Embed Size (px)

Citation preview

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 1

RESEARCH PROJECT ON “RELATIONSHIP BETWEEN

ECONOMIC VALUE ADDED AND SHARE PRICE”

SUBMITTED IN PARTIAL FULFILLMENTOF THE

REQUIREMENTS FOR THE AWARD OF MBA DEGREE OF

BANGALORE UNIVERSITY.

Submitted By

SHOUKAT. P. Reg. No: 06XQCM6079

UNDER THE GUIDANCE OF

Prof. PRAVEEN BHAGAWAN. M. INTERNAL GUIDE

M.P.BIRLA INSTITUTE OF MANAGEMENT

ASSOCIATE BHARTIYA VIDYA BHAVAN

BANGALORE-560001 2006-2008

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 2

DECLARATION

I hereby declare that the research entitled “RELATIONSHIP

BETWEEN ECONOMIC VALUE ADDED AND SHARE PRICE”

has been carried out by me under the guidance and

supervision of Prof. PRAVEEN BHAGAWAN. M., Internal Guide,

M.P.Birla Institute of Management, Bangalore.

I also declare that this report has not been submitted to any

University/Institution for the award of any Degree/Diploma.

Date: (SHOUKAT. P.) Place: Bangalore Reg. No 06XQCM6079

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 3

GUIDE’S CERTIFICATE

This is to certify that Mr. SHOUKAT. P., a student of M.P.BIRLA INSTITUTE OF MANAGEMENT Associate Bharatiya Vidya Bhavan, Bangalore, has successfully completed the research work entitled “RELATIONSHIP BETWEEN ECONOMIC VALUE ADDED AND SHARE PRICE” for the partial fulfillment of the requirements of MASTER OF BUSINESS ADMINISTRATION degree of BANGALORE UNIVERSITY, under my guidance and supervision. Place: Bangalore Prof. Praveen Bhagawan. M. Date: (Internal guide)

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 4

PRINCIPAL’S CERTIFICATE

This is to certify that Mr.SHOUKAT. P. bearing the register number 06XQCM6079 has undertaken a research project and has prepared a report titled “RELATIONSHIP BETWEEN ECONOMIC VALUE ADDED AND SHARE PRICE” under the guidance and supervision of Prof. PRAVEEN BHAGAWAN.M. This has not formed a basis for the award of any degree/ diploma for any university.

Place: Bangalore (Dr. N.S. MALAVALLI) Date: Principal

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 5

ACKNOWLEDGEMENT

I am happy to express my deep sense of gratitude to my

internal guide Prof. PRAVEEN BHAGAWAN. M. for his

enormous guidance and assistance. He has been my mentor and

guide, his continuous encouragement and valuable

suggestions helped me at every stage of this project.

I would also like to express my thanks to Dr. N.S. MALAVALLI,

Principal, M. P. Birla Institute of Management, Bangalore.

Special thanks to my friends and family for their

encouragement and help in completion of the study

successfully.

SHOUKAT. P.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 6

CONTENT SHEET

Chapter No Topics Page No

1 Research Extracts 1

2 Introduction 4

3 Literature Review 18

4 Research Methodology 25

5 Data Analysis and Interpretations 31

6 Summary and Recommendations 60

7 Bibliography 64

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 7

LIST OF TABLES

SI NO NAME OF THE TABLE PAGE NO

1 Sample profile 27

2 Beta of sample companies 32

3 Invested capital of selected companies 33

4 Nopat of selected companies 34

5 WACC of selected companies 35

6 Share prices of selected companies 36

7

Forecasted EVA and Share price of selected

companies

38

8 Degrees of correlation 36

9 EVA, Share price and regression statistics

of selected companies

40-59

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 8

CHAPTER 1

RESEARCH EXTRACTS

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 9

1. RESEARCH EXTRACTS:

Dissatisfaction with traditional accounting-based performance measures has

spawned a number of alternatives, of which Economic Value Added (EVA) is

currently the most prominent. Today, performance of the company with respect

to wealth creation is more important than the profit it earns or the dividend it

pays to the shareholders. Market prices of the shares reflect the performance of

the company

This research examines suitability of Economic Value Added (EVA) as a

performance measure. EVA is an effective measure of the quality of managerial

decisions as well as a reliable indicator of an enterprise’s value growth in

future.

The value-based management performance measure EVA, introduced by Stern

Stewart & Co. is an incarnation of the underlying residual income (RI) concept

EVA and its variability are observed to be strongly affected by the firm's growth

policies because of leverage effects. Methodologically, the paper demonstrates

the advantages of using a controlled simulation approach in financial research.

The EVA is computed and compared with the respective share prices of 20

companies of the SENSEX for a period of 5 years beginning from FY 2002-03

to FY 2006-07.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 10

From the study it is observed that there is there is no relationship between EVA

and share prices but EVA is the true profit that the company is able to generate

which also considers opportunity cost of the capital invested in the business.

The study adds that EVA is the one of the measure, which is used to measure

the performance of the company but it cannot be used to forecast the share

price of the company.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 11

CHAPTER 2

INTROCUCTION

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 12

2. INTRODUCTION:

2.1. Background of the study: Performance measurement has, of late, become an area of considerable

practitioner interest. Consulting firms routinely develop proprietary performance

measures for implementation by their client firms and have attempted to outdo

each other with claims of their own metric's "superiority." This "superiority" has

often been defined in terms of the correlation between the metric and realized

stock returns.

Stern Stewart & Co, a consulting firm based in New York, introduced the concept

of EVA as a measurement tool in 1989, and trademarked it. The EVA concept is

often called Economic Profit (EP) to avoid problems caused by the trade

marking. EVA is so popular and well known that all residual income concepts are

often called EVA even though they do not include the main elements defined by

Stern Stewart & Co (Pinto, 2001)

Stern Stewart developed EVA to help managers incorporate two basic principles

of finance into their decision making:

1. The primary objective of maximizing the wealth of its shareholders; and

2. Accepting that the value of a company depends on the extent to which

investors expect future profits to exceed or fall short of the cost of capital.

Today, this mechanism enable all types of firms to determine their value creation

and share holders to determine the value created on their investments. The first

question coming to our mind after reading this is:

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 13

2.2. WHAT IS EVA?

EVA is a value based financial performance measure, an investment decision

tool and a performance measure reflecting the absolute amount of shareholder

value created. It is computed as the product of the “excess return” made on an

investment or investments and the capital invested in that investment or

investments. EVA is the net operating profit minus an appropriate charge for the

opportunity cost of all capital invested in an enterprise or project. It is an estimate

of true economic profit, or the amount by which earnings exceed or fall short of

the required minimum rate of return investors could get by investing in other

securities of comparable risk (Stewart, 1990).

2.3 Profits the way shareholders count them:

By taking all capital costs into account, including the cost of equity, EVA shows

the monetary amount of wealth a business has created or destroyed in each

reporting period. In other words, EVA is the profit as defined by the share

holders.

The capital charge is the most distinctive and important aspect of EVA. Under

conventional accounting, most companies appear profitable but many in fact are

not. As Peter Drucker put the matter in a Harvard Business Review article, "Until

a business returns a profit that is greater than its cost of capital, it operates at a

loss. Never mind that it pays taxes as if it had a genuine profit. The enterprise still

returns less to the economy than it devours in resources…Until then it does not

create wealth; it destroys it." EVA corrects this error by explicitly recognizing that

when managers employ capital they must pay for it, just as if it were a wage.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 14

If the shareholders expect, say, a 10% return on their investment, they "make

money" only to the extent that their share of after-tax operating profits exceeds

10% of equity capital. Everything before that is just building up to the minimum

acceptable compensation for investing in a risky enterprise.

2.4 HOW EVA CAN BE USED:

In stock selection the EVA tool can be used in four distinct ways.

• Analyzing historical trends:

EVA can measure a company’s historical success in creating shareholder

wealth.

• Using EVA to forecast a target stock price:

EVA can be used to determine whether a stock is fairly valued based on a

forecast of economic profits. Such a forecast converts discounted EVA into

a share price.

• To quantify Competitive Advantage Period (CAP):

Stock prices in many cases may reflect a long competitive advantage

period. Analysts can use the value driver model to look at their assumptions

regarding risk and CAP.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 15

• To examine excess returns and its impact on valuation of a stock:

Another way of exploring the explanatory power of the value drivers in an EVA

model is to perform a regression analysis of invested capital(ROIC) minus the

weighted average cost of capital (WACC) spread as the independent variable

and enterprise value to invest capital as the dependant variable. The correlation

between return spreads and valuation is quite strong.

2.5 APPLICATIONS OF EVA:

1. To measure how much shareholder value the firm has created in the past and

2. To determine investor expectations as they relate to the stock price.

2.6 ADVANTAGES OF EVA:

EVA is frequently regarded as a single, simple measure that provides a real

picture of shareholder wealth creation. In addition to motivating managers to

create shareholder value and to serving as a basis for the calculation of

management compensation, there are further practical advantages that value

based measurement systems can offer. According to Roztoci & Needy an EVA

system helps managers to:

• Make better investment decisions;

• Identify improvement opportunities; and

• Consider long-term and short-term benefits for the company.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 16

EVA is an effective measure of the quality of managerial decisions and a reliable

indicator of a company’s value growth in the future. Constant positive EVA values

over time will increase company values, while negative EVA values might

decrease company values.

Above all, EVA helps in overcoming the ambiguity of financial goals. Most

companies use a plethora of measures to express their financial goals and

objective.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 17

2.7 Development of the concept of EVA:

EVA is not new. Residual income, an accounting performance measure, is

defined to be operating profit with a capital charge subtracted. Thus, EVA is

variant of residual income, with adjustments to how one calculates income and

capital.

Up to 1970 residual income did not get wide publicity and it was not the prime

performance measure for companies (Mäkeläinen, 1998). However, in the

1990’s, the creation of shareholder value has become recognized as the ultimate

economic purpose of a corporation.

Firms adopt this concept to track their financial position and to guide

management decisions regarding resource allocation, capital budgeting and

acquisition analysis.

Two views behind the concept of economic profit:

The financial concept underlying EVA was originally propagated by Adam

Smith, who proclaimed that the social mission of an individual enterprise is

to maximize the value of shareholders.

