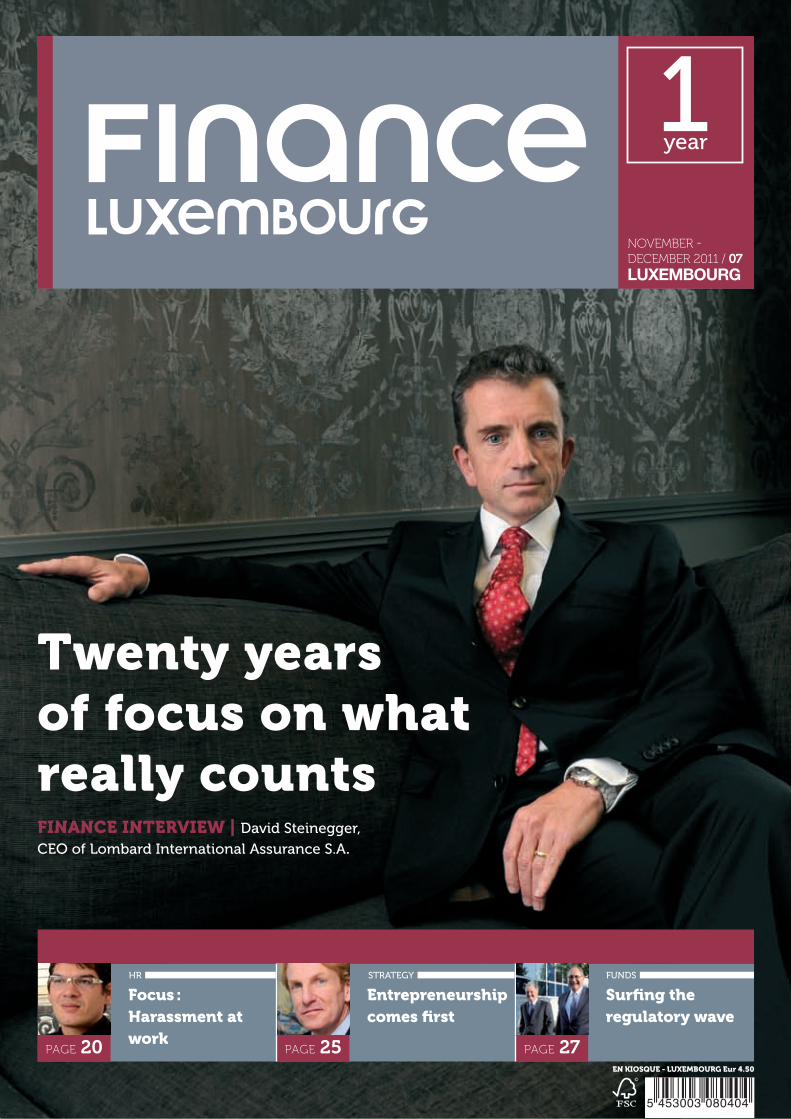

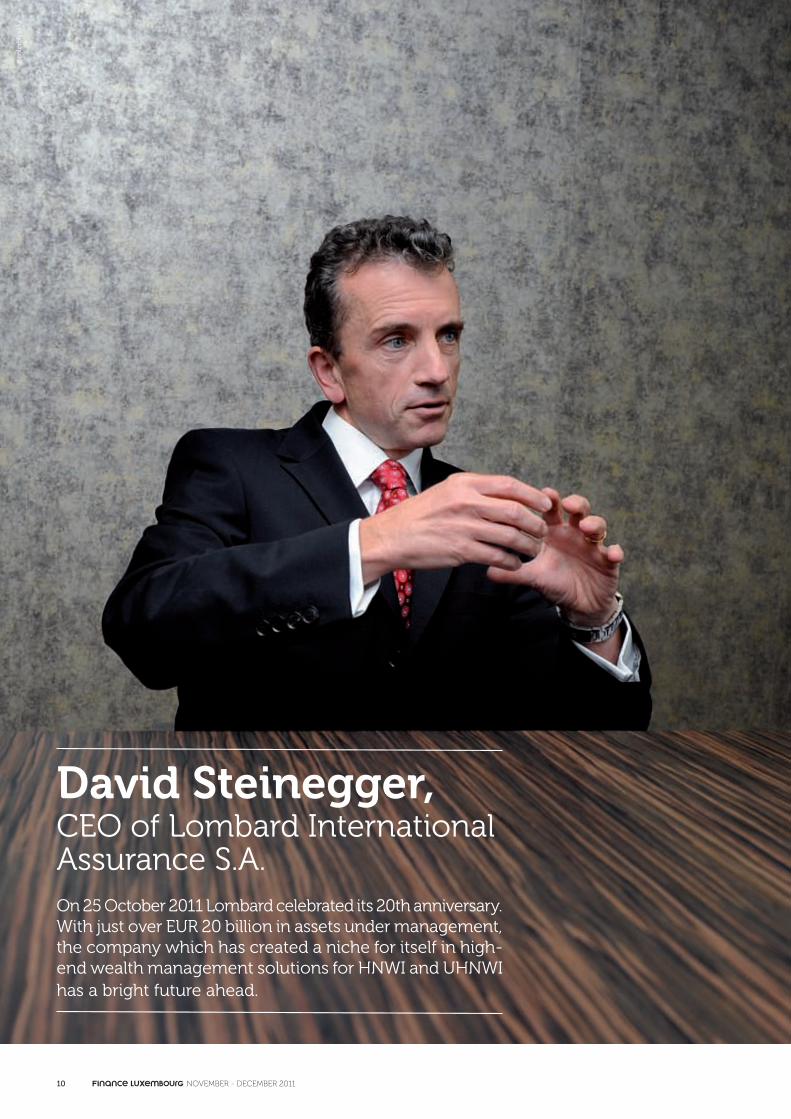

Twenty years of focus on what really countsFINANCE INTERVIEW | David Steinegger,

CEO of Lombard International Assurance S.A.

HR

Focus : Harassment at work

STRATEGY

Entrepreneurshipcomes first

FUNDS

Surfing the regulatory wave

PAGE 20 PAGE 25 PAGE 27EN KIOSQUE - LUXEMBOURG Eur 4.50

5 453003 080404

novEmbEr - dEcEmbEr 2011 / 07LUXEMBOURG

Must one be waryof awarded banks

PRIVATE BANKING

BCEE – rewarded for its stability, year after year.

Äert Liewen. Är Bank.

Banq

ue e

t Cai

sse

d’Ep

argn

e de

l’Et

at, L

uxem

bour

g, é

tabl

isse

men

t pub

lic a

uton

ome,

1, P

lace

de

Met

z, L

-295

4 Lu

xem

bour

g, R

.C.S

. Lux

embo

urg

B 30

775

For the third year running, the fi nancial magazine “Global Finance” awards BCEE with their “Best Bank Award – Luxembourg”. And for the fi fth time, the equally renowned “The Banker” magazine awards its “Bank of the Year – Luxembourg” title to BCEE. The “Spuerkeess” is, thus, perfectly suited to manage your capital and to offer you customised Private Banking services, entirely focused on your needs. Locate your nearest BCEE Financial Centre on www.bcee.lu or call (+352) 4015-4040.

BCEE Private Banking: Your fortune deserves attention

BCEE_FinanceNation_UK_A4_Visu1.indd 1 07/11/11 16:00

by

29, rue Notre-DameL-2240 Luxembourg Grand-Duché de Luxembourg

T. +352 26 10 86 26F. +352 26 10 86 27E. [email protected] Internet: www.financenation.lu

Eric [email protected]

The Editorial [email protected]

Delphine ReuterSub-editorT. +352 26 10 86 [email protected]

Raphaël HenryJournalistM. +352 691 99 11 [email protected]

Editorial Committee Editorial GuestsFlorence StainierFrançois GénauxPatrick Picco

Émilie MounierSales ManagerM. +352 691 99 11 [email protected]

Isabelle LiboutonProject ManagerM. +352 661 50 36 [email protected]

Alexandre TrânWeb Project ManagerM. +352 661 16 44 [email protected]

Photography Sébastien Héraudwww.colorblind.lu

Photos Finance Nation www.financenation.lu/photo

Layout Piranha et Petits Poissons [email protected]

SubscriptionLuxembourg 45,- € - Europe 55,- €abo.financenation.lu

Finance LuxembourgIBAN LU53 0030 7526 7288 1000BIC BGL: BGLLLULL TVA LU 19730379RC Luxembourg B 95210

Maison d’éditions - Autorisation d’établissement N° 102739 © Toute reproduction, même partielle, est soumise à l’approbation écrite préalable de l’éditeur. Tous droits réservés.

