Embed Size (px)

Citation preview

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

20

EXAMINING CONSUMERS’ CONTINUANCE INTENTION AND BRAND LOYALTY IN ISLAMIC INSURANCE (TAKAFUL)

Norazah Mohd Suki1, Mohd Anas Mentoh2 and Norbayah Mohd Suki3

Abstract

The goals of this research are threefold: (1) to examine intrinsic motives, extrinsic motives, and satisfaction impact upon consumers’ positive electronic-word-of-mouth (E-WOM) in respect of Islamic insurance (Takaful), (2) to investigate the influence of positive E-WOM and satisfaction on consumers’ continuance intention in respect of Takaful, and (3) to explain the effect of satisfaction and continuance intention on consumers’ brand loyalty in respect of Takaful. A quantitative approach was applied through a self-administered questionnaire to obtain data from 300 Takaful subscribers in the Generation Y group. They were pre-screened and identified through their online postings, having any Takaful policy, and being referred to by Takaful advisors and operators. Empirical results of the Partial Least Square-Structural Equation Modelling (PLS-SEM) approach discovered that intrinsic motives, extrinsic motives, and satisfaction affect consumers’ positive E-WOM regarding Takaful. Additionally, the effect of positive E-WOM on consumers’ continuance intention in Takaful is found to be significant. Satisfaction emerges as the strongest predictor of consumers’ continuance intention in Takaful. Further, the study reveals that satisfaction influences consumers’ brand loyalty in respect of Takaful. Approachable and pleasant Takaful frontline advisors/agents who can provide a prompt response to consumers, are vital in the process of increasing consumer satisfaction and boosting loyalty to their brand. Understanding positive E-WOM, consumers’ satisfaction, continuance intention, and brand loyalty in respect of Takaful permit Takaful operator to be more active and responsive in the online medium on a daily basis, and thereby be in a position to encourage more interaction and response among consumers with regards to their Takaful participation. This would prolong the positive relationship between the Takaful operators with their consumers. Directions for future research are suggested.

Keywords: brand loyalty, continuance intention, E-WOM, motives, satisfaction

INTRODUCTION The Islamic insurance (Takaful) sector has become one of the leading Islamic finance mechanisms that uphold economic growth. Indeed, it represents the second most valued social organization in all Muslim societies through its instrumentality in combatting impoverishment (Hassan et al., 2014). Syarikat Takaful Malaysia Berhad was the first Takaful operator to offer family Takaful, and general Takaful business in Malaysia; and in order to enhance consumers’ emergent needs and continuance intention in Takaful, it has also introduced an online sales portal and integrated online marketing initiatives (The Star Online, 2017). However, the growth of Takaful is considered marginal compared to that of conventional insurance, despite the fact that Takaful was established over three decades ago (Yazid et al., 2012). For instance, in Malaysia, the penetration rate of life insurance (41% of the population) is higher than family Takaful (15% of the population), as reported by RAM Ratings (2017). This is not surprising since research has identified the low awareness about and understanding of the importance of subscribing to Takaful rather than to life insurance (Zakaria et al., 2016). Consequently, the issue of whether Takaful policyholders remain loyal to their existing Takaful operators or convert to conventional insurance is an important one to explore.

It is true that there has been wide-ranging research activity in the area of consumer behaviour and insurance, but certain aspects of this literature, such as consumers’ positive electronic -word-of-mouth (E-WOM), continuance intention, and brand loyalty in the context of Takaful, have captured

1 Othman Yeop Abdullah Graduate School of Business, Universiti Utara Malaysia, Malaysia 2 Labuan Faculty of International Finance, Universiti Malaysia Sabah, Malaysia 3 School of Creative Industry Management & Performing Arts, Universiti Utara Malaysia, Malaysia

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

21

only slight attention from scholars (Yazid et al., 2012; Zakaria et al., 2016). In terms of consumer purchase decisions, these are shown to be based mainly on WOM and the recommendations made by friends and family members (Méndez-Aparicio et al., 2017). Further, Saad (2012) has stressed that Takaful operators need to identify and treasure those factors that affect consumers’ continuance intention and brand loyalty in respect of Takaful if they wish to elevate their business performance and sustainability, and thereby survive in the current challenging economic development. Consequently, the goals of this research are threefold: (1) to examine intrinsic motives, extrinsic motives, and satisfaction impact upon consumers’ positive E-WOM in respect of Islamic insurance (Takaful), (2) to investigate the influence of positive E-WOM and satisfaction of consumers’ continuance intention in respect of Takaful, and (3) to explain the effect of satisfaction and continuance intention on consumers’ brand loyalty in respect of Takaful. In addressing these goals, the study helps to fill the current gap in the literature. It does this by drawing on the Expectation Confirmation Model and Motivation Theory, and deliberating upon the ways in which positive E-WOM and satisfaction influence the intention of consumers to subscribe to Takaful, and how sa tisfaction with the brand can affect consumers’ loyalty to it. Respondents were pre-screened and identified through their online postings, having any Takaful policy, and being referred to by Takaful advisors and operators.

