Embed Size (px)

Citation preview

INSIDE THIS ISSUEExclusive Interviews with

Hasan Al Jabri, CEO, Sedco CapitalMohd Razlan Mohamed, CEO, Marc

ISFIRE ReportChallenges & Opportunities in Islamic

Finance EducationPersonality

Roslina Abdul Rahman, MD, Amundi Malaysia Sdn Bhd

Published by:

Sponsored by:

ISLAMIC FINANCE REVIEW | WWW.ISFIRE.ORG VOLUME 5 - ISSUE 1 | MARCH 2015 - £20

AN OFFICIAL PUBLICATION OF ISLAMIC BANKERS ASSOCIATION

Edbiz Consulting is a truly unique, international Islamic finance think tank, committed to engendering the value proposition that Islamic finance serves to offer in the global financial markets. Edbiz Consulting provides multiple services that balance the dual purpose of developing thought leadership in this niche industry and strengthening the Islamic finance capacity for businesses and banks. Our client base is diverse and includes financial institutions, governments, education providers, established businesses and entrepreneurs.

Our products and services are underpinned by a common goal: promoting and advocating the ethical values inherent in Islamic finance

w w w . e d b i z c o n s u l t i n g . c o m

EDBIZ CORPORATION

www.isfire.org

GlobalIslamicFinanceReport 2015

Islamic Ec nomist ISLAMIC BANKERS ASSOCIATION

An award winning publication of Edbiz Consulting

The Global Islamic Finance Report (GIFR) is a �edgling yet successful annual report, appraising and analysing the state of the industry for the given year. It sources contributions from leading practitioners and thinkers from the industry, who provide incisive analysis and up to date information. Not only does the GIFR appraise the industry, it tackles key issues, with each report having a central theme. The GIFR intends to be a leading resource book for all those with an interest in Islamic �nance.

www.gifr.net

For more information:Please contact Rizwan Malik

COMINGSOON

4

CONTENTS

Editor-in-ChiefProfessor Humayon DarPhD, Cambridge University

International Editorial BoardDr. Mehmet Asutay Durham University

Dato’ Dr. Asyraf Wajdi DusukiYayasan Dakwah Islamiah MalaysiaDr. Mian Farooq HaqState Bank of PakistanMoinuddin MalimAlternative International Management Services

Professor Kabir HassanUniversity of New OrleansDatuk Noripah KamsoIslamic Finance ExpertDr. Asmadi Mohamed NaimUniversity Utara Malaysia

Professor Joseph FalzonUniversity of MaltaM. Saleem Ahmed Ranjha Wan Miana Rural Development ProgrammeProfessor Muhamad Rahimi OsmanUniversity Teknologi MARA Dr. Usamah Ahmed UthmanKing Fahd University of Petroleum & Minerals

Designed ByFahad [email protected]

Executive StaffZia Ullah ZiaKhuram Shehzad Usaid Hasan

Advertisements, Commercial and Subscription EnquiriesRizwan MalikE: [email protected]: +44 (0) 7791 762 047Usaid HasanE: [email protected]: +92 (0) 323 7533 723

Published byEdbiz Consulting Limited4 Montpelier Street KnightbridgeLondon SW7 1EEUnited KingdomT: +44(0) 207 709 3050E: [email protected]: www.edbizconsulting.com

Printed by: Manor Creative, UK

Talking PoinTs

06 Principles of an Islamic Financial System

Patrick Mahdi O’Neill

18 Band of Brothers

Professor Humayon Dar

26 Do Young Muslims Subscribe to Islamic Finance Products

DrSofizaAzmi

43 Islamic Exchange Trade Funds (ETF) - A Financial Innovation

Dr.NafisAlam

46 Specific Risks Facing Banks and Financial Institutions (IBIFs)

Yousuf Siddiqui

52 Financial Reporting for Islamic Financial Institutions in Malaysia: Issues and Challenges

Mezbah Uddin & Romzie Rosman

PersonaliTy

45 Roslina Abdul Rahman

Managing Director, Amundi Malaysia Sdn Bhd

inTerviews

12 Hasan Shakib Al-Jabri

CEO, Sedco Capital

38 Mohd Razlan Mohamed

CEO of Malaysian Rating Corporation Berhad (MARC)

isfire rePorT

30 Challenges & Opportunities in Islamic Finance Education

Pause for ThoughT

50 Lahore as a Global Centre of Excellence for Islamic Finance?

Professor Humayon Dar

ISLAMIC FINANCE REVIEW | WWW.ISFIRE.ORG

VOLUME 5 - ISSUE 1 | MARCH 2015

ISSN 2049 - 1905

5

From the EDITOR

FROM THE EDITOR

ISFIREcelebratessuccessstoriesinIslamicbankingandfinance(IBF).Thisquarter’ssuccessstoryistold through an extensive interview of Hasan Al Jabri, CEO of SEDCO Capital. This follows some very distinguished cover stories shared with our readers in the last three years. The most notable of the cover stories in 2014 was that of His Excellency Dato’ Seri Najib Razak, Prime Minister of Malaysia, whose government continues to play a lead role in the global developments in IBF. Hasan Al Jabri’s story is equally inspiring, as he led a team of asset managers based in Saudi Arabia to bring the social responsibility concerns to the forefront of Islamic asset management on a global level.

Social responsibility is a focus of policy debate all over the world. Sooner or later, IBF will have to embraceittomaintainitsrelevancetothemasses.TheprofitabilityofIslamicfinancialinstitutionsisonarise,andwithititscommitmenttosocialresponsibilitymustbefirmedup.Pharmaceuticalfirmsaroundtheworld,whilebeingimmenselyprofitable,arenowcommittingthemselvestopatientassistanceprogrammes by way of offering free or discounted access to medicine to those who otherwise cannot affordtopayforcostlymedicaltreatment.Islamicbanksandfinancialinstitutionswillhavetograduallyshowtheircommitmenttothefinanciallyexcluded–thosewhoeitherhavenoaccesstofinancialservicesor cannot afford to pay for such an access.

Withoutcommittingtosocialresponsibility,Islamicbanksandfinancialinstitutionswillfinditdifficulttoappealanewgenerationoftheusersoffinancialservices,whoareincreasinglybecomingawareofandcommittedtosocialissues.DrSofizaAzmi’sarticlehighlightsthisnewtrend.ShepointsoutthatonlyafractionoftheGen-YusesIslamicfinancialservicesbeyondthebasicproductslikecurrentaccounts.Islamic banks can make further inroads into the younger generations by offering the services consistent withamodernfinanciallifestyle.

Corporate governance in IBF is the focus of an article contributed by Mezbah Uddin and Romzie Rosman.FinancialreportinginthecontextofMalaysianIslamicfinancialservicesindustryshouldbeofinterest to the regulators who are looking into developing similar regimes in their respective countries.

A unique feature on ownership and control in IBF is included in this issue. It looks into the shareholdings of some of the major players in IBF to detect any hidden agenda or non-business motives of the promoters. The readers will observe that IBF is a purely business phenomenon, with shareholders driven byprofitmotiveasmuchastheirconventionalcounterparts.SomeoftheleadingpersonalitiesinIBFarealso mentioned in this context.

We have Roslina Abdul Rahman, CEO of Amundi Islamic Malaysia Sdn Bhd, as our featured personality under our regular Personality interview. A detailed interview of Mohd Razlan Mohamed, CEO of MARC, is included to give an insight into the company that won a Global Islamic Finance Award as the best Islamic rating agency in Dubai last year. So big is the success story of MARC that we decided to interview the man who has been behind the recent success of a global Islamic rating agency.

Inthisissue,wealsofocusonIslamicfinancialeducation.Acomprehensivereportisincludedtohighlightchallenges and opportunities in development of human resources and nurturing talent in IBF.

In Pause for Thought, I have argued for developing Lahore as a centre of excellence for IBF. This is followed by my participation in the third Global Forum on Islamic Finance, organised by COMSATS Institute of Information Technology Lahore on March 11-12, 2015. Lahore certainly deserves attention oftheglobalIslamicfinancialservicesindustry,andsoisAlmatywhereweareholdingourfifthGlobalIslamic Finance Awards at the end of September this year.

Patrick Mahdi O’Neil continues with his two-part analysis of the monetary system based on debt-based moneycreation,withaviewtosuggestanIslamicsolution.DrNafisAlamisournewcontributorwhohaswritten on exchange traded funds.

ThereaderswillobservethatthisissueofISFIREhasimprovedsignificantlyintermsofdesignand format. This is due to the collective efforts of Edbiz team, especially Fahad Alvi who has spent considerably more time in improving the outlook of the magazine. I am thankful to the entire team and all the contributors who have made ISFIRE as number one publication in IBF. From this issue, ISFIRE has becomeofficialpublicationofIslamicBankersAssociation–aLondon-basedbodyrepresentinginterestsof the global community of Islamic bankers and associated professionals.

