Embed Size (px)

Citation preview

Finance & Cash Flow Management

Presented by: Sahar El Damati

OUTLINES

I- Banks follow a scientific approach to assess &

evaluate any project in order to identify risks &

structure credit facilities.

II- Cash Flow is a Very important parameter in the

assessment of the viability, strength of a project

& more important tools for:-

a. The determination of the cash needs.

b. Debt service capabilities.

III- Prior to presenting the applicability of the

financials in the credit analysis, it is important to

present a brief overview of all the important

variables in the credit analysis.

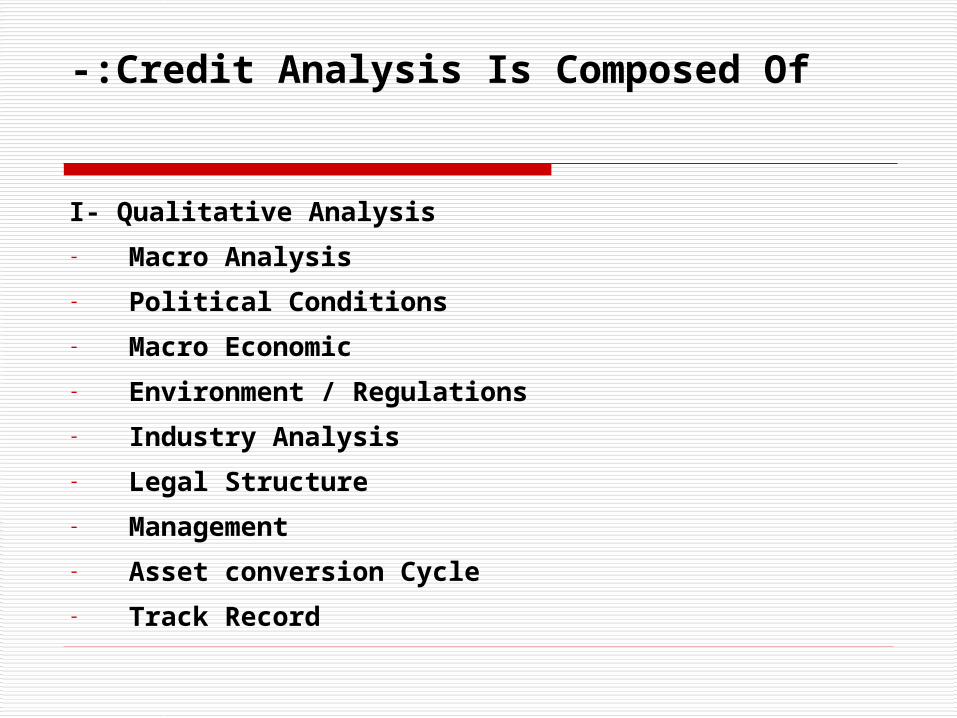

Credit Analysis Is Composed Of-:

I- Qualitative Analysis

- Macro Analysis

- Political Conditions

- Macro Economic

- Environment / Regulations

- Industry Analysis

- Legal Structure

- Management

- Asset conversion Cycle

- Track Record

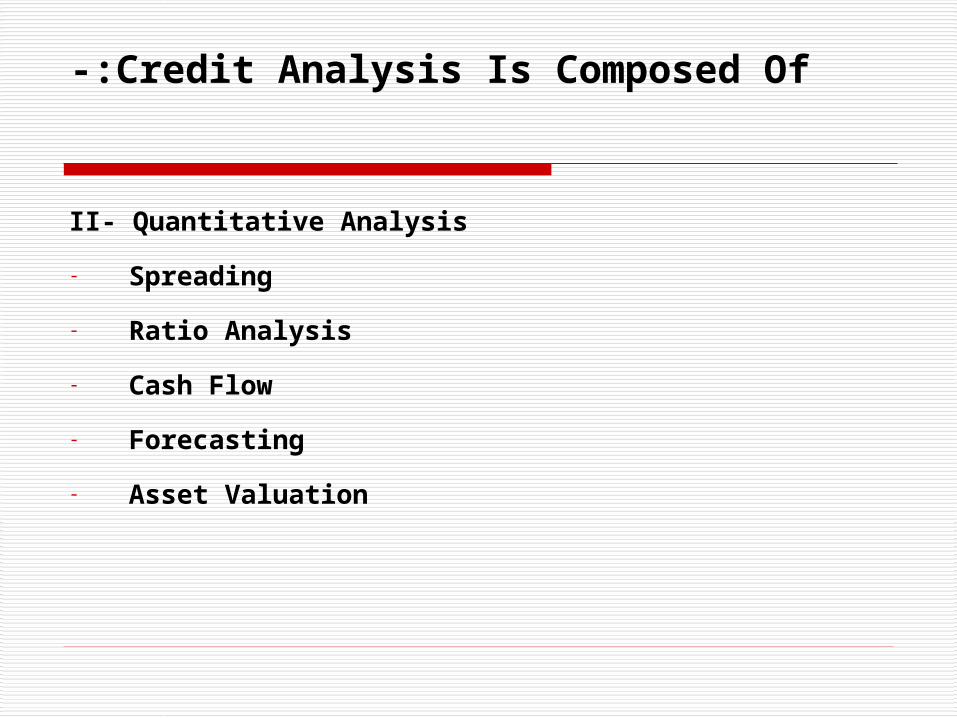

Credit Analysis Is Composed Of-:

II- Quantitative Analysis

- Spreading

- Ratio Analysis

- Cash Flow

- Forecasting

- Asset Valuation

Credit Analysis Is Composed Of-:

III- Risk & Mitigants

- Business & Financial Risks

- SWOT analysis

- Mitigants

IV- Credit Structuring

- Credit facilities parameters

- Risks associated with credit structure

- Structure pertaining to each industry

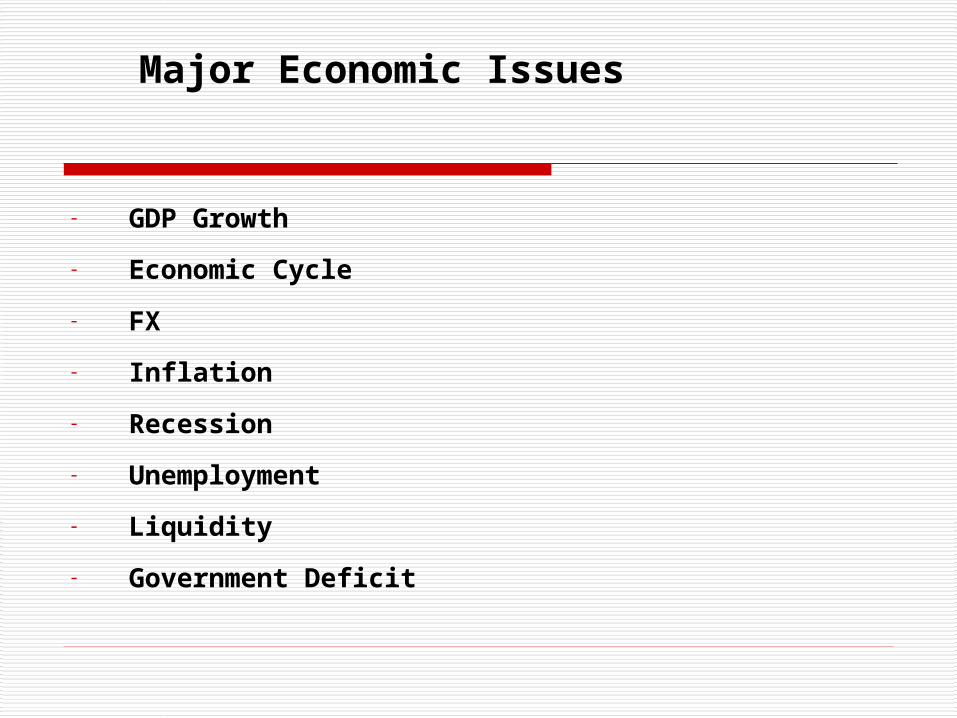

Major Economic Issues

- GDP Growth

- Economic Cycle

- FX

- Inflation

- Recession

- Unemployment

- Liquidity

- Government Deficit

Regulation

- General / specific

- Helpful / Constricting

- Existing / potential

- Effects of regulations on performance / cost

Regulation Environment

- High Risk • Hostile government regulations

• Highly regulated environment

- Moderate Risk • Mild government intervention

• Relatively regulated environment

- Low Risk • Friendly or protective regulations

• Minimum or no government intervention

Industry Risk Analysis

MarketCompany

Communications

Goods & Services

Money (Sales)

Information

Figure (1) A Simple Marketing System

Finance Production Marketing Personnel Etc.