One of the earliest to mention the residual income concept was Alfred

Marshall in 1890. Marshall defined economic profit as total net gains less

the interest on invested capital at the current rate.

At operational level EVA approach leads often to increased shareholder value

through increased capital turnover (Wallace 1997, p.16). In many companies

everything has been done in cutting costs but the capital efficiency has been

ignored. EVA has been helpful because it forces to pay attention to capital

employed and especially to excess working capital. Allocating the capital costs to

their originators i.e. individual functions of organization can further reinforce this

impact.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 18

2.8 What others say about EVA? (Articles published on web)

"There is no profit unless you earn the cost of capital. Alfred Marshall said that in

1896, Peter Drucker said that in 1954 and in 1973, and now EVA (economic

value added) has systematized this idea, thank God."

- Peter Drucker

University of California, Irvine

"Companies that adopt EVA incentives increased their market-to-book value ratio

by nearly 0.6 more than that of non-EVA peer companies. That means for every

$1 billion in book value an EVA firm creates nearly $600 million more in market

value than the non-EVA peer companies."

- Jim Wallace, A. Professor

"EVA based companies outperform their non-EVA peer companies by 9%, 12%,

& 10%, one, two and three years, respectively, following adoption of EVA. Prior

to adoption of EVA, the EVA-based companies demonstrated no significant

excess performance relative to non-EVA peers."

- Robert Kleiman, Professor

"Unlike earnings or ROE or any of those other measures, EVA gets at what we're

really after: the creation of value by earning returns above our required cost of

capital across time."

- Bob Boldt, Senior Investment Officer

Northwest Mutual Fund

"We don't look for companies with the highest EVA for our funds, but for

companies that can positively increase their EVA."

- Michael Butler, President & CEO

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 19

It has been shown that share price has a much higher positive correlation with

EVA than with any other measure of value.

- IPS Advisory, Inc.

WALL STREET RESEARCH ANALYSTS

"The EVA methodology explicitly addresses business and financial risk and

allows the investor to gauge the magnitude and sustainability of returns.

Moreover, this structure examines the three fundamental principles of value

creation: cash flow, risk, and sustainability of returns. Of all financial measures, it

best explains the creation of shareholder value."

- Al Jackson

"The EVA approach to equity analysis has become increasingly popular because

it more accurately reflects economic reality (as opposed to accounting reality)

when compared with many traditional valuation measures, such as earnings per

share (EPS), return on equity (ROE), and free cash flow."

- Steven G.Einhorn

"Economic Value Added (EVA) is a superior metric… EVA has a higher

correlation with wealth creation than do EPS, ROE, or cash flow."

- Steven Milunovic

COMPANIES

COCO-COLA

“Economic Profit is the way to keep score. Why everybody doesn’t use it is a

mystery to me.”

- Roberto Goizueta, Past CEO

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 20

Corporation Bank:

“Economic Value Added is the foundation of everything we do at SPX.”

- John Blystone, CEO

“To help us make all the short- and long-term decisions that affect our company

and help it to grow, we use a highly respected performance indicator,

measurement, and compensation system called Economic Value Added (EVA).”

- Michael Volkema, CEO

2.9 Problem Statement: There are various views with respect to whether traditional measures or value-

based measures influence change in share price.

The question to be addressed is whether there is relationship between EVA and

Wealth creation and whether this relationship is significant

2.10 Significance of the study:

The research provides a fundamental platform to investors to analyze the

companies in terms of its present position; earning capabilities and the growth

potential unleashed which leads to value addition and subsequently increase or

decrease of share prices.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 21

There is a lot of academic and professional research undergoing these days with

the following question common to every research:

Which measure is better suitable in computing the value created on the

investments?

If the research conducted succeeds in the identification of the direct relationship

that exists between EVA and share, there will be a value addition to available

database.

2.11 The objective of the study is:

1) To describes the theory and characteristics of EVA.

2) To analyze the relationship between EVA and share prices.

3) To judge the relation between EVA and change in market capitalization

4) To establish that EVA is a better measure of performance

5) To give the framework to the investors to use EVA considering both its

favorable and unfavorable features in determination of the value created

on their investments

2.12 Scope of the study: The scope for the research investigation is restricted only to the following:-

• The research focuses only on twenty companies listed in BSE Sensex.

• The research is limited to the data available from 2002-03 to 2006-07.

2.13 Calculation of EVA,

Following steps are followed:

1) Calculating NOPAT (Net Operating Profit After Tax) using profit and loss

account.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 22

2) Calculating invested capital using Balance Sheet.

3) Calculating the returns on the market using the indices, which represent

the Market.

4) Extracting the risk free rate from sources.

5) Calculating cost of debt.

6) Calculating the cost of equity using CAPM model.

7) Using the above information, calculating EVA.

EVA calculation: Every calculation is done under Microsoft Excel mostly with the help of inbuilt

functions.

EVA Calculation

EVA = NOPAT - WACC (Capital Invested)

There are three stages involved in this they are

1. Calculation of NOPAT: Net Operating Profit after Taxes

2. Calculation of WACC: Weighted Average Cost of Capital

3. Calculation of Invested Capital

The Stages of the Process: 1. Calculation of NOPAT:

Getting to NOPAT takes three basic steps:

1. Start with earning before interest and taxes (EBIT)

2. Make the key adjustments - these come in two flavors:

a. Eliminating accounting distortions (convert accrual to cash).

b. Reclassifying some expenses as investments (i.e. Capitalizing

them to Balance sheet)

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 23

3. Subtract cash operating taxes

The basic exemption of Stern Stewart is that second step can be adjusted

as per the convenience of the research person but the only condition is that the

same process has to be followed for all the years and all the companies under

research.

The formula adopted to calculate NOPAT is as follows

NOPAT = EBIT (1+ Tax rate)

2. Calculation of WACC:

It refers weighted average cost of capital (equity and debt). WACC used in the

calculations is at book value of equity and debt. It is calculated as follows:

WACC = Ke *W1+ Kd *W2

Where,

W1 is weight of EQUITY

W2 is weight of DEBT

Ke is cost of EQUITY

Kd is cost of DEBT

W1 = Total equity / Total Capital.

W2 = Total debt / Total capital

Ke = Risk-Free Rate + (Beta x Equity Premium)

Equity Premium = Rf + β (Rm - Rf)

Where

Rf is Risk-Free Rate of Return.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 24

Rm is Average Return from Sensex which is considered as proxy to Market.

β is Beta.

Kd = Interest expenses (1- Tax rate) / Amount of Debt

3. Calculation of Invested Capital:

Getting to Capital invested takes three basic steps:

a. Get invested book capital from Balance sheet.

b. Make adjustments that convert accounting accruals to cash.

c. Make adjustments that recognize off-balance sheet sources of

funds. The basic exception of Stern Stewart is that there are many

processes for calculating but while calculating Invested Capital, the

most important condition is that the same process has to be

followed for all the years and all the companies under research.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 25

CHAPTER 3

LITRATURE REVIEW

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 26

3. REVIEW OF LITRATURE:

Stern Stewart in 1990 has first studied this relationship with market data of

618 U.S. companies. Stewart presents the results in his book "The quest

for value". Stewart has studied the relationship between EVA and market

value of the company and he has produced a list of companies’ EVA

annually since 1982, its coverage is limited to the largest 1,000

companies.

Stern Stewart claims that:

• EVA is the only true indicator of business and management performance;

• EVA is "today's hottest financial idea and getting hotter";

• EVA "allows all financial decisions to be modeled, monitored, evaluated,

communicated, and compensated in terms of a single measure";

• "EVA is the only reliable and unambiguous continuous-improvement

metric"

• EVA must be used to guide every decision;

• EVA should be used as the "deciding factor in all business decisions.

• Grant in 1996 showed that

EVA significantly impacts the market value added of a firm and that this wealth

effect stems from the company’s positive residual return on capital. He calculates

regression statistics between the MVA-to-capital and EVA-to-capital ratios from

the data of 983 firms.

• Peterson in 1996 showed that

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 27

Value-added measures are slightly but not significantly more correlated with

stock returns than traditional performance measures.

• Lehn and Makhija in 1996 conducted a study on EVA and MVA as

performance measures and signals for strategic change. Their data

consists of 241 U.S. companies and cover years 1987, 1988, 1992 and

1993. The researchers find out that

“Both measures correlate positively with stock returns and that the correlation is

slightly better than with traditional performance measures like return on assets

(ROA), return on equity (ROE) and return on sales (ROS).

Additionally they study how companies’ performance, as measured in terms of

EVA and MVA, affect on the CEO firings. Finally they examine the relationship

between EVA/MVA and corporate focus. Lehn and Makhija find an inverse

relation between EVA/MVA and abnormal CEO turnover.

They also find that firms with greater focus on their business activities have

significantly higher MVA than their less focused counterparts.

Lehn and Makhija conclude that their results suggest EVA and MVA to be

effective performance measures that contain information about the quality of

strategic decisions and serve as signals of strategic change.”

• Myers study of 1997 states that

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 28

EVA is the most widely used Value-Based performance measure probably just

because it happens to be an easier concept compared to the others. In

implementing EVA, one of the most important things is to get the people in

organizations to commit to EVA and thereby also to understand EVA. Even as

easy concept as EVA seems to be quite hard to communicate down the

organization. That is why complicated measures do not work very well.

• A research conducted by Dodd & Chen in 1998 suggests that

“Some Value-Based measures have been found to correlate better with share

prices than EVA and find that Cash Flow Return on investment (CFROI) explains

share price movements better than EVA. Of course EVA can also be modified in

order to avoid some accounting distortions and to correlate better with share

prices, but then we have almost as complicated measure as CFROI. The best

possible correlation with share prices is not however the main point, especially

when the differences in correlations are quite small and also disputable.

All the shareholder value metrics are said to be identical to discounted free cash

flow -method, so it is no wonder that we can relate the results of these metrics "to

the fourth decimal points". With the complicated shareholder wealth -measures it

is not always the toughest part to communicate these to people, but to calculate

these in day-to-day operations. E.g. CFROI calls for taking into account the

effects of inflation to asset values and this in turn takes time and resources.

In other words: it takes money. Hence it can perhaps in many occasions be

stated that the other metrics do not pass a prudent cost-benefit analysis; the

additional costs with implementing them instead of EVA are often more than the

incremental information achieved with them.”

