Embed Size (px)

Citation preview

PDS(Product Disclosure Statement)

PREPARED 01 APRIL 2021

Executive Super

1. About Executive Super..........................................................2

2. How super works............... ...................................................3

3. Benefits of investing with Executive Super..........................4

4. Risks of super............... ........................................................5

5. How we invest your money...................................................6

6. Fees and costs............... .......................................................8

7. How super is taxed............... ..............................................11

8. Insurance in your super............... .........................................12

9. How to open an account............... ......................................16

Forms included:Application for membership

2021

[ 2 ] EXECUTIVE SUPER PDS | 01 APRIL 2021

1. About Executive Super and this PDS

This Product Disclosure Statement explains the features and benefits of Intrust Super Executive Super.

Executive Super is our premium product, that caters to members who prefer a hands-on approach to their superannuation, with ten investment options and additional insurance cover.

You can find our product dashboard, director and executive remuneration details, Trust Deed and other information that we are required to disclose at intrust.com.au/regulatory-information-product-dashboard.

This PDS summarises significant information about Executive Super. It includes references to Other Important Information that is taken to form part of this PDS.

Important information is indicated throughout this PDS with this icon. As this Product Disclosure Statement is a summary, further detail regarding this information is in booklets called “Other Important Information”, which are available at intrust.com.au. Together with the PDS, the Other Important Information should be considered before investing in Executive Super.

The information provided in this PDS is general information only and does not take into account your individual objectives, financial situation or needs. You should consider the PDS and obtain financial advice tailored to your own personal circumstances before deciding to invest in Executive Super. Visit intrust360.com.au to find out about our financial advice services. To request a printed copy of this PDS or the Other Important Information referred to in this PDS call Intrust Super on 132 467. The information in the document is current at the date it is prepared and may change from time to time. The Trustee may provide updated information, including investment returns, by posting it on intrust.com.au.

Issued by IS Industry Fund Pty Ltd | MySuper Unique Identifier: 65704511371601 | ABN: 45 010 814 623 | AFSL No: 23801| RSE Licence No: L0001298 | Intrust Super ABN: 65 704 511 371 | USI/SPIN: HPP0100AU | RSE Registration No: R1004397.

IS Financial Planning Pty Ltd ABN 64 143 707 439 trading as Intrust360° is a wholly owned subsidiary of IS Industry Fund Pty Ltd. Intrust360° is a corporate authorised representative of Link Advice Pty Limited ABN: 36 105 811 836 | AFSL: 258145 | Corporate Authorised Representative Number: 379207.

2. How super worksYour superannuation grows from money regularly contributed to your account and any positive investment returns.

Contributions to superEmployer contributionsEmployers pay a compulsory contribution to your super known as the Superannuation Guarantee (SG). Currently this is an amount equal to 9.5% of your annual salary (subject to salary cap).

There are also other types of contributions that can grow your super:

Personal contributions

• Before tax (concessional)* – includes salary sacrifice contributions made by you, any personal contributions for which you claim a tax deduction and voluntary contributions made by your employer for which they claim a tax deduction.

• After tax (non-concessional)* – includes any extra additional contributions you make from your take-home pay, for which you don’t claim a tax deduction. After-tax contributions may also attract a Government Co-contribution depending on your income.

• Spouse contributions – you can contribute to your spouse’s super with either an after-tax or before-tax contribution. You may even receive a tax offset by helping them grow their super.

*Depending on your income and personal circumstances, you may be better off contributing before or after tax or using a combination of both. The Government places limits on the amount that can be contributed to super.

Choice of superMost people have the right to choose the superannuation fund their employer pays their SG contributions into (choice of fund). This PDS highlights the key features of Intrust Super Core Super | MySuper so you can easily compare it with other super funds and make sure it’s right for you. Intrust Super can accept contributions from any employer.

Consolidate your super accountsKeeping your super in one place helps reduce unnecessary multiple fees. Visit intrust.com.au/findmysuper/ to find and combine your super accounts today!*

*Before you consolidating, check the fees and benefits of the other fund(s) including any insurance cover you may lose. Seek advice if needed.

Accessing your superYou generally can’t access your super until you’ve reached your preservation age (which will be between 55 and 60, depending on when you were born). In extreme circumstances such as severe financial hardship, you may be able to withdraw some super earlier.

Please visit intrust.com.au/accessing-your-super for more information.

intrust.com.au | 132 467 [ 3 ]

[ 4 ] EXECUTIVE SUPER PDS | 01 APRIL 2021

3. Benefits of investing with Executive SuperWe’re here to help you maximise your super. The many benefits of Intrust Super Executive Super:

Super Concierge – your dedicated Account Manager waiting to help you with your Super. Register at intrust.com.au/super-concierge.

Online account and SuperCents apps – to track and grow your super.

