Embed Size (px)

Citation preview

Experimental Evidence on Tax Compliance

Gareth D. Myles University of Exeter and Institute for Fiscal Studies Lecture 2 CES, February 2014

LECTURE OUTLINE

This lecture is the second in a series of three on the economics of tax compliance

It explores the experimental approach to understanding tax compliance

The topics covered include: The methodology of experimental economics Evidence from tax compliance experiments Increasing external validity by extending the

pool of subjects

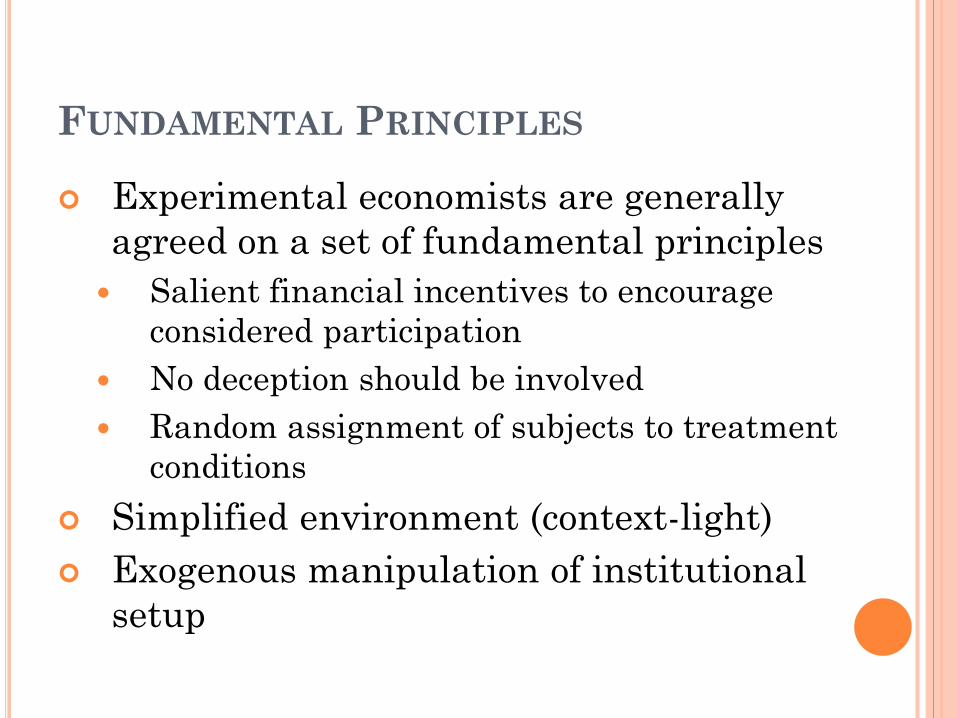

FUNDAMENTAL PRINCIPLES

Experimental economists are generally agreed on a set of fundamental principles Salient financial incentives to encourage

considered participation No deception should be involved Random assignment of subjects to treatment

conditions Simplified environment (context-light) Exogenous manipulation of institutional

setup

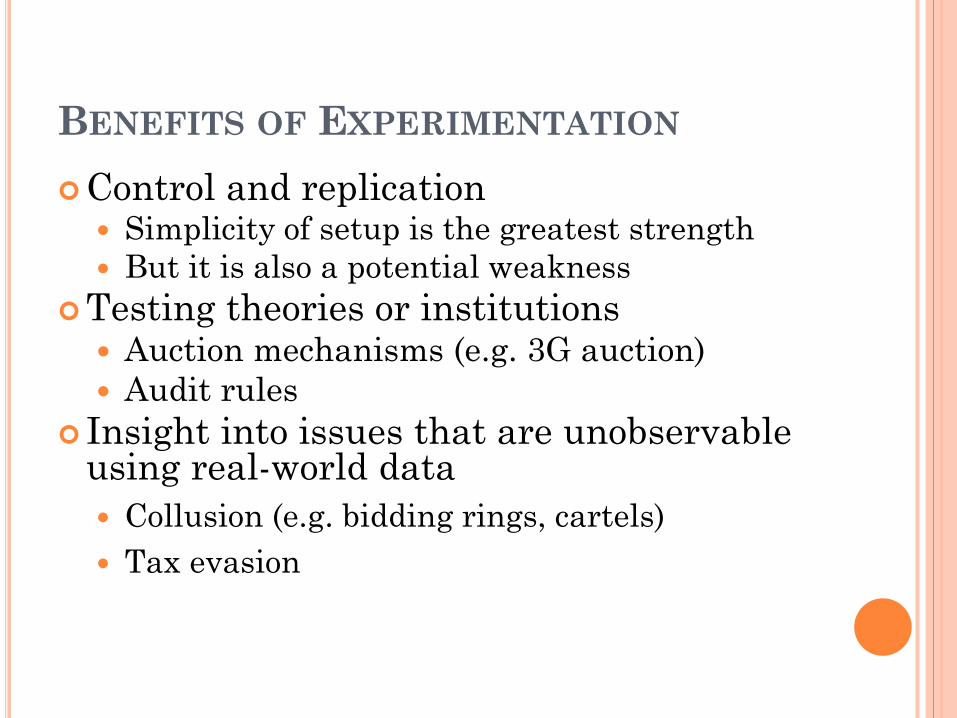

BENEFITS OF EXPERIMENTATION Control and replication

Simplicity of setup is the greatest strength But it is also a potential weakness

Testing theories or institutions Auction mechanisms (e.g. 3G auction) Audit rules

Insight into issues that are unobservable using real-world data Collusion (e.g. bidding rings, cartels) Tax evasion

EXTERNAL VALIDITY

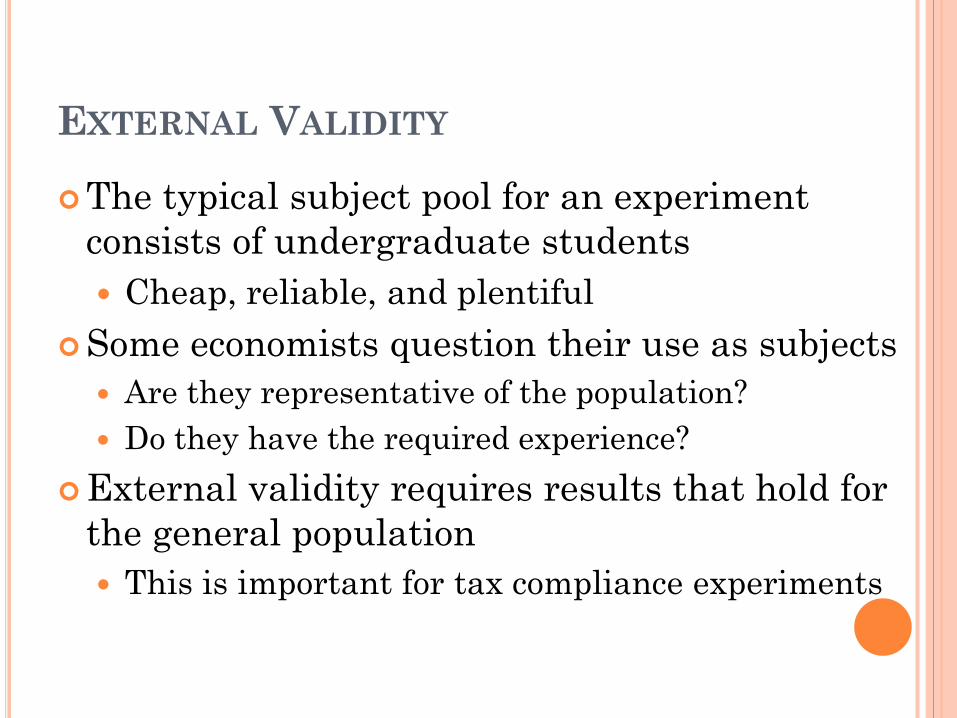

The typical subject pool for an experiment consists of undergraduate students Cheap, reliable, and plentiful

Some economists question their use as subjects Are they representative of the population? Do they have the required experience?

External validity requires results that hold for the general population This is important for tax compliance experiments

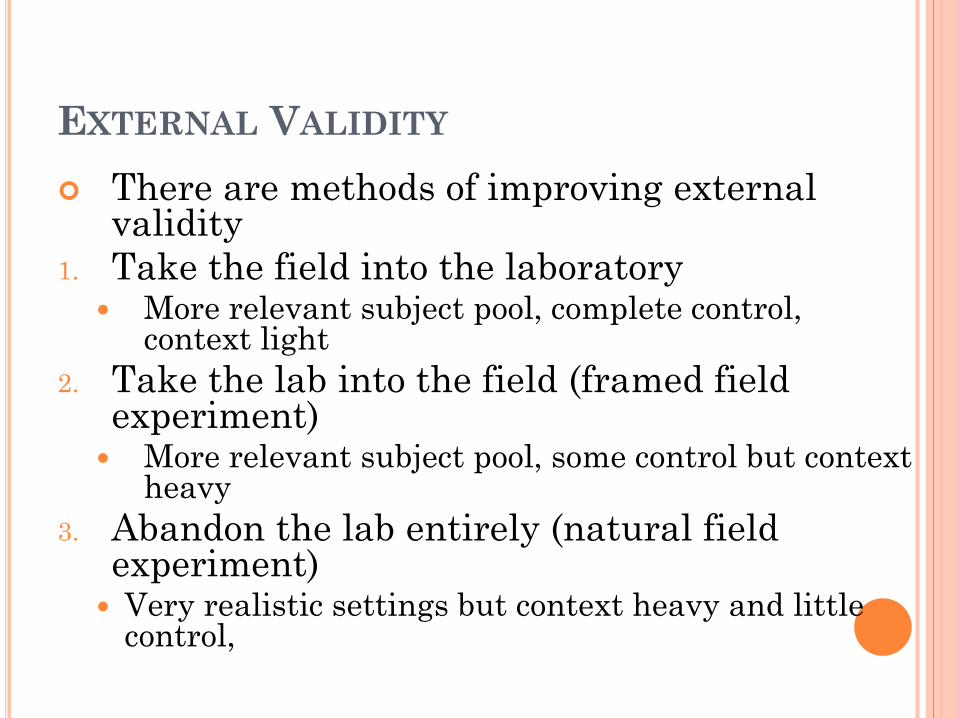

EXTERNAL VALIDITY There are methods of improving external

validity 1. Take the field into the laboratory

More relevant subject pool, complete control, context light

2. Take the lab into the field (framed field experiment) More relevant subject pool, some control but context

heavy 3. Abandon the lab entirely (natural field

experiment) Very realistic settings but context heavy and little

control,

LOGISTICS OF EXPERIMENTS

Duration: typically 30 minutes to 2 hours Sample size: 60-300 participants

This will depend on the nature of the task The number of treatments Group vs. individual decision-making

