Embed Size (px)

DESCRIPTION

The Niche Report - February 2009

Citation preview

FHA Streamlined Refi's

Issue 020

February 2009

TheNicheReport.com

16Put your client into a better loan.

22 Pitch Niche to the Rich!

26What you know, who you know.

13They are waiting for your call.

Orphaned Clients and Customers

The Crux and Craze of Loan ModificationLoan modifications are here to stay.

Complete Real Estate Advisory & Financing

Find out more on page 7

advisory services

With the recent credit crunch crises, conventional funding has become more difficult for borrowers to obtain financing. The real estate industry has always been dependent on the ability of lenders to source loans.

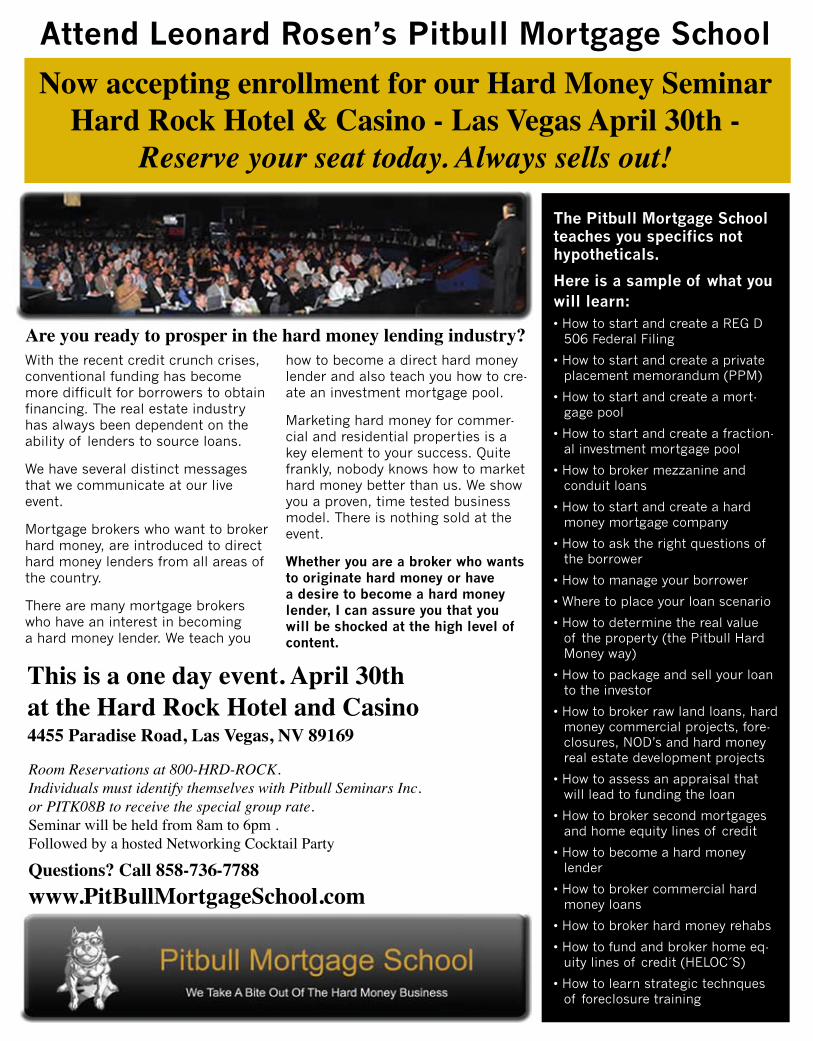

We have several distinct messages that we communicate at our live event.

Mortgage brokers who want to broker hard money, are introduced to direct hard money lenders from all areas of the country.

There are many mortgage brokers who have an interest in becoming a hard money lender. We teach you

how to become a direct hard money lender and also teach you how to cre-ate an investment mortgage pool.

Marketing hard money for commer-cial and residential properties is a key element to your success. Quite frankly, nobody knows how to market hard money better than us. We show you a proven, time tested business model. There is nothing sold at the event.

Whether you are a broker who wants to originate hard money or have a desire to become a hard money lender, I can assure you that you will be shocked at the high level of content.

The Pitbull Mortgage School teaches you specifics not hypotheticals.

Here is a sample of what you will learn:• How to start and create a REG D

506 Federal Filing

• How to start and create a private placement memorandum (PPM)

• How to start and create a mort-gage pool

• How to start and create a fraction-al investment mortgage pool

• How to broker mezzanine and conduit loans

• How to start and create a hard money mortgage company

• How to ask the right questions of the borrower

• How to manage your borrower

• Where to place your loan scenario

• How to determine the real value of the property (the Pitbull Hard Money way)

• How to package and sell your loan to the investor

• How to broker raw land loans, hard money commercial projects, fore-closures, NOD’s and hard money real estate development projects

• How to assess an appraisal that will lead to funding the loan

• How to broker second mortgages and home equity lines of credit

• How to become a hard money lender

• How to broker commercial hard money loans

• How to broker hard money rehabs

• How to fund and broker home eq-uity lines of credit (HELOC´S)

• How to learn strategic technques of foreclosure training

Attend Leonard Rosen’s Pitbull Mortgage School

Now accepting enrollment for our Hard Money SeminarHard Rock Hotel & Casino - Las Vegas April 30th -

Reserve your seat today. Always sells out!

This is a one day event. April 30th at the Hard Rock Hotel and Casino 4455 Paradise Road, Las Vegas, NV 89169

Room Reservations at 800-HRD-ROCK. Individuals must identify themselves with Pitbull Seminars Inc. or PITK08B to receive the special group rate.Seminar will be held from 8am to 6pm . Followed by a hosted Networking Cocktail Party

Questions? Call 858-736-7788www.PitBullMortgageSchool.com

Are you ready to prosper in the hard money lending industry?

Remington Financial Group offers an extensive network of privateand public lending partners, dramatically improving close rates for borrowers. With a successful track record of closing hard money and conventional transactions, Remington delivers expertise and competitive options, evenin these challenging market conditions.

Call us today to find out how Remington Financial Groupcan help make your next transaction a success.

Does commercialfinancing still exist?Does commercialfinancing still exist?

Remington Financial Group offers an extensive network of privateand public lending partners, dramatically improving close rates for borrowers. With a successful track record of closing hard money and conventional transactions, Remington delivers expertise and competitive options, evenin these challenging market conditions.

Call us today to find out how Remington Financial Groupcan help make your next transaction a success.

Does commercialfinancing still exist?Does commercialfinancing still exist?

6 February 2009

agency & FHa pg 35

JUMBO pg 36

PORTFOLIO & aLT–a pg 37

ReVeRSe pg 38

ManUFacTURed pg 38

nOn-PRIMe & HaRd MOney pg 39

cOnSTRUcTIOn/ReHaB pg 42

cOMMeRcIaL pg 43

nIcHe RePORTScOnTenTS Issue 020 February 2009

FOUndeR & PReSIdenT Robert Pegg [email protected]

cO-FOUndeR & PReSIdenT David Pegg [email protected]

edITORIaL / cOnTenT ManageR Kristen Moser [email protected]

cOPy edITOR Stewart Mednick [email protected]

accOUnTIng ManageR Shawna Ingram [email protected]

SaLeS ManageR Mark Moulton [email protected]

PROdUcTIOn ManageR Henry Suchman [email protected]

PROdUcTIOn aSSISTanT Dawn Exner [email protected]

adVISORy BOaRd Aaron Krowne President and CEO, IEHI, Inc.

cOLUMnISTS Stewart Mednick

cOnTRIBUTIng aUTHORS George H. Marentis Tom Ninness Leslie Petersen Andy Warshaw Jack Williams

Orphaned Clients and CustomersTOM nInneSSVice President cherry creek Mortgage

They are waiting for your call.

13

Pitch Niche to the Rich!Jack WILLIaMSwww.gotrates.net

What you know, who you know.

26

Center Stage with Compliance Made SimpleTHe nIcHe RePORT

Compliance - what you don't know will hurt you.

29

The Crux and the Craze of Loan Modificationandy WaRSHaW, J.d

Loan modifications are here to stay.

22

dePaRTMenTS

16 FHA Streamlined Refi'sLeSLIe PeTeRSen

Put your client into a better loan

09 nOTe FROM THe FOUndeR

10 caLendaR OF eVenTS

45 LendeR & ReSOURce dIRecTORy

Tip of the MonthSTeWaRT MednIck

The Golden Rules Part II

32

Start saving today!

Call 1-800-342-8500 or visit kennedyfunding.com

The tremendous resources of Kennedy Funding offer the power and expertise to negotiate directly with your lender…and the funds to help you buy down your existing mortgage—fast. The bottom line: Kennedy Advisory Services may be able to save you 20 to 40% or more off the top.

Complete Real Estate Advisory & Financing

advisory services

WE’LL NEGOTIATEWITH YOUR BANK. YOU COULD CUT MILLIONS

OFF YOUR COMMERCIAL MORTGAGE.

The

Kenn

edy

Fund

ing

seal

is a

regi

ster

ed tr

adem

ark

of K

enne

dy F

undi

ng, I

nc.

Visit us at Booth #202 at MBA CREF – February 8-10, San Diego, California

SUBScRIPTIOnS

This publication is intended for real estate finance professionals. If you are a mortgage broker, lender, loan officer and you do not currently receive The Niche Report, please send your name, company name, and address to [email protected].

Send address change requests to [email protected]. Remember to include the old address.

To opt-out of receiving The Niche Report, please send your request, including name, company name, and address to [email protected].

adVeRTISeMenTS

To inquire about advertising in The Niche Report, please call 866.964.2695, or send an email to [email protected]. Visit our website, www.TheNicheReport.com to download a copy of our Media Kit.

edITORIaLS / aRTIcLeS

To submit an article for consideration in The Niche Report, please send an email to [email protected] or call 866.964.2695. We are interested in original writings relevant to mortgage brokers and other real estate finance professionals.

If you have a comment or question about an article or editorial published in The Niche Report, or if you have a suggestion for a topic you would like to see featured in a future issue, please send an email to [email protected].

