Embed Size (px)

Citation preview

Jim Van LieshoutAugust 16, 2017

Evaluate the Current Biosimilar Landscape and Strategies to Secure Access

1

Disclosure Statement

James R. Van Lieshout, Vice President, Trade and Industry RelationsApobiologix, a division of ApoPharma, USA

This is a non-promotional program. Any product names used in this presentation are only for reference purpose.

2

Learning Objectives

By the end of this session you will be able to …

• Address the current landscape and changes in the marketplace dynamics

• Gain Insight into the shifts in usage, market response and current data available

• Understand approval pathways and strategies to ensure reimbursement and coverage

• Identify potential patient access and reimbursement hurdles and develop strategic plans to address these obstacles

3APOBIOLOGIX CONFIDENTIAL INFORMATION

Test Your Knowledge

4

True or False

• Biosimilars are Biologics

APOBIOLOGIX CONFIDENTIAL INFORMATION

5

TRUE

Descriptions and DefinitionsIntroduction to Biologics

6

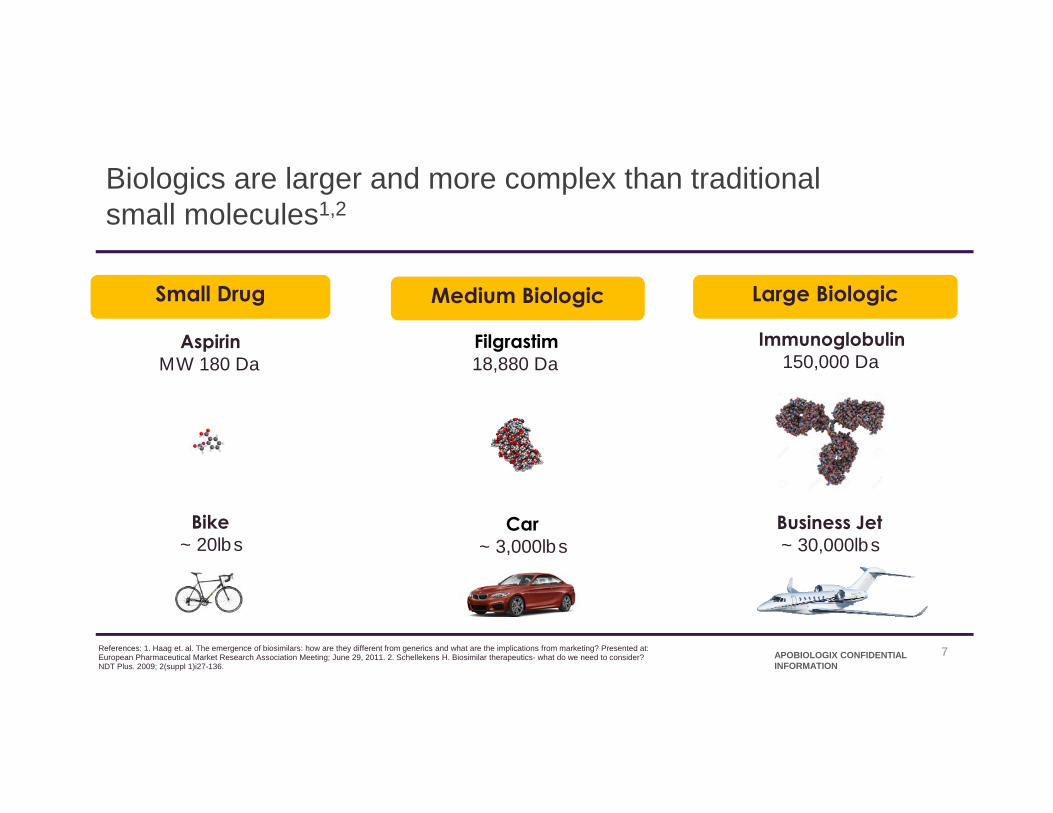

Biologics are larger and more complex than traditional small molecules1,2

References: 1. Haag et. al. The emergence of biosimilars: how are they different from generics and what are the implications from marketing? Presented at: European Pharmaceutical Market Research Association Meeting; June 29, 2011. 2. Schellekens H. Biosimilar therapeutics- what do we need to consider? NDT Plus. 2009; 2(suppl 1)i27-136.

Small Drug

AspirinMW 180 Da

Filgrastim18,880 Da

Immunoglobulin150,000 Da

Bike~ 20lbs

Car~ 3,000lbs

Business Jet~ 30,000lbs

APOBIOLOGIX CONFIDENTIAL INFORMATION

7

Medium Biologic Large Biologic

All biologics undergo manufacturing process updates during their life cycle3,4

0

10

20

30

40

Rituxan Remicade Enbrel Humira

Number of Changes in Manufacturing Process After Approval*

*Products authorized for rheumatological indications in Europe. Changes range from change in supplier of a cell culture to new purification methods or new manufacturing sites.

References: 3. Schneider CK. Ann Rheum Dis. 2013;72:315-318. 4. Mahler, Mojas, Roche Kepler Swiss Seminar, www.roche.com. 2007.

Num

ber o

f cha

nges

APOBIOLOGIX CONFIDENTIAL INFORMATION

8

Test Your Biosimilar Knowledge

9

True or False

• Biosimilars are the same as generic drugs

APOBIOLOGIX CONFIDENTIAL INFORMATION

10

FALSE

BIOSIMILARS ≠ GENERICS

11

Definition of a biosimilar

Biological product that is licensed (approved) by the FDA based on a showing that they are highly similar to an already FDA-approved biological product, known as the reference product have no clinically meaningful differences in terms of safety and effectiveness from the reference product. Only minor differences in clinically inactive components are allowed.