Cost: subject payments = opportunity cost of the time spent in the session (approx. €10/hour) Exchange rate of experimental currency unit (ECU) to

€ is set according to duration and number of repetitions/rounds

LOGISTICS OF EXPERIMENTS

LOGISTICS OF EXPERIMENTS

Most experiments have been undertaken in laboratories

Some have set in the field We have used laboratory experiments But have also used online experiments Going online allows access to a broader subject

pool But presents technical programming challenges Simultaneity presents special difficulties

COMPLIANCE EXPERIMENTS

Basic framework is the Yitzhaki version of the Allingham and Sandmo model

A taxpayer makes an income tax return which is audited with some fixed probability

If audited the payoff the correct tax payment is paid plus a fine on unpaid tax The fine is proportional to amount undeclared

If not audited the payoff is income less the tax due on original return

COMPLIANCE EXPERIMENTS Taxpayer has income Y but reports income X If caught income is Yc = (1 – t)Y – Ft(Y - X) If not caught income is Yn = Y – tX Expected utility is given by E[U(X)] = pU(Yc) + (1 – p)U(Yn) In experiments utility can be linear so E[U(X)] = (1 – t)Y + tE[1 – p[1+F]]

COMPLIANCE EXPERIMENTS Stage 1: Subjects earn/are given earnings (Y)

Earning your own income substantially changes attitudes (Cherry et al. 2002)

Stage 2: Subjects decide how much to report (X) Given a tax rate t, fine F, and probability of audit, p

Stage 3: Audit occurs If caught, subjects pay appropriate fine

Stage 4: Payoffs are determined and round ends The 4 stages are then repeated for several

rounds

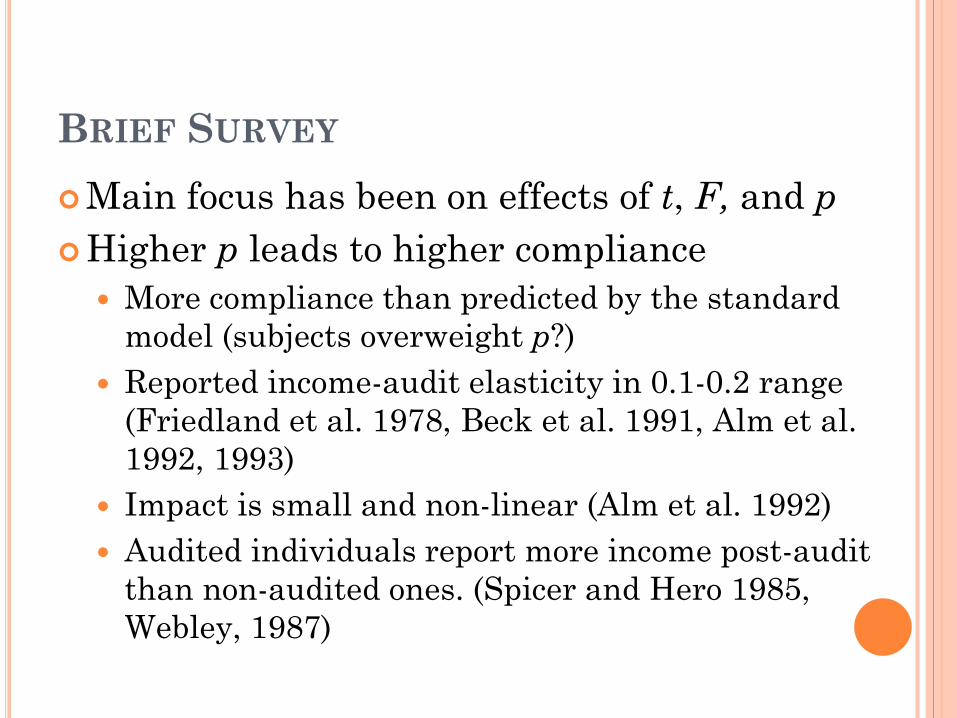

BRIEF SURVEY Main focus has been on effects of t, F, and p Higher p leads to higher compliance

More compliance than predicted by the standard model (subjects overweight p?)

Reported income-audit elasticity in 0.1-0.2 range (Friedland et al. 1978, Beck et al. 1991, Alm et al. 1992, 1993)

Impact is small and non-linear (Alm et al. 1992) Audited individuals report more income post-audit

than non-audited ones. (Spicer and Hero 1985, Webley, 1987)

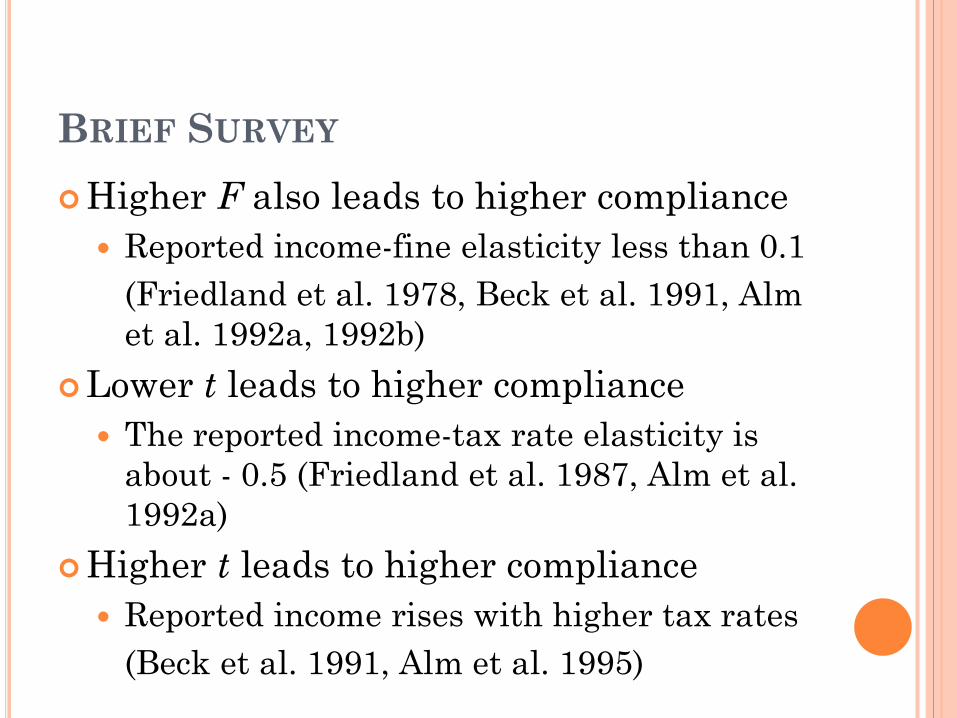

BRIEF SURVEY Higher F also leads to higher compliance

Reported income-fine elasticity less than 0.1 (Friedland et al. 1978, Beck et al. 1991, Alm

et al. 1992a, 1992b) Lower t leads to higher compliance

The reported income-tax rate elasticity is about - 0.5 (Friedland et al. 1987, Alm et al. 1992a)

Higher t leads to higher compliance Reported income rises with higher tax rates (Beck et al. 1991, Alm et al. 1995)

BRIEF SURVEY Uncertainty on p, F or t also affects compliance

Effect linked to public good (Alm et al. 1992a) ‘Cutoff’ audit rules can be more effective than

purely random auditing Collins and Plumlee 1991; Alm et al. 1993

Withholding systems seem not to affect compliance Unexpectedly underwithheld subjects behave no

differently to those who anticipate underwithholding

Behavior of those under- or over-withheld is similar (Martinez-Vazquez et al. 1992)

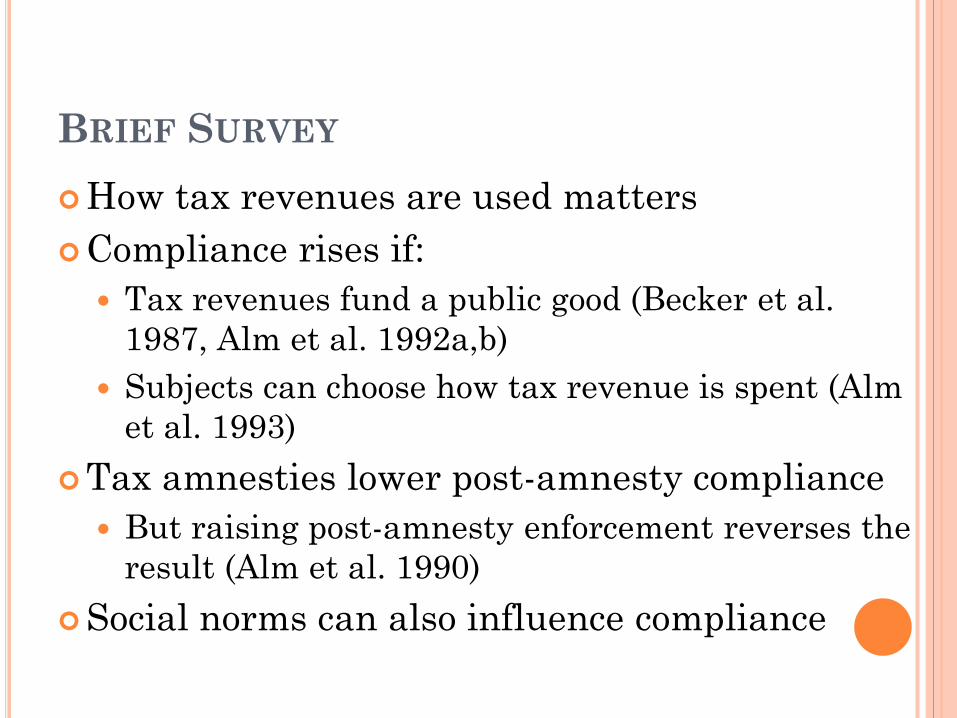

BRIEF SURVEY How tax revenues are used matters Compliance rises if:

Tax revenues fund a public good (Becker et al. 1987, Alm et al. 1992a,b)

Subjects can choose how tax revenue is spent (Alm et al. 1993)