THe nIcHe RePORT POLIcy

The information and opinions expressed by contributing authors and advertisers within The Niche Report do not necessarily reflect those of BODA Publishing, LLC employees and should not be considered as endorsed or recommended by BODA Publishing, LLC.

Published monthly by BODA Publishing, LLC PO Box 2618, Stafford, VA 22555 Phone: 866.964.2695 Fax: 703.991.2362 Email: [email protected] www.TheNicheReport.com

$3.55M Industrial SiteLeominster, MA

Broker Commission: $50,000

$1.975M Residential SubdivisionAsheville, North Carolina

Broker Commission: $19,750

$2.35M Storage CenterCoeur d’Alene, Idaho

Broker Commission: $35,250

$3.875M Luxury SubdivisionCarmel, Indiana

Broker Commission: $77,500

$975,000 Historic Office BuildingAndersen, Indiana

Broker Commission: $40,000

$3.8M Health Spa DevelopmentStaten Island, New York

Broker Commission: $38,000

$1.2M Land LoanApple Valley, Utah

Broker Commission: $36,000

$1.95M Hospitality LoanCleveland, Mississippi

Broker Commission: $78,000

$7.2M Condo ConversionKissimmee, Florida

Broker Commission: $108,000

There is a solution.

HArd MoNeY LoANS wItH MeTRo FunDIng.

Metro Funding Corporationone Kalisa Way, Suite 310, Paramus, nJ 07652

For more information, call toll free: (866) 302-6360 or visit our website:

www.metrofundingcorp.com

nOTe FROM THe FOUndeR

9TheNicheReport.com

This issue of TNR is packed full of great content – including our feature article on FHA Streamlined Refinances by Leslie Petersen, the industry guru on FHA/VA and conventional guidelines. A loan originator cannot survive without having FHA or VA in their portfolio of product offerings. This article gives great insight to one of the best programs on the market.

It has been reported that correspondent lending is rapidly growing while wholesale mortgage brokering is rapidly decreasing. This seems quite obvious with Chase recently shutting down their wholesale operations. I believe the small broker is get-ting squeezed out. To remain competitive in this market these same small brokers are joining correspondent lenders as net branches. By doing this, they are now

able to compete with retail lenders but must now also carry a substantial about of risk on their shoulders, sometimes referred to as “skin in the game”. I won’t go in to all the associated risk because it differs from company to company but I will say this is not a bad thing; in fact, it will help to cleanse our industry of the “bad apples”. I am not saying the small broker is dead, only that there is a popular transformation occur-ring that preserves our competitiveness. Along with this transformation, be ready for much more change in terms of compliance and regulation. This is going to be a bumpy ride, but know that your services are needed and be ready to adapt. Build upon relationships and put the customer first.

If you are interested in learning about net branch/correspondent opportunities, please visit our online fo-rum at TheNicheReport.com. The thread is titled - Net Branching & Correspondent Lending. There are a number of reputable companies already listed for you to begin your research. If you happen to already belong to a net branch/correspondent lender please feel free to post about your experience and offer helpful tips for those searching for a home.

Keep up the fight,

Robert Pegg

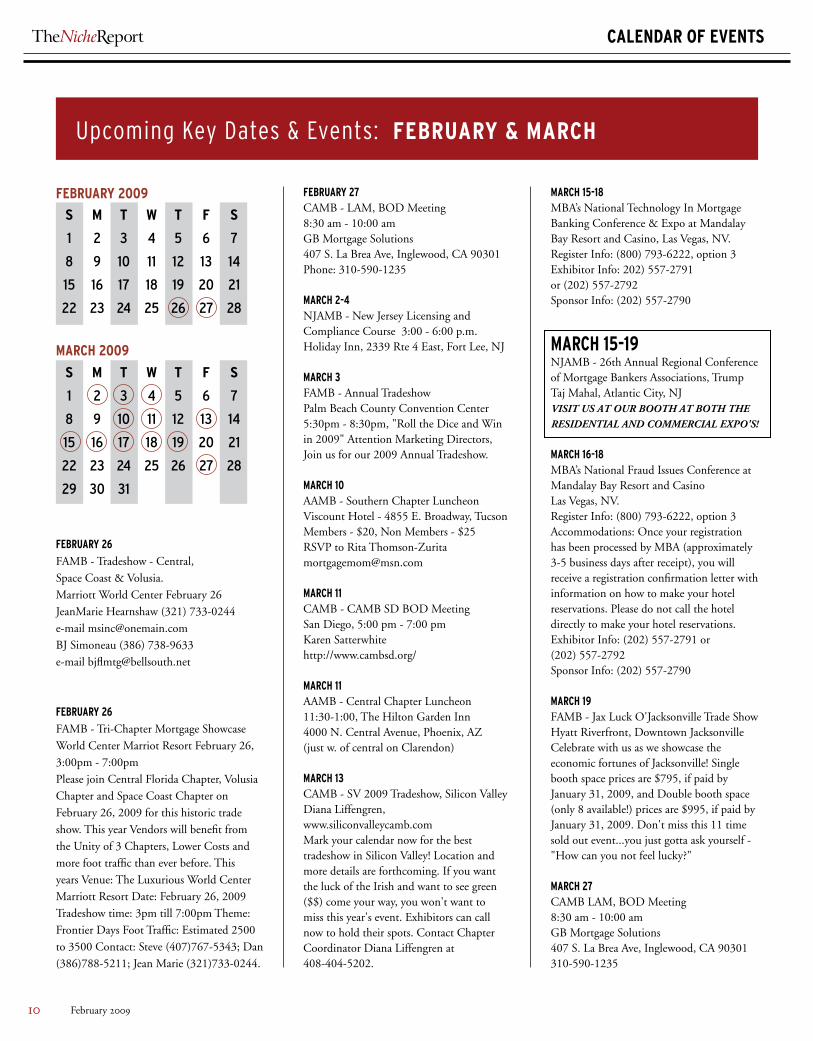

FeBRUaRy 26

FAMB - Tradeshow - Central,

Space Coast & Volusia.

Marriott World Center February 26

JeanMarie Hearnshaw (321) 733-0244

e-mail [email protected]

BJ Simoneau (386) 738-9633

e-mail [email protected]

FeBRUaRy 26

FAMB - Tri-Chapter Mortgage Showcase

World Center Marriot Resort February 26,

3:00pm - 7:00pmPlease join Central Florida Chapter, Volusia Chapter and Space Coast Chapter on

February 26, 2009 for this historic trade

show. This year Vendors will benefit from the Unity of 3 Chapters, Lower Costs and more foot traffic than ever before. This

years Venue: The Luxurious World Center Marriott Resort Date: February 26, 2009

Tradeshow time: 3pm till 7:00pm Theme: Frontier Days Foot Traffic: Estimated 2500 to 3500 Contact: Steve (407)767-5343; Dan

(386)788-5211; Jean Marie (321)733-0244.

FeBRUaRy 27CAMB - LAM, BOD Meeting8:30 am - 10:00 am GB Mortgage Solutions 407 S. La Brea Ave, Inglewood, CA 90301Phone: 310-590-1235

MaRcH 2-4NJAMB - New Jersey Licensing and Compliance Course 3:00 - 6:00 p.m.Holiday Inn, 2339 Rte 4 East, Fort Lee, NJ

MaRcH 3FAMB - Annual TradeshowPalm Beach County Convention Center 5:30pm - 8:30pm, "Roll the Dice and Win in 2009" Attention Marketing Directors, Join us for our 2009 Annual Tradeshow.

MaRcH 10 AAMB - Southern Chapter Luncheon Viscount Hotel - 4855 E. Broadway, TucsonMembers - $20, Non Members - $25RSVP to Rita Thomson-Zurita [email protected]

MaRcH 11CAMB - CAMB SD BOD MeetingSan Diego, 5:00 pm - 7:00 pm Karen Satterwhite http://www.cambsd.org/

MaRcH 11AAMB - Central Chapter Luncheon11:30-1:00, The Hilton Garden Inn4000 N. Central Avenue, Phoenix, AZ(just w. of central on Clarendon)

MaRcH 13 CAMB - SV 2009 Tradeshow, Silicon Valley Diana Liffengren, www.siliconvalleycamb.com Mark your calendar now for the best tradeshow in Silicon Valley! Location and more details are forthcoming. If you want the luck of the Irish and want to see green ($$) come your way, you won't want to miss this year's event. Exhibitors can call now to hold their spots. Contact Chapter Coordinator Diana Liffengren at 408-404-5202.

MaRcH 15-18MBA’s National Technology In Mortgage Banking Conference & Expo at Mandalay Bay Resort and Casino, Las Vegas, NV.Register Info: (800) 793-6222, option 3Exhibitor Info: 202) 557-2791 or (202) 557-2792 Sponsor Info: (202) 557-2790

MaRcH 15-19 NJAMB - 26th Annual Regional Conference of Mortgage Bankers Associations, Trump Taj Mahal, Atlantic City, NJVisit us at our booth at both the

residential and CommerCial expo's!

MaRcH 16-18 MBA’s National Fraud Issues Conference at Mandalay Bay Resort and CasinoLas Vegas, NV.Register Info: (800) 793-6222, option 3 Accommodations: Once your registration has been processed by MBA (approximately 3-5 business days after receipt), you will receive a registration confirmation letter with information on how to make your hotel reservations. Please do not call the hotel directly to make your hotel reservations.Exhibitor Info: (202) 557-2791 or (202) 557-2792 Sponsor Info: (202) 557-2790

MaRcH 19 FAMB - Jax Luck O'Jacksonville Trade ShowHyatt Riverfront, Downtown Jacksonville Celebrate with us as we showcase the economic fortunes of Jacksonville! Single booth space prices are $795, if paid by January 31, 2009, and Double booth space (only 8 available!) prices are $995, if paid by January 31, 2009. Don't miss this 11 time sold out event...you just gotta ask yourself - "How can you not feel lucky?"