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 29

• A research conducted by Ashok Banerjee on “Economic Value Added and

Shareholder Wealth - An empirical study of relationship” on nine industries

in 1999 concludes that

“EVA has proved to be an important explanatory variable with the observation

and it is true that companies, which have started disclosing EVA results in their

Annual Reports, would see a more direct impact on stock price.”

• Another research conducted by Dr. Srinivasan, Professor, National

Institute of Industrial Engineering (NITIE) on “Economic Value Added

(EVA) - An Emerging Tool for Value Creation” in 2000 suggests that

The study points out that EVA alone cannot be an ‘Indicator of

Value.’ At the best it can be used an additional tool. However the

use of EVA analysis in isolation can lead to misleading results.

In India, there is no big correlation between EVA, management

innovation and stock market analysis. EVA serves a useful indicator

only at the conceptual stage rather than on the operational stage.

As regards stock market indicator it cannot be relied upon as a sole

measure.

As far as India is concerned the stock trends depend on a number

of variables of which EVA is one among them. It is clear that only a

blend of EVA and other variables can give a holistic future on stock

market.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 30

• Another research conducted by Gerald T. Garvey and Todd T.

Milbourn states that

“They advance the literature by ascertaining the relative weights that firms should

use in a realistic setting where they do not know all of the relevant attributes of

alternative performance measures a priori.

More surprisingly, they show that the apparently simplistic idea of comparing the

relative ability of alternative measures to explain stock returns is both

theoretically defensible and a reasonable representation of practice. Therefore,

firms contemplating the adoption of EVA would be well advised to begin with an

examination of EVA's R2 with its stock returns.”

• One more research conducted by Madhav V. Rajan on “EVA versus

Earnings: Does It Matter Which Is More Highly Correlated with Stock

Returns?” In 2000 suggests that

“Implementing EVA in a form would have access to sufficient data about the

metrics to again obviate the need for R2 information. This paper concludes with

the message that a researcher who is unaware of the parameters governing the

metrics for a firm can make use of a complex nonlinear function of the metrics'

correlation with price to compute the value of adopting EVA. These are obviously

not the same things.”

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 31

• A research conducted by M Geyser & IE Liebenberg on “CREATING A

NEW VALUATION TOOL” on agricultural co-operatives in South Africa

in 2003 concludes that

“EVA as a value enhancement measure for agricultural co-operatives. EVA

measures the excess return on existing assets. It is important to remember when

using EVA as a value enhancement measure that it will not work unless there is

a commitment on the part of managers to make value maximization their primary

objective.

Finally, there are no magic bullets that create value. Value creation is hard work

in competitive markets and almost always involves a trade off between costs and

benefits. Everyone has a role in value creation and it certainly is not the sole

domain of financial analysts. In fact, the value created by financial engineers is

smaller and less significant than the value created by good strategic marketing,

production and personnel decisions.”

Learning form the review of literature:

From the study of above mentioned research papers, one can understand that

there is only confusion but not any clear idea regarding the usage or non-usage

of EVA in forecasting the share prices of the company.

Here is the research gap and the main objective behind this research

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 32

CHAPTER 4

Research Methodology

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 33

4. Research Methodology

4.1 Type of Research

The research type is historical analytical and quantitative.

Historical as the historical information is used for analysis and interpretation.

Analytical as facts and existing information is used for the analysis.

Quantitative as EVA is calculated and the variables are expressed in measurable

terms.

4.2 Sampling Technique

The Sampling method used here is Simple Random Sampling. The companies

listed in the stock exchange are considered since the market prices can be

obtained. The companies in the Sensex are chosen because it is an ideal index

and it is considered to be a good proxy for the whole market. Also it is a

barometer that indicates the state and health of the economy.

4.3 Sample Description Out of 30 companies included in the list of BSE Sensex, our Sample includes 20

companies for which relevant data is available, for a period of 5 years starting

from FY 2002-03 to FY 2006-07.

At irregular intervals, the Bombay Stock Exchange (BSE) authorities review and

modify its composition to make sure it reflects current market conditions.

Therefore only 20 companies are considered for the research as the data of all

the 30 companies for all the five years is unavailable.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 34

4.4 Sample Profile The following are the sample 20 companies:

Sl.no Company Name Sector

1 Associated Cement Companies Ltd. Housing Related 2 Bharati Airtel. Telecom 3 Bharat Heavy Electricals Ltd. Capital Goods 4 Cipla Ltd. Healthcare 5 Grasim Industries Ltd. Diversified 6 Gujarat Ambuja Cements Ltd. Housing Related 7 HDFC Finance Finance 8 HDFC Bank Finance 9 Hindalco Metal, Metal Products &

Mining 10 Hindustan Lever Ltd. FMCG 11 Infosys Technologies Ltd Information Technology

12 ITC Ltd. FMCG 13 Larsen & Tourbro Ltd. Capital Goods &

Construction

14 Mahindra & Mahindra Transport Equipments 15 Maruti Transport Equipments 16 ONGC Oil & Gas 17 Ranbaxy Laboratories Ltd. Healthcare 18 Reliance Industries Oil & Gas 19 Reliance Energy Power 20 Wipro Ltd. Information Technology

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 35

4.5 Data gathering procedure and instrumentation

Data type: Secondary data

Required data:

• Balance Sheet

• Profit and loss Account

• History of stock prices

• History of market index

• Risk free rate of return

• Corporate tax rate

Data Source

• Balance sheet and Profit and loss Account are taken from the financial

statements of the selected companies from the database of Capital

Market.

• History of stock prices and history of market index are downloaded from

database of Capital Market and Bombay stock exchange.

• Risk free rate of return of relevant years is taken from the RBI bulletin

As 365 days Treasury bill rate is considered to be the proxy for risk free

rate of return.

• Corporate tax rate is taken from the Indian annual budget statements and

KPMG survey 2006.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 36

4.6 Hypothesis

H0: There is no relationship between EVA and Share prices.

H1: There is a relationship between EVA and Share prices.

Tools used for testing of hypothesis:

The hypothesis is tested using linear regression tool, simple co-efficient of

Correlation, co-efficient of determination and t-statistic.

Co-efficient of correlation is used to describe how well one variable is explained

by the other variable. It reveals the magnitude and direction of relationship. The

magnitude is the degree to which variables move in the same or opposite

direction. The co-efficient signifies the direction of the relationship.

Co-efficient of determination measures the extent, or strength of the association

that exists between the two variables.

T-statistic is used for testing the significance of an dependent variable over the

independent variable.

There are two methods of testing the relationship with the help of t-statistics.

They are

1. To compare the values of t- calculated with that of t- tabulated.

In this case if the calculated t-value is greater than that of table value null

hypothesis has to be rejected and alternate hypothesis has to be accepted.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 37

2. To compare the p- value with that of level of significance.

In this research report this method is adopted.

• If the p-value is greater than or equal to level of significance the null

hypothesis is accepted.

• If the p-value is less than the level of significance, the null

hypothesis is rejected.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 38

CHAPTER 5

DATA ANALYSIS AND

INTERPRETATION

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 39

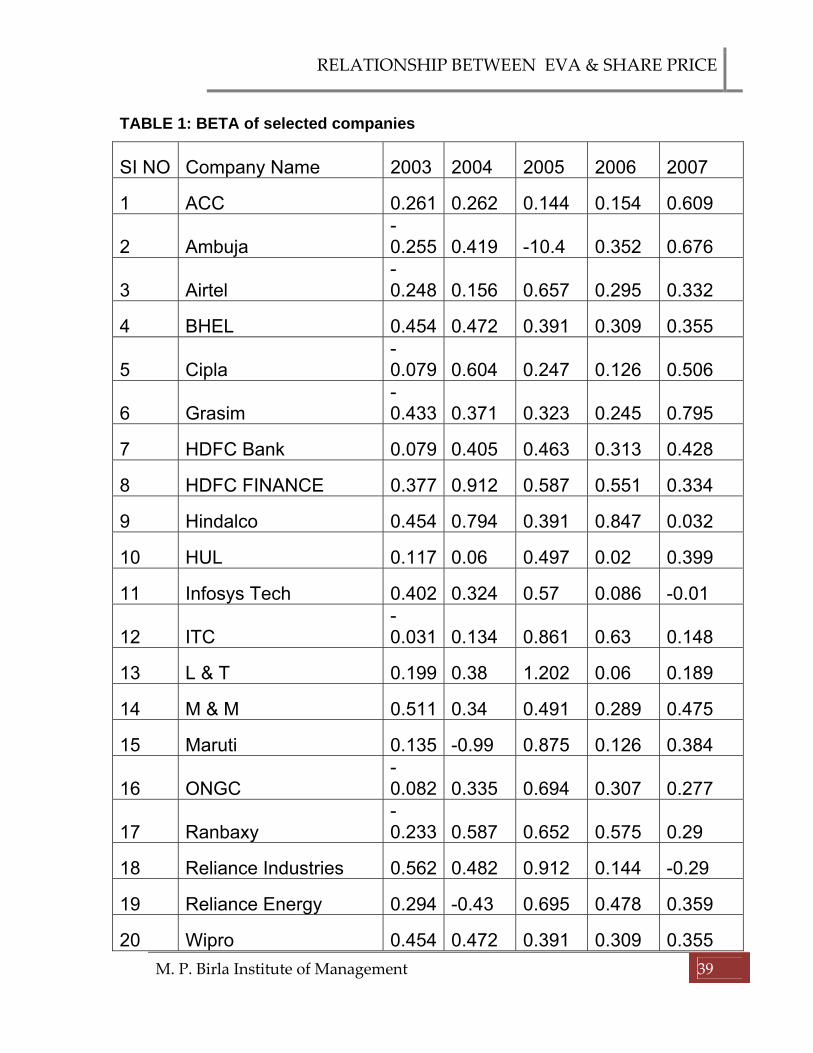

TABLE 1: BETA of selected companies

SI NO Company Name 2003 2004 2005 2006 2007

1 ACC 0.261 0.262 0.144 0.154 0.609

2 Ambuja -0.255 0.419 -10.4 0.352 0.676

3 Airtel -0.248 0.156 0.657 0.295 0.332

4 BHEL 0.454 0.472 0.391 0.309 0.355

5 Cipla -0.079 0.604 0.247 0.126 0.506

6 Grasim -0.433 0.371 0.323 0.245 0.795

7 HDFC Bank 0.079 0.405 0.463 0.313 0.428

8 HDFC FINANCE 0.377 0.912 0.587 0.551 0.334

9 Hindalco 0.454 0.794 0.391 0.847 0.032

10 HUL 0.117 0.06 0.497 0.02 0.399

11 Infosys Tech 0.402 0.324 0.57 0.086 -0.01

12 ITC -0.031 0.134 0.861 0.63 0.148

13 L & T 0.199 0.38 1.202 0.06 0.189

14 M & M 0.511 0.34 0.491 0.289 0.475

15 Maruti 0.135 -0.99 0.875 0.126 0.384

16 ONGC -0.082 0.335 0.694 0.307 0.277

17 Ranbaxy -0.233 0.587 0.652 0.575 0.29

18 Reliance Industries 0.562 0.482 0.912 0.144 -0.29

19 Reliance Energy 0.294 -0.43 0.695 0.478 0.359

20 Wipro 0.454 0.472 0.391 0.309 0.355

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 40

TABLE 2: INVESTED CAPITAL of selected companies:

SI NO Company Name 2003 2004 2005 2006 2007

1 ACC 2982.88 3317.69 3347.51 4100.38 4647.71

2 Ambuja 3367.863 3291.37 3305.84 4355.96 4991.29

3 Airtel 4825.67 5451.22 9527.89 12129.72 16724.01

4 BHEL 5337.89 5835.87 6563.87 5835.87 8877.59

5 Cipla 1164.86 1474.63 1744.83 2454.18 3359.83

6 Grasim 5053.38 5676.38 6336.69 6961.75 9181.6

7 HDFC Bank 91319.29 73586.87 51505.98 42379.98 30482.45

8 HDFC FINANCE 26296.14 32077.83 40530.5 51189.68 62744.42

9 Hindalco 8586.11 9422.5 11466.58 14509.7 19786.64

10 HUL 3843.03 3563.83 2362.56 2796.09 1427.77

11 Infosys Tech 2,860.65 3,253.43 5,242.00 6,897.00 11,162.00

12 ITC 5482.6 6530.91 8140.97 9181.21 10637.96

13 L & T 6738.54 4099.39 5228.19 6093.74 7846.18

14 M & M 2709.68 2504.84 3039.15 3792.25 5188.91

15 Maruti 3554 3903.1 4686.4 5524.3 7484.7

16 ONGC 36539.19 51950.89 56761.64 66682.28 77033

17 Ranbaxy 36539.19 51950.89 56761.64 66682.28 77033

18 Reliance Industries 50132.72 55397.11 59187.91 71699.87 91792.86

19 Reliance Energy 3209.88 7159.54 9532.66 12075.51 15222.2

20 Wipro 3,399.96 3,608.28 4,954.53 6,470.61 9,554.90

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 41

TABLE 3: NOPAT of selected companies:

SI NO Company Name 2003 2004 2005 2006 2007

1 ACC 244.0322 360.3113 500.2317 1129.85 1336.173

2 Ambuja 253.466 331.8299 406.8937 1303.285 1858.893

3 Airtel 2100.105 1440.739 125424.9 170181.8 325578.9

4 BHEL 571.4686 716.5625 1108.709 1748.781 2519.679

5 Cipla 211.3306 271.9536 350.8642 483.9642 546.1206

6 Grasim 448.6824 820.801 961.6947 872.9836 1558.878

7 HDFC Bank 1175.265 1286.738 1529.743 2122.113 3212.294

8 HDFC FINANCE 188064.7 193432.3 214596.1 270334.8 376085.5

9 Hindalco 691.1346 948.5941 1382.836 1553.991 2498.138

10 HUL 1489.901 1076.707 1095.341 1465.567 1568.945

11 Infosys Tech 773.1587 980.8624 1486.741 1824.758 2768.805

12 ITC 1397.697 1568.905 2052.236 2163.622 2628.625

13 L & T 511.8523 596.0165 937.9069 1036.732 1427.851

14 M & M 208.9079 343.4305 486.2981 751.0109 958.9079

15 Maruti 223.2112 542.1604 893.978 1180.326 1545.011

16 ONGC 1082423 910278.8 1313489 1458806 1580592

17 Ranbaxy 282.6992 448.8008 514.7158 452.6917 400.2217

18 Reliance Industries 4353.131 5157.498 7025.245 7721.119 10473.43

19 Reliance Energy 152.6476 324.8496 469.4301 648.9124 748.3974

20 Wipro 622.751 723.683 1174.56 1561.95 2122.37

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 42

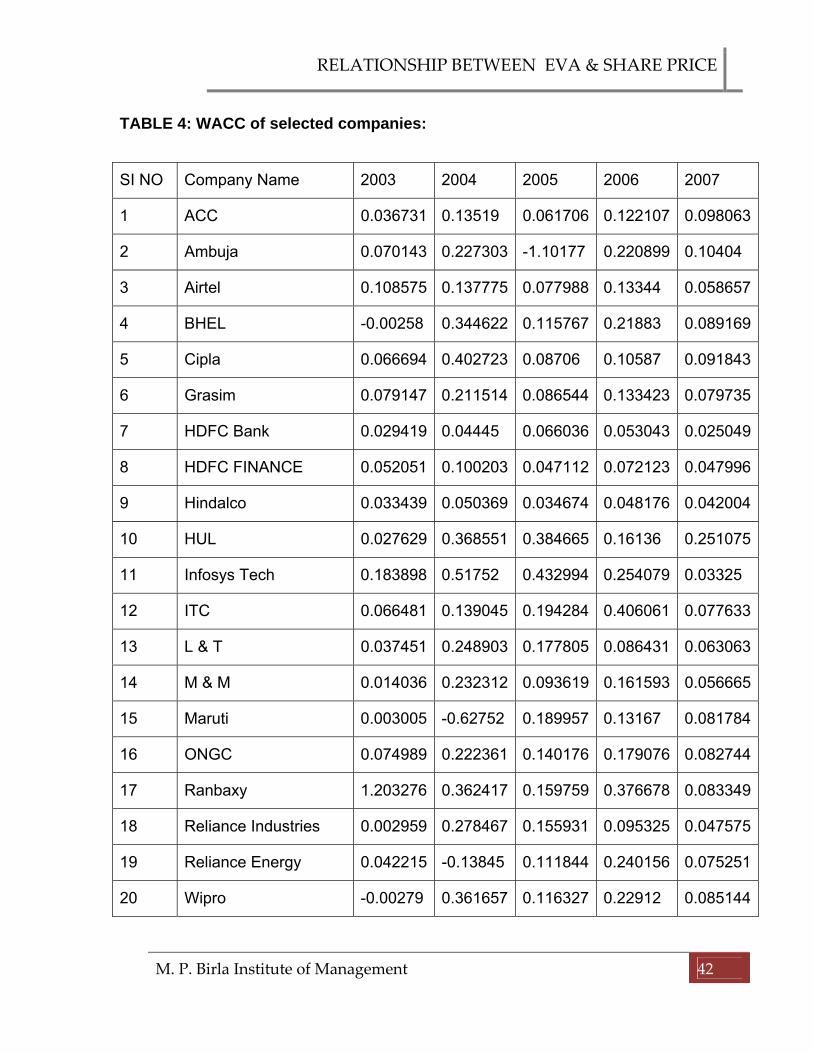

TABLE 4: WACC of selected companies:

SI NO Company Name 2003 2004 2005 2006 2007

1 ACC 0.036731 0.13519 0.061706 0.122107 0.098063

2 Ambuja 0.070143 0.227303 -1.10177 0.220899 0.10404

3 Airtel 0.108575 0.137775 0.077988 0.13344 0.058657

4 BHEL -0.00258 0.344622 0.115767 0.21883 0.089169

5 Cipla 0.066694 0.402723 0.08706 0.10587 0.091843

6 Grasim 0.079147 0.211514 0.086544 0.133423 0.079735

7 HDFC Bank 0.029419 0.04445 0.066036 0.053043 0.025049

8 HDFC FINANCE 0.052051 0.100203 0.047112 0.072123 0.047996

9 Hindalco 0.033439 0.050369 0.034674 0.048176 0.042004

10 HUL 0.027629 0.368551 0.384665 0.16136 0.251075

11 Infosys Tech 0.183898 0.51752 0.432994 0.254079 0.03325

12 ITC 0.066481 0.139045 0.194284 0.406061 0.077633

13 L & T 0.037451 0.248903 0.177805 0.086431 0.063063

14 M & M 0.014036 0.232312 0.093619 0.161593 0.056665

15 Maruti 0.003005 -0.62752 0.189957 0.13167 0.081784

16 ONGC 0.074989 0.222361 0.140176 0.179076 0.082744

17 Ranbaxy 1.203276 0.362417 0.159759 0.376678 0.083349

18 Reliance Industries 0.002959 0.278467 0.155931 0.095325 0.047575

19 Reliance Energy 0.042215 -0.13845 0.111844 0.240156 0.075251

20 Wipro -0.00279 0.361657 0.116327 0.22912 0.085144

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 43

TABLE 5: SHARE PRICES of selected companies:

SI NO Company Name 2003 2004 2005 2006 2007

1 ACC 148.6025 204.3667 289.4408 487.4683 927.9225

2 Ambuja 23.36667 32.2275 43.05583 72.89083 117.9617

3 Airtel 29.895 78.55667 171.5175 507.8867 520.17

4 BHEL 87.97917 198.0733 315.5742 626.155 1118.903

5 Cipla 73.1 79.8225 104.6858 153.6733 246.0817

6 Grasim 314.2883 727.4717 1158.968 1332.09 2359.734

7 HDFC Bank 217.5967 301.9808 438.1608 659.4875 914.3142

8 HDFC FINANCE 329.5208 501.585 662.8167 1018.214 1408.893

9 Hindalco 241.615 94.3425 305.6117 291.6358 172.8783

10 HUL 136.05 153.35 134.7933 176.8075 231.5117

11 Infosys Tech 482.9508 531.025 863.8875 1258.33 1880.815

12 ITC 43.1391 57.3225 75.275 128.1108 178.2592

13 L & T 92.2483 181.6175 402.6267 764.5017 1326.798

14 M & M 49.9025 136.3542 237.8483 397.59 719.2775

15 Maruti 266.47 328.9178 427.8058 575.4542 870.47

16 ONGC 236.0683 399.19 516.6467 684.5133 819.08

17 Ranbaxy 236.0683 399.19 516.6467 684.5133 819.08

18 Reliance Industries 222.1617 348.5825 421.955 605.1217 1154.897

19 Reliance Energy 218.7675 411.07 598.27 581.3517 504.8458

20 Wipro 241.615 207.303 305.612 409.492 543.657

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 44

Interpretation: TABLE 1: BETA It can be seen that beta for most of the companies has increased from year to

year from Table-1. Earlier, in 2003 it was on an average of 0.15 when all the

companies are taken together. But slowly it has increased to about 0.40 by the

end of 2007. Thus we can say that riskiness of the stock is increased during the

period of 2003 to 2007.