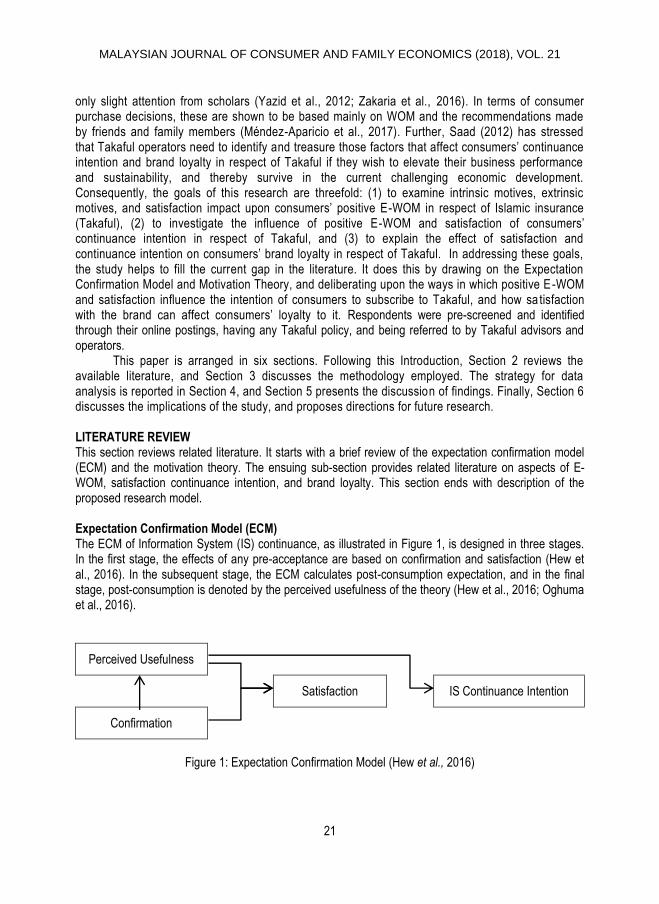

This paper is arranged in six sections. Following this Introduction, Section 2 reviews the available literature, and Section 3 discusses the methodology employed. The strategy for data analysis is reported in Section 4, and Section 5 presents the discussion of findings. Finally, Section 6 discusses the implications of the study, and proposes directions for future research. LITERATURE REVIEW This section reviews related literature. It starts with a brief review of the expectation confirmation model (ECM) and the motivation theory. The ensuing sub-section provides related literature on aspects of E-WOM, satisfaction continuance intention, and brand loyalty. This section ends with description of the proposed research model. Expectation Confirmation Model (ECM) The ECM of Information System (IS) continuance, as illustrated in Figure 1, is designed in three stages. In the first stage, the effects of any pre-acceptance are based on confirmation and satisfaction (Hew et al., 2016). In the subsequent stage, the ECM calculates post-consumption expectation, and in the final stage, post-consumption is denoted by the perceived usefulness of the theory (Hew et al., 2016; Oghuma et al., 2016).

Perceived Usefulness

Satisfaction IS Continuance Intention

Confirmation

Figure 1: Expectation Confirmation Model (Hew et al., 2016)

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

22

Motivation Theory Motive is defined as “a psychological state that induces, directs and maintains human behaviour” (Woolfolk, 1995). It is categorized into intrinsic motives and extrinsic motives (see Figure 2. Intrinsic motives are related to gaining pleasure by completing an activity and not due to receiving rewards (Berdud et al., 2016). Extrinsic motives refer to the reward received due to finishing a task (Ryan and Deci, 2000). Scholars such as Llopis and Foss (2016), Yoo et al. (2013), and Zohar et al. (2015), have found that intrinsic and extrinsic motives affect consumers’ E-WOM participation.

Intrinsic Motivation

E-WOM Participation

Extrinsic Motivation

Figure 2: Motivation Theory (Yoo et al., 2013)

This study predicts that intrinsic and extrinsic motives will influence consumers’ positive E-WOM

about Takaful. Therefore, based on the literature above, the following hypotheses are put forward:

H1: Intrinsic motives positively affect consumers’ positive E-WOM about Takaful. H2: Extrinsic motives positively affect consumers’ positive E-WOM about Takaful.

E-WOM E-WOM can be defined as “any positive or negative statement made by potential, actual, or former customers about a product or company, which is made available to a multitude of people and institutions via the Internet” (Hennig-Thurau and Walsh, 2003, p. 51). Consumer purchase decisions are heavily influenced by E-WOM, and it is an important predictor in the Internet shopping market (Enginkaya and Yilmaz, 2014; Stauss, 1997). Convincing and updated social media messages and campaigns do influence consumers’ brand loyalty (Erdogmus and Cicek, 2012; Pauwels et al., 2016). Indeed, E-WOM has been seen to impact heavily young consumers’ brand loyalty and purchase intention – more so than the influence of their counterparts (Yan et al., 2017). Likewise, other researchers have reported positive E-WOM to have a positive relationship with continuance intention (Chen et al., 2012). In this study, therefore, it is assumed that consumers may develop positive intentions towards Takaful on experiencing favourable E-WOM. Hence, the following hypothesis is postulated:

H3: Positive E-WOM about Takaful favourably affects consumers’ continuance intention in

respect of Takaful. Satisfaction and Continuance Intention Satisfaction is related to the establishment of growing feelings among multiple dealings with products and service providers (San-Martin and López-Catalán, 2013). When consumers are satisfied with their use of certain products, they are incline to spread positive WOM about them via online information channels (Chen et al., 2012; Hennig-Thurau et al., 2004; Jin et al., 2009). Greater customer satisfaction

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

23

results in increased customer intention to remain loyal to the product concerned, and other related products (Bhattacherjee, 2001; Chen et al., 2012; Chou et al., 2010). Research conducted by Hsiao et al. (2016) has asserted satisfaction to be a strong predictor of consumers’ continuance intention, thereby showing that satisfied customers tend to develop an intention to continue their purchases of the product involved. It is also indicated in the marketing literature that satisfaction plays a vigorous role in predicting consumers’ continuous behaviours (Gao et al., 2015; Gilani et al., 2017; Iranmanesh et al., 2017; Weng et al., 2017). In this study, therefore, it is suggested that satisfaction influences consumers’ positive E-WOM and consumers’ continuance intention in subscribing to Takaful. Accordingly, the next hypotheses are posited:

H4: Satisfaction positively affects consumers’ favourable E-WOM in respect of Takaful. H5: Satisfaction positively affects consumers’ continuance intention in respect of Takaful.