Professor Humayon Dar, PhD (Cam-bridge) Editor-in-Chief

6

TALKING POINTS

To know the light, we must also see the darkness. In part 1 (ISFIRE Nov 2014 Issue) we have already taken a look at how the darkness ofthecurrentfinancialsystemhasenvelopedthe world and enslaved most of mankind to unending debt and interest repayments. The result is debt mountains piled upon debt mountainscreatedoutofnothinginflictinginterest compounding without mercy stealing purchasing power and appropriating the wealth and resources of mankind to enrich the globaleliteofourfinancialsystem.Inthe2nd part,wetakealookathowafinancialsystemrooted in the principles of Islam and adheres totheShari’aoffersafinancialsystemwhichisbeneficialandmercytoallofmankind.

Islam is a mercy from Allah. So it follows a financialsystembasedonIslamicprincipleswill be a mercy for all mankind. The philosophy, outlookandorientationofanIslamicfinancialsystemareincompletecontrasttothefinancialsystem we know and govern our lives today. It requires a complete shift in our thinking, attitude and relationship with money and wealth.

Let’s start at the beginning! For Muslims, the meaning of life is no great mystery. Allah (SWT),

says in the holy Quran “I have only created Jinns and men, that they may worship (or serve) Me”. (Surah 51 Al-Dhariyat) For the believer, this life and all its possessions and wealth are but a test. This life is very short andfleeting.Allah(SWT)saidinSurah57AL-Hadid Verse 20:

“Know that the life of this world is only play and amusement, pomp and mutual boasting among you, and rivalry in respect of wealth and children, as the likeness of vegetation after rain, thereof the growth is pleasing to the tiller; Afterwards it dries up and you see it turning yellow; then it Becomes straw. But in the Hereafter (there is both), a severe Torment (For the disbelievers, evil doers), and Forgiveness from Allah and (His) Good Pleasure (for the believers, good doers), whereas the life of the world is only a deceiving enjoyment.”

For those who have been given great wealth, itisbothagreatblessingandbenefittobegrateful to Allah, but also a test as they will have

toaccountfortheirwealthinthenextlife–howyou earned it and spent it. For those with little wealth,itisalsoatest–willoneacceptwhatAllah has bestowed with patience (sabir) and without complaining. “Be sure We shall test you with something of fear and hunger, some loss in goods, lives and the fruits (of your toil), but give glad tidings to those who patiently persevere. (155) Who say: when afflicted with calamity: “To Allah we belong and to Him is our return.” (156) They are those on whom (descend) blessings from their Lord and Mercy and they are the ones that receive guidance”. (Surah 2 Al-Baqara)

Allah (SWT), is the owner of all wealth “To Him belongs what is in the heavens and on earth, and all between them, and all beneath the soil.” (Surah 20 Ta-Ha) There are 2 dimensions to this. Firstly, we recognise and believe that whatever wealth we have is by the will of Allah. Secondly, no matter how wealthy you are, you only possess your wealth for as long as the lifespan Allah has written for you. After you die, your wealth will be passed on to somebody else. Even on our

In the Name of Allah, the Merciful, the Compassionate

Principles of an Islamic Financial SystemPatrick Mahdi O’NeillIndependent Financial Adviser

7

ISLAMIC FINANCE REVIEW | WWW.ISFIRE.ORGTALKING POINTS

death, believers cannot will their estate (except aportion)astheywish–itisstipulatedintheShari’a how one’s estate should be distributed.

Another very important concept in Islam is balance and moderation in all aspects of our lives. Our material pursuits should be balanced with our spiritual needs. Individual’s needs should be weighed against society’s needs. Wearefreetopursueprofitandseektoincrease our wealth, but it should not come at the expense of our worship and duties to our Creator. Our pursuit of personal gain, should not come at the expense of society, nor the detriment of the environment, or impinge on the rights of anyone else.

Allah (SWT) says “Those who, when they spend, are not extravagant and not niggardly, but hold a just balance between those (extremes)” (Surah 25 Al-Furqan)

Who was the best person who embodied the teachings of Islam and set the best example in both actions and words for us to follow? This of course was our beloved Prophet Muhammad (Peace be Upon Him). In a beautiful hadith (reported saying) “None of you (truly) believes until he loves for his brother what he loves for himself.” (Al-Bukhari and Muslim). In another saying ‘He who sleeps on a full stomach whilst his neighbour goes hungry is not one of us’ (Bukhari). Care, compassion and mercy for others are part of our religion and are a duty incumbent upon the Muslims. Imagine if our business dealings, trade and investments reflectedtheseideals–ourworldtrulywouldbe a more prosperous, kind and happy place for all.

WhilstanIslamicfinancialsystemisbuiltonthe foundations of values and beliefs, it must alsohavespecificrulingsanddetailedguidanceto enable us to achieve a system which meets theobjectivesoftheShari’aandfulfilsourroleand duties as trustees of our planet and all the resources and wealth Allah has provided for us.

The best known of these injunctions is the prohibition of Riba, which literally means excess, increase or addition. There are different types or categories of Riba, but the most prevalent and widespread type of Riba practiced in our world today is the charging of interest, which is what this article will focus on.Interestcanbedefinedasthechargeforborrowing money, typically expressed as an annual percentage rate i.e. if you borrow money, you have to pay the principal back plus anadditionalamountofmoney–theadditionalamount or increase is interest.

Today in our modern world, interest by most is viewed as a very normal part of life. The prices of assets, evaluation of investments and projects, lending and even Islamic banking are all effected by interest rates. You could almost say the interest rate is considered to be a ‘universal law of money’. Even many western writers who are very eloquent in their criticism ofdifferentaspectsofthefinancialsystemwillrarely talk about interest as being the root of the problem. Of course this was not always the case. For most of human history, the charging of interest was universally despised by most societies and religions. For example, in England in the 13th century, usury was illegal and linked to blasphemy. In this period, those guilty of usury, had their assets seized. This included 300 English Jews who were hanged and had theirpropertyconfiscated.Aristotle(384–322 BC) the Greek philosopher and one of the fathers of Western thought, wrote about lending of money at interest;

“The most hated sort, and with the greatest reason, is usury, which makes a gain out of money itself, and not from the natural object of it. For money was intended to be used in exchange, but not to increase at interest. And this term interest, which means the birth of money from money, is applied to the breeding of money because the offspring resembles the parent. Wherefore of a mode of getting wealth this is the most unnatural”.

So the prohibition and condemnation of Riba or the charging of interest in the Quran is not new. The verses in the holy Quran use strong and dramatic language to leave no doubt regarding the serious nature of Riba, its prohibition and utter condemnation. In Surah Al-Baqara, Allah (SWT) says;

“Those who devour usury will not stand except as stands one whom the Evil One by his touch hath driven to madness. That is because they say: “Trade is like usury,” but Allah hath permitted trade and forbidden usury. Those who after receiving direction from their Lord, desist, shall be pardoned for the past; their case is for Allah (to judge); but those who repeat (the offence) are companions of the Fire: they will abide therein (for ever). (Surah 2 Al-Baqara)

For those who persist in demanding interest, they are given a very bleak warning from Allah;

“O ye who believe! Fear Allah and give up what remains of your demand for

usury, if ye are indeed believers. (278) If ye do it not, take notice of war from Allah and His Messenger: but if ye repent ye shall have your capital sums; deal not unjustly and ye shall not be dealt with unjustly” (Surah 2 Al-Baqara)

And it is not just the one who charges interest thathastoworry–itisaserioussinforallparties involved in Riba dealings. In a hadith of our Prophet (PBUH) said, “Allah has cursed the one who consumes Riba (interest), the one who gives it, the one who records it and the witnesses.” He said: “they are all the same” (Sahih Muslim)

Moving on from the charging of interest itself, I believe the next important step is to look at the support structures of our Riba or interest basedfinancialsystem.InterestderivesfromDebt. Debt is manufactured by our banking system via Fractional Reserve Banking (FRB) and most of our Fiat Money comes into existence as interest bearing bank debt. This relationship is summarised in the diagram below.

Remember the vast majority of our interest bearing debt has been manufactured by banks out of nothing via FRB which typically accounts for97%ofourfiatmoneysupply.

Amongst the vast majority of the ulema (scholars) and people there is almost unanimous agreement that all forms of interest constitute Riba. What is less clear and certainly much less discussed is the position regarding FRB and Fiat Currency. Of course both of these monetary phenomena did not exist at the time of the Prophet (PBUH) or for most of the existence of the Islamic Empires/Era. FRB did notevolveorganicallyinMuslimlands–ithasbeen imposed via the former colonial powers.

I am not a Shari’a expert, so I will not get entangled in a debate about the Shari’a compliance or not of FRB and Fiat Currency. However, I will certainly argue that they go against the maqasid (objectives) of Shari’a. Please refer to part 1 where I give a comprehensivecritiqueofthefinancialsystem–Iwillnotrepeatallthecriticismshere,butl will just focus on one key aspect which is inflation.