— U.S. Food and Drug Administration

Reference: 5. United States Food and Drug Administration. Information for Healthcare Professionals (Biosimilars). http://www.fda.gov/Drugs/DevelopmentApprovalProcess/HowDrugsareDevelopedandApproved/ApprovalApplications/TherapeuticBiologicApplications/Biosimilars/ucm241719.htm. Accessed January 26, 2017.

APOBIOLOGIX CONFIDENTIAL INFORMATION

12

Address the Current Landscape and Changes In the Marketplace Dynamics

13

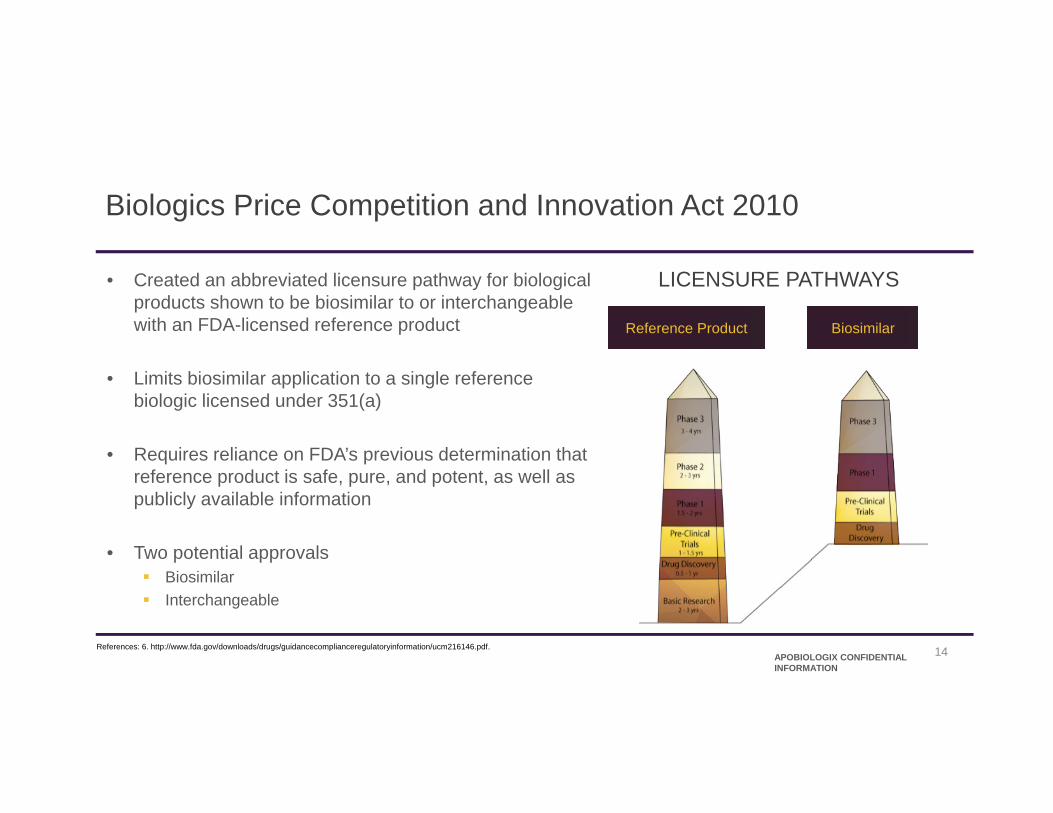

Biologics Price Competition and Innovation Act 2010

• Created an abbreviated licensure pathway for biological products shown to be biosimilar to or interchangeable with an FDA-licensed reference product

• Limits biosimilar application to a single reference biologic licensed under 351(a)

• Requires reliance on FDA’s previous determination that reference product is safe, pure, and potent, as well as publicly available information

• Two potential approvals Biosimilar Interchangeable

References: 6. http://www.fda.gov/downloads/drugs/guidancecomplianceregulatoryinformation/ucm216146.pdf. APOBIOLOGIX CONFIDENTIAL INFORMATION

14

Reference Product

LICENSURE PATHWAYS

Biosimilar

Experience and Expectations in Europe7

APOBIOLOGIX CONFIDENTIAL INFORMATION

15

• Payers expect discounts for oncology biosimilars to align with those observed in EU

• The average price reduction of biologics was 27% in the EU in general Most payers are seeking a 20-25% differential

at the net level (across markets)

• They expect discounts to increase with time, as more competitors enter the market The cost-saving potential of biosimilars in the

EU and US could equal even more than 50 billion EUR over 5 years and reach even 100 billion EUR by 2020

Reference: 7. IMS (2016). Delivering on the Potential of Biosimilar Medicines. The Role of Functioning Competitive Markets. IMS Institute for Healthcare Informatics. Available at: http://www imshealth com/files/web/IMSH%20Institute/Healthcare%20Briefs/Documents/IMS Institute Biosimilar Brief March 2016 pdf

Source: http://www.biosimilarsip.com/2017/06/20/u‐s‐compares‐europe‐biosimilar‐approvals‐products‐pipeline/