Information

Environment Environment

Environment

Information

Management

Strategic Process

Strategy

A Representation of a business system

InputOutput

- Demand

• Limited demand

• High demand

- Competition

• Monopoly

• Oligopoly

• Moderately competitive

• Highly competitive

- Market share

• Equal or above 40%

• From 25 to 40%

• Less than 10%

• Market share formulae

Introduction Growth Maturity Decline

Sales Volume

Inventory

Recovery

Profits

Time

Steps in industry analysis

- Define borrower’s industry

- Identify risks inherent in the industry

- Assess effects of risk on borrower

- Performance

Industry Characteristics

- Cost structure

- Industry maturity

- Industry cyclicality

- Dependence on other industries

- Vulnerability to substitutes

- Regulatory environment

Legal Structure

- Law under which the company is established.

- Importance of identifying shareholders.

• Financial support.

• Know how support.

• Marketing support.

• Management support.

- Capital

• Authorized capital

• Issued capital

• Paid in

Ownership

- Identify owners & understand commitment• Structure or type of business organization• Major shareholders and concentrations • Privately held or traded on a stock exchange • Range of share price, if traded• Major changes in legal structure over the

years and why - Identify sister companies

• Who are they• What is the ownership structureWhat is the ownership structure• What is line of businessWhat is line of business

Line Of Business

- Manufacturer / Trader • What are the products / services soldWhat are the products / services sold• Breakdown of products soldBreakdown of products sold• Location of the businessLocation of the business• Capacity of productionCapacity of production• Emphasis on original capacityEmphasis on original capacity• Any increase which took place over the yearAny increase which took place over the year• Strategy for expansion & whenStrategy for expansion & when

- Contractor Contractor • How long in business How long in business • Line of business per contractor Line of business per contractor • Maximum amount of acceptable projects Maximum amount of acceptable projects • Track record Track record

Management

- Goals and commitmentGoals and commitment

- Organizational characteristics Organizational characteristics

- Delegated authoritiesDelegated authorities

- Market reputation Market reputation

- Management systems / access to technologyManagement systems / access to technology

- Good qualified auditorsGood qualified auditors

- ISO, quality controlISO, quality control

Asset Conversion Cycle Operating Cycle

- What is it?What is it?

