Embed Size (px)

Citation preview

Estate & Asset Estate & Asset Protection Protection PlanningPlanning

Arthur J. Pauly, Jr. Arthur J. Pauly, Jr.

Attorney At LawAttorney At Law

Asset Protection PlanningAsset Protection PlanningAsset Protection PlanningAsset Protection Planning

Protect Your FamilyProtect Your Familyfrom Taxes, Lawsuits from Taxes, Lawsuits and Probateand Probate

Gain Safety & SecurityGain Safety & Security

Have Peace of MindHave Peace of Mind

Protect Your FamilyProtect Your Familyfrom Taxes, Lawsuits from Taxes, Lawsuits and Probateand Probate

Gain Safety & SecurityGain Safety & Security

Have Peace of MindHave Peace of Mind

Givers and TakersGivers and TakersGivers and TakersGivers and Takers

Givers Control the Transfers of Their Own Givers Control the Transfers of Their Own PropertyProperty

Takers are Creditors and PredatorsTakers are Creditors and Predators

Givers Control the Transfers of Their Own Givers Control the Transfers of Their Own PropertyProperty

Takers are Creditors and PredatorsTakers are Creditors and Predators

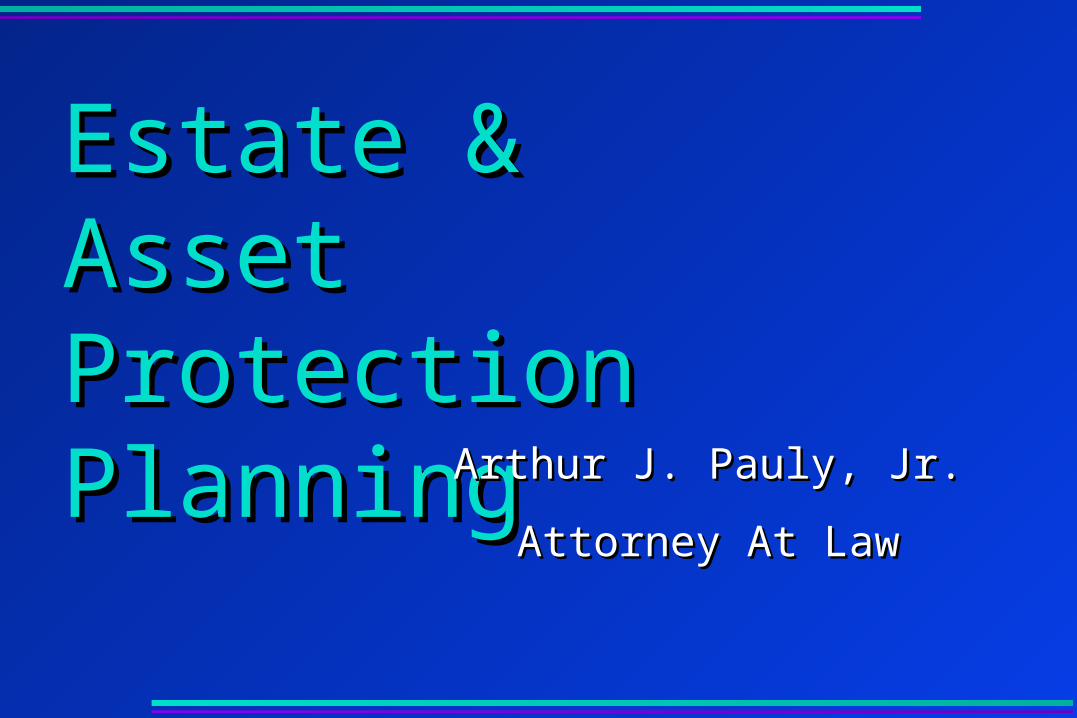

Definition of Asset ProtectionDefinition of Asset ProtectionDefinition of Asset ProtectionDefinition of Asset Protection

Control My Property for My BenefitControl My Property for My Benefit Give What I Want, To Whom I WantGive What I Want, To Whom I Want Give It How, When, and the Way I WantGive It How, When, and the Way I Want Save Every Possible Dollar from Taxes, Save Every Possible Dollar from Taxes,

Probate, Attorney Fees, Court Costs, and Probate, Attorney Fees, Court Costs, and Creditor ClaimsCreditor Claims

Control My Property for My BenefitControl My Property for My Benefit Give What I Want, To Whom I WantGive What I Want, To Whom I Want Give It How, When, and the Way I WantGive It How, When, and the Way I Want Save Every Possible Dollar from Taxes, Save Every Possible Dollar from Taxes,

Probate, Attorney Fees, Court Costs, and Probate, Attorney Fees, Court Costs, and Creditor ClaimsCreditor Claims

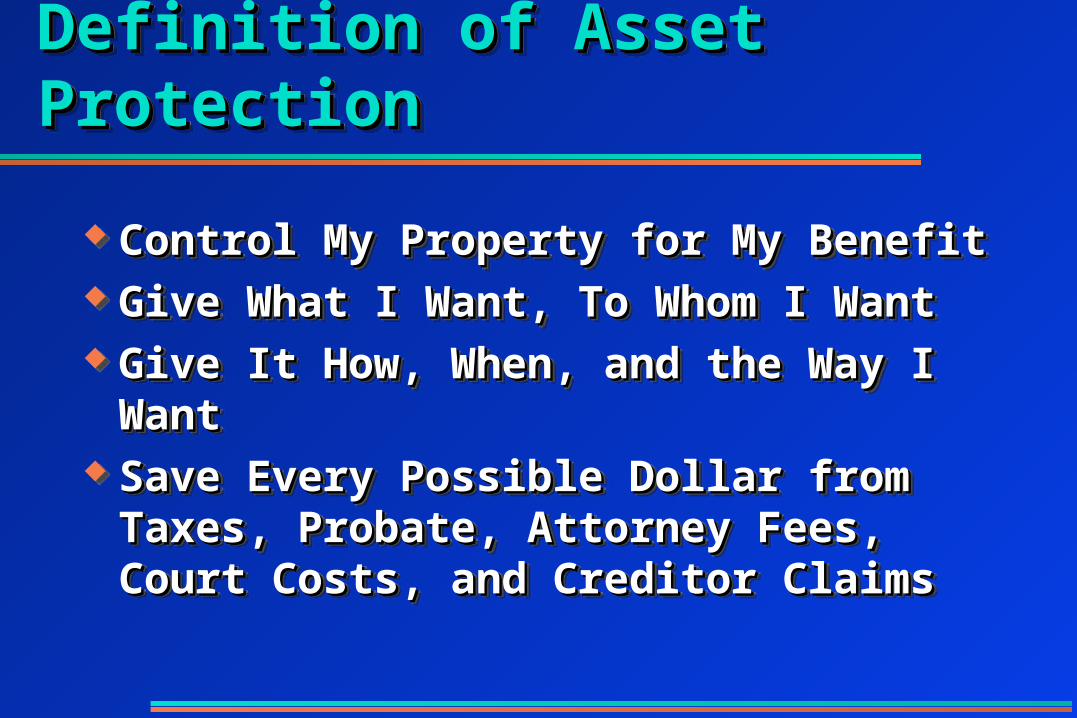

Reasons to Protect AssetsReasons to Protect AssetsReasons to Protect AssetsReasons to Protect Assets

We Focus on Estate We Focus on Estate Building, But Fail to Building, But Fail to Consider RisksConsider Risks

““Sue Society”: Who Can Sue Society”: Who Can I Blame?I Blame?

Juries Play “Robin Juries Play “Robin Hood”; Take from the Hood”; Take from the Rich, Give to the PoorRich, Give to the Poor

We Focus on Estate We Focus on Estate Building, But Fail to Building, But Fail to Consider RisksConsider Risks

““Sue Society”: Who Can Sue Society”: Who Can I Blame?I Blame?

Juries Play “Robin Juries Play “Robin Hood”; Take from the Hood”; Take from the Rich, Give to the PoorRich, Give to the Poor

Cut Your Losses Cut Your Losses (Damage Control)(Damage Control)

Peace of MindPeace of Mind Concentrate on Your Concentrate on Your

JobJob Protect Your Family and Protect Your Family and

Your BusinessYour Business

Cut Your Losses Cut Your Losses (Damage Control)(Damage Control)

Peace of MindPeace of Mind Concentrate on Your Concentrate on Your

JobJob Protect Your Family and Protect Your Family and

Your BusinessYour Business

More Lawsuits Are Filed Each Year*More Lawsuits Are Filed Each Year**Over 20 Million Civil Cases Expected in 1994!*Over 20 Million Civil Cases Expected in 1994!

More Lawsuits Are Filed Each Year*More Lawsuits Are Filed Each Year**Over 20 Million Civil Cases Expected in 1994!*Over 20 Million Civil Cases Expected in 1994!

The Four Liability DragonsThe Four Liability DragonsThe Four Liability DragonsThe Four Liability Dragons

Creditor ClaimsCreditor Claims Income and Estate Income and Estate

TaxesTaxes Living ProbateLiving Probate Death ProbateDeath Probate

Creditor ClaimsCreditor Claims Income and Estate Income and Estate

TaxesTaxes Living ProbateLiving Probate Death ProbateDeath Probate

Title to AssetsTitle to AssetsTitle to AssetsTitle to Assets

The Way You Hold Title to Your Property Affects The Way You Hold Title to Your Property Affects the Rights a Creditor Will Have!the Rights a Creditor Will Have!

The Way You Hold Title to Your Property Affects The Way You Hold Title to Your Property Affects the Rights a Creditor Will Have!the Rights a Creditor Will Have!

Community PropertyCommunity PropertyCommunity PropertyCommunity Property

Community PropertyCommunity Property• Acquired During MarriageAcquired During Marriage• Created by Law or by AgreementCreated by Law or by Agreement

• Result of an “Onerous Acquisition” or Result of an “Onerous Acquisition” or WORK !WORK !

Community PropertyCommunity Property• Acquired During MarriageAcquired During Marriage• Created by Law or by AgreementCreated by Law or by Agreement

• Result of an “Onerous Acquisition” or Result of an “Onerous Acquisition” or WORK !WORK !

Separate PropertySeparate PropertySeparate PropertySeparate Property

Separate PropertySeparate Property• Acquired Before MarriageAcquired Before Marriage• Acquired By Gift or InheritanceAcquired By Gift or Inheritance• Can Convert to Community By Agreement or Can Convert to Community By Agreement or

MistakeMistake• Personal Injury RecoveryPersonal Injury Recovery

Separate PropertySeparate Property• Acquired Before MarriageAcquired Before Marriage• Acquired By Gift or InheritanceAcquired By Gift or Inheritance• Can Convert to Community By Agreement or Can Convert to Community By Agreement or

MistakeMistake• Personal Injury RecoveryPersonal Injury Recovery

Joint TenancyJoint TenancyJoint TenancyJoint Tenancy

100% Co-ownership by More Than One Person 100% Co-ownership by More Than One Person 100% Co-ownership by More Than One Person 100% Co-ownership by More Than One Person

““Last One Left Standing Rule”: Last One Left Standing Rule”: Survivor Owns It All!Survivor Owns It All!

Your DefensesYour DefensesYour DefensesYour Defenses

InsuranceInsurance Exempt AssetsExempt Assets

• State and Federal LawState and Federal Law

• Retirement PlansRetirement Plans TrustsTrusts Property AgreementsProperty Agreements

InsuranceInsurance Exempt AssetsExempt Assets

• State and Federal LawState and Federal Law

• Retirement PlansRetirement Plans TrustsTrusts Property AgreementsProperty Agreements

Limited Liability Limited Liability CompaniesCompanies

CorporationsCorporations Family Limited Family Limited

PartnershipsPartnerships Offshore PlanningOffshore Planning

Limited Liability Limited Liability CompaniesCompanies

CorporationsCorporations Family Limited Family Limited

PartnershipsPartnerships Offshore PlanningOffshore Planning

The First DragonThe First DragonThe First DragonThe First Dragon

Creditor ClaimsCreditor Claims Creditor ClaimsCreditor Claims

Types of ClaimsTypes of ClaimsTypes of ClaimsTypes of Claims

Officer/Director Officer/Director Liability (Corp.)Liability (Corp.)

Employee SuitsEmployee Suits Business or Professional Business or Professional

LiabilityLiability DivorceDivorce Tax LiabilityTax Liability Creditor LawsuitsCreditor Lawsuits

Officer/Director Officer/Director Liability (Corp.)Liability (Corp.)