The grapes of indignity

It started with an email, an invitation or an order slipped in the middle of the message,

sent to the employees: “Pack your things and move”. Then slowly, without their being

aware of a growing problem, isolation swept in, reducing social interaction with their

colleagues to a few polite conversations. Once the damage was done, it was frightening

to see the person they had become - tired, broken, alone.

Psychological harassment is a serious issue that is affecting more and more people in

Luxembourg in the financial sector. Not because it is the financial sector, and not neces-

sarily because it is Luxembourg. But the absence of any legal framework condemning

or even attempting to prevent harassment at work from taking roots is, in a modern

society, unthinkable.

At a time when the financial crisis has weakened company structures, when mergers and

acquisitions are accelerating, and banks are being nationalised or re-capitalised, the un-

certainty that prevails today provides a ripe soil for the grapes of harassment to grow.

For now, the problem is left to rot in a backroom - just like all those who are suffering

in silence, too afraid or confused to speak up. It is time for the Ministry of Labour, the

Ministry of Health and the Ministry of Finance to gather all interested parties around a

table and discuss a law that is clear (to define what harassment is and differ it from stress-

related diseases), just (to give lawyers and magistrates the right instruments to defend

and judge), and simply human (for victims to finally recover their dignity).

By Delphine Reuter

kosm

o.lu

Use the stars to find your way

BUSINESS CONSULTING • TECHNOLOGY CONSULTING • PROFESSIONAL RESEARCH

PARC D’ACTIVITÉS DE CAPELLEN

38 RUE PAFEBRUCH L-8308 CAPELLEN

LUXEMBOURG

www.ngrconsulting.com

Independent and specialized in the financial sector, NGR Consulting provides consulting services to leading financial institutionshelping them to improve their business performance.

Combining business expertise in Fund Services, Private Banking & Asset Management with deep understanding of market trends,we work closely with our clients to design innovative business strategies and solutions which deliver quick added-value results.

Need to experience a new idea of consulting? Contact us at [email protected]

Annoncesimple_NGRstar_A4:Mise en page 2 6/03/09 9:40 Page 1

8

FInAncE InTErvIEW

david Steinegger, Lombard

International Assurances S.A.

InSUrAncE10 - david Steinegger, Lombard International Assurances S.A.

FUndS27 - State Street surfs on the regulatory wave

30 - meet Luxembourg's Private Equity & venture capital Association

42 - Why invest in clean technologies

60 - Snapshots - ALFI Global distribution conference

PrIvATE bAnKInG54 - bankers uncertainty echoed in IT choices

STrATEGY25 - How Allen&overy puts entrepreneurs in the driver's seat

45 - restructuring through Luxembourg

52 - How LFF sells Luxembourg in Asia

64 - Sparking innovation and financing it

Hr20 - Focus - Harassment at work

66 - careers

AmL34 - How a rogue lawyer became financial consultant

38 - risk management in Islamic Finance - Zakat

63 - Event - An AmL & KYc tool for SmEs

AccoUnTInG48 - more coherence needed for tax optimisation

TEcH56 - How the cobIT framework helps bring IT and business closer

58 - Future domain names: a big opportunity

61 - Event - IT-powered governance can deal with management

and regulatory challenges

november - december 2011 / 07

Luxembourg to adopt legal framework for Family Office

The Ministry of Finance is working on a law

clarifying the role and responsibilities of

family offices, entities offering asset man-

agement services to families, individuals

and foundations. The ABBL estimates that

in Luxembourg, the Family Office business

represents about EUR 10 billion of assets

under management. But there could be

many more entities that do not yet use the

term as a reference for the services they

offer and having a legal framework could

entice them to make that choice.

CSSF approves Deutsche Börse and NYSE Euronext merger

In October 2011 the CSSF approved the

merger of Deutsche Börse and NYSE

Euronext, concluding that there are no

banking supervisory reasons against the

merger in Luxembourg. The CSSF exam-

ined the admissibility of the acquisition of

important shareholdings in Clearstream

companies within Deutsche Börse Group

in Luxembourg by the parent company

of the new group, Holdco, domiciled in

the Netherlands. The shareholdings in-

clude Clearstream International S.A. and

Clearstream Services S.A., as well as Clear-

stream Banking S.A. as an international

settlement institution. The BaFin, the

German regulator, had already approved

the merger. The transaction is subject to

further closing conditions.

Chamber of Commerce criticises 2012 budget plan

According to the Chamber of Commerce

the budget presented by the Luxembourg

government for 2012 does not sufficiently

protect the country against the current finan-

cial crises and provides no safeguard if the

Déclarants 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Etablissements de crédit 113 265 375 411 470 387 375 452 636 1166 4629

Autres professionnels du secteur financier 5 15 34 27 43 33 45 50 45 54 63

Assurances 12 49 95 60 43 28 41 26 27 46 78

Notaires 0 0 0 1 3 4 4 0 1 2 4

Réviseurs d'entreprises 1 12 7 4 3 13 6 4 8 12 10

Experts-comptables 0 3 4 5 16 19 11 17 25 29 46

Casinos 1 0 0 0 0 0 1 3 7 15 21

Agents immobiliers 0 0 0 0 0 2 1 0 1 0 0

Avocats 0 0 0 0 0 3 1 0 2 6 13

Conseils économiques et fiscaux 0 0 0 0 0 1 0 0 0 1 2

Marchands de biens 0 0 0 0 0 1 1 0 0 1 0

Total des déclarations 132 344 515 508 578 491 486 552 752 1332 4866

Eurozone crisis were to last. The Chamber

declared that the crises “strongly threaten

Luxembourg’s growth potential on the mid-

and long-term with negative consequences

on its social security system.” The Chamber

calculated the deficit faced in 2012 will be of

EUR 1,143 billion as a result of more expendi-

tures (+6,1 percent) combined to insufficient,

although rising, revenues (+4,9 percent). Cur-

rent expenditures progress too quickly taking

into account mid-term economic growth and

the European average, economists said. “The

need to further be in debt when all countries

lower their lifestyle standards proves that

Luxembourg does not perceive these risks

as threats and prefers worsening its deficit

instead of reforming it,” they said.

Read the whole declaration on http://bit.ly/tNanFz

LuxCSD, access point to TARGET2

On 17 October 2011 LuxCSD started op-

erating as the national access point for

Luxembourg to TARGET2-Securities. Lux-

CSD was designated Securities Settlement

System by the Luxembourg central bank

and is required to operate under the pro-

tection of the Settlement Finality Directive.

Incorporated in July 2010, it is jointly owned

by the Banque centrale du Luxembourg

(BCL) and Clearstream International. Lux-

CSD covers securities settlement in central

bank money, general issuance services,

issuance services for funds, asset servicing,

asset and connectivity.

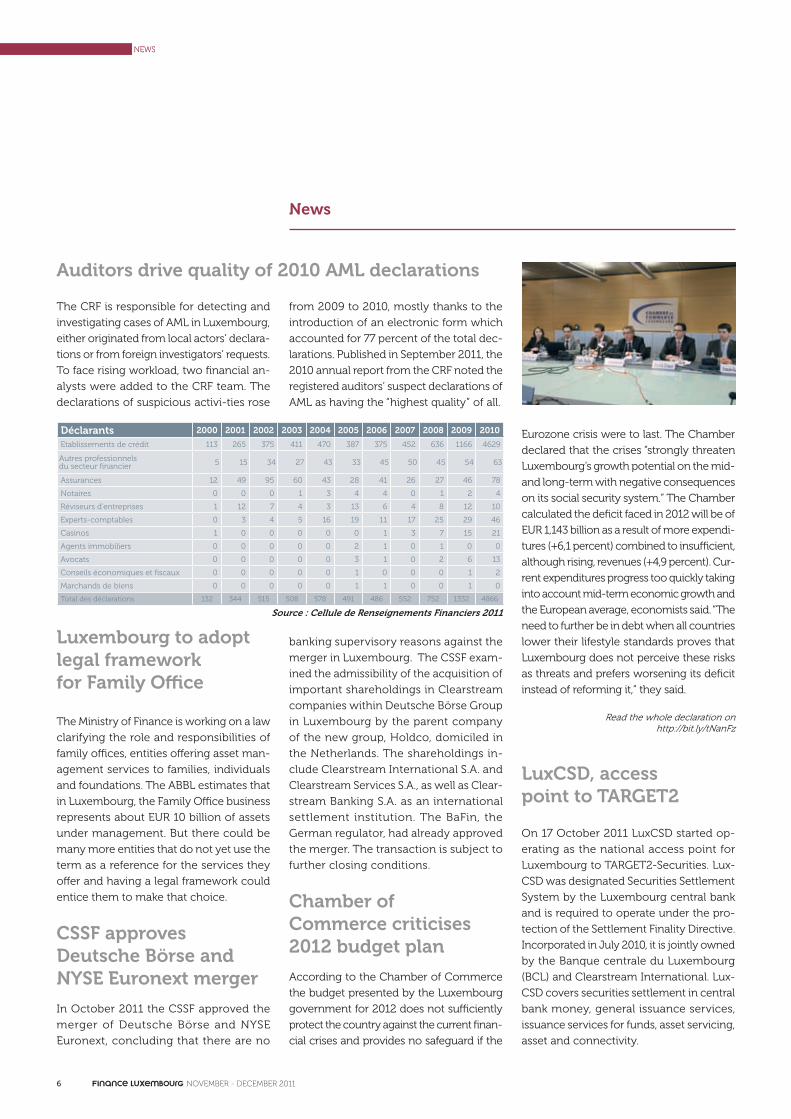

The CRF is responsible for detecting and

investigating cases of AML in Luxembourg,

either originated from local actors’ declara-

tions or from foreign investigators’ requests.