When you increase the supply of something, all other things being equal you reduce its price or value. So it is with money. Via FRB the money supply is dramatically increased. Fiat money (especially the electronic version), because it has no real value can be produced endlessly at almostnocost.However,thoughfiatmoneyhas no real value you can buy real things with it. So essentially the banking system can produce something of no real value with little or no cost

8

ISLAMIC FINANCE REVIEW | MARCH 2015 TALKING POINTS

and via interest repayments acquire money for nothing which entitles them of course to acquire real wealth. FRB and Fiat Currency are a deadly duo working in tandem to increase the money supply/debt levels which is therefore constantly eroding the value of money.

Simply,nowoneneedstoaskwhobenefitsthemostandwhosuffersthemostfrominflation?The poor in society and those on low incomes are the most badly affected. Their cost of living is constantly on the increase and many are forced into high interest debts, just to survive. Wealthybusinessownersandinvestorsbenefitthe most. As prices go up, the prices of the goods and services they provide increase which increasestheirprofitsandbusinessvalue.Overthe long term, asset prices such as property, stock markets and commodities have increased dramatically. Such a system that favours the rich and penalises the poor certainly does not fulfilthemaqasidal-Shari’a.

Some argue in favour of debt, because it allows individuals, businesses and government to spend more (whether for investment or consumption). One person’s expenditure is another person’s income. Thus allowing and increasing debt increases income, wealth and overall economic growth. This narrative paints a very attractive and compelling case for debt.However,itisafalsepromise–yougetashorttermboost,butatthesacrificeoffutureexpenditure as debt and interest have to be repaid. This exponential growth in our debt has beencausedbyourmanmadefinancialsystem.The result is the world crushed by an inverted pyramid of debt. As the debt pile accelerates, increasing amounts of income are required to service it, thus continuously reducing the ability of those in debt to repay. Even with near zero or negative real interest rates much of the world

is straining under its debt burdens. A major debt crisis or default will have a domino effect causing more defaults leading to systemic crisis inourfinancialsystem.Inevitably,theglobalfinancialsystemwilleventuallycollapseunderthe weight of its debts. Just global government debt alone is now over $55 Trillion. To give this colossalfiguremoremeaning,let’slookattheper capita debt of some of the key countries. The public debt per head of population (for every man, woman and child) in USD (source: The Economist):

• USA $46,214

• UK $41,929

• Japan $97,450

This is only public debt. Counting private and public debt, ING estimate total world’s debt at an astounding $223.3 trillion! This amounts to 313% of global gross domestic product.

Many advocate returning to money which has an intrinsic value or at least backed by something of intrinsic value. Traditionally, throughout most of human monetary history this has been gold and silver. Al-Qaadhi Abu Bakar Ibn Al-Arabi, (Ahkaamul Quran, 3/1064) definedmoney“(The gold dinar & silver dirham) is the medium to measure the value of things ... they are the judge in measuring and determining the value of wealth when there are differences in quantity or when the value of the thing is unknown.”

“Money power is the greatest power … in the whole world. It is the power to give and the power to take away, the power to destroy and the power to create, the power to crush opposition or bestow favours” (The Money Trick, by

the Institute of Democracy). By allowing FRB and Fiat Currency to exist we give this power to Central Banks, World Banks, and Commercial Banks. Governments legislate to facilitate and cooperatebecauseintheshortruntheybenefitfrom easy money via quantitative easing i.e. money printing or more correctly loading up more national debt. Money which has intrinsic value or at least backed by such, will take this power away. Interestingly, Personal Income Tax was introduced in US in 1913 the same year astheformationoftheUSFederalReserve–coincidence or collusion between government and banking!

For further reading on this critical subject matter I would also like to refer the reader to a paper by Dr. Ahamed Kameel Mydin Meera and Dr Moussa Larbani (both Professors at International Islamic University Malaysia) “Ownership Effects of Fractional Reserve Banking: An Islamic Perspective”. In great detail they tackle the issues of FRB and Fiat Currency from an Islamic perspective. They assert that FRB “….violates the ownership principle in Islam while inflicting profound injustice on the economy and society”. They further argue that “…money creation through FRB is creation of purchasing power out of nothing which brings about unjust ownership transfers of assets in the economy, to the bank effectively, paid for by the whole economy through inflation. This transfer of ownership is not based on human effort by taking on legitimate risks… They conclude “…. that FRB has elements of riba that goes against the maqasid al-Shari’ah; and therefore can be termed illegal or haram from Islamic perspective”.

The next major prohibition is gambling. In Arabic, it is referred to by Maysir which is the acquisition of wealth by chance instead of by effort and Qimar which refers to a game of chance. Allah (SWT) says in the holy Quran;

“O who you believe! Intoxicants (e.g. alcohol) and gambling and idols and (lottery by) arrows are an abomination of Satan’s work, so avoid them so that you may get salvation. Satan’s only desire is to create among you enmity and hatred by means of intoxicants and gambling and stop you from praying and remembering Allah. Will you not then stop?” (Surah 5 Ma’idah)

Gambling is a huge and lucrative industry. Forbes estimated the global market to be worth $417 billion in 2012 - and this just

I N T E R E S T

DEBIT

BANKING=

FRB

MONEY=

FLAT CURRENCY

9

ISLAMIC FINANCE REVIEW | WWW.ISFIRE.ORGTALKING POINTS

represents ‘legal’ gambling. Black market gamblingishuge–justillegalsportsbettingin Hong Kong alone generates about $64.5 Billion each year. Sports match-betting industry (legal & illegal) is worth anywhere between $700bn and $1tn a year. The world’s biggest market is the U.S., which accounts for 25% of theworld’sgamblingprofits.Chinaisthe2ndbiggest market, but counting illegal gambling it is estimated to be 1.5 to 2 times as large as the U.S.Inmanycountriesupto70to80%oftheadult population participate in some form of gambling.

Obviously from an Islamic perspective there is no distinction between legal and illegal gambling–whethersanctionedbyastateor not all gambling is an abomination. The temptation for many states or governments to legalise gambling is often too much as they can earn huge revenues from taxing it. Of course many public servants have argued and struggled against legalising gambling. The late governor of New York Thomas E. Dewey declared “The entire history of legalized gambling in this country and abroad shows that it has brought nothing but poverty, crime and corruption, demoralization of moral standards, and ultimately lower living standards and misery for all the people.” However, the lure of easy money though it is built on the misery and despair of others has in most cases triumphed over these arguments.

No country Muslim or otherwise is immune from gambling. However, thanks to clear prohibition and condemnation of gambling in the Quran at least legalised gambling in Muslim countries is generally not allowed or if allowed is often restricted to targeting tourists. Casinos do exist in Egypt, Lebanon, Malaysia and even in Palestine (amidst all the trouble!) for a period before being closed down in 2000. Gambling in Israel is illegal, so they used to travel to a casino inJerichoinPalestine–Palestinianswerenotallowed to gamble, but they did comprise most of the workforce!

The growth in online gambling is another hugeproblem–itnowtakesgamblingintothehome making it easily accessible to anyone with internet access and money. According to a survey of the 5,000 secondary students conducted by the Gamblers Rehab Centre Malaysiaindicatedthat89%admittedtohavebeen exposed to gambling before they even hit the age of 12.

The ill effects of gambling on individuals, families and society are well documented. Gambling is all consuming, leading to great stress and anxiety. It takes man away from his prayers and remembrance of Allah leading to a descending spiral of moral decay

and corruption. It is often accompanied by other vices such as drinking and drugs and like a domino leads to many more vices. These include cheating, fraud, stealing and accumulation of gambling debts. The lure of easy money, the glitter and dazzle of casinos make gambling very addictive. Addiction leads tofinancialruinanddisasterforindividualsandbrings heartbreak and sorrow to their families. Mostprofitcomesfromproblemgamblers–howevertheypayaheavypricewiththeirjobs, their houses, their health and their families. It discourages hard and honest work andpromotesselfishness,hatredandgreed.Obsessive gamblers waste an extraordinary amount of their time neglecting family and work.

Unfortunately the common attitude that prevails especially where gambling is legalised is that people should have the freedom to decide what they want to do with their money and their time even if it leads to disgrace and tragedy. Unlike our governments, Allah’s law shows his love for his creation by protecting and keeping us safe from that which is not good for us.

Closely related to gambling is speculation. Speculation needs to be distinguished from investing. It is generally characterised by buying liquid assets for a very short period with the sole intention of betting on short term price movements. Speculation in its extreme form is the same or sometimes even worse than gambling itself i.e. it is possible for the speculator to lose all their capital and in the case of leveraged speculation the losses can easily exceed the initial capital placed.

Speculationisahugeelementofthefinancialmarkets today and earns huge commission and fees for intermediaries. The biggest and most liquid market in the world today is foreign exchange - $5.3tn changes hands every day (FT Nov 2013). According to the economist Bernard Lietaer, author of The Future of Money,backin1975about80%offoreignexchange transactions involved the real trading of a product or a service. However, by 1997 the percentage of foreign exchange which involved transactions in the real economy was only 2.5%! According to the Global Policy Forum, by 2011 only a tiny 0.6% of foreign exchange could be traced to genuine international trade in goods and services. Of the remainder, a minimumof80%wasdirectlyattributabletospeculation. This of course is just the tip of the speculationiceberg.Inallfinancialmarketssuch as the stock market, debts, oil, gold and other commodities speculation is pervasive. Speculation causes bubbles to blow up in asset prices. When the bubble inevitably bursts, it unleashesatsunamioffinancialhardshipandeconomic misery as individuals, companies and

even nations go bust. This is in addition to all the usual problems associated with gambling already mentioned. Huge corporations and governments have been brought to their knees as result of the reckless actions of speculators. Speculation is a huge waste of time and resource–nonewwealthiscreated,itissimplytransferred from one to other and constantly eroded by the fees of brokers and taxes of governments.