Employee SuitsEmployee Suits Business or Professional Business or Professional

LiabilityLiability DivorceDivorce Tax LiabilityTax Liability Creditor LawsuitsCreditor Lawsuits

Vicarious Liability for Vicarious Liability for Other PeopleOther People

Partnership LiabilityPartnership Liability Unknown ClaimsUnknown Claims

• Product LiabilityProduct Liability

• Environmental LiabilityEnvironmental Liability

Vicarious Liability for Vicarious Liability for Other PeopleOther People

Partnership LiabilityPartnership Liability Unknown ClaimsUnknown Claims

• Product LiabilityProduct Liability

• Environmental LiabilityEnvironmental Liability

Results of Creditor ClaimsResults of Creditor ClaimsResults of Creditor ClaimsResults of Creditor Claims

STRESS !STRESS ! Loss of PrivacyLoss of Privacy Delays and HassleDelays and Hassle Attorney FeesAttorney Fees Accounting FeesAccounting Fees Court CostsCourt Costs

STRESS !STRESS ! Loss of PrivacyLoss of Privacy Delays and HassleDelays and Hassle Attorney FeesAttorney Fees Accounting FeesAccounting Fees Court CostsCourt Costs

Attempts to Avoid Creditor ClaimsAttempts to Avoid Creditor ClaimsAttempts to Avoid Creditor ClaimsAttempts to Avoid Creditor Claims

Gimmicks are Methods ThatGimmicks are Methods That

Don’t WorkDon’t Work• Fraudulent TransfersFraudulent Transfers• ““Hiding” AssetsHiding” Assets• Joint OwnershipJoint Ownership• ““Constitutional” TrustsConstitutional” Trusts

Gimmicks are Methods ThatGimmicks are Methods That

Don’t WorkDon’t Work• Fraudulent TransfersFraudulent Transfers• ““Hiding” AssetsHiding” Assets• Joint OwnershipJoint Ownership• ““Constitutional” TrustsConstitutional” Trusts

Creditor RightsCreditor RightsCreditor RightsCreditor Rights

Can Set Aside Fraudulent TransfersCan Set Aside Fraudulent Transfers All Community Property is Exposed to All Community Property is Exposed to

Community CreditorsCommunity Creditors Separate Property is Exposed to Separate Separate Property is Exposed to Separate

Creditor, 1/2 Community Property May Be Creditor, 1/2 Community Property May Be Exposed to Exposed to Separate CreditorSeparate Creditor

Can Set Aside Fraudulent TransfersCan Set Aside Fraudulent Transfers All Community Property is Exposed to All Community Property is Exposed to

Community CreditorsCommunity Creditors Separate Property is Exposed to Separate Separate Property is Exposed to Separate

Creditor, 1/2 Community Property May Be Creditor, 1/2 Community Property May Be Exposed to Exposed to Separate CreditorSeparate Creditor

Creditor Rights (cont.)Creditor Rights (cont.)Creditor Rights (cont.)Creditor Rights (cont.)

Divorce Court May Have Jurisdiction Over Divorce Court May Have Jurisdiction Over Both Community and Separate PropertyBoth Community and Separate Property

All Joint Tenancy Property is at Risk of Any All Joint Tenancy Property is at Risk of Any Single Joint Tenant’s Creditors!Single Joint Tenant’s Creditors!

Divorce Court May Have Jurisdiction Over Divorce Court May Have Jurisdiction Over Both Community and Separate PropertyBoth Community and Separate Property

All Joint Tenancy Property is at Risk of Any All Joint Tenancy Property is at Risk of Any Single Joint Tenant’s Creditors!Single Joint Tenant’s Creditors!

Fraudulent TransfersFraudulent TransfersFraudulent TransfersFraudulent Transfers

Intent to Defraud, Hinder or Delay Known or Intent to Defraud, Hinder or Delay Known or Likely CreditorsLikely Creditors

Intent is Generally PresumedIntent is Generally Presumed Badges of FraudBadges of Fraud

• Transfer of Non-Exempt AssetsTransfer of Non-Exempt Assets• Less than Full & Fair ConsiderationLess than Full & Fair Consideration• Few Assets Remain to Satisfy ClaimFew Assets Remain to Satisfy Claim

Court Can Set Aside!Court Can Set Aside!

Intent to Defraud, Hinder or Delay Known or Intent to Defraud, Hinder or Delay Known or Likely CreditorsLikely Creditors

Intent is Generally PresumedIntent is Generally Presumed Badges of FraudBadges of Fraud

• Transfer of Non-Exempt AssetsTransfer of Non-Exempt Assets• Less than Full & Fair ConsiderationLess than Full & Fair Consideration• Few Assets Remain to Satisfy ClaimFew Assets Remain to Satisfy Claim

Court Can Set Aside!Court Can Set Aside!

The Second DragonThe Second DragonThe Second DragonThe Second Dragon

TaxesTaxes TaxesTaxes

Income TaxesIncome TaxesIncome TaxesIncome Taxes

Rates are High and Climbing HigherRates are High and Climbing Higher

““Inflation Tax”Inflation Tax”

Fewer DeductionsFewer Deductions• No “Fun” Write-OffsNo “Fun” Write-Offs

Hard to Pass Income to Other Family MembersHard to Pass Income to Other Family Members• No Clifford TrustsNo Clifford Trusts

Rates are High and Climbing HigherRates are High and Climbing Higher

““Inflation Tax”Inflation Tax”

Fewer DeductionsFewer Deductions• No “Fun” Write-OffsNo “Fun” Write-Offs

Hard to Pass Income to Other Family MembersHard to Pass Income to Other Family Members• No Clifford TrustsNo Clifford Trusts

Death TaxesDeath TaxesDeath TaxesDeath Taxes

State Inheritance TaxState Inheritance Tax

Federal Estate TaxFederal Estate Tax

State Inheritance TaxState Inheritance Tax

Federal Estate TaxFederal Estate Tax

Inheritance TaxInheritance TaxInheritance TaxInheritance Tax

Is State “Death” TaxIs State “Death” Tax

Some States Have “Pick-Up” TaxSome States Have “Pick-Up” Tax

Is State “Death” TaxIs State “Death” Tax

Some States Have “Pick-Up” TaxSome States Have “Pick-Up” Tax

Federal Estate TaxFederal Estate TaxFederal Estate TaxFederal Estate Tax

Lifetime Exemption of $600,000 per Person for Lifetime Exemption of $600,000 per Person for Taxable Gifts or InheritanceTaxable Gifts or Inheritance• Includes Includes ALLALL Your Assets Your Assets• Includes Pensions, Retirement, InsuranceIncludes Pensions, Retirement, Insurance

Unlimited Marital DeductionUnlimited Marital Deduction• Only Delays the TaxOnly Delays the Tax

Most Couples Fail to Properly PlanMost Couples Fail to Properly Plan Tax Rates are 37% - 55%Tax Rates are 37% - 55%

Lifetime Exemption of $600,000 per Person for Lifetime Exemption of $600,000 per Person for Taxable Gifts or InheritanceTaxable Gifts or Inheritance• Includes Includes ALLALL Your Assets Your Assets• Includes Pensions, Retirement, InsuranceIncludes Pensions, Retirement, Insurance

Unlimited Marital DeductionUnlimited Marital Deduction• Only Delays the TaxOnly Delays the Tax

Most Couples Fail to Properly PlanMost Couples Fail to Properly Plan Tax Rates are 37% - 55%Tax Rates are 37% - 55%

Federal Estate Tax (Cont.)Federal Estate Tax (Cont.)Federal Estate Tax (Cont.)Federal Estate Tax (Cont.)

Due Due IN CASH IN CASH 9 Months From the Date of 9 Months From the Date of DeathDeath• Trust Planning Preserves Two ExemptionsTrust Planning Preserves Two Exemptions• Special Requirements for Non-CitizensSpecial Requirements for Non-Citizens

90% of Family Businesses Die with 90% of Family Businesses Die with the Founderthe Founder

Each Generation Gets Taxed Each Generation Gets Taxed AGAIN!AGAIN!

Due Due IN CASH IN CASH 9 Months From the Date of 9 Months From the Date of DeathDeath• Trust Planning Preserves Two ExemptionsTrust Planning Preserves Two Exemptions• Special Requirements for Non-CitizensSpecial Requirements for Non-Citizens

90% of Family Businesses Die with 90% of Family Businesses Die with the Founderthe Founder

Each Generation Gets Taxed Each Generation Gets Taxed AGAIN!AGAIN!

The Third DragonThe Third DragonThe Third DragonThe Third Dragon

Living ProbateLiving Probate Living ProbateLiving Probate

DefinitionDefinitionDefinitionDefinition

Court Proceeding to Protect an Allegedly Court Proceeding to Protect an Allegedly Incompetent PersonIncompetent Person• Public ProceedingPublic Proceeding• HumiliatingHumiliating• Inter-Family Strife and DissensionInter-Family Strife and Dissension• Costly: Attorneys’ and Experts’ FeesCostly: Attorneys’ and Experts’ Fees

Court Proceeding to Protect an Allegedly Court Proceeding to Protect an Allegedly Incompetent PersonIncompetent Person• Public ProceedingPublic Proceeding• HumiliatingHumiliating• Inter-Family Strife and DissensionInter-Family Strife and Dissension• Costly: Attorneys’ and Experts’ FeesCostly: Attorneys’ and Experts’ Fees

Durable Powers of AttorneyDurable Powers of AttorneyDurable Powers of AttorneyDurable Powers of Attorney

InexpensiveInexpensive

BUTBUT Generally Give Absolute Power Generally Give Absolute Power• Blank Checkbook for Blank Checkbook for ALLALL Property Property• Few Instructions, If AnyFew Instructions, If Any• Financial Institutions May RefuseFinancial Institutions May Refuse

Easy to AbuseEasy to Abuse

InexpensiveInexpensive

BUTBUT Generally Give Absolute Power Generally Give Absolute Power• Blank Checkbook for Blank Checkbook for ALLALL Property Property• Few Instructions, If AnyFew Instructions, If Any• Financial Institutions May RefuseFinancial Institutions May Refuse

Easy to AbuseEasy to Abuse

The Fourth DragonThe Fourth DragonThe Fourth DragonThe Fourth Dragon

Death ProbateDeath Probate Death ProbateDeath Probate

Death ProbateDeath ProbateDeath ProbateDeath Probate

Court Proceeding Where Your Will Does Its JobCourt Proceeding Where Your Will Does Its Job• May Cost 1-3% of Gross Estate or More!May Cost 1-3% of Gross Estate or More!• May Take 4 to More Than 24 monthsMay Take 4 to More Than 24 months

A Lawsuit Against Yourself, Using Your Money, A Lawsuit Against Yourself, Using Your Money, for Benefit of Your Creditors!for Benefit of Your Creditors!

Public Forum; Challenges CommonPublic Forum; Challenges Common

Court Proceeding Where Your Will Does Its JobCourt Proceeding Where Your Will Does Its Job• May Cost 1-3% of Gross Estate or More!May Cost 1-3% of Gross Estate or More!• May Take 4 to More Than 24 monthsMay Take 4 to More Than 24 months

A Lawsuit Against Yourself, Using Your Money, A Lawsuit Against Yourself, Using Your Money, for Benefit of Your Creditors!for Benefit of Your Creditors!

Public Forum; Challenges CommonPublic Forum; Challenges Common

Death Probate (cont.)Death Probate (cont.)Death Probate (cont.)Death Probate (cont.)

Attorney FeesAttorney Fees

• Statutory FeesStatutory Fees

• Reasonable FeesReasonable Fees

Creditor ClaimsCreditor Claims• KnownKnown• UnknownUnknown

Attorney FeesAttorney Fees

• Statutory FeesStatutory Fees

• Reasonable FeesReasonable Fees

Creditor ClaimsCreditor Claims• KnownKnown• UnknownUnknown

Asset Protection TechniquesAsset Protection TechniquesAsset Protection TechniquesAsset Protection Techniques

Methods That WorkMethods That Work• Save Administrative Fees and CostsSave Administrative Fees and Costs• Reduce TaxesReduce Taxes• Provide Multiple Layers of DefenseProvide Multiple Layers of Defense• Allow Opportunity for Early SettlementAllow Opportunity for Early Settlement

Methods That WorkMethods That Work• Save Administrative Fees and CostsSave Administrative Fees and Costs• Reduce TaxesReduce Taxes• Provide Multiple Layers of DefenseProvide Multiple Layers of Defense• Allow Opportunity for Early SettlementAllow Opportunity for Early Settlement

First Line of DefenseFirst Line of DefenseFirst Line of DefenseFirst Line of Defense

InsuranceInsurance InsuranceInsurance

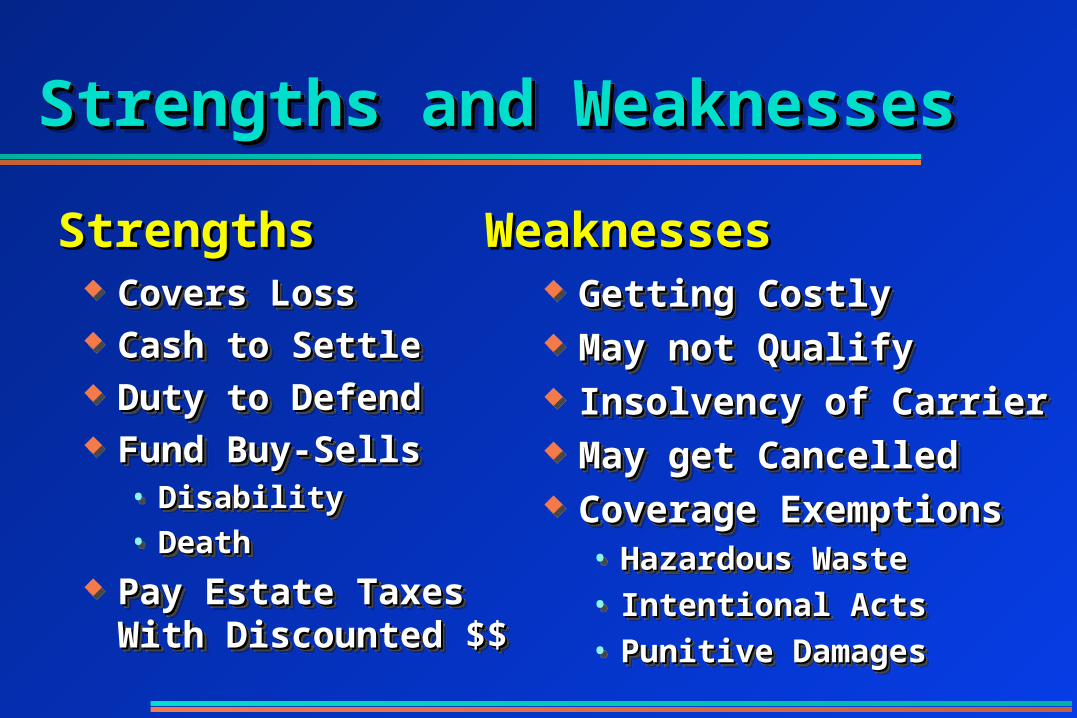

Strengths and WeaknessesStrengths and WeaknessesStrengths and WeaknessesStrengths and Weaknesses