MaRcH 27 CAMB LAM, BOD Meeting8:30 am - 10:00 amGB Mortgage Solutions407 S. La Brea Ave, Inglewood, CA 90301310-590-1235

caLendaR OF eVenTS

10 February 2009

Upcoming key dates & events: FeBRUaRy & MaRcH

FeBRUaRy 2009

S M T W T F S

1 2 3 4 5 6 7

8 9 10 11 12 13 14

15 16 17 18 19 20 21

22 23 24 25 26 27 28

MaRcH 2009

S M T W T F S

1 2 3 4 5 6 7

8 9 10 11 12 13 14

15 16 17 18 19 20 21

22 23 24 25 26 27 28

29 30 31

NicheReportFP.indd 1 1/7/09 3:23:37 PM

Hard Money Loans from $100,000 to $1,500,000

• Minimum Credit 400• No seasoning• No up front fees• 48 hour closing

Lending Territory includes DE, MD, DC, VA, NC, SC, GA and FL.

ALL LoANS For buSiNESS or iNVESTMENT purpoSES oNLy

For an immediate online approval and commitment letter, go to WWW.FMV1.COM and fill out our loan qualifier.

6019 Tower Court, Alexandria, VA 22304Phone: 703-823-6800 or 866-902-FMV1 (3681) Fax: 703-997-2499Paul Fogle or Art Bennett

First Mount Vernon is a privately-owned, equity-based lender which specializes in lending to borrowers who can’t secure funding from traditional financing sources. Loans typically funded within two business days upon receipt of completed package. First Mount Vernon does not make consumer loans.

Financing is for business or investment purposes only, secured by real property.

We’ll help you put the pieces together.

�

TheNicheReport.com 13

Last year, Colorado joined the ranks of states to finally regulate mortgage brokers to register. Over 10,000 loan originators state-wide filled

out the necessary paperwork, got their E&O Insurance, Surety Bond, and criminal background check. Later in the spring, the State of Colorado changed the rules and said that mortgage brokers had to take 40 hours of education along with getting tested by December 31st. The last number I heard, only 1,200 brokers completed and past the test.

Did we lose that many mortgage brokers? Are mortgage brokers procrastinators or did that many leave the business? It’s probably a little of both, and I can only assume that the percentage of exodus in Colorado is similar to those in your territory.

There is a tremendous amount of orphaned builders, Realtors, buyers, sellers and professional referral sources waiting for you to call on them. They are looking for professionals like you to help them with their clients. Now is the time to make prospecting and setting up appointments as a daily discipline.

When it comes to building relationships, it takes more than one sales call. Statistically, 46% of all sales people ask for the business once and stop making calls to the client. 24% ask twice and stop. 14% ask three times and stop. 12% ask 4 times and stop and only 4% ask 5 times or more. An interesting fact is that 60% of all business is sold after the person is called on at least 5 times!

This is the number one reason why I like calling on builders. Most of my competition already assumes that

the builder has a lender in place so why bother making the call. In this kind of market change, most builders do not have a relationship. A number of them closed down their mortgage company and are looking for solid lending relationships. I’ve had builders tell me how surprised to see me call on them multiple times as most lenders stop after the first call. It’s immature for a sales professional to expect business the first time out. It happens sometimes—but rarely. The one who has the “call till it croaks” will have success.

Same goes for Realtors. A Realtor called me a few weeks ago and was surprised how quickly I returned her call. I told the Realtor that I’m neurotic about returning calls quickly and that when someone doesn’t return my call in a timely matter, I consider it unprofessional. Lenders are finally getting busy with refinances and have abandoned the agents. This Realtor ask to set up an appointment with me as she put in a call to her loan officer three days ago and still hadn’t heard from them.

Past clients, buyers and sellers have also been abandoned. Even in normal markets, loan officers do a poor job in staying in touch with their clients. I read an interesting article from Kevin Johnson regarding client satisfaction and client retention in the mortgage industry. Over 1,000 clients were asked the question how satisfied were you with your last lender and how was the experience. Over 89% said that they were satisfied or very satisfied with the service. The next question was, “Did you go back to that lender the next time you did your next purchase or refinance?” Only 16% went back to their previous lender. Why--Because 80% of us do not

ORPHaned cLIenTS and cUSTOMeRS

By TOM nInneSS

They are waiting for your call

stay in touch with our clients. We assume that since we did a good job the first time, that the client will break their necks trying to find us for their next transaction. As mortgage professionals, we have to look at our business long-term and our responsibility to our clients is to manage their mortgage, even though we are not servicing the mortgage. You must have a “Customer Management and Retention System” in place that lets you know when a client’s birthday, mortgage anniversary, ARM is adjusting and alarms when it makes sense for past clients to look at refinancing.

Lastly, buyers and sellers are looking for a lender who will adopt them. Write press releases, articles on market changes. Offer free seminars on what’s going on in your market place. Participate in civil, social and community groups. The one who builds the biggest list, maintains that list and works that list will win big in today’s market.

Tom Ninness is Vice President/Regional Production Manager for Cherry Creek Mortgage in Denver, CO. He is

also the President of Summit Champions, Inc. and creator of the “The 90 Day Journey to Your Sales Success”, a powerful 90 day action plan for the sales professional. To learn more about The Journey and all what Summit Champions has to offer, go to www.90dayjourney.com, www.summitchampions.com or contact Tom at [email protected] Office: 720-221-4396.

We originate commercial loans in all 50 states as well as FHA and Residential Loans in CA, NV, OR and AZ.

Sign-on bonuS based on experience/licensed.

For Qualified Candidates:• Benefits Package • XLNT Commission Structure

Fax resúme (888) 450-7907or call John Miller (800) 530-2489 ext. 301or email to [email protected]

Loan officerS

WE ARE BUYERS AGGRESSIVELY SEEKING OPPORTUNITIES in:ALL DISTRESSED SITUATIONS

HospitalityHotels and Resorts

Commercial Real EstateOffice Buildings

Urban RetailIndustrial

Residential Real Estate Multi-Family

HUD PropertiesBuilder Buyouts

Bank Owned Real Estate, REIT/Fund/personal holdings liquidations, Performing and Non-Performing Debt. Our markets include but are not limited to

North America, UK, Africa, India and the Middle East.We are active in most segments and seek opportunities in:

•ScoreWizard®–aleadingedge creditadvisorytoolwiththeWhat-If Simulatorthatquicklyprovides easy-to-implementsuggestionsfor improvingyourapplicant’screditscore.

•Score Plus–thisprogramallowsyou toupdateconsumercreditinformation in3to5businessdays(ratherthanthe standard30days),andgeneratesanew creditreportreflectingtheupdate.

•PRBC Reports with FICO Expansion Score–analternative creditreportthatmeetsGSEandFHA standards,basedonmonthlypayment dataforitemssuchasrentandutilities.

CreditPlusoffersthreeadditionalservicesthatallowyoutoqualifymoreborrowersanddramaticallyincreaseyourclosedloans:

QUALIFYMOREBORROWERS

Tired of saying No to your loan applicants? Say YES! more often when you partner with Credit Plus, Inc.

Now that you have them approved, close their loan faster…Providingappraisal,titleandsettlementservicesinall50states,Aristonoffersthefastestturntimesacrossthecountry.Callustodaytolearnhowcombiningyourcreditandtitleservicesresultsingreatercostsavingsandreducestimefromapplicationtoclose.

LEARN HOW WE HELP MORTGAGE PROFESSIONALS

ASPECT – It’s easy to add credit reporting to your website with ASPECT – Allow your borrowers to order and pay for their credit report from your website. The consumer receives a ScoreWizard credit score analysis to help understand and improve his or her credit score and a FACTA disclosure. You receive an immediate email notification referencing the credit report and score analysis for evaluation and processing. Offered exclusively by Credit Plus.

800.258.3488creditplus.com

800.569.9951aristonthebest.com

FHA Streamlined refi's

By LeSLIe PeTeRSen

Put your client into a better loan

Work less, make more money and

put your client into a better loan! Yeah, right – heard that before, haven’t you? What about no appraisal and

no income qualifying? Too good to be true, right?

Let’s test it out. All of the following are rumored to be features of the FHA Streamlined Refinance program. How would you answer?

T F

o o 1. Unemployed borrowers are eligible; there is no income qualifying

o o 2. No FICO requirementso o 3. No new appraisal required, even in declining marketso o 4. Borrowers who no longer occupy the home may be

dropped from the new loano o 5. No asset verificationo o 6. Loan can be done at no cost to the borrowero o 7. There is no one-year seasoning requiremento o 8. Borrowers end up with a better loan, usually with lower

payments o o 9. Secondary financing may be subordinated without regard

to CLTVo o 10. Current occupancy is not necessary

You’re correct if you guessed that they are not all true; number 4 is false. But the rest are legitimate, and a fairly comprehensive synopsis of the FHA streamlined refinance features. Read through them again for a better appreciation of the program, skipping over #4 this time.

There are two pretty big catches: (a) an FHA streamlined refi is only for borrowers who currently have an FHA insured mortgage; and (b) to originate an FHA mortgage, streamlined refinance included, you must be a W-2 employee of an FHA approved company.

Pretty big catches.

WHaT aRe STReaMLIned ReFInanceS?The premise of streamlined refinances is to originate a

new mortgage with minimum qualifications that place the borrower and HUD in a better position.

Take Danny Homeowner, for instance, who purchased his home with an FHA insured mortgage. The FHA insurance means that HUD is already on the hook if Danny’s home were to be foreclosed (an unfortunately common occurrence lately). To mitigate this possibility, HUD is willing to insure a new streamlined refinance mortgage that makes it easier for Danny to make payments. So what if Danny lost his job or his home declined in value?

WHO QUaLIFIeSTo qualify. FHA’s basic rule is that the P&I on the

newly created mortgage must be less than the borrower’s current P&I payment.

An exception to this rule allows increasing the current interest rate of an ARM loan by as much as 2% without additional qualifying other than ensuring that the borrower was making timely payments.

There are other exceptions to a P&I reduction, most specifically for those going to or coming from ARM loans or reducing the loan term. Details can be located in HUD’s Handbook 4155.1 REV 5, Mortgagee Letter (ML) 04-28, and ML 05-43; or, in my own FHA and VA Streamline Refinance Handbook, found at my website.