To face rising workload, two financial an-

alysts were added to the CRF team. The

declarations of suspicious activi-ties rose

from 2009 to 2010, mostly thanks to the

introduction of an electronic form which

accounted for 77 percent of the total dec-

larations. Published in September 2011, the

2010 annual report from the CRF noted the

registered auditors’ suspect declarations of

AML as having the “highest quality” of all.

Source : Cellule de Renseignements Financiers 2011

Auditors drive quality of 2010 AML declarations

News

6 novEmbEr - dEcEmbEr 2011

nEWS XXXXXXXXXX nEWS

exigo s.a. 11, rue de Bitbourg L-1273 Luxembourg/Hamm tel: +352 27 04 311 fax: +352 26 43 26 07

exigo consultingWe support you in Banking software implementation proj-ects, business process optimizations, definition of sourcing strategies and the design of related IT architectures.

exigo CIO OfficeAs interim CIO or assistant to the CIO, we assess your IT organisation and help you implementing industry best prac-tices. We define (out)sourcing strategies, IT architectures and survey the project implementation.

exigo sourcingexigo sourcing is an integrated recruitment service that was designed to support our consulting and CIO Office business lines. We offer you win-win sourcing solutions by searching, selecting, & assessing the right profiles for your projects.

Banking experts with IT competence

www.exigo.lu

News

SocGen Private Banking officer awarded

Eric Verleyen, Chief Investment Officer of

Private Banking activities at Société Générale

Bank & Trust, has just been nominated in

the Private Banker International Awards,

outstanding young private bankers 2011.

This prestigious award highlights up-and-

coming private bankers under the age of

40 who are leaders in the industry. "I am

delighted to receive this international award.

It is recognition of the work accomplished

by the teams at Societe Generale Private

Banking in Luxembourg and underlines the

excellent opportunities for career develop-

ment at all levels of the private bank."

PwC handbook on Lux GAAP

After a first successful handbook released

in 2005, PwC Luxembourg has made avail-

able its “Handbook for the preparation of

annual accounts under Luxembourg ac-

counting framework” for companies, PSFs

and holdings. The 2011 version (FR, EN or DE)

contains an updated presentation of the new

information that companies should provide

to the tax authorities, many examples, and

references to the legal framework. It also

explains upcoming changes such as the

e-VAT and the electronic reporting of an-

nual accounts (2012). Contrarily to the 2005

edition which was free, this version can be

bought online on Luxembourg editor Leg-

itech’s website. The aim is to reach a wider

readership than PwC’s customer base.

More info: www.pwc.lu &www.legitech.lu

New fund domiciliator born from strategic cooperation

In October 2011 Luxembourg Investment

Solutions S.A., a regulated (UCITS-licensed)

management company and Butterfield

Fulcrum, a global independent services

provider for the alternative investment

industry, signed a strategic cooperation

agreement to provide management com-

pany and fund administration services in

Luxembourg.

Private Bankers evoke the future of their business

On 27 October 2011 banking software com-

pany Avaloq organised a roundtable on

the future of Private Banking. The speakers

were Roger Hartmann (CEO of VP Bank

group), Luc Rodesch (Member of Banque

de Luxembourg's Executive Committee

and President of the ABBL Private Banking

Group), Claude Marx (former Deputy CEO

of HSBC Private Bank in Luxembourg), Paul

Chambers (Partner at ATOZ) and Francisco

Fernandez (CEO of the Avaloq Group). The

event, moderated by Frédéric Kemp, Man-

aging Director Benelux of Avaloq, gathered

more than 60 participants, most of them

members of Luxembourg banks Executive

Committees. For Luxembourg, participants

underlined the need to attract more and

more Ultra High Net Worth Individuals and

develop the right services for them. The

ability to provide tailor-made products to

customers and the speed at which these

products need to be adapted were also

highlighted. Other topics included transpar-

ency and investor protection; the expertise

of the Relationship Managers and the dif-

ferent initiatives of the ABBL and of the

government in that respect and in the pro-

motion of the financial marketplace; and

the impact of new technologies.

Who are the future owners of Dexia BIL and KBL?

On 10 October 2011 the Luxembourg

Minister of Finance announced that

Qatari investors could save cash-

strapped KBL and Dexia BIL. If the

CSSF approves the procedure, the

Qatari Prime Minister Sheikh Hamad

bin Jassim bin Jabr Al-Thani and his

sons will own part of KBL and Dexia

BIL through their Luxembourg-

based holding Precision Capital. The

Prime Minister started investing in

Luxembourg in 2006 through his

holding Balestra Properties, which

last March became Precision Capital.

Sheikh Hamad also owns UK-based

Challenger Universal, which was

specially created in 2008 to hold shares

in Barclays. The second richest man of

Qatar after the Emir, he is also the CEO

of the ubiquitous Qatar Investment

Authority (QIA), owned by members

of the al-Thani royal family. On the

board of QIA, which is in the world’s

top 10 sovereign wealth funds, sit the

representatives of Qatari institutions

like the governor of the Qatar Central

Bank and the Vice Chairman of the

Qatar Exchange. Luxembourg is not

the al-Thani family’s first coup d’essai in the European banking world. While

QIA is not directly investing in the

Luxembourg banks, it holds 100 percent

shares of Qatar-based Qatar Holding

LLC. Sheikh Hamad is a director of this

company, next to Bahrein-based Ahmad

Mohamed Ahmad Yussef Al-Sayed. Mr

al-Sayed is also one of the managers

of two Luxembourg-based holdings,

Qatar Holding Luxembourg and Qatar

Holding Luxembourg II, which are

both 100 percent subsidiaries of Qatar

Holding LLC - and therefore of QIA.

Qatar Holding LCC holds investments in

Barclays, Credit Suisse, Santander Brazil,

and the London Stock Exchange.

More info:Qatar Financial Centre Authority

http://www.qfc.co

8 novEmbEr - dEcEmbEr 2011

nEWS XXXXXXXXXX nEWS

Essential for Banking

For more than 25 years, Avaloq has been successfully providing major banks with integrated and comprehensive banking software solutions. Avaloq’s ‘ready for banking’ solutions cover a broad range of fully integrated back, middle and front office functionalities which are successfully operated in the most demanding financial centres worldwide. Today, leading retail, wealth management and universal banks in more than 20 countries rely on Avaloq as a compe-tent innovation partner and advisor. The Avaloq community represents a unique network of excellence consisting of customers, partners and experts who co-design the future of banking. Avaloq employs more than 600 banking and IT specialists. The company has its headquarters in Zurich (Switzerland) and two main software development centres in Switzerland and the United Kingdom. In addition, the company maintains branch offices in strategically important financial centres such as London, Frankfurt, Luxembourg, Vienna, Geneva, Moscow, Singapore and Hong Kong.

www.avaloq.com

We deliver what we promise. Therefore we have a

100% success rate in implementing our

integrated banking software solution in the most demanding financial centres around the globe.

Ready to join our community?

2011P U B L I - N E W S

MOST INNOVATIVE

BANKING SOLUTION

2011

David Steinegger, CEO of Lombard InternationalAssurance S.A.On 25 October 2011 Lombard celebrated its 20th anniversary. With just over EUR 20 billion in assets under management, the company which has created a niche for itself in high-end wealth management solutions for HNWI and UHNWI has a bright future ahead.

© c

olo

rblin

d.lu

10 novEmbEr - dEcEmbEr 2011

Fin

ance

Inte

rvie

w

novEmbEr - dEcEmbEr 2011 11

© c

olo

rblin

d.lu

12 novEmbEr - dEcEmbEr 2011

Mr Steinegger, who is Lombard today?