Another very important principle is the avoidance of Uncertainty or using the Arabic term ‘Gharar’. Gharar is a broad concept that encompasses deceit, fraud, uncertainty, danger, peril, delusion, or hazard that might lead to destruction or loss. This means that any trade or transaction should be free from contractual uncertainty. There should be no ambiguity in the key terms and subject matter of the underlying contract or deal. This principle has very important implications for howbusinessshouldbeconducted.Allfinancialand business transactions must be based on full transparency and disclosure, so that no one party has an unfair advantage over the other. The aim is to protect all parties from deceit, ignorance and uncertainty. This has been emphasised in the hadith of the prophet (PBUH); “Do not meet the merchant in the way and enter into business transaction with him, and whoever meets him and buys from him (and in case it is done, see) that when the owner of (merchandise) comes into the market (and finds that he has been paid less price) he has the option (to declare the transaction null and void)” (Muslim). Thus one is not allowed to take advantage of the seller’s ignorance of the market price. In a modern context, this closely aligns with insider tradinglaws.Thefinancialservicesindustryloves to innovate and speculate - contracts such as forwards, futures, options, and other derivatives are rendered invalid because of gharar.

Of course no matter how fair, balanced and justafinancialsystemis,therewillstillbethosewho are rich and those who are poor. Zakat which redistributes wealth from the rich to the poor is such an important element that it is obligatory and is one of the 5 pillars of Islam. It is mentioned many times in the Quran and is associated with prayers, doing good deeds, mercy and forgiveness.

The Believers men and women, are protectors one of another: they enjoin what is just, and forbid what is evil: they observe regular prayers, practice regular charity, and obey Allah and His Messenger. On them will Allah pour His

10

ISLAMIC FINANCE REVIEW | MARCH 2015 TALKING POINTS

mercy: for Allah is Exalted in power, Wise. (Surah 9 Al-Tawba)

It is a serious matter. The prophet (PBUH) said “I have been ordered to fight against the people until they testify that there is none worthy of worship except Allah and that Muhammad is the Messenger of Allah, and until they establish the Salah and pay the Zakat. And if they do so then they will have gained protection from me for their lives and property, unless (they commit acts that are punishable) in accordance to Islam, and their reckoning will be with Allah the Almighty.” (Al-Bukhari & Muslim)

In Arabic, the word Zakat means blessing, purity, growth and uprightness. In the Shari’a (Islamic Law) it denotes the obligatory 2.5% of net wealth Muslims have to pay on an annual basis (lunar year) to recipients as prescribed in the holy Quran. It applies to those Muslims whose wealth is over a certain minimum level called the nisab. The nisab is measured in referencetogold(85gramsofpuregold)andsilver (595 grams of pure solver). One should have absolute possession of the wealth on which Zakat is due. For example, Zakat is not obligatory on money which is out of the owners reach for years or on debts owed but the debtor is insolvent. Certain wealth and assets are excluded from Zakat. These are possessions of a personal nature e.g. one’s private residence, furniture, car, clothes, tools of trade.

ZakatisamercyandablessingfromAllah–itgives the poor a right over a portion of the wealth of the rich. This is turn promotes social harmonyandbrotherlylove.Itpurifiesthewealth of the rich and increases their wealth in blessings.

One of the beautiful aspects of Islam is that it sets basic minimum requirements that all Muslims should adhere to. But it also gives plenty of scope to do much more and achieve greater blessings. So it is with charity giving. This brings us to the concept of Sadaqa i.e. general charity, giving over and above than that required of Zakat. It is highly encouraged and Allah promises huge rewards for charity giving.

“The likeness of those who spend their wealth in Allah’s way is as the likeness of a grain which groweth seven ears, in every ear a hundred grains. Allah giveth increase manifold to whom He will. Allah is All-Embracing, All-Knowing”. (Surah 2 Al-Baqara)

Charityisnotjustconfinedtogivingofwealth

ormoney.Theprophethasdefinedcharityinbroad terms as:

“Every joint of a person must perform a charity each day that the sun rises: to judge justly between two people is a charity. To help a man with his mount, lifting him onto it or hoisting up his belongings onto it, is a charity. And the good word is a charity. And every step that you take towards the prayer is a charity, and removing a harmful object from the road is a charity.” (Bukhari & Muslim)

Another charitable concept in Islam is known as Qard Hasan which means “Benevolent Loan”. This is generally a loan to help those who are needy,torelievefinancialstress,foragoodcause. Hasan means kindness to others and no interestoranyfinancialgainisexpectedfromthe loan. Just the principal of the loan is to be returned. Again this act is highly rewarded and encouraged by Allah.

“Who is he that will loan to Allah a beautiful loan, which Allah will double unto his credit and multiply many times? It is Allah that giveth (you) want or plenty and to Him shall be your return”. (Surah 2Al-Baqara)

The whole religion of Islam is infused with the mercy of giving charity. In a saying of the Prophet (PBUH) “When a man dies, all his acts come to an end, but three; recurring charity (sadaqah jariya) or knowledge (by which people benefit), or a pious offspring, who prays for him” (Sahih Muslim)

This has led to another noble and long-standing Islamic tradition of establishing Awqaf. The singular of Awqaf is Waqf which is a charitable endowment/trust. Monzer Kahf an

IslamicEconomicExperthasdefinedWaqfas“holding a property and preserving it so that its fruits, revenues or usufruct is used exclusively for the benefit of an objective of righteousness while prohibiting any use or disposition of it outside its specific objective”

It is very similar to an English Trust except that its purpose is charitable. There is a long legacy of wealthy Muslims donating property, land, buildings and money to awqaf which have played a very important role in supporting the socio-economic needs of society. Awqaf have taken care of a myriad of needs:

• provision of mosques, schools, and supporting scholars

• building of roads, bridges, and hospitals

• helping the elderly, the traveller, the sick, the orphan, the poor and those in debt

• animal welfare

AnIslamicfinancialsystemcannotbeseparated from Islam. Every aspect of the financialsystemshouldbeinharmonywithachieving the maqasid al-Shari’a. There are 3 key aspects; Firstly the philosophical aspect or our beliefs which provide the foundations of anIslamicfinancialsystem.Allahistheownerof all wealth and we are the trustees of this wealth. Our wealth is a means to achieve the pleasure of Allah. The second key aspect, are the practical rules and principles that we should follow i.e. Staying away from Riba, Gambling andSpeculation.Designingafinancialandmonetary system, which is honest, fair and just for all of mankind. Not a system which is leveraged so wealth can unfairly accumulate in the hands of the few. The third key aspect is the huge focus and emphasis on charity. This helps to redistribute income and wealth from the rich to the poor and create social harmony. Money isthekeyingredientinafinancialsystem.Todaymoneyanddebtarealmostsynonymous–97%of our money is debt. Money should be used as a tool to serve mankind, not mankind enslaved to money.

In both parts, I have painted a very bleak pictureofourcurrentfinanciallandscapewhichcontinues on a downward trajectory towards its inevitable collapse. However, there are reasons we should be optimistic. Firstly, is the realisation that Allah (SWT) is the creator and owner of the Universe and nothing happens anywhere in his creation unless by his will. “With Him are the keys of the unseen, the treasures that none knows but He. He knows whatever there is on the earth and in the sea. Not a leaf falls but with His knowledge: there is not a grain in the darkness (or depths) of the earth, nor anything fresh or dry (green or withered), but is (inscribed) in a record clear (to those who can read).” (Surah 6 Al An‘am). Secondly, though vast amounts of wealth have unfairly accumulated inthehandsoftheglobalelite–thewealthhas not disappeared - it is still here on planet earth! It just needs to be redistributed. Lastly, Allah (SWT) says he will destroy Riba. Though theproblemsofourRibafinancialsystemseem huge and insurmountable, Allah (SWT) has provided us with the solutions. Finally, remember Allah (SWT) said “... How often a small group overcame a mighty host by Allah’s Leave?” And Allah is with As-Sabirun (the patient).” (Surah 2Al-Baqarah)