The bottom line is that it may not be just borrowers with high interest rates who are good candidates for a new FHA streamlined refinance.

WITH OR WITHOUT aPPRaISaLAlthough FHA streamlined refinances may be

performed with or without an appraisal, the typical

reaction is, “Why on earth order a new appraisal if it’s not required?”

‘With’ appraisal is not nearly as common as ‘without’, but it does have an advantage. As you will see in the loan amount calculations, next, the maximum loan amounts for streamlined refinances without appraisals are limited by the original note amount (plus UFMIP). Calculations for ‘with appraisal’ are based on the new appraisal. In other words, if the value of the home increased since the first loan was originated, the maximum allowable loan amount is higher.

Typically, Originators choose the ‘without appraisal’ route, and pay for cost shortages through their yield spread premium (YSP) or servicing release premium (SRP), resulting in a higher interest rate to the borrowers. The ‘with appraisal’ option is desirable if you’re trying to keep the rate low by increasing the loan amount to cover all of the new loan costs.

HOW MUcH can THey BORROW?1. The maximum loan amounts calculations are:• Withoutanappraisal:theoriginalnoteamount

(which includes the UFMIP*) of the FHA insured mortgage being refinanced PLUS the entire new UFMIP.

• Withanappraisal:97.75%ofthenewFHAappraisalplus the new UFMIP (UFMIP is covered below)

2. But we’re not through. Because this is a rate & term and not a cash-out refinance, the clients may never borrow more than the mortgage indebtedness, which is:• ExistingLienCalculation:Addtheexistinglienwith

no more than 60 days interest, new closing costs and prepaids, discount points as applicable to reduce the rate, costs of home repair if required by the appraiser; then subtract the UFMIP refund, if applicable; then add the new UFMIPThe final loan amount is the lower of the two. If

the “existing lien” calculation is higher than the first calculation, the borrower will be short funds to close. The difference is the amount that must be derived through premium pricing (YSP or SRP) for a ‘no cost’ loan.

UPFROnT MIP (UFMIP)The UFMIP premium amount for all new

streamlined refinances is 1.5% [ML 08-23 & ML 08-40.] Borrowers whose loans were in force less than 3 years are due for a pro-rated refund of the UFMIP that they paid

TheNicheReport.com 17

on the original loan. This definitely lessens the burden by eliminating the need to pay UFMIP all over again.

FHA borrowers are hit twice with Mortgage Insurance and must also pay a monthly premium. However, they’ve already been paying a monthly premium on the existing loan. The new premium seldom goes up by very much and depending on the LTV and loan term, the dollar amount to the borrower can actually be reduced or dropped.

SeaSOnIngHUD’s only seasoning requirement is that the current

loan be HUD insured. Some lenders impose a six month loan seasoning, yet it’s not a HUD requirement and not required by all lenders.

The true restriction comes from the lenders of the loans being refinanced. Most lenders contractually require the loan officer on the original loan to refund, or pay back, the YSP/SRP if the loan is paid off within a certain amount of time – usually six months or a year. Often, the pay-back is required regardless of who originates the new loan.

As an originator, this reinforces the need to keep in contact with prior clients. If it’s in the best interest of a prior client to refinance an FHA mortgage currently in the lender-pay-back-the-YSP period, contact the lender and discuss potential options.

OTHeR eLIgIBILITy ReQUIReMenTSSome of the other requirements for FHA streamlined

refis are:• Theborrowercannevergetcashbackinexcessof

$500• Thenewloancanneverpayoffsecondary

financing. However, new or existing secondary financing may be subordinated without regard to CLTV.

• Non-occupantscanneverborrowmorethantheoutstanding balance of the current mortgage. The maximum loan is calculated by taking the current balance plus the new UFMIP minus the UFMIP refund. All costs must be paid by the borrower or derived from premium pricing.

• AvalidSocialSecurityverificationisnecessary.Anytime the current FHA loan was originated with an invalid SS# (it happens), the outstanding loan is ineligible for a streamlined refinance.

• Themaximumloantermistheremainingoutstanding term plus 12 years

• Borrowersmaynotbedroppedfromtitleexceptbydevise of law (i.e., divorce, death), and even then, are subject to additional conditions.

QUaLIFyIng

Without Qualifying: As previously mentioned, qualifying is not required as long as the borrower fits into all of the eligibility requirements. There is no verification of income, employment, or assets.

Additionally, neither credit reports, nor FICO scores, nor CAVIRS are required. A 12 month payment history is customary (or less, if the new loan was originated less than 12 months ago) and is required by the new lender. A payment history is also required by HUD when increasing the P&I.

A word of warning: if you provide the lender with a FICO, the lender will use it. A low FICO may cause your loan to be rejected; so remember to NOT provide a FICO unless it’s specifically mandated by the lender.

With Qualifying: When removing a borrower from title who doesn’t qualify on his/her own through devise of law (last bullet above), or if the P&I on the new mortgage increases by 20% or more over the P&I on the existing loan – the remaining borrowers must go through the entire re-qualification process. Examples include dropping parents who originally co-mortgaged on the loan; or, refinancing from a 30 year term to a 15 year term.

Although it may seem contradictory to originate a streamlined refinance that requires qualifying, the saving grace is the lack of appraisal required. A no-appraisal transaction is often a deal saver in today’s market.

cOMMISSIOnS & FUnd SHORTageSI find it’s common for originators to end up with far

less commission than anticipated. Either that, or funds are required at closing that the borrower just doesn’t have and were never quoted. Both of these circumstances are not only devastating, they are avoidable.

With a streamlined refinance it’s always a numbers game. A couple of suggestions:• Don’tquoteaninterestrateuntilyouhaveallof

the numbers necessary to calculate an accurate loan amount.

• Takecontrolofallcalculations,includingtheloan

18 February 2009

Many mortgage professionals know us simply as “the Mortgage XSite people”, and that’s understandable. The popularity of Mortgage XSites was instant, setting the standard in technology, ease of use, and affordability. In fact, Mortgage XSites have been and continue to be the #1 mortgage website product. But we realize that a website isn’t your whole business, so we’ve spent years rounding out our product line to cut your costs and make you money long term. The “counter-cyclical” marketing products we perfected over the past few years are, thankfully, here and affordable. But forget about the tools for a moment. There are key things common to everything we do which are even more important than our products.

For example, we back everything with an iron-clad, 100 day, 100% money back guarantee. We couldn’t do that if our

products didn’t truly work. We also provide you with live

technical support 24 x 7 x 365, so we’re here when you need help. Our Oklahoma City headquarters is always staffed with live people charged with getting you productive immediately.

Plus, you’re not just buying a mortgage product. You’re buying into our culture of putting the client first, and “doing what’s right.” That’s earned us incredible loyalty among our diverse client base for 23 years.

There’s a reason more than 100,000 mortgage professionals, agents, lenders, inspectors, and appraisers rely on our products to process nearly 50% of all residential mortgages in the U.S. every single day. Simply put, we provide the right solutions, at the right price, backed by the right service. Come see for yourself, and you’ll choose us too.

Increase your business. Cut Costs. Guaranteed.

Mortgage XSites $499/yrSophisticated, rich, hassle-free websites

XSellerate $199/yrAutomated marketing turns leads into sales

SureDocs $299/licenseE-doc signing and delivery solution

FleXApp1003 $199/yrIntuitive online 1003 that works on any site

Daily Rate Lock Advisory $299/yrProvide expert rate float/lock advice

Listings XPress $199/yrMultimedia listing tools that drive traffic

Mercury Network FREEFree appraisal order management solution

Not just a(nother) website company

AD CODE: MANRXSME0209 a la mode and its products are trademarks or registered trademarks of a la mode, inc. Other brand and product names are trademarks or registered trademarks of their respective owners. All prices, terms, policies, and other items are subject to change without notice. Copyright ©2009 a la mode, inc.

XSites XSellerate SureDocs

www.alamode.com/nr 1-800-ALAMODE

Call or visit our website today!

100 DAY MONEY-BACk gUARANTEE

MANRXSME0209.indd 1 1/9/09 4:21:44 PM

amount. The borrower’s interest rate, and your commissions are all intermingled and it shouldn’t be the processor’s problem.

• Alwaysasktheborrowertobringahousepaymentto the closing table.

• Don’tunderestimatethepayoffortheamountofprepaid expenses. Especially the expenses necessary to establish a new escrow account at the new lender. It can make a huge difference in the loan amount.

• Recognizethatanytimethe“existinglien”exceedscalculation number one, (see “How Much Can I Borrow” above) the difference in funds must come from someplace – whether it’s your commission, the YSP/SRP or from the borrower

And then, if the numbers just don’t work – consider the “with appraisal” option.

BOTTOM LIneIt really is legitimately possible to work less, make

more money, and put your client into a better loan. FHA

Streamlined refinances are easy and profitable mortgage

loans to originate, but you must pay attention to all of the

details and nuances.

This current low interest rate environment opens

the door to an exciting mortgage refinance option that

can benefit all parties, including (especially) the loan

originator. If you’re FHA approved and serious about

digging in, you might as well become a Streamlined

Refinance Expert and make your life easier.

Leslie Petersen has over 30 years experience in mortgage

lending. She’s known for her expertise in the rules and regs of

the business, and for showing Originators, Underwriters and

Managers how to make the rules and changes work for them.

Find her recently revised FHA and VA Streamlined Refinance

Handbook at MortgageTrainingTools.com. You can reach

Leslie at [email protected].

Hard Money Loans from $100,000 to $1,500,000

• Minimum Credit 400 • No seasoning • No up front fees • 48 hour closing

Lending Territory includes DE, MD, DC, VA, NC, SC, GA and FL.

ALL LoANS For buSiNESS or iNVESTMENT purpoSES oNLy

For an immediate online approval and commitment letter, go to WWW.FMV1.COM and fill out our loan qualifier.