Lombard is the leader of the ”privatbancas-

surance” market, a niche market that we

created 20 years ago. The privatbancas-

surance concept combines private banking

and investment management services with

the sophisticated use of life assurance as

a financial planning structure to achieve

fiscal advantages and security for wealthy

investors and their families.

Lombard was founded by John Stone in

1991 and was the first company set up with

the vision to create a pan-European insur-

ance business from a Luxembourg base.

This became possible under the Third Life

Directive which was implemented in the

early nineties. The pan-European insurance

idea was very well supported by the Lux-

embourg regulator, the Commissariat aux

Assurances (CAA), and government to create

the right infrastructure so companies like

Lombard could get off the ground. In effect,

we have a passport, through the EU free-

dom of services, to market our solutions into

other European countries without needing

to establish a physical presence there.

We started in Luxembourg with five people

and no assets under management. Today, we

are celebrating our twentieth anniversary and

we’ve just reached EUR 20 billion under man-

agement. I would say it’s been a real success

story, from a small pioneering beginning, to

the leader in the market, a position we have

held for more than 10 years.

How has Lombard evolved over the years?

Lombard started with a few Independent

Financial Adviser (IFA) partners and our first

three countries were Belgium, Sweden and

Germany. In the mid-nineties we had our first

breakthrough with one of the major private

banking groups, Swiss Bank Corporation,

which became UBS. We persuaded them to

try the privatbancassurance concept for their

wealthy clients. Until then, if you had talked

to a private banker about life insurance, they

would have laughed – insurance was not

seen as a solution for wealthy, sophisticated

clients. Since then we have seen a dramatic

change in the acceptance of privatbancas-

surance and today it is widely recognised as

one of the most effective wealth planning

tools for private clients.

In the early days there was little competition

but we have seen this change significantly

in recent years. This has not been bad for us,

because competition has created a much

bigger market place, which in turn has

helped Lombard to grow and develop.

We have also seen the market evolve from

attracting affluent individuals, to HNWIs,

which we define as individuals investing

at least EUR 1 million in a life insurance

solution. More recently again, over the last

four to five years, the UHNWI end of the

market, for investments of EUR 10 million

or more, has risen sharply and now about

40 percent of Lombard’s business is with

these individuals.

Over the last ten years, we’ve seen a growth

of about 25 percent per year in terms of

our total assets under management. Back

in 2001, we were just under EUR 2.1 billion

of assets under management, and now we

have reached EUR 20 billion.

Can you describe what Lombard offers?

At the core of our business model is the

sophisticated use of life insurance as a

wealth planning tool, to convey tax and

estate planning benefits to wealthy indi-

viduals. Our focus is on generational or

succession planning, enabling individuals

or families to plan how assets get passed

on to the next generation. Depending on

where the client resides, there are tax ben-

efits in all European countries associated

with life insurance, but the precise benefits

vary significantly by country.

Innovation is at the heart of our success.

We are a relatively small company and

responding to the ever changing needs

of clients, as well as to legal and regula-

tory changes is something that we have

become very adept at. We have invested

heavily in building a specialist wealth plan-

ning solutions team, which together with

our marketing consultants who operate

in the local countries, are capable of re-

sponding to the ever changing markets in

which we operate. Luxembourg has been a

good centre to find these specialist people.

In many ways, we have a very simple model

– designing long-term wealth planning

solutions to meet the needs of HNWIs.

How do you reach your clients in the first place?

From a distribution point of view, we

never deal directly with end clients. We

work through specialist financial intermedi-

aries, and in particular private banks, HNWI

focused brokers and other independent

advisers to wealthy families such as fam-

ily offices, lawyers and accountants. As a

direct result of the financial crisis we have

seen many more clients turning to inde-

pendent advisers, who work alongside the

clients’ bankers, to advise on long-term

wealth planning solutions. We operate a

completely open architecture approach

to investment management, and Lombard

never undertakes any investment man-

agement. Today we work with over 500

reputable investment managers on behalf

of clients.

Are you seeing big changes in client requirements?

We have seen a significant shift in what cli-

ents want – there is much more talk today

about wealth protection rather than simply

investment growth. One of the clients’ fears

arising from the recent financial crisis is:

‘How do I protect my assets?‘ In the last

quarter of 2008, for example, when the

financial world seemed to be collapsing

and people were wondering if their money

was safe and how they could protect it, we

saw a flood of new money coming into

Lombard, and we had our best quarter ever.

Furthermore, this concept has advantages

beyond Europe. Take Latin America, for

example, where one of the big fears clients

have is of kidnapping or extortion. In this

context, a Luxembourg life policy offers a

safe environment for clients. That has been

DaviD Steinegger FINANCE INTERVIEW

novEmbEr - dEcEmbEr 2011 13

a big factor for us to promote our solutions

outside of the European markets.

Which are your core markets today?

As I mentioned earlier, in the early days we

started in three markets, Germany, Sweden

and Belgium. Over the years, we’ve typical-

ly added one new market every couple of

years. Today, we market our solutions across

a number of major European markets, and

we’ve also extended our presence to Asia

and Latin America.

Italy, Spain, Germany, UK and Belgium are

our five largest European countries. Sweden,

Finland and France have tended to be smaller,

but we do see strong growth prospects in

these three markets and have invested in ad-

ditional resources to further develop these.

Do you write high volumes of business?

Our target clients are those with EUR 1 million

and above, so we’re not a high volume player

in terms of policies but we are in terms of the

average policy value. If you spoke to some

of our competitors, they may write tens of

thousands of policies in a year but average

premium tends to be much smaller.

How do the products come together, does it come a bit from the client’s, partner’s side or from Lombard?

We don’t have products, but instead we work

on developing solutions that are tailor-made

to meet individual client needs. Our starting

point is to understand each client’s needs. We

don’t advise clients but instead work closely

with the client’s advisers and lawyers, our

partners and our own in-house experts.

Wealthy individuals often have complex

needs. Take for example a Swede living

in Sweden and wanting to retire in Spain,

while his children live in Paris and London.

He wants a long-term succession solution

that can work today in Sweden, and which

can be transported to Spain on retirement,

whilst also work as a succession plan-

ning tool. Our partners approach us with

many complex client situations and the

question we face is "can we design a solu-

tion that can meet that client’s needs?” Our

approach is to find ways to be innovative,

with the help of our highly skilled team of

experts, with their insurance, legal, invest-

ment and succession structuring knowledge.

When you look at your partnerships, how important have family offices in Luxembourg become?

Our experience with family offices in Lux-

embourg is limited and Luxembourg has

not been a market we have focused on.

The reason is that Luxembourg is a very

small market, so if you compare it with

Germany, France or elsewhere the oppor-

tunities are much bigger elsewhere. We’ve

worked with a number of family offices,

particularly in Germany where the concept

is an important part of UHNWIs’ wealth

management arrangements. Following the

financial crisis, clients have turned more

to trusted adviser and this can include the

creation of a family office.

How does philanthropy intersect with your business?

Privatbancassurance can be used in the

context of philanthropy. When a client

dies, for example, he may decide to leave

part of his wealth to his children and

another part to a charity. But we’re not

directly involved - it will be the choice of

the client to donate this money.

Does Luxembourg have anything special to offer?

A unique feature of the Luxembourg

insurance regulatory framework is the

unrivalled security and protection which

it offers to clients. The concept itself is

known as the Triangle of Security, reflect-

ing the fact that a tri-partite agreement

is in place between the Luxembourg

insurance regulator, the Commissariat

aux Assurances (CAA), the custodian

bank and the insurance company. This

means that all clients’ assets have to be

held in an approved custodian bank and

those assets are ring-fenced from the

insurance company’s own assets. This

feature of Luxembourg has certainly been

an enormous advantage for the Luxem-

bourg insurance industry in comparison

with what is available in other competing

centres such as Dublin.

So you see Luxembourg more as a gateway to provide solutions in other European countries than in Luxembourg itself?

Yes, for us Luxembourg is a gateway, al-

though ironically after 20 years, we have

finally, last month, launched a solution for

Luxembourg resident clients.

As a base for our business Luxembourg has

been perfect. We have a supportive regu-

latory environment, a stable government,

a strong investor protection regime and

access to highly skilled and multi-lingual

resources.

Any down side?

Well Luxembourg is not cheap, and to be

successful as a business the key is to add

value through know-how, expertise, and

sophistication, so the Ryanairs of the insur-

ance world don’t choose Luxembourg!

In order to continue to prosper, Lux-

embourg needs to address a number of

important issues from a cost and infra-

structure perspective, whilst maintaining

a business supportive regulator and gov-

ernment. If this can be achieved we see

good opportunities to continue to grow,

not only for Lombard, but also for the

wider cross-border life sector.

Do you have competitors in this market?