FearlessTakaful IKHLAS

for the New Generation

C

M

Y

CM

MY

CY

CMY

K

GIFR2015_240x300mm.pdf 1 14/1/2015 10:22:58 AM

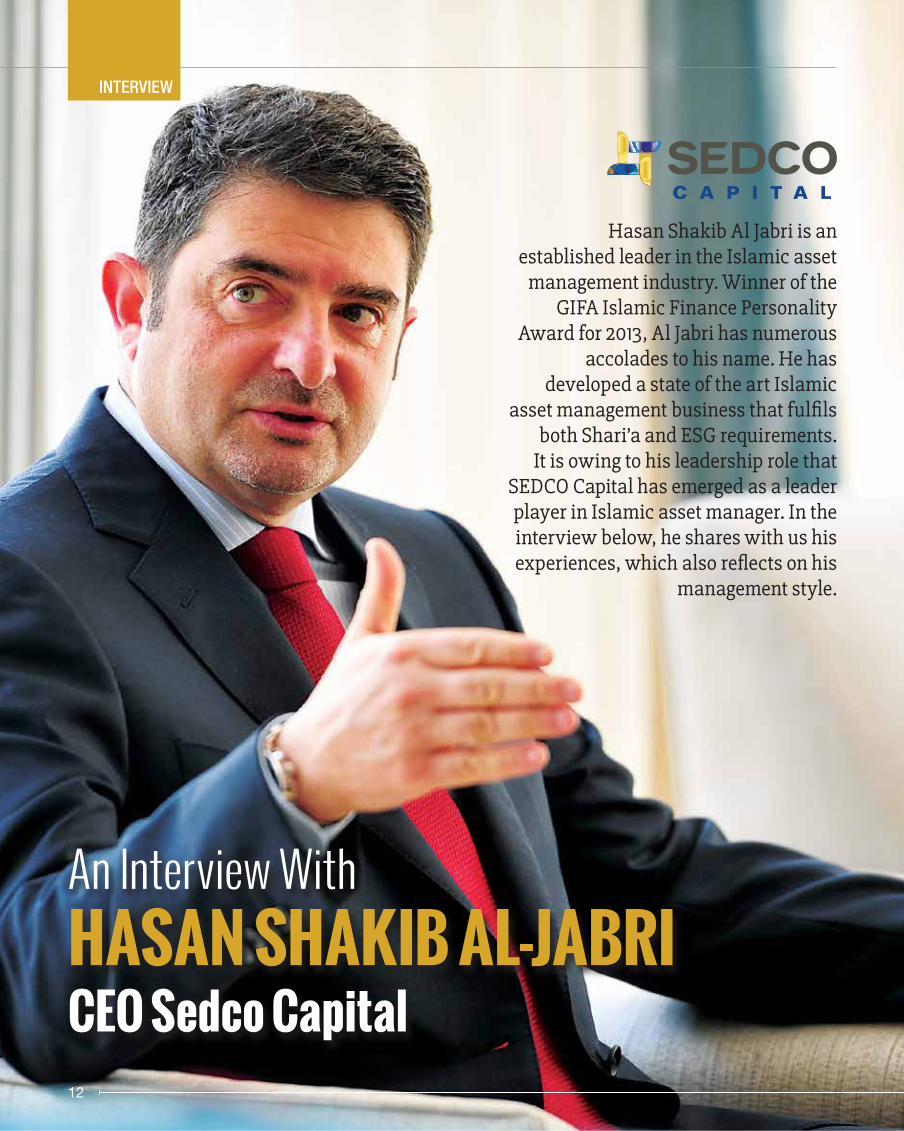

An Interview With

CEO Sedco CapitalHASAN SHAKIB AL-JABRI

INTERVIEW

Hasan Shakib Al Jabri is an established leader in the Islamic asset

management industry. Winner of the GIFA Islamic Finance Personality

Award for 2013, Al Jabri has numerous accolades to his name. He has

developed a state of the art Islamic asset management business that fulfils

both Shari’a and ESG requirements. It is owing to his leadership role that

SEDCO Capital has emerged as a leader player in Islamic asset manager. In the interview below, he shares with us his experiences, which also reflects on his

management style.

12

13

ISLAMIC FINANCE REVIEW | WWW.ISFIRE.ORG

INTERVIEW

Please tell us about Sedco Capital, what it is, what it aims for and what are the different segments within it.

SEDCO Capital is a leading Shari’a and Environmental, Social and Governance (ESG) asset manager in the world. Although we are headquartered in in the Kingdom of Saudi Arabia, we have a global offering covering equities, real estate and private equity. SEDCO Capital currently has the largest set of Shari’a funds registered in Luxembourg than any other asset manager in the World. Our range of investments spans the globe, from the US all the way to the Far East.

Carved out from a family office and formed an independent Capital Market Authority (CMA) licensed company with an initial capital of SAR 50 million in 2010, the journey of SEDCO Capital’s transformation from being afamilyofficeintoaninstitutionalisedassetmanagementfirmrequiredenormousanddedicated efforts.

Please tell us your ownership structure and who are your shareholders?

SEDCO Capital is a subsidiary of SEDCO Holding. The Saudi Economic and Development Company (SEDCO), is a leading conglomerate investing in a number of sectors regionally and internationally. It is considered a major player in real estate development and management, hospitality, wealth management, auto leasing, and healthcare, all conducted in accordance with Islamic guidelines widely known as Shari’a. Itmanagesawideanddiversifiedspectrumofreal estate investments, equities investment, and other businesses in Saudi Arabia and around the world.

Please share with us who are your clients? And how have you assisted them?

Our clients (international, regional and local), range from sovereign wealth funds, pension funds,financialinstitutions,institutionalinvestors,familyofficesandUHNWIs.Weprovide them a range of investment solutions that previously have not been available within a Shari’a investment context. Given our choice of 14 different global equity funds, coupled with our strong real estate and private equity offerings,we can provide a total asset-allocationinawell-diversifiedportfolio,uniquely for the Shari’a sensitive investor. We also provide white-labelled services to manage funds under third party names. SEDCO Capital also provides bespoke discretionary portfolio management services - in Saudi and GCC equities as well as Saudi real estate, we also offer our KSA clients and corporate-

financeadvisory.Amongourinvestmentsolutions, 10 solutions are also ESG compliant (environmentally friendly, socially responsible and follow corporate governance principles), which is a commitment we have bestowed upon ourselves moving forward.

How are you different to other asset management companies in investment advice and choices?

SEDCO Capital has a very strong and solid trackrecordthatspans28yearssinceit’sinceptionasafamilyofficein1976.Ourdiversificationinproductsofferingpairedwithour smart and innovative investment solutions and processes have promoted SEDCO Capital to be the leader in Shari’a compliant asset management. Our founders have played a vital role in the development of the Dow Jones Islamic index as well as recently becoming the first Islamic asset management company to sign the United Nations Principles of Responsible Investments (UNPRI). As a result of UNPRI, SEDCO Capital has opened up the market to conventional, responsible investors as well.

Socially Responsible Investing has lately become a buzz word for the Islamic banking and finance industry. Does that mean that Shari’a compliant investments are not socially responsible? What is the difference between the two and how does Socially Responsible Investments add value?

Following our leadership in Shari’a investing, we are very glad to be the pioneers in Socially Responsible Investing in the Shari’a world (asmentionedearlier,wearethefirstShari’acompliant asset manager to become UNPRI

signatory) and we have supported bridging the gap between the two industries when we announcedthelaunchofourfirst2ESGfundsin February 2013.

Shari’a finance is ethical by nature, this is an industry that has evolved for hundreds of year, and it has developed rapidly over the past 30 yearstoreachalmost1.831trilliondollars.Responsible investing has been evolving as well especially since the late 1996’s when Kofi Anan, UN Secretary General at the time, took a leading role in creating the UNPRI. Today it has become more than 10 trillion dollar industry. With our in-house research we recongnised the commonalities between both the Islamic and ESG industries, as far as the negative screening is concerned and without losing focus on creating sustainable economies. We added value to their existing practices with our prudence approach in investing through our leverage parameter that avoid excessive leverage in investing (which ESG investing doesn’t consider) and we learned more about active involvement which we started applying to our investment processes and our manager selection processes.

An important element in bridging this gap is to help explain to the world what Shari’a compliant investing is all about, and its resemblance to responsible investing.

Sedco Capital has recently launched funds platform in Luxembourg, can you please share more details on it.

SEDCO Capital Global Funds (SCGF) is a family of 14 liquid strategies and 3 illiquid strategies that total to about $1.6 bn of AUM. We saw that Luxembourg is well recognised regulated jurisdiction to ease the access for investors no matter their domicile.

14

ISLAMIC FINANCE REVIEW | MARCH 2015

INTERVIEW

On the SCGF, we continue to conduct our thorough due diligence on the selection process of managers as well as have continuous monitoring and supervision. The platform also offers independent performance calculations, reporting, administration and custody; it is also pluggedintomorereputablefinancialsystemslike Bloomberg, Lipper, FundInfo and Morning Star. The platform has helped introduce strategies not only to Shari’a compliant, but ethical and responsible investors.

How challenging is it to explain benefits of Socially Responsible Investing to your shareholders and Shari’a sensitive investors? How much aware are the Shari’a sensitive investors of ESG issues?

It is a learning curve for us and for our clients; we explain what Shari’a is and what ESG is. We share our practices and inform them that it not only ensures the economic sustainably but also leads to good performance. By comparing the three main indices (Dow Jones Islamic Market

Index, MSCI Social and S&P 500) we realised that both the responsible and Islamic indices performed better than the conventional with a clear advantage for the Islamic (due to low leverage).