Covers LossCovers Loss Cash to SettleCash to Settle Duty to DefendDuty to Defend Fund Buy-SellsFund Buy-Sells

• DisabilityDisability

• DeathDeath Pay Estate Taxes With Pay Estate Taxes With

Discounted $$Discounted $$

Covers LossCovers Loss Cash to SettleCash to Settle Duty to DefendDuty to Defend Fund Buy-SellsFund Buy-Sells

• DisabilityDisability

• DeathDeath Pay Estate Taxes With Pay Estate Taxes With

Discounted $$Discounted $$

Getting CostlyGetting Costly May not QualifyMay not Qualify Insolvency of CarrierInsolvency of Carrier May get CancelledMay get Cancelled Coverage ExemptionsCoverage Exemptions

• Hazardous WasteHazardous Waste

• Intentional ActsIntentional Acts

• Punitive DamagesPunitive Damages

Getting CostlyGetting Costly May not QualifyMay not Qualify Insolvency of CarrierInsolvency of Carrier May get CancelledMay get Cancelled Coverage ExemptionsCoverage Exemptions

• Hazardous WasteHazardous Waste

• Intentional ActsIntentional Acts

• Punitive DamagesPunitive Damages

StrengthsStrengths WeaknessesWeaknesses

Second Line of DefenseSecond Line of DefenseSecond Line of DefenseSecond Line of Defense

Exempt Exempt PropertyProperty

Exempt Exempt PropertyProperty

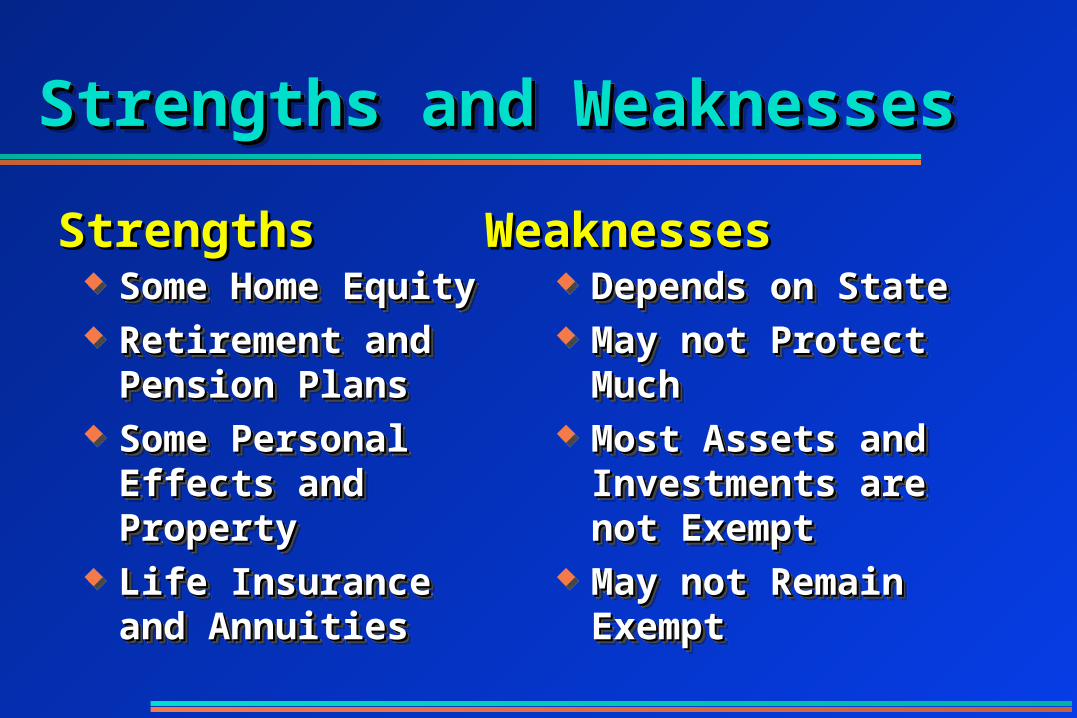

Strengths and WeaknessesStrengths and WeaknessesStrengths and WeaknessesStrengths and Weaknesses

Some Home EquitySome Home Equity Retirement and Pension Retirement and Pension

PlansPlans Some Personal Effects Some Personal Effects

and Propertyand Property Life Insurance and Life Insurance and

AnnuitiesAnnuities

Some Home EquitySome Home Equity Retirement and Pension Retirement and Pension

PlansPlans Some Personal Effects Some Personal Effects

and Propertyand Property Life Insurance and Life Insurance and

AnnuitiesAnnuities

Depends on StateDepends on State May not Protect MuchMay not Protect Much Most Assets and Most Assets and

Investments are not Investments are not ExemptExempt

May not Remain ExemptMay not Remain Exempt

Depends on StateDepends on State May not Protect MuchMay not Protect Much Most Assets and Most Assets and

Investments are not Investments are not ExemptExempt

May not Remain ExemptMay not Remain Exempt

StrengthsStrengths WeaknessesWeaknesses

Third Line of DefenseThird Line of DefenseThird Line of DefenseThird Line of Defense

Property Property AgreementsAgreements

Property Property AgreementsAgreements

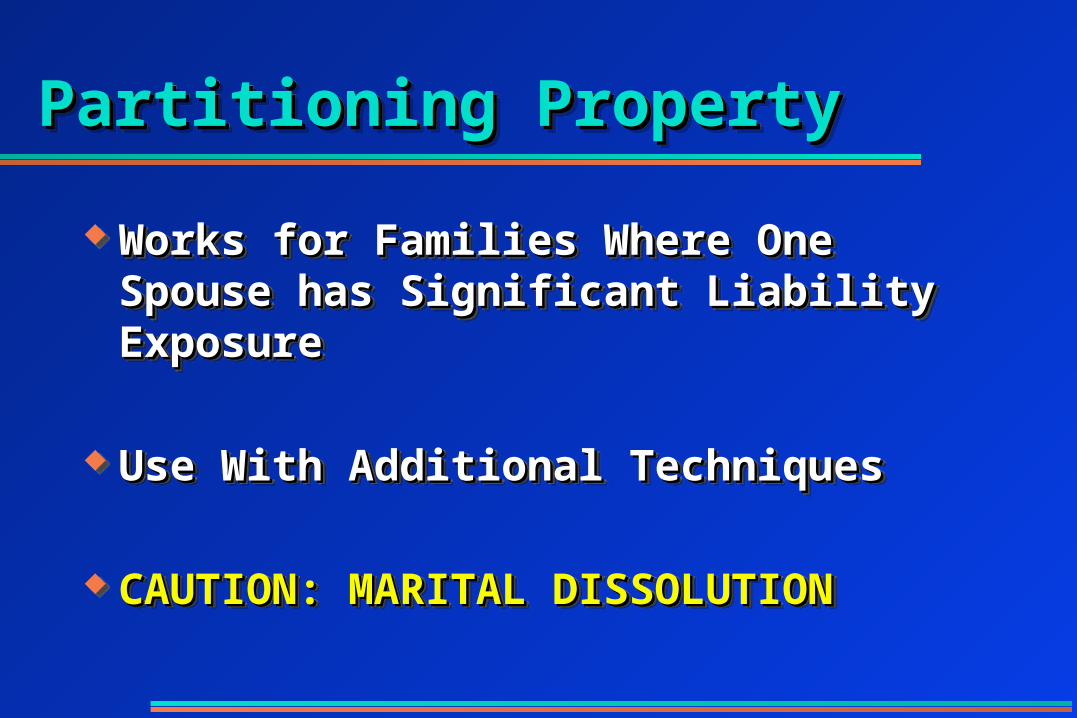

Partitioning PropertyPartitioning PropertyPartitioning PropertyPartitioning Property

Works for Families Where One Spouse has Works for Families Where One Spouse has Significant Liability ExposureSignificant Liability Exposure

Use With Additional TechniquesUse With Additional Techniques

CAUTION: MARITAL DISSOLUTIONCAUTION: MARITAL DISSOLUTION

Works for Families Where One Spouse has Works for Families Where One Spouse has Significant Liability ExposureSignificant Liability Exposure

Use With Additional TechniquesUse With Additional Techniques

CAUTION: MARITAL DISSOLUTIONCAUTION: MARITAL DISSOLUTION

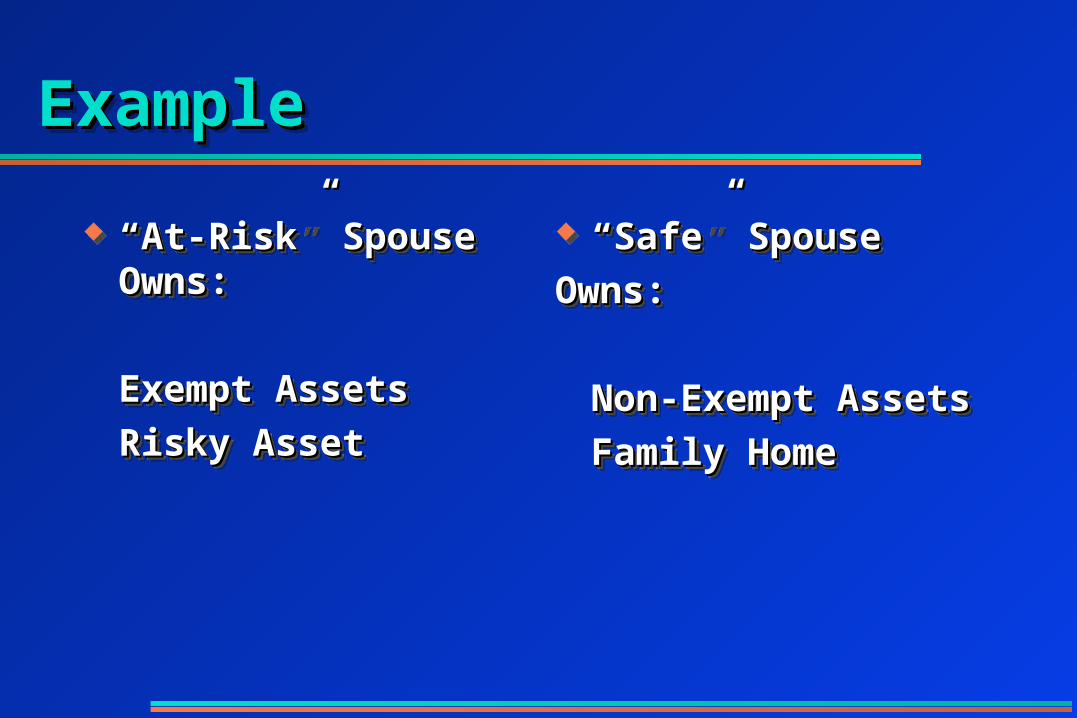

ExampleExampleExampleExample

““At-Risk” Spouse Owns:At-Risk” Spouse Owns:

Exempt AssetsExempt Assets

Risky AssetRisky Asset

““At-Risk” Spouse Owns:At-Risk” Spouse Owns:

Exempt AssetsExempt Assets

Risky AssetRisky Asset

““Safe” SpouseSafe” Spouse

Owns:Owns:

Non-Exempt AssetsNon-Exempt Assets

Family HomeFamily Home

““Safe” SpouseSafe” Spouse

Owns:Owns:

Non-Exempt AssetsNon-Exempt Assets

Family HomeFamily Home

First FortificationFirst FortificationFirst FortificationFirst Fortification

Revocable Revocable Living Trust Living Trust (RLT)(RLT)

Revocable Revocable Living Trust Living Trust (RLT)(RLT)

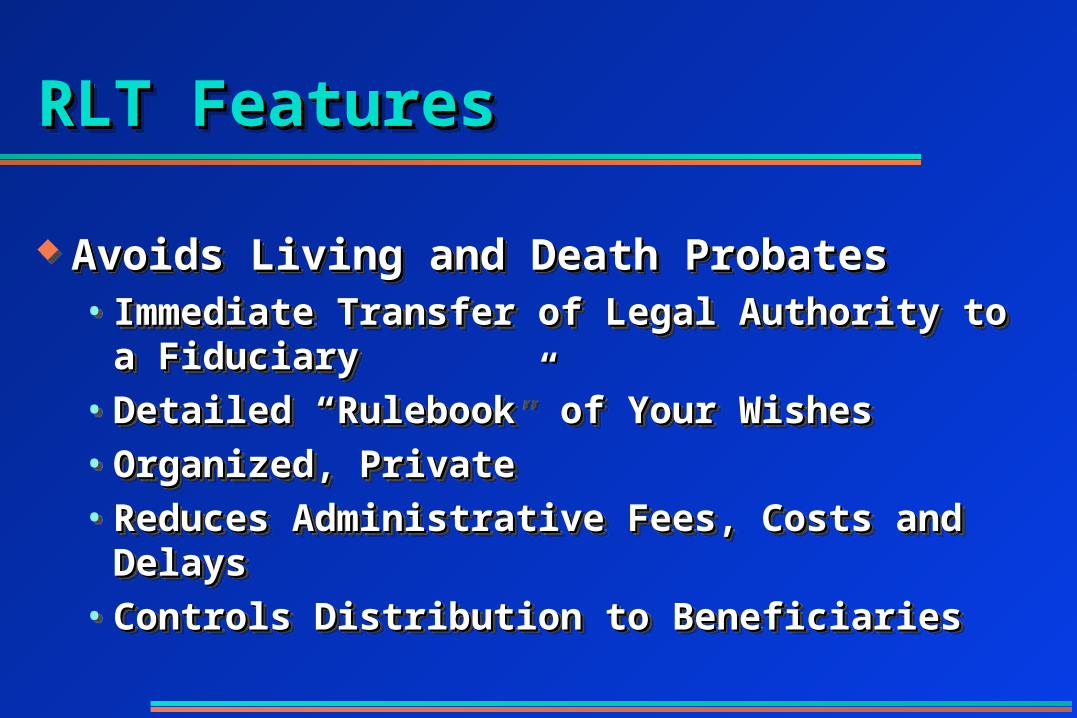

RLT FeaturesRLT FeaturesRLT FeaturesRLT Features

Avoids Living and Death ProbatesAvoids Living and Death Probates• Immediate Transfer of Legal Authority to a FiduciaryImmediate Transfer of Legal Authority to a Fiduciary• Detailed “Rulebook” of Your WishesDetailed “Rulebook” of Your Wishes• Organized, PrivateOrganized, Private• Reduces Administrative Fees, Costs and DelaysReduces Administrative Fees, Costs and Delays• Controls Distribution to BeneficiariesControls Distribution to Beneficiaries