A range of investment options to choose from, with a history of strong long-term performance.*

Multi-award-winning insurance options to protect you and your loved ones from financial stress.#

Intrust Super passes on the benefit of any tax deduction available to the Fund for insurance costs, to reduce your premiums.

Intrust360° – your financial advice solution, available whenever you need it – online with Super Blueprint, over the phone with Phone360° or face-to-face with Advice360°.^

Download SuperCents today!

Set up your online MemberAccess account at intrust.com.au/member-access

Pension Transfer Bonus - members who open a Super Stream** account could be eligible to receive thousands of extra dollars upon retirement.

*SuperRatings Fund Crediting Rate Survey – SR50 Balanced (60-76) Index February 2021. Past performance is no indication of future returns.#Awarded by Money magazine’s Best Value Insurance in Super from 2013-2018.

^There may be a fee for this service. Intrust360° is our financial planning business (its legal name is IS Financial Planning Pty Ltd ABN 64 143 707 439). It’s a wholly owned subsidiary of IS Industry Fund Pty Ltd ABN: 45 010 814 623. It’s also a corporate authorised representative of Link Advice Pty Limited ABN: 36 105 811 836 | AFSL: 258145 | Corporate Authorised Representative Number: 379207.

**Please refer to the Super Stream PDS available at intrust.com.au for further information.

intrust.com.au | 132 467 [ 5 ]

4. Risks of superAll investments carry some risk.

Each person’s risk appetite will vary depending on factors including their age, investment time-frame, other investments and their risk tolerance. Having sufficient time invested in the market is an important consideration when choosing investments with different levels of risk.

The risks associated with superannuation include:

• The value of investment options will rise and fall over time. Investment performance is not guaranteed, and you might lose money. Future returns may differ from past returns. The options with the higher expected long-term returns generally involve higher levels of risk and therefore a higher chance of short-term negative returns. In addition, in a low interest rate environment, investments which are traditionally perceived as low risk, (particularly investments in cash and associated investment options), may attract very low or even negative returns for a period of time. There is a risk that investments in these options may result in your fees and any other deductions from your superannuation account exceeding any gains made through the investment for a limited period.

• Laws affecting super (such as superannuation laws, taxation and social security) may change at any time.

• The amount you save may not be enough to provide adequately for your retirement.

• Inflation may erode the final value of your investment.

• It may not be possible at all times to immediately convert your investments to cash. Intrust Super is aware of this risk and manages its investments and cash holdings to maintain adequate liquidity.

• Some options invest in overseas investments, which means fluctuations in currencies could impact unit prices.

[ 6 ] EXECUTIVE SUPER PDS | 01 APRIL 2021

5. How we invest your moneyYou can choose any combination of our options listed below:

Pre-mixed options Single sector options

• Balanced• Growth• Combined shares• Conservative• Stable

• Australian shares• International shares• Property• Bonds (fixed interest)• Cash

When joining Executive Super, you must complete the Investment Choice section in the Membership Application to indicate your investment choice which must add up to 100%. You should consider the likely return, risk and your investment timeframe when choosing investment options.

Balanced investment optionThe Balanced investment option is designed for members seeking high returns with an investment timeframe of medium to long term, who are willing to accept some volatility.

Investment objective

To outperform (after fees and taxes) the consumer price index + 3% per annum over rolling ten year periods.

Investment mix

Asset Allocation Benchmark % Range %Australian shares 24 15-35International shares 28 15-35Growth opportunities 5 0-10Infrastructure 10 0-20Property 10 5-20Bonds 10 0-30Cash 4 0-30Defensive opportunities 9 0-20

intrust.com.au | 132 467 [ 7 ]

Minimum investment timeframe: Medium to long term: Be prepared to stay invested in this option for at least five years. Under the industry “Standard Risk Measure”* this option falls into Risk Band 5.

Risk band 5: Medium to high. The estimated number of negative annual returns is three to less than four over any 20 year period.

Members will be notified of any material changes that occur to the Balanced option or any other investment option.

For more information please read “Executive Super Other Important Information – Investments” document.

*Superannuation funds are required to disclose the level of risk using the industry Standard Risk Measure for the purposes of comparing the risk attributes of investment options.

Changing your investment optionsYou can choose or switch investments as often as you like through MemberAccess at no cost to you. Switches are processed daily. If you need help choosing investments call us on 132 467. We’ll put you in touch with a qualified financial adviser.

You should read the document: “Executive Super Other Important Information – Investments” regarding all of Executive Super’s investments before making a decision. This material about investments may change between the time you read this PDS and when you acquire the product. Visit intrust.com.au.

Responsible investmentIntrust Super Fund aims to maximise the purchasing power of members’ retirement savings. The Fund believes that asset allocation is the key lever for managing short-term volatility and also the risk of whether long-term returns will be sufficient to meet members’ retirement goals. All investment options must be of a high quality, transparent, easy to understand and represent excellent value for money for members.