We feel responsible towards the industry and how important these investment methodologies are; this is what we communicate to our shareholders, every time we have an opportunity.

Please share with our readers the recent developments at Sedco Capital in terms of acquisition both in international and local markets.

In international real estate, SEDCO Capital has successfully executed transactions worth $1 billion over the past 3 years. We also successfully sold 21 investments in France, Malaysia, Singapore, UK, and Mexico while acquiring 19 investments in strategic markets such as USA, UK and KSA.

In liquid strategies, we have decided to launch a fund with the strategy that allows investors

to navigate the portfolio alongside different stages of the business cycle in terms of durable versus sustainable strategies (more cyclical). As there was an increase in the money market fund (sukuk murabaha), the main purpose of this extended offering is to allow the clients, which are Shari’a compliant, to protect their wealth during market down side.

As far as our offering is concerned, we have added to our portfolio a multi-asset class portfoliocalled“corediversifiedfund”whichasa strategy allows to enter into different terms of risk adjusted returns, using a cyclical asset allocation process, reviewed on quarterly basis.

In 2014, SEDCO Capital’s private equity programme continued its growth streak completing SAR1.4 billion worth of transactions. Exiting about SAR414 million and buying SAR321 million worth of equity deals, in addition to SAR665 million of new fund commitments. The new commitments came from9differentmanagers,diversifiedacross8regions globally. The private companies exited in 2014 were sold at a healthy multiple of 2.4 times (32% IRR).

Mr Al Jabri, you have been a CEO of Sedco Capital for quite some time now, tell us how different Sedco Capital is now from when you started?

It’ssimple.Wewereafamilyofficethattransformed into a well institutionalised, regulated, highly sophisticated and performance driven asset manager. To reach there, we had to beef up the team and build up operational, administrative as well as risk management capabilities to be able to provide good service to the clients. We also invested incompliance&audit,finance,treasuryandmarketing.

Today, we handle third party clients, and we have a good number of institutional investors as well as SWF and HNW investors. We also developed further our strengths in local equities (as an asset manager), real estate and agriculture. Also this required us to change the mindset to deal with all types of sophisticated clients.

What are the short, medium and long term plans of Sedco Capital?

Our aim is to beccome the leading Shari’a asset management company globally. While we have achieved this goal to a large extent, we realise that this is a dynamic goal and we will continue to exert utmost efforts to deliver to our clients the best opportunities and services. We must be well recognised in the Islamic world. Our goal in the medium and long run is to become

ISLAMIC FINANCE REVIEW | WWW.ISFIRE.ORG

the asset manager of choice for Shari’a investors as well as ethical and responsible investors globally. Also we must be able to capture responsible clients who see us as a good investment company that has a superior track record, driven by a strong process and asset management team.

What challenges do you face in achieving your goals and working with investors from different backgrounds? And who are your competitors?

Market volatility is a constant element that we always have to manage, obviously the increasing regulatory requirements are becoming a major point of focus, as well as attracting and retaining the best talent.

Our investors are from different backgrounds, this is a positive challenge. As we have the most diversifiedgroupofinvestmentopportunitiesand fund strategies, we always have to listen to their needs and be able to advise them appropriately rather than be product pushers.

Our investments for the past 3 decades have always been global in nature, including developed as well as emerging markets, and through our Luxembourg platform we can deal with investors from all over the world.

Big private banks saw our products as being stronganddiversifiedintheShari’aworldand they started distributing them globally through fund platforms of some of the largest international and well regarded banks .In Saudi Arabia, we have a dedicated business development team.

We have different competitors for different asset classes and geographies, including GCC asset manager and global international banks.

Sedco Capital has been receiving a lot of industry awards, one of the recent one is the Global Islamic Finance Awards (GIFA) 2014 in Dubai, please share your thoughts on it and what it means to you.

GIFA has been doing a good job in identifying the market makers in the region and all over the world. We are very proud to receive recognition from GIFA as a socially responsible fund manager. All these great initiatives are in line with Shiekh Mohammad Bin Rashed Al Maktoum’s (Ruler of Dubai) vision to make Dubai the islamic economy capital of the world. We are very proud to have won many awards in the industry including the “Islamic Economy Award” for “Best Islamic Fund” presented to us by Sheikh Mohammad bin Rashed Al Maktoum in 2013 during the GIES.

INTERVIEW

15

16

All that Sedco Capital has achieved would not have been possible without the hard work, commitment and support of your team, please share your views on the team and how do you motivate them as their leader.

We all work together, we always give positive feedback, we have a great working atmosphere and we base our culture on mutual respect; all these elements have made us an employer of choice in the industry where top talent is approaching us to join SEDCO Capital. All this is in line with our shareholders’ vision and the strong governance by the authority (and trust) given to management. Today SEDCO has been ranked as the 11th best working environment employer in Saudi Arabia.

Share with us your journey into Islamic banking and finance?

SEDCO Capital was born Shari’a compliant; we started all of our product offerings since inception to be in line with the principles and practices of Shari’a. As we developed over the years, we continuously innovated products and solutions in an industry that is based on interest and hedging; this proved to be very challenging. However our determination, experience of over 20 years and our well rounded team allowed us to develop products that not only lead in the Shari’a world, but also to be at par with conventional offerings from other banks.

Moreover, our scale has also contributed in providing very competitive TER’s in the market, which has put us at a clear advantage.

Share with the readers of ISFIRE a typical day of Hasan Al Jabri. How does it start and how it ends and what is on your must do list?

To have a clear schedule for the day, week, month, and even the year ahead of time is what you need to deliver and achieve. My work involves a lot of travel since a lot of our investments are international in nature. Our strong team manages their portfolio, yet I have to visit our clients and managers globally. Travel takes a lot of my time; nevertheless, we must schedule the time way ahead so you can useitefficiently.Idodelegatealotespeciallyto our strong team. I keep an open door policy to spend time in listening to senior and young staff.

I take lunch as an opportunity to have discussions with our colleagues; this helped to get to know them better and listen to them while keeping me in tune with the whole organisation on both a professional and

personal level.

What are some of the most exciting projects you have worked upon?

Over the past 2 year, our main focus has been on launching the Luxembourg platform as our work in bridging the gap between Shari’a and responsible investing. We are also working on a few projects to support SMEs that are vital for sustainable economic development.

The US real estate timing was spot-on so it was really quite an interesting opportunity to work on. Also developing our co-investment activities where we’re buying into very exciting businesses globally.

On the CSR front, the financial literacy programme developed by SEDCO holding in the name of “Riyali” has gained a lot of ground over the past two years included in the circle of beneficiaries’areyoungbusinessownersandstudent as at all levels. Another interesting CSR initiative that we are involved in is “Foras”, an angel investors programme that helps young Saudis develop their business.

You have contributed to the industry in different ways, through speaking engagements, article contributions etc. How do you balance these with the workload?

Thanks to the strong team that I have, they always help me with great ideas and with the day-to-day workload. This gives me the opportunity to spend more time on other engagements, which is also helpful in developing our knowledge and network.

One has to try and balance the requirements of the day-to-day business and our responsibility to share our knowledge with the industry. This gives us the chance to introduce what we are doing and share our view on the future, on the investment team and on the industry in general through our innovations and services we offer to our clients.

ISLAMIC FINANCE REVIEW | MARCH 2015

INTERVIEW

18

A non-academic investigation into the networks that control Islamic

financial institutions

BANDBROTHERS

OF

Shari’a scholars are too damn powerful, “We must make Shari’a scholars more accountable,” “Islamic banking industry is hostage to a small group of Shari’a scholars” …

These are echoes of conversations many of those who are involved in Islamic banking andfinance(IBF)musthaveheardatvariousconferences, seminars and discussion groups. In fact, once there was a serious attempt (hopefully unintended!) By a small consultancy company to destroy credibility of Shari’a scholars. The so-called “social network” approach adopted therein certainly managed to dint the credibility of Shari’a scholars and in fact brought a lot of genuine issues to the forefront of the policy debate. But… the question remains. Who controls IBF? For disappointment of many (the likes of http://www.shari’ahfinancewatch.org), “Who Controls IBF” is not a who’s who of the people on the sanction lists drawn up by America and the EU. It is also not a guide to the so-called Islamic caliphate that seems to be emerging in parts of Iraq, Syria and the neighbourhood.

IBF has in fact emerged as an Islamic capitalistic movement,whichfitswellintheWesterncapitalism. This is one of the reasons that it failedtoearnpatronageofthelikesofHafizAlAsad (father of the current President Bashar

AlAsadofSyria),MuammarQaddafi,SaddamHussain and other leaders in the Muslim world, with inclination towards socialism. Interestingly enough, IBF initially failed to get traction from many other governments in the Muslim world. It was only after some heavyweight Western financialinstitutionsshowedtheirtrustinIBFthat some governments in the Muslim world started accommodating IBF in their regulatory regimes.

If it is not Al-Qaeda or its remnants who are controlling IBF, who is it that is behind the global movement of IBF? Is it Shari’a scholars who control IBF or the centre of power lies somewhere else? Is it actually a legitimate question to ask after all?