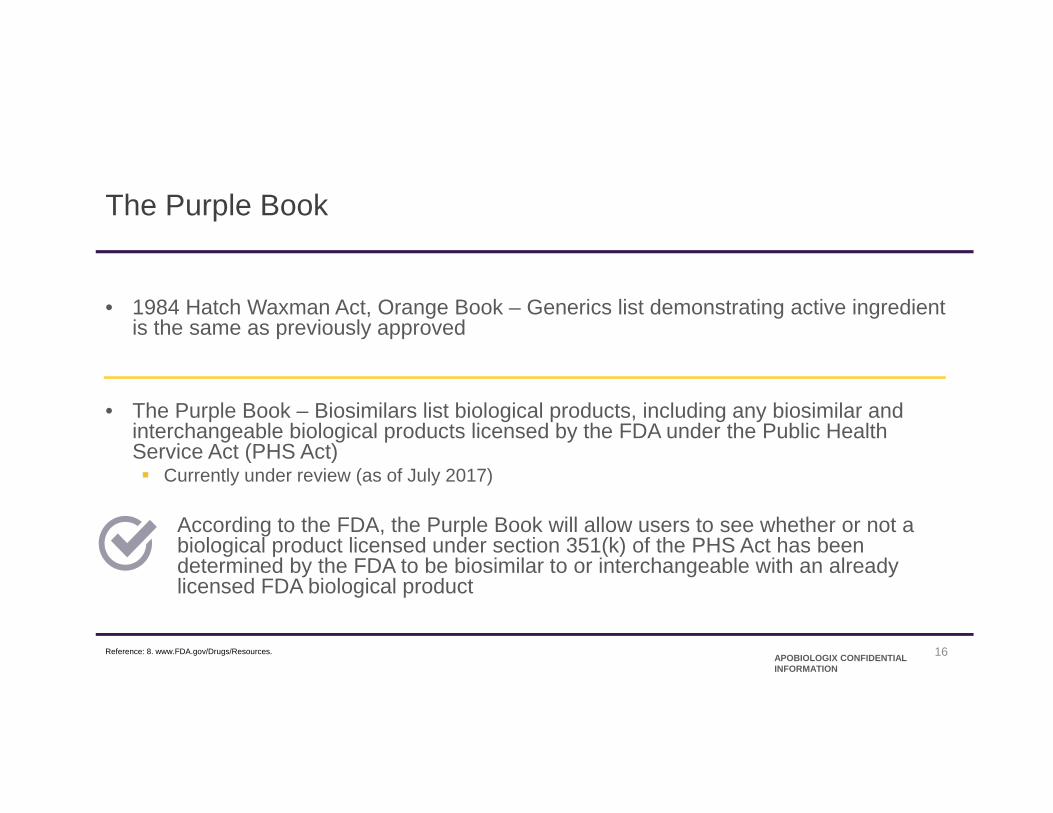

The Purple Book

• 1984 Hatch Waxman Act, Orange Book – Generics list demonstrating active ingredient is the same as previously approved

• The Purple Book – Biosimilars list biological products, including any biosimilar and interchangeable biological products licensed by the FDA under the Public Health Service Act (PHS Act) Currently under review (as of July 2017)

According to the FDA, the Purple Book will allow users to see whether or not a biological product licensed under section 351(k) of the PHS Act has been determined by the FDA to be biosimilar to or interchangeable with an already licensed FDA biological product

Reference: 8. www.FDA.gov/Drugs/Resources.APOBIOLOGIX CONFIDENTIAL INFORMATION

16

State Pharmacy Laws Mandate Substitution of Drugs

APOBIOLOGIX CONFIDENTIAL INFORMATION

17

As of July 2017• Legislation currently progressing in 8 states• Since 2013, 36 states and Puerto Rico

have enacted state pharmacy practice acts to address biologics and biosimilars

• Legislation currently progressing Alabama Arkansas Alaska Connecticut Michigan New York Oklahoma Vermont

Reference: 9. National Conference of State Legislatures: http://www.ncsl.org/research/health/state-laws-and-legislation-related-to-biologic-medications-and-substitution-of-biosimilars.aspx