The Board’s Investment Governance Policy provides a sound governance framework to manage investments in a manner consistent with promoting the interests of Intrust Super members. Environmental, Social and Corporate Governance (ESG) factors relate to the impact that an investment has on people, communities, and the environment. Considering these factors ensures a greater understanding of an asset’s risks and opportunities and can have a material impact on long-term investment outcomes. To be meaningful and effective, the consideration of ESG factors should be integrated into the investment decision making processes across the Fund. To do this, Intrust Super leverages the specialist skills and resources of its Asset Consultant, JANA, and external global investment managers. An integrated approach is taken to the consideration of ESG factors, including climate change, in its investment research and advice processes.

[ 8 ] EXECUTIVE SUPER PDS | 01 APRIL 2021

6. Fees and costsThe following warning is prescribed by Government legislation

Did you know?Small differences in both investment performance and fees and costs can have a substantial impact on your long-term returns.

For example, total annual fees and costs of 2% of your fund balance rather than 1% could reduce your final return by up to 20% over a 30-year period (for example, reduce it from $100,000 to $80,000).

You should consider whether features such as superior investment performance or the provision of better member services justify higher fees and costs. You may be able to negotiate to pay lower contribution fees and management costs where applicable. Ask the fund or your financial adviser.

To find out moreIf you would like to find out more, or see the impact of the fees based on your own circumstances, the Australian Securities and Investments Commission (ASIC) website (www.moneysmart.gov.au) has a superannuation calculator to help you check out different fee options.

You should read the document: “Executive Super Other Important Information - Fees and Costs” regarding all of Executive Super’s fees including the Balanced option, before making a decision. This material about fees and costs may change between the time you read this PDS and when you become a member. Visit intrust.com.au.

The table on page 9 shows the fees and other costs that you may be charged and can be used to compare costs between different superannuation products. These fees and costs may be deducted from your account or from the returns on your investment.

Please note: Intrust Super does not negotiate fees.

intrust.com.au | 132 467 [ 9 ]

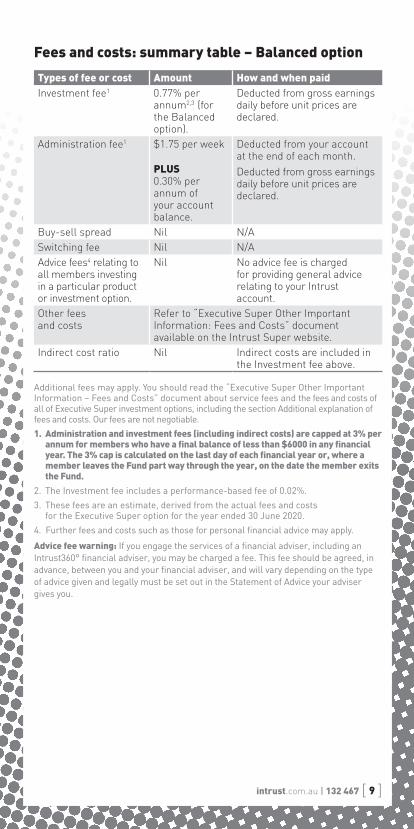

Fees and costs: summary table – Balanced option

Types of fee or cost Amount How and when paidInvestment feeInvestment fee11 0.77% per 0.77% per

annumannum2,3 2,3 (for (for the Balanced the Balanced option).option).

Deducted from gross earnings Deducted from gross earnings daily before unit prices are daily before unit prices are declared. declared.

Administration feeAdministration fee11

$1.75 per week$1.75 per week

PLUS 0.30% per 0.30% per annum of annum of your account your account balance.balance.

Deducted from your account Deducted from your account at the end of each month.at the end of each month.Deducted from gross earnings Deducted from gross earnings daily before unit prices are daily before unit prices are declared. declared.

Buy-sell spreadBuy-sell spread NilNil N/AN/ASwitching feeSwitching fee NilNil N/AN/AAdvice feesAdvice fees44 relating to relating to all members investing all members investing in a particular product in a particular product or investment option.or investment option.

NilNil No advice fee is charged No advice fee is charged for providing general advice for providing general advice relating to your Intrust relating to your Intrust account.account.

Other fees Other fees and costsand costs

Refer to “Executive Super Other Important Refer to “Executive Super Other Important Information: Fees and Costs” document Information: Fees and Costs” document available on the available on the Intrust Super website.Intrust Super website.

Indirect cost ratioIndirect cost ratio NilNil Indirect costs are included in Indirect costs are included in the Investment fee above.the Investment fee above.

Additional fees may apply. You should read the “Executive Super Other Important Information – Fees and Costs” document about service fees and the fees and costs of all of Executive Super investment options, including the section Additional explanation of fees and costs. Our fees are not negotiable.