If ulama’, or Shari’a scholars, are not central to IBF, then who else? Is it the Saudi royal family? Are these the ruling families in UAE and other countries in the Gulf Cooperation Council (GCC) area, which are controlling Islamicfinancialinstitutions?Aretheresomeother invisible hands behind the growing globalIslamicfinancialservicesindustry?

Is there a dotted line between Islamic financialinstitutionsandtheglobalterroristnetworks? Where are most of the assets under managementofIslamicfinancialserviceslocated? To understand all these issues, it is important to look into a number of phenomena, mechanisms and processes:

A. Shareholding composition of some of the largest Islamic banks in the world;

B. RegulatorybodiesforIslamicfinancialinstitutions;

C. AffiliationsoftheShari’ascholarsinvolvedin IBF;

D. Attitudes of terrorist groups towards IBF; and

E. Involvement of non-Muslims in IBF.

WHO OWNS ISLAMIC BANKS?There are three categories of owners of Islamic banks:

A. Governments;

B. High Net Worth Individuals (HNWIs) and families; and

C. General public.

A. Governments

There have been a few governments in the Muslim world, which are friendly towards IBF.

TALKING POINTS

19

ISLAMIC FINANCE REVIEW | WWW.ISFIRE.ORG

Malaysia is an exception where the government has taken an unambiguously strong and favourable approach towards the development of IBF. Almost all other governments in the Muslim world are at best indifferent to IBF and in some cases hostile towards its development. Admittedly, there are countries that have started showing interest in the development of IBF, and the newly elected government in Pakistan is one of them. It must, however, be emphasised that there is nothing sinister about this changing attitude of the governments in the Muslim world towards IBF. Similarly, it is only recent that the government in Turkey has started realising that IBF provides a great opportunity for it to attract Islamic capital from other parts of the Muslim world.

Arguably the strongest opponents of IBF in the Muslim world, the likes of the regimes of MuammarQaddafi,SaddamHussainandHosniMubarak, are no more relevant, but still there exists strong resistance to the introduction of IBF in most of the countries included in the Organisation of Islamic Cooperation (OIC). The opposition has largely come from the authoritarian regimes and, in case of democratic countries, from the bureaucracy.

Two notable countries where government-level support exists for IBF are Iran and Sudan. Both

countries are isolated from the global Islamic financialservicesindustryprimarilybecauseofthe on-going economic sanctions by USA and other allied countries.

Iranian banks account for about 40 per cent of total assets of the world’s top 100 Islamic banks. Bank Melli Iran, with assets of $45.5 billioncamefirst,followedbySaudiArabia’sAl Rajhi Bank, Bank Mellat with $39.7 billion and Bank Saderat Iran with $39.3 billion. Iran holds the world’s largest level of Islamic financeassetsvaluedatUS$489billion,whichis US$150 billion more than the next country in the list, i.e., Saudi Arabia. Six out of ten top Islamic banks in the world are Iranian.

It is also worth mentioning that Bangladesh is perhaps the most under-rated country in the world, although it has over 20% market share foritsIslamicbanks–doubleofthecomparablefigureforPakistan,whichhasbeenoneofthemost talked about and most frequently cited countryintheglobalIslamicfinancialservicesindustry. Although industry observers and analysts refer to Al Rajhi Bank as the largest Islamic bank in the world (excluding Iran), Islami Bank Bangladesh has escaped attention. With nearly 300 branches and about 12,000 strong staff, it has the largest Islamic banking network in Southeast Asia.

It is also worth mentioning that Bangladesh is perhaps the most under-rated country in the world, although it has over 20% market share for its Islamic banks – double of the comparable figure for Pakistan, which has been one of the most talked about and most frequently cited country in the global Islamic financial services industry. Although industry observers and analysts refer to Al Rajhi Bank as the largest Islamic bank in the world (excluding Iran), Islami Bank Bangladesh has escaped attention. With nearly 300 branches and about 12,000 strong staff, it has the largest Islamic banking network in Southeast Asia.

Why government support has not been forthcoming for IBF?

Although a number of factors may have contributed to the lack of support for IBF by Muslim governments in the past, it is however currently by and large a bureaucratic problem. It is no more seen as a political threat, which was erroneously the case in the past. Introduction of IBF requires substantial changes in legal frameworks, taxation laws, bankingandfinancialregulation,andpropertyrights. The bureaucracy in these countries findsitadauntingtask,andhenceisunwillingtochange the status quo.

If someone has to pick up five governments supporting IBF, weighted by their global significance,thefollowinglistwillemerge:

1. Malaysia

2. United Arab Emirates

3. Bahrain

4. Kuwait

5. Qatar

Interestingly,allthesefivecountriesareverysmallintermsofpopulation.TheirsignificanceandinfluenceinthepoliticsoftheMuslimworld is rather limited as well. None of the above countries has a population more than 30 million. While Malaysia has the highest population in the above group, it is notable that the Muslim population therein is only about 60% of the total population in the country. The governments of the countries with the largest Muslim populations are at best indifferent if not hostile to IBF. Indonesia, for example, is a secular country constitutionally; itsgovernmentfindsitdifficulttopatroniseIBFofficially.Intherecentpast,changesincertain laws have allowed Indonesia to use sukuk as a capital market instrument to raise funds for the public sector. Pakistan, which is constitutionally an Islamic republic, has for long resisted demands for transforming its economy

andfinancialsectorincommensuratewiththeIslamic economic doctrine. Similarly, despite having captured the market share of about 20%, Bangladeshi Islamic banks are growing through a market-based approach rather than an explicit government support. The politics of IBF in Turkey (with secular constitution) remains complex, despite recent sympathetic approach by the government. Egypt, despite being the birthplace of modern IBF, has also been careful in its treatment of IBF.

Malaysia

Malaysian government is by far the most committed advocate of IBF in the world. It is primarily due to the successive Malaysian governments and the role of a catalyst of Bank Negara Malaysia that Malaysia enjoys a vibrant Islamicfinancialsystem.Someoftheroyalfamilies in Malaysia have also been involved in IBF. The most obvious leadership role is being played by HRH Sultan Nazrin Shah of Perak (GIFA Laureate 2012) who serves as Financial Ambassador for Malaysia International Islamic Financial Centre (MIFC). The royal family of Negri Sembilan is also involved in IBF through its shareholding in the Bahrain-based Ithmaar Bank.

The government of Malaysia has direct and indirect shareholding in a number of Islamic financialinstitutions.Twonotablegovernmentinvestments are as follows:

Tabung Haji: Tabung Haji is the oldest example ofsuccessofanIslamicfinancialinstitution.Primarily a savings programme for those who intend to travel to Makkah for pilgrimage, TabungHajihasemergedasaninfluentialplayerintheIslamicfinancialservicesindustry,

TALKING POINTS

20

ISLAMIC FINANCE REVIEW | MARCH 2015

withsignificantshareholdingsinBankIslamandanumberofotherIslamicfinancialinstitutions.

Khazanah: Malaysian sovereign fund, Khazanah, has been instrumental in promoting IBF in the country as well as outside Malaysia. It has been instrumental in developing an Islamic capital market through its various roles in the issuance of sukuk in the country. It also has significantshareholdinginFajrCapital,aDubai-basedIslamicprivateequityfirm,whichinturnhas 40% shareholding in Bank Islam Brunei Darussalam.

Furthermore, through MIFC Bank Negara Malaysia and Securities Commission Malaysia are pro-active in promoting and hence controllingtheIslamicfinancialservicesindustry.

Malaysia also hosts Islamic Financial Services Board–theglobalbodysetuptodevelopregulatory and prudential guidelines for the institutionsofferingIslamicfinancialservices.

United Arab Emirates

Although the UAE government has not beeninvolvedinofficialadvocacyofIBF,thegovernments and the ruling families in the country have invested heavily in Islamic banks andfinancialinstitutions.ItisonlyrecentthatthegovernmentofDubaihasofficiallyannounced to make Dubai as a centre of excellence for the global Islamic economy.

Dubai holds the distinction of hosting the oldest Islamic commercial bank in the world, namely Dubai Islamic Bank. Abu Dhabi, the more dominating emirate in the federation hasitsownflagshipIslamicbank,namelyAbuDhabi Islamic Bank (ADIB). In addition to these

two Islamic banks, a number of other Islamic banksandfinancialinstitutionsareoperatingin the UAE. Almost all these initiatives have royal patronage, although the Central Bank of the UAE does not seem to treat Islamic banks any different from their conventional counterparts. Hence, Islamic banks despite having shareholdings from the ruling families do not enjoy any preferential treatment. This is primarily due to the fact that most of the conventional banks are also either owned by the state governments or members of the ruling families.

ThroughtheseIslamicbanksandfinancialinstitutions, governments in the federation of UAEplayaninfluentialroleintheglobalIslamicfinancialservicesindustry.Forexample,DubaiIslamic Bank now operates as an international conglomerate with its investments in Pakistan (Dubai Islamic Bank Pakistan), Jordan and Sudan, etc.