Avoids Living and Death ProbatesAvoids Living and Death Probates• Immediate Transfer of Legal Authority to a FiduciaryImmediate Transfer of Legal Authority to a Fiduciary• Detailed “Rulebook” of Your WishesDetailed “Rulebook” of Your Wishes• Organized, PrivateOrganized, Private• Reduces Administrative Fees, Costs and DelaysReduces Administrative Fees, Costs and Delays• Controls Distribution to BeneficiariesControls Distribution to Beneficiaries

Asset Protection FeaturesAsset Protection FeaturesAsset Protection FeaturesAsset Protection Features

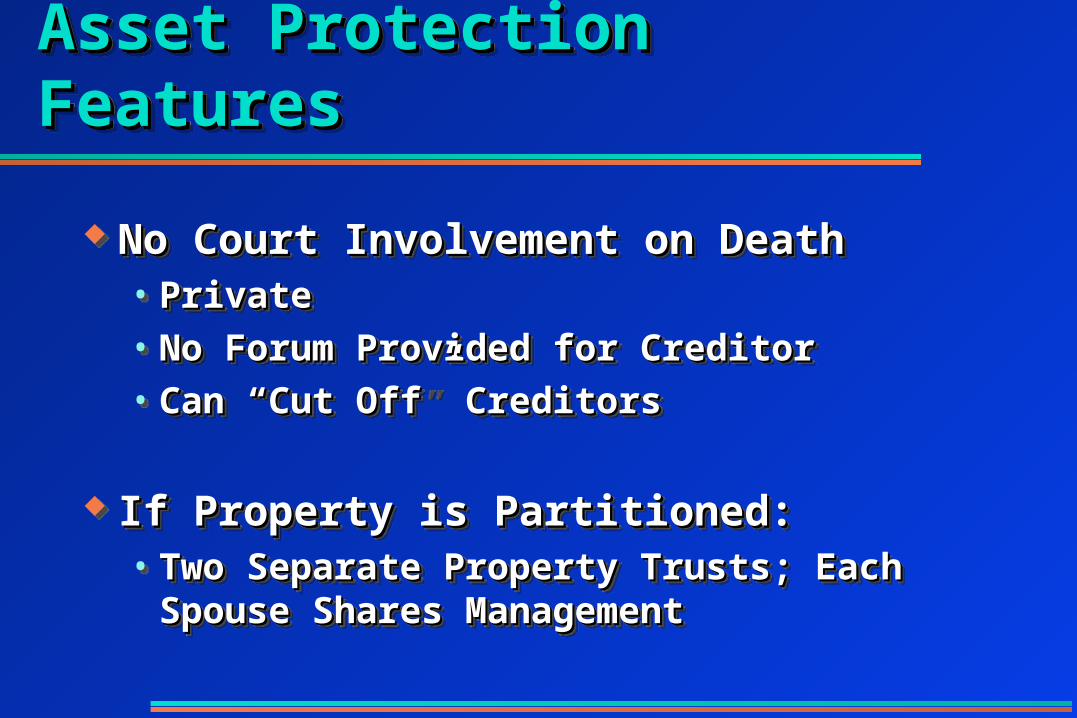

No Court Involvement on DeathNo Court Involvement on Death• PrivatePrivate• No Forum Provided for CreditorNo Forum Provided for Creditor• Can “Cut Off” CreditorsCan “Cut Off” Creditors

If Property is Partitioned:If Property is Partitioned:• Two Separate Property Trusts; Each Spouse Shares Two Separate Property Trusts; Each Spouse Shares

ManagementManagement

No Court Involvement on DeathNo Court Involvement on Death• PrivatePrivate• No Forum Provided for CreditorNo Forum Provided for Creditor• Can “Cut Off” CreditorsCan “Cut Off” Creditors

If Property is Partitioned:If Property is Partitioned:• Two Separate Property Trusts; Each Spouse Shares Two Separate Property Trusts; Each Spouse Shares

ManagementManagement

Asset Protection Features (Cont.)Asset Protection Features (Cont.)Asset Protection Features (Cont.)Asset Protection Features (Cont.)

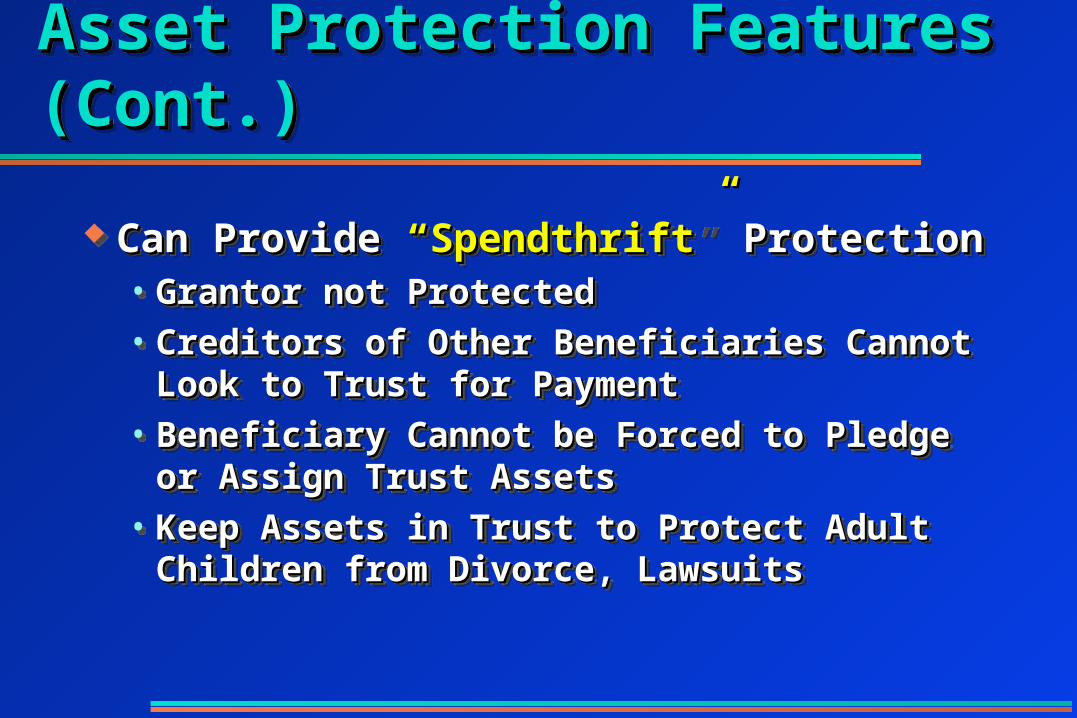

Can Provide Can Provide “Spendthrift” “Spendthrift” ProtectionProtection• Grantor not ProtectedGrantor not Protected• Creditors of Other Beneficiaries Cannot Look to Creditors of Other Beneficiaries Cannot Look to

Trust for PaymentTrust for Payment• Beneficiary Cannot be Forced to Pledge or Assign Beneficiary Cannot be Forced to Pledge or Assign

Trust AssetsTrust Assets• Keep Assets in Trust to Protect Adult Children Keep Assets in Trust to Protect Adult Children

from Divorce, Lawsuitsfrom Divorce, Lawsuits

Can Provide Can Provide “Spendthrift” “Spendthrift” ProtectionProtection• Grantor not ProtectedGrantor not Protected• Creditors of Other Beneficiaries Cannot Look to Creditors of Other Beneficiaries Cannot Look to

Trust for PaymentTrust for Payment• Beneficiary Cannot be Forced to Pledge or Assign Beneficiary Cannot be Forced to Pledge or Assign

Trust AssetsTrust Assets• Keep Assets in Trust to Protect Adult Children Keep Assets in Trust to Protect Adult Children

from Divorce, Lawsuitsfrom Divorce, Lawsuits

Second FortificationSecond FortificationSecond FortificationSecond Fortification

Irrevocable Irrevocable TrustsTrusts

Irrevocable Irrevocable TrustsTrusts

Irrevocable Trust FeaturesIrrevocable Trust FeaturesIrrevocable Trust FeaturesIrrevocable Trust Features

Grantor is Usually not TrusteeGrantor is Usually not Trustee Not Part of Grantor’s Taxable EstateNot Part of Grantor’s Taxable Estate May Own Life InsuranceMay Own Life Insurance

• Income and Federal Estate Tax-Free Income and Federal Estate Tax-Free When ReceivedWhen Received

Spendthrift ProtectionSpendthrift Protection Controlled Distribution to BeneficiariesControlled Distribution to Beneficiaries

Grantor is Usually not TrusteeGrantor is Usually not Trustee Not Part of Grantor’s Taxable EstateNot Part of Grantor’s Taxable Estate May Own Life InsuranceMay Own Life Insurance

• Income and Federal Estate Tax-Free Income and Federal Estate Tax-Free When ReceivedWhen Received

Spendthrift ProtectionSpendthrift Protection Controlled Distribution to BeneficiariesControlled Distribution to Beneficiaries

Special Irrevocable TrustsSpecial Irrevocable TrustsSpecial Irrevocable TrustsSpecial Irrevocable Trusts

Charitable TrustsCharitable Trusts• Grantor Controls, Makes BequestGrantor Controls, Makes Bequest• Income Tax Deduction; Avoid Capital Gains Tax on Income Tax Deduction; Avoid Capital Gains Tax on

Appreciated PropertyAppreciated Property• Increase Retirement IncomeIncrease Retirement Income

Charitable TrustsCharitable Trusts• Grantor Controls, Makes BequestGrantor Controls, Makes Bequest• Income Tax Deduction; Avoid Capital Gains Tax on Income Tax Deduction; Avoid Capital Gains Tax on

Appreciated PropertyAppreciated Property• Increase Retirement IncomeIncrease Retirement Income

Third FortificationThird FortificationThird FortificationThird Fortification

CorporationsCorporations CorporationsCorporations

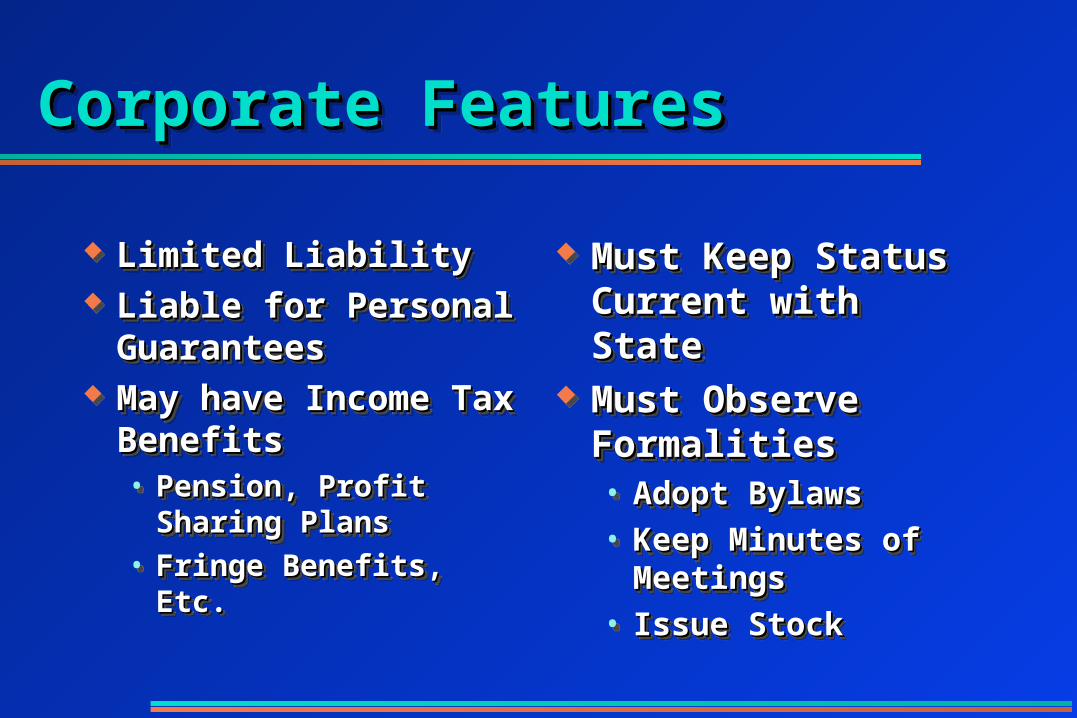

Corporate FeaturesCorporate FeaturesCorporate FeaturesCorporate Features

Limited LiabilityLimited Liability Liable for Personal Liable for Personal

GuaranteesGuarantees May have Income Tax May have Income Tax

BenefitsBenefits• Pension, Profit Sharing Pension, Profit Sharing

PlansPlans

• Fringe Benefits, Etc.Fringe Benefits, Etc.