First Mount Vernon is a privately-owned, equity-based lender which specializes in lending to borrowers who can’t secure funding from traditional financing sources. Loans typically funded within two business

days upon receipt of completed package. First Mount Vernon does not make consumer loans. Financing is for business or investment purposes only, secured by real property.

6019 Tower Court, Alexandria, VA 22304Phone: 703-823-6800 or 866-902-FMV1 (3681) Fax: 703-997-2499Paul Fogle or Art Bennett

We’ll help you put the pieces together.

Let’s face it; things aren’t looking so good right now. In uncertain times like these, your clients need guidance, expertise and experience more than ever.

A hard money commercial loan may be the ideal way for your clients to seize an opportunity or solve a problem. Despite these difficult market conditions, Avatar is financially stable and has plenty of capacity to fund commercial loans from $1,000,000 to $20,000,000+.

So if you’re ready to deal, we’re ready to listen.

Call us today at 888.896.0083 to discuss your loan or visit www.avatarfinancial.com for more information.

Hard money for hard times.

A different kind of loan. A different kind of lender.

As the economy crumbles, more and more Ameri-cans are at risk for losing their home. Lenders and servicers are overrun by distressed homeown-

ers trying to avoid foreclosure. Unfortunately, lenders lack the resources to save every homeowner and many are getting lost in the resulting economic quagmire.

An individual’s sense of pride, joy, and security of home ownership is withering away with the crippling economy. The rate of foreclosure is staggering. But there is a way to avoid this tragedy. That solution is a loan modification, which allows normal, everyday people to save their home. If you are in financial trouble, professional loan modification specialists can act as your white knight, saving you from losing your home. It is a solution that both lenders and borrowers champion because it benefits both parties.

A loan modification benefits the lender because some (or all) of the outstanding principal and interest, as well as other associated fees, can be rolled into the new loan and, as a result, does not result in lost revenues. Homeowners, of course, value the option to stay in their home, even if it means making payments over a longer period of time.

A loan modification, as the Department of Housing and Urban Development defines, is a “a permanent change in one or more of the terms of a mortgagor’s loan,” that “allows the loan to be reinstated, and results in payment the mortgagor can afford.” In essence, a loan modification allows homeowners to continue living in their home while making more affordable payments.

Try not to confuse a loan modification with other banking concepts. A loan modification is not the same as debt consolidation, refinancing, or even forbearance. Debt consolidation combines multiple loans into one loan, often with a lower monthly payment http://www.

investorwords.com/3634/payment.html and a longer repayment period. Refinancing is a similar concept in which the borrower pays off an existing loan with the proceeds from a new loan. Forbearance is a process whereby the lender temporarily changes the terms of the loan allowing the homeowner to get caught up on their late payments. Forbearance is not a great option for most people because the payments increase after the forbearance period and the terms of the loan are left unaltered.

Loan modification is a long-term solution for borrowers with hardships that overwhelm their budgets.

THe LegaLeSeThe loan modification process is a sticky, involved

process. Each lender has its own standards and procedures that make it difficult for borrowers to manage the process on their own. To further complicate matters, these standards and procedures are ever changing as laws and regulations adjust to the current economic crisis. Both federal and state lawmakers are presently involved in the loan modification process, further contributing to the complexity of the rules governing the process.

There are two core pieces of federal legislation affecting the loan modification market: the Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA).

TILA was developed to protect borrowers from predatory lending by requiring clear disclosure of key terms of the lending agreement and the costs associated with it. RESPA similarly requires lender disclosures of closing costs and settlement procedures. Professional loan modification companies sometimes use these statutes as leverage in marketing the modification to the lender.

THe cRUX and cRaZe OF LOan MOdIFIcaTIOn

By andy WaRSHaW, J.d.

Loan modifications are here to stay

22 February 2009

They may also refer the violation to an attorney to proceed against the lender.

PaInTIng a PIcTUReTo give you an overall picture of how the loan

modification process works, it begins with a series of phone calls to the lender during which the caller is greeted by a series of menu options, automatic phone messages, number options, and hours of unpleasant hold time full of static-filled music. It can best be described as miserable. By the time you finally reach a person on the telephone, you will be redirected to a new representative, who has absolutely no idea who you are or what your file is about. They are often overburdened with hundreds, if not thousands of files on a daily basis.

The best solution - Use a professional service company that specializes in loan modification and are there to help you. Professional loan modification specialists are able to dedicate their full attention and expertise to modifying your loan. They will investigate the numerous possibilities to make your loan modification successful, with as little stress as possible.

There are literally thousands of loan modification variations that professionals use, depending on the borrower’s circumstances. The most common modifications available are lowering the interest rate, establishing a fixed interest rate, forgiving payment defaults and fees, or a combination of any or all of these. Principal reductions are sometimes considered but are rarely granted.

The most prevalent method of loan modification is an interest rate reduction, which involves establishing a fixed rate of interest for an extended period of time. Lenders prefer this option because it ensures that there is a continued stream of payment and it prevents more drastic measures, such as foreclosure or a short sale. Lenders, of course, do not want to resort to a foreclosure or a short sale because they stand to lose an inordinate amount of money.

Department of Real Estate in CaliforniaAn example of very strict state licensing is The

Department of Real Estate in California. They have an exclusive list of approved loan modification companies that can assist you. Beware of loan modification companies that are not in compliance with DRE regulations. The DRE requires that loan modification companies have an approved contract and fee agreement prior to collecting advance fees. Do not pay an advanced fee to a company

not in compliance with the law. As of now, only a small percentage of loan modification companies in California are in compliance. Please visit the DRE website for a listing of approved companies. California is one of the first states to regulate this industry, though other states are rapidly following suit.

THe cRUX OF THe decISIOnThe loan modification process is an intricate,

multifaceted procedure. The loan modification decision is not always made by the firm that owns the loan. Instead, the decision is often made by a group of investors who own pieces of the mortgage-backed security. The decisions are based upon what is the most lucrative option for the investor, or what minimizes their losses.

A loan modification with an interest rate reduction is often the preferred avenue. Nonetheless, foreclosure is an option if it generates lower costs to the investor or the lender. The effect of the foreclosure on the borrower is sadly not a consideration to the investor and lender, though the presentation and the facts of the borrower’s condition do impact the decision. This is why it is imperative to use a loan modification specialist to present the strongest possible case to the lender for the modification.

The amount of equity in a home is a crucial factor affecting the modification. The lower the equity in the home, the greater the chances are for a modification service. The level of equity depends on the overall property value, which a homeowner can generally determine by comparing the sale value of other homes in the neighborhood and the trend of the sale prices. The greater the equity in the home, the less motivated a lender is to allow a modification.

Other criteria considered in the loan modification process include whether the loan is based upon an adjustable rate. Adjustable rate loans are preferred for qualifying for the modification. The adjustable rate should be coupled with a borrower who is behind on payments and who has a verifiable, reduced income. This reduced income is known as the homeowner’s hardship and is used as leverage in the modification process. The hardship is a major consideration by the lender in deciding whether to accept the modification or not. An example of hardship is a married couple where one of the spouses loses their job.

SOLVIng THe LendeR’S dILeMMaThe housing crisis has crippled the economy, leaving

TheNicheReport.com 23

many lenders turning to financial instruments such as loan modifications that protect their housing investments. Loan modifications are often a win-win situation for both lender and borrower, but lenders are careful to ensure that loan modifications continue to protect their investment. As a result, many lenders have been flooded with phone calls and inquiries about loan modifications but are unable to move quickly on the applications. Lenders are often understaffed and unwilling to invest in new staff to handle the homeowners’ questions. A loan modification company, whose only job is to assist homeowners for a loan modification, will be able to assist you in dealing with this stressful experience and ensure that the process moves quickly and smoothly for you.

THe FUTUReLoan modifications are here to stay! Legislators

and government officials are pushing new proposals and legislation to save homeowners (and the economy). The FDIC recently unveiled its own proposal from Chairwoman

Sheila Bair to streamline the process. “It is imperative to provide incentives to achieve a sufficient scale in loan modifications to stem the reductions in housing prices and rising foreclosures,” the Federal Deposit Insurance Corp. said in a statement on November 14, 2008.

One of the key elements of the proposal is that housing payments for the delinquent borrowers would be reduced to 31% of their income. The plan would help 2.2 million borrowers in obtaining loan modifications. Bair’s proposal is commendable but it is only one of several options currently being considered. However, regardless of whether the FDIC’s plan is approved or whether alternate legislation prevails, borrowers are the beneficiaries and loan modifications are here to help keep people in their homes.

The economic crisis has no immediate end in sight. Homeowners who need to reduce their current mortgage payments should consider using the resources of a fully compliant loan modification service such as one approved by DRE.

• ads generated via GOOGLE, YaHoo and MSN search engines

• Direct Calls to your phone from homeowner seeking help (not weak telemarketed leads)

• non incentive driven leads

• over 3000 internet leads a week nationwide (filters available)

• no affiliate marketing

We consider ourselves the LOAN MOD LEAD MACHINE. Why? for the simple fact that we generate over 3000 Loan Modification Leads a week. Our Loan Modification Leads are time tested and NON-INCENTIVE driven. Our Loan Modification Leads are from actual customers looking for help with their mortgage. We pride ourselves with unparalleled service and performance and are committed to providing a high quality Loan Modification Lead to our brokers. Our services are always tailored to your unique needs and have a marketing plan for every budget.

http://www.loanmodleadmachine.com

LOAN MOD LEAD MACHINE!

We’re Not Like Other Lenders

Agricultural Real Estate Loans

Accounts Receivable Financing

Ag Production Lending

Short & Long Term Programs

Food Chain Asset-Based Lending

Seeking a creative and collaborative lender? One that understands your concerns and can quickly assess your needs? We offer fast credit decisions and provide rapid funding, all so you get the loan you need.

For complete details on all our loan programs, including our real estate programs for land, commercial, and investment properties – and our specialty business financing programs for the food, beverage, and agricultural industries – contact us today.

agricap.com 213.542.5232

0109-0209_were_not_like_others_half_page_niche_report.indd 1 12/17/2008 2:54:06 PM

© 2008 Cogent Road, Inc. All rights reserved. Funding Suite and the Funding Suite logo are registered trademarks of Cogent Road, Inc. www.cogentroad.com

* * * 2008 Top 50 Service Provider

Mortgage Technology Magazine

* * *

It’s good for business.