Similarly, ADIB has in the recent years expanded into Egypt and UK. It has very aggressive plans to acquire assets around the world, especially in the MENA region. Al Hilal Bank, another bank owned by the government of Abu Dhabi, already has set up a bank in Kazakhstan and has potential to become a globalleaderintheIslamicfinancialservicesindustry.

Bahrain

Bahrain government has for long used itsfinancialsectorstrategytopromoteand develop IBF in the country to attract foreign capital. With the industry-building organisations like AAOIFI, IIFM, IICRA and LMC, Bahrain remains relevant to the global

Islamicfinancialservicesindustry,althoughsome other players like Malaysia, UAE and now Qatar are gradually claiming the leadership turf from it.

BahrainhasalsobeeninfluentialintermsofitsadvocacyroleintheglobalIslamicfinancialservices industry. Long before any other country, it patronised World Islamic Banking Conference (WIBC), arguably the largest annual gathering of practitioners of IBF in the world. Through such initiatives, the government of Bahrain succeeded in integrating the economy of Bahrain with the other economies in the GCC region.

Kuwait

Kuwait has played a globally visible role in the Islamicfinancialservicesindustry,spearheadedby Kuwait Finance House, which has direct presence in a number of countries, most notably in Bahrain (KFH-Bahrain), Turkey (Kuveyt Turk) and Malaysia (KFH-Malaysia). Apart from Kuwait’s role in setting up Islamic banks, it has been involved in setting up other firmsthatarenowofferingtheirservicestoIslamicbanksandfinancialinstitutions.Mostnotable of such an investment is in International Turnkey Systems (ITS), which is a global player intheIslamicfinancialtechnology.

The government of Kuwait has brought IBF into the mainstream by allowing non-ruling families to freely set up Islamic banks and financialinstitutionsandinsomecasesbydirectly investing in the industry. For example, the government of Kuwait holds almost half of sharesinKFH–oneoftheoldestIslamicbanksintheworld–throughKuwaitInvestmentAuthority(24.08%),PublicAuthorityforMinorAffairs(10.48%),AwqafPublicFoundation(8.29%)andPublicInstitutionforSocialSecurity (6.02%).

Through such institutions, the government of KuwaitattemptstoinfluencedevelopmentsinIBF in other major markets. A detailed analysis ofsuchaninfluenceandcontrolisincludedinthe forthcoming Global Islamic Finance Report 2015, to be released by Edbiz Consulting towardstheendofthefirstquarteroftheyear.

Qatar

The government of Qatar has in the recent years has aggressively acquired Islamic financialassetsaroundtheworld.ThroughIslamicfinancialinstitutions,ithasmademajorinvestments in a number of countries, including Pakistan (e.g., Pak-Qatar Takaful), UK (e.g., Al Rayan Bank, UK), and a number of countries in the MENA region. All Islamic banks in the state of Qatar have direct or indirect patronage of the royal family. Qatar Islamic Bank, Qatar International Islamic Bank and Al Rayan Bank have their presence in multiple jurisdictions

TALKING POINTS

21

ISLAMIC FINANCE REVIEW | WWW.ISFIRE.ORG

and are deemed as global players in the Islamic financialservicesindustry.

B. HNWIs and Families

The following HNWIs and families are the movers and shakers of the global Islamic financialservicesindustry:

A. Prince Mohammed Al Faisal

B. Sheikh Saleh Kamil

C. Sheikh Sulaiman Bin Abdulaziz Al Rajhi

Looking at the above list, one is inclined to conclude that Saudi Arabia holds key to the globalIslamicfinancialservicesindustry,asall the three individuals are in fact Saudis. As mentioned earlier, however, IBF is much more than just being a Saudi phenomenon. A number of countries, and the HNW industrial families therein, own and control Islamic financialinstitutions.Forexample,Randereefamily, a UK-based South African family holds shareholdings(albeitsmall)inIslamicfinancialinstitutions in UK, Pakistan, South Africa and the South East Asia. There are numerous other suchfamiliesthatareinfluentialintheglobalIslamicfinancialservicesindustry.Inthisarticle,we shall restrict our focus to the above three HNWIs.

Prince Mohammed Al Faisal

If someone has to trace a royal connection in the globalIslamicfinancialservices industry, the buck goes back to no other than the late King Faisal Bin Abdul Aziz

Al Saud whose eldest son Prince Mohammed Bin Faisal Al Saud played a pioneering role in developing IBF as a pan-Islamic phenomenon.

Initsfirstphaseofdevelopment,IBFbenefitedfrom the support and patronage of the likes of Prince Mohamed Al Faisal, the founder of Dar Al Maal Al Islami (DMI) Trust - technically a trust but in effect a holding company. Founded in1981,ithasanextensivenetworkstretchingover four continents, with well-integrated regional subsidiaries enabling it to respond to local business needs and conditions. Based on this geographic structure, the DMI Group and associatesactasafinancialbridgebetweentheworld’sleadingfinancialcentresandIslamiccountries.

The Group comprises three main business sectors: Islamic banking, Islamic investment and Islamic insurance.

Islamic banking is exercised in different forms: commercial and retail banking in the Gulf region and other parts of the world; fund management andfinancialservicesinSwitzerlandandJersey.

Islamic investment companies are located in Bahrain, Egypt and Pakistan. There are also associated Islamic insurance companies based in Bahrain and Luxembourg, providing services to the Islamic communities in the Middle East and Europe.

The Board of Supervisors of DMI Trust directs and oversees the business of the Group. DMI Administrative Services S.A., located in Geneva, Switzerland, provides assistance to the Board of Supervisors, in particular in the areas oflegalandfinancialcontrol,auditandriskmanagement and information technology.

DMI Trust is an institution that creates, maintainsandpromotesIslamicfinancialinstitutions. Asset management is one of the Group’s core business activities. Primary success of the business lies in the strategy that it invests clients’ funds prudently along with the principal shareholders’ funds with the objective of earning secular returns, although the businesses and transactions are Shari’a compliant. Given the depth of its investors’ base, DMI has devised a comprehensive range ofIslamicfinancialinstrumentstochannelinvestors’ funds into viable Shari’a compatible operations and investments.

Through DMI Trust, Prince Mohammed developed a network of Faisal Banks in different parts of the Islamic world, notably in Pakistan, Egypt and Sudan. After a lot of restructuring of the group and a series of mergers and acquisitions, Faisal Bank brand haslostitssignificanceinthemainstreamIBF,although the founding shareholders in the DMI Trust continues to hold stake in a number of Islamic banks, most notably Ithmaar Bank of Bahrain.

Although Prince Mohammed Al Faisal’s visibility in IBF has decreased following the restructuring of the DMI Trust, there is no doubt that his vision and strategic thinking remain central to the development of institutions owned by the DMI Trust. He is most widely revered in the Muslim world, and is treated with due respect in the Western world. Although after 9/11, there were attempts to tarnish his image, people like Richard A. Debs, an advisory director at Morgan Stanley and vice chairman of the United States-Saudi Arabian Business Council, thinks, “Prince Mohammed has been unfairly persecuted and attacked. I just don’t see the connection between Islamic financeandIslamicextremism.”

The new face of DMI Trust is Prince Amr Mohammed Al Faisal, a son of Prince Mohammed Al Faisal. DMI Trust continues to holdinterestsin55Islamicbanksandfinancialinstitutions around the world, although Ithmaar Bank is now the new face of the businesses owned by it.

Based in Bahrain, Ithmaar Bank is now the flagshipinstitutionofDMITrust,whichholdsinterests in a number of banks and non-bank financialinstitutionsinanumberofcountries.In February 2013, Ithmaar Bank merged with one of its Bahrain-based associates, First LeasingBank,increasingitscapitaltoUS$758million.

Sheikh Saleh Kamil

Anotherinfluentialpersonality in IBF is Sheikh Saleh Kamil, founder and Chairman of Dallah Al Baraka Group that owns Al Baraka Banks in Bahrain, Pakistan, Bangladesh,

with strong presence in other OIC countries Jordan, Tunisia, Sudan, Turkey, Egypt, Algeria, South Africa, Lebanon, Syria, Iraq, Saudi Arabia, Indonesia and Libya.

Interestingly, like his other peer, Prince Mohammed Al Faisal, Sheikh Saleh Kamel chose to operate outside his native Saudi Arabia. This was supposedly a deliberate pan-Islamicstrategytobenefitfromthevastmarketof the OIC comprising 56 countries.

Sheikh Sulaiman Bin Abdul Aziz Al Rajhi

The largest Islamic banks by size are arguably the Iranian state-owned banks. Outside Iran, Al Rajhi Bank is the largest Islamic bank in terms of assets under

management and market capitalisation. The principal shareholders of the bank are Al Rajhi family,whichisaninfluentialindustrialistfamilyin the Kingdom of Saudi Arabia.

Although Sheikh Sulaiman Al Rajhi has now retired from all of his businesses after donating his personal wealth, Al Rajhi Holding continues to play a dominant role through several of his sons. Outside Saudi Arabia, the family owns Al Rajhi Bank in Malaysia, and a number of companies(industrialaswellasfinancial)throughout the world.

C. Regulatory Bodies