Tax amnesties lower post-amnesty compliance But raising post-amnesty enforcement reverses the

result (Alm et al. 1990) Social norms can also influence compliance

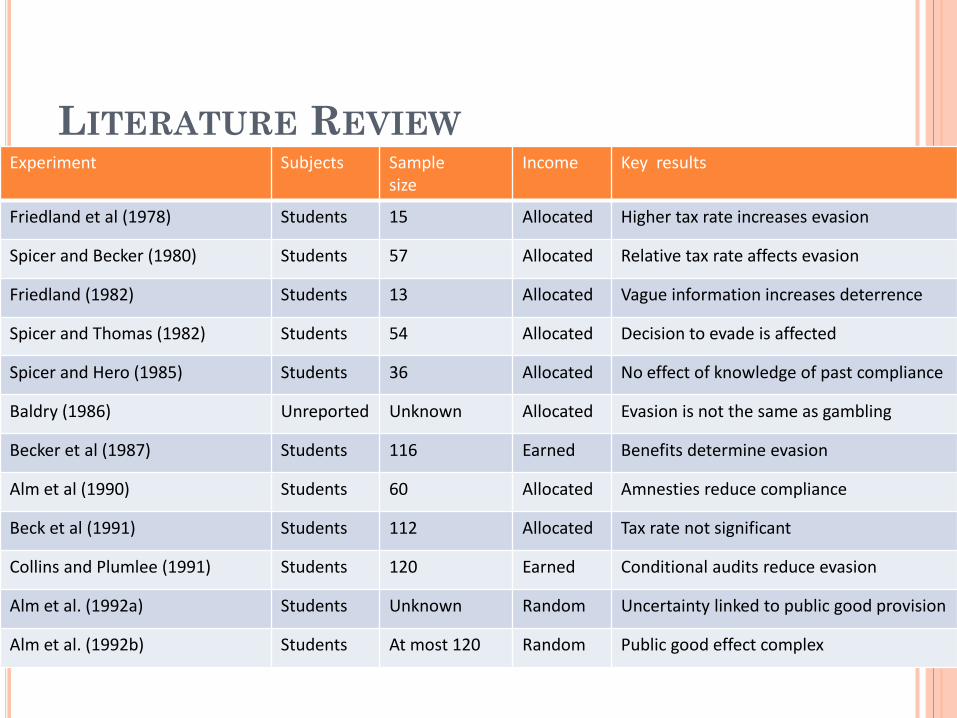

LITERATURE REVIEW Experiment Subjects Sample

size Income Key results

Friedland et al (1978) Students 15 Allocated Higher tax rate increases evasion

Spicer and Becker (1980) Students 57 Allocated Relative tax rate affects evasion

Friedland (1982) Students 13 Allocated Vague information increases deterrence

Spicer and Thomas (1982) Students 54 Allocated Decision to evade is affected

Spicer and Hero (1985) Students 36 Allocated No effect of knowledge of past compliance

Baldry (1986) Unreported Unknown Allocated Evasion is not the same as gambling

Becker et al (1987) Students 116 Earned Benefits determine evasion

Alm et al (1990) Students 60 Allocated Amnesties reduce compliance

Beck et al (1991) Students 112 Allocated Tax rate not significant

Collins and Plumlee (1991) Students 120 Earned Conditional audits reduce evasion

Alm et al. (1992a) Students Unknown Random Uncertainty linked to public good provision

Alm et al. (1992b) Students At most 120 Random Public good effect complex

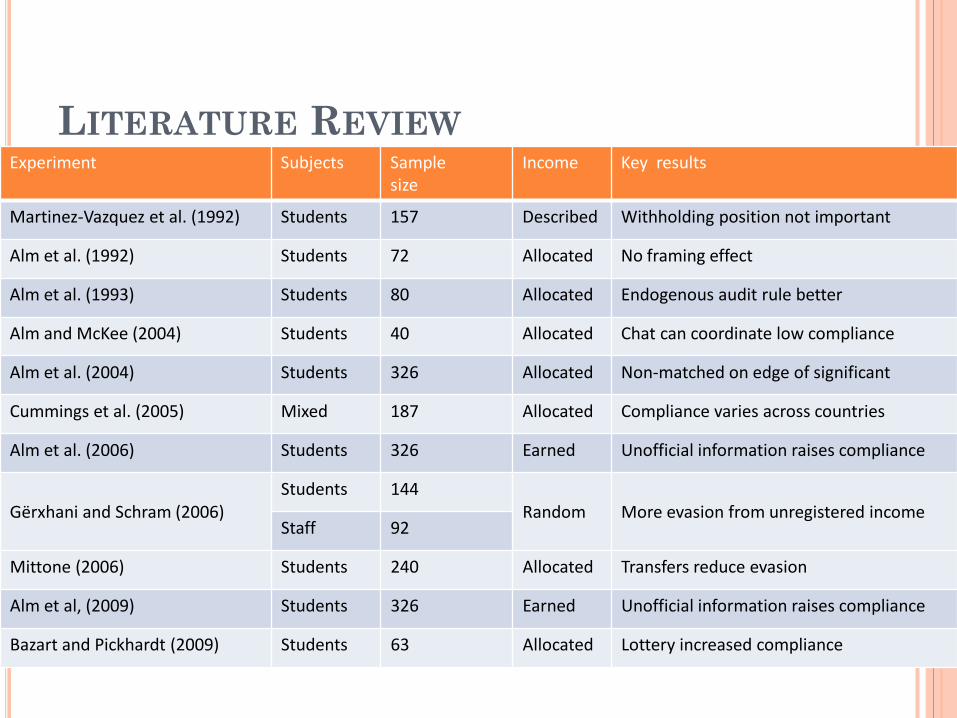

LITERATURE REVIEW Experiment Subjects Sample

size Income Key results

Martinez-Vazquez et al. (1992) Students 157 Described Withholding position not important

Alm et al. (1992) Students 72 Allocated No framing effect

Alm et al. (1993) Students 80 Allocated Endogenous audit rule better

Alm and McKee (2004) Students 40 Allocated Chat can coordinate low compliance

Alm et al. (2004) Students 326 Allocated Non-matched on edge of significant

Cummings et al. (2005) Mixed 187 Allocated Compliance varies across countries

Alm et al. (2006) Students 326 Earned Unofficial information raises compliance

Gërxhani and Schram (2006) Students 144

Random More evasion from unregistered income Staff 92

Mittone (2006) Students 240 Allocated Transfers reduce evasion

Alm et al, (2009) Students 326 Earned Unofficial information raises compliance

Bazart and Pickhardt (2009) Students 63 Allocated Lottery increased compliance

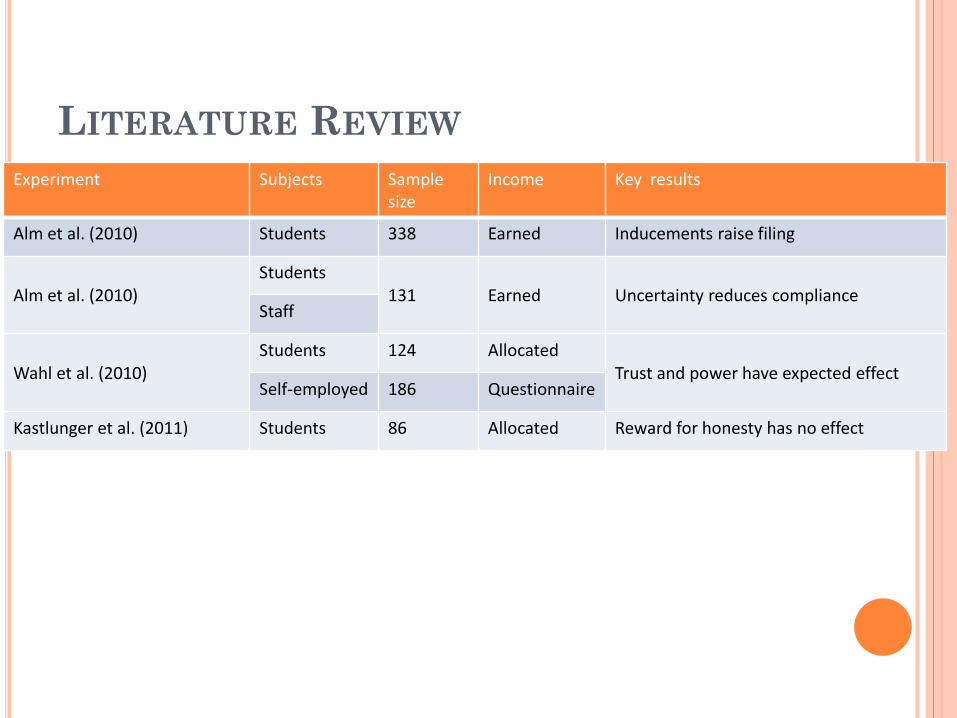

LITERATURE REVIEW Experiment Subjects Sample

size Income Key results

Alm et al. (2010) Students 338 Earned Inducements raise filing

Alm et al. (2010) Students

131 Earned Uncertainty reduces compliance Staff

Wahl et al. (2010) Students 124 Allocated

Trust and power have expected effect Self-employed 186 Questionnaire

Kastlunger et al. (2011) Students 86 Allocated Reward for honesty has no effect

IS TAX EVASION A GAMBLE?

We recently ran a version of Baldry (1986) Participants were enrolled randomly in

one of two experiments In one experiment Part A involved tax

compliance In the other experiment Part A involved a

risky decision (portfolio allocation) For both experiments Part B tested

attitude to risk

IS TAX EVASION A GAMBLE?

What does the model predict about behaviour for tax compliance?