Brand Loyalty Brand loyalty is referred to as “favourable emotion towards the brand and extreme dedication to buy the same products and services frequently of the same brand, despite competitors’ move or changes in the surroundings” (Lazarevic, 2012 p. 45). Through brand loyalty, companies’ expenditure on marketing activities is minimal, which leads to minimal cost being incurred in retaining existing customers compared to that required in attracting new customers (Lazarevic, 2012). The literature to date has asserted that customer satisfaction affects consumers’ brand loyalty (Hassan et al., 2014; Hew et al., 2016), with younger consumers developing higher levels of brand loyalty than their middle-aged counterparts (Yeh et al., 2015). Consumers prolong their intention to continue repurchase, strengthen their loyalty towards product brands, and make recommendations to friends and family members as a result of their having experienced a high level of satisfaction with those products (Georgescu and Popescul, 2015; Hew et al., 2016; Hudson et al., 2015). In line with these observations, therefore, it is predicted that satisfaction and continuance intention affect consumers’ brand loyalty in respect of Takaful, and hence, the following hypotheses are offered:

H6: Satisfaction positively affects consumers’ brand loyalty towards Takaful. H7: Continuance intention positively affects consumers’ brand loyalty towards Takaful.

Research Model This research applies the Expectation Confirmation Model and Motivation Theory as guiding principles, and incorporates brand loyalty in the proposed research model. Specifically, the research tests whether intrinsic motives, extrinsic motives, and satisfaction affect consumers’ positive E-WOM of Takaful (see Figure 3). In addition, it examines the effect of positive E-WOM and satisfaction on consumers’ continuance intention in Takaful, and explores the impact of brand loyalty towards Takaful as resulting from consumers’ satisfaction with and continuance intention towards Takaful.

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

24

Intrinsic Motives H1 H3

Positive E-WOM Continuance Intention

Extrinsic Motives H2 H4 H5 H7

Satisfaction H6 Brand Loyalty

Figure 3: Proposed Research Framework

METHODOLOGY Participants and Procedure A quantitative approach was applied through a self-administered questionnaire to obtain data from 300 Takaful subscribers in the Generation Y grouping. Generation Y was chosen because they are the highest adopters of the mobile Internet and less brand loyal, making them viable as a research category (Chuah et al., 2017). The data were collected via a purposive sampling technique whereby they were pre-screened and identified through their actions of performing online postings, having any Takaful policy, and being referred to by Takaful advisors and operators.

After eliminating unusable questionnaires, a sample of 288 respondents remained, yielding a response rate of 96%. This size of sample is acceptable as it exceeds the criteria identified by Hair et al. (2017), who indicate the need for a sample to be at least ten times the largest number of structural paths directed at a particular latent construct in the structural model. Given the number of measurement items (24) in the current study, the requirement was for 240 samples, which are exceeded.

Questionnaire Development and Instrument The questionnaire was designed in three sections. Section A gathered data relating to general demographic characteristics, Section B contained questions related to the respondents’ experience with Takaful, and Section C included 24 statements concerning intrinsic motives (6 items), extrinsic motives (3 items), satisfaction (4 items), E-WOM (3 items), continuance intention (3 items), and brand loyalty (5 items). These statements were designed using a five-point Likert scale, ranging from 1 (strongly disagree) to 5 (strongly agree). Details of the questionnaire design and the sources of the items adopted appear in Appendix 1.

Statistical Technique The data were analyzed using the descriptive analysis and the Partial Least Square-Structural Equation Modelling (PLS-SEM) approach. The latter was supported by Smart-PLS 2.0 to examine the research hypotheses. PLS-SEM was chosen because “the research has multiple constructs, each represented by several measured variables and allows for all of the relationship/equations to be estimated simultaneously” (Hair et al., 2010, p. 641). It also accentuates aspects such as measurement scales, size of the sample, and residual distributions (Fornell and Bookstein, 1982).

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

25

DATA ANALYSIS The demographic characteristics of the respondents are presented in Table 1. Of the 288 respondents, more than half were males (56%). In terms of age, approximately 44% of the research participants were less than 28 years old, followed by 31% 29-33 years old, and 25% more than 34 years old. More than sixty percent of the respondents possessed a Bachelor’s degree (64%), followed by Diploma (20%), SPM (6%), Master’s Degree (5%), STPM/Matriculation (4%), and PhD (1%). Three-quarters of respondents earned less than RM5,500 per month, and the rest earned over that amount. Such backgrounds denoted that samples comprised young and educated respondents with some spending power.

Table 1: Demographic Profile of Respondents

Variables Frequency Percentage

Gender

Male

Female

162

126

56.2

43.8

Age

≤ 23

24-28

29-33

34-37

6

120

90

72

2.0

41.7

31.3

25.0

Educational Level

SPM

STPM/Matriculation

Diploma

Bachelor Degree

Master

PhD

18

12

57

183

15

3

6.3

4.2

19.8

63.5

5.2

1.0

Monthly Income

≤ RM2,500

RM2,501 – RM3,500

RM3,501 - RM4,500

RM4,501 – RM5,500

≥ RM5,501

102

75

21

18

72

35.4

26.0

7.3

6.3

25.0

Takaful Experiences The frequency distributions of the respondents’ Takaful experiences such as their length of Takaful subscription, how they were introduced to Takaful, the number of Takaful subscriptions in their households, and main reasons for subscribing to Takaful are displayed in Table 2. A small number of respondents (15%) had less than one year’s experience of subscribing to Takaful, 64% had between one and six years’ such experience, and 21% had more than seven years’ experience in this respect.

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

26

Takaful agents were reported as being the most important sources of information, followed by recommendations by friends and family members. The next important sources were documented as brochures and commercial advertisements. When asked about the number of Takaful subscriptions in their household, 40% of the respondents reported less than three, 38% indicated four to six, and 22% had more than seven. Respondents also reported their top three reasons for subscribing to Takaful as being for health protection, Halal (Shariah) compliance, and investment purposes respectively. Based on these experiences, it can be concluded that respondents have positive acceptance towards Takaful subscriptions and are aware of its significance.