1. Administration and investment fees (including indirect costs) are capped at 3% per annum for members who have a final balance of less than $6000 in any financial year. The 3% cap is calculated on the last day of each financial year or, where a member leaves the Fund part way through the year, on the date the member exits the Fund.

2. The Investment fee includes a performance-based fee of 0.02%.

3. These fees are an estimate, derived from the actual fees and costs for the Executive Super option for the year ended 30 June 2020.

4. Further fees and costs such as those for personal financial advice may apply.

Advice fee warning: If you engage the services of a financial adviser, including an Intrust360° financial adviser, you may be charged a fee. This fee should be agreed, in advance, between you and your financial adviser, and will vary depending on the type of advice given and legally must be set out in the Statement of Advice your adviser gives you.

[ 10 ] EXECUTIVE SUPER PDS | 01 APRIL 2021

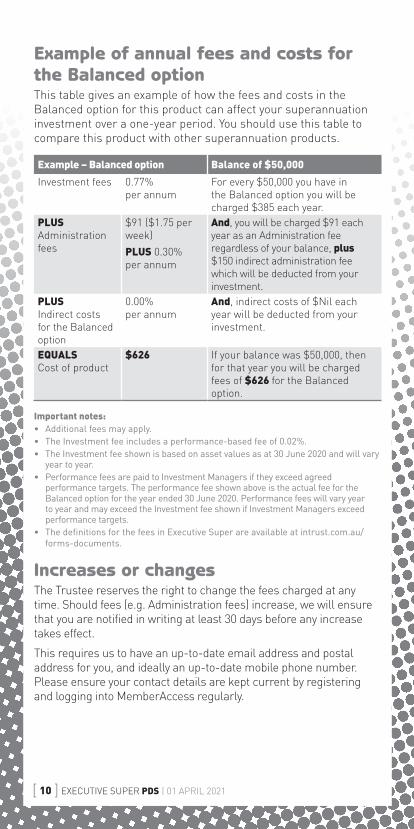

Example of annual fees and costs for the Balanced optionThis table gives an example of how the fees and costs in the Balanced option for this product can affect your superannuation investment over a one-year period. You should use this table to compare this product with other superannuation products.

Example – Balanced option Balance of $50,000

Investment fees 0.77% per annum

For every $50,000 you have in the Balanced option you will be charged $385 each year.

PLUS Administration fees

$91 ($1.75 per week)

PLUS 0.30% per annum

And, you will be charged $91 each year as an Administration fee regardless of your balance, plus $150 indirect administration fee which will be deducted from your investment.

PLUS Indirect costs for the Balanced option

0.00% per annum

And, indirect costs of $Nil each year will be deducted from your investment.

EQUALS Cost of product

$626 If your balance was $50,000, then for that year you will be charged fees of $626 for the Balanced option.

Important notes:• Additional fees may apply.• The Investment fee includes a performance-based fee of 0.02%.• The Investment fee shown is based on asset values as at 30 June 2020 and will vary

year to year. • Performance fees are paid to Investment Managers if they exceed agreed

performance targets. The performance fee shown above is the actual fee for the Balanced option for the year ended 30 June 2020. Performance fees will vary year to year and may exceed the Investment fee shown if Investment Managers exceed performance targets.

• The definitions for the fees in Executive Super are available at intrust.com.au/forms-documents.

Increases or changesThe Trustee reserves the right to change the fees charged at any time. Should fees (e.g. Administration fees) increase, we will ensure that you are notified in writing at least 30 days before any increase takes effect.

This requires us to have an up-to-date email address and postal address for you, and ideally an up-to-date mobile phone number. Please ensure your contact details are kept current by registering and logging into MemberAccess regularly.

intrust.com.au | 132 467 [ 11 ]

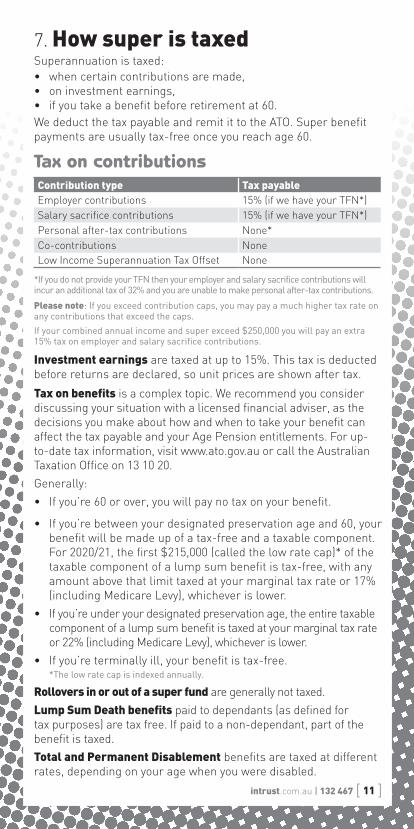

7. How super is taxedSuperannuation is taxed:• when certain contributions are made, • on investment earnings, • if you take a benefit before retirement at 60.We deduct the tax payable and remit it to the ATO. Super benefit payments are usually tax-free once you reach age 60.