For all sets of parameter it was the case that p < 1/[1 + F]

So the model predicts every participant should have been non-compliant

Non-compliance might vary between participants

But the optimal strategy to maximise expected income is to declare nothing

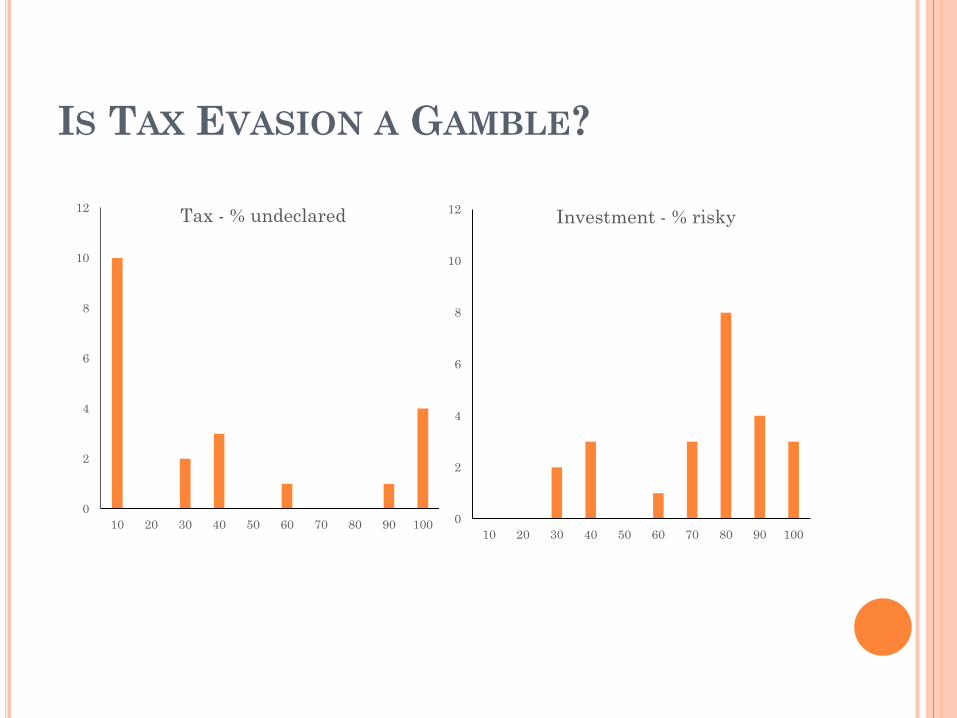

IS TAX EVASION A GAMBLE?

The data did not match these predictions 10 participants out of 21 declared honestly Only 4 declared nothing every time Some participants were partially non-

compliant The choices are summarised in the

histograms that follow

IS TAX EVASION A GAMBLE?

0

2

4

6

8

10

12

10 20 30 40 50 60 70 80 90 100

Tax - % undeclared

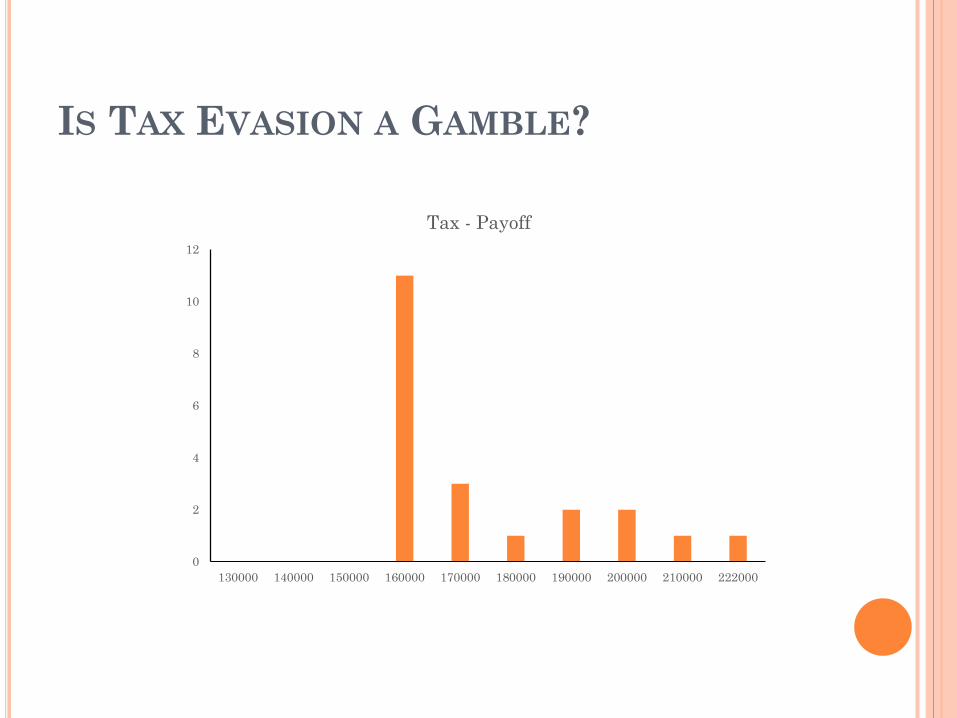

IS TAX EVASION A GAMBLE?

0

2

4

6

8

10

12

130000 140000 150000 160000 170000 180000 190000 200000 210000 222000

Tax - Payoff

IS TAX EVASION A GAMBLE?

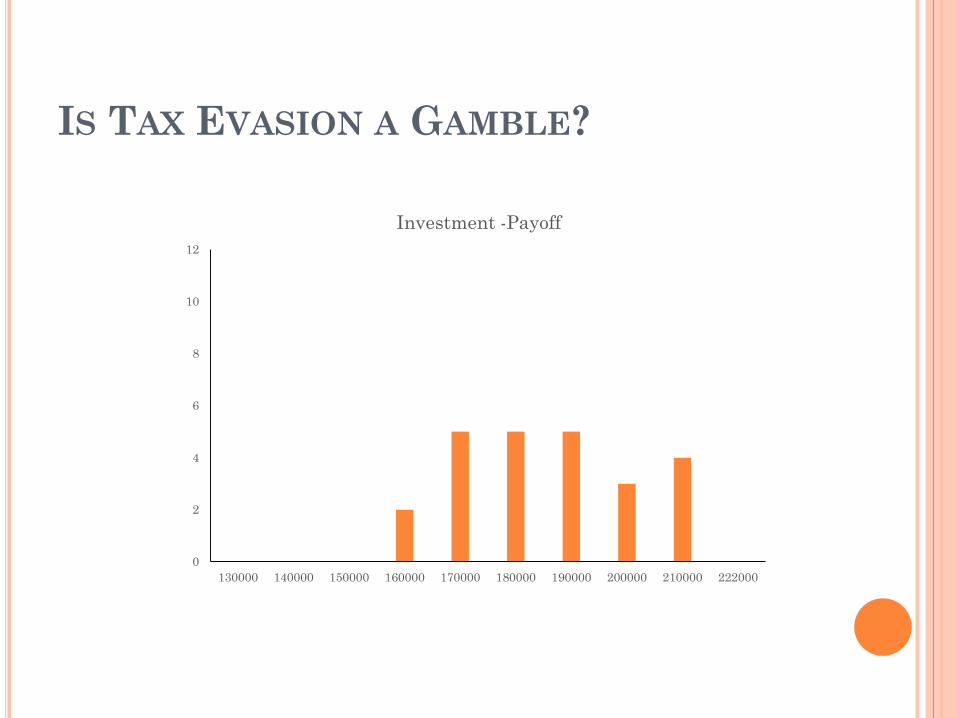

The risky decision involved the allocation of saving to assets in a portfolio

There was a risky asset and a safe asset The payoffs were structured so that the

risky asset was a better-than-fair bet The optimal strategy to maximise

expected income was to put everything into the risky asset

The histograms summarise the responses

IS TAX EVASION A GAMBLE?

0

2

4

6

8

10

12

10 20 30 40 50 60 70 80 90 100

Investment - % risky

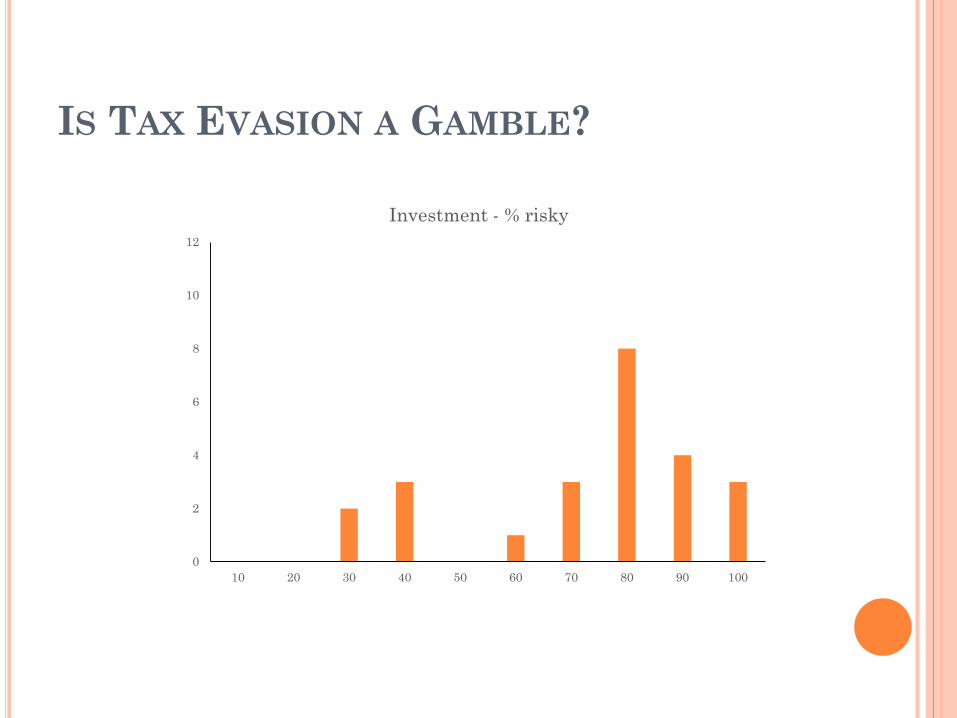

IS TAX EVASION A GAMBLE?

0

2

4

6

8

10

12

130000 140000 150000 160000 170000 180000 190000 200000 210000 222000

Investment -Payoff

IS TAX EVASION A GAMBLE?

Why did we run two versions of Part A? The compliance experiment and the

investment decision had the same payoffs If tax compliance were just a gamble then

the experiments should have the same choices

This was the reason for randomising participants and experiments

The comparison of histograms shows the pattern of choices were very different

IS TAX EVASION A GAMBLE?

0

2

4

6

8

10

12

10 20 30 40 50 60 70 80 90 100

Tax - % undeclared

0

2

4

6

8

10

12

10 20 30 40 50 60 70 80 90 100

Investment - % risky

0

1

2

3

4

5

6

7

8

9

10

0 1 2 3 4 5 6 7 8 9 10 11

Tax- Lottery Switch Point

IS TAX EVASION A GAMBLE?