Table 2: Takaful Experiences

Variables Frequency Percentages

Length of Takaful Subscription

≤1 Year

1-3 Years

4-6 Years

7-10 Years

≥ 10 Years

45

90

93

45

15

15.6

31.3

32.3

15.6

5.2

Sources Introduced to Takaful

Takaful Agent

Family and Friends

Commercial Advertisement

Brochures

144

123

6

15

50.0

42.7

2.1

5.2

Number of Takaful Subscriptions in a household

≤ 3 subscriptions

4-6 subscriptions

7-10 subscriptions

≥ 11 subscriptions

117

108

48

15

40.6

37.5

16.7

5.2

Main Reasons for Subscribing to Takaful

Health Protection

Investment Purpose

Halal (Shariah Compliance)

192

39

57

66.6

13.6

19.8

Partial Least Squares - Structural Equation Modelling A PLS-SEM approach was adopted in which Smart-PLS version 2.0 enabled the assessment and verification of the measurement model, and the testing of the underlying relationships between the variables of the structural model as outlined in the proposed hypotheses. A bootstrapping analysis of 500 subsamples was undertaken to estimate the formulated hypotheses of the structural model. PLS-SEM was chosen to avoid inadmissible solutions and factor indeterminacy, and to allow for instantaneous testing of hypotheses, despite permitting the use of both reflective and formative constructs (Fornell and Bookstein, 1982).

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

27

Measurement Model The measurement model was scrutinized to determine the internal consistency reliability, convergent validity, and discriminant validity of the measured items. Before that, the common method bias was checked by following suggestions of Podsakoff et al. (2003). Firstly, respondents were guaranteed anonymity. Next, while designing the questionnaire, the statements of the dependent variable were not placed near the independent variables. In the third step, Harman's single-factor test was computed based on principal component analysis (PCA) using the varimax rotation method (Podsakoff et al., 2003). Specifically, all variables were entered into an exploratory factor analysis using the Statistical Package for the Social Sciences (SPSS) version 21.0. By doing this, six components with eigenvalues greater than 1.0 were extracted which accounted for 78.7% of the variance in the data. Indeed, the first factor accounted for 38.2% of the variance. Hence, this result suggests that common method bias did not appear to be an issue. Next, Cronbach’s alpha and composite reliability were established to check the reliability of the measurement items. Table 3 presents the Cronbach’s alphas and composite reliability statistics for all the variables, showing these to have surpassed the value of 0.70 as recommended by Hair et al. (2017), and thereby testifying to the robustness of the measurements.

Table 3: Construct Reliability and Validity

Factors Cronbach's Alpha Composite Reliability Average Variance Extracted

Intrinsic Motives 0.964 0.971 0.848

Extrinsic Motives 0.945 0.965 0.901

Satisfaction 0.806 0.888 0.726

E-WOM 0.831 0.899 0.748

Continuance Intention 0.822 0.894 0.738

Brand Loyalty 0.945 0.958 0.819

Convergent Validity Convergent validity was measured based on the factor item loadings, composite reliability, and average variance extracted (AVE). A satisfactory outcome is one where the values of the factor item loading and composite reliability are in excess of 0.70 (Hair et al., 2017), and the AVE values are above 0.50 (Fornell and Larcker, 1981). Table 4 illustrates that these criteria are met, indicating that the factor items represented the classifiable factors well.

Table 4: Standardized Factor Loadings and Cross Loadings

Items Intrinsic

Motives

Extrinsic

Motives

Satisfaction EWOM Continuance

Intention

Brand Loyalty

IntM1 0.923 0.106 0.572 0.680 0.613 0.335

IntM2 0.945 0.159 0.638 0.699 0.686 0.375

IntM3 0.928 0.133 0.612 0.665 0.685 0.361

IntM4 0.934 0.154 0.615 0.681 0.647 0.321

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

28

IntM5 0.882 0.185 0.484 0.614 0.519 0.354

IntM6 0.910 0.192 0.505 0.622 0.544 0.356

ExtM1 0.126 0.933 -0.098 0.142 -0.087 0.033

ExtM2 0.208 0.978 -0.015 0.186 0.011 0.111

ExtM3 0.123 0.936 -0.023 0.119 -0.042 0.000

Sat1 0.475 -0.076 0.733 0.637 0.573 0.366

Sat3 0.543 0.022 0.889 0.580 0.738 0.561

Sat4 0.568 -0.038 0.922 0.614 0.711 0.527

EWOM1 0.455 0.185 0.443 0.770 0.496 0.290

EWOM2 0.639 0.152 0.686 0.895 0.567 0.422

EWOM3 0.734 0.101 0.687 0.923 0.656 0.378

Ci1 0.521 -0.025 0.651 0.490 0.844 0.392

Ci2 0.622 -0.015 0.717 0.578 0.915 0.453

Ci3 0.581 -0.053 0.679 0.646 0.816 0.433

BL1 0.265 -0.021 0.471 0.314 0.397 0.880

BL2 0.320 0.008 0.566 0.381 0.462 0.943

BL3 0.362 0.026 0.535 0.380 0.530 0.901

BL4 0.425 0.105 0.521 0.444 0.486 0.906

BL5 0.342 0.156 0.501 0.395 0.360 0.891

Note: Bold values are item loadings above 0.70. Discriminant Validity Discriminant validity was assessed by ensuring that the square root of the AVE of each factor was higher than the inter-construct correlations in the model (Fornell and Larcker, 1981). Table 5 shows this to be the case, thereby endorsing the claim of discriminant validity. Furthermore, all the inter-construct correlation coefficients were below 0.70, thus testifying to adequate discriminant validity, and the absence of multicollinearity (Sussman and Siegal, 2003; Tabachnick and Fidell, 2007).

Table 5: Inter-construct Correlations and Square Root of AVE Measures

Factors 1 2 3 4 5 6

1 Intrinsic Motives 0.921

2 Extrinsic Motives 0.167 0.949

3 Satisfaction 0.623 -0.033 0.852

4 E-WOM 0.618 0.162 0.613 0.865

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

29

5 Continuance Intention 0.671 -0.036 0.695 0.668 0.859

6 Brand Loyalty 0.380 0.060 0.575 0.424 0.497 0.905

Mean 4.609 2.594 4.743 4.757 4.795 4.535

Standard deviation 0.720 1.575 0.461 0.476 0.437 0.655

Skewness -2.254 0.434 -1.850 -2.527 -2.669 -1.351

Kurtosis 5.124 -1.398 3.004 7.476 7.815 1.040

Note: The diagonal element in Italics and bold font shows the square root of AVE of each factor.