Limited LiabilityLimited Liability Liable for Personal Liable for Personal

GuaranteesGuarantees May have Income Tax May have Income Tax

BenefitsBenefits• Pension, Profit Sharing Pension, Profit Sharing

PlansPlans

• Fringe Benefits, Etc.Fringe Benefits, Etc.

Must Keep Status Must Keep Status Current with StateCurrent with State

Must Observe Must Observe FormalitiesFormalities• Adopt BylawsAdopt Bylaws

• Keep Minutes of MeetingsKeep Minutes of Meetings

• Issue StockIssue Stock

Must Keep Status Must Keep Status Current with StateCurrent with State

Must Observe Must Observe FormalitiesFormalities• Adopt BylawsAdopt Bylaws

• Keep Minutes of MeetingsKeep Minutes of Meetings

• Issue StockIssue Stock

Fourth FortificationFourth FortificationFourth FortificationFourth Fortification

Family Limited Family Limited PartnershipsPartnerships(FLP)(FLP)

Family Limited Family Limited PartnershipsPartnerships(FLP)(FLP)

FLP FeaturesFLP FeaturesFLP FeaturesFLP Features

File Certificate with StateFile Certificate with State Partners: General and LimitedPartners: General and Limited General Partner has 100% ControlGeneral Partner has 100% Control Income Tax NeutralIncome Tax Neutral Easy to Gift SharesEasy to Gift Shares May Substantially Lower Federal Estate TaxMay Substantially Lower Federal Estate Tax

File Certificate with StateFile Certificate with State Partners: General and LimitedPartners: General and Limited General Partner has 100% ControlGeneral Partner has 100% Control Income Tax NeutralIncome Tax Neutral Easy to Gift SharesEasy to Gift Shares May Substantially Lower Federal Estate TaxMay Substantially Lower Federal Estate Tax

FLP Features (Cont.)FLP Features (Cont.)FLP Features (Cont.)FLP Features (Cont.)

Converts Real Property to Personal PropertyConverts Real Property to Personal Property Can Set Up Multiple FLPs to Protect Different Can Set Up Multiple FLPs to Protect Different

AssetsAssets• Divide and ConquerDivide and Conquer

Charging Order is the Exclusive Remedy for Charging Order is the Exclusive Remedy for Claims Against a PartnerClaims Against a Partner

Converts Real Property to Personal PropertyConverts Real Property to Personal Property Can Set Up Multiple FLPs to Protect Different Can Set Up Multiple FLPs to Protect Different

AssetsAssets• Divide and ConquerDivide and Conquer

Charging Order is the Exclusive Remedy for Charging Order is the Exclusive Remedy for Claims Against a PartnerClaims Against a Partner

Claims vs. PartnershipClaims vs. PartnershipClaims vs. PartnershipClaims vs. Partnership

Take InsuranceTake Insurance Take Partnership AssetsTake Partnership Assets Collect Against General PartnerCollect Against General Partner

Use Entity General PartnerUse Entity General Partner Use Multiple PartnershipsUse Multiple Partnerships

• Divide and ConquerDivide and Conquer

Take InsuranceTake Insurance Take Partnership AssetsTake Partnership Assets Collect Against General PartnerCollect Against General Partner

Use Entity General PartnerUse Entity General Partner Use Multiple PartnershipsUse Multiple Partnerships

• Divide and ConquerDivide and Conquer

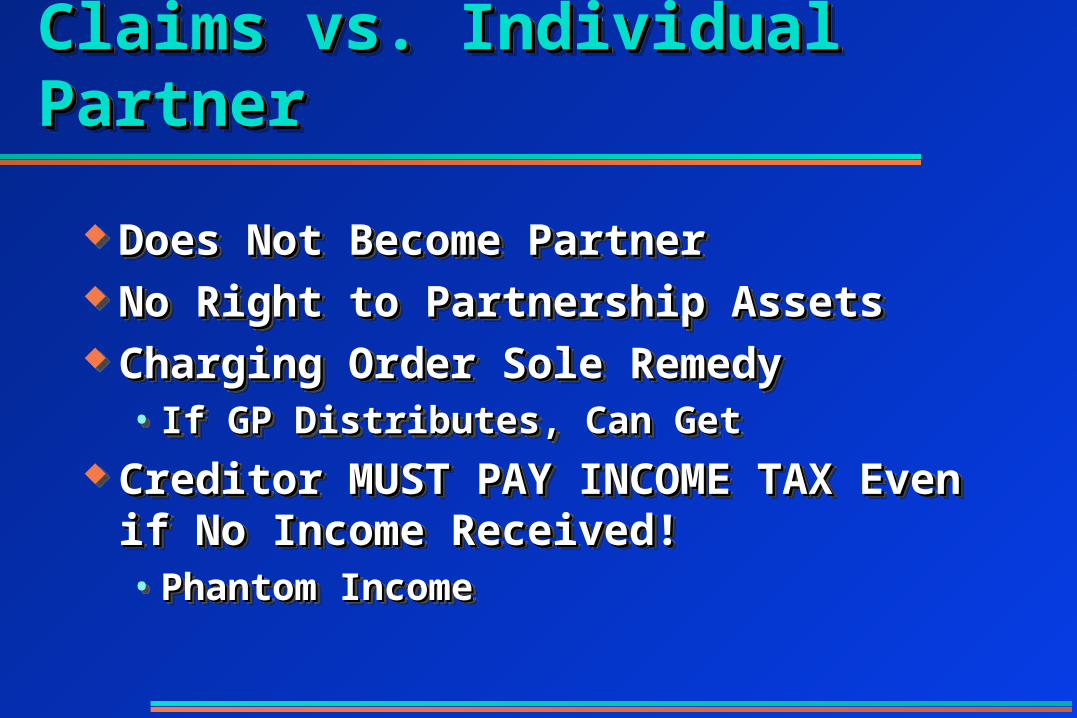

Claims vs. Individual PartnerClaims vs. Individual PartnerClaims vs. Individual PartnerClaims vs. Individual Partner

Does Not Become PartnerDoes Not Become Partner No Right to Partnership AssetsNo Right to Partnership Assets Charging Order Sole RemedyCharging Order Sole Remedy

• If GP Distributes, Can GetIf GP Distributes, Can Get Creditor MUST PAY INCOME TAX Even if Creditor MUST PAY INCOME TAX Even if

No Income Received!No Income Received!• Phantom IncomePhantom Income

Does Not Become PartnerDoes Not Become Partner No Right to Partnership AssetsNo Right to Partnership Assets Charging Order Sole RemedyCharging Order Sole Remedy

• If GP Distributes, Can GetIf GP Distributes, Can Get Creditor MUST PAY INCOME TAX Even if Creditor MUST PAY INCOME TAX Even if

No Income Received!No Income Received!• Phantom IncomePhantom Income

Creditor NightmareCreditor NightmareCreditor NightmareCreditor Nightmare

Does not Become a Does not Become a Limited PartnerLimited Partner

No Right to Demand No Right to Demand AssetsAssets

No Transfer of Assets No Transfer of Assets Without Partner Without Partner ApprovalApproval

Does not Become a Does not Become a Limited PartnerLimited Partner

No Right to Demand No Right to Demand AssetsAssets

No Transfer of Assets No Transfer of Assets Without Partner Without Partner ApprovalApproval

No Fraudulent Transfer No Fraudulent Transfer When FLP EstablishedWhen FLP Established

Can’t Force Termination Can’t Force Termination of FLPof FLP

General Partner General Partner Maintains Income Maintains Income ControlControl

No Fraudulent Transfer No Fraudulent Transfer When FLP EstablishedWhen FLP Established

Can’t Force Termination Can’t Force Termination of FLPof FLP

General Partner General Partner Maintains Income Maintains Income ControlControl

FLPs Leverage GiftsFLPs Leverage GiftsFLPs Leverage GiftsFLPs Leverage Gifts

Each Person May Gift Up to $10,000 per Each Person May Gift Up to $10,000 per Person in SharesPerson in Shares

Value of Gifts is the Fair Market Value of GiftValue of Gifts is the Fair Market Value of Gift Partnership Rules Can Allow Value of Shares Partnership Rules Can Allow Value of Shares

to be Deeply Discounted!to be Deeply Discounted!

Each Person May Gift Up to $10,000 per Each Person May Gift Up to $10,000 per Person in SharesPerson in Shares

Value of Gifts is the Fair Market Value of GiftValue of Gifts is the Fair Market Value of Gift Partnership Rules Can Allow Value of Shares Partnership Rules Can Allow Value of Shares

to be Deeply Discounted!to be Deeply Discounted!

FLP DiscountsFLP DiscountsFLP DiscountsFLP Discounts

What is a FLP Share Worth?What is a FLP Share Worth?• Can’t be Easily Sold or TransferredCan’t be Easily Sold or Transferred• Can’t be PledgedCan’t be Pledged• Can’t Demand DistributionsCan’t Demand Distributions• Income Allocated to LP for Income Tax Even if not Income Allocated to LP for Income Tax Even if not

PaidPaid FMV of LP Share is Substantially Less than the FMV of LP Share is Substantially Less than the

Value of the Assets! Value of the Assets!

What is a FLP Share Worth?What is a FLP Share Worth?• Can’t be Easily Sold or TransferredCan’t be Easily Sold or Transferred• Can’t be PledgedCan’t be Pledged• Can’t Demand DistributionsCan’t Demand Distributions• Income Allocated to LP for Income Tax Even if not Income Allocated to LP for Income Tax Even if not

PaidPaid FMV of LP Share is Substantially Less than the FMV of LP Share is Substantially Less than the

Value of the Assets! Value of the Assets!

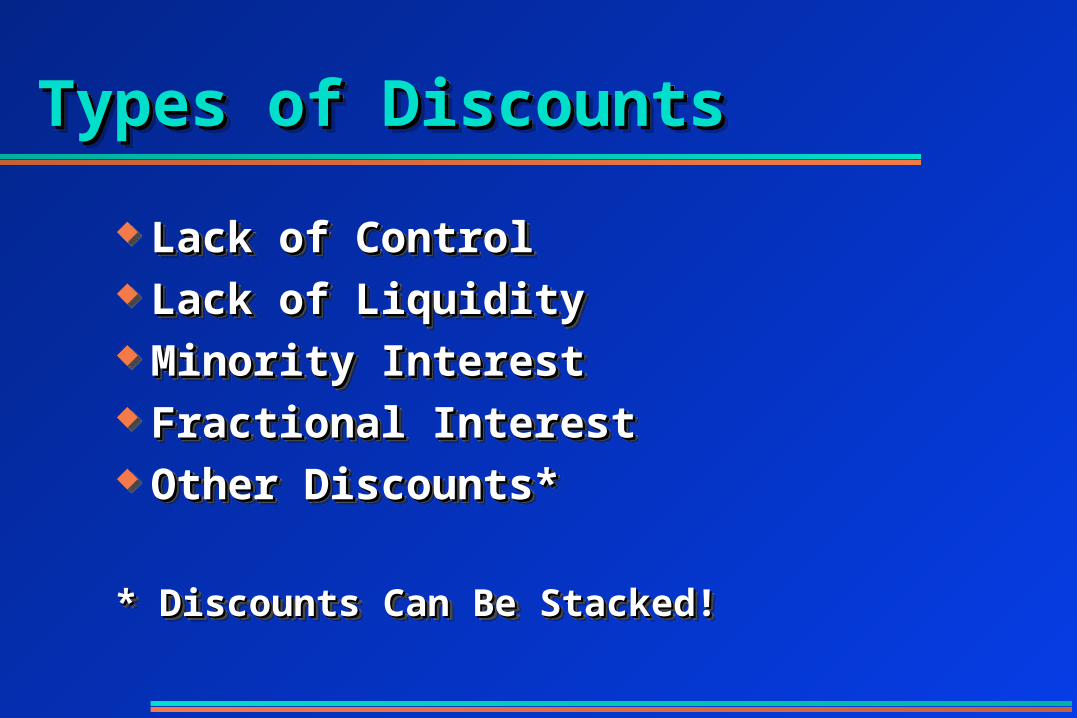

Types of DiscountsTypes of DiscountsTypes of DiscountsTypes of Discounts

Lack of ControlLack of Control Lack of LiquidityLack of Liquidity Minority InterestMinority Interest Fractional InterestFractional Interest Other Discounts*Other Discounts*

* Discounts Can Be Stacked!* Discounts Can Be Stacked!

Lack of ControlLack of Control Lack of LiquidityLack of Liquidity Minority InterestMinority Interest Fractional InterestFractional Interest Other Discounts*Other Discounts*

* Discounts Can Be Stacked!* Discounts Can Be Stacked!