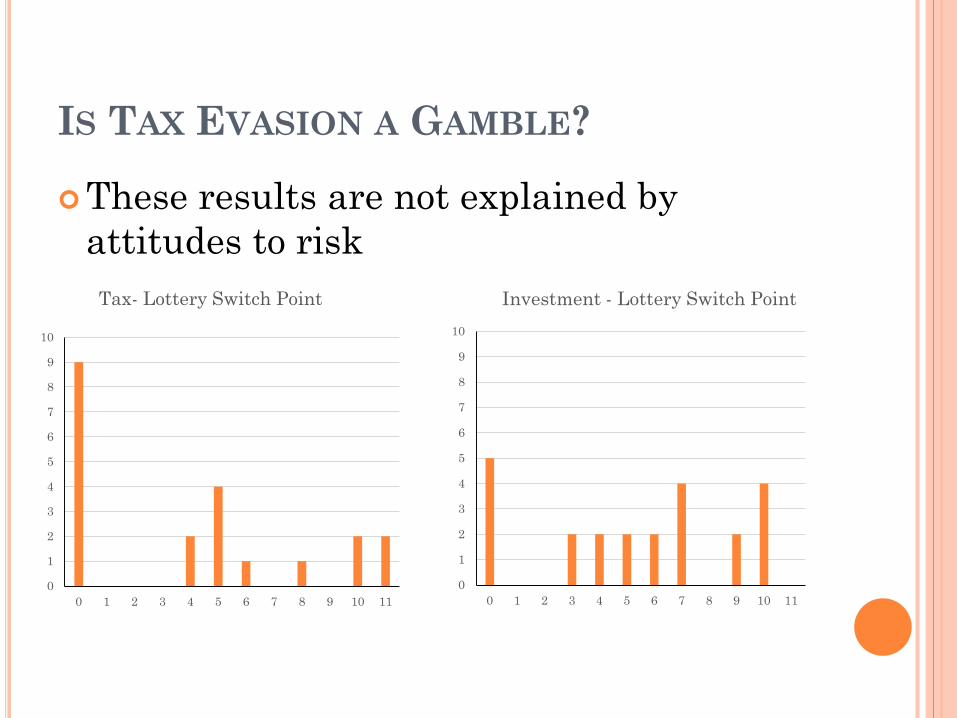

These results are not explained by attitudes to risk

0

1

2

3

4

5

6

7

8

9

10

0 1 2 3 4 5 6 7 8 9 10 11

Investment - Lottery Switch Point

IS TAX EVASION A GAMBLE?

This experiment on framing was first reported by Baldry in 1986

It always works! He concluded from the results that tax

compliance was not just a gamble The comparison between the results

shows that the orthodox analysis is not adequate

UNDER-EXPLORED AREAS

We identified three areas in which existing experiments could be improved

1. Individual differences This is generally unexplored Typical subject pool is 18-22 years old What about those who actually pay taxes?

2. Network effects In theory compliance cultures can arise in

occupational groups Can these be captured within the lab?

INNOVATIONS

3. Sample size in previous experiments typically small

In our experiment: Equal mix of students and non-students Use of on-line experiments eliminating need

for attendance at laboratory Large sample size (1000 subjects)

Enrolment via a market research company Provides greater variation in sample Allows focus of sample on specific group

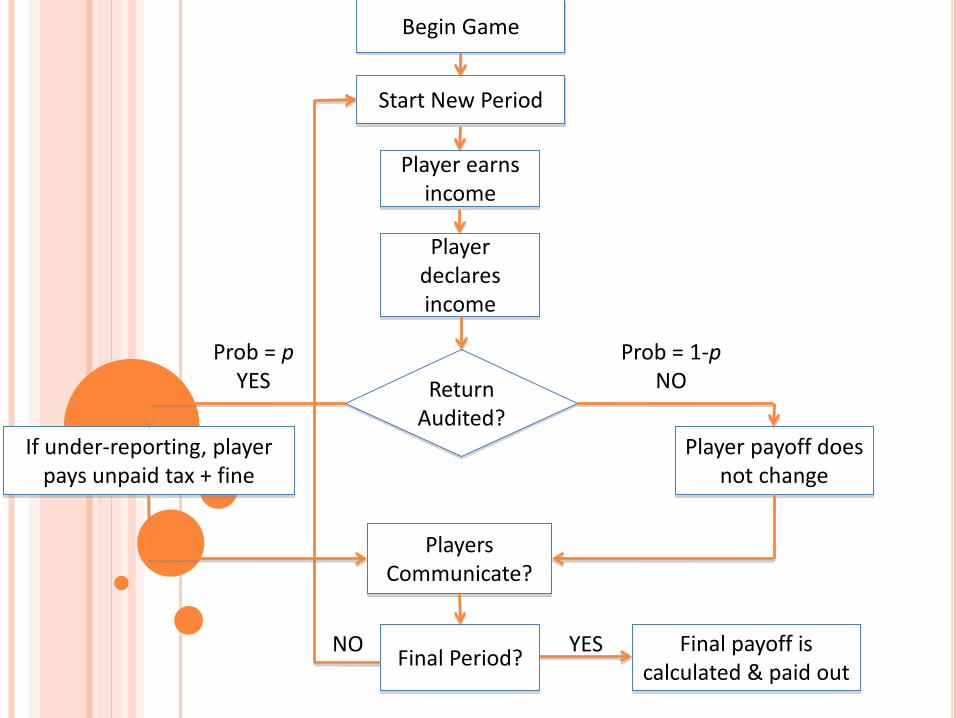

Begin Game

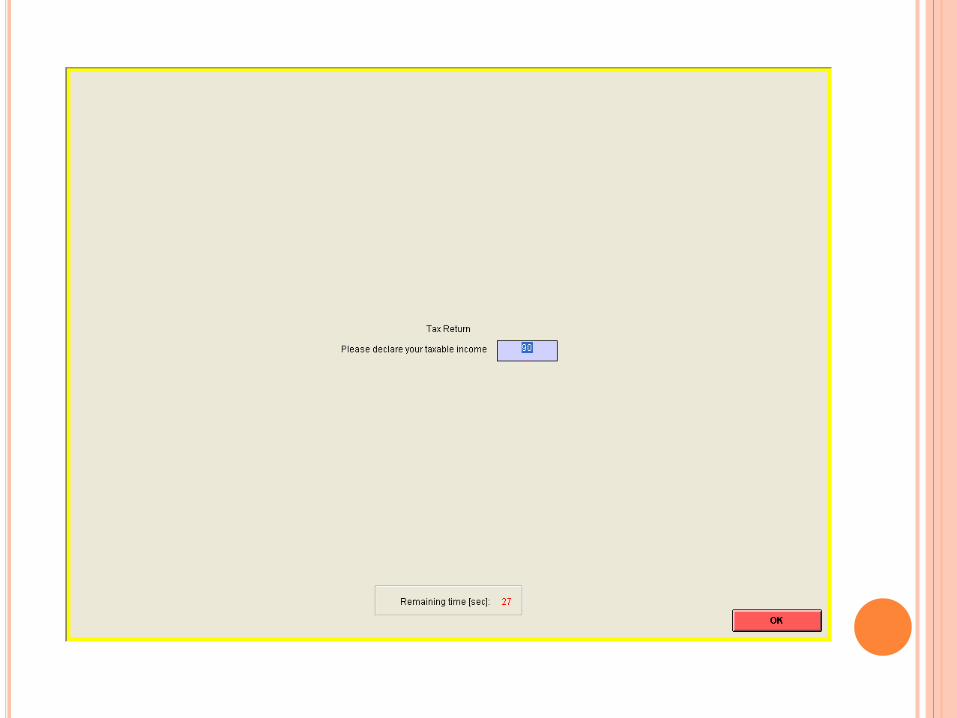

Start New Period

Player earns income

Player declares income

Return Audited?

If under-reporting, player pays unpaid tax + fine

Player payoff does not change

Players Communicate?