The Value of Biosimilars and Cost Considerations

18

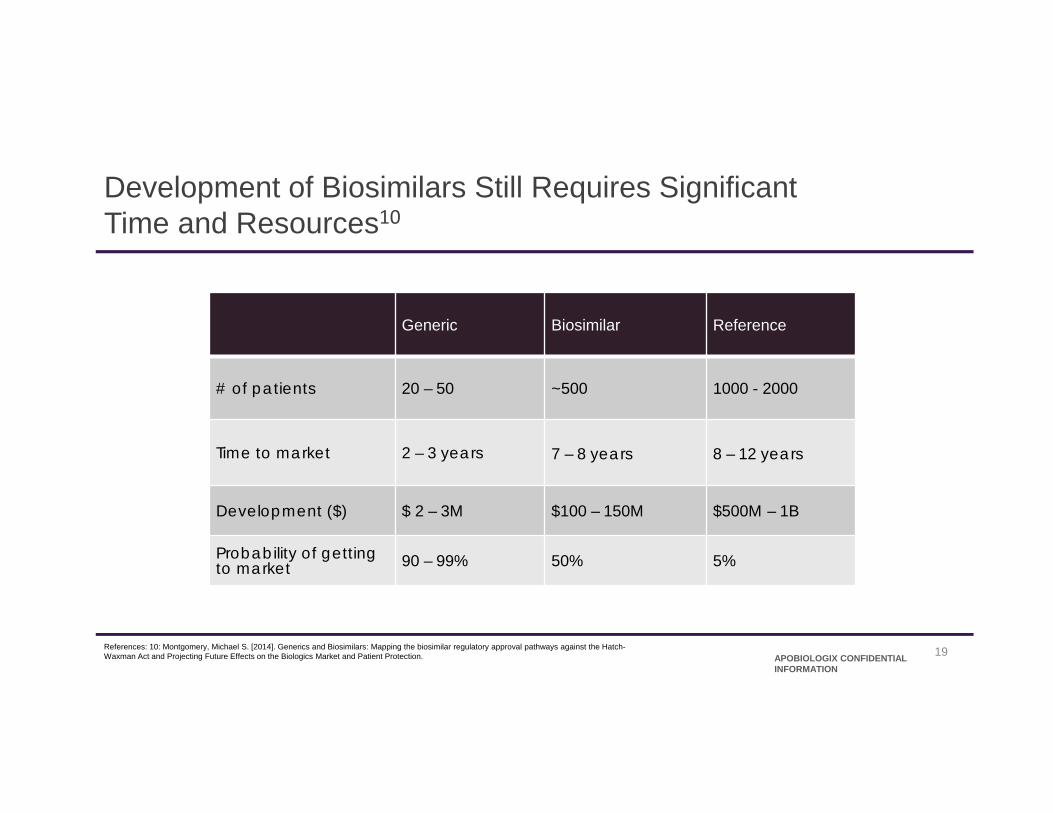

Development of Biosimilars Still Requires Significant Time and Resources10

Generic Biosimilar Reference

# of patients 20 – 50 ~500 1000 - 2000

Time to market 2 – 3 years 7 – 8 years 8 – 12 years

Development ($) $ 2 – 3M $100 – 150M $500M – 1B

Probability of getting to market 90 – 99% 50% 5%

APOBIOLOGIX CONFIDENTIAL INFORMATION

References: 10: Montgomery, Michael S. [2014]. Generics and Biosimilars: Mapping the biosimilar regulatory approval pathways against the Hatch-Waxman Act and Projecting Future Effects on the Biologics Market and Patient Protection. 19

Potential Cost Savings from Biosimilars to the U.S. Healthcare System for 11 Products11

• Competition from biosimilars could reduce federal drug spending in the United States by roughly $25 billion over 10 years12

• Potential savings with biosimilars could reach $250 billion by 202413

Projected U.S. Spend on 11 Specific Biologics (in 000s)

$0

$20,000,000

$40,000,000

$60,000,000

$80,000,000

$100,000,000

$120,000,000

$140,000,000

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

Without Biosimilars

With Biosimilars

Savings Projectionwith Biosimilars

References: 11. Rovira J, et al. GaBI J. 2013;2(1):30-35. 12. Congressional Budget Office. Biologics price competition and innovation act of 2007. S. 1695. 13. Miller S. The $250 billion potential of biosimilars. http://lab.express-scripts.com/lab/insights/industry-updates/the-$250-billion-potential-of-biosimilars. Accessed January 26, 2017. APOBIOLOGIX CONFIDENTIAL