TABLE 2: INVESTED CAPITAL Total capital employed of almost companies is increased consistently from

2003-2007. While, HUL has reduced its capital fund from 3843.03 crore to

1427.77 crore in 2007. L&T and Ambuja have also reduced its capital fund during

2004 but it has again increased the capital fund in 2005 and 2006.

TABLE 3: NOPAT NOPAT is increased consistently increased and improved from year to year of

almost companies. There are some variations in case of Airtel, HUL, ONGC and

Ranbaxy.

TABLE 4: WACC From the table it is concluded that weighted average cost of capital (WACC) of

the all companies during 2003 and 2004 is very low. WACC is around 0.02

during these years. But in 2004 WACC is increased drastically because of

increasing beta. In case of Infosys there is only equity fund employed and they

are known as debt free company.

TABLE 5: SHARE PRICES From the table it is clear that the share prices went on increasing from year to

year because of increase in beta. It is because as the market is becoming more

and more risky investors expected return is going on a hike.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 45

Forecasted Eva & Share price for the year 2008. Sl No Company EVA SHARE PRICE

1 ACC 1032.674 908.8834

2 Ambuja 2086.779 60.73627

3 Airtel 368196.9 645.0349

4 BHEL 1583.445 799.9634

5 Cipla 320.6328 167.6571

6 Grasim 734.6403 1894

7 HDFC Bank 2324.705 918.177

8 HDFC FINANCE -2153.76 838.026

9 Hindalco 1749.137 230.4962

10 HUL 983.0629 172.6005

11 Infosys Tech 1769.17 1563.617

12 ITC 274.7111 96.18761

13 L & T 941.7613 1119.56

14 M & M 596.8598 574.6667

15 Maruti 589.3737 496.8845

16 ONGC ‐6713.34

530.9883

17 Ranbaxy Laboratories Ltd. 451.9943

756.4965

18 Reliance Industries 4232.465

678.2184

19 Reliance Energy -1701.04

550.3152

20 Wipro Ltd. 1011.646 421.6915

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 46

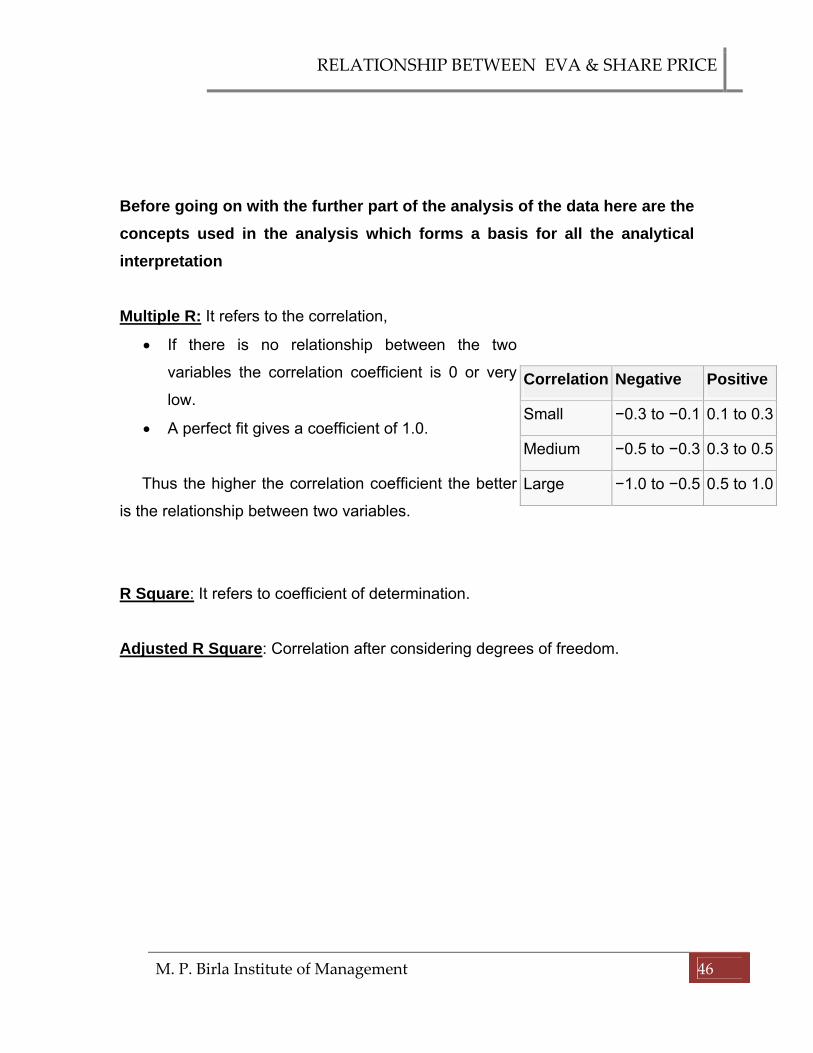

Before going on with the further part of the analysis of the data here are the concepts used in the analysis which forms a basis for all the analytical interpretation Multiple R: It refers to the correlation,

• If there is no relationship between the two

variables the correlation coefficient is 0 or very

low.

• A perfect fit gives a coefficient of 1.0.

Thus the higher the correlation coefficient the better

is the relationship between two variables.

R Square: It refers to coefficient of determination.

Adjusted R Square: Correlation after considering degrees of freedom.

Correlation Negative Positive

Small −0.3 to −0.1 0.1 to 0.3

Medium −0.5 to −0.3 0.3 to 0.5

Large −1.0 to −0.5 0.5 to 1.0

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 47

ACC:

→Large positive correlation. If EVA moves by one, share

price will move by 0.9189 in the same direction.

→84.44% of change in share price is due to change in EVA.

The t-statistics of this is 4.034568. The p- value in this case is 0.027384, which is less than 5% level of significance.

Therefore Alternate hypothesis is accepted.

As such there is a relationship between EVA and share.

Year EVA(X) Share price(Y)

2003 134.466784 148.6025

2004 -88.205619 204.3667

2005 293.671408 289.4408

2006 629.166754 487.4683

2007 880.402994 927.9225

Regression

Statistics

Multiple R 0.918902

R Square 0.84438

Adjusted R Square 0.792507

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 48

Airtel:

→Large positive correlation. If EVA moves by one, share

price will move by 0.9189 in the same direction.

→84.44% of change in share price is due to change in EVA.

The t-statistics of this is 3.479578. The p- value in this case is 0.040067, which is less than 5% level of significance.

Therefore Alternate hypothesis is accepted.

As such there is relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 1576.15597 29.895

2004 689.694416 78.55667

2005 124681.872 171.5175

2006 168563.252 507.8867

2007 324597.963 520.17

Regression

Statistics

Multiple R 0.895222

R Square 0.801423

Adjusted R Square 0.73523

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 49

BHEL:

→Large positive correlation. If EVA moves by one, share

price will move by 0.708 in the same direction.

→50%of change in share price is due to change in EVA.

The t-statistics of this is 1.737359. The p- value in this case is 0.180718, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 585.241841 87.97917

2004 -1294.6058 198.0733

2005 348.829449 315.5742

2006 471.716669 626.155

2007 1728.07144 1118.903

Regression

Statistics

Multiple R 0.708188

R Square 0.50153

Adjusted R Square 0.335373

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 50

CIPLA:

→Large positive correlation. If EVA moves by one, share

price will move by 0.529 in the same direction.

→27.97% of change in share price is due to change in EVA.

The t-statistics of this is 1.079284 The p- value in this case is 0.3595, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 133.641809 73.1

2004 -321.91415 79.8225

2005 198.95983 104.6858

2006 224.140919 153.6733

2007 237.544622 246.0817

Regression

Statistics

Multiple R 0.528854

R Square 0.279687

Adjusted R Square 0.039582

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 51

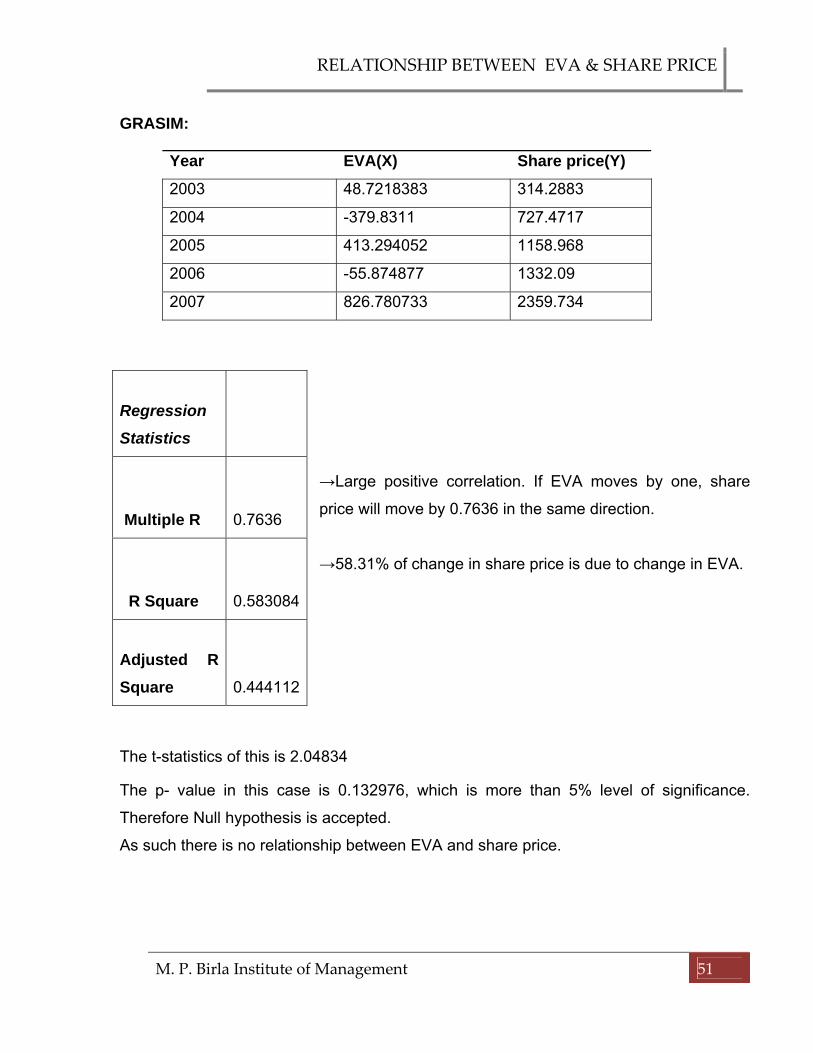

GRASIM:

→Large positive correlation. If EVA moves by one, share

price will move by 0.7636 in the same direction.