Referring to the correlation coefficients in Table 5, it is seen that satisfaction is significantly correlated with the consumers’ continuance intention in respect of their subscription to Takaful (r=0.695, p<0.01). Indeed, this linkage is extremely significant among the inter-construct correlations. Additionally, the means for all the constructs range from 2.594 to 4.795 on a 5-point Likert scale of 1=strongly disagree to 5=strongly agree, confirming that the respondents mainly expressed positive opinions regarding Takaful.

Structural Model In the structural model, the statistical significance of the path estimates of the hypothesized relationships between the latent variables was assessed by using path estimates and t-tests through a bootstrapping resampling technique with 500 sub-samples (Yi and Davis, 2003). The R² of the endogenous latent variables of the structural model is comprised of 65% continuance intention, 64% E-WOM, and 34% brand loyalty (see Table 6). The R-squares are beyond 0.10, which infers the appropriateness of the predictive fitness of the structural model with the collected data (Falk and Miller, 1992).

Table 6: PLS Results of Path Coefficients and Hypothesis Testing for Direct Effects

Relationships Path Estimates t-values R² Results

H1 Intrinsic Motives EWOM 0.415* 11.760 0.640 Supported

H2 Extrinsic Motives EWOM 0.107* 5.988 Supported

H3 EWOM Continuance Intention

0.205* 3.516 0.650 Supported

H4 Satisfaction EWOM 0.458* 10.792 Supported

H5 Satisfaction Continuance Intention

0.649* 12.345 Supported

H6 Satisfaction Brand Loyalty 0.489* 6.208 0.340 Supported

H7 Continuance Intention

Brand Loyalty 0.108 1.489 Not Supported

Note: * p<0.05

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

30

Table 6 displays the results of the path estimates and t-values of the structural model showing that H1 to H6 are supported, but that H7 is not. Specifically, intrinsic motives have a significantly positive influence on consumers’ E-WOM regarding Takaful (β1=0.415, t=11.760, p<0.05), and thus, H1 is retained. Likewise, extrinsic motives exert a significant positive influence on the consumers’ E-WOM about Takaful (β2=0.107, t=5.988), hence proving the validity of H2. Indeed, the linkages between the positive E-WOM regarding Takaful and the consumers’ continuance intention in Takaful are significant at p<0.05 (β3= 0.205, t=3.516). Hence, H3 is maintained, as expected. Further examination of the PLS-SEM results of the structural model in Table 6 shows that satisfaction has a significant positive impact on the consumers’ E-WOM about Takaful (β4=0.458, t=10.792, p<0.05), accepting H4 as predicted. Indeed, the relationships between satisfaction and consumers’ continuance intention in Takaful is positive and significant (β5=0.649, t=12.345). Thus, H5 is reinforced. Path coefficients also show that satisfaction is significant and positively influences the consumers’ brand loyalty in respect of Takaful (β6= 0.489, t=6.208), as postulated by H6. Thus, H6 is reinforced. However, the empirical result indicates a non-significant effect between the continuance intention and consumers’ brand loyalty towards Takaful (β7=0.108, t=1.489, p>0.05). Thus, H7 is not upheld.

DISCUSSION This study has examined the impacts of intrinsic motives, extrinsic motives, and satisfaction on consumers’ E-WOM about Islamic insurance (Takaful). It has also investigated the influence of positive E-WOM and satisfaction on consumers’ continuance intention to subscribe to Takaful, and it has explored the effect of satisfaction and continuance intention on consumers’ brand loyalty towards Takaful. The PLS-SEM approach, as pictured in Figure 4, reveals that intrinsic (t-value=11.760) and extrinsic (t-value=5.988) significantly affect consumers’ positive E-WOM concerning Takaful, implying that H1 and H2 are supported. This finding conforms to findings from previous studies which have shown that intrinsic motives and extrinsic motives significantly affect E-WOM in a positive way (Yoo et al., 2013).

Figure 4: Path Diagram of PLS-SEM (bootstrapping)

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

31

The respondents indicated their inclination to make statements or post reviews online regarding Takaful because of their positive experience of Takaful and their subsequent desire to share this with others. Essentially, they believe it is right to enlighten others, since through doing so others may be motivated to purchase Takaful policies that suit their needs, and bring benefit to them. In other words, they voluntarily share their positive Takaful experiences online (E-WOM) so that others can benefit. Sometimes, these individuals are given remuneration for their reviews or other comments about Takaful, and they are also offered discount coupons/rebates on their monthly savings in Takaful. Furthermore, these Takaful reviewers may include those who are existing Takaful consultants who are knowledgeable about the same subject area. Most importantly, intrinsic motives are the strongest predictor of consumers’ positive E-WOM concerning Takaful, followed by satisfaction, and extrinsic motives.

Next, the analysis of the data shows that H3 is upheld as it was found that positive E-WOM about Takaful significantly influences consumers’ continuance intention to subscribe to Takaful (t-value=3.516). Customers are keen to disseminate positive information regarding Takaful to others and are prepared to invite family and friends to also take part in Takaful. This outcome concurs with that found in other studies reported in the literature. For instance, Chen et al. (2012), and Hennig-Thurau et al. (2004) found that satisfaction results in positive E-WOM among consumers. And the current study reports the same, i.e., satisfaction is a significant predictor of consumers’ positive E-WOM about Takaful (t-value=10.792). Thus, H4 is also supported. Indeed, the participants in this study admitted that subscribing to Takaful makes them feel secure and fully satisfied with their decisions. These findings echo the results obtained by Chen et al. (2012).

A closer inspection of the quantitative results as pictured in Figure 4 disclosed that H5 is strongly held for the reason that satisfaction significantly and positively affected consumers’ continuance intention in subscribing to Takaful (t-value=12.345). With a satisfactory experience of Takaful, consumers anticipated that they would continue with their Takaful membership and subscriptions. They also believed they could and would be inspirational in persuading others to subscribe to Takaful. These results corroborate the findings of prior studies. Amblee (2016) affirmed that the sales of insurance and continuance intention are influenced by satisfaction and positive E-WOM of the consumer, the higher the satisfaction and positive E-WOM among consumers, the higher the generated sales and continuance intention. This is because one prior positive experience in using the product or services may influence other future experiences.