Final Period? Final payoff is calculated & paid out

YES NO

Prob = p YES

Prob = 1-p NO

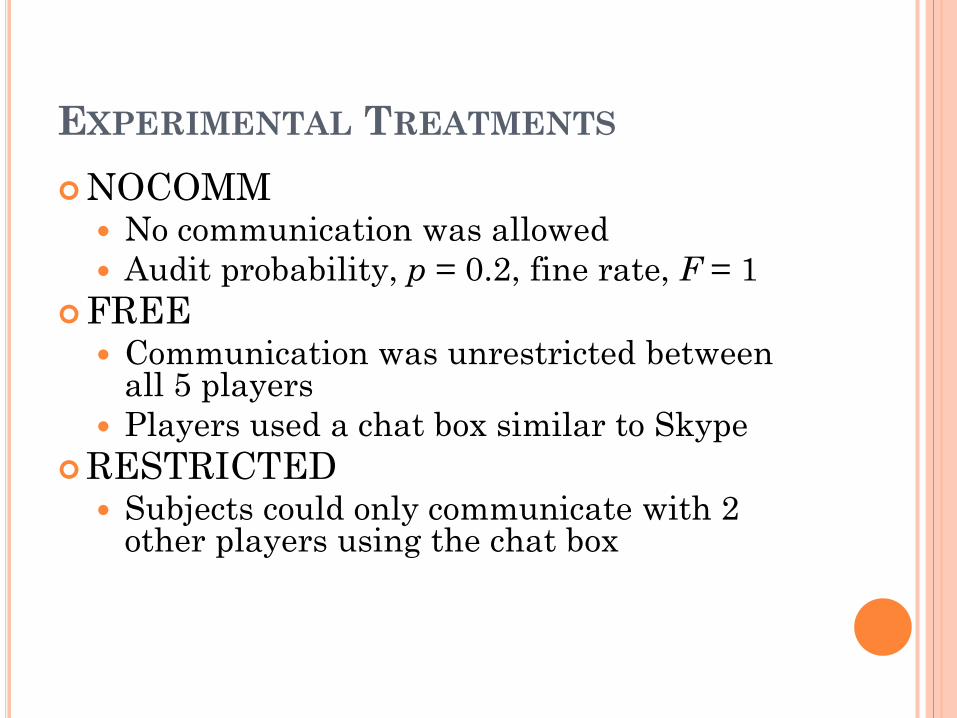

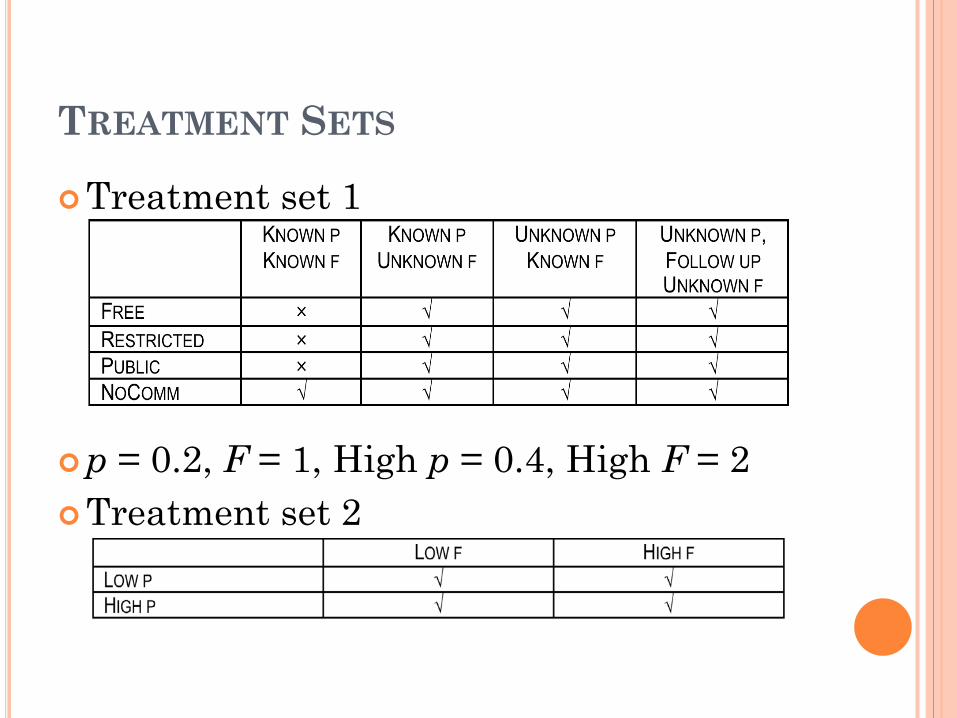

EXPERIMENTAL TREATMENTS NOCOMM

No communication was allowed Audit probability, p = 0.2, fine rate, F = 1

FREE Communication was unrestricted between

all 5 players Players used a chat box similar to Skype

RESTRICTED Subjects could only communicate with 2

other players using the chat box

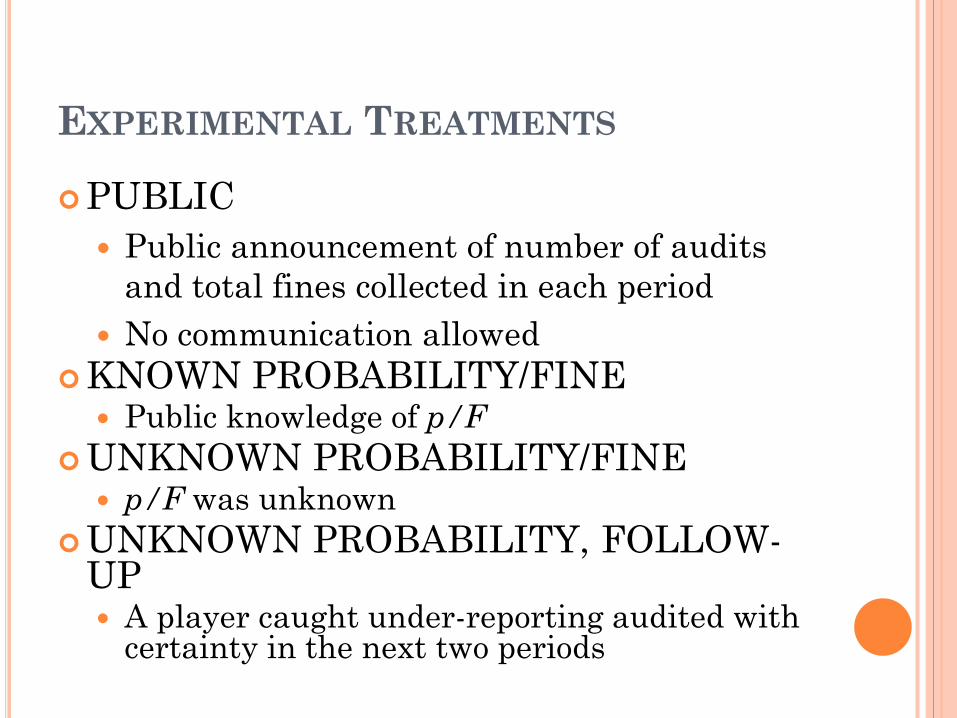

EXPERIMENTAL TREATMENTS

PUBLIC Public announcement of number of audits

and total fines collected in each period No communication allowed

KNOWN PROBABILITY/FINE Public knowledge of p/F

UNKNOWN PROBABILITY/FINE p/F was unknown

UNKNOWN PROBABILITY, FOLLOW-UP A player caught under-reporting audited with

certainty in the next two periods

TREATMENT SETS

Treatment set 1

p = 0.2, F = 1, High p = 0.4, High F = 2 Treatment set 2

OTHER INFORMATION We also collected information on financial

risk aversion Subjects had to pick between pairs of lotteries One lottery had extreme values (e.g.£7.70 and

.£0.20) The other had intermediate (e.g. £4 and £3.20)

Also collected data on personality traits: Extraversion, Agreeableness, Emotional

Stability, Conscientiousness, Openness Alaheto (2003) finds the first 3 traits

correlated with likelihood to commit white-collar crime.

SUBJECT POOL 500 Students

Students at the University of Exeter aged 18-61, 50% male.

Participated at the FEELE lab Average payment: £15.89

523 Workers UK tax residents aged 19-68, 50% male Participated at the FEELE lab (Exeter

residents, 22% of sample) or online (rest of the UK, 78%)

Average payment: £36.03

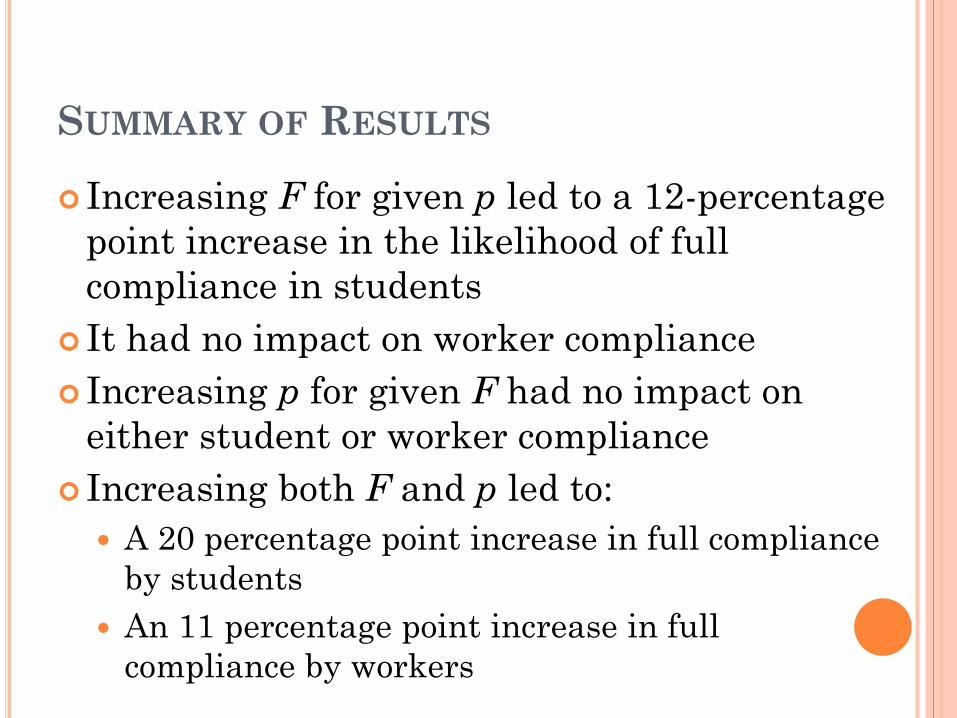

SUMMARY OF RESULTS

We found three significant differences between the two main samples:

1. Workers have significantly higher compliance rates than students

2. Students are more responsive to incentives than workers

3. Workers respond to information about fines, while students respond to information about audit rates

SUMMARY OF RESULTS

Social networks had very little impact on compliance but weak evidence that communication led to a higher rate of tax compliance among workers

Publicising aggregated information about evaders has no significant effect on compliance by workers or students

A known audit rate causes non-complying students to declare a lower proportion of their income but has no effect on worker compliance behaviour

SUMMARY OF RESULTS

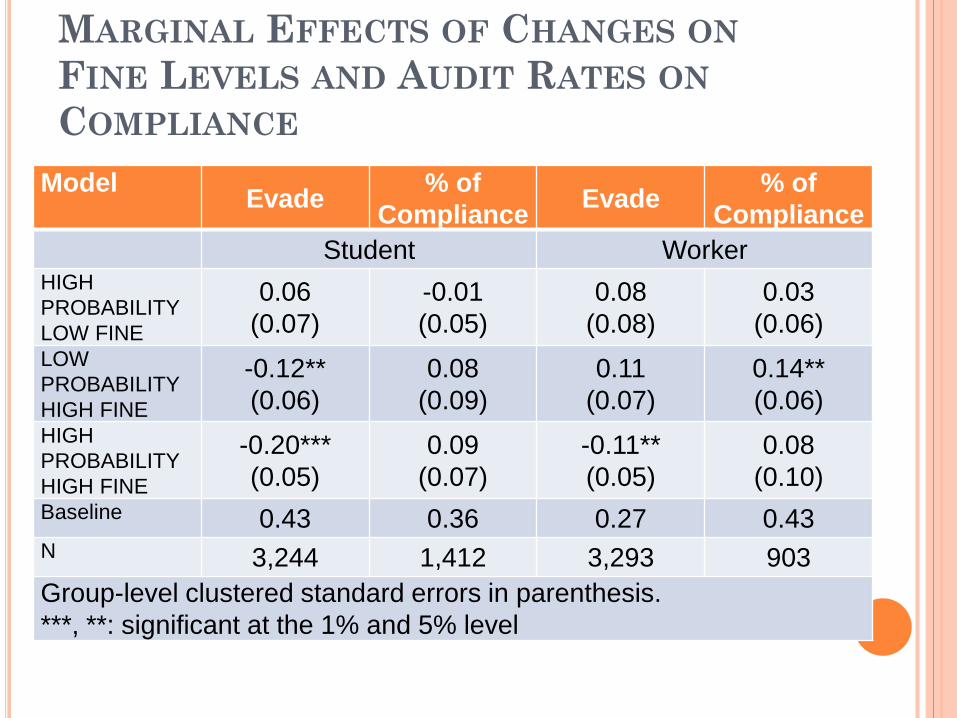

Increasing F for given p led to a 12-percentage point increase in the likelihood of full compliance in students