→58.31% of change in share price is due to change in EVA.

The t-statistics of this is 2.04834 The p- value in this case is 0.132976, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 48.7218383 314.2883

2004 -379.8311 727.4717

2005 413.294052 1158.968

2006 -55.874877 1332.09

2007 826.780733 2359.734

Regression

Statistics

Multiple R 0.7636

R Square 0.583084

Adjusted R Square 0.444112

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 52

Gujarat Ambuja

→Small positive correlation. If EVA moves by one, share

price will move by 0.129 in the same direction.

→1.67% of change in share price is due to change in EVA.

The t-statistics of this is 0.225943.

The p- value in this case is 0.835764, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 17.233118 23.36667

2004 -416.30818 32.2275

2005 4049.15398 43.05583

2006 341.058943 72.89083

2007 1339.60156 117.9617

Regression

Statistics

Multiple R 0.129352

R Square 0.016732

Adjusted R Square -0.31102

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 53

HDFC Bank:

→Large positive correlation. If EVA moves by one, share

price will move by 0.9252 in the same direction.

→85.56% of change in share price is due to change in EVA.

The t-statistics of this is 4.223525.

The p- value in this case is 0.02427, which is less than 5% level of significance.

Therefore Alternate hypothesis is accepted.

As such there is a relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 -1511.2649 217.5967

2004 -1984.2215 301.9808

2005 -1871.5028 438.1608

2006 -125.84661 659.4875

2007 2448.75096 914.3142

Regression

Statistics

Multiple R 0.925221

R Square 0.856033

Adjusted R Square 0.808045

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 54

HDFC Finance:

→Small positive correlation. If EVA moves by one, share

price will move by 0.24 in the same direction.

→5.76% of change in share price is due to change in EVA.

The t-statistics of this is -0.42825.

The p- value in this case is 0.697356, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 186695.968 329.5208

2004 16127.9931 501.585

2005 212686.62 662.8167

2006 266642.834 1018.214

2007 373074.025 1408.893

Regression

Statistics

Multiple R 0.240021

R Square 0.05761

Adjusted R Square -0.25652

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 55

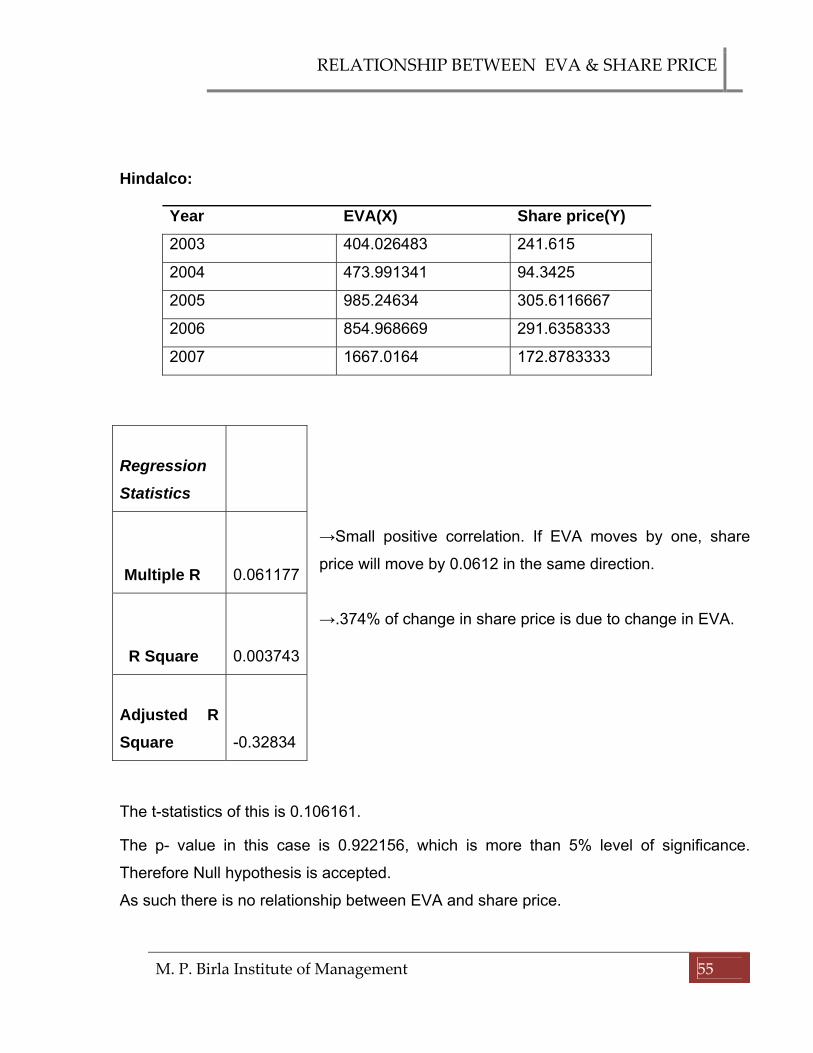

Hindalco:

→Small positive correlation. If EVA moves by one, share

price will move by 0.0612 in the same direction.

→.374% of change in share price is due to change in EVA.

The t-statistics of this is 0.106161. The p- value in this case is 0.922156, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 404.026483 241.615

2004 473.991341 94.3425

2005 985.24634 305.6116667

2006 854.968669 291.6358333

2007 1667.0164 172.8783333

Regression

Statistics

Multiple R 0.061177

R Square 0.003743

Adjusted R Square -0.32834

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 56

HUL:

→Medium positive correlation. If EVA moves by one, share

price will move by 0.392784 in the same direction.

→15.43% of change in share price is due to change in EVA.

The t-statistics of this is 0.739777

The p- value in this case is 0.513066, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 1383.72394 136.05

2004 -236.74715 153.35

2005 186.546737 134.7933

2006 1014.38882 176.8075

2007 1210.46748 231.5117

Regression

Statistics

Multiple R 0.392784

R Square 0.154279

Adjusted R Square -0.12763

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 57

Infosys:

→Large positive correlation. If EVA moves by one, share

price will move by 0.9189 in the same direction.

→84.44% of change in share price is due to change in EVA.

The t-statistics of this is 2.43647. The p- value in this case is 0.092792, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 247.089698 482.9508

2004 -702.85272 531.025

2005 -783.01145 863.8875

2006 72.375037 1258.33

2007 2397.6686 1880.815

Regression

Statistics

Multiple R 0.815042

R Square 0.664294

Adjusted R Square 0.552392

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 58

ITC:

→Small positive correlation. If EVA moves by one, share

price will move by 0.0254 in the same direction.

→.0646% of change in share price is due to change in EVA.

The t-statistics of this is 0.04402

The p- value in this case is 0.967654, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 1033.20737 43.1391

2004 660.817448 57.3225

2005 470.572946 75.275

2006 -1564.5084 128.1108

2007 1802.76922 178.2592

Regression

Statistics

Multiple R 0.025407

R Square 0.000646

Adjusted R Square -0.33247

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 59

L & T:

→Large positive correlation. If EVA moves by one, share

price will move by 0.8394 in the same direction.

→70.46% of change in share price is due to change in EVA.

The t-statistics of this is 2.674852

The p- value in this case is 0.075378, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 259.48926 92.2483

2004 -424.3343 181.6175

2005 8.30691828 402.6267

2006 510.042795 764.5017

2007 933.05102 1326.798

Regression

Statistics

Multiple R 0.839389

R Square 0.704574

Adjusted R Square 0.606099

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 60

M & M:

→Large positive correlation. If EVA moves by one, share

price will move by 0.7924 in the same direction.

→62.78% of change in share price is due to change in EVA.