Furthermore, this study also testifies that satisfaction significantly influences the consumers’ brand loyalty towards Takaful as its t-value=6.208, implying that H6 is also supported. Thus, the result suggests that consumers who have a higher level of satisfaction with Takaful will develop strong loyalty to the same Takaful brand. This finding is also comparable with previous research works by Hassan et al. (2014) who found that satisfaction positively impacted upon consumers’ brand loyalty. Brand loyalty stimulates strong price premiums, revenue and profit growth, reduces marketing and operating costs, increases referrals, and adds competitive advantage (Tepeci, 1999). However, this research discovers that continuance intention has an insignificant impact on consumers’ brand loyalty towards Takaful (t-value=1.489), thereby rejecting H7. This shows that even if consumers are willing to continue their Takaful participation with a specific Takaful operator, they tend to participate in other policy plans with other Takaful operators as their loyalty is not permanent. The finding of a non-significant relationship between continuance intention and consumers’ brand loyalty towards Takaful is inconsistent with the works of Georgescu and Popescul (2015), Hew et al. (2016), and Hudson et al. (2015).

CONCLUSION As a conclusion, intrinsic motives, extrinsic motives, and satisfaction affect consumers’ E-WOM about

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

32

Takaful, promoting favourable impressions of the product among readers. What’s more, the effect of positive E-WOM on consumers’ continuance intention in Takaful is significant. Interestingly, satisfaction is found to be the strongest significant contributing factor in predicting consumers’ continuance intention in respect of Takaful. Indeed, consumers’ brand loyalty towards Takaful is also affected by satisfaction. Implications of Study The findings from this empirical study have highlighted some important research and practical implications for consumers, as E-WOM, consumers’ continuance intention, and brand loyalty remain as essential research issues. Takaful marketers should stimulate the intrinsic motives and extrinsic motives within consumers so that they want to share their experience, belief, satisfaction, and excitement through E-WOM. These intrinsic motives can be triggered by creating better online platform such as a forum page where each consumer can share his/her experience with the others. Such an improved platform would allow the Takaful operator to be active and responsive in the online medium on a daily basis, and thereby be in a position to encourage more interaction and response among consumers with regards to their Takaful participation. To increase the consumers’ extrinsic motives, Takaful operators should introduce more rewards/discounts or promotional compensation for those who are willing to share their positive experiences through the online medium. This is mainly because positive E-WOM among consumers has a favourable impact on their continuance intention in respect of Takaful participation, and this effect may prolong the positive relationship between the Takaful operators with their consumers. It is imperative for Takaful operators to retain their existing customers rather than seeking new customers for business sustainability.

Besides, marketers should start to think in a serious way about capitalizing upon the availability of online platforms that can obviously reach out to their customers. Since it has been proven that consumers’ E-WOM does affect their continuance intentions in respect of Takaful participation, cyber marketing, electronic marketing and/or digital marketing are necessary strategies if this particular industry is to guarantee its customer retention. Building a continuous rapport with the consumers, through online social media such as Facebook, Instagram, LinkedIn, and many other leading social media networking sites is imperative. Most importantly, an online platform permits business brands to capture more loyal customers within the circle of virtual social communities, as observed by Bagozzi and Dholakia (2002), Dwyer (2007), Laroche et al. (2013), and Nambisan and Baron (2007). Communication and the dissemination of information about favourite brands via social media encourages consumers to cultivate strong bonds with the brands, and cause them to be keen to recommend the brands company to others (Georgescu and Popescul, 2015; Hudson et al., 2015). Marketers need to strive harder in creating optimum satisfaction among other consumers including those from Generation Y because this market segment is prone to resist traditional marketing and to become loyal customers (Lazarevic, 2012).

Further, Takaful operators should strive to enhance their level of service to maximize consumers’ satisfaction. Prompt responses given by approachable and pleasant Takaful advisors who are the frontline agents in this scenario, help to increase customer satisfaction. The underwriting and claiming processes should be efficiently and swiftly undertaken to avoid dissatisfaction among consumers. Increasing the satisfaction level of Takaful’s participants would help to build their brand loyalty; and customers with a high sense of brand loyalty are beneficial to all organizations as they help to increase revenue and profit, as well as to develop organizational productivity. From the academic perspective, this study advances the body of knowledge regarding the factors that affect E-WOM, continuance intention, and brand loyalty of consumers in respect of Takaful.

This study has integrated the Expectation Confirmation Model and Motivation Theory with the model used, to produce a framework which is relevant to the concept of Takaful in a developing nation.

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

33

Its empirical results have confirmed both models as being appropriate to examine the impacts of positive E-WOM and satisfaction on consumers’ continuance intention. They are also found to be appropriate models to investigate the effect of satisfaction and continuance intention on consumers’ brand loyalty towards Takaful. Empirically, through the PLS-SEM approach, the postulated hypotheses are supported as predicted, with the exception of H7. The findings of this research identify satisfaction as being a significant predictor of consumers’ continuance intention to subscribe to Takaful. Additionally, this study reveals that satisfaction influences consumers’ brand loyalty towards Takaful.

Limitation and Recommendations Future studies are recommended to inspect the suitability of the proposed model for various types of insurance policies, such as life insurance and general insurance, apart from Takaful. The inclusion of these new areas would broaden the scope of the research; enlarging the size of the sample to go beyond the setting of developing nations is also necessary to improve the generalizability of the results. Additionally, a comparative study involving Takaful operators to determine the level of positive or negative E-WOM is also imperative. Issues of trust and loyalty are also applicable for examinations (Suki, 2012; Suki and Suki, 2016). APPENDIX

Appendix 1: Measurement Constructs

Construct Items Source

Intrinsic Motives

(I write comments on customer review because…)

I want to help others with my own positive experience in Takaful participation.

I want to give others the opportunity of buying the right Takaful participation.

This way I can express my joy about good Takaful participation.

I feel good when I can tell others about my Takaful participation successes.

I believe a chat among like-minded people is nice thing.