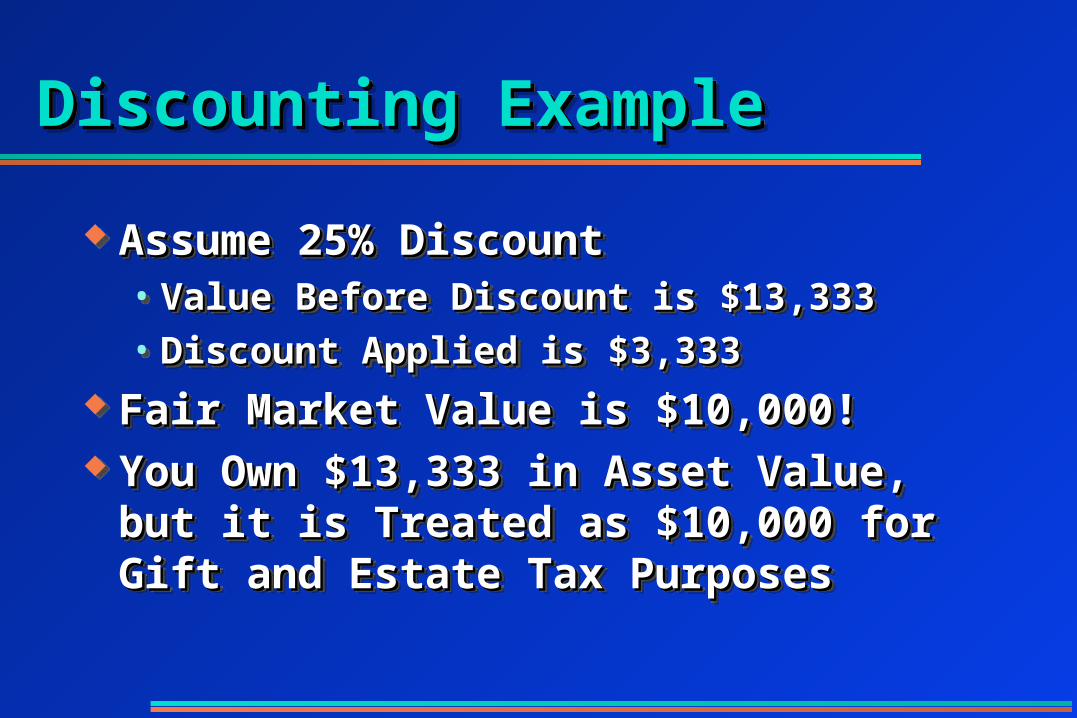

Discounting ExampleDiscounting ExampleDiscounting ExampleDiscounting Example

Assume 25% DiscountAssume 25% Discount• Value Before Discount is $13,333Value Before Discount is $13,333• Discount Applied is $3,333Discount Applied is $3,333

Fair Market Value is $10,000!Fair Market Value is $10,000! You Own $13,333 in Asset Value, but it is You Own $13,333 in Asset Value, but it is

Treated as $10,000 for Gift and Estate Tax Treated as $10,000 for Gift and Estate Tax PurposesPurposes

Assume 25% DiscountAssume 25% Discount• Value Before Discount is $13,333Value Before Discount is $13,333• Discount Applied is $3,333Discount Applied is $3,333

Fair Market Value is $10,000!Fair Market Value is $10,000! You Own $13,333 in Asset Value, but it is You Own $13,333 in Asset Value, but it is

Treated as $10,000 for Gift and Estate Tax Treated as $10,000 for Gift and Estate Tax PurposesPurposes

FLP SummaryFLP SummaryFLP SummaryFLP Summary

Juicy Red Apple is a Sour Lemon for CreditorsJuicy Red Apple is a Sour Lemon for Creditors Family Involved, Parents Control the AssetsFamily Involved, Parents Control the Assets Estate Tax ReductionEstate Tax Reduction Can Distribute Income to Children or Others at Can Distribute Income to Children or Others at

Lower Tax RatesLower Tax Rates

Juicy Red Apple is a Sour Lemon for CreditorsJuicy Red Apple is a Sour Lemon for Creditors Family Involved, Parents Control the AssetsFamily Involved, Parents Control the Assets Estate Tax ReductionEstate Tax Reduction Can Distribute Income to Children or Others at Can Distribute Income to Children or Others at

Lower Tax RatesLower Tax Rates

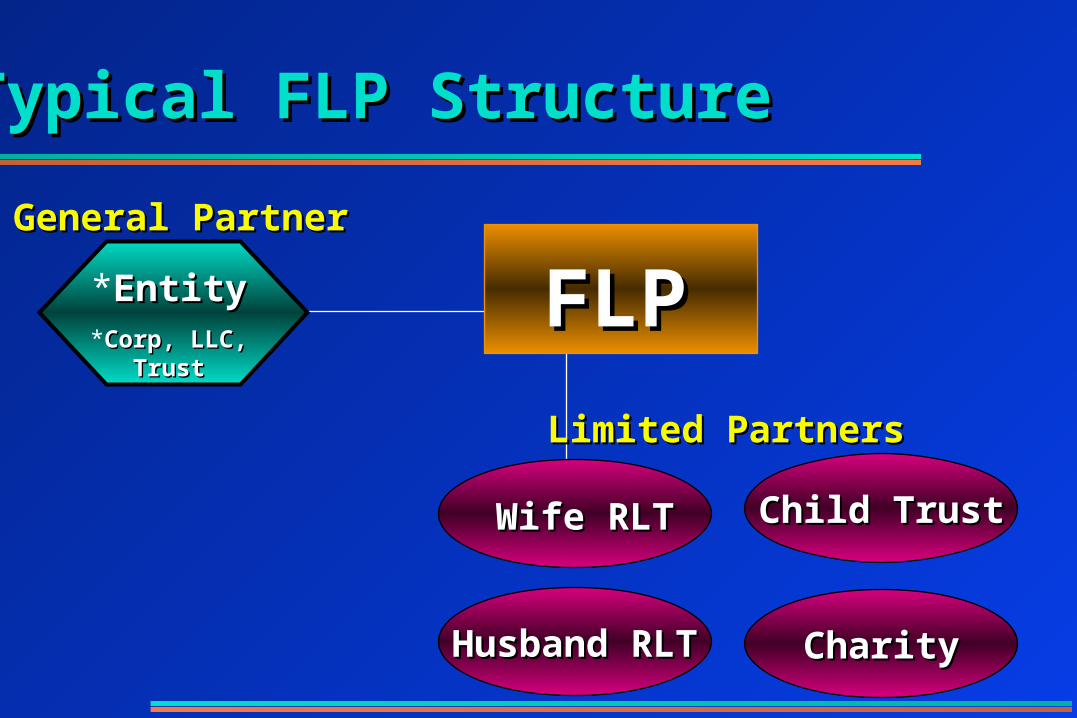

Typical FLP StructureTypical FLP Structure

FLPFLP*EntityEntity*Corp, LLC, Corp, LLC,

TrustTrust

Husband RLTHusband RLT

Child TrustChild Trust

CharityCharity

Wife RLTWife RLT

General PartnerGeneral Partner

Limited PartnersLimited Partners

Fifth FortificationFifth FortificationFifth FortificationFifth Fortification

Limited Limited Liability Liability CompaniesCompanies(LLC)(LLC)

Limited Limited Liability Liability CompaniesCompanies(LLC)(LLC)

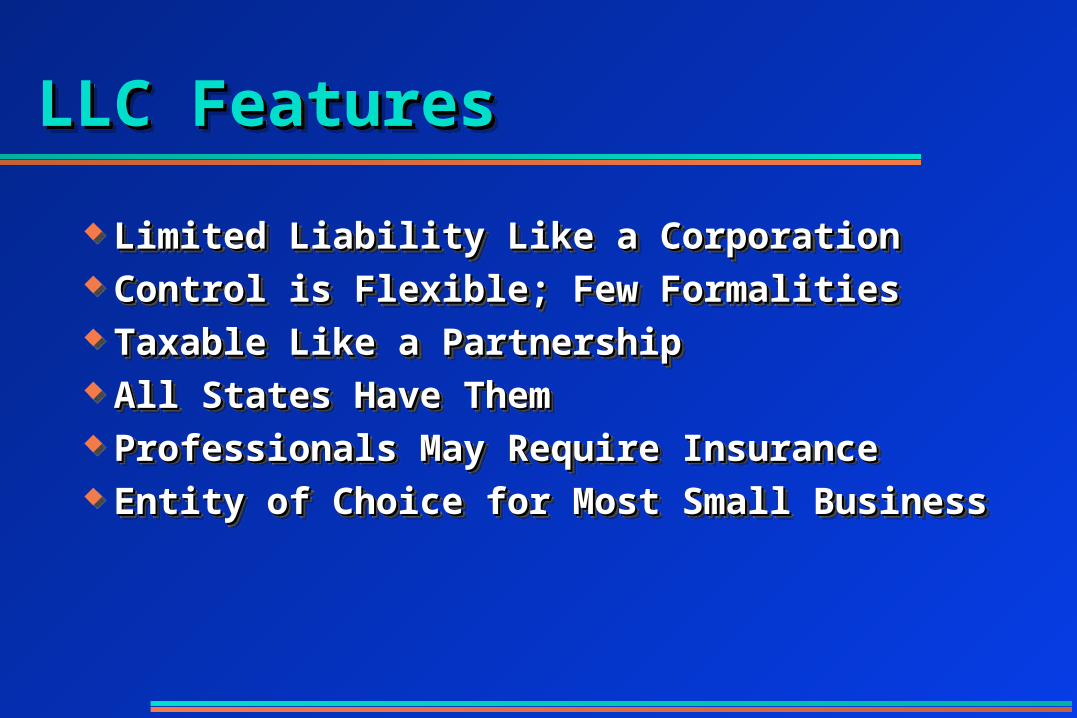

LLC FeaturesLLC FeaturesLLC FeaturesLLC Features

Limited Liability Like a CorporationLimited Liability Like a Corporation Control is Flexible; Few FormalitiesControl is Flexible; Few Formalities Taxable Like a PartnershipTaxable Like a Partnership All States Have ThemAll States Have Them Professionals May Require InsuranceProfessionals May Require Insurance Entity of Choice for Most Small BusinessEntity of Choice for Most Small Business

Limited Liability Like a CorporationLimited Liability Like a Corporation Control is Flexible; Few FormalitiesControl is Flexible; Few Formalities Taxable Like a PartnershipTaxable Like a Partnership All States Have ThemAll States Have Them Professionals May Require InsuranceProfessionals May Require Insurance Entity of Choice for Most Small BusinessEntity of Choice for Most Small Business

Sixth FortificationSixth FortificationSixth FortificationSixth Fortification

Business Business Transition Transition PlanningPlanning

Business Business Transition Transition PlanningPlanning

Business Transition IssuesBusiness Transition IssuesBusiness Transition IssuesBusiness Transition Issues

Most Businesses Die with the FounderMost Businesses Die with the Founder Reasons Include:Reasons Include:

• Lack of Liquidity to Pay Estate TaxesLack of Liquidity to Pay Estate Taxes• Lack of Ability to Manage BusinessLack of Ability to Manage Business• Infighting: Family Strife and DissensionInfighting: Family Strife and Dissension

Do Your Family Members Really Want to be in Do Your Family Members Really Want to be in Business Together?Business Together?

Most Businesses Die with the FounderMost Businesses Die with the Founder Reasons Include:Reasons Include:

• Lack of Liquidity to Pay Estate TaxesLack of Liquidity to Pay Estate Taxes• Lack of Ability to Manage BusinessLack of Ability to Manage Business• Infighting: Family Strife and DissensionInfighting: Family Strife and Dissension

Do Your Family Members Really Want to be in Do Your Family Members Really Want to be in Business Together?Business Together?

Successful TransitionsSuccessful TransitionsSuccessful TransitionsSuccessful Transitions

Interested Family Interested Family Member(s) Continue Member(s) Continue BusinessBusiness

Different Benefits to Different Benefits to Other Family MembersOther Family Members• InsuranceInsurance

• BuyoutBuyout

Interested Family Interested Family Member(s) Continue Member(s) Continue BusinessBusiness

Different Benefits to Different Benefits to Other Family MembersOther Family Members• InsuranceInsurance

• BuyoutBuyout

Key Employee Key Employee InvolvementInvolvement

Tax Advantaged SaleTax Advantaged Sale Estate Tax ReductionEstate Tax Reduction Retirement Income Retirement Income

IncreasedIncreased

Key Employee Key Employee InvolvementInvolvement

Tax Advantaged SaleTax Advantaged Sale Estate Tax ReductionEstate Tax Reduction Retirement Income Retirement Income

IncreasedIncreased

Seventh FortificationSeventh FortificationSeventh FortificationSeventh Fortification