INFORMATION20

Based on 11 most likely

biologic drugs to come off

patent in the next 10 years

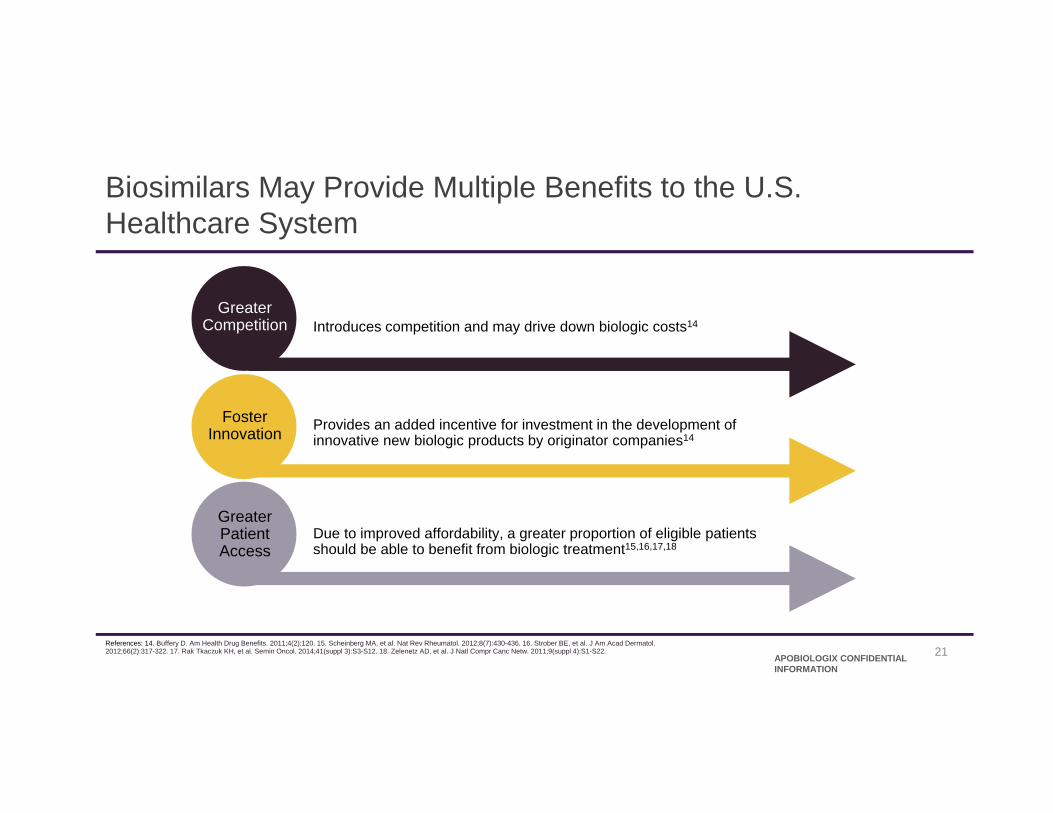

Biosimilars May Provide Multiple Benefits to the U.S. Healthcare System

GreaterCompetition

FosterInnovation

GreaterPatientAccess

Introduces competition and may drive down biologic costs14

Provides an added incentive for investment in the development of innovative new biologic products by originator companies14

Due to improved affordability, a greater proportion of eligible patients should be able to benefit from biologic treatment15,16,17,18

References: 14. Buffery D. Am Health Drug Benefits. 2011;4(2):120. 15. Scheinberg MA, et al. Nat Rev Rheumatol. 2012;8(7):430-436. 16. Strober BE, et al. J Am Acad Dermatol. 2012;66(2):317-322. 17. Rak Tkaczuk KH, et al. Semin Oncol. 2014;41(suppl 3):S3-S12. 18. Zelenetz AD, et al. J Natl Compr Canc Netw. 2011;9(suppl 4):S1-S22.

APOBIOLOGIX CONFIDENTIAL INFORMATION

21

Gain Insights Into the Shifts In Usage Market Response and Current Data Available

22

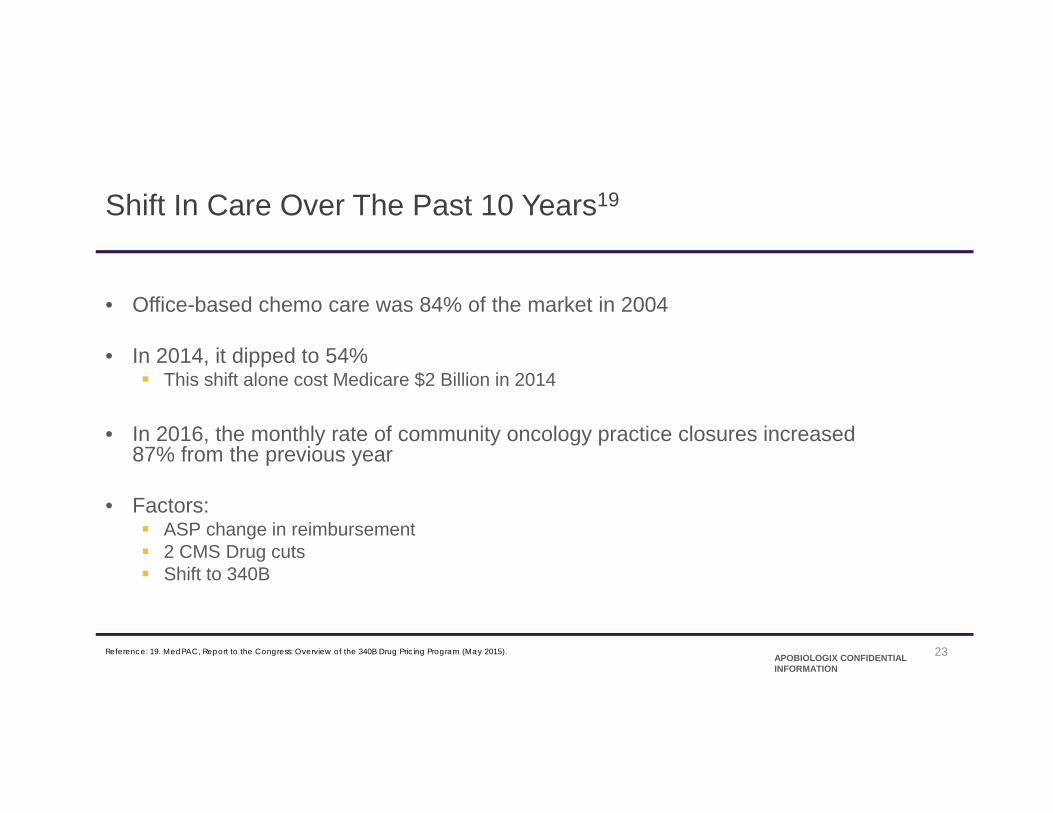

Shift In Care Over The Past 10 Years19

• Office-based chemo care was 84% of the market in 2004

• In 2014, it dipped to 54% This shift alone cost Medicare $2 Billion in 2014

• In 2016, the monthly rate of community oncology practice closures increased 87% from the previous year

• Factors: ASP change in reimbursement 2 CMS Drug cuts Shift to 340B

Reference: 19. MedPAC, Report to the Congress: Overview of the 340B Drug Pricing Program (May 2015).APOBIOLOGIX CONFIDENTIAL INFORMATION