It’s fun to communicate this way with other people in the community.

Yoo et al. (2013)

Extrinsic Motives

(I write comments on customer review about Takaful because…)

…of incentives I receive (e.g cyber money)

…I receive a reward for my writing

…I can get discount coupons/rebates on my monthly savings in Takaful.

Yoo et al. (2013)

Positive

E-WOM

I am willing to recommend this Takaful service and its other product/services to others

I usually say positive things about this Takaful and its product/services.

I will tell my family/friends to participate in Takaful Policy.

Hew et al. (2016)

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

34

Satisfaction My choice to participate in Takaful was a wise one.

I am happy that I participate in Takaful savings.

Participating Takaful subscription makes me feel very satisfied.

Participating Takaful subscription makes me feel very

delightful.

Hew et al. (2016)

Continuance Intention to use Takaful

I intend to continue my participation in Takaful Insurance rather than discontinue it.

If I could, I would like to continue participating Takaful subscription.

I will strongly recommend others to participate in Takaful.

Hew et al. (2016)

Brand Loyalty (If a business brand provides Takaful schemes services),

…I like it more than other brands.

…I have strong preference for it.

…I give prior consideration to it when I have a need for a product or service of this type.

…I would recommend it to others.

…I will stay with the brand.

Hew et al. (2016)

REFERENCES Amblee, N. (2016). The impact of E-WOM density on sales of travel insurance. Annals of Tourism

Research, 56(2016), 128-163. Bagozzi, R.P., & Dholakia, U.M. (2002). Intentional social action in virtual communities. Journal of

Interactive Marketing, 15(2), 2-21. Berdud, M., Cabasés, J.M., & Nieto, J. (2016). Incentives and intrinsic motivation in healthcare. Gaceta

Sanitaria, 30(6), 408-414. Bhattacherjee, A. (2001). Understanding information systems continuance: An expectation-confirmation

model. MIS Quarterly, 25(3), 351-370. Chen, S.C., Yen, D.C., & Hwang, M.I. (2012). Factors influencing the continuance intention of the usage

Web 2.0: An empirical study. Computers in Human Behaviour, 28(2012), 933-941. Chou, S.H., Min, H.T., Chang, Y.C., & Lin, C.T. (2010). Understanding continuance intention of

knowledge creation using extended expectation-confirmation theory: An empirical study of Taiwan and China online communities. Behaviour & Information Technology, 29(6), 557-570.

Chuah, S.H.W., Marimuthu, M., Kandampully, J., & Bilgihan, A. (2017). What drives Gen Y loyalty? Understanding the mediated moderating roles of switching costs and alternativeness in the value–satisfaction–loyalty chain. Journal of Retailing and Consumer Services, 36(2017), 124-136.

Dwyer, P. (2007). Measuring the value of electronic word of mouth and its impact in consumer communities. Journal of Interactive Marketing, 21(2), 63-79.

Enginkaya, E., & Yılmaz, H. (2014). What drives consumers to interact with brands through social media? A motivation scale development study. Procedia-Social and Behavioural Sciences, 148(2014), 219-226.

Erdogmus, I.E., & Çiçek, M. (2012). The impact of social media marketing on brand loyalty. Procedia-Social and Behavioural Sciences, 58(2012), 1353-1360.

Falk, R.F., & Miller, N.B. (1992). A Primer for Soft Modelling, University of Akron Press, Akron, Ohio. Fornell, C., & Bookstein, F.L. (1982). Two structural equation models: LISREL and PLS applied to

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

35

consumer exit-voice theory. Journal of Marketing Research, 19(4), 440-452. Fornell, C., & Larcker, D.F. (1981). Evaluating structural equation models with unobservable variables

and measurement error. Journal of Marketing Research, 18(1), 39-50. Gao, L., Waechter, K.A., & Bai, X. (2015). Understanding consumers’ continuance intention towards

mobile purchase: A theoretical framework and empirical study – A case of China. Computers in Human Behaviour, 53(2015), 249-262.

Georgescu, M., & Popescul, D. (2015). Social Media - the new paradigm of collaboration and communication for business environment. Procedia Economics and Finance, 20(2015), 277-282.

Gilani, M.S., Iranmanesh, M., Nikbin, D., & Zailani, S. (2017). EMR continuance usage intention of healthcare professionals. Informatics for Health and Social Care, 42(2), 153-165.

Hair, J.F., Black, W.C., Babin, B.J., & Anderson, R.E. (2010). Multivariate Data Analysis: A Global Perspective, Pearson Education Inc., New Jersey.

Hair, J.F., Hult, G.T.M., Ringle, C.M., & Sarstedt, M. (2017). A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), Sage Publications, Thousand Oaks, California.

Hassan, L.F., Wan Jusoh, W.J., & Hamid, Z. (2014). Determinant of customer loyalty in Malaysian Takaful industry. Procedia-Social and Behavioural Sciences, 130(2014), 362-370.

Hennig-Thurau, T., & Walsh, G. (2003). Electronic word of mouth: Motives for and consequences of reading customer articulations on the Internet. International Journal of Electronic Commerce, 8(2), 51-74.

Hennig-Thurau, T., Gwinner, K.P., Walsh, G., & Gremler, D.D. (2004). Electronic word-of-mouth via consumer-opinion platforms: What motivates consumers to articulate themselves on the Internet? Journal of Interactive Marketing, 18(1), 38–52.

Hew, J.J., Lee, V.H., Ooi, K.B., & Lin, B. (2016). Mobile social commerce: The booster for brand loyalty. Computers in Human Behaviour, 59(2016), 142-154.

Hsiao, C.H., Chang, J.J., & Tang, K.Y. (2016). Exploring the influential factors in continuance usage of mobile social apps: Satisfaction, habit, and customer value perspectives. Telematics and Informatics, 33(2016), 342-355

Hudson, S., Huang, L., Roth, M.S., & Madden, T.J. (2015). The influence of social media interactions on consumer - brand relationships: A three-country study of brand perceptions and marketing behaviours. International Journal of Research in Marketing, 33(1), 27-41.