For the first fifteen years of Lombard’s

existence, if people asked us about com-

petition, we said that we didn’t really have

any comparable competitors. We met

competition in individual markets, but

not cross-border competitors with the

geographical diversification of Lombard.

Typically we found other players operated

FINANCE INTERVIEW DaviD Steinegger

14 novEmbEr - dEcEmbEr 2011

© c

olo

rblin

d.lu

novEmbEr - dEcEmbEr 2011 15

© c

olo

rblin

d.lu

in one or two countries, rather than a

wide spectrum. In the last four to five

years, with our spectacular growth, com-

petition has arrived. Today there are three

or four significant players who are looking

to compete directly in our niche.

For Lombard, in some ways, it’s a good

thing because it keeps us from ever getting

complacent. The challenge is to remain

the market leader, by continuing to focus

on the things that have given us the edge

in the first place – fantastic distribution

partner relationships, innovation and ser-

vice. These building blocks are even more

important now that competition is here.

A further benefit from the arrival of

competitors is the fact that privatbancas-

surance is much better understood today

than it was ten years ago. In the past,

Lombard was a lone voice in the wealth

management. Today, because there are

many more companies in the market, the

understanding and the use of life insur-

ance is much clearer.

How are you approaching Asian clients?

Asia is an amazing place in wealth cre-

ation terms, and a great opportunity for

the wealth management businesses. Whilst

there are no real tax advantages associated

with our solutions, privatbancassurance

solutions can be used to provide clients

with security, asset protection and succes-

sion planning benefits. The right structured

solution can enable a client - a typical client

for us is a successful entrepreneur - to con-

trol these assets over his lifetime and even

beyond, whilst providing maximum investor

protection for those assets.

Our Asian business is small, typically it

has been less than 5 percent of our to-

tal business, but is growing significantly.

We intend to gear up our investment in

Asia over the coming years - we oper-

ate through a licensed broker in Hong

Kong and we’re considering a base in

Singapore. We see that as an exciting

opportunity for the longer term. We

think a lot more education and time is

needed working alongside private bankers

and other client advisers to explore and

explain the role of privatbancassurance,

16 novEmbEr - dEcEmbEr 2011

as well as the benefits of Luxembourg

within the Asian market.

Do you need to be present there in order to attract clients?

You certainly need a marketing presence.

Following our successful business model,

we would not set up an insurance com-

pany in Hong Kong or elsewhere. It’s about

operating there in a compliant way, working

through an authorised broker or a regulated

entity and marketing the Luxembourg story

into the Asian market. Our intention is to qua-

druple our Asian team in the coming years.

What about your growth in Latin America, is it comparable?

Latin America also represents less than 5

percent of our total business and we remain

committed to growing our Latin American

business too. The rate of growth is likely to

be slower however.

How do you see Lombard growing in terms of distribution partners?

If you name ten private banks, I’m sure

we have relationships with nine of them

today. Our aim therefore is to focus on

deepening our existing relationships with

key partners and extending our presence

with them in new markets. We may work

with a private bank in two markets to-

day, for example, so the challenge for us

is how we can extend this to work with

them in, say, four markets in the future.

So in essence we double our geographic

presence with that bank, but it’s still the

same relationship and at the same time

we remain focussed on our core markets.

We typically work on a very small percent-

age of a bank’s client base, we can focus

on doubling or tripling it from 0.1 to 0.2

percent. For the bank it’s still tiny but for

Lombard it can be very significant.

An area of growth in terms of the numbers

of partners is the sector described as inde-

pendent practitioners. They can be family

offices, tax advisers, legal advisers, etc.

This is an area we have certainly seen

growing since the financial crisis. Cli-

ents still have the money in three or four

different banks, and they turn to their

trusted adviser or independent practitio-

ner to decide on their wealth management

strategy.

At the same time, I believe there can be

a bright future for private banking, but it’s

about much more sophisticated products

than in the past. It’s about holistic wealth

management. The insurance industry and

private banking can complement each

other to ensure that together, we build

solutions that are useful and valuable for

clients in a context of a transparent, com-

pliant world.

So the future is bright?

The future is bright. And in many ways, it’s

even brighter than it was. As I said earlier

competition has helped to create a much

bigger market place – so the cake is much

bigger today than years ago. The erosion of

banking secrecy and the drive from clients

and partners to find compliant solutions is

also helping to create significant opportuni-

ties for our business.

Our optimism is also founded on the fact

that today’s global private clients’ wealth,

which can be estimated at more than

EUR30 trillion will be passed on to a fu-

ture generation over the next four or five

decades. Privatbancassurance’s penetration

of the generation planning market today

is still relatively small so there are strong

prospects for growth.

There’s growing pressure for compliance in the financial sector, How is this affecting Lombard?

The new world is all about compliance and

transparency and in this regard, privatban-

cassurance solutions have come of age.

I’m a great supporter of Luxembourg and

I think there are excellent opportunities for

Luxembourg in the future. But these oppor-

tunities have to be built around compliance.

We only provide solutions which are 100

percent compliant with the legal and fiscal

requirements of the client’s country of resi-

dence. For example, for a Finnish client, we

will provide a Finnish policy, in the Finnish

language, that meets the Finnish rules, but

it’s manufactured in Luxembourg.

Let’s go into the details of what you mean

by banking secrecy, what should be kept

and what should not.

The old world banking secrecy was where

clients hid their money somewhere and there

was no chance the taxman would ever find

out. That old world is largely dead in Europe

with all the recent changes we’ve seen. These

changes are irreversible and it’s moving in

one direction - the new world is about trans-

parency and disclosure, at least in Europe. The

future for Luxembourg has to be based on

fully compliant solutions for clients.

There is one part of banking secrecy which

remains important, and that is privacy. We

have a number of very wealthy clients,

and a number of famous clients. Wealthy

individuals want privacy – not to avoid

taxes – but to protect themselves and their

families from personal financial information

leaking out to the press or elsewhere. So

privacy is important. I think this is an area

where Luxembourg must remain strong in

the future. In Latin America, an important

feature for clients is this privacy, to minimise

the risk of extortion or kidnapping. As a se-

cure and stable environment Luxembourg

and the Triangle of Security can offer real

benefits to such clients.

How has the acquisition by Friends Provident and then its acquisition by Resolution affected Lombard?

Lombard was independent until 2005 when

we were acquired by Friends Provident, which

has now changed its name to Friends Life. We

have successfully maintained autonomy as

part of that deal. Our shareholder is happy to

leave us relatively autonomous, so long as we

deliver strong results and ensure that com-

pliance, risk and control is tightly managed.

We’re almost like a plug and play model;

you could unplug Lombard tomorrow

from the group and we would continue to

DaviD Steinegger FINANCE INTERVIEW

novEmbEr - dEcEmbEr 2011 17

operate as we are today. We’re ultimately

part of a bigger financial group so in terms

of support, we have it available if needed.

But in fact we haven’t had new capital since

we started in 1991.

So overall we have enjoyed a good rela-

tionship, and have delivered strong results

for our parent.

How are you affected by the volatility in the markets?

Privatbancassurance is not focused at all

on short-term investment performance.

Of course, clients will choose an invest-

ment strategy, but within the range of the

client’s investment risk appetite, privatban-

cassurance is all about a long-term wealth

planning solution, and not the short-term

market performance. It’s much more about

looking at the next ten or 20 years and

what’s going to happen even beyond that

period. The downside of volatility is that

certain clients and their advisers may prefer

to delay long term decisions.

What are the core issues the Luxembourg government should focus on in the future?

If you look at the insurance statistics, the

cross border sector is the dominant seg-

ment, and yet it’s been under-promoted

as an asset for Luxembourg. I'm on the

board of ACA, the insurance association,

and one initiative that has been kicked off

at last, is collaboration with Luxembourg-

for-Finance to improve the promotion of

this sector internationally. I’m happy that

progress is being made.

The government and the regulator have been

supportive of our business and it would not

be at the level it is at today had it not been

for their support. Over the years we have

seen some significant improvements in this

regard in terms of the regulatory flexibility,

for example of asset admissibility that we

provide to clients from Luxembourg. In this

regard, I think that an important factor for the

government is to make sure that Luxembourg

remains flexible and competitive.

The world changes very quickly and one

of Luxembourg’s advantages as a smaller

country is access to the political leaders and

decision makers. In my view, there’s a parallel

between the benefits for Luxembourg in the

phrase “small is beautiful” and for Lombard

too - using flexibility and focusing on under-

standing business and customer needs is an

advantage that some of the other economies

and bigger competitors will never have.