- Components of ACCComponents of ACC

- Working investment conceptWorking investment concept

- Seasonal WISeasonal WI

- Permanent WIPermanent WI

- Growth WIGrowth WI

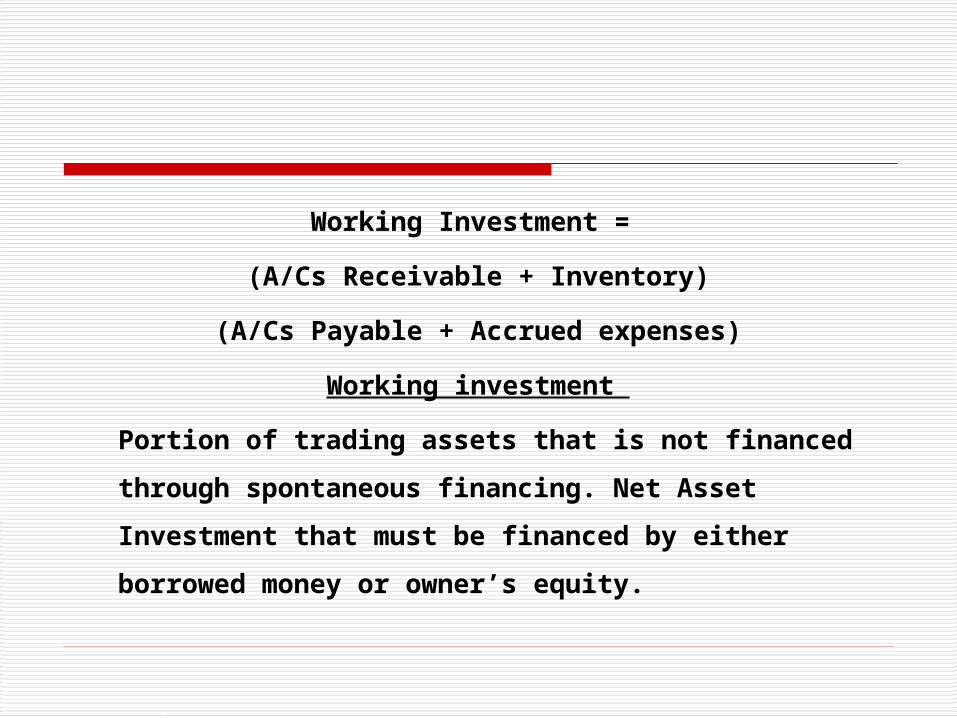

Working Investment =

(A/Cs Receivable + Inventory)

(A/Cs Payable + Accrued expenses)

Working investment

Portion of trading assets that is not financed

through spontaneous financing. Net Asset

Investment that must be financed by either

borrowed money or owner’s equity.

Asset Conversion Cycle

Identification / Risk

Cash

Receivables

Finished Goods (FG)

Work in Progress (WIP)

Raw Materials (RM)

Business Risk

The uncertainty that management will be able to The uncertainty that management will be able to

recover the costs invested in the asset conversion recover the costs invested in the asset conversion

cycle.cycle.

Credit Analysis FSA & Cash Flow

Objectives:- Objectives:-

1- Assess the performance of a company1- Assess the performance of a company

2-Evaluate the asset management2-Evaluate the asset management

3- Evaluate the capital structure & liquidity 3- Evaluate the capital structure & liquidity

4- Determine the financial risks4- Determine the financial risks

5- Determine the financial needs.5- Determine the financial needs.

6- Determine company’s ability to meet current and 6- Determine company’s ability to meet current and

future debt service and expansion needs.future debt service and expansion needs.

7- Approximate cash inflows & outflows 7- Approximate cash inflows & outflows

8- Identify sources and uses of cash 8- Identify sources and uses of cash

Credit Analysis FSA & Cash Flow

- Positive cash flow depends onPositive cash flow depends on

• Ability to complete ACCAbility to complete ACC

• Manage asset investmentManage asset investment

• Manage risks properlyManage risks properly

• Manage capital structureManage capital structure

Forecasting

- Critical tool for lending Critical tool for lending

- Repayment depends on future performance, Repayment depends on future performance,

especially with term loans especially with term loans

- Need to determine how much to lend, for how Need to determine how much to lend, for how

long and under what conditions long and under what conditions

- Best to use various scenariosBest to use various scenarios

Objectives of Forecasting

- Determine need & capacity to repayDetermine need & capacity to repay

- Spot opportunities Spot opportunities

- Structure facilities Structure facilities

- Set covenants Set covenants

- Establish basis for valuationEstablish basis for valuation

Purpose of LTL

- Acquisitions Acquisitions

- New plant (CAPEX) New plant (CAPEX)

- Refinance existing debtRefinance existing debt

- Finance growthFinance growth

Analytical Emphasis

- Quality is criticalQuality is critical

• Consistency Consistency

• Stability predictability Stability predictability

• Mitigation of risksMitigation of risks

• Reaction to recessionReaction to recession

• Ease of analysis Ease of analysis

Forecasting

- Should be:- Should be:-

• LogicalLogical

• Reasonable Reasonable

• Defensible Defensible

• Historical consistentHistorical consistent

• Related to management’s strategies Related to management’s strategies

• Reflective of industry & economic Reflective of industry & economic

projections projections

• sensitizedsensitized

Final Assessment

- Purpose Purpose

- Source of repaymentSource of repayment

- Risks Risks

- Protection against lossProtection against loss

- Form of controlForm of control

Purpose

- Finance short term trading assets WI (WC)Finance short term trading assets WI (WC)

- Finance long term assets Finance long term assets

• PermanentPermanent

• Capital expenditures Capital expenditures

• Investment activities Investment activities

Risks

- Inability to generate cash Inability to generate cash

• Business risks Business risks

• Financial risksFinancial risks

- Inability of managementInability of management

• To manage sources & uses of cashTo manage sources & uses of cash

Protection

- Stability of profits Stability of profits

- Strong financial status of the companyStrong financial status of the company

- Covenants to preserve cash flow & financial Covenants to preserve cash flow & financial

position of the company.position of the company.