Iranmanesh, M., Zailani, S., & Nikbin, D. (2017). RFID continuance usage intention in health care industry. Quality Management in Healthcare, 26(2), 116-123.

Jin, X.L., Lee, M.K.O., & Cheung, C.M.K. (2009). Predicting continuance in online communities: Model development and empirical test. Behaviour & Information Technology, 29(4), 383-394.

Laroche, M., Habibi, M.R., & Richard, M.O. (2013). To be or not to be in social media: How brand loyalty is affected by social media? International Journal of Information Management, 33(1), 76-82.

Lazarevic, V. (2012). Encouraging brand loyalty in fickle generation Y consumers. Young Consumers, 13(1), 45-61.

Llopis, O., & Foss, N.J. (2016). Understanding the climate-knowledge sharing relation: The moderating roles of intrinsic motivation and job autonomy. European Management Journal, 34(2), 135-144.

Méndez-Aparicio, M.D., Izquierdo-Yusta, A., & Jiménez-Zarco, A.I. (2017). Consumer expectations of online services in the insurance industry: An exploratory study of drivers and outcomes. Frontiers in Psychology, 8(2017), doi: 10.3389/fpsyg.2017.01254

Nambisan, S., & Baron, R.A. (2007). Interactions in virtual customer environments: implications for product support and customer relationship management. Journal of Interactive Marketing, 21(2), 42-62.

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

36

Oghuma, A.P., Libaque-Saenz, C.F., Wong, S.F., & Chang, Y. (2016). An expectation-confirmation model of continuance intention to use mobile instant messaging. Telematics and Informatics, 33(2016), 34-47.

Pauwels, K., Aksehirli, Z., & Lackman, A. (2016). Like the ad or the brand? Marketing stimulates different electronic word-of-mouth content to drive online and offline performance. International Journal of Research in Marketing, 33(3), 639-655.

Podsakoff, P.M., MacKenzie, S.B., Lee, J.Y., & Podsakoff, N.P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of Applied Psychology, 8(5), 879-903.

RAM Ratings (2017). Malaysian Insurance and Takaful: Growth prospects favourable despite near-term moderation. available at: https://www.ram.com.my/pressrelease/?prviewid=4161 (accessed 21 December 2017).

Ryan, R.M., & Deci, E.L. (2000). Self-determination theory and the facilitation of intrinsic motivation, social development, and well-being. American Psychologist, 55(1), 68-78.

Saad, N.M. (2012). An analysis on the efficiency of Takaful and insurance companies in Malaysia: A non-parametric approach. Review of Integrative Business and Economics, 1(1), 33-54.

San-Martin, S., & López‐Catalán, B. (2013). How can a mobile vendor get satisfied customers? Industrial Management & Data Systems, 113(2), 156-170.

Stauss, B. (1997). Global word-of-mouth: Service bashing on the Internet is a thorny issue. Marketing Management, 6(3), 28-30.

Suki, N.M. (2012). Correlations of perceived flow, perceived system quality, perceived information quality and perceived user trust on mobile social networking service (SNS) users’ loyalty. Journal of Information Technology Research, 5(2), 1-14.

Suki, N.M., & Suki, N.M. (2016). Mobile social networking service (SNS) users’ trust and loyalty: A structural approach. International Journal of Social Ecology and Sustainable Development, 7(3), 57-70.

Sussman, S.W., & Siegal, W.S. (2003). Informational influence in organizations: An integrated approach to knowledge adoption. Information Systems Research, 14(1), 47-65.

Tabachnick, B.G., & Fidell, L.S. (2007). Using Multivariate Statistics, Pearson/Allyn & Bacon, Boston. Tepeci, M. (1999). Increasing brand loyalty in the hospitality industry. International Journal of

Contemporary Hospitality Management, 11(5), 223-229. The Star Online (2017). Takaful Malaysia posts better net profit. available at:

https://www.thestar.com.my/business/business-news/2017/10/20/takaful-malaysia-posts-better-net-profit/ (accessed 27 December 2017).

Weng G.S., Zailani, S., Iranmanesh, M., & Hyun, S.S. (2017). Mobile taxi booking application service’s continuance usage intention by users. Transportation Research Part D, 57(2017), 207-216.

Woolfolk, A. (1995). Educational Psychology 6th edition. Allyn and Bacon, Boston, Massachusetts. Yan Q., Wu, S., Wang, L., Wu, P., Chen, H., & Wei, G. (2016). E-WOM from e-commerce websites and

social media: Which will consumers adopt? Electronic Commerce Research and Applications, 17(2016), 62-73.

Yazid, A.S., Arifin, J., Hussin, M.R., & Wan Daud, W.N. (2012). Determinants of family Takaful (Islamic life insurance) demand: A conceptual framework for a Malaysian study. International Journal of Business and Management, 7(6), 115-127.

Yeh C.H., Wang, Y.S., & Yieh, K. (2016). Predicting smartphone brand loyalty: Consumer value and consumer-brand identification perspectives. International Journal of Information Management, 36(2016), 245-257.

MALAYSIAN JOURNAL OF CONSUMER AND FAMILY ECONOMICS (2018), VOL. 21

37

Yi, M.Y., & Davis, F.D. (2003). Developing and validating an observational learning model of computer software training and skill acquisition. Information Systems Research, 14(2), 146-169.

Yoo, C.W., Sanders, G.L., & Moon, J. (2013). Exploring the effect of e-WOM participation on e-loyalty in e-commerce. Decision Support Systems, 55(3), 669-678.

Zakaria Z., Azmi, N.M., Nik Hassan, N.F.H., Salleh, W.A., Mohd Tajuddin, M.T.H., Mohd Sallem, N.R., & Mohd Noor, J.M. (2016). The Intention to purchase life insurance: A case study of staff in public universities. Procedia Economics and Finance, 37(2016), 358-365.

Zohar D., Huang, Y.H., Lee, J., & Robertson, M.M. (2015). Testing extrinsic and intrinsic motivation as explanatory variables for the safety climate-safety performance relationship among long-haul truck drivers. Transportation Research Part F, 30(2015), 84-96.