23

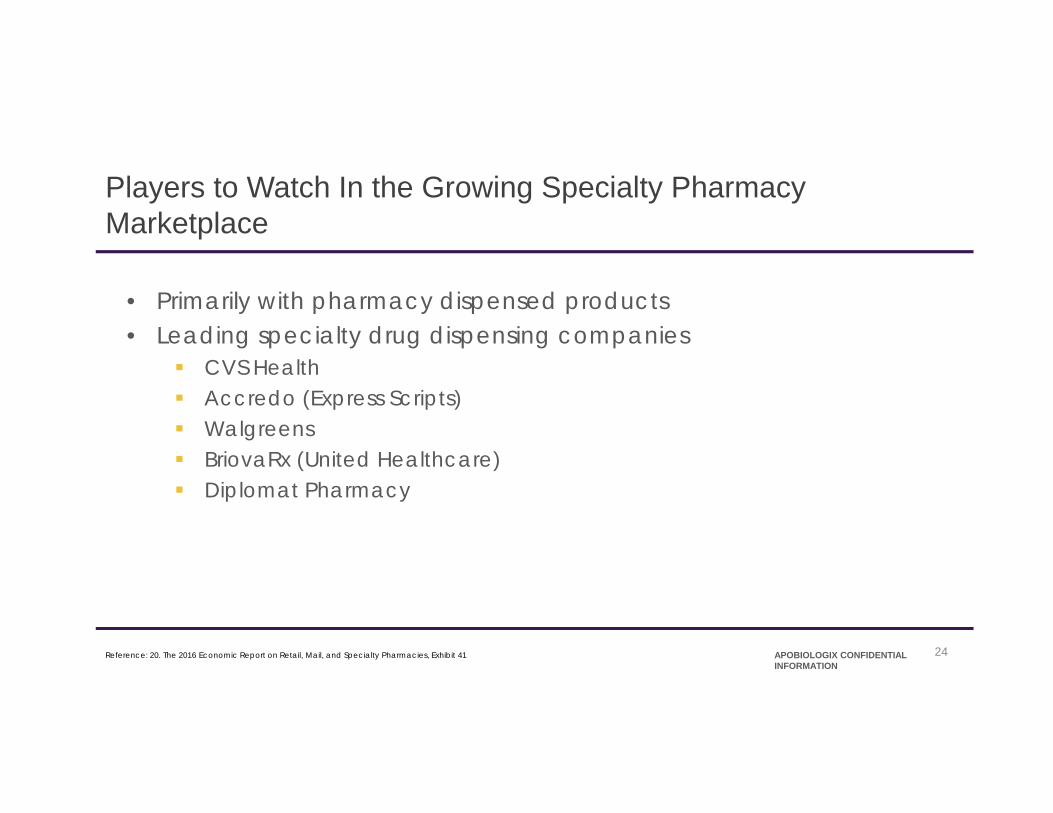

Players to Watch In the Growing Specialty Pharmacy Marketplace

APOBIOLOGIX CONFIDENTIAL INFORMATION

24

• Primarily with pharmacy dispensed products• Leading specialty drug dispensing companies

CVS Health Accredo (Express Scripts) Walgreens BriovaRx (United Healthcare) Diplomat Pharmacy

Reference: 20. The 2016 Economic Report on Retail, Mail, and Specialty Pharmacies, Exhibit 41

Understand Approval Pathways and Strategiesto Ensure Reimbursement and Coverage

25

Approval Pathways in the United States

Small MoleculesApproved via Food, Drugand Cosmetic Act (FDCA)

New Drug Application(NDA)

Safety and efficacymust be demonstrated

Generics

Abbreviated new drugapplication (ANDA),

“Hatch-Waxman”

Bioequivalence mustbe demonstrated

BiologicsApproved via Public

Health Service Act (PHSA)

Biologics licenseapplication (BLA)

351(a)

Safety and efficacymust be demonstrated

Biosimilars

Biosimilar biologicslicense application(BPCI Act) 351(k)

Must demonstrate highsimilarity to reference

No clinicallymeaningful differences

BPCI = Biologics Price Competition and Innovation

References: 21. http://www.fda.gov/downloads/drugs/guidancecomplianceregulatoryinformation/ucm216146.pdf.

Current Regulatory and Legislative Issues with Biosimilars

• Naming• Labeling• Interchangeability• BDUFA funding• REMS/Sampling access• Patent litigation

APOBIOLOGIX CONFIDENTIAL INFORMATION.

27

340B Growth & the Impact on the Oncology Marketplace22

• In 2004, 340B was 3% of Part B, compared to 25% in 2014 CMS provided a new proposal to significantly affect 340B care and costing for hospitals

• Med PAC Part B recommendations Lower cost options in Oncology drug care PBM’s to negotiate drug prices for Part B Formularies by PBM’S

• Market needs to look at the Oncology Care Model

Reference: 22. http://archive.communityoncology.org/site/blog/tag/millman.htmlAPOBIOLOGIX CONFIDENTIAL INFORMATION

28

Identify Patient Access and Reimbursement Hurdlesand Develop Strategic Plans to Address Obstacles