For the longer-term growth of Luxembourg

more investment is needed in infrastructure,

for example in relation to transportation and

schools – this is crucial to address. The au-

tomatic indexation of salaries mechanism is

also a competitive disadvantage for Luxem-

bourg. I hope this will change.

Luxembourg has a real multi-lingual capac-

ity and broad skill base in financial services.

Everything should be done to continue to sup-

port and promote this important advantage.

We’re been here 20 years now if these issues

can be addressed then I'm confident that

we, and others, will continue to thrive and

prosper for at least another years.

So what’s the key to Lombard’s future?

We’ve developed a business model that

provides innovative, tailor made solutions

and a very high level of service for partners

and their clients.

We intend to stay ahead of the com-

petition and remain the leader in the

market, by investing in innovation, ser-

vice and by continuing to build successful

partnerships.

But more important than anything are the

people we have. The real value of Lombard

is the team we have and we’re very proud

to have such a talented and committed

team. At the heart of our success is this

great team, and the entrepreneurial flame

that continues to burn brightly in Lombard.

So retaining, motivating and developing

the team is the key.

Interview by Depline Reuter

© c

olo

rblin

d.lu

banner_180x25.indd 1 3/1/2010 5:06:29 PM

© c

olo

rblin

d.lu

FINANCE INTERVIEW DaviD Steinegger

18 novEmbEr - dEcEmbEr 2011

Focus

In 2007, Mrs H. took a promising new po-

sition at a bank based in Luxembourg. A

hostile situation with a colleague progres-

sively degenerated until she decided to refer

it to her hierarchy. She says that while an

expert in mediations came to hear both

her and her colleague, the situation did

not improve. Less than a year after her

arrival, she received what she considers

was a really bad work evaluation. “It was

an aggressive and degrading judgment of

the quality of my work. It made me feel

worthless.” Feeling more and more isolated

from her colleagues with whom she barely

shared daily tasks, she was transferred for

a month to another service below her pay

grade – archives. “My colleagues were ask-

ing what I was doing there. I didn’t even

know myself. I was alone, surrounded by

empty desks.” She says that at the time

she only thought about her salary and her

17-year-old son. But a doctor appointment

changed everything.

At the end of November 2008, Mrs H. start-

ed seeing a psychotherapist on her doctor’s

advice. “She had been shocked to see the

state I was in.” The doctor diagnosed a

burn-out and told her to stop working to

prevent the situation from worsening. “I

cried, I knew she had nailed it. I knew I was

experiencing violence at work, but nobody

seemed to be able to help me.” The fol-

lowing January, she finally followed her

therapist’s advice and went on sick leave.

She says the relationship with her hierar-

chy became tenser after she came back. “I

felt more isolated than ever.” In July 2009,

she left the bank for another three months,

trying to pull herself back together. The fol-

lowing October, aware of her fragility, she

contacted the Human Resources depart-

ment to find a position more suitable to her

qualifications. “I still hadn’t let go of the idea

that I could succeed in my work.” She said

there was no clear indication as to what her

objectives or deadlines were. “I didn’t even

know when I could take days off.” She said

she continued seeing her therapist while

her moves at the bank were being watched

more closely. “I had to show certificates on

the same day of my appointments.” She

said she saw a colleague of hers victim of

the same lack of privacy. “She didn’t have

Luxembourg’s silenced victims”I feel like the ground was taken from under my feet. Maybe you cannot see it from the outside, but inside I’m a broken person; I’m completely destroyed.” Mrs H.’s bright blue eyes do not betray the secret she painfully carries around with her. She has the typical, carefully-planned career of a successful employee of the financial sector in Luxembourg. At 52, she can speak seven languages and use to her advantage more than twenty years of experience in the banking industry. Self-described as “dynamic and positive”, she keeps herself busy. But she says that since she was a victim of harassment in a slow process that started four years ago, she has lost her will to achieve anything.

Luxembourg texts:

- 25 June 2009 Collective Labour Agreement

http://bit.ly/uj3ag3

- 15 December 2009 Grand-ducal rule.

http://bit.ly/uIoRZw

- 18 November 2003 Initial Projet de loi on

harassment at work.

http://bit.ly/vSVf2P

- 15 November 2005 Opinion by the

Conseil d’Etat

http://bit.ly/ur0wxV

- 10 July 2010 Opinion by the Chamber of

Commerce, the Chambre des Métiers and

Chambre des Salariés http://bit.ly/vFaS7m

- 12 July 2010 Opinion by the Chambre des

fonctionnaires et employés publics

http://bit.ly/rA2IAO European texts:

- 2007 European framework agreement on

harassment and violence at work http://

bit.ly/t47SOW

- 2010 WHO report

http://bit.ly/tPq1D2

Luxembourg points of contact:

- Association for health

at work in the financial sector

http://www.astf.lu

- Mobbing asbl

http://www.mobbing.lu

- Luxembourg mental hygiene league

http://www.llhm.lu

- Health at work division, Ministry of Health

http://bit.ly/uFaL0m

20 novEmbEr - dEcEmbEr 2011

Hr

Karim Sorel, Lawyer at Etude Tastet & Sorel

A Court decision

promotes employees protection

In an October 2010 ruling the Labour

Court sentenced a private company to

pay EUR 7,500 for harassment. In June

2011 the Luxembourg Court of Appeal

agreed with the ruling and underlined

its importance in the absence of a

national law defining harassment. The

Labour Court had stated that it is the

employer’s duty to focus on results

rather than means in order to protect

employees’ health and safety.

More information can be found in

the September 2011 legal newsletter

prepared by the Chambre des Salariés

(in French):

http://bit.ly/vrPZTo

© c

olo

rblin

d.lu

novEmbEr - dEcEmbEr 2011 21

the energy or the strength to fight back.

During her sick leave they accused her of

not having sent a certificate, and she was

fired on the spot.”

Mrs H. finally left the bank in 2009 and found

a lawyer. Today she wants the bank to rec-

ognise the harassment they caused partly

because of their lack of reaction. “Why did

I stay? Had I left my job, it could have taken

months before I found another position. I

wanted it to work. I contacted everyone I

could at the bank to make it work.”

No definition, no problem?

In Luxembourg there exists no law prohibiting

harassment in the private sector. The only

official record of concern from the private

sector was a collective labour agreement

signed between the trade unions and the

employers’ association (UEL) in June 2009.

In December 2009, this convention was de-

clared a general obligation via Grand-ducal

rule. But, although a special commission

investigates harassment cases in the pub-

lic sector since 2008, putting a framework

preventing harassment at work is still a vol-

untary move for Luxembourg-based financial

institutions. Only a handful seem to have

bothered with precautionary measures.

In 2010, a survey led by Astrid Martinez,

a French graduate student in psychology

on behalf of the Association pour la Santé

au travail du Secteur Financier (ASTF),

showed how little Human Resources de-

partments are prepared for the situations

involving harassment at work. Out of the

130 companies that replied to her survey,

28 percent said they had never heard of the

2009 convention. Seventy-eight percent

said they had not put in place a preventive

plan against harassment. Seventy-three

percent said they would be ready to start

to work on their internal rules in order to

prevent these issues, while about a quarter

said they would not. Only two companies

at the time said they had known a case of

psychological violence. From the answers

she gathered, Ms Martinez concluded that

“not many companies seem to be actively

looking for solutions”.

Only four companies asked the ASTF to

organise stress management workshops in

2010: European Fund Administration; the

law firm Wildgen, Partners in Law; Nordea

Bank; and State Street Luxembourg. Others

may have included such a workshop in

general employee health training. Today,

companies seem to prefer to promote their

employees’ well-being through physical

exercise and a healthy diet.

Anyone can be a victim

Ms S. was really happy during the first

month of her internship. But at the end

of August 2008, she found out that her

boss’s idea of an intern was to spend some

worktime in the bedroom. She said that

her refusal sparked a vengeful response

from her manager who quickly started

using all instruments he could to destroy

her work, and ultimately, her. He would

prevent her from eating lunch and tell her

to continue working on “files he had kept

in his drawer for months and suddenly

urgently needed to close”. She said she was

“yelled at” when her colleagues were not

around. “He would criticise the quality of

my work or the way I dressed. I was always

on the lookout for his shouts. I lost 5 kg

in one month. My family and friends did

not recognise me anymore.”

She said she smiled so her colleagues

would not ask questions. “Had they come

forward and asked how I was, I would have

collapsed into tears. Every day I went to

work crying and I came home the same.”

She said she often had to look for work

inside the bank. “Eight-hour days can be

very long when you have nothing at all to

do”, she said. “It was a good strategy he had

found there”. After five months of hostility,

she grabbed an opportunity to write to

the top manager, who agreed to transfer

her to another service within the bank.

There, her new boss gave her some time

to adapt. “She saw I was making mistakes.