The t-statistics of this is 2.2496

The p- value in this case is 0.109975, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 170.875309 49.9025

2004 -238.47406 136.3542

2005 201.775889 237.8483

2006 138.209798 397.59

2007 664.878032 719.2775

Regression

Statistics

Multiple R 0.792358

R Square 0.627831

Adjusted R Square 0.503774

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 61

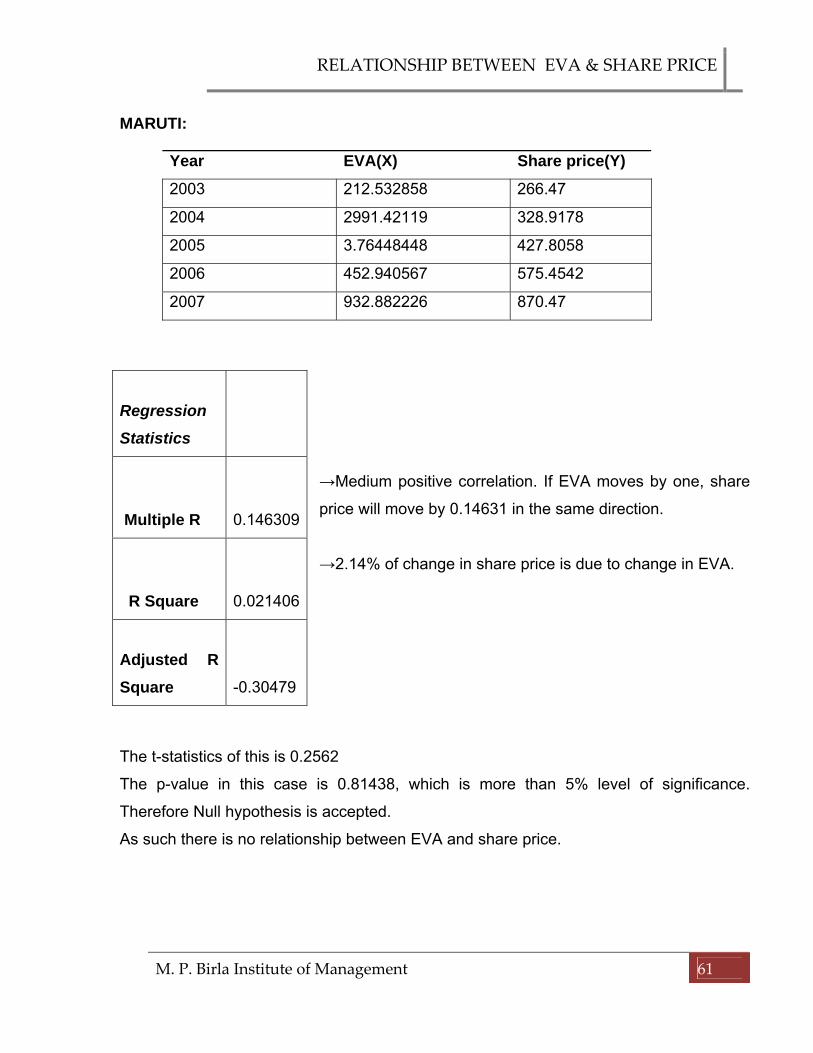

MARUTI:

→Medium positive correlation. If EVA moves by one, share

price will move by 0.14631 in the same direction.

→2.14% of change in share price is due to change in EVA.

The t-statistics of this is 0.2562

The p-value in this case is 0.81438, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 212.532858 266.47

2004 2991.42119 328.9178

2005 3.76448448 427.8058

2006 452.940567 575.4542

2007 932.882226 870.47

Regression

Statistics

Multiple R 0.146309

R Square 0.021406

Adjusted R Square -0.30479

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 62

ONGC:

→Very small positive correlation. If EVA moves by one,

share price will move by 0.0130 in the same direction.

→0.0168% of change in share price is due to change in EVA.

The t-statistics of this is -0.022.

The p- value in this case is 0.983482, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 -2719.0387 236.0683

2004 -11537.433 399.19

2005 -6702.3579 516.6467

2006 -10239.35 684.5133

2007 -3118.1909 819.08

Regression

Statistics

Multiple R 0.012974

R Square 0.000168

Adjusted R Square -0.33311

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 63

Ranbaxy:

→Very small positive correlation. If EVA moves by one,

share price will move by 0.0130 in the same direction.

→0.0168% of change in share price is due to change in EVA.

The t-statistics of this is 1.7715.

The p- value in this case is 0.983482, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 -1979.8566 236.0683

2004 -404.34376 399.19

2005 92.5464295 516.6467

2006 -830.58204 684.5133

2007 -60.508 819.08

Regression

Statistics

Multiple R 0.012974

R Square 0.000168

Adjusted R Square -0.33311

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 64

Reliance Industries:

→ Medium positive correlation. If EVA moves by one, share

price will move by 0.50152 in the same direction.

→ 25.15% change in share price is due to change in EVA.

The t-statistics of this is 0.3893.

The p- value in this case is 0.389327, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 4204.79832 222.1617

2004 -10268.775 348.5825

2005 -2203.991 421.955

2006 886.327229 605.1217

2007 6106.42638 1154.8971

Regression

Statistics

Multiple R 0.50152

R Square 0.251522

Adjusted R Square 0.002029

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 65

Reliance Energy:

→Large positive correlation. If EVA moves by one, share

price will move by 0.5480 in the same direction.

→30% of change in share price is due to change in EVA.

The t-statistics of this is 0.3389

The p- value in this case is 0.33894, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 17.1439079 411.07

2004 -10268.775 348.5825

2005 -596.73733 598.27

2006 -2251.0993 581.3517

2007 -397.08924 504.8458

Regression

Statistics

Multiple R 0.548017

R Square 0.300323

Adjusted R Square 0.067097

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 66

Wipro:

→Large positive correlation. If EVA moves by one, share

price will move by 0.5480 in the same direction.

→30% of change in share price is due to change in EVA.

The t-statistics of this is 1.6221.

The p- value in this case is 0.203243, which is more than 5% level of significance.

Therefore Null hypothesis is accepted.

As such there is no relationship between EVA and share price.

Year EVA(X) Share price(Y)

2003 632.23431 241.615

2004 -581.2762 207.3025

2005 598.2125 305.6117

2006 79.405193 409.4917

2007 1308.8339 543.6567

Regression

Statistics

Multiple R 0.683551

R Square 0.467242

Adjusted R Square 0.289656

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 67

CHAPTER 6

SUMMARY AND

RECOMMENDATIION

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 68

6.1 Findings form the study:

• Investing in the market is becoming more and more risky as the beta of the

individual securities is increasing year by year.

• The increase in beta is increasing weighted average cost of capital; it specifies

that capital is becoming more and more costly.

• Majority of the companies are increasing their capital to meet the increased

expenses.

• As the market is becoming more and more risky, investors’ expectations are

increasing and therefore share prices of almost all the companies for almost all

the years showed an increasing trend.

• Data analysis of 20 companies shows that

Share prices of two companies’ shows high correlation of coefficient and

coefficient of determination with EVA.

Share prices of eighteen companies’ shows low correlation of coefficient

and coefficient of determination with EVA.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 69

This specifies that there is no relationship between EVA and share price.

6.2 Conclusion from the study: This report explains the importance of using EVA as a tool for measuring

financial performance. The study reveals that there is no strong pattern of EVA of

selected companies during the period.

The wealth created by most companies in year 2004 is negative because of

higher cost of capital. The central idea of EVA is subtracting the cost of capital

from the firm's profits to measure, as the term indicates, the economic additional

value produced by the firm to its owners over the weighted cost of the capital

employed. It reveals that the the decision of managers between using equity fund

or debt fund will influence EVA to the greater extent. This raised the question of

the effect of the debt and equity cost components on the behavior of EVA. It was

observed that the cost of debt has little effect on the EVA's. On the other hand,

as is expected, EVA behaves in a linear fashion with respect to the cost of equity

It is also observed that there is no strong relation between EVA and market

prices of the companies. Thus, it can be understood that investor do not give so

importance to EVA for its investment decision. Extensive study is required to

establish the influence of other factors like non-fund based income, spread,

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 70

deployment of funds, market price, etc. It is also expected that the usage of EVA

as a financial performance tool will also be more in India.

The study adds that EVA is the one of the measure, which can be used to

measure the performance of the company but it cannot be used to forecast the

share price of the company.

6.2 Suggestions for further research:

This research has a limited scope, that is only five years and the data of only

twenty companies is taken into consideration. These five years had showed a lot

of variations with respect to beta, invested capital, weighted average cost of

capital and share prices.

To overcome this limitation of the study, the sample size and the years of

consideration for the research has to be increased, so as to decrease the

variations with respect to the above mentioned variables.

Extensive study is required to establish the influence of other factors like

expectations of investors with respect to mergers and acquisitions, sold outs and

various other factors which influence investors to undertake investing decisions.

It is because in these days all the above mentioned factors are common and it is

expected that it will also influence share prices.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 71

Bibliography: A. Books

• Chandra, Prasanna, Financial management, Second Edition, New Delhi:

Tata McGraw-Hill Publishing Company Limited, 2005.

• Kulkarni, P.V. and Sathyaprasad B.G., Financial Management, Ninth

Edition, Himalaya Publishing House, 1999.

• Pandey, I.M., Financial Management, Eighth Edition, Vikas Publishing

House Pvt. Ltd., 1999.

B. Articles • Lehn and Makhija., “a study on EVA and MVA as performance measures

and signals for strategic change”.

• Banerjee, Ashok., “Economic Value Added and Shareholder Wealth - An

empirical study of relationship”.

• Dr. Srinivasan, Professor, National Institute of Industrial Engineering

(NITIE) on “Economic Value Added (EVA) - An Emerging Tool for Value

Creation”

• “Relationship between EVA and share price”, The ICFAI Journal of

Applied Finance, Vol. 13, No.1, (January, 2007), pp. 5-20.

• Sheik, Aamir M., “How EVA influences stock market”, The Journal of

Finance, Vol. 44, No. 5. (December, 1987), pp. 1361-1372.

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 72

C. Databases

• Prowess

• Capital-online

D. Websites • www.nseindia.com

• www.google.com

• www.rediff.com/finance

• www.jstor.com

• www.eva.com

• www.wikepedia.com

• www.sternstewart.com

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 73

APPENDICES:

ACC

year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 0.2606441 0.0487292 0.023202 0.53 0.47 0.0367314 2982.88 244.0322 148.6025

2003-04 0.2617192 0.0401992 0.2264548 0.49 0.51 0.1351895 3317.69 360.31135 204.3667

2004-05 0.1444204 0.037272 0.0754496 0.36 0.64 0.0617056 3347.51 500.23168 289.4408

2005-06 0.1536011 0.0540168 0.142445 0.23 0.77 0.1221065 4100.38 1129.8498 487.4683

2006-07 0.6089198 0.1031633 0.0974968 0.1 0.9 0.0980635 4647.71 1336.1735 927.9225

AMBUJA year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 -

0.2551141 0.0482033 0.0939115 0.52 0.48 0.0701433 3367.863 253.46601 23.36667 2003-04 0.4185113 0.0599761 0.3342824 0.39 0.61 0.2273029 3291.37 331.82992 32.2275

2004-05 -

10.383869 0.0542668 -

1.6972972 0.34 0.66 -

1.1017655 3305.84 406.89368 43.05583 2005-06 0.3516393 0.0872339 0.254315 0.2 0.8 0.2208988 4355.96 1303.2852 72.89083 2006-07 0.6758358 0.1534891 0.1003175 0.07 0.93 0.1040395 4991.29 1858.8929 117.9617