Tax on contributionsContribution type Tax payableEmployer contributions 15% (if we have your TFN*)Salary sacrifice contributions 15% (if we have your TFN*)Personal after-tax contributions None*Co-contributions NoneLow Income Superannuation Tax Offset None

*If you do not provide your TFN then your employer and salary sacrifice contributions will incur an additional tax of 32% and you are unable to make personal after-tax contributions.

Please note: If you exceed contribution caps, you may pay a much higher tax rate on any contributions that exceed the caps.

If your combined annual income and super exceed $250,000 you will pay an extra 15% tax on employer and salary sacrifice contributions.

Investment earnings are taxed at up to 15%. This tax is deducted before returns are declared, so unit prices are shown after tax.

Tax on benefits is a complex topic. We recommend you consider discussing your situation with a licensed financial adviser, as the decisions you make about how and when to take your benefit can affect the tax payable and your Age Pension entitlements. For up-to-date tax information, visit www.ato.gov.au or call the Australian Taxation Office on 13 10 20.

Generally:

• If you’re 60 or over, you will pay no tax on your benefit.

• If you’re between your designated preservation age and 60, your benefit will be made up of a tax-free and a taxable component. For 2020/21, the first $215,000 (called the low rate cap)* of the taxable component of a lump sum benefit is tax-free, with any amount above that limit taxed at your marginal tax rate or 17% (including Medicare Levy), whichever is lower.

• If you’re under your designated preservation age, the entire taxable component of a lump sum benefit is taxed at your marginal tax rate or 22% (including Medicare Levy), whichever is lower.

• If you’re terminally ill, your benefit is tax-free. *The low rate cap is indexed annually.

Rollovers in or out of a super fund are generally not taxed.

Lump Sum Death benefits paid to dependants (as defined for tax purposes) are tax free. If paid to a non-dependant, part of the benefit is taxed.

Total and Permanent Disablement benefits are taxed at different rates, depending on your age when you were disabled.

[ 12 ] EXECUTIVE SUPER PDS | 01 APRIL 2021

8. Insurance in your superEligible members will automatically receive the below insurance cover subject to meeting the Putting Members’ Interests First (PMIF) Eligibility Conditions (age limits and other conditions apply*). This cover provides a basic level of protection if you die, or become ill or injured.

• PayGuard Income Protection – can provide fortnightly payments if you become sick or injured and can’t work temporarily.

• Life cover – can provide a lump sum to you if you are terminally ill or to your beneficiaries if you die.

• Total & Permanent Disablement (TPD) cover – can provide a lump sum payment if you become totally and permanently disabled and can no longer work.

*Members who are under the age of 25 and have an account balance under $6,000 will not receive Life and TPD cover automatically until they satisfy this requirement (PMIF Eligibility Conditions) but can opt into Default Cover within 180 days of being First Eligible. Cover is Limited Cover until you satisfy an Active Employment requirement. Refer to the “Executive Super Other Important Information - Insurance” document for the definition of First Eligible, Limited Cover and other eligibility requirements.

You should read the document: “Executive Super Other Important Information – Insurance” regarding all of Executive Super’s insurance before making a decision. This material about insurance may change between the time you read this PDS and when you acquire the product. Visit intrust.com.au.

PayGuard Income Protection Insurance PayGuard provides a fortnightly in-arrears benefit of up to 90% of the income you received before you became sick or injured, plus an additional 10% of the benefit paid into your super, for up to two years (104 weeks)*. PayGuard default premiums are calculated as follows:

Waiting period Premium21 days (default) 0.615% of your income30 days 0.556% of your income45 days 0.496% of your income90 days 0.377% of your income

Your insurance premiums are used to cover the cost of the insurance policy as well as the cost of its administration, i.e. 3% of the insurance premiums are retained by the Fund and go towards the administration cost of providing insurance.

*The maximum benefit period for a disablement caused by a Mental Condition is 52 weeks.

intrust.com.au | 132 467 [ 13 ]

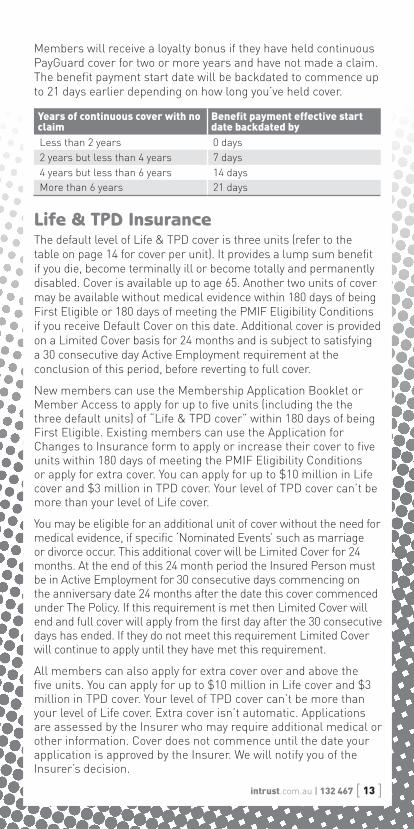

Members will receive a loyalty bonus if they have held continuous PayGuard cover for two or more years and have not made a claim. The benefit payment start date will be backdated to commence up to 21 days earlier depending on how long you’ve held cover.