29

Lower Prices Increase Patient Access and Product Utilization

30

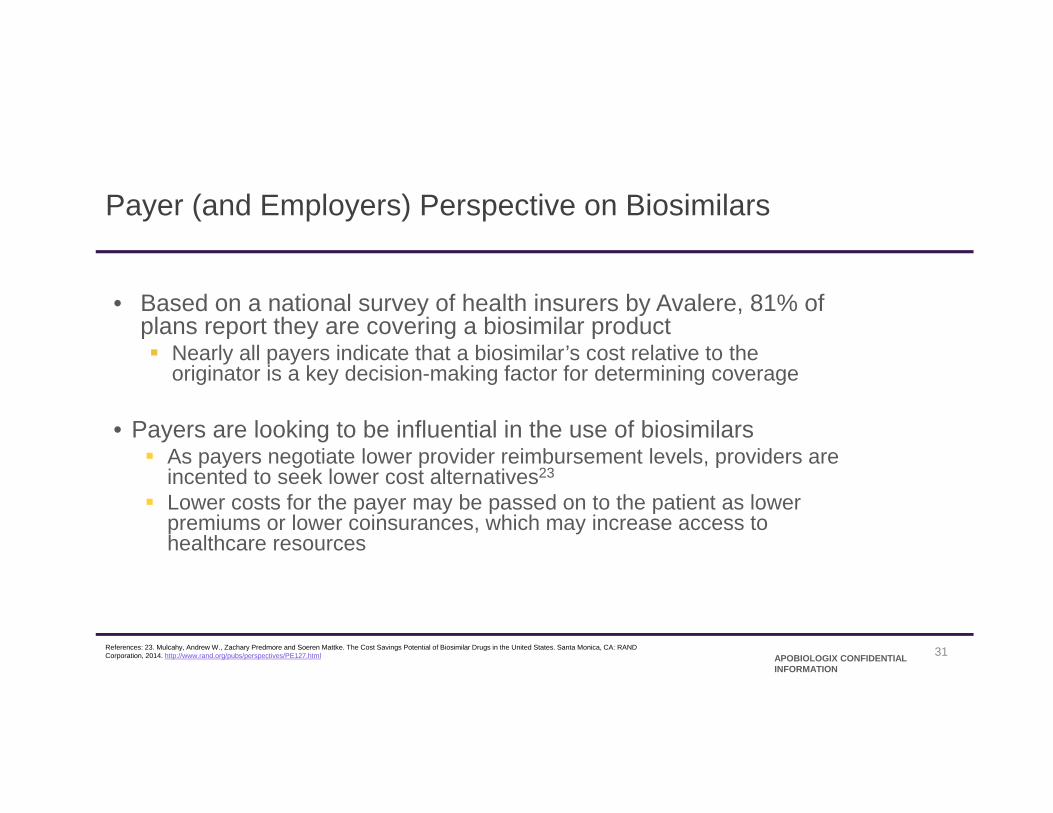

Payer (and Employers) Perspective on Biosimilars

• Based on a national survey of health insurers by Avalere, 81% of plans report they are covering a biosimilar product Nearly all payers indicate that a biosimilar’s cost relative to the

originator is a key decision-making factor for determining coverage

• Payers are looking to be influential in the use of biosimilars As payers negotiate lower provider reimbursement levels, providers are

incented to seek lower cost alternatives23

Lower costs for the payer may be passed on to the patient as lower premiums or lower coinsurances, which may increase access to healthcare resources

References: 23. Mulcahy, Andrew W., Zachary Predmore and Soeren Mattke. The Cost Savings Potential of Biosimilar Drugs in the United States. Santa Monica, CA: RAND Corporation, 2014. http://www.rand.org/pubs/perspectives/PE127.html APOBIOLOGIX CONFIDENTIAL

INFORMATION

31

Patient Perspective on Biosimilars

• Patient out-of-pocket expenses are becoming a crucial element in Rx care of patients

• Lower cost alternatives should expand access to important medicines in the US, as has been seen in Europe

• Greater patient access, conceptually, will lead to improved health status, thus lowering overall healthcare costs24

References: 24. Mulcahy, Andrew W., Zachary Predmore and Soeren Mattke. The Cost Savings Potential of Biosimilar Drugs in the United States. Santa Monica, CA: RAND Corporation, 2014. http://www.rand.org/pubs/perspectives/PE127.html APOBIOLOGIX CONFIDENTIAL

INFORMATION

32

Reimbursement: What You Need To Know

Reference: 25. 2016 Physician Fee Schedule Final Rule, 80 Fed. Reg. 71906 (Nov. 16, 2015) APOBIOLOGIX CONFIDENTIAL INFORMATION.

33

CMS final rule CY 2016: Revisions to Payment Policies Under the Physician Fee Schedule21

• More than one biosimilar product to the same reference product• Biosimilars are excluded from coverage gap discount program (donut hole)

• Provider reimbursed at ASP + 6% of reference product (4.23% with sequestration)• At launch, Medicare will pay 106% of WAC until ASP is provided% of WAC

• CMS will group biosimilar products that rely on a common reference product’s biologics license application into the same payment calculation; products will share a common payment limit and HCPCS code.

• Modifiers will be used to distinguish between biosimilar products that appear in the same HCPCS code but are made by different manufacturers

All biosimilars to the same reference

product will share the same J-code and

payment rate

Each biosimilar will have a “random”

4-letter suffix

Fighting Shared J-Codes

APOBIOLOGIX CONFIDENTIAL INFORMATION

34

• The need to eliminate shared J-codes is getting attention in Congress 52 representatives and 9 GOP senators

have sent letters to Secretary Price and Administrator Verma

• AAM Biosimilar Council is working in Washington D.C. to try to revise the biosimilar coding policy

Federal Reimbursement Landscape

Medicare Part B• Reimbursement treats biosimilars as multiple-source, generic-like products• Shared J- code

APOBIOLOGIX CONFIDENTIAL INFORMATION

35

Medicare Part D• CMS views biosimilars as non-branded products• Excluded in coverage cap (Donut hole)

Medicaid• Manufacturer rebates position biosimilars as branded products• 23% product rebate