I had lost confidence. I did not know how

to properly write an email, how to write

a date on a letter. I was always afraid to

do something wrong and being yelled at.

I had to learn to work again.”

All experts agree that anyone can be-

come a victim. “There is no specific type

of victim, although there are risk factors

like the general context of “fragilisation”

of the financial sector,” said Dr Bollen-

dorf, director of the ASTF and doctor. He

added that harassment is not a modern

phenomenon, contrarily to what could be

believed. “The risk of being a victim may

have risen, but not the abuse itself.” There

are no statistics on harassment cases in

Luxembourg. “It is not considered as a

disease” and therefore no data can be

compiled, explained Dr Bollendorf. The

Mobbing asbl, an association financed

by the Ministry of Labour since 2003, of-

fered 2,134 psychological consultations

between 2005 and 2010.

“We have seen a surge of demands after

mergers,” said Patrice Marchal a sociolo-

gist trained in family therapy, social work

and coaching who has worked with the

ASTF for more than ten years. “These de-

mands can be very diverse with only a

fraction harassment-related.” But some

of these cases can actually start a long

process that lasts for years. “It has a ripple

effect,” he said. During this period which

can be really stressful, people are more

prone to being victims of harassment.

“People can resist to this kind of context

but it’s like a stretched elastic band; it

cannot stretch forever. People can endure

stress until it creates a breaking point and

a loss of balance in their professional,

even personal life.”

Claude Bollendorf said that his patients

usually know about harassment, but do

not understand they are being victims

and often even believe they are respon-

sible for the situation. He said people

above 50 can be more at risk. “The finan-

cial sector has an active population with

workers’ average age being 32-34.” People

above 50 “climbed up the ladder slowly

but surely and are now in a world they

do not necessarily understand. They do

not feel as well-prepared as their younger

colleagues to use technology or to re-

adapt to new procedures. They may feel

alienated.”

22 novEmbEr - dEcEmbEr 2011

Hr

While the financial sector is not as risky

as the education sector, the financial and

economic crises have put pressure on Hu-

man Resources departments, like elsewhere,

to yield results. Whether it takes place in

small companies, where the management

and HR are very close, or big companies,

where the management is directly involved

in the recruitment and training strategy,

harassment can more easily take root when

there are no rules defining how it can be

prevented or addressed.

Christiane Deckenbrunnen, HR manager

Shared Service Centre at BGL BNP Paribas,

said a convention was signed in 2005 be-

tween BGL’s management and the trade

unions, which was extended to BNP Paribas

employees after the merger in 2010. “We did

not put it in place because we had harass-

ment cases, but because we were pioneers”,

she said, agreeing that not many companies

make that choice. “Some cases we thought

were psychological abuse were in fact not;

rather it was the management style not

being adequate.” Still, she acknowledged

that “it’s true it’s difficult to define what ha-

rassment is about”.

Knowing whom to trust

The lack of clarity in what constitutes ha-

rassment makes it hard for victims to know

whom to address and what information

they need to gather to efficiently protect

themselves. Doctor and psychotherapist

appointments are usually the first step to-

ward finding a solution as they can start

mediation processes. But even doctors

reckon their power is often limited in that

respect. “Helping patients is hard because

you always need to find a solution with their

colleagues,” explained Dr Bollendorf. The

ASTF is one of the organisations to which

harassment victims go or are referred, of-

ten by their own doctor or trade unionist.

“The company will, indirectly or directly,

have to intervene in the process”, he said.

He added that it can be even harder to work

with small companies where “colleagues

are so close” and “the abuser can be in a

high position.”

Discriminatory harassment

Labour Code Art. L.241-1 to L.244-3

Sexual harassmentLabour Code Art. L.245-1 to L.245-8

Obsessional harassmentPenal Code Art. 442-2

Psychological harassment2009 Convention / Case LawCharters

Dupont de Nemours

Bram

Ville de Luxembourg

Goodyear

Collective labour agreementsLabour Code Art. L. 162-1 to 162-15

Psychological abuse in the Public SectorSpecial commission

Grand-ducal rule of 1 December 2008

Delegate to equality

Grand-ducal rule of 5 March 2004

Legal documents

Some victims may lose patience with media-

tion processes they deem too long or with

mediators they believe they cannot trust.

Mr M., who hailed from France 11 years ago

and was a victim of harassment at a French

banking institution in Luxembourg, said he

had at first placed all his hopes in the ASTF

after he was fired for gross negligence in

February 2011. But then he said the ASTF

did not send letters to the HR department

of his former employer, nor was there any

meeting as promised. “I felt like I had been

let down by everyone,” he said. “I could not

defend myself.”

Mediators should be trained to listen and

help victims find their own path to recov-

ery, according to Patrice Marchal. “I need to

establish a relationship made of trust with a

clear framework of collaboration,” he said. If

such a collaboration already exists between

the ASTF and the company, he may reach out

to them for help, but he may also choose not

to contact them depending on the victim’s

preferences. “All personnel representatives are

not the same,” he said. “And some information

cannot be shared with the employer.”

According to Ms Martinez’s survey, confi-

dentiality is the harassment victims’ highest

concern. Claude Bollendorf explained that

it may stem from the victim’s fear of be-

ing the cause of the problem. “Harassment

victims show the same symptoms as those

of war veterans: anxiety, guilt, isolation that

can lead to agoraphobia, etc. Isolation is

a classic symptom; the victim wants to

avoid all social contact. It’s directly linked

to guilt. The person goes through doubts:

“did I not myself cause this situation?”, or

“is it my personality which is at stake?”.” He

said these symptoms are close to those of

PTSD, post-traumatric stress disorder. “The

victims of harassment go through the same

episodes over and over again. They fear they

can start the process again if they go back to

their workplace. Some may avoid work, the

building itself, or even the city where they

used to work. They are scared of re-living

the same experience.”

Mrs H. said she has severe trust issues and

can’t see herself going back to work before

some time. “I can’t be in an office by my-

self. I’m scared of being isolated again, of

being humiliated. It’s like when you break

your leg; it can heal but it will always hurt

somewhat. I feel the same way.”

Luxembourg’s minor size: a major issue

The fact that the Grand Duchy’s rather

modest size is a driver for rapid growth has

been often saluted. But it also may provide

for a disastrous environment in the case of

harassment victims looking for a second

chance. As Astrid Martinez wrote in her

novEmbEr - dEcEmbEr 2011 23

Hr

The Minister of Labour promises change

In an interview with Finance

Luxembourg, the Minister of Labour

Nicolas Schmit said he was “favourable

for a legislation defining what

psychological harassment is”. “We

need to fight against harassment and

protect victims,” he said. He announced

he would come forward with a law

proposal in 2012 and that the text

of 2003 which was rejected by the

governmental commission at the time

would be amended with information

gathered from neighbouring countries

legislation. He said “it was not normal”

that the public sector has a legislation

prohibiting harassment at work while

the private sector does not. “This

inequality should be solved”, he said.

But he said employers are against such

a law and trade unions are “divided”

over the issue. About the 25 December

2009 collective labour agreement not

being known by the majority of HR

departments, he said that trade unions

should have made more publicity. He

also said it “would probably be useful”

to get representatives from the HR

departments involved when the law

proposal is discussed next year.

survey, “What seems to compel employees

to silently suffer from these situations is

the financial sector’s specificities: a small

geographical location and a small number

of companies employing the same profiles.

In other words, everybody knows every-

body and everything ends up being known:

complaining means reducing one’s chance

of finding another job.”

Karim Sorel, a lawyer specialised in ha-

rassment cases who was instrumental in

helping the Minister of Labour approve the

2009 convention, said there is still a lot of

work left for the law to favour employees

rather than employers in Luxembourg.

“My personal opinion is that there is a

special economic and political context

in Luxembourg where the investors must

be protected and the workplace environ-

ment made attractive for them”, he said.

“Employers here enjoy a working environ-

ment where everyone knows everyone

and everything is known. In the rare cases

where harassment cases were brought to

court in Luxembourg, people have been

fined between EUR 500 and 5,000, which

is ridiculous. Magistrates are kind towards

harassment and only deliver small fines.”

According to Monique Breisch from the

Mobbing asbl, harassment issues “should be

taken much more seriously by politicians

and trade unionists. There are still suicide

attempts due to harassment at work.”

The court battle: not for everyone

Patrice Marchal said that during his work-

ing hours at the ASTF he has met different

people with very different needs. While

some of them may consider going to

court, others prefer a quiet way of solv-

ing issues. “I’m asking people to reflect

on the complaint process; it means giv-

ing their problem a public sphere, with

professionals opening an investigation,

finding witnesses, etc. It requires people

outside the situation to become in-

volved. It can create conflicts and worsen

the problem.”