AIRTEL year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 -

0.2482196 1.65545 0.0929504 0.01 0.99 0.1085754 4825.67 2100.105 29.895 2003-04 0.1563647 0.0037467 0.1543408 0.11 0.89 0.1377754 5451.22 1440.7387 78.55667 2004-05 0.656729 0.0007436 0.1616704 0.52 0.48 0.0779884 9527.89 125424.94 171.5175 2005-06 0.2948477 0.0004351 0.22211 0.4 0.6 0.13344 12129.72 170181.84 507.8867 2006-07 0.3315816 0.0009038 0.0858351 0.32 0.68 0.0586571 16724.01 325578.94 520.17

BHEL

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 74

year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 0.4537341 0.0683648 -

0.0032969 0.01 0.99 -

0.0025803 5337.89 571.46857 87.97917 2003-04 0.4720303 0.0741724 0.3713696 0.09 0.91 0.3446219 5835.87 716.56249 198.0733 2004-05 0.391259 0.1010765 0.1170444 0.08 0.92 0.115767 6563.87 1108.7088 315.5742 2005-06 0.3086232 0.0701645 0.23002 0.07 0.93 0.2188301 5835.87 1748.7808 626.155 2006-07 0.3548143 0.3233864 0.0868034 0.01 0.99 0.0891692 8877.59 2519.6793 1118.903

CIPLA

GRASIM year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 -

0.4334252 0.0540824 0.1183509 0.61 0.39 0.0791471 5053.38 448.68243 314.2883 2003-04 0.3714894 0.0506442 0.3020028 0.36 0.64 0.2115137 5676.38 820.80104 727.4717 2004-05 0.3231908 0.0460636 0.1055932 0.32 0.68 0.0865437 6336.69 961.69475 1158.968 2005-06 0.2448064 0.0348156 0.19386 0.38 0.62 0.1334231 6961.75 872.98365 1332.09 2006-07 0.7951595 0.0252625 0.1053695 0.32 0.68 0.0797353 9181.6 1558.8779 2359.734

HDFC BANK year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 0.0786464 0.0280062 0.0481906 0.93 0.07 0.0294191 30482.45 1175.2654 217.5967 2003-04 0.4053889 0.023307 0.325354 0.93 0.07 0.0444503 42379.98 1286.7377 301.9808 2004-05 0.4626458 0.0598086 0.1290008 0.91 0.09 0.0660359 51505.98 1529.7432 438.1608 2005-06 0.3128944 0.0416023 0.23228 0.94 0.06 0.053043 73586.87 2122.1128 659.4875 2006-07 0.4277428 0.0201691 0.0898767 0.93 0.07 0.0250486 91319.29 3212.2939 914.3142

HDFC FINANCE year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 0.3766111 0.056479 0.0072752 0.91 0.09 0.0520507 26296.14 188064.7 329.5208 2003-04 0.9118899 0.0435655 0.6728748 0.91 0.09 0.1002034 32077.83 19342.3 501.585 2004-05 0.5867557 0.0356933 0.1498824 0.9 0.1 0.0471122 40530.5 214596.1 662.8167

year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 -

0.0790866 0.0315835 0.0697467 0.08 0.92 0.0666936 1164.86 211.33057 73.1 2003-04 0.6039599 0.0426463 0.4613404 0.14 0.86 0.4027232 1474.63 271.9536 79.8225 2004-05 0.2471491 0.0406575 0.0927948 0.11 0.89 0.0870597 1744.83 350.86421 104.6858 2005-06 0.1258566 0.0228485 0.126625 0.2 0.8 0.1058697 2454.18 483.9642 153.6733 2006-07 0.5056715 0.0602167 0.0931605 0.04 0.96 0.0918427 3359.83 546.12064 246.0817

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 75

2005-06 0.5514618 0.0356389 0.367315 0.89 0.11 0.0721233 51189.68 270334.8 1018.214 2006-07 0.334217 0.0428188 0.0859614 0.88 0.12 0.0479959 62744.42 376085.5 1408.893

HINDALCO year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 0.4537341 0.038209 0.0292084 0.47 0.53 0.0334387 8586.11 691.13456 241.6152003-04 0.7938111 0.0460524 0.0537608 0.44 0.56 0.0503691 9422.5 948.59409 94.34252004-05 0.391259 0.029819 0.0383361 0.43 0.57 0.0346738 11466.58 1382.8358 305.6116667 2005-06 847.43935 0.0306154 0.0546713 0.27 0.73 0.0481762 14509.7 1553.991 291.6358333 2006-07 0.03179 0.0219311 0.0498104 0.28 0.72 0.0420042 19786.64 2498.1382 172.8783333

HUL year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 0.1166857 0.0261155 0.0277424 0.07 0.93 0.0276285 3843.03 1489.9012 136.05 2003-04 0.0602001 0.0589059 0.378128 0.03 0.97 0.3685513 3563.83 1076.7072 153.35 2004-05 0.4965496 0.2248093 0.3879276 0.02 0.98 0.3846652 2362.56 1095.3414 134.7933 2005-06 0.0196613 0.0985357 0.205018 0.41 0.59 0.1613603 2796.09 1465.5666 176.8075 2006-07 0.3986352 0.1920349 0.297464 0.44 0.56 0.2510752 1427.77 1568.9451 231.5117

INFOSYS year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 0.4021504 0 0.1838984 0 1 0.1838984 2,860.65 773.15866 482.95082003-04 0.3240143 0 0.51752 0 1 0.51752 3,253.43 980.86237 531.0252004-05 0.5702256 0 0.4329936 0 1 0.4329936 5,242.00 1486.741 863.88752005-06 0.0863103 0 0.254079 0 1 0.254079 6,897.00 1824.7579 1258.33

2006-07 -

0.0115387 0 0.03325 0 1 0.03325 11,162.00 2768.8051 1880.815

ITC year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 -0.031024 0.2293954 0.0631563 0.02 0.98 0.0664811 5482.6 1397.6965 43.1391 2003-04 0.1338316 0.1885627 0.1385444 0.01 0.99 0.1390446 6530.91 1568.9051 57.3225 2004-05 0.8607638 0.1380354 0.196024 0.03 0.97 0.1942843 8140.97 2052.2359 75.275 2005-06 0.6300881 0.1174924 0.41195 0.02 0.98 0.4060608 9181.21 2163.6215 128.1108 2006-07 0.14834 0.0532351 0.0781308 0.02 0.98 0.0776329 10637.96 2628.6248 178.2592

L & T year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 0.1991978 0.0541673 0.0315773 0.26 0.74 0.0374507 6738.54 511.85226 92.2483 2003-04 0.3795847 0.063355 0.3074972 0.24 0.76 0.2489031 4099.39 596.01647 181.6175 2004-05 1.2017352 0.0433287 0.2534484 0.36 0.64 0.1778053 5228.19 937.90689 402.6267

RELATIONSHIP BETWEEN EVA & SHARE PRICE

M. P. Birla Institute of Management 76

2005-06 0.0603446 0.0790599 0.0899 0.32 0.68 0.0864312 6093.74 1036.7318 764.5017 2006-07 0.1887499 0.0441718 0.0798148 0.47 0.53 0.0630626 7846.18 1427.8514 1326.798

M & M year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 0.5111344 0.0677901 -

0.0112603 0.32 0.68 0.0140358 2709.68 208.9079 49.90252003-04 0.3403584 0.0702775 0.280712 0.23 0.77 0.2323121 2504.84 343.4305 136.35422004-05 0.4909302 0.0191532 0.133716 0.35 0.65 0.093619 3039.15 486.2981 237.84832005-06 0.2891674 0.0203471 0.219285 0.29 0.71 0.161593 3792.25 751.0109 397.592006-07 0.4748729 0.0080689 0.0918554 0.42 0.58 0.0566651 5188.91 958.9079 719.2775

MARUTI year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 0.13487 0.0770506 -

0.0034342 0.08 0.92 0.0030046 3554 223.21116 266.47

2003-04 -0.99352 0.0927694 -

0.6347924 0.01 0.99 -

0.6275168 3903.1 542.16044 328.91782004-05 0.8747752 0.0780273 0.1983816 0.07 0.93 0.1899568 4686.4 893.97803 427.80582005-06 0.1257093 0.1896887 0.126625 0.08 0.92 0.1316701 5524.3 1180.3257 575.45422006-07 0.3841321 0.0397399 0.0880664 0.13 0.87 0.081784 7484.7 1545.0106 870.47

ONGC year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 -0.082004 0.0943109 0.0701586 0.2 0.8 0.0749891 36539.19 21.00105 236.0683 2003-04 0.3352983 0.0026919 0.277278 0.2 0.8 0.2223608 51950.89 14.407387 399.19 2004-05 0.6944469 0.0025112 0.1680696 0.27 0.83 0.1401758 56761.64 1254.2494 516.6467 2005-06 0.3068171 0.0024608 0.22889 0.22 0.78 0.1790756 66682.28 1701.8184 684.5133 2006-07 0.2773362 0.0017421 0.0835617 0.01 0.99 0.0827435 77033 3255.7894 819.08

RANBAXY year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 -

0.2333128 2.0087961 0.0908909 0.58 0.42 1.2032759 1880.33 282.6992 236.0683 2003-04 0.5873083 0.1572369 0.4503516 0.3 0.7 0.3624172 2354.04 448.8008 399.19 2004-05 0.6515054 0.0538817 0.1608284 0.01 0.99 0.1597589 2642.54 514.7158 516.6467 2005-06 0.5748039 0.017098 0.38031 0.01 0.99 0.3766779 3406.82 452.6917 684.5133 2006-07 0.2896844 0.0122576 0.0840669 0.01 0.99 0.0833488 5527.73 400.2217 819.08

RELIANCE INDUSTRIES year beta kd Ke wd we wacc Capital NOPAT Share price

2002-03 0.562 0.0524754 -

0.0182626 0.3 0.7 0.0029588 50132.72 4353.131 222.16172003-04 0.482 0.0456693 0.3782376 0.3 0.7 0.2784671 55397.11 5157.4979 348.5825 2004-05 0.912 0.0521255 0.2047808 0.32 0.68 0.1559311 59187.91 7025.2446 421.955 2005-06 0.144 0.0267417 0.13736 0.38 0.62 0.095325 71699.87 7721.1194 605.1217

RELATIONSHIP BETWEEN EVA & SHARE PRICE