Years of continuous cover with no claim

Benefit payment effective start date backdated by

Less than 2 years 0 days2 years but less than 4 years 7 days4 years but less than 6 years 14 daysMore than 6 years 21 days

Life & TPD InsuranceThe default level of Life & TPD cover is three units (refer to the table on page 14 for cover per unit). It provides a lump sum benefit if you die, become terminally ill or become totally and permanently disabled. Cover is available up to age 65. Another two units of cover may be available without medical evidence within 180 days of being First Eligible or 180 days of meeting the PMIF Eligibility Conditions if you receive Default Cover on this date. Additional cover is provided on a Limited Cover basis for 24 months and is subject to satisfying a 30 consecutive day Active Employment requirement at the conclusion of this period, before reverting to full cover.

New members can use the Membership Application Booklet or Member Access to apply for up to five units (including the the three default units) of “Life & TPD cover” within 180 days of being First Eligible. Existing members can use the Application for Changes to Insurance form to apply or increase their cover to five units within 180 days of meeting the PMIF Eligibility Conditions

or apply for extra cover. You can apply for up to $10 million in Life cover and $3 million in TPD cover. Your level of TPD cover can’t be more than your level of Life cover.

You may be eligible for an additional unit of cover without the need for medical evidence, if specific ‘Nominated Events’ such as marriage or divorce occur. This additional cover will be Limited Cover for 24 months. At the end of this 24 month period the Insured Person must be in Active Employment for 30 consecutive days commencing on the anniversary date 24 months after the date this cover commenced under The Policy. If this requirement is met then Limited Cover will end and full cover will apply from the first day after the 30 consecutive days has ended. If they do not meet this requirement Limited Cover will continue to apply until they have met this requirement.

All members can also apply for extra cover over and above the five units. You can apply for up to $10 million in Life cover and $3 million in TPD cover. Your level of TPD cover can’t be more than your level of Life cover. Extra cover isn’t automatic. Applications are assessed by the Insurer who may require additional medical or other information. Cover does not commence until the date your application is approved by the Insurer. We will notify you of the Insurer’s decision.

[ 14 ] EXECUTIVE SUPER PDS | 01 APRIL 2021

Age last birthday Cover per unit16 to 39 $150,00040 $141,60041 $134,50042 $127,30043 $120,10044 $113,00045 $105,80046 $98,70047 $91,50048 $84,50049 $77,30050 $70,20051 $63,10052 $56,00053 $48,80054 $41,60055 $38,10056 $34,50057 $30,90058 $27,30059 $23,70060 $20,20061 $16,60062 $13,00063 $9,40064 $5,80065 Nil

Cost of Life & TPD insurance coverYour premium for Life & TPD cover will vary depending on your age, sex, whether you smoke or not, and the type of cover you choose. Premium rates range from $0.15 (Life insurance only for a female non-smoker up to 21 years of age) to $19.98 (Life & TPD insurance for a 64 year-old male smoker).* *Cost is annual premium per $1,000 of cover

Value of one unit of Life & TPD insurance cover by age

For full details of restrictions and eligibility conditions, examples of ‘Nominated Events’ and information you need to decide whether additional units are appropriate for you, read the “Executive Super Other Important Information – Insurance” document available at intrust.com.au.

intrust.com.au | 132 467 [ 15 ]

Paying for insuranceThe cost of both Life & TPD and PayGuard insurance is deducted from your Executive Super account each month. If you don’t want this cover, just indicate on your membership application form that you do not wish to take it up. You can also cancel or reduce cover by writing to Intrust Super at any time.

If you do not change or cancel your default cover, the Trustee will continue to deduct premiums for your default insurance cover from your account unless your account becomes inactive, refer to ‘Cancellation of inactive insurance’ below for further details.

Eligibility conditions and exclusionsThe insurance cover provided under Executive Super is subject to eligibility conditions and exclusions. These may affect your entitlements to insurance cover or the circumstances when an insurance benefit may be payable under the Policy.

Eligibility extends to Putting Members’ Interests First legislation which prevents us from providing insurance cover to members under the age of 25 years of age or members with an account balance under $6,000.