But companies may sometimes use this cli-

mate of fear to their advantage. When Ms

S. left the bank for another job two weeks

before the end of her temporary contract,

she had to break her contract. That’s when

the HR department stepped in with a peculiar

condition - an agreement she would sign

never attack the bank on any ground. “If I

had not needed to leave two weeks before

the end of my temporary contract, I would

never have signed this clause”, she said.

Mr M. said that he lawyered up but it will

be hard to come forward with evidence in

court. “They will refute everything I say. It

will be hard for me to counter this gross

negligence I’m being accused of. It’s not

easy to fight a 500-people monster. It’s

kind of scary.” He said he cannot access

his emails anymore or ask his former col-

leagues to gather evidence on his behalf.

“Without proof you cannot do anything,” said

Karim Sorel. “Contrarily to what is being done

in France, in the Grand Duchy, there is no law

to lighten up the burden of proof. It needs

to be brought forward by the employee.” He

said that while the magistrates’ hesitancy to

fine employers has no dissuasive effect, a

specific law “defining harassment, facilitating

its recognition, easing the burden of proof

and making harassment a crime” would be

the solution.

Dr Carlo Steffes, Head of the Health at Work

division at the Ministry of Health, has been

closely following the legal debate around

harassment and is himself treating victims of

abuse. He said the Ministry of Labour should

come forward with a new proposal. “A law

carries a lot of weight,” he said. “Having a law

would be an advantage especially since the

jurisprudence is not really favourable.”

“The problem is that harassment needs to be

recognised as it is,” said Karim Sorel. “There

is no reason for harassment not to take place

in Luxembourg; problems like these do not

stop at countries’ borders. In the general

context of the financial crisis, a law would

find its essence in these moments when

profitability becomes the main gone. That’s

when harassment takes roots.”

For Mrs H., going to court means getting an

opportunity to make an example of her case

for other victims. While she said she is not

interested in starting a personal vendetta

against her former employer, she wants to

get her dignity back. And she relies on the

court to do just that.

By Delphine Reuter

24 novEmbEr - dEcEmbEr 2011

Hr

Entrepreneurs before anything else

Entrepreneurship. That’s the keyword Henri Wagner, the managing partner of Allen & Overy Luxembourg will put at the top of his list when he’ll draft the two-year strategy for the law firm. “World forces have become incredibly complex and we have to adapt to ongoing structural changes,” said Mr. Wagner. Opening international desks. Setting up a hotline for key clients, a top priority for clients who come first and foremost. Assisting regulators. Investing time and expertise in promising markets. Through the firm’s “global reach and local depth” approach, it has the ambition to “set the pace for other firms and be ahead of the game”.

There might be enough business gener-

ated by a global law firm like Allen & Overy

without its Luxembourg office needing in-

ternational desks in Russia, Latin America

and Asia-Pacific. But that would contradict

the spirit of entrepreneurship Henri Wagner

has been instigating in the firm since the

crises hit.

Over the past two months, Allen & Overy

Luxembourg’s busy Asia-Pacific desk in

Hong Kong, officially launched in Octo-

ber 2011, has already participated in five

important events, including two with a

delegation of ALFI and one with Luxem-

bourgforFinance. The managing partner

reckons these desks are “the most visible

element of our strategy, in terms of setting

milestones.” “People will ask us why we

need such desks, given that Allen & Overy

now has 39 offices in 27 different jurisdic-

tions. But through the international desks

we can focus on Luxembourg; it’s a perfect

representation of our country and of the

Luxembourg office of Allen & Overy.” While

jurisdictions may not consider Luxembourg

as a priority, it’s the desk’s job to make sure

it happens. “It’s a lot of investment. But if

we don’t do this, it does not echo with our

ambition to innovate,” he explained.

Since the Lehman Brothers collapse, pro-

activeness is promoted at every level of

the global firm, translated into the opening

of new offices in Australia, in Washington

D.C., in Asia and North Africa. Aligned in

this vision, Mr Wagner is planning to open

a new desk in a strategically important high

growth market in 2012. “Our brand allows us

to penetrate these fantastic markets while

continuing to stand out in developed mar-

kets,” he said. “If you stay in Luxembourg

and have a passive attitude, you stagnate.

In our profession, you’re as good as dead

if you are not proactive.”

Beyond the normal advisor: an advisor that is trusted

The firm has adopted more of a corporate

mindset and being an entrepreneur is part

of this approach. It’s also about being a

go-getter, Henri Wagner explained. “The

years when clients came in automatically

are over. Today, we go to visit our clients in

London and elsewhere. We send them all

the information we think will be relevant to

their business. We want to achieve a level of

boardroom advisor where we can closely

help the decision-makers. In the past, we

dedicated our resources to pure legal work.

These days, you have to do more for clients

who are subject to pressure themselves.

This spirit and the new focus on service

levels can make a difference.”

In Luxembourg, Allen & Overy reaches out

to a broader base of clients - meaning any

financial institution that can benefit from

their insight. For the first time, the law firm

approached key European regulators, so as

to explain how banks and the investment

funds industry would be affected by the

U.S.'s Dodd-Frank Act. They are also assisting

a number of Ministries, drawing from their

experience in other countries. "We're sitting

on a number of internal expert groups. We

know what has been done in France by

the Autorité des Marchés Financiers or in

Germany by the BaFin. We can draw on our

resources in this respect." Responding to

current concerns, the firm has just created

a cross-border "Eurozone crisis working

group" dealing with currency union issues.

novEmbEr - dEcEmbEr 2011 25

Strategy

The firm continues to focus on key industry

sectors and financial markets they think are

important, while developing expertise in

promising markets with growth potential

like bio science, new technologies, alterna-

tive investment funds and private equity.

“People generally say that the European

markets are mature and the potential for

growth here is smaller than in BRICS coun-

tries. But this does not prevent us from

investing heavily in the investment funds

segment and other strategically relevant

industries. We go on economic missions

overseas, we participate to industry profes-

sional committees, etc.” He said recruitment

has also needed to adapt. “To become a

partner at the firm, the box of having an

entrepreneur’s mind needs to be ticked. Of

course, a good lawyer can always make a

career here. It’s not a black and white world,

we need experts. But to have clients come

to us, having initiatives is central. Entrepre-

neurship is key and is at the centre of our

profession. It will go beyond me and other

people working today at the firm.”

By Delphine Reuter

Henri Wagner, Managing Partner at Allen & Overy Luxembourg

© c

olo

rblin

d.lu

26 novEmbEr - dEcEmbEr 2011

Strategy

Henri Wagner, Managing Partner at Allen & Overy Luxembourg

Good vibrationsThis year’s ALFI conference certainly highlighted the role alternative investments solutions can play in attracting new customers and opening new markets for Luxembourg. One of the long-time believers in Luxembourg’s potential in this business is Joseph Antonellis, vice chairman and head of Europe and Asia-Pacific Global Services at State Street. Together with Martin Dobbins, senior vice president and managing director of State Street Luxembourg, they explain how one of the world’s leading providers of financial services to institutional investors will surf on the wave of regulations to create value in servicing.

What are your projects for Luxembourg?

Joseph Antonellis: Our objective is to

double our non-US revenues over the

next five years. Globally, our focus is on

offshore markets, alternative investment

services and middle office outsourcing.

We’re the largest provider of fund ac-

counting and administration for mutual

funds in the US, plus SICAV and UCITS

in Luxembourg, and in-country types of

funds into Europe and Asia and we do

both local and global servicing through

the Luxembourg UCITS brand. Within

Europe, Luxembourg is the crown jewel

for derivatives.

The UCITS brand helps us stay close to

the industry, especially from a regula-

tory perspective. State Street has built a

solid reputation in the Luxembourg mar-

ket, proven by the excellent scores and

feedback that we have received for the

services we provide here.

The feedback received from the Asian

region is that clients want to understand

how regulation governs the use of de-

rivatives and with emphasis on investor

protection. Complex products can be

challenging for clients, however, it’s es-

sential that we help to explain how it fits

within the UCITS framework.

How do you eye upcoming regulations?

First and foremost, we work closely with

regulators to ensure the rules are clear

for our clients. There’s a need to educate

regulators in Luxembourg and elsewhere,

and particularly in Asia, where investors

want to have a better grasp of these regu-

latory changes and how they impact the

funds. We have seen this in UCITS III and

it’s even more noticeable with UCITS IV.

What we find ultimately is that sharing

information with regulators helps them

to better understand industry issues.

New regulations can bring additional

costs, and unfortunately, these costs are

often paid by the end-investor. That said,

some new regulations do help to mitigate

risk and are clearly worth the additional

cost. In the case of AIFMD, it is primar-