It had no impact on worker compliance Increasing p for given F had no impact on

either student or worker compliance Increasing both F and p led to:

A 20 percentage point increase in full compliance by students

An 11 percentage point increase in full compliance by workers

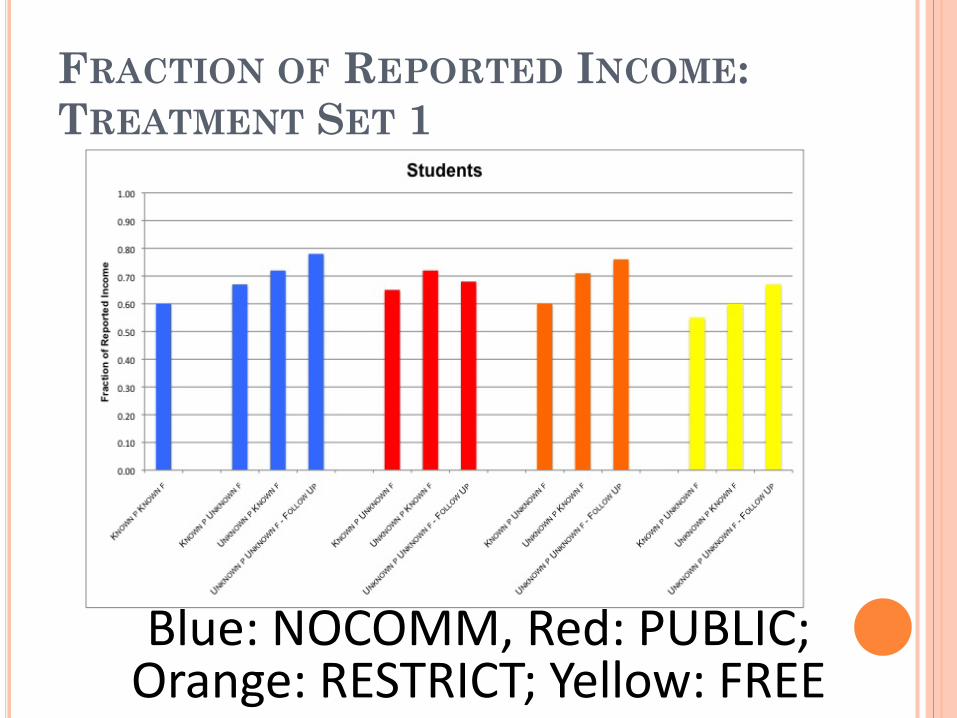

FRACTION OF REPORTED INCOME: TREATMENT SET 1

Blue: NOCOMM, Red: PUBLIC; Orange: RESTRICT; Yellow: FREE

FRACTION OF REPORTED INCOME: TREATMENT SET 1

Blue: NOCOMM, Red: PUBLIC; Orange: RESTRICT; Yellow: FREE

EFFECT OF CHANGING THE FINE SIZE AND THE AUDIT RATE

0,00

0,10

0,20

0,30

0,40

0,50

0,60

0,70

0,80

0,90

1,00

KNOWN P KNOWN F HIGH P LOW F LOW P HIGH F HIGH P HIGH F

Frac

tion

of R

epor

ted

Inco

me

Students

Workers

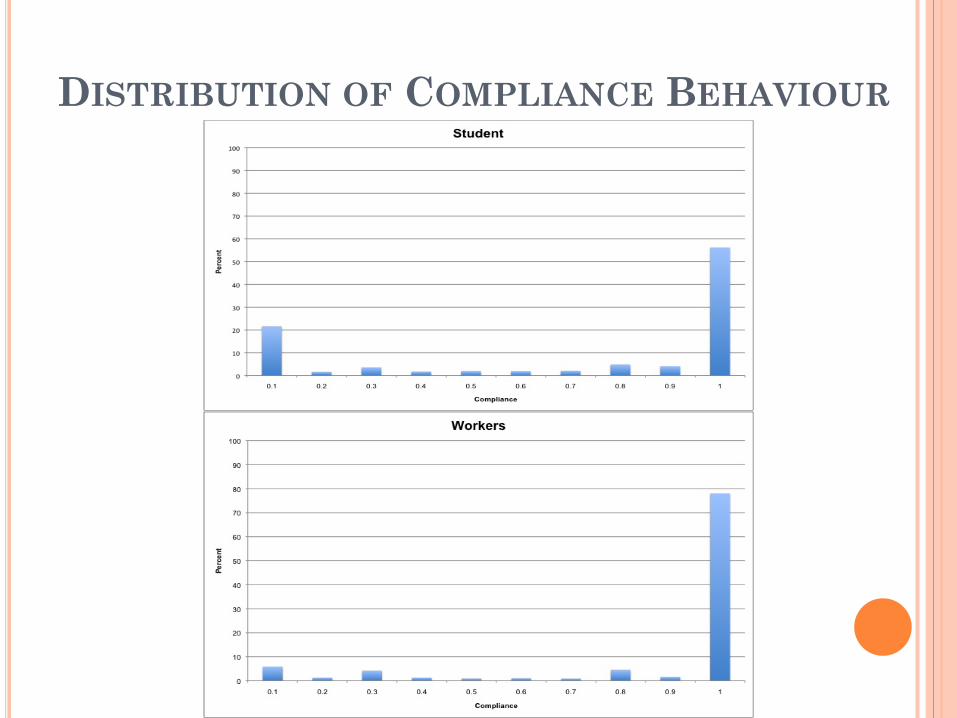

DISTRIBUTION OF COMPLIANCE BEHAVIOUR

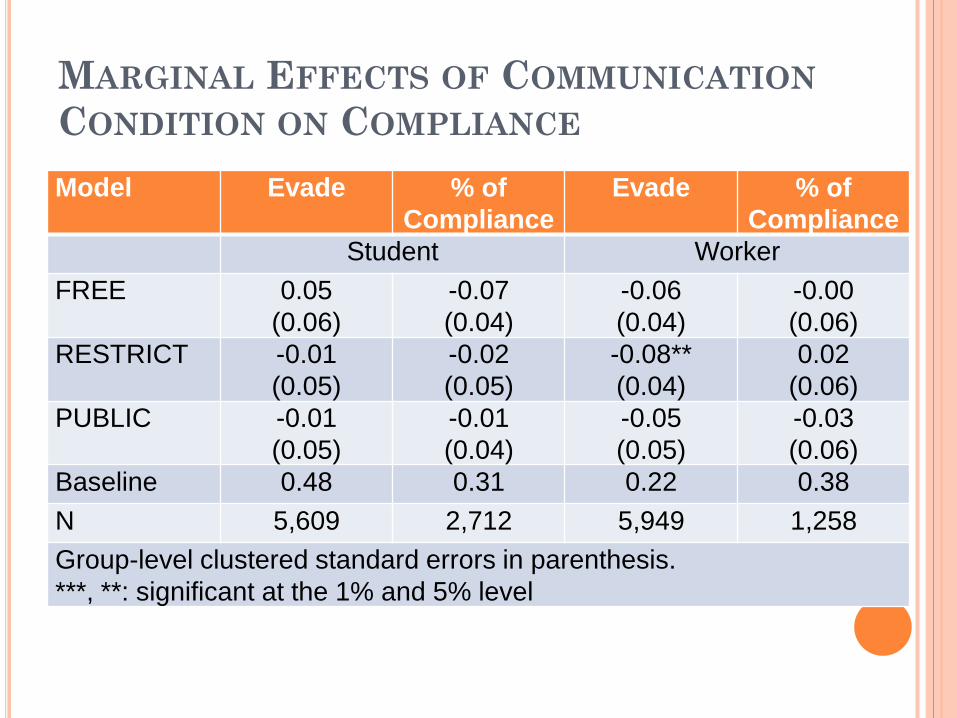

MARGINAL EFFECTS OF COMMUNICATION CONDITION ON COMPLIANCE Model Evade % of

Compliance Evade % of

Compliance Student Worker

FREE 0.05 (0.06)

-0.07 (0.04)

-0.06 (0.04)

-0.00 (0.06)

RESTRICT -0.01 (0.05)

-0.02 (0.05)

-0.08** (0.04)

0.02 (0.06)

PUBLIC -0.01 (0.05)

-0.01 (0.04)

-0.05 (0.05)

-0.03 (0.06)

Baseline 0.48 0.31 0.22 0.38 N 5,609 2,712 5,949 1,258 Group-level clustered standard errors in parenthesis. ***, **: significant at the 1% and 5% level

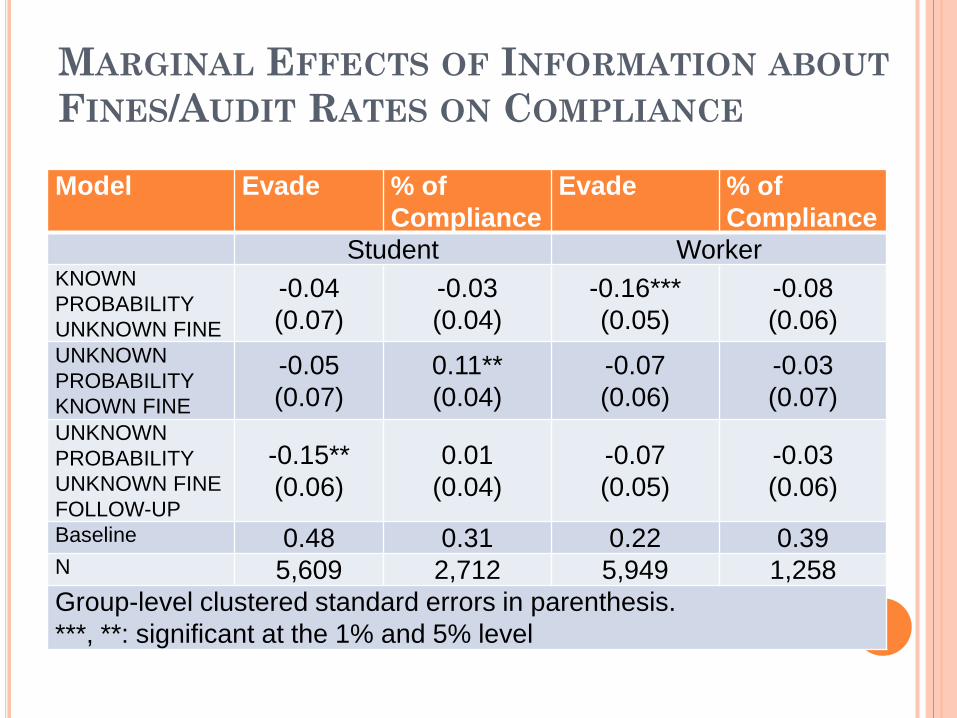

MARGINAL EFFECTS OF INFORMATION ABOUT FINES/AUDIT RATES ON COMPLIANCE

Model Evade % of Compliance

Evade % of Compliance

Student Worker KNOWN PROBABILITY UNKNOWN FINE

-0.04 (0.07)