®

Get Geared Up.To a cyclist, gears offer greater speed

with less effort. To a watch maker,

they create precision and efficiency.

Like gears in your business, Funding

Suite credit software gives you the

leverage to power more production

from your current lead flow and generate

more efficiency from employees.

Whether it’s separate loan officer

billing, one click credit rescoring, or our

low cost $9.99 intelligent credit reports,

Funding Suite improves performance.

See Funding Suite in action at www.fundingsuite.com/leverageOr give us a call at 800.848.3162

Upon fleeing the wreck that was Enron Corp. after 6 years of corporate commu-

nications positions within Fortune 10 Corporations, I realized I needed a new line of work. A sales position opened up for me as a Title Sales AE here in San Jose CA. Thereafter, mort-gage sales positions of ever-increasing

seniority and scope began to come to me in rapid fashion. This was in direct proportion to the passion I brought to the table and to the service I provided to my clients. Once I learned that proportional ROI, I could never do anything else again. Just think – mobile, connected electronically and in relationships – I could never go back to “driving a cube” again. I needed to figure out a way to make sure that I was presenting a unique and valuable sales proposition.

“He Who Loves Cherries Soon Learns to Climb” – ancient Chinese proverb.

Within wholesale and later retail mortgage banking experiences, I was doing the “complicated” loans when everyone else was being all “NINJA’d” back in the “good old bad old days”. Things like Pledged Asset Lending, One-Time Close Custom Construction, Asset-Dissipation Loans, Trust/LLC/Corporate Lending, Foreign National Lending, and Structured/Laddered Financing were all “too much paper” for the lazy folks to get behind back then.

That left ME to become known as a niche player. NICHE NOTE: My recommendation to all of

you out there who desire to work in the niche lending marketplace is to become an expert in all things FHA while you pick up speed in the niche market. The first few years can be frustrating if you’re doing it on your own.

How to Navigate the Stormy Seas of Niche Residential & Commercial Lending: OK. You’ve got a great package on your desk. What do you do with it? Other vague resources can give you a few places to check out, but you most likely don’t have an established relationship with these resources, someone who can advise you and help you keep your errors to a minimum. You need a mentor. Make friends with seasoned commercial lenders. Use online networking tools to learn as much as you can about how these seas are navigated.

NICHE NOTE: Get familiar with the following concepts: Executive Summary, Personal Financial Statement (PFS), Expression of Interest (EOI), Letter of Interest (LOI), Non-Compete Non-Disclosure Agreement (NCND), Exclusivity Agreement (if you are DIRECT to the client you need this RIGHT AWAY before you shop), Consulting Agreement, and last but not least – the dreaded “daisy chain” – the success of your deal is in an inverse proportion to your success. The more cooks in the kitchen, the worse the sauce, I say. Climb that cherry tree, if you really like cherries!

“At each stage of the game, and with each new rung position on the ladder, make sure you update your database, reflect on your connections, and decide what

PITcH nIcHe TO THe RIcH!

By Jack WILLIaMS

What you know, who you know

26 February 2009

your focus will be when you’re positioning yourself for battle on the High Seas of International Niche Financing”

Niche Lending Providers: Just as in the conventional lending world, the niche market has various classes of residential and commercial funding providers. NICHE NOTE: Today’s standard for custom SFR construction is 70% LTC – NOT LTV.

BANKS: There’re many mortgage banking niche products in the conforming world (more on the way, too). These are the government products for the most part. Some direct lenders will offer their own “competition buster” conforming products. Other national and international banks have what they call “Private Mortgage Banking” divisions – this is where the banks do their magic super jumbo products for high net worth individuals.

PRIVATE EQUITY FIRMS: There are many, many private funding firms around the country. Some deal with their own portfolio, others have uncommon access to international trusts and institutions. The may have “hard”, or better yet, what I call “jello money” – not quite bank rate/fee but still not SO hard as to be considered hard money. The emphasis here is not on full doc/credit qualification, rather on collateral or “skin in the game”.

HEDGE/PENSION/TRUST/INSURANCE FUNDS: This is where the HUGE projects go – into the BILLIONS and beyond! Each fund or entity has its own appetite for difference niche deals – be it Green Energy, Humanitarian, Spec, Custom Estate, Developments, Mines, Accounts Receivables…

SELLERS: We can’t forget the seller of the destination property. When we can’t find conventional or even exotic funding sources, a good consultant will approach the seller to see if seller-financing can be arranged. I recently came across a $4MM Knob Hill SF Condo deal where the seller is willing to carry 80%!

“What You Know, Who You Know” – Putting that Last Best Deal to Good Use: You’re only as good, and as intelligent, as your last deal. What does this mean to you? And by last deal, is that necessarily closed and funded? Hopefully so. But in the niche marketplace, there’s a lot of sweat equity in climbing that ladder. Make sure your transactions are rock solid. Take a look at that nasty, three-times-faxed executive summary and make sure the loan adds up before you use up a “duh” marker with your funding source. If for some reason the deal doesn’t close – what’d you learn? The things you’ll learn, and the people you’ll meet each increase your What/Who factor – your W/W factor will then give you the knowledge to close the next one, as well as decrease the degree of separation from you and the actual principal party.

NICHE NOTE: Make darn sure that you get “one what and one who” out of anything you do! Make it your mission to get a what and a who every single day. Make collecting the w/w’s a new passion. Use internet business networking sites to meet new people, ask questions, and increase your position as a trusted, valued, and beloved advisor to your circle of influence.

It may take time but if you stick to it you will be successful beyond your wildest dreams. Remember to climb for those cherries, or they’ll all be picked over when you get to the tree.

Jack Williams lives in California’s Silicon Valley with his wife and 3 children, and loves good music, good company, and spicy Szechuan food. Jack can be reached for questions and relationship referrals at his website http://www.gotrates.net and is often working when other people are not.

LENDERLAB Niche . Alt-A . Non-Prime . Commercial . DPA . High LTV . Hard Money . Commercial

MORE Lenders, MORE Programs, & MORE Ways to SearchLENDERLAB.COM (800) 339-1863

SEARCH POWER

cenTeR STage

This month, I would like to introduce you to George Marentis, President of Com-

pliance Made Simple, LLC. Com-pliance Made Simple, LLC (CMS) is a privately owned company that specializes in assisting the mortgage professionals with compliance related services.

Can you tell our readers what is Compliance made simple (Cms)?

First, I’d like to thank The Niche Report for the opportunity to introduce CMS.

As you said, Compliance Made Simple is a privately held company that was formed to provide compliance related services to the mortgage industry. In today’s market place, the mortgage broker and banker are struggling to stay in business. Smaller mortgage brokers and bankers in many cases have been forced to reduce staff levels to only themselves and maybe a few originators to stay in business. That is were CMS comes in. For a relatively low expense, CMS can be as involved with the broker’s business as much as the broker or banker desires. In some cases, our complementary services are helpful.

Our goal is to keep the mortgage broker and banker informed of industry changes because whether they like it or not, those changes will impact how they conduct their business as well as their continued success. For example, a new state regulation may require a new disclosure and if the broker is not aware of the regulation change or effective date, the broker is out of compliance. It can take only one complaint to the states lending authority for problems to arise.

As everyone knows, the industry has undergone increased scrutiny at both the state and federal levels and will likely continue this year and beyond. The days where a broker used to get away with “ignorance” are gone and those brokers will be forced out of the industry through enforcement.

As I said, this is where CMS comes in. It is our goal to make our services economical and easy enough that the small resource-strapped broker can be informed and compliant.

tell our readers about your background and how that will help them.

My background in lending and compliance goes back well over 15 years. I started out as an underwriter where I underwrote all types of loans and conducted loan due diligence reviews for more then 10 years. These loans ranged from your standard FNMA/FHLMC to the infamous non-prime (subprime) mortgage. In addition to my underwriting background, I originated loans for many years as a broker. In addition to my lending background, I have a law degree. Since earning my JD, I took my lending knowledge and moved into compliance where I did regulatory and legislative compliance. In this capacity, I reviewed state and federal legislation & regulatory amendments impacting the lending industry and analyzed those changes to determine impact to various lending operations. Prior to forming CMS I handled compliance related issues as a compliance officer for a medium size financial institution.

describe some of the key services offered by Cms.The services CMS provides the mortgage professional

are diverse. Our level of involvement depends on the

cenTeR STage WITH cOMPLIance Made SIMPLe, LLc

Compliance – What you don’t know will hurt you.

BROUgHT TO yOU By THe nIcHe RePORT

TheNicheReport.com 29

putting in place to be compliant? Hopefully the broker knows what HVCC stands for?

• WhatdoestheSAFEActmeantoyou?• AreyoucompliantwiththenewIdentityTheft

“Red Flags” program?• HowwilltheamendedTILAandHOEPAchanges

affect your business?• WhendoesthenewRESPArulebegin?Will

brokers still get YSP? What about after 1/16/2009? • AmendmentstoREGZandHMDA• Nationalmortgagelicensinglegislation

What is the biggest obstacle facing the mortgage broker and banker today?

That compliance is going to be an integral part of the mortgage business whether you are an individual broker or larger shop. No broker can claim an exception based on the size of their company. Thus, the mortgage broker and banker need to realize that they need to actively monitor compliance and failure to be compliant will only create a bigger issue as the financial crisis continues to evolve and more and more homeowners face foreclosure.

cenTeR STage

needs of the mortgage professional. Some brokers and bankers outsource their entire compliance department, while others use our monthly service to be updated on relevant state-by- state and federal legislative and regulatory changes. Others use our nationwide licensing services where we assist the broker or banker with various licensing needs. CMS also performs forensic loan file reviews for those lenders having investor buybacks or other loan file issues.