Summary

36

Summary26,27

• Biosimilars are biological compounds that are highly similar to their reference drugs with no clinically meaningful differences in safety, purity, and potency

• Biosimilars, like their reference biologic products, are more complex in structure than pure chemical substances

The active ingredient of a generic drug is structurally identical to the active ingredient of the reference drug

Biosimilars are structurally highly similar, but not identical, to their reference biologic products

• Market access in reimbursement will be critical factors in the adoption of biosimilars

• Biosimilars will create greater competition in the marketplace, increasing the number of safe and effective treatment options

References: 26. http://www.fda.gov/Drugs/DevelopmentApprovalProcess/HowDrugsareDevelopedandApproved/ApprovalApplications/ TherapeuticBiologicApplications/Biosimilars/ucm241718.htm. 27. Zelenetz et al. J Natl Compr Canc Netw. 2011;9(suppl 4):S1-S22. APOBIOLOGIX CONFIDENTIAL

INFORMATION

37

Thank you for your participation

38

Reference List

1. Haag et. al. The emergence of biosimilars: how are they different from generics and what are the implications from

marketing? Presented at: European Pharmaceutical Market Research Association Meeting; June 29, 2011.

2. Schellekens H. Biosimilar therapeutics- what do we need to consider? NDT Plus. 2009; 2(suppl 1)i27-136.

3. Schneider CK. Ann Rheum Dis. 2013;72:315-318.

4. Mahler, Mojas, Roche Kepler Swiss Seminar, www.roche.com. 2007.

5. United States Food and Drug Administration. Information for Healthcare Professionals (Biosimilars).

http://www.fda.gov/Drugs/DevelopmentApprovalProcess/HowDrugsareDevelopedandApproved/ApprovalApplications

/TherapeuticBiologicApplications/Biosimilars/ucm241719.htm. Accessed January 26, 2017.

6. http://www.fda.gov/downloads/drugs/guidancecomplianceregulatoryinformation/ucm216146.pdf.

7. IMS (2016). Delivering on the Potential of Biosimilar Medicines. The Role of Functioning Competitive Markets. IMS Institute

for Healthcare Informatics. Available at:

http://www.imshealth.com/files/web/IMSH%20Institute/Healthcare%20Briefs/Documents/IMS_Institute_Biosimilar_Brief_Mar

ch_2016.pdf

39

Reference List (cont.)

8. www.FDA.gov/Drugs/Resources.

9. National Conference of State Legislatures: http://www.ncsl.org/research/health/state-laws-and-legislation-related-to-

biologic-medications-and-substitution-of-biosimilars.aspx

10. Montgomery, Michael S. [2014]. Generics and Biosimilars: Mapping the biosimilar regulatory approval pathways against the

Hatch-Waxman Act and Projecting Future Effects on the Biologics Market and Patient Protection.

11. Rovira J, et al. GaBI J. 2013;2(1):30-35.

12. Congressional Budget Office. Biologics price competition and innovation act of 2007. S. 1695.

13. Miller S. The $250 billion potential of biosimilars. http://lab.express-scripts.com/lab/insights/industry-updates/the-$250-billion-

potential-of-biosimilars. Accessed January 26, 2017.

14. Buffery D. Am Health Drug Benefits. 2011;4(2):120.

15. Scheinberg MA, et al. Nat Rev Rheumatol. 2012;8(7):430-436.

16. Strober BE, et al. J Am Acad Dermatol. 2012;66(2):317-322.

17. Rak Tkaczuk KH, et al. Semin Oncol. 2014;41(suppl 3):S3-S12.

18. Zelenetz AD, et al. J Natl Compr Canc Netw. 2011;9(suppl 4):S1-S22.

40

Reference List (cont.)

19. MedPAC, Report to the Congress: Overview of the 340B Drug Pricing Program (May 2015).

20. The 2016 Economic Report on Retail, Mail, and Specialty Pharmacies, Exhibit 41

21. http://www.fda.gov/downloads/drugs/guidancecomplianceregulatoryinformation/ucm216146.pdf.

22. http://archive.communityoncology.org/site/blog/tag/millman.html

23. Mulcahy, Andrew W., Zachary Predmore and Soeren Mattke. The Cost Savings Potential of Biosimilar Drugs in the United

States. Santa Monica, CA: RAND Corporation, 2014. http://www.rand.org/pubs/perspectives/PE127.html

24. Mulcahy, Andrew W., Zachary Predmore and Soeren Mattke. The Cost Savings Potential of Biosimilar Drugs in the United

States. Santa Monica, CA: RAND Corporation, 2014. http://www.rand.org/pubs/perspectives/PE127.html

25. 2016 Physician Fee Schedule Final Rule, 80 Fed. Reg. 71906 (Nov. 16, 2015)

26. http://www.fda.gov/Drugs/DevelopmentApprovalProcess/HowDrugsareDevelopedandApproved/ApprovalApplications

/ TherapeuticBiologicApplications/Biosimilars/ucm241718.htm.

27. Zelenetz et al. J Natl Compr Canc Netw. 2011;9(suppl 4):S1-S22.

41

![[Product Monograph Template - Standard]€¦ · Web view is a biosimilar biologic drug (biosimilar) to](https://img.dokumen.tips/doc/110x75/5ed9c1d0fa48703dd5136997/product-monograph-template-standard-web-view-is-a-biosimilar-biologic-drug-biosimilar.jpg)