-0.03 (0.04)

-0.16*** (0.05)

-0.08 (0.06)

UNKNOWN PROBABILITY KNOWN FINE

-0.05 (0.07)

0.11** (0.04)

-0.07 (0.06)

-0.03 (0.07)

UNKNOWN PROBABILITY UNKNOWN FINE FOLLOW-UP

-0.15** (0.06)

0.01 (0.04)

-0.07 (0.05)

-0.03 (0.06)

Baseline 0.48 0.31 0.22 0.39 N 5,609 2,712 5,949 1,258 Group-level clustered standard errors in parenthesis. ***, **: significant at the 1% and 5% level

MARGINAL EFFECTS OF CHANGES ON FINE LEVELS AND AUDIT RATES ON COMPLIANCE

Model Evade % of Compliance Evade % of

Compliance Student Worker

HIGH PROBABILITY LOW FINE

0.06 (0.07)

-0.01 (0.05)

0.08 (0.08)

0.03 (0.06)

LOW PROBABILITY HIGH FINE

-0.12** (0.06)

0.08 (0.09)

0.11 (0.07)

0.14** (0.06)

HIGH PROBABILITY HIGH FINE

-0.20*** (0.05)

0.09 (0.07)

-0.11** (0.05)

0.08 (0.10)

Baseline 0.43 0.36 0.27 0.43 N 3,244 1,412 3,293 903 Group-level clustered standard errors in parenthesis. ***, **: significant at the 1% and 5% level

OTHER FACTORS AFFECTING COMPLIANCE

1 extra ECU in taxable income resulted in a 0.5 (0.6) percentage point increase in declared income by workers (students)

Being audited but not caught in a given period significantly reduced the likelihood of evasion in the subsequent period 12 percentage points for students 7 percentage points for workers

OTHER FACTORS AFFECTING COMPLIANCE

Subjects audited and caught were more likely to evade in the following period than those who were audited and not caught because they had fully declared their income

The same applies to those audited and caught in the first five periods of the experiment

Risk aversion was not a significant predictor of tax compliance

IMPLICATIONS

Results support the behavioural perspective that individuals act on a subjective probability

A similar argument explains why awareness of the audit rate does not affect compliance behaviour

A joint increase of the audit rate and the fine rate was effective perhaps because of credibility

STUDENTS VS. WORKERS

Students were more responsive than workers to parameters changes E.g. level of fine for non-compliance and audit

rates We found the audit rate elasticity is close

to zero, while the fine elasticity is slightly above 0.1 Alm and Jacobson (2007) reported income-

audit rate elasticities of 0.1-0.2, and income-fine rates < 0.1

STUDENTS VS. WORKERS

Workers have a higher compliance rate in the experiment than students…

… but students are more responsive to the incentives than workers

Workers respond to changes in information about the fine rate…

… students respond to changes in information about the audit rate

ARE STUDENTS A GOOD SUBJECT POOL?

Our results suggest that students may not be ideally suited for tax compliance experiments

Students have had little or no socialisation in the process of tax payment They approach the experiment intending to

extract the maximum payoff This makes their behaviour conform more

closely to the traditional prediction

ARE STUDENTS A GOOD SUBJECT POOL?

In contrast, workers appear to have been socialised into the tax payment process

An explanation for the observed behaviour: They carry into the experiment the social

customs, beliefs, and norms of behaviour that they have adopted outside the lab

Their behaviour in the lab is insensitive to treatments because it is driven by longstanding attitudes and beliefs

CONCLUSIONS

Experiments can test theories and generate data

Good design is critical for success External validity is important especially if

results relevant for policy Tax experiments have produced a range of

results Most have had small student samples Students behave differently to workers Social custom model explains observations

FURTHER READING Alm, J., Cherry, T., Jones, M.L., and McKee, M. (2010)

"Taxpayer information assistance services and tax compliance behavior", Journal of Economic Psychology, 31, 577 - 586.

Alm, J., Cherry, T., and McKee, M., and Jones, M.L. (2009) "Encouraging filing via tax credits and social safety nets", The IRS Research Bulletin, Number 1500.

Alm, J., Cherry, T., and McKee, M., and Jones, M.L. (2010) "Investigating behavioral responses to positive inducements for filing tax returns", Working paper 10-11, Appalachian State University.

Alm, J., Cronshaw, M.B., and McKee, M. (1993) "Tax compliance with endogenous audit selection rules", Kyklos, 46, 27 - 45.

Alm, J., Deskins, J., and McKee, M. (2004) "Tax evasion and entrepreneurship: the effect of income reporting policies on evasion", Working paper, Georgia State University.

FURTHER READING Alm, J., Deskins, J., and McKee, M. (2007) "Do individuals

comply on income not reported by their employer", Working paper 07-34, Georgia State University.

Alm, J., Jackson, B.R., and McKee, M. (1992a) "Institutional uncertainty and taxpayer compliance", American Economic Review, 82, 1018 - 1026.

Alm, J., Jackson, B.R., and McKee, M. (1992b) "Estimating the Determinants of Taxpayer Compliance with Experimental Data", National Tax Journal, 45, 107 - 114.

Alm, J., Jackson, B.R., and McKee, M. (2009) "Getting the word out: enforcement information dissemination and compliance behavior", Journal of Public Economics, 93, 392 - 402.

Alm, J., McClelland, G.H., and Schulze, W.D. (1992) "Why do people pay taxes?" Journal of Public Economics, 48, 21 - 38.

FURTHER READING Alm, J. and McKee, M. (2004) "Tax compliance as a

coordination game", Journal of Economic Behavior and Organization, 54, 297 - 312.

Alm, J., McKee, M., and Beck, W. (1990) "Amazing grace: tax amnesties and tax compliance", National Tax Journal, 43, 23 - 37.

Barile, L. (2012) "Does tax evasion affect firms' internal control? Some evidence from an experimental approach", Labsi Working Papers, N.39.

Baldry, J.C. (1986) "Tax evasion is not a gamble", Economics Letters, 22, 333 - 335.

Bazart, C., and Pickhardt, M. (2009) "Fighting income tax evasion with positive rewards: experimental evidence", University of Montpellier Working Papers, No. 09-01.

Beck, P.J., Davis, J.S., and Jung, W.-O. (1991) "Experimental evidence on taxpayer reporting behaviour", The Accounting Review, 66, 535 - 558.

FURTHER READING Becker, W., Büchner, H.-J., and Sleeking, S. (1987) "The

impact of public transfer expenditures on tax evasion", Journal of Public Economics, 34, 243 - 252.

Collins, J.H. and Plumlee, R.D. (1991) "The taxpayer's labor and reporting decision: the effect of audit schemes", The Accounting Review, 66, 559 - 576.

Cummings, R.G., Martinez-Vazquez, J., McKee, M., and Torgler, B. (2005) "Effects of tax morale on tax compliance: experimental and survey evidence", Leitner Program Working Papers, No. 22.

Friedland, N. (1982) "A note on tax evasion as a function of the quality of information about the credibility of threatened fines: some preliminary research", Journal of Applied Social Psychology, 12, 54 - 59.

FURTHER READING Friedland, N., Maital, S. and Rutenberg, A. (1978) "A

simulation study of income taxation", Journal of Public Economics, 10, 107 - 116.

Gërxhani, K. (2007) "Explaining gender differences in tax evasion: the case of Tirana, Albania", Feminist Economics, 13, 119 - 155.

Gërxhani, K., and Schram, A. (2006) "Tax evasion and income source: a comparative experimental study", Journal of Economic Psychology, 27, 402 - 422.

Harrison, G.W., and List, J.A. (2004) "Field Experiments", Journal of Economic Literature, 42, 1009 - 1055.

Kastlunger, B., Muehlbacher, S., Kirchler, E., and Mittone, L. (2011) "What goes around comes around? Experimental evidence of the effect of rewards on tax compliance", Public Finance Review, 29, 150 - 167.

FURTHER READING Kleven, H.J., Knudesn, M.B., Kreiner, C.T., Pedersen, S., and

Saez, E. (2011) "Unwilling or unable to cheat? Evidence from a tax audit experiment in Denmark", Econometrica, 79, 651 - 692.

Martinez-Vazquez, J., Harwood, G.B., and Larkins, E.R. (1992) "Withholding position and income tax compliance: some experimental evidence", Public Finance Review, 20, 152 - 174.

Mittone, L. (2006) "Dynamic behaviour in tax evasion: an experimental approach", The Journal of Socio-Economics, 35, 813 - 835.

Slemrod, J., Blumenthal, M., and Christian, C. (2001) "Taxpayer response to an increased probability of audit: evidence from a controlled cxperiment in Minnesota", Journal of Public Economics, 79, 455 - 483.

Spicer, M.W. and Hero, R.E. (1985) "Tax evasion and heuristics: a research note", Journal of Public Economics, 26, 263 - 267.

FURTHER READING Spicer, M.W. and Thomas, J.E. (1982) "Audit probabilities and

the tax evasion decision: an experimental approach", Journal of Economic Psychology, 2, 241 - 245.

Wahl, I., Kastlunger, B., and Kirchler, E. (2010) "Trust in authorities and power to enforce tax compliance: an empirical analysis of the "slippery slope framework"", Law and Policy, 32, 383 - 406.