PersonalPersonalAssetAssetProtectionProtectionTrustsTrusts

PersonalPersonalAssetAssetProtectionProtectionTrustsTrusts

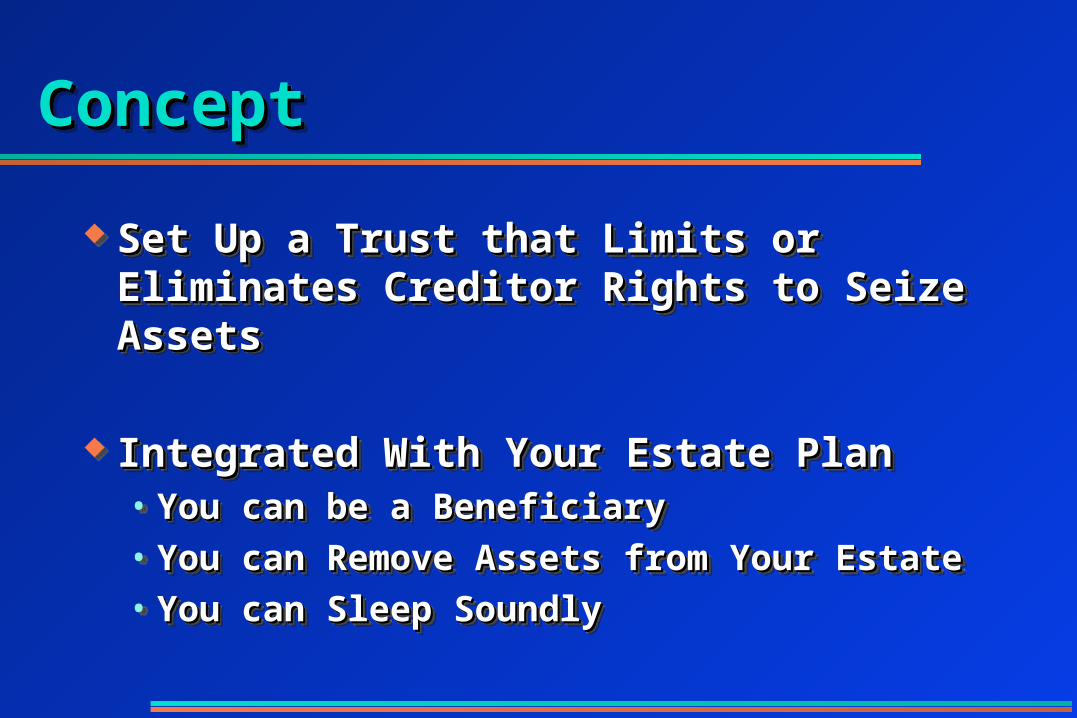

ConceptConceptConceptConcept

Set Up a Trust that Limits or Eliminates Set Up a Trust that Limits or Eliminates Creditor Rights to Seize AssetsCreditor Rights to Seize Assets

Integrated With Your Estate PlanIntegrated With Your Estate Plan• You can be a BeneficiaryYou can be a Beneficiary• You can Remove Assets from Your EstateYou can Remove Assets from Your Estate• You can Sleep SoundlyYou can Sleep Soundly

Set Up a Trust that Limits or Eliminates Set Up a Trust that Limits or Eliminates Creditor Rights to Seize AssetsCreditor Rights to Seize Assets

Integrated With Your Estate PlanIntegrated With Your Estate Plan• You can be a BeneficiaryYou can be a Beneficiary• You can Remove Assets from Your EstateYou can Remove Assets from Your Estate• You can Sleep SoundlyYou can Sleep Soundly

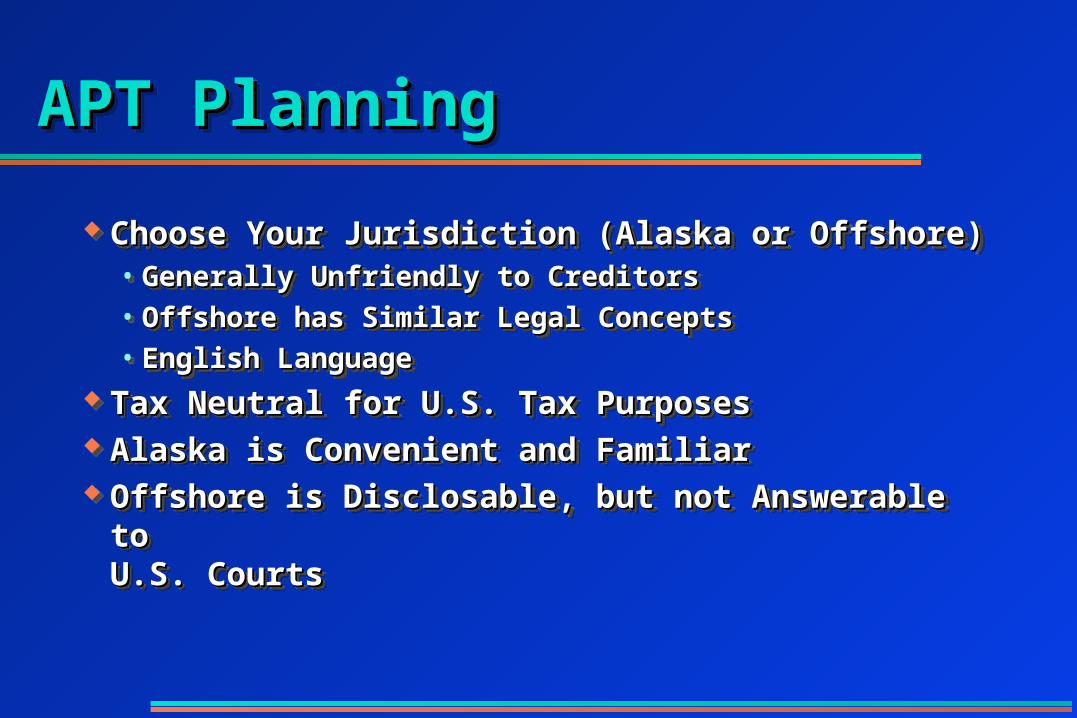

APT PlanningAPT PlanningAPT PlanningAPT Planning

Choose Your Jurisdiction (Alaska or Offshore)Choose Your Jurisdiction (Alaska or Offshore)• Generally Unfriendly to CreditorsGenerally Unfriendly to Creditors• Offshore has Similar Legal ConceptsOffshore has Similar Legal Concepts• English LanguageEnglish Language

Tax Neutral for U.S. Tax PurposesTax Neutral for U.S. Tax Purposes Alaska is Convenient and FamiliarAlaska is Convenient and Familiar Offshore is Disclosable, but not Answerable to Offshore is Disclosable, but not Answerable to

U.S. Courts U.S. Courts

Choose Your Jurisdiction (Alaska or Offshore)Choose Your Jurisdiction (Alaska or Offshore)• Generally Unfriendly to CreditorsGenerally Unfriendly to Creditors• Offshore has Similar Legal ConceptsOffshore has Similar Legal Concepts• English LanguageEnglish Language

Tax Neutral for U.S. Tax PurposesTax Neutral for U.S. Tax Purposes Alaska is Convenient and FamiliarAlaska is Convenient and Familiar Offshore is Disclosable, but not Answerable to Offshore is Disclosable, but not Answerable to

U.S. Courts U.S. Courts

APT Planning (cont.)APT Planning (cont.)APT Planning (cont.)APT Planning (cont.)

Eliminates or Reduces Coercion in LawsuitsEliminates or Reduces Coercion in Lawsuits Is Done For Estate Planning and Business Is Done For Estate Planning and Business

ReasonsReasons Is not a Suitcase of Money on a Midnight FlightIs not a Suitcase of Money on a Midnight Flight Is not a Violation of U.S. LawIs not a Violation of U.S. Law Is not Tax EvasionIs not Tax Evasion

Eliminates or Reduces Coercion in LawsuitsEliminates or Reduces Coercion in Lawsuits Is Done For Estate Planning and Business Is Done For Estate Planning and Business

ReasonsReasons Is not a Suitcase of Money on a Midnight FlightIs not a Suitcase of Money on a Midnight Flight Is not a Violation of U.S. LawIs not a Violation of U.S. Law Is not Tax EvasionIs not Tax Evasion

Alaska as JurisdictionAlaska as JurisdictionAlaska as JurisdictionAlaska as Jurisdiction

A Great Castle MoatA Great Castle Moat• Judgments May not Be Judgments May not Be

Enforceable Against Enforceable Against TrustTrust

• U.S. JurisdictionU.S. Jurisdiction

• Perpetual TrustsPerpetual Trusts

• Use With Domestic FLPs Use With Domestic FLPs and LLCsand LLCs

• Power to RelocatePower to Relocate

A Great Castle MoatA Great Castle Moat• Judgments May not Be Judgments May not Be

Enforceable Against Enforceable Against TrustTrust

• U.S. JurisdictionU.S. Jurisdiction

• Perpetual TrustsPerpetual Trusts

• Use With Domestic FLPs Use With Domestic FLPs and LLCsand LLCs

• Power to RelocatePower to Relocate

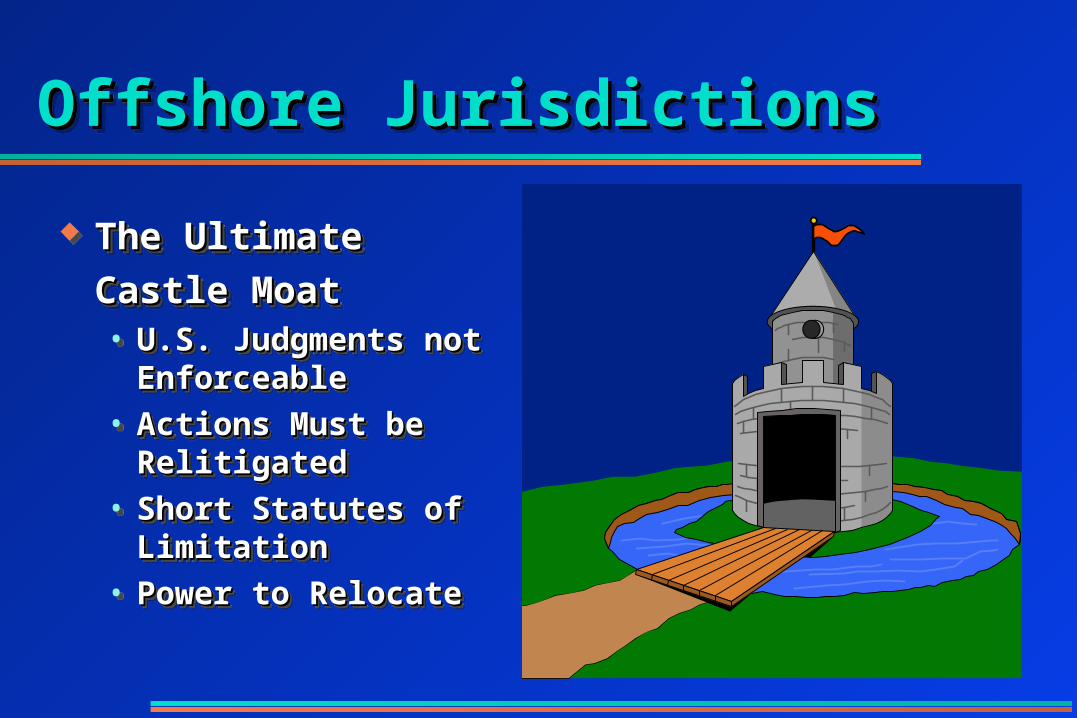

Offshore JurisdictionsOffshore JurisdictionsOffshore JurisdictionsOffshore Jurisdictions

The UltimateThe Ultimate

Castle MoatCastle Moat• U.S. Judgments not U.S. Judgments not

EnforceableEnforceable

• Actions Must be Actions Must be RelitigatedRelitigated

• Short Statutes of Short Statutes of LimitationLimitation

• Power to RelocatePower to Relocate

The UltimateThe Ultimate

Castle MoatCastle Moat• U.S. Judgments not U.S. Judgments not

EnforceableEnforceable

• Actions Must be Actions Must be RelitigatedRelitigated

• Short Statutes of Short Statutes of LimitationLimitation

• Power to RelocatePower to Relocate

Case StudyCase StudyCase StudyCase Study

The SurgeonThe SurgeonThe SurgeonThe Surgeon

Leon Cutter, M.D., F.A.C.S.Leon Cutter, M.D., F.A.C.S.Leon Cutter, M.D., F.A.C.S.Leon Cutter, M.D., F.A.C.S.

Orthopedic SurgeonOrthopedic Surgeon• Six Suits in Ten Years; Six Suits in Ten Years;

All SettledAll Settled

• Large Insurance Large Insurance PremiumsPremiums

Professional Corp.Professional Corp.• Leases BuildingLeases Building

• Owns EquipmentOwns Equipment

Orthopedic SurgeonOrthopedic Surgeon• Six Suits in Ten Years; Six Suits in Ten Years;

All SettledAll Settled

• Large Insurance Large Insurance PremiumsPremiums

Professional Corp.Professional Corp.• Leases BuildingLeases Building

• Owns EquipmentOwns Equipment

Married to JanetMarried to Janet• Former TeacherFormer Teacher

• Expert InvestorExpert Investor Two ChildrenTwo Children

• Mary, TimMary, Tim Family Owns Home, Family Owns Home,

Investments, Retirement Investments, Retirement PlanPlan

Married to JanetMarried to Janet• Former TeacherFormer Teacher

• Expert InvestorExpert Investor Two ChildrenTwo Children

• Mary, TimMary, Tim Family Owns Home, Family Owns Home,

Investments, Retirement Investments, Retirement PlanPlan

Cutter Family GoalsCutter Family GoalsCutter Family GoalsCutter Family Goals

Protect Nonexempt AssetsProtect Nonexempt Assets• Keep Home Absolutely SafeKeep Home Absolutely Safe

Protect Practice AssetsProtect Practice Assets• Building and EquipmentBuilding and Equipment

Lower Malpractice PremiumsLower Malpractice Premiums Maintain Control and PrivacyMaintain Control and Privacy Plan for Federal Estate TaxesPlan for Federal Estate Taxes

Protect Nonexempt AssetsProtect Nonexempt Assets• Keep Home Absolutely SafeKeep Home Absolutely Safe

Protect Practice AssetsProtect Practice Assets• Building and EquipmentBuilding and Equipment

Lower Malpractice PremiumsLower Malpractice Premiums Maintain Control and PrivacyMaintain Control and Privacy Plan for Federal Estate TaxesPlan for Federal Estate Taxes