Why should a mortgage professional use Cms?Whether a mortgage professional uses CMS or their

own staff, they must understand that being compliant is critical. As I mentioned earlier, the level of increased scrutiny at the state and federal levels has increased dramatically and will not decrease. The mortgage broker is the target and the regulatory bodies will no longer tolerate mortgage brokers failing to comply. What’s scary is that a broker recently said to me “COMPLIANCE IS A WASTE OF TIME.” With this type of mentality, it’s no wonder the industry is in the position it’s in and why brokers are the targets.

Not many mortgage brokers and bankers can afford their own in-house counsel or paralegal to handle all the required compliance functions. Those brokers who try to keep up with changes themselves soon realize that the regulations and laws are complex, convoluted and downright confusing. That’s where CMS comes in, we can help the broker navigate those complex regulations and other compliance related issues.

Here are some recent changes facing the industry today:• Untilrecently,Coloradodidnothaveanyloan

officer licensing, education or testing requirements. Now they are all required.

• AreyoufamiliarwithHVCC?Whatstepsareyou

Manaseh, Epharim & Associates

Direct Private Lender

www.MEANDASSOCIATES.COM770-840-0112 or 770-840-0113

Fax: 678-302-6444

Your source for commercial real estate financing.

Funding nationwide and internationally!!

Rates from 3.9%

This is a continuation of last month’s column.

4. Benefit – Cost = ValueThe ultimate goal in any

transaction is to offer a good product at a fair price to the satisfaction of the customer. In this formula, “cost” is

the fair price. Cost can be monetary, emotional, time, or effort. Cost is measured by the customer. You offer benefit. If your benefit far exceeds the customer’s cost of the transaction, then the customer will experience an inherent value. The greater the benefit you offer, more enjoyable or pleasurable the experience will be to the customer and the greater the value they will have for their investment.

5. Listen to the words, not an interpretation in your mind.This is a personal pet-peeve of mine. I hate when

people interpret what I say instead of listening to the literal meaning of my words. I am sure we have all had a disturbing experience of this. For example, I would tell a client that I MAY be able to lock in at a certain rate for them. The next day they want to know if I DID lock in that rate because I said that was what I would do for him. That client interpreted my words to mean I WILL perform that task when I said I MAY be able to perform the task.

This may also run the other way when a client talks to you and you may interpret what they say. The sure-fire cure to avoid this is a military concept call “repeat back.” Simply repeat back to the client what was said so the words are clear and no misinterpretation is conceived.

CLIENT: “I want a 30 year mortgage and I prefer a

payment below $1200 per month.”LO: “I understand that you want a payment below

$1200.”CLIENT: “yes, that includes escrow.”LO: “So, you want a $1200 per month payment on a

30year mortgage that includes escrow. What if the payment is over that? You said that you prefer it to be under, will you consider a bit of a higher payment?”

CLIENT: “That will be fine, just let me know that best monthly payment you are able to get for me….”

In this example, may variables that were not fully understood or possibly misinterpreted could have gummed up a solid deal and turned it into a nightmare for the LO. Repeat back to the customer for clarity and make sure nothing is interpreted.

6. Don’t make assumptions.This is an obvious, but dangerous Golden Rule. I

made the mistake many times of assuming that a client may want something, and performed that task. It bit me in the butt. The classic situation was when I was working on a refinance for a recently divorced female client. The property was not properly documented on title, so I took the liberty of having it corrected for her at a small additional cost to the title fees. When I told her of the correction at the closing, I thought I would be adding value by performing this act. Instead, she became angry stating that this was supposed to have been accomplished already by her husband’s lawyer as part of the divorce settlement and she walked out of the closing. My assumption of a good deed was a deal-breaker.

If any question arises, or any parameter of the transaction is not clear, do not assume and find out what is expected.

TIP OF THe MOnTH

By STeWaRT MednIck

Golden Rules, Part 2

TIP OF THe MOnTH

32 February 2009

TIP OF THe MOnTH

7. The customer does not always know what they want, nor is always right.

The customer is always right. Wrong. The customer does not always know what he or she wants. The customer is as right as the knowledge held on the topic. This dovetails a bit into the last Golden Rule about being the expert. A customer may want a 30 year fixed rate just because it is the lowest interest rate available. The customer may not be aware that another type of mortgage exists that could be a better fit for the customer’s needs. You are the professional and with some basic education to the customer, the options may be clearer. Always ensure you know exactly the customer’s intentions and goals in every transaction, so you can serve his or her needs completely.

8. You are the expert, not the customer.This ties nicely with the previous Golden Rule. Many

times the customer will want to drive the transaction in the direction he or she thinks it should go. That could be a recipe for disaster. Ensure that you serve the customer in a professional and courteous manner in explaining

the benefits and detriments to various situations and scenarios. Provide complete information and listen to the customer. The customer may want to flex some knowledge of the business, but you are the expert. You can serve the customer best by driving the transaction in a manner that benefits the customer the most.

I hope these Golden Rules help. I am sure many of you reading this column have rules and guideline that you follow. I would love to hear them and perhaps write a follow-up column of Golden Rules that you use. Many of these rules may translate well into your everyday life. The gist of these rules is to be ethical, professional, honest, passionate and fair in all you do.

Stewart Mednick is a seasoned mortgage banker and published author. His writing focuses on relationship development, personal empowerment, customer satisfaction, marketing and sales techniques. Stewart is available for marketing consulting, personal coaching and training sessions. If you have a comment or a question for Stewart, contact him at 651-895-5122 or [email protected]

©2008 Gregory Funding LLC, an Aspen Capital a�liated company. This is not a commitment to lend. Restrictions may apply. For Wholesale only. Not for distribution to the general public. LTV based on current valuation by Gregory Funding. Gregory Fundingreserves the right to amend rates and guidelines. All loans are made in compliance with federal, state and local laws. High-CostLoans prohibited. Gregory Funding LLC is an Oregon LLC, Oregon Division of Finance & Corporate Securities Lic#ML3575. GregoryFunding LLC, 425 NW 10th Ave Suite 307 Portland, OR 97209. Toll free: 888-324-3578.