Cancellation of inactive insurancePlease note that Life & TPD cover will automatically be cancelled where your account is deemed to be ‘inactive’ under Government legislation. To avoid this, please ensure you make a contribution or rollover at least every 16 months, or nominate to retain this insurance by notifying the Fund, in writing, in advance. Intrust Super will notify you of the likely cancellation of your insurance cover in advance of its cancellation. Refer to the “Executive Super Other Important Information – Insurance” for further information.

BeneficiariesYou can nominate who receives your death benefit when completing a member application on the form provided or in MemberAccess. You can make a preferred, or a binding nomination. There are laws regarding who you can nominate. Go to intrust.com.au/beneficiaries for more information.

[ 16 ] EXECUTIVE SUPER PDS | 01 APRIL 2021

9. How to open an account1. Read this PDS and the following booklets:

• “Executive Super Other Important Information – Fees and Costs”

• “Executive Super Other Important Information – Investments”

• “Executive Super Other Important Information – Insurance”

These booklets contain important details about Executive Super. If you need advice tailored to your personal situation, speak with a licensed financial adviser. Visit intrust360.com.au to find out more about these services.

2. Complete the membership application which accompanies this PDS, or join online at intrust.com.au.

3. Return your completed membership application to Intrust Super. On joining Executive Super, you will receive a welcome pack and your member number.

Cooling-off periodA 14-day cooling off period only applies if you have made the choice to be an Intrust Super member yourself. During this period, you may write to the Trustee to cancel your membership and have any contributions transferred to a complying super fund, approved deposit fund or retirement savings account of your choice. We will not deduct fees from the repayment, however, the balance may be adjusted to take into account any positive or negative investment earnings and taxes payable.

ComplaintsWe aim to deal with enquiries and any complaints as quickly and effectively as possible. Please contact us using the details below to discuss your complaint:

Email [email protected] 132 467In writing Intrust Super

GPO Box 1416 Brisbane QLD 4001

We will do our best to acknowledge all complaints in writing within one working day of receipt. We aim to resolve all complaints within five working days where possible. In all other cases, we will resolve complaints within a maximum of 90 days.

intrust.com.au | 132 467 [ 17 ]

If an issue is not resolved to your satisfaction, you can lodge a complaint with the Australian Financial Complaints Authority (AFCA). AFCA has been set up by the Federal Government to provide fair and independent financial services complaint resolution that is free to consumers.

Web [email protected] Email [email protected] 1800 931 678 (free call) In writing Australian Financial Complaints Authority

GPO Box 3 Melbourne VIC 3001

Protect your super from being transferred to the ATO Lost Accounts. The Australian Taxation Office (ATO) takes control of superannuation accounts deemed as ‘lost’ every year. Please keep your details (phone number, email & address) up to date and inform your employer of your Intrust Super member number to ensure you receive all your membership benefits and don’t become ‘lost’. You can also opt in for SuperMatch and electronic communications, which enables us to search for lost super, stay in contact with you and avoid returned mail. You can do this via the membership application form, or by contacting us directly.

Inactive Accounts. To ensure accounts aren’t inappropriately eroded by fees, we are required to transfer accounts to the ATO if the account is below $6,000 and is inactive for 16 months. If this is likely to occur and you would like your account to remain ‘active’ you can take one of the following steps:

• make a contribution, or regular contributions, to your Intrust Super account;

• rollover one or more accounts held with another superannuation fund to Intrust Super*;

• make or change a binding beneficiary nomination;• review and change your investments options or insurance

cover; or• advise the ATO, in writing, that you are not a member of an

inactive low-balance account.

*You should consider comparative fees and benefits, including the impact on your insurance cover, before consolidating superannuation accounts.

Respecting your privacyProtecting your personal information is important to Intrust Super and is also a legal requirement. Our privacy policy outlines the type of information we will keep about you. It explains how we, and any organisation we appoint to provide services to you on our behalf, will use this information. For more information about our privacy policy and the way we handle your personal information, visit intrust.com.au/privacy-policy/.

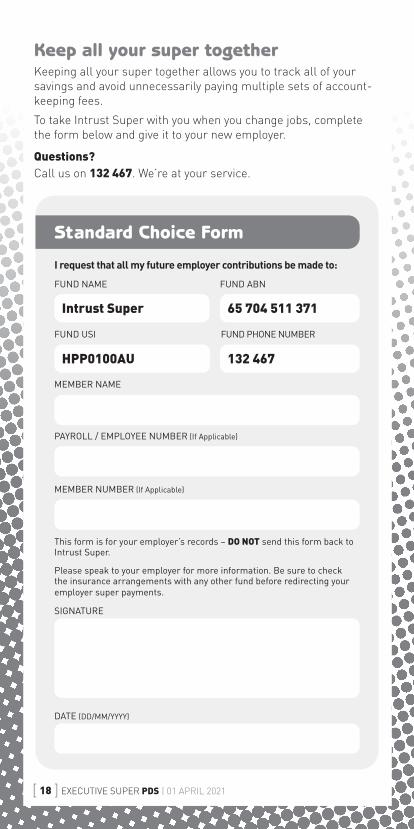

I request that all my future employer contributions be made to:

FUND NAME FUND ABN

FUND USI FUND PHONE NUMBER

MEMBER NAME

PAYROLL / EMPLOYEE NUMBER (If Applicable)

MEMBER NUMBER (If Applicable)

This form is for your employer’s records – DO NOT send this form back to Intrust Super.