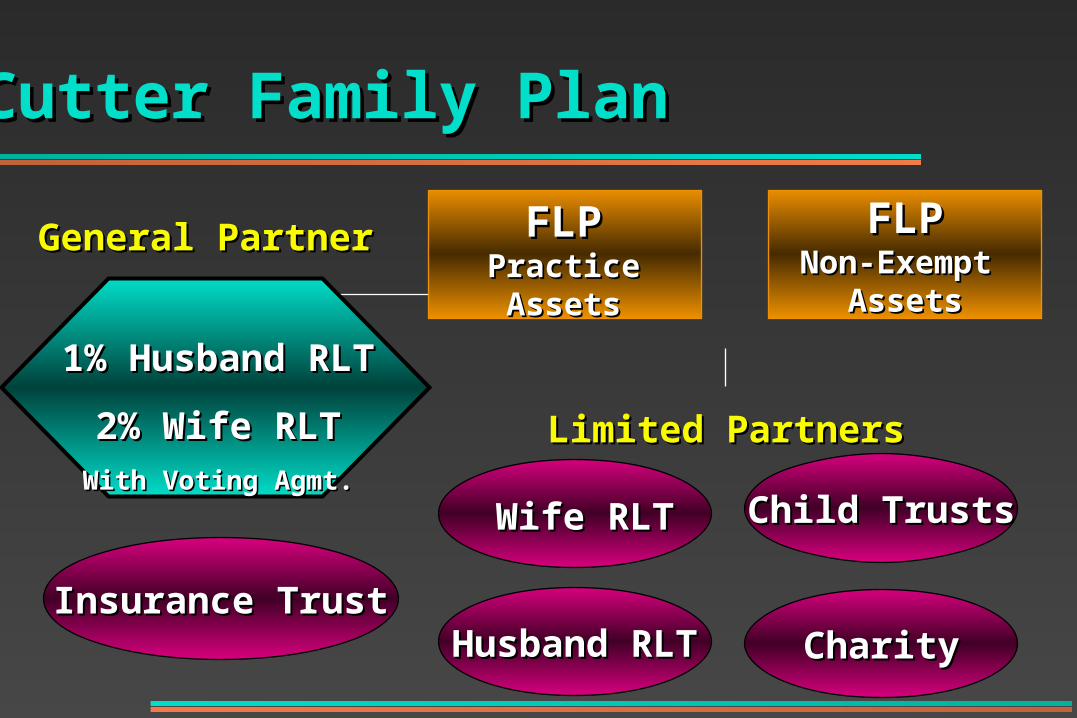

FLPFLPNon-Exempt Non-Exempt

AssetsAssets

Cutter Family PlanCutter Family Plan

1% Husband RLT1% Husband RLT

2% Wife RLT2% Wife RLTWith Voting Agmt.With Voting Agmt.

Husband RLTHusband RLT

Child TrustsChild Trusts

CharityCharity

Wife RLTWife RLT

General PartnerGeneral Partner

Limited PartnersLimited Partners

FLPFLPPractice Practice AssetsAssets

Insurance TrustInsurance Trust

Estate Discount ExampleEstate Discount ExampleEstate Discount ExampleEstate Discount Example

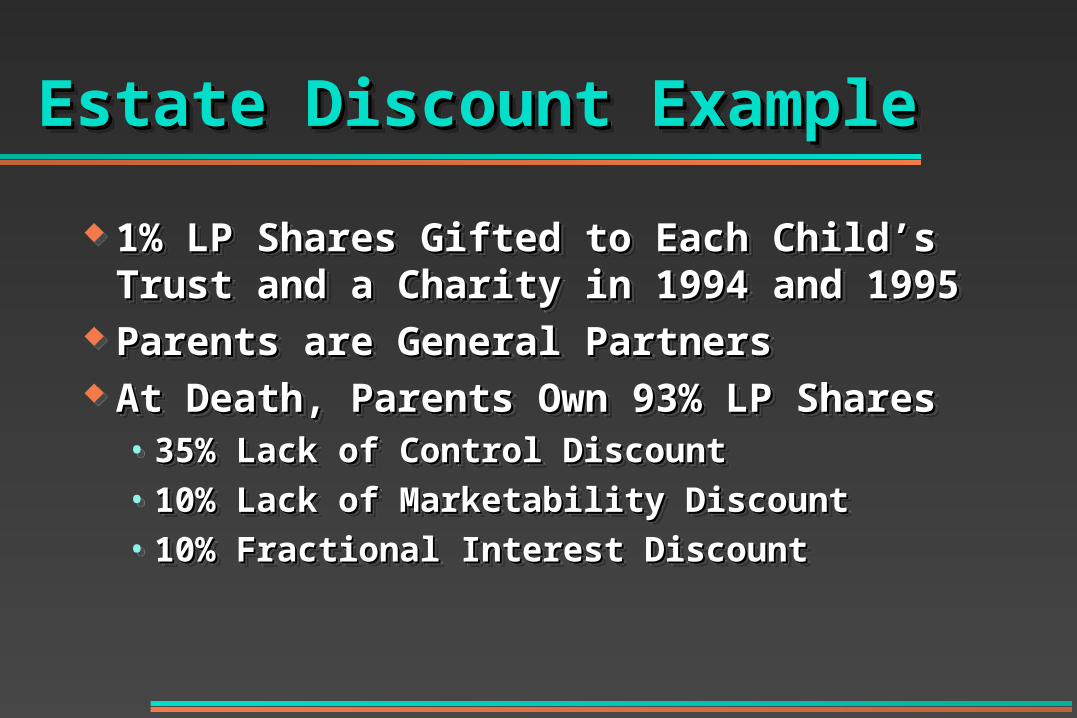

1% LP Shares Gifted to Each Child’s Trust 1% LP Shares Gifted to Each Child’s Trust and a Charity in 1994 and 1995and a Charity in 1994 and 1995

Parents are General PartnersParents are General Partners At Death, Parents Own 93% LP SharesAt Death, Parents Own 93% LP Shares

• 35% Lack of Control Discount35% Lack of Control Discount• 10% Lack of Marketability Discount10% Lack of Marketability Discount• 10% Fractional Interest Discount 10% Fractional Interest Discount

1% LP Shares Gifted to Each Child’s Trust 1% LP Shares Gifted to Each Child’s Trust and a Charity in 1994 and 1995and a Charity in 1994 and 1995

Parents are General PartnersParents are General Partners At Death, Parents Own 93% LP SharesAt Death, Parents Own 93% LP Shares

• 35% Lack of Control Discount35% Lack of Control Discount• 10% Lack of Marketability Discount10% Lack of Marketability Discount• 10% Fractional Interest Discount 10% Fractional Interest Discount

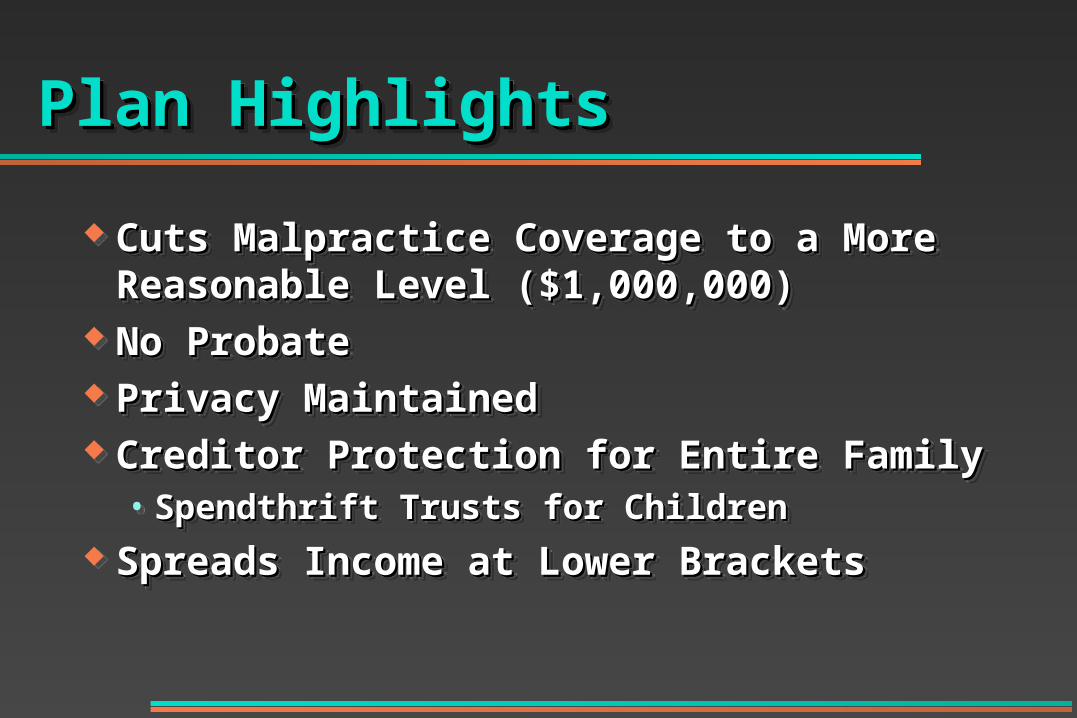

Plan HighlightsPlan HighlightsPlan HighlightsPlan Highlights

Cuts Malpractice Coverage to a More Cuts Malpractice Coverage to a More Reasonable Level ($1,000,000)Reasonable Level ($1,000,000)

No ProbateNo Probate Privacy MaintainedPrivacy Maintained Creditor Protection for Entire FamilyCreditor Protection for Entire Family

• Spendthrift Trusts for ChildrenSpendthrift Trusts for Children Spreads Income at Lower BracketsSpreads Income at Lower Brackets

Cuts Malpractice Coverage to a More Cuts Malpractice Coverage to a More Reasonable Level ($1,000,000)Reasonable Level ($1,000,000)

No ProbateNo Probate Privacy MaintainedPrivacy Maintained Creditor Protection for Entire FamilyCreditor Protection for Entire Family

• Spendthrift Trusts for ChildrenSpendthrift Trusts for Children Spreads Income at Lower BracketsSpreads Income at Lower Brackets

Plan HighlightsPlan HighlightsPlan HighlightsPlan Highlights

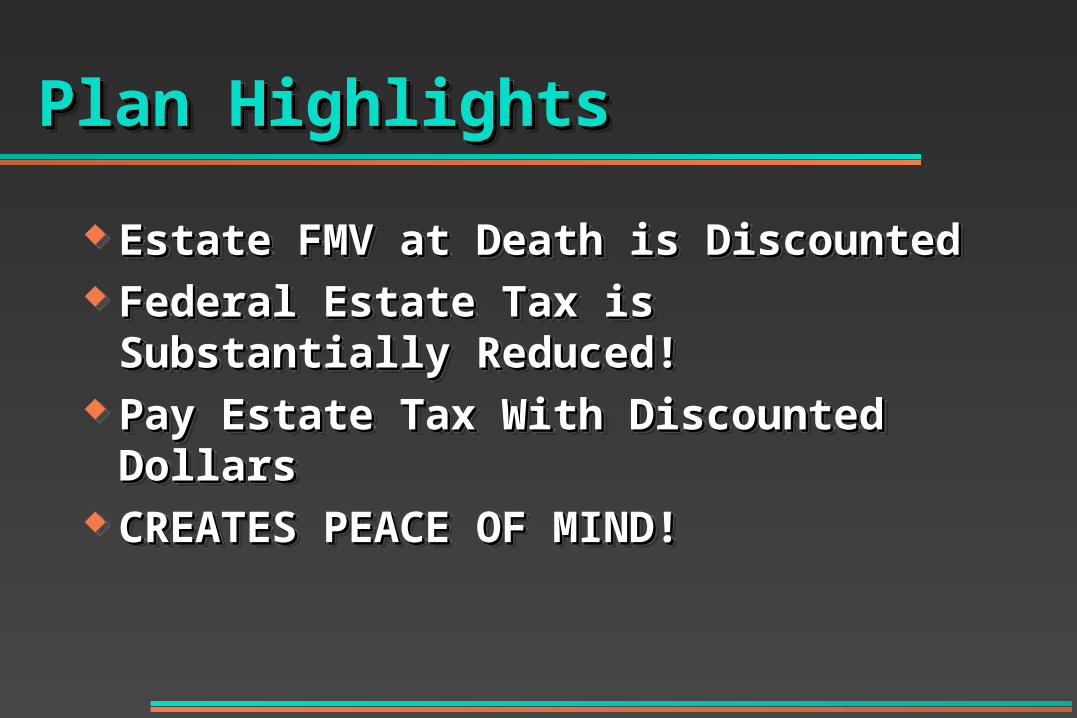

Estate FMV at Death is DiscountedEstate FMV at Death is Discounted Federal Estate Tax is Substantially Reduced!Federal Estate Tax is Substantially Reduced! Pay Estate Tax With Discounted DollarsPay Estate Tax With Discounted Dollars CREATES PEACE OF MIND!CREATES PEACE OF MIND!

Estate FMV at Death is DiscountedEstate FMV at Death is Discounted Federal Estate Tax is Substantially Reduced!Federal Estate Tax is Substantially Reduced! Pay Estate Tax With Discounted DollarsPay Estate Tax With Discounted Dollars CREATES PEACE OF MIND!CREATES PEACE OF MIND!

Before PlanningBefore PlanningBefore PlanningBefore Planning

Your Entire Estate is at Risk!Your Entire Estate is at Risk!Your Entire Estate is at Risk!Your Entire Estate is at Risk!

After PlanningAfter PlanningAfter PlanningAfter Planning

Your Estate has Defenses!Your Estate has Defenses!Your Estate has Defenses!Your Estate has Defenses!

Keys to a Successful PlanKeys to a Successful Plan

Team ApproachTeam Approach

Custom DesignCustom Design

Cutting Edge SolutionsCutting Edge Solutions

Team ApproachTeam Approach

Custom DesignCustom Design

Cutting Edge SolutionsCutting Edge Solutions

Thank You for AttendingThank You for Attending

Questions?Questions?Questions?Questions?