GF_nichereport_.25pgVert10.08.indd 1 10/7/2008 1:43:04 PM

TM

TM

TM

Chris FuellingBusiness Development Manager

[email protected] Free 877-812-4327Direct 786-735-1188

nIcHe RePORTS

TheNicheReport.com 35

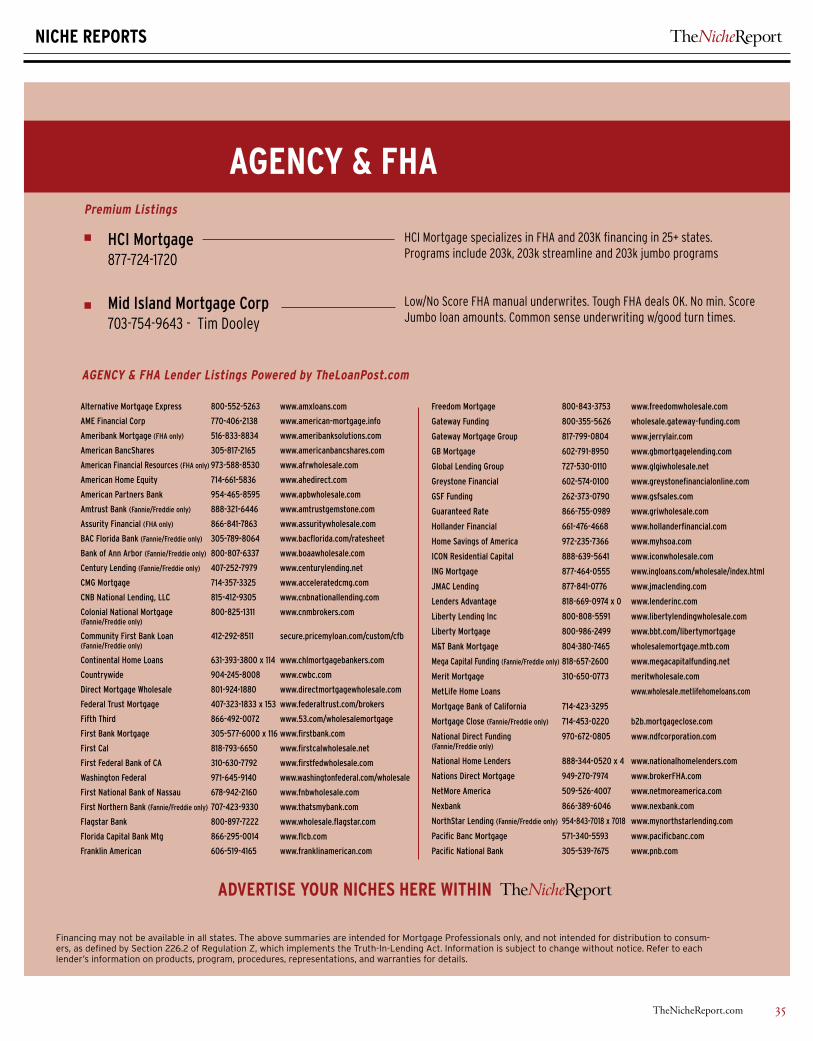

agency & FHa

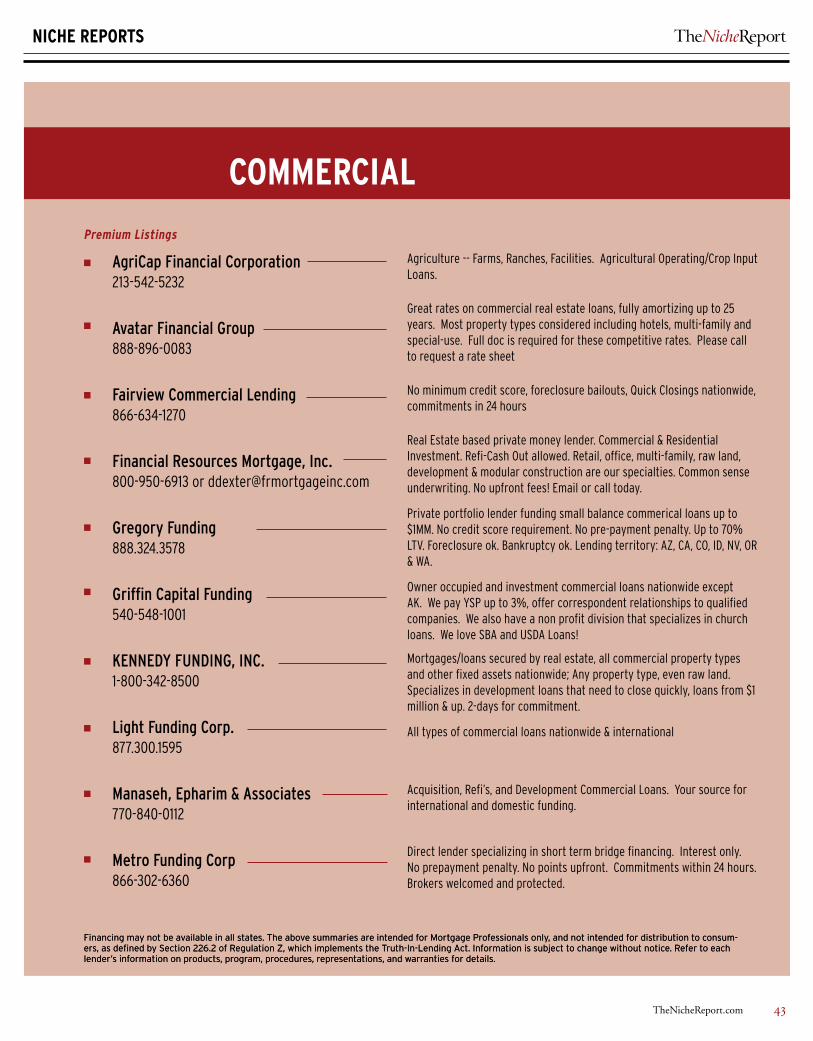

Financing may not be available in all states. The above summaries are intended for Mortgage Professionals only, and not intended for distribution to consum-ers, as defined by Section 226.2 of Regulation Z, which implements the Truth-In-Lending Act. Information is subject to change without notice. Refer to each lender’s information on products, program, procedures, representations, and warranties for details.

Premium Listings

HCIMortgage877-724-1720

MidIslandMortgageCorp703-754-9643 - tim dooley

hci Mortgage specializes in Fha and 203k financing in 25+ states. Programs include 203k, 203k streamline and 203k jumbo programs

Low/no score Fha manual underwrites. tough Fha deals ok. no min. score Jumbo loan amounts. common sense underwriting w/good turn times.

AlternativeMortgageExpress 800-552-5263 www.amxloans.com

AMEFinancialCorp 770-406-2138 www.american-mortgage.info

AmeribankMortgage(FHAonly) 516-833-8834 www.ameribanksolutions.com

AmericanBancShares 305-817-2165 www.americanbancshares.com

AmericanFinancialResources(FHAonly)973-588-8530 www.afrwholesale.com

AmericanHomeEquity 714-661-5836 www.ahedirect.com

AmericanPartnersBank 954-465-8595 www.apbwholesale.com

AmtrustBank(Fannie/Freddieonly) 888-321-6446 www.amtrustgemstone.com

AssurityFinancial(FHAonly) 866-841-7863 www.assuritywholesale.com

BACFloridaBank(Fannie/Freddieonly) 305-789-8064 www.bacflorida.com/ratesheet

BankofAnnArbor(Fannie/Freddieonly) 800-807-6337 www.boaawholesale.com

CenturyLending(Fannie/Freddieonly) 407-252-7979 www.centurylending.net

CMGMortgage 714-357-3325 www.acceleratedcmg.com

CNBNationalLending,LLC 815-412-9305 www.cnbnationallending.com

ColonialNationalMortgage 800-825-1311 www.cnmbrokers.com(Fannie/Freddieonly)

CommunityFirstBankLoan 412-292-8511 secure.pricemyloan.com/custom/cfb(Fannie/Freddieonly)

ContinentalHomeLoans 631-393-3800x114 www.chlmortgagebankers.com

Countrywide 904-245-8008 www.cwbc.com

DirectMortgageWholesale 801-924-1880 www.directmortgagewholesale.com

FederalTrustMortgage 407-323-1833x153 www.federaltrust.com/brokers

FifthThird 866-492-0072 www.53.com/wholesalemortgage

FirstBankMortgage 305-577-6000x116www.firstbank.com

FirstCal 818-793-6650 www.firstcalwholesale.net

FirstFederalBankofCA 310-630-7792 www.firstfedwholesale.com

WashingtonFederal 971-645-9140 www.washingtonfederal.com/wholesale

FirstNationalBankofNassau 678-942-2160 www.fnbwholesale.com

FirstNorthernBank(Fannie/Freddieonly)707-423-9330 www.thatsmybank.com

FlagstarBank 800-897-7222 www.wholesale.flagstar.com

FloridaCapitalBankMtg 866-295-0014 www.flcb.com

FranklinAmerican 606-519-4165 www.franklinamerican.com

FreedomMortgage 800-843-3753 www.freedomwholesale.com

GatewayFunding 800-355-5626 wholesale.gateway-funding.com

GatewayMortgageGroup 817-799-0804 www.jerrylair.com

GBMortgage 602-791-8950 www.gbmortgagelending.com

GlobalLendingGroup 727-530-0110 www.glgiwholesale.net

GreystoneFinancial 602-574-0100 www.greystonefinancialonline.com

GSFFunding 262-373-0790 www.gsfsales.com

GuaranteedRate 866-755-0989 www.griwholesale.com

HollanderFinancial 661-476-4668 www.hollanderfinancial.com

HomeSavingsofAmerica 972-235-7366 www.myhsoa.com

ICONResidentialCapital 888-639-5641 www.iconwholesale.com

INGMortgage 877-464-0555 www.ingloans.com/wholesale/index.html

JMACLending 877-841-0776 www.jmaclending.com

LendersAdvantage 818-669-0974x0 www.lenderinc.com

LibertyLendingInc 800-808-5591 www.libertylendingwholesale.com

LibertyMortgage 800-986-2499 www.bbt.com/libertymortgage

M&TBankMortgage 804-380-7465 wholesalemortgage.mtb.com

MegaCapitalFunding(Fannie/Freddieonly)818-657-2600 www.megacapitalfunding.net

MeritMortgage 310-650-0773 meritwholesale.com

MetLifeHomeLoans www.wholesale.metlifehomeloans.com

MortgageBankofCalifornia 714-423-3295

MortgageClose(Fannie/Freddieonly) 714-453-0220 b2b.mortgageclose.com

NationalDirectFunding 970-672-0805 www.ndfcorporation.com(Fannie/Freddieonly)

NationalHomeLenders 888-344-0520x4 www.nationalhomelenders.com

NationsDirectMortgage 949-270-7974 www.brokerFHA.com

NetMoreAmerica 509-526-4007 www.netmoreamerica.com

Nexbank 866-389-6046 www.nexbank.com

NorthStarLending(Fannie/Freddieonly) 954-843-7018x7018 www.mynorthstarlending.com

PacificBancMortgage 571-340-5593 www.pacificbanc.com

PacificNationalBank 305-539-7675 www.pnb.com

agency & FHa Lender Listings Powered by TheLoanPost.com

adVeRTISe yOUR nIcHeS HeRe WITHIn

nIcHe RePORTS

36 February 2009

Financing may not be available in all states. The above summaries are intended for Mortgage Professionals only, and not intended for distribution to consum-ers, as defined by Section 226.2 of Regulation Z, which implements the Truth-In-Lending Act. Information is subject to change without notice. Refer to each lender’s information on products, program, procedures, representations, and warranties for details.

ParamountResidential(FHAonly) 866-966-8989x300 www.prmglending.net

PerfectFHA(FHAonly) 800-201-2317 www.perfectfha.com

PhoenixFunding 877-562-6414x230 www.phoenix-funding.com

PlazaHomeMortgage 949-910-1055x450 www.plazahomemortgage.com

PMCBancorp 626-964-4040x8199www.pmcmtg.com

PolarisFunding(FL,IN,MI,OH) 616-667-9000 www.polarishfc.com

PreferredCapital(Fannie/Freddieonly) 727-418-4189 www.prefercapital.com

PremierMortgageCapital,Inc. 786-243-3101x2 www.premierwholesale.com

PresidentsFirst 877-773-7178 www.presidentsfirst.com

PrimaryCapital 678-308-0257 www.primarycapital.com

ProtoFund 813-436-6803 www.protofund.com

ProvidentFunding 800-733-3657x1712 pfloans.provident.com

ReliantFunding 412-942-1010x18 www.reliantfunding.us

ResidentialLendingNetwork 800-749-5363x5276 www.reslend.com(Fannie/Freddieonly)

ReunionMortgage 559.476.0937 www.reunionwholesale.com

RoyalCrownBancorp 877-507-6925 www.crownloan.com

SecurityAtlantic(FHAonly) 800-956-3863 www.fhaland.com

SecurityMortgageFunding 619-249-9166 www.smfcloans.com/brokers(Fannie/Freddieonly)

SecurityNationalMortgage 619-857-2700 www.securitynational.com

SenderraFunding 704-831-3600 www.senderra.com

SierraPacific 661-713-6564 www.spm1.com

SouthPointFinancial(Fannie/Freddieonly) 239-949-1406 www.spfs.com

Stearns 925-628-0704 www.stearnswholesale.com

SunTrustWholesale 913-982-2150 www.stmpartners.com

SWCFinancialCorp. 714-680-7050x113 www.swcfinancial.com

Taylor,Bean&Whitaker 888-678-8547 www.taylorbeandirect.com

TheJumboLender 800-826-0360 www.TheJumboLender.com

TitanWholesale 775-852-6888x225 www.titan-wholesale.com

TrustOneMortgage 949-450-1888x2430 www.trustone.com

U.S.BankConsumerFinance 941-539-1603 www.usbank.com

UnitedInternationalBank 313-903-2082 www.unitedinternational.us

UnitedResidentialLending 404-661-4632 www.urlending.com