Please speak to your employer for more information. Be sure to check the insurance arrangements with any other fund before redirecting your employer super payments.

SIGNATURE

DATE (DD/MM/YYYY)

Standard Choice Form

65 704 511 371

132 467HPP0100AU

Intrust Super

Keep all your super togetherKeeping all your super together allows you to track all of your savings and avoid unnecessarily paying multiple sets of account-keeping fees.

To take Intrust Super with you when you change jobs, complete the form below and give it to your new employer.

Questions?Call us on 132 467. We’re at your service.

[ 18 ] EXECUTIVE SUPER PDS | 01 APRIL 2021

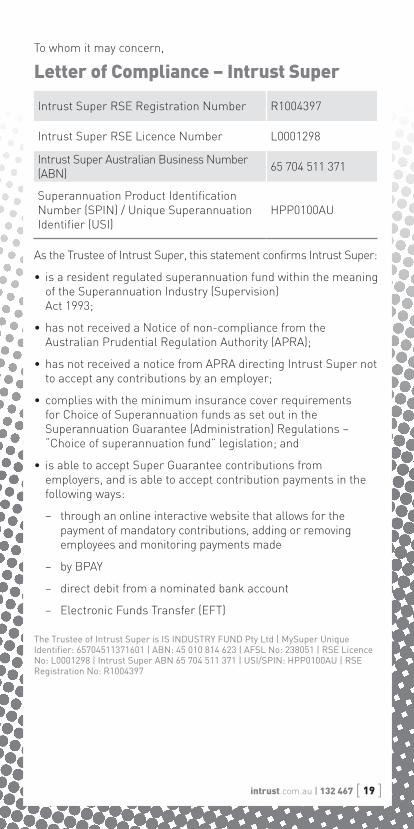

To whom it may concern,

Letter of Compliance – Intrust Super

Intrust Super RSE Registration Number R1004397

Intrust Super RSE Licence Number L0001298

Intrust Super Australian Business Number (ABN) 65 704 511 371

Superannuation Product Identification Number (SPIN) / Unique Superannuation Identifier (USI)

HPP0100AU

As the Trustee of Intrust Super, this statement confirms Intrust Super:

• is a resident regulated superannuation fund within the meaning of the Superannuation Industry (Supervision) Act 1993;

• has not received a Notice of non-compliance from the Australian Prudential Regulation Authority (APRA);

• has not received a notice from APRA directing Intrust Super not to accept any contributions by an employer;

• complies with the minimum insurance cover requirements for Choice of Superannuation funds as set out in the Superannuation Guarantee (Administration) Regulations – “Choice of superannuation fund” legislation; and

• is able to accept Super Guarantee contributions from employers, and is able to accept contribution payments in the following ways:

– through an online interactive website that allows for the payment of mandatory contributions, adding or removing employees and monitoring payments made

– by BPAY

– direct debit from a nominated bank account

– Electronic Funds Transfer (EFT)

The Trustee of Intrust Super is IS INDUSTRY FUND Pty Ltd | MySuper Unique Identifier: 65704511371601 | ABN: 45 010 814 623 | AFSL No: 238051 | RSE Licence No: L0001298 | Intrust Super ABN 65 704 511 371 | USI/SPIN: HPP0100AU | RSE Registration No: R1004397

intrust.com.au | 132 467 [ 19 ]

[ 20 ] EXECUTIVE SUPER PDS | 01 APRIL 2021

VISIT Level 21, 10 Eagle Street, Brisbane QLD 4000

MAIL GPO Box 1416, Brisbane QLD 4001

PHONE 132 467 131 450 – Free translation service

EMAIL [email protected]

WEB intrust.com.au

Connect with us

HX/SHORT/PDS 869.5 04/21

Complete your membership!Complete your membership by registering for MemberAccess!

Manage your account online 24/7 - view your balance, consolidate your super, change your investment options, update your contact details and more! Visit memberaccess.com.au to get started.

Need help?Call 132 467. We’re at your service.

![Executive Super | 132 467 [3] Insurance cover explained Life and TPD cover The amount of cover you can have Life and TPD insurance in Executive Super is denominated in units. You may](https://img.dokumen.tips/doc/110x75/5ad6cf2c7f8b9a9d5c8b4baa/executive-132-467-3-insurance-cover-explained-life-and-tpd-cover-the-amount.jpg)